Embed Size (px)

Citation preview

Full Terms & Conditions of access and use can be found athttps://www.tandfonline.com/action/journalInformation?journalCode=rero20

Economic Research-Ekonomska Istraživanja

ISSN: 1331-677X (Print) 1848-9664 (Online) Journal homepage: https://www.tandfonline.com/loi/rero20

Managers’ perception of the managementaccounting information system in transitioncountries

Justyna Dobroszek, Ewelina Zarzycka, Alina Almasan & Cristina Circa

To cite this article: Justyna Dobroszek, Ewelina Zarzycka, Alina Almasan & CristinaCirca (2019) Managers’ perception of the management accounting information system intransition countries, Economic Research-Ekonomska Istraživanja, 32:1, 2798-2817, DOI:10.1080/1331677X.2019.1655466

To link to this article: https://doi.org/10.1080/1331677X.2019.1655466

© 2019 The Author(s). Published by InformaUK Limited, trading as Taylor & FrancisGroup

Published online: 29 Aug 2019.

Submit your article to this journal

Article views: 269

View related articles

View Crossmark data

Managers’ perception of the management accountinginformation system in transition countries

Justyna Dobroszeka , Ewelina Zarzyckaa , Alina Almasanb andCristina Circab

aFaculty of Management, University of Lodz, Ł�od�z, Poland; bFaculty of Economics and BusinessAdministration, West University of Timisoara, Timisoara, Romania

ABSTRACTThe aim of this study is to investigate the perception of managersfrom transition countries, as regards the management accountinginformation system. The research was conducted between May2015 and March 2016 among businesses operating in Poland andRomania. The data were processed by means of cluster analysis.The findings indicate that the financial information used in oper-ational management is highly rated by managers. Of the threeprofiles of managers distinguished, those defined as supportersand neutrals dominate in both countries.

ARTICLE HISTORYReceived 16 August 2018Accepted 28 February 2019

KEYWORDSManagement accountinginformation system;manager; perception;transition country

JEL CLASSIFICATIONSM12; M21; M41

1. Introduction

According to the Institute of Management Accountants, management accounting‘involves partnering in management decision making, devising planning and performancemanagement systems, and providing expertise in financial reporting and control to assistmanagement in the formulation and implementation of an organization’s strategy’(Definition of Management Accounting, 2008). Hence, a management accounting infor-mation system (M.A.I.S.) is a major source of information for management and manager-ial decision making (Mia & Chenhall, 1994). This kind of information is provided bymanagement accountants and used by managers operating in different organisations andeconomics (Arsov & Bucevska, 2017). Byrne and Pierce (2007), Fleischman, Walker, andJohnson (2010) and Pierce and O’Dea (2003) emphasised the difference in the perceptionof M.A.I.S. between management accountants and managers. However, how the percep-tion of M.A.I.S. is shaped among managers depending on economic conditions and man-agement accounting development in business organisations can also be investigated.

The objective of the study is to present the perception of M.A.I.S. among Polishand Romanian managers. As a result, three different profiles of managers operatingin the studied companies were distinguished.

CONTACT Justyna Dobroszek [email protected]� 2019 The Author(s). Published by Informa UK Limited, trading as Taylor & Francis Group.This is an Open Access article distributed under the terms of the Creative Commons Attribution License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work isproperly cited.

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA2019, VOL. 32, NO. 1, 2798–2817https://doi.org/10.1080/1331677X.2019.1655466

This empirical study shows not only which management accounting tools (i.e.,whether operational or strategic tools) are used in business, and what type of infor-mation is used in the management process (financial or non-financial information),but also how these aspects are perceived by managers in the decision-making pro-cess. In turn, the separation into three separate profiles may indicate whether furtherprofessional development of managers in the area of management accounting, ororganisational changes in M.A.I.S.s are necessary, for example by increasing access tostrategic decision making. Poland and Romania were chosen for the study becausethey have much in common, for example similarities in the development of theireconomies, including joining the European Union, and, in recent years, the dynamicsof their economic development (Kacprzyk & Dory�n, 2017; The Growth of Polishand Romanian Economy, 2018). These two transition countries were selected becausesuch countries are most often identified with socio-political conditions consisting ofprivatisation, liberalisation of markets, weaker market capital or inefficient bureau-cracy and regulations, and rapid changes (Joseph, 2008). These points have influ-enced the shape of business, for example accounting systems in organisations inPoland and Romania. As emphasised by Anderson and Lanen (1999), the accountingsystem should, as a result of these changes, move towards satisfying the needs ofexternal and internal users, rather than concentrating on traditional bookkeeping,which is a tendency actually shown by both countries. Especially after 1990, andmore intensively after 2000, management accounting has aroused enormous interestin research and business (e.g., Zarzycka, 2016). It is worth noting that the impact ofmarket globalisation, as well as the growth of foreign investments, has made a majorcontribution to the implementation of Western practices in the field of managementin transition countries (Alawattage, Hopper, & Wickramasinghe, 2007).

Previous research findings on the perception of M.A.I.S. refer mainly to developedcountries, where M.A.I.S. is an inseparable part of business practice. Considering theglobalisation processes in economies and accounting, it may be concluded that manage-ment accounting practice has the same dimension in most countries. Grandlund andLukka (1998) stated that the convergence of management accounting practice out-weighs any worldwide divergence processes nowadays. In this context, this study inves-tigates whether this view is valid, not only at the macro but also at the micro level.

The remainder of the paper is organised as follows: the second section includes aliterature review, structured on three relevant topics: M.A.I.S. and its dimension, aperception concept, and management accounting development in transition countries.The literature review is followed by a presentation of the research methodology, aswell as by the description of the study’s findings using cluster analysis. The conclu-sions are presented in the final section.

2. Literature review

2.1. The management accounting information system as a part of themanagement information system

M.A.I.S. in organisations provides data for both management performance and deci-sion making (Grandlund & Lukka, 1998). However, an effective decision requires

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA 2799

high-quality and useful information. The usefulness of management accounting infor-mation for management was characterised by Chenhall and Morris (1986), based ondifferent attributes, which are timeliness, aggregation, integration and scope.

M.A.I.S. should be perceived as a management information system, because man-agement accounting is analysed with reference to the effectiveness of using informa-tion for management, thus improving its efficiency. The user perception of theimportance, usefulness and efficiency of information has already been a topic in themanagement literature (Pierce & O’Dea, 2003). The management information systemhelps managers to reach the targets specified in the given functional area, with aknock-on impact on the goals of the company. Kim (1989) described that these tar-gets can be expressed in terms of decision-making efficiency, performance, interper-sonal relations and job satisfaction. Adeoti-Adekeye (1997) defined four elementscharacterising the management information system: focus on the informationdesigned for the manager in the organisation, structural flow of information, dataintegration as part of the business function in the organisation and reporting. Thesecan be linked to M.A.I.S. and, partly, to the proposal of Chenhall and Morris (1986),especially in the case of data integration and reporting. In turn, Bjørnenak and Olson(1999) indicated that M.A.I.S. can be classified, considering its role and functionalityin the organisation, according to its scope and system.

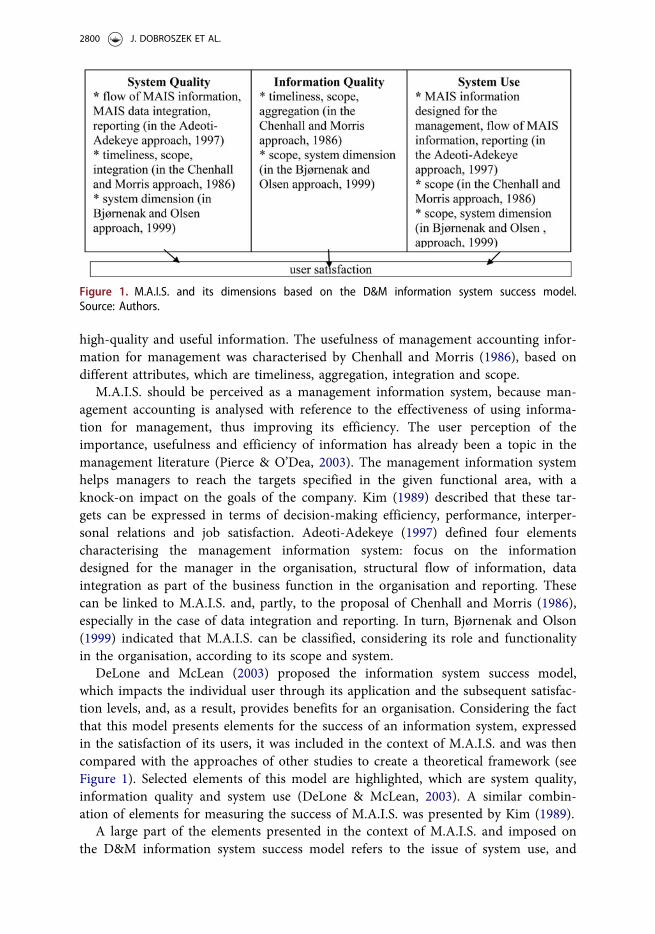

DeLone and McLean (2003) proposed the information system success model,which impacts the individual user through its application and the subsequent satisfac-tion levels, and, as a result, provides benefits for an organisation. Considering the factthat this model presents elements for the success of an information system, expressedin the satisfaction of its users, it was included in the context of M.A.I.S. and was thencompared with the approaches of other studies to create a theoretical framework (seeFigure 1). Selected elements of this model are highlighted, which are system quality,information quality and system use (DeLone & McLean, 2003). A similar combin-ation of elements for measuring the success of M.A.I.S. was presented by Kim (1989).

A large part of the elements presented in the context of M.A.I.S. and imposed onthe D&M information system success model refers to the issue of system use, and

Figure 1. M.A.I.S. and its dimensions based on the D&M information system success model.Source: Authors.

2800 J. DOBROSZEK ET AL.

hence information use by addressees. This perspective can be translated directly intothe satisfaction or dissatisfaction of M.A.I.S. users. However, it should be noted thatboth the acceptable quality assurance of this system and the quality of informationwill have a significant impact on system use, and, as a result, on the perception, satis-faction and assessment of the system’s effectiveness by its users.

Byrne and Pierce (2007), Fleischman et al. (2010), Pierce and O’Dea (2003) andVan der Veeken and Wouters (2002) studied the perception of M.A.I.S. by manage-ment accountants and managers. They pointed to the gap between the informationneeds of managers and the output of management accountants, leading to the emer-gence of conflicts in organisations. This study focuses on the users of M.A.I.S. Theusers’ perspective has already been investigated by Bruns and McKinnon (1993),Simon, Guetzkow, Kozmetsky, and Tyndall (1954), but these studies refer to theentire accounting system and consider only those enterprises operating in highlydeveloped countries, where management accounting is well known in business, aswell as in research and education. Therefore, the findings of the present study regard-ing the situation in transition countries will contribute to the existing managementaccounting literature.

2.2. Perception of the management accounting information system

Cutting (1987) investigated the meaning and nature of the information, as well as themanner in which the information impacts the perceptual system. Information andperception are complementary concepts. Etymologically, to inform means ‘to install aform within’ and, on this basis, perception is understood as installing external ele-ments in the mind of the perceiver (Cutting, 1987). Perception is widely associatedwith thinking (Cutting, 1987).

The subject matter of information and perception finds its foundation in theSocial Perception Theory, because it allows the examination of differences in percep-tion between providers and users (Baron & Byrne, 1991). The theory focuses on howdifferent people perceive others, in particular, in terms of what they see as important(Ristiono & Michalak, 2018). It was also employed to highlight and explain the differ-ences in the perception of information systems between users and providers(Fleischman et al., 2010; Laudon & Laudon, 2006), as well as in the context of theusers themselves (Sadi�c, Pu�skak, & Beganovi�c, 2016).

Perception can be discussed in the contexts of speech perception and visual per-ception (Cutting, 1987).Therefore, it can be stated that the perception of M.A.I.S. bymanagers will depend on interpersonal conditioning, their knowledge, the extent ofmanagers’ influences on decisions, as well as internal features, top-down formal struc-tures and standards (Baron & Byrne, 1991). On the one hand, in the same environ-ment (i.e., with the same specificity) managers may have a similar perception ofM.A.I.S., while on the other hand their individual predispositions (knowledge, educa-tion background, experience) may lead to a different perception.

The perception of M.A.I.S. will translate into the assessment of its usability andvalue (Sadi�c et al., 2016). Whether the information will be highly appreciated dependson whether management accounting and the shared information meet the

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA 2801

expectations of managers. Managers need M.A.I.S. to ensure the accuracy and reliablemeasurement of outcomes. Simon et al. (1954) described that managers use informa-tion for three purposes: problem solving, score carding and attention directing. Thehigher the support for M.A.I.S. in a company, the better the evaluation (positive per-ception) of the usage thereof by managers in terms of the completion of their tasksand achievements; or, in other words, user satisfaction.

The perception of M.A.I.S. by managers may vary depending on different circum-stances, which may include the economy of a given country, the state of managementaccounting practice development and knowledge about management accounting. Inparticular, this may be noticeable in transition countries, in particular, post-trade.

2.3. Management accounting in transition countries

Granlund and Lukka (1998) investigated whether management accounting differsacross countries. Relying on previous research, they pointed out differences resultingfrom economic, cultural and institutional conditions. However, a global harmonisa-tion in management accounting practices at the macro level is observed, though thisrefers only to the main concepts, ideas, techniques, M.A.I.S. designs and goals ofusing management accounting information (Granlund & Lukka, 1998).

Many researchers from transition countries, especially from Central and EastEuropean countries, studying management accounting after 1990, indicated greatinterest in this concept among practitioners, hence its dynamic development inorganisations operating in these geographical areas, for example, Lithuania –Strumickas and Valanciene (2009), Estonia – L€a€ats and Haldma (2012), Poland –Szychta (2008, 2018); Romania – Albu and Albu (2012) and Jinga and Dumitru(2015) or Czech Republic – �Si�ska (2016).

What is specific for management accounting development in transition countries isthe fact that these countries were under Russian control until 1990, at which timemanagement accounting was mainly known as a cost accounting procedure andplayed only a marginal role in state-owned enterprises. From this point on, however,management accounting practice started to develop, especially in Poland, in line withthe Anglo-Saxon and German approach (Szychta & Dobroszek, 2016) and, later, inRomania following the French approach and International Financial ReportingStandards implementation (Feleaga,1996; Jianu & Jianu, 2012).

To assess the usefulness of M.A.I.S. for management in organisations operating inPoland and Romania, it is worth gauging the implementation state of managementaccounting tools and tasks. Traditional tools of management accounting, includingtraditional costs and performance systems (full costing system), operational budgetingand calculation still dominate in business practice in Poland (see Nita, 2014). Ahigher interest in modern methods can be noticed, however, mainly in activity-basedcosting (in Wnuk-Pel, 2014) and target costing, as well as kaizen costing, life cyclecosting or open book accounting (in Szychta, 2008, in press 2018). In the case ofRomania, the empirical study by Glavan, Braescu, Dumitru, Jinga, and Laptes (2007)and Jinga, Dumitru, Dumitrana, and Vulpoi (2010) showed that managers are satis-fied with the financial data from financial accounting to support management. This

2802 J. DOBROSZEK ET AL.

confirms that management accounting does not play an important role there. Albuand Alexe (2009) investigated the use of modern tools of management accounting,such as customer performance analysis, financial and non-financial measures for themanagement of employees and activity-based costing, employed mainly in large andprivate foreign capital.

Despite the findings presented above indicating that M.A.I.S.s are better developedin Poland, in both countries managers use mainly financial information in their man-agerial tasks.

3. Research questions and methodology

3.1. Objective of the study and research questions

The objective of the study was focused on the perception of M.A.I.S. among Polishand Romanian managers. To present the findings, the authors applied elements ofthe D&M information system success model, a perception concept, having an impacton the evaluation of M.A.I.S. and hence on managers’ satisfaction (see Figure 2). Thestudy started from the following research questions:

RQ 1: How do managers perceive the importance of management accountinginformation for management?

RQ 2: How do managers perceive the specific characteristics of the receivedmanagement accounting information in the form of reports?

RQ 3: To what extent do managers use M.A.I.S. for the performance of the indicatedmanagement activities?

RQ 1 covers the quality system, and it can be combined with importance, integra-tion, aggregation or functionality for operational or strategic management. RQ 2 hasbeen assigned to information quality, referring to such elements as accuracy and con-sistency. This applies to data quality, functionality, integration, reliability, and alsocompleteness and relevance. RQ 3 relates to information use, referring to frequencyof use.

The selected theoretical bases, i.e., information system success model, perception,including Social Perception Theory, were aligned with the cluster analysis methodapplied in the empirical section.

Figure 2. Combination of elements of D&M information system success model with RQs.Source: Authors.

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA 2803

3.2. Research methodology

The research data were collected as a result of an empirical study in the form of asurvey, conducted between May 2015 and March 2016, based on randomly selectedbusinesses across various industries operating in Poland and Romania and character-ised by the varied origins of their funding capital. The survey used in the study wasan online questionnaire, structured into four different sections: the first two outlineda brief characterisation of the company, as well as the respondents themselves, thethird section inquired about the existence and form of M.A.I.S. within the companies,while the fourth section included questions meant to capture the perception of themanagers on the information delivered by management accounting. The question-naire consisted of a total of 26 half-open and closed questions. The questionsincluded single- and multiple-choice questions, span and matrix questions. Thesewere based on earlier research conducted on: the purposes for which the informationis used, on the suitability of the information, on the suitability of the informationand on the qualitative characteristics of the information (e.g., Bruns & McKinnon,1992a, 1992b; Chenhall & Morris, 1986; Mendoza & Bescos, 2001; Pierce &O’Dea, 2003).

The questionnaire was sent to managers (mainly operations managers). The com-panies, of various size, were randomly selected for the research. Mostly large andmedium enterprises were included in the analysed sample. However, because of thedifficulties encountered in gathering enough data (explained by the fact that domesticcompanies do not willingly participate in scientific research, while foreign branchesoften need the consent of the headquarters to do so), small companies were alsoincluded in the study, but to a lesser extent than medium and large organisations.

An analysis of the collected questionnaires showed that 154 were completed cor-rectly, providing high-quality data for the analysis. Out of the 154 questionnaires, 116originated from Poland and 38 from Romania. Each questionnaire corresponded toone respondent participating in the study; however, there were cases in which thequestionnaires were completed by different managers from within the same company.The disproportion between the numbers of questionnaires sent shows the slightly bet-ter access to companies from Poland for the researchers.

In order to thoroughly analyse the set of data obtained from the conducted survey,cluster analysis was applied. This method allows for the segregation of the observeddata into specific groups so that the degree of association of certain objects withothers belonging to the same group is as high as possible, while association withobjects from other groups is as low as possible. This tool systematises, to a largeextent, the gathered information into specific structures and, consequently, gives anoverview of the surveyed objects. Cluster analysis is a very commonly used approachin analysing research data collected in sociological, marketing or psychologicalresearch to group specific phenomena or objects, such as consumers, clients, andmanagers (e.g., Khan, Bakkappa, Metri, & Sahay, 2009; Saunders, 1980). Accounting,including management accounting (e.g., Ingram & Margetis, 2010; Nimtrakoon &Tayles, 2015) may also be subjected to grouping. In addition to cluster analysis,descriptive statistics (occurrence frequency of the phenomenon, mean standard devi-ation, variance) were used in the presentation of the findings. For cluster analysis

2804 J. DOBROSZEK ET AL.

purposes, the variables were classified by means of the agglomerative (hierarchical)method, in which Euclidean distance was applied in order to calculate the distancebetween objects, and Ward’s method, considered one of the most efficient, as themethod to combine the objects and classes (Online Manual on Statistics, 2016).

3.3. Research sample

The companies from Poland and Romania involved in the study were mainly manu-facturing enterprises (52%, 61% respectively), with about 30% of the companies beingservice providers, while slightly over 10% were trade companies. Over 60% of the sur-veyed companies from both Poland and Romania could be classified as large in termsof their number of employees. The majority of the companies from Poland andRomania had foreign capital: 42%, 57%, respectively, of the study population. Theprevailing share of foreign capital may indicate that the enterprises participating inthe study were branches of foreign companies. This may have an impact on theM.A.I.S.s dimension, because this system when used in a subsidiary is often based onoperational tools (mainly reporting and budgeting), or on managers’ perception.

The educational level of the surveyed managers should also be noted. Some 98% ofthe Polish managers hold a master’s degree, 40% have completed an MBA and 9%hold a PhD, while 68% of the Romanian managers hold a master’s degree with only13% having an MBA. These results show the slightly higher education level of manag-ers from Poland than for those from Romania. This aspect is significant for the inter-pretation of the findings, since it may have a bearing on the satisfaction andperception of management accounting information. For example, those managerswithout the depth of educational background may not obtain information from mod-ern management accounting tools, as they may not be familiar with theseopportunities.

Among the studied organisations, management accounting tasks were mostly per-formed within a distinct department; yet, the companies often prefer to integratemanagement accountants with employees from other departments. Only two of thePolish companies outsourced management accounting.

4. Findings – managers’ perception of the management accountinginformation system

The cluster analysis and other selected indicators of descriptive statistics (to confirmthe frequency of responses) were used to analyse and present the findings. Takinginto account the similarity of the respondents’ answers in the areas of RQ1, RQ2 andRQ3, the findings were then integrated for Poland and Romania.

4.1. The importance of selected management accounting information – RQ 1

For the analysis, the following variables were taken into account and grouped: finan-cial information (financial results, costs, revenues, financial ratios), budgetary datawith variance analysis and non-financial indicators (on quality, operations, customer

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA 2805

satisfaction, employee satisfaction) (Definition of Management Accounting, 2008).After the first stage of clustering, the variables formed two clusters. The first one wascomposed of financial and budgetary data, while the second includes non-financialindicators and ratios (see Graph 1).

The division shows that the answers of managers in respect of the perceivedimportance of the financial information and budget & variance analysis are in line.These two clusters may indicate two groups of managers, i.e., those applying financialinformation and budgetary data (cluster 1) and those using non-financial indicators(cluster 2) for their tasks. In addition, it may be determined that the perceivedimportance of financial and budgetary data was similar, meaning that if respondentsevaluated the importance of financial information as high, they generally also ratedthe importance of budgetary information and information on variance as high.

The above conclusions are complemented with the results on the grouping of man-agers with the k-means method (where k¼ 3), as shown in Graph 2.

In the classification into three clusters, three divisions are obvious: managers whoperceive and rate the importance of studied variables in their professional work aslow (cluster 2), moderate (cluster 1), and high (cluster 3). Hence, the surveyed man-agers will be classified into sceptics, neutrals and supporters. The differences in theresponses of these three groups are presented in Table 1.

It is worth noting that the size of the first cluster (managers viewing and assessingan importance of studied variables) is the largest (62 persons vs. 20 from the secondcluster and vs. 44 from the first cluster).

4.2. Managers’ perception of specific characteristics of internal reports – RQ 2

The agglomerative method was also used for the cluster analysis in respect of the per-ception of the selected characteristics of M.A.I.S. provided in the form of reports. Forthe purpose of cluster analysis, these characteristics were grouped into four categories

Graph 1. A dendrogram of managers’ perception of the importance of selected information ofmanagement accounting. Source: Authors.

2806 J. DOBROSZEK ET AL.

(quality, content, presentation and comments – see Graph 3). The first category‘quality’ contained an assessment of comprehensibility, clarity and timeliness ofM.A.I.S. ‘Content’ measures satisfaction with the completeness, relevance and thedegree of details. ‘Form of presentation’ focuses on the appraisal of standardisation,graphical presentation and technical tools used to provide information to users.Finally, ‘comments’ evaluates the quality of comments and future references.

After the first stage of clustering, two clusters were formed: quality and content(cluster 1) and presentation of data and comments (cluster 2). The first cluster iscomposed of quality and substantive aspects, since the accuracy and the appropriate

Table 1. The three clusters of managers perceiving and assessing selected managementaccounting information moderately, low or high.Selected management accountinginformation/descriptive statistics

Financialinformation

Non-financialindicators & ratios

Budget & varianceanalysis

Cluster 1 contains 62 cases – (moderate average assessment)Mean 4.210 3.363 3.688Standard-Deviation 0.465 0.436 0.381Variance 0.216 0.190 0.145Cluster 2 contains 20 cases – (low average assessment)Mean 2.567 2.175 2.833Standard-Deviation 0.845 1.004 0.753Variance 0.715 1.007 0.567Cluster 3 contains 44 cases – (high average assessment)Mean 4.591 4.364 4.462Standard-Deviation 0.393 0.394 0.483Variance 0.154 0.155 0.234

Source: Authors.

Graph 2. The grouping of managers with the k-means method in respect of the perception of theimportance of selected management accounting information. Source. Authors.

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA 2807

selection of data are reflected in the quality of the reports. The second cluster isformed by visual and explanatory aspects which create added value to internalreports, facilitating their accurate reading by managers and supporting them in theprocess of ongoing assessment of the business situation and decision making (seeGraph 3).

The Graph 3 confirms that the managers’ perception in respect of such elements asquality and content are similar. Comparable results were obtained in the case of theperception of elements of reports such as presentation and comments. This means thatif managers, based on their perception, rate the quality as high, they also rate the con-tent of the reports as high. In the second group, if managers evaluate the presentationof data (the form) as high, they also rate comments in the internal reports as high.

The higher level of aggregation may suggest a division of the managers into twohomogeneous groups, i.e., the first cluster of managers who perceive the quality andcontent of the reports as high, and the second cluster of managers who perceive thepresentation of data and comments as high. At this point it is possible to divide thesurveyed managers into those who put an emphasis on the traditional aspects ofreports, i.e., their appropriate content and quality – ‘traditionally oriented managers’,and the managers for whom the appropriate form of presentation (e.g., graphs) andcomments are essential – ‘modern managers’.

The above conclusions are complemented with the result of the managers groupingwith the k-means method (where k¼ 3), as shown in Graph 4.

Graph 3. A dendrogram on managers’ perception in terms of the characteristics of M.A.I.S. pro-vided in the form of reports. Source: Authors.

2808 J. DOBROSZEK ET AL.

The division into three clusters indicates the arrangement of the managers intothose who evaluate studied characteristics as low (cluster 3) – sceptics; moderately(cluster 1) – neutrals; or as high (cluster 2) – supporters.

Accurate information on the differences in responses of the three groups seen inGraph 6 is presented in Table 2.

It is worth highlighting that the size of group 1 (65 respondents), making a moder-ate evaluation of the elements of internal reports, differs significantly from the sizesof cluster 2 (38 respondents) and 3 (23 respondents). This means that in the majorityof cases, the managers perceived the analysed characteristics of M.A.I.S. neither ashigh nor low.

Table 2. The three clusters of managers perceiving and assessing selected characteristics ofM.A.I.S. provided in the form of reports moderately, low or high.Characteristics of M.A.I.S. in form reports/Descriptive statistic Quality Content Presentation Comments

Cluster 1 contains 65 cases (moderate average assessment)Mean 3.821 3.826 3.282 2.946Standard-Deviation 0.413 0.453 0.401 0.594Variance 0.170 0.205 0.161 0.353Cluster 2 - Cluster contains 38 cases (high average assessment)Mean 4.474 4.482 4.193 4.118Standard-Deviation 0.385 0.450 0.551 0.499Variance 0.148 0.202 0.304 0.249Cluster 3 - Cluster contains 23 cases (low average assessment)Mean 2.609 2.696 2.319 2.000Standard-Deviation 0.574 0.512 0.607 0.603Variance 0.330 0.262 0.368 0.364

Source: Authors.

Graph 4. The grouping of managers with the k-means method in the context of characteristics ofM.A.I.S. provided in the form of reports. Source: Authors.

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA 2809

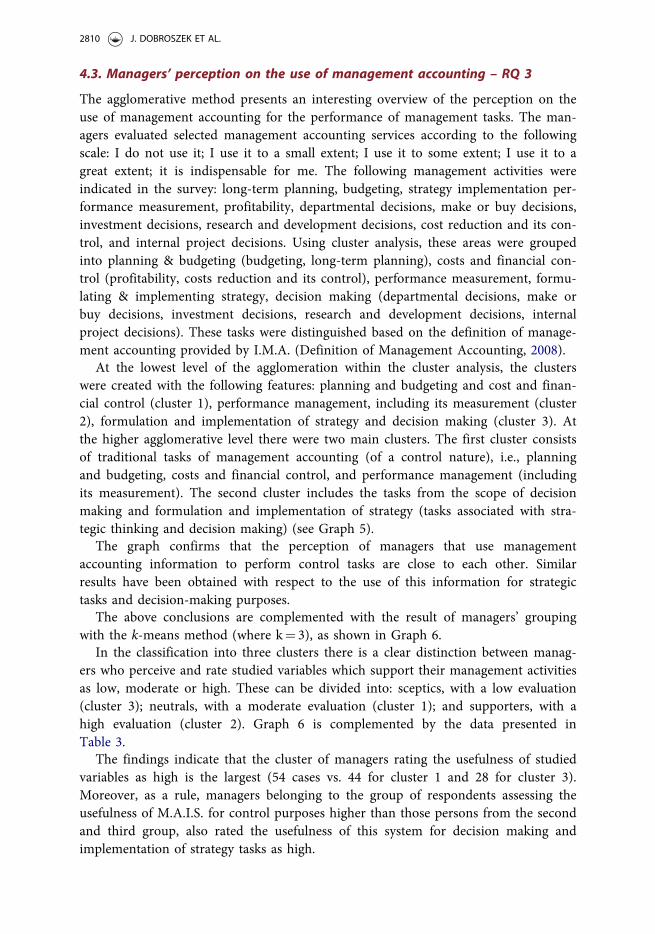

4.3. Managers’ perception on the use of management accounting – RQ 3

The agglomerative method presents an interesting overview of the perception on theuse of management accounting for the performance of management tasks. The man-agers evaluated selected management accounting services according to the followingscale: I do not use it; I use it to a small extent; I use it to some extent; I use it to agreat extent; it is indispensable for me. The following management activities wereindicated in the survey: long-term planning, budgeting, strategy implementation per-formance measurement, profitability, departmental decisions, make or buy decisions,investment decisions, research and development decisions, cost reduction and its con-trol, and internal project decisions. Using cluster analysis, these areas were groupedinto planning & budgeting (budgeting, long-term planning), costs and financial con-trol (profitability, costs reduction and its control), performance measurement, formu-lating & implementing strategy, decision making (departmental decisions, make orbuy decisions, investment decisions, research and development decisions, internalproject decisions). These tasks were distinguished based on the definition of manage-ment accounting provided by I.M.A. (Definition of Management Accounting, 2008).

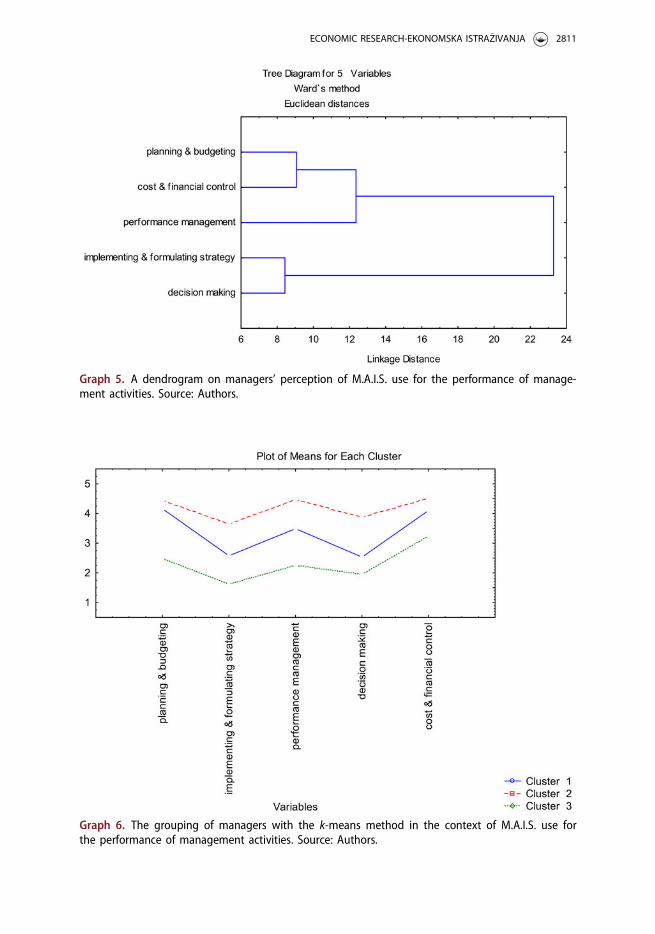

At the lowest level of the agglomeration within the cluster analysis, the clusterswere created with the following features: planning and budgeting and cost and finan-cial control (cluster 1), performance management, including its measurement (cluster2), formulation and implementation of strategy and decision making (cluster 3). Atthe higher agglomerative level there were two main clusters. The first cluster consistsof traditional tasks of management accounting (of a control nature), i.e., planningand budgeting, costs and financial control, and performance management (includingits measurement). The second cluster includes the tasks from the scope of decisionmaking and formulation and implementation of strategy (tasks associated with stra-tegic thinking and decision making) (see Graph 5).

The graph confirms that the perception of managers that use managementaccounting information to perform control tasks are close to each other. Similarresults have been obtained with respect to the use of this information for strategictasks and decision-making purposes.

The above conclusions are complemented with the result of managers’ groupingwith the k-means method (where k¼ 3), as shown in Graph 6.

In the classification into three clusters there is a clear distinction between manag-ers who perceive and rate studied variables which support their management activitiesas low, moderate or high. These can be divided into: sceptics, with a low evaluation(cluster 3); neutrals, with a moderate evaluation (cluster 1); and supporters, with ahigh evaluation (cluster 2). Graph 6 is complemented by the data presented inTable 3.

The findings indicate that the cluster of managers rating the usefulness of studiedvariables as high is the largest (54 cases vs. 44 for cluster 1 and 28 for cluster 3).Moreover, as a rule, managers belonging to the group of respondents assessing theusefulness of M.A.I.S. for control purposes higher than those persons from the secondand third group, also rated the usefulness of this system for decision making andimplementation of strategy tasks as high.

2810 J. DOBROSZEK ET AL.

Graph 5. A dendrogram on managers’ perception of M.A.I.S. use for the performance of manage-ment activities. Source: Authors.

Graph 6. The grouping of managers with the k-means method in the context of M.A.I.S. use forthe performance of management activities. Source: Authors.

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA 2811

4.4. Summary of findings

The application of cluster analysis for the verification of the data enabled the authorsto obtain interesting findings about information and system quality and system usewith reference to M.A.I.S. The selected and studied variables were dependent onmanagers’ perception, and thus their evaluation.

The findings enable the identification of two groups of managers: those traditionallyapplying financial information and budgetary data and those using non-financial indi-cators for managerial tasks. The perception of the selected kinds of information allowedidentification of those managers who use the traditional, financial information, andthose who use the more qualitative information for management processes. It is worthpointing out that non-financial information (including indicators) is more useful in adynamic environment or for companies introducing innovative concepts such as just intime or total quality management (Chenhall, 2006), meaning it is used mainly in devel-oped M.A.I.S. In this scope, managers declared overall moderate and higher levels ofimportance of financial information and budgetary data with variance analysis, while inthe case of non-financial indicators the level is lower. This may confirm the fact thatM.A.I.S.s supporting management processes in companies located in transition coun-tries are less developed. These findings are only partially consistent with Fleischmanet al. (2010), as these authors show that users of management accounting actually placemore emphasis on planning & budgeting and management reporting but rank financialaccounts lower. In addition, Bruns and McKinnon (1992a, 1992b) suggest that manag-ers sometimes consider non-financial indicators more useful than financial ones inorder to make a relevant diagnosis of a situation. However, Pierce and O’Dea (2003)confirm that managers seek traditional types of information. Taking into considerationthe contention of Johnson and Kaplan (1987) that management accounting is domi-nated by the requirements of financial reporting, it is assumed that the researchedmanagers repeat this approach, declaring a high or moderate valuation of the financialdata and revealing their greater satisfaction with it.

This study distinguished the clusters of managers who evaluated managementaccounting information for control tasks as high and those who make such an

Table 3. The three clusters of managers perceiving and assessing M.A.I.S. use moderately, lowor high.MAIS for managementactivities/DescriptiveStatistic

Planning &budgeting

Formulating &implementing

strategyPerformancemanagement

Decisionmaking

Cost &financialcontrol

Cluster 1 contains 44 cases (moderate average assessment)Mean 4.159 2.576 3.489 2.530 4.102Standard-Deviation 0.617 0.636 0.886 0.581 0.625Variance 0.381 0.405 0.785 0.338 0.390Cluster 2 contains 54 cases (high average assessment)Mean 4.444 3.642 4.463 3.877 4.519Standard-Deviation 0.564 0.644 0.522 0.619 0.475Variance 0.318 0.414 0.272 0.383 0.226Cluster 3 contains 28 cases (low average assessment)Mean 2.482 1.631 2.250 1.940 3.232Standard-Deviation 0.855 0.597 0.752 0.667 0.986Variance 0.731 0.357 0.565 0.445 0.972

Source: Authors.

2812 J. DOBROSZEK ET AL.

assessment for the use of this information for decision-making purposes and forstrategy implementation. The number of managers who perceived managementaccounting information for the realisation of studied tasks as high or moderate waslarger than those who perceived it as low. However, the relatively lower assessment ofmanagement accounting information usefulness for decision making and implement-ing strategy is in contrast with the frequently encountered opinion that informationis mainly useful and valuable in the context of decision making (e.g., Chenhall &Morris, 1986), but is in line with Bruns and McKinnon (1992a, 1992b), who statethat managers needing to make decisions search for other sources of information.The research also identified two groups of managers: those satisfied with the qualityand content of the reports and those content with the presentation of the data andcomments. This is in line with Pierce and O’Dea (2003), who pointed to graphic rep-resentation as one of the most unsatisfactory elements of the reports prepared bymanagement accounting departments. Moreover, excessive concentration on financialdata means that information is past-oriented and lacks references to the future. Thus,this decreases the information’s usefulness with regard to operational activities andmanagement processes, as stated by Johnson and Kaplan (1987), thereby leading to alow level of satisfaction among managers. In addition, the same situation occurs inthe case of the comments provided by M.A.I.S., i.e., that they are insufficient andthere is a lack of guidance for the future.

5. Conclusions

The aim of the research was to explore managers’ perception of M.A.I.S. in businessesoperating in transition countries. Taking into account the similarity of the Polish andRomanian respondents’ answers, findings were integrated for Poland and Romaniaand cluster analysis enabled grouping of the integrated data according to similaritiesand thus to present differences between clusters. Based on this, three profiles of man-agers were distinguished: sceptics, neutrals and supporters. The findings show thatperception, and therefore the evaluation of the studied variables, in the context ofM.A.I.S. is different. Clusters of managers who rated M.A.I.S. elements as high, mod-erately and low were distinguished. In the vast majority of cases, the managersassessed the studied variables at a moderate level. This means that they were neithervery satisfied with M.A.I.S. nor dissatisfied. Slight differences were recognised in thecase of RQ 2, where the support cluster had a large size for both countries.

Generally, this study reveals that M.A.I.S.s providing mainly financial informationare used for operational management in Poland and Romania. However, there aresome managers, especially in Poland, who have a better perception of the value ofmodern management accounting methods and tools and their importance for stra-tegic management. The mentioned differences between perception, and thus evalu-ation, of M.A.I.S. between Polish and Romanian managers may result from differentmanagement accounting development in these countries and the influence on themof other countries’ economies. In order to understand managers’ perception ofM.A.I.S., one needs to understand management accounting practice and its develop-ment. The description of this issue in the first section of the article indicated that

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA 2813

management accounting practice is better developed in Poland than in Romania,given the German influence in this area (e.g., more German subsidiaries with man-agement accounting departments). Moreover, this research showed that the studiedPolish managers are slightly better educated than Romanian managers, which mightimpact on their understanding of new solutions (tools, I.T.) of M.A.I.S. However, themore traditional, operational solutions are employed in both countries, owing to thefact that the strategic ones are used in the headquarters located in Germany orFrance, etc.

In addition, three groups of managers have been identified: supporters, scepticsand neutrals. No clear differences have been observed between the manager profiles,in either of the two countries. Most of them react neutrally, meaning they evaluatethe studied M.A.I.S.s as average for their informational needs and management tasks.It can be stated that despite some differences between the two countries with regardto the development of management accounting practice (in Poland because of theinfluence of German businesses, in Romania as a result of I.F.R.S. implementation),the perception of M.A.I.S.s by managers is much the same. The separate groups ofmanagers indicate the avenues of their further development. For example, supportersshould develop their strategic and network management competences using the stra-tegic tools and methods of management accounting. In turn, the sceptics shouldimprove their awareness of know-how of management accounting to find ways forthe better use of available M.A.I.S. for their management tasks in the future. In thecase of the neutrals, use of M.A.I.S. should be developed further, and this group ofmanagers should have greater opportunity to use M.A.I.S. (better access), both foroperational as well as strategic management. In this way they may see the higheradded value of it.

The present study indicated that management accounting practice on the one handaims to homogenise at the macro level, while on the other hand, mainly at the microlevel, it highlights differences between individual countries in this respect.

5.1. Limitation and future research

This study makes a contribution to the research on management accounting, in spiteof its limitations. First, only selected elements of the D&M information system suc-cess model were used, which precludes the evaluation of M.A.I.S. in terms of its suc-cesses. Moreover, the small number of responses should be acknowledged, whichdoes not allow universal conclusions to be made. Second, the study did not discussthe results separately for the small and medium enterprises and large organisations,as no differences were observed. Neither did the study focus on small and mediumenterprises, although this could be a direction for future research, allowing the inves-tigation of the separate management accounting needs of managers from small andmedium enterprises as well as large organisations. Third, the use of questionnaire-based surveys only is generally not sufficient for thoroughly assessing the perceptionof managers. Therefore, future research should be completed by an interview-basedapproach that enables better understanding of the perception of managementaccounting and the information it provides to businesses. It will also be worth

2814 J. DOBROSZEK ET AL.

expanding the study to managers from organisations operating in other countries, forexample developed countries, and to compare the usefulness of M.A.I.S. in the con-text of operational and strategic management.

Disclosure statement

No potential conflict of interest was reported by the author(s).

ORCID

Justyna Dobroszek https://orcid.org/0000-0003-4728-9019Ewelina Zarzycka https://orcid.org/0000-0002-5347-2883Alina Almasan https://orcid.org/0000-0002-5416-2465Cristina Circa https://orcid.org/0000-0002-5518-9352

References

Alawattage, C., Hopper, T., & Wickramasinghe, D. (2007). Introduction to managementaccounting in less developed countries. Journal of Accounting & Organizational Change,3(3), 183–191. doi:10.1108/18325910710820256

Adeoti-Adekeye, W. B. (1997). The importance of management information systems. Library,46(5), 318–327.

Albu, N., & Albu, C. N. (2012). Factors associated with the adoption and use of managementaccounting techniques in developing countries: The case of Romania. Journal ofInternational Financial Management and Accounting, 23(3), 245–276.

Albu, C. N., & Alexe, S. (2009). The role of organizational learning in performance manage-ment. Contabilitatea, Expertiza si Auditul Afacerilor, 9, 42–46.

Anderson, S. W., & Lanen, W. (1999). Economic transition, strategy and the evolution of man-agement accounting practices: case of India. Accounting, Organizations and Society, 24(5–6),379–412.

Arsov, S., & Bucevska, V. (2017). Determinants of transparency and disclosure – evidencefrom post-transition economies. Economic Research-Ekonomska Istra�zivanja, 30(1), 745–760.doi:10.1080/1331677X.2017.1314818

Baron, R., & Byrne, D. (1991). Social psychology. Understanding human interaction (6th ed.).Boston, MA: Allyn and Bacon.

Bjørnenak, T., & Olson, O. (1999). Unbundling management accounting innovations.Management Accounting Research, 10(4), 13–32. doi:10.1006/mare.1999.0110

Bruns, W. J., & McKinnon, S. M. (1992a). The information mosaic. Boston, MA: HarvardBusiness School Press.

Bruns, W. J., & McKinnon, S. M. (1992b). Management information and accounting informa-tion: What do managers want? In M. J. Epstein (Ed.), Advances in management accounting(Vol. 1, pp. 55–80). Greenwich: Jail Press Inc.

Bruns, W. J., & McKinnon, S. M. (1993). Information and managers: A field study. Journal ofManagement Accounting Research, 5, 84–108.

Byrne, S., & Pierce, B. (2007). Towards a more comprehensive understanding of the roles ofmanagement accountants. European Accounting Review, 16(3), 469–498. doi:10.1080/09638180701507114

Chenhall, R. H. (2006). The contingent design of performance measures. In A. Bhimani (Ed.),Contemporary issues in management accounting (pp. 92–116), Oxford: Oxford UniversityPress.

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA 2815

Chenhall, R. H., & Morris, D. (1986). The impact of structure, environment, and interdepend-ence on the perceived usefulness of management accounting systems. The AccountingReview, 61(1), 16–35. doi:10.1016/0361-3682(94)90010-8

Cutting, J. E. (1987). Perception and information. Annual Review of Psychology, 38, 61–90. doi:10.1146/annurev.ps.38.020187.000425

Definition of Management Accounting. (2008). Practice of management accounting. https://www.imanet.org.cn/uploads/resource/2015-11/1447061510-17551.pdf.

DeLone, W. H., & McLean, E. R. (2003). The DeLone and McLean model of information sys-tem success: A ten-year update. Journal of Management Information Systems, 19(4), 9–30.

Feleaga, N. (1996). Controverse contabile. Dificultati conceptuale si credibilitatea contabilitatii.Bucharest: Economica.

Fleischman, G., Walker, K., & Johnson, E. (2010). A field study of user versus provider percep-tions of management accounting system services. International Journal of Accounting &Information Management, 18(3), 252–285. doi:10.1108/18347641011068992

Glavan, M. E., Braescu, M., Dumitru, V., Jinga, G., & Laptes, R. (2007). The relevance andquality of the accounting information in the managerial decisions. Accounting andManagement Information Systems, 6(Supplement), 103–115.

Granlund, M., & Lukka, K. (1998). It’s a small world of management accounting practices.Journal of Management Accounting Research, 10, 151–179. doi:10.1016/j.mar.2010.10.004

Granlund, M., & Lukka, K. (1998). Towards increasing business orientation: Finnish manage-ment accountants in a changing cultural context Management Accounting Research, 9(2),185–211.

Ingram, M., & Margetis, S. (2010). A practical method to estimate the cost of equity capitalfor a firm using cluster analysis. Managerial Finance, 36(2), 160–167. doi:10.1108/03074351011014569

Jinga, G., & Dumitru, M. (2015). The Change in Management Accounting from anInstitutional and Contingency Perspective: A Case Study for a Romanian Company.International Journal of Social, Behavioral, Educational, Economic, Business and IndustrialEngineering, 9, 6, 1913–1920.

Jinga, G., Dumitru, M., Dumitrana, M., & Vulpoi, M. (2010). Accounting systems for costmanagement used in the Romanian economic entities. Accounting and ManagementInformation Systems, 9, 242–267.

Jianu, I., & Jianu, G. (2012). The told and retold story of Romanian accounting. Journal ofAccounting and Management Information Systems, 11(3), 391–423.

Joseph, G. (2008). A rationale for stakeholder-based management in developing nations. Journalof Accounting & Organizational Change, 4, 136–161. doi:10.1108/18325910810878946

Johnson, H. T., & Kaplan, R. (1987). Relevance lost: The rise and fall of management account-ing. Boston, MA: Harvard Business School Press.

Kacprzyk, A., & Dory�n, W. (2017). Innovation and economic growth in old and new memberstates of the European Union. Economic Research-Ekonomska Istra�zivanja, 30(1), 1724–1742.doi:10.1080/1331677X.2017.1383176

Khan, A. K., Bakkappa, B., Metri, B. A., & Sahay, B. S. (2009). Impact of agile supply chains’delivery practices on firms’ performance: Cluster analysis and validation. Supply ChainManagement: An International Journal, 14(1), 41–48. doi:10.1108/13598540910927296

Kim, K. K. (1989). User satisfaction: A synthesis of three different perspectives. Journal ofInformation Systems, Fall, 1–12.

Laudon, K., & Laudon, J. (2006). Management information system. Managing the digital firm.Upper Saddle River, NJ: Prentice-Hall.

L€a€ats, K., & Haldma, T. (2012). Changes in the scope of management accounting systems inthe dynamic economic context. Economics and Management, 17(2), 441–447. doi:10.5755/j01.em.17.2.2164

Mia, L., & Chenhall, R. (1994). The usefulness of MAS functional differentiation and manage-ment effectiveness. Accounting, Organization and Society, 19(1), 1–13. doi:10.1016/0361-3682(94)90010-8

2816 J. DOBROSZEK ET AL.

Mendoza, C., & Bescos, P. L. (2001). An explanatory model of managers’ information needs:Implications for management accounting. European Accounting Review, 10(2), 257–289. doi:10.1080/09638180126636

Nimtrakoon, S., & Tayles, M. (2015). Explaining management accounting practices and strat-egy in Thailand: A selection approach using cluster analysis. Journal of Accounting inEmerging Economies, 5(3), 269–298. doi:10.1108/JAEE-02-2013-0012

Nita, B. (2014). Sprawozdawczo�s�c zarzadcza. Analizy i raporty wewneR trzne w controllingu.Warszawa: Wydawnictwo Naukowe PWN.

Online Manual on Statistics. (2016). Stat soft electronic statistics textbook. http://www.statsoft.com/Textbook.

Pierce, B., & O’Dea, T. (2003). Management accounting information and the needs of manag-ers: Perceptions of managers and accountants compared. The British Accounting Review,35(3), 257–290. doi:10.1016/S0890-8389(03)00029-5

Ristiono, R. J., & Michalak, J. M. (2018). Employee perceptions of organizational culture’sinfluence on their attitudes and behaviour. Journal of East European Management Studies,23(2), 277–294. doi:10.5771/0949-6181-2018-2-295

Sadi�c, S., Pu�skak, A., & Beganovi�c, A. (2016). Information support model and its impact onutility, satisfaction and loyalty of user. The European Journal of Applied Economics, 13(2),30–44.

Saunders, J. A. (1980). Cluster analysis for market segmentation. European Journal ofMarketing, 14(7), 422–435. doi:10.1108/EUM0000000004918

Simon, H. A., Guetzkow, H., Kozmetsky, G., & Tyndall, G. (1954). Centralization vs. decentral-ization in organizing the controller’s department, Houston, TX: Controllership Foundation.

�Si�ska, L. (2016). The contingency factors affecting management accounting in Czech compa-nies. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 64(4),1320–1383. doi:10.11118/actaun201664041383

Strumickas, M., & Valanciene, L. (2009). Research of management accounting changes in lithu-anian business organizations. Engineering Economics, 3(63), 26–32

Szychta, A. (2008). Etapy ewolucji i kierunki integracji metod rachunkowo�sci zarzadczej. Ł�od�z:Wydawnictwo UŁ.

Szychta, A. (2018). Management accounting practices in developing countries since the 1990s:The case of Poland. Zeszyty Teoretyczne Rachunkowo�sci, 2018(99), 119. doi:10.5604/01.3001.0012.2936

Szychta, A., & Dobroszek, J. (2016). Perception of management accounting and controlling byPolish authors in publications in 1990–2016. Advances in Economics Business andManagement Research, 27, 450–467.

The Growth of Polish and Romanian Economy. (2018) https://businessinsider.com.pl/finanse/makroekonomia/dynamika-pkb-polski-w-2018-r-prognozaoecd/brr2wljand https://businessin-sider.com.pl/finanse/makroekonomia/rumunia-najszybszy-wzrost-gospodarczy-w-ue/hk85w58.

Van der Veeken, H. J. M., & Wouters, M. J. F. (2002). Using accounting information systemsby operations managers in a project company. Management Accounting Research, 13(3),345–370. doi:10.1006/mare.2002.0188

Wnuk-Pel, T. (2014). Management accounting innovations. The case of ABC in Poland. Ł�od�z:Wydawnictwo Uniwersytetu Ł�odzkiego.

Zarzycka, E. (2016). Koncepcje i tendencje rozwoju zawodu specjalisty rachunkowo�sci zarzadczej.Wymiar krajowy i mieRdzynarodowy. Ł�od�z: Wydawnictwo Uniwersytetu Ł�odzkiego.

ECONOMIC RESEARCH-EKONOMSKA ISTRA�ZIVANJA 2817