Embed Size (px)

Citation preview

A survey by YES SECURITIES (INDIA) LIMITED, a wholly owned subsidiary of YES BANK LTD.

M&A and Capital Raising Outlook

S U R V E Y 2 0 1 7

Introduction

M&A and Capital Raising OUTLOOK SURVEY 2017

Pg. 1

Over the past years, India has retained its position as the fastest growing economy in the world, basis its strong domestic fundamentals, despite a weak global economic backdrop. Supporting the positive investment outlook have been factors such as improved inflation-growth mix, favorable external sector ratios and fiscal prudence. The government has maintained its unambiguous focus on raising medium and long-term growth potential through programs such as Smart Cities, Make in India, Start-up India and Digital India. Adding to this are the structural bearings of India’s growth story, which remain intact, including young demograph ics , abundant l abor , h igh intellectual, technical and engineering skills, and large consumer base.

Whi le growth momentum may have moderated after late-FY17 on the back of demonetization-induced liquidity shortage and GST-related uncertainty, these must be viewed as ‘short term disruptions’ in return for ‘long-term gains’. In FY18, we continue to expect GDP to recover to 7.4%, supported by steady consumpt ion and gradua l rev i va l i n investments. Some recovery in exports amid support from incremental recovery in global GDP can also be expected, with the IMF recently raising its 2017 growth forecast to 3.5% (2016: 3.1%) on the back of higher growth in developed economies. However, headwinds in the form of global trade protectionism, geopolitical tensions and financial market gyrations continue to be downside risks.

Even as a majority of domestic indicators have held well, sluggish private sector capex and high corporate debt are some of the key issues that remain unresolved. FY17 saw initiation of deleveraging in some sectors driven by asset sales- a preference for ‘buy vs. build’- in a scenario of subdued domestic and global macros. With consolidation rather than creation being the need of the hour, the past year witnessed a significant increase in M&A activity involving domestic assets of non-financial companies with deals amounting to INR 1.4 lakh Cr (Previous: INR 0.5 lakh Cr). The weakest links have begun to taper with share of weak companies in debt (% of total debt) declining to 14.5% as of Sep-16 (Sep-15: 25%). Going further, we expect this trend to gain more traction in FY18.

This view has been re-affirmed by the respondents of our M&A & Capital Raising Outlook Survey filled by 124 business leaders across industry sectors with an attempt to gauge the future outlook of corporates for strategic investments and raising capital in the next 12 months. A significant majority (65%) of the respondents have voted in favor of reacting to an opportunity of a M&A transaction over the next year- as they consolidate on India’s existing strengths of rising consumer demand and improving economic growth. M&A, PE fund-raising and capital market activity expected to gather pace in the coming year.

Introduction

M&A and Capital Raising OUTLOOK SURVEY 2017

Pg. 1

Over the past years, India has retained its position as the fastest growing economy in the world, basis its strong domestic fundamentals, despite a weak global economic backdrop. Supporting the positive investment outlook have been factors such as improved inflation-growth mix, favorable external sector ratios and fiscal prudence. The government has maintained its unambiguous focus on raising medium and long-term growth potential through programs such as Smart Cities, Make in India, Start-up India and Digital India. Adding to this are the structural bearings of India’s growth story, which remain intact, including young demograph ics , abundant l abor , h igh intellectual, technical and engineering skills, and large consumer base.

Whi le growth momentum may have moderated after late-FY17 on the back of demonetization-induced liquidity shortage and GST-related uncertainty, these must be viewed as ‘short term disruptions’ in return for ‘long-term gains’. In FY18, we continue to expect GDP to recover to 7.4%, supported by steady consumpt ion and gradua l rev i va l i n investments. Some recovery in exports amid support from incremental recovery in global GDP can also be expected, with the IMF recently raising its 2017 growth forecast to 3.5% (2016: 3.1%) on the back of higher growth in developed economies. However, headwinds in the form of global trade protectionism, geopolitical tensions and financial market gyrations continue to be downside risks.

Even as a majority of domestic indicators have held well, sluggish private sector capex and high corporate debt are some of the key issues that remain unresolved. FY17 saw initiation of deleveraging in some sectors driven by asset sales- a preference for ‘buy vs. build’- in a scenario of subdued domestic and global macros. With consolidation rather than creation being the need of the hour, the past year witnessed a significant increase in M&A activity involving domestic assets of non-financial companies with deals amounting to INR 1.4 lakh Cr (Previous: INR 0.5 lakh Cr). The weakest links have begun to taper with share of weak companies in debt (% of total debt) declining to 14.5% as of Sep-16 (Sep-15: 25%). Going further, we expect this trend to gain more traction in FY18.

This view has been re-affirmed by the respondents of our M&A & Capital Raising Outlook Survey filled by 124 business leaders across industry sectors with an attempt to gauge the future outlook of corporates for strategic investments and raising capital in the next 12 months. A significant majority (65%) of the respondents have voted in favor of reacting to an opportunity of a M&A transaction over the next year- as they consolidate on India’s existing strengths of rising consumer demand and improving economic growth. M&A, PE fund-raising and capital market activity expected to gather pace in the coming year.

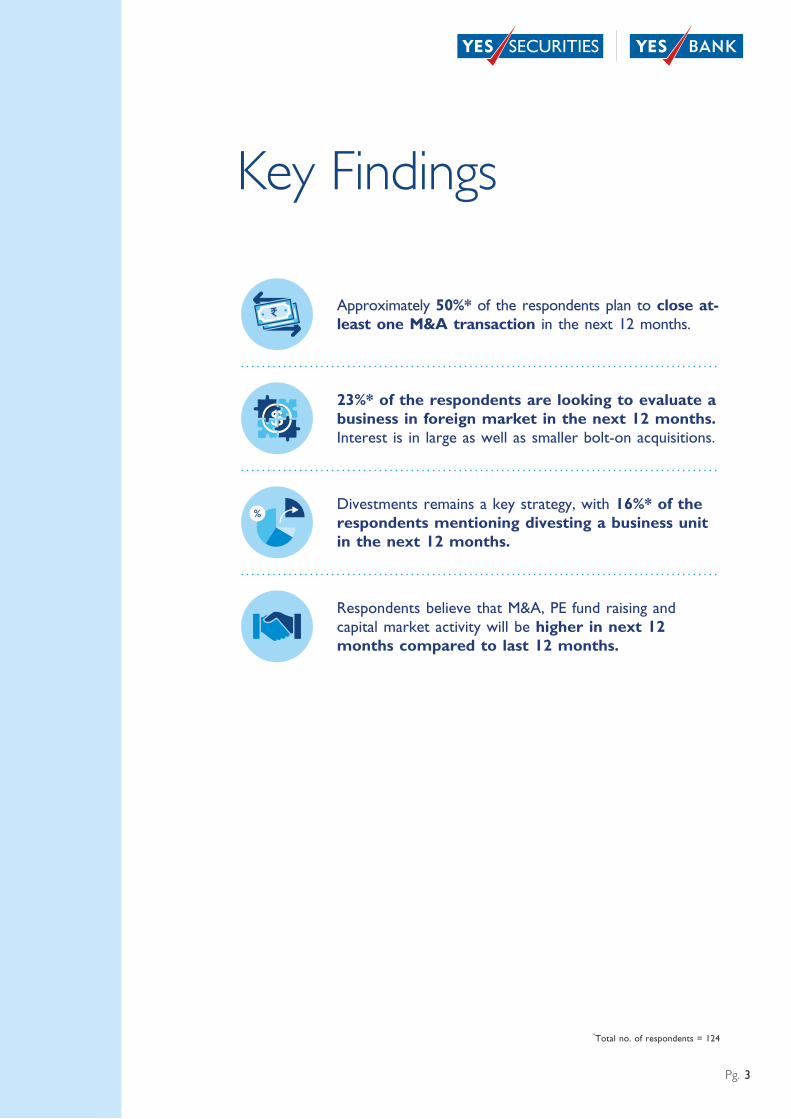

Key Findings

Approximately 50%* of the respondents plan to close at-least one M&A transaction in the next 12 months.

23%* of the respondents are looking to evaluate a business in foreign market in the next 12 months. Interest is in large as well as smaller bolt-on acquisitions.

Divestments remains a key strategy, with 16%* of the respondents mentioning divesting a business unit in the next 12 months.

Respondents believe that M&A, PE fund raising and capital market activity will be higher in next 12 months compared to last 12 months.

M&A and Capital Raising OUTLOOK SURVEY 2017

Pg. 3Pg. 2

*Total no. of respondents = 124

Key Findings

Approximately 50%* of the respondents plan to close at-least one M&A transaction in the next 12 months.

23%* of the respondents are looking to evaluate a business in foreign market in the next 12 months. Interest is in large as well as smaller bolt-on acquisitions.

Divestments remains a key strategy, with 16%* of the respondents mentioning divesting a business unit in the next 12 months.

Respondents believe that M&A, PE fund raising and capital market activity will be higher in next 12 months compared to last 12 months.

M&A and Capital Raising OUTLOOK SURVEY 2017

Pg. 3Pg. 2

*Total no. of respondents = 124

Perspective – Mergers & Acquisitions

Business leaders from the Pharma, Healthcare & Life Sciences sector expressed maximum interest with large chains keen to acquire regional players. It is closely followed by Agribusiness, food & allied services and Technology & Communication showing that leaders are open to M&A if the right opportunity presents itself.

In line with the market scenario, a significant majority of respondents have voted in favor of M&A transactions over the next year.

React to an M&A Opportunity?

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

34% 66%

Yes No

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

82%

Con

sum

er

Goo

ds/R

etai

l

40%

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

20%

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

70%

Man

ufac

turin

g

56%

Med

ia &

En

terta

inm

ent

75%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

88%

Tech

nolo

gy &

C

omm

unic

atio

n

82%

YES

Two-third of the respondents said that they would react to an opportunity and initiate a Mergers & Acquisitions deal in the next 12 months as compared to last 12 months.

M&A and Capital Raising OUTLOOK SURVEY 2017

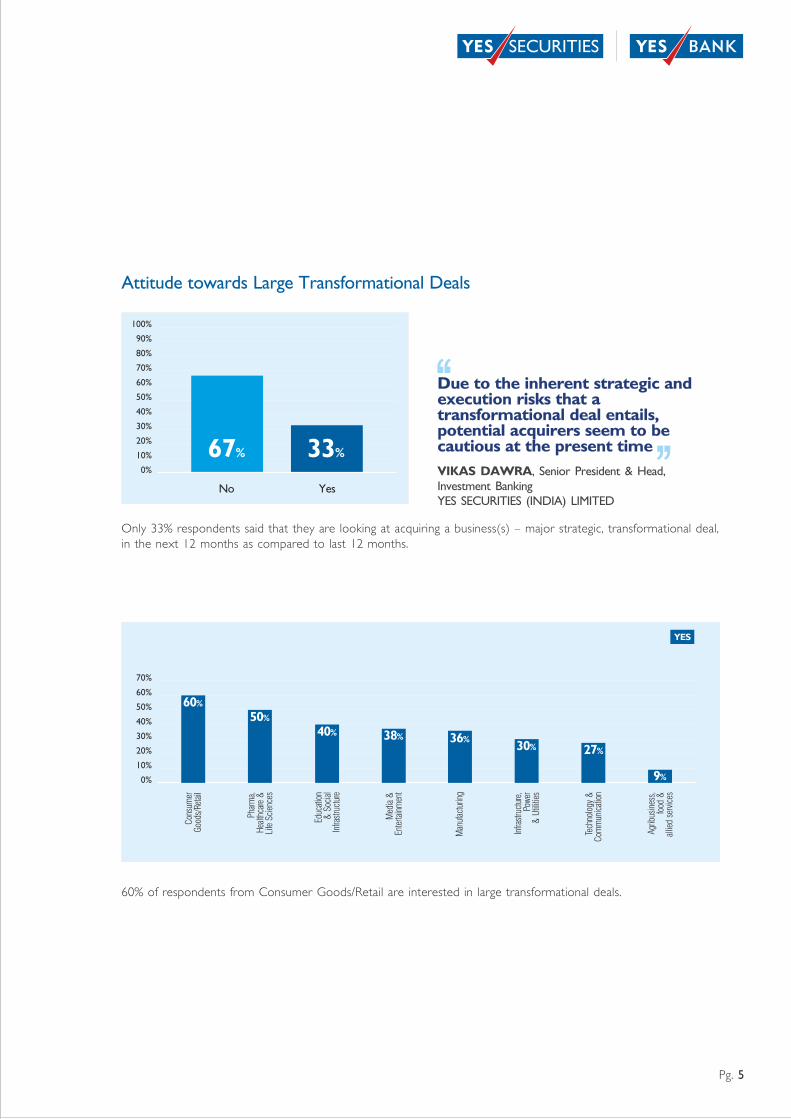

60% of respondents from Consumer Goods/Retail are interested in large transformational deals.

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

33%67%

Yes No

Attitude towards Large Transformational Deals

Due to the inherent strategic and execution risks that a transformational deal entails, potential acquirers seem to be cautious at the present time

VIKAS DAWRA, Senior President & Head, Investment BankingYES SECURITIES (INDIA) LIMITED

Pg. 5Pg. 4

0%

20%

30%

40%

50%

60%

70%

10%

40%

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

9%

36%

Man

ufac

turin

g

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

30%

Med

ia &

En

terta

inm

ent

38%

50%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

Con

sum

er

Goo

ds/R

etai

l

60%

27%

Tech

nolo

gy &

C

omm

unic

atio

n

YES

Only 33% respondents said that they are looking at acquiring a business(s) – major strategic, transformational deal, in the next 12 months as compared to last 12 months.

Perspective – Mergers & Acquisitions

Business leaders from the Pharma, Healthcare & Life Sciences sector expressed maximum interest with large chains keen to acquire regional players. It is closely followed by Agribusiness, food & allied services and Technology & Communication showing that leaders are open to M&A if the right opportunity presents itself.

In line with the market scenario, a significant majority of respondents have voted in favor of M&A transactions over the next year.

React to an M&A Opportunity?

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

34% 66%

Yes No

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

82%

Con

sum

er

Goo

ds/R

etai

l

40%

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

20%

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

70%

Man

ufac

turin

g

56%

Med

ia &

En

terta

inm

ent

75%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

88%

Tech

nolo

gy &

C

omm

unic

atio

n

82%

YES

Two-third of the respondents said that they would react to an opportunity and initiate a Mergers & Acquisitions deal in the next 12 months as compared to last 12 months.

M&A and Capital Raising OUTLOOK SURVEY 2017

60% of respondents from Consumer Goods/Retail are interested in large transformational deals.

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

33%67%

Yes No

Attitude towards Large Transformational Deals

Due to the inherent strategic and execution risks that a transformational deal entails, potential acquirers seem to be cautious at the present time

VIKAS DAWRA, Senior President & Head, Investment BankingYES SECURITIES (INDIA) LIMITED

Pg. 5Pg. 4

0%

20%

30%

40%

50%

60%

70%

10%

40%

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

9%

36%

Man

ufac

turin

g

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

30%

Med

ia &

En

terta

inm

ent

38%

50%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

Con

sum

er

Goo

ds/R

etai

l

60%

27%

Tech

nolo

gy &

C

omm

unic

atio

n

YES

Only 33% respondents said that they are looking at acquiring a business(s) – major strategic, transformational deal, in the next 12 months as compared to last 12 months.

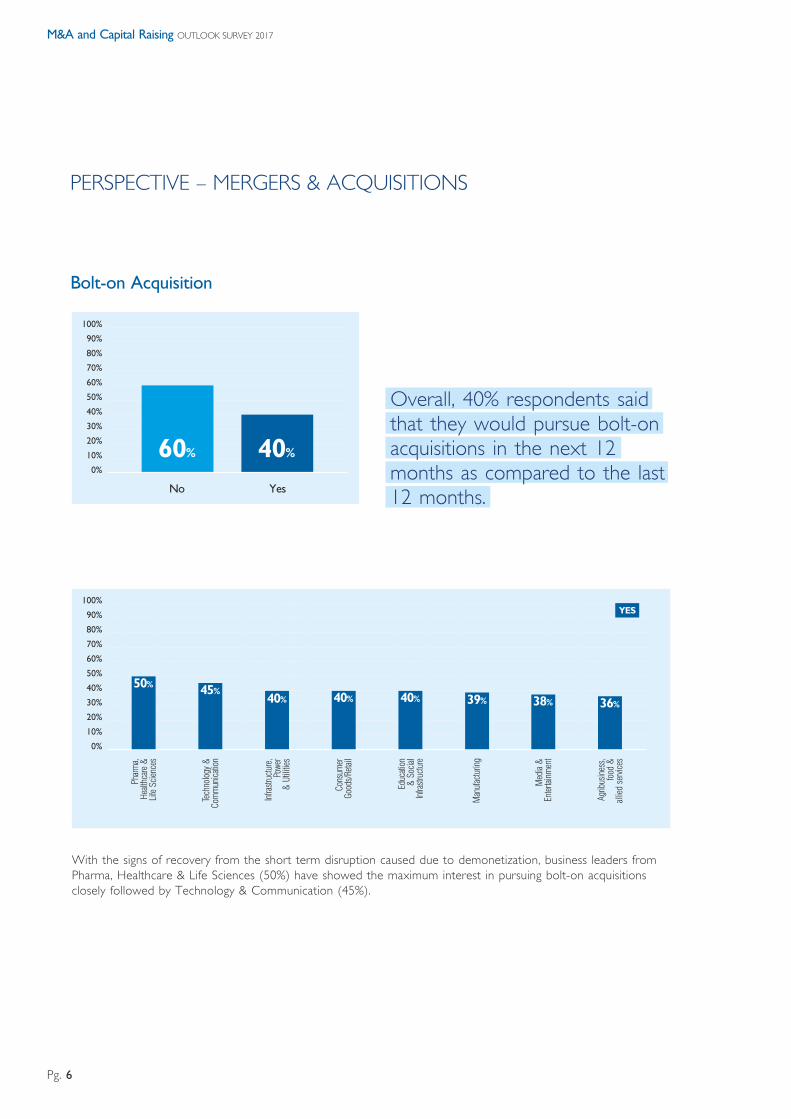

With the signs of recovery from the short term disruption caused due to demonetization, business leaders from Pharma, Healthcare & Life Sciences (50%) have showed the maximum interest in pursuing bolt-on acquisitions closely followed by Technology & Communication (45%).

Bolt-on Acquisition

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

40%60%

Yes No

M&A and Capital Raising OUTLOOK SURVEY 2017

PERSPECTIVE – MERGERS & ACQUISITIONS

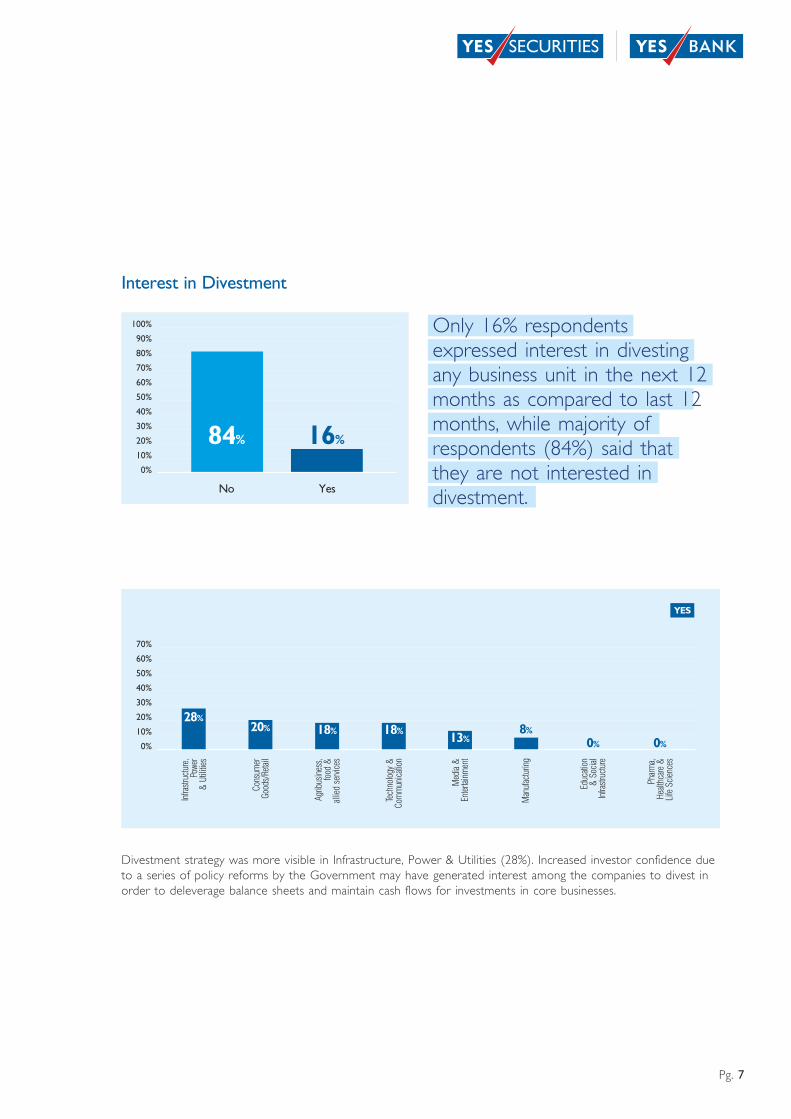

Divestment strategy was more visible in Infrastructure, Power & Utilities (28%). Increased investor confidence due to a series of policy reforms by the Government may have generated interest among the companies to divest in order to deleverage balance sheets and maintain cash flows for investments in core businesses.

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

16%84%

Yes No

Interest in Divestment

Pg. 7Pg. 6

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

36%40%

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

40% 38%

Med

ia &

En

terta

inm

ent

Con

sum

er

Goo

ds/R

etai

l

40%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

50%45%

Tech

nolo

gy &

C

omm

unic

atio

n

Man

ufac

turin

g

39%

YES

0%

20%

30%

40%

50%

60%

70%

10%

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

18%

0%

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

28%

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

Man

ufac

turin

g

8%13%

Med

ia &

En

terta

inm

ent

18%

Tech

nolo

gy &

C

omm

unic

atio

n

Con

sum

er

Goo

ds/R

etai

l

20%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

0%

YES

Overall, 40% respondents said that they would pursue bolt-on acquisitions in the next 12 months as compared to the last 12 months.

Only 16% respondents expressed interest in divesting any business unit in the next 12 months as compared to last 12 months, while majority of respondents (84%) said that they are not interested in divestment.

With the signs of recovery from the short term disruption caused due to demonetization, business leaders from Pharma, Healthcare & Life Sciences (50%) have showed the maximum interest in pursuing bolt-on acquisitions closely followed by Technology & Communication (45%).

Bolt-on Acquisition

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

40%60%

Yes No

M&A and Capital Raising OUTLOOK SURVEY 2017

PERSPECTIVE – MERGERS & ACQUISITIONS

Divestment strategy was more visible in Infrastructure, Power & Utilities (28%). Increased investor confidence due to a series of policy reforms by the Government may have generated interest among the companies to divest in order to deleverage balance sheets and maintain cash flows for investments in core businesses.

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

16%84%

Yes No

Interest in Divestment

Pg. 7Pg. 6

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

36%40%

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

40% 38%

Med

ia &

En

terta

inm

ent

Con

sum

er

Goo

ds/R

etai

l

40%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

50%45%

Tech

nolo

gy &

C

omm

unic

atio

n

Man

ufac

turin

g

39%

YES

0%

20%

30%

40%

50%

60%

70%

10%

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

18%

0%

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

28%

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

Man

ufac

turin

g

8%13%

Med

ia &

En

terta

inm

ent

18%

Tech

nolo

gy &

C

omm

unic

atio

n

Con

sum

er

Goo

ds/R

etai

l

20%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

0%

YES

Overall, 40% respondents said that they would pursue bolt-on acquisitions in the next 12 months as compared to the last 12 months.

Only 16% respondents expressed interest in divesting any business unit in the next 12 months as compared to last 12 months, while majority of respondents (84%) said that they are not interested in divestment.

With market trends of expansion of healthcare services in tier 2 and 3 cities and domestic consolidation in branded generics, the respondents from the Pharma, Healthcare & Life Sciences sector (63%) expressed the maximum interest in closing atleast one M&A transaction.

Single or Multiple Acquisitions?

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

47%52%

1 to 40 more than 4

1%

Pg. 8 Pg. 9

PERSPECTIVE – MERGERS & ACQUISITIONS

M&A and Capital Raising OUTLOOK SURVEY 2017

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

23%77%

Yes No

Foreign Acquisition

Build or Buy?

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

Less than10%

66%

10%-30% 30%-60% Over 60%

26% 3% 5%

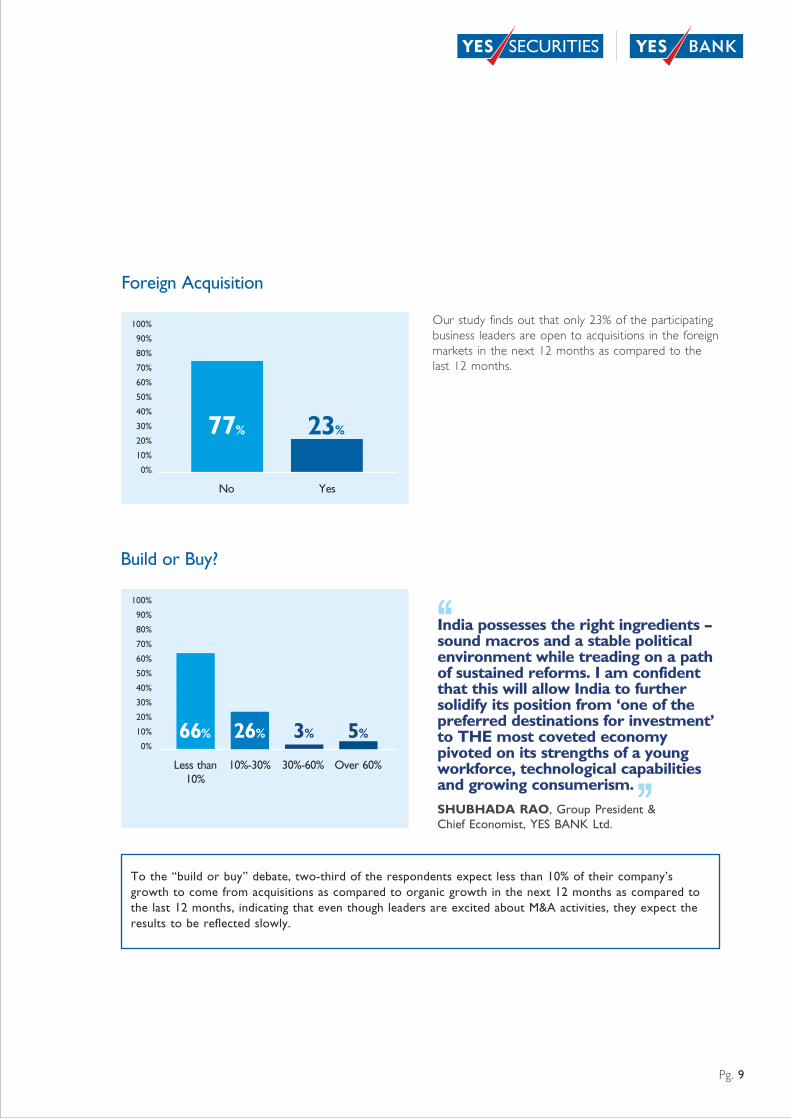

Our study finds out that only 23% of the participating business leaders are open to acquisitions in the foreign markets in the next 12 months as compared to the last 12 months.

India possesses the right ingredients – sound macros and a stable political environment while treading on a path of sustained reforms. I am confident that this will allow India to further solidify its position from ‘one of the preferred destinations for investment’ to THE most coveted economy pivoted on its strengths of a young workforce, technological capabilities and growing consumerism.

SHUBHADA RAO, Group President & Chief Economist, YES BANK Ltd.

To the “build or buy” debate, two-third of the respondents expect less than 10% of their company’s growth to come from acquisitions as compared to organic growth in the next 12 months as compared to the last 12 months, indicating that even though leaders are excited about M&A activities, they expect the results to be reflected slowly.

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

40%

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

27%

53%

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

Man

ufac

turin

g

44%

Med

ia &

En

terta

inm

ent

50%

63%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

45%

Tech

nolo

gy &

C

omm

unic

atio

n

Con

sum

er

Goo

ds/R

etai

l

60%

YES

The respondents are almost equally divided on whether they plan to close any M&A transactions in the ensuing 12 months, with 47% of the respondents stating that they plan to close 1-4 transactions

With market trends of expansion of healthcare services in tier 2 and 3 cities and domestic consolidation in branded generics, the respondents from the Pharma, Healthcare & Life Sciences sector (63%) expressed the maximum interest in closing atleast one M&A transaction.

Single or Multiple Acquisitions?

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

47%52%

1 to 40 more than 4

1%

Pg. 8 Pg. 9

PERSPECTIVE – MERGERS & ACQUISITIONS

M&A and Capital Raising OUTLOOK SURVEY 2017

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

23%77%

Yes No

Foreign Acquisition

Build or Buy?

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

Less than10%

66%

10%-30% 30%-60% Over 60%

26% 3% 5%

Our study finds out that only 23% of the participating business leaders are open to acquisitions in the foreign markets in the next 12 months as compared to the last 12 months.

India possesses the right ingredients – sound macros and a stable political environment while treading on a path of sustained reforms. I am confident that this will allow India to further solidify its position from ‘one of the preferred destinations for investment’ to THE most coveted economy pivoted on its strengths of a young workforce, technological capabilities and growing consumerism.

SHUBHADA RAO, Group President & Chief Economist, YES BANK Ltd.

To the “build or buy” debate, two-third of the respondents expect less than 10% of their company’s growth to come from acquisitions as compared to organic growth in the next 12 months as compared to the last 12 months, indicating that even though leaders are excited about M&A activities, they expect the results to be reflected slowly.

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

40%

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

27%

53%

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

Man

ufac

turin

g

44%

Med

ia &

En

terta

inm

ent

50%

63%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

45%

Tech

nolo

gy &

C

omm

unic

atio

n

Con

sum

er

Goo

ds/R

etai

l

60%

YES

The respondents are almost equally divided on whether they plan to close any M&A transactions in the ensuing 12 months, with 47% of the respondents stating that they plan to close 1-4 transactions

Drivers for Acquisition - Rising Customer Demand & Improving Economic Growth

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

42%58%

Yes No

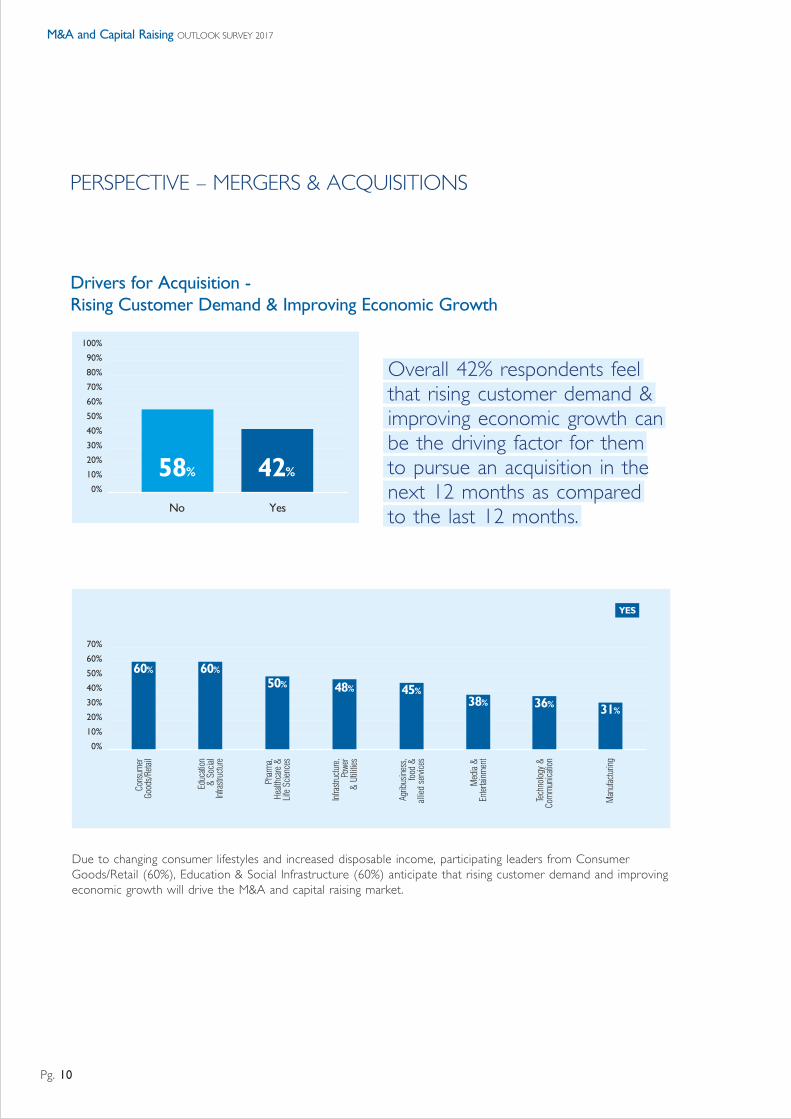

Overall 42% respondents feel that rising customer demand & improving economic growth can be the driving factor for them to pursue an acquisition in the next 12 months as compared to the last 12 months.

PERSPECTIVE – MERGERS & ACQUISITIONS

M&A and Capital Raising OUTLOOK SURVEY 2017

Due to changing consumer lifestyles and increased disposable income, participating leaders from Consumer Goods/Retail (60%), Education & Social Infrastructure (60%) anticipate that rising customer demand and improving economic growth will drive the M&A and capital raising market.

Market Sentiments

Increase

Decrease

Stable

0% 100%20% 40% 60% 80%

16%

52%

31%

Increase

Decrease

Stable

0% 100%20% 40% 60% 80%

14%

54%

32%

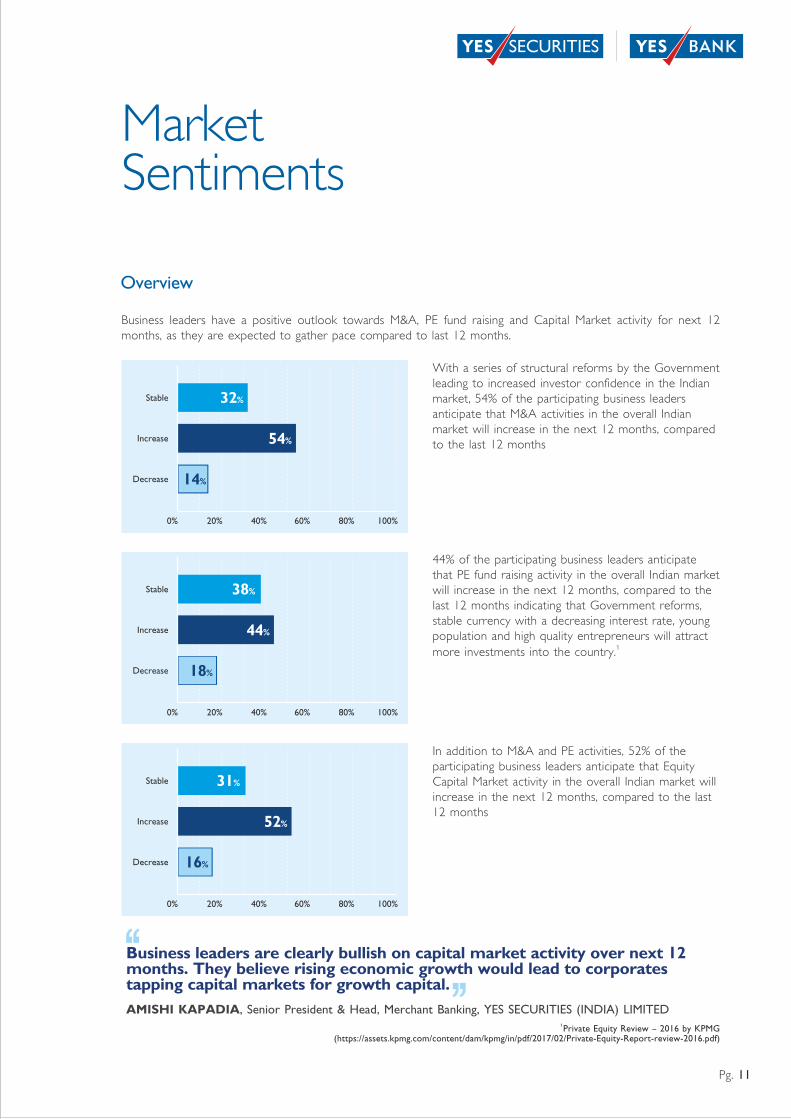

With a series of structural reforms by the Government leading to increased investor confidence in the Indian market, 54% of the participating business leaders anticipate that M&A activities in the overall Indian market will increase in the next 12 months, compared to the last 12 months

Increase

Decrease

Stable

0% 100%20% 40% 60% 80%

18%

44%

38%

44% of the participating business leaders anticipate that PE fund raising activity in the overall Indian market will increase in the next 12 months, compared to the last 12 months indicating that Government reforms, stable currency with a decreasing interest rate, young population and high quality entrepreneurs will attract

1more investments into the country.

In addition to M&A and PE activities, 52% of the participating business leaders anticipate that Equity Capital Market activity in the overall Indian market will increase in the next 12 months, compared to the last 12 months

1Private Equity Review – 2016 by KPMG (https://assets.kpmg.com/content/dam/kpmg/in/pdf/2017/02/Private-Equity-Report-review-2016.pdf)

Overview

Business leaders have a positive outlook towards M&A, PE fund raising and Capital Market activity for next 12 months, as they are expected to gather pace compared to last 12 months.

Business leaders are clearly bullish on capital market activity over next 12 months. They believe rising economic growth would lead to corporates tapping capital markets for growth capital.

AMISHI KAPADIA, Senior President & Head, Merchant Banking, YES SECURITIES (INDIA) LIMITED

Pg. 11Pg. 10

0%

20%

30%

40%

50%

60%

70%

10%

48%

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

38%

Med

ia &

En

terta

inm

ent

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

45%

Con

sum

er

Goo

ds/R

etai

l

60%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

50%

Man

ufac

turin

g

31%

Tech

nolo

gy &

C

omm

unic

atio

n

36%

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

60%

YES

Drivers for Acquisition - Rising Customer Demand & Improving Economic Growth

0%

100%

20%

30%

40%

50%

60%

70%

80%

10%

90%

42%58%

Yes No

Overall 42% respondents feel that rising customer demand & improving economic growth can be the driving factor for them to pursue an acquisition in the next 12 months as compared to the last 12 months.

PERSPECTIVE – MERGERS & ACQUISITIONS

M&A and Capital Raising OUTLOOK SURVEY 2017

Due to changing consumer lifestyles and increased disposable income, participating leaders from Consumer Goods/Retail (60%), Education & Social Infrastructure (60%) anticipate that rising customer demand and improving economic growth will drive the M&A and capital raising market.

Market Sentiments

Increase

Decrease

Stable

0% 100%20% 40% 60% 80%

16%

52%

31%

Increase

Decrease

Stable

0% 100%20% 40% 60% 80%

14%

54%

32%

With a series of structural reforms by the Government leading to increased investor confidence in the Indian market, 54% of the participating business leaders anticipate that M&A activities in the overall Indian market will increase in the next 12 months, compared to the last 12 months

Increase

Decrease

Stable

0% 100%20% 40% 60% 80%

18%

44%

38%

44% of the participating business leaders anticipate that PE fund raising activity in the overall Indian market will increase in the next 12 months, compared to the last 12 months indicating that Government reforms, stable currency with a decreasing interest rate, young population and high quality entrepreneurs will attract

1more investments into the country.

In addition to M&A and PE activities, 52% of the participating business leaders anticipate that Equity Capital Market activity in the overall Indian market will increase in the next 12 months, compared to the last 12 months

1Private Equity Review – 2016 by KPMG (https://assets.kpmg.com/content/dam/kpmg/in/pdf/2017/02/Private-Equity-Report-review-2016.pdf)

Overview

Business leaders have a positive outlook towards M&A, PE fund raising and Capital Market activity for next 12 months, as they are expected to gather pace compared to last 12 months.

Business leaders are clearly bullish on capital market activity over next 12 months. They believe rising economic growth would lead to corporates tapping capital markets for growth capital.

AMISHI KAPADIA, Senior President & Head, Merchant Banking, YES SECURITIES (INDIA) LIMITED

Pg. 11Pg. 10

0%

20%

30%

40%

50%

60%

70%

10%

48%

Infra

stru

ctur

e,

Pow

er

& U

tiliti

es

38%

Med

ia &

En

terta

inm

ent

Agrib

usin

ess,

fo

od &

al

lied

serv

ices

45%

Con

sum

er

Goo

ds/R

etai

l

60%

Phar

ma,

H

ealth

care

&

Life

Sci

ence

s

50%

Man

ufac

turin

g

31%

Tech

nolo

gy &

C

omm

unic

atio

n

36%

Educ

atio

n &

Soc

ial

Infra

stru

ctur

e

60%

YES

M&A and Capital Raising OUTLOOK SURVEY 2017

About the Survey

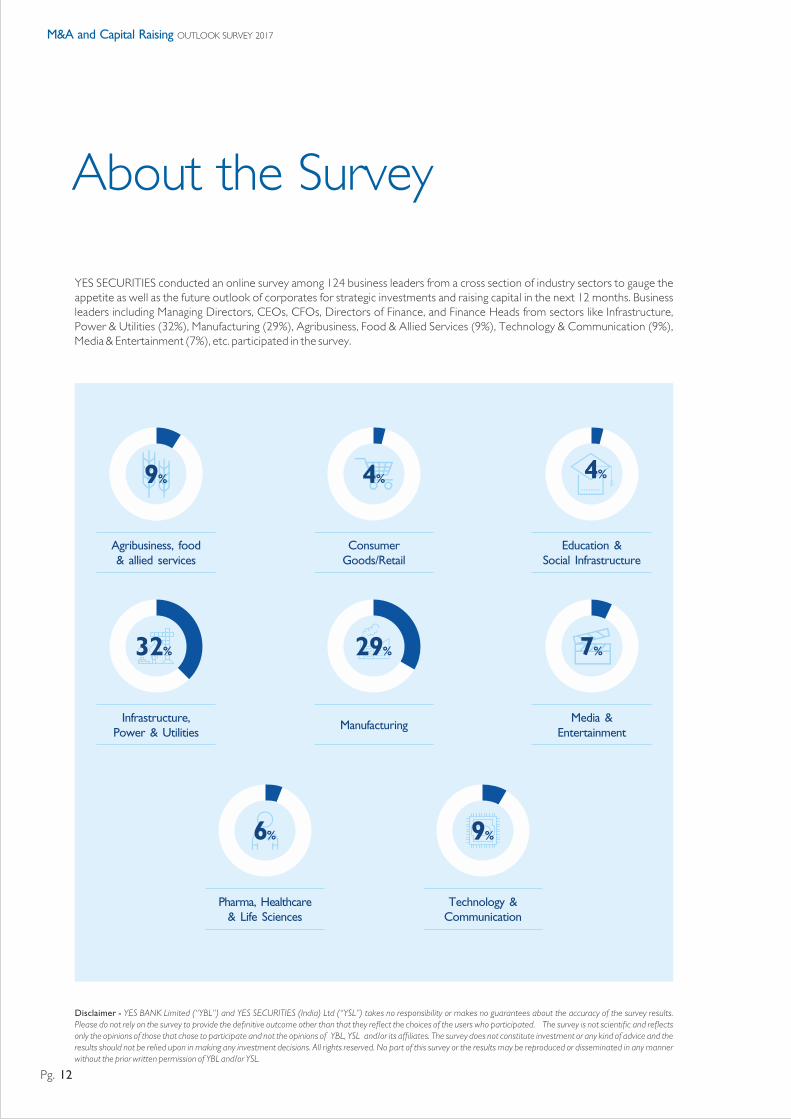

YES SECURITIES conducted an online survey among 124 business leaders from a cross section of industry sectors to gauge the appetite as well as the future outlook of corporates for strategic investments and raising capital in the next 12 months. Business leaders including Managing Directors, CEOs, CFOs, Directors of Finance, and Finance Heads from sectors like Infrastructure, Power & Utilities (32%), Manufacturing (29%), Agribusiness, Food & Allied Services (9%), Technology & Communication (9%), Media & Entertainment (7%), etc. participated in the survey.

Pg. 12

YES SECURITIES, a wholly-owned subsidiary of YES BANK, India’s fifth largest private sector bank, is one of the leading financial advisors in India. It offers a gamut of services including investment banking, merchant banking, institutional sales and trading and equity research. The firm has a robust track record of over 250+ successful deal closures in investment banking and capital markets transactions and is consistently recognized by leading domestic and global league tables. YES SECURITIES is a registered category one merchant banker with SEBI and a member of NSE and BSE.

YES SECURITIES executed 24 marquee transactions during Jan - Dec, 2016, covering M&A, Private Equity placement and Capital Markets transactions for its clients across sectors.

About YES SECURITIES

Agribusiness, food & allied services

9%

Consumer Goods/Retail

4%

Education & Social Infrastructure

4%

Infrastructure, Power & Utilities

32%

Manufacturing

29%

Media & Entertainment

7%

Pharma, Healthcare & Life Sciences

6%

Technology & Communication

9%

Disclaimer - YES BANK Limited (“YBL”) and YES SECURITIES (India) Ltd (“YSL”) takes no responsibility or makes no guarantees about the accuracy of the survey results. Please do not rely on the survey to provide the definitive outcome other than that they reflect the choices of the users who participated. The survey is not scientific and reflects only the opinions of those that chose to participate and not the opinions of YBL, YSL and/or its affiliates. The survey does not constitute investment or any kind of advice and the results should not be relied upon in making any investment decisions. All rights reserved. No part of this survey or the results may be reproduced or disseminated in any manner without the prior written permission of YBL and/or YSL.

M&A and Capital Raising OUTLOOK SURVEY 2017

About the Survey

YES SECURITIES conducted an online survey among 124 business leaders from a cross section of industry sectors to gauge the appetite as well as the future outlook of corporates for strategic investments and raising capital in the next 12 months. Business leaders including Managing Directors, CEOs, CFOs, Directors of Finance, and Finance Heads from sectors like Infrastructure, Power & Utilities (32%), Manufacturing (29%), Agribusiness, Food & Allied Services (9%), Technology & Communication (9%), Media & Entertainment (7%), etc. participated in the survey.

Pg. 12

YES SECURITIES, a wholly-owned subsidiary of YES BANK, India’s fifth largest private sector bank, is one of the leading financial advisors in India. It offers a gamut of services including investment banking, merchant banking, institutional sales and trading and equity research. The firm has a robust track record of over 250+ successful deal closures in investment banking and capital markets transactions and is consistently recognized by leading domestic and global league tables. YES SECURITIES is a registered category one merchant banker with SEBI and a member of NSE and BSE.

YES SECURITIES executed 24 marquee transactions during Jan - Dec, 2016, covering M&A, Private Equity placement and Capital Markets transactions for its clients across sectors.

About YES SECURITIES

Agribusiness, food & allied services

9%

Consumer Goods/Retail

4%

Education & Social Infrastructure

4%

Infrastructure, Power & Utilities

32%

Manufacturing

29%

Media & Entertainment

7%

Pharma, Healthcare & Life Sciences

6%

Technology & Communication

9%

Disclaimer - YES BANK Limited (“YBL”) and YES SECURITIES (India) Ltd (“YSL”) takes no responsibility or makes no guarantees about the accuracy of the survey results. Please do not rely on the survey to provide the definitive outcome other than that they reflect the choices of the users who participated. The survey is not scientific and reflects only the opinions of those that chose to participate and not the opinions of YBL, YSL and/or its affiliates. The survey does not constitute investment or any kind of advice and the results should not be relied upon in making any investment decisions. All rights reserved. No part of this survey or the results may be reproduced or disseminated in any manner without the prior written permission of YBL and/or YSL.

VIKAS DAWRA

Senior President & Head, Investment Banking, YES SECURITIES (INDIA) LIMITED

AMISHI KAPADIA

Senior President & Head, Merchant Banking, YES SECURITIES (INDIA) LIMITED

The Team

YES SECURITIES (INDIA) LIMITEDRegistered Office: IFC, Tower I, 6th Floor, Elphinstone Road, Senapati Bapat Marg, Mumbai - 400 013

![Olcott...Multiple Sclerosis Mumps Osteoporosis Pacemaker Yes Cl Yes [2 Yes Yes Yes [2 Yes Parkinson's Disease [2 Yes ... Yes [2 Yes D Yes Yes C] Yes Yes Rheumatoid Arthritis Yes HABITS](https://img.pdfslide.net/doc/110x75/5f437d8dde860906673fc43a/olcott-multiple-sclerosis-mumps-osteoporosis-pacemaker-yes-cl-yes-2-yes-yes.jpg)