Embed Size (px)

Citation preview

Managing revenues from mining –Experience of Mongolia

Tumendelger Baljinnyam

Specialist, Research and Analysis office, Division of Sector Development Policy and

Regulation, National Development Agency, Mongolia

2016-12-07

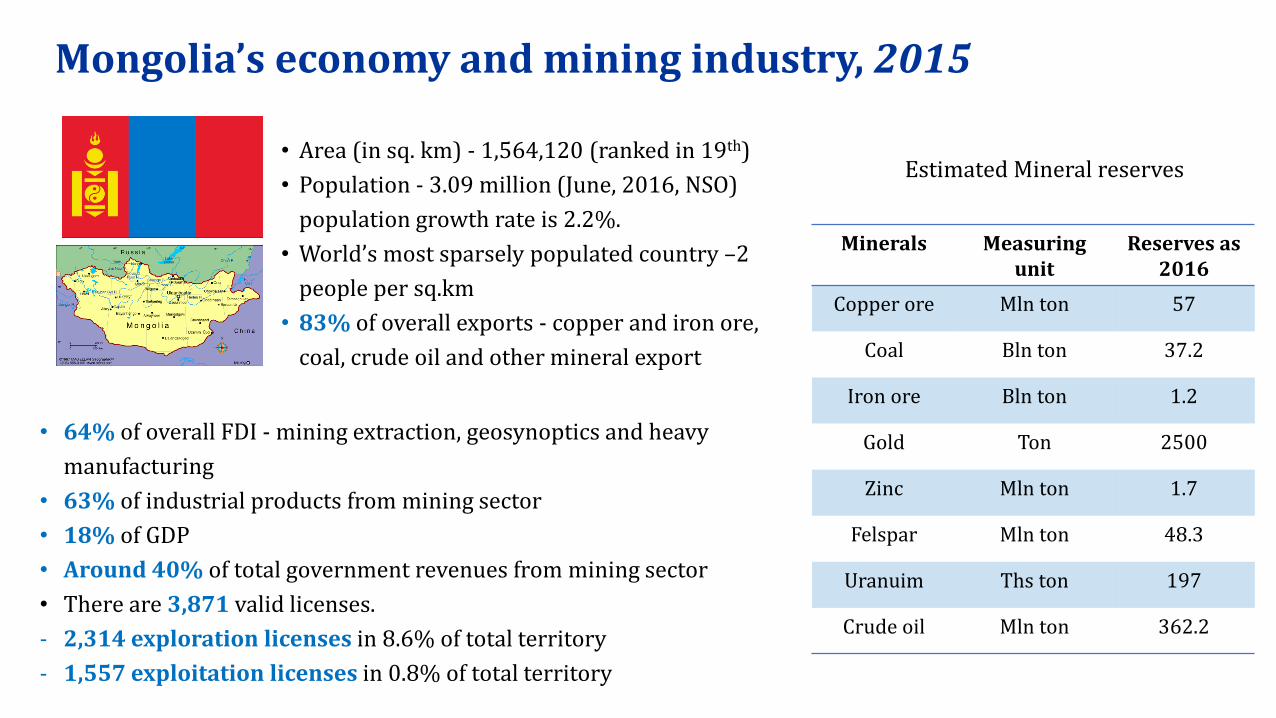

Mongolia’s economy and mining industry, 2015

• 64% of overall FDI - mining extraction, geosynoptics and heavy

manufacturing

• 63% of industrial products from mining sector

• 18% of GDP

• Around 40% of total government revenues from mining sector

• There are 3,871 valid licenses.

- 2,314 exploration licenses in 8.6% of total territory

- 1,557 exploitation licenses in 0.8% of total territory

Minerals Measuringunit

Reserves as 2016

Copper ore Mln ton 57

Coal Bln ton 37.2

Iron ore Bln ton 1.2

Gold Ton 2500

Zinc Mln ton 1.7

Felspar Mln ton 48.3

Uranuim Ths ton 197

Crude oil Mln ton 362.2

Estimated Mineral reserves• Area (in sq. km) - 1,564,120 (ranked in 19th)

• Population - 3.09 million (June, 2016, NSO)

population growth rate is 2.2%.

• World’s most sparsely populated country –2

people per sq.km

• 83% of overall exports - copper and iron ore,

coal, crude oil and other mineral export

• Mining experts estimate that the country possesses as much as $1.3 trillion worth of over 80 different minerals in at least 6000 known deposits. That, in theory, works out to over $333,333 for every man, woman and child in the country.

• Mongolia’s vast mineral resources undoubtedly have a potential to make a significant contribution to country’s economic and social development, but only if they are developed and managed appropriately.

• The challenge for the government is to get the right mix of policies that can to succeed in converting the mineral resources into an inclusive growth path that spreads prosperity to all Mongolians and all provinces (aimags, soums) across the country.

• In order to sustainably reduce poverty and mitigate environmental degradation, it is crucial to include poverty and environmental issues into development policy documents and ensure synergy between such documents.

• In addition to social welfare type of activities, “productive” activities designed to create employment and generate incomes need to be included under poverty reduction actions and expenditures.

Mongolia’s economy and mining industry

• Natural resources revenue sharing is a concept that has gained much attention in Mongolia over the last

decade. Relevant laws and policies were developed and different revenue sharing schemes were tested by the

Government of Mongolia with varying degrees of success over the past years.

• There are a number of studies in Mongolia which assessed the socioeconomic impact of these initiatives and

programs, which focused on their implementations on whether these programs have been implemented in

accordance with the related laws and regulations.

• However, there are no studies that assess whether the design of the system is optimal. Thus, there was a

need to study questions such as: What are the mechanisms of allocating extractive industry revenues among

local governments? How optimal is the allocation mechanism of revenues from the extractive industry,

especially that of Local Development Funds?

• In this regard, UNDP-UNEP Poverty Environment Initiative and UNDP Bangkok Regional Hub have

initiated a Study, recognizing that good management of natural resource revenues as an important

contribution toward poverty and environmental issues.

Natural resources revenue sharing in Mongolia

Extractive Industries Revenue Collection and Distribution System (C/prof/15/019 review study)

• This study was conducted with the funding from UNDP Bangkok Regional Hub and UNDP-UNEP

Poverty-Environment Initiative (PEI), implemented by the Mongolian Ministry of Finance.

Research was carried out by a national consulting company Gerege Partners LLC.

• The main objective of the study was to analyse extractive industry revenue sharing and

distribution system in Mongolia including extractive industry revenue types and magnitudes,

collection mechanisms and vertical and horizontal distribution of extractive industry revenues at

national and sub-national levels.

• Also, the study reviewed whether extractive industry revenues has any impact on reducing

poverty and environmental degradation;

LegislationLEGISLATION ON ADMINISTRATION,

BUDGET, TAXES, MINING REVENUES AND SPECIAL FUNDS

The Constitution of Mongolia

The law on the territorial and administrative units, and their Governing bodies

The budget law

The fiscal stability law

The general taxation law

The law on income tax of economic entities and organizations

The law on gasoline and diesel fuel taxation

The value added tax law

The law on social insurance

The law on immovable property tax

The law on customs tariffs and taxes

The law on Government special funds

The law on the Human development fund

The law on stamp duty

LAWS ON MINERAL RESOURCES, PETROLEUM, AND INDIVIDUAL AND

ENTERPRISES OPERATING IN THIS SECTOR

The law on mineral resources

The law on special permits of business

entity

The law on sending labor force to abroad

and receiving labor force and specialist

from abroad

The investment law

The law on common mineral

The petroleum law

The law on customs

The law on nuclear energy

LAWS ON ENVIRONMENT, WATER AND LAND

The law of environmental protection

The law on Environmental Impact

Assessment

The law on land

The law on land fees

The law on subsoil

The law to prohibit mineral exploration and

mining operations at headwaters of rivers,

protected zones of water reservoirs and

forest

The law on water

The law on air pollution fees

MORE THAN 30 LAWS BEING ENFORCED RELATING TO THE STUDY

Amendments and changes on legislation

Year EI revenue contribution to the

budget

Total budget revenues

Percentage(%)

2010 901.7 2,488.5 36.2

2011 864.0 3,351.4 25.82012 830.8 3,481.2 23.9

2013 1,057.3 4,057.3 26.12014 1,040.9 4,244.3 24.5

Extractive Industry revenue contribution to the State budget (million

MNT)

Where EI revenues came from?/2014/

• Commercial enterprises operating in the EI in Mongolia pay

over 20 types of taxes, mineral royalties, fees and charges

to the state and local budgets.

VAT7.4%

Social and health

insurance7.6%

Petroleum receipt18.7%

Corporate income tax

12.3%

Royalties35.7%

Others18.3%

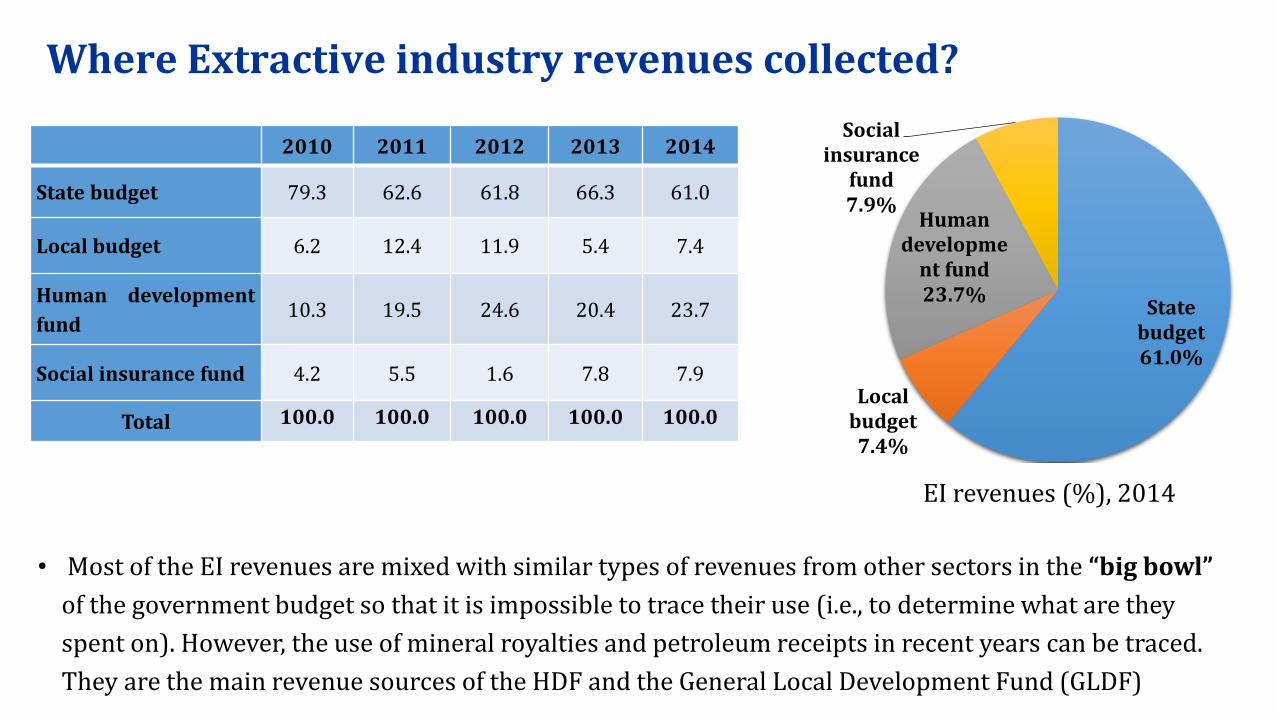

Where Extractive industry revenues collected?

2010 2011 2012 2013 2014

State budget 79.3 62.6 61.8 66.3 61.0

Local budget 6.2 12.4 11.9 5.4 7.4

Human development

fund10.3 19.5 24.6 20.4 23.7

Social insurance fund 4.2 5.5 1.6 7.8 7.9

Total 100.0 100.0 100.0 100.0 100.0

State budget 61.0%

Local budget 7.4%

Human developme

nt fund 23.7%

Social insurance

fund 7.9%

EI revenues (%), 2014

• Most of the EI revenues are mixed with similar types of revenues from other sectors in the “big bowl”

of the government budget so that it is impossible to trace their use (i.e., to determine what are they

spent on). However, the use of mineral royalties and petroleum receipts in recent years can be traced.

They are the main revenue sources of the HDF and the General Local Development Fund (GLDF)

• Between 1992 and the end of 2001, mineral royalties went to local government budgets, while from 2002

until 2006, they were shared by the state and local government budgets. During this time, the shares going

to central and local governments were not specified in in the law or regulations. Since then, the development of

the mining industry intensified and hence the allocation mechanism has been clearly legalized.

• The allocation of EI revenues in 2006-2011 was derivation-based, so that aimags with more developed EI

such as Umnugobi and Orkhon received more revenues than others. However, in 2013-2015 the mechanism

was changed and became more need-based through the allocation of GLDF. From 2016, the allocation

mechanism has become again more derivation-based.

Extractive Industry revenue distribution system

Extractive Industry revenue distribution system

The following EI revenue distribution model is being practiced in Mongolia:E

I re

ve

nu

e d

istr

ibu

tio

n

mo

de

ls1. No specific allocation mechanism of EI revenueEI revenues are paid to the central budget and HDF, and spent in a centralised way. This excludes direct taxes and payments paid to GLDF and aimags/soums.

2А. Specific allocation mechanism of EI revenue - needs-based budget transfersGLDF (funded by 5% of mineral royalties, 25% of VAT etc., )

2B. Specific allocation mechanims of EI revenue - derivation-based budget transfersAllocate more revenues to localities with extractive industries (5% of mineral royalites in GLDF)

3. Specific allocation mechanims of EI revenue - via collection of EI taxesDirect taxes and payments from extractive companies to aimags/ soums

4. Direct transfers.Direct financial transfers from extractive companies to local governments and communities

• Today. Mongolia’s Extractive Industry revenue allocated in:

- Human development fund

- General local development fund and Local development funds

- Community development agreements

Extractive Industry revenue distribution system

Human development fund

• While the Child Money Program and the Human

Development Fund are tools for allocating a part of EI

revenues collected by the government directly to

citizens.

• The Targeted Child Money Program (Jan 2005 - Jun 2006)

was the first of several schemes which were set-up and

implemented by the Government of Mongolia to

redistribute mining revenues since 2005. Subsequent

programs included Universal Child Money Program (Jul

2006 – Dec 2009), Human Development Fund (universal

payments to the whole population of Mongolia in Feb 2010

- Jun 2012), Child Money Program (Oct 2012 onwards).

• Of the EI revenues, 23.7 percent was allocated to the

Human Development Fund (HDF), a type of a wealth fund

in 2014.

HDF revenues and expenditure (MNT billion)

-

200

400

600

800

1,000

2010 2011 2012 2013 2014 2015

Total expenditure and net lending

Total revenue

Tax revenue

• The Local Development Fund initiative is a different policy instrument of delivering a part of the EI

revenues to individuals, by transferring resources from the central government to local governments.

• A Local Development Fund (LDF) initiative has been implementing since 2013.

• The LDFs have generally financed one-time and temporary projects and programs with limited

impact on creating permanent jobs and supporting sustainable development. In addition, due to lack of

guidance (regulation), projects funded by the LDFs tend to be less focused on poverty reduction and

environment– only 10-16 percent of the total is spent on projects more or less related to poverty

reduction and environmental protection. This shows a room for improvement in regulations of the LDF

initiative.

• The current method of allocating the GLDF among the LDFs has several drawbacks. In particular, the Local

Development Index, used as one of the criteria for allocation, has not been updated since 2010.

• In terms of the GLDF, more than 70 percent of the revenues were contributed by 25 percent (reduced to

10 percent since 2016) of domestic VAT payments, and over 10 percent of the GLDF was contributed

by mineral royalties.

Local development funds

Local development funds

LDF amounts allocated to aimags and the capital city in 2013-2015 (per capita, MNT thousand)

<200 200-300 >300

• Within 3 years of implementation of LDF initiative, MNT 468 billion was allocated to aimag and the capital city LDFs.

• Ulaanbaatar city received the largest share equalling MNT 75 billion;

• Gobisumber aimag received the smallest amount (MNT 13 billion);

• All other aimags were allocated between MNT 15 to 23 billion.

In terms of LDF per capita:• Ulaanbaatar city received 55 thousand

tugrugs• Gobisumber got 845 thousand tugrugs

Community development agreements2011 2012 2013 2014

Number of EI companies

that established

agreements with local

governments or

communities (duplicates

possible)

29 50 68 42

Total number of contracts

and agreements39 132 97 167

Of which:

Cooperation

agreements2 4 14 11

Social responsibility

agreements9 18 12 14

Environmental

protection agreements2 4 8 6

Other 26 106 63 136

• Another type of EI revenues is Community

Development Agreements (CDA), although it is not

strictly a type of fiscal revenues.189 companies in

the extractive industry established 435 CDAs with

local authorities in 2011-2014.

• Law on Minerals (2006) states “A license holder shall

work in cooperation with the local administrative

bodies and conclude agreements on issues of

environmental protection, mine exploitation,

infrastructure development in relation to the mine site

development and jobs creation.” The government's

authority must approve this agreement.

Lessons learnt and main challenges

1. National policies and laws need to be stable. Lack of stability makes difficult or impossible to evaluate

economic, social or environmental impacts of such measures.

2. LDF and other EI revenue sharing mechanisms should be planned and implemented in line with the SDG,

SDV and action plans of the national and local governments.

3. Need to build capacity of local governments, elected representatives and citizens. The lack of capacity of

stakeholders on identifying needs and prioritizing critical development issues results in one-off, fragmented

and ineffective uses of funds rather than for development.

4. The objectives, importance and implementation methods of any project need to be clearly explained to

local citizens. Due to lack of understanding, there is some conflict between local citizens and project

implementers.

5. Possibly due to insufficient requirements set in LDF guideline on addressing poverty and environmental

issues, only around 10-16 percent of LDFs were spent on such projects and initiatives. Rather, it should be

spent on the basis of long-term objectives of the local development indicators.

6. LDF has been very popular with local governments and citizens and achieved a lot within its three years

of implementation. It enabled significant ‘practicing’ of in participatory decision making and inducing local

initiative, strengthening self-governing capacity of local governments, providing financial responsibilities and

giving confidence.

7. The amount of LDF allocated to one soum may not be enough to finance medium and large-scale

projects. To ensure long-term benefits of the GLDF, the government can consider an alternative allocation

system whereby instead of allocating small amounts of funding to each soum every year, greater amounts can

be distributed to soums once every 2-3 years.

8. The LDF guideline needs revision. In its current form, it is inflexible and limits the use of LDF on long-term

developmental projects especially related to social and environmental issues. LDF expenditure decisions

should be aligned with longer term development strategy and action plans of individual soums and aimags and

also be in synergy with SDV and plans.

9. Soum level governments need capacity building on negotiating skills with higher level government

authorities and mining companies to maximize benefits of financial dealings. This can generate financial

payoffs to soums.

10. All types of revenues collected in accordance with CDAs should be used to reduce actual and potential

negative socioeconomic and environmental impacts, to compensate for damages to local communities

caused by extractive activities and to finance other projects supporting development.

Lessons learnt and main challenges

THANK YOU FOR YOUR ATTENTION