Embed Size (px)

Citation preview

04.09.2003

1

2 September 2003

Managing a MBS Portfolio

Robert Scott

Portfolio Manager

BIS Asset Management

Outline:

l Aggregating the risks in an MBS Portfolio

l Index Replication

l Relative Value Analysis

04.09.2003

2

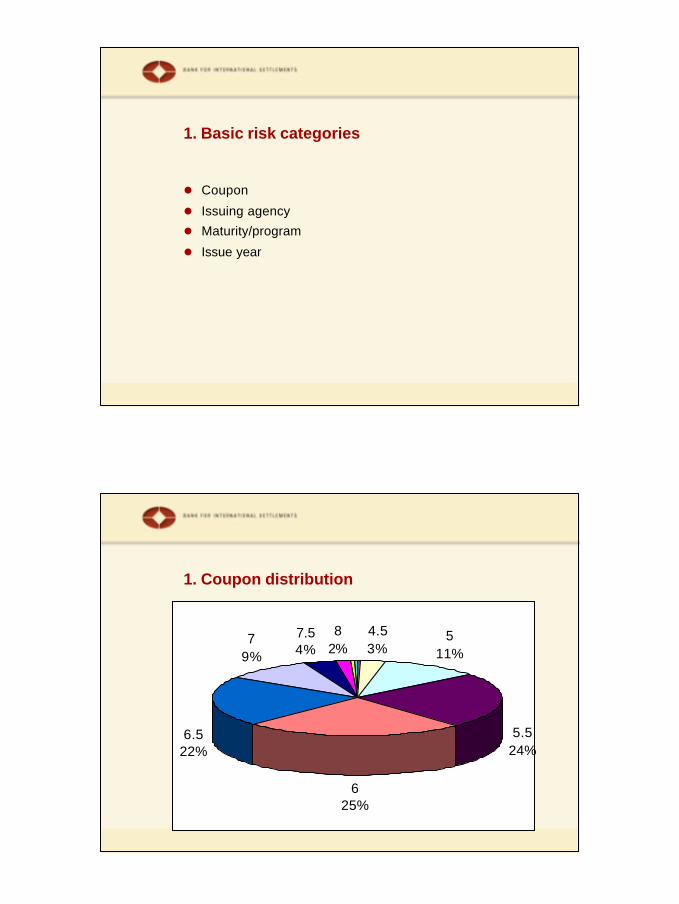

1. Basic risk categories

l Coupon

l Issuing agency

l Maturity/program

l Issue year

1. Coupon distribution

4.53%

511%

5.524%

625%

6.522%

79%

7.54%

82%

04.09.2003

3

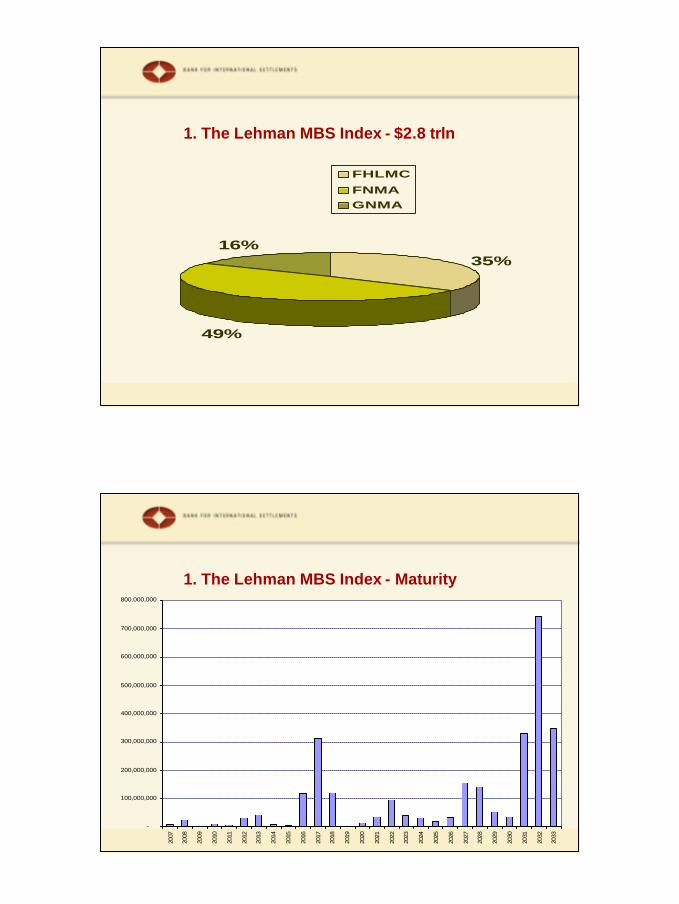

1. The Lehman MBS Index - $2.8 trln

35%

49%

16%

FHLMC

FNMAGNMA

1. The Lehman MBS Index - Maturity

-

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

700,000,000

800,000,000

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

04.09.2003

4

1. Factors impacting price changes

l Duration l Yield curve re-shapingl Current-coupon spreadl Volatilityl MBS-Treasury spreadl Convexityl OAS

1. Further difficulties: effective vs empirical durations

l Effective duration assumes all risk factors remain constant

l Empirical duration assumes correlation of all risk factors with interest rates remains constant

l Differ most when OAS has significant negative correlation with interest rates

04.09.2003

5

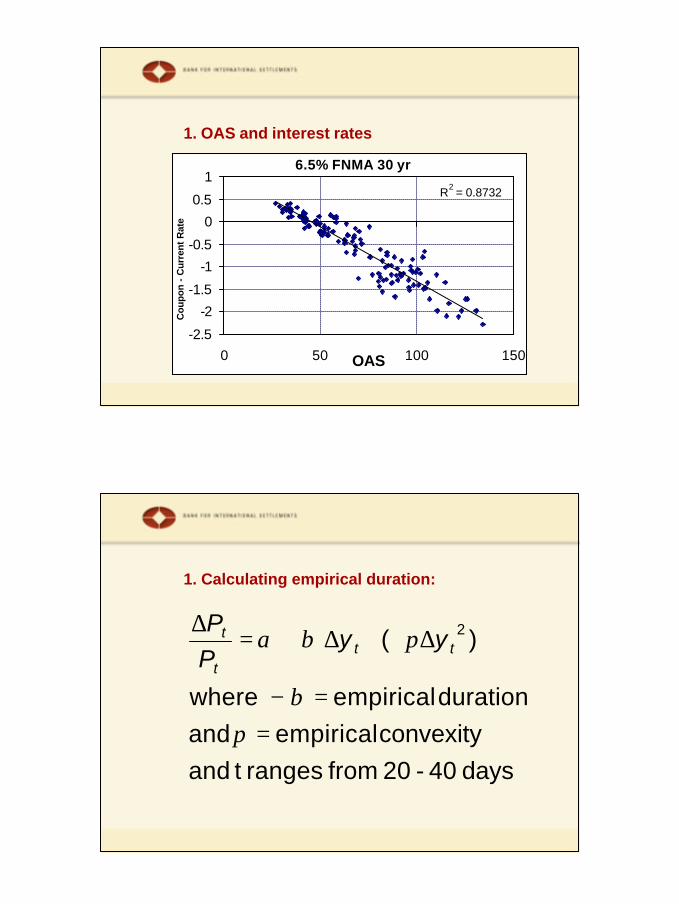

1. OAS and interest rates

6.5% FNMA 30 yr

R2 = 0.8732

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

0 50 100 150OAS

Cou

pon

- C

urre

nt R

ate

1. Calculating empirical duration:

days 40-20 from ranges t andconvexity empirical and

duration empirical where

) ( 2

==−

∆+∆+=∆

πβ

πβα ttt

t yyPP

04.09.2003

6

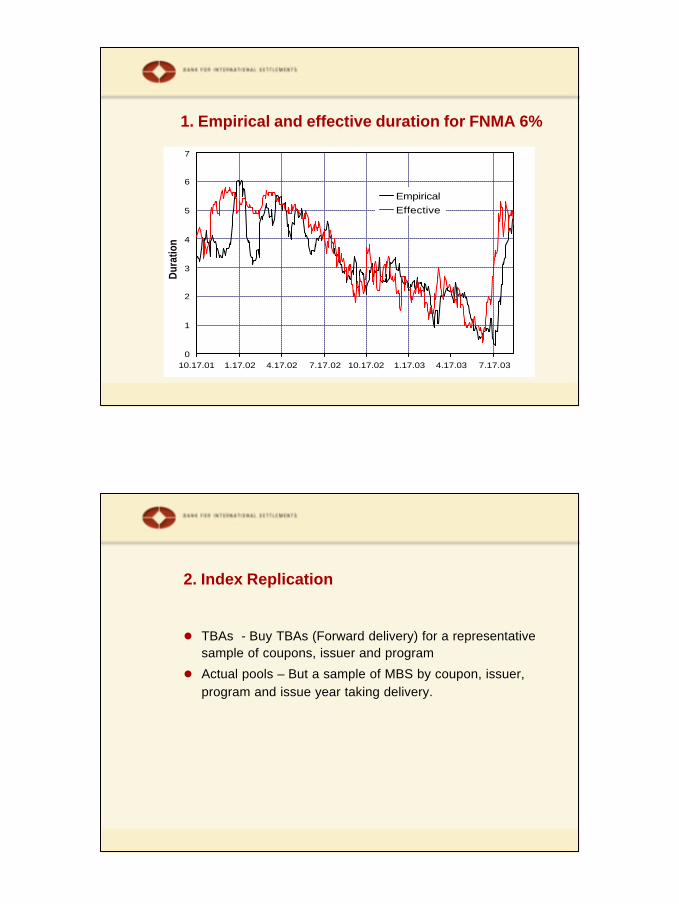

1. Empirical and effective duration for FNMA 6%

0

1

2

3

4

5

6

7

10.17.01 1.17.02 4.17.02 7.17.02 10.17.02 1.17.03 4.17.03 7.17.03

Dur

atio

n

EmpiricalEffective

2. Index Replication

l TBAs - Buy TBAs (Forward delivery) for a representative sample of coupons, issuer and program

l Actual pools – But a sample of MBS by coupon, issuer, program and issue year taking delivery.

04.09.2003

7

2. Index replication – Available indexes

l Lehman MBS Index – 523 issues, 2.8 trln

l Salomon – 1.9 trln (30 yr )

l Merrill Lynch – 423 issues, $2.55 trln

2. Index Replication – About the Lehman Index

l Each bond in the index is a generic – i.e. not tradable

l 526 bonds in the index

l 15 different programs / maturities

l Only 6 programs have 3% or more weighting

04.09.2003

8

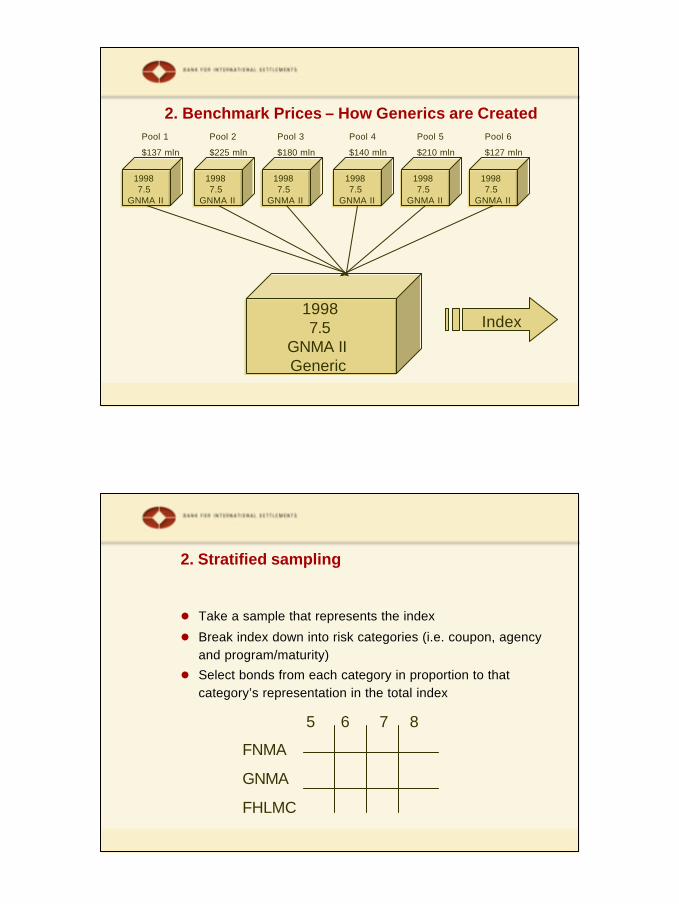

2. Benchmark Prices – How Generics are Created

1998 7.5

GNMA II

1998 7.5

GNMA II

1998 7.5

GNMA II

1998 7.5

GNMA II

1998 7.5

GNMA II

1998 7.5

GNMA II

Pool 1

$137 mln

19987.5

GNMA II Generic

Index

Pool 2

$225 mln

Pool 3

$180 mln

Pool 4

$140 mln

Pool 5

$210 mln

Pool 6

$127 mln

2. Stratified sampling

l Take a sample that represents the index

l Break index down into risk categories (i.e. coupon, agency and program/maturity)

l Select bonds from each category in proportion to that category’s representation in the total index

5 6 7 8

FNMA

GNMA

FHLMC

04.09.2003

9

2. An example portfolio – Generic pools Coupon Weight Coupon Weight

4.5 0.3% 5 0.0%5 1.3% 5.5 0.1%

5.5 0.9% 5 1.4%6 1.1% 5.5 4.2%

6.5 0.7% 6 6.8%7 0.4% 6.5 7.2%5 1.7% 7 3.6%

5.5 12.0% 7.5 1.5%6 14.4% 8 0.6%

6.5 17.7% 8.5 0.1%7 12.4%

7.5 5.3% 27 Total 8 3.6% 22 Available as TBA

8.5 1.0% Missing amount: 2.8%9 1.0%

9.5 0.5% Not available as TBA10 0.2%

GNMA I Single Family 'Midget' - 15 years

GNMA I Single Family Pool - 30 years

GNMA II Single Family 'Midget' - 15 years

GNMA II Single Family Pool - 30 years

Effective Duration

Yield

Lehman GNMA MBS Index 2.06 5.17 Generic portfolio 2.01 5.16

An Example Portfolio – TBAs

Program CouponNominal Amount Weight

4.5 660,419 0.3%5 2,621,468 1.3%

5.5 1,777,402 0.9%6 2,310,187 1.2%

6.5 1,376,146 0.7%7 887,138 0.4%5 3,579,151 1.8%

5.5 24,626,704 12.3%6 29,633,028 14.8%

6.5 36,427,822 18.2%7 25,605,481 12.8%

7.5 10,998,343 5.5%8 7,384,985 3.7%5 81,895 0.0%

5.5 110,025 0.1%5 2,935,802 1.5%

5.5 8,609,112 4.3%6 14,046,347 7.0%

6.5 14,729,808 7.4%7 7,356,561 3.7%

7.5 3,048,676 1.5%8 1,193,498 0.6%

200,000,000 100%

GNMA II Single Family Pool - 30 years

GNMA II Single Family 'Midget' - 15 years

GNMA I Single Family Pool - 30 years

GNMA I Single Family 'Midget' - 15 years

04.09.2003

10

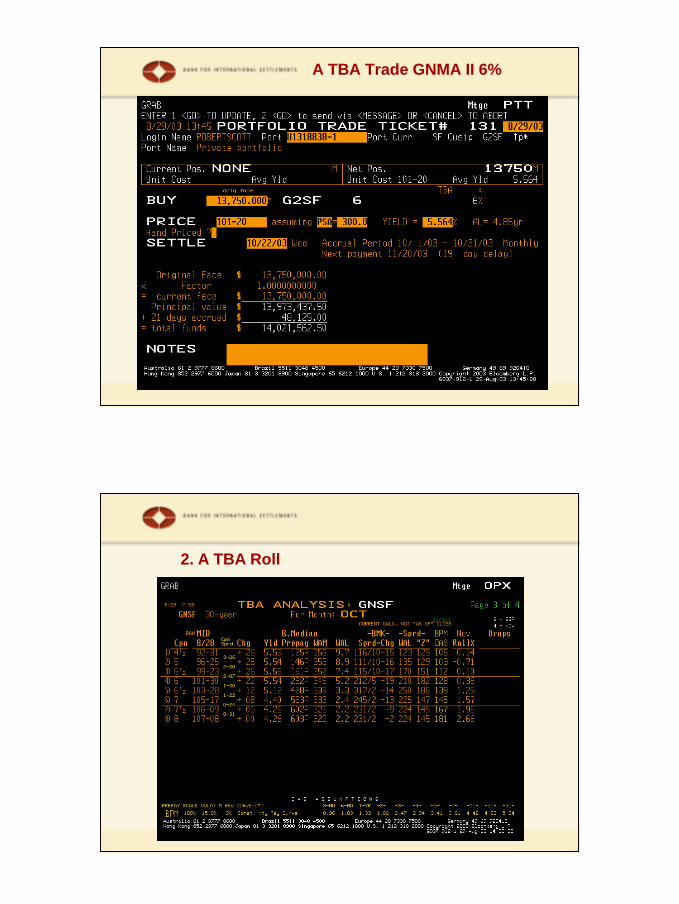

A TBA Trade GNMA II 6%

2. A TBA Roll

04.09.2003

11

2. Replication performance*

l TBA only strategy averages 21 bps annual tracking error

l Large pool strategy averages 15 bps annual tracking error

Source: “Tradable proxy portfolios for the Lehman Brothers MBS Index”, Lehman Brothers Fixed Income Research, July 2001

04.09.2003

12

3. Relative value

l Bottom up or pool specific

l Top-down or Macro-driven

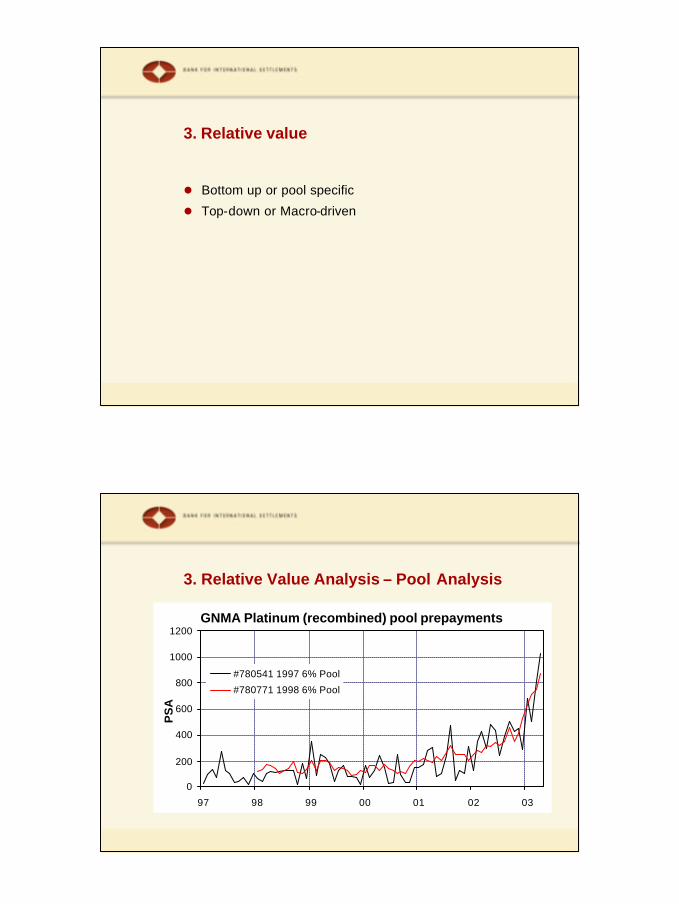

3. Relative Value Analysis – Pool Analysis

GNMA Platinum (recombined) pool prepayments

0

200

400

600

800

1000

1200

97 98 99 00 01 02 03

PS

A

#780541 1997 6% Pool

#780771 1998 6% Pool

04.09.2003

13

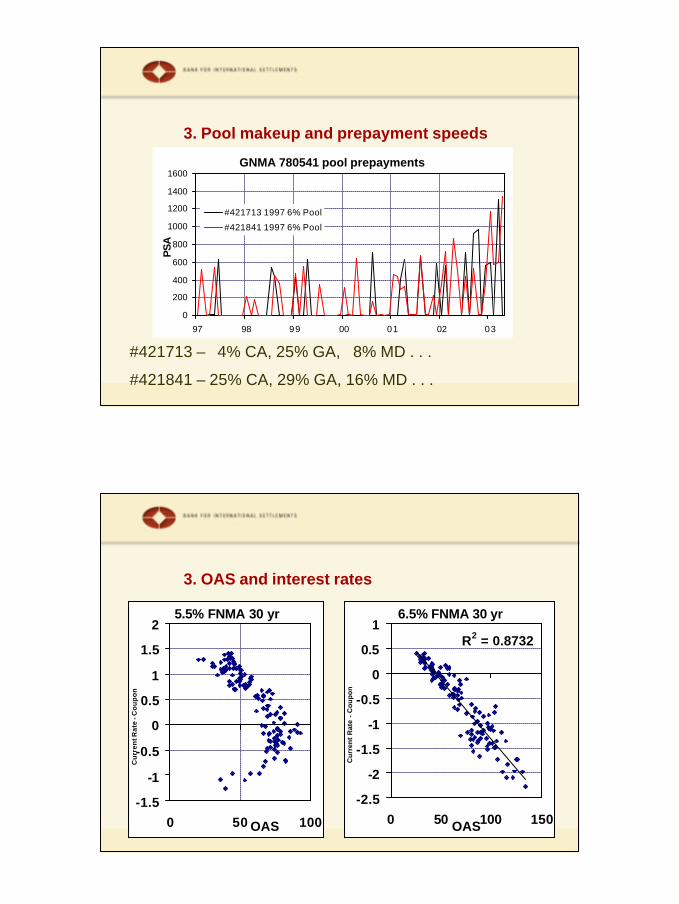

3. Pool makeup and prepayment speeds

#421713 – 4% CA, 25% GA, 8% MD . . .

#421841 – 25% CA, 29% GA, 16% MD . . .

GNMA 780541 pool prepayments

0

200

400

600

800

1000

1200

1400

1600

97 98 99 00 01 02 03

PS

A

#421713 1997 6% Pool

#421841 1997 6% Pool

3. OAS and interest rates

5.5% FNMA 30 yr

-1.5

-1

-0.5

0

0.5

1

1.5

2

0 50 100OAS

Cu

rren

t Rat

e - C

ou

po

n

6.5% FNMA 30 yr

R2 = 0.8732

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

0 50 100 150OAS

Cu

rren

t R

ate

- C

ou

po

n

04.09.2003

14

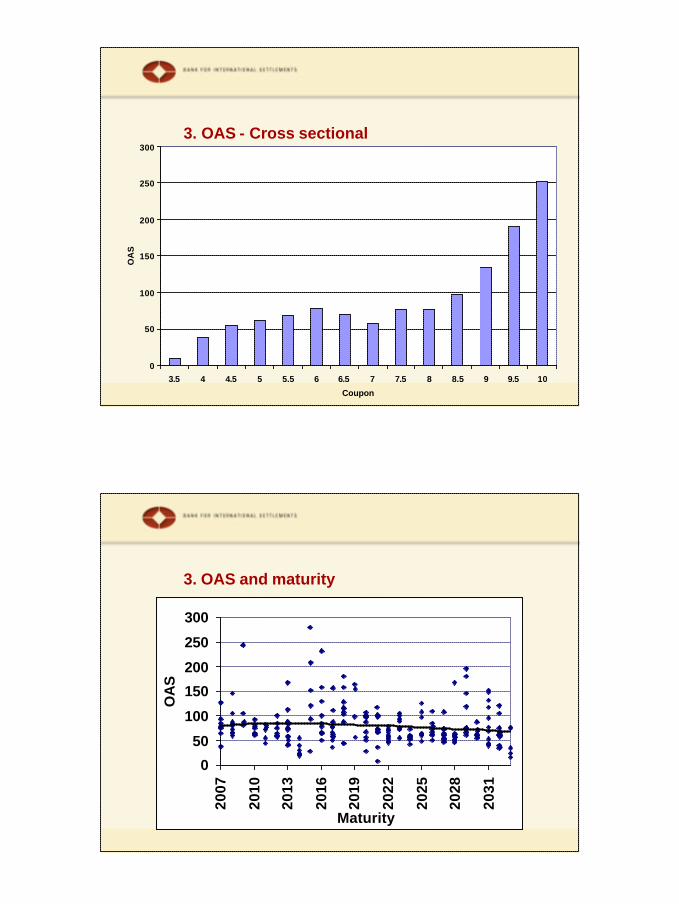

3. OAS - Cross sectional

0

50

100

150

200

250

300

3.5 4 4.5 5 5.5 6 6.5 7 7.5 8 8.5 9 9.5 10

Coupon

OA

S

3. OAS and maturity

0

50

100

150

200

250

300

2007

2010

2013

2016

2019

2022

2025

2028

2031

Maturity

OA

S

04.09.2003

15

In Summary

l Coupon, issue year, agency, program are important for classifying risks

l Duration as a risk measure, effective or empirical, requires assumptions

l TBA-only portfolio can reasonably replicate the Lehman MBS index

l Top-down or bottom -up analysis can be used for more active management

References

l Breeden, Douglas, “Complexities of Hedging Mortgages”, Journal of Fixed-Income, December 1994, pp. 6-41

l DeRosa, P., L. Goodman and M. Zazzarino, 1993, "Duration estimates on Mortgage-backed securities", Journal of Portfolio Management, Winter

l Dynkin, Lev; Vadim Konstantinovsky, Bruce Phelps, “Tradable Proxy Portfolios for the Lehman Brothers MBS Index”, Lehman Brothers Fixed Income Research, July 2001

l Fabozzi, Frank, The Handbook of Mortgage-Backed Securities, McGraw-Hill, NY, 1995 . .

l Hayre, Lakhbir, Guide to Mortgage-Backed and Asset-Backed Securities, John Wiley and Sons, NY, 2001