Embed Size (px)

Citation preview

Mangalore SEZ Ltd.

Building & Powering Industry Cluster for Petrochemical/ chemical Industry at Mangalore SEZ

ASSOCHAM Conference, New Delhi 16th Feb ‘15

• Strategic Context• Industry Outlook, growth drivers and issues• Significance of cluster based development

• Why Mangalore - Karnataka as an investment destination• MSEZ proposition•Opportunities for Petrochemical/ Chemical & Allied industries at MSEZ•Current Status of Industrial Projects in the Catchment

• Strategic Context• Industry Outlook, growth drivers and issues• Significance of cluster based development

• Why Mangalore - Karnataka as an investment destination• MSEZ proposition•Opportunities for Petrochemical/ Chemical & Allied industries at MSEZ•Current Status of Industrial Projects in the Catchment

Building & Powering an Industry Cluster at Mangalore SEZBuilding & Powering an Industry Cluster at Mangalore SEZ

Strategic context: Industry outlook, growth drivers and key issues

Strategic Context for Petrochemical/ Chemical industryStrategic Context for Petrochemical/ Chemical industry Sector wise break up of Indian Chemical

Industry In USD Bln• Indian chemical industry :

• Sixth largest by output globally, at USD 118 Bln.

• accounts for 3% of the global market

• Indian market:

• is the world’s third largest consumer of polymers and third largest producer of agro-chemicals

• accounts for 16% of the world production of dyestuff and dye intermediates.

• Highly diversified with above 70,000 products

• The production of chemicals at 19.5 Mln Tons lags consumption of 25 Mln tons

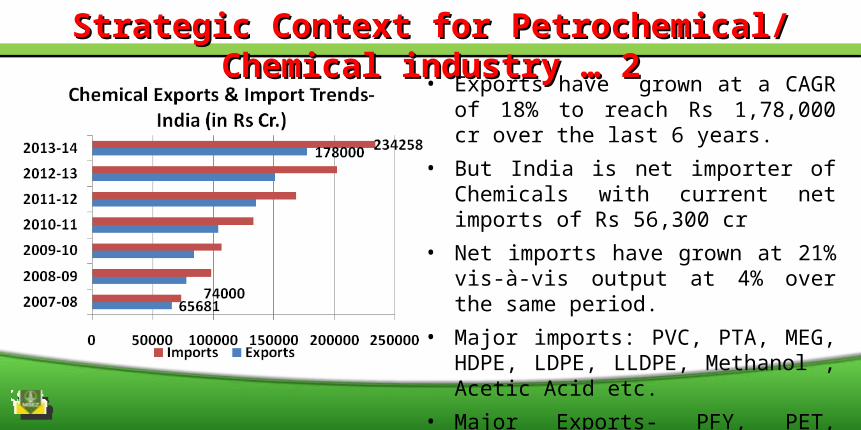

Strategic Context for Petrochemical/ Chemical industry … 2Strategic Context for Petrochemical/ Chemical industry … 2 • Exports have grown at a CAGR of 18% to

reach Rs 1,78,000 cr over the last 6 years.• But India is net importer of Chemicals with

current net imports of Rs 56,300 cr• Net imports have grown at 21% vis-à-vis

output at 4% over the same period.• Major imports: PVC, PTA, MEG, HDPE, LDPE,

LLDPE, Methanol , Acetic Acid etc. • Major Exports- PFY, PET, Benzene, Dyes,

Agro chemicals , Pigments etc.

Strategic context - Industry Growth DriversStrategic context - Industry Growth Drivers• Robust GDP growth projections over next decade – one of the highest in the world• Large head room for growth :

• Low per capita consumption of Petrochemicals at 7kgs against 109 kgs in USA; 32 kgs in Brazil and 29 kgs in China

• Growing disposable incomes and increased urbanisation• High demographic dividend• Rapid growth in domestic market for end products

• “Make in India” campaign seeking to enhance the share of manufacturing in GDP• Setting up of PCPIR’s ( & SEZ’s), with cluster approach

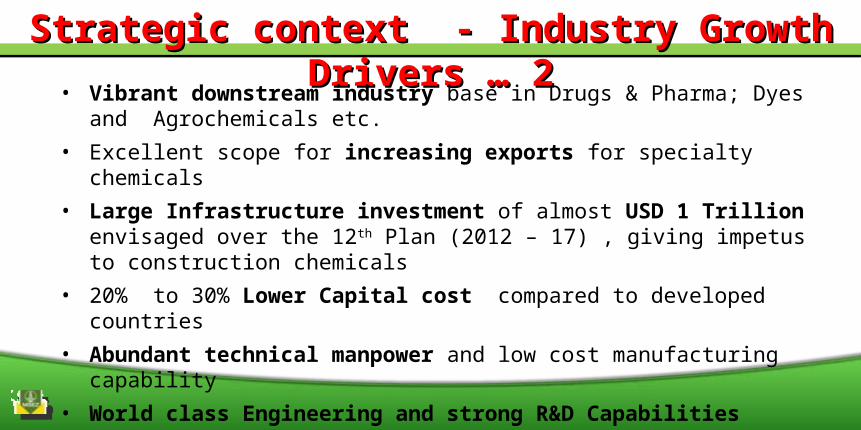

Strategic context - Industry Growth Drivers … 2Strategic context - Industry Growth Drivers … 2• Vibrant downstream industry base in Drugs & Pharma; Dyes and Agrochemicals etc.• Excellent scope for increasing exports for specialty chemicals• Large Infrastructure investment of almost USD 1 Trillion envisaged over the 12th Plan

(2012 – 17) , giving impetus to construction chemicals • 20% to 30% Lower Capital cost compared to developed countries• Abundant technical manpower and low cost manufacturing capability• World class Engineering and strong R&D Capabilities• Diversified manufacturing base

Strategic context - Growth Outlook Strategic context - Growth Outlook In another decade, India expected to double its share in the Global Chemical Market

FY 13Global : USD 3.4 TlnIndia : USD 118 Bln

FY 23Global : USD 5 TlnIndia : USD 300 Bln

Potential Growth

8-12% pa.

Source: Data Monitor, Industry reports and In -house analysis

Key Issues impacting Growth in Petrochemicals/ Key Issues impacting Growth in Petrochemicals/ ChemicalsChemicals• Inadequate basic infrastructure

• Pricing/ availability issues with feedstock• Highly fragmented downstream industry with low technology/R&D• Sub-optimal plant sizes in the global context• High cost of environmental compliance• Relatively higher Logistics costs• Unfavorable FTA Regime • Complexities in tax structure• Need for compliance with REACH Regulations

Strategic Context : significance of cluster based development for Petrochemical/ chemical industry

Strategic context – Cluster based developmentStrategic context – Cluster based development• Thriving clusters can drive broad based economic development

• Industrial sectors best developed in clusters for:• Cost competitiveness at a global scale thru’:

• Functional/ co-location synergies enhanced by proximity to Port• Proximity to feedstock/ raw materials & potential markets • Forging Partnerships and collaborations• Common shared infrastructure:

• Optimized Capital investments by leveraging scale • Reduced area requirement • Improved environment management

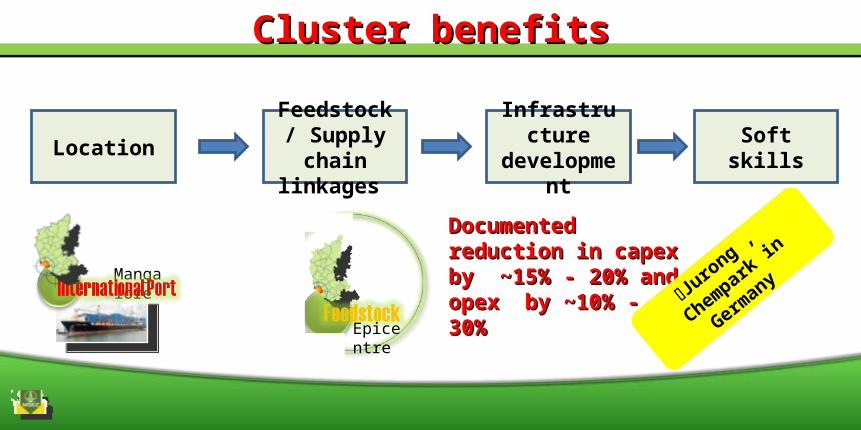

Cluster benefitsCluster benefits

LocationFeedstock/

Supply chain linkages

Infrastructuredevelopment Soft skills

Mangalore

Epicentre

Documented reduction in Documented reduction in capex by ~15% - 20% and capex by ~15% - 20% and opex by ~10% - 30%opex by ~10% - 30%

Jurong , C

hempark in

Germany

Why is Mangalore - Karnataka suited as an investment destination?

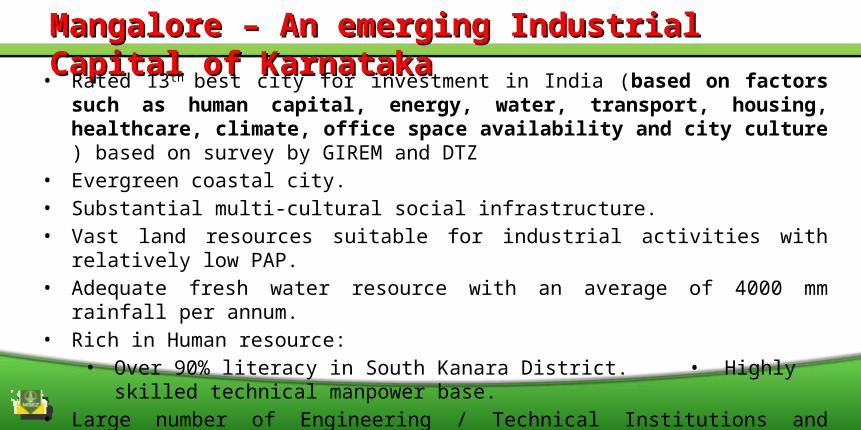

Mangalore – An emerging Industrial Capital of KarnatakaMangalore – An emerging Industrial Capital of Karnataka

• Rated 13th best city for investment in India (based on factors such as human capital, energy, water, transport, housing, healthcare, climate, office space availability and city culture ) based on survey by GIREM and DTZ

• Evergreen coastal city.• Substantial multi-cultural social infrastructure.• Vast land resources suitable for industrial activities with relatively low PAP. • Adequate fresh water resource with an average of 4000 mm rainfall per annum. • Rich in Human resource:

• Over 90% literacy in South Kanara District. • Highly skilled technical manpower base. • Large number of Engineering / Technical Institutions and centers of excellence. • A huge resource base to support multiple growth opportunities

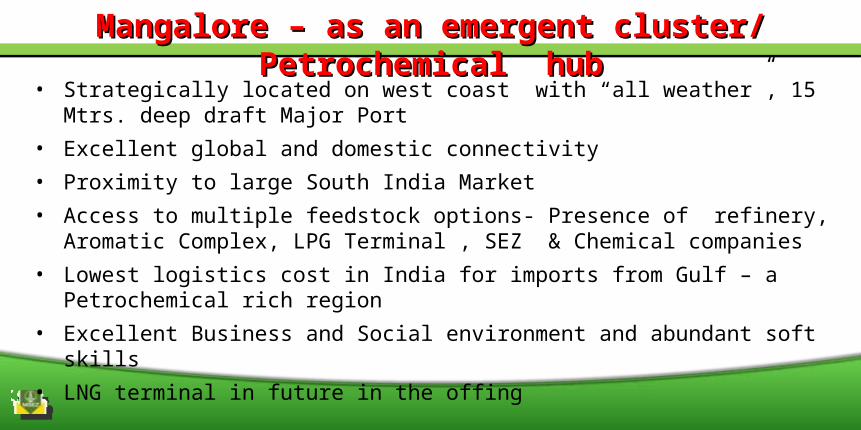

Mangalore – as an emergent cluster/ Petrochemical hubMangalore – as an emergent cluster/ Petrochemical hub

• Strategically located on west coast with “all weather”, 15 Mtrs. deep draft Major Port• Excellent global and domestic connectivity• Proximity to large South India Market• Access to multiple feedstock options- Presence of refinery, Aromatic Complex, LPG

Terminal , SEZ & Chemical companies• Lowest logistics cost in India for imports from Gulf – a Petrochemical rich region• Excellent Business and Social environment and abundant soft skills• LNG terminal in future in the offing

Mangalore - an emerging hub of chemical industriesMangalore - an emerging hub of chemical industriesLeading Petrochemical/Chemical companies in Mangalore – the changing landscape

JBF Industries Ltd.

SPECIAL ECONOMIC SPECIAL ECONOMIC ZONEZONE

Seeks to enable solutions to the emergent issues, as a destination for catering to new opportunities…

An Emergent Industry Cluster

MSEZ - propositionMSEZ - proposition

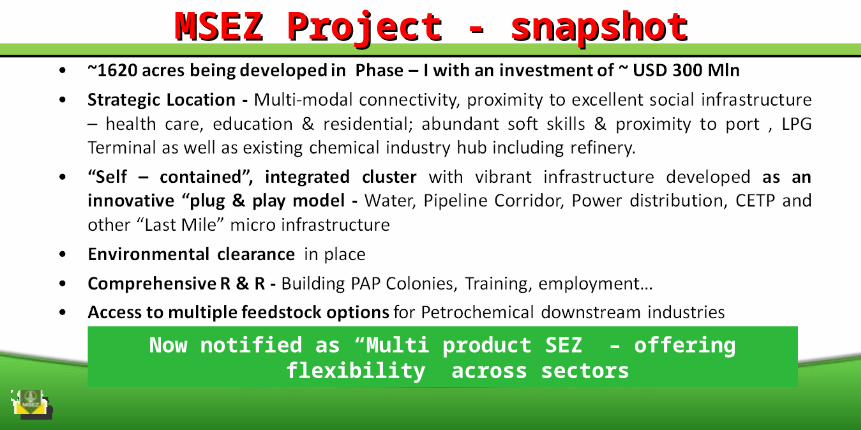

• MSEZL : SPV incorporated in Feb ’06, with the objective of developing a multi-product SEZ. • Reputed Promoters :

• Oil and Natural Gas Corporation (ONGC) - 26%• Karnataka Industrial Area Development Board (KIADB) - 23%• Infrastructure Leasing and Financial Services (IL & FS) - 50%• Kanara Chamber of Commerce & Industry (KCCI) & others - 1%

• Non – Government company structure :• Unique combination of Central, State Govt. entities with fin. institution & industry body.

• Environment Clearance : in place for Phase – I (~1800 acres) for Petrochemical, Chemical & Allied industries

MSEZL – Company profile & structureMSEZL – Company profile & structure

MSEZ Project - snapshotMSEZ Project - snapshot

Now notified as “Multi product SEZ” – offering flexibility across sectors

MSEZ VIDEO

Current Project Status - MSEZLCurrent Project Status - MSEZL

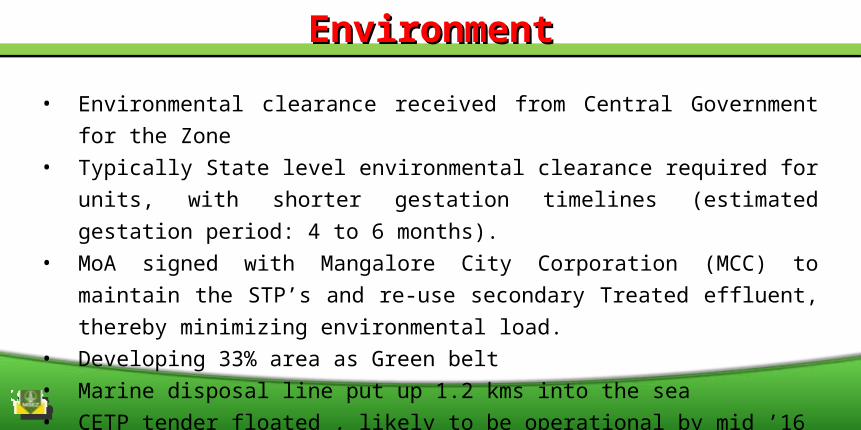

• Environmental clearance received from Central Government for the Zone• Typically State level environmental clearance required for units, with shorter

gestation timelines (estimated gestation period: 4 to 6 months). • MoA signed with Mangalore City Corporation (MCC) to maintain the STP’s and re-use

secondary Treated effluent, thereby minimizing environmental load. • Developing 33% area as Green belt • Marine disposal line put up 1.2 kms into the sea• CETP tender floated , likely to be operational by mid ’16

EnvironmentEnvironment

Well endowed Social Infrastructure

Cosmopolitan

Beautiful Beach City

Availability of Talent poolUrban

International Airport

Emerging as State Industrial ‘Capital’

&&Enjoy Living Working in inin

Social infrastructureSocial infrastructure

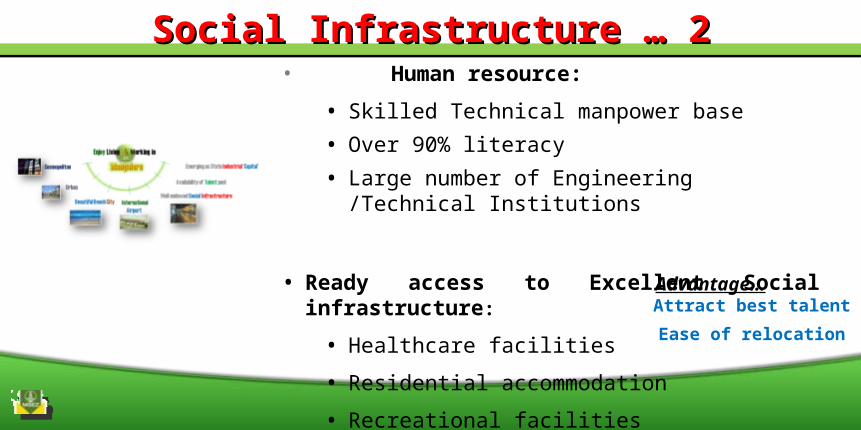

• Human resource:

• Skilled Technical manpower base

• Over 90% literacy

• Large number of Engineering /Technical Institutions

• Ready access to Excellent Social infrastructure:

• Healthcare facilities

• Residential accommodation

• Recreational facilities

Advantage… Attract best talent

Ease of relocation

Social Infrastructure … 2Social Infrastructure … 2

•Excellent Global Connectivity to Europe & SE Asia through Mangalore Port• International Airport in close proximity•One of the lowest logistics costs from India to Gulf - key source of feedstock•Free Trade Warehousing zone/ Logistics Park facilitating international trade•Duty free regime & tax benefits for export income•Streamlined systems & procedures Export and import•Flexible labour Laws

Export AdvantageExport Advantage

A large, fast growing consumption market for Petroleum, Petrochemical & Specialty Chemicals.

Area in 600 km radius of MSEZ accounts for 20% of India’s GDP.

Yet this area accounts for only 5% of Petrochemical production !

While Exports is the focus for units located in SEZ, they have the flexibility of catering to the Domestic markets as well – as long as the Net Foreign Exchange (NFE) criteria

is met over 5 years.

Handsome Cluster benefits

Domestic Market AdvantageDomestic Market Advantage

SEZ BenefitsSEZ BenefitsFiscal Benefits Exemption (E)/

Refund (R)Development

StageOperation

StageOn Capital Goods, Components, Consumables, Raw Materials & Spares

• Customs Duty E • Domestic Procurement - Excise Duty E • - Sales Tax/ VAT R • - Service Tax E / R • - Purchase Tax E

On Other Transactions• Stamp duty & Registration Fees 50% E • Stamp duty on Mortgages 50% E • Electricity Duty and Taxes E • Domestic Sales –Subject to NFE Conditions X • Income Tax (100% for 5 yrs. + 50% for next 5 yrs + 50% ploughed back export profit from next 5 years ) X

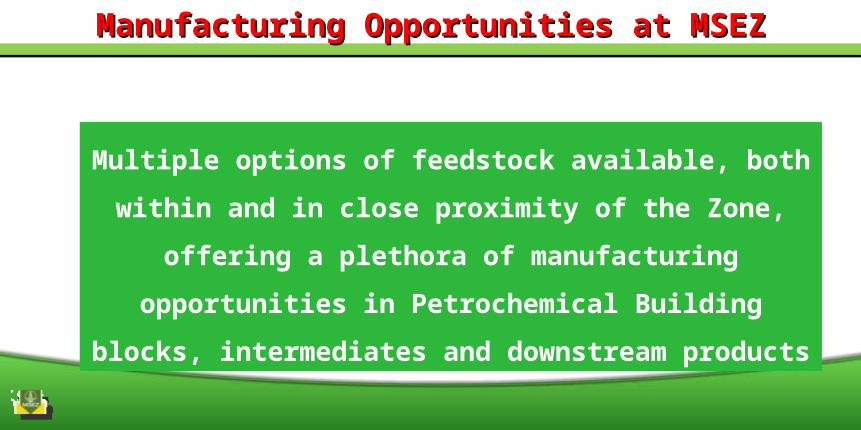

Multiple options of feedstock available, both within and in close

proximity of the Zone, offering a plethora of manufacturing

opportunities in Petrochemical Building blocks, intermediates

and downstream products

Manufacturing Opportunities at MSEZManufacturing Opportunities at MSEZ

Feedstock AvailabilityFeedstock Availability

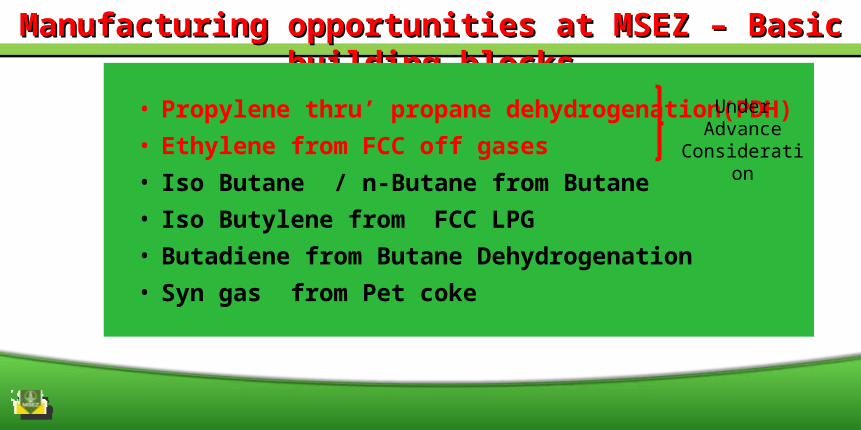

Manufacturing opportunities at MSEZ – Basic building blocksManufacturing opportunities at MSEZ – Basic building blocks

• Propylene thru’ propane dehydrogenation(PDH)• Ethylene from FCC off gases• Iso Butane / n-Butane from Butane• Iso Butylene from FCC LPG• Butadiene from Butane Dehydrogenation• Syn gas from Pet coke

Under Advance

Consideration

Manufacturing opportunities at MSEZ – IntermediatesManufacturing opportunities at MSEZ – Intermediates

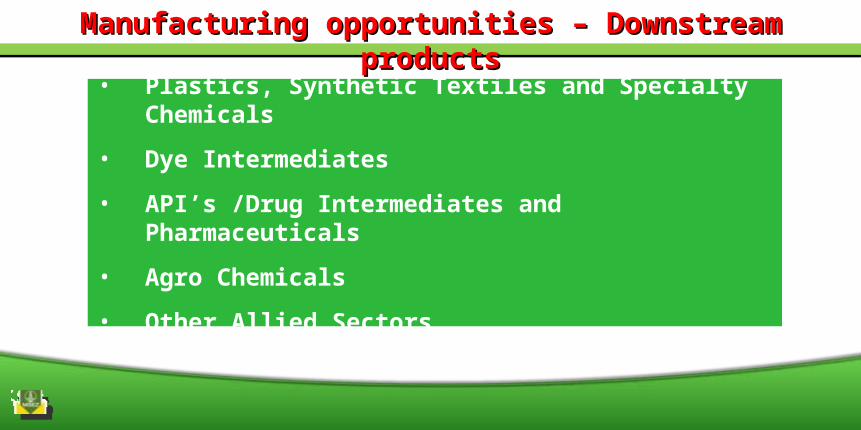

Manufacturing opportunities – Downstream productsManufacturing opportunities – Downstream products

• Plastics, Synthetic Textiles and Specialty Chemicals

• Dye Intermediates

• API’s /Drug Intermediates and Pharmaceuticals

• Agro Chemicals

• Other Allied Sectors

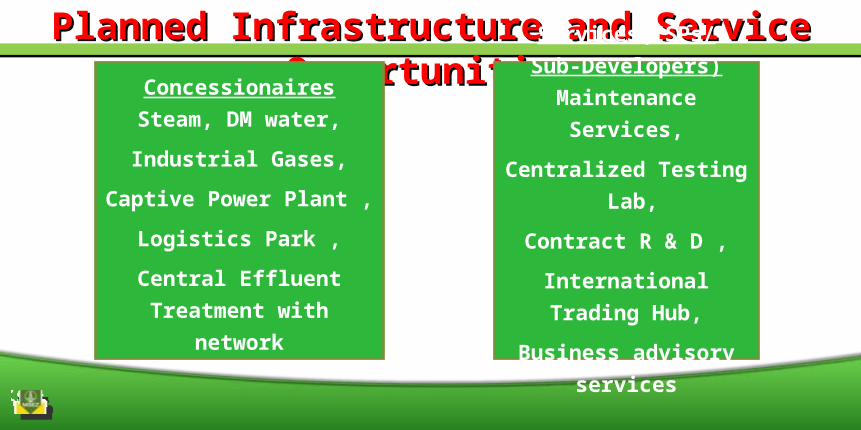

Planned Infrastructure and Service OpportunitiesPlanned Infrastructure and Service Opportunities

ConcessionairesSteam, DM water,

Industrial Gases,

Captive Power Plant ,

Logistics Park ,

Central Effluent Treatment with network

Services(ISPs/Sub-Developers)

Maintenance Services,

Centralized Testing Lab,

Contract R & D ,

International Trading Hub,

Business advisory services

Current Status of Infrastructure and Industrial

Projects in the MSEZ catchment

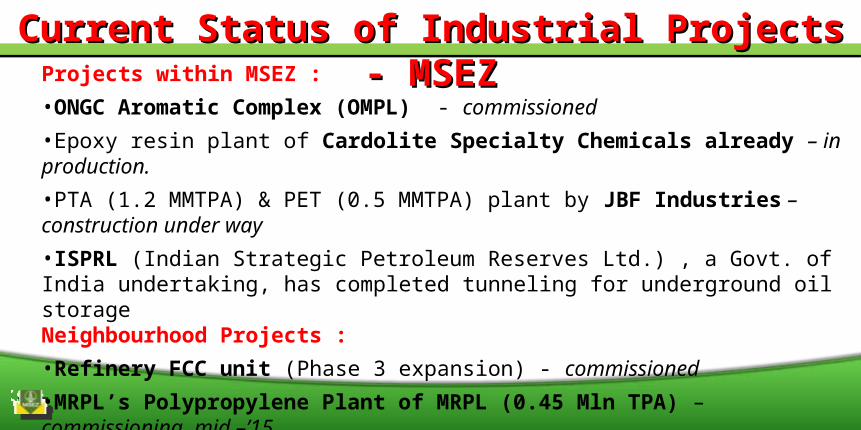

Current Status of Industrial Projects - MSEZCurrent Status of Industrial Projects - MSEZProjects within MSEZ :•ONGC Aromatic Complex (OMPL) - commissioned•Epoxy resin plant of Cardolite Specialty Chemicals already – in production.•PTA (1.2 MMTPA) & PET (0.5 MMTPA) plant by JBF Industries – construction under way•ISPRL (Indian Strategic Petroleum Reserves Ltd.) , a Govt. of India undertaking, has completed tunneling for underground oil storageNeighbourhood Projects :•Refinery FCC unit (Phase 3 expansion) - commissioned •MRPL’s Polypropylene Plant of MRPL (0.45 Mln TPA) – commissioning mid –’15

Thank You

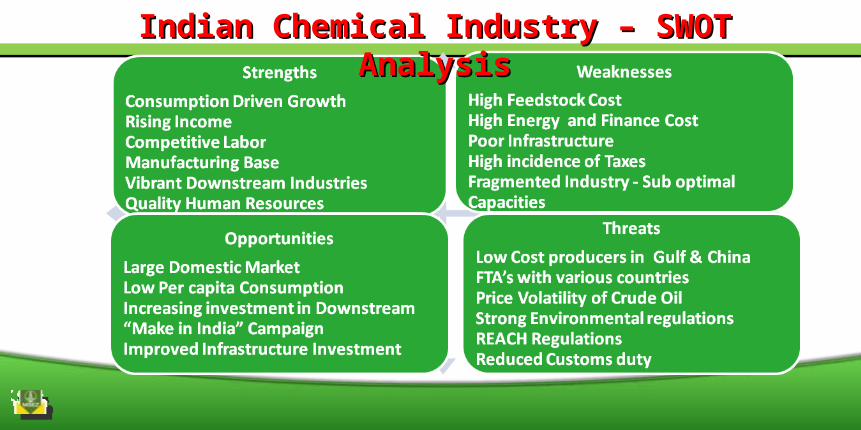

Indian Chemical Industry – SWOT AnalysisIndian Chemical Industry – SWOT Analysis

MANGALOREA PORT CITY

MSEZ - locationMSEZ - location

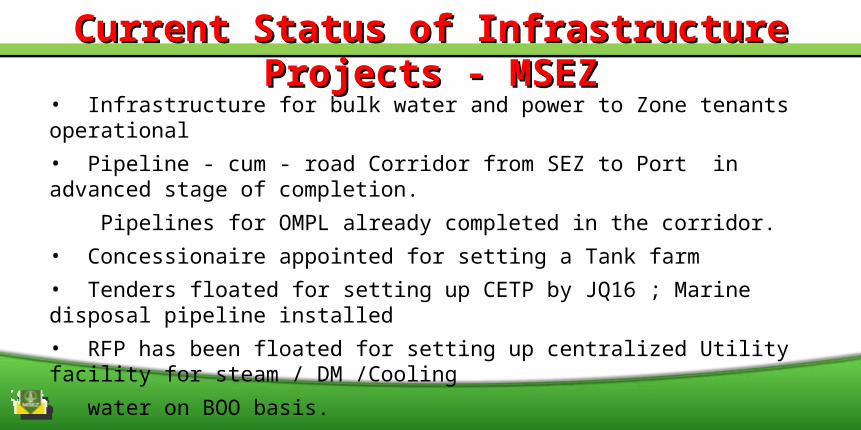

Current Status of Infrastructure Projects - MSEZCurrent Status of Infrastructure Projects - MSEZ

• Infrastructure for bulk water and power to Zone tenants operational• Pipeline - cum - road Corridor from SEZ to Port in advanced stage of completion.

Pipelines for OMPL already completed in the corridor.• Concessionaire appointed for setting a Tank farm• Tenders floated for setting up CETP by JQ16 ; Marine disposal pipeline installed• RFP has been floated for setting up centralized Utility facility for steam / DM /Cooling

water on BOO basis.