Embed Size (px)

Citation preview

William Chittenden edited and updated the PowerPoint slides for this edition.

MANAGING NONINTEREST INCOME & NONINTEREST EXPENSE

Chapter 3

Bank ManagementBank Management, 6th edition.6th edition.Timothy W. Koch and S. Scott MacDonaldTimothy W. Koch and S. Scott MacDonaldCopyright © 2006 by South-Western, a division of Thomson Learning

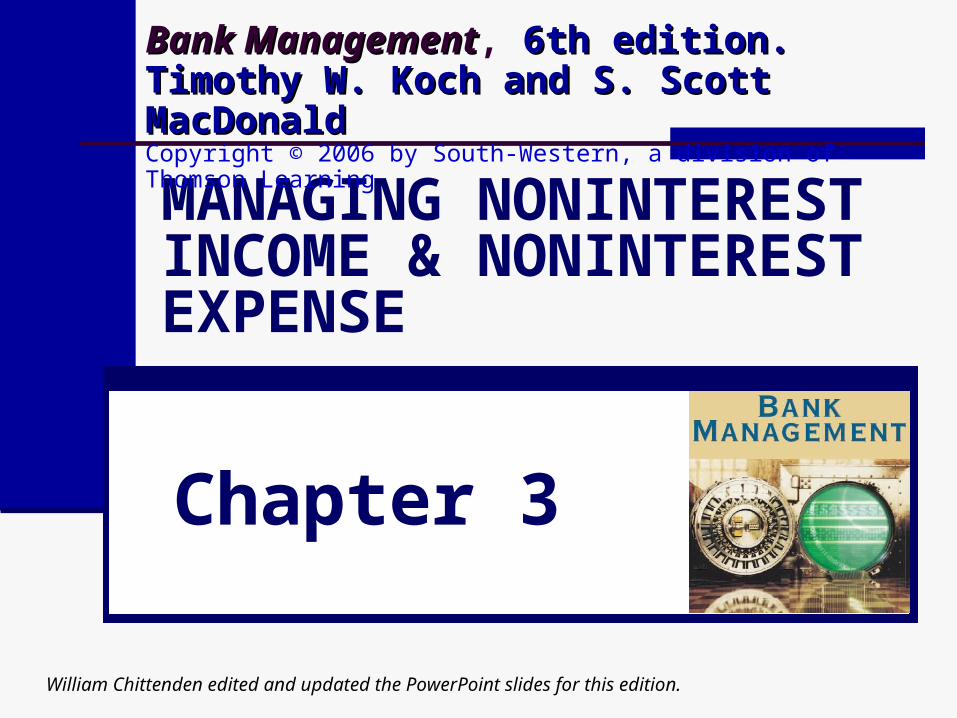

Issues in Interest Income and Interest Expense Deregulation in the 1990s lead to an

increase in competition Average NIM fell since 1992 due to this

increased competitionNet Interest Margin over Time

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

'34 '39 '44 '49 '54 '59 '64 '69 '74 '79 '84 '89 '94 '99 '04

19924.32%

20043.61%

19451.46%

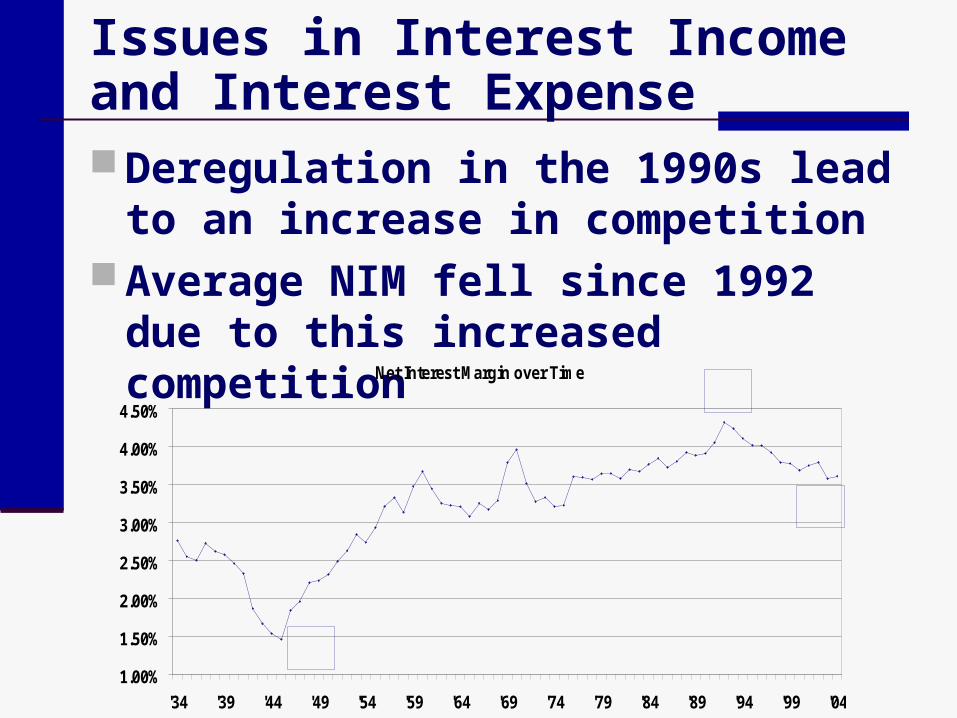

Net Interest Margins by Bank Asset Size, 1992–2004

3.4%

3.6%

3.8%

4.0%

4.2%

4.4%

4.6%

4.8%

5.0%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Net

Inte

rest

Mar

gins $100M - $B

< $100M

> $1B

Issues in Interest Income and Interest Expense Core deposit growth has slowed due

to “disintermediation” Loan yields have fallen on a relative

basis due to credit scoring and increased competition among lenders

NIM is being squeezed, so banks must concentrate more on non-interest income to grow profits.

Issues in Non-Interest Income and Non-Interest Expense Banks must rely less on net interest

income and more on non-interest income to be more successful Banks must grow their non-interest

income relative to non-interest expense if they want to see net income grow.

Issues in Non-Interest Income and Non-Interest Expense The highest earning banks will be

those that generate an increasing share of operating revenue from non-interest sources, like fee income All fees are NOT created equal

Some fees are stable and predictable over time, while others are highly volatile because they are cyclical

Consider NSF charges on checkwriting

Sources of Non-Interest Income Fiduciary Activities Deposit Service Charges Trading Revenue, Venture Capital Revenue, and

Securitization Income Investment Banking, Advisory, Brokerage, and

Underwriting Fees and Commissions Insurance Commission Fees and Income Net Servicing Fees Net Gains (Losses) on Sales of Loans Other Net Gains (Losses)

Sale of premises and other fixed assets Other Non-Interest Income

Safe Deposit, Money Order & Notary Fees

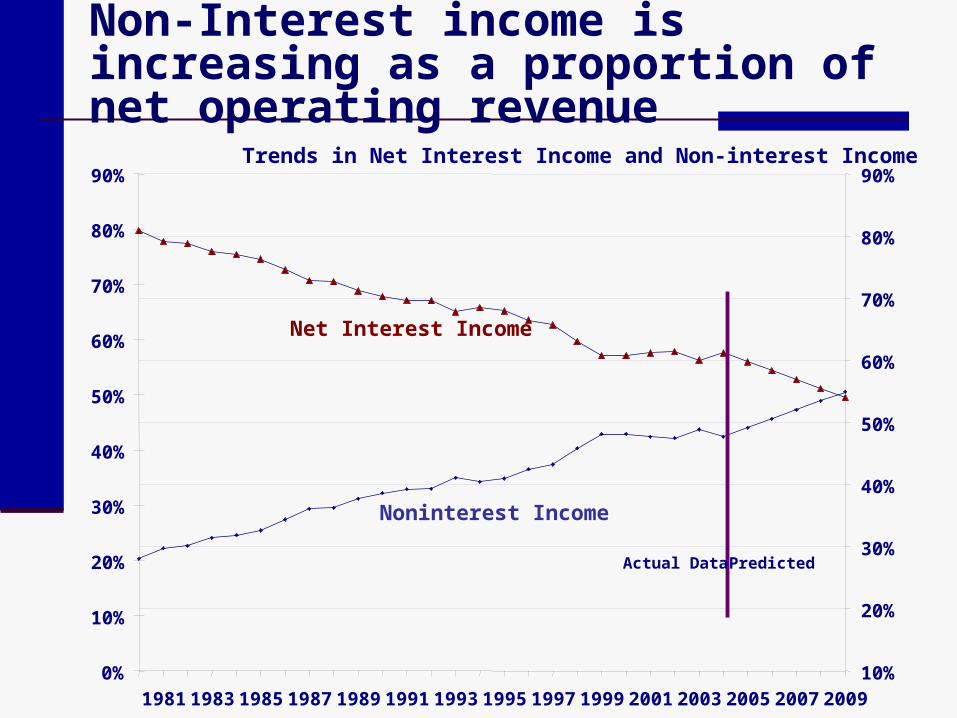

Non-Interest Income is increasing as a proportion of net operating revenue

Largest contributors are deposit service charges and other non-interest income

Largest banks rely more on non-interest income than their smaller counterparts

Composition of Noninterest Income by Bank Size as a Percentage of Total Assets, 2004

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%D

epos

itse

rvic

ech

arge

s

Fidu

ciar

yac

tiviti

es

Trad

ing,

vent

ure

cap.

and

secu

ritiz

atio

ns

Net

ser

vici

ngfe

es

Inve

stm

ent

bank

ing,

advi

sory

,br

oker

age,

Net

gai

ns(lo

sses

) on

sale

s of

loan

san

d ot

her

Net

gai

ns(lo

sses

) on

othe

r ass

ets

Oth

erno

nint

eres

tin

com

e

< $100M $100M-$1B>$1B All Comm. Banks

Non-Interest income is increasing as a proportion of net operating revenue

Trends in Net Interest Income and Non-interest Income

10%

20%

30%

40%

50%

60%

70%

80%

90%

2009200720052003200119991997199519931991198919871985198319810%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Net Interest Income

Noninterest Income

Actual Data Predicted

Deposit Service Fees

Stable source of revenue Relatively price inelastic What level of fees is too high given a

bank’s desire for strong customer relationships?

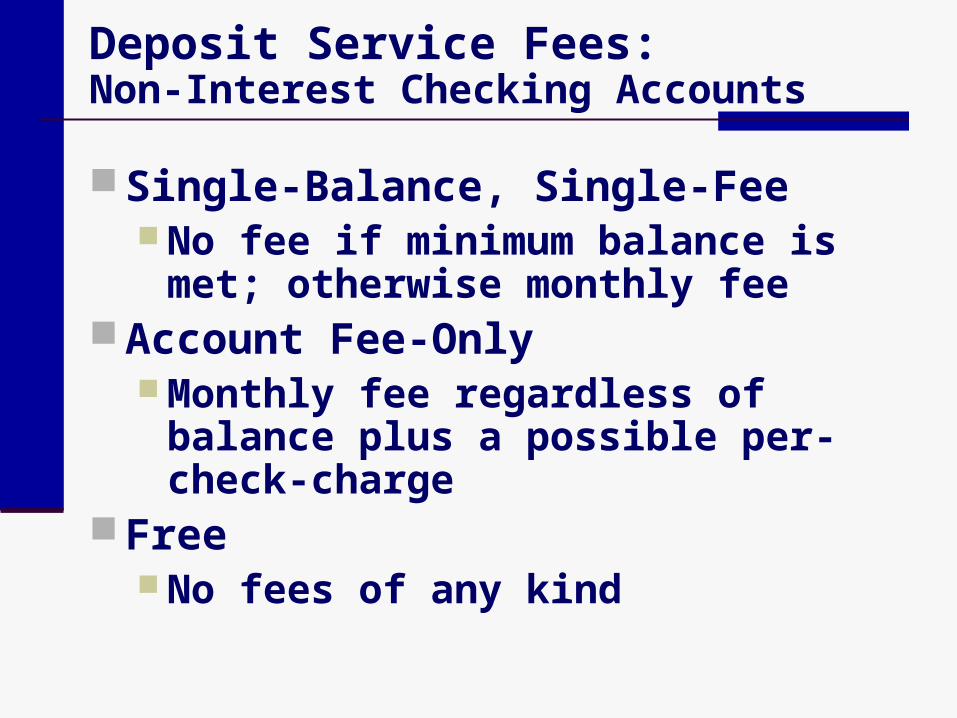

Deposit Service Fees:Non-Interest Checking Accounts

Single-Balance, Single-Fee No fee if minimum balance is met;

otherwise monthly fee Account Fee-Only

Monthly fee regardless of balance plus a possible per-check-charge

Free No fees of any kind

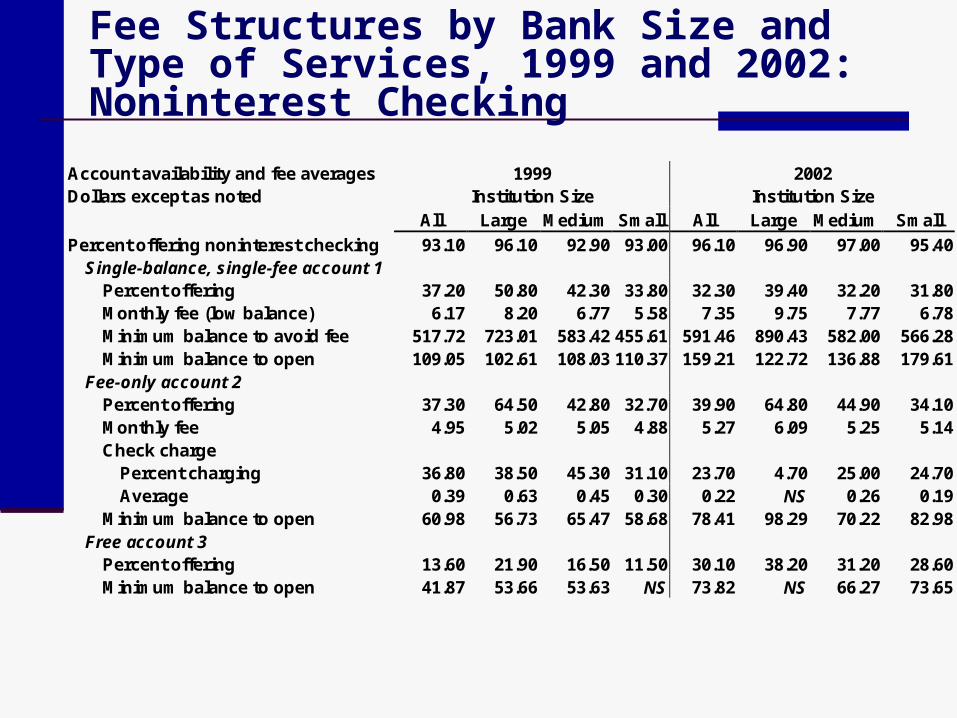

Fee Structures by Bank Size and Type of Services, 1999 and 2002: Noninterest Checking

Account availability and fee averages 1999 2002 Dollars except as noted Institution Size Institution Size All Large Medium Small All Large Medium Small Percent offering noninterest checking 93.10 96.10 92.90 93.00 96.10 96.90 97.00 95.40

Single-balance, single-fee account 1 Percent offering 37.20 50.80 42.30 33.80 32.30 39.40 32.20 31.80 Monthly fee (low balance) 6.17 8.20 6.77 5.58 7.35 9.75 7.77 6.78 Minimum balance to avoid fee 517.72 723.01 583.42 455.61 591.46 890.43 582.00 566.28 Minimum balance to open 109.05 102.61 108.03 110.37 159.21 122.72 136.88 179.61

Fee-only account 2 Percent offering 37.30 64.50 42.80 32.70 39.90 64.80 44.90 34.10 Monthly fee 4.95 5.02 5.05 4.88 5.27 6.09 5.25 5.14 Check charge

Percent charging 36.80 38.50 45.30 31.10 23.70 4.70 25.00 24.70 Average 0.39 0.63 0.45 0.30 0.22 NS 0.26 0.19

Minimum balance to open 60.98 56.73 65.47 58.68 78.41 98.29 70.22 82.98 Free account 3

Percent offering 13.60 21.90 16.50 11.50 30.10 38.20 31.20 28.60 Minimum balance to open 41.87 53.66 53.63 NS 73.82 NS 66.27 73.65

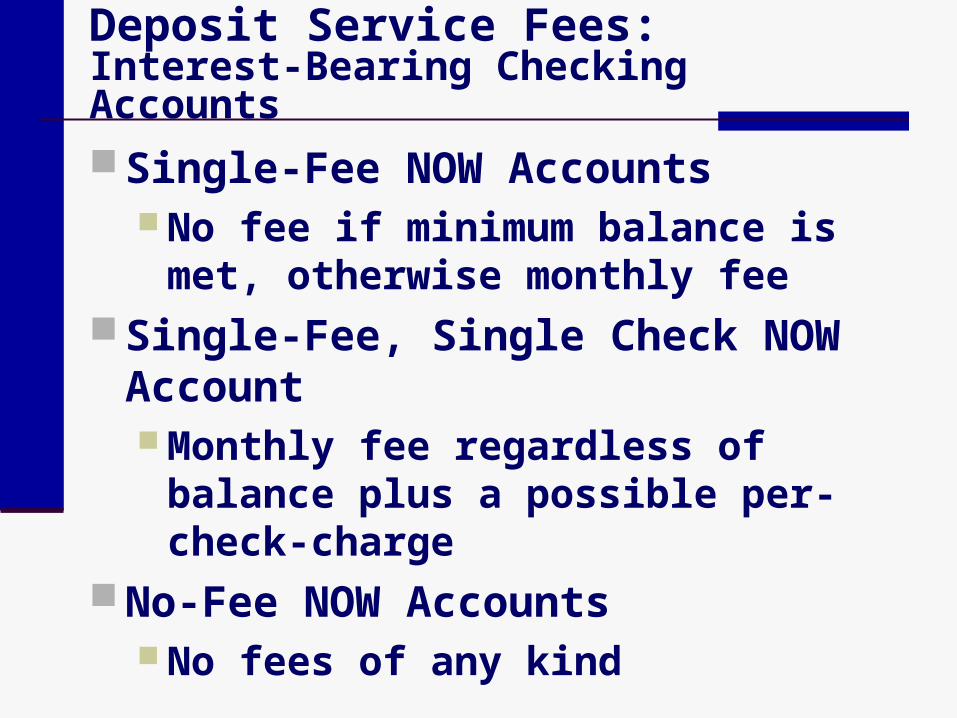

Deposit Service Fees:Interest-Bearing Checking Accounts

Single-Fee NOW Accounts No fee if minimum balance is met,

otherwise monthly fee Single-Fee, Single Check NOW

Account Monthly fee regardless of balance plus

a possible per-check-charge No-Fee NOW Accounts

No fees of any kind

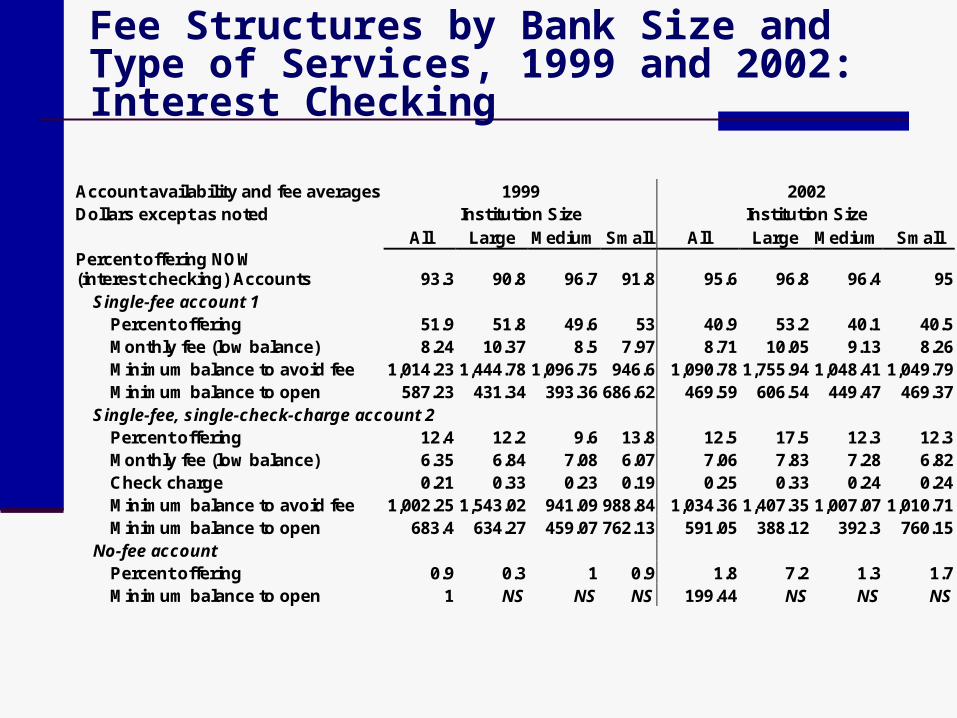

Fee Structures by Bank Size and Type of Services, 1999 and 2002: Interest Checking

Account availability and fee averages 1999 2002 Dollars except as noted Institution Size Institution Size All Large Medium Small All Large Medium Small Percent offering NOW (interest checking) Accounts 93.3 90.8 96.7 91.8 95.6 96.8 96.4 95

Single-fee account 1 Percent offering 51.9 51.8 49.6 53 40.9 53.2 40.1 40.5 Monthly fee (low balance) 8.24 10.37 8.5 7.97 8.71 10.05 9.13 8.26 Minimum balance to avoid fee 1,014.23 1,444.78 1,096.75 946.6 1,090.78 1,755.94 1,048.41 1,049.79 Minimum balance to open 587.23 431.34 393.36 686.62 469.59 606.54 449.47 469.37

Single-fee, single-check-charge account 2 Percent offering 12.4 12.2 9.6 13.8 12.5 17.5 12.3 12.3 Monthly fee (low balance) 6.35 6.84 7.08 6.07 7.06 7.83 7.28 6.82 Check charge 0.21 0.33 0.23 0.19 0.25 0.33 0.24 0.24 Minimum balance to avoid fee 1,002.25 1,543.02 941.09 988.84 1,034.36 1,407.35 1,007.07 1,010.71 Minimum balance to open 683.4 634.27 459.07 762.13 591.05 388.12 392.3 760.15

No-fee account Percent offering 0.9 0.3 1 0.9 1.8 7.2 1.3 1.7 Minimum balance to open 1 NS NS NS 199.44 NS NS NS

Deposit Service Fees:Special Fees

NSF Checks Check is returned

Overdrafts Check is honored

Deposit Items Returned Stop-Payment Order

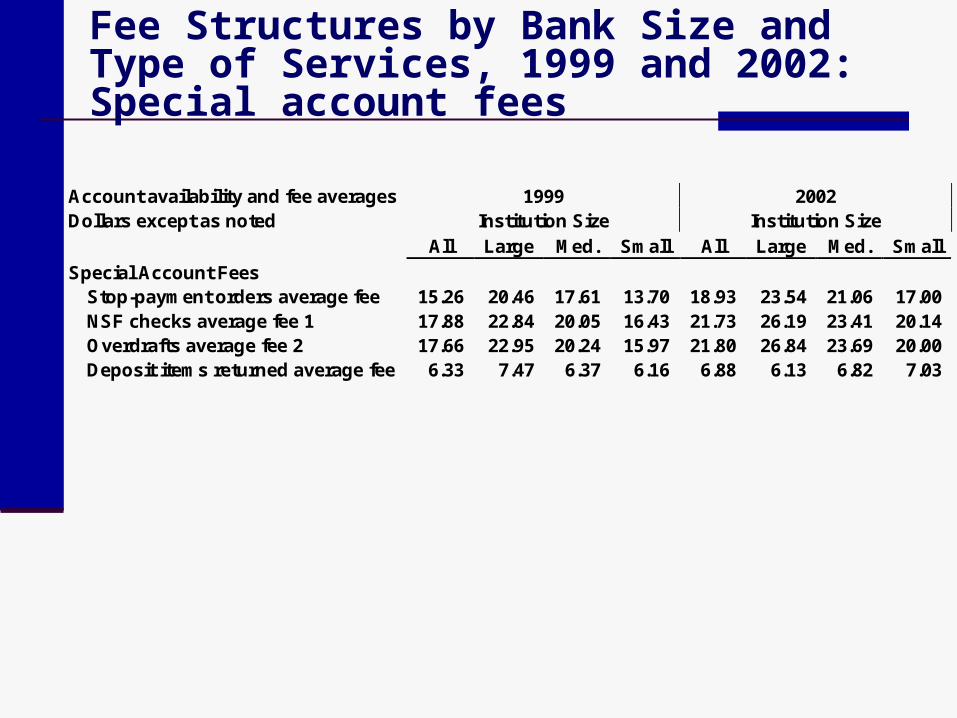

Fee Structures by Bank Size and Type of Services, 1999 and 2002: Special account fees

Account availability and fee averages 1999 2002 Dollars except as noted Institution Size Institution Size All Large Med. Small All Large Med. Small Special Account Fees

Stop-payment orders average fee 15.26 20.46 17.61 13.70 18.93 23.54 21.06 17.00 NSF checks average fee 1 17.88 22.84 20.05 16.43 21.73 26.19 23.41 20.14 Overdrafts average fee 2 17.66 22.95 20.24 15.97 21.80 26.84 23.69 20.00 Deposit items returned average fee 6.33 7.47 6.37 6.16 6.88 6.13 6.82 7.03

Deposit Service Fees:ATM Services

Annual Fees ATM Card Fees “On us” Withdrawal Fees

Fees levied on bank’s own customers for withdrawals from the bank’s own ATMs

“On others” Withdrawal Fees Fees levied on bank’s own customers

for withdrawals from another bank’s ATM

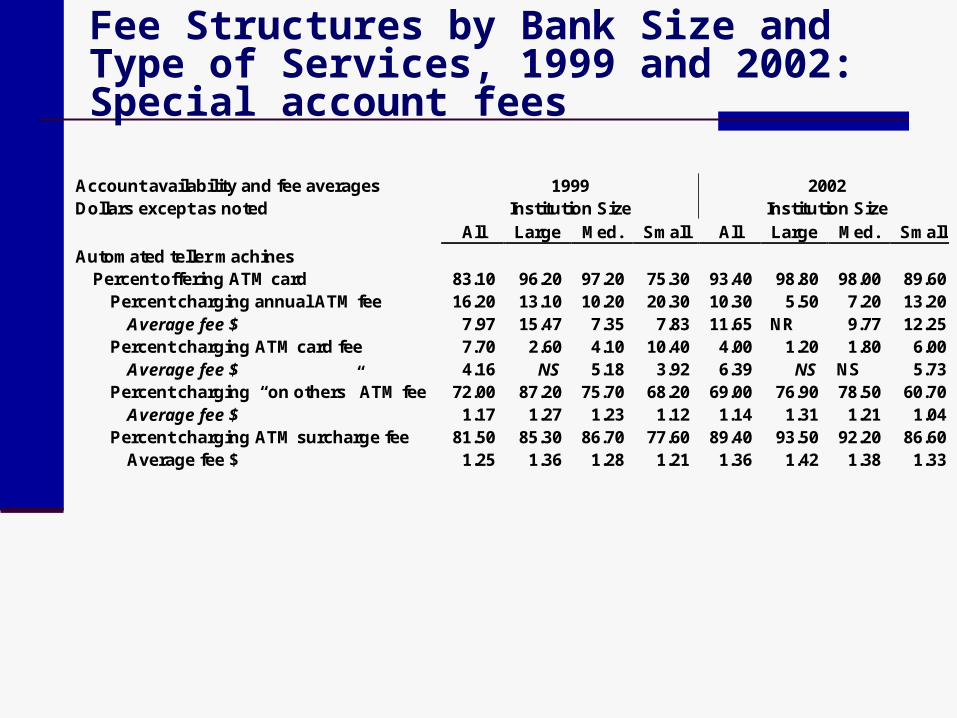

Fee Structures by Bank Size and Type of Services, 1999 and 2002: Special account fees

Account availability and fee averages 1999 2002 Dollars except as noted Institution Size Institution Size All Large Med. Small All Large Med. Small Automated teller machines

Percent offering ATM card 83.10 96.20 97.20 75.30 93.40 98.80 98.00 89.60 Percent charging annual ATM fee 16.20 13.10 10.20 20.30 10.30 5.50 7.20 13.20

Average fee $ 7.97 15.47 7.35 7.83 11.65 NR 9.77 12.25 Percent charging ATM card fee 7.70 2.60 4.10 10.40 4.00 1.20 1.80 6.00

Average fee $ 4.16 NS 5.18 3.92 6.39 NS NS 5.73 Percent charging “on others” ATM fee 72.00 87.20 75.70 68.20 69.00 76.90 78.50 60.70

Average fee $ 1.17 1.27 1.23 1.12 1.14 1.31 1.21 1.04 Percent charging ATM surcharge fee 81.50 85.30 86.70 77.60 89.40 93.50 92.20 86.60

Average fee $ 1.25 1.36 1.28 1.21 1.36 1.42 1.38 1.33

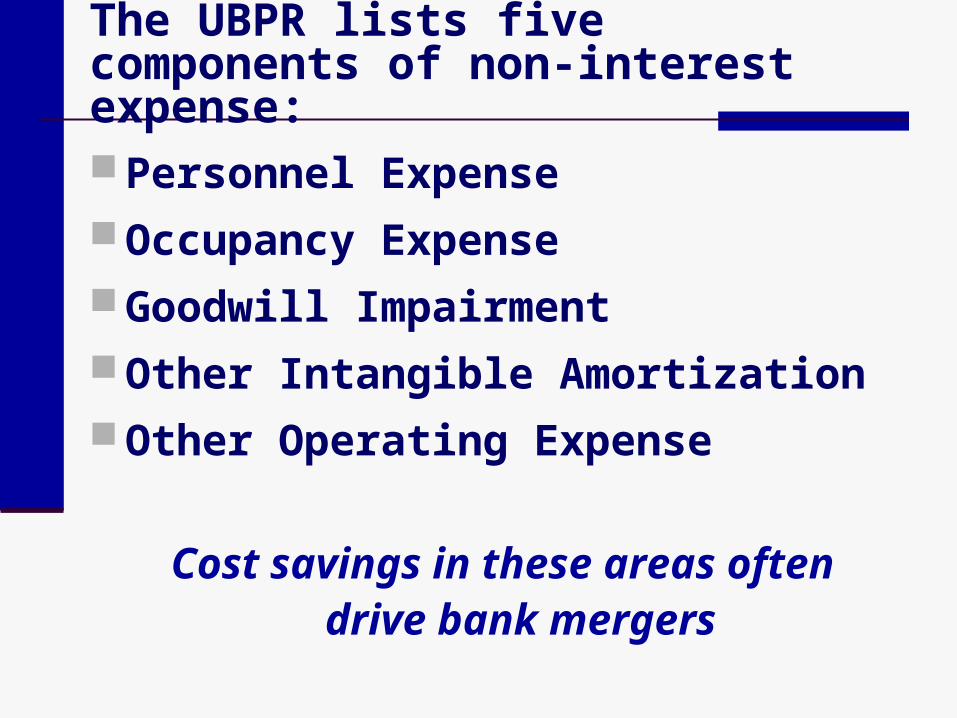

The UBPR lists five components of non-interest expense:

Personnel Expense Occupancy Expense Goodwill Impairment Other Intangible Amortization Other Operating Expense

Cost savings in these areas oftendrive bank mergers

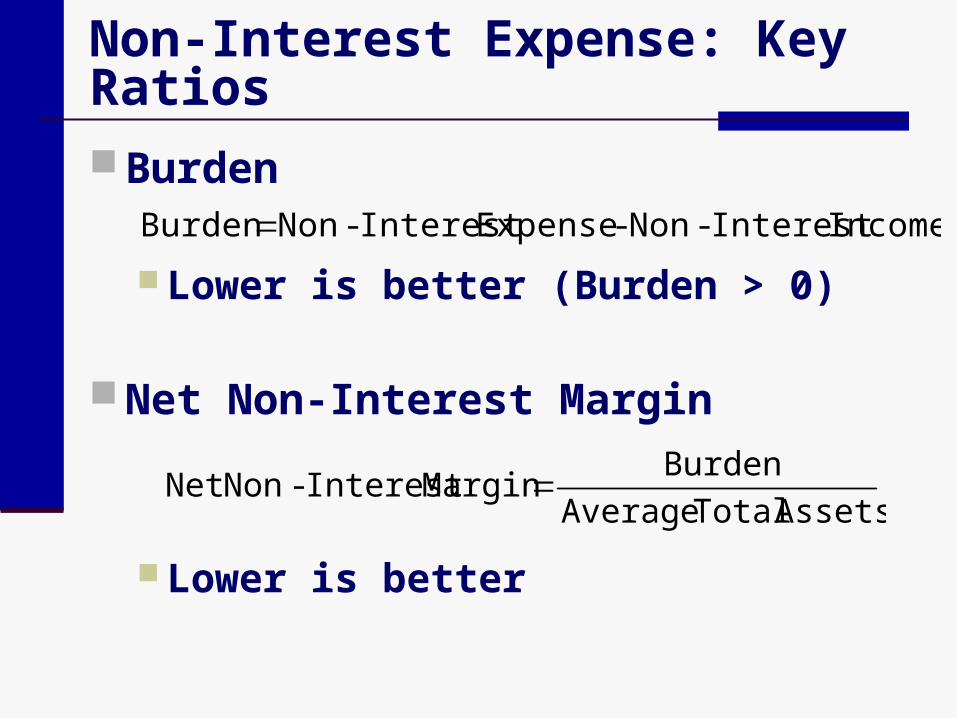

Non-Interest Expense: Key Ratios

Burden

Lower is better (Burden > 0)

Net Non-Interest Margin

Lower is better

Income Interest-Non - Expense Interest-Non Burden

Assets Total AverageBurden Margin Interest-Non Net

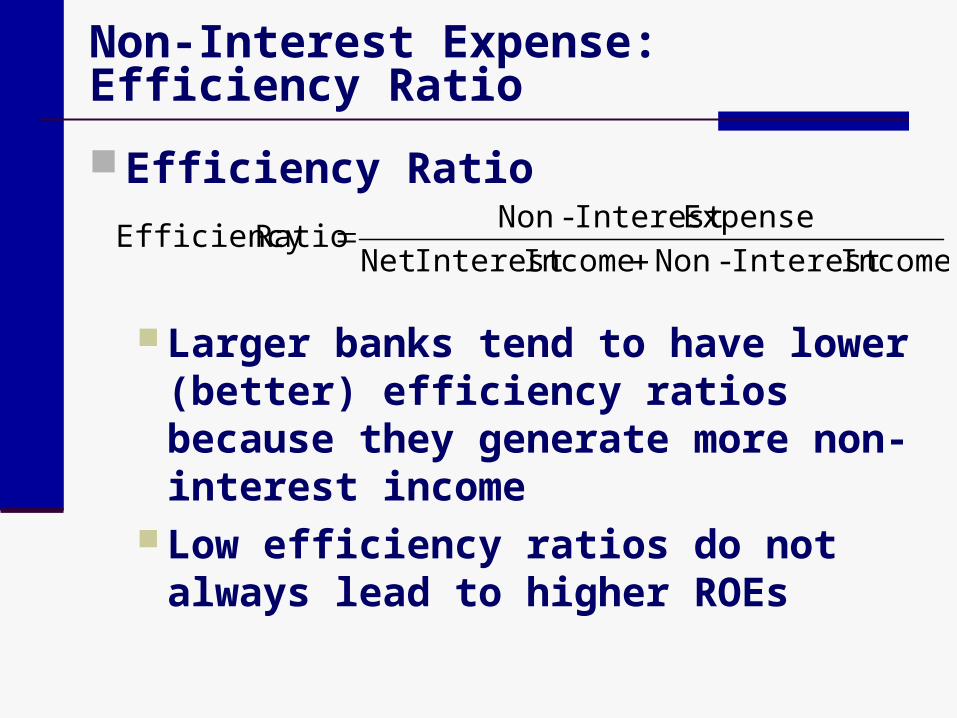

Non-Interest Expense: Efficiency Ratio

Efficiency Ratio

Larger banks tend to have lower (better) efficiency ratios because they generate more non-interest income

Low efficiency ratios do not always lead to higher ROEs

Income Interest-Non Income Interest NetExpense Interest-Non Ratio Efficiency

Efficiency Ratios of U.S. Commercial Banks, 1992–2004

50.0%

55.0%

60.0%

65.0%

70.0%

75.0%

Dec

-92

Dec

-93

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

<$100M

$100M-$1B

>$1B

Effic

ienc

y R

atio

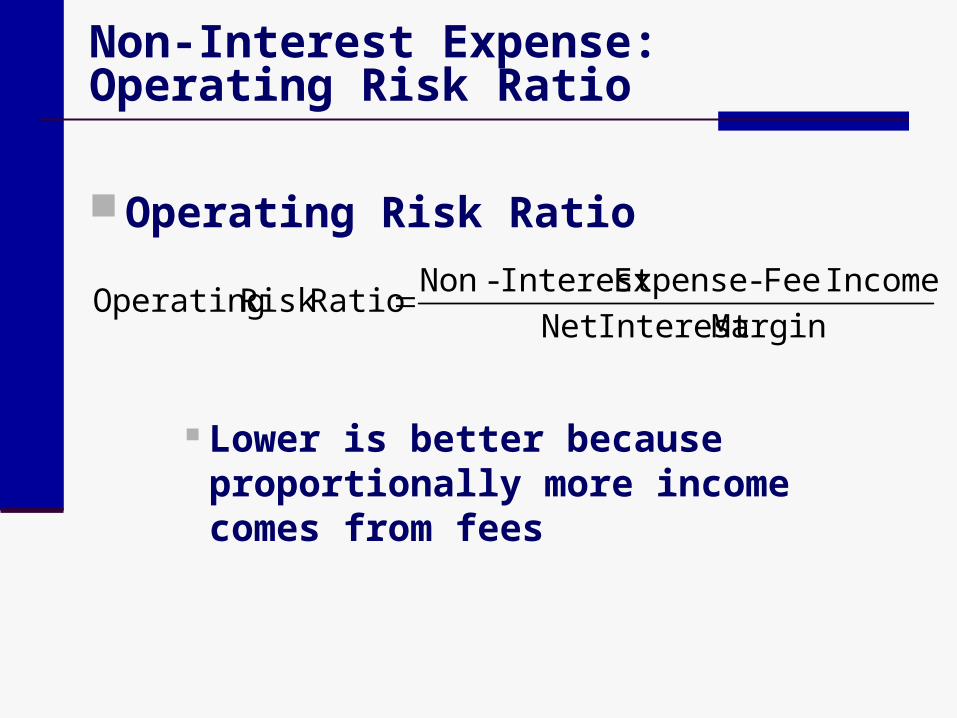

Non-Interest Expense: Operating Risk Ratio

Operating Risk Ratio

Lower is better because proportionally more income comes from fees

Margin Interest NetIncome Fee - Expense Interest-Non Ratio Risk Operating

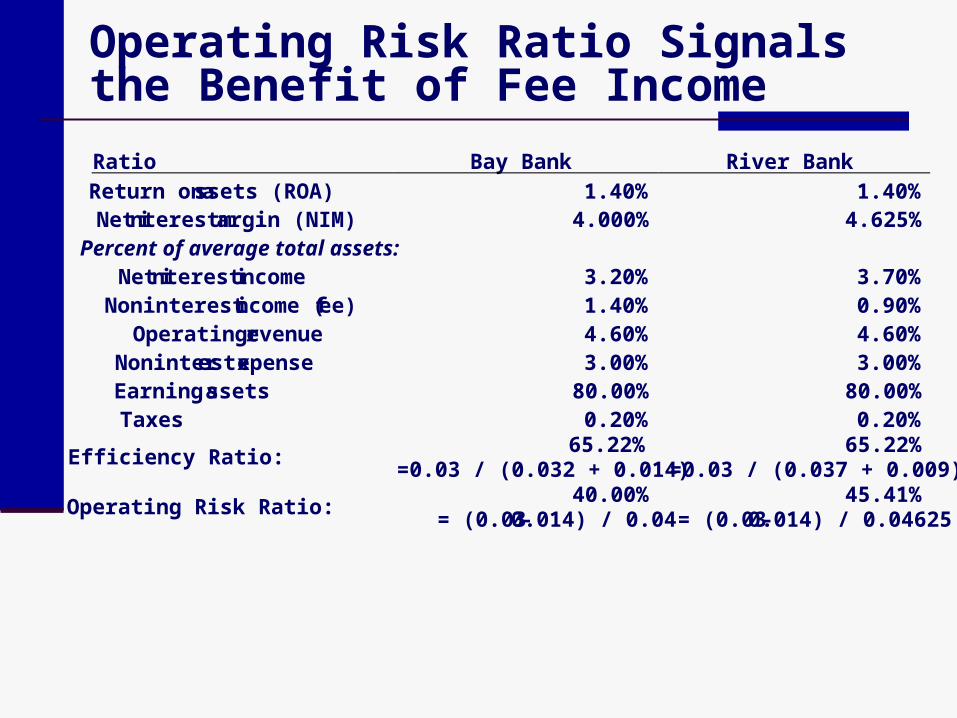

Operating Risk Ratio Signals the Benefit of Fee Income

Ratio Bay Bank River Bank Return on assets (ROA) 1.40% 1.40% Net interest margin (NIM) 4.000% 4.625% Percent of average total assets:

Net interest income 3.20% 3.70% Noninterest income (fee) 1.40% 0.90%

Operating revenue 4.60% 4.60% Noninterest expense 3.00% 3.00% Earning assets 80.00% 80.00% Taxes 0.20% 0.20%

Efficiency Ratio: 65.22% =0.03 / (0.032 + 0.014)

65.22% =0.03 / (0.037 + 0.009)

Operating Risk Ratio: 40.00% = (0.03 - 0.014) / 0.04

45.41% = (0.03 - 0.014) / 0.04625

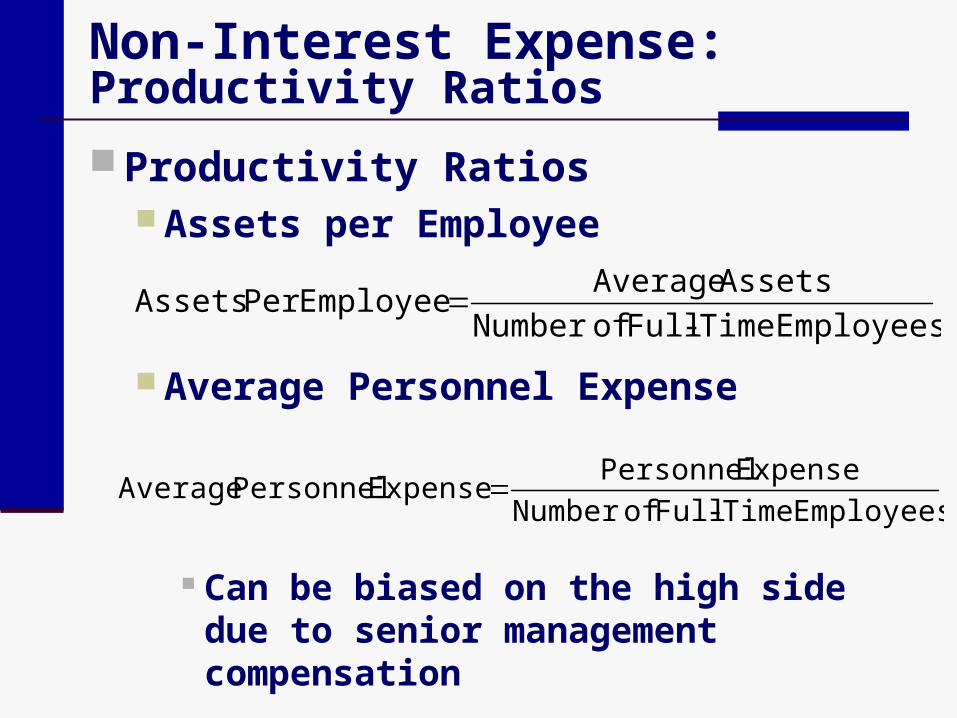

Non-Interest Expense:Productivity Ratios Productivity Ratios

Assets per Employee

Average Personnel Expense

Can be biased on the high side due to senior management compensation

Employees Time-Full of NumberAssets Average Employee Per Assets

Employees Time-Full of NumberExpense Personnel Expense Personnel Average

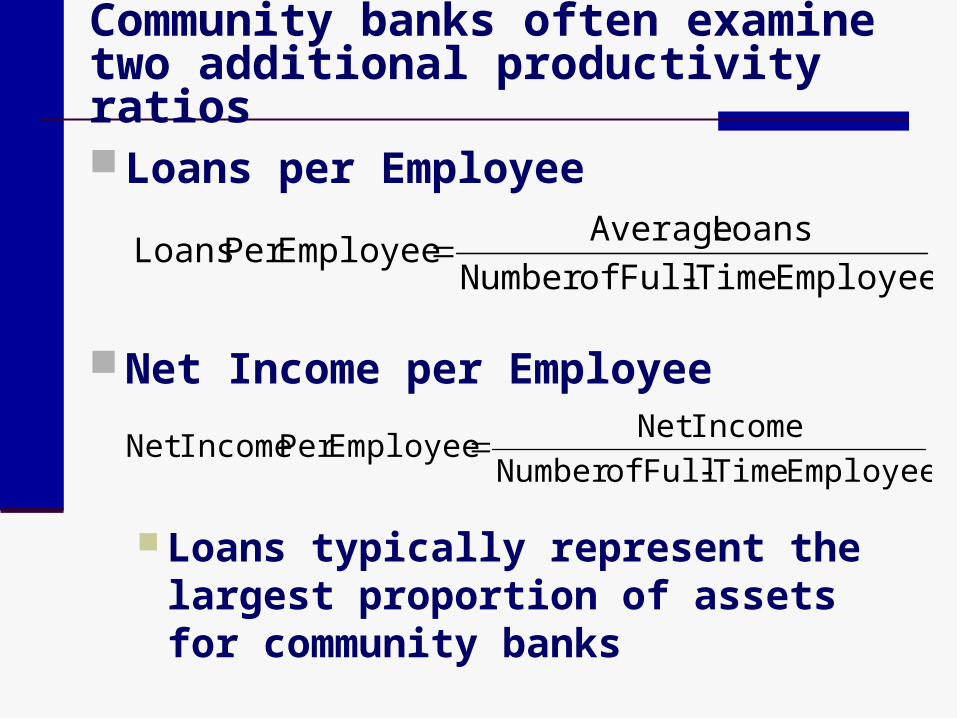

Community banks often examine two additional productivity ratios

Loans per Employee

Net Income per Employee

Loans typically represent the largest proportion of assets for community banks

Employees Time-Full ofNumber Loans Average EmployeePer Loans

Employees Time-Full ofNumber IncomeNet EmployeePer IncomeNet

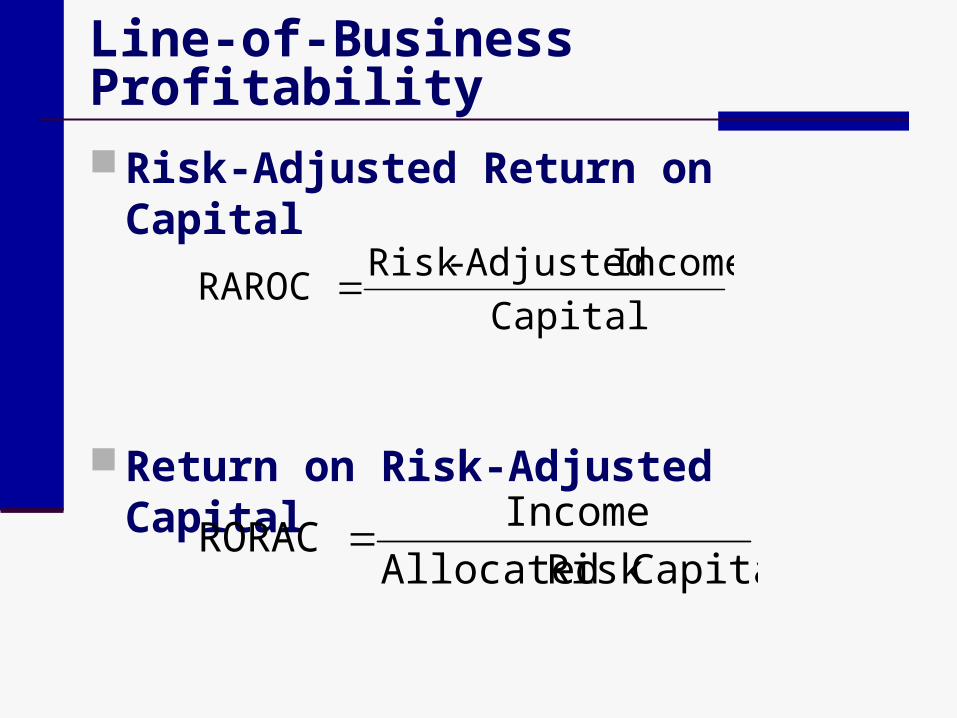

Line-of-Business Profitability

Risk-Adjusted Return on Capital

Return on Risk-Adjusted Capital

CapitalIncome Adjusted -Risk RAROC

CapitalRisk AllocatedIncome RORAC

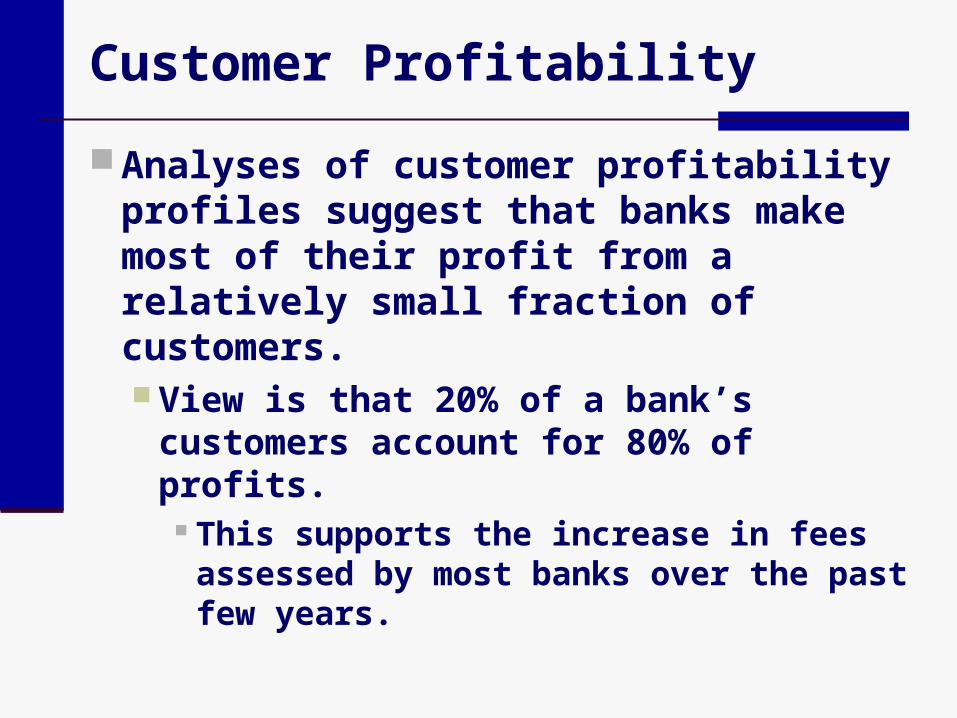

Customer Profitability

Analyses of customer profitability profiles suggest that banks make most of their profit from a relatively small fraction of customers. View is that 20% of a bank’s customers

account for 80% of profits. This supports the increase in fees

assessed by most banks over the past few years.

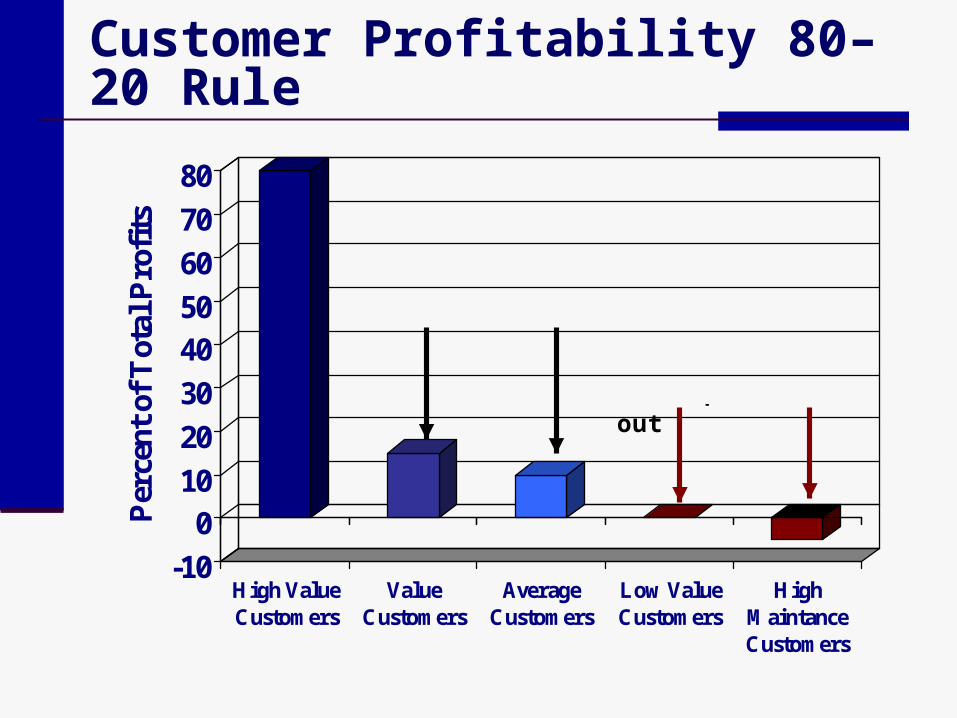

Customer Profitability 80–20 Rule

-100

1020304050607080Pe

rcen

t of T

otal

Pro

fits

High ValueCustomers

ValueCustomers

AverageCustomers

Low ValueCustomers

HighMaintanceCustomers

Who are they, what do they need?

How do you move them up?

Move up or move out

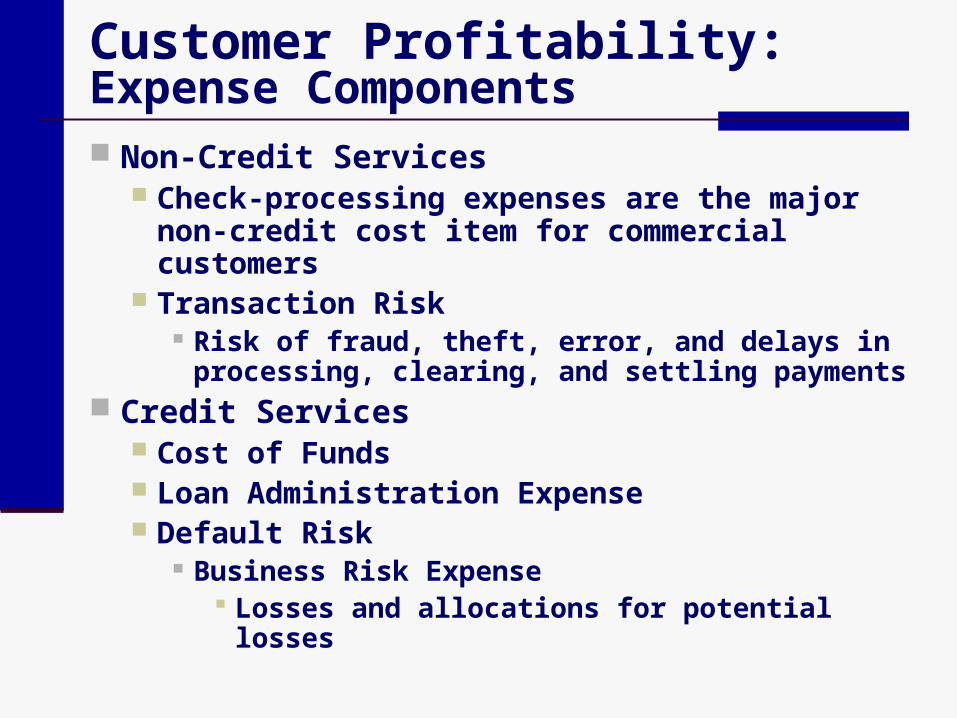

Customer Profitability: Expense Components Non-Credit Services

Check-processing expenses are the major non-credit cost item for commercial customers

Transaction Risk Risk of fraud, theft, error, and delays in

processing, clearing, and settling payments Credit Services

Cost of Funds Loan Administration Expense Default Risk

Business Risk Expense Losses and allocations for potential losses

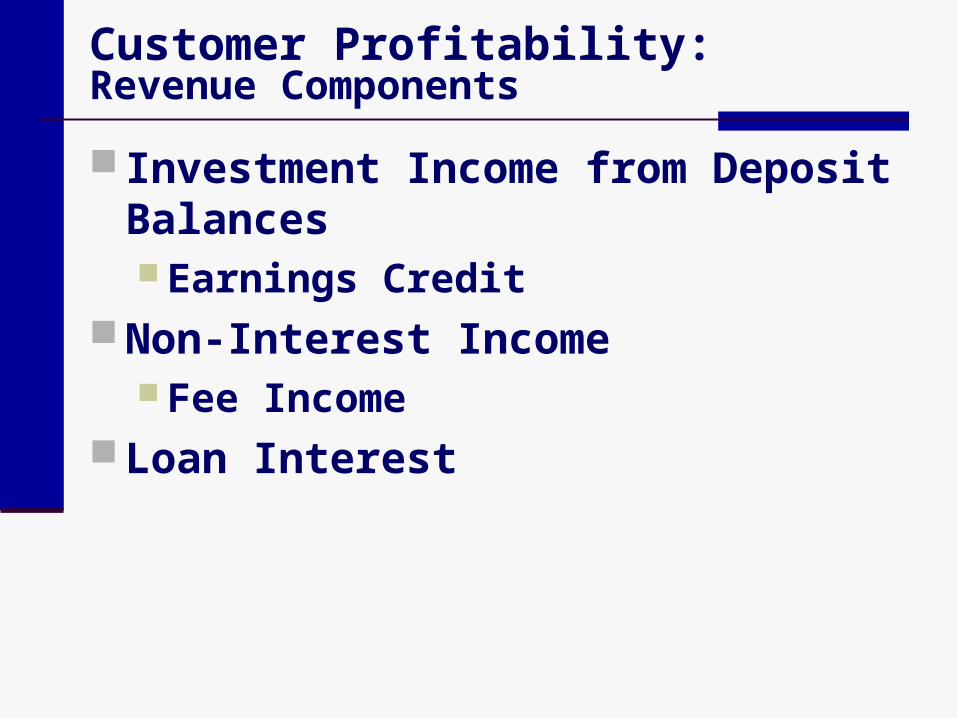

Customer Profitability:Revenue Components

Investment Income from Deposit Balances Earnings Credit

Non-Interest Income Fee Income

Loan Interest

Customer Profitability:Aggregate Profitability Results

Profitable customers maintain multiple relationships with the bank

Unprofitable customers tend to “shop” for the lowest price and do not use multiple products

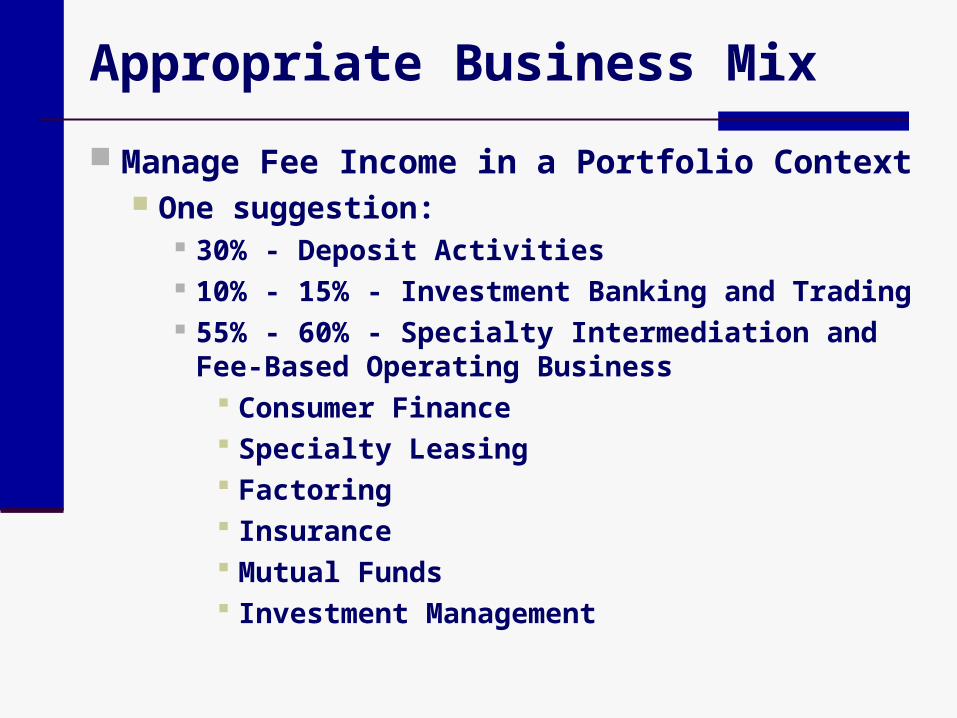

Appropriate Business Mix

Manage Fee Income in a Portfolio Context One suggestion:

30% - Deposit Activities 10% - 15% - Investment Banking and Trading 55% - 60% - Specialty Intermediation and Fee-

Based Operating Business Consumer Finance Specialty Leasing Factoring Insurance Mutual Funds Investment Management

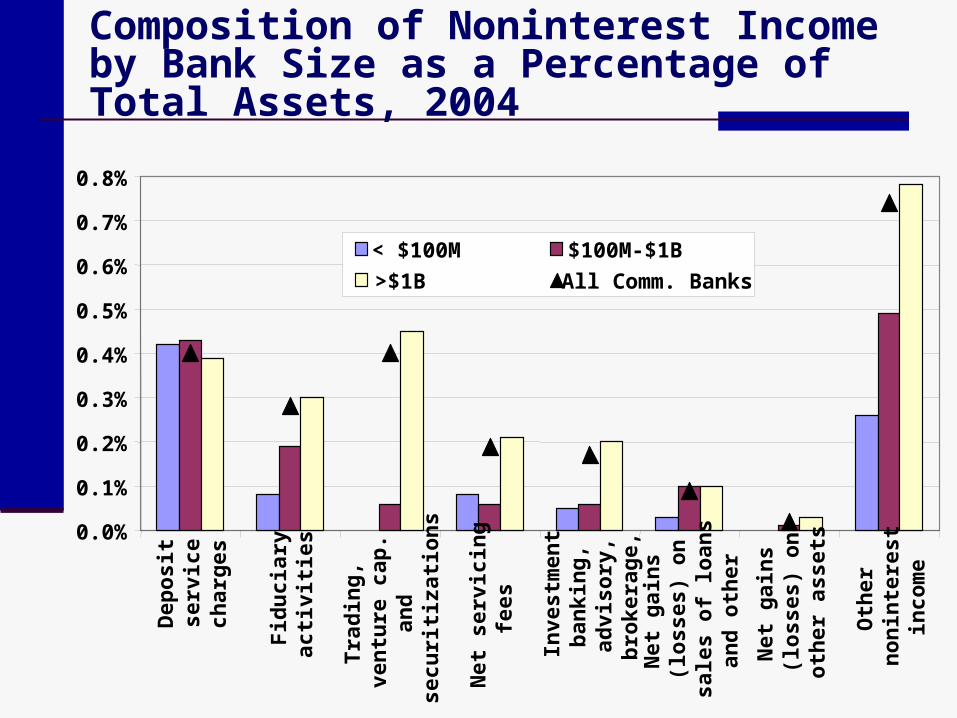

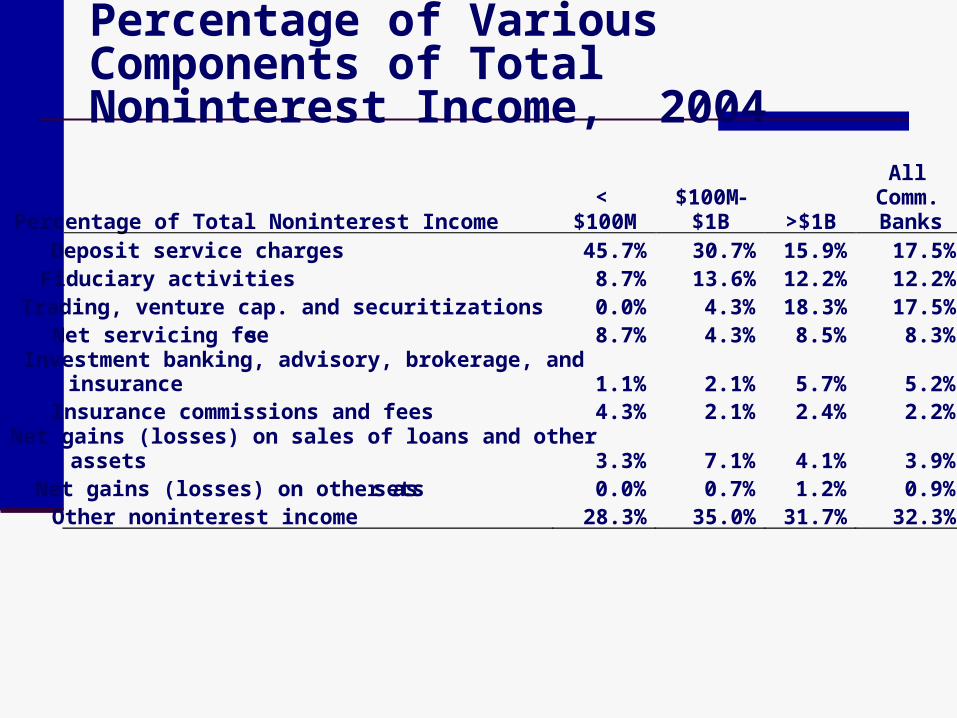

Percentage of Various Components of Total Noninterest Income, 2004

Percentage of Total Noninterest Income <

$100M $100M-

$1B >$1B

All Comm. Banks

Deposit service charges 45.7% 30.7% 15.9% 17.5% Fiduciary activities 8.7% 13.6% 12.2% 12.2% Trading, venture cap. and securitizations 0.0% 4.3% 18.3% 17.5% Net servicing fees 8.7% 4.3% 8.5% 8.3% Investment banking, advisory, brokerage, and insurance 1.1% 2.1% 5.7% 5.2% Insurance commissions and fees 4.3% 2.1% 2.4% 2.2% Net gains (losses) on sales of loans and other assets 3.3% 7.1% 4.1% 3.9% Net gains (losses) on other assets 0.0% 0.7% 1.2% 0.9% Other noninterest income 28.3% 35.0% 31.7% 32.3%

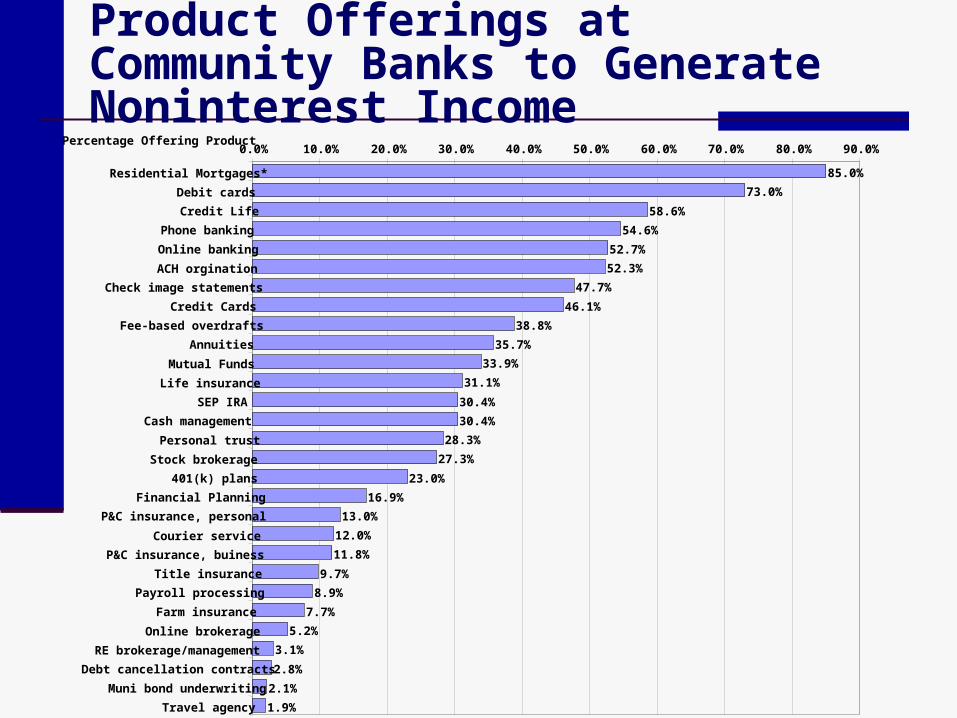

Product Offerings at Community Banks to Generate Noninterest Income

Percentage Offering Product

85.0%73.0%

58.6%54.6%

52.7%52.3%

47.7%46.1%

38.8%35.7%

33.9%31.1%

30.4%30.4%

28.3%27.3%

23.0%16.9%

13.0%12.0%11.8%

9.7%8.9%

7.7%5.2%

3.1%2.8%

2.1%1.9%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0%

Residential Mortgages*Debit cardsCredit Life

Phone bankingOnline bankingACH orgination

Check image statementsCredit Cards

Fee-based overdraftsAnnuities

Mutual FundsLife insurance

SEP IRACash management

Personal trustStock brokerage

401(k) plansFinancial Planning

P&C insurance, personalCourier service

P&C insurance, buinessTitle insurance

Payroll processingFarm insurance

Online brokerageRE brokerage/managementDebt cancellation contracts

Muni bond underwritingTravel agency

Strategies to Manage Non-Interest Expense

Cost Management Strategies Expense Reduction Operating Efficiencies Revenue Enhancement

Cost Management StrategiesExpense Reduction Be careful not to just focus on reducing

costs, rather, move them in line with strategic objectives.

Begin by identifying excessive expenses and eliminating them Largest non-interest expenses are personnel,

occupancy, and data processing costs. These are often the areas where cuts are initially made.

Outsourcing

Cost Management Strategies:Operating Efficiencies Reducing costs while maintaining

existing level of products and services Increasing the level of output while

maintaining the level of current expenses

Improving work flow (doing things faster)

Operating efficiencies of: Economies of Scale Economies of Scope

Cost Management Strategies:Revenue Enhancement Price Elasticity

Identify products or services that exhibit price inelastic demand

Change the pricing of specific products while maintaining a sufficiently high volume of business so that total revenue increases

Contribution Growth Management allocates resources to best improve

overall long-term profitability Increases in expenses are acceptable, but they must

coincide with greater anticipated increases in associated revenues

In the short-run, expenses rise, but expenses are cut in the long-run

William Chittenden edited and updated the PowerPoint slides for this edition.

MANAGING NONINTEREST INCOME & NONINTEREST EXPENSE

Chapter 3

Bank ManagementBank Management, 6th edition.6th edition.Timothy W. Koch and S. Scott MacDonaldTimothy W. Koch and S. Scott MacDonaldCopyright © 2006 by South-Western, a division of Thomson Learning