Embed Size (px)

Citation preview

1

Managing Risk off the

Balance Sheet with

Derivative Securities

23-2

Managing Risk off the Balance

Sheet

Managers are increasingly turning to off-balance-sheet

their financial institutions

from derivative securities

Managers are increasingly turning to off-balance-sheet

(OBS) instruments such as forwards, futures, options,

and swaps to hedge the risks their financial institutions

(FIs) face

interest rate risk

foreign exchange risk

credit risk

FIs also generate fee income from derivative securities

transactions

23-3

Managing Risk off the Balance

Sheet

A spot contract is an agreement to transact

transact at a point in the future with the terms of the

A spot contract is an agreement to transact

involving the immediate exchange of assets and

funds

A forward contract is a negotiated agreement to

transact at a point in the future with the terms of the

deal set today

Any amount can be negotiated

Not generally liquid, so each party must perform

Counterparty default risk can be significant

23-4

Managing Risk off the Balance

Sheet

A futures contract is an exchange-traded agreement to

Futures are liquid, most traders close their position before

traders’ gains and losses on outstanding futures contracts

A futures contract is an exchange-traded agreement to

transact involving the future exchange of a set amount

of assets for a price that is fixed today

Futures are liquid, most traders close their position before

the delivery date so the underlying transaction may never

take place

Futures contracts are marked to market daily—i.e., the

traders’ gains and losses on outstanding futures contracts

are realized each day as futures prices change

Exchange clearinghouse stands behind all contracts so

there is no counterparty default risk and trading is

anonymous

2

23-5

Hedging with Forwards

A naïve hedge is a hedge of a cash asset on a direct

assets against risk by using hedging to

A naïve hedge is a hedge of a cash asset on a direct

dollar-for-dollar basis with a forward (or futures) contract

Managers can predict capital loss (ΔP) using the duration

formula:

where P = the initial value of an asset

D = the duration of the asset

R = the interest rate (and thus ΔR is the change in interest)

FIs can immunize assets against risk by using hedging to

fully protect against adverse movements in interest rates

)1( R

RPDP

23-6

Hedging with Futures

Microhedging is using futures (or forwards) contracts to

price is not perfectly correlated with the movement in

firms use short positions in futures contracts to hedge

Microhedging is using futures (or forwards) contracts to hedge a specific asset or liability

basis risk is a residual risk that occurs in a hedged position because the movement in an asset’s spot price is not perfectly correlated with the movement in the price of the asset delivered under a futures (or forwards) contract

firms use short positions in futures contracts to hedge an asset that declines in value as interest rates rise

Macrohedging is hedging the entire (leverage-adjusted) duration gap of an FI

23-7

Futures Gain and Loss and Hedging with Futures Futures Gain and Loss and Hedging with Futures

23-8

Hedging Considerations

Microhedging and macrohedging

derivatives used to hedge must be recognized immediately

requirements imposed by bank regulators (forward can be)

Microhedging and macrohedging

Risk-return considerations

FIs hedge based on expectations of future interest rate movements

FIs may microhedge, macrohedge, or even overhedge

Accounting rules can influence hedging strategies

in 1997 FASB required that all gains and losses from derivatives used to hedge must be recognized immediately

U.S. companies must report derivative-related trading activity in annual reports

futures contracts are not subject to risk-based capital requirements imposed by bank regulators (forward can be)

3

23-9

Hedging Considerations

Routine hedging: In a full hedge or ‘routine

Most managers engage in partial hedging or

Routine hedging: In a full hedge or ‘routine hedge’ the bank eliminates all or most of its risk exposure such as interest rate risk

Most managers engage in partial hedging or what the text terms ‘selective hedging’ where some risks are reduced and others are borne by the institution

23-10

The Effects of Hedging

23-11

Options

Buying a call option on a bond

Buying a call option on a bond

As interest rates fall, bond prices rise, and the call option buyer has a large profit potential

As interest rates rise, bond prices fall, but the call option losses are no larger than the call option premium

Writing a call option on a bond

As interest rates fall, bond prices rise, and the call option writer has a large potential loss

As interest rates rise, bond prices fall, but the call option gains will be no larger than the call option premium

23-12

Purchased and Written Call Option Positions Purchased and Written Call Option Positions

4

23-13

Options

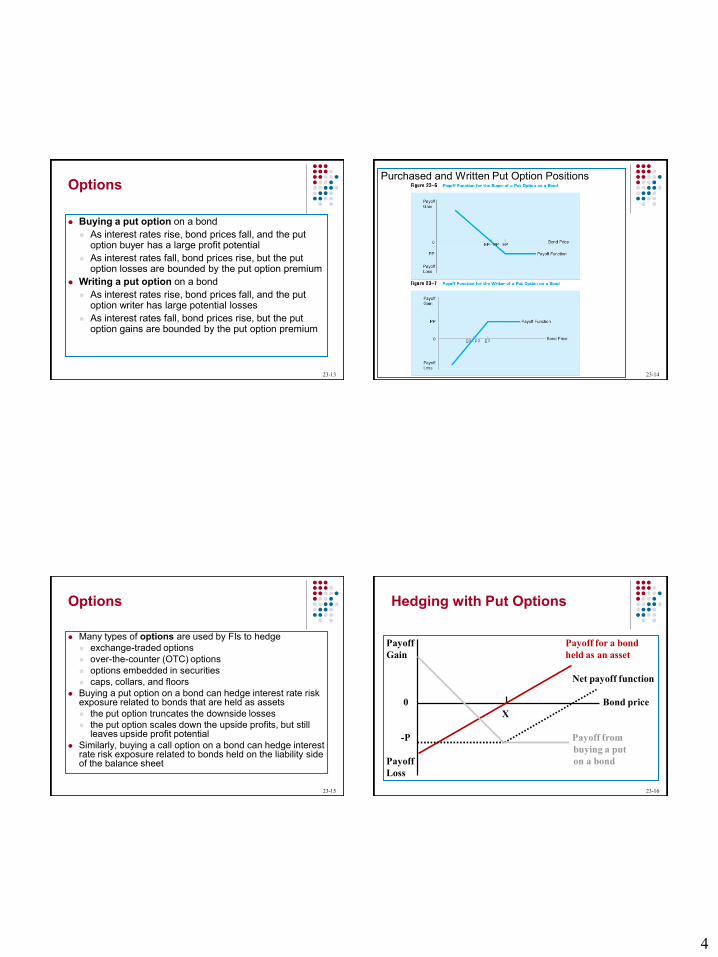

Buying a put option on a bond

option losses are bounded by the put option premium

Buying a put option on a bond

As interest rates rise, bond prices fall, and the put option buyer has a large profit potential

As interest rates fall, bond prices rise, but the put option losses are bounded by the put option premium

Writing a put option on a bond

As interest rates rise, bond prices fall, and the put option writer has large potential losses

As interest rates fall, bond prices rise, but the put option gains are bounded by the put option premium

23-14

Purchased and Written Put Option Positions Purchased and Written Put Option Positions

23-15

Options

Many types of options are used by FIs to hedge

Buying a put option on a bond can hedge interest rate risk

Similarly, buying a call option on a bond can hedge interest rate risk exposure related to bonds held on the liability side

Many types of options are used by FIs to hedge

exchange-traded options

over-the-counter (OTC) options

options embedded in securities

caps, collars, and floors

Buying a put option on a bond can hedge interest rate risk exposure related to bonds that are held as assets

the put option truncates the downside losses

the put option scales down the upside profits, but still leaves upside profit potential

Similarly, buying a call option on a bond can hedge interest rate risk exposure related to bonds held on the liability side of the balance sheet

23-16

Hedging with Put Options

Payoff

Gain

Payoff

Loss

Payoff

Gain

0 Bond price

X

-P Payoff from

buying a put

Payoff on a bond

Loss

Net payoff function

Payoff for a bond

held as an asset

5

23-17

Caps, Floors, and Collars

Buying a cap means buying a call option, or a succession

like buying insurance against an (excessive) increase in

amounts to a simultaneous position in a cap and a

usually involves buying a cap and selling a floor to offset

Buying a cap means buying a call option, or a succession of call options, on interest rates rather than on bond prices like buying insurance against an (excessive) increase in

interest rates Buying a floor is akin to buying a put option on interest

rates seller compensates the buyer should interest rates fall

below the floor rate like caps, floors can have one or a succession of

exercise dates A collar amounts to a simultaneous position in a cap and a

floor usually involves buying a cap and selling a floor to offset

cost of cap

23-18

Contingent Credit Risk

Contingent credit risk is the risk that the counterparty defaults on payment

forward contracts and all OTC derivatives

Contingent credit risk is the risk that the counterparty defaults on payment obligations

forward contracts and all OTC derivatives are exposed to counterparty default risk as they are nonstandard contracts entered into bilaterally

23-19

Swaps

Swap agreements are contracts where two parties

Swap agreements are contracts where two parties agree to exchange a series of payments over time

There are several types of swaps:

Interest rate swaps

Parties agree to swap interest payments on a stated notional principal amount for a set period of time (some are for more than 5 years) (No principal is usually exchanged)

Currency swaps

Parties agree to swap interest and principal payments in different currencies at a preset exchange rate

23-20

Swaps

Types of swaps (continued)

Types of swaps (continued) Credit default swaps (aka credit swaps)

Total return swap (TRS):

o A TRS buyer agrees to make a fixed rate payment to the seller plus the capital gain or minus the capital loss on the underlying instrument

o In exchange, the TRS seller may pay a variable or a fixed rate of interest to the buyer

o Pure Credit Swap (PCS): o The swap buyer makes fixed payments to the seller

and the seller pays the swap buyer only in the event of default. The payment is usually equal to par – secondary market value of the underlying instrument

6

23-21

Swaps

Credit Swaps and the crisis

markets was more widespread than it would have been

would not otherwise make and earn fee income on other

Credit Swaps and the crisis Lehman Brothers and AIG sold credit default swaps

worth billions of dollars in payments insuring mortgage-backed securities (MBS)

When mortgage security values collapsed, required outflows at these firms far exceeded capital

Other institutions invested more heavily in MBS because they were insured; exposure to mortgage markets was more widespread than it would have been otherwise

Credit swaps may cause lenders to make loans they would not otherwise make and earn fee income on other services offered to borrowers.

23-22

Swaps

There are also some less common types of

The notional value of swap contracts outstanding at U.S. commercial banks was more than $146.9

There are also some less common types of swaps: commodity swaps

equity swaps

The market for swaps has grown enormously in recent years The notional value of swap contracts outstanding

at U.S. commercial banks was more than $146.9 trillion in 2010

23-23

Swaps

Hedging with interest rate swaps: An Example Hedging with interest rate swaps: An Example a money center bank (MCB) may have floating-rate

loans and fixed-rate liabilities the MCB has a negative duration gap

a savings bank (SB) may have fixed-rate mortgages funded by short-term liabilities such as retail deposits the SB has a positive duration gap

accordingly, an interest swap can be entered into between the MCB and the SB either: directly between the two FIs OR indirectly through a broker or agent who charges a fee

to accept the credit risk exposure and guarantee the cash flows

23-24

Swaps

A plain vanilla swap is:

fixed rate of interest and the other party pays a variable

rate inflows are now matched to

A plain vanilla swap is:

A standard agreement where one participant pays a

fixed rate of interest and the other party pays a variable

rate of interest on a stated notional principal; no

principal is exchanged

The SB sends fixed-rate interest payments to the MCB

thus, the MCB’s fixed-rate inflows are now matched to

its fixed-rate payments

the MCB sends variable-rate interest payments to the SB

thus, the SB’s variable-rate inflows are now matched to

its variable-rate payments

7

23-25

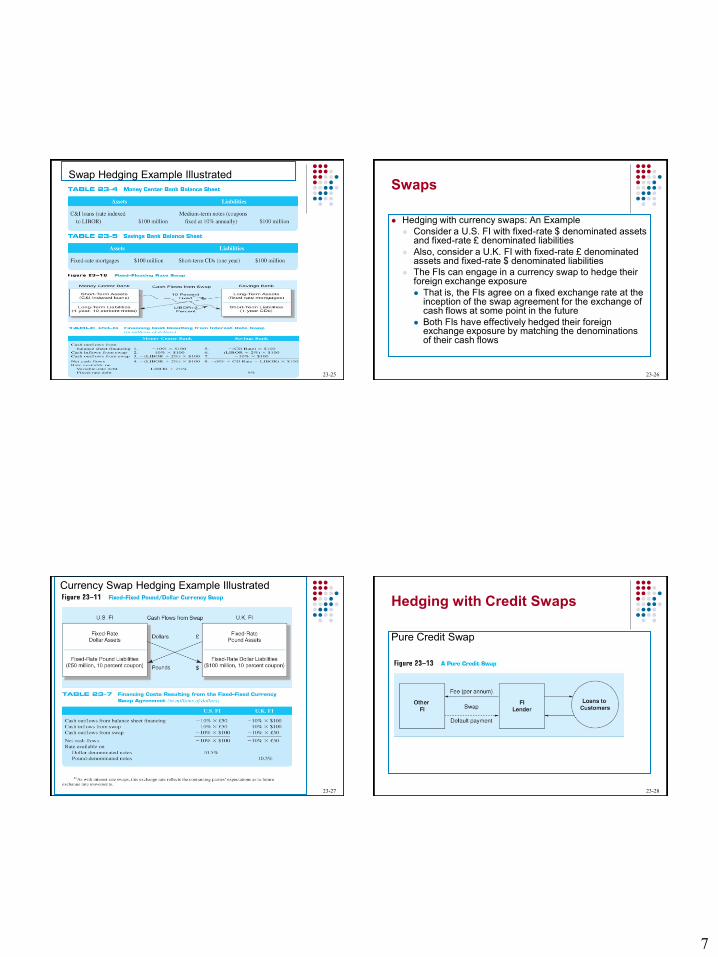

Swap Hedging Example Illustrated Swap Hedging Example Illustrated

23-26

Swaps

Hedging with currency swaps: An Example

rate $ denominated assets

That is, the FIs agree on a fixed exchange rate at the

Hedging with currency swaps: An Example

Consider a U.S. FI with fixed-rate $ denominated assets and fixed-rate £ denominated liabilities

Also, consider a U.K. FI with fixed-rate £ denominated assets and fixed-rate $ denominated liabilities

The FIs can engage in a currency swap to hedge their foreign exchange exposure

That is, the FIs agree on a fixed exchange rate at the inception of the swap agreement for the exchange of cash flows at some point in the future

Both FIs have effectively hedged their foreign exchange exposure by matching the denominations of their cash flows

23-27

Currency Swap Hedging Example Illustrated Currency Swap Hedging Example Illustrated

23-28

Hedging with Credit Swaps

Pure Credit Swap Pure Credit Swap

8

23-29

Credit Risk on Swaps

The growth of the over-the-counter swap market was a

money counterparties would

BIS now requires capital to be held against interest rate,

The growth of the over-the-counter swap market was a major factor underlying the imposition of the BIS risk-based capital requirements

the fear was that out-of-the-money counterparties would have incentives to default

BIS now requires capital to be held against interest rate, currency, and other swaps

Credit risk on swaps differs from that on loans

Netting: only the difference between the fixed and the floating payment is exchanged between swap parties

Payment flows are often interest and not principal

Standby letters of credit are required of poor-quality swap participants

23-30

Comparing Hedging Methods

Writing vs. buying options

Writing vs. buying options

writing options limits upside profits, but not downside losses

buying options limits downside losses, but not upside profits

CBs are prohibited from writing options in some areas

Futures vs. options hedging

futures produce symmetric gains and losses

options protect against losses, but do not fully reduce gains

Swaps vs. forwards, futures, and options

swaps and forwards are OTC contracts, unlike options and futures

futures are marked to market daily

swaps can be written for longer-time horizons

23-31

Regulation

Regulators specify “permissible activities” that FIs may

Institutions engaging in permissible activities are subject to

Regulators specify “permissible activities” that FIs may

engage in

Institutions engaging in permissible activities are subject to

regulatory oversight

Regulators judge the overall integrity of FIs engaging in

derivatives activity based on capital adequacy regulation

The Securities and Exchange Commission (SEC) and

the Commodity Futures Trading Commission (CFTC)

are the functional regulators of derivatives securities

markets

23-32

Regulation

The Federal Reserve, the Federal Deposit Insurance

have implemented uniform guidelines that require

Frank Act, swap markets were governed by relatively

The Federal Reserve, the Federal Deposit Insurance

Corporation (FDIC) and the Office of the Comptroller of the

Currency (OCC) have implemented uniform guidelines that require

banks to:

establish internal guidelines regarding hedging activity

establish trading limits

disclose large contract positions that materially affect the risk to

shareholders and outside investors

As of 2000 the FASB requires all firms to reflect the marked-to-market

value of their derivatives positions in their financial statements

Prior to the Dodd-Frank Act, swap markets were governed by relatively

little regulation—except indirectly at FIs through bank regulatory

agencies

9

23-33

Regulation

The Dodd-Frank Act of 2010 requires most

The Dodd-Frank Act of 2010 requires most

OTC derivatives to be exchange-traded to

ensure performance by all parties

The act also requires OTC derivatives be

regulated by the SEC and/or the CFTC

Managing Liquidity

Risk on the

Balance Sheet

23-35

Liquidity Risk Management

Unlike other risks, liquidity risk is a normal aspect

of the everyday management of financial institutions

Unlike other risks, liquidity risk is a normal aspect

of the everyday management of financial institutions

(FIs)

At the extreme, liquidity risk can lead to insolvency

Some FIs are more exposed to liquidity risk than

others

Depository institutions (DIs) are highly exposed

Mutual funds, pension funds, life insurers and property-

casualty insurers have relatively low liquidity risk

23-36

Liquidity Risk Management

One type of liquidity risk arises when an FI’s liability

Alternately, FIs may have to sell assets to generate cash, which

A second type of liquidity risk arises from the exercise of

One type of liquidity risk arises when an FI’s liability holders seek to withdraw their financial claims FIs must meet the withdrawals with stored or borrowed funds

Alternately, FIs may have to sell assets to generate cash, which can be costly if assets can only be sold at fire-sale prices

A second type of liquidity risk arises from the exercise of off-balance-sheet commitments made by the FI Unexpected loan demand can occur when off-balance-sheet

loan commitments are drawn down suddenly and in large volumes

FIs are contractually obliged to supply funds through loan commitments immediately should they be drawn down

10

23-37

Liquidity Risk and

Depository Institutions (DIs)

DIs’ balance sheets typically have:

DIs’ balance sheets typically have:

Large amounts of short-term liabilities such as deposits and other transaction accounts that must be paid out immediately if demanded by depositors

Large amounts of relatively illiquid long-term assets such as commercial loans and mortgages

DIs know that normally only a small portion of demand deposits will be withdrawn on any given day

Most demand deposits act as core deposits—i.e., they are a stable and long-term funding source

Deposit withdrawals are normally offset by the inflow of new deposits

23-38

Liquidity Risk and Depository

Institutions

DI managers monitor net deposit drains—i.e., the

amount by which cash withdrawals exceed additions; a

DI managers monitor net deposit drains—i.e., the

amount by which cash withdrawals exceed additions; a

net cash outflow

DIs manage liquidity needs by two methods:

1. Stored liquidity

Maintaining liquid assets to meet cash needs

Primary method for community banks

23-39

Liquidity Risk and Depository

Institutions

DIs manage liquidity needs by two methods:

Used primarily by the largest banks with access to

DIs manage liquidity needs by two methods: (continued)

1. Purchased liquidity

Rely on the ability to acquire funds from brokered deposits and borrowings

Used primarily by the largest banks with access to the money market and other nondeposit sources of funds

Most DIs utilize a combination of stored and purchased liquidity management

23-40

Liquidity Risk and Depository

Institutions

Stored liquidity

Banks hold cash reserves in their vaults and at the

Stored liquidity

Liquidating cash stores and selling existing assets

Banks hold cash reserves in their vaults and at the Federal Reserve in excess of minimum requirements

When managers utilize stored liquidity to fund deposit drains, the size of the balance sheet is reduced and its composition changes

11

23-41

Liquidity Risk and Depository

Institutions

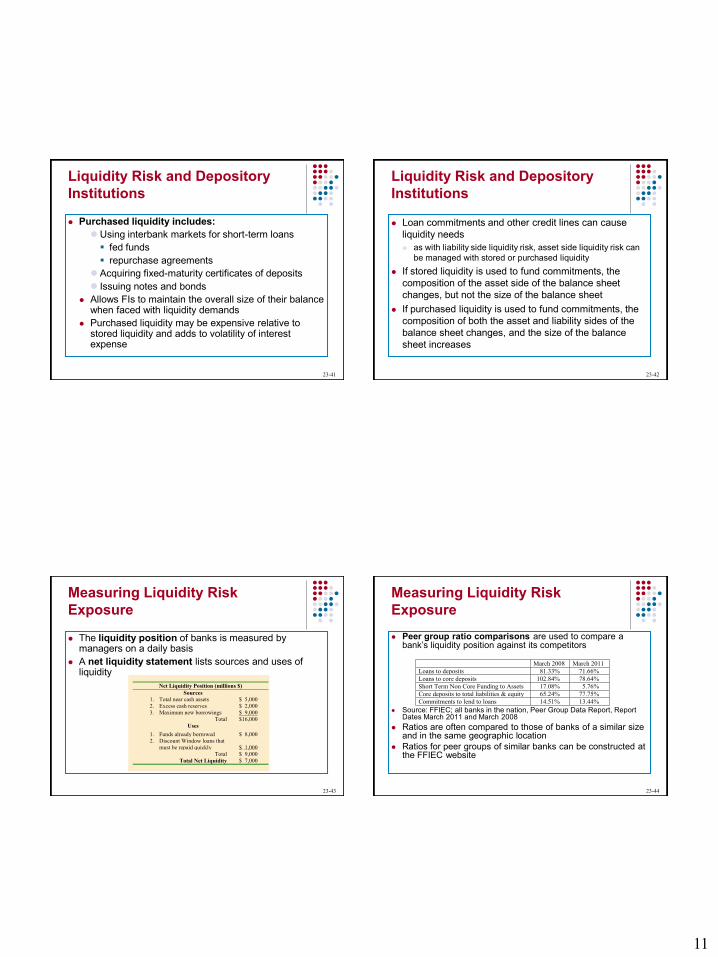

Purchased liquidity includes:

Allows FIs to maintain the overall size of their balance

Purchased liquidity includes:

Using interbank markets for short-term loans

fed funds

repurchase agreements

Acquiring fixed-maturity certificates of deposits

Issuing notes and bonds

Allows FIs to maintain the overall size of their balance when faced with liquidity demands

Purchased liquidity may be expensive relative to stored liquidity and adds to volatility of interest expense

23-42

Liquidity Risk and Depository

Institutions

Loan commitments and other credit lines can cause

Loan commitments and other credit lines can cause

liquidity needs

as with liability side liquidity risk, asset side liquidity risk can

be managed with stored or purchased liquidity

If stored liquidity is used to fund commitments, the

composition of the asset side of the balance sheet

changes, but not the size of the balance sheet

If purchased liquidity is used to fund commitments, the

composition of both the asset and liability sides of the

balance sheet changes, and the size of the balance

sheet increases

23-43

Measuring Liquidity Risk

Exposure

The liquidity position of banks is measured by

The liquidity position of banks is measured by managers on a daily basis

A net liquidity statement lists sources and uses of liquidity

I.

Net Liquidity Position (millions $)

Sources

1. Total near cash assets $ 5,000

2. Excess cash reserves $ 2,000

3. Maximum new borrowings $ 9,000

Total $16,000

Uses

1. Funds already borrowed $ 8,000

2. Discount Window loans that

must be repaid quickly

$ 1,000

Total $ 9,000

Total Net Liquidity $ 7,000

23-44

Measuring Liquidity Risk

Exposure

Peer group ratio comparisons are used to compare a

Ratios are often compared to those of banks of a similar size

Ratios for peer groups of similar banks can be constructed at

Peer group ratio comparisons are used to compare a bank’s liquidity position against its competitors

Source: FFIEC; all banks in the nation, Peer Group Data Report, Report

Dates March 2011 and March 2008

Ratios are often compared to those of banks of a similar size and in the same geographic location

Ratios for peer groups of similar banks can be constructed at the FFIEC website

March 2008 March 2011

Loans to deposits 81.33% 71.66%

Loans to core deposits 102.84% 78.64%

Short Term Non Core Funding to Assets 17.08% 5.76%

Core deposits to total liabilities & equity 65.24% 77.75%

Commitments to lend to loans 14.51% 13.44%

12

23-45

Measuring Liquidity Risk

Exposure

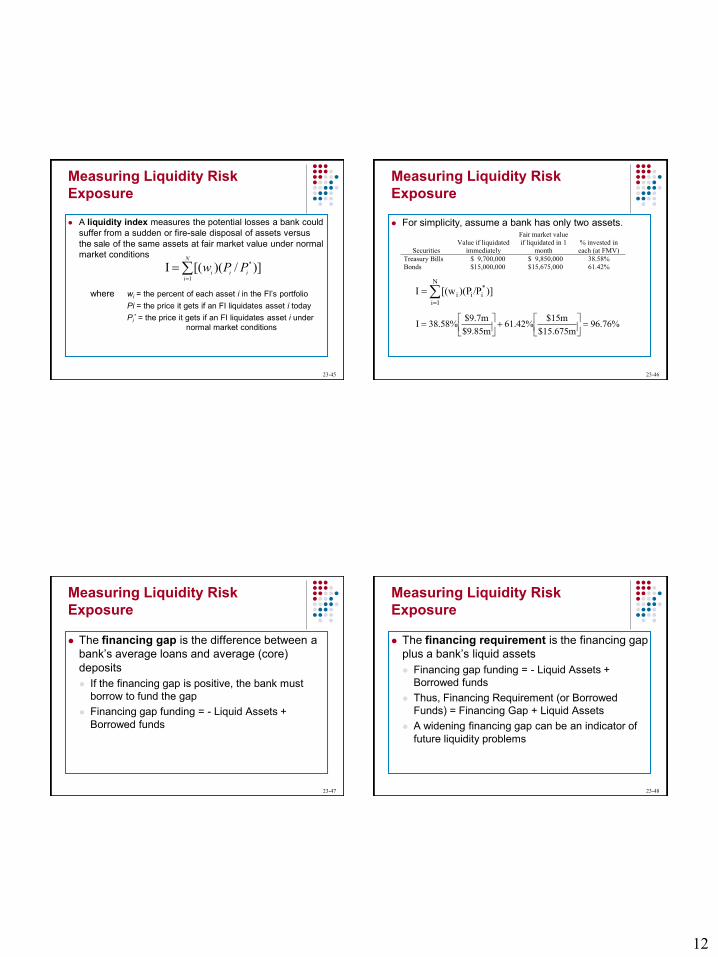

A liquidity index measures the potential losses a bank could

the sale of the same assets at fair market value under normal

A liquidity index measures the potential losses a bank could

suffer from a sudden or fire-sale disposal of assets versus

the sale of the same assets at fair market value under normal

market conditions

where wi = the percent of each asset i in the FI’s portfolio

Pi = the price it gets if an FI liquidates asset i today

Pi* = the price it gets if an FI liquidates asset i under

normal market conditions

N

iiiiPPw

1

* )]/)([(I

23-46

Measuring Liquidity Risk

Exposure

For simplicity, assume a bank has only two assets. For simplicity, assume a bank has only two assets.

N

1i

*iii )]/P)(P[(wI

Securities

Value if liquidated

immediately

Fair market value

if liquidated in 1

month

% invested in

each (at FMV)

Treasury Bills $ 9,700,000 $ 9,850,000 38.58%

Bonds $15,000,000 $15,675,000 61.42%

96.76%$15.675m

$15m61.42%

$9.85m

$9.7m38.58%I

23-47

Measuring Liquidity Risk

Exposure

The financing gap is the difference between a The financing gap is the difference between a

bank’s average loans and average (core)

deposits

If the financing gap is positive, the bank must

borrow to fund the gap

Financing gap funding = - Liquid Assets +

Borrowed funds

23-48

Measuring Liquidity Risk

Exposure

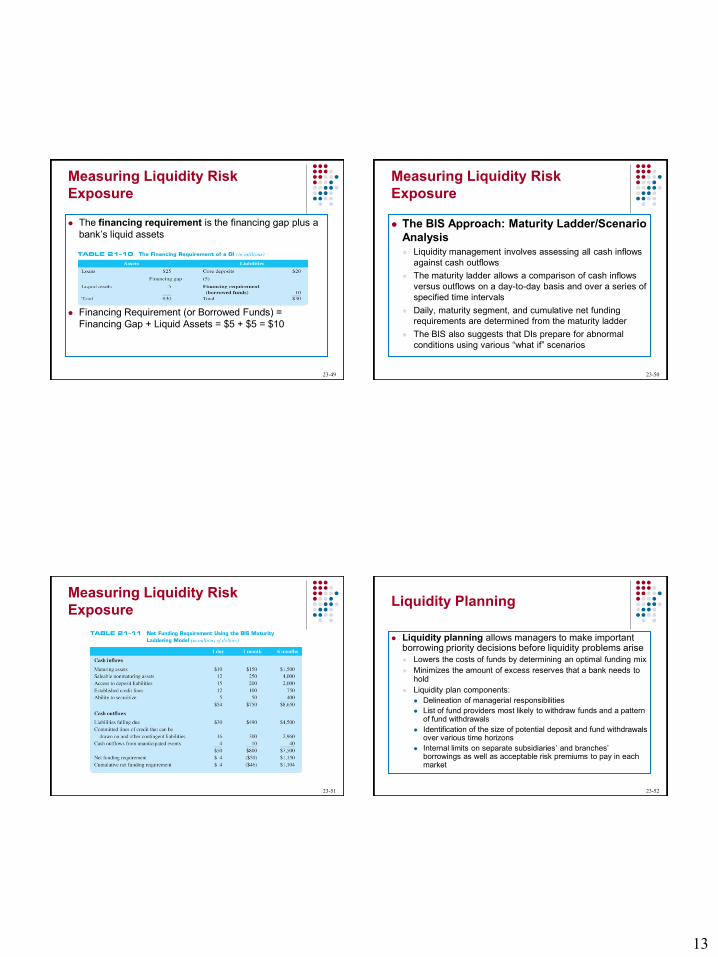

The financing requirement is the financing gap The financing requirement is the financing gap

plus a bank’s liquid assets

Financing gap funding = - Liquid Assets +

Borrowed funds

Thus, Financing Requirement (or Borrowed

Funds) = Financing Gap + Liquid Assets

A widening financing gap can be an indicator of

future liquidity problems

13

23-49

Measuring Liquidity Risk

Exposure

The financing requirement is the financing gap plus a

The financing requirement is the financing gap plus a

bank’s liquid assets

Financing Requirement (or Borrowed Funds) =

Financing Gap + Liquid Assets = $5 + $5 = $10

23-50

Measuring Liquidity Risk

Exposure

The BIS Approach: Maturity Ladder/Scenario

day basis and over a series of

The BIS Approach: Maturity Ladder/Scenario

Analysis

Liquidity management involves assessing all cash inflows

against cash outflows

The maturity ladder allows a comparison of cash inflows

versus outflows on a day-to-day basis and over a series of

specified time intervals

Daily, maturity segment, and cumulative net funding

requirements are determined from the maturity ladder

The BIS also suggests that DIs prepare for abnormal

conditions using various “what if” scenarios

23-51

Measuring Liquidity Risk

Exposure

23-52

Liquidity Planning

Liquidity planning allows managers to make important

Lowers the costs of funds by determining an optimal funding mix

List of fund providers most likely to withdraw funds and a pattern

Identification of the size of potential deposit and fund withdrawals

Liquidity planning allows managers to make important borrowing priority decisions before liquidity problems arise

Lowers the costs of funds by determining an optimal funding mix

Minimizes the amount of excess reserves that a bank needs to hold

Liquidity plan components:

Delineation of managerial responsibilities

List of fund providers most likely to withdraw funds and a pattern of fund withdrawals

Identification of the size of potential deposit and fund withdrawals over various time horizons

Internal limits on separate subsidiaries’ and branches’ borrowings as well as acceptable risk premiums to pay in each market

14

23-53

Example: Liquidity Plan Example: Liquidity Plan

Potential Deposit

Withdrawals

From most likely to withdraw to least likely

Mutual Funds $ 70

Pension Funds $ 40

Correspondent banks $ 50

Large corporations $ 45

Small businesses $ 25

Consumers $ 75

Total $305

Expected total withdrawals per period Average Maximum Likely

One week $ 60 $100

One month $ 70 $150

Three months $130 $220

Total $260 $470

Sequence of funding

options as needed

One Week

One month

Three month

New deposits $ 15 $ 35 $ 75

Sale liquid assets $ 15 $ 25 $ 55

Sale investment portfolio $ 30 $ 40 $ 50

Borrowings from other FIs $ 30 $ 40 $ 35

Borrowings from Fed $ 10 $ 10 $ 5

Total $100 $150 $220

23-54

Liquidity Risk

Major liquidity problems arise if deposit drains are

Major liquidity problems arise if deposit drains are abnormally large and unexpected

Abnormal deposit drains can occur because:

Concerns about a bank’s solvency

Failure of another bank (i.e., the contagion effect)

Sudden changes in investors’ preferences regarding holding nonbank financial assets relative to bank deposits

A bank run is a sudden and unexpected increase in deposit withdrawals from a bank

23-55

Liquidity Risk

Demand deposits are first-come, first-served contracts

the first sign of trouble creates a fundamental instability

is a systemic or contagious run on the deposits of

Demand deposits are first-come, first-served contracts

The incentives for depositors to withdraw their funds at

the first sign of trouble creates a fundamental instability

in the banking system

a bank panic is a systemic or contagious run on the deposits of

the banking industry as a whole

Regulatory mechanisms are in place to ease banks’

liquidity problems and to deter bank runs and panics

deposit insurance ($250,000 per account since the

financial crisis of 2008-2009)

the discount window

23-56

Deposit Insurance

Deposit insurance was first introduced in the U.S. in

Deposit insurance was first introduced in the U.S. in 1933 with coverage up to $2,500

Coverage was increased to $100,000 in 1980

Beginning in 2011 the Federal Deposit Insurance Corporation (FDIC) will increase coverage every year based on the Consumer Price Index (CPI)

The Federal Deposit Insurance Reform Act of 2005 increased deposit insurance for retirement accounts from $100,000 to $250,000

15

23-57

Deposit Insurance

Individuals can achieve many times the $250,000

program to evaluate and assign deposit

Individuals can achieve many times the $250,000 coverage cap on deposits by creatively structuring their deposits and by using multiple banks

The FDIC now uses a risk-based deposit insurance program to evaluate and assign deposit insurance premiums

Some states operate state guarantee funds to insure investments made with insurance firms, but they are not federally backed

23-58

The Discount Window

The Federal Reserve also provides a “discount

In response to the liquidity problems caused by

The Federal Reserve also provides a “discount window” lending facility

Historically, the borrowing rate was below market rates and borrowing was restricted

In response to the liquidity problems caused by the credit crunch in 2007 and 2008, the Fed announced in March 2008 that it would lend up to $200 billion to both commercial and investment banks through its new Primary Dealer Credit Facility (PDCF)

23-59

The Discount Window

New federal borrowing programs emerged

New federal borrowing programs emerged over the succeeding months providing funding to money market mutual funds, commercial paper, insurance companies, and others

The Fed also lowered interest rates to near zero and reduced the spread between the discount rate and the Fed funds rate

23-60

Liquidity Risk and Insurance

Companies

Life insurance companies hold cash reserves and other

of a life insurance policy is the amount that

Life insurance companies hold cash reserves and other liquid assets

Meet policy payments

Meet cancellation (surrender) payments

The surrender value of a life insurance policy is the amount that an insurance policyholder receives when cashing in a policy early

Fund working capital needs which can be unpredictable

Property-casualty (P&C) insurance companies

Claims against P&C insurers are hard to predict

Thus, P&C insurance companies have a greater need for liquidity than life insurance companies

16

23-61

Liquidity Risk and Mutual Funds

Mutual funds (MFs) can be subject to dramatic

assets are distributed on a pro rate basis (i.e., rather than

Mutual funds (MFs) can be subject to dramatic liquidity needs if investors become nervous about the true value of the funds’ assets

However, the way MFs are valued reduces the incentive of fund shareholders to engage in bank-like runs on any given day assets are distributed on a pro rate basis (i.e., rather than

a first-come, first-served basis)

losses are incurred to shareholders on a proportional basis