Embed Size (px)

Citation preview

Manufacturing Bulletin Q3-2011

Presentation : Media Briefing

8 December 2011

By

Dr Iraj AbedianPan-African Investment & Research Services(Pty) Ltd.

Slide # 2

Outline

1. Introduction

2. Overall Manufacturing Business Confidence

3. Current South African Manufacturing Trends

4. Manufacturing Survey Results: Q3-2011

5. Concluding Remarks

Slide # 3

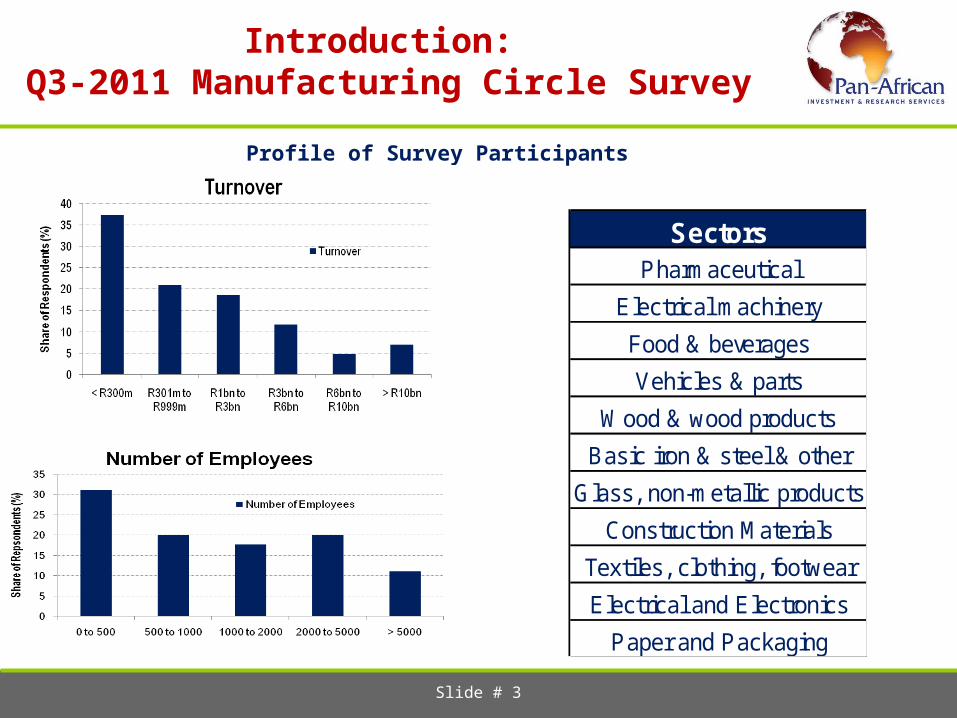

Introduction: Q3-2011 Manufacturing Circle Survey

SectorsPharmaceutical

Electrical machinery

Food & beverages

Vehicles & parts

Wood & wood products

Basic iron & steel & other

Glass, non-metallic products

Construction Materials

Textiles, clothing, footwear

Electrical and Electronics

Paper and Packaging

Profile of Survey Participants

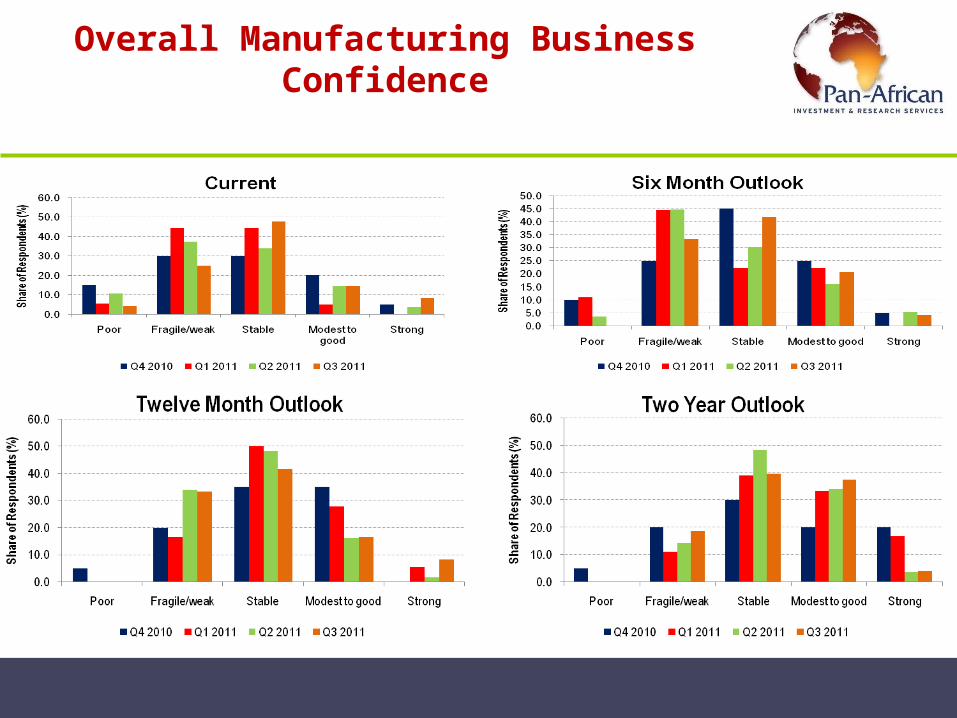

Overall Manufacturing Business Confidence

Current South African

Manufacturing Trends

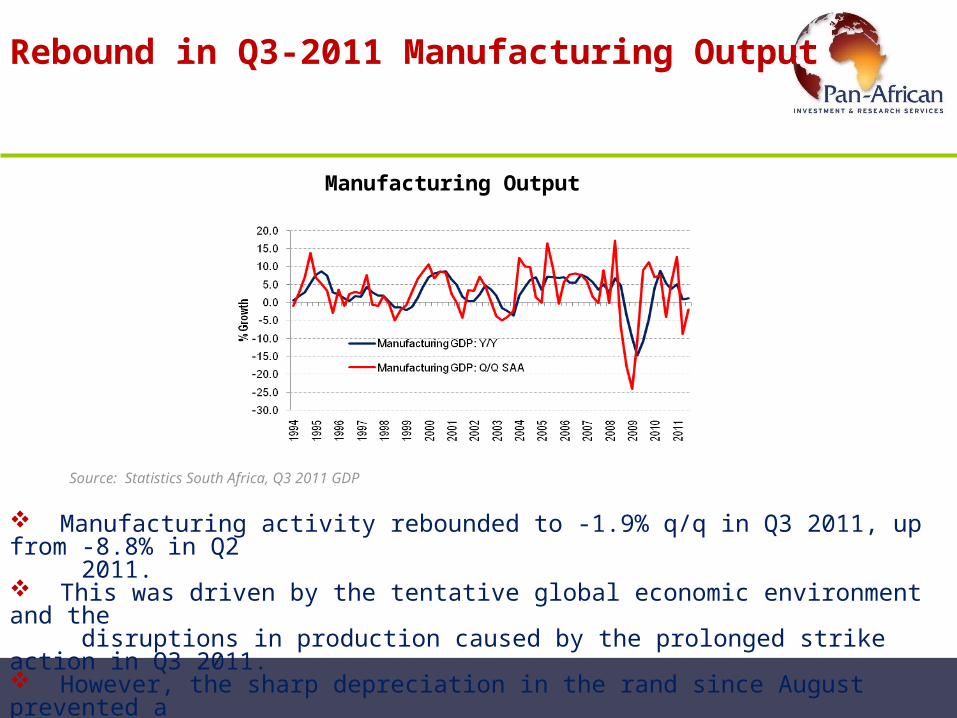

Rebound in Q3-2011 Manufacturing Output

Source: Statistics South Africa, Q3 2011 GDP

Manufacturing activity rebounded to -1.9% q/q in Q3 2011, up from -8.8% in Q2 2011. This was driven by the tentative global economic environment and the disruptions in production caused by the prolonged strike action in Q3 2011. However, the sharp depreciation in the rand since August prevented a steep decline continuing into Q3.

Manufacturing Output

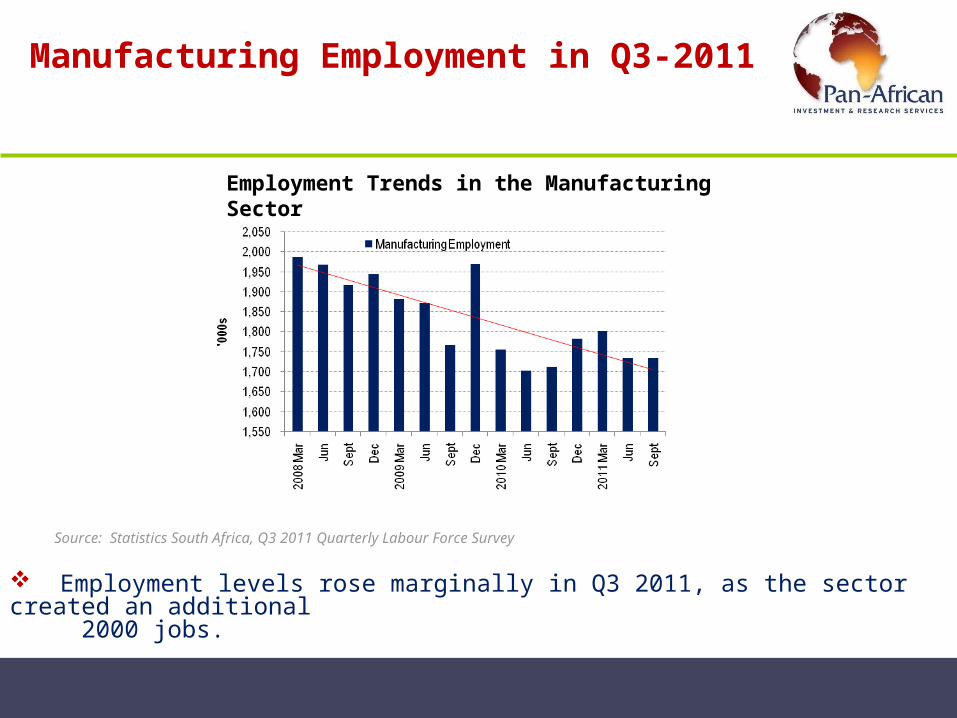

Manufacturing Employment in Q3-2011

Source: Statistics South Africa, Q3 2011 Quarterly Labour Force Survey

Employment levels rose marginally in Q3 2011, as the sector created an additional 2000 jobs.

Employment Trends in the Manufacturing Sector

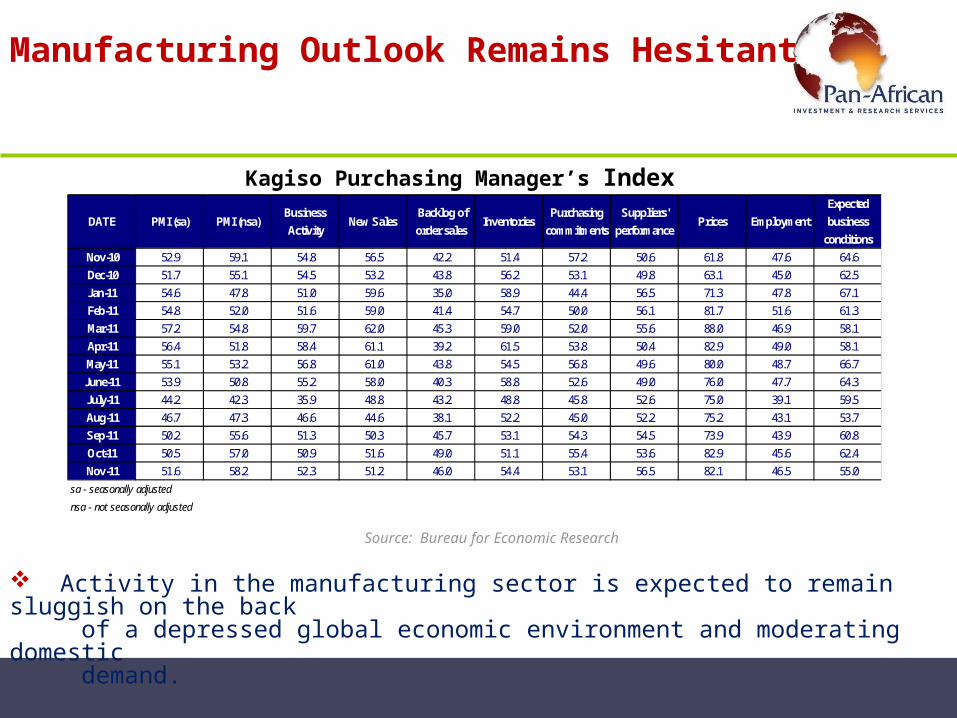

Manufacturing Outlook Remains Hesitant

Source: Bureau for Economic Research

Activity in the manufacturing sector is expected to remain sluggish on the back of a depressed global economic environment and moderating domestic demand.

Kagiso Purchasing Manager’s Index

DATE PMI (sa) PMI (nsa)Business

ActivityNew Sales

Backlog of

order salesInventories

Purchasing

commitments

Suppliers'

performancePrices Employment

Expected

business

conditions

Nov-10 52.9 59.1 54.8 56.5 42.2 51.4 57.2 50.6 61.8 47.6 64.6Dec-10 51.7 55.1 54.5 53.2 43.8 56.2 53.1 49.8 63.1 45.0 62.5Jan-11 54.6 47.8 51.0 59.6 35.0 58.9 44.4 56.5 71.3 47.8 67.1Feb-11 54.8 52.0 51.6 59.0 41.4 54.7 50.0 56.1 81.7 51.6 61.3Mar-11 57.2 54.8 59.7 62.0 45.3 59.0 52.0 55.6 88.0 46.9 58.1Apr-11 56.4 51.8 58.4 61.1 39.2 61.5 53.8 50.4 82.9 49.0 58.1May-11 55.1 53.2 56.8 61.0 43.8 54.5 56.8 49.6 80.0 48.7 66.7June-11 53.9 50.8 55.2 58.0 40.3 58.8 52.6 49.0 76.0 47.7 64.3July-11 44.2 42.3 35.9 48.8 43.2 48.8 45.8 52.6 75.0 39.1 59.5Aug-11 46.7 47.3 46.6 44.6 38.1 52.2 45.0 52.2 75.2 43.1 53.7Sep-11 50.2 55.6 51.3 50.3 45.7 53.1 54.3 54.5 73.9 43.9 60.8Oct-11 50.5 57.0 50.9 51.6 49.0 51.1 55.4 53.6 82.9 45.6 62.4Nov-11 51.6 58.2 52.3 51.2 46.0 54.4 53.1 56.5 82.1 46.5 55.0

sa - seasonally adjusted

nsa - not seasonally adjusted

Manufacturing Survey: Q3-2011

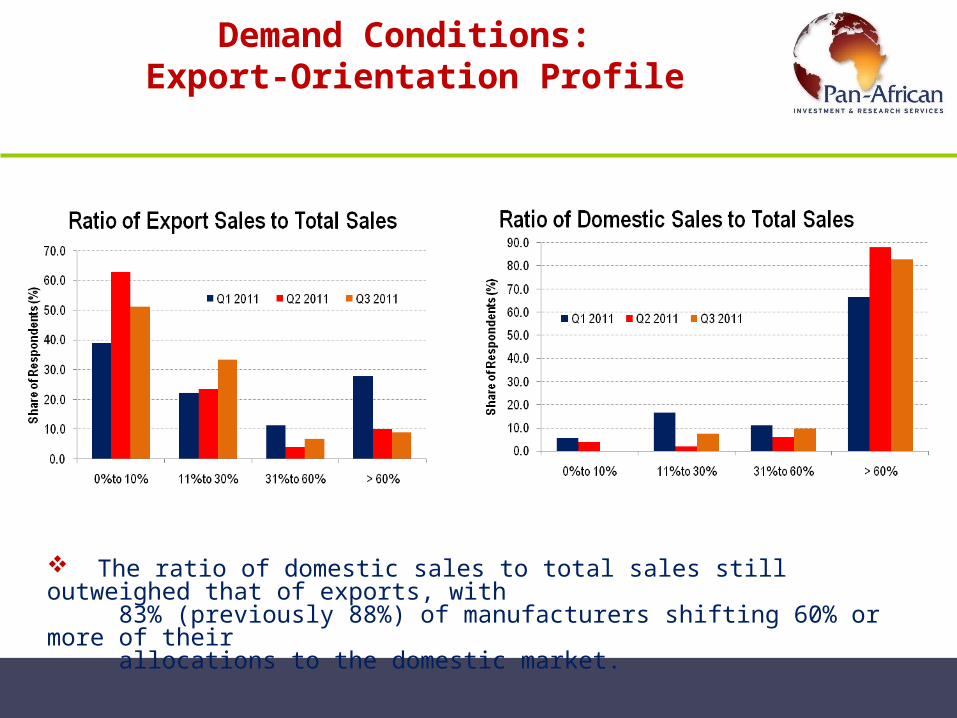

Demand Conditions: Export-Orientation Profile

The ratio of domestic sales to total sales still outweighed that of exports, with 83% (previously 88%) of manufacturers shifting 60% or more of their allocations to the domestic market.

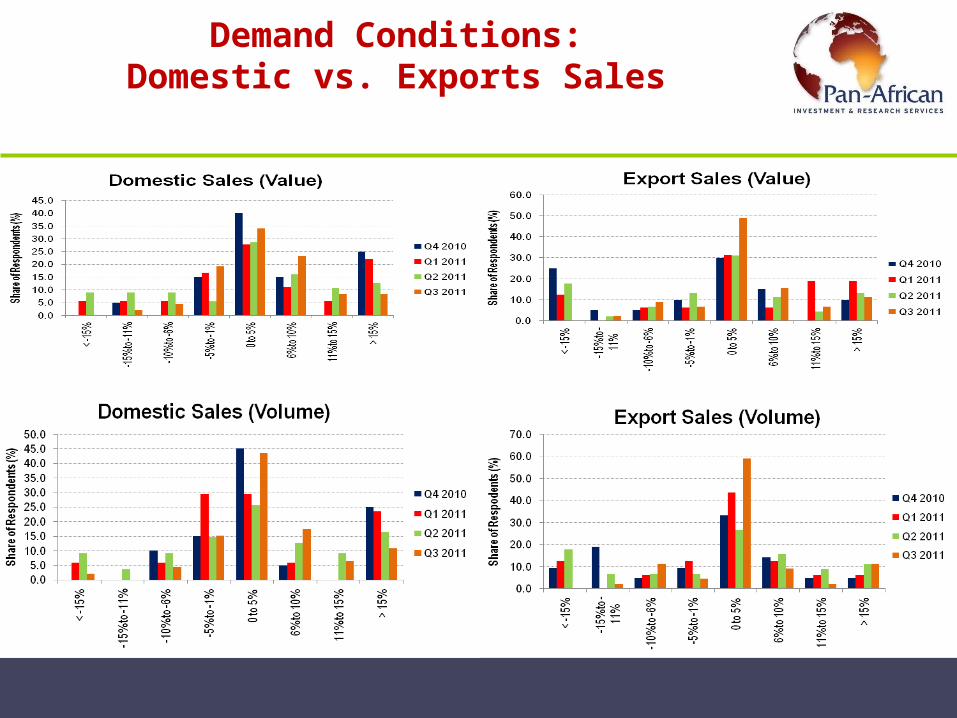

Demand Conditions:Domestic vs. Exports Sales

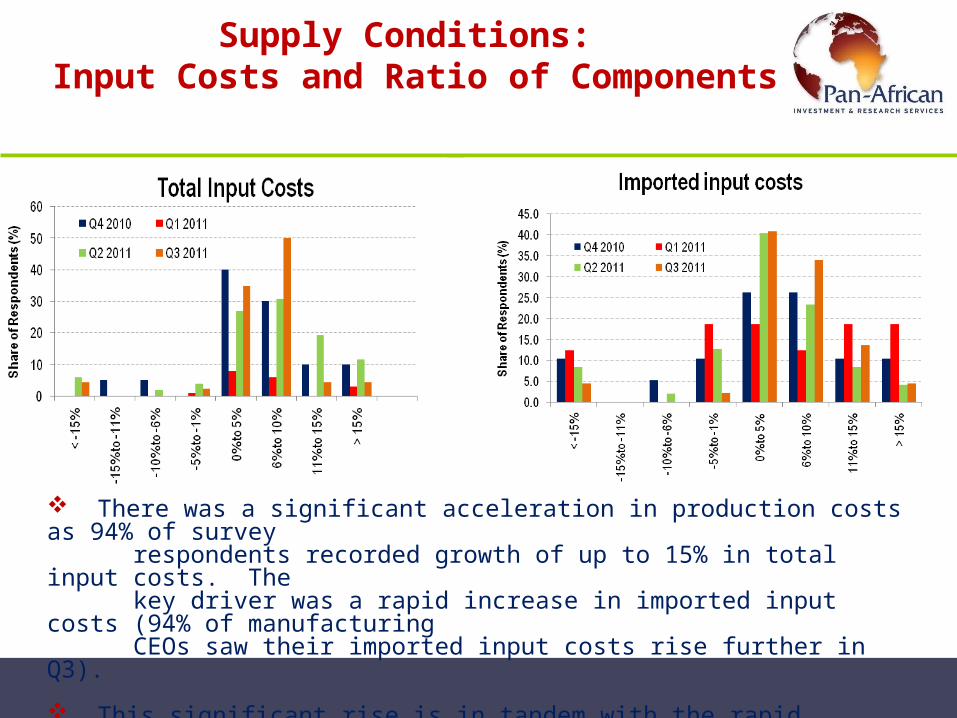

Supply Conditions: Input Costs and Ratio of Components

There was a significant acceleration in production costs as 94% of survey respondents recorded growth of up to 15% in total input costs. The key driver was a rapid increase in imported input costs (94% of manufacturing CEOs saw their imported input costs rise further in Q3).

This significant rise is in tandem with the rapid acceleration in producer prices.

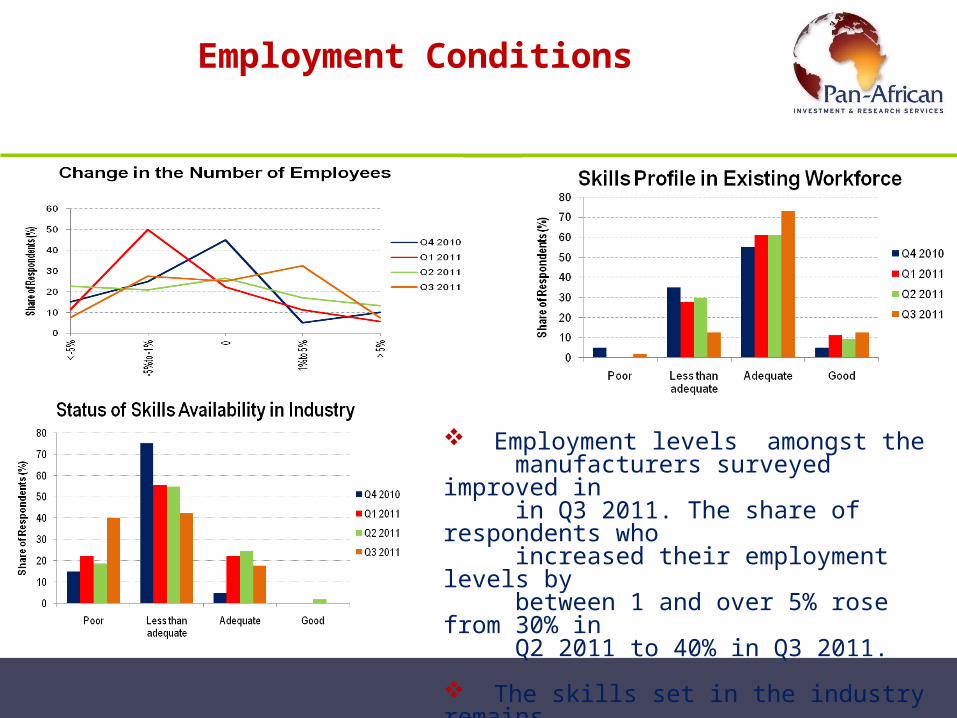

Employment Conditions

Employment levels amongst the manufacturers surveyed improved in in Q3 2011. The share of respondents who increased their employment levels by between 1 and over 5% rose from 30% in Q2 2011 to 40% in Q3 2011. The skills set in the industry remains mediocre.

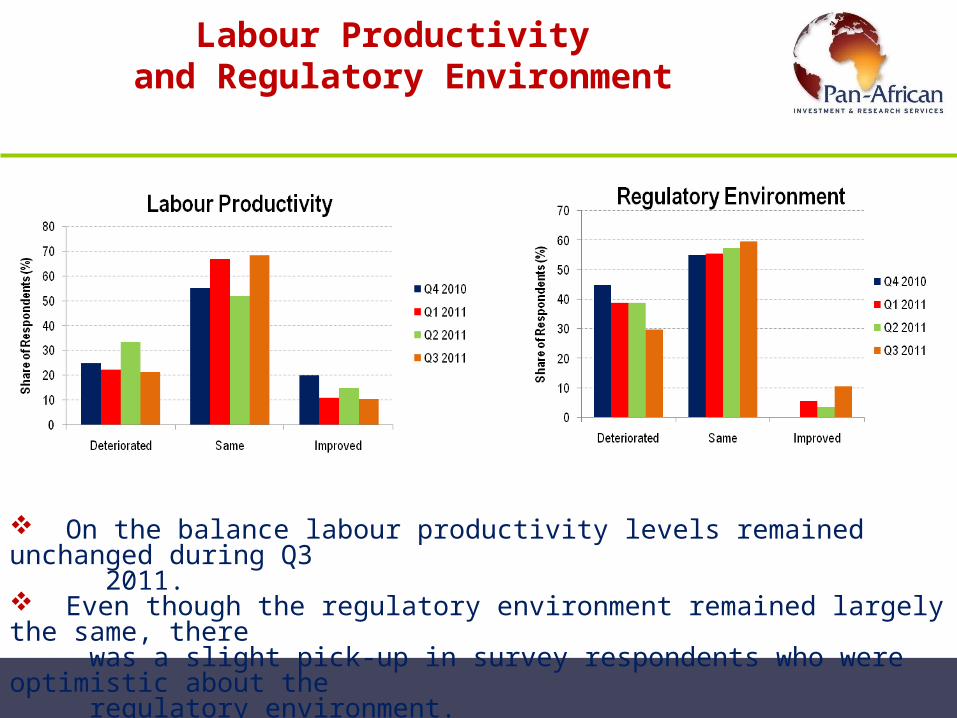

Labour Productivity and Regulatory Environment

On the balance labour productivity levels remained unchanged during Q3 2011. Even though the regulatory environment remained largely the same, there was a slight pick-up in survey respondents who were optimistic about the regulatory environment.

Financial Conditions

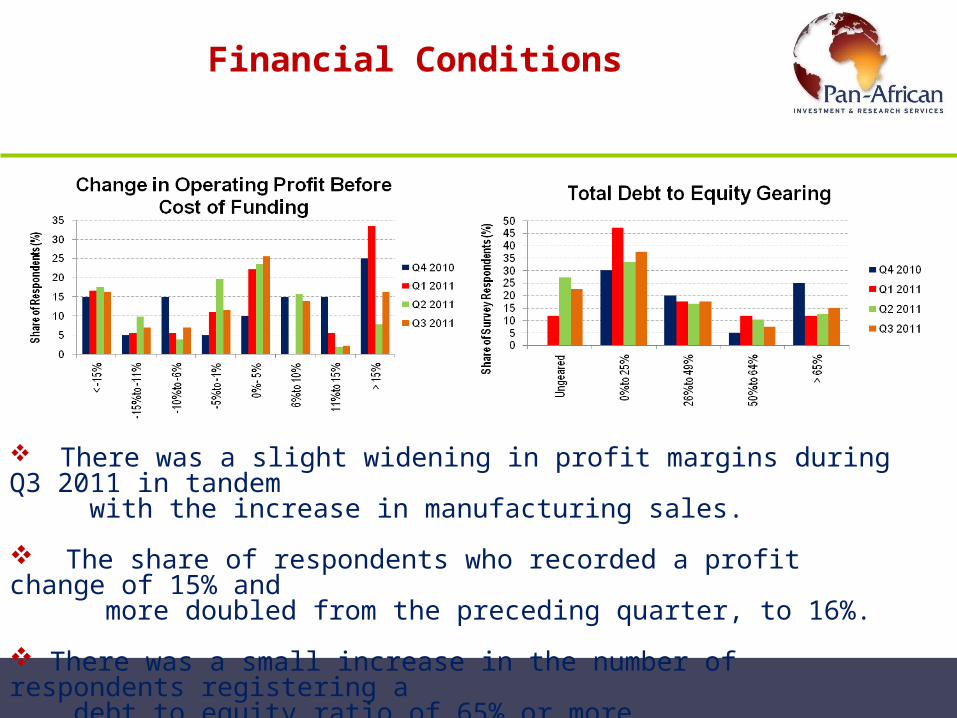

There was a slight widening in profit margins during Q3 2011 in tandem with the increase in manufacturing sales.

The share of respondents who recorded a profit change of 15% and more doubled from the preceding quarter, to 16%.

There was a small increase in the number of respondents registering a debt to equity ratio of 65% or more.

Financial Conditions

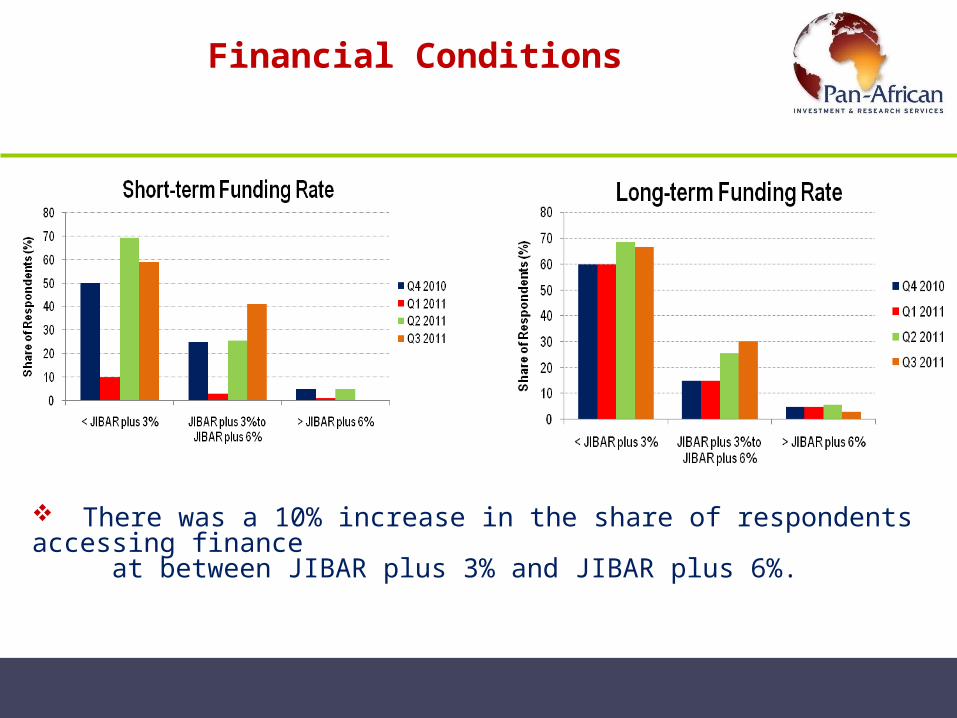

There was a 10% increase in the share of respondents accessing finance at between JIBAR plus 3% and JIBAR plus 6%.

Concluding Remarks:

The manufacturing sector continues to face serious bottlenecks;

Based on the survey results, the domestic manufacturing sector should see further improvement during Q4- 2011.

However, the unfavourable global economic environment and moderating domestic demand will keep the growth in the sector contained.

Slide # 18

Thank you for your attention

![SOHEIL ABEDIAN Executive Chairman SAHBA ABEDIAN Managing ...€¦ · [2004] lumiere [2004] newstead terraces [2005] arbour in the park [2005] q1 [2005] q1 [2006] cammeray residences](https://img.pdfslide.net/doc/110x75/5fc9c496cb33416f5b2cd306/soheil-abedian-executive-chairman-sahba-abedian-managing-2004-lumiere-2004.jpg)

![[Iraj Bashiri] the Samanids & the Revival of the Civilisation of Iranian Peoples_1998](https://img.pdfslide.net/doc/110x75/55cf9d3e550346d033acd4ad/iraj-bashiri-the-samanids-the-revival-of-the-civilisation-of-iranian-peoples1998.jpg)