Embed Size (px)

Citation preview

ed-CK / sa- WMT, PY

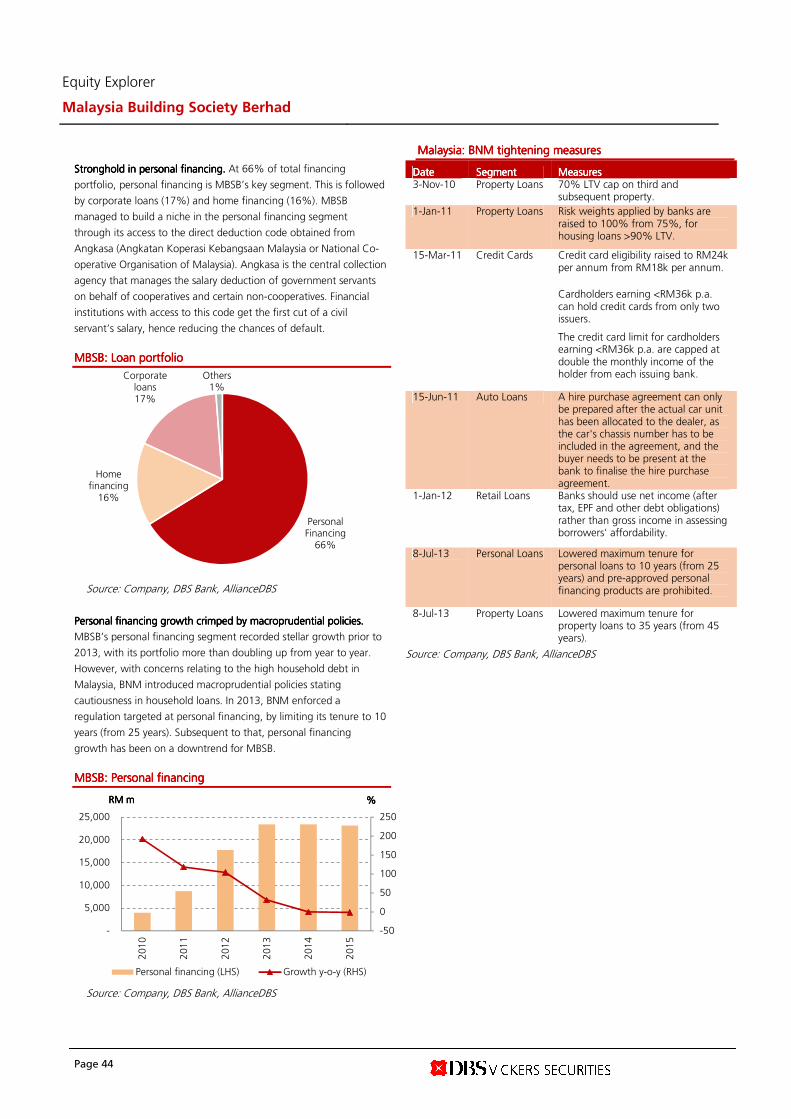

The unconventional banking aspect • Domestic Islamic financing growth expected to

continue outpacing conventional loan growth, driven by regulatory push for internationalization of Islamic finance

• Hopes for further growth pinned on increase in financial inclusion through product innovation

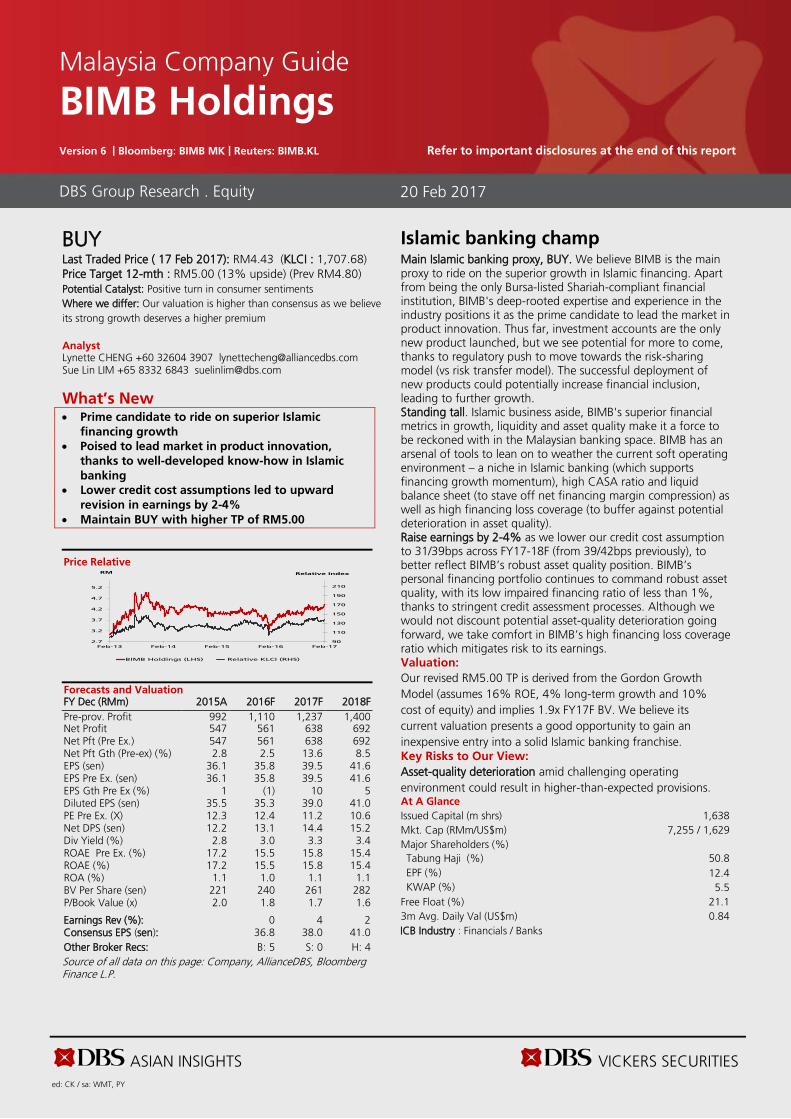

• Main Islamic banking proxy – BIMB – as the largest Bursa-listed Shariah compliant financial institution with strong potential to lead product innovation

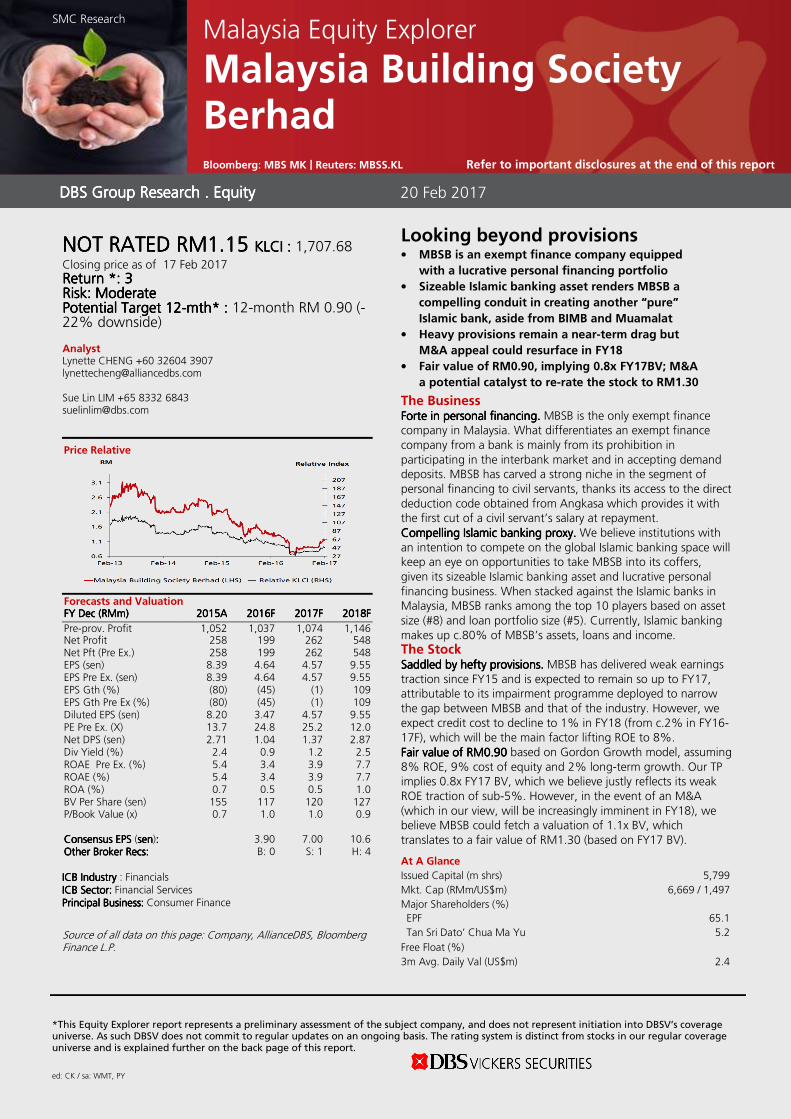

• Traction on BURSA’s commodity trading platform makes it an indirect proxy; MBSB is a potential M&A play

Profit-sharing principle of banking. Islamic banking is based on Islamic principle transactions of which profit (and loss) sharing is a major feature ensuring justice and equity in an economy. The financial relationships established are deemed to be participatory in nature. Islamic banking technically bans the receipt and payment of interest in any of its operations. In the most basic way, this sets Islamic banking apart from conventional banking. To realize the full potential of demand for Islamic banking from sizeable Muslim population and other Muslim-dominant countries, issues to overcome include non-uniformity in Shariah views, establishing an even playing field, and strengthening resources and awareness are among the key issues for this segment. Product innovation to be the game-changer for industry. Given the knowledge and expertise acquired through actively pioneering initiatives and delivering solutions in the Islamic banking industry, Malaysia is indisputably making inroads to becoming the global hub for Islamic finance. We expect domestic Islamic financing growth to continue outpacing conventional loan growth with a 4-year CAGR of 12% over FY15-20F, as opposed to 2% for conventional loans. This is mainly underpinned by a growing push by the banks to fulfil BNM’s target of 40% proportion of Islamic financing to total system loans. Further upside to this could come from improvement in financial inclusion and regionalisation of Islamic finance. In order to achieve this, we believe Islamic banks should differentiate itself from their conventional peers through product innovation. BIMB, the main Islamic banking proxy in Malaysia. We like BIMB (holding company of Bank Islam) for its deep-rooted expertise in the industry, which we believe forms a strong competitive advantage as it positions them as a likely leader in product innovation. Maybank Islamic complements the Islamic banking scene for its size and established regional presence which will work to its advantage in competing on the global front. A new wave of M&A activities in the Islamic banking space is plausible although the timing remains the key risk. Potential M&A candidates include MBSB (whose appeal lies in its lucrative personal financing business and sizeable Islamic banking asset; featured as an Equity Explorer in this report) and unlisted MUAMALAT (from a long-awaited pare-down in stake by its largest shareholder, DRB). Albeit more indirectly, Bursa Malaysia is an indirect proxy as transactions on its commodity trading platform are expected to increase in conjunction with Islamic financing growth.

KLCI : 1,707.68

Analyst Lynette CHENG +60 32604 3907 Sue Lin LIM +65 8332 6843 [email protected] [email protected]

STOCKS

Source: DBS Bank, Bloomberg Finance L.P. Closing price as of 17 Feb 2017 Financing growth for Islamic banking to outpace conventional banking in Malaysia

Source: BNM, DBS Bank, AllianceDBS Maybank Islamic and BIMB among the biggest global Islamic banks

Source: World Islamic Banking Conference Leaderboard, DBS Bank, AllianceDBS

0

5

10

15

20

25

30

-

500

1,000

1,500

2,000

2009

2010

2011

2012

2013

2014

2015

2016

2017

F

2018

F

2019

F

2020

F

%RM bn

Islamic banking Conventional bankingConventional banking growth Islamic banking growthTotal banking system growth

84.154.5

40.836.4

34.932.2

24.623.622.8

21.516.9

14.614.513.613.3

0 10 20 30 40 50 60 70 80 90

AL RAJHI BANK (SA)KUWAIT FINANCE HOUSE (KU)

MAYBANK ISLAMIC (MY)DUBAI ISLAMIC (UAE)

ABU DHABI ISLAMIC (UAE)QATAR ISLAMIC (QA)BANK RAKYAT (MY)

ALBARAKA BANKING (BAH)MASRAF AL RAYAN (QA)

ALINMA BANK (SA)BANK AL-JAZIRA (SA)

KUWAIT TURKISH (KU)TURKIYE FINANS (TU)

CIMB ISLAMIC (MY)BANK ISLAM (MY)

Total Assets (US$ bn)

DBS Group Research . Equity

20 Feb 2017

Malaysia Industry Focus

Islamic Banks

Refer to important disclosures at the end of this report

Price Mkt Cap Target Price Performance (%)

RM US$m RM 3 mth 12 mth Rating

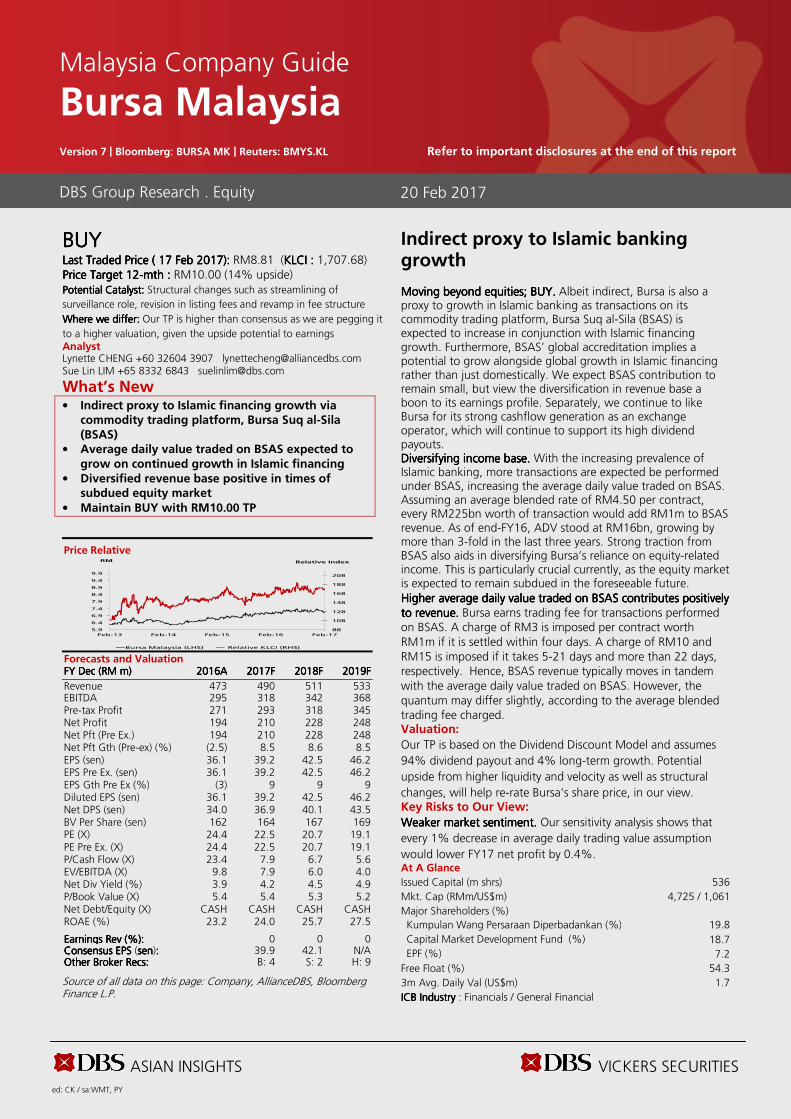

Maybank 8.46 19,363 7.50 10.2 (1.2) HOLD BIMB Holdings

4.43 1,629 5.00 4.5 25.5 BUY

Bursa Malaysia 8.81 1,061 10.00 3.0 5.3 BUY Malaysia Building Society Berhad

1.15 1,497 NA 27.8 (14.5) NOT RATED

Industry Focus

Islamic Banks

Page 2

Table of Contents Malaysia’s journey to becoming the Global Hub for Islamic Finance 3

Unleashing the potential 9

Two of a kind 12

Opportunities in Islamic Financing 17

Challenges for the industry 20

Industry players at a glance 21

Islamic banking proxies 22

Conclusion 24

Company profiles 25

BIMB Company Guide 26

Bursa Malaysia Company Guide 34

Malaysia Building Society Equity Explorer 42

Maybank Islamic 50

Bank Rakyat 52

Bank Muamalat 54

Appendix:

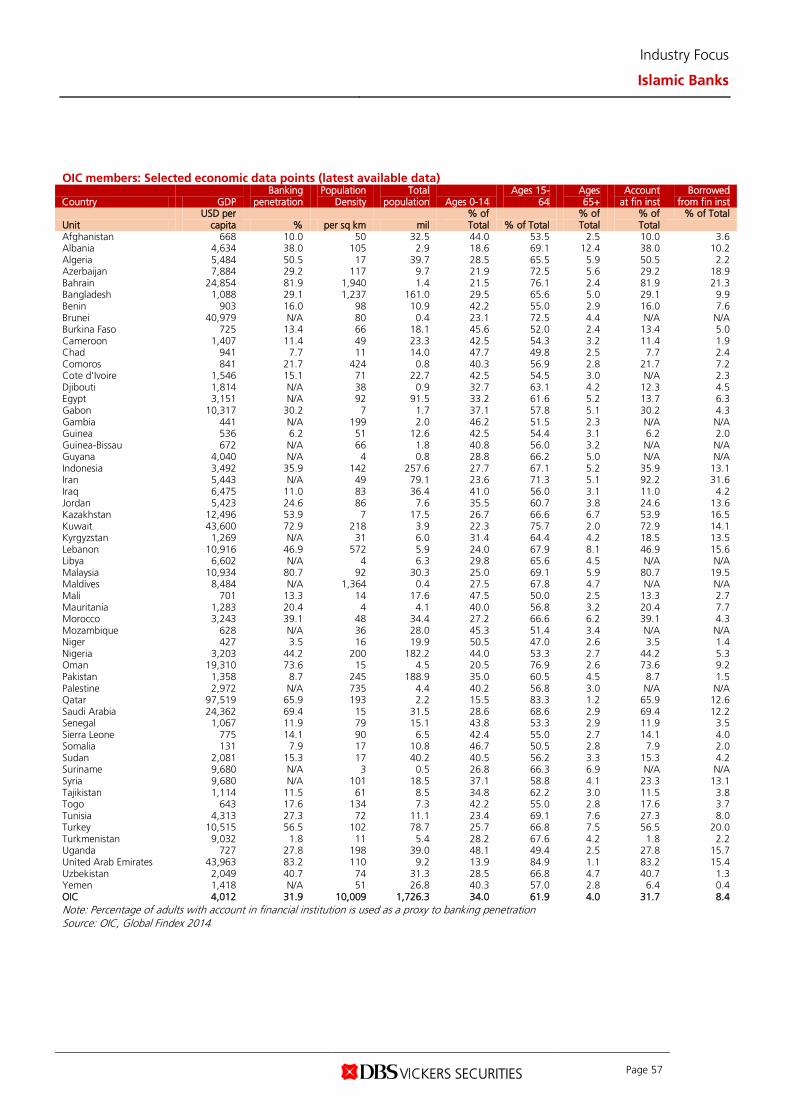

OIC members: Selected economic data points 57

Industry benchmarking 58

Islamic Banking: Definition of terms 61

Industry Focus

Islamic Banks

Page 3

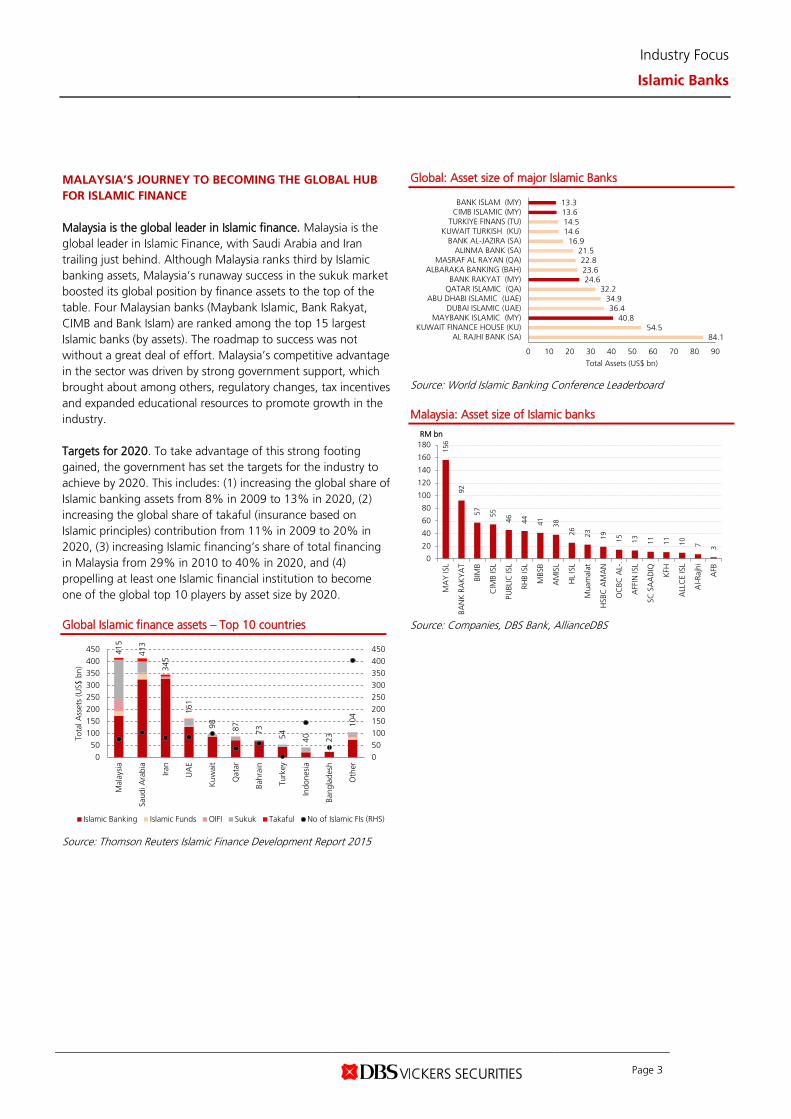

MALAYSIA’S JOURNEY TO BECOMING THE GLOBAL HUB FOR ISLAMIC FINANCE Malaysia is the global leader in Islamic finance. Malaysia is the global leader in Islamic Finance, with Saudi Arabia and Iran trailing just behind. Although Malaysia ranks third by Islamic banking assets, Malaysia’s runaway success in the sukuk market boosted its global position by finance assets to the top of the table. Four Malaysian banks (Maybank Islamic, Bank Rakyat, CIMB and Bank Islam) are ranked among the top 15 largest Islamic banks (by assets). The roadmap to success was not without a great deal of effort. Malaysia’s competitive advantage in the sector was driven by strong government support, which brought about among others, regulatory changes, tax incentives and expanded educational resources to promote growth in the industry. Targets for 2020. To take advantage of this strong footing gained, the government has set the targets for the industry to achieve by 2020. This includes: (1) increasing the global share of Islamic banking assets from 8% in 2009 to 13% in 2020, (2) increasing the global share of takaful (insurance based on Islamic principles) contribution from 11% in 2009 to 20% in 2020, (3) increasing Islamic financing’s share of total financing in Malaysia from 29% in 2010 to 40% in 2020, and (4) propelling at least one Islamic financial institution to become one of the global top 10 players by asset size by 2020. Global Islamic finance assets – Top 10 countries

Source: Thomson Reuters Islamic Finance Development Report 2015

Global: Asset size of major Islamic Banks

Source: World Islamic Banking Conference Leaderboard Malaysia: Asset size of Islamic banks

Source: Companies, DBS Bank, AllianceDBS

415

413

345

161

98 87 73 54 40 23

104

0

50

100

150

200

250

300

350

400

450

0

50

100

150

200

250

300

350

400

450

Mal

aysi

a

Saud

i Ara

bia

Iran

UA

E

Kuw

ait

Qat

ar

Bahr

ain

Turk

ey

Indo

nesi

a

Bang

lade

sh

Oth

er

Tota

l Ass

ets

(US$

bn)

Islamic Banking Islamic Funds OIFI Sukuk Takaful No of Islamic FIs (RHS)

84.154.5

40.836.4

34.932.2

24.623.622.8

21.516.9

14.614.513.613.3

0 10 20 30 40 50 60 70 80 90

AL RAJHI BANK (SA)KUWAIT FINANCE HOUSE (KU)

MAYBANK ISLAMIC (MY)DUBAI ISLAMIC (UAE)

ABU DHABI ISLAMIC (UAE)QATAR ISLAMIC (QA)BANK RAKYAT (MY)

ALBARAKA BANKING (BAH)MASRAF AL RAYAN (QA)

ALINMA BANK (SA)BANK AL-JAZIRA (SA)

KUWAIT TURKISH (KU)TURKIYE FINANS (TU)

CIMB ISLAMIC (MY)BANK ISLAM (MY)

Total Assets (US$ bn)

156

92

57

55

46

44

41

38

26

23

19

15

13

11

11

10

7 3

0

20

40

60

80

100

120

140

160

180M

AY

ISL

BAN

K R

AK

YA

T

BIM

B

CIM

B IS

L

PUBL

IC IS

L

RHB

ISL

MBS

B

AM

ISL

HL

ISL

Mua

mal

at

HSB

C A

MA

N

OC

BC A

L-…

AFF

IN IS

L

SC S

AA

DIQ

KFH

ALL

CE

ISL

Al-R

ajhi

AFB

RM bn

Industry Focus

Islamic Banks

Page 4

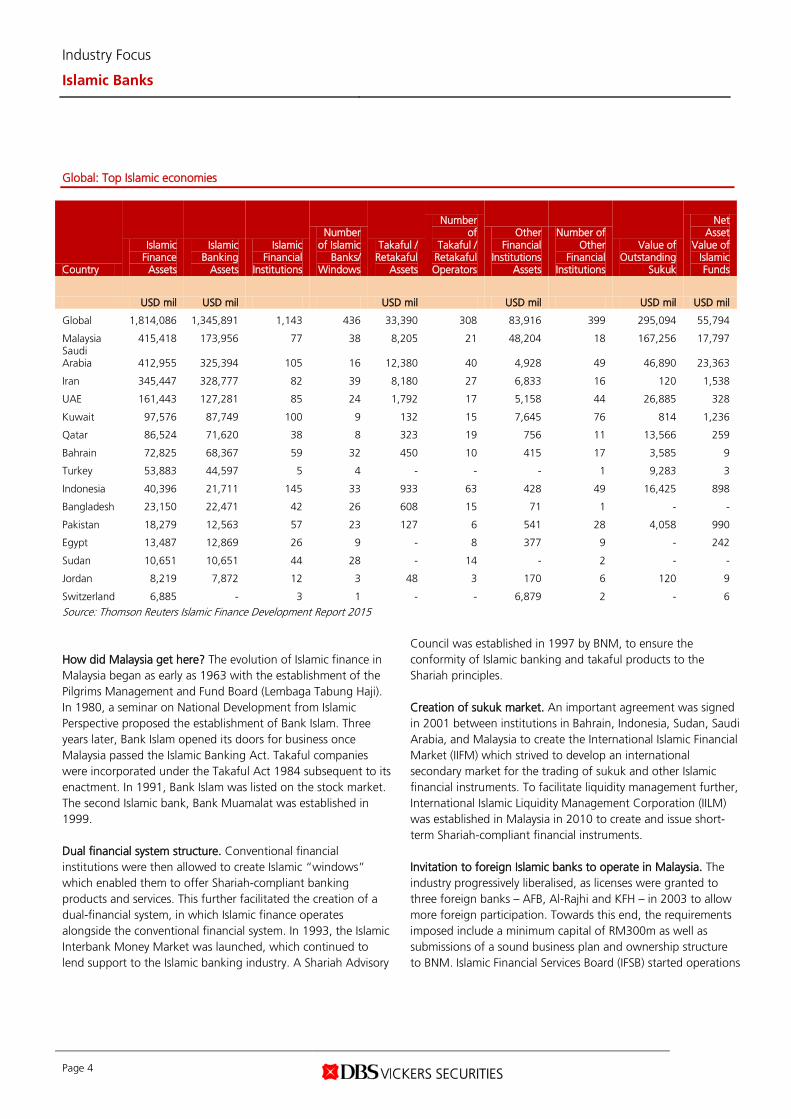

Global: Top Islamic economies

Country

Islamic Finance

Assets

Islamic Banking

Assets

Islamic Financial

Institutions

Number of Islamic

Banks/ Windows

Takaful / Retakaful

Assets

Number of

Takaful / Retakaful Operators

Other Financial

Institutions Assets

Number of Other

Financial Institutions

Value of Outstanding

Sukuk

Net Asset

Value of Islamic Funds

USD mil USD mil USD mil USD mil USD mil USD mil

Global 1,814,086 1,345,891 1,143 436 33,390 308 83,916 399 295,094 55,794

Malaysia 415,418 173,956 77 38 8,205 21 48,204 18 167,256 17,797 Saudi Arabia 412,955 325,394 105 16 12,380 40 4,928 49 46,890 23,363

Iran 345,447 328,777 82 39 8,180 27 6,833 16 120 1,538

UAE 161,443 127,281 85 24 1,792 17 5,158 44 26,885 328

Kuwait 97,576 87,749 100 9 132 15 7,645 76 814 1,236

Qatar 86,524 71,620 38 8 323 19 756 11 13,566 259

Bahrain 72,825 68,367 59 32 450 10 415 17 3,585 9

Turkey 53,883 44,597 5 4 - - - 1 9,283 3

Indonesia 40,396 21,711 145 33 933 63 428 49 16,425 898

Bangladesh 23,150 22,471 42 26 608 15 71 1 - -

Pakistan 18,279 12,563 57 23 127 6 541 28 4,058 990

Egypt 13,487 12,869 26 9 - 8 377 9 - 242

Sudan 10,651 10,651 44 28 - 14 - 2 - -

Jordan 8,219 7,872 12 3 48 3 170 6 120 9

Switzerland 6,885 - 3 1 - - 6,879 2 - 6 Source: Thomson Reuters Islamic Finance Development Report 2015 How did Malaysia get here? The evolution of Islamic finance in Malaysia began as early as 1963 with the establishment of the Pilgrims Management and Fund Board (Lembaga Tabung Haji). In 1980, a seminar on National Development from Islamic Perspective proposed the establishment of Bank Islam. Three years later, Bank Islam opened its doors for business once Malaysia passed the Islamic Banking Act. Takaful companies were incorporated under the Takaful Act 1984 subsequent to its enactment. In 1991, Bank Islam was listed on the stock market. The second Islamic bank, Bank Muamalat was established in 1999. Dual financial system structure. Conventional financial institutions were then allowed to create Islamic “windows” which enabled them to offer Shariah-compliant banking products and services. This further facilitated the creation of a dual-financial system, in which Islamic finance operates alongside the conventional financial system. In 1993, the Islamic Interbank Money Market was launched, which continued to lend support to the Islamic banking industry. A Shariah Advisory

Council was established in 1997 by BNM, to ensure the conformity of Islamic banking and takaful products to the Shariah principles. Creation of sukuk market. An important agreement was signed in 2001 between institutions in Bahrain, Indonesia, Sudan, Saudi Arabia, and Malaysia to create the International Islamic Financial Market (IIFM) which strived to develop an international secondary market for the trading of sukuk and other Islamic financial instruments. To facilitate liquidity management further, International Islamic Liquidity Management Corporation (IILM) was established in Malaysia in 2010 to create and issue short-term Shariah-compliant financial instruments. Invitation to foreign Islamic banks to operate in Malaysia. The industry progressively liberalised, as licenses were granted to three foreign banks – AFB, Al-Rajhi and KFH – in 2003 to allow more foreign participation. Towards this end, the requirements imposed include a minimum capital of RM300m as well as submissions of a sound business plan and ownership structure to BNM. Islamic Financial Services Board (IFSB) started operations

Industry Focus

Islamic Banks

Page 5

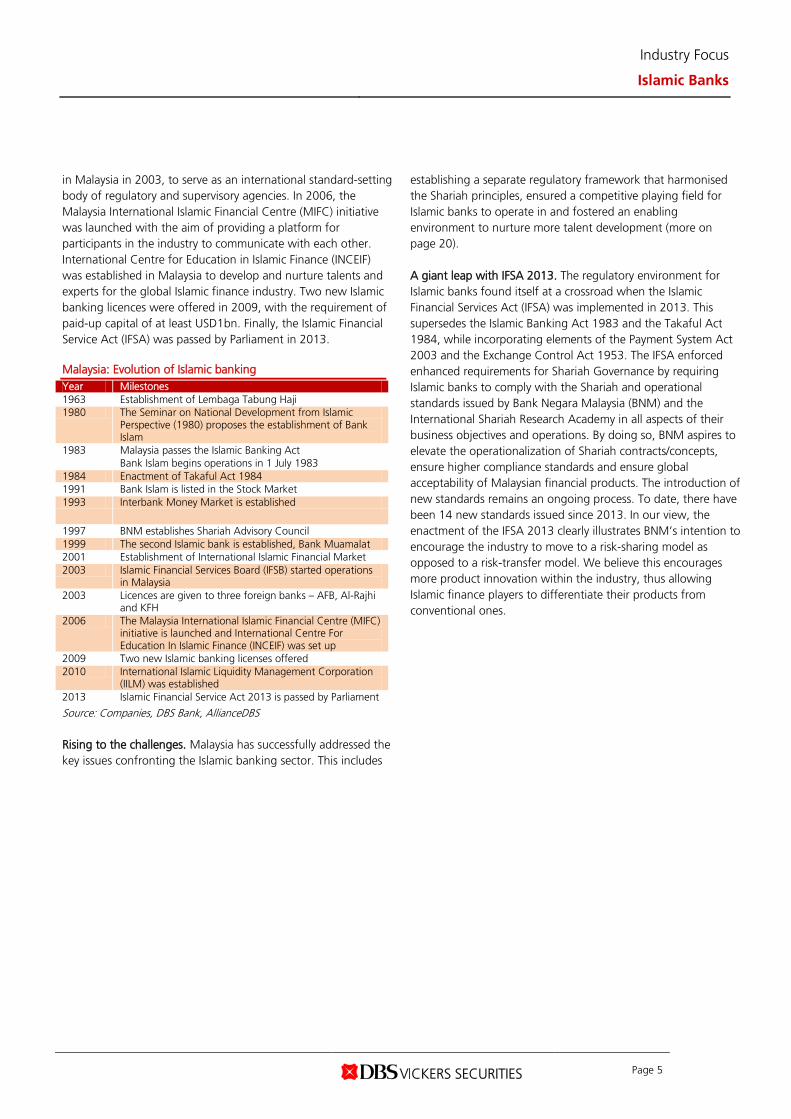

in Malaysia in 2003, to serve as an international standard-setting body of regulatory and supervisory agencies. In 2006, the Malaysia International Islamic Financial Centre (MIFC) initiative was launched with the aim of providing a platform for participants in the industry to communicate with each other. International Centre for Education in Islamic Finance (INCEIF) was established in Malaysia to develop and nurture talents and experts for the global Islamic finance industry. Two new Islamic banking licences were offered in 2009, with the requirement of paid-up capital of at least USD1bn. Finally, the Islamic Financial Service Act (IFSA) was passed by Parliament in 2013. Malaysia: Evolution of Islamic banking Year Milestones 1963 Establishment of Lembaga Tabung Haji 1980 The Seminar on National Development from Islamic

Perspective (1980) proposes the establishment of Bank Islam

1983 Malaysia passes the Islamic Banking Act Bank Islam begins operations in 1 July 1983

1984 Enactment of Takaful Act 1984 1991 Bank Islam is listed in the Stock Market 1993 Interbank Money Market is established

1997 BNM establishes Shariah Advisory Council 1999 The second Islamic bank is established, Bank Muamalat 2001 Establishment of International Islamic Financial Market 2003 Islamic Financial Services Board (IFSB) started operations

in Malaysia 2003 Licences are given to three foreign banks – AFB, Al-Rajhi

and KFH 2006 The Malaysia International Islamic Financial Centre (MIFC)

initiative is launched and International Centre For Education In Islamic Finance (INCEIF) was set up

2009 Two new Islamic banking licenses offered 2010 International Islamic Liquidity Management Corporation

(IILM) was established 2013 Islamic Financial Service Act 2013 is passed by Parliament

Source: Companies, DBS Bank, AllianceDBS Rising to the challenges. Malaysia has successfully addressed the key issues confronting the Islamic banking sector. This includes

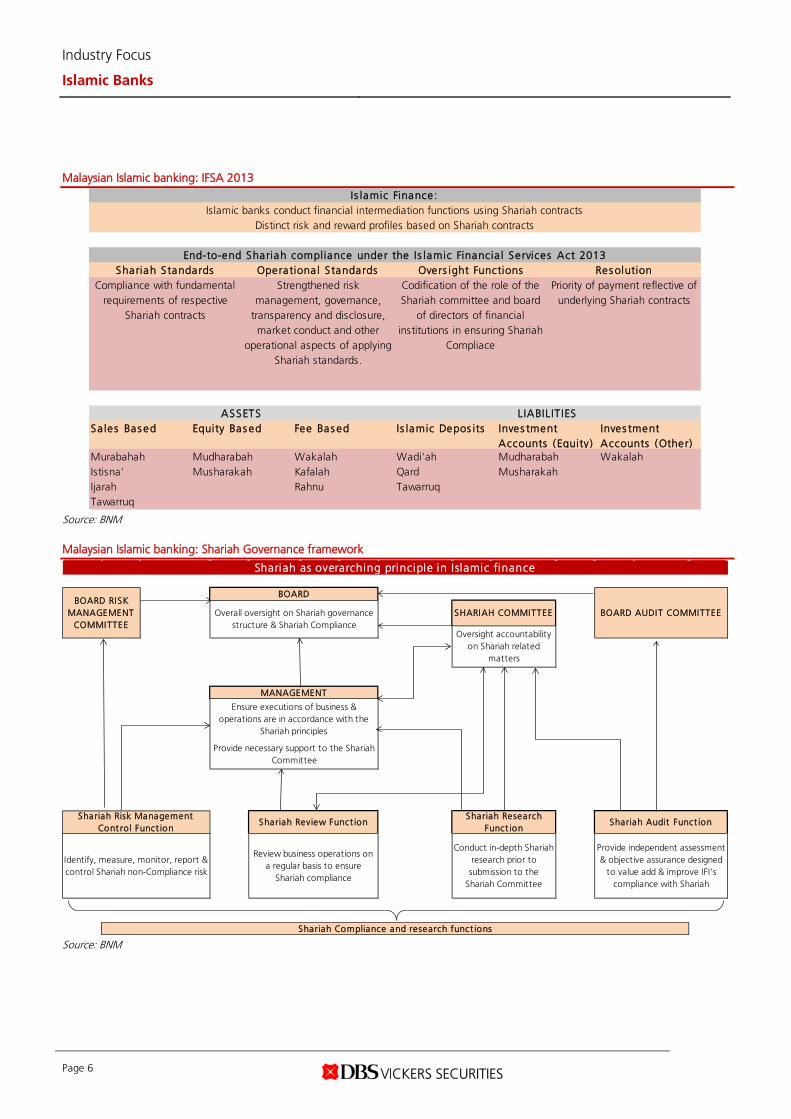

establishing a separate regulatory framework that harmonised the Shariah principles, ensured a competitive playing field for Islamic banks to operate in and fostered an enabling environment to nurture more talent development (more on page 20). A giant leap with IFSA 2013. The regulatory environment for Islamic banks found itself at a crossroad when the Islamic Financial Services Act (IFSA) was implemented in 2013. This supersedes the Islamic Banking Act 1983 and the Takaful Act 1984, while incorporating elements of the Payment System Act 2003 and the Exchange Control Act 1953. The IFSA enforced enhanced requirements for Shariah Governance by requiring Islamic banks to comply with the Shariah and operational standards issued by Bank Negara Malaysia (BNM) and the International Shariah Research Academy in all aspects of their business objectives and operations. By doing so, BNM aspires to elevate the operationalization of Shariah contracts/concepts, ensure higher compliance standards and ensure global acceptability of Malaysian financial products. The introduction of new standards remains an ongoing process. To date, there have been 14 new standards issued since 2013. In our view, the enactment of the IFSA 2013 clearly illustrates BNM’s intention to encourage the industry to move to a risk-sharing model as opposed to a risk-transfer model. We believe this encourages more product innovation within the industry, thus allowing Islamic finance players to differentiate their products from conventional ones.

Industry Focus

Islamic Banks

Page 6

Malaysian Islamic banking: IFSA 2013

Source: BNM Malaysian Islamic banking: Shariah Governance framework

Source: BNM

End-to-end Shariah compliance under the Is lamic Financia l Services Act 2013

Is lamic Finance:Islamic banks conduct financial intermediation functions using Shariah contracts

Distinct risk and reward profiles based on Shariah contracts

ASSETS LIABILIT IES

Shariah StandardsCompliance with fundamental

requirements of respective Shariah contracts

Operationa l S tandardsStrengthened risk

management, governance, transparency and disclosure, market conduct and other

operational aspects of applying Shariah standards.

Overs ight FunctionsCodification of the role of the Shariah committee and board

of directors of financial institutions in ensuring Shariah

Compliace

Res olutionPriority of payment reflective of

underlying Shariah contracts

Inves tment Accounts (Other)Wakalah

Equity Bas ed

MudharabahMusharakah

Tawarruq

Fee Bas ed

WakalahKafalahRahnu

Is lamic Depos its

Wadi'ahQardTawarruq

MudharabahMusharakah

Inves tment Accounts (Equity)

Sa les Bas ed

MurabahahIstisna'Ijarah

BOARD RISK MANAGEMENT

COMMITTEEOverall oversight on Shariah governance

structure & Shariah ComplianceOversight accountability

on Shariah related matters

BOARD AUDIT COMMITTEE

Shariah as overarching principle in Islamic finance

SHARIAH COMMITTEE

BOARD

Provide independent assessment & objective assurance designed

to value add & improve IFI's compliance with Shariah

Shariah Audit Funct ionShariah Research

Funct ion

Conduct in-depth Shariah research prior to submission to the

Shariah Committee

Shariah Compliance and research funct ions

Shariah Review Funct ion

Review business operations on a regular basis to ensure

Shariah compliance

MANAGEMENT

Ensure executions of business & operations are in accordance with the

Shariah principles

Shariah Risk Management Cont ro l Funct ion

Identify, measure, monitor, report & control Shariah non-Compliance risk

Provide necessary support to the Shariah Committee

Industry Focus

Islamic Banks

Page 7

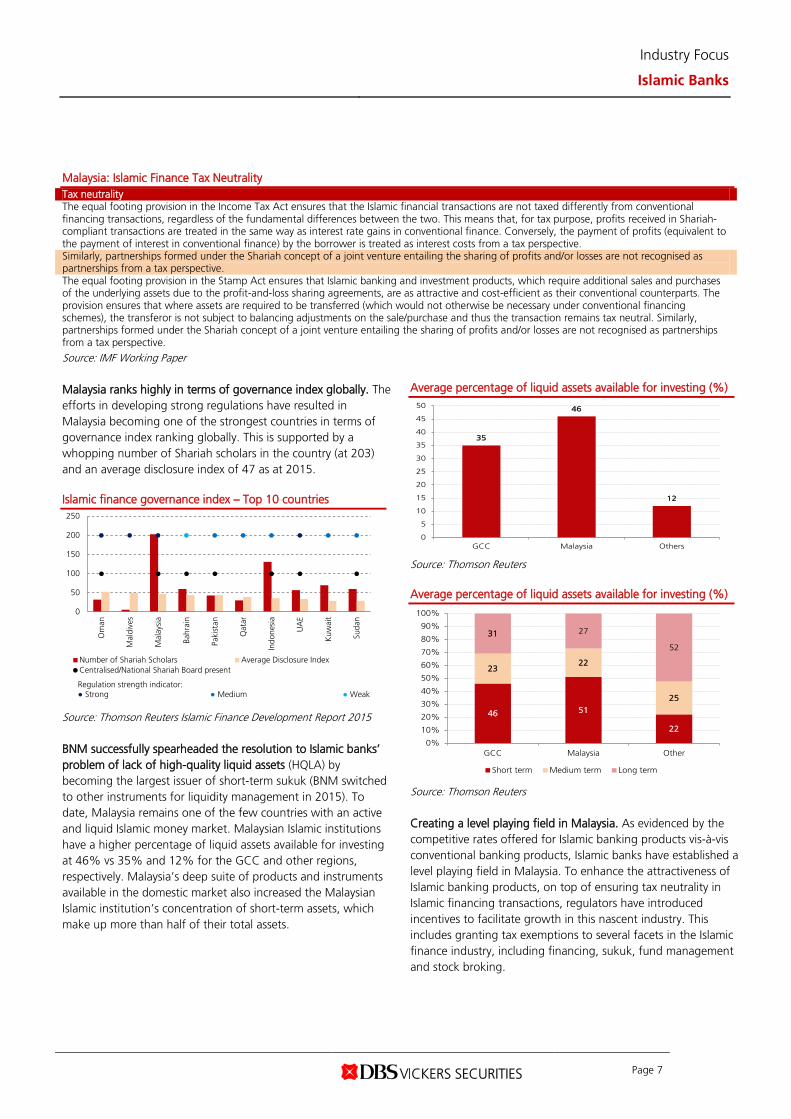

Malaysia: Islamic Finance Tax Neutrality Tax neutrality The equal footing provision in the Income Tax Act ensures that the Islamic financial transactions are not taxed differently from conventional financing transactions, regardless of the fundamental differences between the two. This means that, for tax purpose, profits received in Shariah-compliant transactions are treated in the same way as interest rate gains in conventional finance. Conversely, the payment of profits (equivalent to the payment of interest in conventional finance) by the borrower is treated as interest costs from a tax perspective. Similarly, partnerships formed under the Shariah concept of a joint venture entailing the sharing of profits and/or losses are not recognised as partnerships from a tax perspective. The equal footing provision in the Stamp Act ensures that Islamic banking and investment products, which require additional sales and purchases of the underlying assets due to the profit-and-loss sharing agreements, are as attractive and cost-efficient as their conventional counterparts. The provision ensures that where assets are required to be transferred (which would not otherwise be necessary under conventional financing schemes), the transferor is not subject to balancing adjustments on the sale/purchase and thus the transaction remains tax neutral. Similarly, partnerships formed under the Shariah concept of a joint venture entailing the sharing of profits and/or losses are not recognised as partnerships from a tax perspective. Source: IMF Working Paper Malaysia ranks highly in terms of governance index globally. The efforts in developing strong regulations have resulted in Malaysia becoming one of the strongest countries in terms of governance index ranking globally. This is supported by a whopping number of Shariah scholars in the country (at 203) and an average disclosure index of 47 as at 2015. Islamic finance governance index – Top 10 countries

Source: Thomson Reuters Islamic Finance Development Report 2015 BNM successfully spearheaded the resolution to Islamic banks’ problem of lack of high-quality liquid assets (HQLA) by becoming the largest issuer of short-term sukuk (BNM switched to other instruments for liquidity management in 2015). To date, Malaysia remains one of the few countries with an active and liquid Islamic money market. Malaysian Islamic institutions have a higher percentage of liquid assets available for investing at 46% vs 35% and 12% for the GCC and other regions, respectively. Malaysia’s deep suite of products and instruments available in the domestic market also increased the Malaysian Islamic institution’s concentration of short-term assets, which make up more than half of their total assets.

Average percentage of liquid assets available for investing (%)

Source: Thomson Reuters Average percentage of liquid assets available for investing (%)

Source: Thomson Reuters Creating a level playing field in Malaysia. As evidenced by the competitive rates offered for Islamic banking products vis-à-vis conventional banking products, Islamic banks have established a level playing field in Malaysia. To enhance the attractiveness of Islamic banking products, on top of ensuring tax neutrality in Islamic financing transactions, regulators have introduced incentives to facilitate growth in this nascent industry. This includes granting tax exemptions to several facets in the Islamic finance industry, including financing, sukuk, fund management and stock broking.

0

50

100

150

200

250

0

50

100

150

200

250

Om

an

Mal

dive

s

Mal

aysi

a

Bahr

ain

Paki

stan

Qat

ar

Indo

nesi

a

UA

E

Kuw

ait

Suda

n

Number of Shariah Scholars Average Disclosure IndexCentralised/National Shariah Board present

Regulation strength indicator:● Strong ● Medium ● Weak

35

46

12

0

5

10

15

20

25

30

35

40

45

50

GCC Malaysia Others

46 51

22

2322

25

31 27

52

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

GCC Malaysia Other

Short term Medium term Long term

Industry Focus

Islamic Banks

Page 8

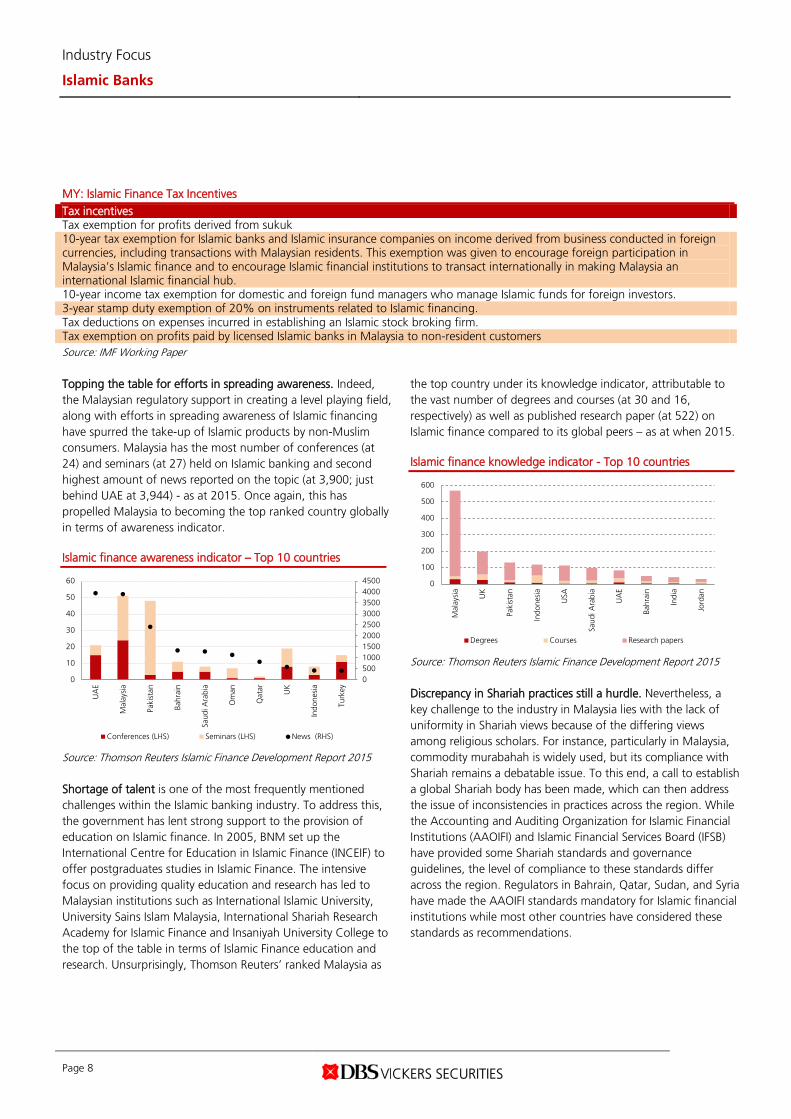

MY: Islamic Finance Tax Incentives Tax incentives Tax exemption for profits derived from sukuk 10-year tax exemption for Islamic banks and Islamic insurance companies on income derived from business conducted in foreign currencies, including transactions with Malaysian residents. This exemption was given to encourage foreign participation in Malaysia’s Islamic finance and to encourage Islamic financial institutions to transact internationally in making Malaysia an international Islamic financial hub. 10-year income tax exemption for domestic and foreign fund managers who manage Islamic funds for foreign investors. 3-year stamp duty exemption of 20% on instruments related to Islamic financing. Tax deductions on expenses incurred in establishing an Islamic stock broking firm. Tax exemption on profits paid by licensed Islamic banks in Malaysia to non-resident customers Source: IMF Working Paper Topping the table for efforts in spreading awareness. Indeed, the Malaysian regulatory support in creating a level playing field, along with efforts in spreading awareness of Islamic financing have spurred the take-up of Islamic products by non-Muslim consumers. Malaysia has the most number of conferences (at 24) and seminars (at 27) held on Islamic banking and second highest amount of news reported on the topic (at 3,900; just behind UAE at 3,944) - as at 2015. Once again, this has propelled Malaysia to becoming the top ranked country globally in terms of awareness indicator. Islamic finance awareness indicator – Top 10 countries

Source: Thomson Reuters Islamic Finance Development Report 2015 Shortage of talent is one of the most frequently mentioned challenges within the Islamic banking industry. To address this, the government has lent strong support to the provision of education on Islamic finance. In 2005, BNM set up the International Centre for Education in Islamic Finance (INCEIF) to offer postgraduates studies in Islamic Finance. The intensive focus on providing quality education and research has led to Malaysian institutions such as International Islamic University, University Sains Islam Malaysia, International Shariah Research Academy for Islamic Finance and Insaniyah University College to the top of the table in terms of Islamic Finance education and research. Unsurprisingly, Thomson Reuters’ ranked Malaysia as

the top country under its knowledge indicator, attributable to the vast number of degrees and courses (at 30 and 16, respectively) as well as published research paper (at 522) on Islamic finance compared to its global peers – as at when 2015. Islamic finance knowledge indicator - Top 10 countries

Source: Thomson Reuters Islamic Finance Development Report 2015 Discrepancy in Shariah practices still a hurdle. Nevertheless, a key challenge to the industry in Malaysia lies with the lack of uniformity in Shariah views because of the differing views among religious scholars. For instance, particularly in Malaysia, commodity murabahah is widely used, but its compliance with Shariah remains a debatable issue. To this end, a call to establish a global Shariah body has been made, which can then address the issue of inconsistencies in practices across the region. While the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) and Islamic Financial Services Board (IFSB) have provided some Shariah standards and governance guidelines, the level of compliance to these standards differ across the region. Regulators in Bahrain, Qatar, Sudan, and Syria have made the AAOIFI standards mandatory for Islamic financial institutions while most other countries have considered these standards as recommendations.

050010001500200025003000350040004500

0

10

20

30

40

50

60

UA

E

Mal

aysi

a

Paki

stan

Bahr

ain

Saud

i Ara

bia

Om

an

Qat

ar UK

Indo

nesi

a

Turk

ey

Conferences (LHS) Seminars (LHS) News (RHS)

0

100

200

300

400

500

600

Mal

aysi

a

UK

Paki

stan

Indo

nesi

a

USA

Saud

i Ara

bia

UA

E

Bahr

ain

Indi

a

Jord

an

Degrees Courses Research papers

Industry Focus

Islamic Banks

Page 9

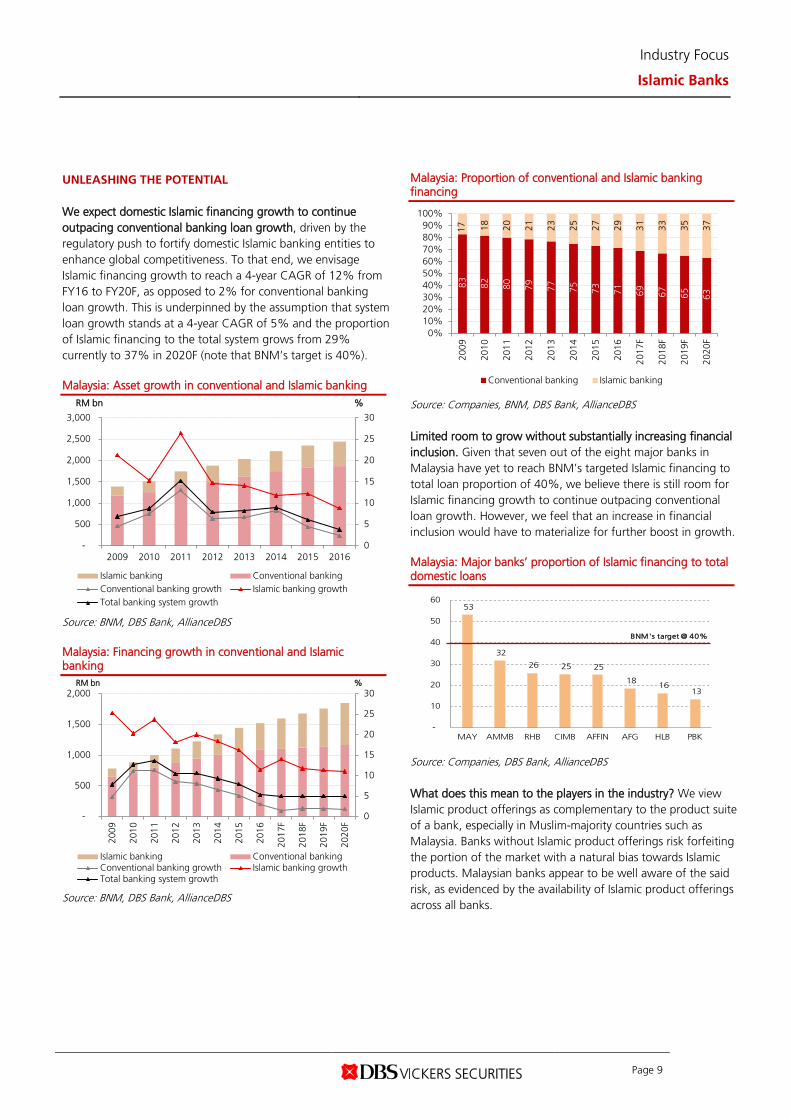

UNLEASHING THE POTENTIAL We expect domestic Islamic financing growth to continue outpacing conventional banking loan growth, driven by the regulatory push to fortify domestic Islamic banking entities to enhance global competitiveness. To that end, we envisage Islamic financing growth to reach a 4-year CAGR of 12% from FY16 to FY20F, as opposed to 2% for conventional banking loan growth. This is underpinned by the assumption that system loan growth stands at a 4-year CAGR of 5% and the proportion of Islamic financing to the total system grows from 29% currently to 37% in 2020F (note that BNM’s target is 40%). Malaysia: Asset growth in conventional and Islamic banking

Source: BNM, DBS Bank, AllianceDBS Malaysia: Financing growth in conventional and Islamic banking

Source: BNM, DBS Bank, AllianceDBS

Malaysia: Proportion of conventional and Islamic banking financing

Source: Companies, BNM, DBS Bank, AllianceDBS Limited room to grow without substantially increasing financial inclusion. Given that seven out of the eight major banks in Malaysia have yet to reach BNM’s targeted Islamic financing to total loan proportion of 40%, we believe there is still room for Islamic financing growth to continue outpacing conventional loan growth. However, we feel that an increase in financial inclusion would have to materialize for further boost in growth. Malaysia: Major banks’ proportion of Islamic financing to total domestic loans

Source: Companies, DBS Bank, AllianceDBS What does this mean to the players in the industry? We view Islamic product offerings as complementary to the product suite of a bank, especially in Muslim-majority countries such as Malaysia. Banks without Islamic product offerings risk forfeiting the portion of the market with a natural bias towards Islamic products. Malaysian banks appear to be well aware of the said risk, as evidenced by the availability of Islamic product offerings across all banks.

0

5

10

15

20

25

30

-

500

1,000

1,500

2,000

2,500

3,000

2009 2010 2011 2012 2013 2014 2015 2016

%RM bn

Islamic banking Conventional bankingConventional banking growth Islamic banking growthTotal banking system growth

0

5

10

15

20

25

30

-

500

1,000

1,500

2,000

2009

2010

2011

2012

2013

2014

2015

2016

2017

F

2018

F

2019

F

2020

F

%RM bn

Islamic banking Conventional bankingConventional banking growth Islamic banking growthTotal banking system growth

83

82

80

79

77

75

73

71

69

67

65

63

17

18

20

21

23

25

27

29

31

33

35

37

0%10%20%30%40%50%60%70%80%90%

100%

2009

2010

2011

2012

2013

2014

2015

2016

2017

F

2018

F

2019

F

2020

F

Conventional banking Islamic banking

53

32

26 25 25

18 16 13

-

10

20

30

40

50

60

MAY AMMB RHB CIMB AFFIN AFG HLB PBK

BNM's target @ 40%

Industry Focus

Islamic Banks

Page 10

Challenging to improve financial inclusion with current product offering. According to the Global Findex by World Bank, while the percentage of Malaysian population that owns an account in financial institutions stands at 81%, the percentage of Malaysian population that has borrowed from a financial institution is only at 20% in 2014. We believe further improvement in access to borrowing is challenging, as the current product offering has limited suitability for the remaining portion of the unserved population. However, product innovation could act as the game changer in this aspect as new offerings could increasingly meet the different risk and return requirements of this dissimilar segment of consumers. Product innovation will be the game changer for the Islamic banking industry... Currently, Islamic products largely mirror their conventional equivalents, rendering minimal product differentiation between the two models. However, since the implementation of IFSA 2013 which encouraged a move towards a risk-sharing model (from risk-transfer model), we have seen some developments on the product innovation aspect. For example, a new guideline on distinguishing Islamic deposits and investment accounts was introduced in early 2013, with the aim of improving the alignment of the salient features of Shariah contracts to its legal recognition. Consequently, Islamic banks now offer investment accounts as an additional alternative on top of the typical current account, savings account and term deposit products. ..especially with sufficient consumer education. Insufficient education on these products could result in customers finding difficulty in accepting the differences of the new product offerings. In the case of investment accounts, despite higher returns to compensate for the higher risk assigned, differences such as the absence of principal guarantee, loss of insurance deposit coverage and the additional disclosure requirements and terminologies pose a risk of a customer exodus back to more familiar conventional products. Nonetheless, in our view, it is crucial for Islamic banks to take this risk in order to enable differentiation from banks operating under the conventional model. Hence, the ability of Islamic banks in executing this is the critical success factor of the industry. We expect the industry’s ability to offer a wider range of products to meet risk and return requirements of consumers, to serve as a stepping-stone in producing “real growth” (as opposed to displacement of conventional loan growth) in Islamic financing. Hence, we advise investors to keep a lookout for developments in this space. Digital disruption or enabler? Digital disruption has indeed intensified in the past few years, with services such as crowdfunding and peer-to-peer lending gradually creeping into the banking industry. Notably, these alternatives are based on a

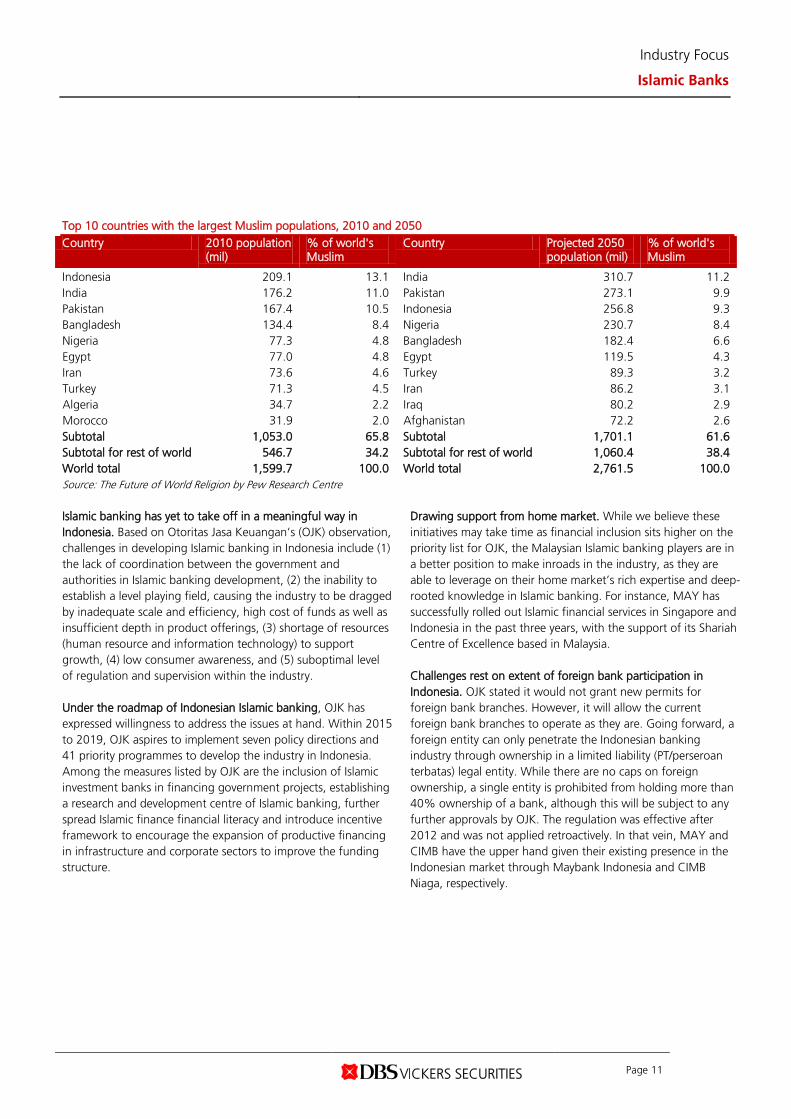

risk-sharing model, which overlaps with the premise of Islamic banking. In peer-to-peer lending and crowdfunding, lenders are matched directly to the borrowers. To that end, we opine that these new digital innovations have opened up more alternatives for the Islamic banks, in particular to embark on more product innovation and align its products and services more towards the true spirit of Islamic banking. Case in point: Investment account platform. We have seen Islamic banks riding the digital wave through the launch of the Investment Account Platform (IAP; more on page 13). The IAP works in the same vein as a crowdfunding platform where investors can participate in the funding of ventures or projects by making monetary contributions to the projects listed on the platform. The key factor distinguishing IAP from other technology-based fund raising platforms lies in the intermediation roles played by the Islamic banks (for e.g., due-diligence, performance monitoring, suitability assessment and investment management). While other fund raising platforms largely feature ventures by SMEs and start-ups, the IAP also includes ventures by listed companies and multinational companies. Independent ratings are also provided to facilitate the users’ investment decisions. IAP yet to gain traction. There are four sponsoring banks (MAY ISL, AFFIN ISL, Bank Islam, Bank Muamalat) involved in the IAP, but to date, only three projects have been listed on the IAP (since its launch in Feb 2016). Nevertheless, we expect this platform to gain traction in the near future as participating banks have expressed keen interest in improving the flow of project listing. Regionalising Islamic banking products and services is the other engine to fire up. Another growth lever for Islamic finance lies in the ability of Islamic banking players to leverage on the strong regulatory support from domestic authorities, to extend their presence regionally to countries whose Islamic finance industry remains under-developed and banking penetration remains low. Consistently, we still expect the successful aforementioned product innovation to be the key success factor in fuelling substantial growth traction within the region. Case in point: Indonesia. The closest market for the Malaysian Islamic bank players to explore is the Indonesian market. With 13% of the world’s Muslim population, Indonesia is the world’s most populous Muslim nation (209.1m Muslim population as at 2010). Banking penetration in terms of both conventional and Islamic is low (13% of population have borrowed from a financial institution, 5% of total banking assets are Islamic), thus implying ample room for growth.

Industry Focus

Islamic Banks

Page 11

Top 10 countries with the largest Muslim populations, 2010 and 2050 Country 2010 population

(mil) % of world's Muslim

Country Projected 2050 population (mil)

% of world's Muslim

Indonesia 209.1 13.1 India 310.7 11.2 India 176.2 11.0 Pakistan 273.1 9.9 Pakistan 167.4 10.5 Indonesia 256.8 9.3 Bangladesh 134.4 8.4 Nigeria 230.7 8.4 Nigeria 77.3 4.8 Bangladesh 182.4 6.6 Egypt 77.0 4.8 Egypt 119.5 4.3 Iran 73.6 4.6 Turkey 89.3 3.2 Turkey 71.3 4.5 Iran 86.2 3.1 Algeria 34.7 2.2 Iraq 80.2 2.9 Morocco 31.9 2.0 Afghanistan 72.2 2.6 Subtotal 1,053.0 65.8 Subtotal 1,701.1 61.6 Subtotal for rest of world 546.7 34.2 Subtotal for rest of world 1,060.4 38.4 World total 1,599.7 100.0 World total 2,761.5 100.0 Source: The Future of World Religion by Pew Research Centre Islamic banking has yet to take off in a meaningful way in Indonesia. Based on Otoritas Jasa Keuangan’s (OJK) observation, challenges in developing Islamic banking in Indonesia include (1) the lack of coordination between the government and authorities in Islamic banking development, (2) the inability to establish a level playing field, causing the industry to be dragged by inadequate scale and efficiency, high cost of funds as well as insufficient depth in product offerings, (3) shortage of resources (human resource and information technology) to support growth, (4) low consumer awareness, and (5) suboptimal level of regulation and supervision within the industry. Under the roadmap of Indonesian Islamic banking, OJK has expressed willingness to address the issues at hand. Within 2015 to 2019, OJK aspires to implement seven policy directions and 41 priority programmes to develop the industry in Indonesia. Among the measures listed by OJK are the inclusion of Islamic investment banks in financing government projects, establishing a research and development centre of Islamic banking, further spread Islamic finance financial literacy and introduce incentive framework to encourage the expansion of productive financing in infrastructure and corporate sectors to improve the funding structure.

Drawing support from home market. While we believe these initiatives may take time as financial inclusion sits higher on the priority list for OJK, the Malaysian Islamic banking players are in a better position to make inroads in the industry, as they are able to leverage on their home market’s rich expertise and deep-rooted knowledge in Islamic banking. For instance, MAY has successfully rolled out Islamic financial services in Singapore and Indonesia in the past three years, with the support of its Shariah Centre of Excellence based in Malaysia. Challenges rest on extent of foreign bank participation in Indonesia. OJK stated it would not grant new permits for foreign bank branches. However, it will allow the current foreign bank branches to operate as they are. Going forward, a foreign entity can only penetrate the Indonesian banking industry through ownership in a limited liability (PT/perseroan terbatas) legal entity. While there are no caps on foreign ownership, a single entity is prohibited from holding more than 40% ownership of a bank, although this will be subject to any further approvals by OJK. The regulation was effective after 2012 and was not applied retroactively. In that vein, MAY and CIMB have the upper hand given their existing presence in the Indonesian market through Maybank Indonesia and CIMB Niaga, respectively.

Industry Focus

Islamic Banks

Page 12

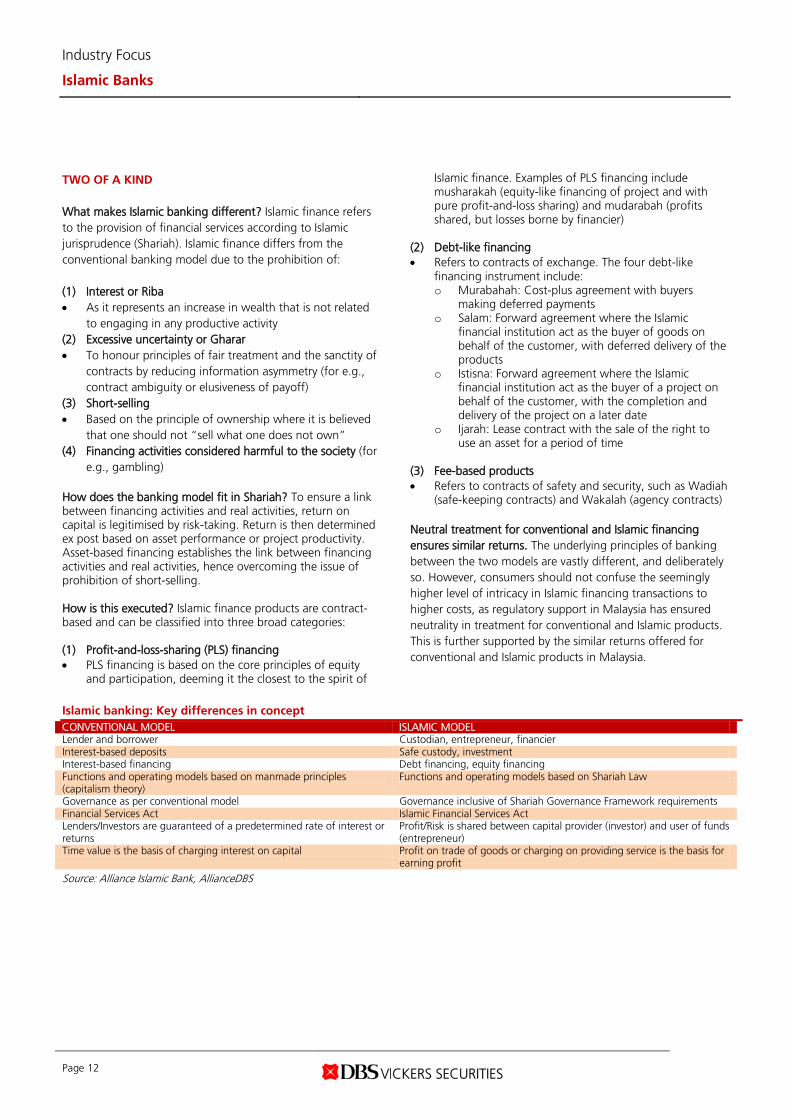

TWO OF A KIND What makes Islamic banking different? Islamic finance refers to the provision of financial services according to Islamic jurisprudence (Shariah). Islamic finance differs from the conventional banking model due to the prohibition of: (1) Interest or Riba • As it represents an increase in wealth that is not related

to engaging in any productive activity (2) Excessive uncertainty or Gharar • To honour principles of fair treatment and the sanctity of

contracts by reducing information asymmetry (for e.g., contract ambiguity or elusiveness of payoff)

(3) Short-selling • Based on the principle of ownership where it is believed

that one should not “sell what one does not own” (4) Financing activities considered harmful to the society (for

e.g., gambling)

How does the banking model fit in Shariah? To ensure a link between financing activities and real activities, return on capital is legitimised by risk-taking. Return is then determined ex post based on asset performance or project productivity. Asset-based financing establishes the link between financing activities and real activities, hence overcoming the issue of prohibition of short-selling. How is this executed? Islamic finance products are contract-based and can be classified into three broad categories: (1) Profit-and-loss-sharing (PLS) financing • PLS financing is based on the core principles of equity

and participation, deeming it the closest to the spirit of

Islamic finance. Examples of PLS financing include musharakah (equity-like financing of project and with pure profit-and-loss sharing) and mudarabah (profits shared, but losses borne by financier)

(2) Debt-like financing • Refers to contracts of exchange. The four debt-like

financing instrument include: o Murabahah: Cost-plus agreement with buyers

making deferred payments o Salam: Forward agreement where the Islamic

financial institution act as the buyer of goods on behalf of the customer, with deferred delivery of the products

o Istisna: Forward agreement where the Islamic financial institution act as the buyer of a project on behalf of the customer, with the completion and delivery of the project on a later date

o Ijarah: Lease contract with the sale of the right to use an asset for a period of time

(3) Fee-based products • Refers to contracts of safety and security, such as Wadiah

(safe-keeping contracts) and Wakalah (agency contracts) Neutral treatment for conventional and Islamic financing ensures similar returns. The underlying principles of banking between the two models are vastly different, and deliberately so. However, consumers should not confuse the seemingly higher level of intricacy in Islamic financing transactions to higher costs, as regulatory support in Malaysia has ensured neutrality in treatment for conventional and Islamic products. This is further supported by the similar returns offered for conventional and Islamic products in Malaysia.

Islamic banking: Key differences in concept CONVENTIONAL MODEL ISLAMIC MODEL Lender and borrower Custodian, entrepreneur, financier Interest-based deposits Safe custody, investment Interest-based financing Debt financing, equity financing Functions and operating models based on manmade principles (capitalism theory)

Functions and operating models based on Shariah Law

Governance as per conventional model Governance inclusive of Shariah Governance Framework requirements Financial Services Act Islamic Financial Services Act Lenders/Investors are guaranteed of a predetermined rate of interest or returns

Profit/Risk is shared between capital provider (investor) and user of funds (entrepreneur)

Time value is the basis of charging interest on capital Profit on trade of goods or charging on providing service is the basis for earning profit

Source: Alliance Islamic Bank, AllianceDBS

Industry Focus

Islamic Banks

Page 13

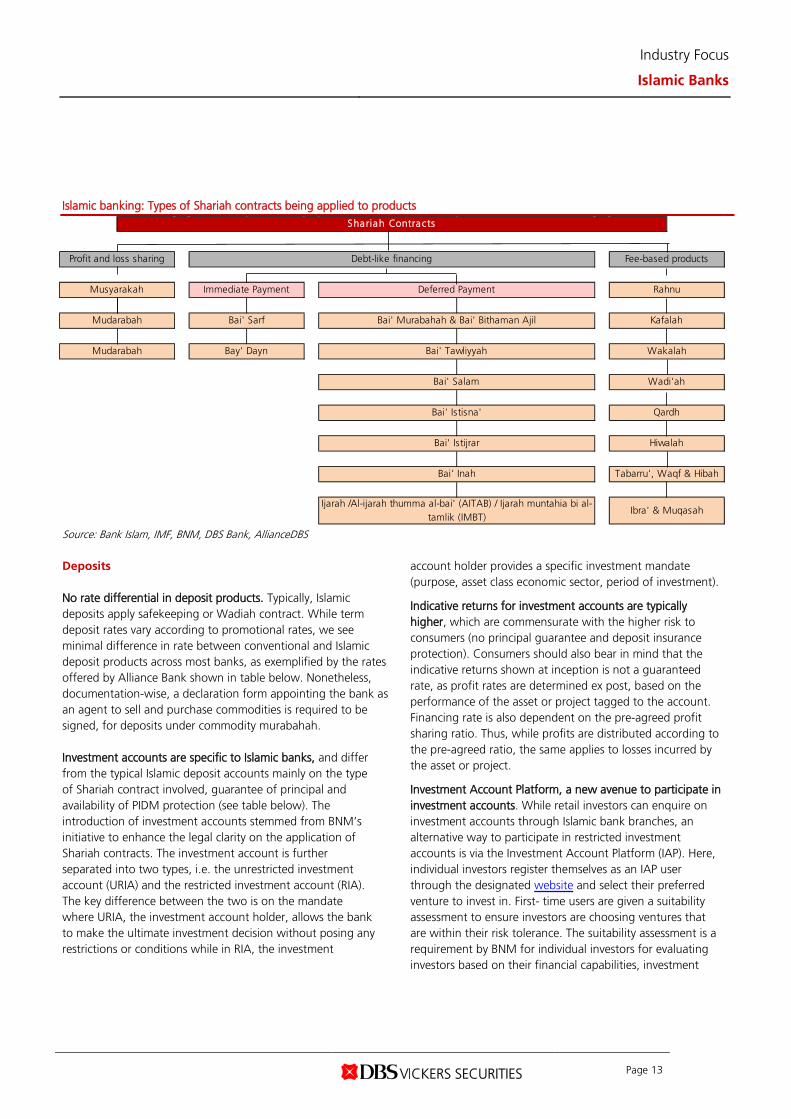

Islamic banking: Types of Shariah contracts being applied to products

Source: Bank Islam, IMF, BNM, DBS Bank, AllianceDBS Deposits No rate differential in deposit products. Typically, Islamic deposits apply safekeeping or Wadiah contract. While term deposit rates vary according to promotional rates, we see minimal difference in rate between conventional and Islamic deposit products across most banks, as exemplified by the rates offered by Alliance Bank shown in table below. Nonetheless, documentation-wise, a declaration form appointing the bank as an agent to sell and purchase commodities is required to be signed, for deposits under commodity murabahah. Investment accounts are specific to Islamic banks, and differ from the typical Islamic deposit accounts mainly on the type of Shariah contract involved, guarantee of principal and availability of PIDM protection (see table below). The introduction of investment accounts stemmed from BNM’s initiative to enhance the legal clarity on the application of Shariah contracts. The investment account is further separated into two types, i.e. the unrestricted investment account (URIA) and the restricted investment account (RIA). The key difference between the two is on the mandate where URIA, the investment account holder, allows the bank to make the ultimate investment decision without posing any restrictions or conditions while in RIA, the investment

account holder provides a specific investment mandate (purpose, asset class economic sector, period of investment).

Indicative returns for investment accounts are typically higher, which are commensurate with the higher risk to consumers (no principal guarantee and deposit insurance protection). Consumers should also bear in mind that the indicative returns shown at inception is not a guaranteed rate, as profit rates are determined ex post, based on the performance of the asset or project tagged to the account. Financing rate is also dependent on the pre-agreed profit sharing ratio. Thus, while profits are distributed according to the pre-agreed ratio, the same applies to losses incurred by the asset or project.

Investment Account Platform, a new avenue to participate in investment accounts. While retail investors can enquire on investment accounts through Islamic bank branches, an alternative way to participate in restricted investment accounts is via the Investment Account Platform (IAP). Here, individual investors register themselves as an IAP user through the designated website and select their preferred venture to invest in. First- time users are given a suitability assessment to ensure investors are choosing ventures that are within their risk tolerance. The suitability assessment is a requirement by BNM for individual investors for evaluating investors based on their financial capabilities, investment

Shariah Contracts

Wadi'ah

Qardh

Hiwalah

Mudarabah

Mudarabah

Fee-based productsProfit and loss sharing

Deferred PaymentImmediate PaymentMusyarakah Rahnu

Debt-like financing

Bai' Sarf

Bay' Dayn

Ibra' & Muqasah

Bai' Murabahah & Bai' Bithaman Ajil

Bai' Tawliyyah

Bai' Salam

Bai' Istisna'

Bai' Istijrar

Kafalah

Wakalah

Ijarah /Al-ijarah thumma al-bai' (AITAB) / Ijarah muntahia bi al-tamlik (IMBT)

Tabarru', Waqf & HibahBai' Inah

Industry Focus

Islamic Banks

Page 14

needs and appetite, and investment knowledge and experience. Institutional investors are not required to take the suitability assessment as they are deemed to have sufficient resources to make an informed investment decision. Upon completion of the suitability assessment, the results are compared against the chosen venture. Investors who have chosen ventures beyond their risk tolerance will be alerted and asked to seek additional consultation at dedicated branches of participating Islamic banks before proceeding with the chosen venture. Once the investor declares an understanding of the risk involved and agrees to proceed with the investment, the Islamic bank creates the

investment account for the investor and sends periodical reports on the venture.

Impact to the banks. Although banks provide better returns to the customers under the investment accounts, the benefits to the bank comes in the form of (1) savings from non-payment of Malaysia Deposit Insurance Corporation (PIDM) premium, (2) more effective capital management as tagged assets are excluded from capital adequacy ratio calculation, and (3) reduced regulatory cost as investment accounts are excluded from Eligible Liabilities base for the purposes of statutory reserve requirement computations.

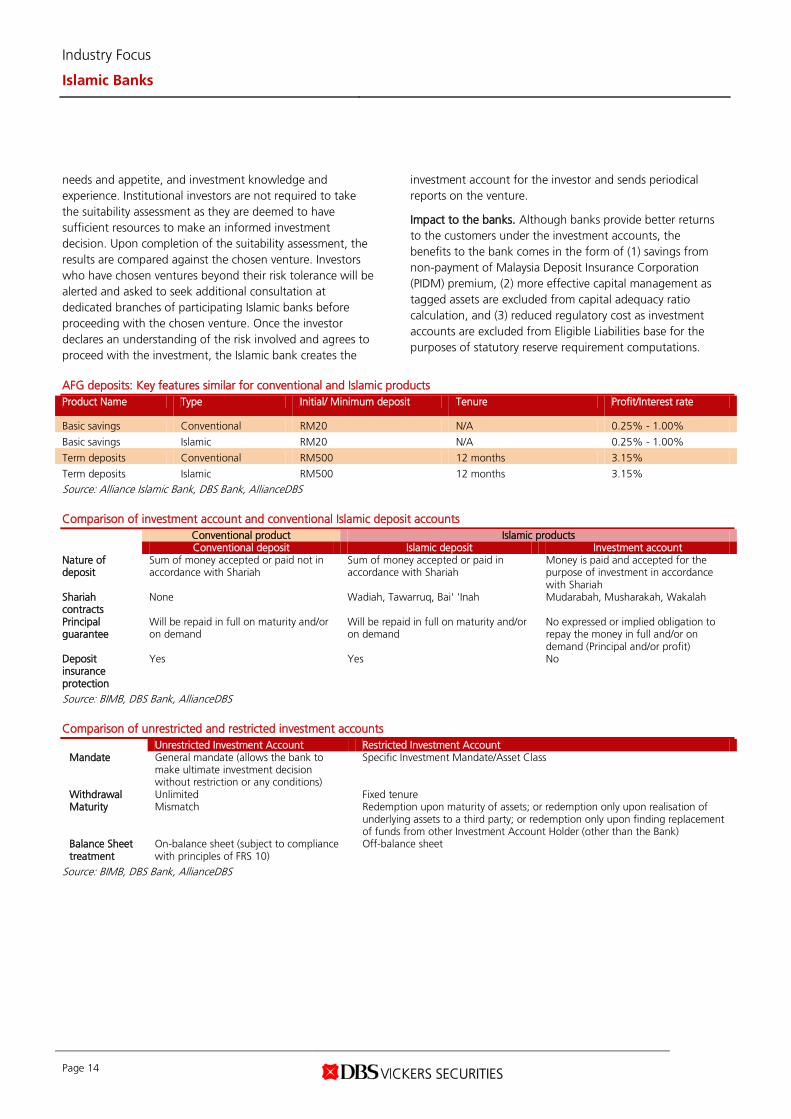

AFG deposits: Key features similar for conventional and Islamic products Product Name Type Initial/ Minimum deposit Tenure Profit/Interest rate

Basic savings Conventional RM20 N/A 0.25% - 1.00%

Basic savings Islamic RM20 N/A 0.25% - 1.00%

Term deposits Conventional RM500 12 months 3.15%

Term deposits Islamic RM500 12 months 3.15% Source: Alliance Islamic Bank, DBS Bank, AllianceDBS Comparison of investment account and conventional Islamic deposit accounts

Conventional product Islamic products

Conventional deposit Islamic deposit Investment account

Nature of deposit

Sum of money accepted or paid not in accordance with Shariah

Sum of money accepted or paid in accordance with Shariah

Money is paid and accepted for the purpose of investment in accordance with Shariah

Shariah contracts

None Wadiah, Tawarruq, Bai' 'Inah Mudarabah, Musharakah, Wakalah

Principal guarantee

Will be repaid in full on maturity and/or on demand

Will be repaid in full on maturity and/or on demand

No expressed or implied obligation to repay the money in full and/or on demand (Principal and/or profit)

Deposit insurance protection

Yes Yes No

Source: BIMB, DBS Bank, AllianceDBS Comparison of unrestricted and restricted investment accounts

Unrestricted Investment Account Restricted Investment Account

Mandate General mandate (allows the bank to make ultimate investment decision without restriction or any conditions)

Specific Investment Mandate/Asset Class

Withdrawal Unlimited Fixed tenure Maturity Mismatch Redemption upon maturity of assets; or redemption only upon realisation of

underlying assets to a third party; or redemption only upon finding replacement of funds from other Investment Account Holder (other than the Bank)

Balance Sheet treatment

On-balance sheet (subject to compliance with principles of FRS 10)

Off-balance sheet

Source: BIMB, DBS Bank, AllianceDBS

Industry Focus

Islamic Banks

Page 15

Financing

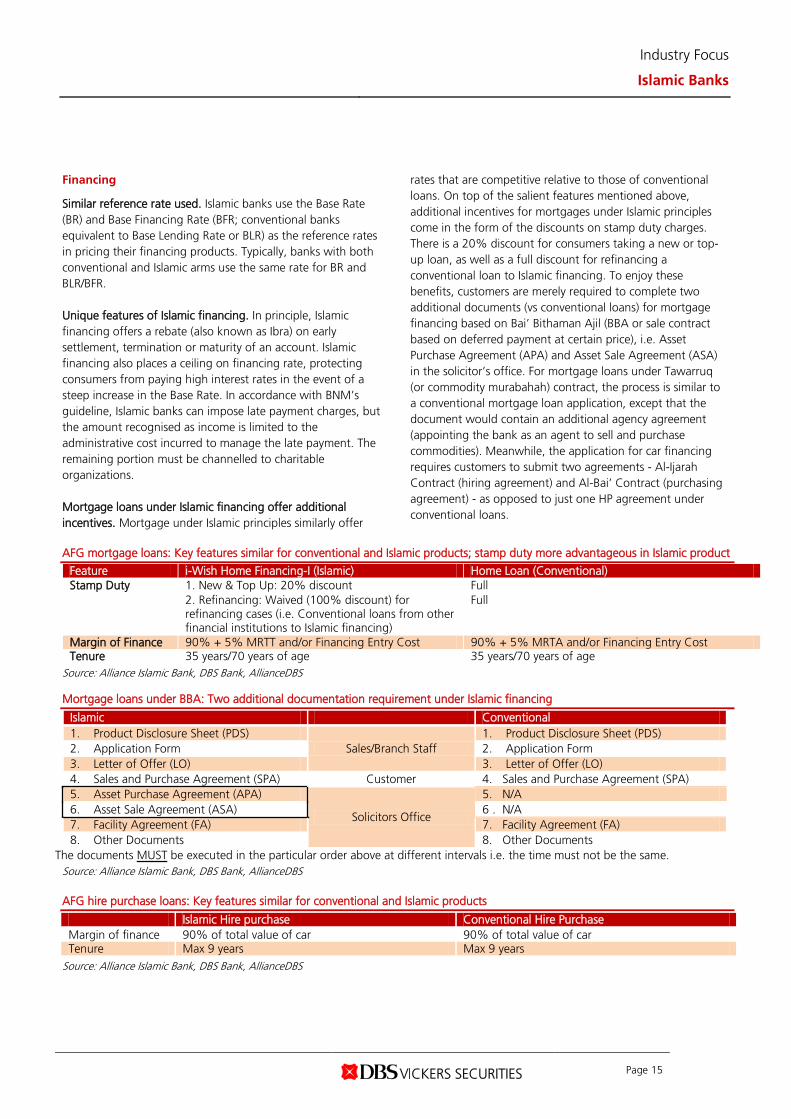

Similar reference rate used. Islamic banks use the Base Rate (BR) and Base Financing Rate (BFR; conventional banks equivalent to Base Lending Rate or BLR) as the reference rates in pricing their financing products. Typically, banks with both conventional and Islamic arms use the same rate for BR and BLR/BFR. Unique features of Islamic financing. In principle, Islamic financing offers a rebate (also known as Ibra) on early settlement, termination or maturity of an account. Islamic financing also places a ceiling on financing rate, protecting consumers from paying high interest rates in the event of a steep increase in the Base Rate. In accordance with BNM’s guideline, Islamic banks can impose late payment charges, but the amount recognised as income is limited to the administrative cost incurred to manage the late payment. The remaining portion must be channelled to charitable organizations. Mortgage loans under Islamic financing offer additional incentives. Mortgage under Islamic principles similarly offer

rates that are competitive relative to those of conventional loans. On top of the salient features mentioned above, additional incentives for mortgages under Islamic principles come in the form of the discounts on stamp duty charges. There is a 20% discount for consumers taking a new or top- up loan, as well as a full discount for refinancing a conventional loan to Islamic financing. To enjoy these benefits, customers are merely required to complete two additional documents (vs conventional loans) for mortgage financing based on Bai’ Bithaman Ajil (BBA or sale contract based on deferred payment at certain price), i.e. Asset Purchase Agreement (APA) and Asset Sale Agreement (ASA) in the solicitor’s office. For mortgage loans under Tawarruq (or commodity murabahah) contract, the process is similar to a conventional mortgage loan application, except that the document would contain an additional agency agreement (appointing the bank as an agent to sell and purchase commodities). Meanwhile, the application for car financing requires customers to submit two agreements - Al-Ijarah Contract (hiring agreement) and Al-Bai’ Contract (purchasing agreement) - as opposed to just one HP agreement under conventional loans.

AFG mortgage loans: Key features similar for conventional and Islamic products; stamp duty more advantageous in Islamic product

Feature i-Wish Home Financing-I (Islamic) Home Loan (Conventional) Stamp Duty 1. New & Top Up: 20% discount Full

2. Refinancing: Waived (100% discount) for refinancing cases (i.e. Conventional loans from other financial institutions to Islamic financing)

Full

Margin of Finance 90% + 5% MRTT and/or Financing Entry Cost 90% + 5% MRTA and/or Financing Entry Cost Tenure 35 years/70 years of age 35 years/70 years of age

Source: Alliance Islamic Bank, DBS Bank, AllianceDBS

Mortgage loans under BBA: Two additional documentation requirement under Islamic financing

The documents MUST be executed in the particular order above at different intervals i.e. the time must not be the same.

Islamic Conventional 1. Product Disclosure Sheet (PDS)

Sales/Branch Staff 1. Product Disclosure Sheet (PDS)

2. Application Form 2. Application Form 3. Letter of Offer (LO) 3. Letter of Offer (LO) 4. Sales and Purchase Agreement (SPA) Customer 4. Sales and Purchase Agreement (SPA) 5. Asset Purchase Agreement (APA)

Solicitors Office

5. N/A 6. Asset Sale Agreement (ASA) 6 . N/A 7. Facility Agreement (FA) 7. Facility Agreement (FA) 8. Other Documents 8. Other Documents

Source: Alliance Islamic Bank, DBS Bank, AllianceDBS AFG hire purchase loans: Key features similar for conventional and Islamic products

Islamic Hire purchase Conventional Hire Purchase Margin of finance 90% of total value of car 90% of total value of car Tenure Max 9 years Max 9 years

Source: Alliance Islamic Bank, DBS Bank, AllianceDBS

Industry Focus

Islamic Banks

Page 16

Islamic financing provided to listed companies aiming to attain Shariah-compliant status. While the terms of business loans are negotiated on a case-by-case basis between the bank and customer, we understand that banks generally do not practice price discrimination whether the loans are under conventional or Islamic. However, listed companies seeking to attain Shariah-compliant status should apply for lines under Islamic banks. Shariah-compliant status are granted to listed companies provided that (1) contribution of Shariah non-compliant activities to the overall revenue and profit before tax is below the 5% benchmark (20% for activities such as hotels and resorts, stock broking and share trading), (2) the company’s ratio of cash (placed in conventional accounts and instruments) over total assets does not exceed 33%, and (3) the company’s ratio of debt (under conventional financing) over total assets does not exceed 33%. Listed companies are generally inclined to seek Shariah-compliant status in order to attract a larger pool of investors. Other incentives offered include waiver of commitment fees for the unutilised portion of the facility limit and full exemption of stamp duty for refinancing of conventional financing facility to Islamic facility.

Industry Focus

Islamic Banks

Page 17

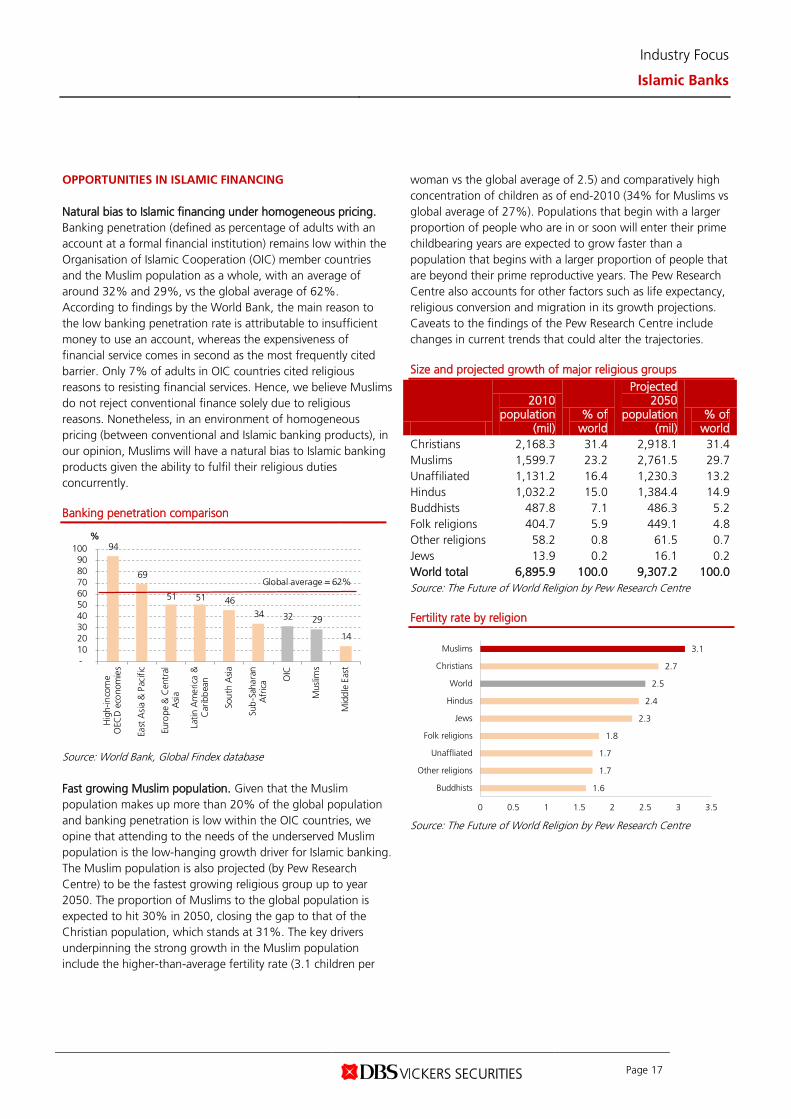

OPPORTUNITIES IN ISLAMIC FINANCING Natural bias to Islamic financing under homogeneous pricing. Banking penetration (defined as percentage of adults with an account at a formal financial institution) remains low within the Organisation of Islamic Cooperation (OIC) member countries and the Muslim population as a whole, with an average of around 32% and 29%, vs the global average of 62%. According to findings by the World Bank, the main reason to the low banking penetration rate is attributable to insufficient money to use an account, whereas the expensiveness of financial service comes in second as the most frequently cited barrier. Only 7% of adults in OIC countries cited religious reasons to resisting financial services. Hence, we believe Muslims do not reject conventional finance solely due to religious reasons. Nonetheless, in an environment of homogeneous pricing (between conventional and Islamic banking products), in our opinion, Muslims will have a natural bias to Islamic banking products given the ability to fulfil their religious duties concurrently. Banking penetration comparison

Source: World Bank, Global Findex database Fast growing Muslim population. Given that the Muslim population makes up more than 20% of the global population and banking penetration is low within the OIC countries, we opine that attending to the needs of the underserved Muslim population is the low-hanging growth driver for Islamic banking. The Muslim population is also projected (by Pew Research Centre) to be the fastest growing religious group up to year 2050. The proportion of Muslims to the global population is expected to hit 30% in 2050, closing the gap to that of the Christian population, which stands at 31%. The key drivers underpinning the strong growth in the Muslim population include the higher-than-average fertility rate (3.1 children per

woman vs the global average of 2.5) and comparatively high concentration of children as of end-2010 (34% for Muslims vs global average of 27%). Populations that begin with a larger proportion of people who are in or soon will enter their prime childbearing years are expected to grow faster than a population that begins with a larger proportion of people that are beyond their prime reproductive years. The Pew Research Centre also accounts for other factors such as life expectancy, religious conversion and migration in its growth projections. Caveats to the findings of the Pew Research Centre include changes in current trends that could alter the trajectories. Size and projected growth of major religious groups

2010 population

(mil) % of

world

Projected 2050

population (mil)

% of world

Christians 2,168.3 31.4 2,918.1 31.4 Muslims 1,599.7 23.2 2,761.5 29.7 Unaffiliated 1,131.2 16.4 1,230.3 13.2 Hindus 1,032.2 15.0 1,384.4 14.9 Buddhists 487.8 7.1 486.3 5.2 Folk religions 404.7 5.9 449.1 4.8 Other religions 58.2 0.8 61.5 0.7 Jews 13.9 0.2 16.1 0.2 World total 6,895.9 100.0 9,307.2 100.0 Source: The Future of World Religion by Pew Research Centre Fertility rate by religion

Source: The Future of World Religion by Pew Research Centre

94

69

51 51 46 34 32 29

14

- 10 20 30 40 50 60 70 80 90

100

Hig

h-in

com

eO

ECD

eco

nom

ies

East

Asi

a &

Pac

ific

Euro

pe &

Cen

tral

Asi

a

Latin

Am

eric

a &

Car

ibb

ean

Sou

th A

sia

Sub

-Sah

aran

Afr

ica O

IC

Mus

lims

Mid

dle

Eas

t

%

Global average = 62%

1.6

1.7

1.7

1.8

2.3

2.4

2.5

2.7

3.1

0 0.5 1 1.5 2 2.5 3 3.5

Buddhists

Other religions

Unaffliated

Folk religions

Jews

Hindus

World

Christians

Muslims

Industry Focus

Islamic Banks

Page 18

Age distribution by religious group in 2010

Source: The Future of World Religion by Pew Research Centre Projected age distribution by religious group in 2050

Source: The Future of World Religion by Pew Research Centre Young Muslim population an attractive market to the banks. Despite projections of a narrowing proportion of global population under the age of 60, the Muslim population is expected to remain relatively youthful as the said proportion is expected to remain higher than the global average (84% vs 78%). A young market is beneficial to the banks as the financing needs of this group of consumers have yet to peak, implying room for banks to grow further in the long term. Attracting the non-Muslim market is the cherry on the cake. Although Islamic banking is based on Islamic teachings, many of these values may also appeal to non-Muslims given the risk-sharing and ethical nature of its business model. In our view, two factors – pricing and awareness – remain the key determinants to favourable take-up by the non-Muslim market. Given the slight incentives offered by Islamic products (lower late payment charges, ceiling rates), we believe that with sufficient education on Islamic banking products, there are non-

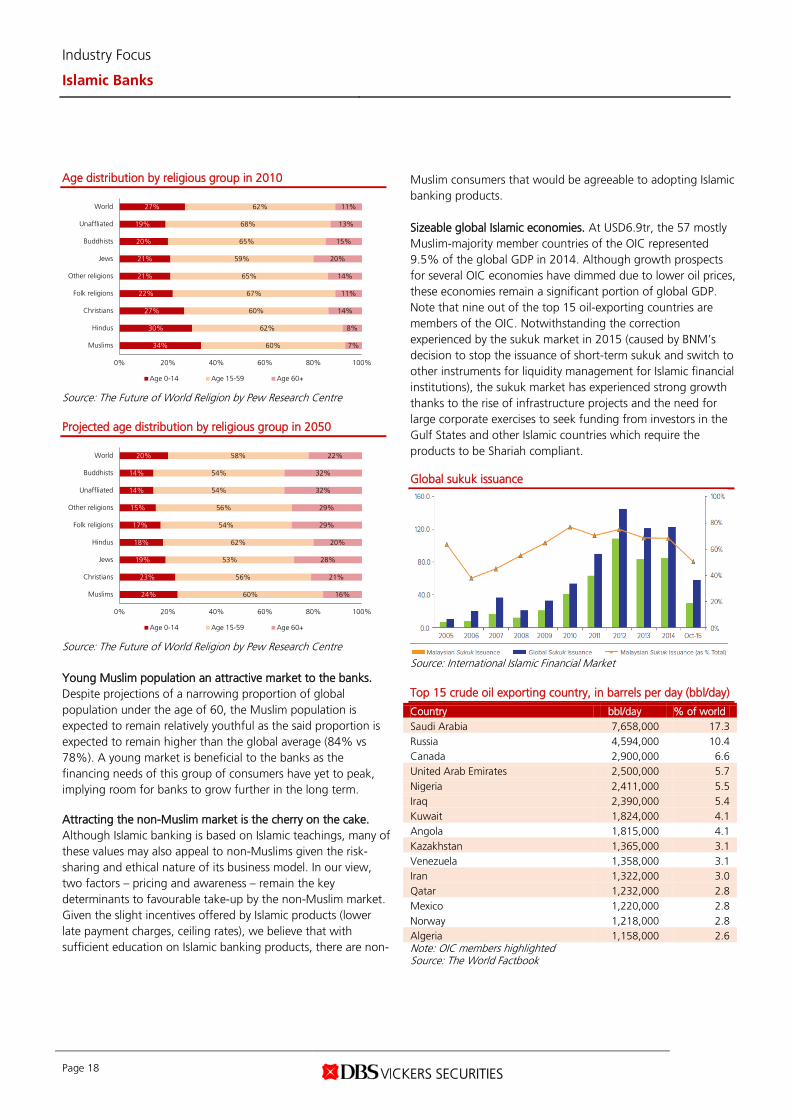

Muslim consumers that would be agreeable to adopting Islamic banking products. Sizeable global Islamic economies. At USD6.9tr, the 57 mostly Muslim-majority member countries of the OIC represented 9.5% of the global GDP in 2014. Although growth prospects for several OIC economies have dimmed due to lower oil prices, these economies remain a significant portion of global GDP. Note that nine out of the top 15 oil-exporting countries are members of the OIC. Notwithstanding the correction experienced by the sukuk market in 2015 (caused by BNM’s decision to stop the issuance of short-term sukuk and switch to other instruments for liquidity management for Islamic financial institutions), the sukuk market has experienced strong growth thanks to the rise of infrastructure projects and the need for large corporate exercises to seek funding from investors in the Gulf States and other Islamic countries which require the products to be Shariah compliant. Global sukuk issuance

Source: International Islamic Financial Market Top 15 crude oil exporting country, in barrels per day (bbl/day)

Country bbl/day % of world Saudi Arabia 7,658,000 17.3 Russia 4,594,000 10.4 Canada 2,900,000 6.6 United Arab Emirates 2,500,000 5.7 Nigeria 2,411,000 5.5 Iraq 2,390,000 5.4 Kuwait 1,824,000 4.1 Angola 1,815,000 4.1 Kazakhstan 1,365,000 3.1 Venezuela 1,358,000 3.1 Iran 1,322,000 3.0 Qatar 1,232,000 2.8 Mexico 1,220,000 2.8 Norway 1,218,000 2.8 Algeria 1,158,000 2.6 Note: OIC members highlighted Source: The World Factbook

34%

30%

27%

22%

21%

21%

20%

19%

27%

60%

62%

60%

67%

65%

59%

65%

68%

62%

7%

8%

14%

11%

14%

20%

15%

13%

11%

0% 20% 40% 60% 80% 100%

Muslims

Hindus

Christians

Folk religions

Other religions

Jews

Buddhists

Unaffliated

World

Age 0-14 Age 15-59 Age 60+

24%

23%

19%

18%

17%

15%

14%

14%

20%

60%

56%

53%

62%

54%

56%

54%

54%

58%

16%

21%

28%

20%

29%

29%

32%

32%

22%

0% 20% 40% 60% 80% 100%

Muslims

Christians

Jews

Hindus

Folk religions

Other religions

Unaffliated

Buddhists

World

Age 0-14 Age 15-59 Age 60+

Industry Focus

Islamic Banks

Page 19

Growing intra-OIC trade. The clear drive to develop Intra-OIC trade is also facilitating the development of the Islamic economic sectors. The Intra-OIC trade among the member countries has grown from 13% in 2005 to 19.9% in 2014, close to the OIC’s 2015 target of 20%. Under the OIC’s ten-year programme of action leading up to 2025, the target for intra-OIC trade is to hit 6% north of 2015 levels.

Intra-OIC merchandise exports and imports (USD bn)

Source: OIC Economic Outlook 2015

Industry Focus

Islamic Banks

Page 20

CHALLENGES Regulatory gap. Existing legal and regulatory frameworks should take into consideration the value propositions promulgated by Shariah. For instance, the legal definition of banking and financial services in certain jurisdictions does not recognise Islamic financial transactions, which leads to potential conflict and adverse legal effects. The government should also be supportive in granting neutral tax treatments for Islamic financial transactions to ensure that Islamic banking products are cost efficient. Establishing an even playing field. To avoid an exodus back to conventional finance, at the very least, there is a need for Islamic products to be on par with conventional products in terms of diversity, cost effectiveness, ability to meet the risk and return requirement of investors as well as the service level, while remaining Shariah compliant. On the other hand, to get one up on conventional banking, these Islamic products are expected to be superior to their conventional peers in these aspects. Liquidity management. Liquidity problems exist in the Islamic capital market due to the lack of derivatives and an organised secondary market for dealing with Islamic instruments. An early exit may be difficult or costly for an investor without an effective secondary market where financial instruments are easily tradable. In addition, most central banks have not been very active in issuing short-term sukuk, limiting the availability of high-quality liquid assets (HQLA) in Islamic finance. Lack of awareness. Despite the strong presence of Islamic finance in the Gulf Cooperation Council (five out of the six member countries are among the top 10 Islamic economies), findings by PWC show that residents in this region lack familiarity with Islamic banking. 56% of the Muslim respondents believe that they are familiar with Islamic banking while 64% of non-Muslims cited insufficient knowledge of Islamic financial products as the reason for not using Islamic financial services.

Talent shortage. Islamic financial industry requires a specific set of competencies and skills, such as Shariah understanding and market insight. The shortage of talents, especially on the expert level such as Shariah scholars, may impede the growth of Islamic finance, as the views of these scholars are highly valuable in product development and innovation. On an extreme case, scarcity in talent may also cause inflated salaries and lead to a drag on the cost structure of the Islamic banks. Hence, the abundance of educational institutions focusing on Islamic banking is crucial for the development of the industry. Lack of uniformity between Shariah’s views. Different interpretations of the Shariah lead to different practice and use of concepts across jurisdiction. Certain products may be accepted in some jurisdictions but not in others, thus this may impede the growth and internationalisation of Islamic finance. Differences in opinion among religious scholars regarding the Shariah compliance of specific financial arrangements can expose Islamic banks to the risk of non-compliance with Shariah principles, which may have serious implications on the industry. Harmonising differences in the Shariah compliance of different instruments would reduce uncertainty and foster industry growth. It also ensures that Islamic banks are able to capture opportunities from the entire Muslim market, instead of being sidelined by a portion who perceive Islamic banks are not true to Shariah values. By the same token, the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) and Islamic Financial Services Board (IFSB) have provided some Shariah standards and governance guidelines.

Industry Focus

Islamic Banks

Page 21

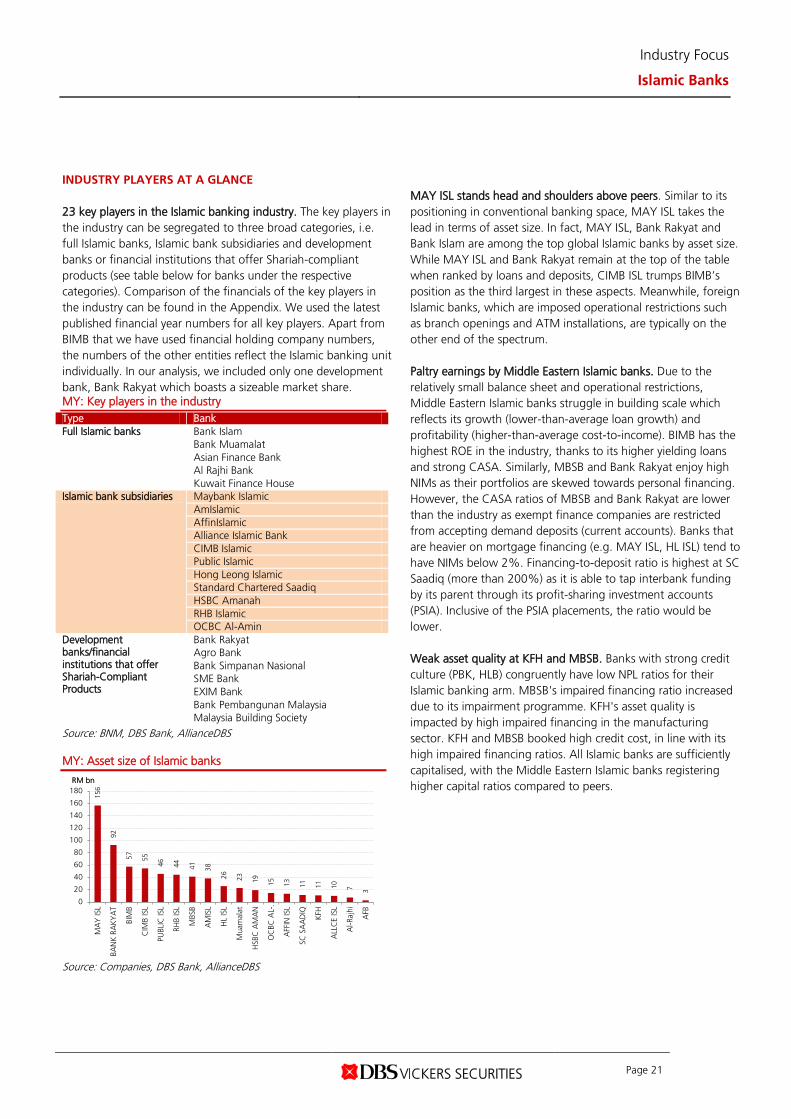

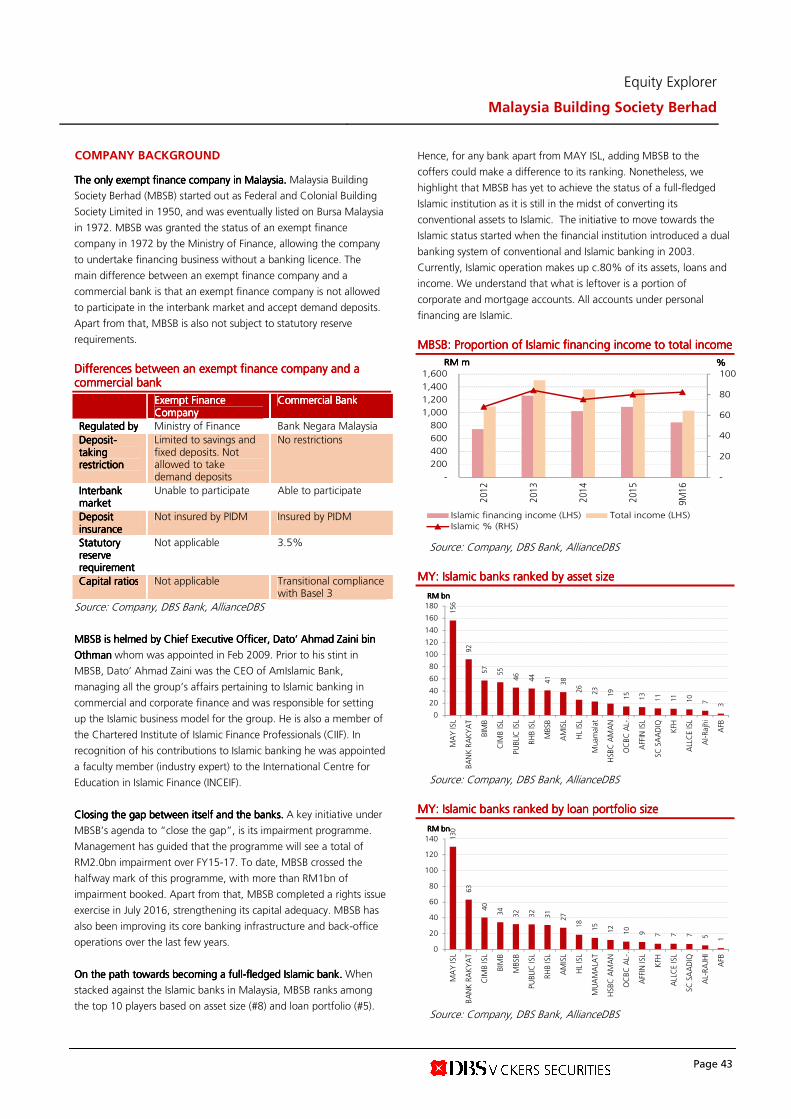

INDUSTRY PLAYERS AT A GLANCE 23 key players in the Islamic banking industry. The key players in the industry can be segregated to three broad categories, i.e. full Islamic banks, Islamic bank subsidiaries and development banks or financial institutions that offer Shariah-compliant products (see table below for banks under the respective categories). Comparison of the financials of the key players in the industry can be found in the Appendix. We used the latest published financial year numbers for all key players. Apart from BIMB that we have used financial holding company numbers, the numbers of the other entities reflect the Islamic banking unit individually. In our analysis, we included only one development bank, Bank Rakyat which boasts a sizeable market share. MY: Key players in the industry Type Bank Full Islamic banks Bank Islam

Bank Muamalat Asian Finance Bank Al Rajhi Bank Kuwait Finance House

Islamic bank subsidiaries Maybank Islamic AmIslamic AffinIslamic Alliance Islamic Bank CIMB Islamic Public Islamic Hong Leong Islamic Standard Chartered Saadiq HSBC Amanah RHB Islamic OCBC Al-Amin

Development banks/financial institutions that offer Shariah-Compliant Products

Bank Rakyat Agro Bank Bank Simpanan Nasional SME Bank EXIM Bank Bank Pembangunan Malaysia Malaysia Building Society

Source: BNM, DBS Bank, AllianceDBS MY: Asset size of Islamic banks

Source: Companies, DBS Bank, AllianceDBS

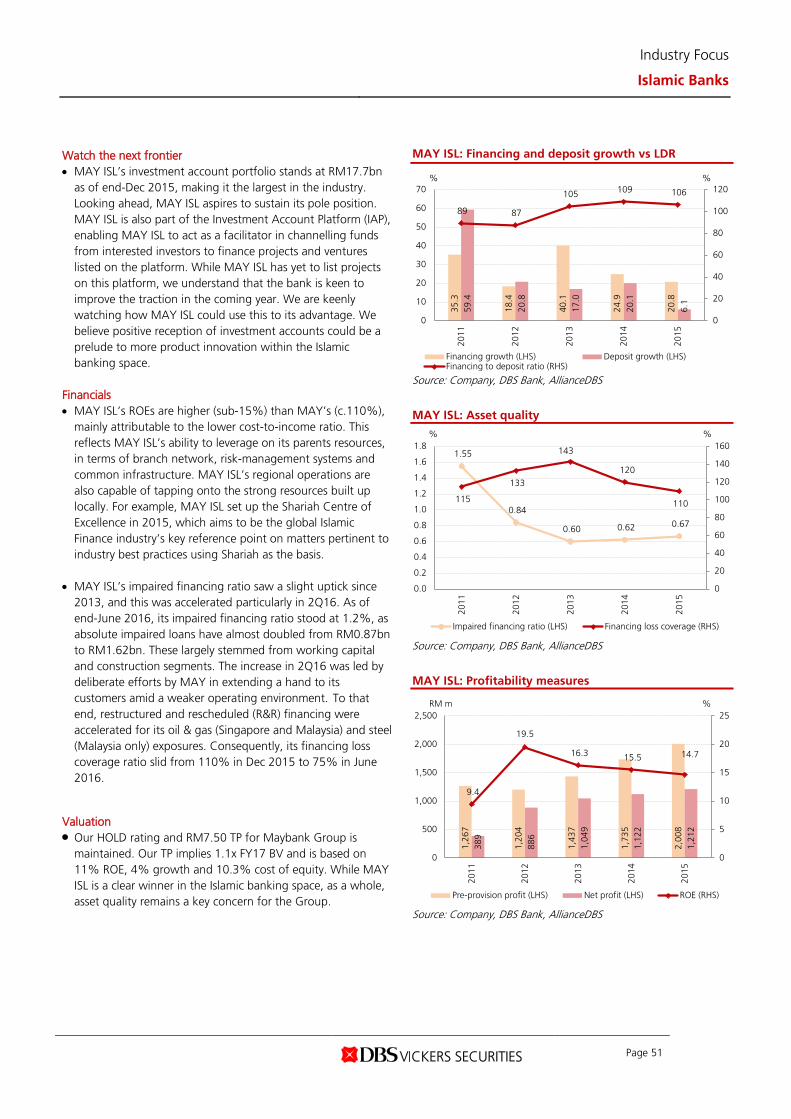

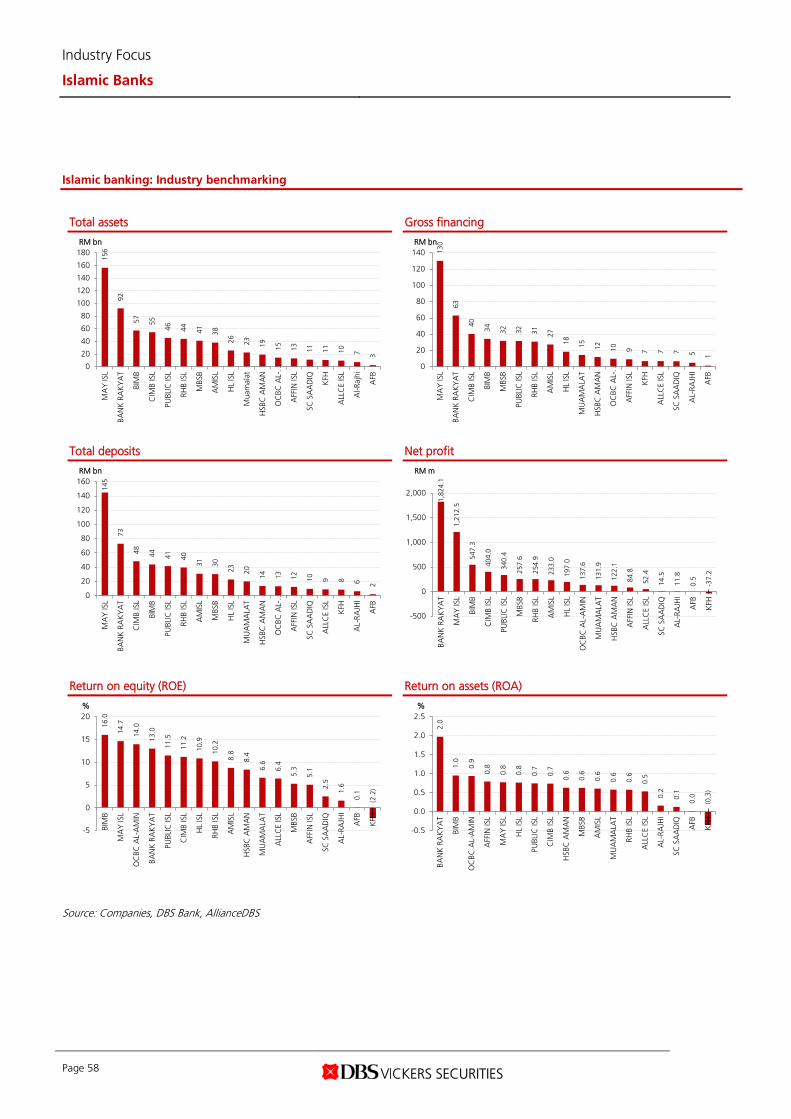

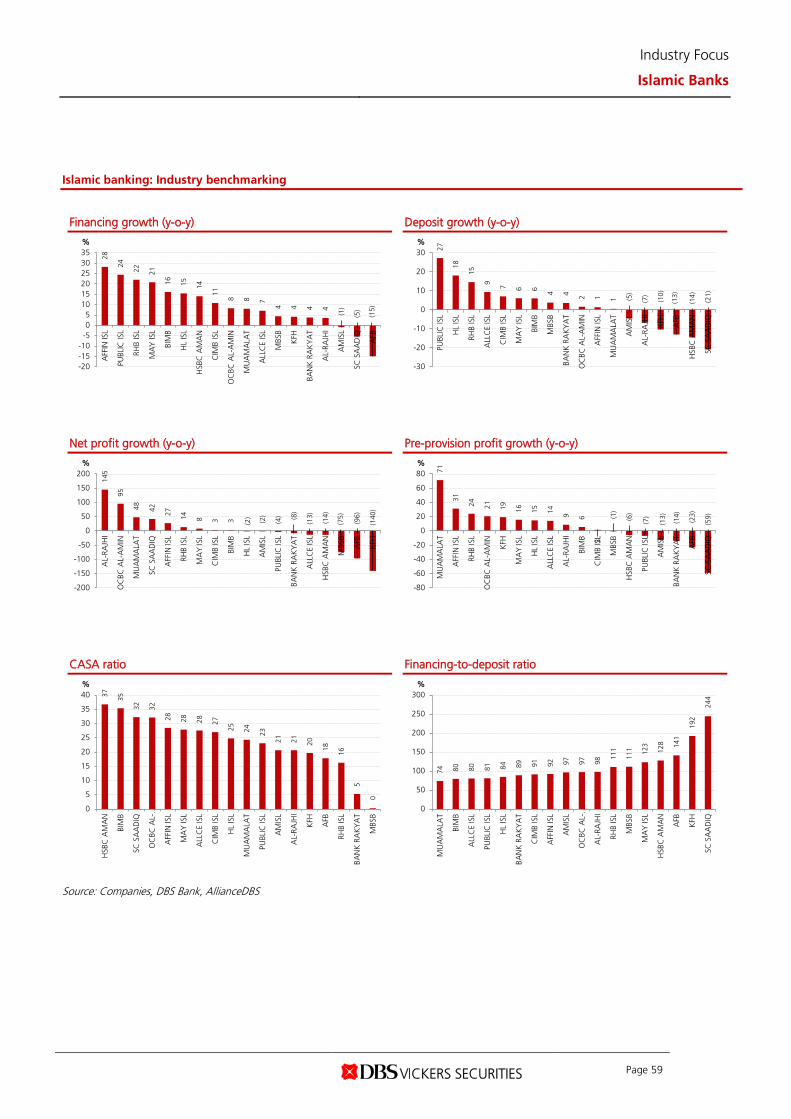

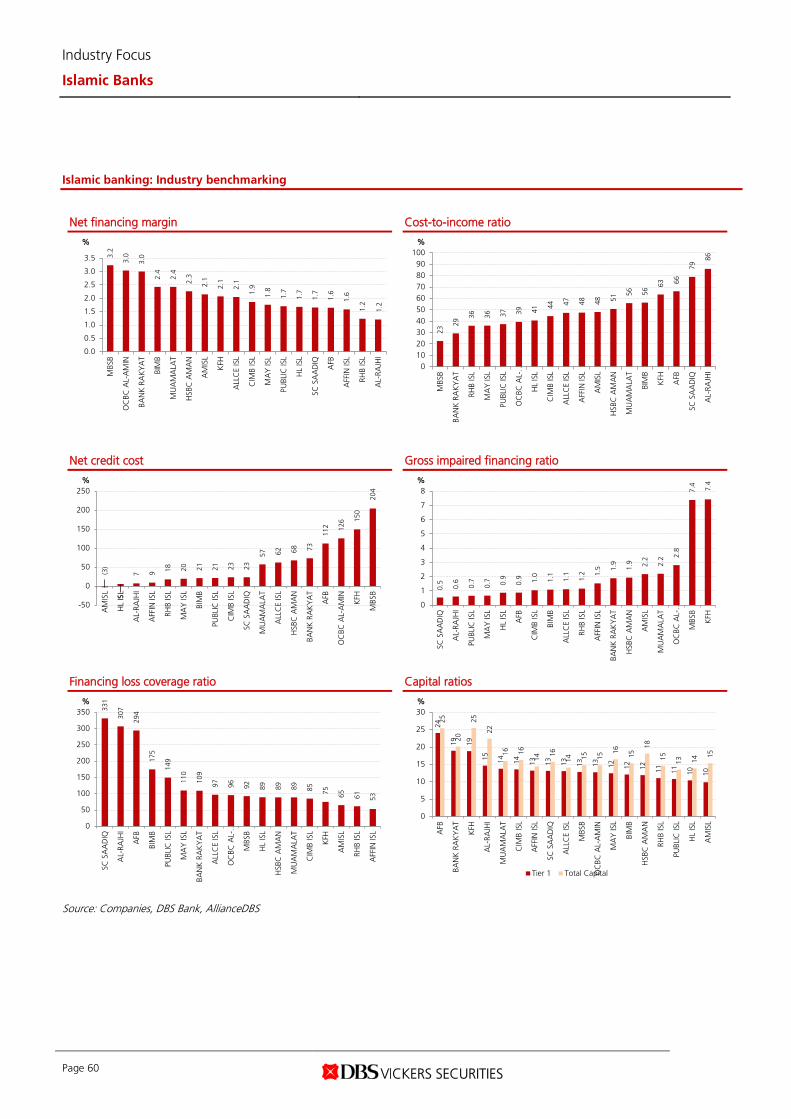

MAY ISL stands head and shoulders above peers. Similar to its positioning in conventional banking space, MAY ISL takes the lead in terms of asset size. In fact, MAY ISL, Bank Rakyat and Bank Islam are among the top global Islamic banks by asset size. While MAY ISL and Bank Rakyat remain at the top of the table when ranked by loans and deposits, CIMB ISL trumps BIMB’s position as the third largest in these aspects. Meanwhile, foreign Islamic banks, which are imposed operational restrictions such as branch openings and ATM installations, are typically on the other end of the spectrum. Paltry earnings by Middle Eastern Islamic banks. Due to the relatively small balance sheet and operational restrictions, Middle Eastern Islamic banks struggle in building scale which reflects its growth (lower-than-average loan growth) and profitability (higher-than-average cost-to-income). BIMB has the highest ROE in the industry, thanks to its higher yielding loans and strong CASA. Similarly, MBSB and Bank Rakyat enjoy high NIMs as their portfolios are skewed towards personal financing. However, the CASA ratios of MBSB and Bank Rakyat are lower than the industry as exempt finance companies are restricted from accepting demand deposits (current accounts). Banks that are heavier on mortgage financing (e.g. MAY ISL, HL ISL) tend to have NIMs below 2%. Financing-to-deposit ratio is highest at SC Saadiq (more than 200%) as it is able to tap interbank funding by its parent through its profit-sharing investment accounts (PSIA). Inclusive of the PSIA placements, the ratio would be lower. Weak asset quality at KFH and MBSB. Banks with strong credit culture (PBK, HLB) congruently have low NPL ratios for their Islamic banking arm. MBSB's impaired financing ratio increased due to its impairment programme. KFH's asset quality is impacted by high impaired financing in the manufacturing sector. KFH and MBSB booked high credit cost, in line with its high impaired financing ratios. All Islamic banks are sufficiently capitalised, with the Middle Eastern Islamic banks registering higher capital ratios compared to peers.

156

92

57

55

46

44

41

38

26

23

19

15

13

11

11

10

7 3

0

20

40

60

80

100

120

140

160

180

MA

Y IS

L

BAN

K R

AK

YA

T

BIM

B

CIM

B IS

L

PUBL

IC IS

L

RHB

ISL

MBS

B

AM

ISL

HL

ISL

Mua

mal

at

HSB

C A

MA

N

OC

BC A

L-…

AFF

IN IS

L

SC S

AA

DIQ

KFH

ALL

CE

ISL

Al-R

ajhi

AFB

RM bn

Industry Focus

Islamic Banks

Page 22

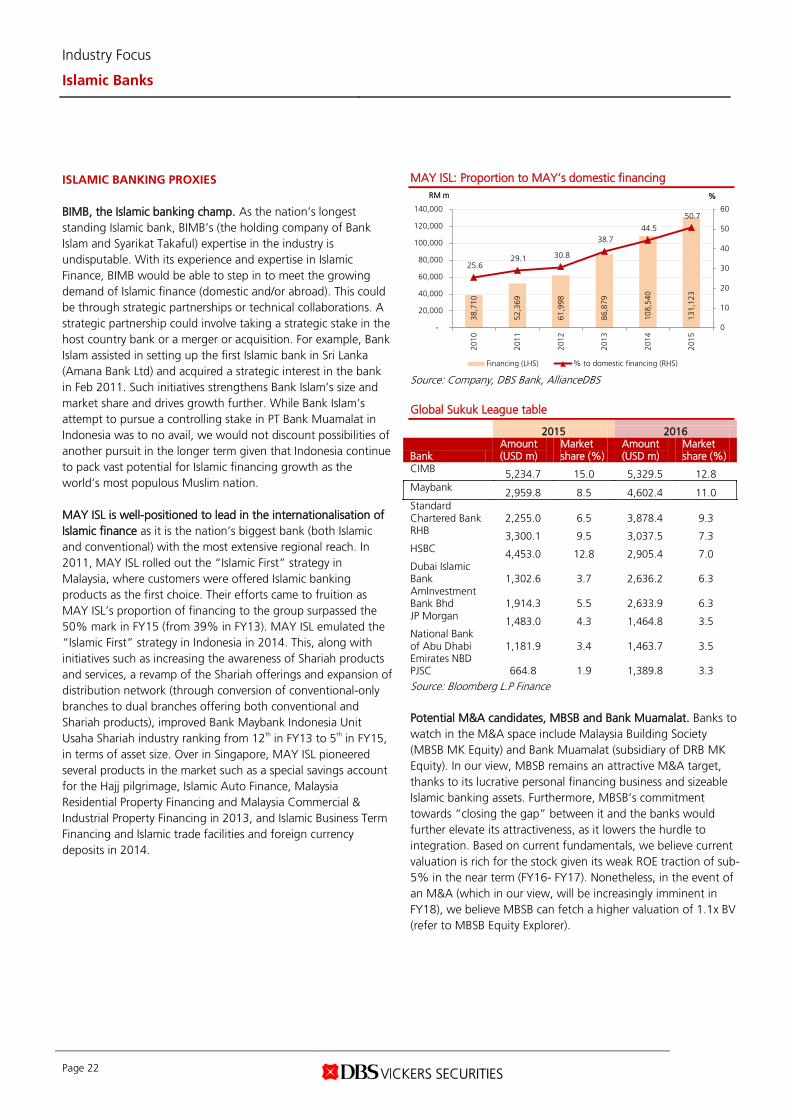

ISLAMIC BANKING PROXIES BIMB, the Islamic banking champ. As the nation’s longest standing Islamic bank, BIMB’s (the holding company of Bank Islam and Syarikat Takaful) expertise in the industry is undisputable. With its experience and expertise in Islamic Finance, BIMB would be able to step in to meet the growing demand of Islamic finance (domestic and/or abroad). This could be through strategic partnerships or technical collaborations. A strategic partnership could involve taking a strategic stake in the host country bank or a merger or acquisition. For example, Bank Islam assisted in setting up the first Islamic bank in Sri Lanka (Amana Bank Ltd) and acquired a strategic interest in the bank in Feb 2011. Such initiatives strengthens Bank Islam’s size and market share and drives growth further. While Bank Islam’s attempt to pursue a controlling stake in PT Bank Muamalat in Indonesia was to no avail, we would not discount possibilities of another pursuit in the longer term given that Indonesia continue to pack vast potential for Islamic financing growth as the world’s most populous Muslim nation. MAY ISL is well-positioned to lead in the internationalisation of Islamic finance as it is the nation’s biggest bank (both Islamic and conventional) with the most extensive regional reach. In 2011, MAY ISL rolled out the “Islamic First” strategy in Malaysia, where customers were offered Islamic banking products as the first choice. Their efforts came to fruition as MAY ISL’s proportion of financing to the group surpassed the 50% mark in FY15 (from 39% in FY13). MAY ISL emulated the “Islamic First” strategy in Indonesia in 2014. This, along with initiatives such as increasing the awareness of Shariah products and services, a revamp of the Shariah offerings and expansion of distribution network (through conversion of conventional-only branches to dual branches offering both conventional and Shariah products), improved Bank Maybank Indonesia Unit Usaha Shariah industry ranking from 12th in FY13 to 5th in FY15, in terms of asset size. Over in Singapore, MAY ISL pioneered several products in the market such as a special savings account for the Hajj pilgrimage, Islamic Auto Finance, Malaysia Residential Property Financing and Malaysia Commercial & Industrial Property Financing in 2013, and Islamic Business Term Financing and Islamic trade facilities and foreign currency deposits in 2014.

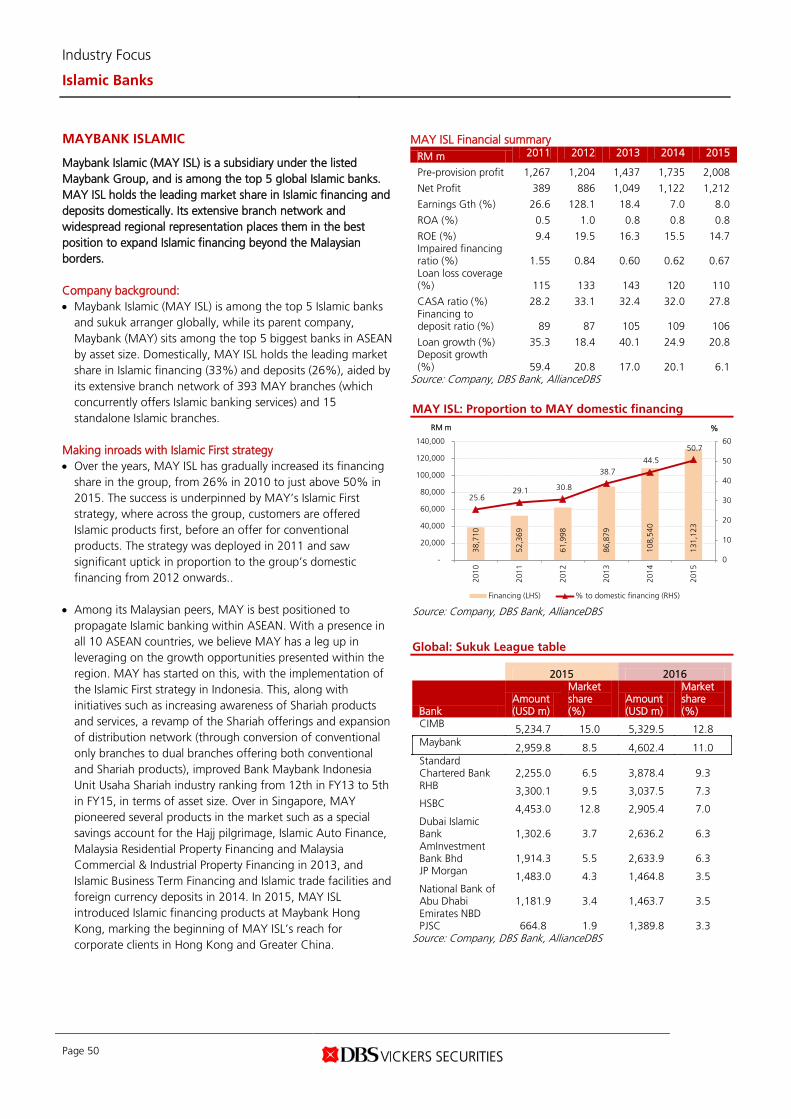

MAY ISL: Proportion to MAY’s domestic financing

Source: Company, DBS Bank, AllianceDBS Global Sukuk League table

2015 2016

Bank Amount (USD m)

Market share (%)

Amount (USD m)

Market share (%)

CIMB 5,234.7 15.0 5,329.5 12.8 Maybank 2,959.8 8.5 4,602.4 11.0 Standard Chartered Bank 2,255.0 6.5 3,878.4 9.3 RHB 3,300.1 9.5 3,037.5 7.3 HSBC 4,453.0 12.8 2,905.4 7.0 Dubai Islamic Bank 1,302.6 3.7 2,636.2 6.3 AmInvestment Bank Bhd 1,914.3 5.5 2,633.9 6.3 JP Morgan 1,483.0 4.3 1,464.8 3.5 National Bank of Abu Dhabi 1,181.9 3.4 1,463.7 3.5 Emirates NBD PJSC 664.8 1.9 1,389.8 3.3

Source: Bloomberg L.P Finance Potential M&A candidates, MBSB and Bank Muamalat. Banks to watch in the M&A space include Malaysia Building Society (MBSB MK Equity) and Bank Muamalat (subsidiary of DRB MK Equity). In our view, MBSB remains an attractive M&A target, thanks to its lucrative personal financing business and sizeable Islamic banking assets. Furthermore, MBSB’s commitment towards “closing the gap” between it and the banks would further elevate its attractiveness, as it lowers the hurdle to integration. Based on current fundamentals, we believe current valuation is rich for the stock given its weak ROE traction of sub-5% in the near term (FY16- FY17). Nonetheless, in the event of an M&A (which in our view, will be increasingly imminent in FY18), we believe MBSB can fetch a higher valuation of 1.1x BV (refer to MBSB Equity Explorer).

38,7

10

52,3

69

61,9

98

86,8

79

108,

540

131,

123

25.6 29.1 30.8

38.7 44.5

50.7

0

10

20

30

40

50

60

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2010

2011

2012

2013

2014

2015

%RM m

Financing (LHS) % to domestic financing (RHS)

Industry Focus

Islamic Banks

Page 23

MUAMALAT, a long awaited M&A play. While MUAMALAT is a relatively small entity, M&A talks have surfaced several times as its largest shareholder, DRB-HICOM (which has a 70% stake in MUAMALAT), had been required by BNM to pare down its significant stake to 40%. Alternatively, the pare down in shareholding could take the route of an initial public offering (IPO). In such a case, we expect the bank to fetch a valuation that is comparable to Affin (closest comparable to its ROE profile). At a conservative valuation of 0.5x BV, Bank Muamalat could be listed at a market capitalisation of close to RM1bn. BIMB (2011), Affin (2013) and MBSB (2016) had made an attempt to acquire MUAMALAT, but no firm developments have materialised to date

Quest for the next mega Islamic bank. Talks of a mega Islamic bank surfaced as early as 2010 when the Central Bank was said to be issuing two mega Islamic bank licences to foreign players with the condition of having a minimum RM1bn in paid-up capital. M&A spin-offs in the Islamic banking space are plausible, in our view, potentially creating a new wave of M&A activities in the Islamic banking space. In 2014, MBSB was involved in talks to merge with CIMB and RHB. Together, the merged entity was expected to displace MAY from its #1 ranking in Malaysia by asset size. More interestingly, MBSB was slated to remain listed and to act as a vehicle for any proposed mega Islamic Bank, i.e. the banking operations of CIMB Islamic and RHB Islamic would be injected into MBSB if the three-way merger were to succeed.

Industry Focus

Islamic Banks

Page 24