Embed Size (px)

Citation preview

Management’s Discussion and Analysis of Financial Results

For the three and six months ended June 30, 2010

Advisories

The following Management’s Discussion and Analysis of Financial Results (MD&A), dated August 4, 2010, should be read in

conjunction with the cautionary statement regarding forward-looking statements below, as well as the unaudited interim

consolidated financial statements and notes thereto as at and for the three and six months ended June 30, 2010 and 2009, and the

consolidated financial statements, notes thereto and MD&A included in the annual report as at and for the years ended December

31, 2009 and 2008. For a detailed description of risks and uncertainties, financial instruments and risk management and critical

accounting estimates, please refer to these respective sections within the 2009 MD&A dated February 16, 2010. The consolidated

financial statements have been prepared in accordance with Canadian generally accepted accounting principles (GAAP). All amounts

in the following MD&A are in Canadian dollars unless otherwise stated. Certain prior-period balances in the consolidated financial

statements have been reclassified to conform to current period’s presentation and policies. References to “WestJet,” “the

Company,” “we,” “us” or “our” mean WestJet Airlines Ltd., its subsidiaries, partnership and special-purpose entities, unless the

context otherwise requires. Additional information relating to WestJet filed with Canadian securities commissions, including periodic

quarterly and annual reports and Annual Information Forms (AIF), is available on SEDAR at www.sedar.com and our website at

www.westjet.com. An additional advisory with respect to the use of non-GAAP measures is set out on page 34 of this MD&A under

the heading “Non-GAAP Measures.”

Cautionary statement regarding forward-looking statements

This MD&A offers our assessment of WestJet’s future plans and operations and contains forward-looking statements as defined

under applicable Canadian securities legislation, including our expectation that WestJet Vacations has the capacity and capabilities

in place to continue to expand, referred to under the heading “Results of Operations – Revenue” on page 10; our expectation that

our commission structure and the added functionalities of WestJet Vacations’ reservation system will allow us to grow the WestJet

Vacations business, referred to under the heading “Results of Operations – Revenue” on page 10; our future destination launches of

seasonal, non-stop service to new destinations, referred to under the heading “Results of Operations – Revenue” on page 10; our

hedging expectations and the intent to hedge anticipated jet fuel purchases, referred to under the heading “Results of Operations –

Aircraft Fuel” on page 13; our sensitivity to changes in crude oil and fuel pricing, referred to under the heading “Results of

Operations – Aircraft Fuel” on page 13; our expectation that our incremental maintenance expense will grow for the remainder of

the year, referred to under the heading “Results of Operations – Maintenance” on page 17; our sensitivity to the change in the

value of the Canadian dollar versus the US dollar, referred to under the heading “Results of Operations – Foreign Exchange” on

page 20; our expected effective tax rate for 2010, referred to under the heading “Results of Operations – Income Taxes” on page

21; our future aircraft deliveries, referred to under the headings “Capital Resources” on page 24 and “Outlook” on page 33; our

assessment that the outcome of legal proceedings in the normal course of business will not have a material effect upon our financial

position, results of operations or cash flows, referred to under the heading “Liquidity and Capital Resources – Contingencies” on

page 25; our assessment of the impact of the transition to international financial reporting standards (IFRS), referred to under the

heading “Accounting – Recent Accounting Pronouncements and Changes” on page 27; our belief that we remain cautiously

optimistic about the second half of 2010, referred to under the heading “Outlook” on page 33; our expectation to see continued

pressure on yield, referred to under the heading “Outlook” on page 33; our anticipation that third quarter RASM will be positive on a

year-over-year basis, referred to under the heading “Outlook” on page 33; our expectation that we will end the year with 91

aircraft, referred to under the heading “Outlook” on page 33; our belief that the Canadian economy needs to rebound further before

it can support more new domestic capacity growth, referred to under the heading “Outlook” on page 33; our plan to deploy most of

the new capacity outside of Canada in the third quarter in order to better match demand with supply, referred to under the heading

“Outlook” on page 33; our expected third quarter and full year capacity increases for 2010, referred to under the heading “Outlook”

on page 33; our expected fuel costs per litre excluding hedging, referred to under the heading “Outlook” on page 33; our

expectation of the impact that settlements of fuel hedging contracts will have on our fuel costs per litre, referred to under the

heading “Outlook” on page 33; our expectation that third quarter CASM excluding fuel and employee profit share will increase,

referred to under the heading “Outlook” on page 33; our expectation of total capital expenditures for 2010, with the majority of the

WestJet Second Quarter 2010│2

spending related to aircraft deposits and rotables, referred to under the heading “Outlook” on page 33; our belief that our enviable

balance sheet and healthy underlying fundamentals will help us control costs and remain profitable during the lingering uncertainty

present in the airline industry, referred to under the heading “Outlook” on page 33; and our expectation about the future success

and profitability of our airline, referred to under the heading “Outlook” on page 33. These forward-looking statements typically

contain the words “anticipate,” “believe,” “estimate,” “intend,” “expect,” “may,” “will,” “should,” “potential,” “plan” or other similar

terms.

Readers are cautioned that our expectations, estimates, projections and assumptions used in the preparation of such information,

although considered reasonable at the time of preparation, may prove to be imprecise and, as such, undue reliance should not be

placed on forward-looking statements. With respect to forward-looking statements contained within this MD&A, we have made the

following key assumptions:

• our expectation that WestJet Vacations has the capacity and capabilities in place to continue to expand, was based on our

current strategic plan;

• our expectation that our commission structure and the added functionalities of WestJet Vacations’ reservation system will

allow us to grow the WestJet Vacations business was based on our current strategic plan;

• our future destination launches of seasonal, non-stop service to new destinations was based on our current and

forecasted commercial schedule;

• our hedging expectations and intent to hedge anticipated jet fuel purchases was based on our current approved hedging

strategy;

• our sensitivity to changes in crude oil and fuel pricing was based on our fuel consumption for our existing schedule and

historical fuel burn, as well as a Canadian-US dollar exchange rate similar to the current market rate;

• our expectation that our incremental maintenance expense will grow for the remainder of the year was based on

regulatory maintenance requirements, forecasts and budgets;

• our sensitivity to the change in the value of the Canadian dollar versus the US dollar was based on forecasted US-dollar

spend for 2010, excluding a percentage of aircraft leasing expense hedged under foreign exchange forward contracts, as

well as the exchange rate for the Canadian dollar similar to the current market rate;

• our expected effective tax rate for 2010 was based on forecasted financial information, tax rates based on current

legislation and expectations about the timing of when temporary differences between accounting and tax bases will

occur;

• our expectation of future aircraft deliveries was based on an aircraft delivery schedule from Boeing;

• our assessment that the outcome of legal proceedings in the normal course of business will not have a material effect

upon our financial position, results of operations or cash flows was based on a review of current legal proceedings by

management and legal counsel;

• our assessment of the impact of transition to IFRS was based on standards adopted by the International Accounting

Standards Board (IASB) thus far and our initial assessment of Canadian GAAP and IFRS differences;

• our belief that we remain cautiously optimistic about the second half of 2010 was based on actual and forecasted

bookings;

• our expectation to see continued pressure on yield was based on actual and forecasted bookings;

• our anticipation that third quarter RASM will be positive on a year-over-year basis was based on actual and forecasted

bookings;

• our expectation that we will end the year with 91 aircraft was based on our aircraft delivery schedule from Boeing;

• our belief that the Canadian economy needs to rebound further before it can support more new domestic capacity growth

was based on recent Canadian GDP forecasts and market commentaries;

• our plan to deploy most of the new capacity outside of Canada in the third quarter in order to better match demand with

supply was based on current forecasts and budgets, financial analysis and strategic plan;

WestJet Second Quarter 2010│3

• our expected third quarter and full year capacity increases for 2010 were based on our actual and forecasted commercial

schedules, as well as additional aircraft to be delivered throughout 2010, as per our revised aircraft delivery schedule

from Boeing;

• our expected fuel costs per litre excluding hedging for the third quarter of 2010 and our expectation of the impact that

settlements of fuel hedging contracts will have on our fuel costs per litre were based on realized jet fuel prices for July

2010 and forward curve prices for August and September 2010, as well as the exchange rate for the Canadian dollar in

the third quarter similar to the current market rate;

• expectation that third quarter CASM excluding fuel and employee profit share will increase was based on current costs

and forecasts;

• our expectation of total capital expenditures for 2010, with the majority of the spending related to aircraft deposits and

rotables, was based on our current budget and forecasts;

• our belief that our enviable balance sheet and healthy underlying fundamentals will help us control costs and remain

profitable during the lingering uncertainty present in the airline industry was based on our preliminary financial analysis

and 2009 financial results; and

• our expectation about the future success and profitability of our airline was based on our past financial results and

experience, as well as our current budget and forecasts.

Our actual results, performance or achievements could differ materially from those expressed in, or implied by, these forward-

looking statements. We can give no assurance that any of the events anticipated will transpire or occur or, if any of them do, what

benefits or costs we will derive from them. By their nature, forward-looking statements are subject to numerous risks and

uncertainties including, but not limited to, the impact of general economic conditions, changing domestic and international industry

conditions, volatility of fuel prices, terrorism, pandemics, currency fluctuations, interest rates, competition from other industry

participants (including new entrants and generally as to capacity fluctuations and the pricing environment), labour matters,

government regulation, stock-market volatility, the ability to access sufficient capital from internal and external sources and

additional risk factors discussed in our AIF and other documents we file from time to time with securities regulatory authorities,

which are available through the Internet on SEDAR at www.sedar.com or our website at www.westjet.com or, upon request,

without charge from us. Additionally, risks and uncertainties are discussed in detail within the 2009 MD&A dated February 16, 2010.

The forward-looking information contained in this MD&A is expressly qualified by this cautionary statement. Our assumptions

relating to the forward-looking statements referred to above are updated quarterly and, except as required by law, we do not

undertake to update any other forward-looking statements.

WestJet Second Quarter 2010│4

Definition of key operating indicators

Our key operating indicators are airline industry metrics, which are useful in assessing the operating performance of an airline.

Flight leg: A segment of a flight involving a stopover, change of aircraft or change of airline from one landing site to another.

Segment guest: Any person who has been booked to occupy a seat on a flight leg and is not a member of the crew assigned to the

flight.

Average stage length: The average distance of a non-stop flight leg between take-off and landing as defined by International Air

Transport Association (IATA) guidelines.

Available seat miles (ASM): A measure of total guest capacity, calculated by multiplying the number of seats available for guest use

in an aircraft by stage length.

Revenue passenger miles (RPM): A measure of guest traffic, calculated by multiplying the number of segment guests by stage

length.

Load factor: A measure of total capacity utilization, calculated by dividing revenue passenger miles by total available seat miles.

Yield (revenue per revenue passenger mile): A measure of unit revenue, calculated as the gross revenue generated per revenue

passenger mile.

Revenue per available seat mile (RASM): Total revenues divided by available seat miles.

Cost per available seat mile (CASM): Operating expenses divided by available seat miles.

Cycle: One flight, counted by the aircraft leaving the ground and landing.

Utilization: Operating hours per day per operating aircraft.

WestJet Second Quarter 2010│5

OVERVIEW

The second quarter of 2010 was once again a profitable quarter for WestJet. We reported our 21st consecutive

quarter of positive net earnings and maintained our strong financial position, as evidenced by one of the healthiest

balance sheets in the North American airline industry. During the period, we increased our revenue by 15.2 per cent

as compared to the second quarter of 2009, and we continued to see improved RASM trends, up four per cent year

over year. The increases in revenue and RASM were primarily a result of strong traffic and load factor, on capacity

growth of nearly 11 per cent from the second quarter of 2009. This marks the first time in eight quarters we have

reported positive year-over-year RASM growth. In particular, we were encouraged by the improvement in yield and

RASM domestically, both positive for the quarter. Additionally, we were pleased with our CASM excluding fuel and

employee profit share performance, which was flat as compared to the second quarter of 2009. Our continued

profitability and delivery of a world-class guest experience were both a direct result of the dedication and effort of

over 7,800 WestJetters.

Quarterly highlights

• Recognized total revenues of $612.1 million for the three months ended June 30, 2010, an increase of 15.2

per cent over the same period of 2009.

• Recorded RASM of 12.80 cents in the second quarter of 2010, up 4.0 per cent from the comparable period

of 2009.

• Increased capacity by 10.9 per cent in the second quarter of 2010, as compared to the same period of

2009.

• Realized CASM of 11.96 cents for the three months ended June 30, 2010, from 11.46 cents in the second

quarter of 2009, an increase of 4.4 per cent.

• Realized CASM excluding fuel and employee profit share of 8.44 cents for the second quarter of 2010, down

0.1 per cent over the same quarter of 2009.

• Recorded an earnings before tax (EBT) margin of 5.4 per cent for the quarter ended June 30, 2010, up 2.8

points from the same quarter in 2009.

• Realized net earnings of $21.0 million in the second quarter of 2010, an increase of 129.7 per cent from the

same period of 2009.

• Realized diluted earnings per share of $0.14 for the three months ended June 30, 2010, an increase of

100.0 per cent compared to the second quarter of 2009.

• Excluding special items, net earnings for the second quarter of 2010 were $23.4 million, or 16 cents per

diluted share, compared to reported net earnings of $9.2 million, or seven cents per diluted share, in the

second quarter of 2009.

• Generated cash flows from operations of $84.8 million for the quarter ended June 30, 2010, an increase

from $25.8 million for the three months ended June 30, 2009.

• Ended the quarter with a cash and cash equivalents balance of $1,108.2 million.

WestJet Second Quarter 2010│6

Please refer to page 34 of this MD&A for a reconciliation of non-GAAP measures, including net earnings and diluted

earnings per share excluding special items and CASM excluding fuel and employee profit share, to the nearest

measure under Canadian GAAP.

Operational highlights2010 2009 Change 2010 2009 Change

ASMs 4,783,649,533 4,314,869,886 10.9% 9,483,168,878 8,671,675,025 9.4%RPMs 3,824,847,258 3,284,898,568 16.4% 7,664,794,818 6,786,827,711 12.9%Load factor 80.0% 76.1% 3.9 pts. 80.8% 78.3% 2.5 pts.Yield (cents) 16.00 16.17 (1.1%) 16.07 16.36 (1.8%)RASM (cents) 12.80 12.31 4.0% 12.99 12.81 1.4%CASM (cents) 11.96 11.46 4.4% 12.16 11.68 4.1%CASM excluding fuel and employee profit share (cents) 8.44 8.45 (0.1%) 8.67 8.48 2.2%Fuel consumption (litres) 232,129,892 207,532,865 11.9% 462,598,271 423,293,745 9.3%Fuel costs per litre (dollars) 0.71 0.62 14.5% 0.70 0.64 9.4%Segment guests 3,752,818 3,417,877 9.8% 7,441,308 6,869,562 8.3%Average stage length (miles) 962 908 5.9% 963 923 4.3%Utilization (hours) 11.5 11.5 - 11.6 11.9 (2.5%)Number of full-time equivalent employees at period end 6,388 6,140 4.0% 6,388 6,140 4.0%Fleet size at period end 89 79 12.7% 89 79 12.7%

Three months ended June 30 Six months ended June 30

We are pleased with our improvements in net earnings and diluted earnings per share as compared to the second

quarter of 2009. For the three months ended June 30, 2010, our RASM increase of 4.0 per cent was more than offset

by a 4.4 per cent increase in CASM, resulting in a slight decline in operating margin. This variance was almost

entirely due to higher year-over-year fuel costs, as the prior period was the lowest point for fuel in 2009. Excluding

fuel and employee profit share, our per unit costs remained relatively flat due to a prudent focus on cost control,

favourable foreign exchange and increase in average stage length, as compared to the second quarter of 2009 and

the first quarter of 2010.

As at June 30, 2010, our cash and cash equivalents balance was $1,108.2 million, an increase of almost $103 million

from December 31, 2009. For the second quarter of 2010, our key ratios remain among the best in the North

American airline industry and continue to improve. Our current ratio, defined as current assets over current liabilities,

remained healthy at 1.46 as compared to 1.48 as at December 31, 2009, and our adjusted debt-to-equity ratio

improved to 1.41 as compared to 1.43 at December 31, 2009. Similarly, our adjusted net debt to earnings before

interest, taxes, depreciation, aircraft rent and other items (EBITDAR) ratio improved by 5.9 per cent to 2.07 as

compared to 2.20 as at December 31, 2009. Please refer to page 34 of this MD&A for a reconciliation of the non-

GAAP measures listed above, including our adjusted debt-to-equity and adjusted net debt to EBITDAR ratios, to the

nearest measure under Canadian GAAP.

During the three months ended June 30, 2010, we increased our fleet size by one aircraft, ending the quarter with

89. With an average age of 4.8 years, we continue to operate one of the youngest fleets of any large North American

commercial airline.

WestJet Second Quarter 2010│7

Subsequent to the second quarter of 2010, we negotiated changes to our future owned aircraft delivery schedule.

These changes have allowed us to defer scheduled delivery of one 700-series owned aircraft from 2011 to 2017, and

two 700-series aircraft from 2012 to 2017 to continue more effectively managing capacity and future growth.

Our second quarter capacity increase, directly attributable to the addition of 10 aircraft since June 30, 2009, was

matched with a corresponding increase in demand for our service. This was evidenced by a load factor of 80.0 per

cent, up 3.9 points from 76.1 per cent in the same quarter of 2009. We are encouraged with our strong load factor,

particularly with our significant quarter-over-quarter capacity growth. Our quarterly load factors for the past eight

quarters are depicted in the following graph.

Quarterly load factor

70%

75%

80%

85%

2008 Q3 2008 Q4 2009 Q1 2009 Q2 2009 Q3 2009 Q4 2010 Q1 2010 Q2

During the first quarter 2010, Delta Air Lines and US Airways requested United States Department of Transportation

(DOT) and Federal Aviation Administration (FAA) approval to complete a slot exchange at New York’s LaGuardia and

Washington’s Reagan National airports. DOT’s response was that Delta and US Airways would be required to dispose

of slots at these airports to new entrant airlines. Of the 20 LaGuardia takeoff and landing slot pairs that Delta was

required to dispose of, WestJet was one of four airlines that secured the option to purchase up to five LaGuardia

airport slot pairs. The transfers were contingent upon regulatory approval and subsequent closing of the separate

transaction between Delta and US Airways. During the second quarter of 2010, the DOT and FAA subsequently

rejected the proposed Delta / US Airways slot transaction with the four new entrant airlines and stipulated that the

slots be made available by auction. As a result, Delta and US Airways do not currently plan to trade slots at

LaGuardia or Reagan National airports. The option was contingent upon the Delta / US Airways transaction being

completed and as such, we no longer have the option to purchase five LaGuardia slot pairs, which differs from our

previously-disclosed statement.

WestJet Second Quarter 2010│8

We continue to evaluate other potential interline and code-sharing partnerships to increase our presence in the U.S.

and international markets. Recently, we reached a major milestone in making our inbound interline agreement with

Cathay Pacific Airways operational. In July we implemented interline capability with Cathay’s wholly-owned subsidiary

Dragon Air, which provides feed from China. We have also recently implemented electronic thru check-in

functionality, which allows guests to check in and receive boarding passes and bag tags for all flight segments from

origin to destination.

SELECTED QUARTERLY UNAUDITED FINANCIAL INFORMATION

Three months endedJun. 30 Mar. 31 Dec. 31 Sept. 30

2010 2010 2009 2009($ in thousands, except per share data)

Total revenues 612,117$ 619,765$ 570,042$ 600,630$ Net earnings 21,029$ 13,800$ 20,175$ 31,418$

Basic earnings per share 0.14$ 0.10$ 0.14$ 0.24$ Diluted earnings per share 0.14$ 0.10$ 0.14$ 0.24$

Three months endedJun. 30 Mar. 31 Dec. 31 Sept. 30

2009 2009 2008 2008($ in thousands, except per share data) Restated Restated

Total revenues 531,163$ 579,285$ 615,783$ 718,375$ Net earnings 9,153$ 37,432$ 42,026$ 57,876$

Basic earnings per share 0.07$ 0.29$ 0.33$ 0.45$ Diluted earnings per share 0.07$ 0.29$ 0.33$ 0.45$

Our business is seasonal in nature with varying levels of activity throughout the year. We experience increased

demand for domestic travel in the summer months (second and third quarters) and more demand for sun

destinations over the winter period (fourth and first quarters). By growing our transborder and international

destinations, we have been able to partially alleviate the effects of seasonality on our net earnings.

Excluding special items, net earnings were $23.4 million for the second quarter of 2010, or 16 cents per diluted

share. Year-to-date net earnings were $40.9 million or 28 cents per diluted share excluding special items, as

compared to $44.3 million or 35 cents per diluted share in the same period of 2009, also excluding special items.

Please refer to page 34 of this MD&A for a reconciliation of non-GAAP measures, including net earnings and diluted

earnings per share excluding special items, to the nearest measure under Canadian GAAP.

WestJet Second Quarter 2010│9

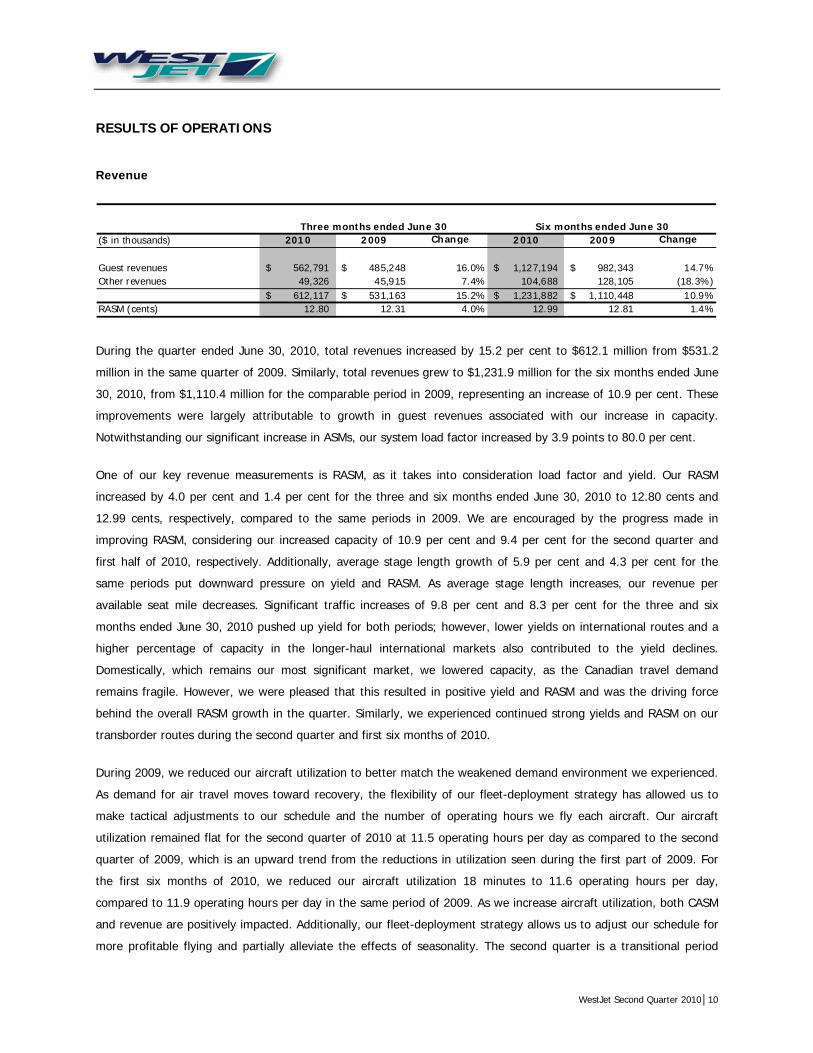

RESULTS OF OPERATIONS

Revenue

($ in thousands) 2010 2009 Change 2010 2009 Change

Guest revenues 562,791$ 485,248$ 16.0% 1,127,194$ 982,343$ 14.7%Other revenues 49,326 45,915 7.4% 104,688 128,105 (18.3%)

612,117$ 531,163$ 15.2% 1,231,882$ 1,110,448$ 10.9%RASM (cents) 12.80 12.31 4.0% 12.99 12.81 1.4%

Three months ended June 30 Six months ended June 30

During the quarter ended June 30, 2010, total revenues increased by 15.2 per cent to $612.1 million from $531.2

million in the same quarter of 2009. Similarly, total revenues grew to $1,231.9 million for the six months ended June

30, 2010, from $1,110.4 million for the comparable period in 2009, representing an increase of 10.9 per cent. These

improvements were largely attributable to growth in guest revenues associated with our increase in capacity.

Notwithstanding our significant increase in ASMs, our system load factor increased by 3.9 points to 80.0 per cent.

One of our key revenue measurements is RASM, as it takes into consideration load factor and yield. Our RASM

increased by 4.0 per cent and 1.4 per cent for the three and six months ended June 30, 2010 to 12.80 cents and

12.99 cents, respectively, compared to the same periods in 2009. We are encouraged by the progress made in

improving RASM, considering our increased capacity of 10.9 per cent and 9.4 per cent for the second quarter and

first half of 2010, respectively. Additionally, average stage length growth of 5.9 per cent and 4.3 per cent for the

same periods put downward pressure on yield and RASM. As average stage length increases, our revenue per

available seat mile decreases. Significant traffic increases of 9.8 per cent and 8.3 per cent for the three and six

months ended June 30, 2010 pushed up yield for both periods; however, lower yields on international routes and a

higher percentage of capacity in the longer-haul international markets also contributed to the yield declines.

Domestically, which remains our most significant market, we lowered capacity, as the Canadian travel demand

remains fragile. However, we were pleased that this resulted in positive yield and RASM and was the driving force

behind the overall RASM growth in the quarter. Similarly, we experienced continued strong yields and RASM on our

transborder routes during the second quarter and first six months of 2010.

During 2009, we reduced our aircraft utilization to better match the weakened demand environment we experienced.

As demand for air travel moves toward recovery, the flexibility of our fleet-deployment strategy has allowed us to

make tactical adjustments to our schedule and the number of operating hours we fly each aircraft. Our aircraft

utilization remained flat for the second quarter of 2010 at 11.5 operating hours per day as compared to the second

quarter of 2009, which is an upward trend from the reductions in utilization seen during the first part of 2009. For

the first six months of 2010, we reduced our aircraft utilization 18 minutes to 11.6 operating hours per day,

compared to 11.9 operating hours per day in the same period of 2009. As we increase aircraft utilization, both CASM

and revenue are positively impacted. Additionally, our fleet-deployment strategy allows us to adjust our schedule for

more profitable flying and partially alleviate the effects of seasonality. The second quarter is a transitional period

WestJet Second Quarter 2010│10

where a large portion of our transborder and international capacity is shifted back into our domestic markets, as

depicted in the following graph.

Charter & scheduled transborder and international as a percentage of total ASMs

0%

5%

10%15%

20%

25%

30%

35%40%

45%

50%

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Jan-10

Feb-10

Mar-10

Apr-10

May-10

Jun-10

During the second quarter of 2010, we adjusted our fare structure with two primary implications: 1) introduction of

lower-value fares that will be available to book across the entire published schedule and 2) the reduction of our full-

price fares at an average of 25 per cent for all flights. The objectives of this restructure were to encourage guests to

purchase flights when they are ready to book, rather than waiting for a seat sale, as well as to provide full-fare

pricing that is better aligned with our brand and increases value to our guests. We have also implemented our first

business traveller segmented-fare product by requiring a seven day advance purchase on deeply-discounted fares.

Less price-sensitive business travellers usually book close to departure and this will preclude them from being able to

book our deeply-discounted fares during the peak business travel booking window. A future addition to our business

fare product will be offering refundability on the highest fares. The full impact of these changes will take time, as

they will require a change in our guest purchase behaviour. We believe this provides most of our guests with value,

while at the same time, allows us to save advertising costs and enhance our inventory management capability.

For the three months ended June 30, 2010, other revenues increased by 7.4 per cent to $49.3 million, versus the

comparable period of 2009. This improvement was driven mainly by a large increase in WestJet Vacations non-air

revenue, offset partially by the termination of our charter agreement with Air Transat, effective May 10, 2009. During

the six months ended June 30, 2010, other revenues were $104.7 million as compared to $128.1 million in the same

period of 2009, representing a decrease of 18.3 per cent. This decline was due to decreased charter revenues as a

result of the Air Transat contract termination. Despite the absence of this charter agreement during the second

quarter and first half of 2010, our strong load factor and traffic growth indicate that our increased capacity is being

profitably absorbed by the market.

WestJet Vacations continued to provide incremental profit in the second quarter and first half of 2010. The launch of

our new WestJet Vacations reservation system in the third quarter of 2009 has contributed to WestJet Vacations’

growth. As the travel agent community uses this system as a distribution arm, WestJet Vacations has the capacity

and capabilities in place to continue to expand. WestJet Vacations’ commission structure continues to receive strong

support from the travel agent trade, and we believe our competitive commission structure contributes to our strong

financial results. This, coupled with the added functionalities of WestJet Vacations’ reservation system, will allow us

WestJet Second Quarter 2010│11

to continue to grow the WestJet Vacations business. As part of our winter schedule, we recently announced future

service to three new destinations. Beginning in November, WestJet and WestJet Vacations will launch seasonal, non-

stop service to New Orleans, Santa Clara (Cuba) and Grand Cayman Island. We now serve a total of 71 destinations

in 13 countries.

Ancillary revenues, which include service fees, onboard sales and partner and program revenue, provide an

opportunity to maximize our profits through the sale of significantly higher-margin goods and services, while also

enhancing our overall guest experience. For the second quarter of 2010, ancillary revenues were $23.2 million,

representing a decrease of 1.1 per cent from the same period of 2009. Ancillary revenue per guest decreased by 10.4

per cent to $6.22 per guest in the second quarter of 2010, from $6.94 in the comparable period of 2009. This decline

was attributable to lower revenue from fees, primarily as a result of lower pre-reserved seating and change and

cancellation fees. The variance in pre-reserved seating fees is mainly due to a shift in distribution methods to more

indirect channels, such as the use of travel agents, with the implementation of our new reservation system. As the

global distribution system (GDS) channel, which is widely used by travel agents, is limited in its ability to sell pre-

reserved seating, this ancillary revenue stream is down year over year. Change and cancellation fees, although down,

are beginning to improve versus the declines seen in the first quarter of 2010.

Ancillary revenues also declined by 8.9 per cent in the six months ended June 30, 2010 to $44.0 million, from $48.3

million in the same period of 2009. As such, ancillary revenue per guest for the year-to-date period in 2010

decreased by 18.2 per cent, to $5.95 versus $7.28 in the comparable period of 2009. The declines for the year-to-

date period was also due to lower fees revenue related to pre-reserved seating, as well as change and cancellation

fees. Subsequent to the cutover to our new reservation system, certain fees, such as change and cancellation, were

temporarily waived in order to accommodate guests during the adjustment to the new system. This was prevalent

during the first quarter of 2010. Now that the reservation system has stabilized, we are returning to normal with

respect to charging fees, and we have seen our ancillary revenue improve over the first quarter of 2010. We have

seen strong year-over-year growth in the sales of onboard food and beverages, driven mainly by our unique

approach to regional food offerings, as well as our improved onboard point-of-sale system.

WestJet Second Quarter 2010│12

Expenses

CASM (cents) 2010 2009 Change 2010 2009 Change

Aircraft fuel 3.44 2.98 15.4% 3.42 3.13 9.3%Airport operations 1.94 1.92 1.0% 2.04 2.03 0.5%Flight operations and navigational charges 1.72 1.75 (1.7%) 1.70 1.70 -Marketing, general and administration 1.01 1.13 (10.6%) 1.03 1.17 (12.0%)Sales and distribution 1.20 0.91 31.9% 1.31 0.93 40.9%Depreciation and amortization 0.70 0.80 (12.5%) 0.70 0.79 (11.4%)Inflight 0.66 0.70 (5.7%) 0.65 0.68 (4.4%)Aircraft leasing 0.73 0.63 15.9% 0.73 0.60 21.7%Maintenance 0.48 0.61 (21.3%) 0.51 0.58 (12.1%)Employee profit share 0.08 0.03 166.7% 0.07 0.07 -

11.96 11.46 4.4% 12.16 11.68 4.1%CASM, excluding fuel and employee profit share 8.44 8.45 (0.1%) 8.67 8.48 2.2%

Three months ended June 30 Six months ended June 30

During the second quarter and first half of 2010, our per unit costs increased, due largely to higher aircraft fuel costs

per ASM, as well as sales and distribution and aircraft leasing expense per ASM, as compared to the same periods in

2009. These variances were offset somewhat by declines in marketing, general and administration, maintenance and

depreciation and amortization expense per ASM. Our CASM excluding fuel and employee profit share declined to 8.44

cents in the second quarter of 2010, representing a decrease of 0.1 per cent over the second quarter of 2009. For

the year-to-date period ended June 30, 2010, our CASM excluding fuel and employee profit share increased by 2.2

per cent. Our focus remains on operating one of the most cost-effective airlines in North America.

Aircraft fuel

Fuel is our most significant cost, representing approximately 29 per cent and 28 per cent of our total operating costs

for the three and six months ended June 30, 2010, respectively. This is an increase from approximately 26 per cent

and 27 per cent for the same periods of 2009. During the second quarter of 2010, our fuel costs per ASM increased

by 15.4 per cent to 3.44 cents, as compared to 2.98 cents in the second quarter of 2009. Similarly, our fuel costs per

ASM increased to 3.42 cents from 3.13 cents for the six months ended June 30, 2010, representing an increase of

9.3 per cent. For both periods in 2010, these unfavourable changes were primarily due to a run-up in US-dollar West

Texas Intermediate (WTI) crude oil prices, offset partially by a stronger Canadian dollar.

Under our fuel price risk management policy, we are permitted to hedge a portion of our future anticipated jet fuel

purchases for up to 36 months, as approved by our board of directors. The policy establishes hedging limits based on

time horizon. Management continuously reviews and adjusts its strategy based on market conditions and

competitors’ positions. Jet fuel is not traded on an organized North American futures exchange, and there are limited

opportunities to hedge directly in jet fuel through the over-the-counter market. Financial derivatives in other crude-

oil-based commodities that are traded directly on organized exchanges, such as crude oil and heating oil, are also

useful in decreasing the risk of volatile fuel prices. During the three and six months ended June 30, 2010, we

purchased Canadian-dollar WTI and jet fuel swaps, call options and collars. The cash premium paid during the three

WestJet Second Quarter 2010│13

and six months ended June 30, 2010 related to the call options and collars was $1.7 million and $2.1 million,

respectively.

As at July 31, 2010, we had a mixture of Canadian-dollar WTI and jet fuel swaps, call options and collars to hedge

approximately 19 per cent (December 31, 2009 – 14 per cent) of our anticipated jet fuel requirements for 2010. The

following tables outline, per type, as at July 30, 2010, the notional volumes per barrel (bbl.) or per gallon (gal.),

along with the weighted average contracted prices.

Notional volumes WTI average strike price WTI average call price Type Year Instrument (bbl.) (CAD$/bbl.) (CAD$/bbl.)WTI 2010 Swaps 185,000 102 -

Call options 130,000 - 92WTI 2011 Call options 330,000 - 97

Notional volumes Jet average strike price Jet average call price Jet average put priceType Year Instrument (gal.) (CAD$/gal.) (CAD$/gal.) (CAD$/gal.)Jet 2010 Swaps 10,850,000 2.27 - -

Call options 1,250,000 - 2.50 -Collars 7,100,000 - 2.47 2.05

Jet 2011 Collars 1,260,000 - 2.50 2.00

As at July 30, 2010, for the period that we are hedged, the closing forward curve for crude oil ranged from

approximately US $79 to US $84 (December 31, 2009 – US $79 to US $84) with the average forward foreign

exchange rate being 1.0334 Canadian dollars to US dollars (December 31, 2009 – 1.0536).

Upon proper qualification, we account for our fuel derivatives as cash flow hedges. Under cash flow hedge

accounting, the effective portion of the change in the fair value of the hedging instrument is recognized in

accumulated other comprehensive loss (AOCL), while the ineffective portion is recognized in non-operating income

(expense). Upon maturity of the derivative instrument, the effective gains and losses previously recognized in AOCL

are recorded in net earnings as a component of aircraft fuel expense.

The following table displays our fuel costs per litre including and excluding fuel hedging for the three and six months

ended June 30, 2010. Please refer to page 34 of this MD&A for a discussion on the use of non-GAAP measures,

including aircraft fuel expense excluding hedging, which is reconciled to GAAP in the table below.

($ in thousands, except per litre data) 2010 2009 Change 2010 2009 Change

Aircraft fuel expense – GAAP 164,450$ 128,677$ 27.8% 324,504$ 271,068$ 19.7%Realized loss on designated fuel derivatives – effective portion (2,460) (7,060) (65.2%) (4,644) (19,034) (75.6%)Aircraft fuel expense, excluding hedging – Non-GAAP 161,990$ 121,617$ 33.2% 319,860$ 252,034$ 26.9%

Fuel consumption (thousands of litres) 232,130 207,533 11.9% 462,598 423,294 9.3%

Fuel costs per litre (dollars) – including hedging 0.71 0.62 14.5% 0.70 0.64 9.4%Fuel costs per litre (dollars) – excluding hedging 0.70 0.59 18.6% 0.69 0.60 15.0%

Three months ended June 30 Six months ended June 30

WestJet Second Quarter 2010│14

Our fuel costs per litre including fuel hedging increased by 14.5 per cent to $0.71 per litre during the second quarter

of 2010, from $0.62 per litre in the same period of 2009. Excluding the effects of the realized loss on fuel derivatives

designated in an effective hedging relationship, our fuel costs per litre were $0.70 for the second quarter of 2010, an

increase of 18.6 per cent from the second quarter of 2009. Similarly, we saw fuel costs per litre including fuel

hedging increase for the six months ended June 30, 2010 by 9.4 per cent compared to the same period in 2009.

Excluding the effects of the realized loss on fuel derivatives designated in an effective hedging relationship, our fuel

costs per litre were $0.69 for the six months ended June 30, 2009.

The following table presents the financial impact and statement presentation of our fuel derivatives on the

consolidated balance sheet as at June 30, 2010 and December 31, 2009:

($ in thousands) Statement presentationJune 30,

2010December 31,

2009

Fair value of fuel derivatives Prepaid expenses, deposits and other 1,664$ -$ Receivable from counterparties for settled fuel contracts Prepaid expenses, deposits and other - 96 Fair value of fuel derivatives Accounts payable and accrued liabilities (4,747) (7,521) Payable to counterparties for settled fuel contracts Accounts payable and accrued liabilities (876) (1,242) Unrealized loss from fuel derivatives AOCL – before tax impact 4,614 6,713

The following table presents the financial impact and statement presentation of our fuel derivatives on the

consolidated statement of earnings for the three and six months ended June 30, 2010 and 2009:

($ in thousands) Statement presentation 2010 2009Realized loss on designated fuel derivatives – effective portion Aircraft fuel (2,460)$ (7,060)$

Gain (loss) on designated fuel derivatives – ineffective portion Gain (loss) on derivatives (558) 4,760

($ in thousands) Statement presentation 2010 2009

Realized loss on designated fuel derivatives – effective portion Aircraft fuel (4,644)$ (19,034)$

Gain on designated fuel derivatives – ineffective portion Gain (loss) on derivatives 152 4,843

Three months ended June 30

Six months ended June 30

During the three and six months ended June 30, 2010, we cash-settled fuel derivatives in favour of the

counterparties of $2.4 million and $4.7 million, respectively (three and six months ended June 30, 2009 – $7.2 million

and $21.3 million, respectively).

The estimated amount reported in AOCL that is expected to be reclassified to net earnings as a component of aircraft

fuel expense when the underlying jet fuel is consumed during the next 12 months is a loss before tax of $4.6 million.

For 2010, excluding the impact of fuel hedging, we estimate our sensitivity to changes in crude oil to be

approximately $6 million annually to our fuel costs for every one US-dollar change per barrel of WTI crude oil.

Additionally, we estimate our sensitivity to changes in fuel pricing to be approximately $9 million for every one-cent

change per litre of fuel.

WestJet Second Quarter 2010│15

Sales and distribution

Sales and distribution encompasses a wide variety of expenses, including travel agency commissions and incentives,

credit card settlement fees, GDS fees, transaction fees related to our new reservation system, costs of our call

centres, as well as sales and distribution costs associated with WestJet Vacations. During the second quarter of 2010,

our sales and distribution expenses per ASM increased to 1.20 cents, up 31.9 per cent from 0.91 cents in the same

quarter of 2009. Approximately 40 per cent of this increase relates to the growth of WestJet Vacations. The nature of

this product generates higher sales and distribution expenses, as sales are predominantly sourced through indirect

channels, such as the use of travel agents. The balance of the increase relates to costs associated with our new

reservation system, such as reservation system transaction fees and higher GDS fees due to an increased use of

indirect sales channels. We saw a similar increase for the first half of 2010 to 1.31 cents from 0.93 cents in the

comparable period of 2009, representing a change of 40.9 per cent. The year-to-date variance was also driven by

certain transition costs associated with the reservation system implementation, including incremental staffing in the

call centre and certain one-time costs, such as the outsourcing of our call centre operations due to higher-than-

normal call volumes and wait times.

Aircraft leasing

Our most significant infrastructure cost is aircraft. During the second quarter of 2010, we assumed delivery of one

leased 737-800 aircraft. This brings our total leased aircraft to 36 as at June 30, 2010, and represents approximately

40 per cent of our total fleet. At the end of the second quarter of 2009, we had a total of 26 aircraft under operating

leases, representing approximately 33 per cent of our total registered fleet.

Our aircraft leasing costs per ASM increased by 15.9 per cent in the second quarter of 2010 to 0.73 cents, from 0.63

cents in the same period of 2009. This variance related primarily to incremental leasing costs on 10 additional leased

aircraft delivered since the end of the second quarter of 2009. For the six months ended June 30, 2010, our aircraft

leasing costs per ASM were 0.73 cents, an increase of 21.7 per cent from the first half of 2009. This increase was

comprised primarily of incremental leasing costs on 10 additional leased aircraft since the end of the second quarter

of 2009, and a full period of aircraft leasing costs for three leased aircraft delivered in the first half of 2009.

We consider aircraft ownership costs to include aircraft leasing, depreciation and amortization and interest expense,

and when combined, our per-unit expenses associated with aircraft ownership declined for the three and six months

ended June 30, 2010 as compared to the same periods in the prior year.

As our aircraft leasing payments are denominated in US dollars, favourable foreign exchange movements partially

offset the increases in aircraft leasing costs for both periods. Additionally, we have an active foreign exchange

hedging program to offset our US-dollar-denominated aircraft lease payments on the majority of our leased aircraft.

Please refer to Results of Operations – Foreign Exchange on page 20 of this MD&A for further information.

WestJet Second Quarter 2010│16

Marketing, general and administration

Marketing largely consists of expenses such as advertising and promotions and live satellite television licensing fees.

General and administration costs consist of our corporate office departments, professional fees, insurance costs and

transaction costs related to aircraft acquisitions. During the second quarter of 2010, our marketing, general and

administration charge per ASM decreased by 10.6 per cent to 1.01 cents, compared to 1.13 cents in the same period

of 2009. This decrease was attributable to lower consulting costs incurred during the second quarter of 2010 as

compared to the same period in 2009, primarily associated with the implementation of our new reservation system.

This was partially offset by revisions to the calculation of capital taxes, based on the estimated impacts of changes to

our provincial income allocation, resulting in an increase of $1.2 million. Similarly, our year-to-date per unit

marketing, general and administration charge declined to 1.03 cents from 1.17 cents in the comparable period of

2009, a decrease of 12.0 per cent. In addition to lower information technology consulting costs, this variance was

also driven by lower year-over-year costs associated with future travel credits awarded to each of our WestJetters.

This was partially offset by costs of $4.1 million relating to our former CEO’s departure during the first quarter of

2010. Although relatively comparable on a total dollar basis for both second quarter and first half of 2010, marketing,

general and administration expense benefited from ASM dilution for both periods.

Maintenance

Our maintenance costs per ASM were 0.48 cents in the second quarter of 2010, representing a decrease of 21.3 per

cent from 0.61 cents in the second quarter of 2009. For the three months ended June 30, 2010, approximately 40

per cent of the decrease was attributable to the stronger Canadian dollar, as approximately 45 per cent of our

maintenance costs were denominated in US dollars. Additionally, we received proceeds from an insurance claim

resulting from a damaged engine during the second quarter of 2010, for which the maintenance expense was

recorded in the first quarter of 2010, also contributing to the favourable variance for the quarter. Our year-to-date

maintenance costs per ASM decreased by 12.1 per cent to 0.51 cents from 0.58 cents in the first half of 2009, largely

driven by the dilutive impact of our increased capacity. We expect our incremental scheduled maintenance expense

to grow for the remainder of the year, as three aircraft are scheduled to undergo their first major overhauls in 2010.

WestJet Second Quarter 2010│17

Compensation

Our compensation philosophy is designed to align corporate and personal success. We have designed a

compensation plan whereby a portion of our expenses are variable and are tied to our financial results. Our

compensation strategy encourages employees to become owners in WestJet, which inherently creates a personal

vested interest in our financial results and accomplishments.

($ in thousands) 2010 2009 Change 2010 2009 Change

Salaries and benefits 110,677$ 97,980$ 13.0% 223,576$ 196,804$ 13.6%Employee share purchase plan 13,039 11,600 12.4% 25,388 22,691 11.9%Employee profit share 3,898 1,185 228.9% 6,213 6,902 (10.0%)Stock option plan 3,437 2,872 19.7% 5,971 5,318 12.3%Key employee and pilot plan 509 - N/A 509 - N/AExecutive share unit plan 200 277 (27.8%) 2,951 466 533.3%

131,760$ 113,914$ 15.7% 264,608$ 232,181$ 14.0%

Three months ended June 30 Six months ended June 30

Salaries and benefits

Salaries and benefits are determined via a framework of job levels based on internal experience and external market

data. During the second quarter of 2010, salaries and benefits increased by 13.0 per cent to $110.7 million from

$98.0 million in the same period of 2009, due primarily to higher pilot salaries and benefits resulting from the new

pilot agreement effective July 1, 2009 and annual market and merit increases. For the six months ended June 30,

2010, salaries and benefits were $223.6 million as compared to $196.8 million in the comparable period of the prior

year, representing an increase of 13.6 per cent. The increase for the year-to-date period was due primarily to higher

pilot salaries and benefits as discussed previously; a cash payout of $1.5 million relating to our former CEO’s

departure from the Company in the first quarter of 2010; incremental salary costs associated with the challenges

posed by the reservation system implementation; and annual market and merit increases. Salaries and benefits

expense for each department is included in the respective department’s operating expense line item.

Employee share purchase plan (ESPP)

Our ESPP encourages employees to become owners of WestJet shares. Under the terms of the ESPP, WestJetters

may acquire voting shares of WestJet at the current fair market value, and these acquisitions will be matched by us

up to a maximum of 20 per cent of their gross pay. As at June 30, 2010, 84 per cent of our eligible active employees

participated in the ESPP, contributing an average of 13 per cent. During the quarter ended June 30, 2010, we

matched contributions for every dollar contributed by our employees. For the quarter ended June 30, 2010, our

matching expense was $13.0 million, a 12.4 per cent increase from the same period of 2009. Similarly, our matching

expense grew by 11.9 per cent for the six months ended June 30, 2010, compared to the same period of 2009, to

$25.4 million from $22.7 million, respectively. The additional expense for both periods was driven primarily by an

increase in salary expense, as well as a greater number of participating WestJetters in the ESPP versus last year.

WestJet Second Quarter 2010│18

Employee profit share

All employees are eligible to participate in the employee profit sharing plan. As the profit share system is a variable

cost, employees receive larger awards when we are more profitable. Conversely, the amount distributed to

employees is reduced and adjusted in less profitable periods. Our profit share expense for the quarter ended June

30, 2010 was $3.9 million, a 228.9 per cent increase from the same quarter of 2009. This increase was directly

attributable to higher earnings eligible for profit share. For the six months ended June 30, 2010, our profit share

expense decreased by 10.0 per cent to $6.2 million, as compared to the first half of 2009. This decline was due to

lower earnings eligible for profit share during this period.

Stock option plan

Stock-based compensation expense related to stock options for the quarter ended June 30, 2010, was $3.4 million,

representing an increase of 19.7 per cent over the second quarter of 2009, due primarily to additional grants over

the prior year, as well as the effect of a new retirement policy, effective July 3, 2009, which resulted in a greater

number of employees being eligible for retirement than under our previous policy. Under our accounting policy for

stock-based compensation, for any employees eligible to retire during the vesting period of the award, the

compensation expense is recognized over the period from the grant date to the retirement eligibility date. In

instances where an employee is eligible to retire on the grant date of the stock-based award, compensation expense

is recognized immediately. For the six months ended June 30, 2010, stock-based compensation expense related to

stock options was $6.0 million, an increase of 12.3 per cent from the comparable period of 2009. This increase in

stock option expense for the year-to-date period related primarily to the accelerated expense of $0.3 million resulting

from our former CEO’s departure from the Company, as well as the effect of the new retirement policy. Stock-based

compensation expense related to pilots’ options is included in flight operations and navigational charges, while the

expense related to senior executives’ and certain non-executive employees’ options is included in marketing, general

and administration expense.

Key employee and pilot (KEP) restricted share unit plan

During the second quarter of 2010, a new stock-based compensation plan was approved by our shareholders, the

key employee and pilot restricted share unit plan, whereby restricted share units (RSUs) are issued to key employees

and pilots. The fair market value of the RSUs at the time of grant is equal to the weighted average trading price of

our voting shares for the five trading days immediately preceding the grant date. Each RSU entitles the employee to

receive payment upon vesting in the form of voting shares. The RSUs time vest at the end of a two or three-year

period, with compensation expense being recognized in net earnings on a straight-line basis over the vesting period.

The Corporation has the option to settle the RSUs through the purchase of voting shares on the open market or to

issue new shares from treasury up to a maximum of 1,000,000. For both the second quarter and first half of 2010,

$0.5 million in compensation expense was recognized in relation to the KEP plan.

WestJet Second Quarter 2010│19

Executive share unit (ESU) plan

We have an equity-based ESU plan, whereby RSUs and performance share units (PSUs) may be issued to our senior

executive officers. For the three months ended June 30, 2010, $0.2 million in compensation expense was recognized

in relation to the ESU plan, a decrease from $0.3 million in compensation expense recognized in the same quarter of

2009. This decrease was primarily attributable to revised probabilities for attaining growth rate targets for the PSUs.

For the first half of 2010, compensation expense for the ESU plan was $3.0 million, an increase of 533.3 per cent

from the comparable period of 2009. This increase mainly resulted from the acceleration of expense of $2.3 million

due to our former CEO leaving the Company, as well as revised probabilities for the PSUs. Stock-based compensation

expense related to the ESU plan is included in marketing, general and administration expense.

Foreign exchange

The gain or loss on foreign exchange included in our consolidated statement of earnings is mainly attributable to the

effect of the changes in the value of our US-dollar-denominated net monetary assets. As at June 30, 2010, US-dollar-

denominated net monetary assets totalled approximately US $73.7 million (December 31, 2009 – US $19.9 million)

and consist mainly of US-dollar cash and cash equivalents and security deposits on various leased and financed

aircraft, US-dollar accounts payable and accrued liabilities and our US-dollar long-term debt facility signed in the

fourth quarter of 2009. We hold US-denominated cash and short-term investments to reduce the foreign currency

risk inherent in our US-dollar expenditures. We reported foreign exchange gains of $6.0 million and $2.1 million for

the three and six months of 2010, respectively, on the revaluation of our US-dollar net monetary assets. This

compares to foreign exchange losses of $9.0 million and $4.4 million during the same three and six month periods,

respectively, in the prior year.

We periodically use financial derivatives to manage our exposure to foreign exchange risk. As at June 30, 2010, we

are entered into foreign exchange forward contracts for US $10.4 million per month for the period of July 2010 to

April 2011, for a total of US $103.7 million at a weighted average contract price of 1.0323 per US dollar to offset a

portion of our future US-dollar-denominated aircraft lease payments. Upon proper qualification, we designated the

forward contracts as effective cash flow hedges for accounting purposes. Upon maturity of the derivative instrument,

the effective gains and losses previously recognized in AOCL are recorded in net earnings as a component of aircraft

leasing expense. As at June 30, 2010, no portion of the forward contracts was considered ineffective.

As at June 30, 2010, the fair value of the forward contracts was $3.4 million, included in prepaid expenses, deposits

and other, and $0.005 million recorded in accounts payable and accrued liabilities (December 31, 2009 – $1.0

million). For the three and six months ended June 30, 2010, we realized a loss before tax on forward contracts of

$1.1 million and $1.5 million, respectively, (three and six months ended June 30, 2009 – gain of $2.3 million and

$5.6 million, respectively) included in net earnings as an increase to aircraft leasing expense. The estimated amount

reported in AOCL that is expected to be reclassified to net earnings as a component of aircraft leasing expense in the

next 12 months is a gain before tax of $3.4 million. The fair value of the foreign exchange forward contracts is

measured based on the difference between the contracted rate and the current forward price obtained from the

counterparty, which can be observed and corroborated in the marketplace.

WestJet Second Quarter 2010│20

For 2010, including the impact of foreign exchange hedging, we estimate that every one-cent change in the value of

the Canadian dollar versus the US dollar will have an approximate $8 million impact on our annual operating costs

(approximately $6 million for fuel and $2 million related to other US-dollar-denominated expenses).

Income taxes

Our operations span several Canadian tax jurisdictions, subjecting our income to various rates of taxation. As such,

the computation of the provision for income taxes involves judgments based on the analysis of several different

pieces of legislation and regulation.

Our effective consolidated income tax rates for the three and six months ended June 30, 2010 were 36.1 per cent

and 35.4 per cent, respectively, as compared to 33.3 per cent and 27.4 per cent for the same periods in 2009. The

increase in our effective tax rate for the three-month period ended June 30, 2010 was primarily due to revisions to

the valuation of our future income tax liability based on the estimated impacts of changes to our provincial income

allocation, resulting in an increase of future income tax expense of $1.5 million. The year-to-date variance was driven

primarily by the same issue, in addition to the acceleration of non-deductible stock-based compensation expense,

resulting mainly from the departure of our former CEO, which resulted in future income tax expense being greater

than expected by an additional $0.7 million.

Excluding these non-recurring items, the effective consolidated income tax rate for the first half of 2010 would have

been 31.2 per cent, which is more in line with expectations of 29 to 31 per cent previously set for the year.

Guest experience

As an airline, we are focused on meeting the needs of our guests while maintaining the highest safety standards. We

are committed to delivering a positive guest experience during every aspect of our service, from the time the flight is

booked to completion of the flight. During the second quarter of 2010, we expanded our self-service options to

include self-serve baggage tagging, to be rolled out to many Canadian airports within the next year.

Key operating performance indicators

On-time performance and completion rates are calculated based on the U.S. Department of Transportation’s

standards of measurement for the North American airline industry. Our bag ratio represents the number of delayed

or lost baggage claims made per 1,000 guests.

2010 2009 Change 2010 2009 Change

On-time performance 81.1% 89.5% (8.4 pts.) 77.0% 80.7% (3.7 pts.)Completion rate 99.3% 99.4% (0.1 pts.) 98.9% 98.5% 0.4 pts.Bag ratio 3.02 2.54 (18.9%) 3.59 3.47 (3.5%)

Three months ended June 30 Six months ended June 30

WestJet Second Quarter 2010│21

On-time performance, indicating the percentage of flights that arrived within 15 minutes of their scheduled time, is a

key factor in measuring our guest experience. During the second quarter of 2010, our on-time performance declined

by 8.4 points, due to several factors, such as more significant operational-impacting weather instances versus 2009

in our largest four airports, as well as our mid-range to small operation cities; a NAV CANADA inbound traffic control

program initiated in the second quarter; higher aircraft servicing delay minutes; and a network continually growing in

complexity. For the six months ended June 30, 2010, our on-time performance declined by 3.7 points due mainly to

harsher weather events versus the same period of the prior year.

Our completion rates remained relatively flat for both the second quarter and first half of 2010 at 99.3 per cent and

98.9 per cent, respectively, as compared to the same periods in 2009. This indicator represents the percentage of

flights completed from flights originally scheduled.

We also saw declines in our bag ratio for the second quarter and first half of 2010, as compared to the same periods

in the prior year.

LIQUIDITY AND CAPITAL RESOURCES

The airline industry is highly sensitive to unpredictable circumstances, and as such, maintaining a strong financial

position is imperative to an airline’s success. We continued to maintain one of the most favourable balance sheets in

the airline industry in 2010, and we produced our 21st consecutive quarter of profitability in the second quarter of

2010.

We ended the quarter with a significant cash and cash equivalents balance of $1,108.2 million, compared to $1,005.2

million as at December 31, 2009. Part of our cash and cash equivalents balance relates to cash collected with respect

to advance ticket sales, for which the balance at June 30, 2010, was $325.7 million, as compared to $286.4 million at

December 31, 2009. Typically, we have cash and cash equivalents on hand to have sufficient liquidity to meet our

liabilities when due, under both normal and stressed conditions. As at June 30, 2010, we had cash on hand of 3.40

(December 31, 2009 – 3.51) times the advance ticket sales balance. Our cash and cash equivalents balance as at

June 30, 2010 was approximately 46 per cent of our trailing 12 months of revenues, and our current ratio was 1.46

at the end of the quarter. These ratios are indicative of our healthy balance sheet and liquidity.

Credit risk associated with cash and cash equivalents is minimized substantially by ensuring that these financial

assets are invested primarily in debt instruments with highly-rated financial institutions. As at June 30, 2010, we have

not been required to post collateral with respect to any of our outstanding derivative contracts.

We monitor capital on a number of measures, including adjusted debt-to-equity and adjusted net debt to EBITDAR

ratios. These ratios are among the best in the North American airline industry and continue to improve. Our adjusted

debt-to-equity ratio improved by 1.4 per cent to 1.41 as at June 30, which included $906.4 million in off-balance-

sheet aircraft operating leases. This compared favourably to our adjusted debt-to-equity ratio of 1.43 at December

31, 2009, mainly attributable to the increase in adjusted shareholders’ equity proportionately offsetting the increase

in our off-balance-sheet aircraft lease financing. As at June 30, 2010, our adjusted net debt to EBITDAR ratio

WestJet Second Quarter 2010│22

improved by 5.9 per cent to 2.07, compared to 2.20 as at December 31, 2009, due primarily to the increase in our

cash and cash equivalents more than offsetting the slight decrease in EBITDAR. Both of these ratios met our internal

targets for June 30, 2010 and December 31, 2009, of an adjusted debt-to-equity measure and an adjusted net debt

to EBITDAR ratio of no more than 3.00.

Operating cash flow

We continued to generate positive cash flows from operations to fund our working capital requirements. In the

second quarter of 2010, cash flow from operations increased to $84.8 million, from $25.8 million for the same period

of 2009, representing an increase of 228.7 per cent. Increased cash flow from operations for the second quarter of

2010 related primarily to increases in net earnings and non-cash working capital due to a higher advance ticket sales

balance, offset somewhat by decreases in accounts payable and accrued liabilities and non-refundable guest credits

balances, versus the amounts as at March 31, 2010. Similarly, cash flow from operations increased by 73.1 per cent

for the six months ended June 30, 2010, to $210.0 million, from $121.3 million in the comparable period of 2009.

Cash flow from operations for the year-to-date period of 2010 related mainly to non-cash working capital due to

higher advance ticket sales and accounts payable and accrued liabilities balances, versus the amounts as at

December 31, 2009.

Financing cash flow

For the second quarter of 2010, our total cash flow used in financing activities was $44.1 million, primarily used

toward repayments of long-term debt. During the same quarter of 2009, our cash flow used in financing activities

was $42.7 million, consisting substantially of long-term debt repayments. Our financing cash outflows of $88.9 million

in the first half of 2010 consisted primarily of $85.5 million in long-term debt repayments, as well as deposits relating

to future leased aircraft. In the comparable period of 2009, our financing cash outflows of $84.3 million consisted

primarily of $83.1 million in long-term debt repayments, largely relating to our aircraft.

We have grown through aircraft acquisitions financed by low-interest-rate debt supported by the Export-Import Bank

of the United States (Ex-Im Bank). The loan guarantees from the U.S. government represent approximately 85 per

cent of the purchase price of these aircraft. The cumulative number of aircraft financed with Ex-Im Bank loan

guarantees is 52, with an outstanding debt balance of $1.1 billion associated with those aircraft. All of this debt has

been financed in Canadian dollars at fixed interest rates, thus eliminating all future foreign exchange and interest-

rate exposure on these US-dollar aircraft purchases.

To facilitate the financing of our Ex-Im Bank supported aircraft, we utilize five special-purpose entities (SPEs). We

have no equity ownership in the SPEs; however, we are the beneficiary of their operations. The accounts of the SPEs

have been consolidated in the financial statements.

WestJet Second Quarter 2010│23

Investing cash flow

Cash used in investing activities for the second quarter and first six months of 2010 totalled $12.5 million and $20.0

million, respectively, compared to $75.6 million and $120.7 million in the comparable periods of 2009. During the

three months ended June 30, 2010, our investing activities consisted of $10.0 million in aircraft additions, largely

comprised of deposits paid to Boeing on future owned aircraft deliveries. Additionally, we incurred $2.5 million in

other property and equipment and intangible asset additions. Cash used in investing activities for the second quarter

of 2009 included $57.2 million in aircraft additions, related primarily to the addition of a leased 737-800 aircraft

subsequently purchased from the lessor, as well as deposits on future owned aircraft deliveries. Additionally, we

incurred $18.4 million in other property and equipment additions, mainly related to our new Campus office space. For

the six months ended June 30, 2010, investing activities consisted of $14.8 million in aircraft additions, largely due to

deposits on future owned aircraft. We also incurred $5.2 million in other property and equipment and intangible asset

additions. In the comparable period of 2009, investing activities consisted of $84.2 million in aircraft additions, largely

resulting from the leased aircraft purchase and the conversion to an accelerated deposit schedule with Boeing during

the first quarter of 2009 to mitigate carrying costs. We also incurred $36.5 million in capital spending, mainly

associated with the Campus facility in the same period.

Contractual obligations and commitments

We currently have 36 aircraft under operating leases. We have entered into agreements with independent third

parties to lease five additional 737-700 aircraft and three 737-800 aircraft for terms ranging between eight and 10

years, to be delivered throughout 2010 to 2012. Although the current obligations related to our aircraft operating

lease agreements are not recognized on our balance sheet, we include these commitments in assessing our overall

leverage through our adjusted debt-to-equity and adjusted net debt to EBITDAR ratios. In addition to aircraft, we

have entered into operating leases and commitments for land, buildings, equipment, computer hardware, software

licenses and satellite programming. As at June 30, 2010, our future payments to 2015 and thereafter relating to

operating leases and commitments were $1,520.3 million (US $1,331.9 million), to be funded through our operating

cash flow.

Capital resources

During the second quarter of 2010, we took delivery of one leased 737-800 aircraft, increasing our total registered

fleet to 89 as at June 30, 2010. Subsequent to the second quarter of 2010, we negotiated changes to our fleet plan

with Boeing, as summarized in the revised delivery schedule on the following page. These changes have allowed us

to defer one 700-series owned aircraft from 2011 to 2017, and two 700-series aircraft from 2012 to 2017.

Additionally, under our current fleet plan, we have 32 aircraft leases expiring between 2013 and 2017, each with the

option to renew. This provides us with the flexibility to end 2017 with a fleet size between 103 and 135 aircraft,

dependent on the exercise of the lease renewal options. As at July 31, 2010, we had existing commitments to take

delivery of an additional 45 aircraft, as depicted in the delivery schedule on the following page.

WestJet Second Quarter 2010│24

Leased Owned Total Leased Owned Total Leased Owned Total Leased Owned TotalFleet at December 31, 2009 - 13 13 25 38 63 8 2 10 33 53 86 Fleet at July 31, 2010 - 13 13 27 38 65 10 2 12 37 53 90 Commitments:

2010 - - - - - - 1 - 1 1 - 1 2011 - - - 4 1* 5 1 - 1 5 1 6 2012 - - - - 4* 4 1 - 1 1 4 5 2013 - - - - 6* 6 - - - - 6 6 2014 - - - - 6* 6 - - - - 6 6 2015 - - - - 10* 10 - - - - 10 10 2016 - - - - 8* 8 - - - - 8 8 2017 - - - - 3* 3 - - - - 3 3

Total commitments - - - 4 38 42 3 - 3 7 38 45 Committed fleet as of 2017 - 13 13 31 76 107 13 2 15 44 91 135 *We have an option to convert any of these future aircraft to 737-800s.

Series600s 800s Total fleet700s

As at July 27, 2010, our total purchased aircraft commitment, including amounts to be paid for live satellite television

systems on purchased and leased aircraft, was $1,727.6 million (US $1,667.3 million).

We have a revolving operating line of credit with a syndicate of three Canadian banks available to us. The line of

credit is available for up to a maximum of $80.8 million (December 31, 2009 – $85.0 million), is secured by our

Campus facility and expires in May 2012. The line of credit bears interest at prime plus 0.50 per cent per annum, or a

bankers acceptance rate at a 2.0 per cent annual stamping fee, and is available for general corporate expenditures

and working capital purposes. We are required to pay a standby fee of 15 basis points, based on the average unused

portion of the line of credit for the previous quarter, payable quarterly. As at June 30, 2010, no amounts were drawn

on this facility.

Contingencies

We are party to certain legal proceedings that arise during the ordinary course of business. It is the opinion of

management that the ultimate outcome of these matters will not have a material effect upon our financial position,

results of operations or cash flows.

WestJet Second Quarter 2010│25

Share capital

Our issued and outstanding voting shares, along with voting shares potentially issuable, are as follows:

July 31, 2010 June 30, 2010

Issued and outstanding: Common voting shares 139,717,973 139,677,79 Variable voting shares 5,576,585 5,616,4Total voting shares issued and outstanding 145,294,558 145,294,209

Voting shares potentially issuable: Stock options 8,204,292 8,345,8 RSUs – KEP plan 166,316 166,316 RSUs – ESU plan 147,060 147,060 PSUs – ESU plan 196,074 196,074Total voting shares potentially issuable 8,713,742 8,855,263

Total outstanding and potentially issuable voting shares 154,008,300 154,149,472

0 19

13

Number of shares

Related-party transactions

We have debt financing and investments in short-term deposits with a financial institution that is related through two

common directors, one of whom is also the President and CEO of the financial institution. As at June 30, 2010, total