Embed Size (px)

Citation preview

NOTES:Section A - Questions 1 and 2 are compulsory.You have to answer Part A or Part B only of Question 2. (If youprovide answers to both Part(s) A and B of Question 2, you must draw a clearly distinguishable line through theanswer not to be marked. Otherwise, only the first answer to hand for this question will be marked).Section B - You are required to answer any three out of Questions 3 to 6. (If you provide answers to all ofQuestions 3 to 6, you must draw a clearly distinguishable line through the answer not to be marked. Otherwise,only the first three answers to hand for these four questions will be marked).

TIME ALLOWED:3 hours, plus 10 minutes to read the paper.

INSTRUCTIONS:During the reading time you may write notes on the examination paper but you may not commencewriting in your answer book. Please read each Question carefully.

Marks for each question are shown. The pass mark required is 50% in total over the whole paper.

Start your answer to each question on a new page.

You are reminded to pay particular attention to your communication skills and care must be takenregarding the format and literacy of the solutions. The marking system will take into account the contentof your answers and the extent to which answers are supported with relevant legislation, case law orexamples where appropriate.

List on the cover of each answer booklet, in the space provided, the number of each question(s)attempted.

MANAGEMENT ACCOUNTING

FORMATION 2 EXAMINATION - APRIL 2013

The Institute of Certified Public Accountants in Ireland, 17 Harcourt Street, Dublin 2.

Page 1

THE INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS IN IRELAND

MANAGEMENT ACCOUNTINGFORMATION 2 EXAMINATION - APRIL 2013

Time allowed: 3 hours, plus 10 minutes to read the paper.Section A: Answer Question 1 and either Part A or Part B of Question 2.Section B:You are required to answer any three out of Questions 3 to 6.

SECTION A - QUESTIONS 1 AND 2 ARE COMPULSORY

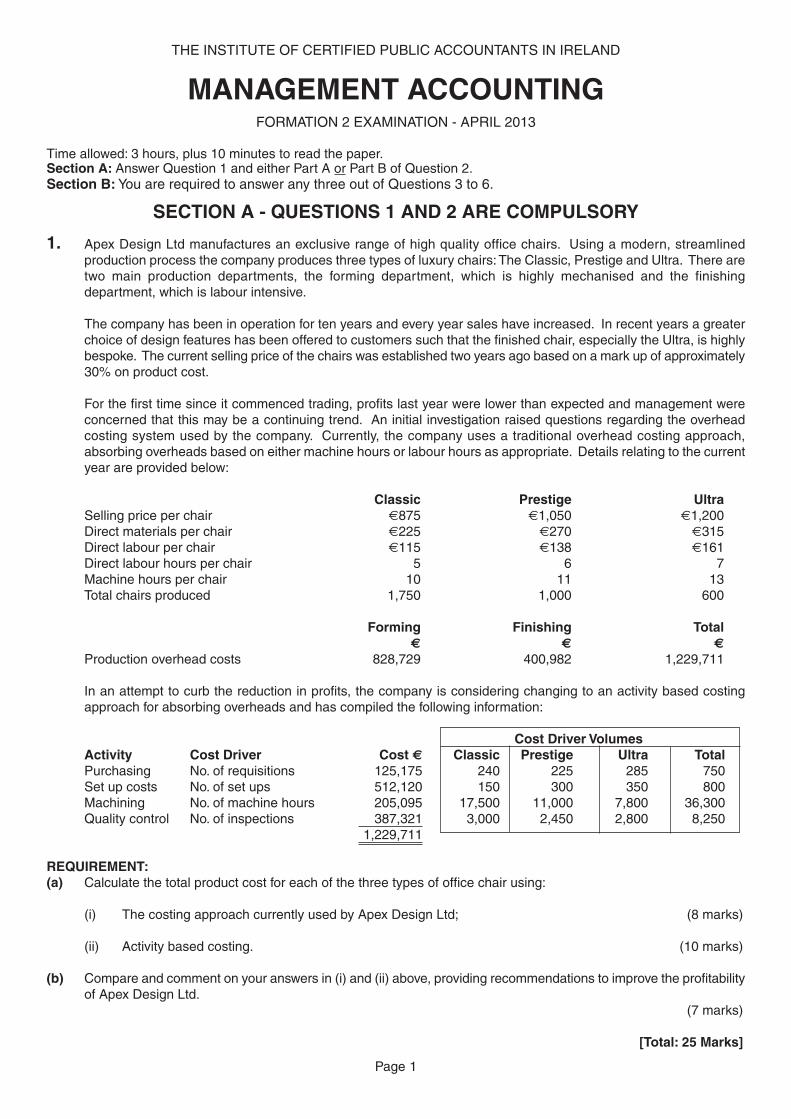

1. Apex Design Ltd manufactures an exclusive range of high quality office chairs. Using a modern, streamlinedproduction process the company produces three types of luxury chairs:The Classic, Prestige and Ultra. There aretwo main production departments, the forming department, which is highly mechanised and the finishingdepartment, which is labour intensive.

The company has been in operation for ten years and every year sales have increased. In recent years a greaterchoice of design features has been offered to customers such that the finished chair, especially the Ultra, is highlybespoke. The current selling price of the chairs was established two years ago based on a mark up of approximately30% on product cost.

For the first time since it commenced trading, profits last year were lower than expected and management wereconcerned that this may be a continuing trend. An initial investigation raised questions regarding the overheadcosting system used by the company. Currently, the company uses a traditional overhead costing approach,absorbing overheads based on either machine hours or labour hours as appropriate. Details relating to the currentyear are provided below:

Classic Prestige UltraSelling price per chair €875 €1,050 €1,200Direct materials per chair €225 €270 €315Direct labour per chair €115 €138 €161Direct labour hours per chair 5 6 7Machine hours per chair 10 11 13Total chairs produced 1,750 1,000 600

Forming Finishing Total€ € €

Production overhead costs 828,729 400,982 1,229,711

In an attempt to curb the reduction in profits, the company is considering changing to an activity based costingapproach for absorbing overheads and has compiled the following information:

Cost Driver VolumesActivity Cost Driver Cost € Classic Prestige Ultra TotalPurchasing No. of requisitions 125,175 240 225 285 750Set up costs No. of set ups 512,120 150 300 350 800Machining No. of machine hours 205,095 17,500 11,000 7,800 36,300Quality control No. of inspections 387,321 3,000 2,450 2,800 8,250

1,229,711

REQUIREMENT:(a) Calculate the total product cost for each of the three types of office chair using:

(i) The costing approach currently used by Apex Design Ltd; (8 marks)

(ii) Activity based costing. (10 marks)

(b) Compare and comment on your answers in (i) and (ii) above, providing recommendations to improve the profitabilityof Apex Design Ltd.

(7 marks)

[Total: 25 Marks]

Page 2

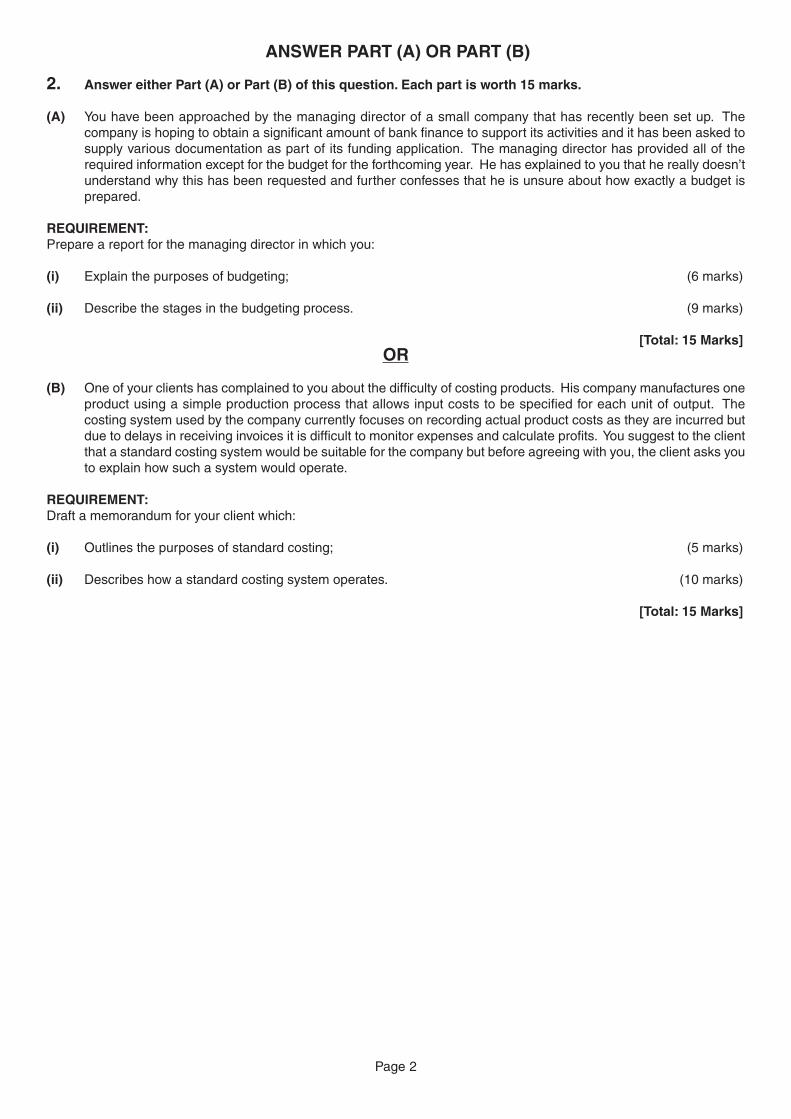

ANSWER PART (A) OR PART (B)

2. Answer either Part (A) or Part (B) of this question. Each part is worth 15 marks.

(A) You have been approached by the managing director of a small company that has recently been set up. Thecompany is hoping to obtain a significant amount of bank finance to support its activities and it has been asked tosupply various documentation as part of its funding application. The managing director has provided all of therequired information except for the budget for the forthcoming year. He has explained to you that he really doesn’tunderstand why this has been requested and further confesses that he is unsure about how exactly a budget isprepared.

REQUIREMENT:Prepare a report for the managing director in which you:

(i) Explain the purposes of budgeting; (6 marks)

(ii) Describe the stages in the budgeting process. (9 marks)

[Total: 15 Marks]OR

(B) One of your clients has complained to you about the difficulty of costing products. His company manufactures oneproduct using a simple production process that allows input costs to be specified for each unit of output. Thecosting system used by the company currently focuses on recording actual product costs as they are incurred butdue to delays in receiving invoices it is difficult to monitor expenses and calculate profits. You suggest to the clientthat a standard costing system would be suitable for the company but before agreeing with you, the client asks youto explain how such a system would operate.

REQUIREMENT:Draft a memorandum for your client which:

(i) Outlines the purposes of standard costing; (5 marks)

(ii) Describes how a standard costing system operates. (10 marks)

[Total: 15 Marks]

Page 3

SECTION B - ANSWER ANYTHREE QUESTIONS.

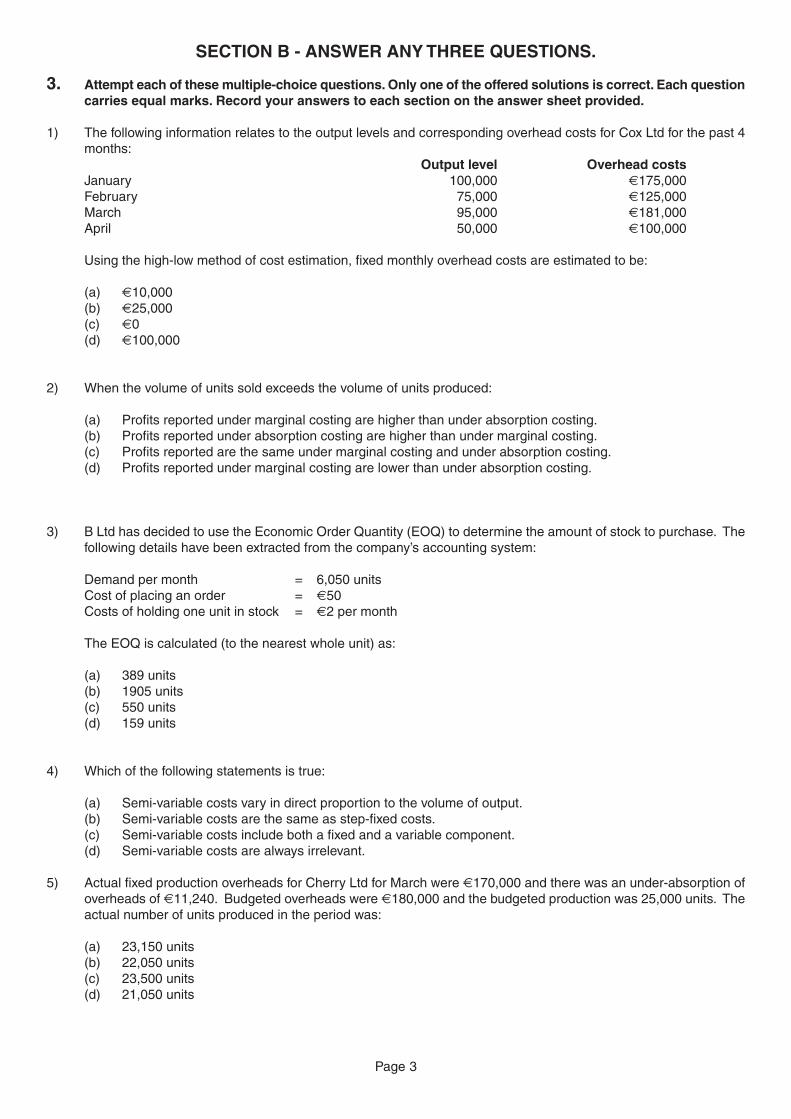

3. Attempt each of these multiple-choice questions. Only one of the offered solutions is correct. Each questioncarries equal marks. Record your answers to each section on the answer sheet provided.

1) The following information relates to the output levels and corresponding overhead costs for Cox Ltd for the past 4months:

Output level Overhead costsJanuary 100,000 €175,000February 75,000 €125,000March 95,000 €181,000April 50,000 €100,000

Using the high-low method of cost estimation, fixed monthly overhead costs are estimated to be:

(a) €10,000(b) €25,000(c) €0(d) €100,000

2) When the volume of units sold exceeds the volume of units produced:

(a) Profits reported under marginal costing are higher than under absorption costing.(b) Profits reported under absorption costing are higher than under marginal costing.(c) Profits reported are the same under marginal costing and under absorption costing.(d) Profits reported under marginal costing are lower than under absorption costing.

3) B Ltd has decided to use the Economic Order Quantity (EOQ) to determine the amount of stock to purchase. Thefollowing details have been extracted from the company’s accounting system:

Demand per month = 6,050 unitsCost of placing an order = €50Costs of holding one unit in stock = €2 per month

The EOQ is calculated (to the nearest whole unit) as:

(a) 389 units(b) 1905 units(c) 550 units(d) 159 units

4) Which of the following statements is true:

(a) Semi-variable costs vary in direct proportion to the volume of output.(b) Semi-variable costs are the same as step-fixed costs.(c) Semi-variable costs include both a fixed and a variable component.(d) Semi-variable costs are always irrelevant.

5) Actual fixed production overheads for Cherry Ltd for March were €170,000 and there was an under-absorption ofoverheads of €11,240. Budgeted overheads were €180,000 and the budgeted production was 25,000 units. Theactual number of units produced in the period was:

(a) 23,150 units(b) 22,050 units(c) 23,500 units(d) 21,050 units

Page 4

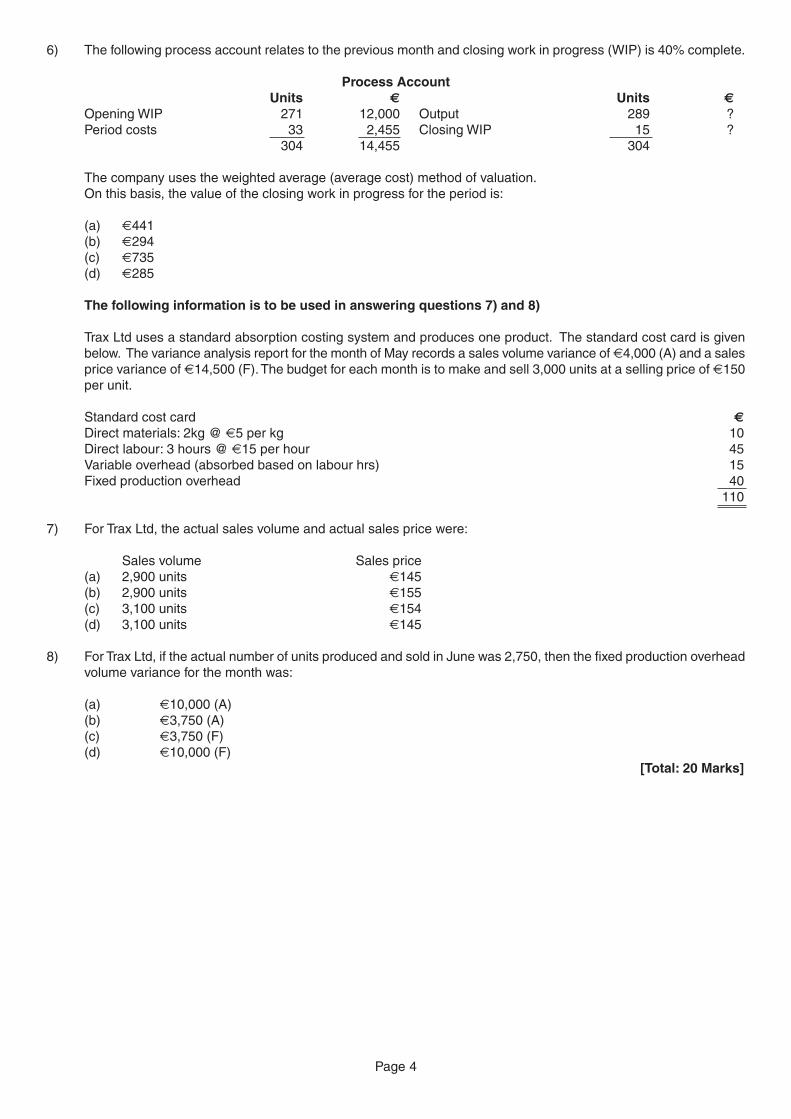

6) The following process account relates to the previous month and closing work in progress (WIP) is 40% complete.

Process AccountUnits € Units €

Opening WIP 271 12,000 Output 289 ?Period costs 33 2,455 Closing WIP 15 ?

304 14,455 304

The company uses the weighted average (average cost) method of valuation.On this basis, the value of the closing work in progress for the period is:

(a) €441(b) €294(c) €735(d) €285

The following information is to be used in answering questions 7) and 8)

Trax Ltd uses a standard absorption costing system and produces one product. The standard cost card is givenbelow. The variance analysis report for the month of May records a sales volume variance of €4,000 (A) and a salesprice variance of €14,500 (F).The budget for each month is to make and sell 3,000 units at a selling price of €150per unit.

Standard cost card €

Direct materials: 2kg @ €5 per kg 10Direct labour: 3 hours @ €15 per hour 45Variable overhead (absorbed based on labour hrs) 15Fixed production overhead 40

110

7) For Trax Ltd, the actual sales volume and actual sales price were:

Sales volume Sales price(a) 2,900 units €145(b) 2,900 units €155(c) 3,100 units €154(d) 3,100 units €145

8) For Trax Ltd, if the actual number of units produced and sold in June was 2,750, then the fixed production overheadvolume variance for the month was:

(a) €10,000 (A)(b) €3,750 (A)(c) €3,750 (F)(d) €10,000 (F)

[Total: 20 Marks]

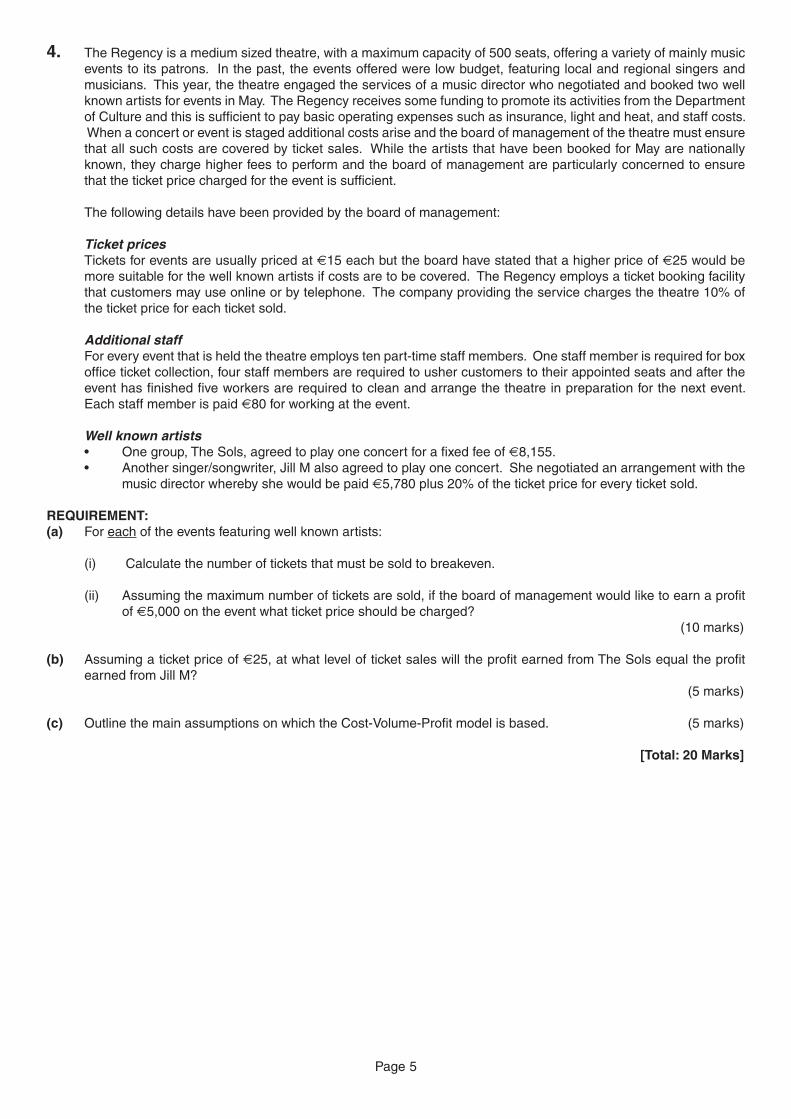

4. The Regency is a medium sized theatre, with a maximum capacity of 500 seats, offering a variety of mainly musicevents to its patrons. In the past, the events offered were low budget, featuring local and regional singers andmusicians. This year, the theatre engaged the services of a music director who negotiated and booked two wellknown artists for events in May. The Regency receives some funding to promote its activities from the Departmentof Culture and this is sufficient to pay basic operating expenses such as insurance, light and heat, and staff costs.When a concert or event is staged additional costs arise and the board of management of the theatre must ensurethat all such costs are covered by ticket sales. While the artists that have been booked for May are nationallyknown, they charge higher fees to perform and the board of management are particularly concerned to ensurethat the ticket price charged for the event is sufficient.

The following details have been provided by the board of management:

Ticket pricesTickets for events are usually priced at €15 each but the board have stated that a higher price of €25 would bemore suitable for the well known artists if costs are to be covered. The Regency employs a ticket booking facilitythat customers may use online or by telephone. The company providing the service charges the theatre 10% ofthe ticket price for each ticket sold.

Additional staffFor every event that is held the theatre employs ten part-time staff members. One staff member is required for boxoffice ticket collection, four staff members are required to usher customers to their appointed seats and after theevent has finished five workers are required to clean and arrange the theatre in preparation for the next event.Each staff member is paid €80 for working at the event.

Well known artists• One group, The Sols, agreed to play one concert for a fixed fee of €8,155.• Another singer/songwriter, Jill M also agreed to play one concert. She negotiated an arrangement with the

music director whereby she would be paid €5,780 plus 20% of the ticket price for every ticket sold.

REQUIREMENT:(a) For each of the events featuring well known artists:

(i) Calculate the number of tickets that must be sold to breakeven.

(ii) Assuming the maximum number of tickets are sold, if the board of management would like to earn a profitof €5,000 on the event what ticket price should be charged?

(10 marks)

(b) Assuming a ticket price of €25, at what level of ticket sales will the profit earned from The Sols equal the profitearned from Jill M?

(5 marks)

(c) Outline the main assumptions on which the Cost-Volume-Profit model is based. (5 marks)

[Total: 20 Marks]

Page 5

Page 6

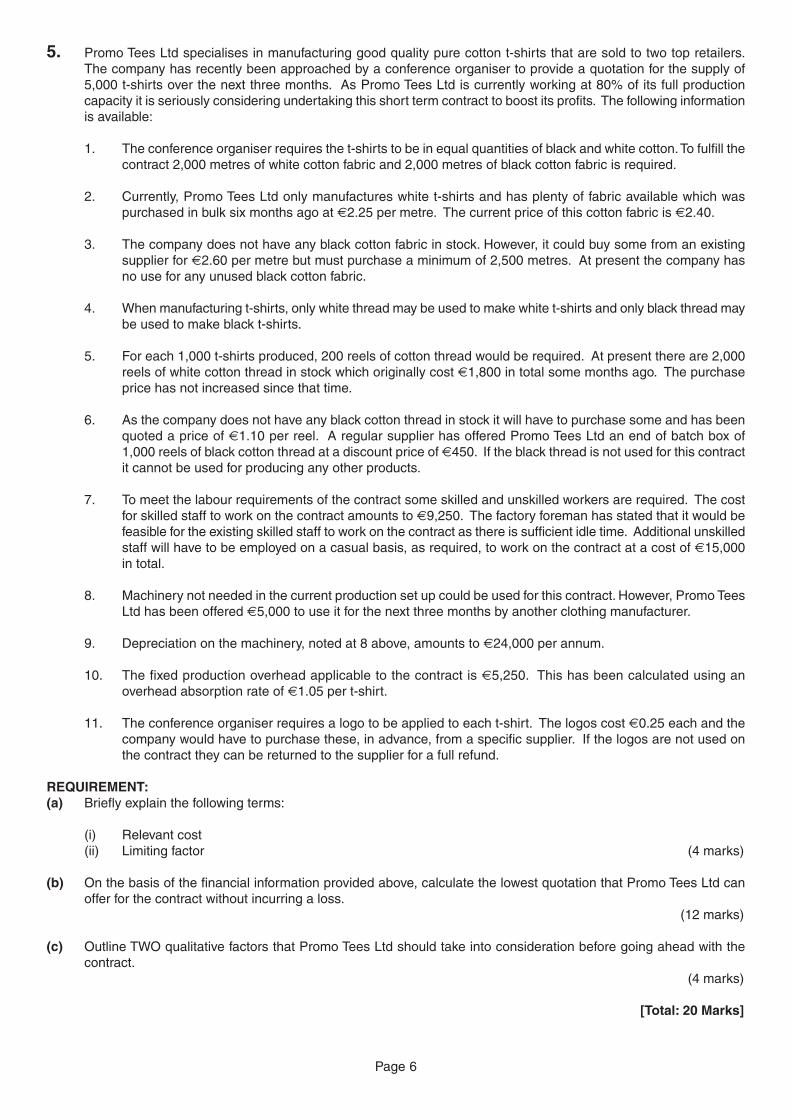

5. Promo Tees Ltd specialises in manufacturing good quality pure cotton t-shirts that are sold to two top retailers.The company has recently been approached by a conference organiser to provide a quotation for the supply of5,000 t-shirts over the next three months. As Promo Tees Ltd is currently working at 80% of its full productioncapacity it is seriously considering undertaking this short term contract to boost its profits. The following informationis available:

1. The conference organiser requires the t-shirts to be in equal quantities of black and white cotton.To fulfill thecontract 2,000 metres of white cotton fabric and 2,000 metres of black cotton fabric is required.

2. Currently, Promo Tees Ltd only manufactures white t-shirts and has plenty of fabric available which waspurchased in bulk six months ago at €2.25 per metre. The current price of this cotton fabric is €2.40.

3. The company does not have any black cotton fabric in stock. However, it could buy some from an existingsupplier for €2.60 per metre but must purchase a minimum of 2,500 metres. At present the company hasno use for any unused black cotton fabric.

4. When manufacturing t-shirts, only white thread may be used to make white t-shirts and only black thread maybe used to make black t-shirts.

5. For each 1,000 t-shirts produced, 200 reels of cotton thread would be required. At present there are 2,000reels of white cotton thread in stock which originally cost €1,800 in total some months ago. The purchaseprice has not increased since that time.

6. As the company does not have any black cotton thread in stock it will have to purchase some and has beenquoted a price of €1.10 per reel. A regular supplier has offered Promo Tees Ltd an end of batch box of1,000 reels of black cotton thread at a discount price of €450. If the black thread is not used for this contractit cannot be used for producing any other products.

7. To meet the labour requirements of the contract some skilled and unskilled workers are required. The costfor skilled staff to work on the contract amounts to €9,250. The factory foreman has stated that it would befeasible for the existing skilled staff to work on the contract as there is sufficient idle time. Additional unskilledstaff will have to be employed on a casual basis, as required, to work on the contract at a cost of €15,000in total.

8. Machinery not needed in the current production set up could be used for this contract. However, Promo TeesLtd has been offered €5,000 to use it for the next three months by another clothing manufacturer.

9. Depreciation on the machinery, noted at 8 above, amounts to €24,000 per annum.

10. The fixed production overhead applicable to the contract is €5,250. This has been calculated using anoverhead absorption rate of €1.05 per t-shirt.

11. The conference organiser requires a logo to be applied to each t-shirt. The logos cost €0.25 each and thecompany would have to purchase these, in advance, from a specific supplier. If the logos are not used onthe contract they can be returned to the supplier for a full refund.

REQUIREMENT:(a) Briefly explain the following terms:

(i) Relevant cost(ii) Limiting factor (4 marks)

(b) On the basis of the financial information provided above, calculate the lowest quotation that Promo Tees Ltd canoffer for the contract without incurring a loss.

(12 marks)

(c) Outline TWO qualitative factors that Promo Tees Ltd should take into consideration before going ahead with thecontract.

(4 marks)

[Total: 20 Marks]

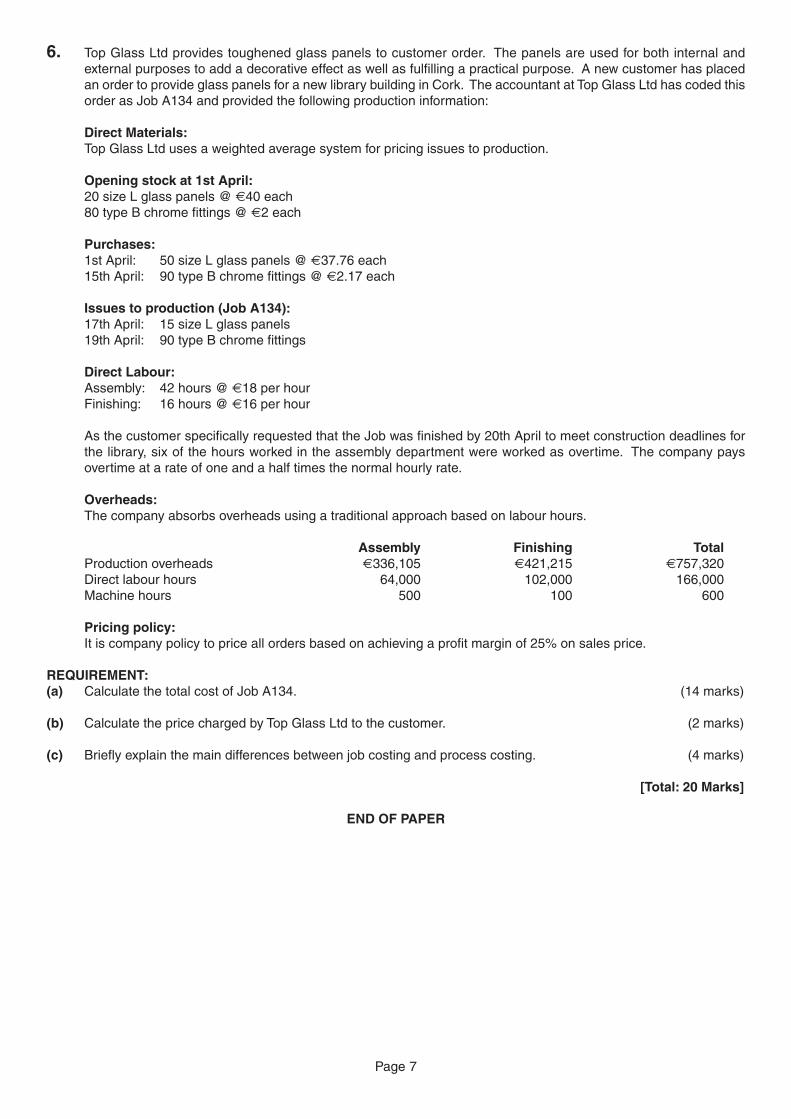

6. Top Glass Ltd provides toughened glass panels to customer order. The panels are used for both internal andexternal purposes to add a decorative effect as well as fulfilling a practical purpose. A new customer has placedan order to provide glass panels for a new library building in Cork. The accountant at Top Glass Ltd has coded thisorder as Job A134 and provided the following production information:

Direct Materials:Top Glass Ltd uses a weighted average system for pricing issues to production.

Opening stock at 1st April:20 size L glass panels @ €40 each80 type B chrome fittings @ €2 each

Purchases:1st April: 50 size L glass panels @ €37.76 each15th April: 90 type B chrome fittings @ €2.17 each

Issues to production (Job A134):17th April: 15 size L glass panels19th April: 90 type B chrome fittings

Direct Labour:Assembly: 42 hours @ €18 per hourFinishing: 16 hours @ €16 per hour

As the customer specifically requested that the Job was finished by 20th April to meet construction deadlines forthe library, six of the hours worked in the assembly department were worked as overtime. The company paysovertime at a rate of one and a half times the normal hourly rate.

Overheads:The company absorbs overheads using a traditional approach based on labour hours.

Assembly Finishing TotalProduction overheads €336,105 €421,215 €757,320Direct labour hours 64,000 102,000 166,000Machine hours 500 100 600

Pricing policy:It is company policy to price all orders based on achieving a profit margin of 25% on sales price.

REQUIREMENT:(a) Calculate the total cost of Job A134. (14 marks)

(b) Calculate the price charged by Top Glass Ltd to the customer. (2 marks)

(c) Briefly explain the main differences between job costing and process costing. (4 marks)

[Total: 20 Marks]

END OF PAPER

Page 7

THE INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS IN IRELAND

MANAGEMENT ACCOUNTINGFORMATION 2 EXAMINATION - APRIL 2013

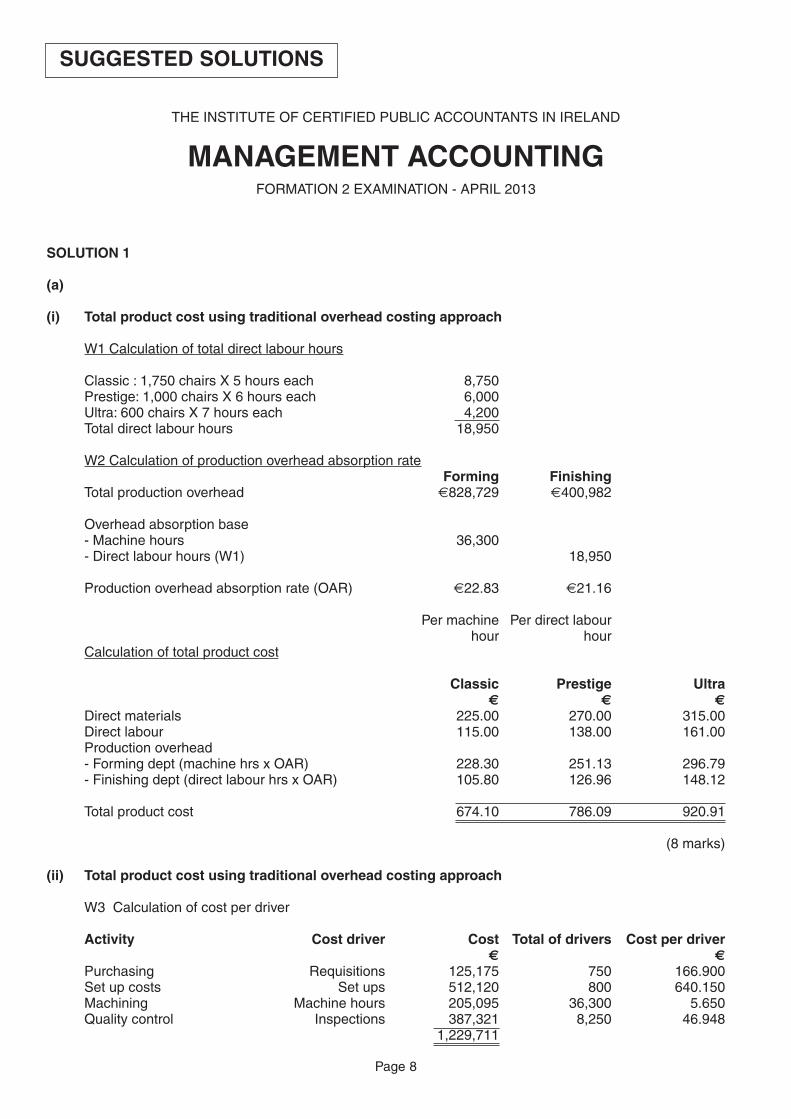

SOLUTION 1

(a)

(i) Total product cost using traditional overhead costing approach

W1 Calculation of total direct labour hours

Classic : 1,750 chairs X 5 hours each 8,750Prestige: 1,000 chairs X 6 hours each 6,000Ultra: 600 chairs X 7 hours each 4,200Total direct labour hours 18,950

W2 Calculation of production overhead absorption rateForming Finishing

Total production overhead €828,729 €400,982

Overhead absorption base- Machine hours 36,300- Direct labour hours (W1) 18,950

Production overhead absorption rate (OAR) €22.83 €21.16

Per machine Per direct labourhour hour

Calculation of total product cost

Classic Prestige Ultra€ € €

Direct materials 225.00 270.00 315.00Direct labour 115.00 138.00 161.00Production overhead- Forming dept (machine hrs x OAR) 228.30 251.13 296.79- Finishing dept (direct labour hrs x OAR) 105.80 126.96 148.12

Total product cost 674.10 786.09 920.91

(8 marks)

(ii) Total product cost using traditional overhead costing approach

W3 Calculation of cost per driver

Activity Cost driver Cost Total of drivers Cost per driver€ €

Purchasing Requisitions 125,175 750 166.900Set up costs Set ups 512,120 800 640.150Machining Machine hours 205,095 36,300 5.650Quality control Inspections 387,321 8,250 46.948

1,229,711

Page 8

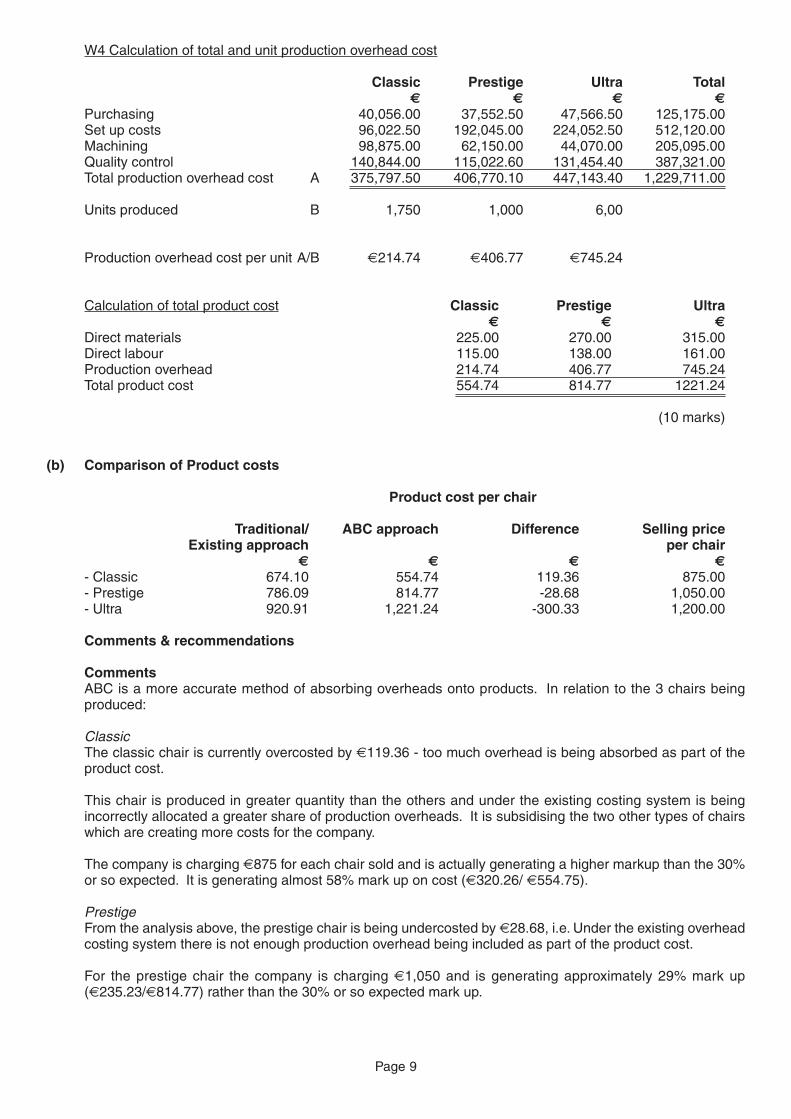

SUGGESTED SOLUTIONS

W4 Calculation of total and unit production overhead cost

Classic Prestige Ultra Total€ € € €

Purchasing 40,056.00 37,552.50 47,566.50 125,175.00Set up costs 96,022.50 192,045.00 224,052.50 512,120.00Machining 98,875.00 62,150.00 44,070.00 205,095.00Quality control 140,844.00 115,022.60 131,454.40 387,321.00Total production overhead cost A 375,797.50 406,770.10 447,143.40 1,229,711.00

Units produced B 1,750 1,000 6,00

Production overhead cost per unit A/B €214.74 €406.77 €745.24

Calculation of total product cost Classic Prestige Ultra€ € €

Direct materials 225.00 270.00 315.00Direct labour 115.00 138.00 161.00Production overhead 214.74 406.77 745.24Total product cost 554.74 814.77 1221.24

(10 marks)

(b) Comparison of Product costs

Product cost per chair

Traditional/ ABC approach Difference Selling priceExisting approach per chair

€ € € €

- Classic 674.10 554.74 119.36 875.00- Prestige 786.09 814.77 -28.68 1,050.00- Ultra 920.91 1,221.24 -300.33 1,200.00

Comments & recommendations

CommentsABC is a more accurate method of absorbing overheads onto products. In relation to the 3 chairs beingproduced:

ClassicThe classic chair is currently overcosted by €119.36 - too much overhead is being absorbed as part of theproduct cost.

This chair is produced in greater quantity than the others and under the existing costing system is beingincorrectly allocated a greater share of production overheads. It is subsidising the two other types of chairswhich are creating more costs for the company.

The company is charging €875 for each chair sold and is actually generating a higher markup than the 30%or so expected. It is generating almost 58% mark up on cost (€320.26/ €554.75).

PrestigeFrom the analysis above, the prestige chair is being undercosted by €28.68, i.e. Under the existing overheadcosting system there is not enough production overhead being included as part of the product cost.

For the prestige chair the company is charging €1,050 and is generating approximately 29% mark up(€235.23/€814.77) rather than the 30% or so expected mark up.

Page 9

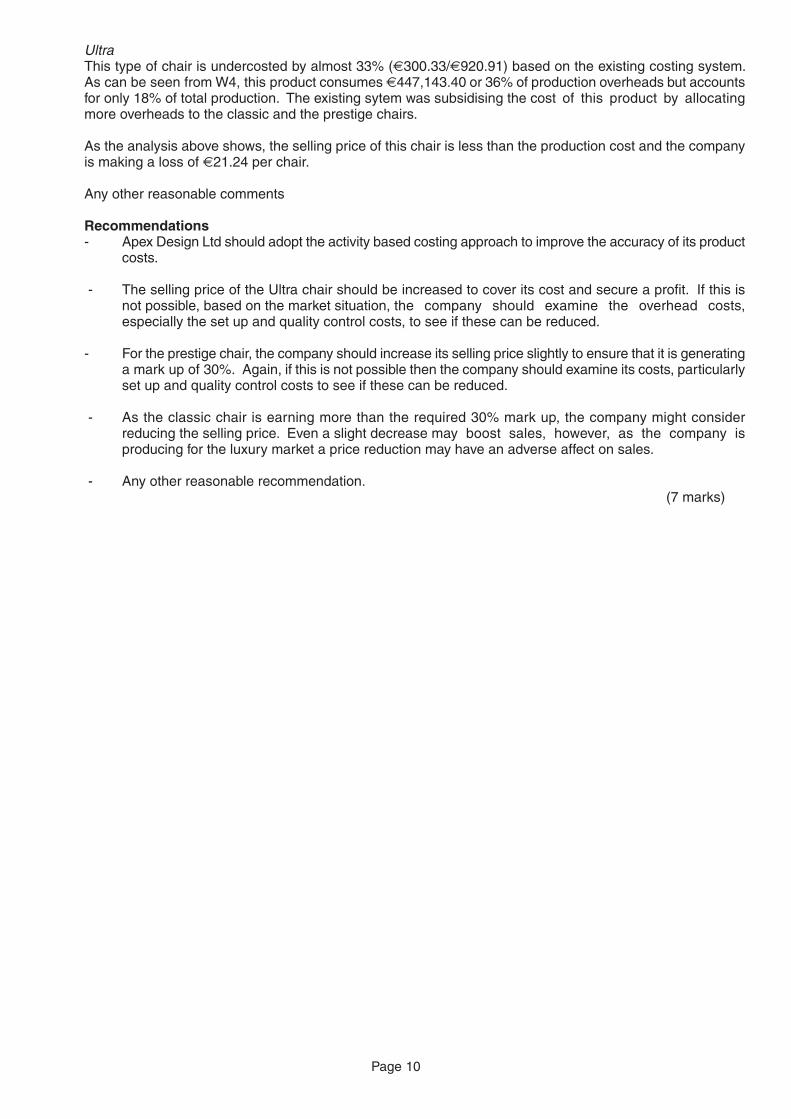

UltraThis type of chair is undercosted by almost 33% (€300.33/€920.91) based on the existing costing system.As can be seen fromW4, this product consumes €447,143.40 or 36% of production overheads but accountsfor only 18% of total production. The existing sytem was subsidising the cost of this product by allocatingmore overheads to the classic and the prestige chairs.

As the analysis above shows, the selling price of this chair is less than the production cost and the companyis making a loss of €21.24 per chair.

Any other reasonable comments

Recommendations- Apex Design Ltd should adopt the activity based costing approach to improve the accuracy of its product

costs.

- The selling price of the Ultra chair should be increased to cover its cost and secure a profit. If this isnot possible, based on the market situation, the company should examine the overhead costs,especially the set up and quality control costs, to see if these can be reduced.

- For the prestige chair, the company should increase its selling price slightly to ensure that it is generatinga mark up of 30%. Again, if this is not possible then the company should examine its costs, particularlyset up and quality control costs to see if these can be reduced.

- As the classic chair is earning more than the required 30% mark up, the company might considerreducing the selling price. Even a slight decrease may boost sales, however, as the company isproducing for the luxury market a price reduction may have an adverse affect on sales.

- Any other reasonable recommendation.(7 marks)

Page 10

SOLUTION 2

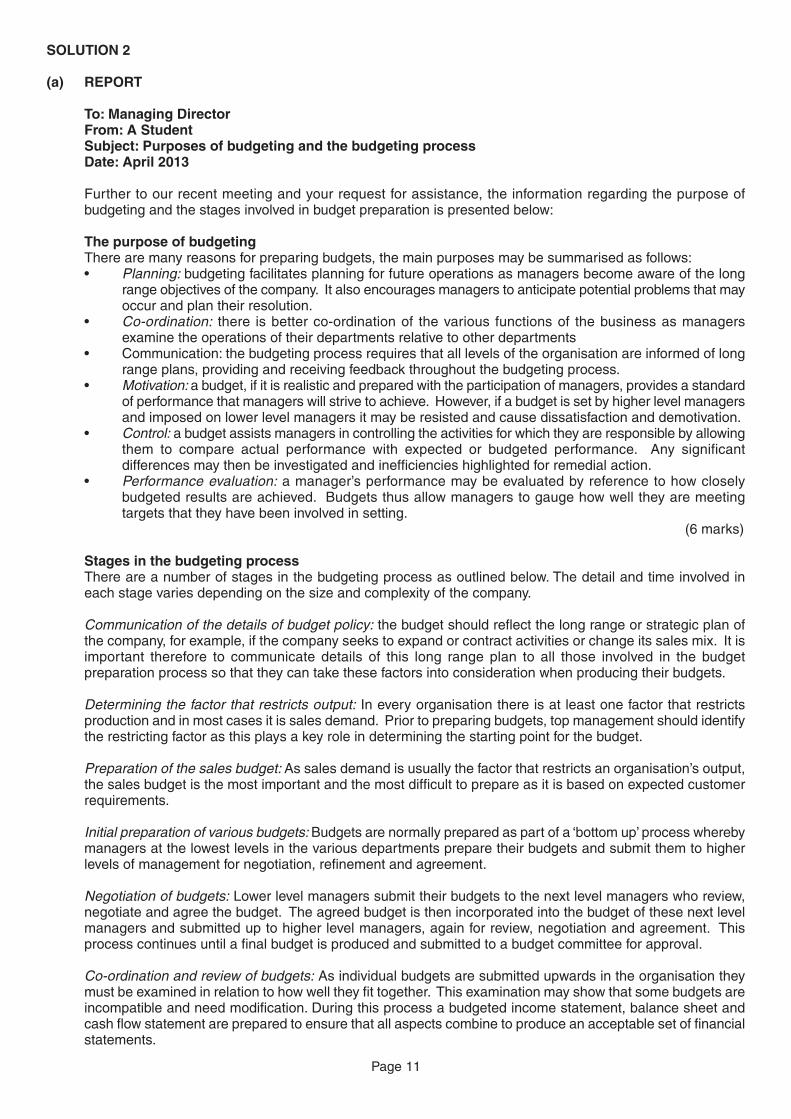

(a) REPORT

To: Managing DirectorFrom: A StudentSubject: Purposes of budgeting and the budgeting processDate: April 2013

Further to our recent meeting and your request for assistance, the information regarding the purpose ofbudgeting and the stages involved in budget preparation is presented below:

The purpose of budgetingThere are many reasons for preparing budgets, the main purposes may be summarised as follows:• Planning: budgeting facilitates planning for future operations as managers become aware of the long

range objectives of the company. It also encourages managers to anticipate potential problems that mayoccur and plan their resolution.

• Co-ordination: there is better co-ordination of the various functions of the business as managersexamine the operations of their departments relative to other departments

• Communication: the budgeting process requires that all levels of the organisation are informed of longrange plans, providing and receiving feedback throughout the budgeting process.

• Motivation: a budget, if it is realistic and prepared with the participation of managers, provides a standardof performance that managers will strive to achieve. However, if a budget is set by higher level managersand imposed on lower level managers it may be resisted and cause dissatisfaction and demotivation.

• Control: a budget assists managers in controlling the activities for which they are responsible by allowingthem to compare actual performance with expected or budgeted performance. Any significantdifferences may then be investigated and inefficiencies highlighted for remedial action.

• Performance evaluation: a manager’s performance may be evaluated by reference to how closelybudgeted results are achieved. Budgets thus allow managers to gauge how well they are meetingtargets that they have been involved in setting.

(6 marks)

Stages in the budgeting processThere are a number of stages in the budgeting process as outlined below. The detail and time involved ineach stage varies depending on the size and complexity of the company.

Communication of the details of budget policy: the budget should reflect the long range or strategic plan ofthe company, for example, if the company seeks to expand or contract activities or change its sales mix. It isimportant therefore to communicate details of this long range plan to all those involved in the budgetpreparation process so that they can take these factors into consideration when producing their budgets.

Determining the factor that restricts output: In every organisation there is at least one factor that restrictsproduction and in most cases it is sales demand. Prior to preparing budgets, top management should identifythe restricting factor as this plays a key role in determining the starting point for the budget.

Preparation of the sales budget: As sales demand is usually the factor that restricts an organisation’s output,the sales budget is the most important and the most difficult to prepare as it is based on expected customerrequirements.

Initial preparation of various budgets:Budgets are normally prepared as part of a ‘bottom up’ process wherebymanagers at the lowest levels in the various departments prepare their budgets and submit them to higherlevels of management for negotiation, refinement and agreement.

Negotiation of budgets: Lower level managers submit their budgets to the next level managers who review,negotiate and agree the budget. The agreed budget is then incorporated into the budget of these next levelmanagers and submitted up to higher level managers, again for review, negotiation and agreement. Thisprocess continues until a final budget is produced and submitted to a budget committee for approval.

Co-ordination and review of budgets: As individual budgets are submitted upwards in the organisation theymust be examined in relation to how well they fit together. This examination may show that some budgets areincompatible and need modification. During this process a budgeted income statement, balance sheet andcash flow statement are prepared to ensure that all aspects combine to produce an acceptable set of financialstatements.

Page 11

Final acceptance of budgets:When all budgets have been co-ordinated they are approved and summarisedinto a master budget consisting of a final budgeted income statement, balance sheet and cash flow statement.Once they have been approved they are passed down to all of the managers involved in the budgeting process.

Ongoing review of budgets: The budget provides a mechanism for comparing actual performance withexpected or budgeted performance and this should done on an ongoing basis. The final budget should bereviewed periodically by the budget committee. There may be changes in the actual operating conditions thatwere not anticipated by the budget and if so it should be adjusted to more realistically reflect expectedperformance.

I hope this report clearly explains the many purposes of budgeting and the various stages involved in thebudgeting process. If you have any further queries related to matters mentioned in this report, please do nothesitate to contact me.

Yours sincerely,A Student

(Note: marks will be awarded for use of report format as required by question) (9 marks)

[Total: 15 marks]

Page 12

(b) MEMORANDUMTo: A ClientFrom: A StudentSubject: Standard costing systemsDate: April 2013

Further to your request for assistance, the information regarding standard costing systems is presented below.To emphasise the importance of a standard costing system I have listed the purposes of standard costing andpresented a brief description of how a standard costing system operates.

(a) Purposes of standard costing

A standard costing system:• Aids the setting of budgets and evaluation of managerial performance.• Acts as a control mechanism by highlighting activities which deviate from plan.• Provides an estimate of future costs that may be used for decision making purposes.• Facilitates the accumulation of product costs for stock valuation purposes.• Assists in motivating individuals to achieve predetermined targets.

(5 marks)

(b) How a standard costing system operatesThere are a series of steps in the standard costing process:Set standard costsStandard costs should be established for each operation. The standard cost of a product is anaccumulation of the standard costs of the operations necessary to make the product. Standard costsmay be set using past historical data or data from engineering studies.

Record actual resultsThe actual costs involved in the particular operation should be carefully recorded so that they may becompared with their corresponding standard costs.

Compare results and calculate variancesTotal actual costs should be compared with total standard costs for each operation and variances arisingcalculated. These variances may be further analysed into those arising as a result of price differencesand those arising from usage or efficiency differences.

Investigation of variances and corrective actionVariances arising may be investigated to ascertain their cause so that corrective action may be taken.For example, if investigation of a materials variance indicated that there was excessive usage ofmaterial, the manager responsible should then try to establish the reasons for the problem. This shouldthen result in remedial action being taken to ensure that the problem did not recur.

Monitoring of standardsAs a result of investigating variances, the manager responsible may find that the original standard wastoo stringent, in which case the standard should be adjusted to reflect a more attainable level. Standardcosts should be monitored on an ongoing basis to ensure that they reflect currently attainable standards.

If you have any questions relating to information contained in this memorandum I will be pleased to providefurther clarification.

Yours sincerely,A Student

(Note: marks will be awarded for use of memorandum format as required by question) (10 marks)

[Total: 15 marks]

Page 13

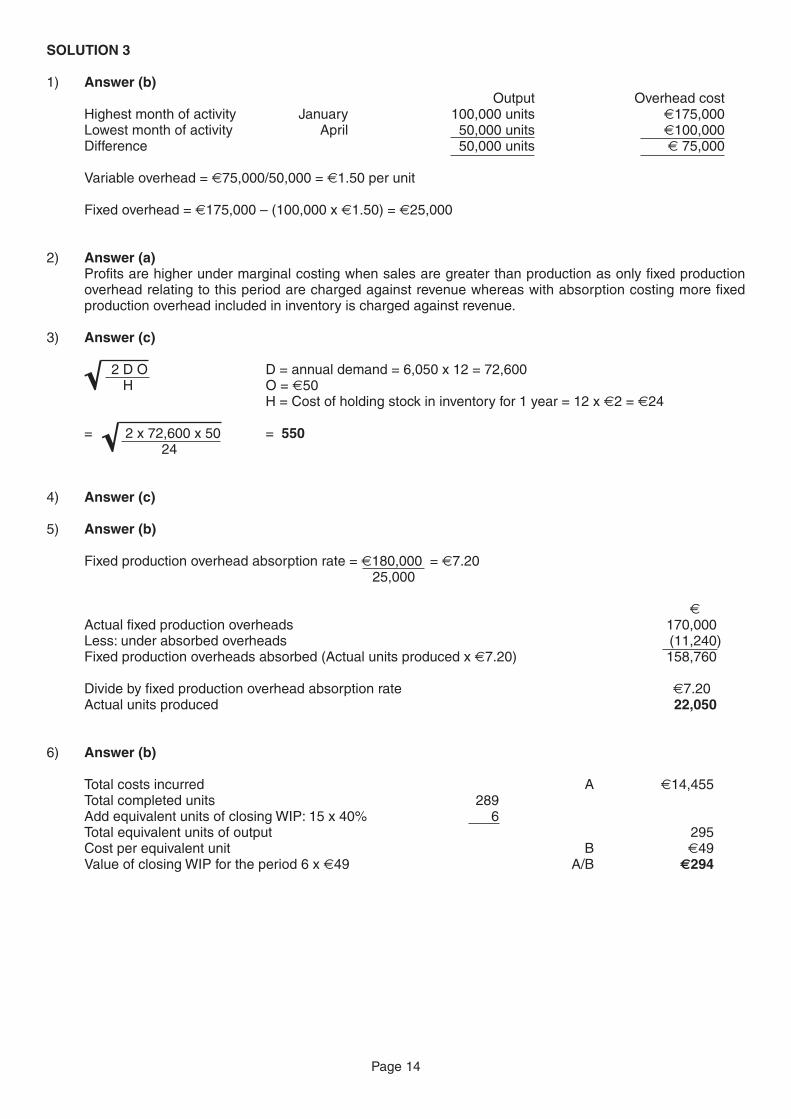

SOLUTION 3

1) Answer (b)Output Overhead cost

Highest month of activity January 100,000 units €175,000Lowest month of activity April 50,000 units €100,000Difference 50,000 units € 75,000

Variable overhead = €75,000/50,000 = €1.50 per unit

Fixed overhead = €175,000 – (100,000 x €1.50) = €25,000

2) Answer (a)Profits are higher under marginal costing when sales are greater than production as only fixed productionoverhead relating to this period are charged against revenue whereas with absorption costing more fixedproduction overhead included in inventory is charged against revenue.

3) Answer (c)

2 D O D = annual demand = 6,050 x 12 = 72,600H O = €50

H = Cost of holding stock in inventory for 1 year = 12 x €2 = €24

= 2 x 72,600 x 50 = 55024

4) Answer (c)

5) Answer (b)

Fixed production overhead absorption rate = €180,000 = €7.2025,000

€

Actual fixed production overheads 170,000Less: under absorbed overheads (11,240)Fixed production overheads absorbed (Actual units produced x €7.20) 158,760

Divide by fixed production overhead absorption rate €7.20Actual units produced 22,050

6) Answer (b)

Total costs incurred A €14,455Total completed units 289Add equivalent units of closing WIP: 15 x 40% 6Total equivalent units of output 295Cost per equivalent unit B €49Value of closing WIP for the period 6 x €49 A/B €294

Page 14

√

√

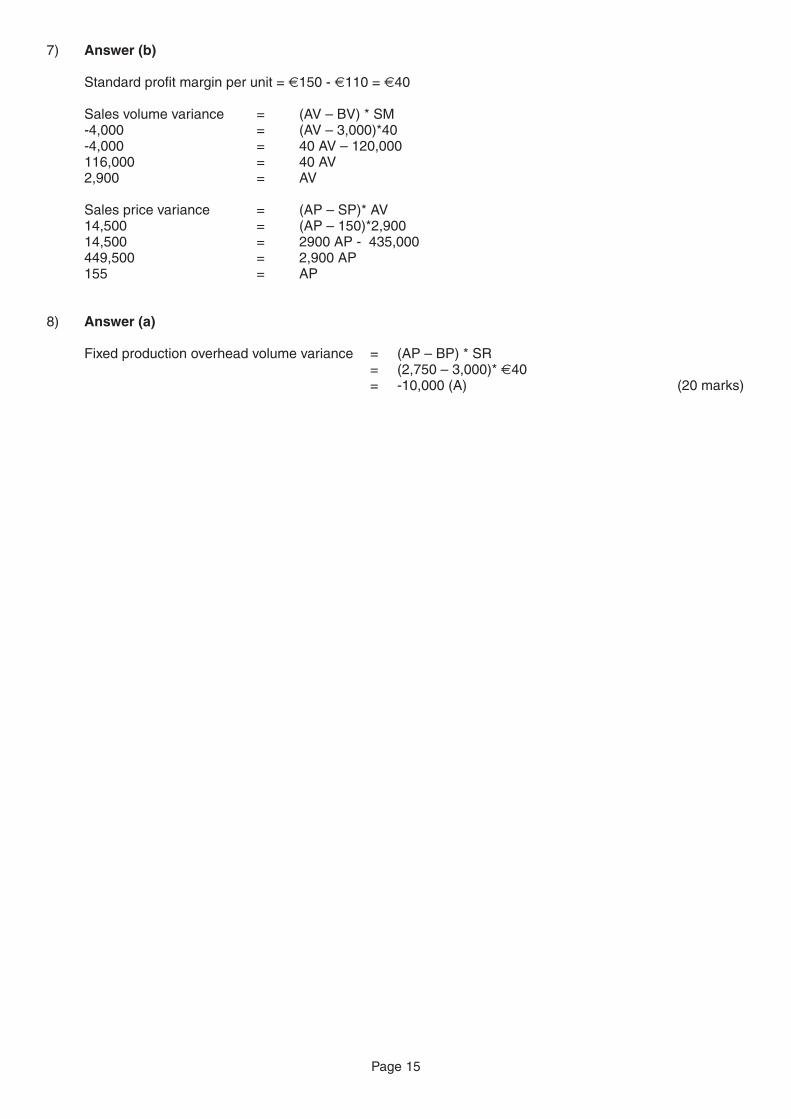

7) Answer (b)

Standard profit margin per unit = €150 - €110 = €40

Sales volume variance = (AV – BV) * SM-4,000 = (AV – 3,000)*40-4,000 = 40 AV – 120,000116,000 = 40 AV2,900 = AV

Sales price variance = (AP – SP)* AV14,500 = (AP – 150)*2,90014,500 = 2900 AP - 435,000449,500 = 2,900 AP155 = AP

8) Answer (a)

Fixed production overhead volume variance = (AP – BP) * SR= (2,750 – 3,000)* €40= -10,000 (A) (20 marks)

Page 15

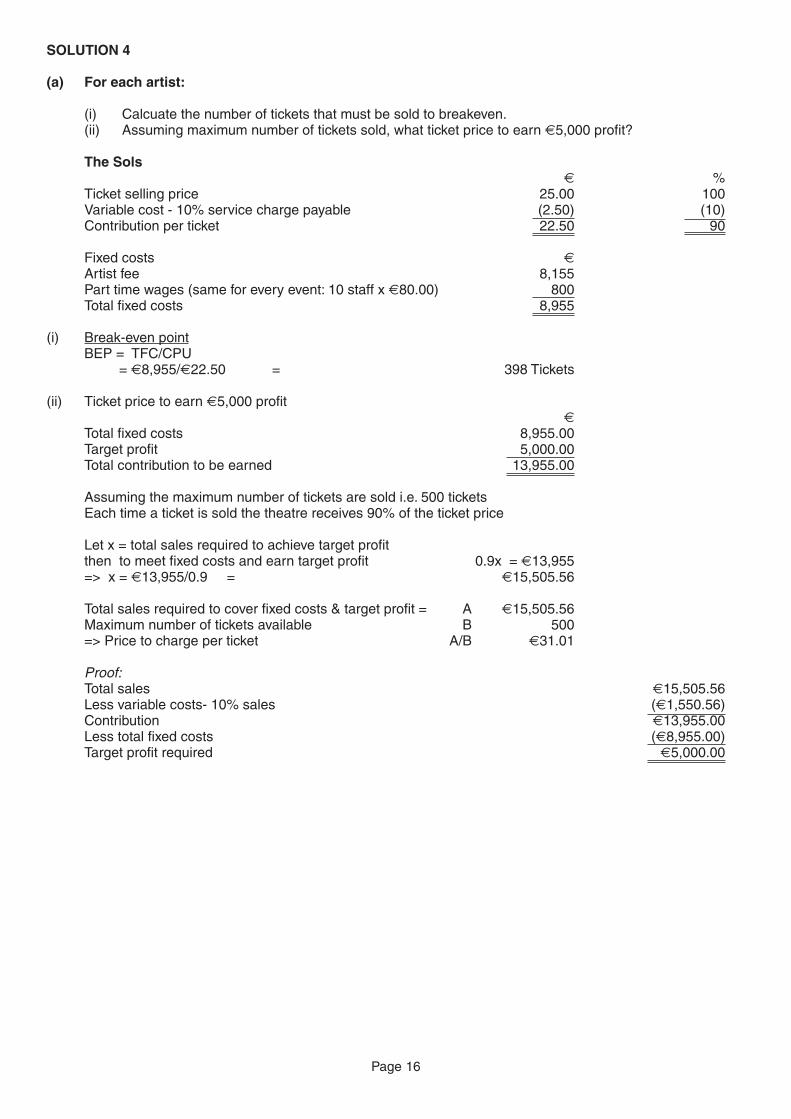

SOLUTION 4

(a) For each artist:

(i) Calcuate the number of tickets that must be sold to breakeven.(ii) Assuming maximum number of tickets sold, what ticket price to earn €5,000 profit?

The Sols€ %

Ticket selling price 25.00 100Variable cost - 10% service charge payable (2.50) (10)Contribution per ticket 22.50 90

Fixed costs €

Artist fee 8,155Part time wages (same for every event: 10 staff x €80.00) 800Total fixed costs 8,955

(i) Break-even pointBEP = TFC/CPU

= €8,955/€22.50 = 398 Tickets

(ii) Ticket price to earn €5,000 profit€

Total fixed costs 8,955.00Target profit 5,000.00Total contribution to be earned 13,955.00

Assuming the maximum number of tickets are sold i.e. 500 ticketsEach time a ticket is sold the theatre receives 90% of the ticket price

Let x = total sales required to achieve target profitthen to meet fixed costs and earn target profit 0.9x = €13,955=> x = €13,955/0.9 = €15,505.56

Total sales required to cover fixed costs & target profit = A €15,505.56Maximum number of tickets available B 500=> Price to charge per ticket A/B €31.01

Proof:Total sales €15,505.56Less variable costs- 10% sales (€1,550.56)Contribution €13,955.00Less total fixed costs (€8,955.00)Target profit required €5,000.00

Page 16

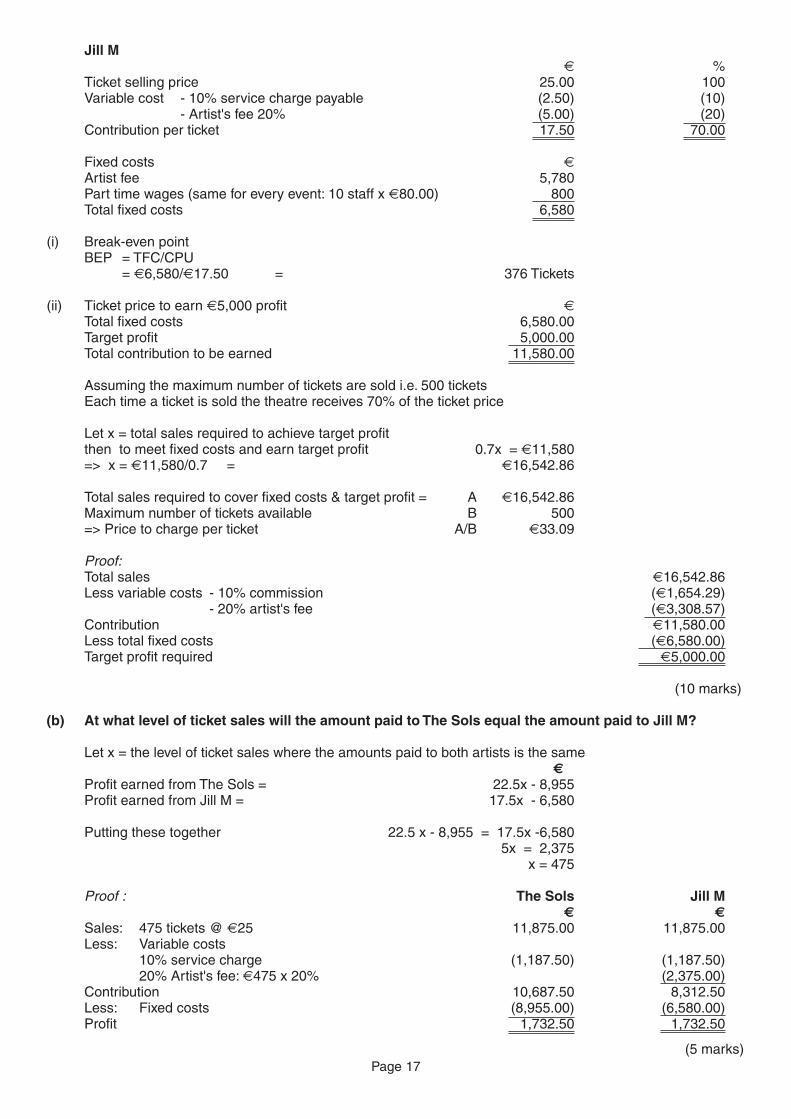

Jill M€ %

Ticket selling price 25.00 100Variable cost - 10% service charge payable (2.50) (10)

- Artist's fee 20% (5.00) (20)Contribution per ticket 17.50 70.00

Fixed costs €

Artist fee 5,780Part time wages (same for every event: 10 staff x €80.00) 800Total fixed costs 6,580

(i) Break-even pointBEP = TFC/CPU

= €6,580/€17.50 = 376 Tickets

(ii) Ticket price to earn €5,000 profit €

Total fixed costs 6,580.00Target profit 5,000.00Total contribution to be earned 11,580.00

Assuming the maximum number of tickets are sold i.e. 500 ticketsEach time a ticket is sold the theatre receives 70% of the ticket price

Let x = total sales required to achieve target profitthen to meet fixed costs and earn target profit 0.7x = €11,580=> x = €11,580/0.7 = €16,542.86

Total sales required to cover fixed costs & target profit = A €16,542.86Maximum number of tickets available B 500=> Price to charge per ticket A/B €33.09

Proof:Total sales €16,542.86Less variable costs - 10% commission (€1,654.29)

- 20% artist's fee (€3,308.57)Contribution €11,580.00Less total fixed costs (€6,580.00)Target profit required €5,000.00

(10 marks)

(b) At what level of ticket sales will the amount paid to The Sols equal the amount paid to Jill M?

Let x = the level of ticket sales where the amounts paid to both artists is the same€

Profit earned from The Sols = 22.5x - 8,955Profit earned from Jill M = 17.5x - 6,580

Putting these together 22.5 x - 8,955 = 17.5x -6,5805x = 2,375

x = 475

Proof : The Sols Jill M€ €

Sales: 475 tickets @ €25 11,875.00 11,875.00Less: Variable costs

10% service charge (1,187.50) (1,187.50)20% Artist's fee: €475 x 20% (2,375.00)

Contribution 10,687.50 8,312.50Less: Fixed costs (8,955.00) (6,580.00)Profit 1,732.50 1,732.50

(5 marks)Page 17

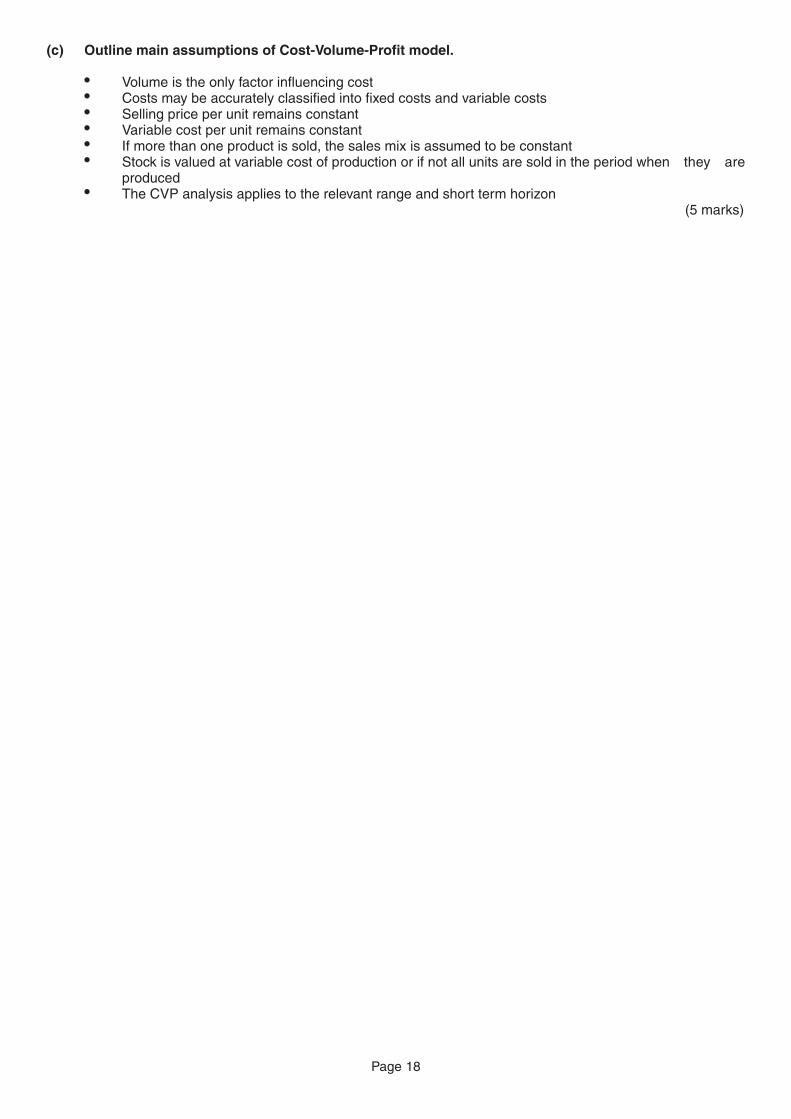

(c) Outline main assumptions of Cost-Volume-Profit model.

� Volume is the only factor influencing cost� Costs may be accurately classified into fixed costs and variable costs� Selling price per unit remains constant� Variable cost per unit remains constant� If more than one product is sold, the sales mix is assumed to be constant� Stock is valued at variable cost of production or if not all units are sold in the period when they are

produced� The CVP analysis applies to the relevant range and short term horizon

(5 marks)

Page 18

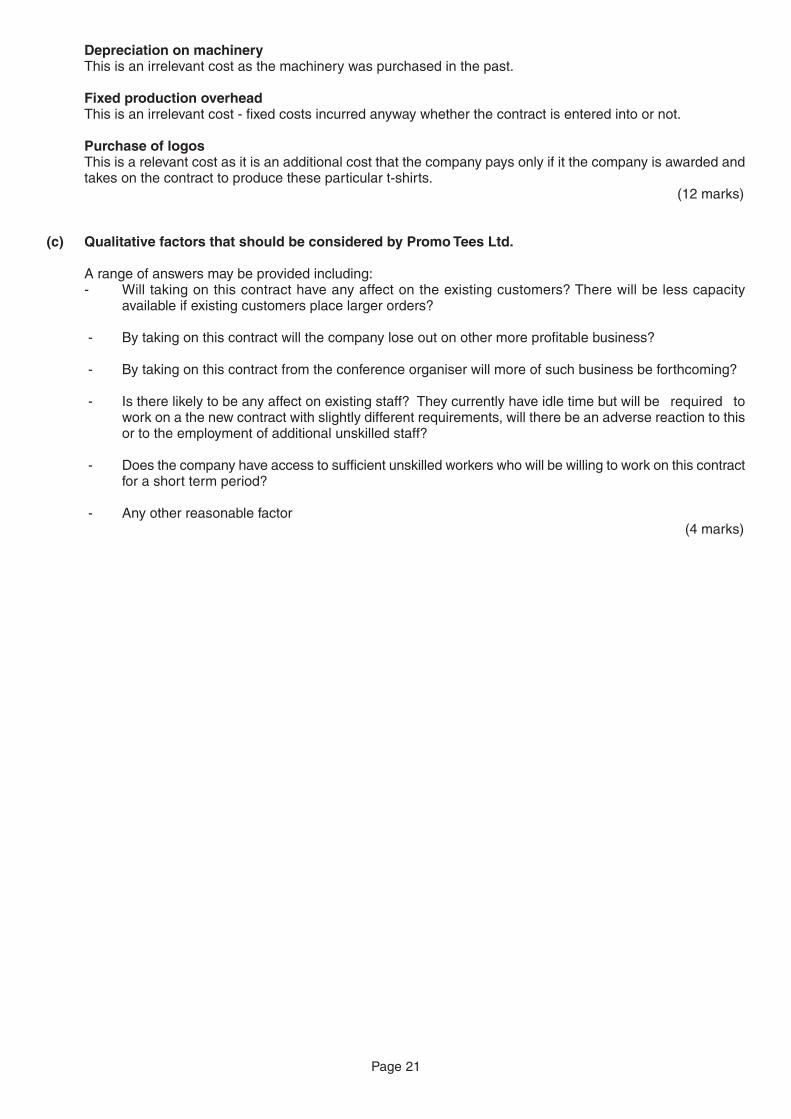

SOLUTION 5

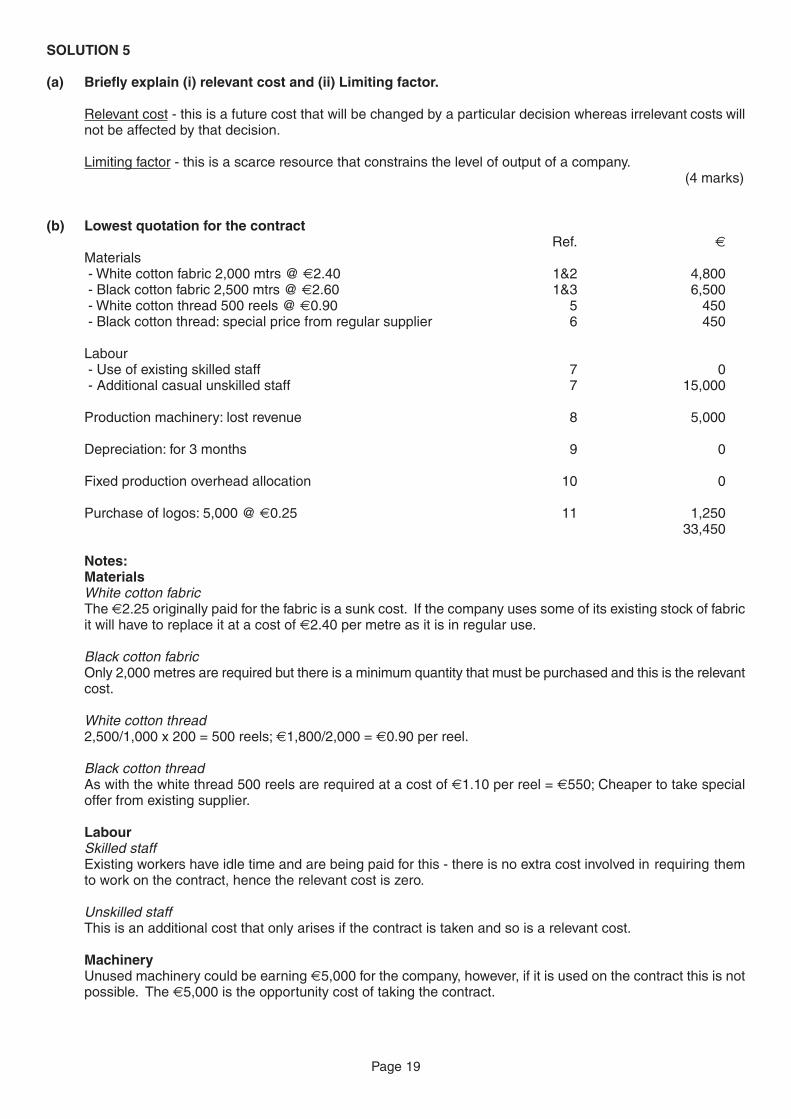

(a) Briefly explain (i) relevant cost and (ii) Limiting factor.

Relevant cost - this is a future cost that will be changed by a particular decision whereas irrelevant costs willnot be affected by that decision.

Limiting factor - this is a scarce resource that constrains the level of output of a company.(4 marks)

(b) Lowest quotation for the contractRef. €

Materials- White cotton fabric 2,000 mtrs @ €2.40 1&2 4,800- Black cotton fabric 2,500 mtrs @ €2.60 1&3 6,500- White cotton thread 500 reels @ €0.90 5 450- Black cotton thread: special price from regular supplier 6 450

Labour- Use of existing skilled staff 7 0- Additional casual unskilled staff 7 15,000

Production machinery: lost revenue 8 5,000

Depreciation: for 3 months 9 0

Fixed production overhead allocation 10 0

Purchase of logos: 5,000 @ €0.25 11 1,25033,450

Notes:MaterialsWhite cotton fabricThe €2.25 originally paid for the fabric is a sunk cost. If the company uses some of its existing stock of fabricit will have to replace it at a cost of €2.40 per metre as it is in regular use.

Black cotton fabricOnly 2,000 metres are required but there is a minimum quantity that must be purchased and this is the relevantcost.

White cotton thread2,500/1,000 x 200 = 500 reels; €1,800/2,000 = €0.90 per reel.

Black cotton threadAs with the white thread 500 reels are required at a cost of €1.10 per reel = €550; Cheaper to take specialoffer from existing supplier.

LabourSkilled staffExisting workers have idle time and are being paid for this - there is no extra cost involved in requiring themto work on the contract, hence the relevant cost is zero.

Unskilled staffThis is an additional cost that only arises if the contract is taken and so is a relevant cost.

MachineryUnused machinery could be earning €5,000 for the company, however, if it is used on the contract this is notpossible. The €5,000 is the opportunity cost of taking the contract.

Page 19

Depreciation on machineryThis is an irrelevant cost as the machinery was purchased in the past.

Fixed production overheadThis is an irrelevant cost - fixed costs incurred anyway whether the contract is entered into or not.

Purchase of logosThis is a relevant cost as it is an additional cost that the company pays only if it the company is awarded andtakes on the contract to produce these particular t-shirts.

(12 marks)

(c) Qualitative factors that should be considered by PromoTees Ltd.

A range of answers may be provided including:- Will taking on this contract have any affect on the existing customers? There will be less capacity

available if existing customers place larger orders?

- By taking on this contract will the company lose out on other more profitable business?

- By taking on this contract from the conference organiser will more of such business be forthcoming?

- Is there likely to be any affect on existing staff? They currently have idle time but will be required towork on a the new contract with slightly different requirements, will there be an adverse reaction to thisor to the employment of additional unskilled staff?

- Does the company have access to sufficient unskilled workers who will be willing to work on this contractfor a short term period?

- Any other reasonable factor(4 marks)

Page 21

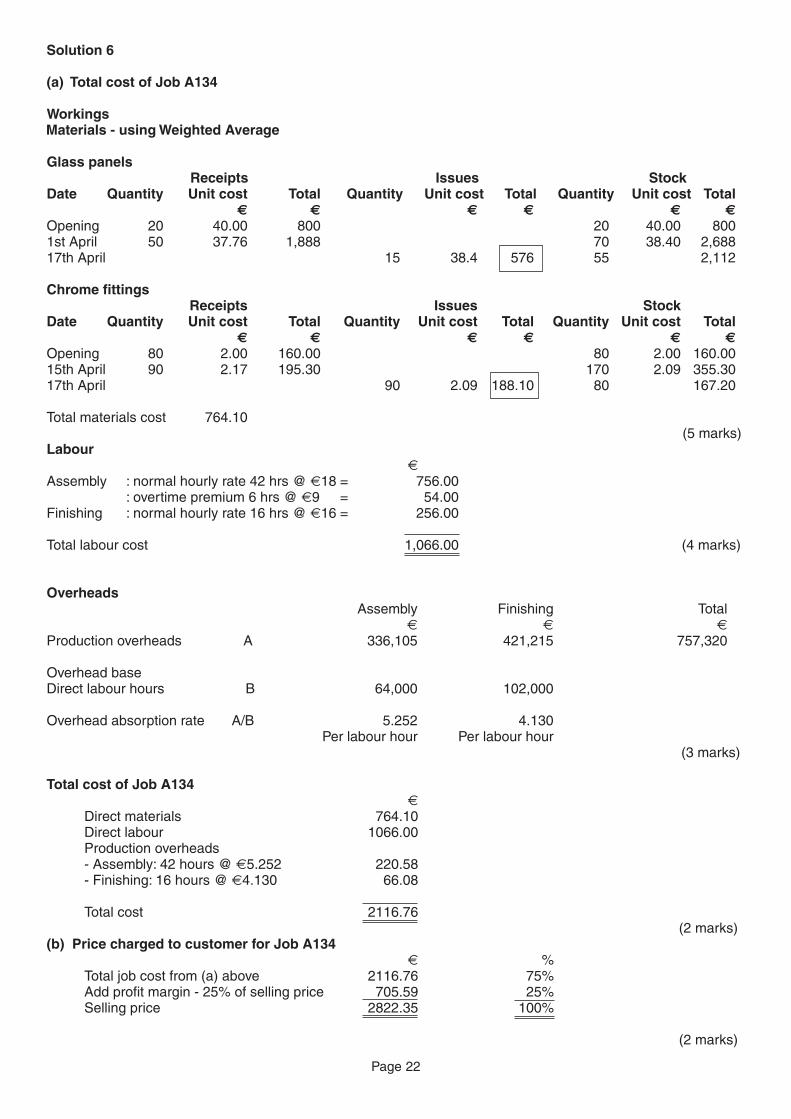

Solution 6

(a) Total cost of Job A134

WorkingsMaterials - usingWeighted Average

Glass panelsReceipts Issues Stock

Date Quantity Unit cost Total Quantity Unit cost Total Quantity Unit cost Total€ € € € € €

Opening 20 40.00 800 20 40.00 8001st April 50 37.76 1,888 70 38.40 2,68817th April 15 38.4 576 55 2,112

Chrome fittingsReceipts Issues Stock

Date Quantity Unit cost Total Quantity Unit cost Total Quantity Unit cost Total€ € € € € €

Opening 80 2.00 160.00 80 2.00 160.0015th April 90 2.17 195.30 170 2.09 355.3017th April 90 2.09 188.10 80 167.20

Total materials cost 764.10(5 marks)

Labour€

Assembly : normal hourly rate 42 hrs @ €18 = 756.00: overtime premium 6 hrs @ €9 = 54.00

Finishing : normal hourly rate 16 hrs @ €16 = 256.00

Total labour cost 1,066.00 (4 marks)

OverheadsAssembly Finishing Total

€ € €

Production overheads A 336,105 421,215 757,320

Overhead baseDirect labour hours B 64,000 102,000

Overhead absorption rate A/B 5.252 4.130Per labour hour Per labour hour

(3 marks)

Total cost of Job A134€

Direct materials 764.10Direct labour 1066.00Production overheads- Assembly: 42 hours @ €5.252 220.58- Finishing: 16 hours @ €4.130 66.08

Total cost 2116.76(2 marks)

(b) Price charged to customer for Job A134€ %

Total job cost from (a) above 2116.76 75%Add profit margin - 25% of selling price 705.59 25%Selling price 2822.35 100%

(2 marks)

Page 22

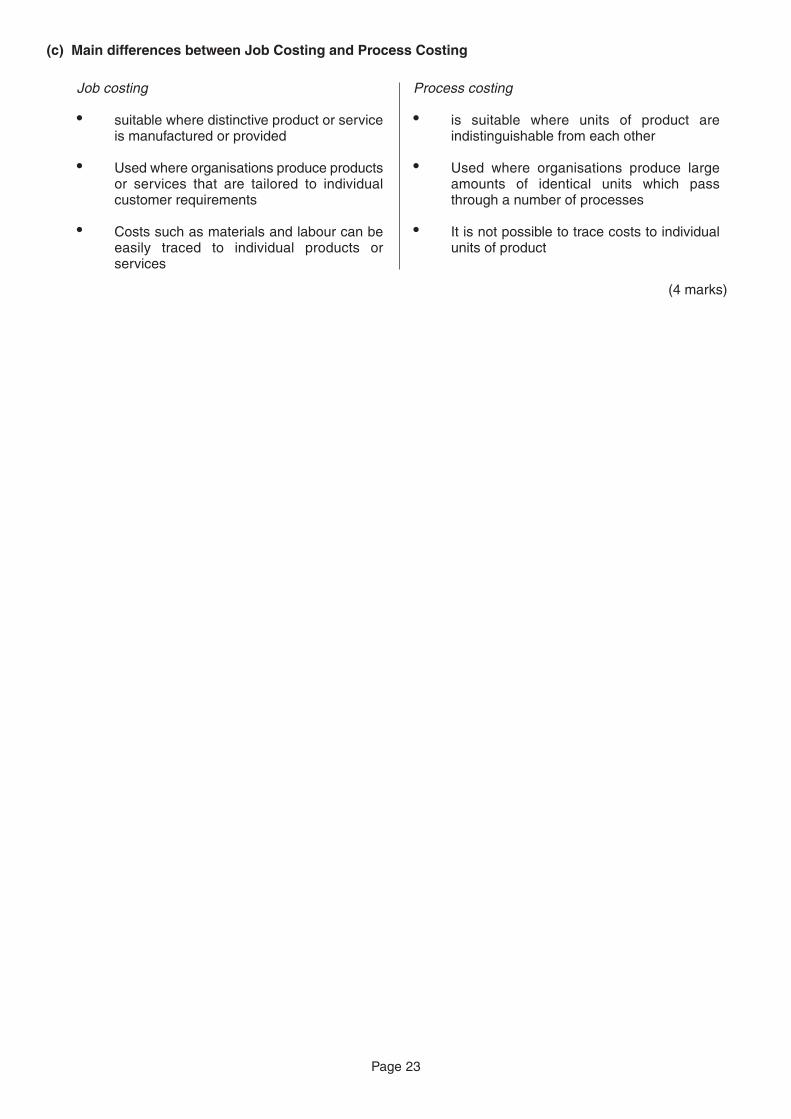

(c) Main differences between Job Costing and Process Costing

(4 marks)

Page 23

Job costing

� suitable where distinctive product or serviceis manufactured or provided

� Used where organisations produce productsor services that are tailored to individualcustomer requirements

� Costs such as materials and labour can beeasily traced to individual products orservices

Process costing

� is suitable where units of product areindistinguishable from each other

� Used where organisations produce largeamounts of identical units which passthrough a number of processes

� It is not possible to trace costs to individualunits of product