Embed Size (px)

Citation preview

Market Access Climate Change: the Evolving Impact of Product Listing Agreements

October 30, 2015 Arvind Mani, Director of Market Access and Policy Research

PDCI Market Access: Background

Established in 1996, PDCI is Canada's leading pharmaceutical pricing and reimbursement consultancy

Based in Ottawa and Toronto, with a staff of 19 featuring senior, experienced consultants

2

O tta w a

To r o nto

About PDCI

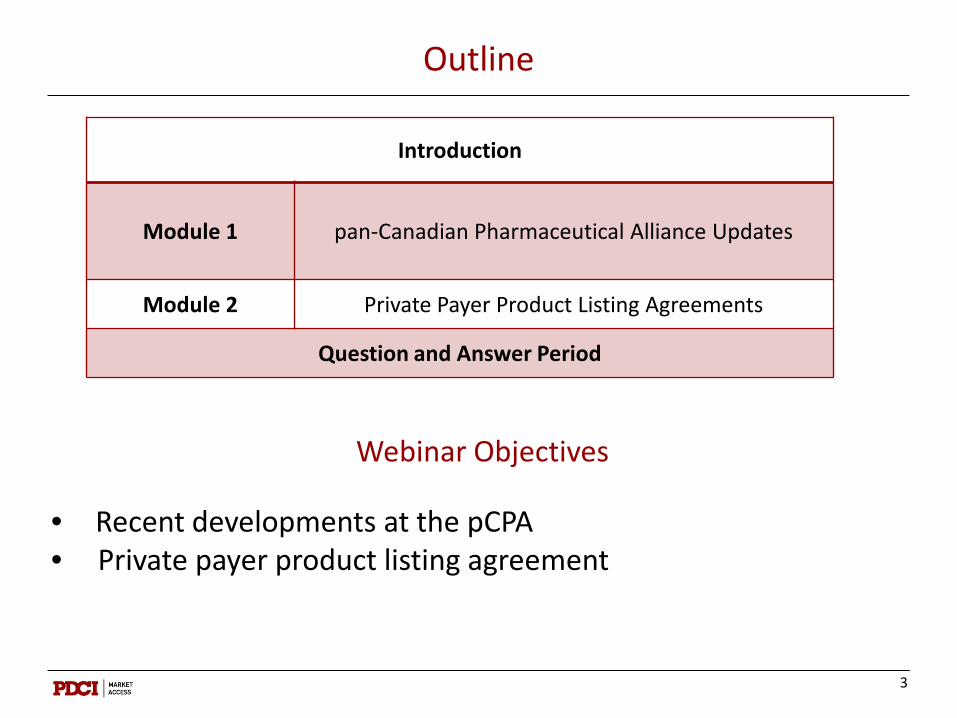

Outline

Introduction

Module 1 pan-Canadian Pharmaceutical Alliance Updates

Module 2 Private Payer Product Listing Agreements

Question and Answer Period

3

Webinar Objectives

• Recent developments at the pCPA • Private payer product listing agreement

Introduction

4

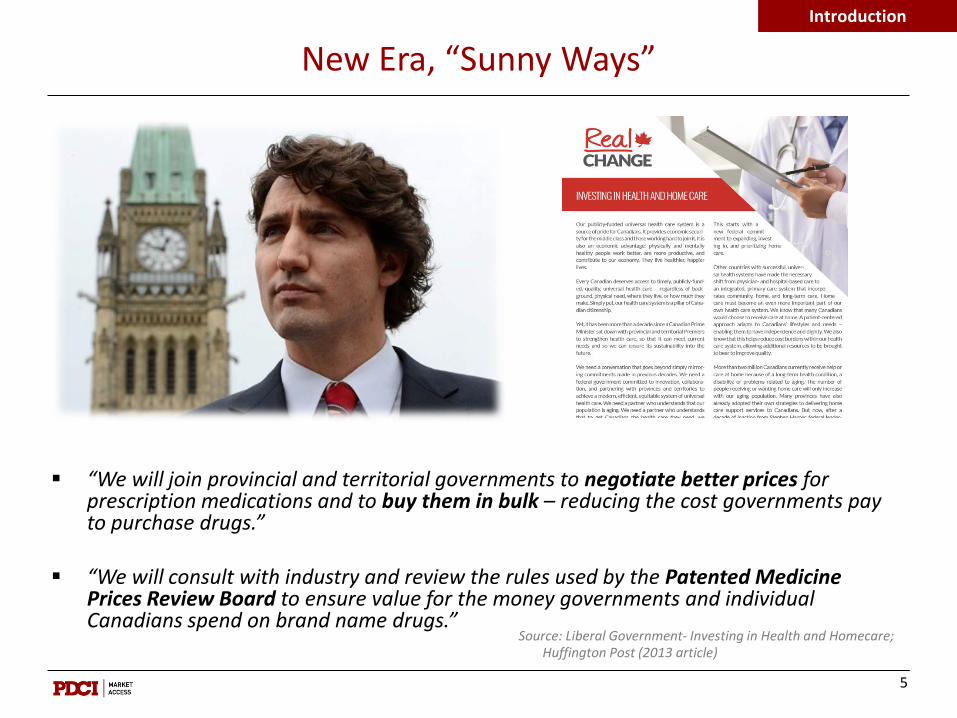

New Era, “Sunny Ways”

“We will join provincial and territorial governments to negotiate better prices for

prescription medications and to buy them in bulk – reducing the cost governments pay to purchase drugs.”

“We will consult with industry and review the rules used by the Patented Medicine

Prices Review Board to ensure value for the money governments and individual Canadians spend on brand name drugs.”

5

Introduction

Source: Liberal Government- Investing in Health and Homecare; Huffington Post (2013 article)

Question 1

Given the Liberal government’s interest in bulk purchasing to reduce costs, how likely do you think it is that the pan-Canadian Pharmaceutical Alliance

(pCPA) will be the starting point for some form of national Pharmacare program?

a) Highly Likely b) Likely c) Neutral d) Unlikely e) Highly Unlikely

6

Introduction

Question 2

Given the Liberal government’s interest in reviewing the rules of the PMPRB, do you believe the federal government will aim to make this regulatory body

more “relevant”?

a) Yes b) No

7

Introduction

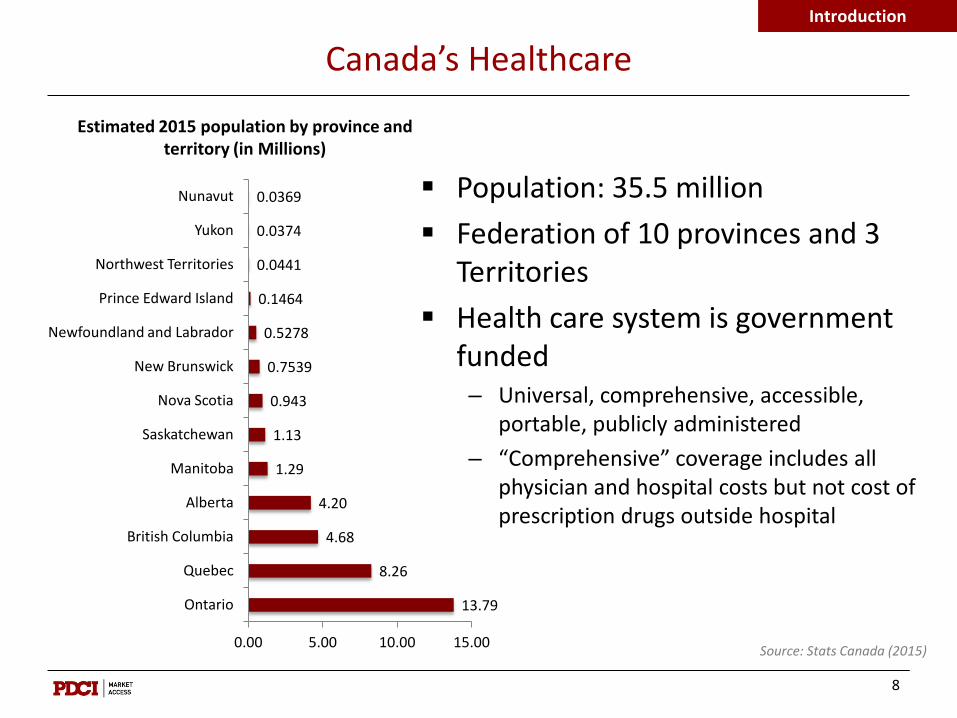

Canada’s Healthcare

Population: 35.5 million Federation of 10 provinces and 3

Territories Health care system is government

funded – Universal, comprehensive, accessible,

portable, publicly administered – “Comprehensive” coverage includes all

physician and hospital costs but not cost of prescription drugs outside hospital

8

Introduction

13.79

8.26

4.68

4.20

1.29

1.13

0.943

0.7539

0.5278

0.1464

0.0441

0.0374

0.0369

0.00 5.00 10.00 15.00

Ontario

Quebec

British Columbia

Alberta

Manitoba

Saskatchewan

Nova Scotia

New Brunswick

Newfoundland and Labrador

Prince Edward Island

Northwest Territories

Yukon

Nunavut

Estimated 2015 population by province and territory (in Millions)

Source: Stats Canada (2015)

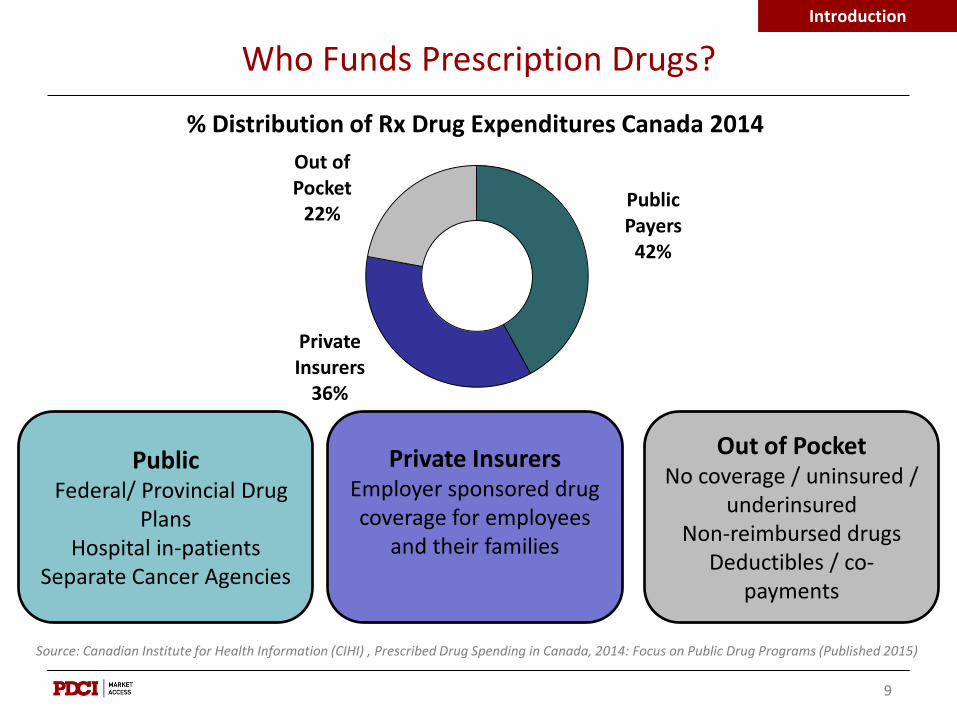

Who Funds Prescription Drugs?

Source: Canadian Institute for Health Information (CIHI) , Prescribed Drug Spending in Canada, 2014: Focus on Public Drug Programs (Published 2015)

Public Federal/ Provincial Drug

Plans Hospital in-patients

Separate Cancer Agencies

Private Insurers Employer sponsored drug coverage for employees

and their families

Out of Pocket No coverage / uninsured /

underinsured Non-reimbursed drugs

Deductibles / co-payments

% Distribution of Rx Drug Expenditures Canada 2014

9

Introduction

Public Payers

42%

Private Insurers

36%

Out of Pocket

22%

Prescription Drug Landscape: The Market

10

Introduction

Consistent health care access among Canadians, including prescription drugs, regardless of residence

Timely access to innovative therapies as they are “rolled out”, no matter the price tag

"It was a shock to me that I had to pay for cancer treatment. That's not how it's supposed to be in Canada."’— Julie Easley, Cancer Patient

'We cannot put a price tag on the health and well-being of any Canadian’— Ken Chan, VP at Cystic Fibrosis Canada

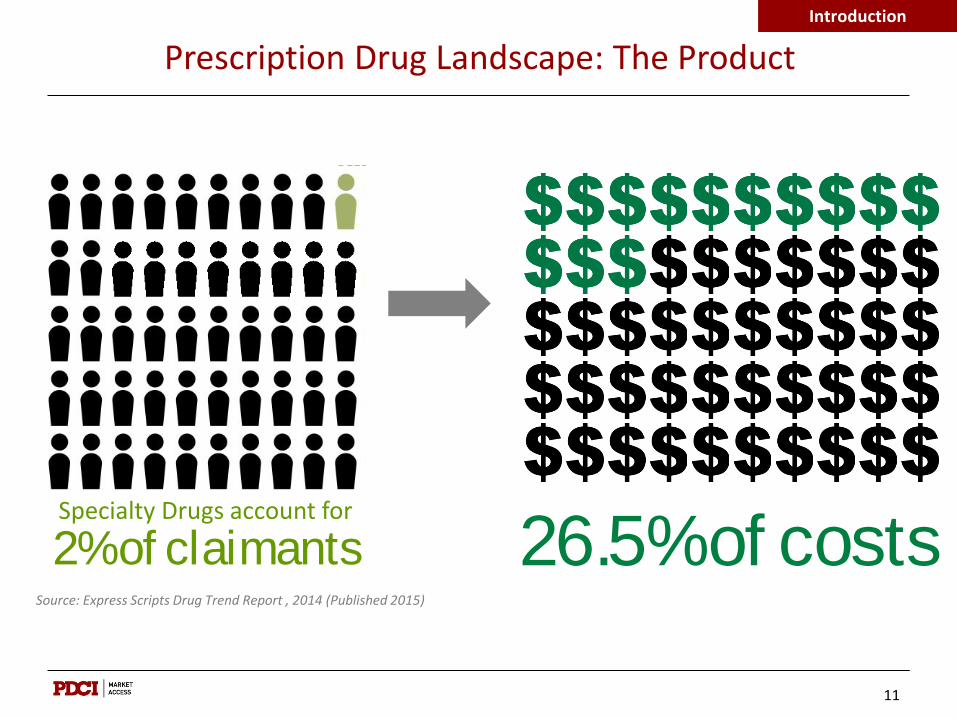

Prescription Drug Landscape: The Product

11

Introduction

2% of claimants Specialty Drugs account for 26.5% of costs

Source: Express Scripts Drug Trend Report , 2014 (Published 2015)

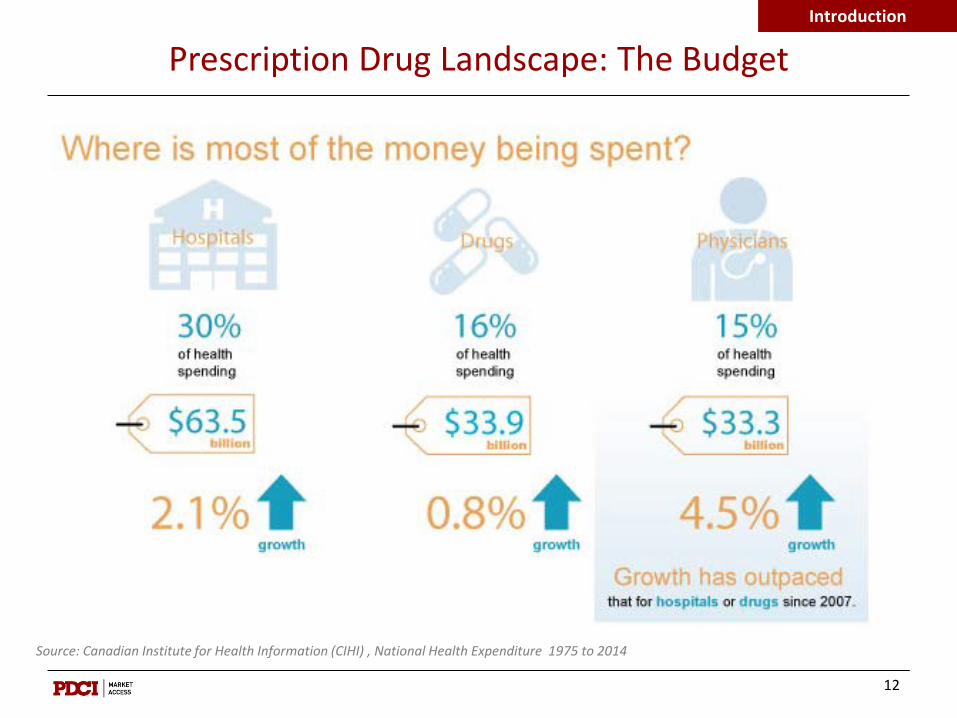

Prescription Drug Landscape: The Budget

12

Introduction

Source: Canadian Institute for Health Information (CIHI) , National Health Expenditure 1975 to 2014

Product Listing Agreements

13

Introduction

Uncertainty exists surrounding the product’s: – New therapies for unmet needs; – Efficacy (heterogeneity); – Real world effectiveness; – Safety risks; – Cost-effectiveness; and – Budget impact.

A product listing agreement (PLA) is a contract negotiated between a pharmaceutical manufacturer and a drug benefit plan outlining specific conditions related to the drug plan’s reimbursement of a drug product.

Question 3

Has your company negotiated a product listing agreement with the pCPA?

a) Yes b) No

14

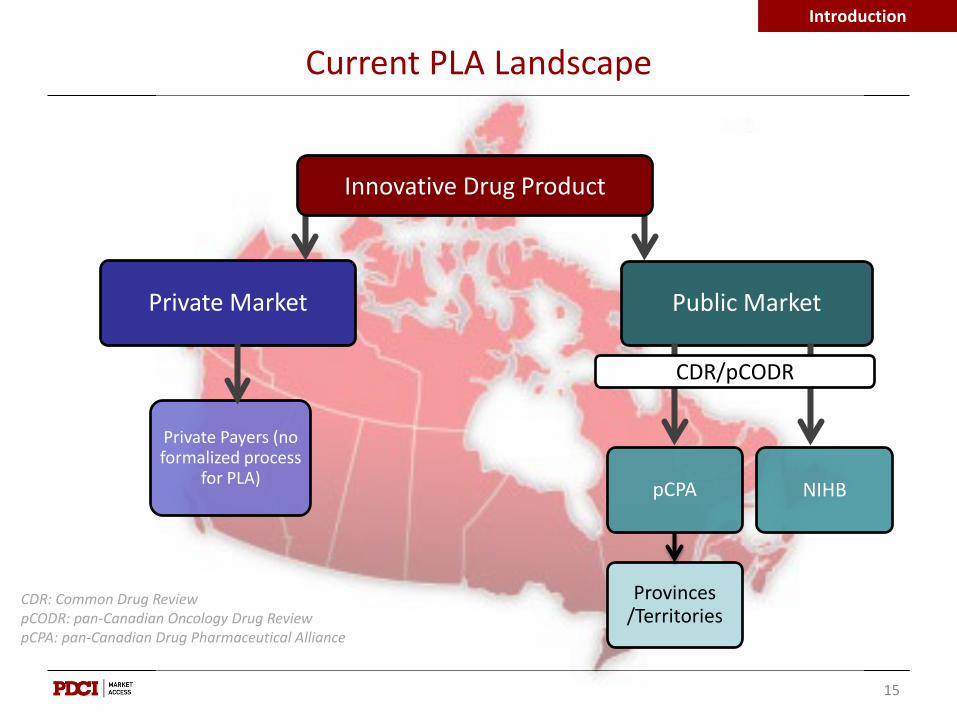

Introduction

Public Market

NIHB

Provinces /Territories

pCPA

Private Market

Private Payers (no formalized process

for PLA)

15

Current PLA Landscape Introduction

Innovative Drug Product

CDR: Common Drug Review pCODR: pan-Canadian Oncology Drug Review pCPA: pan-Canadian Drug Pharmaceutical Alliance

CDR/pCODR

Key Takeaways

Political change and uncertainty

Growing importance of specialty treatments

Political pressure to cover new treatments

Drug expenditures controlled temporarily

PLAs are here to stay

16

Module 1: pCPA Updates

17

pan-Canadian Initiative

18

pCPA Updates

The pan-Canadian Pharmaceutical Alliance (pCPA) is pan Canadian initiative made up of most provincial/territorial (P/T) jurisdictions whom conduct joint negotiations for

brand name and generic drug products being considered for reimbursement in Canada through their respective public drug plans.

The pillar of the public PLA environment in Canada is the pCPA Created in 2010 Objectives for Brand Name Pharmaceuticals:

– Access – Consistency – Lower drug costs – Efficiency – Bargaining power

Objectives for Generic Pharmaceuticals: – Consistency – Lower drug costs

Question 4

Which of the following developments at the pCPA do you find to be most positive over the past few years?

a) Improved communication between pCPA and manufacturers b) A better understanding of the pCPA process c) Agreement by all parties that HTA recommendation forms the content

basis of agreement d) None of the above

19

pCPA Updates

pCPA 5 year Status

20

pCPA Updates

Activity Report (as of August 2015) 146 drugs considered 79 complete 22 ongoing Price reductions for 14 generics 27% of the Canadian generic market is priced at 18% to brand Process becoming more efficient

Source: Pharmaceutical Trends- Pubic Payer Perspective (Presented at CAHR Western Day October 2015, Kevin Wilson)

Question 5

Which of the following elements of the negotiation are the most challenging?

a) Adjustment to the BIA during negotiations b) Significant variance in timeliness of listing and lead province's

capacity/capabilities c) Difficulty negotiating an outcome-based agreement d) None of the above

21

pCPA Updates

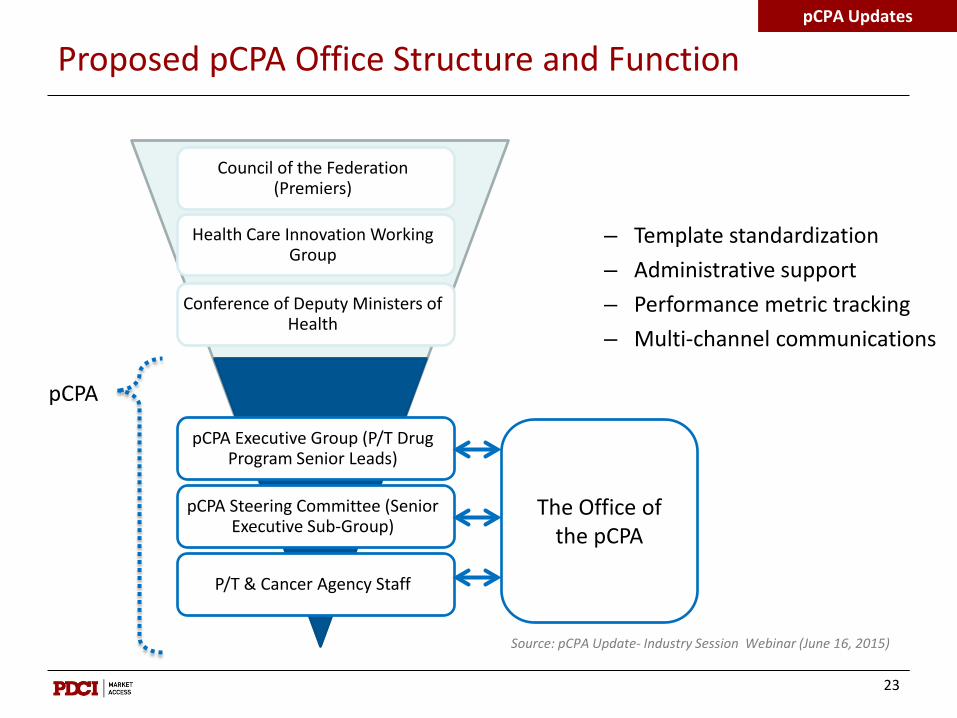

pCPA Office

22

pCPA Updates

Pan Canadian Drugs Negotiations Report recommended create of a Secretariat

The Office supports pCPA work and provide expertise to support negotiation and performance monitoring – Proposed Mission: Driving collective

pCPA success through achievement of value-driven, effectively communicated and evaluated outcomes.

– Proposed Mandate: Providing leadership and operational excellence to participating public drug plans to collectively achieve the objectives of the pan-Canadian Pharmaceutical Alliance

Source: pCPA Update- Industry Session Webinar (June 16, 2015)

Proposed pCPA Office Structure and Function

23

pCPA Updates

– Template standardization – Administrative support – Performance metric tracking – Multi-channel communications

Council of the Federation (Premiers)

Health Care Innovation Working Group

Conference of Deputy Ministers of Health

pCPA Executive Group (P/T Drug Program Senior Leads)

pCPA Steering Committee (Senior Executive Sub-Group)

P/T & Cancer Agency Staff

The Office of the pCPA

pCPA

Source: pCPA Update- Industry Session Webinar (June 16, 2015)

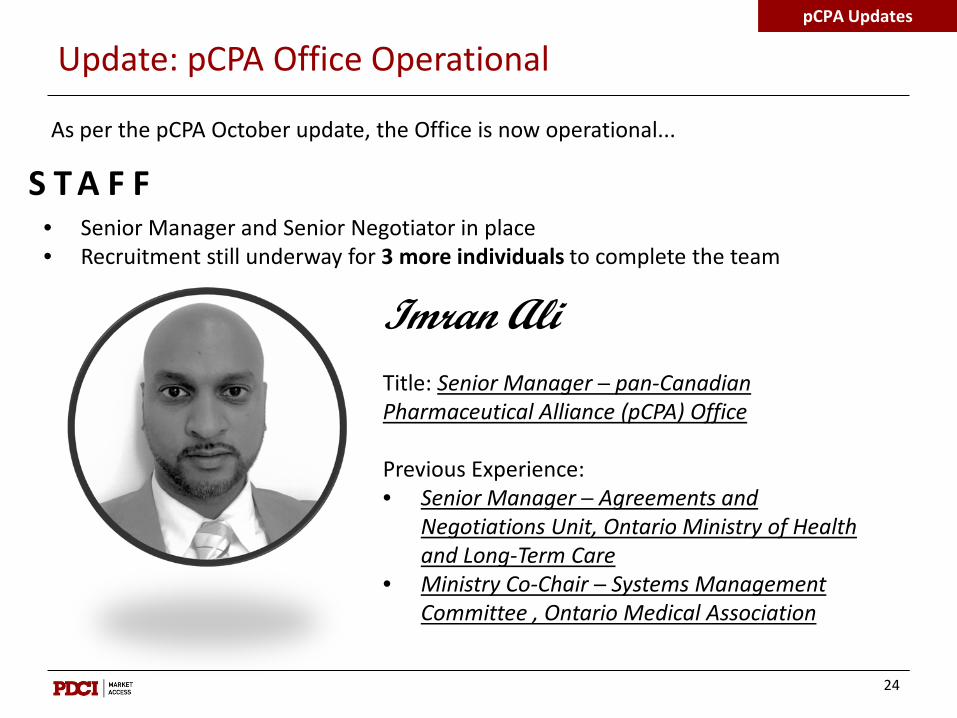

Update: pCPA Office Operational

24

pCPA Updates

S T A F F As per the pCPA October update, the Office is now operational...

• Senior Manager and Senior Negotiator in place • Recruitment still underway for 3 more individuals to complete the team

Imran Ali Title: Senior Manager ─ pan-Canadian Pharmaceutical Alliance (pCPA) Office Previous Experience: • Senior Manager ─ Agreements and

Negotiations Unit, Ontario Ministry of Health and Long-Term Care

• Ministry Co-Chair ─ Systems Management Committee , Ontario Medical Association

Update: pCPA Office Operational

25

pCPA Updates

S T A F F As per the pCPA October update, the Office is now operational...

• Senior Manager and Senior Negotiator in place • Recruitment still underway for 3 more individuals to complete the team

Anchalee Srisombun Title: Senior Negotiator ─ pan-Canadian Pharmaceutical Alliance (pCPA) Office Previous Experience: • Health Policy Advisor ─ Cystic Fibrosis Canada • Business Manager, Pricing and Supply ─ UK

Department of Health • Workforce Programme Officer, Allied Health

Professions ─UK Department of Health

Update: pCPA Office Operational

26

pCPA Updates

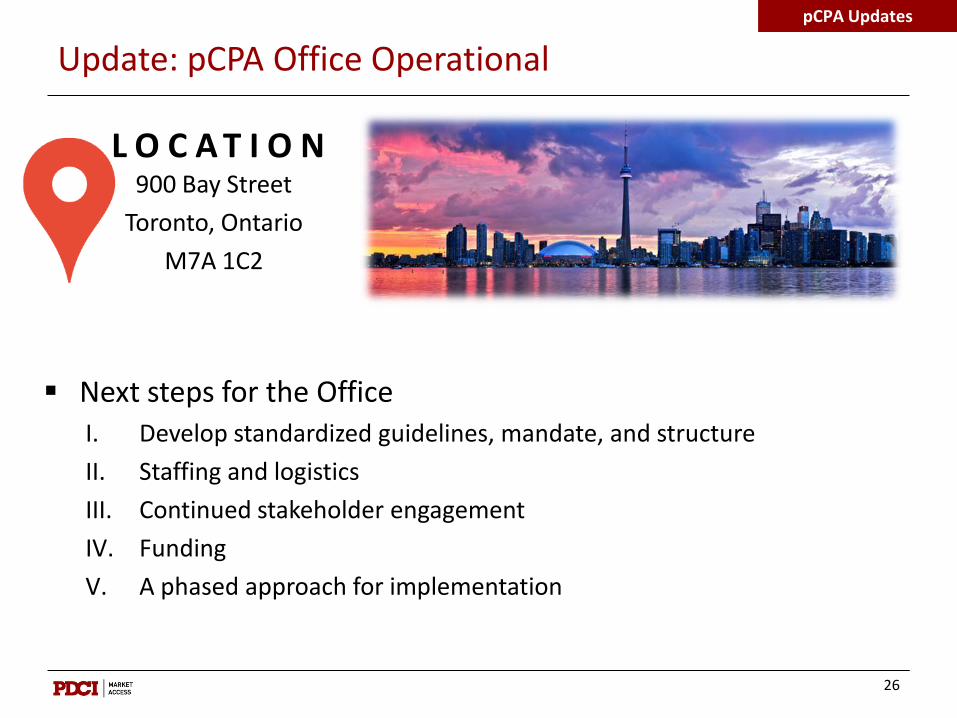

900 Bay Street Toronto, Ontario

M7A 1C2

L O C A T I O N

Next steps for the Office

I. Develop standardized guidelines, mandate, and structure II. Staffing and logistics III. Continued stakeholder engagement IV. Funding V. A phased approach for implementation

Impact: pCPA Office Operational

27

pCPA Updates

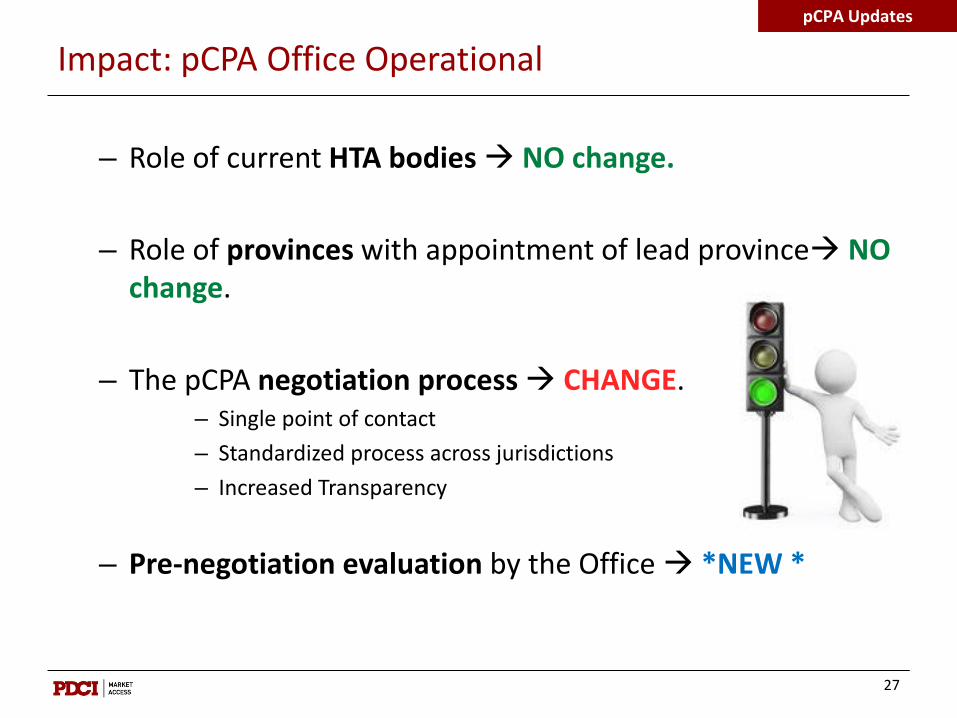

– Role of current HTA bodies NO change.

– Role of provinces with appointment of lead province NO change.

– The pCPA negotiation process CHANGE. – Single point of contact – Standardized process across jurisdictions – Increased Transparency

– Pre-negotiation evaluation by the Office *NEW *

Question 6

Please indicate the level of agreement with the following statement: “The creation of the new pCPA office will significantly improve the negotiation

process between the pCPA and manufacturers.”

a) Strongly agree b) Agree c) Neutral d) Disagree e) Strongly disagree

28

pCPA Updates

Québec versus Pan-Canadian

2nd largest market in Canada Largest net debt per capita ($23.2 thousand; 2014-2015) Lowest price provisions.

– Since the creation of the pCPA this has not been the case – QC is paying full list price for drugs – Significant foregone savings

29

Source: Canadian Institute for Health Information (CIHI) , National Health Expenditure Trends , 1975 to 2014 (Published 2014); RBC Canada, Canadian Federal and Provincial Fiscal Tables (published 2015) ; Government of Quebec Politique du medicament (2007)

pCPA Updates

Bill 28

Quebec Bill 28 receives Royal Assent on April 21, 2015

QC Health Minister (the Minister) can enter into a PLA with a manufacturer prior to having the drug added on the Liste des médicaments

Important Bill amendments: – Temporary exclusion

– Publication of INESSS recommendations

– Reporting on Impact by October 2017

30

pCPA Updates

Update: Québec joins pCPA

As per the pCPA October 16th update, QC has now joined pCPA...

• Brand and generic initiatives • Ongoing and completed negotiations

31

Quebec PLAs

Impact: Québec joins the pCPA

- New negotiations CHANGE o QC will participate and possibly lead

- Ongoing negotiations CHANGE o QC will be joining majority of ongoing

negotiations which have INESSS recommendations o Manufacturers will be notified

- Completed negotiations CHANGE o Process in place for jurisdictions wishing to become a

“new” party to a Letter Of Intent (LOI) o Consent of all original participating parties within the

LOI

32

pCPA Updates

Question 7

What impact do you believe the inclusion of Quebec into the pCPA process will have on listing performance (number of products and time to listing) in

Quebec?

a) Improve the performance (quicker listing of more products) b) Deteriorate the performance (slower listing of fewer products) c) Will not impact the performance

33

pCPA Updates

Outlook ─ pCPA Office Operational

34

pCPA Updates

Greater clarity, structure, and efficiency in the negotiation process

Better sense of timeline expectations and administration point of contact

Question: Will the Office will encourage more formal linkages/ cooperation between CADTH, PMPRB and the pCPA

Outlook ─ Québec joins pCPA

Listing previously rejected products

More private payer PLAs in QC

Increased access challenges

Question: Given the variance in how INESSS reviews products compared to CADTH, it remains to be seen how negotiations will occur when there is incongruence on clinical recommendations

35

pCPA Updates

Question 8

How likely do you think it is that private payers will be joining the pCPA?

a) Highly Likely b) Likely c) Neutral d) Unlikely e) Highly Unlikely

36

pCPA Updates

Module 2: Private Payer PLAs

37

Private Payers in Canada

38

Private Payer PLAs

Starting to build internal competencies aimed at negotiating product listing agreements (PLAs)

Concerns about increasing drug costs, particularly for specialty products

Expressed interest in participating in pCPA negotiations

Need to better understand the prevalence, objectives and content of PLAs in this important market segment

Question 9

Has your company negotiated a product listing agreement with a private payer?

a) Yes b) No

39

Private Payer PLAs

Survey Objective

40

Private Payer PLAs

Pharma

Private Payers

• How many insurers and PBMs have experience with PLAs?

• Will PLAs become a requirement for coverage?

• What types of agreements are preferred?

• How many companies have experience with private payer PLAs?

• Why would companies seek to negotiate with insurers or PBMs?

• What types of agreements have been negotiated?

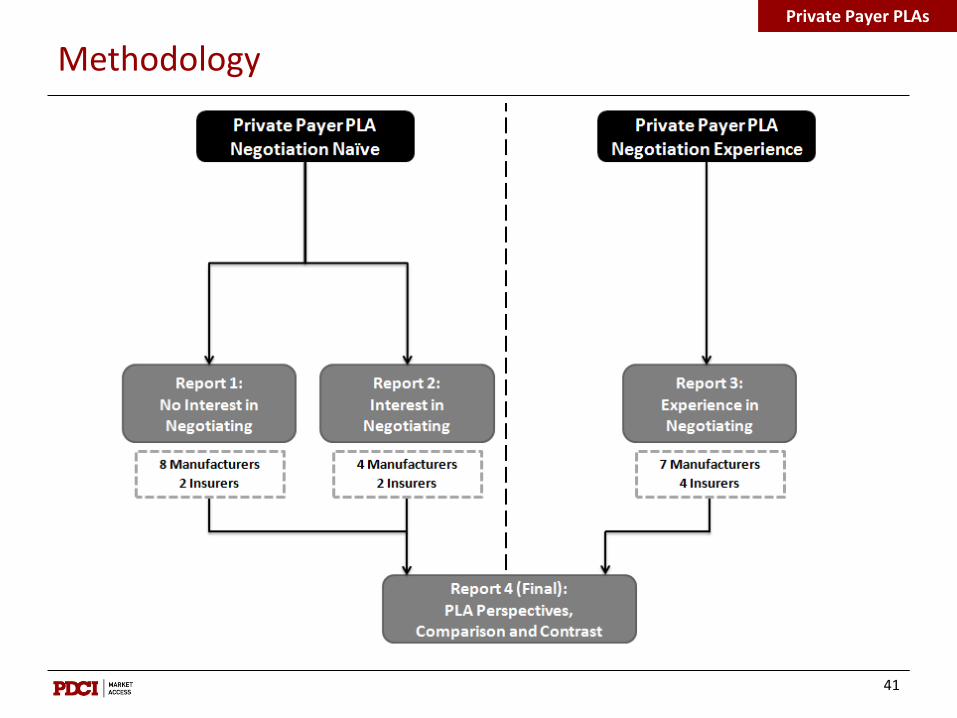

Methodology

41

Private Payer PLAs

Private Payer PLA Series

42

Private Payer PLAs

Once closed, survey responses were analyzed and four summary reports were created and released to the public.

To obtain free copies of the Private Payer PLA Series please visit our website at pdci.ca.

Key Findings - Negotiation Leaders

Grow in importance over time. Private payers will likely pursue PLAs in a more organized and

aggressive manner Without any tangible threats to access, it may be up to private

payers to initiate discussions, similar to the lead taken by their provincial counterparts

Strong incentive amongst smaller private payers to negotiate collectively

Larger private payers will likely be able to negotiate more competitive agreements

43

Private Payer PLAs

Key Findings - Product Types

Non-specialty products, will likely be initiated by manufacturers seeking preferential listing over comparators

Specialty products, will likely be initiated by private payer as a precondition to listing

Questions - There remain intriguing questions about how drugs for rare diseases will be dealt with.

44

Private Payer PLAs

Question 10

What type of product(s) are you prepared to negotiate a private payer product listing agreement for?

a) Specialty product (e.g. Enbrel) b) Drug for rare disease (e.g. Kalydeco) c) Non-specialty product d) All of the above e) None of the above

45

Private Payer PLAs

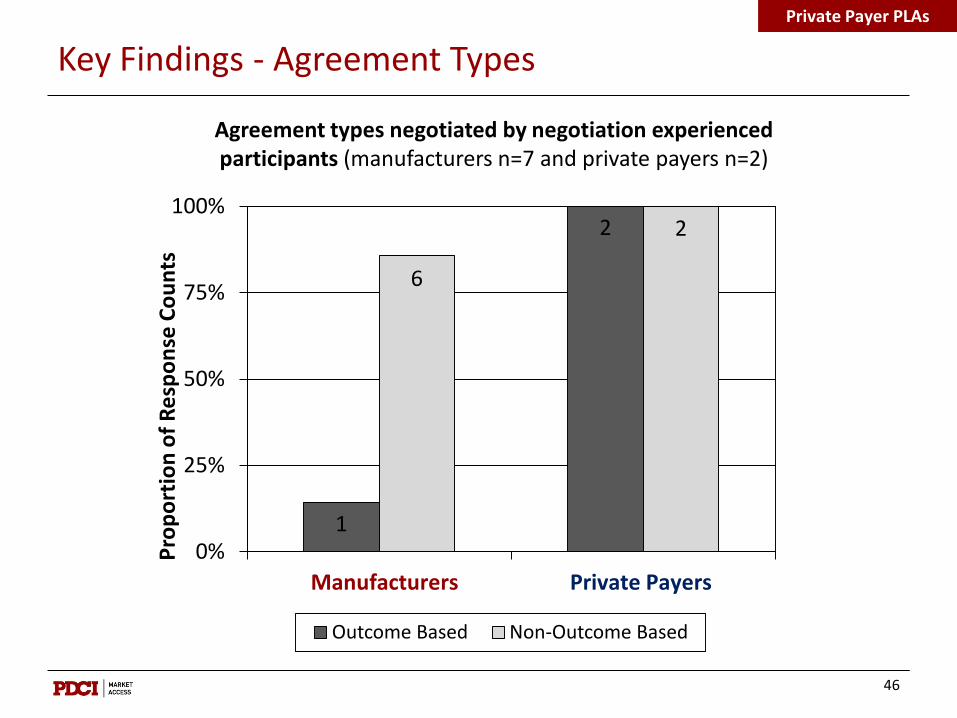

Key Findings - Agreement Types

46

Private Payer PLAs

1

2

6

2

0%

25%

50%

75%

100%

Manufacturer Private Payer

Prop

ortio

n of

Res

pons

e Co

unts

Outcome Based Non-Outcome Based

Manufacturers Private Payers

Agreement types negotiated by negotiation experienced participants (manufacturers n=7 and private payers n=2)

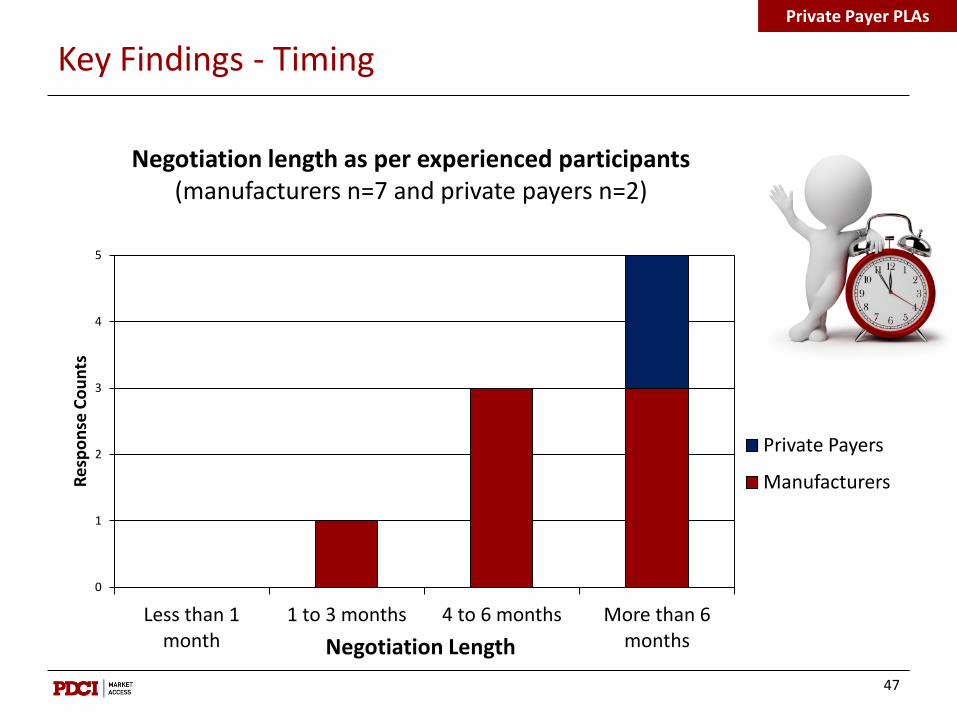

Key Findings - Timing

47

Private Payer PLAs

0

1

2

3

4

5

Less than 1 month

1 to 3 months 4 to 6 months More than 6 months

Resp

onse

Cou

nts

Negotiation Length

Private Payers

Manufacturers

Negotiation length as per experienced participants (manufacturers n=7 and private payers n=2)

Key Findings - Challenges

Transparency - Learning from the US private market, payers may begin to request more open PLAs that present more obvious advantages (in value and transparency) to their employer clients and plan members

PE Expertise - Capacity for insurers to conduct/better understand pharmacoeconomic analyses of new products

Competition Bureau - Private payers need to examine any anti-competitive hurdles

48

Private Payer PLAs

Question 11

Do you believe confidentiality of private payer PLAs is a significant challenge for manufacturers?

a) Yesb) No

49

Private Payer PLAs

Outlook ─ Private Payer PLAs

50

PLAs as pre-condition of listing for (expensive) new specialty products.

If Manulife DrugWatch™ gains traction in the market, it’s only a matter of time before other large carriers develop competing offers.

Increased pressure to negotiate private payer PLAs in Quebec.

Private Payer PLAs

Question 12

Manulife recently released its DrugWatch Program™ aimed at providing greater scrutiny on specialty products. Do you believe that other major

carriers will follow Manulife’s lead and create similar programs?

a) Yes b) No

51

Private Payer PLAs

Outlook ─ Private Payer PLAs

52

Smaller sized private payers will likely look to work together to negotiate competitive agreements

Payers will need to resolve concerns about collusion and anti-competitive behaviour

Given that more stakeholders are involved in private payer PLAs increasing the risk of information spillage.

Private Payer PLAs

Question and Answer Period

53

54

Thank you

Arvind Mani - Director, Market Access and Policy Research (613) 742-8225, Ext. 31 [email protected] Arvind Mani is the Director of Market Access and Policy Research at PDCI Market Access Inc. (PDCI), a leading Canadian pricing and reimbursement consultancy. Through his 20 years of experience working in consulting, associations (pharmaceutical and pharmacy) and industry, Arvind has developed an in-depth understanding of the Canadian and international pharmaceutical market access environment. At PDCI, he leads and provides strategic advice in the development of reimbursement submission dossiers that help clients demonstrate clinical- and cost-effectiveness to payers and health technology assessment agencies. Arvind has established expertise on emerging market access topics related to product listing agreements (PLAs), biosimilars, and drugs for rare diseases. He has published on a wide array of subjects ranging from companion diagnostics to healthcare reform. Arvind’s payer research project work has helped establish a solid relationship with both public and private payer stakeholders in Canada and allows him to offer clients strategic advice to help negotiate PLAs. Aside from facilitating advisory board meetings and conducting training sessions on topics related to the Canadian market access environment, he also presents/moderates sessions at market access conferences and academic institutions.