Embed Size (px)

Citation preview

Managing the Liquidity Constraints In IndiaConstraints In India

KrishnamurthyReserve Bank of India

May 2009

1

An overviewAn overview

•Regulatory and Institutional Structure forg yHousing Finance.

•Sources of Funds for Housing financeSources of Funds for Housing finance

•Emergence of constraints in the market

•Measures taken by RBI

• Future Perspectives• Future Perspectives

2

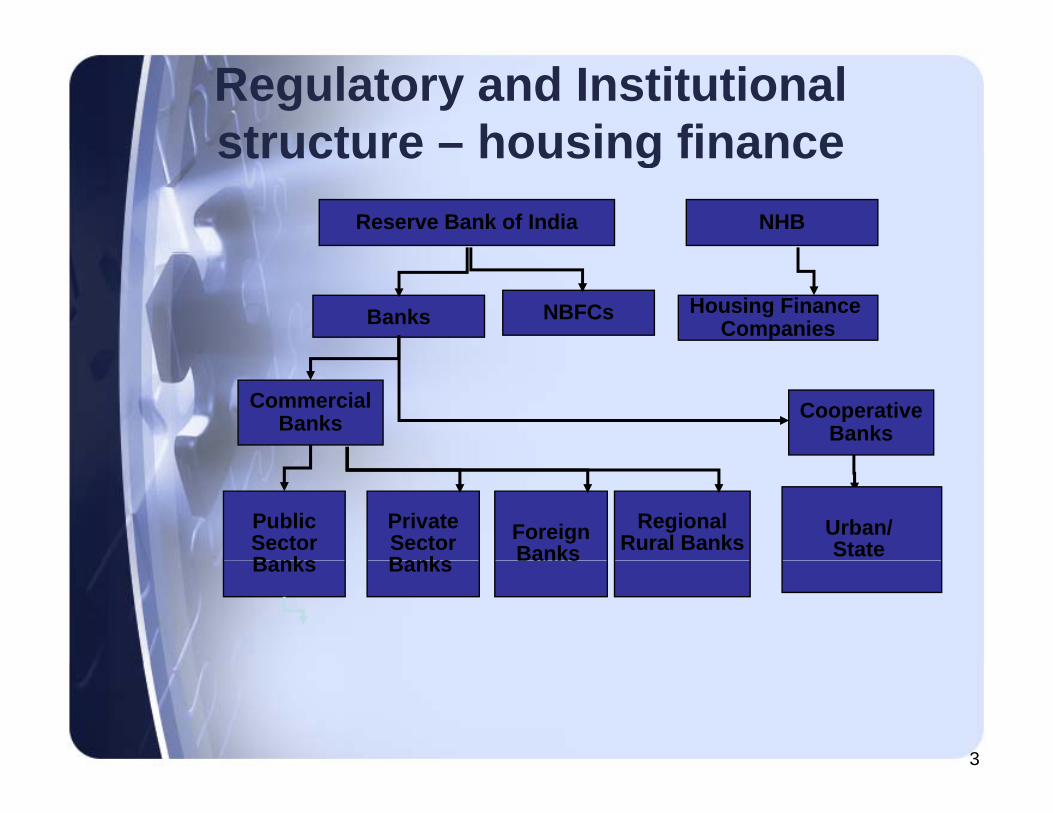

Regulatory and Institutional structure – housing finance

Reserve Bank of India NHB

structure housing finance

NBFCsBanks Housing Finance Companies

Commercial Banks Cooperative

Banks

ForeignBanks

PrivateSectorBanks

PublicSectorBanks

RegionalRural Banks

Urban/ State Banks Banks Banks

3

Sources of Funds for HFCsSources of Funds for HFCs• Borrowing from Banks

• Debentures

• ICDs

• NCDs

• Refinance support

4

• Public deposits

Emergence of constraints in the marketmarket

• Factors• Factors

• Liquidity position of large HFCs• Liquidity position of large HFCs

Li idit iti f h d l d• Liquidity position of scheduled commercial banks

• Resource availability

5

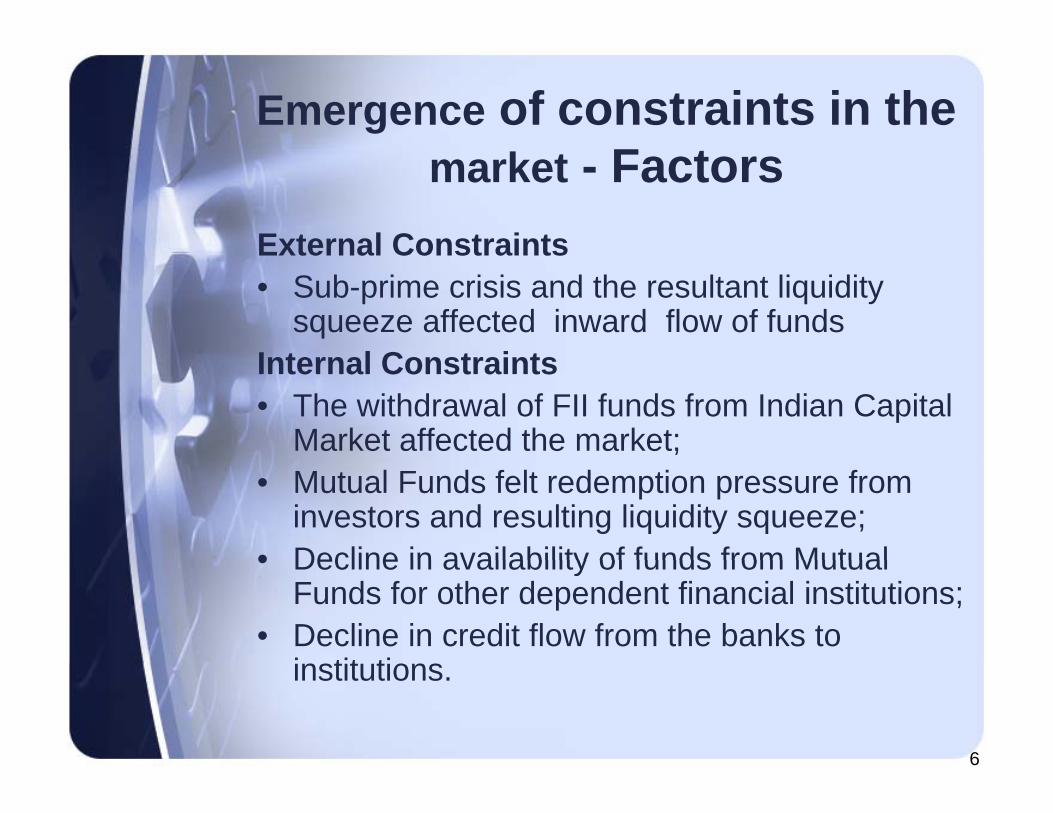

Emergence of constraints in the F tmarket - Factors

External ConstraintsExternal Constraints• Sub-prime crisis and the resultant liquidity

squeeze affected inward flow of funds I t l C t i tInternal Constraints• The withdrawal of FII funds from Indian Capital

Market affected the market;• Mutual Funds felt redemption pressure from

investors and resulting liquidity squeeze;• Decline in availability of funds from Mutual• Decline in availability of funds from Mutual

Funds for other dependent financial institutions; • Decline in credit flow from the banks to

i tit ti

6

institutions.

The emergence of constraintsi f HFC– Liquidity issues of HFCs

• The liquidity constraints emerged in theThe liquidity constraints emerged in the economy, though not HF focused, did impact the HFCs also.

• However, the balance sheet size of the HFCs did not shrink

• The growth had been moderate with a slight• The growth had been moderate with a slight weakness only in the last quarter of 08

• The structure of resources underwent adjustments .

• No resource crunch has been felt by Large HFCs as on March 31 2009;

7

HFCs as on March 31, 2009;

Liquidity position of large HFCs@

Sources underwent slight restructuring.Sources underwent slight restructuring.

•Debentures as a source of funds decreased.

•ICDs Increased•Deposits continued to remain steady•Deposits continued to remain steady •The data from selected HFCs reveal, currently there are no liquidity constraints

•No resource crunch has been felt bymajor HFCs at the end of I Qtr of 09

8

major HFCs at the end of I Qtr of 09.@Data from some major HFCs

Application of funds – HFCs(Selected Study)

Application of fundsppMajor HFCs

14000.00

16000.00

8000.00

10000.00

12000.00

nt R

s. B

illio

n

0.00

2000.00

4000.00

6000.00

Am

oun

30-Jun-08 Sept. 30, 2008 Dec. 31, 2008 31-Mar-09

Quarter ending

Loans - HFCs investment-Share/Deb Total Assets

9

Liquidity position of large HFCs

Application of fundsApplication of funds

L d d f L HFC•Loans and advances of Large HFCs have indicated growth, However quarter to quarter growth in Decemberquarter to quarter growth in December 2008 was somewhat subdued;

10

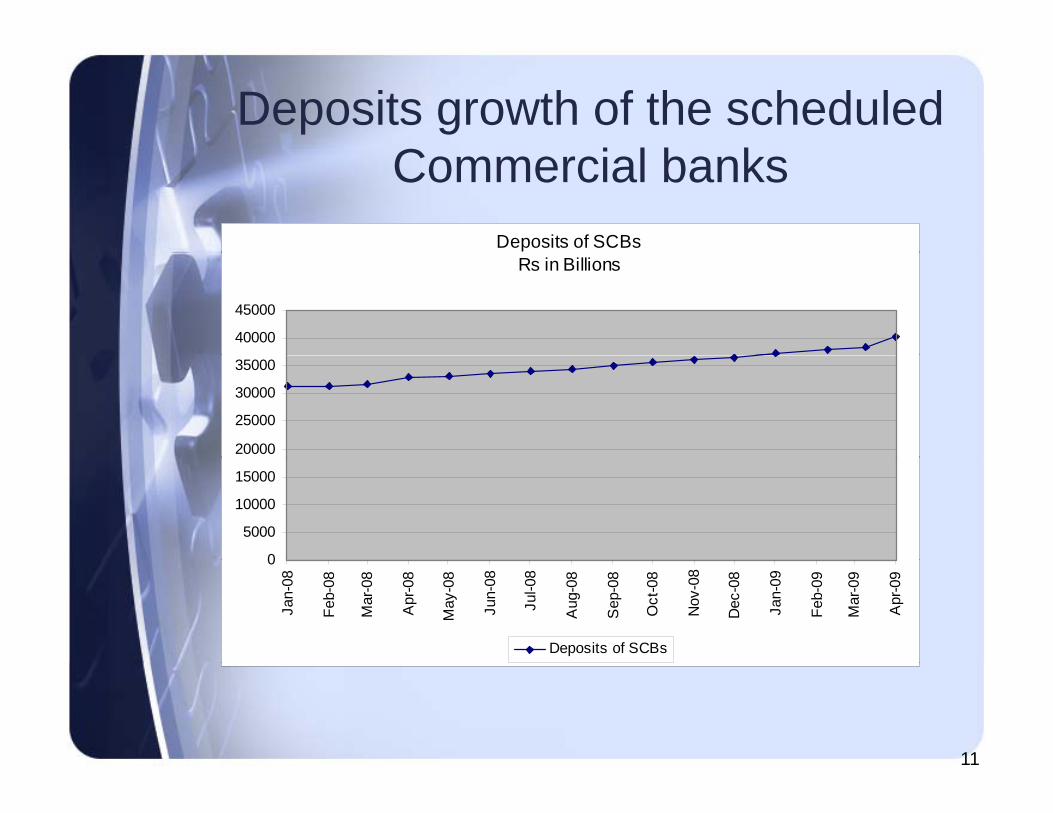

Deposits growth of the scheduled C i l b kCommercial banks

Deposits of SCBsRs in Billions

40000

45000

20000

25000

30000

35000

0

5000

10000

15000

0

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr

-09

Deposits of SCBs

11

Emergence of constraints Liquidity position of banksLiquidity position of banks

(a) Pre September 2008(a) Pre-September 2008Liquidity influenced by Focus onContaining InflationContaining Inflation

(a) Post September 2008(a) Post September 2008Liquidity influenced by Focus onproviding adequate liquidity

12

providing adequate liquidity

Macro PictureMacro Picture

• The demand for housing loan is reportedly less robust due toreportedly less robust due to

expectations of decline in real estate prices.p

• Though Liquidity stress had been faced enough liquidity was available as part of

Central bank efforts.

13

RBIs Approach

•Providing ample rupee liquidity•Providing ample rupee liquidity

E i f t bl d ll li idit•Ensuring comfortable dollar liquidity

M i t i i k t i t•Maintaining market environment conducive to flow of credit to productive sector

14

sector

Impact of measures to ease t i tconstraints

– What were the measures taken ?– How conventional orHow conventional or

unconventional the measures were?

– How effective were the unconventional measures?

15

Policy Measures taken by RBI

– CRR reduced by 400 basis pointsCRR reduced by 400 basis points

– SLR reduced by 100 basis pointsy p

– Export Credit refinance eligibility enhanced to50% of Outstanding export

Special 14 day term repo introduced– Special 14 day term repo introduced

– Special Refinance facility for banks

16

Special Refinance facility for banks

Measures taken by RBI (contd…)

– Special refinance facilities for SIDBI NHBSpecial refinance facilities for SIDBI, NHBand EXIM Bank

– Forex swap facility made available to banks– All in costs ceiling for ECBs raised.– NBFC-ND-SI permitted to raise short term

foreign currency borrowingsforeign currency borrowings– Provision for liquidity to NBFC-ND-SI by SPV– Non Resident Deposits allowed higherNon Resident Deposits allowed higher

interest rates

17

Measures taken by RBI (contd…)

– Repo rate reduced by 400 basis points– Risk weight and provisioning requirements

relaxed.

18

Emergence of Constraints -Absolute inflows into the system on account of

MSS CRR d LAFMSS, CRR and LAFLiquidity Scenario

1500000

2000000

500000

1000000

s. M

illio

n

0

an-0

8

eb-0

8

ar-0

8

pr-0

8

ay-0

8

un-0

8

ul-0

8

ug-0

8

ep-0

8

ct-0

8

ov-0

8

ec-0

8

an-0

9

eb-0

9

ar-0

9

pr-0

9

Amt.

Rs

-1000000

-500000 Ja Fe M A Ma Ju J Au

Se O No

De Ja Fe M A

19

MSS CRR LAF

Impact of Measures - Potential LiquidityLiquidity

Sr. No.

Measure/Facility Amount (Rs. Billion)

1. CRR Reduction 16000.00

2. Unwinding/Buyback/De-sequestering of MSS Securities

9778.10

3. Term Repo Facility 6000.00

4. Increase in Export Refinance 2551.20

5. Special Refinance Facility for SCBs (Non-RRBs)

3850.00( )

6. Refinance Facility for SIDBI/NHB/EXIM 1600.00

7. Liquidity Facility for NBFCs – SPV(I l di ti f R 50000 Milli )

2500.00(Including option of Rs 50000 Million)Total 42279.30

8. SLR Reduction 4000.00

20

9. Open market Operations 688.35

Against the above limits(1-7) Outstanding Amt. as on April 16, 2009 – Rs 1464.90

billi

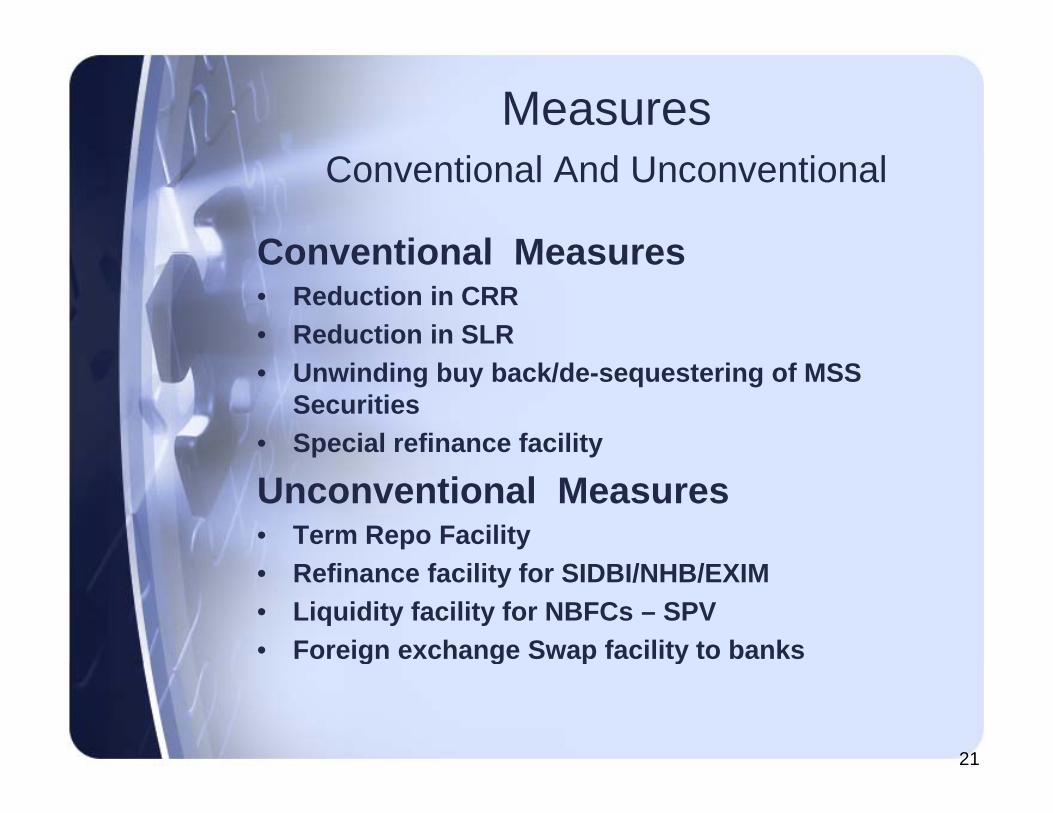

Measures Conventional And Unconventional

Conventional MeasuresConventional Measures• Reduction in CRR• Reduction in SLR• Unwinding buy back/de-sequestering of MSS

Securities • Special refinance facility

Unconventional Measures• Term Repo Facility• Refinance facility for SIDBI/NHB/EXIM• Liquidity facility for NBFCs – SPV• Foreign exchange Swap facility to banks

21

g g p y

Some Key Aspects of Regulation & S i i& Supervision

• Calibrated approach for opening the• Calibrated approach for opening the Capital Account.

• External debt flows subject to ceilingsExternal debt flows subject to ceilings and end use restrictions.

• Participation in the overnight unsecuredParticipation in the overnight unsecured money market restricted to banks and PD

• Ceilings on lendings and borrowings in g g gthis market.

• Prudential limits on inter bank liabilities in

22

relation to net worth

Some Key Aspects of Regulation & S i i& Supervision

• Complex structures like synthetic• Complex structures like synthetic securitisation have not yet been permitted.p

• Dynamic provisioning for selected sectors like real estate, housing loans, gconsumer credit

• Non-Banking finance institutions have been subject to tightened regulation.

23

Future perspective

– As Indian Economy increasingly integratesAs Indian Economy increasingly integrateswith Global Financial System, contagioneffect in case of financial turmoil overseascan be intensivecan be intensive.

– Regulation of systemically importantinstitutions would attract more attention.Li bilit t ld i i it– Liability management would acquire priorityin the management of balance sheet.

– An active domestic debt market would be animportant focus area.

– Well regulated Mortgage guaranteecompanies can provide for credit risk

24

companies can provide for credit riskmitigation for housing finance

Monitoring would continue to gcontinuously evaluate the market

needs.

Thank You.

25