Embed Size (px)

Citation preview

Osborne Books Tutor Zone

ManagementAccounting:CostingChapter activities

© Osborne Books Limited, 2016

2 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

1.1 The following table shows explanations of some terms used in costing. Select the correct term fromthe list to match each explanation.

Explanation TermA cost which remains unchanged over a rangeof output levelsA cost that cannot be identified with each unitof output A unit of output to which costs can be chargedA cost which is neither a material cost nor alabour costA cost which varies directly with outputThe total of all direct costs

Select term from:• Semi-variable cost • Prime cost• Fixed cost • Cost unit• Direct cost • Indirect cost• Cost centre • Expense• Variable cost

1.2 Analyse the following examples of costs for a manufacturing business into those that behave asfixed costs and those that behave as variable costs, by ticking the appropriate column.

Examples of costs Fixed cost Variable cost(a) Materials used in production (b) Business rates of factory premises (c) Salary of Production Manager (d) Royalties paid for each unit produced (e) Packaging costs (f) Factory building insurance (g) Direct labour paid by piece-work

An introduction to cost accounting1

c h a p t e r a c t i v i t i e s 3

1.3 From the following list of statements, select those that are true.

True(a) Cost centres, profit centres and investment centres are all examples of

responsibility centres

(b) A cost centre is a section of a business to which costs can be charged, revenuecan be identified and profit can be calculated

(c) Costs can be classified by element, nature, function and behaviour

(d) Classification of costs by nature involves analysing the costs into direct costsand indirect costs

(e) Classification of costs by function means dividing them into materials, labour andexpenses

(f) The total cost of a unit of output can be calculated by dividing the total of the directand indirect costs for a period by the number of units of output for that period

(g) Indirect costs are also known as overheads

(h) Direct costs always behave as fixed costs

1.4 Analyse the costs shown in the following table into their cost behaviour by ticking the appropriatecolumn.

Fixed Variable Semi-variable(a) Raw materials (b) Employees paid a flat rate plus a production based

bonus (c) Factory rates (d) Repairs to factory building(e) Royalties paid per unit produced(f) Packing materials(g) Supervisor’s salary

1.5 You work for a company that manufactures a range of office furniture. The following list of costs hasbeen compiled from the company records. You have been asked to classify these costs into a tableto illustrate to a new trainee how the company costing system works.List of costs:(a) Factory rent(b) Wages of employee who assembles desks(c) Steel used to make desk legs(d) Costs of advertising(e) Wages of factory maintenance employee(f) Royalties paid to designer of office chair(g) Bank loan interest(h) Repair to photocopier in Administration Department(i) Wages of warehouse employee(j) Machinery oil for use in the factory(k) Wages of employee in Administration Department(l) Stationery used in administration(m) Fuel for fork lift truck in warehouseComplete the table below by inserting all the costs on the above list in the appropriate place.

Production (‘factory’) costs Non-production (‘warehouse & office’) costs Direct costs Indirect costs Administration Selling and Finance (overheads) indirect costs distribution indirect costs (overheads) indirect costs (overheads) (overheads)

Materials

Labour

Expenses

4 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

1.6 Which of these is an example of unethical behaviour by an accounting technician? Tick one option.

(a) All the variances in the management accounts have been correctly calculatedand explained

(b) Direct materials have been classified correctly in the management accounts(c) The inventory valuation has been changed from AVCO to FIFO to make the profit

look better (d) All confidential payroll information is kept in a locked cupboard

1.7 (a) You work as an Accounts Assistant for Traditional Cabinets Limited, a company thatproduces kitchen and bathroom cabinets. Your Finance Director has asked you to reviewthe performance of each of the departments for the year ended 31 March 20-5 and you haveextracted the following information:

Kitchen Department Bathroom Department £000 £000Cost : Materials 95 55

Labour 87 60Overheads 25 15

Income 505 200Money invested 405 45

The Finance Director asks you to produce a report which shows the costs, profit, and returnon investment (to the nearest percentage point) for each department and comment onwhich department is performing better for each.

(b) Traditional Cabinets Limited is going to appoint two Departmental Managers, to assist theManaging Director in running the business.

Which of the following should they be given responsibility for if the Managing Director wantsto maximise profits?

Tick all that apply.

(a) The department’s variable costs(b) The departments fixed costs(c) The department’s revenue, fixed and variable costs(d) The department’s costs, revenue, assets and liabilities

c h a p t e r a c t i v i t i e s 5

6 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

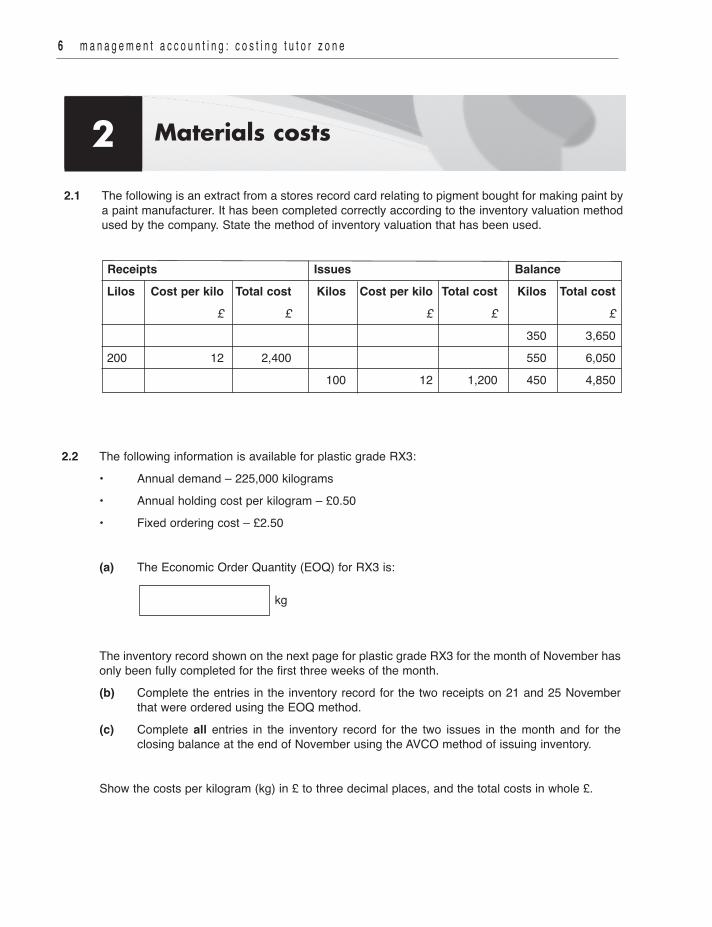

2.1 The following is an extract from a stores record card relating to pigment bought for making paint bya paint manufacturer. It has been completed correctly according to the inventory valuation methodused by the company. State the method of inventory valuation that has been used.

Receipts Issues BalanceLilos Cost per kilo Total cost Kilos Cost per kilo Total cost Kilos Total cost £ £ £ £ £ 350 3,650200 12 2,400 550 6,050 100 12 1,200 450 4,850

2.2 The following information is available for plastic grade RX3:• Annual demand – 225,000 kilograms• Annual holding cost per kilogram – £0.50• Fixed ordering cost – £2.50

(a) The Economic Order Quantity (EOQ) for RX3 is:

kg

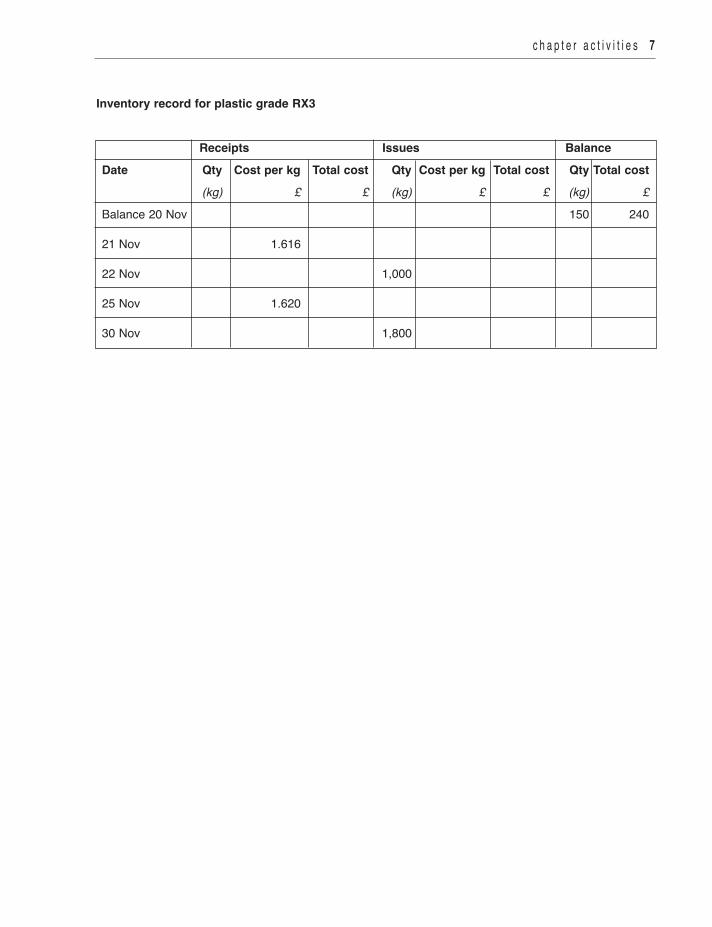

The inventory record shown on the next page for plastic grade RX3 for the month of November hasonly been fully completed for the first three weeks of the month.(b) Complete the entries in the inventory record for the two receipts on 21 and 25 November

that were ordered using the EOQ method.(c) Complete all entries in the inventory record for the two issues in the month and for the

closing balance at the end of November using the AVCO method of issuing inventory.

Show the costs per kilogram (kg) in £ to three decimal places, and the total costs in whole £.

Materials costs2

c h a p t e r a c t i v i t i e s 7

Inventory record for plastic grade RX3

Receipts Issues BalanceDate Qty Cost per kg Total cost Qty Cost per kg Total cost Qty Total cost (kg) £ £ (kg) £ £ (kg) £Balance 20 Nov 150 240

21 Nov 1.616

22 Nov 1,000

25 Nov 1.620

30 Nov 1,800

2.3 Complete the following inventory record for material KZ90. The company policy is to use the firstin first out (FIFO) method of inventory valuation. (Cost per kilogram entries should be completed in£ to three decimal places.)

Receipts Issues BalanceDate Qty Cost per kg Total cost Qty Cost per kg Total cost Qty Total cost (kg) £ £ (kg) £ £ (kg) £

Balance 1 Sept 480 2,400

2 Sept 500 5.120

4 Sept 1,500 5.100

5 Sept 400

7 Sept 1,000

2.4 A company orders a specific material that has a lead time of 10 days. The daily usage of thematerial is 50 kg. The company wishes to keep at least 150 kg in stock at all times. The companypolicy is to order 2,000 kg at a time. Complete the following table.

kg

Re-order level

Maximum inventory level

Average inventory level

8 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

c h a p t e r a c t i v i t i e s 9

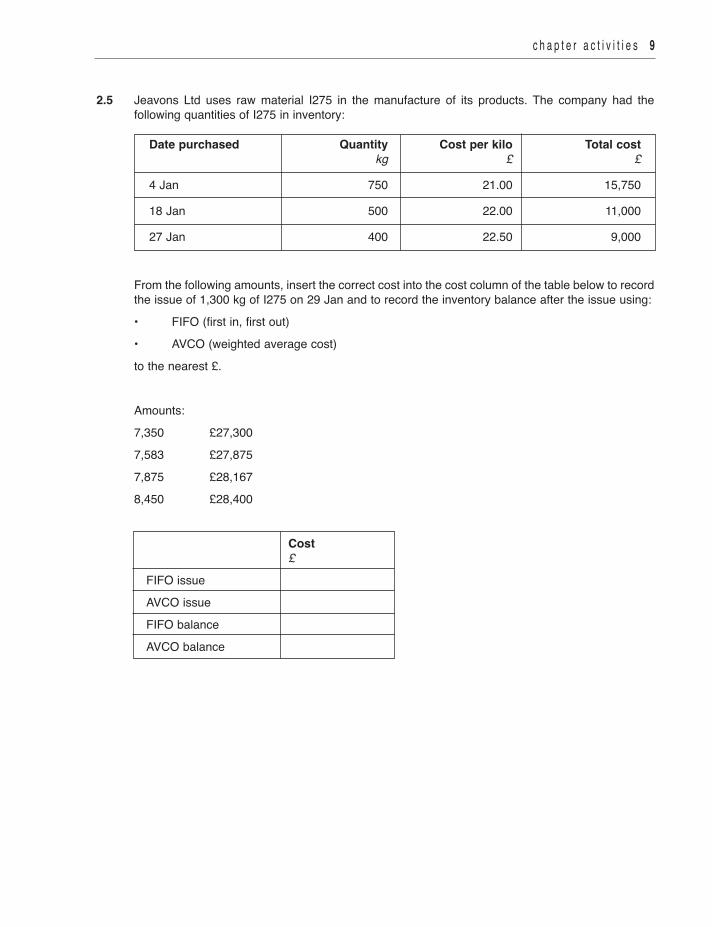

2.5 Jeavons Ltd uses raw material I275 in the manufacture of its products. The company had thefollowing quantities of I275 in inventory:

Date purchased Quantity Cost per kilo Total cost kg £ £

4 Jan 750 21.00 15,750

18 Jan 500 22.00 11,000

27 Jan 400 22.50 9,000

From the following amounts, insert the correct cost into the cost column of the table below to recordthe issue of 1,300 kg of I275 on 29 Jan and to record the inventory balance after the issue using:• FIFO (first in, first out)• AVCO (weighted average cost)to the nearest £.

Amounts:7,350 £27,3007,583 £27,8757,875 £28,1678,450 £28,400

Cost £FIFO issueAVCO issueFIFO balanceAVCO balance

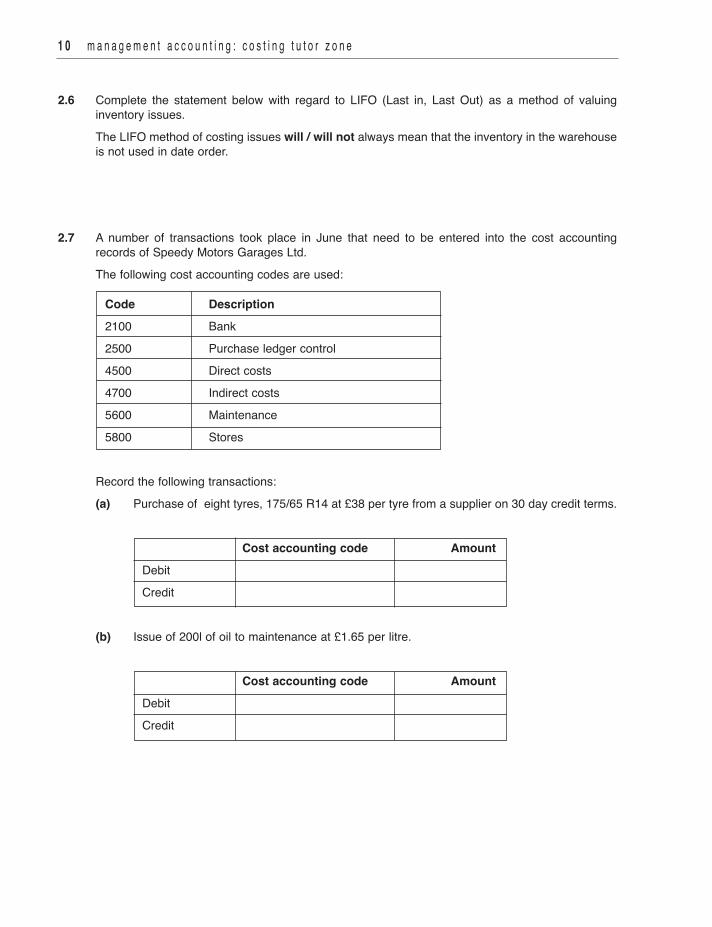

2.6 Complete the statement below with regard to LIFO (Last in, Last Out) as a method of valuinginventory issues.The LIFO method of costing issues will / will not always mean that the inventory in the warehouseis not used in date order.

2.7 A number of transactions took place in June that need to be entered into the cost accountingrecords of Speedy Motors Garages Ltd.The following cost accounting codes are used:

Code Description2100 Bank2500 Purchase ledger control4500 Direct costs4700 Indirect costs5600 Maintenance5800 Stores

Record the following transactions:(a) Purchase of eight tyres, 175/65 R14 at £38 per tyre from a supplier on 30 day credit terms.

Cost accounting code AmountDebit Credit

(b) Issue of 200l of oil to maintenance at £1.65 per litre.

Cost accounting code AmountDebit Credit

1 0 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

c h a p t e r a c t i v i t i e s 1 1

3.1 A company employs 10 direct labour staff making production units, each working a 40 hour week.Employees are paid £10.00 per hour basic pay, with a £5.00 per hour premium for overtime hoursworked. During the four weeks ending 28 November, the staff worked:• 1,600 normal hours, and• 300 overtime hours, and made• 800 units.

Calculate the cost of direct labour for the four weeks, assuming(a) that the overtime premium is charged to direct labour,

(b) that the overtime premium is charged to operating overheads.

(c) Assuming that the overtime premium is charged to operating overheads, complete thefollowing journal entry for the four weeks to 28 November.

Debit £ Credit £Work in progress Operating overheads Wages control

(d) Assuming that the overtime premium is charged to operating overheads, calculate the directlabour cost per unit of production for the period (to three decimal places).

£

£

Labour costs3

£

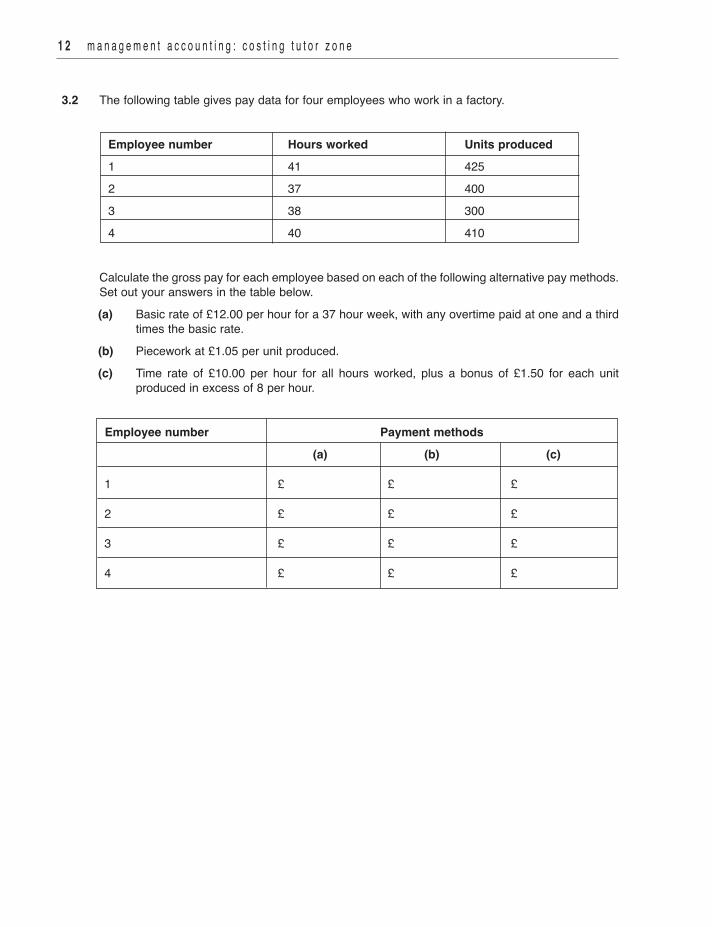

3.2 The following table gives pay data for four employees who work in a factory.

Employee number Hours worked Units produced1 41 4252 37 4003 38 3004 40 410

Calculate the gross pay for each employee based on each of the following alternative pay methods.Set out your answers in the table below.(a) Basic rate of £12.00 per hour for a 37 hour week, with any overtime paid at one and a third

times the basic rate.(b) Piecework at £1.05 per unit produced.(c) Time rate of £10.00 per hour for all hours worked, plus a bonus of £1.50 for each unit

produced in excess of 8 per hour.

Employee number Payment methods (a) (b) (c)

1 £ £ £

2 £ £ £

3 £ £ £

4 £ £ £

1 2 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

c h a p t e r a c t i v i t i e s 1 3

3.3 Below is a weekly timesheet for one of Butterworth Ltd’s employees, who is paid as follows:• For a basic seven-hour shift every day from Monday to Friday – basic pay.• For any overtime in excess of the basic seven hours, on any day from Monday to Friday –

the extra hours are paid at time-and-a-half (basic pay plus an overtime premium equal tohalf of basic pay).

• For two contracted hours each Saturday morning – basic pay. • For any hours in excess of two hours on Saturday – the extra hours are paid at double time

(basic pay plus an overtime premium equal to basic pay). • For any hours worked on Sunday – paid at double time (basic pay plus an overtime premium

equal to basic pay).

Complete the columns headed Basic rate, Overtime premium and Total pay.

Employee: P. Boyd Profit Centre: Plastic extrusionEmployee number: K089 Basic pay per hour: £15.00 Hours spent Hours worked Notes Basic rate Overtime Total pay on production on indirect work £ premium £ £Monday 7 Tuesday 3 4 9am – 1pm setting up equipmentWednesday 8

Thursday 6 2 10 – 12am cleaning of machinery Friday 6 1 3 – 4pm weekly meeting Saturday 4

Sunday 2

Total 36 7

1 4 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

3.4 Newham Limited, a manufacturing business, has a Production Department where the employeeswork in teams. Their basic rate is £15.00 per hour and there are two rates of overtime as follows:• Overtime rate 1: basic pay + 25%• Overtime rate 2: basic pay + 50%Newham Limited sets a target for production of every component each month. A team bonus equalto 15% of basic hourly rate is payable for every equivalent unit of production in the month in excessof the target.The target for May was 10,000 units.In May the production was 11,000 equivalent units.All overtime and bonuses are included as part of the direct labour cost.

(a) Complete the gaps in the table below to calculate the total labour cost.

(b) Calculate the average labour rate per hour, including bonus, for the production employeesfor May. Give your answer in £s to two decimal places.

The average labour cost per hour for may is £

(c) There are five production employees employed in May.

Complete the following sentence by filling in the blanks.

The total pay per employee, including bonus, for May will be £and the bonus payable will be £ per employee.

Labour cost Hours £Basic pay 450Overtime rate 1 60Overtime rate 2 40Total cost before team bonus 550Bonus paymentTotal cost including team bonus

c h a p t e r a c t i v i t i e s 1 5

3.5 Speedy Motors Limited needs to record some wages into the cost accounting records in Week 47. The following cost accounting codes are used:

Code Description4100 Bank6500 Wages control8500 Direct costs9700 Indirect costs9800 Maintenance and repairs

Record the following transactions:(a) Three staff worked a 38 hour week at £10.30 per hour, all chargeable to specific jobs.

Cost accounting code AmountDebit Credit

(b) Two staff spent three hours repairing one of the machines that had broken and were paid £15.00 per hour.

Cost accounting code AmountDebit Credit

1 6 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

Overheads and expenses4

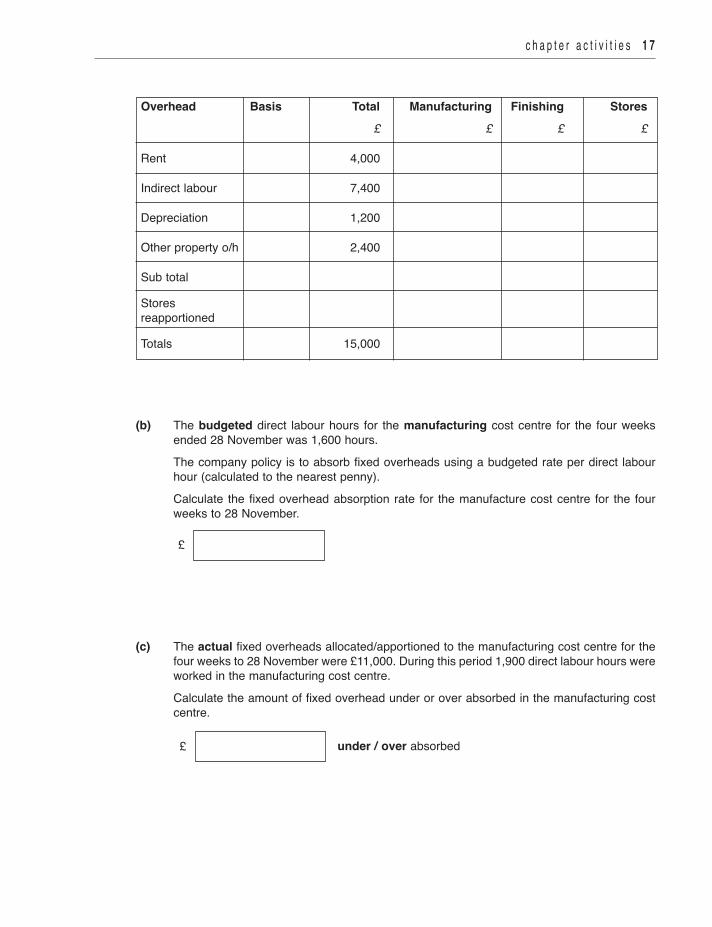

4.1 Zed Limited has three cost centres: Manufacturing, Finishing, and Stores.The budgeted fixed overheads for the four weeks ending 28 November were as follows:

£Rent 4,000Indirect Labour: Manufacturing 2,500 Finishing 1,500 Stores 3,400Depreciation of non-current assets 1,200Other property overheads 2,400 15,000

The following data is available: Floor space Carrying value non-current assetsManufacturing 800 sq mts £30,000Finishing 400 sq mts £10,000Stores 400 sq mts £20,000

Overheads are allocated and apportioned using the most appropriate method. The storesoverheads are then reapportioned on the basis of the cost centres that benefit from the StoresDepartment. Records show that 75% of the stores activity benefits the manufacturing cost centre,whilst the other 25% benefits the finishing cost centre.

(a) Complete the following table relating to the allocation and apportionment of the budgetedfixed overheads.

c h a p t e r a c t i v i t i e s 1 7

Overhead Basis Total Manufacturing Finishing Stores £ £ £ £

Rent 4,000

Indirect labour 7,400

Depreciation 1,200

Other property o/h 2,400

Sub total

Stores reapportioned

Totals 15,000

(b) The budgeted direct labour hours for the manufacturing cost centre for the four weeksended 28 November was 1,600 hours.The company policy is to absorb fixed overheads using a budgeted rate per direct labourhour (calculated to the nearest penny).Calculate the fixed overhead absorption rate for the manufacture cost centre for the fourweeks to 28 November.

(c) The actual fixed overheads allocated/apportioned to the manufacturing cost centre for thefour weeks to 28 November were £11,000. During this period 1,900 direct labour hours wereworked in the manufacturing cost centre.Calculate the amount of fixed overhead under or over absorbed in the manufacturing costcentre.

under / over absorbed

£

£

1 8 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

4.2 Select the best basis for apportioning the overheads shown in the following table by ticking theappropriate column.

Carrying Number of Area of Power No of quality value of plant employees cost centres consumption control of plant inspectionsStaff canteen costs Buildings insurance Power for plant Heating and lighting Staff uniform costs Maintenance of plant Rent and ratesQuality control costs

4.3 Buccaneer Ltd’s budgeted overheads for the next financial year are:

£ £Depreciation of plant and equipment 235,450Power for production machinery 401,200Rent and rates 98,500Light and heat 43,560Indirect labour costs: Maintenance 67,400 Stores 55,300 Administration 151,650 Total indirect labour cost 274,350Total budgeted overheads 1,053,060

The following information is also available:

c h a p t e r a c t i v i t i e s 1 9

Department Carrying value Production machinery Floor space Number of of plant and power usage employees equipment £ (KwH) (square metres)

Production centres: Assembly 981,000 1,900,000 40,000 15 Finishing 519,000 600,000 29,000 9 Support cost centres: Maintenance 16,000 5 Stores 9,600 3Administration 5,400 8 Total 1,500,000 2,500,000 100,000 40

Overheads are allocated or apportioned on the most appropriate basis. The total overheads of thesupport cost centres are then reapportioned to the two production centres using the direct method.• 85% of the maintenance cost centre’s time is spent maintaining production machinery in the

assembly production centre and the remainder in the finishing production centre.• The stores cost centre makes 65% of its issues to the assembly production centre, and 35%

to the finishing production centre.• General administration supports assembly 60% and finishing 40%.• There is no reciprocal servicing between the three support cost centres.

Complete the apportionment table on the next page. Show amounts rounded to the nearest £where appropriate.

2 0 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

Basis Assembly Finishing Maint’ce Stores Admin Totals £ £ £ £ £ £

Depreciation of plantand equipment

Power for productionmachinery

Rent and rates

Light and heat

Indirect labour

Totals

Reapportionmaintenance

Reapportion stores

Reapportion generaladmin

Total overheads toproduction centres

c h a p t e r a c t i v i t i e s 2 1

4.4 Which of the following statements shows the correct calculation of the overhead absorption ratewhen based on direct labour hours?

(a) Actual overhead costs divided by budgeted direct labour hours

(b) Budgeted direct labour hours divided by budgeted overhead costs

(c) Actual overhead costs divided by actual direct labour hours

(d) Actual direct labour hours divided by actual overhead costs

(e) Budgeted overhead costs divided by actual direct labour hours

(f) Actual direct labour hours divided by budgeted overhead costs

(g) Budgeted overhead costs divided by budgeted direct labour hours

2 2 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

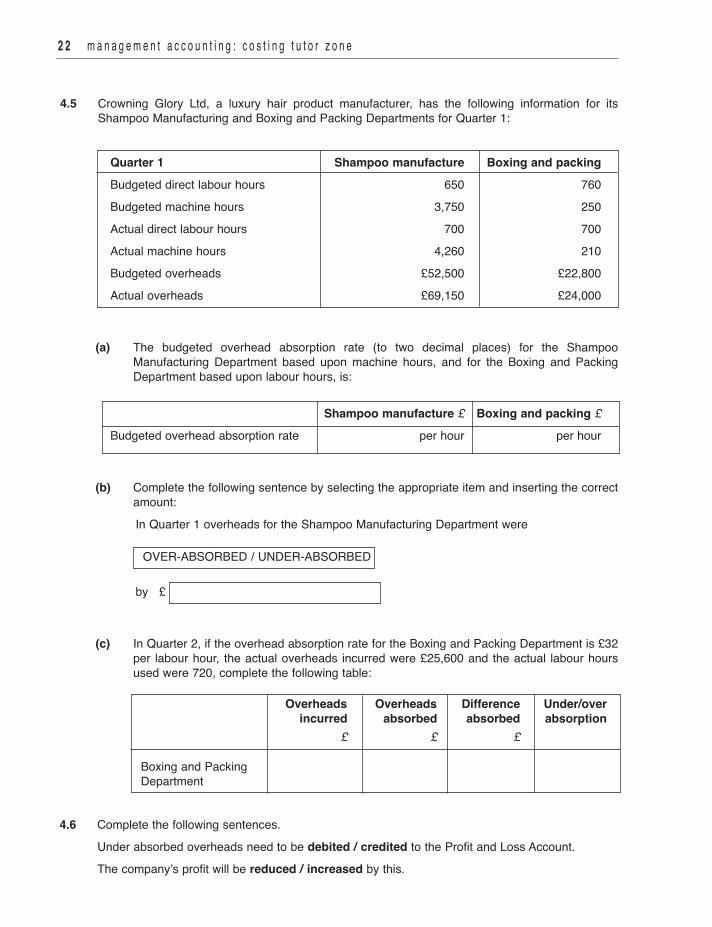

4.5 Crowning Glory Ltd, a luxury hair product manufacturer, has the following information for itsShampoo Manufacturing and Boxing and Packing Departments for Quarter 1:

Quarter 1 Shampoo manufacture Boxing and packingBudgeted direct labour hours 650 760Budgeted machine hours 3,750 250Actual direct labour hours 700 700Actual machine hours 4,260 210Budgeted overheads £52,500 £22,800Actual overheads £69,150 £24,000

(a) The budgeted overhead absorption rate (to two decimal places) for the ShampooManufacturing Department based upon machine hours, and for the Boxing and PackingDepartment based upon labour hours, is:

Shampoo manufacture £ Boxing and packing £Budgeted overhead absorption rate per hour per hour

(b) Complete the following sentence by selecting the appropriate item and inserting the correctamount:

In Quarter 1 overheads for the Shampoo Manufacturing Department were

OVER-ABSORBED / UNDER-ABSORBED

by £

(c) In Quarter 2, if the overhead absorption rate for the Boxing and Packing Department is £32per labour hour, the actual overheads incurred were £25,600 and the actual labour hoursused were 720, complete the following table:

Overheads Overheads Difference Under/over incurred absorbed absorbed absorption £ £ £

Boxing and PackingDepartment

4.6 Complete the following sentences.Under absorbed overheads need to be debited / credited to the Profit and Loss Account. The company’s profit will be reduced / increased by this.

c h a p t e r a c t i v i t i e s 2 3

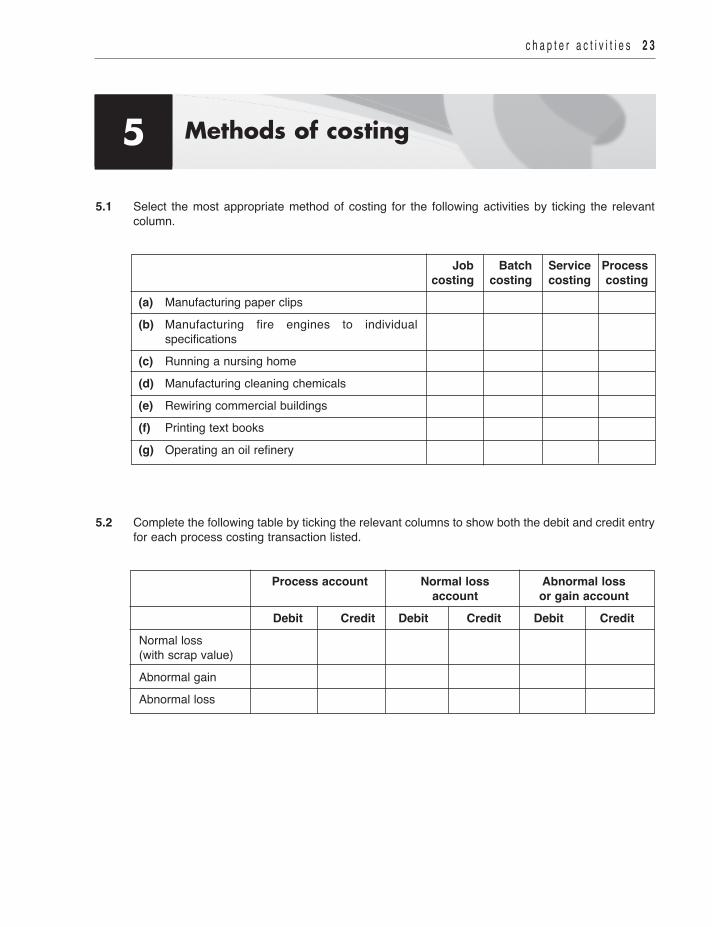

5.1 Select the most appropriate method of costing for the following activities by ticking the relevantcolumn.

Job Batch Service Process costing costing costing costing(a) Manufacturing paper clips(b) Manufacturing fire engines to individual

specifications(c) Running a nursing home(d) Manufacturing cleaning chemicals(e) Rewiring commercial buildings(f) Printing text books(g) Operating an oil refinery

5.2 Complete the following table by ticking the relevant columns to show both the debit and credit entryfor each process costing transaction listed.

Process account Normal loss Abnormal loss account or gain account Debit Credit Debit Credit Debit CreditNormal loss (with scrap value) Abnormal gain Abnormal loss

Methods of costing5

5.3 A company operates a process in which the normal loss is 10% of the input. This normal loss hasa scrap value of £1.30 per kg. During November 120,000 kg were input into the process. The total process costs were £604,200(materials, labour and overheads).The actual output of the process was 109,000 kg finished product and 11,000 kg scrap.

(a) Calculate the data used in the process account to complete the following table.

Weight (kg) Value per kg £ Total Value £Normal loss Abnormal gain Finished product

(b) If the amount received from the actual 11,000 kg scrap is £1.30 per kg, the balance in theabnormal gain account will be a debit / credit of

2 4 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

£

5.4 A company uses process costing for some of its products.The process account for October for one particular process has been partly completed but thefollowing information is also relevant:• Three employees worked on this process during October. Each employee worked 40 hours

per week for FOUR weeks and was paid £12 per hour.• Overheads are absorbed on the basis of £17 per labour hour.• The company expects a normal loss of 5% during this process, which it then sells for scrap

at £1 per kg. Complete the process account below for October.

Description kg Unit Total Description kg Unit Total cost cost cost cost £ £ £ £

Material AH1 700 1.30 Normal loss 1.00

Material AH3 500 1.60 Output 1,425

Material AH5 300 0.40

Labour

Overheads

6.1 Analyse the following features based on whether they apply to marginal costing or absorptioncosting by ticking the appropriate column in the table.

Feature Marginal Absorption costing costing(a) Uses just the variable costs to value a unit of production

(b) Complies with standard IAS 2 for inventory valuation

(c) Is often used in conjunction with the preparation of amanufacturing account

(d) Can be used in conjunction with break-even analysis

(e) It does not consider cost behaviour when classifying costs

(f) It uses the idea of contribution to help with short-termdecision making

c h a p t e r a c t i v i t i e s 2 5

Marginal, absorption and activitybased costing6

2 6 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

6.2 Execo Ltd makes one product, with the following costs:

Variable direct materials £12 per unitVariable direct labour £15 per unitFixed overheads £120,000 per year

During the last year the company made 20,000 units and sold 15,000 units for £50 each. There wasno inventory at the start of the year.Use the following tables to show how the statement of profit or loss would appear under absorptioncosting and marginal costing.

Statement of profit or loss – absorption costing £ £Sales Direct materials Direct labour Fixed overheads Total cost of production Less closing inventory Cost of sales Profit

Statement of profit or loss – marginal costing £ £Sales Variable materials Variable labour Variable cost of production Less closing inventory Variable cost of sales Fixed costs Profit

c h a p t e r a c t i v i t i e s 2 7

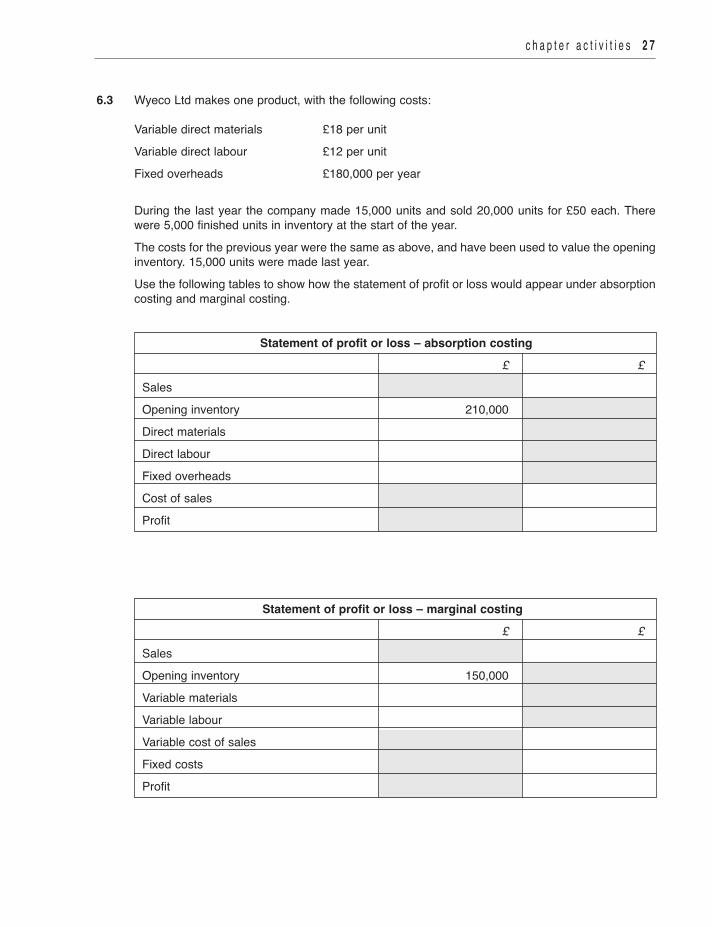

6.3 Wyeco Ltd makes one product, with the following costs:

Variable direct materials £18 per unitVariable direct labour £12 per unitFixed overheads £180,000 per year

During the last year the company made 15,000 units and sold 20,000 units for £50 each. Therewere 5,000 finished units in inventory at the start of the year.The costs for the previous year were the same as above, and have been used to value the openinginventory. 15,000 units were made last year.Use the following tables to show how the statement of profit or loss would appear under absorptioncosting and marginal costing.

Statement of profit or loss – absorption costing £ £Sales Opening inventory 210,000 Direct materials Direct labour Fixed overheads Cost of sales Profit

Statement of profit or loss – marginal costing £ £Sales Opening inventory 150,000 Variable materials Variable labour Variable cost of sales Fixed costs Profit

2 8 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

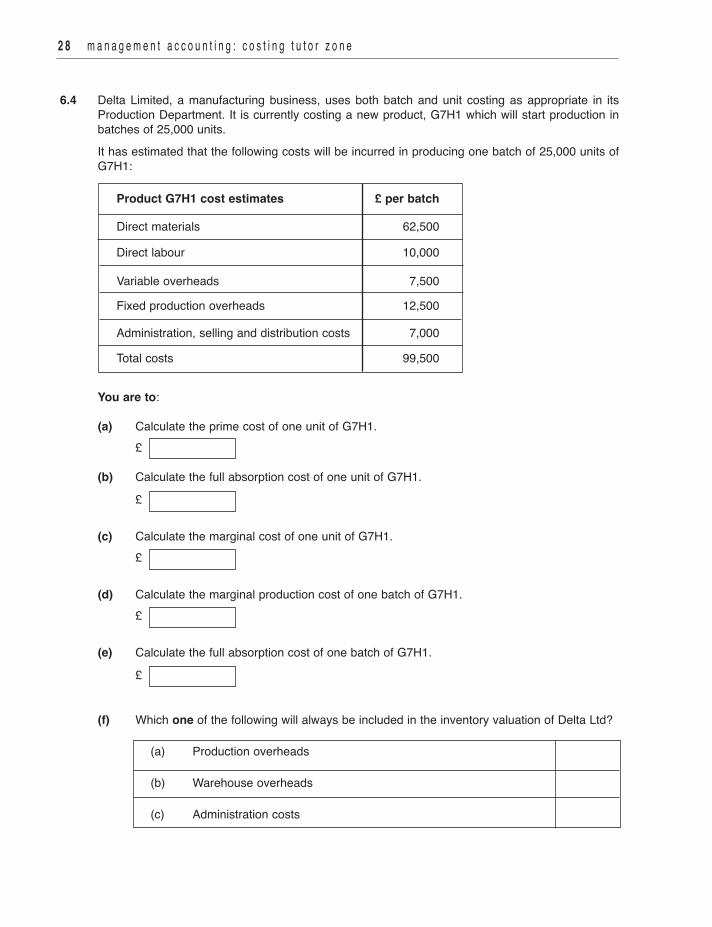

6.4 Delta Limited, a manufacturing business, uses both batch and unit costing as appropriate in itsProduction Department. It is currently costing a new product, G7H1 which will start production inbatches of 25,000 units.It has estimated that the following costs will be incurred in producing one batch of 25,000 units ofG7H1:

You are to:

(a) Calculate the prime cost of one unit of G7H1. £

(b) Calculate the full absorption cost of one unit of G7H1. £

(c) Calculate the marginal cost of one unit of G7H1. £

(d) Calculate the marginal production cost of one batch of G7H1. £

(e) Calculate the full absorption cost of one batch of G7H1. £

(f) Which one of the following will always be included in the inventory valuation of Delta Ltd?

(a) Production overheads

(b) Warehouse overheads

(c) Administration costs

Product G7H1 cost estimates £ per batch

Direct materials 62,500

Direct labour 10,000

Variable overheads 7,500

Fixed production overheads 12,500

Administration, selling and distribution costs 7,000

Total costs 99,500

6.6 Place the following headings and amounts into the correct format of a manufacturing account onthe right side of the table, making sure that the arithmetic of your account is accurate.

£ £Prime (Direct) cost 146,000

Opening inventory of raw materials 20,000

Closing inventory of work in progress 38,000

Direct labour 60,000

Opening inventory of work in progress 20,000

Factory cost 188,000

Closing inventory of raw materials 22,000

Manufacturing overheads 42,000

Raw materials used in manufacture 86,000

Purchases of raw materials 88,000

Factory cost of goods manufactured 170,000

6.5 The bank has asked for some information on your business’s recent performance, in support of aloan application, and you have been asked to value the closing inventory for inclusion in theseaccounts. Which one of these would be ethical behaviour?

(a) Using marginal costing for the closing inventory valuation(b) Using absorption costing for the closing inventory valuation(c) Using the method which gives you the highest closing inventory value(d) Using the method which gives you the lowest closing inventory value

c h a p t e r a c t i v i t i e s 2 9

3 0 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

Aspects of budgeting7

7.1 A company wishes to estimate how its expenses behave when production volumes change. (a) Complete the following table, and by using the high-low method calculate the expected

variable costs (per unit) and fixed costs (per month).

Cost per month £ Output per month (units)

Data provided 65,000 11,500

95,000 19,000

Difference Variable cost per unit

Fixed cost per month

(b) Using the information calculated in part (a), complete the following table to show thebreakdown of estimated costs at a monthly production level of 12,800 units.

£Variable costs Fixed costs Total costs

c h a p t e r a c t i v i t i e s 3 1

7.2 From the following list of statements, select those that are true.

True

(a) Capital expenditure relates to expenditure on assets that will benefit theorganisation for more than one accounting period

(b) All direct costs behave as variable costs

(c) Costs of the installation of non-current assets are treated as capital expenditure

(d) Semi-variable costs contain both a fixed element and a variable element

(e) Fixed costs may change from time to time due to factors other than output levels

(f) Variable costs per unit of output do not alter when volumes change

(g) Total fixed costs change when the volume of output changes

3 2 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

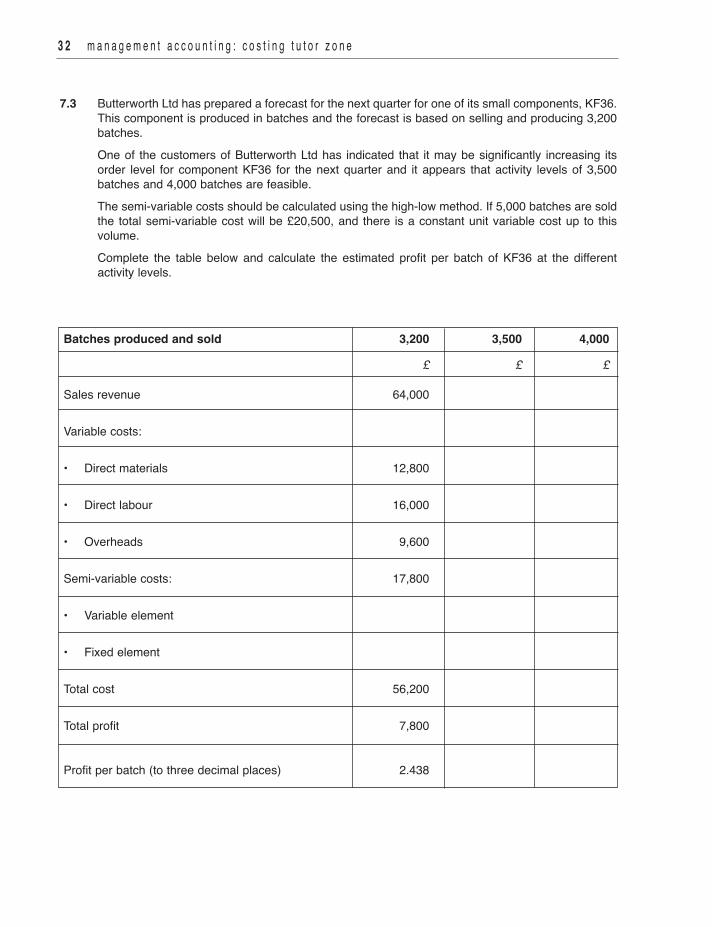

7.3 Butterworth Ltd has prepared a forecast for the next quarter for one of its small components, KF36.This component is produced in batches and the forecast is based on selling and producing 3,200batches.One of the customers of Butterworth Ltd has indicated that it may be significantly increasing itsorder level for component KF36 for the next quarter and it appears that activity levels of 3,500batches and 4,000 batches are feasible.The semi-variable costs should be calculated using the high-low method. If 5,000 batches are soldthe total semi-variable cost will be £20,500, and there is a constant unit variable cost up to thisvolume.Complete the table below and calculate the estimated profit per batch of KF36 at the differentactivity levels.

Batches produced and sold 3,200 3,500 4,000

£ £ £

Sales revenue 64,000 Variable costs: • Direct materials 12,800 • Direct labour 16,000 • Overheads 9,600 Semi-variable costs: 17,800 • Variable element • Fixed element Total cost 56,200 Total profit 7,800

Profit per batch (to three decimal places) 2.438

7.4 Greene Ltd has produced a performance report detailing budgeted and actual revenue and costsfor last month. The actual volume of production and sales was in line with the budgets. Calculate the amount of the variance for each budget and then determine whether it is adverse (A)or favourable (F) by putting a tick in the relevant column of the table below.

Budget Budget £ Actual £ Variance A FSales 155,000 149,500 £ Direct materials 34,200 36,200 £ Direct labour 41,200 42,100 £ Production overheads 25,600 25,500 £ Administration overheads 10,200 10,450 £ Selling and distribution overheads 18,800 20,100 £

7.5 Complete the following table to show flexible budgets based on both 75% and 120% of the originalbudgeted level of activity.Direct materials and direct labour both behave as variable costs. Overheads are a fixed cost.

Original budget Budget flexed at Budget flexed at 75% activity level 120% activity levelNumber of units 120,000 £ £ £

Sales 4,920,000

Direct materials 1,320,000

Direct labour 1,800,000

Overheads 1,300,000 Profit from operations 500,000

c h a p t e r a c t i v i t i e s 3 3

3 4 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

7.6 From the following list of statements, select those that are true.

True

(a) To prepare a flexible budget statement, the actual costs must be flexed to theactivity level of the budget

(b) When the actual sales revenue is greater than the sales revenue shown in theflexed budget, the result is a favourable variance

(c) A sales revenue variance is impossible when comparing actual revenue with aflexed budget, as they are both based on the same sales volume

(d) Variances produced by comparing actual costs with a fixed budget aremeaningless if the actual activity level is significantly different from that of thebudget

(e) Fixed budgets are useful for planning purposes or for when the activity level isunlikely to change

(f) A sales revenue variance based on a flexed budget can arise when goods arenot always sold at budgeted prices

(g) When actual costs are greater than those shown in the flexed budget, the resultis a favourable variance

7.7 Buccaneer Ltd has the following original budget for product LK9 for the year ending 31 December.

BudgetVolume sold 200,000 £000Sales revenue 1,200Less costs: Direct materials 300Direct labour 480Overheads 210Profit from operations 210

Both direct materials and direct labour are variable costs, but the overheads are fixed.(a) Complete the table below to show a flexed budget and the resulting variances against this

budget for the year. Show the actual variance amount, for sales and each cost, in thecolumn headed ‘Variance’ and indicate whether this is Favourable or Adverse by entering For A in the final column. If neither F nor A, enter 0.

Flexed budget Actual Variance (F), (A) or 0 Volume sold 194,000 £ £ £

Sales revenue 1,160,000

Less costs:

Direct materials 290,000

Direct labour 450,000

Overheads 218,000

Profit from operations 202,000

(b) Which one of the variances was the main reason for the difference between the actual profitand the flexed budget profit from operations? Choose one option.

(a) Sales revenue(b) Direct materials(c) Direct labour(d) Overheads

c h a p t e r a c t i v i t i e s 3 5

8.1 The following table shows how to calculate various information that is useful for short-term decisionmaking. Select the appropriate performance indicator description from the list supplied and matchit with its calculation method.

Calculation method Performance indicatorFixed costs divided by contribution per unit

Selling price per unit minus variable costs per unit

Sales volume minus break-even sales volume

(Fixed costs plus target profit) divided by contribution to sales ratio

(Sales minus variable costs) divided by sales

Select from:(a) Contribution per unit(b) Turnover to reach target profit(c) Contribution to sales ratio(d) Total contribution per period(e) Break-even point in units(f) Sales units to reach target profit(g) Margin of safety in units(h) Break-even point in sales value

3 6 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

Short-term decisions8

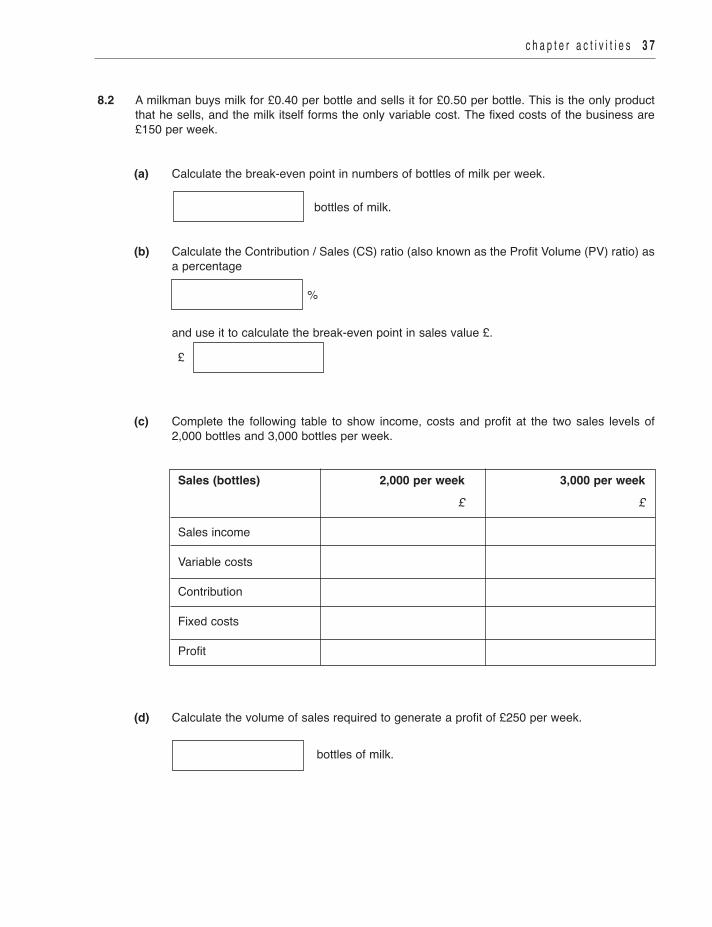

8.2 A milkman buys milk for £0.40 per bottle and sells it for £0.50 per bottle. This is the only productthat he sells, and the milk itself forms the only variable cost. The fixed costs of the business are£150 per week.

(a) Calculate the break-even point in numbers of bottles of milk per week.

bottles of milk.

(b) Calculate the Contribution / Sales (CS) ratio (also known as the Profit Volume (PV) ratio) asa percentage

%

and use it to calculate the break-even point in sales value £.

(c) Complete the following table to show income, costs and profit at the two sales levels of2,000 bottles and 3,000 bottles per week.

Sales (bottles) 2,000 per week 3,000 per week £ £

Sales income

Variable costs

Contribution

Fixed costs

Profit

(d) Calculate the volume of sales required to generate a profit of £250 per week.

bottles of milk.

c h a p t e r a c t i v i t i e s 3 7

£

3 8 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

8.3 A small general shop produced the following statement of profit or loss for last month: £ Sales 25,000 less cost of goods sold (15,000) less fixed overheads ( 4,000) Profit 6,000

The costs of goods sold are variable costs.

(a) Calculate the Contribution / Sales (CS) ratio as a percentage %

and use it to calculate the monthly break-even point in sales value.

(b) Calculate the margin of safety for the last month, in terms of the percentage of the month’ssales value.

%

(c) Complete the following table to show income, costs and profit at the two sales levels of£20,000 and £30,000 per month.

£ £

Sales income

Variable costs

Contribution

Fixed costs

Profit (d) Calculate the amount of monthly sales value required to generate a profit of £10,000 per

month.

£

£

8.4 A company currently makes tables and chairs with monthly data as follows:

Tables ChairsUnit selling price £200 £80Unit material cost £40 £20Unit labour cost £60 £30Monthly sales units 200 400

Both materials and labour are variable costs. The fixed costs of the business are £25,000 permonth, and do not relate to any specific product.

(a) Complete the following statement of profit or loss based on a typical month:

Tables £ Chairs £ Total £Sales income less variable costs Contribution less fixed costs Profit

(b) If, in the future, the company decided to make and sell only tables, calculate:

The contribution per table

The break-even point in numbers of tables per month

The number of tables that would need to be made and sold to achieve the current profit level

tables per month.

The company has a labour shortage this month and will not be able to meet the demand for bothtables and chairs. It takes 2 hours to make a table and 1 hour to make a chair. (c) Complete the following table to show the contribution per labour hour for a table and a chair

and rank which should be made first.

Table ChairContribution per unit Labour hours per unit 2 1Contribution per labour hour Ranking

(d) If the business has 700 hours of labour available in the month, how many tables and chairswill it make?Tables Chairs

c h a p t e r a c t i v i t i e s 3 9

£

4 0 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

9.1 The following table describes various information that is useful for long-term decision making.Select the key term from the list supplied, and match it with its description.

Description Name of key term

The length of time that it would take to get back the initialinvestment in a project

The difference between the present value of the total cashinflows and total cash outflows of a project

The system that converts cash flows that occur at variouspoints in time to their present value by taking account of thetime value of money

The rate which when used to discount the cash flows in aproject results in a net present value of zero

The result of comparing the present value of the total cashinflows and total cash outflows of a project when theoutflows are greater than the inflows

Select from:(a) Net present cost(b) Internal rate of return(c) Payback period(d) Discounted cash flow(e) Net present value

Long-term decisions9

9.2 A company is considering investing a capital sum of £90,000 in one of two possible projects. Thecompany’s cost of capital is 10%. Each project would have the same initial capital cost, but theremaining cashflows would differ as follows:

Year 0 Year 1 Year 2 Year 3 Year 4 £000 £000 £000 £000 £000Project A: Cash inflows 0 110 130 140 0Project A: Cash outflows 90 70 70 86 0Project B: Cash inflows 0 180 180 180 180Project B: Cash outflows 90 150 150 150 150PV Factors (10%) 1.000 0.909 0.826 0.751 0.683

(a) Complete the following table to calculate the NPV of project A.

Year 0 Year 1 Year 2 Year 3 Year 4 £000 £000 £000 £000 £000

Net cashflows

PV factors 1.000 0.909 0.826 0.751 0.683

Present values (to nearest £000)

Net present value (to nearest £000)

(b) Complete the following table to calculate the NPV of project B.

Year 0 Year 1 Year 2 Year 3 Year 4 £000 £000 £000 £000 £000

Net cashflows

PV factors 1.000 0.909 0.826 0.751 0.683

Present values (to nearest £000)

Net present value (to nearest £000)

continued

c h a p t e r a c t i v i t i e s 4 1

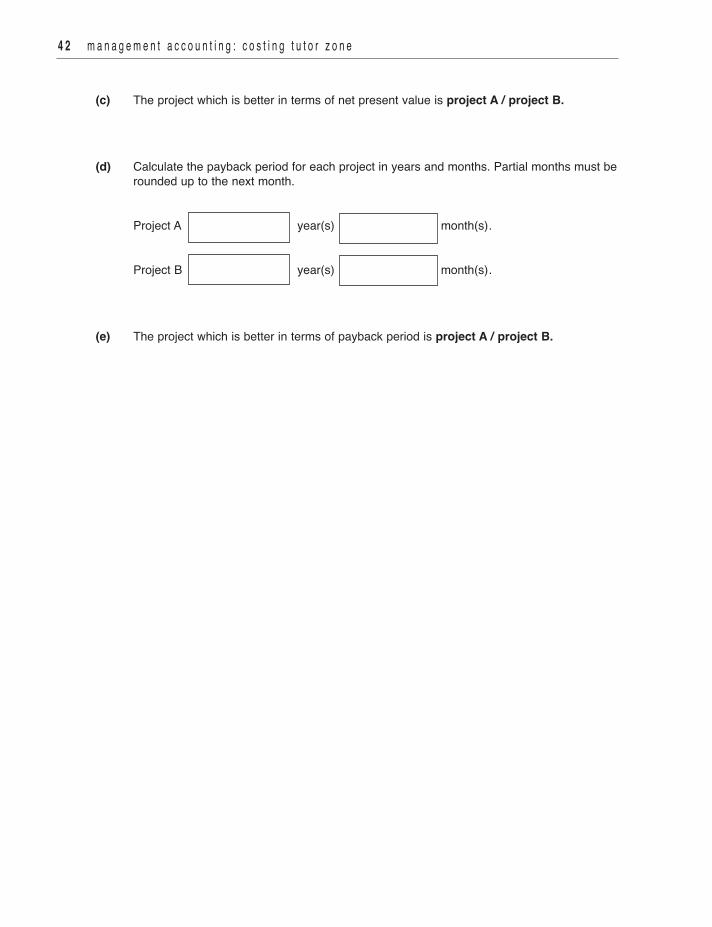

(c) The project which is better in terms of net present value is project A / project B.

(d) Calculate the payback period for each project in years and months. Partial months must berounded up to the next month.

Project A year(s) month(s).

Project B year(s) month(s).

(e) The project which is better in terms of payback period is project A / project B.

4 2 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

9.3 John Greene is considering installing additional insulation in his offices to reduce his energy bills.The insulation will cost £1,750 to purchase and install, and will result in an annual saving of £500in energy costs. The office lease expires in 5 years, so no savings after that point need beconsidered. John’s cost of capital is 10%, and this rate has been used for the discount factors inthe table shown below.

(a) Complete the following table to calculate the net present value of the additional insulation.

Year Detail Cash flow Discount factor Present value £ £0 Purchase and installation 1.000

1 Savings 0.909

2 0.826

3 0.751

4 0.683

5 0.621

Net present value

(b) Calculate the payback period for the project in years and months. Partial months must berounded up to the next month.

year(s) month(s).

(c) Is the investment in the insulation economically viable?

Yes / No

c h a p t e r a c t i v i t i e s 4 3

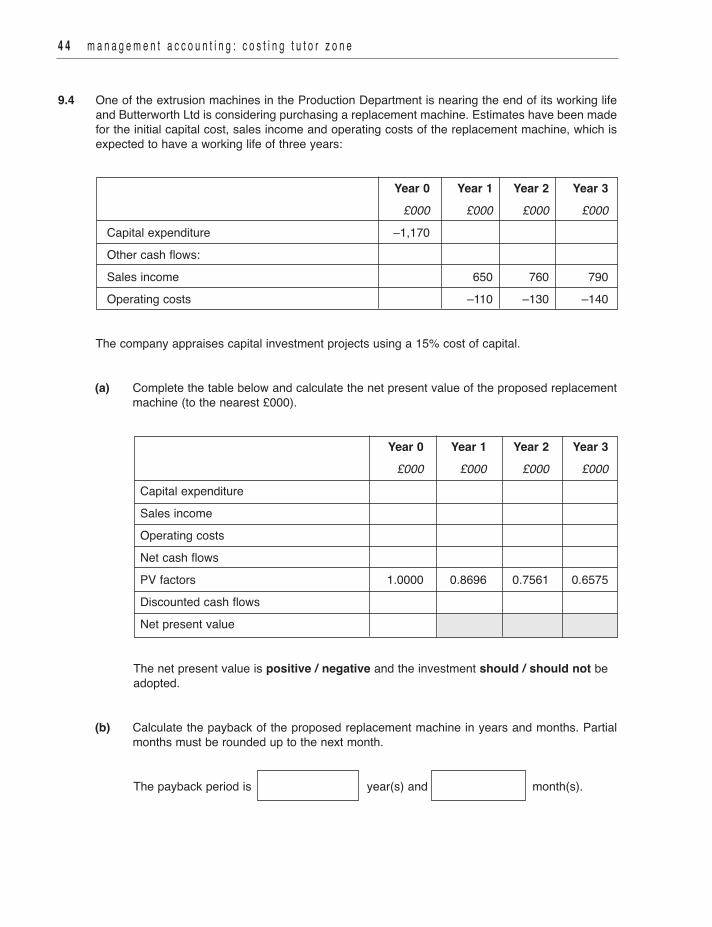

9.4 One of the extrusion machines in the Production Department is nearing the end of its working lifeand Butterworth Ltd is considering purchasing a replacement machine. Estimates have been madefor the initial capital cost, sales income and operating costs of the replacement machine, which isexpected to have a working life of three years:

Year 0 Year 1 Year 2 Year 3 £000 £000 £000 £000

Capital expenditure –1,170 Other cash flows: Sales income 650 760 790Operating costs –110 –130 –140

The company appraises capital investment projects using a 15% cost of capital.

(a) Complete the table below and calculate the net present value of the proposed replacementmachine (to the nearest £000).

Year 0 Year 1 Year 2 Year 3 £000 £000 £000 £000

Capital expenditure Sales income Operating costs Net cash flows PV factors 1.0000 0.8696 0.7561 0.6575Discounted cash flows Net present value

The net present value is positive / negative and the investment should / should not be adopted.

(b) Calculate the payback of the proposed replacement machine in years and months. Partialmonths must be rounded up to the next month.

The payback period is year(s) and month(s).

4 4 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

9.5 What is meant by the internal rate of return (IRR) of a project?

(a) The discount factor that results in a net present value of zero

(b) The discount factor that results in a positive net present value

(c) The discount factor that results in a negative net present value

(d) The discount factor that is closest to the Bank of England’s base rate

c h a p t e r a c t i v i t i e s 4 5

4 6 m a n a g e m e n t a c c o u n t i n g : c o s t i n g t u t o r z o n e

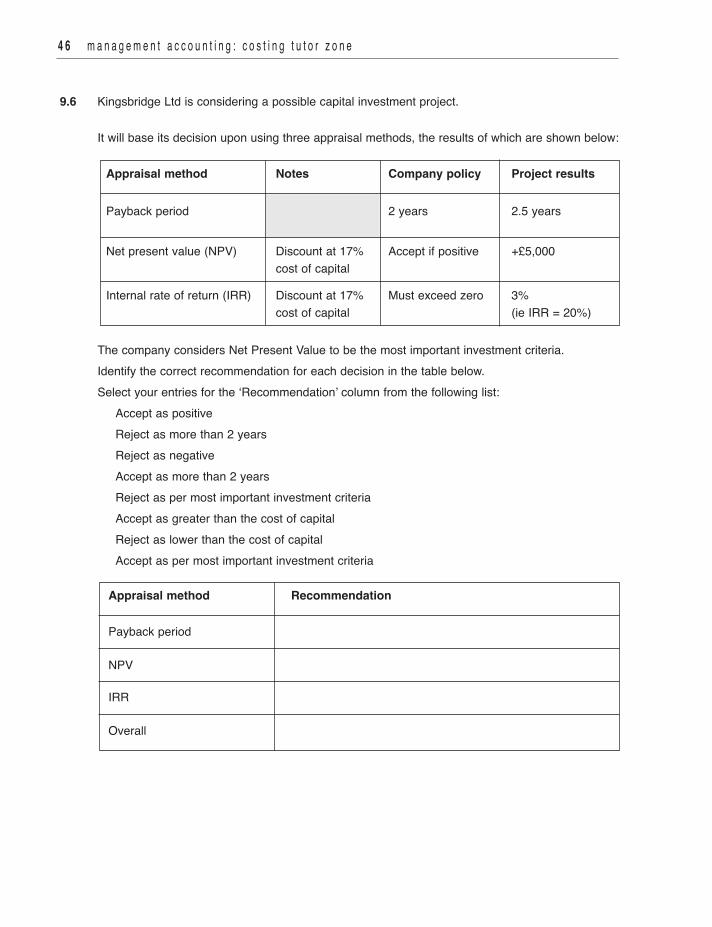

9.6 Kingsbridge Ltd is considering a possible capital investment project.

It will base its decision upon using three appraisal methods, the results of which are shown below:

The company considers Net Present Value to be the most important investment criteria. Identify the correct recommendation for each decision in the table below. Select your entries for the ‘Recommendation’ column from the following list:

Accept as positive Reject as more than 2 years Reject as negative Accept as more than 2 years Reject as per most important investment criteria Accept as greater than the cost of capital

Reject as lower than the cost of capital Accept as per most important investment criteria

Appraisal method Recommendation

Payback period

NPV

IRR

Overall

Appraisal method Notes Company policy Project results

Payback period 2 years 2.5 years

Net present value (NPV) Discount at 17% Accept if positive +£5,000 cost of capital

Internal rate of return (IRR) Discount at 17% Must exceed zero 3% cost of capital (ie IRR = 20%)