Embed Size (px)

Citation preview

Maritime Transportation and Inland Freight Distribution: The Challenge of the Coast

Dr. Jean-Paul RodrigueDept. of Economics & GeographyHofstra UniversityHempstead, NY

http://people.hofstra.edu/faculty/jean-paul_rodrigue/

Outline

■ 1. Dislocation of Commercial Flows■ 2. Coping with Economies of Scale■ 3. Transforming Hinterlands■ 4. Conclusion: The Challenge of the Coast

1. Dislocation of Trade Flows

■ Differential growth• New origins and different growth rates for freight.

■ The kindness of strangers• Imbalanced trade and balance of payments.

■ What comes in does not come out• Imbalanced freight flows.

■ Going with the flow• A new reality for ports.

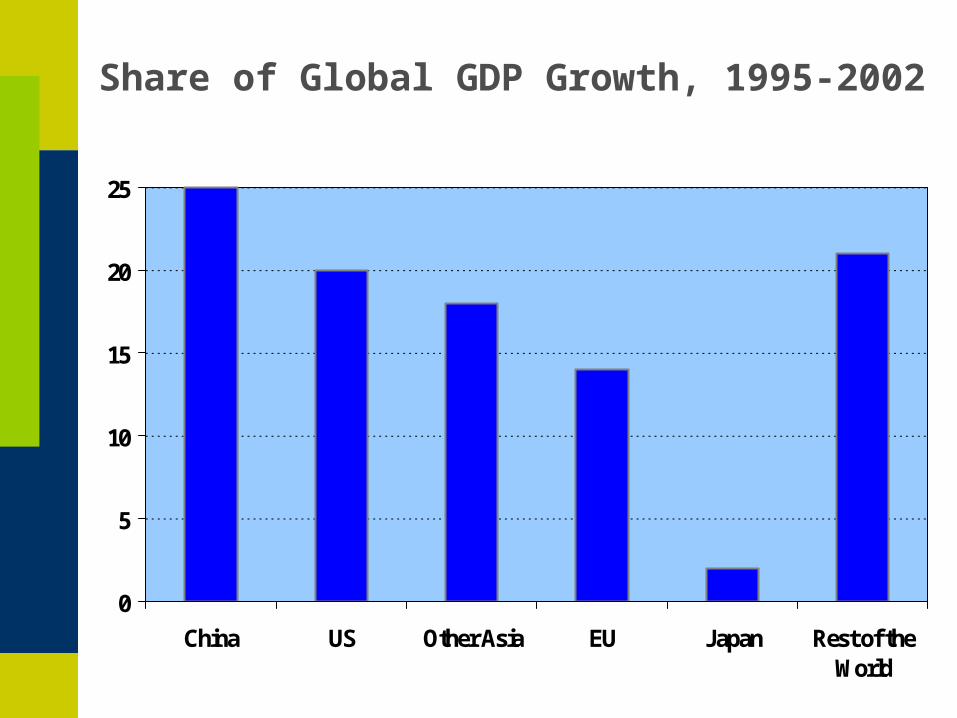

Share of Global GDP Growth, 1995-2002

0

5

10

15

20

25

China US Other Asia EU Japan Rest of theWorld

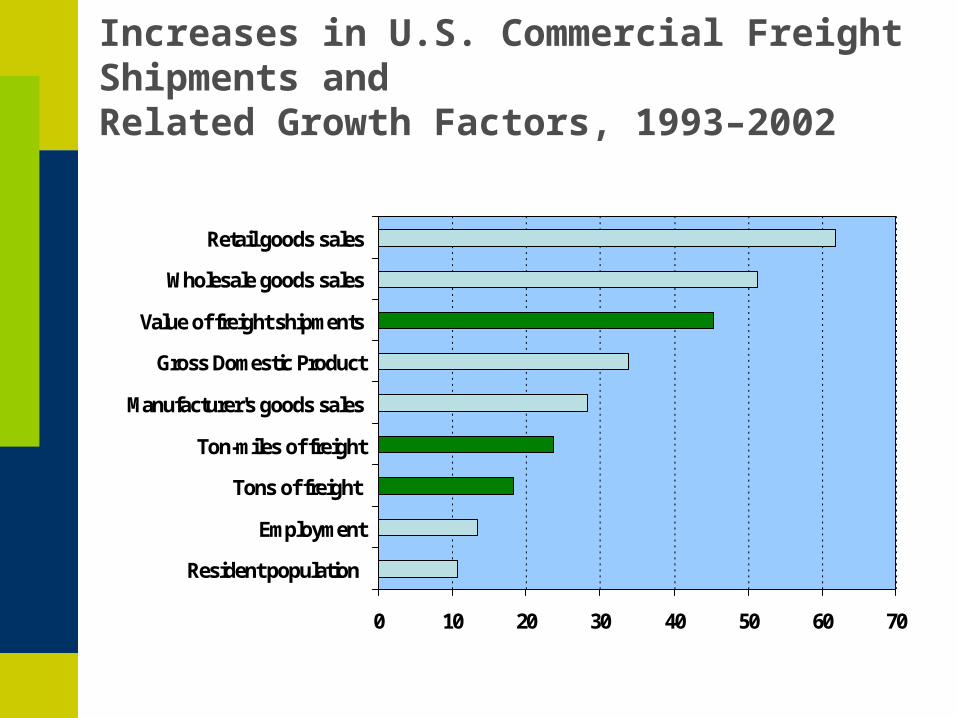

Increases in U.S. Commercial Freight Shipments andRelated Growth Factors, 1993–2002

0 10 20 30 40 50 60 70

Resident population

Employment

Tons of freight

Ton-miles of freight

Manufacturer's goods sales

Gross Domestic Product

Value of freight shipments

Wholesale goods sales

Retail goods sales

U.S. Trade in Goods and Services - Balance of Payments, 1970-2003 (billions of $US)

-600

-500

-400

-300

-200

-100

0

100

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Total

Goods

Services

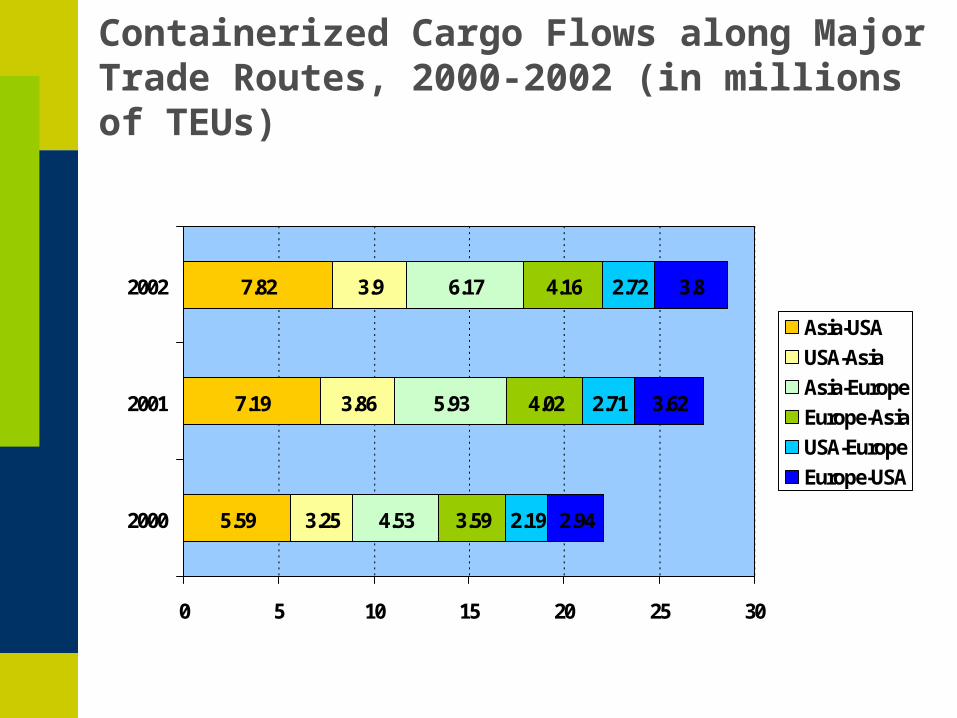

Containerized Cargo Flows along Major Trade Routes, 2000-2002 (in millions of TEUs)

5.59

7.19

7.82

3.25

3.86

3.9

4.53

5.93

6.17

3.59

4.02

4.16

2.19

2.71

2.72

2.94

3.62

3.8

0 5 10 15 20 25 30

2000

2001

2002

Asia-USA

USA-Asia

Asia-Europe

Europe-Asia

USA-Europe

Europe-USA

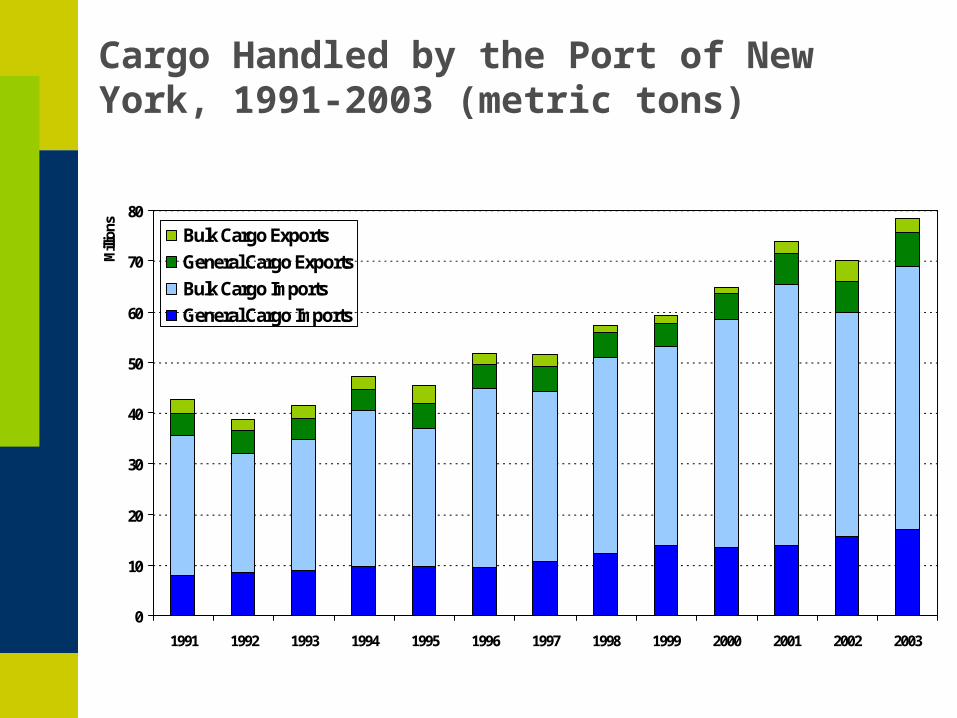

Cargo Handled by the Port of New York, 1991-2003 (metric tons)

0

10

20

30

40

50

60

70

80

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Mill

ions Bulk Cargo Exports

General Cargo Exports

Bulk Cargo Imports

General Cargo Imports

!(!(

!(

!(

!(

!(

!(

!(

!(

!(

Container Traffic at Major East Coast Ports, 1990-2003 (TEU)

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5

1) New York/New Jersey

2) Charleston

3) Hampton Roads

4) Savannah

5) Miami

6) Jacksonville

7) Port Everglades

8) Baltimore

9) Wilmington

10) Palm Beach

11) Boston

12) Philadelphia

Millions

1990

1995

2000

20031

2

3

4

5

6

7

89

10

11

12

2. Coping with Economies of Scale

■ A heavyweight tendency• Larger containerships.

■ Costs being externalized• Pressures on transshipment and inland distribution.

■ Dredge it and they will come?• The “race to the bottom”.

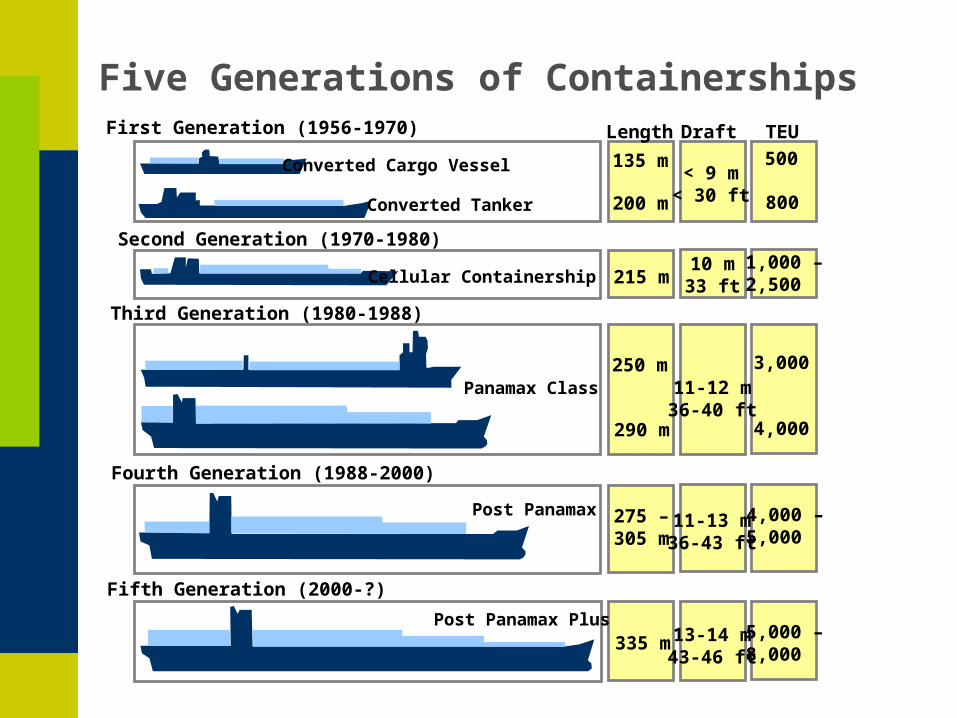

First Generation (1956-1970)

Converted Tanker

Second Generation (1970-1980)

Cellular Containership

Third Generation (1980-1988)

Panamax Class

Fourth Generation (1988-2000)

Post Panamax Plus

Fifth Generation (2000-?)

Post Panamax

Converted Cargo Vessel

Five Generations of Containerships TEULength

135 m

200 m

500

800

215 m1,000 –2,500

250 m 3,000

290 m 4,000

275 –305 m

4,000 –5,000

335 m5,000 –8,000

Draft

< 9 m< 30 ft

10 m33 ft

11-12 m36-40 ft

11-13 m36-43 ft

13-14 m43-46 ft

The Largest Available Containership, 1980-2000 (in TEUs)

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1980 1985 1990 1995 2000

Fourth Generation Containership (4,000 TEU), Le Havre

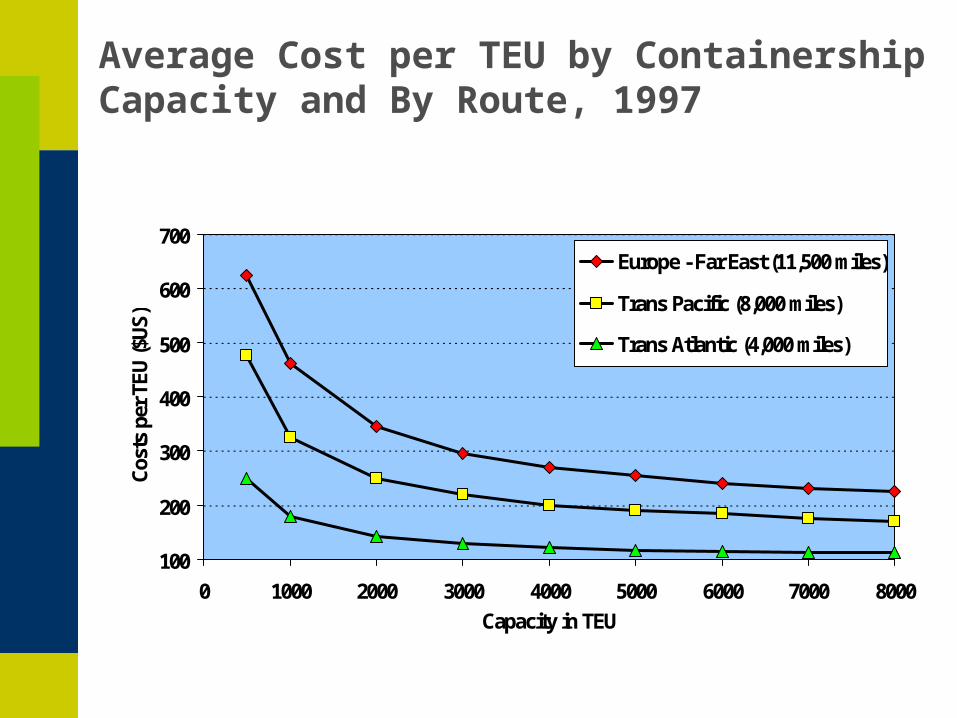

Average Cost per TEU by Containership Capacity and By Route, 1997

100

200

300

400

500

600

700

0 1000 2000 3000 4000 5000 6000 7000 8000

Capacity in TEU

Cos

ts p

er T

EU

($U

S)

Europe - Far East (11,500 miles)

Trans Pacific (8,000 miles)

Trans Atlantic (4,000 miles)

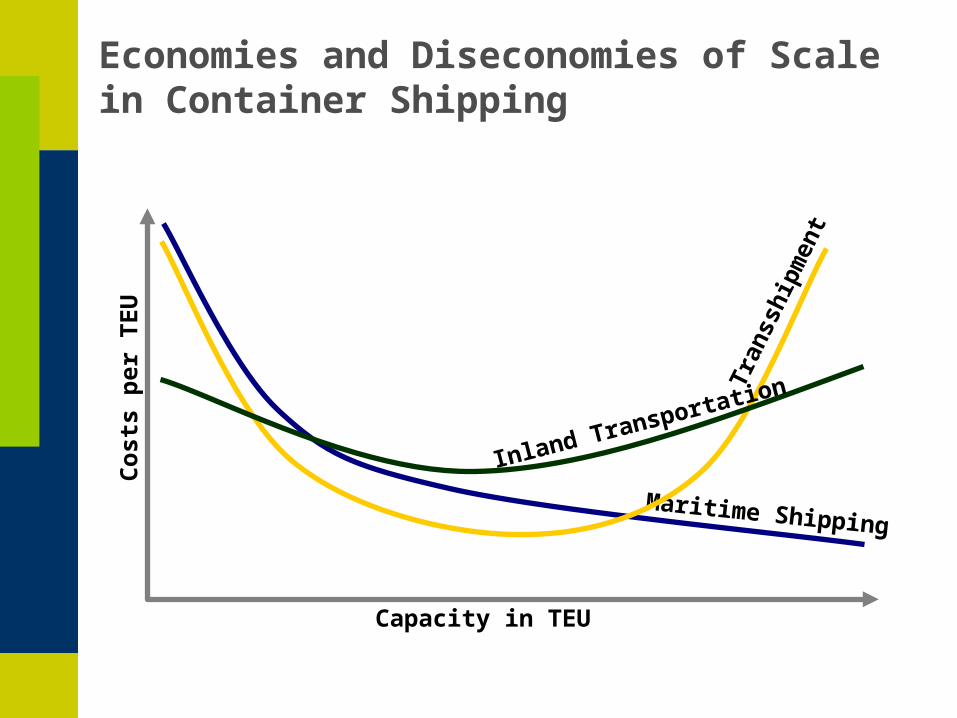

Economies and Diseconomies of Scale in Container Shipping

Cos

ts p

er T

EU

Capacity in TEU

Maritime Shipping

Tran

sshi

pmen

t

Inland Transportation

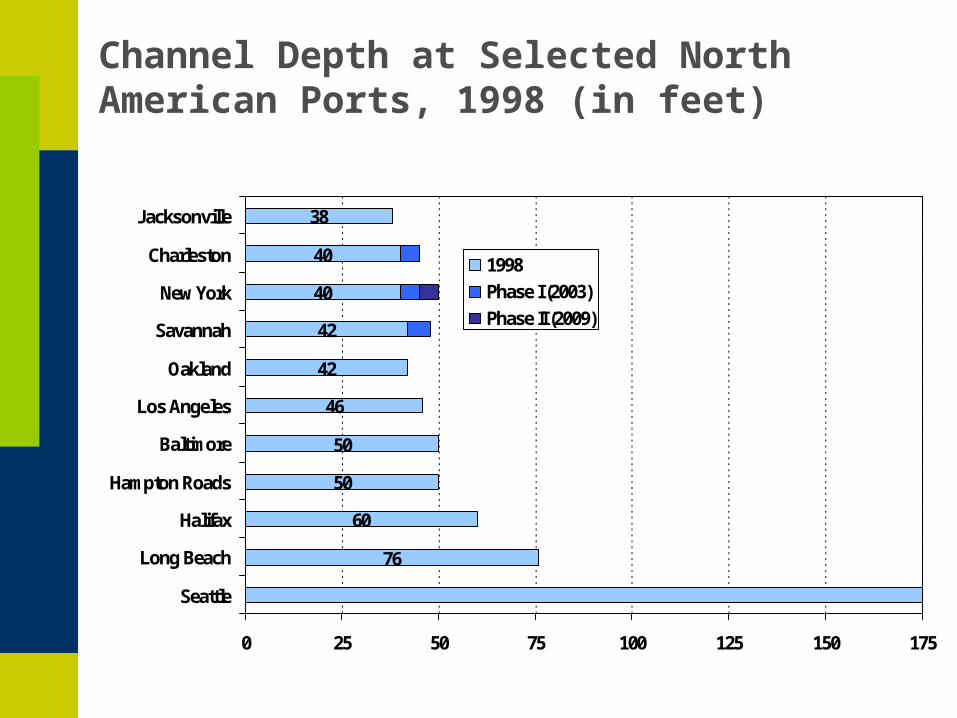

Channel Depth at Selected North American Ports, 1998 (in feet)

76

60

50

50

46

42

42

40

40

38

0 25 50 75 100 125 150 175

Seattle

Long Beach

Halifax

Hampton Roads

Baltimore

Los Angeles

Oakland

Savannah

New York

Charleston

Jacksonville

1998

Phase I (2003)

Phase II (2009)

!(

!(!(

!(

!(

!(

!(

!(!(!(

!(

!(

!(!(

!(!(!(

!(!(

!(

!(!(

!(

!(

!(

!(!(!(

!(!( !(

!(

!(

!(

!(

!(!(

!(

!(

!(

!(

!(

!(

!(

!(

!(

!(

!(

!(

!(

!(

!(

!(

!(!(!(

!(

!(

!(

!(

!(

!(!(

!(!(

!(!(

!(!(

!(

!(

!(

!(!(

!(

!(

!(

!(!(

!(!(!(

!(

!(

!(!(

!(

!(

!(

!(

!(

!(

!(

!(

!(!(

!(

!(

!(!(

!(!(

!(

!(

!(

!(

!(

!(!(

4 0 42 Miles

45

Navigation Channel

Control Depth (feet)

Intermodal Terminal

Container Port (proposed)

Major Highway

Proposed rail tunnel

4530

3737

37

45

45

40

43

40

45

40

37

Ambrose Channel

Main Ship Channel

Raritan Bay Channel

Arthur Kill Channel

Arthur Kill Channel

Kill Van KullChannel

Newark BayChannel

Upper Bay Channel

Hudson River

East River

45

The Narrows

Bro

okly

n

Stat

en Is

land

New

Jer

sey

N

2

1

Howland Hook

Red Hook

South Brooklyn

3

1- Port Newark2- Port Elizabeth3- Global Marine

Albers Equal-Area Conic Projection

Intermodal Facilities and Navigation Channels of the Port of New York, 2003

Port Elizabeth

Howland Hook

Port Newark

Global Marine

Red Hook

0 2000 4000 6000 8000 10000

Daily Truck Movements (one way), 2001

3. Transforming Hinterlands

■ The flexibility and adaptability of supply chains• Growing functional integration.

■ Between a port and a hard place• New hinterland structures.

■ The intermodal coast• Regionalization and modal shift.

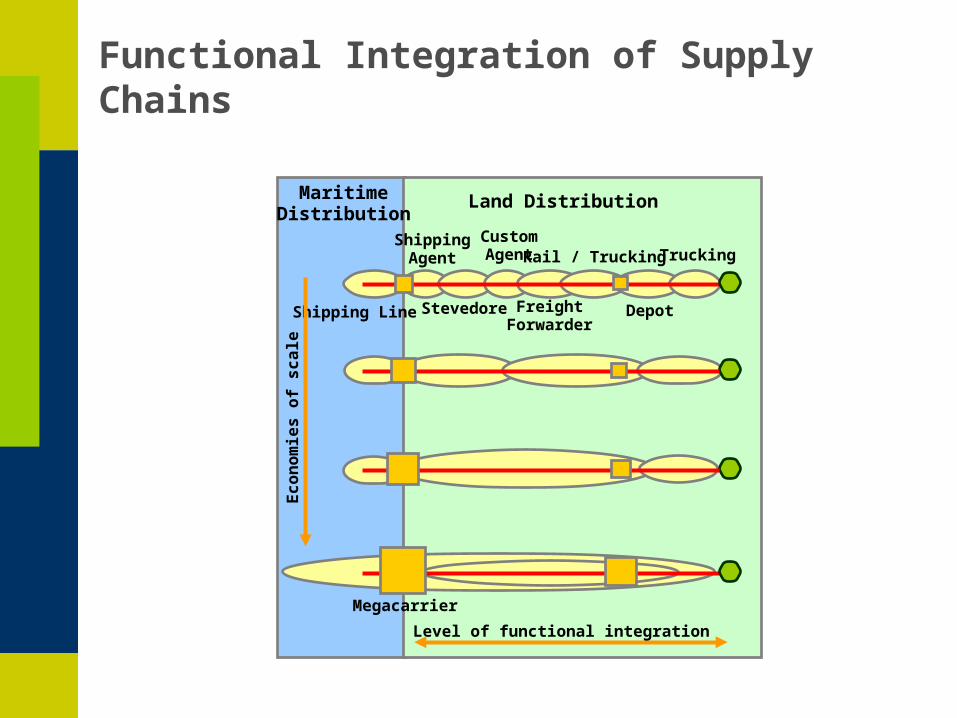

Functional Integration of Supply Chains

Shipping Line

ShippingAgent

Stevedore

CustomAgent

FreightForwarder

Rail / Trucking

Depot

Trucking

Megacarrier

Econ

omie

s of

sca

le

Land DistributionMaritimeDistribution

Level of functional integration

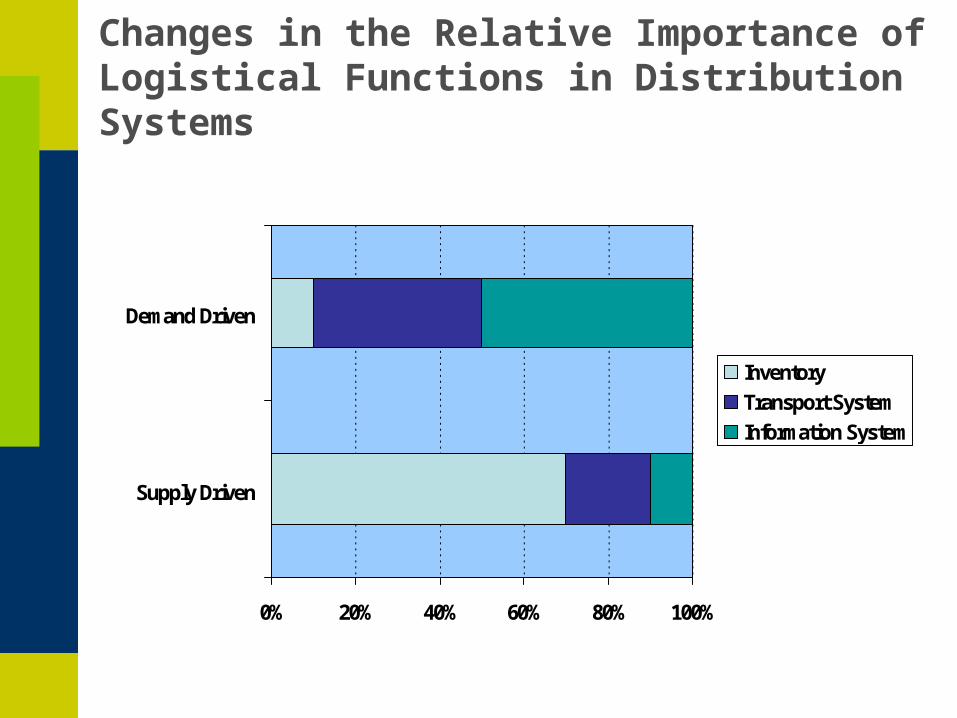

Changes in the Relative Importance of Logistical Functions in Distribution Systems

0% 20% 40% 60% 80% 100%

Supply Driven

Demand Driven

Inventory

Transport System

Information System

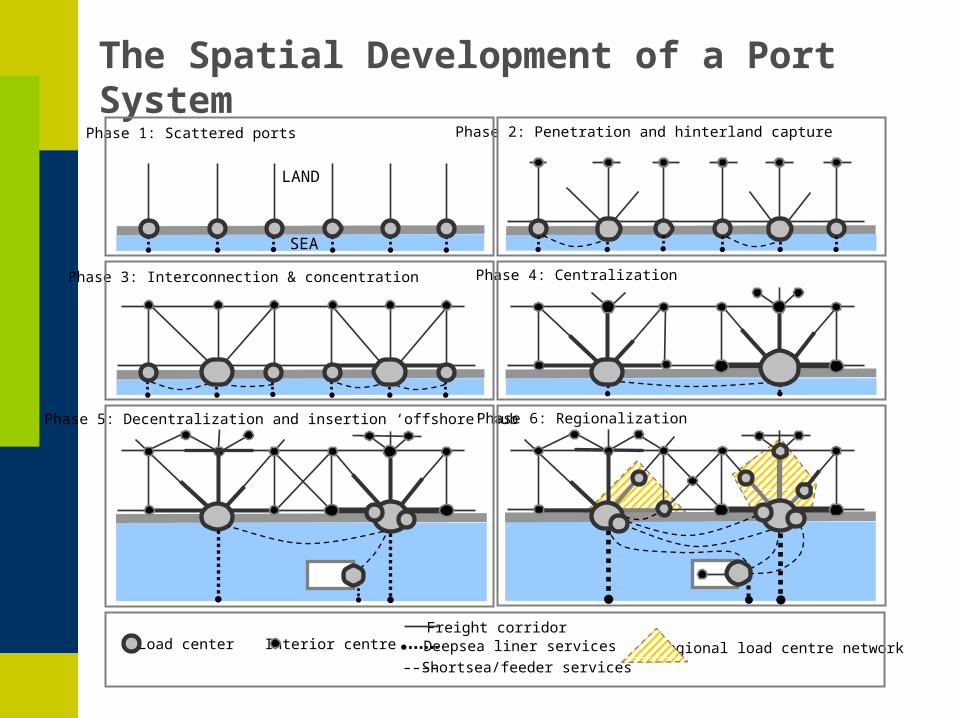

The Spatial Development of a Port SystemPhase 1: Scattered ports Phase 2: Penetration and hinterland capture

Phase 3: Interconnection & concentration Phase 4: Centralization

Phase 5: Decentralization and insertion ‘offshore’ hub Phase 6: Regionalization

Load center Interior centre Regional load centre network

Freight corridor

LAND

SEA

Deepsea liner services

Shortsea/feeder services

Pendulum Route: OOCL Container Services on the North Atlantic, 1997

BostonNew YorkNorfolk

SavannahJacksonville

MiamiHouston

BremenhavenFelixstowe

Rotterdam

Le Havre

NAX-1NAX-2

Atlantic Ocean

National Trade Areas, Articulation Points and Major Land Freight Gateways of the United States

Articulation Point

Land FreightGateway

Trade Area

Corridor

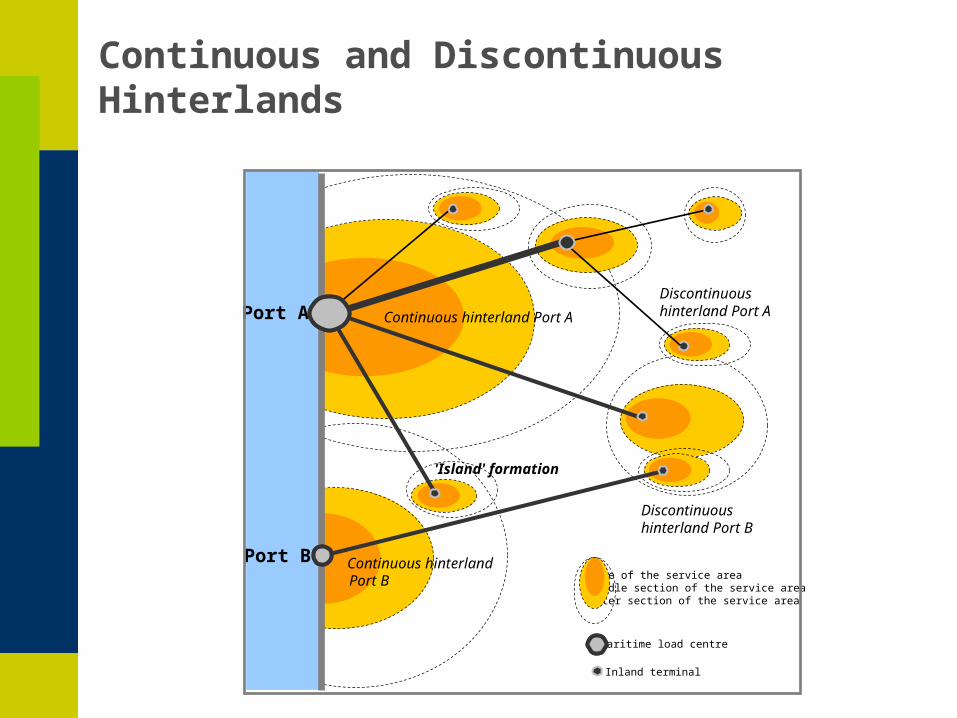

Continuous and Discontinuous Hinterlands

Core of the service areaMiddle section of the service areaOuter section of the service area

Maritime load centre

Inland terminal

Continuous hinterland Port A

Continuous hinterland Port B

Discontinuous hinterland Port A

Discontinuous hinterland Port B

'Island' formation

Port A

Port B

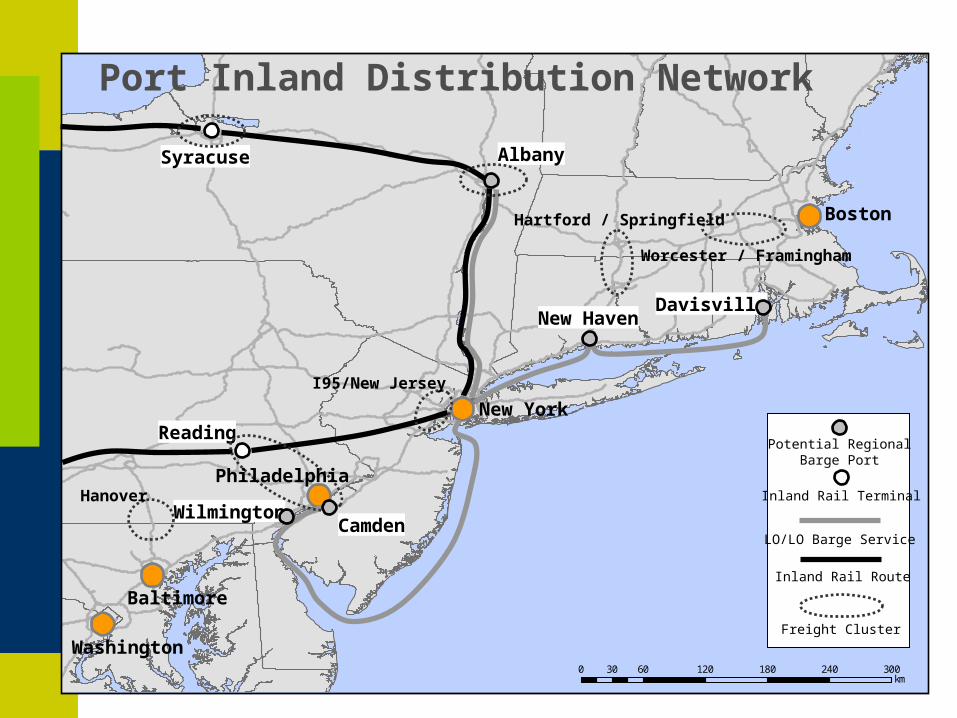

0 60 120 180 240 30030km

Albany

CamdenWilmington

New HavenDavisville

New York

Boston

Baltimore

Washington

Potential RegionalBarge Port

LO/LO Barge Service

Reading

Syracuse

Inland Rail Terminal

Inland Rail Route

Worcester / Framingham

Hanover

Hartford / Springfield

Freight Cluster

Philadelphia

I95/New Jersey

Port Inland Distribution Network

Potential Modal Split Changes Due to the PIDN

0% 20% 40% 60% 80% 100%

2001

2020

Truck

Rail

Barge

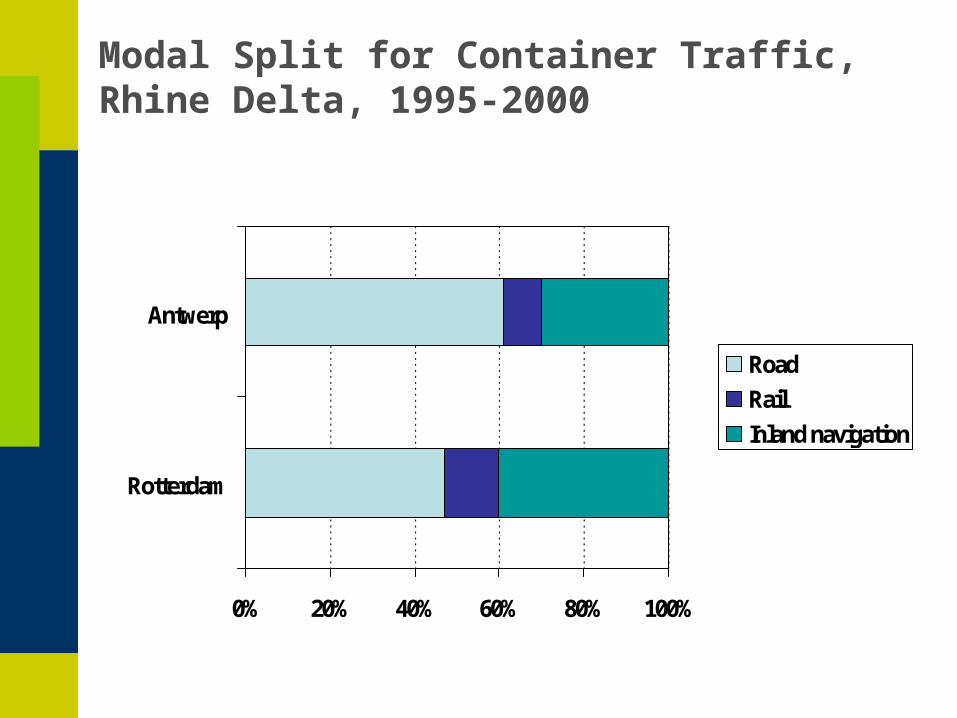

Modal Split for Container Traffic, Rhine Delta, 1995-2000

0% 20% 40% 60% 80% 100%

Rotterdam

Antwerp

Road

Rail

Inland navigation

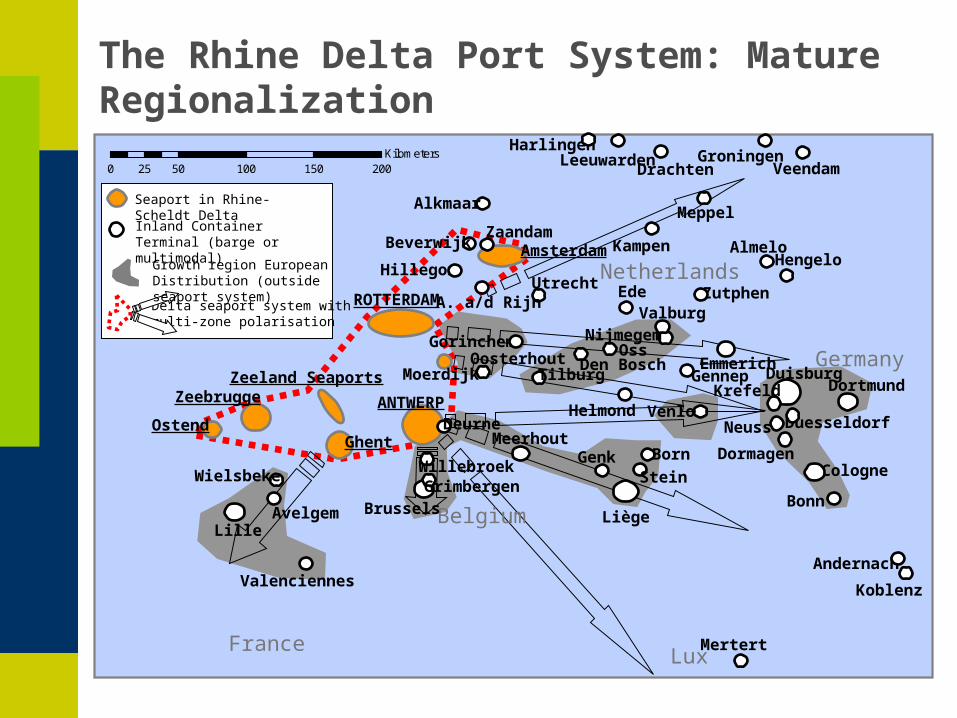

0 50 100 150 20025Kilometers

France

Belgium

Lux

Germany

NetherlandsROTTERDAM

Zeeland Seaports

ANTWERPZeebrugge

GhentOstend

BrusselsLille

Liège

WielsbekeGenk

DuisburgEmmerich

Nijmegem

Avelgem

Born

Venlo

Valenciennes

GrimbergenWillebroek

DeurneMeerhout

Duesseldorf

Cologne

Krefeld

Neuss

Bonn

Andernach

Dortmund

Amsterdam

Alkmaar

BeverwijkZaandam

HarlingenLeeuwarden Veendam

Meppel

GroningenDrachten

Kampen AlmeloHengelo

ZutphenEdeHillegom

UtrechtA. a/d Rijn

TilburgOosterhout

Helmond

Gorinchem

MoerdijkDen Bosch

Oss

Valburg

Stein

Gennep

Mertert

Koblenz

Dormagen

Seaport in Rhine-Scheldt Delta

Delta seaport system with multi-zone polarisation

Inland Container Terminal (barge or multimodal)

Growth region EuropeanDistribution (outside seaport system)

The Rhine Delta Port System: Mature Regionalization

Conclusion: The Challenge of the Coast

■ A changing geography of maritime and inland distribution• Global changes:

• New geography of production.• Imbalanced trade flows.

• Regional gains:• Consumption and distribution.

• Local pains:• Congestion.• Stressed capacities.

■ The challenge of the coast• Port regionalization.• Modal shift: readjustment of freight flows.• Efficiency in distribution derived from the hinterland.