Embed Size (px)

Citation preview

1

Management I: Financial Accounting

2

Contact Information:

Office: Vilfredo-Pareto-Building (G22), Room E-209

Office hours: Thursdays 11-12 a.m., or by appointment

Email: [email protected]

Phone: 0391 – 67 18 728

3

Class Schedule:Lectures on Wednesday, 11:15 – 13:30Tutorials on Tuesday, 9:15 – 10:45

Course website:http://www.uni-magdeburg.de/bwl1/

notes and exercises

Grading scheme: Final Exam 100Assignments ?Total 100+?

4

Basic text:

Tim Sutton (2004). “Corporate Financial Accounting and Reporting“ 2nd ed., Prentice Hall.

Also of interest:

Jane L. Reimers (2008), “Financial Accounting, A Business Process Approach”, 2nd ed. Pearson International Edition

5

Chapter 1: Introduction

Purpose and Object of Financial Accounting

6

What is Accounting?“Accounting is the Language of Business”

Sound understanding of accounting is essential for all business people

Financial Accounting: external focus• Primary objectives

Stewardship, reports on past performanceInstrument to facilitate decisions for investors in the capital market

Management Accounting: internal focus• Primary objectives:

Decision facilitating for the management• Financial planning Instruments• Cost accounting for decision making

Control of management behavior• Budgeting: goal setting and control of achievement• Incentive system based on performance measures to be

delivered by accounting

7

Financial Accounting: who is addressed?

Investor orientationowners and potential acquirers of residual claims• shareholders

parties that consider to or have committed resources to a relation with the reporting entity in exchange for future compensation• creditors• suppliers / customers (maybe)

Tax authority orientationother interest groups could use the information to the detriment of investors

• regulators• trade unions• competitors

8

Contents of Financial Statements

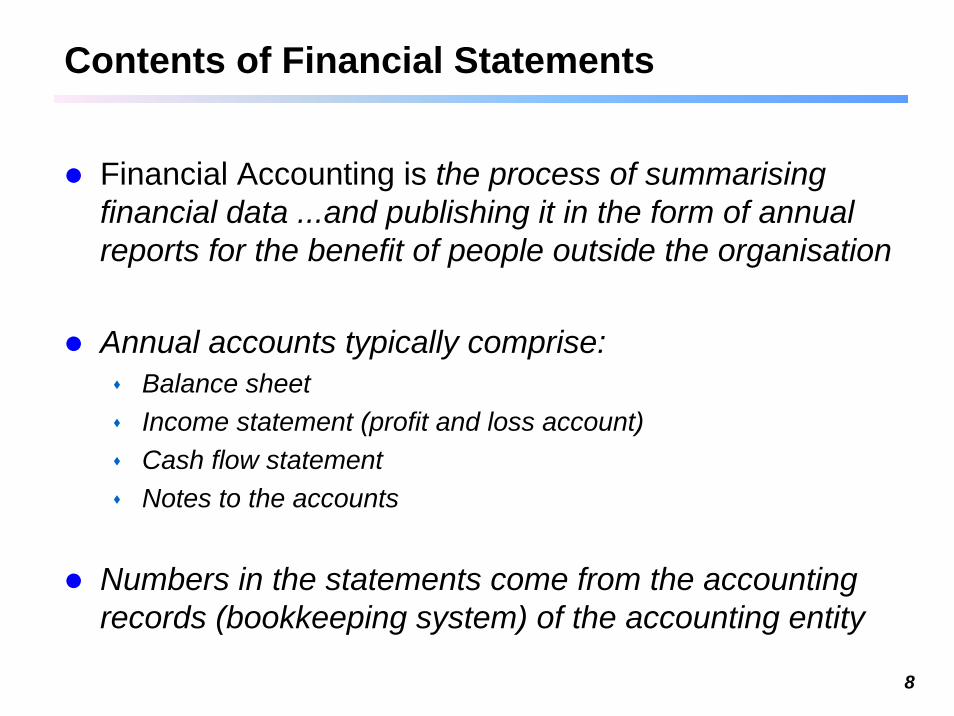

Financial Accounting is the process of summarising financial data ...and publishing it in the form of annual reports for the benefit of people outside the organisation

Annual accounts typically comprise:Balance sheetIncome statement (profit and loss account)Cash flow statementNotes to the accounts

Numbers in the statements come from the accounting records (bookkeeping system) of the accounting entity

9

Contents of Financial StatementsBalance Sheet

Helps assess the company’s financial strengthIncome Statement

Helps measure the firm’s financial performanceCash flow statement

Helps to assess the firm’s ability to survive

Stock variablesrelate to the situation of the company at a specific point in timeExamples: stocks of goods, assets, liabilities

Flow variablesrelate to the change of situation over a specific period of timeExamples: expenses, income; change in value of a fixed asset, e.g. due to exchange rate changes

10

Objectives of Financial ReportingAccording to investor orientation:

Providing information that investors find helpful in making economic decisions

What is useful information?Forward looking informationBackward looking information

Information that is • Relevant,• Reliable• Comparable

Alternatively: monitoring and disciplining role of accounting?

11

Desirable characteristics of AccountingRelevant

timelyReliable

unbiased, neutral, comprehensive, objectiveComparable

between entitiesover time (consistency principle)

transaction cost-efficientcost of information should not exceed its valueinfluence on cost of capital• unreliable and scarce information may lead to market

failure (accounting scandals)

12

Decision Usefulness according to IFRS Framework include:

RelevanceInformation is relevant if it has the potential to influence a decision • by changing expectations or predictions• by feedback on the performance of past decision rules • by enhancing assessment of risk, esp. default risk

Information relevance depends on timely availability.Reliability

Four dimensions of reliability1. Verifiability2. Representational faithfulness3. Neutrality4. Prudence

ComparabilityAbsolute performance difficult to assess. Investment decisions depend on expected relative performance. So accounting information is more useful if similar facts can be compared over different • periods and • companies.

ConsistencyConsistency: using the same accounting procedures over several periods. • Changes in accounting procedures must be indicated and explained.

13

Accounting Entities

Who is required to prepare financial statements?Specific rules apply in different countries• Various business organizations• Non for profit organizations

E.g. Charities, government agencies

Since we focus on investor-oriented accounting we restrict ourselves to companies and groups

14

Legal Forms of Business Organization

1. sole proprietorship / sole traderliable with personal resourcesif business is sold, a new proprietorship is established

2. partnershipnot a separate legal entityunlimited liability of at least one partnerany change in participation requires new partnership

3. corporation (also private limited company)separate legal entityrisk of ownership limited to investment in the companyshares can be sold to others without an effect on the identity of the corporation

Common property: separate accountingaccounting entity

15

Source: US Bureau of Census (1992); IfM Bonn (1997)

Remark: German data apply only to small and medium-sized businesses, andpartnerships include limited-liability partnerships.

Legal forms of business organization

*) e.g. cooperatives

16

RegulationGermany, Austria

Regulation in codified law: Handelsgesetzbuch (HGB)= commercial code

DPR (Deutsche Prüfstelle für Rechnungswesen)BAFin (Bundesanstalt für Finanzdienstleistungen)

tax accounting rules influence financial accounting German Accounting Standards Committee (DeutschesRechnungslegungs Standards Committee (DRSC)), 1998

The United StatesUS-GAAP (generally accepted accounting principles); numerous detailed regulationsFASB (Financial Accounting Standards Board) established in 1973;private-sector bodySEC (Securities and Exchange Commission) established in 1934; federal agency

on the web: http://www.drsc.dehttp://www.fasb.org/http://www.sec.gov/

17

Accounting in Europe

IASC (International Accounting Standards Board) founded in 1973; privately-funded accounting standard setter (based in London)Sets International Accounting Standards (IAS), now IFRS (International Financial Reporting Standards)

http://www.iasb.org.uk/

European Union authorities influence regulations of member states by rulings that have to be translated into the law of theindividual member states.

Since 2005 companies listed in member states are required to publish group accounts following International Accounting standards as far as endorsed by the European Union

18

What is decent disclosure?

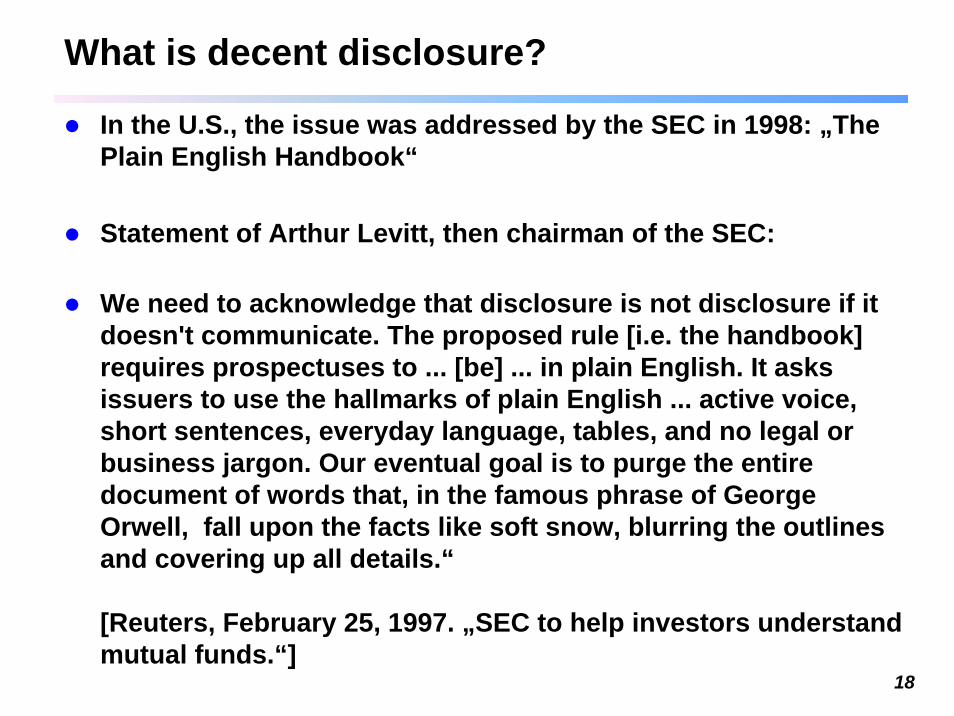

In the U.S., the issue was addressed by the SEC in 1998: „The Plain English Handbook“

Statement of Arthur Levitt, then chairman of the SEC:

We need to acknowledge that disclosure is not disclosure if it doesn't communicate. The proposed rule [i.e. the handbook] requires prospectuses to ... [be] ... in plain English. It asks issuers to use the hallmarks of plain English ... active voice, short sentences, everyday language, tables, and no legal or business jargon. Our eventual goal is to purge the entire document of words that, in the famous phrase of George Orwell, fall upon the facts like soft snow, blurring the outlines and covering up all details.“

[Reuters, February 25, 1997. „SEC to help investors understand mutual funds.“]

19

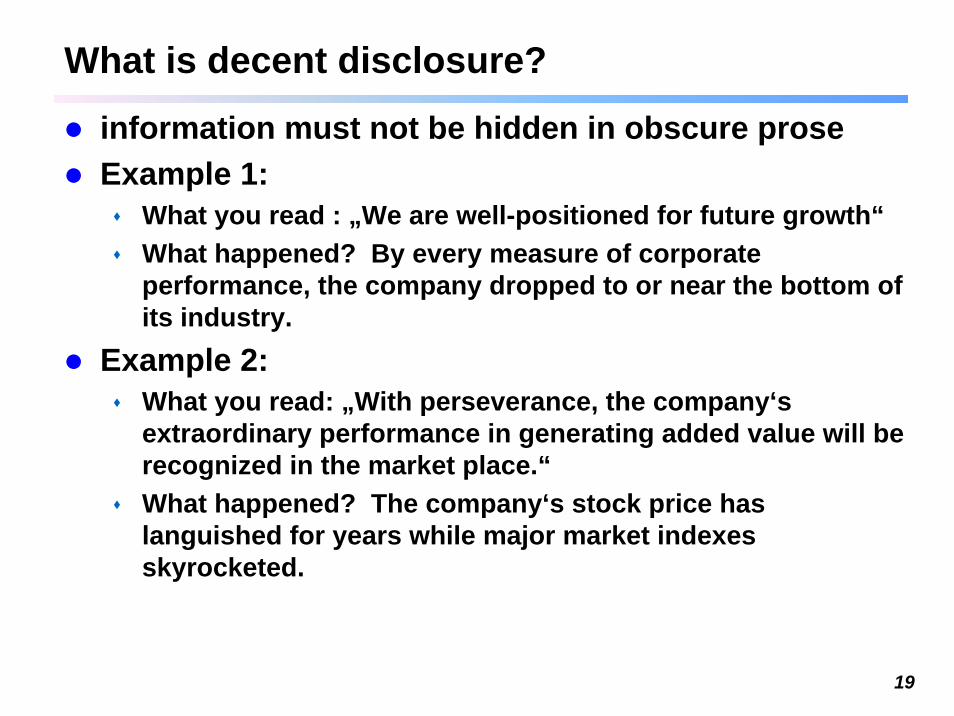

What is decent disclosure?

information must not be hidden in obscure proseExample 1:

What you read : „We are well-positioned for future growth“What happened? By every measure of corporate performance, the company dropped to or near the bottom of its industry.

Example 2:What you read: „With perseverance, the company‘s extraordinary performance in generating added value will be recognized in the market place.“What happened? The company‘s stock price has languished for years while major market indexes skyrocketed.

20

Full disclosure principle – Case studyPorsche AG vs. Deutsche Börse on interim reporting in 2001

sports car manufacturer Porsche got thrown out of the MDax, the German Midcap-Index listing 70 companies, for its reluctance to issue quarterly reports... as the Deutsche Börse AG sees it: "Porsche and Spar are being taken out of the MDAX because the two companies do not publish quarterly reports, which Deutsche Börse requires in the interest of transparency for investors." (press release, 7 August 2001)

... as Porsche sees it: "We feel that quarterly reports are first and foremost a plan to drum up business for Deutsche BörseAG and the banks. … Porsche has always … informed investors … - and this not just every three months. It is therefore not surprising that Porsche, even without ever having submitted quarterly reports, received the Investor Relations Award this May as the MDAX-listed company with the best information sharing policy. … " (press release, 18 July 2001)Who has a point? Do both have a point?

21

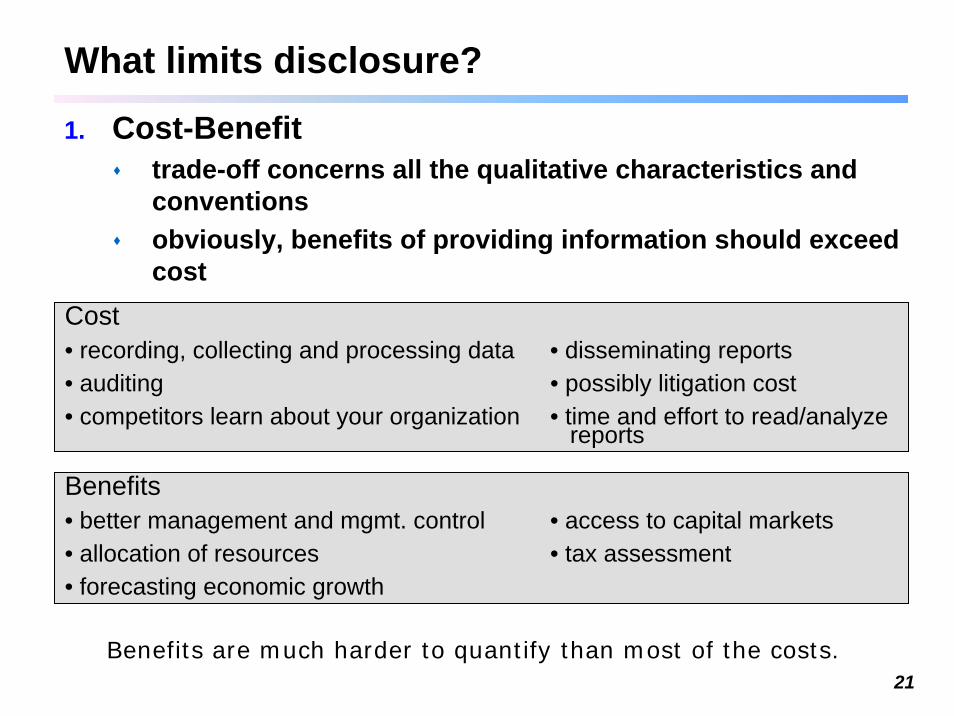

What limits disclosure?

1. Cost-Benefittrade-off concerns all the qualitative characteristics and conventionsobviously, benefits of providing information should exceed cost

Cost• recording, collecting and processing data • disseminating reports• auditing • possibly litigation cost• competitors learn about your organization • time and effort to read/analyze

reports

Benefits• better management and mgmt. control • access to capital markets• allocation of resources • tax assessment• forecasting economic growth

Benefits are much harder to quantify than most of the costs.