Embed Size (px)

Citation preview

The CenterWatch Monthly (ISSN 1556-3367). Volume 23, Issue 03. © 2016 CenterWatch centerwatch.com

Adopt customized EDC and CTMS while offering own niche solutionsBy Karyn Korieth

T hird-party vendors have come to dominate the clinical trial technol-ogy sector, which was led by CROs a

decade ago. At the same time, many large CROs continue to invest in technology so-lutions to differentiate their services and offer greater efficiencies in clinical devel-opment processes.

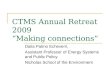

The eClinical solutions market, which includes electronic data capture (EDC) and clinical trial management systems (CTMS), could generate total global sales of $5 billion by 2018, representing a five-year annual growth rate of 13.5%, according to a recent report from global market research company MarketsandMarkets. Yet much of the growth in clinical trial technologies is expected to come from niche providers rather than in-house systems developed by CROs.

Icon Chief Information Officer Tom O’Leary said there has been a “seismic shift” away from internally developed EDC and CTMS systems during the past 15 years. Today, the majority of CROs use commercially developed enterprise appli-cations to support clinical development in phase II and phase III trials. Phase IV and post-marking studies tend to have more unique requirements that are often supported by specialist applications and software systems from CROs and niche providers.

“There is little doubt that a number of niche providers have taken a revenue

stream away from CROs when it comes to technologies. There are fewer CROs in the market today than there were 15 years ago. The CROs who didn’t have a broad technol-ogy and service offering have been acquired or left the market completely,” said O’Leary.

Yet technology remains a big part of CRO service offerings, particularly as CROs and sponsors feel pressure to con-tain costs and expedite the clinical trial process. Leading CROs have adapted their businesses to customize commercially available EDC and CTMS application sys-tems and continue to grow and diversify their technology offerings. As the market has evolved, large CROs have focused on ways to differentiate their technology sys-tems, work cooperatively with a range of third-party providers and develop solu-tions to integrate platforms across compa-nies and trials.

“There is a huge opportunity for smart CROs to do things with technology to distinguish and differentiate their servic-es,” said Glen de Vries, president and co-founder of Medidata Solutions.

Changing EDC landscape

The industry began implementing EDC, which has become the most widely used clinical trial technology, in the late 1990s after the rise of the Internet allowed for development of Web-based software that investigative site staff could access with ex-isting computers.

In the early days, CROs worried that EDC technology would cut into core rev-enue streams by requiring fewer monitors and fewer billable hours. Many developed in-house technologies and systems or ac-quired small EDC companies to support digitalized data collection. Around the same time, a variety of new and established technology vendors entered the market-place.

About eight years ago, the eClinical space began to consolidate through more than a dozen deals, including Oracle’s ac-quisition of Phase Forward in 2010. Tech-nology companies aimed to offer sponsors a single platform to meet all of their data collection and management needs on a

CROs juggle proprietary and commercial systemsMarch 2016 A CenterWatch Feature Article Reprint Volume 23, Issue 03

Size of the global EDC market($U.S. in billions)

Source: MarketsandMarkets

2014

$3

2018p 2020p

$4.8

$5.9

2016e

$3.7

e=estimatedp=projected

CenterWatch Publications and ServicesClinical Trials Data Library A valuable online resource providing access to comprehensive charts and tables on the life sciences and clinical research industry.

CWWeeklyA digital newsletter that reports on breaking news in the clinical trials industry distributed every Monday morning. Annual subscriptions are $249.

CenterWatch News OnlineA free, virtual newsletter that covers news, developments and drug and professional updates of the clinical research enterprise as it unfolds.

Research PractitionerA bi-monthly publication providing educational articles and practical insights and tools for study conduct professionals. Subscribers can earn up to 18 ANCC contact hours each year. Annual subscriptions start at $143.

JobWatchA Web-based service featuring clinical research jobs, career resources and a searchable resume database.

Drugs in Clinical Trials DatabaseA searchable database of 4,500+ detailed profiles of new drugs in development. Custom drug intelligence reports covering a variety of medical conditions can be prepared.

Clinical Trials Listing Service™An international listing service of actively enrolling clinical trials to support sponsors, CROs and sites in their patient enrollment initiatives.

Market Analytics ServicesCustom surveys for organizations to gain competitive insight into the market and their business.

Training Guides/SOPs/Reports l Benchmark Data Reportsl Global Issues in Patient

Recruitment and Retentionl Protecting Study Volunteers in

Research, 4th Ed.l The CRA’s Guide to Monitoring

Clinical Research, 3rd Ed.l The CRC’s Guide to Coordinating

Clinical Research, 2nd Ed.l The PI’s Guide to Conducting

Clinical Research l SOPs for Clinical Research Sitesl SOPs for SponsorslSOPs for Medical Device Sponsors

ContactSales, (617) 948-5100, or [email protected].

global level. EDC platforms, for example, could be coupled with clinical data man-agement systems (CDMS) or interactive voice response systems (IVRS) as an inte-grated process. As the market consolidated and evolved, it became increasingly diffi-cult and expensive for CROs to maintain their own in-house systems. Some CROs divested their clinical trial technology of-ferings.

“The CROs discovered that once they had a system, they needed to be able to maintain it to adjust to a new regulatory environment. It’s a full-time job,” said François Audibert, vice president of Global Consulting in the eHealth Solutions seg-ment at Bioclinica, a specialty clinical tri-als services provider. “They had to make a decision. Do we want to invest all of that money and effort into this? Or do we want to work with a company that can provide tech as a core offering and concentrate on bringing innovation to our services?”

Today, most major CROs use commer-cially developed EDC and CTMS systems from multiple vendors; some large CROs continue to support internally developed CTMS systems, but most also use systems

developed by third-party vendors in or-der to accommodate sponsor-company preferences. CRO teams with both IT and clinical trials expertise typically work with vendors to customize the software for par-ticular studies or therapeutic needs.

“Our IT department works hand-in-hand with our business counterparts to ensure the functionality required in the system reflects our market-leading prac-tices,” said Quintiles Global Chief Tech-nology Officer Malcolm Postings. “There is effort required to customize the ‘off-the-shelf ’ versions, which is an overhead, but one we balance with additional services. We always speak with the main IT suppli-ers to help influence future versions with our requirements.”

Medidata’s de Vries said CRO teams can add value to commercially available plat-forms. Customization work allows them to differentiate their in-house technology systems.

“There are really good technology teams at CROs. They figure out how to integrate what they are getting at scale from a com-pany like Medidata with things that are go-ing to help them differentiate parts of their

2 The CenterWatch Monthly | March 2016 centerwatch.com

IndustryNews

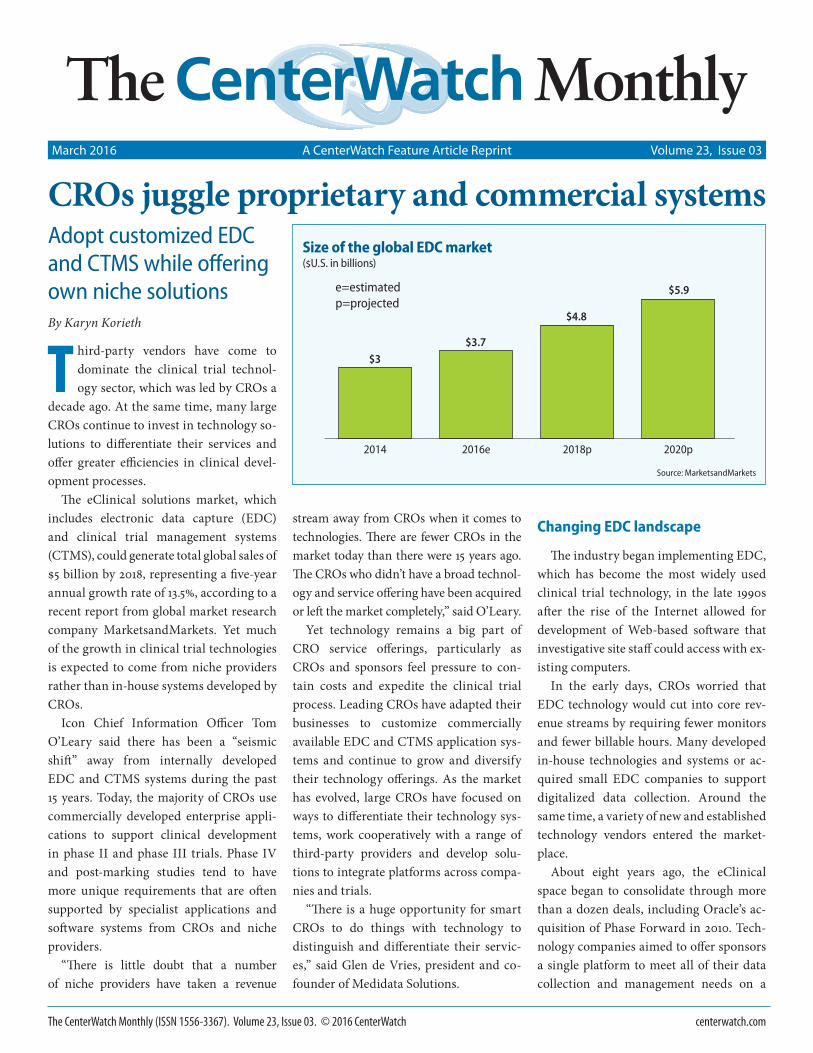

Recent CRO acquisitions of clinical trial technologies

Buyer Acquired company Primary solution(s) Year

Bioclinica Clinverse Automated clinical trial payment firm

2016

PRA Health Sciences

Value Health Solutions

Clinical trial management applications

2015

Icon MediMedia Integrated scientific and market access

2015

Parexel ClinIntel Randomization trial and supply management

2014

Bioclinica Blueprint Clinical Risk-based monitoring 2014

Icon AptivSolutions Design and execution of adaptive

2014

Icon Firecrest Site management and performance

2011

Source: CenterWatch analysis of company reports and websites

business. Whether it’s figuring out how to look at or enhance the way they deal with analytics or connect it to their other op-erational systems, the idea is that they are going to build on that core platform,” said de Vries.

Leading companies also invest in tech-nology segments through acquisitions. This can expand and diversify their service offerings, and support the in-house tech-nology teams that develop and integrate software applications and systems across their service lines.

For example, last year PRA Health Sci-ences acquired clinical development soft-ware company Value Health Solutions to further develop its Predictivv clinical trial management platform. Icon has also made several acquisitions recently to build its technology and service offerings and to differentiate its technology systems. The acquisitions of Firecrest Clinical and Aptiv Solutions provided technologies for patient recruitment and adaptive clinical trials that are different than what other CROs offer. Icon also has teams that develop and integrate software applications across all of its service lines, which include platforms for data collection, information resources

and technology (IRT) and imaging. But O’Leary said the CRO doesn’t view its technology as a core business.

“Technology enables us to differentiate our services more efficiently, which in turn enables us to help our clients to take time and cost from the development program,” he said.

Parexel is unique in that it continues to invest in its technology division, Parexel Informatics, as a core area. The division competes directly with third-party clini-cal development software vendors. Par-exel hosts and maintains its own DataLabs EDC, but the company also can build and

maintain third-party EDC software de-pending on a specific client’s preference. In December, Parexel launched a new, simpli-fied version of its CTMS aimed at small-to-midsized biopharmaceutical companies. Its technology platform includes ran-domization and trial supply management (RTSM) and medical imaging applica-tions. The CRO integrates the technologies into its research processes and also makes them commercially available through a partner program.

David Kiger, vice president, product strategy at Parexel Informatics, said CRO software teams have unique clinical, regu-latory and commercialization expertise that can lead to innovations in the re-search and development process. For ex-ample, Parexel created a platform called LIQUENT InSight to manage the entire lifecycle of a regulatory product, from ear-ly planning through retirement, as a result of many direct conversations with custom-ers about the challenges they encountered in standardizing data to meet legislative requirements.

“Independent software vendors tend to focus on features. As part of a CRO, the Parexel Informatics team brings industry domain expertise to the technology solu-tions,” Kiger said. “With our focus in regu-latory services, Parexel begins the design and capture of data with the end in mind. Domain expertise is critical for the thera-

IndustryNews

3 The CenterWatch Monthly | March 2016 centerwatch.com

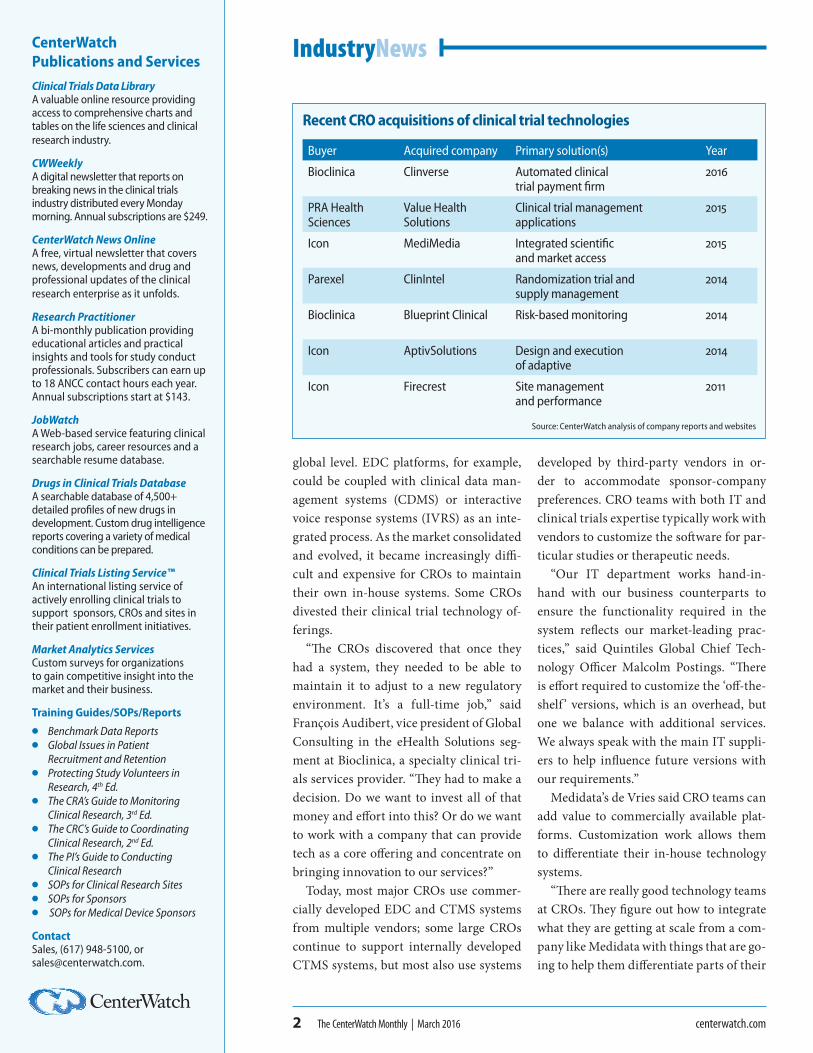

Leading CROs with internally developed CTMS systems

Leading CRO (in alphabetical order) System

Covance Xcellerate

Icon Iconik

Medpace ClinTrak

Parexel Impact

PPD Preclarus

PRA Health Sciences Predictivv

Quintiles Infosario

Source: CenterWatch analysis of company reports and websites

Notable recent acquisitions by technology solutions providers

Buyer Acquired company Primary solution(s) Year

ERT PHT ePRO and mobile clinical trial applications

2015

Medidata Solutions

Patient Profiles Risk-based monitoring applications

2014

IMS Health Cegedim Customer relationshipsmanagement

2014

ERT InvivoData ePRO 2012

IMS Health DecisionView Study planning and execution 2012

Oracle ClearTrial Resource and capacityplanning

2012

Medidata Solutions

Clincial Force CTMS 2011

Oracle PhaseForward EDC/CTMS 2010

Source: CenterWatch analysis of company reports and websites

peutic area requirements. For example, how you design electronic collection for a disease such as Lupus can be very different than how you design an obesity study for outcomes/events capture.”

A new direction

The shift away from internally devel-oped EDC systems has forced major CROs to rethink their business strategies and evaluate how technologies can best be used to improve clinical trial processes going forward.

“We needed new thinking to take that extra step into the 2020 world, which is where we are heading pretty quickly, and define a future roadmap,” said Quintiles’ Postings, an IT and business strategy ex-pert who joined Quintiles last year. “How do you have wider connections to multiple data sources? How do you offer insight as a service? How do we use our data scientists to really look at biomarkers and amazing amounts of detail?”

Quintiles has a suite of integrated data systems and services under the Infosario brand, which includes CTMS, clinical trial design, safety, an investigative site por-tal, analytics and regulatory information management technologies. As it moves forward, an important component of the IT strategy involves forming partnerships with technology companies—both large and small—to develop products and ser-vices that can address critical issues such as integrating systems across companies and trials, improving analytics and report-ing, connecting information through data hubs or aggregating data from wearable sensors.

“It’s a mixture of the software, which is IT-focused, blended with our knowledge,” said Postings. “We are not developing soft-ware to sell software. But it’s a core compo-

nent of everything we do and it’s going to become more and more important.”

One of the future challenges for CROs is keeping ahead of new technology devel-opments in the marketplace. Not only is there a profusion of new systems flooding the market, such as CTMS, electronic trial master files (eTMF) and regulatory infor-mation management (RIM), new clinical trial platforms increasingly require a mo-bile service component and mobile inter-face. The market also is moving toward technologies developed by more niche ex-pert providers in smaller areas.

Postings said Quintiles is focusing its integration efforts across four domains: business process management and work-flow; event management; API gateway; and systems/applications integration.

“There is a convergence of systems and technologies taking place and a greater de-mand for a more seamless and integrated solutions with single sign-on capabilities,” said O’Leary. “CROs who have learned to collaborate and integrate their capabilities and processes with third-party providers are the CROs who will continue to succeed in the future.”

Looking ahead

Third-party vendors are expected to in-crease their market share in the clinical tri-

al technology sector going forward; com-panies are continuing to make acquisitions that expand their technology offerings and can be integrated into existing platforms or business segments. Bioclinica’s recent acquisition of Clinverse, for example, adds clinical trial payment services to its offer-ings, while Medidata recently boosted its risk-based monitoring software through the acquisition of Patient Profiles.

CROs, however, can continue to operate successfully in this space if they can adapt their technology businesses, diversify their offerings and differentiate themselves in the marketplace.

“Technology now is creating new ways of performing monitoring, new ways of looking at decision-making through ther-apeutic experts and new business-process tools. The world is changing and it’s chang-ing for the better. But you have to get on the train and ride with it. You can’t really afford to be left behind,” said Quintiles’ Postings.

Karyn Korieth has been covering the clinical trials industry for CenterWatch since 2003. Her 30-year journalism career includes work in local news, the healthcare indus-try and national magazines. Karyn holds a Master of Science degree from the Columbia University Graduate School of Journalism. Email [email protected].

IndustryNews

4 The CenterWatch Monthly | March 2016 centerwatch.com

Primary EDC platforms used by select CROs

Leading CRO (in alphabetical order)

Icon Medidata Solutions, Oracle, sponsor systems, Datatrak for phase IV studies

Parexel Parexel Informatics DataLabs EDC

PPD Medidata Solutions, Oracle, OmniComm Systems

Quintiles Oracle, Medidata Solutions

Source: CenterWatch analysis of company reports and websites