Embed Size (px)

Citation preview

Managing Channel Conflict

Philip G Scott

Chief ExecutiveNorwich Union Life

ABN AMRO Pan European Bankingand Insurance Conference - 27th June 2001

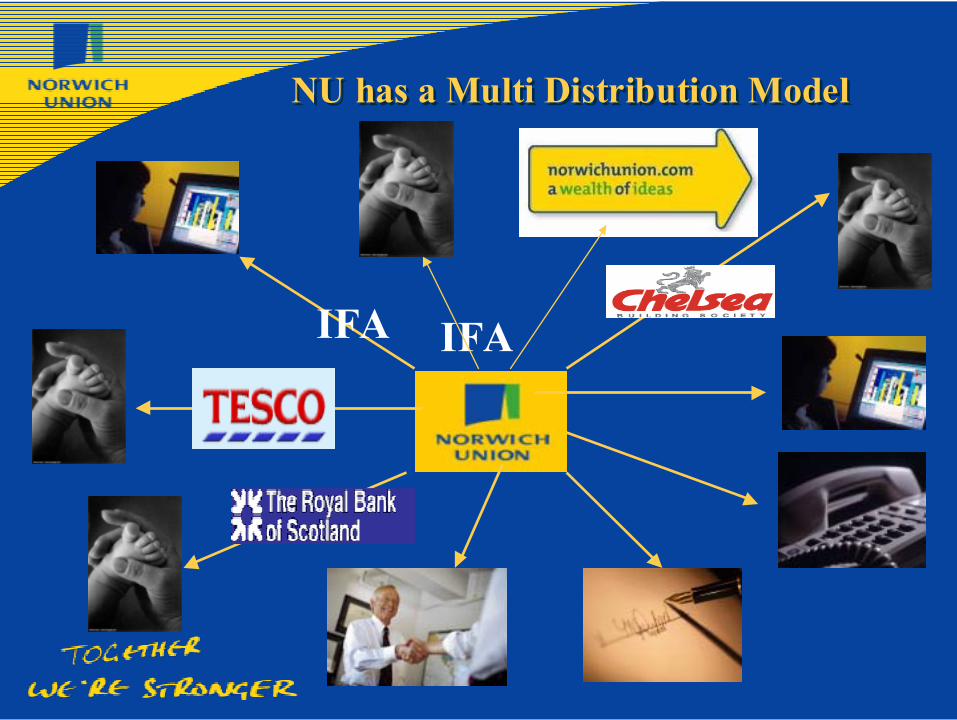

NU has a Multi Distribution ModelNU has a Multi Distribution Model

IFA IFA

Multiple Brands Single Brand

Consumer AwarenessCost

Market Consolidation

‘V’

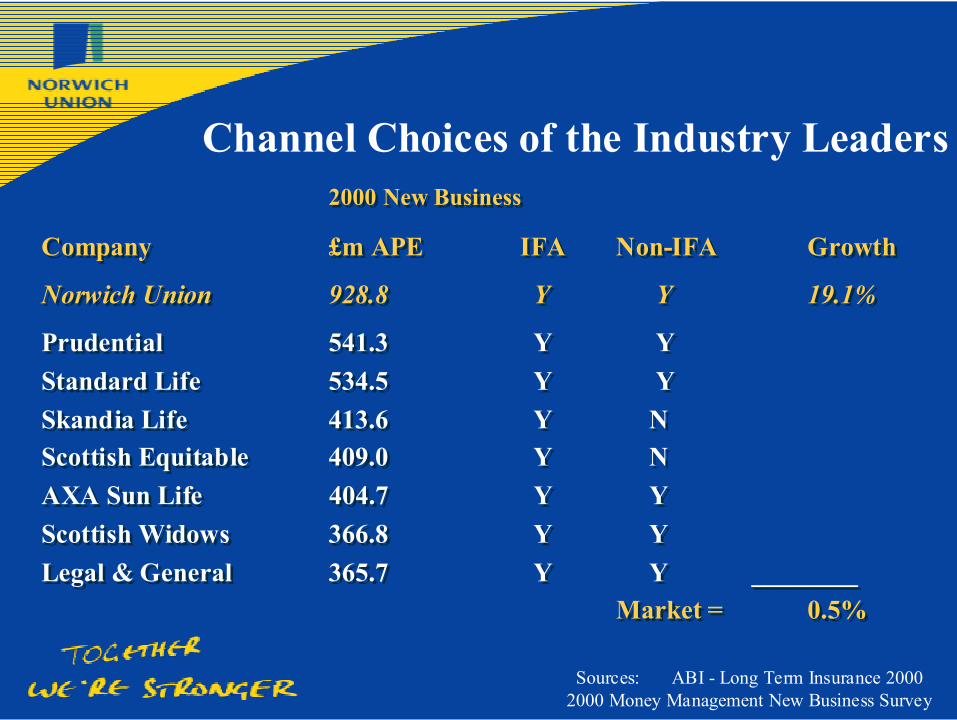

2000 New Business

Company £m APE IFA Non-IFA Growth

Norwich Union 928.8 Y Y 19.1%

Prudential 541.3 Y YStandard Life 534.5 Y YSkandia Life 413.6 Y NScottish Equitable 409.0 Y NAXA Sun Life 404.7 Y YScottish Widows 366.8 Y YLegal & General 365.7 Y Y ________

Market = 0.5%

2000 New Business

Company £m APE IFA Non-IFA Growth

Norwich Union 928.8 Y Y 19.1%

Prudential 541.3 Y YStandard Life 534.5 Y YSkandia Life 413.6 Y NScottish Equitable 409.0 Y NAXA Sun Life 404.7 Y YScottish Widows 366.8 Y YLegal & General 365.7 Y Y ________

Market = 0.5%

Sources: ABI - Long Term Insurance 20002000 Money Management New Business Survey

Channel Choices of the Industry Leaders

Norwich Union Business by ChannelNorwich Union Business by Channel

IF A

D irect

C ore P artn ership s

Introdu cer P artn ers

A ffin ity

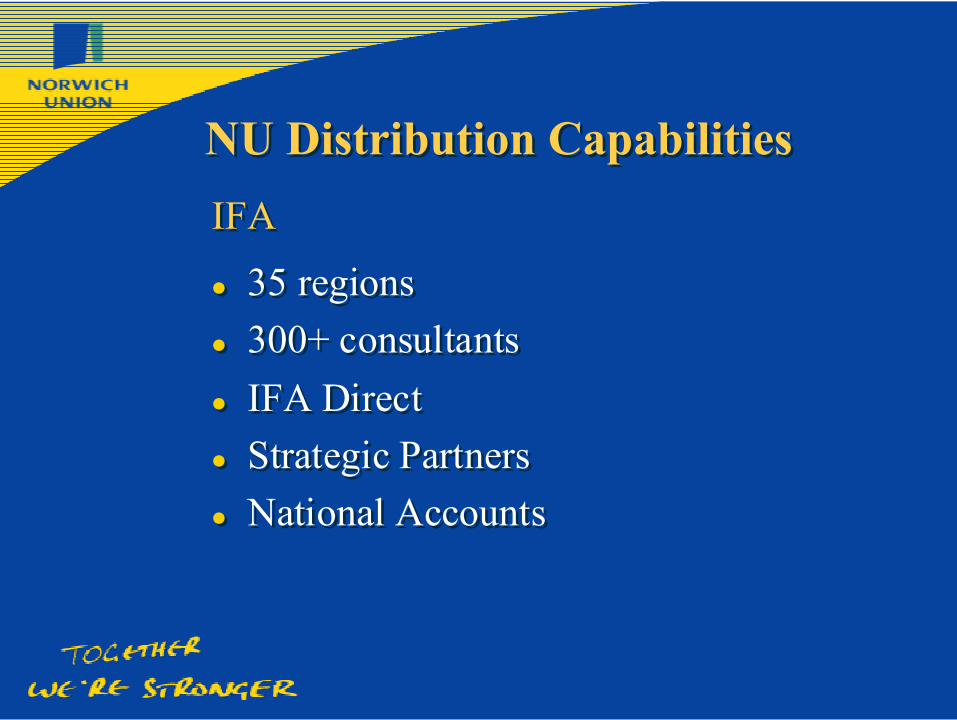

NU Distribution CapabilitiesNU Distribution CapabilitiesIFA

35 regions300+ consultantsIFA DirectStrategic PartnersNational Accounts

IFA

35 regions300+ consultantsIFA DirectStrategic PartnersNational Accounts

NU Distribution CapabilitiesNU Distribution CapabilitiesDirect

Direct Financial Services - 325consultantsDirect Corporate Sales - 40 consultantsTelesalesEstate Agency - 340 branches

Direct

Direct Financial Services - 325consultantsDirect Corporate Sales - 40 consultantsTelesalesEstate Agency - 340 branches

NU Distribution CapabilitiesNU Distribution Capabilities

Partnerships

520 consultants6 Appointed Representative BuildingSocieties15 Introducer Building Societies2 Estate Agencies

Partnerships

520 consultants6 Appointed Representative BuildingSocieties15 Introducer Building Societies2 Estate Agencies

NU Distribution CapabilitiesNU Distribution Capabilities

Affinities

Tesco Personal FinanceAge ConcernGoldfish

Joint VentureRoyal Bank of Scotland / NatWest Life

Affinities

Tesco Personal FinanceAge ConcernGoldfish

Joint VentureRoyal Bank of Scotland / NatWest Life

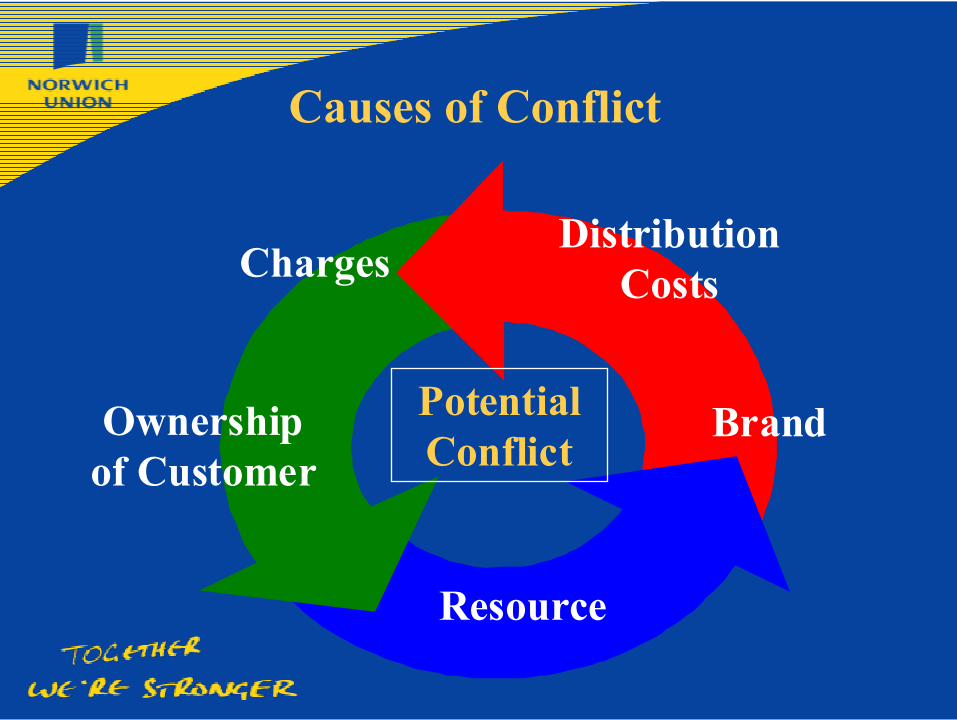

Causes of Conflict

PotentialConflict

ChargesDistribution

Costs

Brand

Resource

Ownershipof Customer

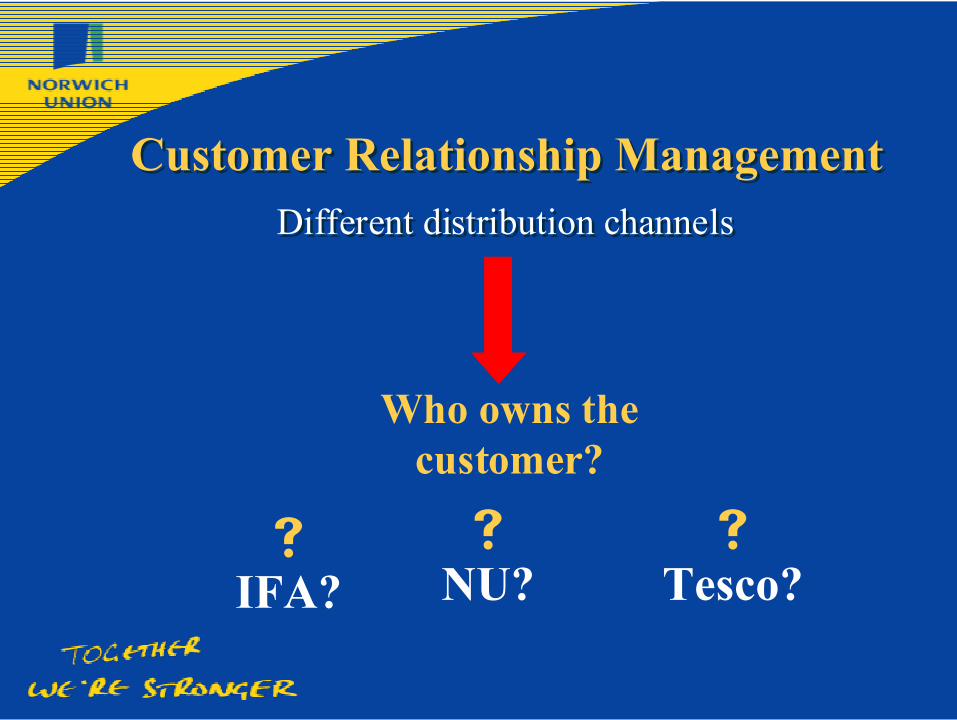

Customer Relationship ManagementCustomer Relationship ManagementDifferent distribution channelsDifferent distribution channels

Who owns thecustomer?

sIFA?

sNU?

sTesco?

The essence of managing channel conflictis understanding the

Value Chain

Management

Proposition Development

FundManagement

ProductAdmin

CustomerManagement Distribution

Support Services

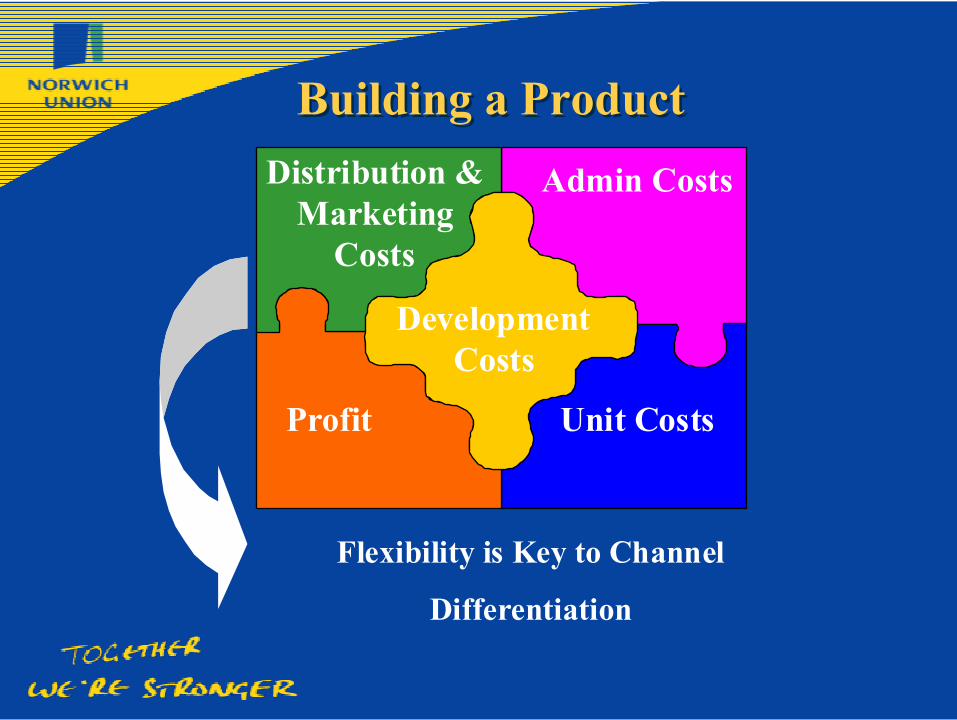

Building a ProductBuilding a ProductDistribution &

MarketingCosts

Admin Costs

Profit Unit Costs

DevelopmentCosts

Flexibility is Key to Channel

Differentiation

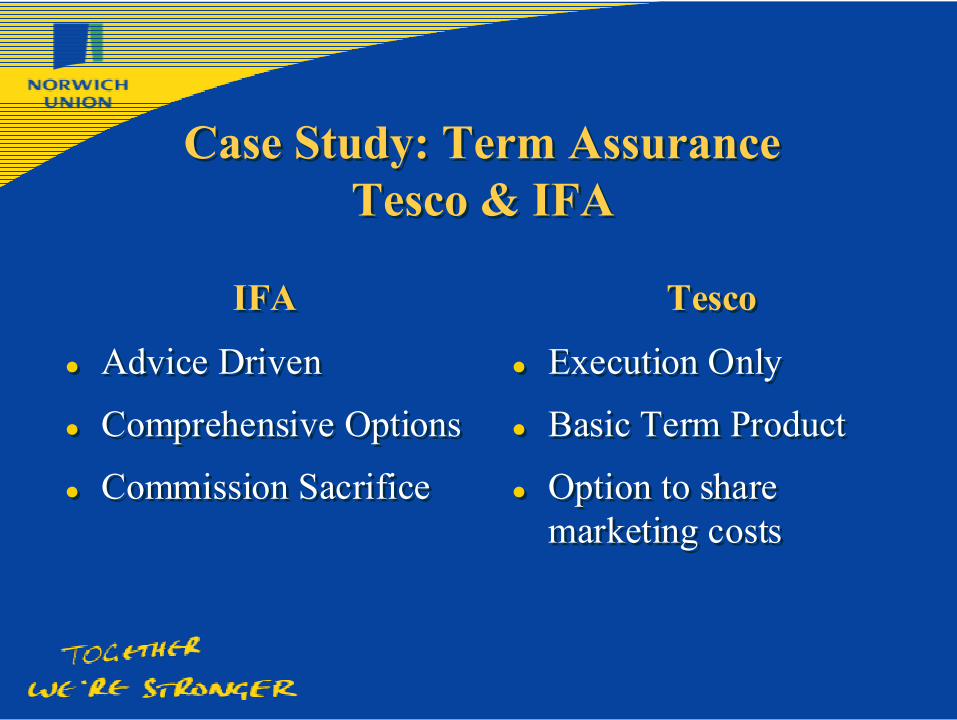

Case Study: Term AssuranceTesco & IFA

Case Study: Term AssuranceTesco & IFA

IFA

Advice Driven

Comprehensive Options

Commission Sacrifice

IFA

Advice Driven

Comprehensive Options

Commission Sacrifice

Tesco

Execution Only

Basic Term Product

Option to sharemarketing costs

Tesco

Execution Only

Basic Term Product

Option to sharemarketing costs

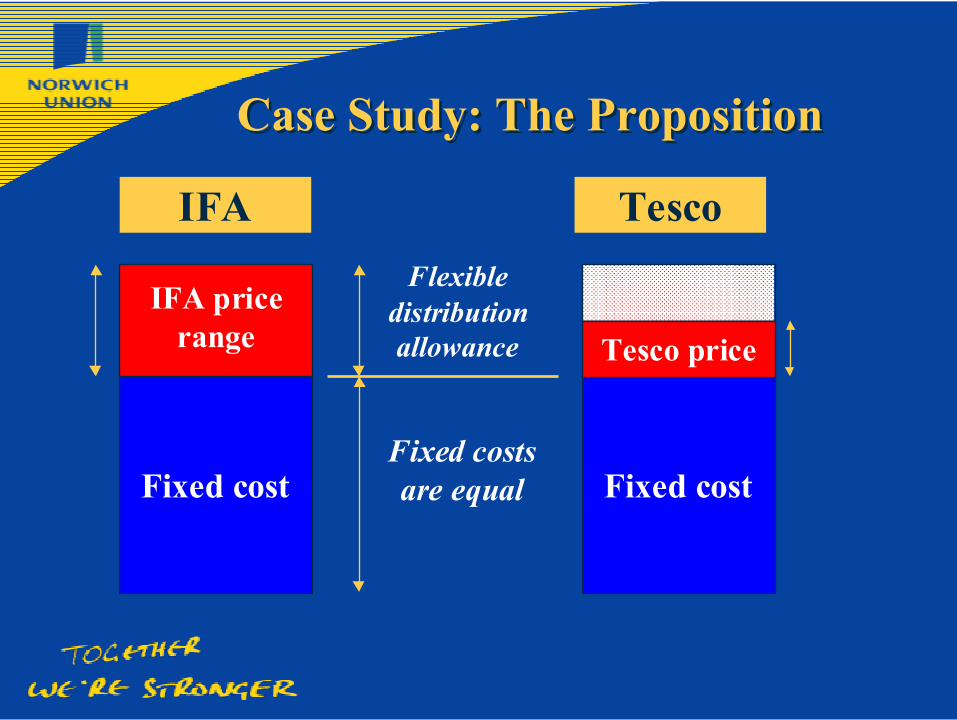

Case Study: The PropositionCase Study: The Proposition

Fixed cost

IFA Tesco

Fixed costFixed costsare equal

Tesco price

Flexibledistributionallowance

IFA pricerange

�������������������������������������������������������������������������

�������������������������������������������������������������������������

�������������������������������������������������������������������������

�������������������������������������������������������������������������

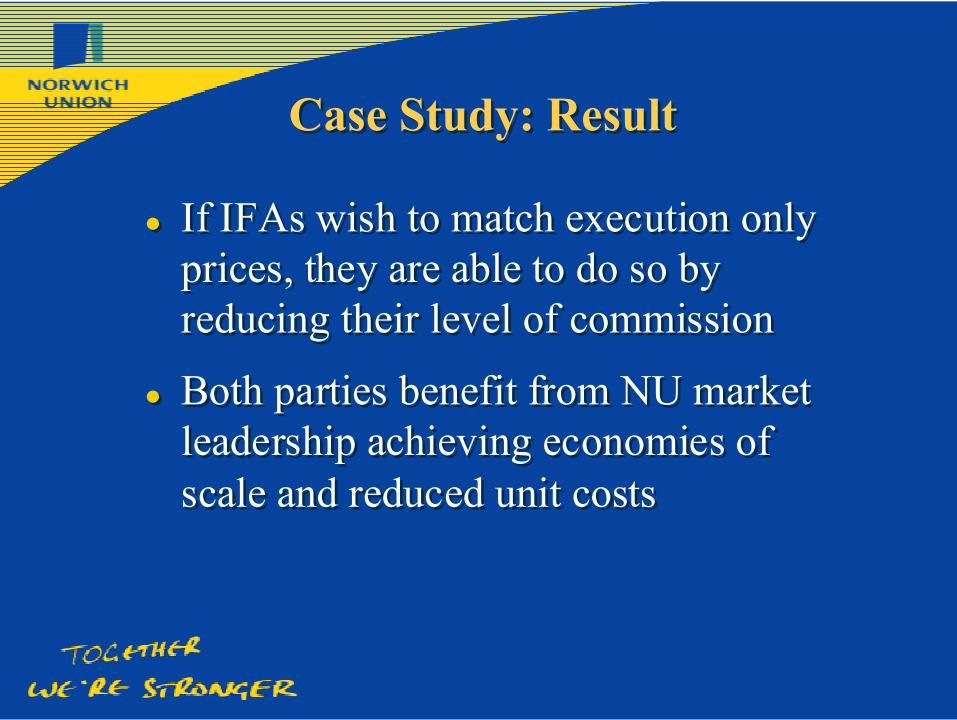

Case Study: ResultCase Study: Result

If IFAs wish to match execution onlyprices, they are able to do so byreducing their level of commission

Both parties benefit from NU marketleadership achieving economies ofscale and reduced unit costs

If IFAs wish to match execution onlyprices, they are able to do so byreducing their level of commission

Both parties benefit from NU marketleadership achieving economies ofscale and reduced unit costs

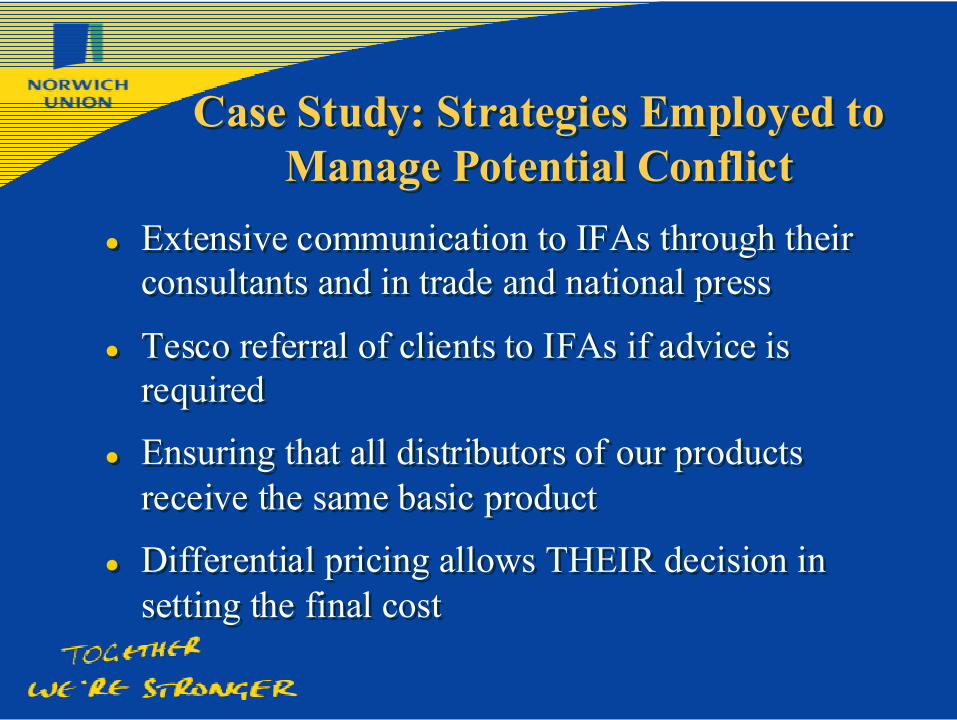

Case Study: Strategies Employed toManage Potential Conflict

Case Study: Strategies Employed toManage Potential Conflict

Extensive communication to IFAs through theirconsultants and in trade and national press

Tesco referral of clients to IFAs if advice isrequired

Ensuring that all distributors of our productsreceive the same basic product

Differential pricing allows THEIR decision insetting the final cost

Extensive communication to IFAs through theirconsultants and in trade and national press

Tesco referral of clients to IFAs if advice isrequired

Ensuring that all distributors of our productsreceive the same basic product

Differential pricing allows THEIR decision insetting the final cost

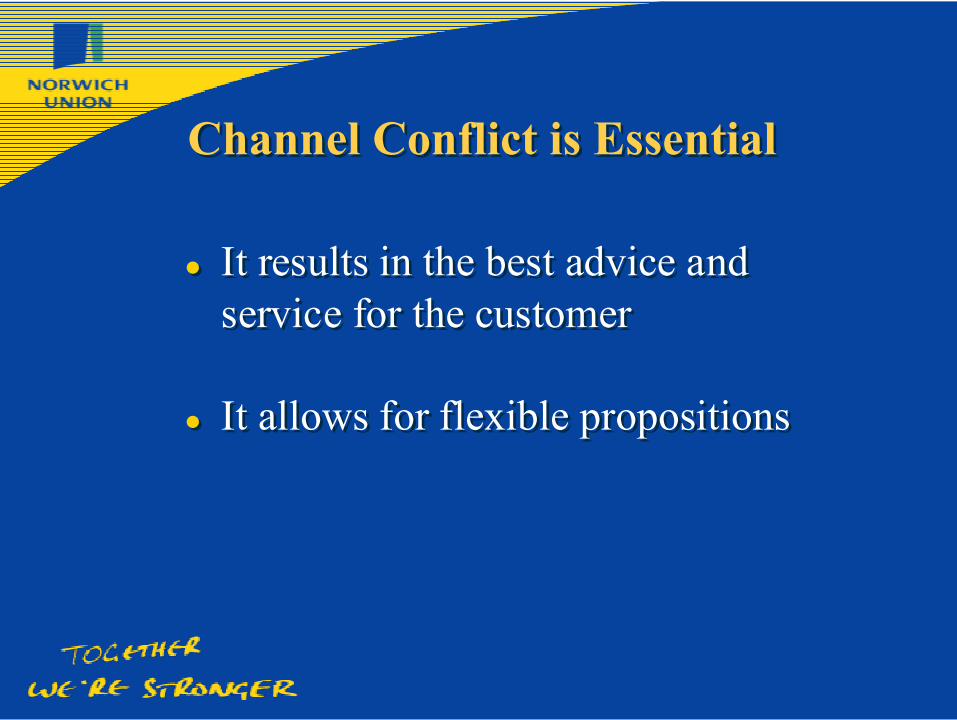

Channel Conflict is EssentialChannel Conflict is Essential

It results in the best advice andservice for the customer

It allows for flexible propositions

It results in the best advice andservice for the customer

It allows for flexible propositions

The key is giving all distributorsthe same scope for creating addedvalue within the transaction to thecustomer

Through flexible propositionsallowing differential pricing

The key is giving all distributorsthe same scope for creating addedvalue within the transaction to thecustomer

Through flexible propositionsallowing differential pricing

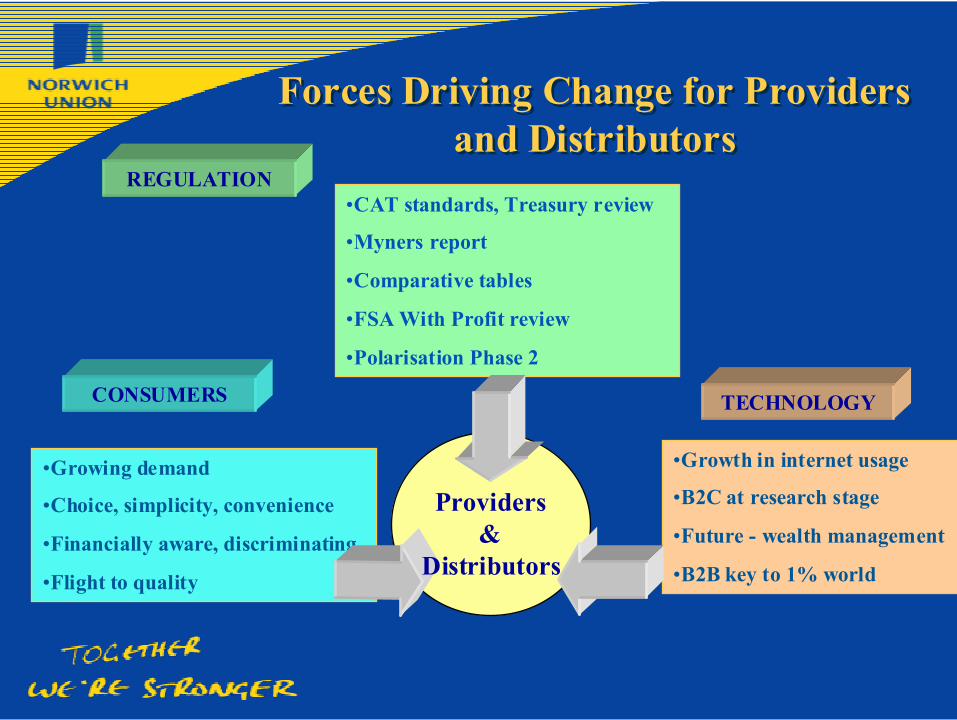

Keys to Success

•CAT standards, Treasury review

•Myners report

•Comparative tables

•FSA With Profit review

•Polarisation Phase 2

•Growing demand

•Choice, simplicity, convenience

•Financially aware, discriminating

•Flight to quality

•Growth in internet usage

•B2C at research stage

•Future - wealth management

•B2B key to 1% world

REGULATION

TECHNOLOGYCONSUMERS

Forces Driving Change for Providersand Distributors

Forces Driving Change for Providersand Distributors

Providers&

Distributors

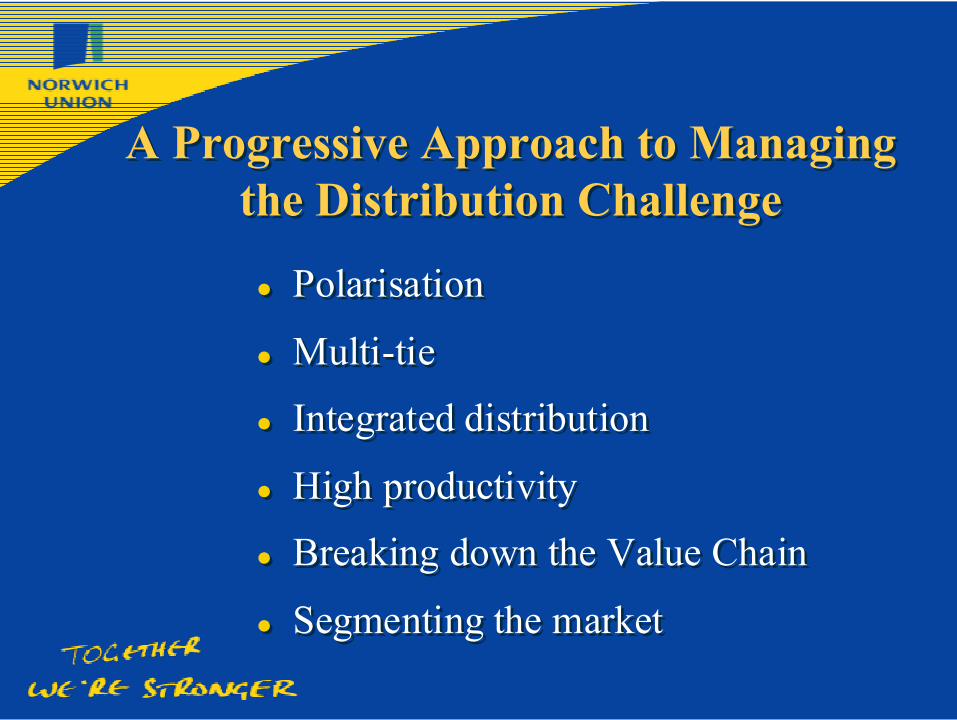

A Progressive Approach to Managingthe Distribution Challenge

A Progressive Approach to Managingthe Distribution Challenge

Polarisation

Multi-tie

Integrated distribution

High productivity

Breaking down the Value Chain

Segmenting the market

Polarisation

Multi-tie

Integrated distribution

High productivity

Breaking down the Value Chain

Segmenting the market

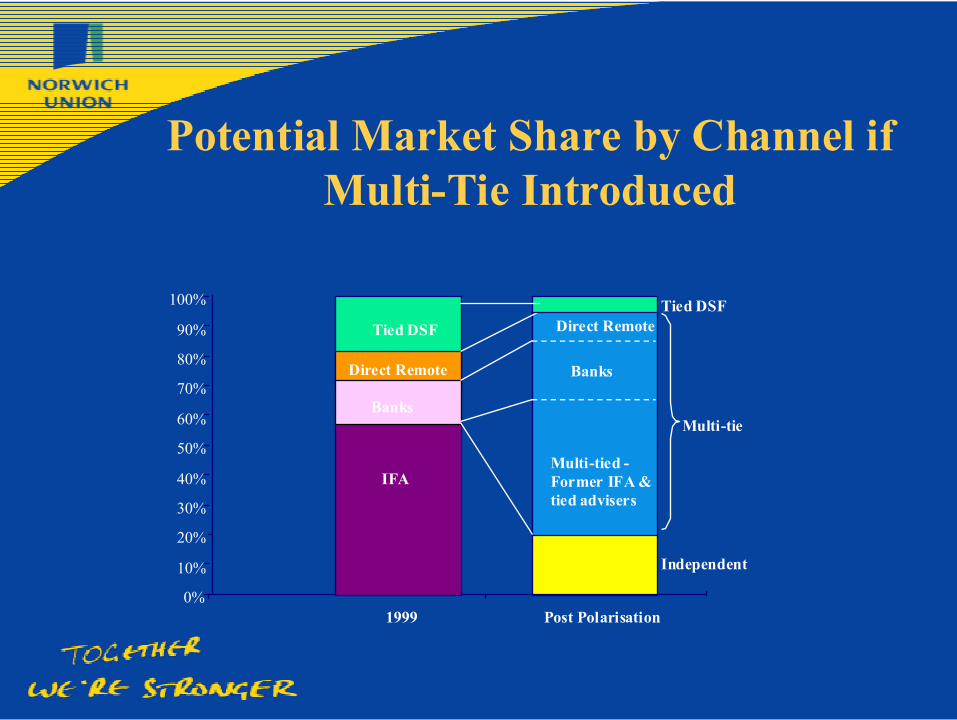

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1999 Post Polarisation

Direct RemoteTied DSF

Banks

Multi-tied -Former IFA &tied advisers

Independent

Direct Remote

Tied DSF

Banks

IFA

Multi-tieBanks

IFA

Potential Market Share by Channel ifMulti-Tie Introduced

Progressive Product StrategiesProgressive Product StrategiesStakeholder market positioning

Flexible Products to meet consumer focus

Investment Choice and SRI’s

Impact of Mutual Funds

Non-traditional products

Corporate market and EBC strategy

Transparency and open architecture

Phase 1 SALTR accreditation

E-products

Stakeholder market positioning

Flexible Products to meet consumer focus

Investment Choice and SRI’s

Impact of Mutual Funds

Non-traditional products

Corporate market and EBC strategy

Transparency and open architecture

Phase 1 SALTR accreditation

E-products

Progressive Marketing StrategiesProgressive Marketing Strategies

Leading brand

Reduced unit costs

Economies of size and scale

Increased distribution capability

Increased segmentation

Tailored propositions

Leading brand

Reduced unit costs

Economies of size and scale

Increased distribution capability

Increased segmentation

Tailored propositions

M anaging Channel ConflictsM anaging Channel Conflicts

PartnershipsPartnerships

Different approach to strategic alliancesPrice differentiation - value chainEconomies of scaleWhite labellingProduct diversificationE-commerce

Strategies for Channel Diversification

Norwich Union Life is to be a market leading providerof Life, Pensions and Long Term financial servicesproducts in the UK and to generate superior return

on capital and substantial contribution to groupprofitability.

Our aspirational vision is to be the worlds mostcustomer driven, innovative and trusted provider of

wealth creation and protection products.

Norwich Union Life is to be a market leading providerof Life, Pensions and Long Term financial servicesproducts in the UK and to generate superior return

on capital and substantial contribution to groupprofitability.

Our aspirational vision is to be the worlds mostcustomer driven, innovative and trusted provider of

wealth creation and protection products.

Norwich Union VisionNorwich Union Vision