Embed Size (px)

Citation preview

Completion Report

Project Number: 37265 Loan Number: 2327 October 2013

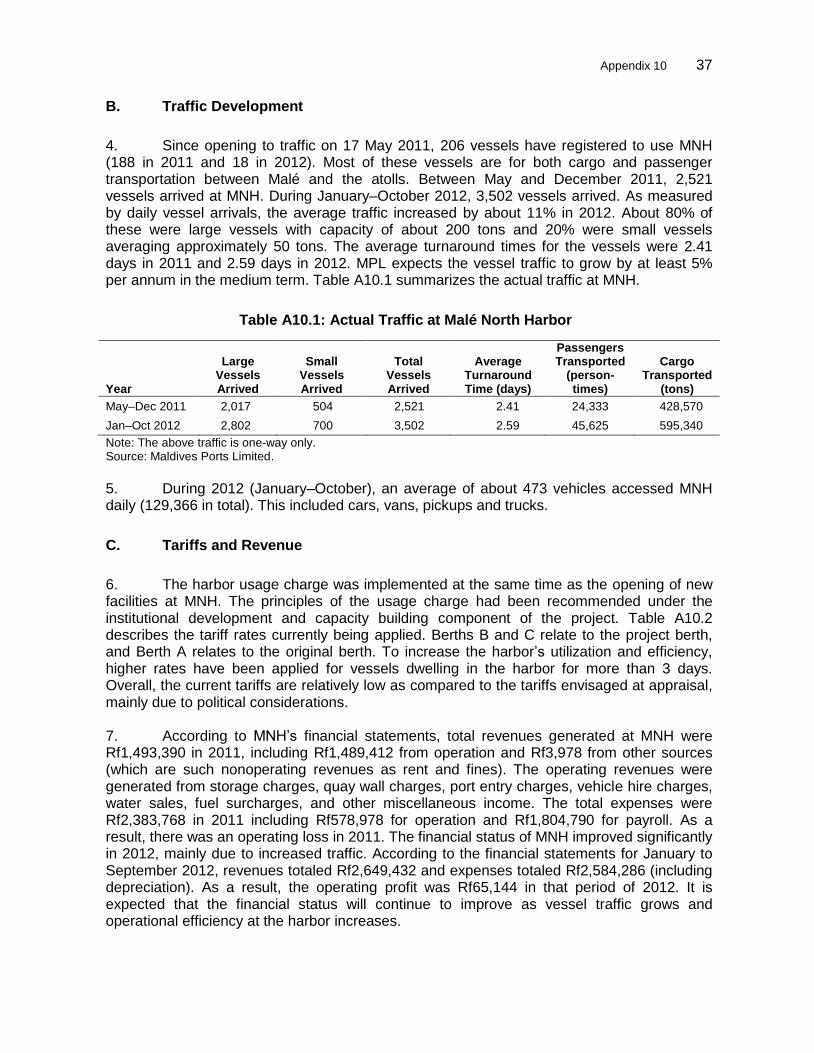

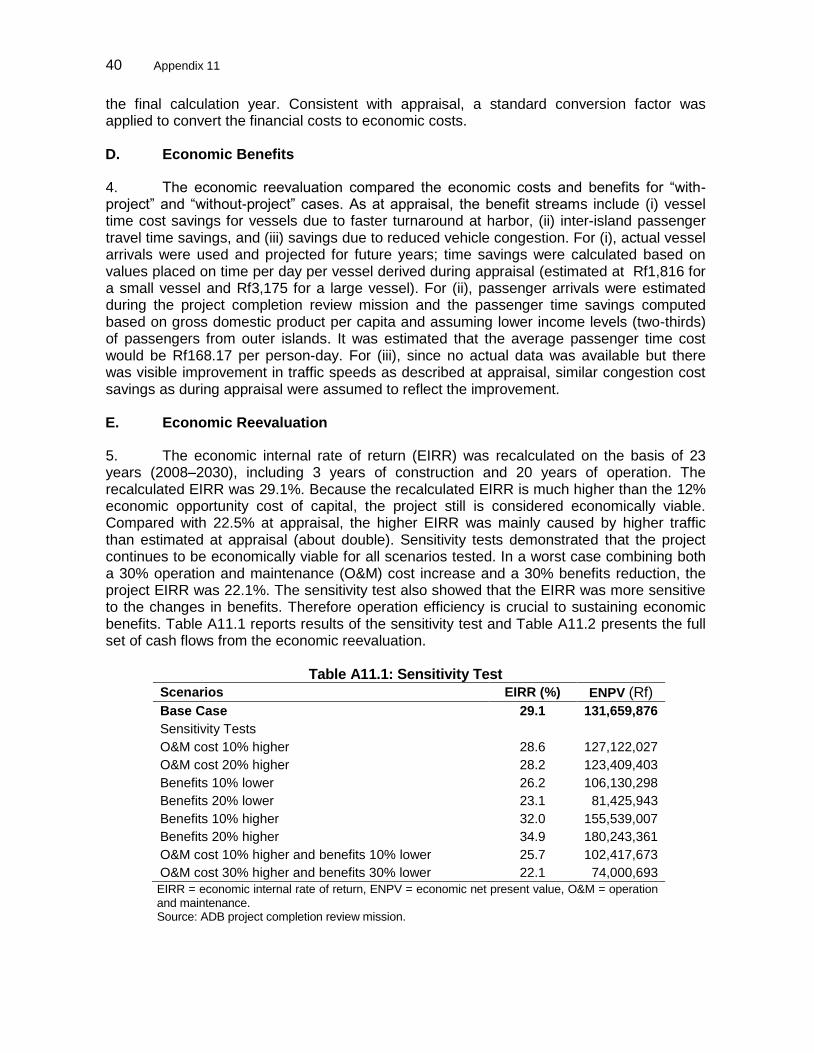

Maldives: Domestic Maritime Transport Project

CURRENCY EQUIVALENTS

Currency Unit – Rufiyaa (Rf)

At Appraisal At Project Completion (1 March 2007) (31 December 2010)

Rf1.00 = $0.078 $0.078 $1.00 = Rf12.850 Rf12.780

ABBREVIATIONS

ADB – Asian Development Bank EIRR – economic internal rate of return EMP – environment management plan FIRR – financial internal rate of return IDCB – institutional development and capacity building IIC – infrastructure investment component MCPI – Ministry of Construction and Public Infrastructure MNH – Malé North Harbor MPL – Maldives Ports Limited MTC – Ministry of Transport and Communication NDP – national development plan PIU – project implementation unit SDR – special drawing rights

NOTE

In this report, “$” refers to U.S. dollars.

Vice President X. Zhao, Operations 1 Director General J. Miranda, South Asia Department (SARD) Director S. Widowati, Transport and Communications Division, SARD Team leader P. Chiang, Transport and Communications Division, SARD Team member T. Prado, Transport and Communications Division, SARD

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the

Asian Development Bank does not intend to make any judgments as to the legal or other status

of any territory or area.

CONTENTS

Page BASIC DATA i

I. PROJECT DESCRIPTION 1

II. EVALUATION OF DESIGN AND IMPLEMENTATION 1

A. Relevance of Design and Formulation 1 B. Project Outputs 2 C. Project Costs 3 D. Disbursements 4 E. Project Schedule 4 F. Implementation Arrangements 5 G. Conditions and Covenants 6 H. Consultant Recruitment and Procurement 6 I. Performance of Consultants and Contractors 7 J. Performance of the Borrower and the Executing Agency 8 K. Performance of the Asian Development Bank 9

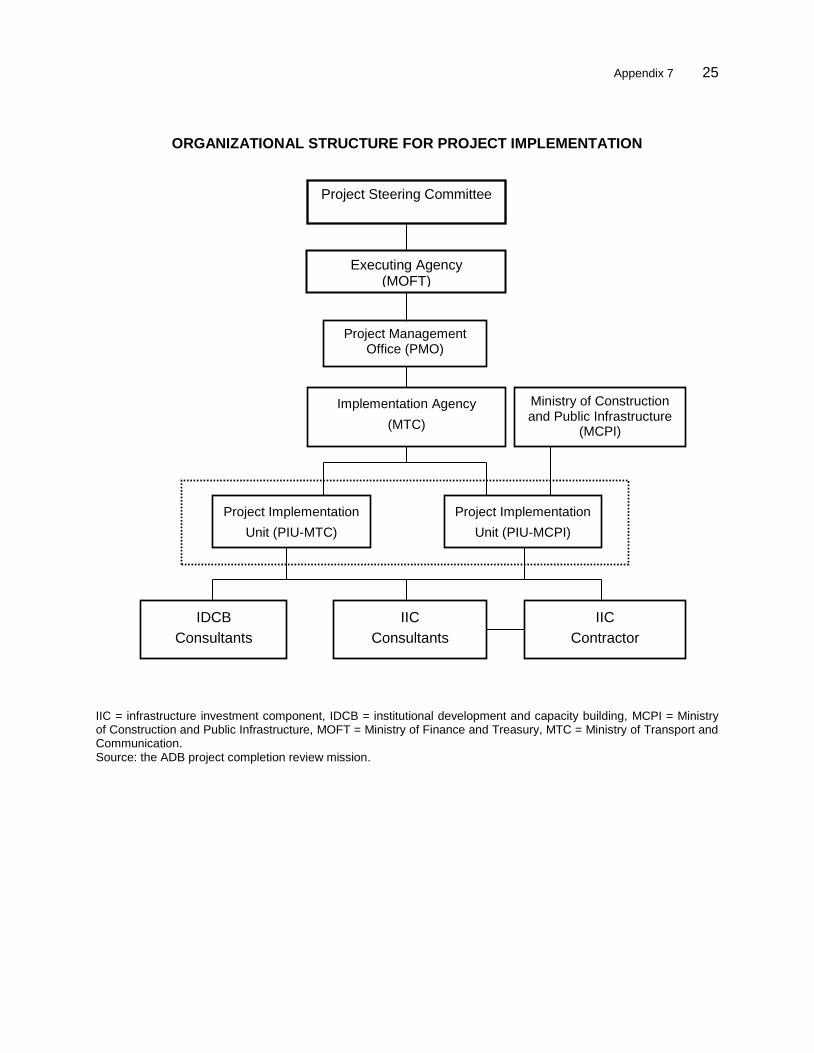

III. EVALUATION OF PERFORMANCE 9

A. Relevance 9 B. Effectiveness in Achieving Outcome 10 C. Efficiency in Achieving Outcome and Outputs 10 D. Preliminary Assessment of Sustainability 11 E. Impact 12

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS 13

A. Overall Assessment 13 B. Lessons 13 C. Recommendations 14

APPENDIXES 1. Design and Monitoring Framework 15 2. Details of Project Outputs 19 3. Project Cost and Financing Plan 20 4. Disbursement of ADB Loan Proceeds 21 5. Actual Project Implementation Schedules 22 6. Chronology of Major Events 23 7. Organizational Structure for Project Implementation 25 8. Status of Compliance with Major Loan Covenants 26 9. Summary of Contract Packages 35 10. Initial Operation of the Project 36 11. Reevaluation of Economic Analysis 39 12. Reevaluation of Financial Analysis 42

i

BASIC DATA

A. Loan Identification

1. Country 2. Loan Number 3. Project Title 4. Borrower 5. Executing Agency 6. Amount of Loan

7. Project Completion Report Number

The Republic of the Maldives Loan 2327-MLD Domestic Maritime Transport Project The Republic of the Maldives Ministry of Finance and Treasury SDR 3,544,000 ($ 5,330,000 equivalent) MLD 1416

B. Loan Data 1. Appraisal – Date Started – Date Completed 2. Loan Negotiations – Date Started – Date Completed 3. Date of Board Approval 4. Date of Loan Agreement 5. Date of Loan Effectiveness – In Loan Agreement – Actual – Number of Extensions 6. Closing Date – In Loan Agreement – Actual – Number of Extensions 7. Terms of Loan – Interest Rate – Maturity (number of years) – Grace Period (number of years)

28 January 2007 2 February 2007 19 March 2007 20 March 2007 24 April 2007 29 August 2007 27 November 2007 23 October 2007 None 31 December 2009 31 December 2010 1 1.0% per annum during grace period 1.5% per annum after grace period 32 years 8 years

8. Disbursements a. Dates

Initial Disbursement 20 May 2008

Final Disbursement 16 March 2012

Time Interval 46 months

Effective Date 23 October 2007

Original Closing Date 31 December 2009

Time Interval 26 months

ii

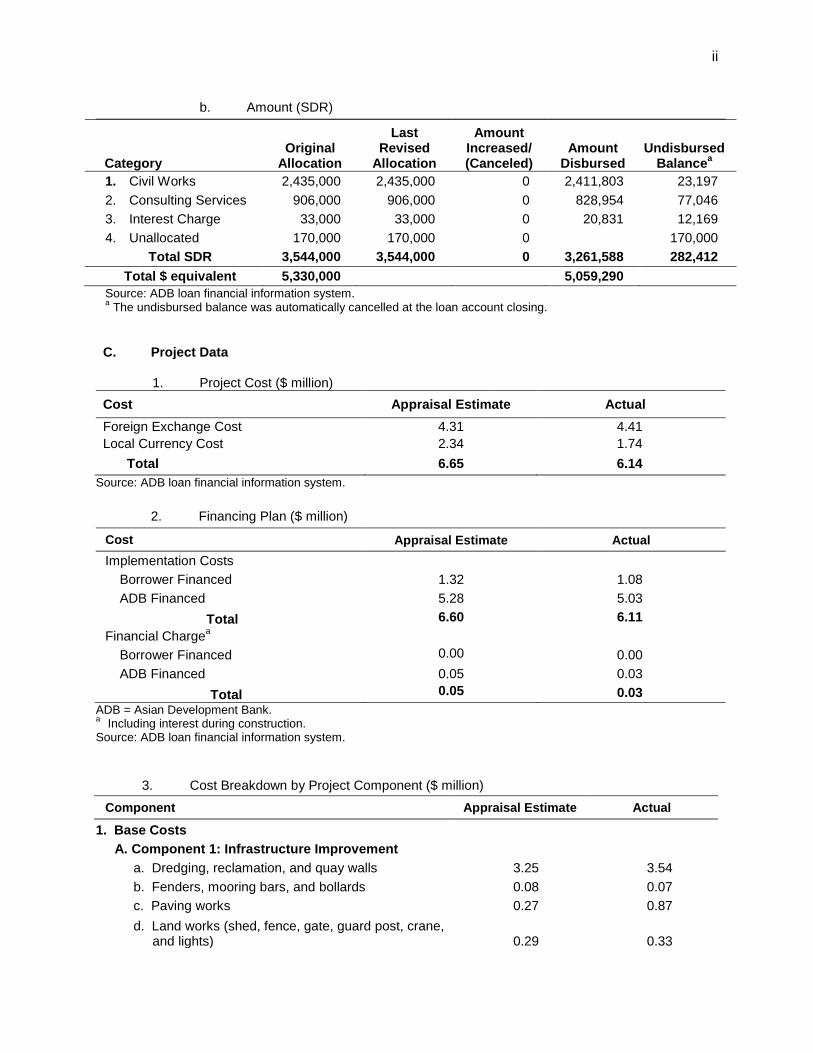

b. Amount (SDR)

Category Original

Allocation

Last Revised

Allocation

Amount Increased/ (Canceled)

Amount Disbursed

Undisbursed Balance

a

1. Civil Works 2,435,000 2,435,000 0 2,411,803 23,197

2. Consulting Services 906,000 906,000 0 828,954 77,046

3. Interest Charge 33,000 33,000 0 20,831 12,169

4. Unallocated 170,000 170,000 0 170,000

Total SDR 3,544,000 3,544,000 0 3,261,588 282,412

Total $ equivalent 5,330,000 5,059,290

Source: ADB loan financial information system. a The undisbursed balance was automatically cancelled at the loan account closing.

C. Project Data

1. Project Cost ($ million)

Cost Appraisal Estimate Actual

Foreign Exchange Cost 4.31 4.41

Local Currency Cost 2.34 1.74

Total 6.65 6.14

Source: ADB loan financial information system.

2. Financing Plan ($ million)

Cost Appraisal Estimate Actual

Implementation Costs

Borrower Financed 1.32 1.08

ADB Financed 5.28 5.03

Total 6.60 6.11

Financial Chargea

Borrower Financed 0.00

0.00

ADB Financed 0.05 0.03

Total 0.05 0.03

ADB = Asian Development Bank. a Including interest during construction.

Source: ADB loan financial information system.

3. Cost Breakdown by Project Component ($ million)

Component Appraisal Estimate Actual

1. Base Costs

A. Component 1: Infrastructure Improvement

a. Dredging, reclamation, and quay walls 3.25 3.54

b. Fenders, mooring bars, and bollards 0.08 0.07

c. Paving works 0.27 0.87

d. Land works (shed, fence, gate, guard post, crane, and lights) 0.29 0.33

iii

e. Detailed design, bid preparation, site supervision, and project management 0.54 0.64

B. Component 2: Institutional Development and Capacity Building

a. Institutional development and capacity building 0.65 0.66

b. Environmental impact assessment 0.05 0.00

2. Taxes and Duties 0.43 0.00

3. Contingencies

a. Physical 0.72 0.00

b. Price 0.32 0.00

4. Financing Charges: Interest Capitalized during Construction 0.05 0.03

Total (1+2+3+4) 6.65 6.14

Source: ADB loan financial information system.

4. Project Schedule

Item Appraisal Estimate Actual

Consultant for IIC component

Recruitment Q4 2006–Q2 2007 Q1 2007–Q4 2007

Implementation Q3 2007–Q1 2009 Q1 2008–Q4 2010

IIC component

Procurement Q4 2006–Q4 2007 Q3 2008–Q4 2009

Implementation Q1 2008–Q2 2009 Q4 2009–Q4 2010

IDCB component

Recruitment Q4 2006–Q3 2007 Q1 2007–Q2 2008

Implementation Q4 2007–Q2 2009 Q3 2008–Q4 2010

IIC = infrastructure investment component, IDCB = institutional development and capacity building. Source: ADB loan financial information system.

5. Project Performance Report Ratings

Implementation Period

Ratings

Development Objectives Implementation Progress

From 30 Apr 2007 to 31 Dec 2007 Satisfactory Satisfactory

From 1 Jan 2008 to 30 Jun 2008 Satisfactory Satisfactory

From 1 Jul 2008 to 31 Dec 2008 Satisfactory Satisfactory

From 1 Jan 2009 to 31 Jun 2009 Satisfactory Satisfactory

From 1 Jul 2009 to 31 Dec 2009 Satisfactory Satisfactory

From 1 Jan 2010 to 30 Jun 2012 Satisfactory Satisfactory

From 1 Jul 2010 to 31 Jul 2010 Satisfactory Unsatisfactory

From 1 Aug 2010 to 31 Dec 2010 Satisfactory Satisfactory

iv

D. Data on Asian Development Bank Missions

Name of Mission Date No. of

Persons

No. of Person-

Days Specialization of Members

Fact-finding 19–30 Nov 2006 7 70 p, e, t (2), s, f, l Loan appraisal 28 Jan–2 Feb 2007 6 30 p, f, l, e, t, a Special loan administration 23–24 Jul 2007 2 4 t, i Inception 13–17 Jan 2008 3 15 t (2) i Special loan administration 5–7 Aug 2008 2 6 t (2) Review 6–9 Jul 2009 3 12 t (2), a Special loan administration 13–15 Dec 2009 1 3 t Review 28 Feb–2 Mar 2010 1 3 t Review 26–30 Sep 2010 2 10 t (2) Special loan administration 12–13 Apr 2011 2 4 t, a Completion review 21–24 Oct 2012 3 18 t, a, c

a = analyst, c = consultant, e = environment specialist, f = financial specialist, i = implementation officer, l = counsel, p = private sector development specialist, s = social specialist, t = transport specialist.

I. PROJECT DESCRIPTION

1. The Asian Development Bank (ADB) approved a loan of SDR3,544,000 ($5.33 million equivalent) from its Special Funds resources to the Republic of the Maldives on 24 April 2007 for the Domestic Maritime Transport Project. The project’s objective was to deliver sustained, equitable, and regionally balanced economic growth within the Maldives through facilitating access to markets and social services. 2. At appraisal, the project comprised (i) an infrastructure investment component (IIC), and (ii) an institutional development and capacity building (IDCB) component. 1 The IIC was to expand the existing Malé North Harbor (MNH) through (i) construction of a new quay 290 meters (m) long, projecting northward at right angles to Marine Drive alongside the boundary to Malé Commercial Harbor; (ii) ancillary civil works; (iii) provision of cargo handling equipment; (iv) construction of a temporary transit area for goods and passengers; and (v) consulting services for detailed design, preparation of tender documents, bid evaluation, construction supervision, and project management assistance. The IDCB component aimed to increase sustainability of the investment and enhance ongoing sector initiatives by providing support for (i) current efforts to align the organizational structure of the Ministry of Transport and Communication (MTC) to its sector mandate, in particular focusing on policy, planning, and regulatory functions of international and domestic maritime transport infrastructure and transport services; (ii) capacity building within MTC in the areas of (a) strategic planning and policy analysis, (b) establishment of harbor usage charges, (c) maritime safety regulations and vessel inspection and registration procedures, and (d) project performance and impact monitoring; and (iii) capacity building within the Ministry of Construction and Public Infrastructure (MCPI) to enable it to manage, operate, and maintain maritime transport infrastructure in Malé in a sustainable manner through (a) harbor management, and (b) financial management training. 3. The investment cost of the project was estimated at $6.65 million, including taxes and duties of $0.43 million. The project cost would be financed by an ADB loan of $5.33 million and government counterpart funds of $1.32 million. The executing agency was to be the Ministry of Finance and Treasury. The implementing agency was to be MTC. Project implementation units (PIUs) were to be established in MTC and MCPI, respectively, to implement the IDCB component and IIC. The project will directly benefit vessel owners, passengers (domestic and international), and cargo owners and shippers from outer atolls. The economic internal rate of return was originally estimated at 22.5%. The project was scheduled for completion before 31 December 2009.

II. EVALUATION OF DESIGN AND IMPLEMENTATION

A. Relevance of Design and Formulation

4. Malé North Harbor is the lifeline access point to the social and economic development opportunities available in the capital for 70% of the population living in outer atolls, where the incidence of poverty is highest. At appraisal, congestion in MNH was chronic, constituting a bottleneck for the poorest population to enter the capital as a result of inadequate harbor capacity and weak harbor management. Improvement of the existing harbor facilities was ranked the highest priority within the government’s Seventh National Development Plan 2006–

1 ADB. 2007. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to the

Republic of the Maldives for the Domestic Maritime Transport Project. Manila.

2

2010 (7th NDP).2 Constructing an additional quay and associated facilities would alleviate congestion at the harbor and on the feeder road. Together with the IDCB component, the infrastructure investment would enhance sustainability and increase MNH’s operational efficiency. 5. ADB shared the government’s view on MNH’s importance within the country’s socioeconomic context. 3 Therefore, assistance to improve the country’s main inter-atoll transport hub became a priority investment project. This was also included in ADB’s country strategy and program update. ADB supported the government’s long-term sector objectives of (i) separating maritime transport sector policy, planning, and regulatory functions from operational activities; (ii) realigning MTC to materialize the changes; and (iii) introducing efficiency and sustainability into public sector provision of domestic maritime transport infrastructure, as outlined in the 7th NDP. The project was designed to address both investment and institutional aspects in the transport sector. Availability of skilled and experienced staff for project implementation and monitoring was identified as a major constraint which was to be mitigated through the deployment of consulting services for the IIC and capacity building in the IDCB component. 6. At both appraisal and completion, the project was deemed relevant4 to the government‘s objectives and policies, as well as to ADB‘s country strategy. Upon completion, a new quay of 268 m was constructed to enhance the existing MNH. The required ancillary facilities and cargo handling equipment were also installed at the new quay. The project was supported with substantial consulting services, including those for the IIC and IDCB. Despite its slightly longer implementation period, the project successfully achieved its objectives at appraisal. The outputs and outcomes of the project meet the government’s development objectives and ADB’s country strategy. The design and monitoring framework of the project with results is in Appendix 1.

B. Project Outputs

1. Infrastructure Investment Component

7. During implementation, it was found that the original budget was insufficient to implement the full length of the proposed quay wall. As such, there was a minor revision to build a quay wall 268 m long, rather than 290 m long. The IIC entailed (i) dredging of the harbor basin to a mean sea level of 4.0 m deep and reclamation of 26,500 cubic meters; (ii) construction of additional drive-on access and cargo handling area of 6,500 square meters paved with interlocking concrete blocks; (iii) provision of such ancillary harbor facilities as mooring bollards, fenders, gates, fencing, guard posts, and lighting system; (iv) a covered shelter of 480 square meters to protect passengers and cargos, as well as for a management office and guard room; and (v) utility works such as electricity, water supply, drainage, and sewer lines. Project outputs are detailed in Appendix 2. The IIC was completed by 31 December 2010, the extended loan closing date. No serious quality problem was reported during the defects liability period.5 The project completion review mission found that the new infrastructure was constructed in good quality and is currently in operation.

2 The 7th NDP, endorsed by the ministers in the Cabinet, covers the period 2006–2010.

3 ADB. 2005. Country Strategy and Program Updates (2006-2008): Maldives. Manila

4 The rating is determined based on ADB. 2013. Guidelines for Preparing Performance Evaluation Reports for Public

Sector Operations. Manila. 5 One year after physical completion of the civil work.

3

2. Institutional Development and Capacity Building Component 8. The IDCB was focused on (i) institutional alignment of MTC’s maritime transport activities with its sector mandate; (ii) capacity building in MTC to effectively plan and regulate the maritime transport sector; and (iii) capacity building in MCPI, especially for harbor management and financial management training. 9. The key recommendation of the IDCB was to set up a Maldives Ports and Maritime Authority to separate planning, policy, and regulatory functions from operational functions. The authority is currently being implemented. As part of improving capacity to better regulate the maritime sector, a new harbor usage charge was also developed and introduced successfully. 10. It had been envisioned during appraisal that MCPI would take over and operate the new harbor facilities. Due to internal restructuring, however, the government decided to hand over management and operation of the new facilities to Maldives Ports Limited (MPL) rather than MCPI. Since MPL already owned and operated the commercial port activities at the commercial harbor adjacent to MNH, the training and financial management component under the IDCB was no longer relevant. Consequently, this was removed from the original scope of the IDCB.

C. Project Costs

11. At appraisal, the total project cost, including IIC and IDCB, was estimated at $6.65 million. This included the base cost, tax, contingency, and financial charge. Upon completion, the actual project cost totaled $6.14 million, or about 7.7% less than estimated. 12. The actual cost for the IIC was about 23% higher than originally estimated. This was mainly due to increase in scope and price inflation, since the costs were estimated in 2002 but procurement was during 2007–2009.6 Nevertheless, the additional costs could be fully covered by contingencies.7 At the same time, the actual cost for the IDCB component was diminished from $0.69 million to $0.65 million due to the reduction in scope. Hence, the actual cost at completion turned out to be only slightly (7.7%) lower than originally estimated. Appendix 3 compares the details of the project costs at appraisal and at completion. 13. The project was financed by the ADB loan of $5.33 million (80.2% of total project cost) and the government’s counterpart funds of $1.32 million (19.8% or total). The ADB loan came from ADB’s Special Funds resources with a 32-year term (including a grace period of 8 years) and annual interest rate of 1.0% during the grace period and 1.5% thereafter. The interest charges were capitalized. Under the loan, ADB was to finance 80% of civil works and 100% of consultancy services for both the IIC and IDCB. The government was to provide counterpart funding for the remaining 20% of civil works costs. During implementation, however, the cost of the civil works component increased, while the cost of consulting services decreased. To maximize use of the loan, ADB’s financing portion for civil works was raised. Overall, ADB’s financing portion rose from 80% to 82.3% and the government’s counterpart financing share declined from 20% to 17.7%. Detailed comparison of the financing plan at appraisal and actual is in Appendix 3.

6 During implementation, it was found that additional scope was required for demolition of existing structures and

constructing additional facilities (including a management office with guard room). 7 In Maldives, the average consumer price index was 4.15% per annum during 2002–2009.

4

D. Disbursements

14. The ADB loan was approved on 24 April 2007, signed on 29 August 2007, and became effective on 23 October 2007. Initial disbursement of the ADB loan was slow, mainly due to start-up delays in procuring civil works. Moreover, a lengthy withdrawal application process was used initially and involved several agencies. This was resolved during a review mission, whereby the process was streamlined and shortened to involve only key agencies. To enable completion of the project, the government requested, and ADB approved in December 2009, an extension of the loan closing date by 12 months from original 31 December 2009 to 31 December 2010. 15. The ADB loan closed on 31 December 2010, by which time the IIC was completed. The loan account was kept open to facilitate loan disbursement beyond the loan closing. In 2011, the total loan disbursement was $1.97 million (38.6% of the total loan amount). After resolving some disputes between the government and the IDCB consultants regarding the reduction of scope in the IDCB, the final disbursement of $79,153.30 was made on 16 March 2012, at which time the ADB loan account was closed. Overall, SDR3,261,587.84 ($5,059,290.00 equivalent) was disbursed. The undisbursed amount of SDR282,412.16 was automatically cancelled. Appendix 4 shows the projected and actual disbursements of the loan proceeds.

E. Project Schedule

1. Infrastructure Investment Component (IIC) 16. Although advanced actions were taken to engage consulting services for the IIC in December 2006, the recruitment took longer than expected. The IIC consultants contract was awarded in November 2007, which was about 5 months behind the original schedule. The consultants made rapid progress to undertake detailed design and produced the bidding documents ready for tender of the IIC works by March 2008. During the first bidding exercise, the bids opened in August 2008 were substantially higher than the original budget. To fit the budget, the government made a minor revision by reducing the length of the quay wall. The retender was issued in May 2009. The contract for IIC works was awarded in October 2009, and mobilized in November 2009.

17. The construction works were completed by December 2010. The construction took 2 months longer than estimated at appraisal, which resulted in a 12-month delay in project completion. To enable project completion, ADB extended the loan from 31 December 2009 to 31 December 2010. The consulting service for the IIC was completed at the same time, with extensions approved by ADB.

2. Institutional Development and Capacity Building Component

18. Similarly to the case for the IIC, advanced actions were taken to engage the IDCB consultants in December 2006. The first round of selection was not successful, however, since none of the submitted bids met the minimum qualifications stated in the terms of reference. Moreover, the bidders also lacked familiarity with local conditions. The second round of selection that was re-advertised in October 2007 was successful, and the IDCB consultants contract was awarded on 7 August 2008 and mobilized on 17 September 2008. 19. Since the IDCB was initially designed to develop capacity within MCPI to undertake operational responsibilities for the new harbor infrastructure, the operational training component

5

was postponed by the delays in constructing the new harbor. Moreover, the government underwent major restructuring during project implementation and there were delays due to the time taken by the government to decide on the appropriate agency to operate and manage the new harbor. The government eventually decided to hand over this responsibility to MPL. Since MPL was already managing existing ports, the financial management and training components in the IDCB were no longer required and accordingly were removed from the IDCB scope.

20. Although the consultant made requests to extend the contract expiry date beyond the original expiry date of 30 November 2010 to complete the outstanding tasks, the government did not approve these, as it was felt that the remaining tasks were no longer required and should be removed from the original scope. This resulted in some disputes between the government and the IDCB consultants regarding the final payment. Eventually, this was resolved successfully by mutual agreement for partial payment to the consultant, and the contract was concluded on 31 December 2010. The actual project implementation schedule is in Appendix 5 and a chronology of major events is in Appendix 6. 21. Overall, it is assessed that the IIC constituted the project’s critical path. The main contributor to delay in project completion was the delay in procuring the civil works. F. Implementation Arrangements

22. At appraisal, the Ministry of Finance and Treasury was identified as the executing agency and MTC as the implementing agency. During implementation, a project implementation unit (PIU) was established within MTC for the IDCB component and another PIU was established within MCPI for the IIC. Due to restructuring of the government after the presidential election in November 2008, key persons responsible for implementing and administering the transport project were reappointed. MTC and MCPI were merged with other ministries and formed a new ministry—the Ministry of Housing, Transport and Environment. Consequently, the two PIUs merged. 23. A project steering committee was established during project preparation. This was chaired by MTC and included representatives at director level from the Ministry of Finance and Treasury; MCPI; Ministry of Environment, Energy, and Water; Ministry of Planning and National Development; Ministry of Housing and Urban Development; and Malé Municipality. The project steering committee held regular meetings and provided overall policy and operational advice and guidance to project implementation. 24. The PIU was further supported by the IIC consultants, who were organized into two sub-teams—the design and supervision group and the project management assistance group. The project management group assisted the PIU in many aspects, including to prepare work schedules, monitor progress, check tender documents and drawings, review construction costs and payments, assist with procurement and contract management, coordinate meetings, prepare monthly reports, and carry out environmental monitoring. The design and supervision group focused on the engineering design and construction quality control. Given the successful completion of the civil works, this arrangement proved to be effective.

25. The IDCB consultants also supported the PIU to facilitate efficient loan administration and implementation. The organizational structure for project implementation is in Appendix 7.

6

G. Conditions and Covenants

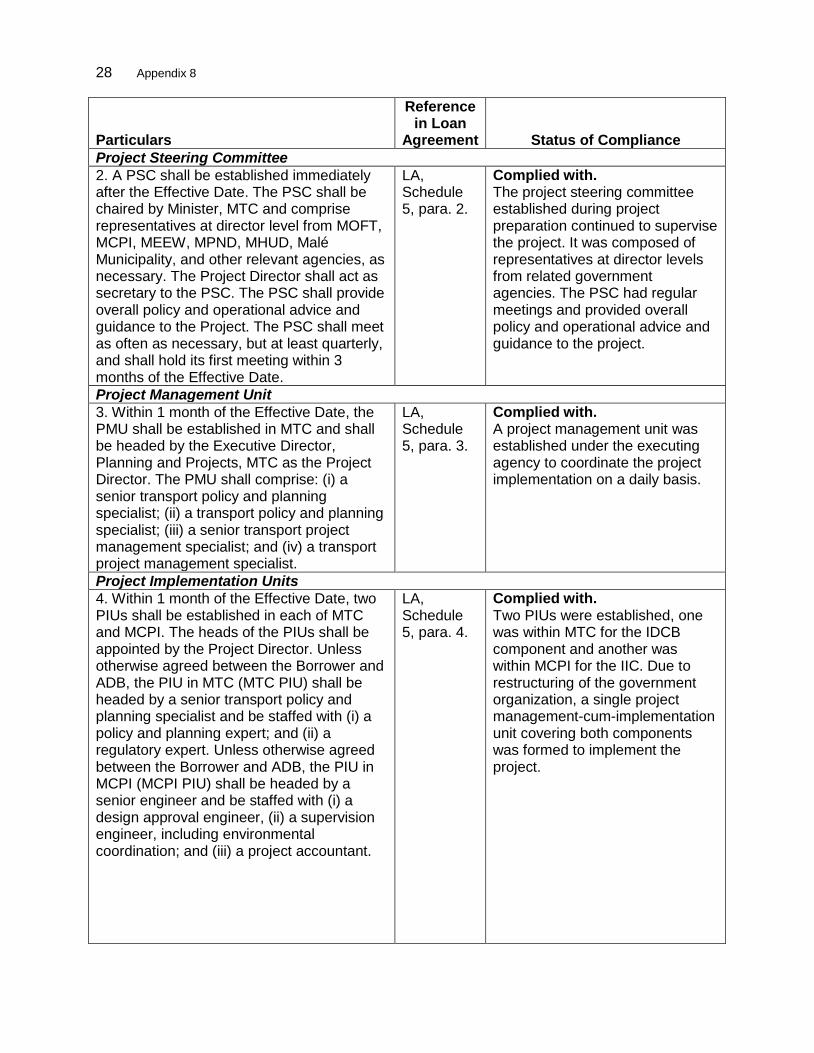

26. The project implementation mostly complied with most of the loan conditions and covenants, including institutional arrangement, counterpart fund provision, financial and contract management, environmental and social safeguard, report preparation and submission, and initial operation arrangement. As part of enhancing governance, the IIC consultants successfully provided support to the PIU on procurement and project management. A separate financial account was established for the project, an external editor was recruited to audit the financial statements, and audited project accounts were submitted up to 2009. There were delays encountered in the submission of financial statements, mainly due to shortage of experienced staff. Nevertheless, the establishment of the financial audit system itself presents a significant improvement toward enhancing governance. In terms of monitoring, the project performance monitoring system for socioeconomic impact was not implemented as planned. This has caused some difficulties in monitoring the performance of the project. Nevertheless, some of this impact is mitigated as MPL collects some of the required data as part of its operations. The status of compliance with key loan covenants of the project is summarized in Appendix 8. H. Consultant Recruitment and Procurement

27. At appraisal, two consulting services packages and one civil works package were designed. During implementation, both consultancy services packages were recruited in compliance with ADB’s Guidelines on the Use of Consultants (2006, as amended from time to time). These packages are summarized in Appendix 9. At appraisal, the government requested ADB’s assistance for undertaking advance actions necessary to facilitate the consultant recruitment, which was approved by ADB. The consulting services were advertised on ADB’s Business Opportunities website on 19 December 2006, and the expressions of interest were requested by 15 February 2007 for the IIC consultants and by 15 March 2007 for the IDCB consultant. For the IIC consultants, quality- and cost-based selection on biodata proposals was used. Following ADB’s approval of the short list and evaluation criteria, the request for proposals was issued on 23 March 2007 with a submission date of 14 April 2007. The evaluation result of the technical proposals was approved by ADB on a no-objection basis on 14 May 2007, and the subsequent opening and evaluation of financial proposals led to the conclusion that Japan Port Consultants was the only eligible firm.8 On 14 June 2007, ADB advised the government to proceed with inviting the firm for contract negotiations and reminded the government that the consultant should not be mobilized prior to the loan effectiveness. On this basis, the government proceeded with inviting Japan Port Consultants for contract negotiation and requested ADB’s participation as an observer. The contract between the government and the IIC consultants was signed on 15 November 2007. 28. Quality- and cost-based selection was also used for recruiting the IDCB consultants, and simplified technical proposals were required. ADB approved the short list and evaluation criteria for the IDCB consultants on 19 April 2007. The request for proposals was issued on 26 April 2007, but the technical evaluation concluded on 18 July 2007 that none of the firms were qualified. Following discussions with the government, the IDCB component was re-advertised. This time, a consortium of firms was selected.9 Contract negotiations on the consulting services were held in Malé on 5 August 2008, and the contract was signed on 7 August 2008.

8 Japan Port Consultants, Tokyo, Japan.

9 SMEC International Pty Ltd (Australia), in association with GreenTech Consultants Pvt. Ltd (Sri Lanka) and

Commerce, Development and Environment Pvt. Ltd (Maldives).

7

29. The civil works for the IIC, comprising just one contract of $3.89 million, was procured using international competitive bidding and the single-stage, one-envelope procurement method. Following the bid opening on 7 August 2008, however, it was found that the bidding price was substantially higher than budgeted. The government reduced and revised the scope of the project, and reissued the retender documents on May 2009. The bids of the retenders were opened and evaluated on 9 July 2009. This time a domestic firm was successfully selected, and the civil works contract was signed on 27 October 2009. Overall, the procurement for civil works was compliant with ADB’s Procurement Guidelines (2007, as amended from time to time). I. Performance of Consultants and Contractors

1. IIC Consultants 30. The performance of the IIC consultants was highly satisfactory. As anticipated at appraisal and as specified in the terms of reference, the IIC consultants successfully completed (i) detailed design, (ii) preparation of tender documents, (iii) bid evaluation support, (iv) construction supervision, (v) project management assistance to the government, and (vi) environment monitoring. Due to delay in the civil works procurement and implementation, however, the contract for the IIC consultants was extended several times upon requests from the government. The IIC consultants completed their services on 31 December 2010 with total inputs of 36.14 person-months that included 18.00 person-months for international consultants and 18.14 person-months for domestic consultants. Upon completion, two reports were submitted by the consultant, including the main completion report and an environmental monitoring report.10 The main report was comprehensive, covering the necessary aspects of the project implementation, including major activities, implementation schedule, institutional framework, and project cost. The environmental reports included the results of the environmental monitoring survey and assessed the environmental impacts. These reports were comprehensive and sufficiently addressed all environmental issues.

2. IDCB Consultants

31. The performance of the IDCB consultants was partly satisfactory. The IDCB component consisted of three subcomponents: (i) institutional alignment of MTC’s maritime transport activities with its sector mandate, particularly focusing on policy, planning, and regulatory functions of international and domestic maritime transport infrastructure and domestic maritime transport services; (ii) capacity building in MTC in the areas of (a) strategic planning and policy analysis, (b) establishment of harbor usage charges, (c) maritime safety regulations and vessel inspections and registration procedures, and (d) project performance and impact monitoring; and (iii) capacity building in MCPI, especially on harbor management and financial management training. The contract was time-based, with a total ceiling of $764,992 and subceilings for each of 18 milestones. Most of the components were implemented successfully except for capacity building of MCPI due to restructuring of responsibilities within the government. The project performance and impact monitoring system was also not implemented.

32. Capacity building of MCPI. Although, the contract was implemented smoothly at first, there were challenges toward the end. Since the construction was delayed, some of the milestones could not be completed by the consultant before the contract expiry date of 30

10

JPC. 2011. Completion Report—Domestic Maritime Transport Project (Consulting Services for Infrastructure Investment Component); JPC. 2011. Environmental Monitoring Report (July to December 2010)—Domestic Maritime Transport Project (ADB Loan Agreement No. 2327-MLD).

8

November 2010. Moreover, the government decided that MPL would operate the new facilities, rather than MCPI as originally envisaged during appraisal. Since MPL was already an experienced operator of existing commercial ports, the government decided not to extend the contract and to cancel the contract milestones relating to harbor management and financial training of the port operator. Thereafter, the consultant submitted a set of invoices on 31 March 2011, requesting payment for preparatory works that had already been undertaken for the cancelled milestones. The implementing agency, upon review of the invoices, requested the consultant to submit proof of the physical work carried out. There were some disputes on the final payment. As requested, the consultant submitted a revised draft final report in December 2010.11 After reviewing the draft reports prepared by the consultant, the government issued a letter to inform the consultant that the contract was concluded on 31 December 2010 and the disputed issue was settled with partial payment. The project completion review mission confirmed that there were no outstanding payment issues. 33. Project performance and impact monitoring. Although a project performance monitoring system was proposed at appraisal, the necessary surveys and monitoring activities were not implemented during the project.

3. IIC Contractor 34. Overall, the performance of the IIC contractor was satisfactory. A domestic construction company was engaged to undertake the civil works. There was some initial delay in physical progress. This was caused by difficulties in transporting construction materials to the project site, which continued to operate as a harbor during construction. This necessitated contract extension for both the IIC consultants and the contractors. An ADB mission in September 2010 also found that the construction progress was far behind of schedule due to the lengthy withdrawal application process that was used. To expedite matters, the ADB mission and the government took necessary actions to streamline and shorten the withdrawal application process. Thereafter, the disbursements accelerated considerably and the infrastructure component was substantially completed by 31 December 2010. The completion certificate was also issued on 31 December 2010, and the final inspection of the project site was conducted by the client and the IIC consultants team on 6 February 2011. J. Performance of the Borrower and the Executing Agency

35. The performance of the borrower and the executing agency was satisfactory. The borrower is the Republic of the Maldives and the executing agency is the Ministry of Finance and Treasury. MTC was designated as the implementation agency. During implementation, a project steering committee was established to provide substantial guidance and coordination support to the project. The government provided counterpart funds and all necessary support in a timely manner. The PIU was responsible for day-to-day project management and facilitated the project’s successful completion. The PIU was well staffed and responsible. Staff members worked in a collaborative manner with ADB, consultants, and contractors to resolve implementation challenges. With assistance from the IIC consultants, the PIU was able to prepare all the project progress reports. An external auditor was recruited to audit the project’s financial statements.12 The audited report for 2008 was submitted to ADB a year late, however, and this resulted in the Project Performance Report Rating being “at risk”.

11

SMEC. 2010. Draft Final Report—Domestic Maritime Transport Project—Institutional Development and Capacity Building (ADB Loan 2327-MLD).

12 The financial accounts were audited by AH&ASSOCIATES, Maldives.

9

K. Performance of the Asian Development Bank

36. Overall, the performance of ADB was satisfactory. The project was administered and supervised from ADB headquarters. ADB provided substantial guidance and support to the government and the PIU in all aspects of project implementation, such as approving advance actions, preparing documents and evaluation reports related to procurement, engaging consultants and contractor, and commenting on technical issues. ADB maintained close engagement with the implementing agency during project implementation. Eight project review missions were conducted, during which ADB participated in joint coordination and review meetings together with the Ministry of Finance and Treasury, the implementing agency, and the contractor and consultants. ADB was closely involved in monitoring progress. It identified project issues—especially time-critical issues—and worked with the government to resolve these. The loan closing date was extended once to accommodate the revised project schedule. The role of the ADB missions in advising on contract administration and technical issues was also recognized by the government.

III. EVALUATION OF PERFORMANCE

A. Relevance

37. At appraisal and completion, the project was rated relevant and consistent with the government’s development strategy and ADB’s country partnership strategy. Given its geographic and physical characteristics, maritime transport is the country’s lifeline. The MNH project was and remains crucial to enhancing distribution of essential supplies and accessibility from the capital city of Malé to the other atolls for the majority of the population. The outputs and outcomes have proven that the project is important, timely, and effective in enhancing domestic maritime transport sector development in the Maldives and promoting economic development. 38. The project is a continuation of ADB’s efforts to support the government’s development plans. The 7th NDP outlines a development path based on economic growth, social equity, poverty reduction, environmental protection, and good governance. It provides a policy framework for realizing the long-term goals of the President’s Vision 2020. The plan, which continues the strategies and lessons from implementing the Sixth National Development Plan, focuses on creating equitable opportunities and more fairly distributing income and wealth. 39. Recognizing the paramount importance of the maritime transport sector in ensuring population-wide access to social and economic development opportunities, the 7th NDP includes 12 policies with supporting sub-strategies in the form of a combined land and sea transport roadmap. Considering the lifeline characteristics of MNH in enhancing access for the majority of the population living in the outer atolls, where the incidence of poverty is higher, the project has been considered a high priority investment within that roadmap. 40. In terms of institutional capacity, and in line with the 7th NDP objectives of improving the overall management and efficiency of the transport sector, the project also identified the need to separate maritime regulatory functions from operational functions. The recommendation to establish a Maldives Ports and Maritime Authority is currently being implemented. The project was also particularly successful in developing and successfully implementing harbor usage charges at MNH. This promotes better financial and operational sustainability over the long-term, and it fits with the 7th NDP objective to enhance harbor management capacity at Malé.

10

B. Effectiveness in Achieving Outcome

41. The project is rated highly effective in achieving its outcome. At appraisal, MNH, served as the gateway to the capital for the outer atoll population and for inter-atoll passenger and cargo vessels. It had a quay wall of just 200 m. The harbor area had no infrastructure to support loading and unloading, and its operational efficiency was hindered by lack of harbor management. The insufficient capacity resulted in long vessel waiting times, severe congestion, and, consequently, economic losses for vessel owners. The combination of the aforementioned factors essentially increased transport costs for passenger movement and cargo distribution to and from Malé, thereby limiting access to social and economic development opportunities. 42. The project successfully delivered a new quay 268 m long that has drive-on access, a cargo handling area, ancillary facilities, and utilities. Upon completion, MNH’s operation was handed over to MPL, which has been operating the adjacent Malé Commercial Port for many years. Hence, MPL already possessed the capacity needed to operate the new facilities in terms of management, staffing, funding, and maintenance. Since taking over the new facilities, MPL has implemented various traffic management measures which have been effective in ensuring smooth operations on both the road side and harbor side.

43. Before the physical improvements at MNH, the average turnaround time for vessels was 3.99 days. According to MPL, after the new facilities were opened, the turnaround times for the vessels was reduced to 2.41 days in 2011 and 2.59 days in 2012. This was estimated based on the 2,521 vessel arrivals at MNH during 2011 (May to December) and 3,502 vessel arrivals during 2012 (January to October). The drive-on access and cargo handling area have substantially improved the efficiency in loading and unloading cargo. This drive-on access area has been well utilized, being used on average by about 473 vehicles daily. The operation of the new quay and improvement of the harbor facilities have well facilitated the rapidly growing traffic. Reduced waiting and handling times have brought significant economic benefits to the Maldives. Meanwhile, the project is also generating increased revenue through new harbor usage charges that were developed under the IDCB component. This, too, has supported more efficient harbor operations while at the same time contributing to recovery of the investment costs. Appendix 10 provides a summary of the project’s initial operation. 44. The key recommendations under the IDCB component have been implemented. For example, the proposed creation of the Maldives Ports and Maritime Authority (in order to separate regulatory and operational functions) is currently being implemented; a harbor usage charging system has been introduced at the new facilities (see Appendix 10); and the review of maritime safety regulations has been completed. Although the project performance monitoring system was not implemented, this did not impact on project outcome since MPL already had an existing system that collects information similar to that required by the performance monitoring system for the new facilities. C. Efficiency in Achieving Outcome and Outputs

45. Overall, despite the year-long delay in project completion, the project is still rated efficient in consideration of its robust economic benefits and generation of additional revenues from the introduction of harbor usage charges. 46. The economic reevaluation compared the economic costs and benefits for the “with-project” and “without-project” cases. Economic benefits considered in the reevaluation include (i) passenger time cost savings, (ii) vessel turnaround time cost savings, and (iii) vehicle

11

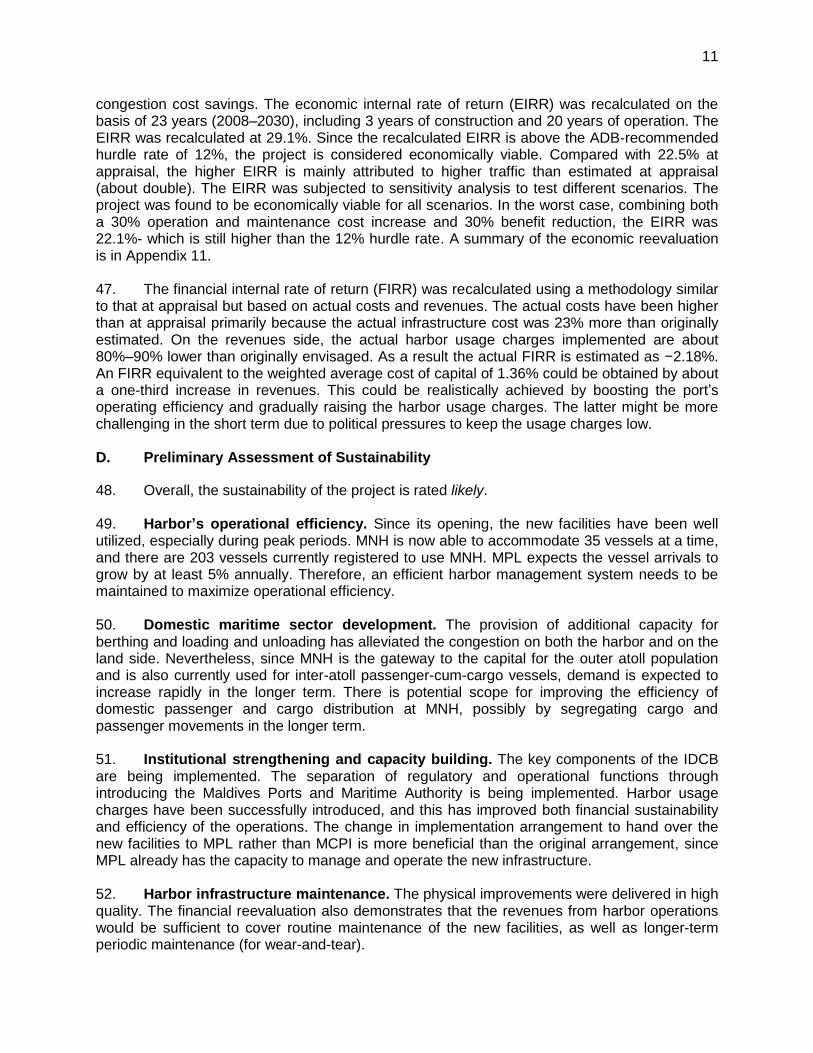

congestion cost savings. The economic internal rate of return (EIRR) was recalculated on the basis of 23 years (2008–2030), including 3 years of construction and 20 years of operation. The EIRR was recalculated at 29.1%. Since the recalculated EIRR is above the ADB-recommended hurdle rate of 12%, the project is considered economically viable. Compared with 22.5% at appraisal, the higher EIRR is mainly attributed to higher traffic than estimated at appraisal (about double). The EIRR was subjected to sensitivity analysis to test different scenarios. The project was found to be economically viable for all scenarios. In the worst case, combining both a 30% operation and maintenance cost increase and 30% benefit reduction, the EIRR was 22.1%- which is still higher than the 12% hurdle rate. A summary of the economic reevaluation is in Appendix 11. 47. The financial internal rate of return (FIRR) was recalculated using a methodology similar to that at appraisal but based on actual costs and revenues. The actual costs have been higher than at appraisal primarily because the actual infrastructure cost was 23% more than originally estimated. On the revenues side, the actual harbor usage charges implemented are about 80%–90% lower than originally envisaged. As a result the actual FIRR is estimated as −2.18%. An FIRR equivalent to the weighted average cost of capital of 1.36% could be obtained by about a one-third increase in revenues. This could be realistically achieved by boosting the port’s operating efficiency and gradually raising the harbor usage charges. The latter might be more challenging in the short term due to political pressures to keep the usage charges low. D. Preliminary Assessment of Sustainability

48. Overall, the sustainability of the project is rated likely. 49. Harbor’s operational efficiency. Since its opening, the new facilities have been well utilized, especially during peak periods. MNH is now able to accommodate 35 vessels at a time, and there are 203 vessels currently registered to use MNH. MPL expects the vessel arrivals to grow by at least 5% annually. Therefore, an efficient harbor management system needs to be maintained to maximize operational efficiency. 50. Domestic maritime sector development. The provision of additional capacity for berthing and loading and unloading has alleviated the congestion on both the harbor and on the land side. Nevertheless, since MNH is the gateway to the capital for the outer atoll population and is also currently used for inter-atoll passenger-cum-cargo vessels, demand is expected to increase rapidly in the longer term. There is potential scope for improving the efficiency of domestic passenger and cargo distribution at MNH, possibly by segregating cargo and passenger movements in the longer term. 51. Institutional strengthening and capacity building. The key components of the IDCB are being implemented. The separation of regulatory and operational functions through introducing the Maldives Ports and Maritime Authority is being implemented. Harbor usage charges have been successfully introduced, and this has improved both financial sustainability and efficiency of the operations. The change in implementation arrangement to hand over the new facilities to MPL rather than MCPI is more beneficial than the original arrangement, since MPL already has the capacity to manage and operate the new infrastructure. 52. Harbor infrastructure maintenance. The physical improvements were delivered in high quality. The financial reevaluation also demonstrates that the revenues from harbor operations would be sufficient to cover routine maintenance of the new facilities, as well as longer-term periodic maintenance (for wear-and-tear).

12

53. Financial cost recovery. Although MNH operated at a loss in 2011, its financial status turned modestly profitable in 2012 due to build-up of vessel demand. This should improve, as traffic is anticipated to increase. To capture this growth, MNH should continuously enhance port operational efficiency to manage additional demand. MPL recognizes that the actual tariffs are much lower than envisaged during appraisal. Although there are no firm plans to increase tariffs immediately, the financial position of port operations could be improved by increasing revenues from efficiency improvements as well as gradual increase in usage charges. To further boost revenues, MPL is planning to rent part of the spare capacity in the passenger facilities for retail shops.

E. Impact

1. Environmental Safeguards 54. At appraisal, the project was classified as category “B” according to ADB’s Environmental Assessment Guidelines (2003). In compliance with the Environmental Protection and Preservation Act, 1993, an initial environmental examination report was prepared during project preparation. Provisions were made in the project cost to cover environmental mitigation and monitoring. The initial environmental examination also provided a framework for developing the environmental management plan. The framework included a rolling action plan with periodic monitoring and appropriate budget allocations. The IIC contractors prepared and submitted the environmental management plan in accordance with the initial environmental examination. 55. All impacts identified in the initial environmental examination were addressed during implementation. The IIC contractor executed the environmental measures in the environmental management plan. The key measures included (i) installing a temporary steel sheet pile wall to prevent water-quality impacts; (ii) installing a silt curtain to protect the water quality of the basin; (iii) selecting proper equipment to minimize noise impact on the surrounding area; and (iv) adjusting the timing for transporting construction materials to mitigate additional congestion around the adjacent commercial market. The contractor also conducted regular environmental monitoring in relation to water quality, waste treatment, oil spillage, noise levels, and air pollution at the project site. The IIC consultants supervised the implementation of such surveys and monitoring. The IIC consultants’ final report confirmed that the project caused no significant environmental impacts, and the environmental conditions were generally maintained within original conditions.13

2. Land Acquisition and Social Safeguards 56. During project preparation, it was identified that all land required for the project was owned by the government, no additional land would need to be acquired from private landowners, and no resettlement would be involved. During implementation, the executing agency confirmed that no significant changes occurred from the project design.

3. Socioeconomic Impact

57. At appraisal, the social impact analysis (including a poverty analysis) indicated that the project influence area would be nationwide and approximately 70% of the population (about 209,189 people) residing in outer atolls would benefit from enhanced domestic connectivity with

13

JPC. 2010. Environmental Monitoring Report (July to December 2010), Domestic Maritime Transport Project (ADB Loan 2327-MLD.

13

Malé. Island-based communities have benefitted from reduced turnaround time for vessels in Malé, thereby increasing accessibility and vessel frequencies between outer islands and Malé. 58. For better monitoring of the socioeconomic and environmental impacts, the project required development of a results-based project performance monitoring system in the early stage of project implementation. Although this was not implemented satisfactorily by the IDCB consultant, similar information is being collected by MPL as part of its operations. 59. Site visits and interviews were conducted during the project completion review mission. Vessel operators and passengers revealed that the project has had significant positive socioeconomic benefits, especially for the poor in remote atolls. For example, (i) average monthly inter-atoll traffic and total cargo at MNH grew by 11% from 2011 to 2012; (ii) the turnaround time for vessels decreased from 3.99 days before the project to about 2.59 days; (iii) the average monthly number of passengers passing through MNH rose by about 20% from 2011 to 2012; (iv) most vessels are now able to make about three trips per month as compared to two trips per month before the project; (v) congestion along Marine Drive has been alleviated significantly, and the average speed on Marine Drive is now 25 kilometers per hour versus 8 kilometers per hour at appraisal; (vi) total sales in the farm market in front of MNH have grown by about 50% since the new MNH facilities opened.

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS

A. Overall Assessment

60. Overall, the project is rated successful. It was relevant to the government’s development objectives and ADB’s country partnership strategy. The project’s main objectives have been realized, ensuring redistribution of benefits, as well as sustained, equitable, and regionally balanced economic growth within the Maldives. Vessel arrivals and total cargo passing through MNH rose by 11% from 2011 to 2012 while the number of passengers through MNH grew by 20%. Total sales at the adjacent farm market grew by about 50%. Congestion around the harbor and on the adjacent Marine Drive improved significantly as a result of providing a better organized loading and unloading area within the harbor. 61. In terms of institutional capacity, the project contributed to better aligning MTC’s organizational structure with its mandate. The IDCB component achieved this by recommending establishment of a Maldives Ports and Maritime Authority, which is currently being implemented. A new harbor usage charging system has been successfully introduced as planned. This has improved the efficiency of port operations and reduced vessel congestion. Due to restructuring within the government and the decision to transfer operations to MPL, part of the original scope on financial management and harbor management training was removed. This did not negatively impact the project outcome, since MPL already had the capacity to manage and operate the new facilities. Overall, the project objectives have been met, and the impacts, outputs, and outcomes planned at appraisal have been substantially achieved.

B. Lessons

1. Project Readiness 62. Although the project cost estimate was made in 2002, procurement for the civil works was during 2008–2009. Due to price escalation, the bid prices received were much higher than originally estimated. Eventually, the implementing agency reduced the project scope so as to fit

14

the project costs within the original cost allocation. In the future, it would be beneficial to shorten the time between detailed design and procurement and to use advance procurement to minimize start-up delays. Price escalation should also be factored into the project cost estimate.

2. Project Implementation Schedule

63. There were initial start-up delays due to re-advertising of the IDCB component and rebidding of the IIC. The latter impacted the implementation schedule most and resulted in a one-year delay in completing the IIC. This also necessitated extending the loan by one year to December 2010. In the future, it would be beneficial to undertake more robust feasibility studies.

3. Procurement and Project Management Support 64. Due to frequent restructuring within the government agencies, the PIU team was unstable throughout implementation. For future projects, permanent technical staff within the PIU team should be retained as much as possible to ensure continuity of key knowledge and information throughout the project. To further mitigate this situation, future projects could include strong procurement and project management support to the PIU to ensure smooth project implementation. C. Recommendations

65. Project benefit monitoring and evaluation. Although monitoring and valuation surveys were designed to be conducted annually and the survey report to be submitted to ADB 5 years after project completion, this aspect has not been implemented. In the future, such targeted monitoring and evaluation of project impact should be strengthened and monitored more closely during implementation to ensure its successful delivery. 66. Timing of the project performance evaluation report. The project performance evaluation report could be prepared in 2014 or later. Even better would be for it to be undertaken after the foregoing survey and evaluation activity. By that time, the project will have fully operated for more than 3 years and the project benefits can be more accurately assessed.

A

pp

en

dix

1 1

5

DESIGN AND MONITORING FRAMEWORK

Design Summary Performance Targets/Indicators Data Sources/

Reporting Mechanisms Assumptions and Risks Results

Impact

Sustained equitable and regionally balanced economic growth within the Maldives

Increase Malé North Harbor’s contribution to GDP by 0.1% by 2015 10% volume increase in key outputs of domestic agricultural produce (coconut, watermelon, banana, cucumber, pumpkin, and mango) sold in Malé North Harbor markets by 2014

National Economic Data and Statistics Baseline survey

Assumption

The Agricultural Master Plan targets 100% growth in key agricultural produce by 2015. Improved transport only accounts for a portion of this expected growth, estimated at 2% annually. Risk

Other support mechanisms targeting the agricultural sector may fail to materialize, apart from improved access to markets through transport infrastructure investments.

Achieved.

Maldives’ national GDP grew by 5.7% and 7.5% in 2010 and 2011, respectively. The survey of domestic agricultural produce was not conducted. Hence, the following data have been used as a proxy to measure increases in economic productivity: (i) Vessel arrivals at MNH were

2,521 in 2011 (May–Dec) and 3,502 in 2012 (Jan–Oct), with average monthly gain of 11% in 2012 as compared to 2011.

(ii) Total cargo transported at MNH was 428,570 tons in 2011 (May-Dec) and 595,340 tons in 2012 (Jan–Oct), with average monthly increase of 11% in 2012 as compared to 2011.

(iii) Total passengers at MNH were 60,833 in 2011 (May-Dec) and 91,250 in 2012 (Jan–Oct), with average monthly increase of 20% in 2012 as compared to 2011.

(iv) Total sales of the farm market in front of MNH grew by about 50% in the last 2 years.

Outcome

1. Improved services of Malé North Harbor

1. Operation

Reduction of congestion and increase in the amount of larger vessels calling at Malé North Harbor (i) Total time spent in Malé North

Harbor for small vessels reduced from an average of 10 days to 8 days by August 2014, i.e. after 5 years of operations

(i) Harbor operation

service records

Assumptions

Construction of additional 290 meter quay wall is completed on time. The government will introduce harbor management and harbor usage charges in Malé

Achieved.

As there were no formal surveys for monitoring and evaluation, these indicators from MPL provide the best available comparison: (i) Average turnaround time for

small vessels at MNH was 2.41 days in 2011 (May-Dec) and 2.59 days in 2012.(Jan-Oct)

Design Summary Performance Targets/Indicators Data Sources/

Reporting Mechanisms Assumptions and Risks Results

(ii) Total time spent in Malé North Harbor for large vessels decreased from an average of 15 days to 13 days by August 2014.

(iii) At least 70% of service users (i.e., vessel operators, passengers, and cargo shippers) rate the harbor services “satisfactory” by 2011

(iv) By 2014, at least 1% of passengers and cargo sellers visiting Malé North Harbor report that their trip was induced by improved services

(v) Average traffic flow through (as defined by number of vehicles passing through a given point) on Marine Drive along Malé North Harbor will increase by 25% by 2014

(ii) Harbor operation service records

(iii) Annual harbor user

survey and government reports or feedback

(iv) Annual harbor user

survey and government reports or feedback

(v) Baseline survey

North Harbor based on the training and capacity building outputs. Risk

Factors outside the direct project scope, such as improvements to transport and cargo services provided by vessel owners, may influence harbor usage satisfaction.

(ii) The average turnaround time for large vessels at MNH was 2.41 days in 2011 (May-Dec) and 2.59 days in 2012 (Jan-Oct).

(iii) Most of the vessels made 3 trips a month versus 2 trips before the project.

(iv) The average speed of the vehicles on Marine Drive is about 25 kilometers per hour.

(v)

2. Alignment of MTC’s organizational structure with its mandate

2. Institutional development and capacity building

(i) Action plan for institutional alignment of MTC’s maritime transport activities in line with its sector mandate developed by end February 2008

(ii) Action plan for introduction of harbor usage charges, with supportive documentation, developed by end September 2008

(iii) Action plan for recommended changes to maritime safety regulations, vessel inspections, and registration procedures developed by end December 2008

(iv) Action plan for improvements to financial management systems by end May 2009

(i) Institutional

development and capacity building consultants’ reports

(ii) Institutional

development and capacity building consultants’ reports

(iii) Institutional

development and capacity building consultants’ reports

(iv) Institutional

development and capacity building consultants’ reports

Assumption

Political will exists to implement institutional alignment and human resources enhancement efforts.

Achieved:

(i) The recommendation to set up the Maldives Ports and Maritime Authority was accepted and is now being implemented.

(ii) Harbor usage charges have

been successfully introduced at MNH.

(iii) A local vessel safety regulation

was developed (1999) and a local ferry regulation was implemented in 2009. Some other related regulations have been developed in draft format.

(iv) MPL has a financial management system sufficient for the operations of MNH.

16 A

pp

end

ix 1

A

pp

en

dix

1 1

7

Design Summary Performance Targets/Indicators Data Sources/

Reporting Mechanisms Assumptions and Risks Results

Outputs

1. Capacity of Malé North Harbor enhanced

2. Institutional capacity of

MTC and MCPI upgraded

(i) Construction of quay wall and

ancillary civil works, provision of cargo handling equipment, and construction of a temporary transit area for goods and passengers completed and operational by end February 2009

(i) Strategic policy and planning

capacity building provided (ii) Regulatory capacity building in

harbor usage charges conducted by end September 2008

(iii) Capacity building in maritime safety regulations, vessel inspections, and registration procedures for MTC staff completed by end December 2008

(iv) Project performance monitoring system, comprising impact indicators (including environmental and social aspects) developed by end October 2007

(v) Training in harbor management for MCPI staff completed by end March 2009

(vi) Development of best practices

Design and supervision consultants’ reports Institutional development and capacity building consultants’ reports Government reports or feedback

Assumption

Contracts for detailed design, supervision consultants, and civil works are awarded on time. Risk

Delays in construction caused by weather conditions will affect construction schedule. Assumption

Contracts for institutional development and capacity building consultants are awarded on time. Risks

Staffing of PMU and PIUs in accordance with competency requirements. Trained staff will be retained.

Achieved.

Physical component has been completed, including a quay 268 meters long; dredging of harbor basin; additional drive-on access and cargo handling area; and provision of ancillary harbor facilities, a covered shelter, and utilities.

Mostly achieved.

Institutional component was mostly completed: (i) The strategic policy and

planning capacity were reviewed, and the key recommendation to establish an independent Maldives Ports and Maritime Authority is being implemented.

(ii) Harbor usage charges were

developed and successfully implemented.

(iii) Review of safety regulations

was completed.

(iv) Project performance monitoring system was not satisfactorily implemented, but operational data is now routinely collected by MPL and is suitable for monitoring purposes

(v) Harbor management training was not conducted, because MPL is already an experienced port operator.

(vi) Harbor management manual

Design Summary Performance Targets/Indicators Data Sources/

Reporting Mechanisms Assumptions and Risks Results

operations manual for harbor management completed by mid-May 2009

(vii) Development of best practices operations manual for financial management completed by mid-May 2009

(viii) Project management training

for MCPI completed by end February 2009

has been produced and handed over to MPL.

(vii) Financial management operations manual is no longer required, because the new infrastructure was handed over to an existing, experienced port operator rather than MCPI. Project management training for MCPI is no longer required, because infrastructure was handed over to an existing, experienced port operator.

Inputs 1. Investment

component

Total cost: $4.43 million, with ADB to finance $3.65 million (excluding taxes and duties, interest during construction, and contingencies). The government is to finance $777,112. Consulting services: 25 person-months of international input and 15 person-months of national experts

Inception report Monthly progress reports Final reports ADB review missions

Total project cost: $5.46 million (excluding interest during construction), with ADB financing $4.37 million and the government financing $1.09 million Consulting services: 18.0 person-months of international input and 18.14 person-months of national experts

2. Institutional Development and Capacity Building component

Total cost: $697,500, with ADB to finance $697,500 (excluding taxes and duties, interest during construction, and contingencies). Consulting services: 25.5 person-months of international experts and 18 person-months of national experts

Inception report Monthly progress reports Final reports ADB review missions

Total cost: $0.65 million, wholly financed by ADB Consulting services: 25.5 person-months of international experts and 18 person-months of national experts

ADB = Asian Development Bank, GDP = gross domestic product, MCPI = Ministry of Construction and Public Infrastructure, MNH = Malé North Harbor, MPL = Maldives Ports Limited, MTC = Ministry of Transport and Communication, PIU = project implementation unit, PMU = project management unit. Source: ADB project completion review mission.

18 A

pp

end

ix 1

DETAILS OF PROJECT OUTPUTS

Component or Subcomponent Outputs and Quantity

A. Infrastructure Investment Component

a. Dredging and reclamation Dredging for harbor basin to mean sea level of -4.0 meter (m) depth and reclamation of 26,500 cubic meters

b. Quay walls Construction of quay wall 268 m long with mean sea level of-4.0 m depth, including (1) main part of quay projecting northward at right angles to Marine Dive (123 m long, 30 m wide); (2) eastward leg of quay, placed along and inside existing breakwater (120 m long, 11 m wide); and (3) quay wall between main part and eastward leg (25 m long)

c. Drive-on access and cargo handling area

Additional drive-on access and cargo handling area of 6,500 square meters with interlocking concrete blocks pavement

d. Ancillary facilities Provision of ancillary harbor facilities such as mooring bollards, fenders, gates, fencing, guard posts, and lighting system

e. Shelter Covered shelter of 480 square meters to protect passengers and cargoes, plus management office and guard room

f. Utility works Utility works such as electricity, water supply, drainage and sewer lines

B. Institutional Development and Capacity Building Component

a. Final report for this component (main report)

Draft final report, which covered many aspects of maritime development in Maldives, including (i) review of relevant policies and programs, (ii) recommendations for creation of a ports and maritime authority, (iii) project performance monitoring system, (iv) analysis and recommendations for a legal and regulatory framework, (v) recommended training programs, (vi) Malé North Harbor management and operation, and (vii) assessment of the financial management system

b. Independent reports and appendices

(i) Harbor Management Manual Report, (ii) Baseline Data Report, (iii) Training Program Report, and (iv) Boat Census Report

Source: ADB project completion review mission.

Ap

pe

ndix

2

19

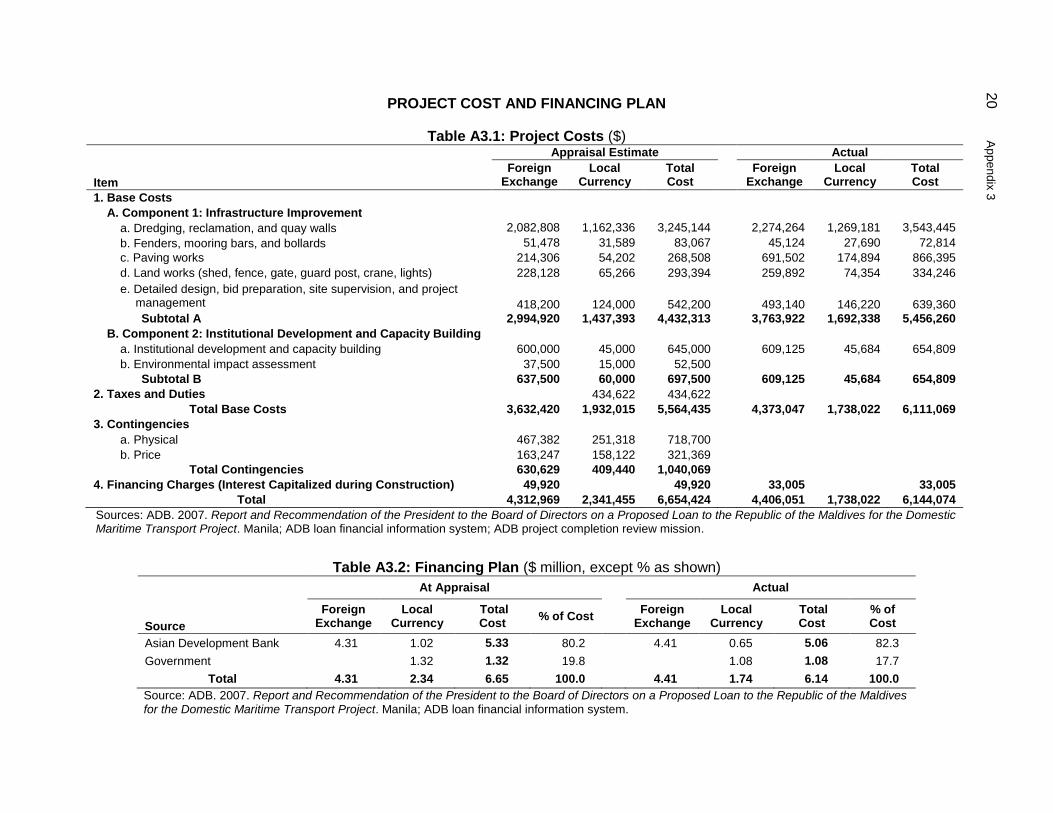

PROJECT COST AND FINANCING PLAN

Table A3.1: Project Costs ($) Appraisal Estimate Actual

Item

Foreign Exchange

Local Currency

Total Cost

Foreign

Exchange Local

Currency Total Cost

1. Base Costs

A. Component 1: Infrastructure Improvement

a. Dredging, reclamation, and quay walls 2,082,808 1,162,336 3,245,144

2,274,264 1,269,181 3,543,445

b. Fenders, mooring bars, and bollards 51,478 31,589 83,067

45,124 27,690 72,814

c. Paving works 214,306 54,202 268,508

691,502 174,894 866,395

d. Land works (shed, fence, gate, guard post, crane, lights) 228,128 65,266 293,394

259,892 74,354 334,246

e. Detailed design, bid preparation, site supervision, and project management 418,200 124,000 542,200 493,140 146,220 639,360

Subtotal A 2,994,920 1,437,393 4,432,313

3,763,922 1,692,338 5,456,260

B. Component 2: Institutional Development and Capacity Building

a. Institutional development and capacity building 600,000 45,000 645,000

609,125 45,684 654,809

b. Environmental impact assessment 37,500 15,000 52,500

Subtotal B 637,500 60,000 697,500

609,125 45,684 654,809

2. Taxes and Duties

434,622 434,622

Total Base Costs 3,632,420 1,932,015 5,564,435

4,373,047 1,738,022 6,111,069

3. Contingencies

a. Physical 467,382 251,318 718,700

b. Price 163,247 158,122 321,369

Total Contingencies 630,629 409,440 1,040,069

4. Financing Charges (Interest Capitalized during Construction) 49,920

49,920

33,005

33,005

Total 4,312,969 2,341,455 6,654,424 4,406,051 1,738,022 6,144,074

Sources: ADB. 2007. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to the Republic of the Maldives for the Domestic Maritime Transport Project. Manila; ADB loan financial information system; ADB project completion review mission.

Table A3.2: Financing Plan ($ million, except % as shown)

Source

At Appraisal Actual

Foreign Exchange

Local Currency

Total Cost

% of Cost Foreign

Exchange Local

Currency Total Cost

% of Cost

Asian Development Bank 4.31 1.02 5.33 80.2

4.41 0.65 5.06 82.3

Government

1.32 1.32 19.8

1.08 1.08 17.7

Total 4.31 2.34 6.65 100.0 4.41 1.74 6.14 100.0

Source: ADB. 2007. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to the Republic of the Maldives for the Domestic Maritime Transport Project. Manila; ADB loan financial information system.

20

Ap

pe

ndix

3

Appendix 4 21

DISBURSEMENT OF ADB LOAN PROCEEDS

Table A4: Annual and Cumulative Disbursement of ADB Loan Proceeds

i.

Annual Disbursement ii. Cumulative Disbursement

Amount

% of Total SDR

Amount

% of Total SDR

Planned Actual

($ million) ($ million) (SDR million)

(SDR million)

2008 4.50 0.19 0.12 3.6

0.12 3.6

2009 3.90 0.50 0.32 9.8

0.44 13.4

2010

2.32 1.51 46.4

1.95 59.8

2011

1.97 1.26 38.6

3.21 98.4

2012

0.08 0.05 1.6

3.26 100.0

Total

5.06 3.26 100.0

ADB = Asian Development Bank. Source: Asian Development Bank.

Figure A4.1: Annual Disbursement of ADB Loan Proceeds ($ million)

Figure A4.2: Cumulative Disbursement of ADB Loan Proceeds

($ million)

ACTUAL PROJECT IMPLEMENTATION SCHEDULES

IDCB = institutional development and capacity building, IIC = infrastructure investment component. Source: ADB project completion review mission.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

At appraisal At actual

The IDBC consultant

Implementation

Civil Works

2008 2009 2010

Implementation

Procurement

Item2006 2007

The infrastructure improvement

The IIC consultant

Recruitment

Recruitment

22

Ap

pe

ndix

5

Appendix 6 23

CHRONOLOGY OF MAJOR EVENTS

Date Main Event

A. Project preparation

2006

19–30 November ADB project fact-finding mission

2007

12 January ADB Management Review Meeting

28 January–2 February ADB project appraisal mission

23 February ADB staff review committee meeting

March Loan negotiation

24 April Board approval

23–24 July ADB special loan administration mission

29 August Loan signing

23 October Loan effectiveness

B. Project implementation

2006

19 December Publishing request for expressions of interest in ADB Business

Opportunities for IIC and IDCB consultants

2007

14 April ADB approval of short list for IIC consultants

19 April ADB approval of short list for IDCB consultants

14 May ADB approval on no-objection basis of IIC consultants selection

result

15 November Contract signing between the government and IIC consultants

2008

13–17 January ADB project inception mission

20 May First disbursement of ADB loan

5–7 August ADB special loan administration mission

7 August First bid opening for IIC component

7 August Contract signing between the government and IDCB consultants

17 September Mobilization of IDCB consultants

2009

30 June Original project completion date

6–9 July ADB project review mission

27 October Contract signing between the government and IIC contractors

4 November Starting of IIC civil work

31 December Original loan closing date

24 Appendix 6

2010

28 February Submission of draft final report for IDCB component

28 February–2 March ADB project review mission

26–30 September ADB project review mission

31 December Substantial completion of IIC component

31 December Contract completion of IIC consultant

31 December Contract completion of IDCB consultant

31 December Actual loan closing date

2011

6 February Final inspection of IIC component

12–13 April ADB special loan administration mission

2012

16 March Actual loan account closing and final disbursement of loan

21–24 October ADB project completion review mission

ADB = Asian Development Bank, IDCB = institutional development and capacity building, IIC = infrastructure investment component. Source: The ADB project completion review mission.

Appendix 7 25

ORGANIZATIONAL STRUCTURE FOR PROJECT IMPLEMENTATION

IIC = infrastructure investment component, IDCB = institutional development and capacity building, MCPI = Ministry of Construction and Public Infrastructure, MOFT = Ministry of Finance and Treasury, MTC = Ministry of Transport and Communication. Source: the ADB project completion review mission.

Project Steering Committee

Project Management Office (PMO)

Project Implementation

Unit (PIU-MTC)

Executing Agency (MOFT)

IDCB

Consultants

Project Implementation

Unit (PIU-MCPI)

Implementation Agency

(MTC)

IIC

Contractor

IIC

Consultants

Ministry of Construction and Public Infrastructure

(MCPI)

26 Appendix 8

STATUS OF COMPLIANCE WITH MAJOR LOAN COVENANTS

Particulars

Reference in Loan

Agreement Status of Compliance

Section 4.02. (a) The Borrower shall (i) maintain, or cause to be maintained, separate accounts for the Project; (ii) have such accounts and related financial statements audited annually, in accordance with appropriate auditing standards consistently applied, by independent auditors whose qualifications, experience and terms of reference are acceptable to ADB; (iii) furnish to ADB, as soon as available but in any event not later than 6 months after the end of each related fiscal year, certified copies of such audited accounts and financial statements and the report of the auditors relating thereto (including the auditors' opinion on the use of the Loan proceeds and compliance with the financial covenants of this Loan Agreement, all in the English language; and (iv) furnish to ADB such other information concerning such accounts and financial statements and the audit thereof as ADB shall from time to time reasonably request.