Embed Size (px)

Citation preview

MARKET ASSESSMENT ON MICROTAKAFUL IN INDONESIA

Presented by on behalf of

i

ACKNOWLEDGMENT

This market assessment was commissioned by the Deutsche Gesellschaft für Internationale Zusammenarbeit Regulatory Framework Promotion of Pro-poor Insurance Markets in Asia program (GIZ RFPI Asia), funded by the German Federal Ministry for Economic Cooperation and Development (BMZ). Its completion is made possible by the support of the Otoritas Jasa Keuangan (OJK, Financial Services Authority) of Indonesia and the Asosiasi Asuransi Syariah Indonesia (Indonesia Syariah Insurance Association). GIZ RFPI Asia expresses its gratitude to colleagues from OJK and AASI who were instrumental in the design, implementation and evaluation of the results of this assessment. Further contact details: GIZ RFPI Asia Dr. Antonis Malagardis Program Director Insurance Commission Complex 1071 U.N. Avenue, Ermita, Manila Philippines 1000 Telephone: +63 2 353 1044 -45 E-mail: [email protected] OJK Mr. Moch. Muchlasin Directorate of ShariahShariah Non-Bank Financial Institutions Sumitro Joyohadikusumo Building 13FL, Jl. Lapangan Banteng Timur 2-4 Jakarta Pusat 10710 Telephone: +61 21-3858001 ext 21330 E-mail: [email protected] AASI Ms. Srikandi Utami (Vice Chairperson) Graha Takaful Indonesia, Tower A, Fl. 2 Jl. Mampang Prapatan Kingdom No.100 South Jakarta 12970 Telephone: +62-21 5289 0000 E-mail: [email protected]

PREPARED BY:

Mr. Nick Thornton (freelance consultant) and Ms. Hajah Zuriah Abdul Rahman AFC Consultants International GmbH (AFC) Dottendorfer Str. 82, 53129 Bonn, Germany Telephone: +49 – 228 – 98 57 9 – 0 E-mail: [email protected] Web: www.afci.de For any further information please contact at AFC: Mr Johannes Buschmeier Telephone: +49 – 228 – 98 57 9 – 0 E-mail: [email protected] Mr Marcel Pape Telephone +49 – 228 – 98 57 9 – 74 Email: [email protected]

Jakarta, September 2014

ii

TABLE OF CONTENTS

ACRONYMS ......................................................................................................................... iv

1 INTRODUCTION ........................................................................................................... 1

1.1 Background 1

1.2 Objectives of assessment 2

1.3 Market Survey Methodology 2

2 THE RISK PROFILES OF LOW-INCOME INDONESIAN MUSLIMS ............................ 3

2.1 Sources of risks 3

2.2 Risk coverage needs 4

3 UNDERSTANDING AND PERCEPTIONS OF TAKAFUL ............................................. 5

4 CREATING AWARENESS AND EDUCATING THE MARKET ..................................... 6

5 THE POTENTIAL MARKET FOR MICROTAKAFUL .................................................... 8

5.1 Strength of the microtakaful business in Indonesia 10

6 THE MICROTAKAFUL SUPPLY CHAIN ..................................................................... 12

6.1 Microtakaful providers 12

6.2 Microtakaful distribution channels 13

6.3 Partnership arrangements 14

7 MICROTAKAFUL PRODUCTS: FEATURES AND ISSUES ....................................... 17

7.1 Potential microtakaful product features 20

8 THE REGULATORY ENVIRONMENT FOR MICROTAKAFUL MARKET DEVELOPMENT ......................................................................................................... 22

8.1 Prevailing regulatory issues 22

8.2 Considerations for the regulatory framework 24

8.3 Industry perspectives on regulatory improvement needs 26

8.4 Financial literacy and consumer protection 27

9 SUMMARY AND CONCLUSIONS .............................................................................. 28

10 STRATEGIC RECOMMENDATIONS.......................................................................... 29

10.1 The Microtakaful market 29

10.2 Microtakaful business model 29

10.3 The distribution channel 29

10.4 Human resource plan 30

10.5 Regulatory framework 30

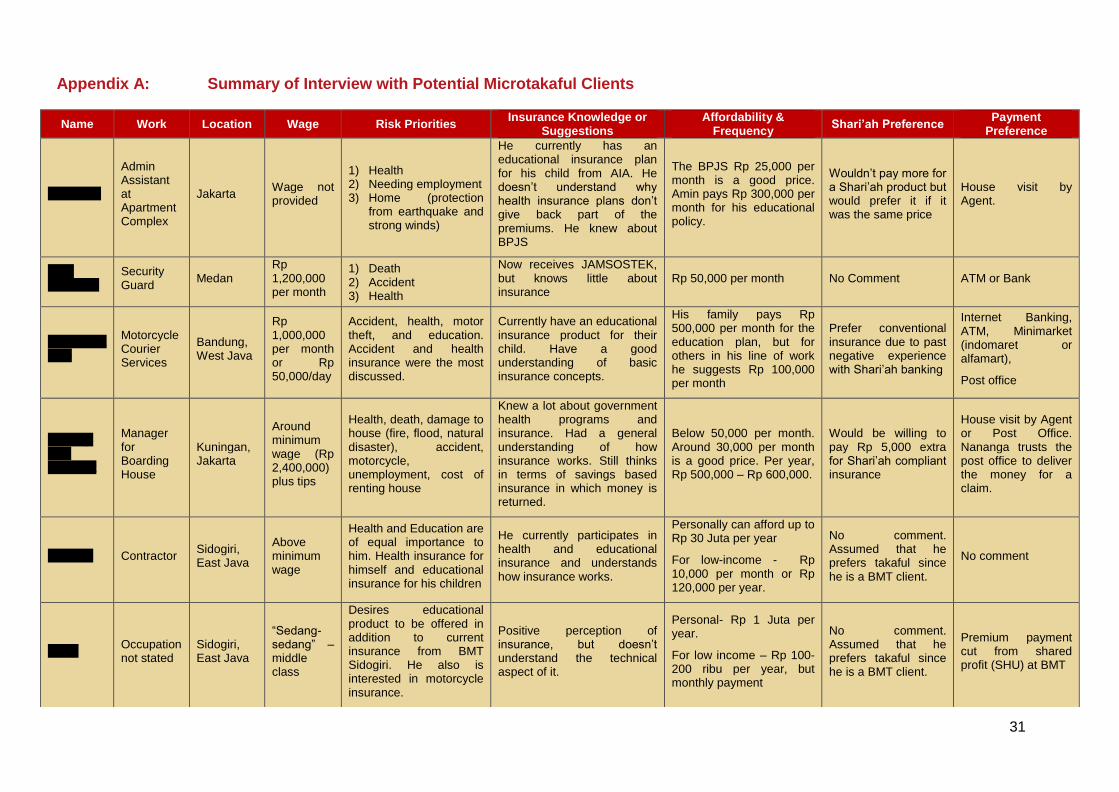

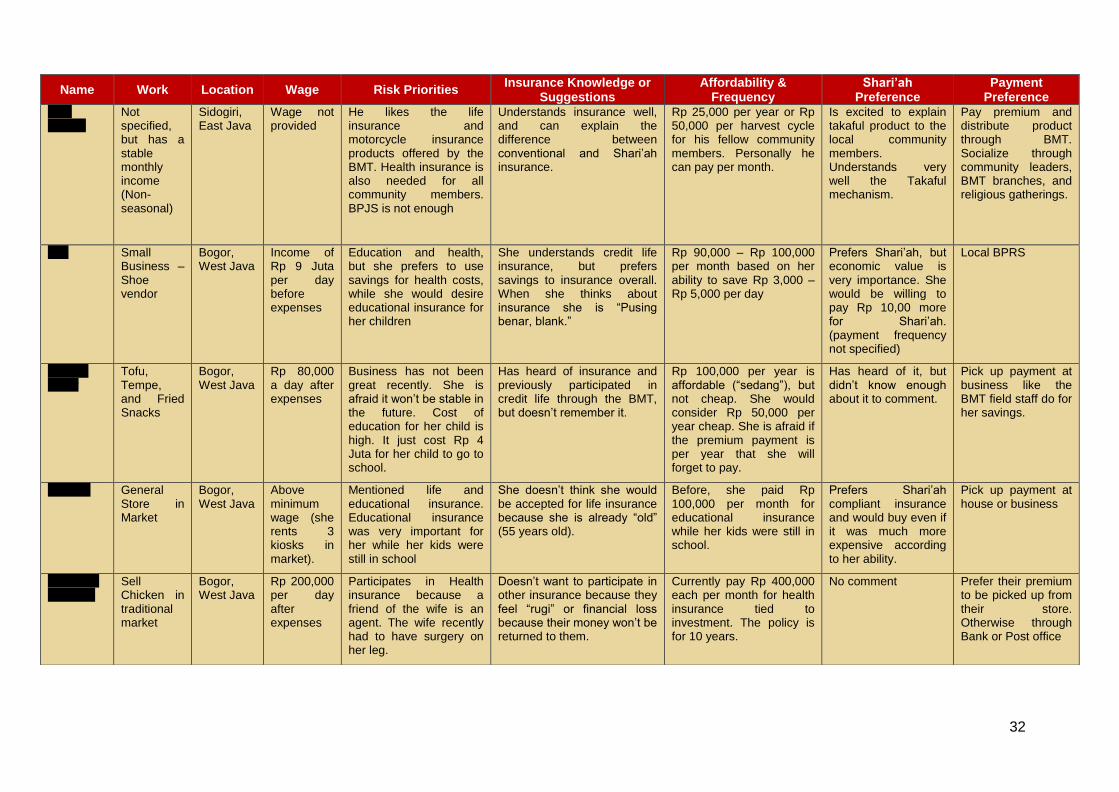

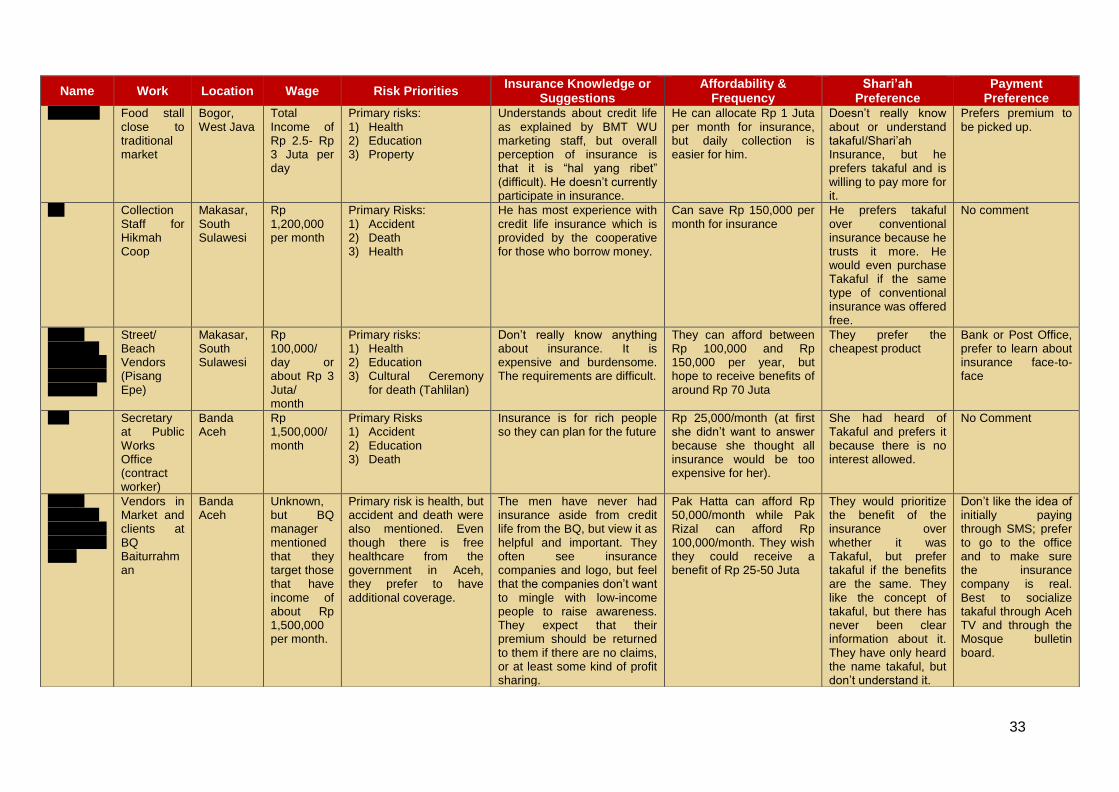

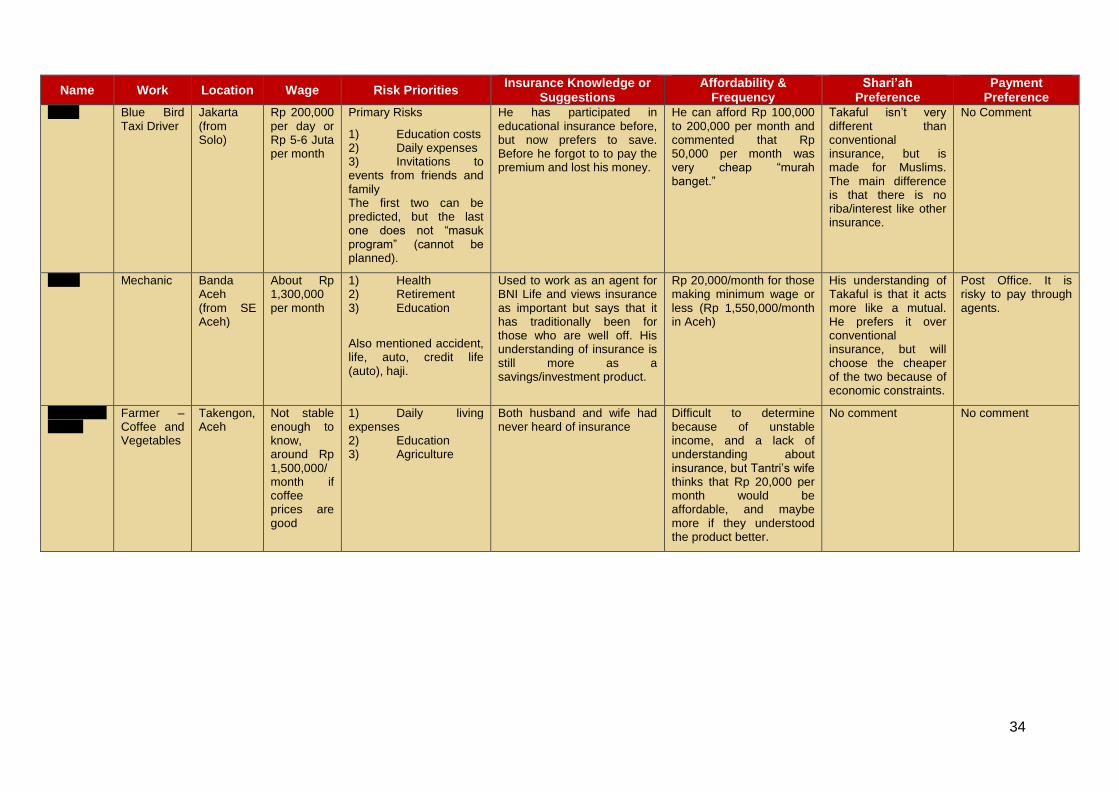

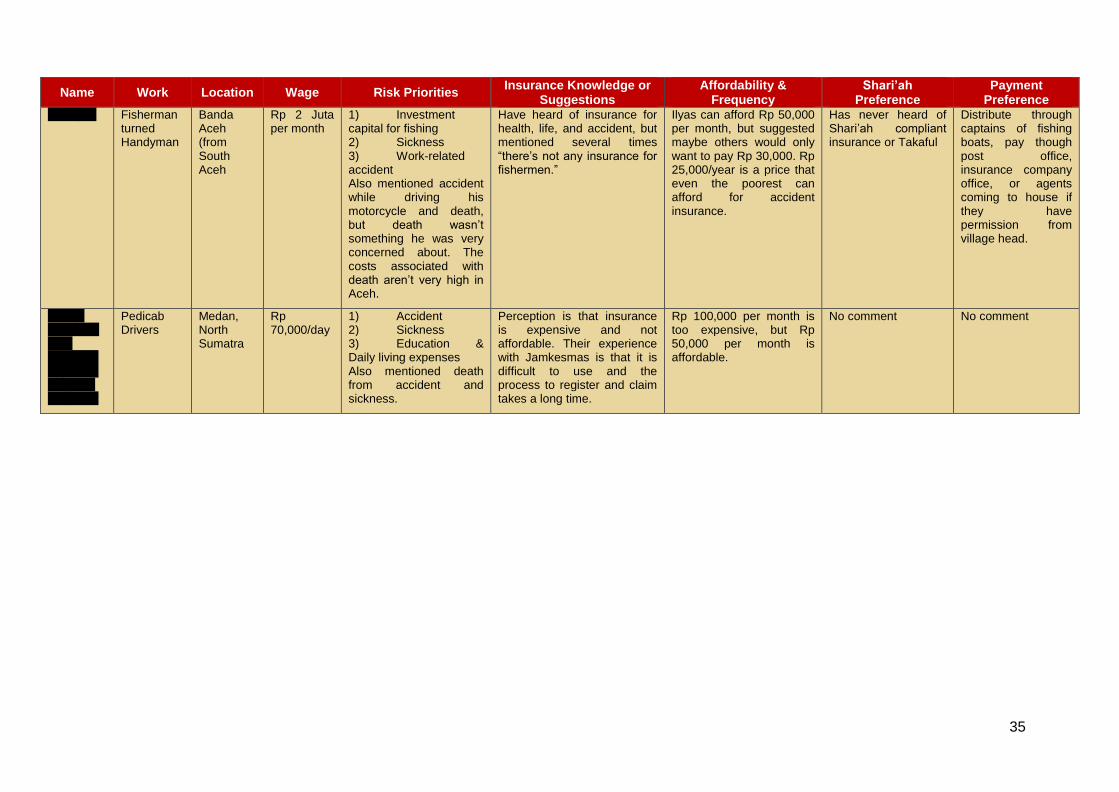

Appendix A: Summary of Interview with Potential Microtakaful Clients ...................... 31

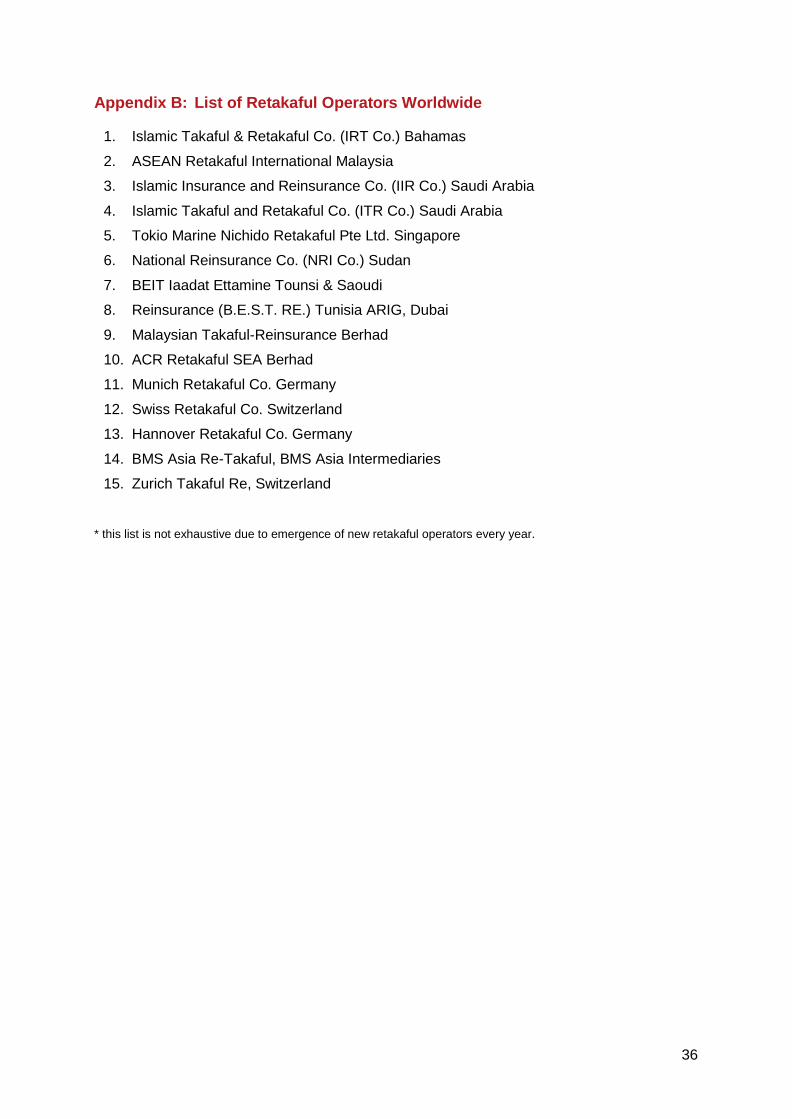

Appendix B: List of Retakaful Operators Worldwide .................................................... 36

Appendix C: Questionnaire for field staff ...................................................................... 37

Appendix D: Questionnaire for Shariah insurance entities .......................................... 39

iii

LIST OF TABLES

Table 1: Takaful vs Conventional Insurance ........................................................................... 1

Table 2: Ranking of Perceived Risks ...................................................................................... 3

Table 3: Demographic profile of microtakaful target market in Indonesia ................................ 9

Table 4: Full-fledged Takaful operators ................................................................................ 12

Table 5: Summary of Microtakaful Products Features, Delivery Channel in 8 Countries ....... 16

Table 6: Existing microtakaful products offered in Indonesia ................................................ 18

Table 7: Proposed microtakaful product features.................................................................. 20

LIST OF BOXES

Box 1: Profile of a typical “micro” policyholder ......................................................................... 9

Box 2: Reasons for the interest in microtakaful – It can generate profits ............................... 11

Box 3: Takaful Standards ..................................................................................................... 22

Box 4: Challenges of providing microtakaful to the poor ....................................................... 24

iv

ACRONYMS

AAOFI Accounting and Auditing Organization for Islamic Financial Institutions

AASI Asosiasi Asuransi Syariah Indonesia (Indonesia Syariah Insurance Association)

BMT Baitul Maal wat Tamil (Islamic Cooperative)

BPR Bank Perkreditan Rakyat (Rural Bank)

BPRS Bank Pembiayaan Rakyat Syariah (Islamic Rural Bank)

BPS Badan Pusat Statistik (Central Bureau of Statistics)

BTM Baitul Tamwil Muhammadiyah (Muhammadiyah Islamic Cooperative)

CSR Corporate Social Responsibility

ESCC Economic Syariah Committee Center

FGD Focus Group Discussion

GIZ Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH

IDR Indonesian Rupiah

IFSB Islamic Financial Services Board

IMFI Islamic Microfinance Institution

LKM Lembaga Keuangan Mikro (Microfinance Organization)

MFI Microfinance Institution

MI Microinsurance

OJK Otoritas Jasa Keuangan (Financial Services Authority)

PA Personal Accident

RFPI Regulatory Framework Promotion of Pro-poor Insurance Markets in Asia (RFPI Asia)

UPK Unit Pengelola Keuangan (Financial Administrative Unit)

1

1 INTRODUCTION

1.1 Background

In many Islamic countries, significant portions of the population live in poverty and lack the access to financial services, such as insurance, that will help prevent the further worsening of their economic situations. In such countries as Indonesia, the creation of a microtakaful market, an appropriate market for insurance that is compliant with Islamic laws and that will cater to the low-income sector, is a need that is slowly gaining attention and priority. But while initial efforts have led to the development and offer of some microtakaful products, the pace of development needs speed and the approach needs concerted collaboration between the government and the insurance industry. The current situation needs to be understood to inform the future progress of the microtakaful market.

As a country with the largest Muslim population in the world, Indonesia has a vast untapped takaful market potential. In 2011, gross premiums of total Islamic insurance or takaful were reported to be less than 5% of total insurance market premiums. Despite the low market share, Indonesia is one of the world’s fastest-growing takaful markets. Based on preliminary industry estimates, gross premiums in the takaful industry were reported to have grown almost tenfold from IDR 498.9bn in 2006 to IDR 4.97tn in 2011 (Fitch Rating, 2013).

Takaful is defined as an insurance which is Shariah compliant and offered as an alternative to Muslims and non-Muslims alike who prefer to be covered by a product which is both ethical and in line with the Islamic religious teachings. Microtakaful, on the other hand are takaful products that are tailor-made in terms of policy size, (which are usually small), limited coverage, small contribution amounts, and flexible mode of payment to cater to the low income and poor who have some risk priorities but could not afford the mainstream takaful products offered in the market. Microtakaful products are crafted to meet the special needs of the economically challenged members of the society or market segment to enable their financial inclusivity and to provide a risk management solution that fits their needs.

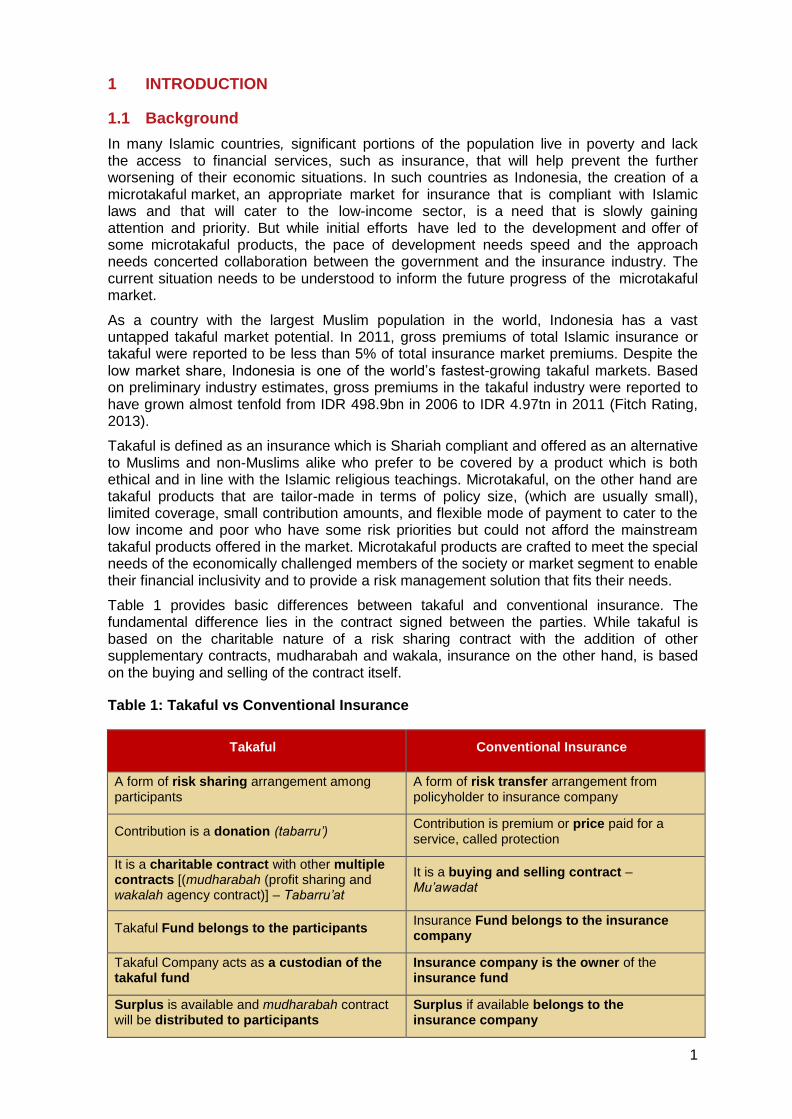

Table 1 provides basic differences between takaful and conventional insurance. The fundamental difference lies in the contract signed between the parties. While takaful is based on the charitable nature of a risk sharing contract with the addition of other supplementary contracts, mudharabah and wakala, insurance on the other hand, is based on the buying and selling of the contract itself.

Table 1: Takaful vs Conventional Insurance

Takaful Conventional Insurance

A form of risk sharing arrangement among participants

A form of risk transfer arrangement from policyholder to insurance company

Contribution is a donation (tabarru’) Contribution is premium or price paid for a service, called protection

It is a charitable contract with other multiple contracts [(mudharabah (profit sharing and wakalah agency contract)] – Tabarru’at

It is a buying and selling contract – Mu’awadat

Takaful Fund belongs to the participants Insurance Fund belongs to the insurance company

Takaful Company acts as a custodian of the takaful fund

Insurance company is the owner of the insurance fund

Surplus is available and mudharabah contract will be distributed to participants

Surplus if available belongs to the insurance company

2

1.2 Objectives of assessment

This report highlights the results of a market assessment on microtakaful in Indonesia, conducted to contribute to the improvement of the regulatory and supervisory conditions for the effective development of a microtakaful market that offers protection to the low-income Indonesians. The market assessment also aims to serve as a basis for the development of appropriate microtakaful products and business models by the members of the Asosiasi Asuransi Syariah Indonesia (Indonesia Syariah Insurance Association).

The assessment analyzed the existing and potential demand for microtakaful through the documentation of the socio-cultural, economic and demographic profiles, payment modes and frequency and product preferences of low-income respondents. The supply side of the market was also assessed, examining the supply chain that includes takaful operators, distribution channels and other relevant networks and support institutions. Moreover, the assessment describes the existing regulatory environment within which the market operates and the initiatives taken by the Otoritas Jasa Keuangan (OJK, Financial Services Authority) to promote the market for microtakaful, particularly through financial literacy and consumer awareness.

1.3 Market Survey Methodology

The microtakaful survey was qualitative in nature and primarily used Focus Group Discussions (FGDs) and interviews in addition to a secondary research review. FGDs also employed both individual and group risk ranking exercises. In total, 13 FGDs were facilitated in four (4) provinces and in DKI Jakarta, consisting of seven (7) mixed gender groups, three (3) groups of men only, and three (3) groups of only women. Interviews with potential microtakaful clients were conducted in an additional two (2) provinces and consisted of 22 non-in depth interviews, four (4) in-depth interviews, and three (3) group interviews. In order to benefit from the insights of those working directly with the low-income segment, the assessment also conducted 25 interviews with staff from microfinance institutions (MFIs) and cooperatives, and one (1) interview with a community leader. For additional information and triangulation, a short questionnaire was given to the staff of the MFIs and cooperatives visited. To gather industry data, the assessment team met with the Financial Services Authority (OJK), conducted 11 interviews with insurance professionals, had a small group discussion with Indonesia Syariah Insurance Association (AASI) members, and sent a questionnaire to all members of AASI.

The assessment tried to capture the thoughts and attitudes concerning microtakaful from the low-income Muslim population as defined in the Grand Design for Microinsurance published by OJK as those with an income of less than IDR 2.5 million per month. In particular, perspectives were gathered from low-income Muslims from conventional and Islamic MFIs, community groups not connected with MFIs or cooperatives, and those in the farming trade. Locations of the FGDs were determined based on the most recent BPS population and poverty data. Determining factors included the total Muslim population, total number of poor (BPS definition of poverty), percentage of poor, and population density. The primary focus on MFIs for FGDs and interviews was due to four reasons 1) MFIs have traditionally been a partner in piloting microinsurance products around the world and represent a natural distribution channel for microinsurance, 2) there are MFIs in Indonesia which are currently partnering with Takaful providers 3) the opportunity to compare the responses of low-income Muslims participating in Islamic MFIs with those participating in conventional MFIs, and 4) facilitate the efficient gathering of groups of members for discussion.

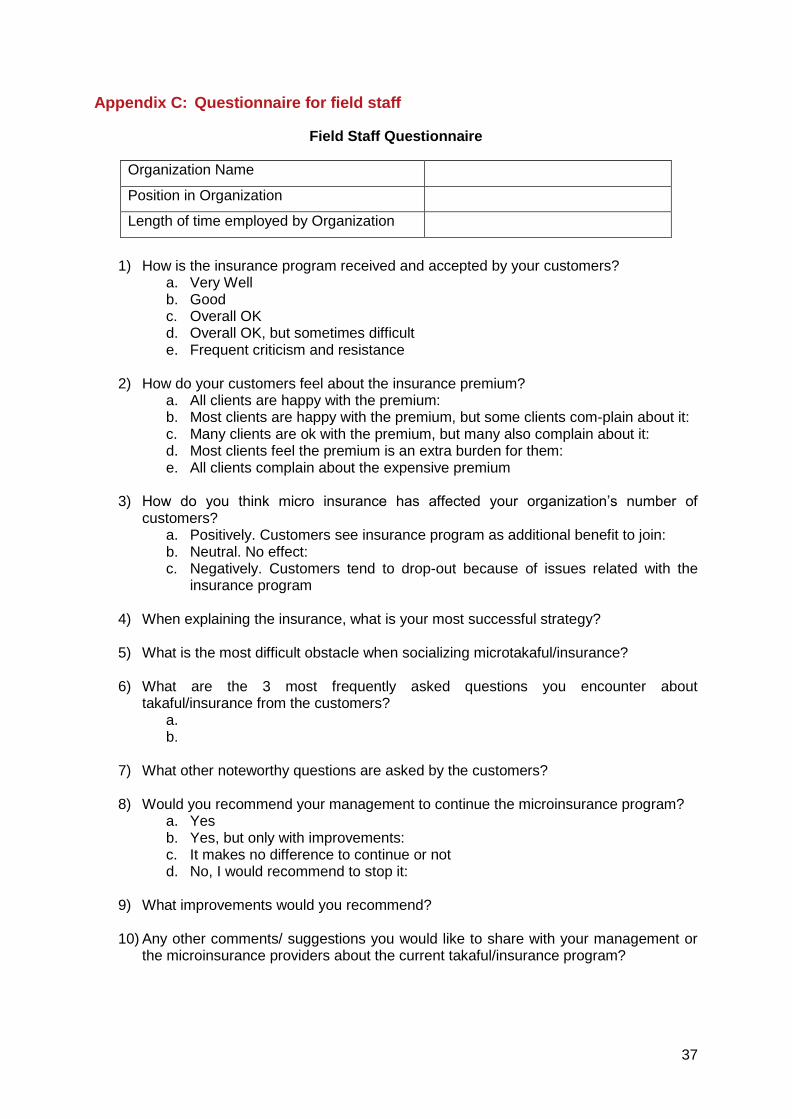

Questionnaires for field staff were adapted from the research of Martin Hintz (2009, pp. 251-253) and questionnaires for AASI were adapted from the research of Anja Erlbeck (2010, pp. 71-76).

3

2 THE RISK PROFILES OF LOW-INCOME INDONESIAN MUSLIMS

2.1 Sources of risks

Reiterating the results of past microinsurance surveys in Indonesia, this assessment identified illness and education expenses as the two main life events that determine the vulnerability of the poor to risks. Other factors that impact their risk vulnerability include daily living expenses, need for business capital/lump sums of money, occurrence of accidents and death.

In contrast to past surveys, though, natural disasters were not identified as a major risk event or a common problem among those surveyed. While natural disasters were mentioned, they never made it high in the ranking of most burdensome problems.

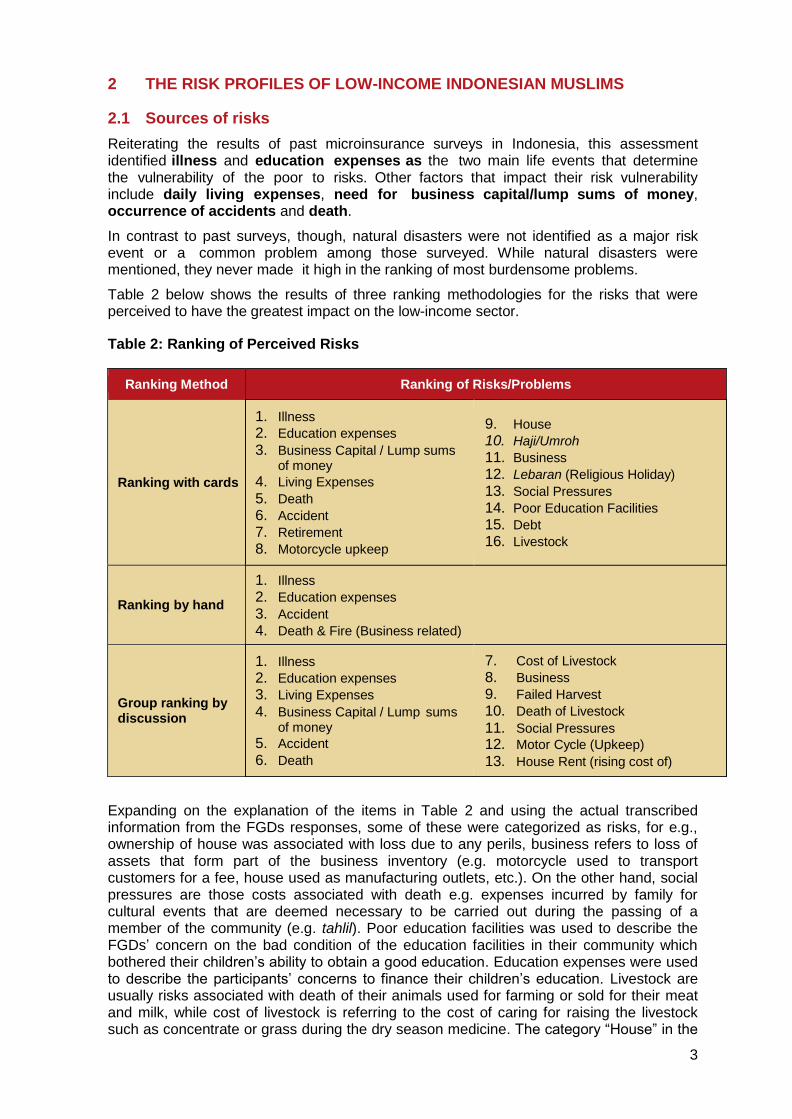

Table 2 below shows the results of three ranking methodologies for the risks that were perceived to have the greatest impact on the low-income sector.

Table 2: Ranking of Perceived Risks

Ranking Method Ranking of Risks/Problems

Ranking with cards

1. Illness

2. Education expenses

3. Business Capital / Lump sums of money

4. Living Expenses

5. Death

6. Accident

7. Retirement

8. Motorcycle upkeep

9. House

10. Haji/Umroh

11. Business

12. Lebaran (Religious Holiday)

13. Social Pressures

14. Poor Education Facilities

15. Debt

16. Livestock

Ranking by hand

1. Illness

2. Education expenses

3. Accident

4. Death & Fire (Business related)

Group ranking by discussion

1. Illness

2. Education expenses

3. Living Expenses

4. Business Capital / Lump sums of money

5. Accident

6. Death

7. Cost of Livestock

8. Business

9. Failed Harvest

10. Death of Livestock

11. Social Pressures

12. Motor Cycle (Upkeep)

13. House Rent (rising cost of)

Expanding on the explanation of the items in Table 2 and using the actual transcribed information from the FGDs responses, some of these were categorized as risks, for e.g., ownership of house was associated with loss due to any perils, business refers to loss of assets that form part of the business inventory (e.g. motorcycle used to transport customers for a fee, house used as manufacturing outlets, etc.). On the other hand, social pressures are those costs associated with death e.g. expenses incurred by family for cultural events that are deemed necessary to be carried out during the passing of a member of the community (e.g. tahlil). Poor education facilities was used to describe the FGDs’ concern on the bad condition of the education facilities in their community which bothered their children’s ability to obtain a good education. Education expenses were used to describe the participants’ concerns to finance their children’s education. Livestock are usually risks associated with death of their animals used for farming or sold for their meat and milk, while cost of livestock is referring to the cost of caring for raising the livestock such as concentrate or grass during the dry season medicine. The category “House” in the

4

individual ranking refers to the rent itself and the desire to protect the house from natural disaster, fire, or from thievery. House rent (in the group ranking) refers to the rising cost of rent, not necessarily for those that had businesses in their home. Some of the FGD participants were employed outside the home, and thus an increase in rent didn’t cause a threat to loss of income, but a higher expense of rental which poses a risk to most of the FGDs because these buildings served simultaneously as their dwellings and business premises, hence the loss of income seemed real due to the direct dependency on these units.

2.2 Risk coverage needs

The majority of the surveyed participants indicated their willingness to participate in a microinsurance program that provides health insurance, a finding that is similar to the results of market surveys undertaken in Bangladesh and Peru (Ahmed, M. 2013; Iravantchi, S. 2012).

Demand for risk coverage of illness, accident, and death is common globally. However, what is distinct in the Indonesian market from the survey is the indication that the market felt the need to have coverage for education. This could be explained in the context of the demographic profile of the rural and urban poor, where 70 percent of basic needs in household were met by women and they make 60 percent of purchasing decision while 84 percent controlled their family’s money (Jakarta Post, April, 20, 2014). This is especially true from the FGDs of the female respondents where 9 out of 10 women interviewed say education is important for their children.

Deductions made from the market survey also indicated that they gave a priority ranking which is considerably so much higher than the other risks (health insurance: 25; education: 18 while the other risks ranged between 1-9). To a certain extent this explains their seriousness in wanting these two products for their families.

5

3 UNDERSTANDING AND PERCEPTIONS OF TAKAFUL

Many of the assessment participants were not aware of takaful or Shariah-compliant insurance. Even so, after receiving some information about it, most of them expressed positive perception of takaful though they had never heard of it before. As Muslims, they assume that it is better to use takaful rather than conventional insurance, but would like to know more about it first prior to deciding to purchase.

Those that had heard of takaful usually knew one of two things about it:

It is Halal, made specifically for Muslims and not associated with Riba.

It is similar to the approach of mutual organizations, with profit sharing.

Even some members of Islamic cooperatives that currently are using takaful credit life products were not aware of the general concept of takaful. The general lack of awareness greatly limited the discussion of takaful products. After receiving some information on takaful, questions and comments regarding the differences between takaful and conventional insurance were raised. The highlights of the perceptions below show that various factors influence the preference or aversion for takaful.

A few respondents still expressed preference for conventional insurance due to the following reasons:

Past bad experience in Islamic banking

Perception of “takaful” as only a change in name, but with still the same approach, which signals a “munafik” or hypocritical strategy

Lack of knowledge about takaful while abundant information about conventional insurance makes for comfortable decision-making

Preference for a national product that everyone would feel comfortable using and would not exclude anyone

The price and benefit of the product were the most important factors for the preference or aversion for takaful, rather than its compliance or non-compliance with Shariah rules. Some participant expressed willingness to choose a takaful product over a conventional insurance product if the price and benefits are good or better.

For those who preferred takaful products, the willingness to pay for the additional premium range of IDR 5,000 to IDR 10,000 more per payment period (month or year) was expressed. However, if offered a cheaper conventional insurance product, preference was still for this cheaper product.

Still, some participants expressed the willingness to purchase takaful even if the price were more expensive than the conventional insurance product, as long as they are able to pay for it “mampu”.

Information was also received that some students and teachers at a local Islamic boarding school would absolutely not purchase insurance unless it was Shariah-compliant.

6

4 CREATING AWARENESS AND EDUCATING THE MARKET

The relative lack of awareness and understanding of the distinction among microinsurance, takaful, and microtakaful is a glaring challenge to the market. Without the understanding, the perception is that the product does not differ from microinsurance. The bullet points below list the themes for which information seems to be highly needed by consumers, as evidence by some of the questions expressed in FGDs:

Benefits

Will I get my premiums back if I don’t have a claim?

If I am in an accident and receive the payout, but I haven’t paid in as much as I receive, what happens?

Does the educational insurance pay directly to the school or to me?

If we have only paid health insurance premiums for a few months and then get sick, are we covered?

Does insurance pay interest?

I can get my money back for educational insurance, why can’t I get it back for health insurance?

If my loan is paid off before the term is up, do I get back any of my premium/tabarru?

Eligibility

What is the age limit?

Distinction of features

What’s the difference between conventional insurance and takaful?

Is there insurance for retirement?

What is covered for homeowners insurance?

How does disability insurance work?

Is there insurance for livestock?

Is insurance the same as saving?

Can insurance cover more than one risk at one time or only one risk at a time?

Payment modes

If I die and the policy period is still not complete, who will continue payments?

Is it cheaper to pay per year, rather than per month?

Where does my money go if I don’t make any claims?

In addition to the need for education on the general topics of microinsurance and microtakaful, the need for education on the Shariah compliance element of insurance is also important. A number of initiatives are expected to provide this educational need. OJK’s education and socialization on microinsurance through the “Grand Design: Development of Microinsurance” in Indonesia has, to a certain extent, opened the door to an awareness campaign. However, the outreach is currently rather limited. With the establishment of the Economic Syariah Committee Center (ESCC), various activities have been implemented for the microtakaful inclusion of the low-income. This included the socialization/education on microtakaful which included topics such as benefits of microtakaful, how to obtain the product, and how to contribute and how to claim.

A dedicated website, mass media, via TV Muamalat, bazaars, book launching event, Shariah Economic Writing Competition, Program Sejuta have all been designed by the center to reach out to a much larger audience. The ESCC works closely with the MUI

7

(Islamic Scholars Council), the AASI and the BMTs in these initiatives. On the measurement of its Key Performance Indicators, the center establishes a system of color to identify groups who had been identified as initially poor (below poverty line) with the color Red and advancing to Yellow (crossed the poverty line, but still financially weak), Green, ready to be developed and Blue, moving on to become financially independent. However this color coding system does not necessarily indicate whether the education on microtakaful actually reached its intended audience and uplifted their economic status.

Finally the most notable initiative is the design of the Asuransi Mikro Syariah Indonesia, or GRES! which it hoped to dispel all doubts on the Shariah compliancy and permissibility of the microtakaful product. The GRES! with the term Syariah included in it connotes that the product is permissible hence suitable for Muslims. The ESCC also partners with various other channel distributors (membuka lorong komunikasi) to ensure it covers both microtakaful and Islamic finance and banking.

8

5 THE POTENTIAL MARKET FOR MICROTAKAFUL

An accurate description or profile of the existing microtakaful market clientele (demand-side) cannot be completed at present since the market itself is still evolving and a monitoring system has yet to be adopted by either takaful / insurance providers or the regulator. In addition, the issue of defining the market is an on-going debate. The potential microtakaful market is influenced by how “micro” is defined. Is the definition based on who the target consumers are - the unbanked or under banked? Can it be defined based on the product features that specifically target the poor? If so, who are the poor? Allianz has stated in its 2013 Half Year Report that the micro market is that which pertains to low-income individuals who are not the very poorest, but rather are those who live on $1.25 to $4 a day.

This survey has also documented that some Islamic Microfinance Institutions do not consider the very poor as ready to participate in profit-sharing Islamic credit models but can and are only participating as loan clients without the burden of profit-sharing, until they are ready to share with the profits.

Perceptions from microfinance providers also highlight the micro market segment is not always perceived as poor, but rather those with unpredictable and unstable incomes. To restrict the definition of “micro” segment too much would result in the exclusion of those who would benefit from a takaful product, but who might not be ready to avail of one yet.

The 2013 Millennium Development Goals report suggested that 60% of populations in the developing world live on less than $4 a day. The Indonesian population, as recorded in the 2010 census, is a total of 238,518,800 million people, hence if we generalize, there are approximately 143,111,280 people that live on less than $4 a day in Indonesia. In September of 2013, BPS data reported a total of 28,553,930 Indonesians living under the poverty line. If we take the Allianz definition and apply it to Indonesia, using the local poverty line measurement rather than $1.25, then the potential market for microinsurance is somewhere around 114,557,350 people which represents those living above the poverty line, but still on less than $4 a day. Assuming that 86.1% of these people are Muslims (2000 census data), the specific low-income Muslim segment is a total of 98,633,878 people.

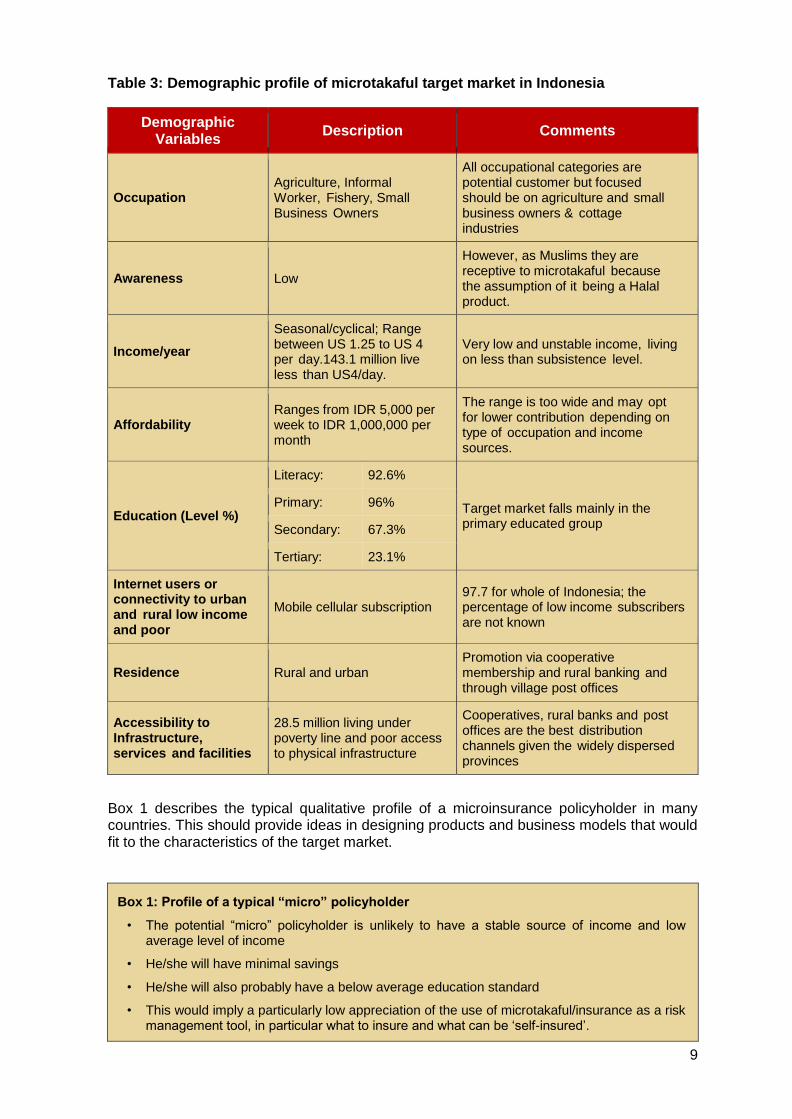

This survey and secondary literature search has come up with a general overview of the profile of the potential target market for microtakaful (see Table 3). Studies on creating demand for Islamic finance specifically takaful indicated a few factors that would hasten the process. Firstly, demographic factors including occupation, income (explains affordability), education level, and locality (urban vs. rural) are determinants for the products demand (Abdul Rahman et. al, 2009; Redzuan et.al, 2009; Sherif and Shaairi, 2013). Secondly, increased visibility and awareness level is considered important for consumer consumption of any products or services because these are determinants that could accelerate sales and growth. This is illustrated by Colley’s (1961) DAGMAR Model (Defining Advertising Goals for Measured Advertising Results), which suggests that the ultimate objective of advertising must carry a consumer through four levels of understanding; from unawareness to awareness, comprehension (comprehend what the product is and its benefits), conviction (arrive at a mental disposition to buy the product), and finally buy that product. Thirdly, connectivity especially in this digital age brings products right to the doorstep of the customers in an instant. Finally, accessibility both virtual (mobile phones, PDA, laptops etc.) and physical (services and facilities) are the two most important factors that would help increase awareness levels and create demand for products or services, while improving productivity and continued economic growth and development (Smart 2009-0072, McKinsey Global Institute, 2013).

9

Table 3: Demographic profile of microtakaful target market in Indonesia

Demographic Variables

Description Comments

Occupation Agriculture, Informal Worker, Fishery, Small Business Owners

All occupational categories are potential customer but focused should be on agriculture and small business owners & cottage industries

Awareness Low

However, as Muslims they are receptive to microtakaful because the assumption of it being a Halal product.

Income/year

Seasonal/cyclical; Range between US 1.25 to US 4 per day.143.1 million live less than US4/day.

Very low and unstable income, living on less than subsistence level.

Affordability Ranges from IDR 5,000 per week to IDR 1,000,000 per month

The range is too wide and may opt for lower contribution depending on type of occupation and income sources.

Education (Level %)

Literacy: 92.6%

Target market falls mainly in the primary educated group

Primary: 96%

Secondary: 67.3%

Tertiary: 23.1%

Internet users or connectivity to urban and rural low income and poor

Mobile cellular subscription 97.7 for whole of Indonesia; the percentage of low income subscribers are not known

Residence Rural and urban Promotion via cooperative membership and rural banking and through village post offices

Accessibility to Infrastructure, services and facilities

28.5 million living under poverty line and poor access to physical infrastructure

Cooperatives, rural banks and post offices are the best distribution channels given the widely dispersed provinces

Box 1 describes the typical qualitative profile of a microinsurance policyholder in many countries. This should provide ideas in designing products and business models that would fit to the characteristics of the target market.

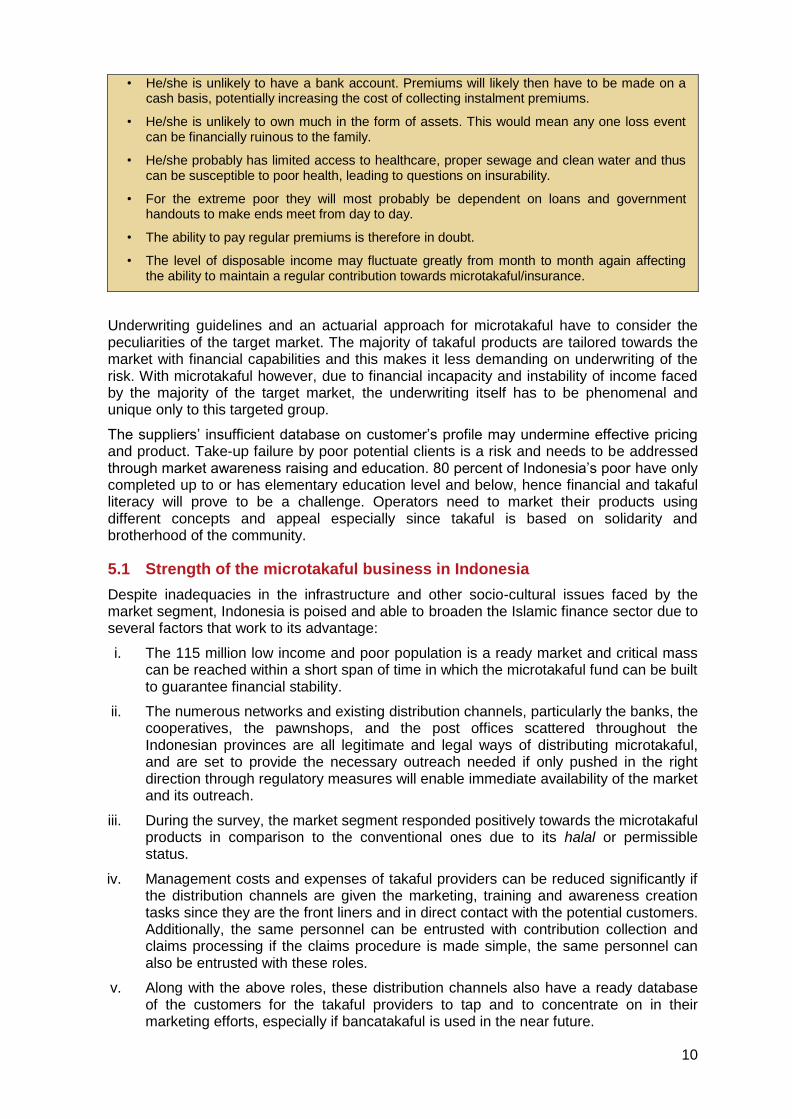

Box 1: Profile of a typical “micro” policyholder

• The potential “micro” policyholder is unlikely to have a stable source of income and low average level of income

• He/she will have minimal savings

• He/she will also probably have a below average education standard

• This would imply a particularly low appreciation of the use of microtakaful/insurance as a risk management tool, in particular what to insure and what can be ‘self-insured’.

10

• He/she is unlikely to have a bank account. Premiums will likely then have to be made on a cash basis, potentially increasing the cost of collecting instalment premiums.

• He/she is unlikely to own much in the form of assets. This would mean any one loss event can be financially ruinous to the family.

• He/she probably has limited access to healthcare, proper sewage and clean water and thus can be susceptible to poor health, leading to questions on insurability.

• For the extreme poor they will most probably be dependent on loans and government handouts to make ends meet from day to day.

• The ability to pay regular premiums is therefore in doubt.

• The level of disposable income may fluctuate greatly from month to month again affecting the ability to maintain a regular contribution towards microtakaful/insurance.

Underwriting guidelines and an actuarial approach for microtakaful have to consider the peculiarities of the target market. The majority of takaful products are tailored towards the market with financial capabilities and this makes it less demanding on underwriting of the risk. With microtakaful however, due to financial incapacity and instability of income faced by the majority of the target market, the underwriting itself has to be phenomenal and unique only to this targeted group.

The suppliers’ insufficient database on customer’s profile may undermine effective pricing and product. Take-up failure by poor potential clients is a risk and needs to be addressed through market awareness raising and education. 80 percent of Indonesia’s poor have only completed up to or has elementary education level and below, hence financial and takaful literacy will prove to be a challenge. Operators need to market their products using different concepts and appeal especially since takaful is based on solidarity and brotherhood of the community.

5.1 Strength of the microtakaful business in Indonesia

Despite inadequacies in the infrastructure and other socio-cultural issues faced by the market segment, Indonesia is poised and able to broaden the Islamic finance sector due to several factors that work to its advantage:

i. The 115 million low income and poor population is a ready market and critical mass can be reached within a short span of time in which the microtakaful fund can be built to guarantee financial stability.

ii. The numerous networks and existing distribution channels, particularly the banks, the cooperatives, the pawnshops, and the post offices scattered throughout the Indonesian provinces are all legitimate and legal ways of distributing microtakaful, and are set to provide the necessary outreach needed if only pushed in the right direction through regulatory measures will enable immediate availability of the market and its outreach.

iii. During the survey, the market segment responded positively towards the microtakaful products in comparison to the conventional ones due to its halal or permissible status.

iv. Management costs and expenses of takaful providers can be reduced significantly if the distribution channels are given the marketing, training and awareness creation tasks since they are the front liners and in direct contact with the potential customers. Additionally, the same personnel can be entrusted with contribution collection and claims processing if the claims procedure is made simple, the same personnel can also be entrusted with these roles.

v. Along with the above roles, these distribution channels also have a ready database of the customers for the takaful providers to tap and to concentrate on in their marketing efforts, especially if bancatakaful is used in the near future.

11

There is a growing interest from the industry to pursue microtakaful market development. Box 2 provides an excerpt from testimonies of speakers in the 2014 Microtakaful Conference in Indonesia1.

Box 2: Reasons for the interest in microtakaful – It can generate profits (testimony from various speakers participating in the 2014 Microtakaful Conference in Indonesia)

• Microtakaful is a new market compared to upper income markets that are often saturated.

• Microtakaful helps to get the company’s brand name into the market. Brand recognition is important since today’s low-income client is tomorrow’s middle class client.

• Microtakaful helps develop good relationship with the regulator and government.

• Microtakaful can be presented as an act of corporate social responsibility, but should not be limited to that.

1 For further information, please visit www.inclusiveinsuranceasia.com

12

6 THE MICROTAKAFUL SUPPLY CHAIN

6.1 Microtakaful providers

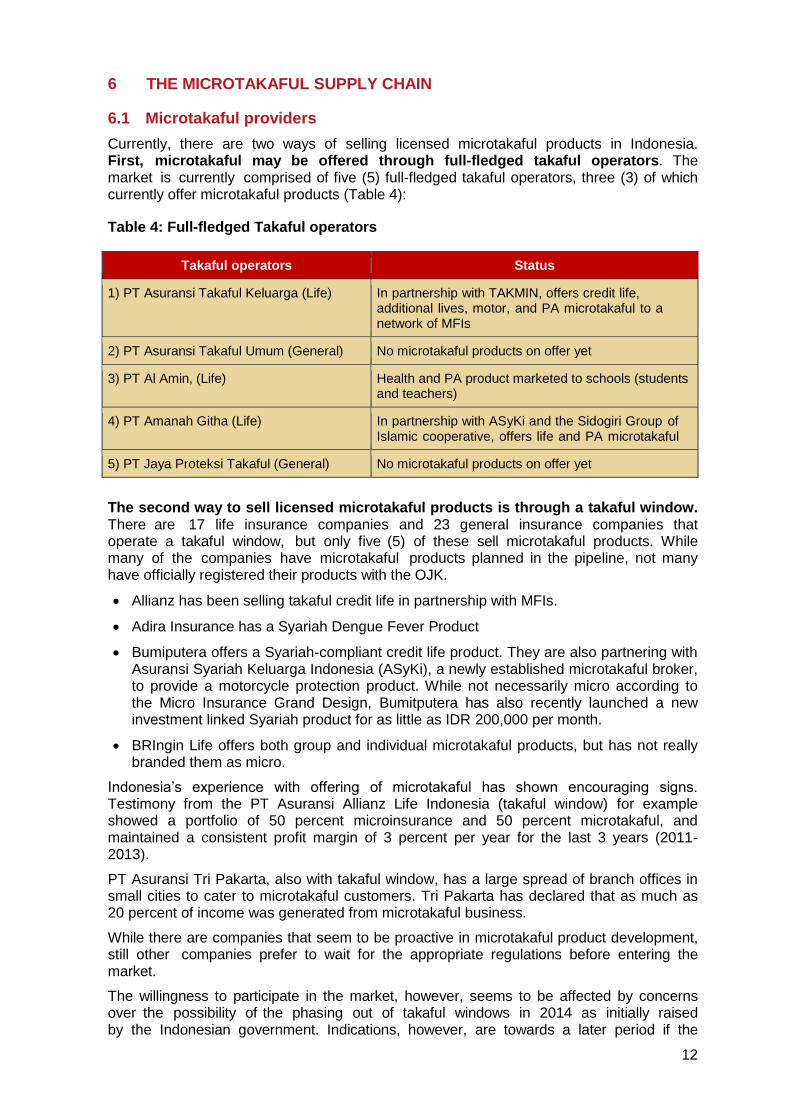

Currently, there are two ways of selling licensed microtakaful products in Indonesia. First, microtakaful may be offered through full-fledged takaful operators. The market is currently comprised of five (5) full-fledged takaful operators, three (3) of which currently offer microtakaful products (Table 4):

Table 4: Full-fledged Takaful operators

Takaful operators Status

1) PT Asuransi Takaful Keluarga (Life) In partnership with TAKMIN, offers credit life, additional lives, motor, and PA microtakaful to a network of MFIs

2) PT Asuransi Takaful Umum (General) No microtakaful products on offer yet

3) PT Al Amin, (Life) Health and PA product marketed to schools (students and teachers)

4) PT Amanah Githa (Life) In partnership with ASyKi and the Sidogiri Group of Islamic cooperative, offers life and PA microtakaful

5) PT Jaya Proteksi Takaful (General) No microtakaful products on offer yet

The second way to sell licensed microtakaful products is through a takaful window. There are 17 life insurance companies and 23 general insurance companies that operate a takaful window, but only five (5) of these sell microtakaful products. While many of the companies have microtakaful products planned in the pipeline, not many have officially registered their products with the OJK.

Allianz has been selling takaful credit life in partnership with MFIs.

Adira Insurance has a Syariah Dengue Fever Product

Bumiputera offers a Syariah-compliant credit life product. They are also partnering with Asuransi Syariah Keluarga Indonesia (ASyKi), a newly established microtakaful broker, to provide a motorcycle protection product. While not necessarily micro according to the Micro Insurance Grand Design, Bumitputera has also recently launched a new investment linked Syariah product for as little as IDR 200,000 per month.

BRIngin Life offers both group and individual microtakaful products, but has not really branded them as micro.

Indonesia’s experience with offering of microtakaful has shown encouraging signs. Testimony from the PT Asuransi Allianz Life Indonesia (takaful window) for example showed a portfolio of 50 percent microinsurance and 50 percent microtakaful, and maintained a consistent profit margin of 3 percent per year for the last 3 years (2011-2013).

PT Asuransi Tri Pakarta, also with takaful window, has a large spread of branch offices in small cities to cater to microtakaful customers. Tri Pakarta has declared that as much as 20 percent of income was generated from microtakaful business.

While there are companies that seem to be proactive in microtakaful product development, still other companies prefer to wait for the appropriate regulations before entering the market.

The willingness to participate in the market, however, seems to be affected by concerns over the possibility of the phasing out of takaful windows in 2014 as initially raised by the Indonesian government. Indications, however, are towards a later period if the

13

windows are indeed to be phased out. One potential impact of this phasing out is that those offering takaful products through windows will be forced to operate as full-fledged takaful providers, even though they might not be organizationally equipped and poor performance might lead to failure.

6.2 Microtakaful distribution channels

Only a few of the existing insurance agents, brokers, microfinance institutions and cooperatives are documented as microtakaful distribution channels. The exact proportion of the 151 insurance brokers and 25 company-agents in Indonesia that currently offer microtakaful is unclear. However, some few documented offering of microtakaful has shown encouraging signs.

The BMT Sidogiri set up of ASyKi (microtakaful broker) services are provided more efficiently and their cooperative (ta’awuni) concept of microtakaful has reached out to more than 14,000 small business owners and 400,000 members through their credit and savings scheme. ASyKi is working towards collaborating with companies with a “micro character” and creating value for consumers through efficient claims payment services. ASyKi management believes that the company can respond to claims under IDR 20 million within 1-2 days, and claims up to IDR 70 million within a week. Both of ASyKi’s current products are being offered through scratch-off vouchers that can be activated by a mobile phone text message.

The Pawnshop (Pergaidaian) owner’s experience also indicates positive growth of microtakaful bundled with pawned products. According to the owners, microtakaful is easy to market, well understood by the customers (contrary to findings from the FGDs), distinguishable from conventional ones, delivery is kept simple which handling cost is low.

Non-government organizations have played a crucial role in introducing and expanding the distribution of microtakaful to microfinance institutions. A well-documented success story is that of Peramu, a local NGO, which organized the microtakaful-focused working group TAKMIN to pilot initiatives in 2006 with the Islamic cooperative, UPK Ikhtiar in Bogor. TAKMIN is not an insurance broker, but served a similar capacity to link the company Family Takaful of Indonesia with a network of MFIs, including LKMs, BMTs and Islamic rural banks. This linkage resulted in 43 partnerships. Their alliance had borne fruit with more than 100,000 members and has reaped with contributions reaping a contribution of IDR 150 million per month. The bond with the cooperative members generally has been strong and to retain membership, each receives 10 percent share of the cooperative. Most of the contributions (premiums) are deducted directly from members’ subscription and in the words of their members “tabungan tidak dirasa” (the deduction and fund build-up is not felt).

While the Grand Design for Microinsurance specifically mentions MFIs as one of the main distribution channels of microtakaful, their legality in distribution seems to be interpreted differently in different regions in the country. Clarifying the understanding of the legal implications and guiding the potential distribution channels calls for action from OJK.

Among commercial insurance companies, Allianz has taken the lead in tapping MFIs for microtakaful distribution. Other companies, such as AIG, Astra Buana, Sun Life, Prudential and Jaya Proteksi Takaful are also beginning to move towards selling microtakaful through MFIs, IMFIs, and cooperatives.

In the Islamic cooperative sector, BMTs are the leading Islamic cooperatives acting as microtakaful distribution channels. BMT Sidogiri, the largest Islamic cooperative in the country with 400,000 members, offers microtakaful by bundling it with their other financial products. BTM, a collection of 332 cooperatives, also offers microtakaful through a variety of partnership modes.

As in other countries, mobile phone technology is being considered as a potential microtakaful distribution c hannel in Indonesia. Communications company Telkomsel has already explored the market by offering a short-term personal accident

14

takaful product called Takaful Safari that can be purchased through SMS. A similar approach could be adopted for microtakaful in the future.

The effective use of mobile phones as a microtakaful distribution platform, however, will rely on the resolution of some identified challenges. For example, air time deduction is not allowed by current regulations. Moreover, mobile money is still not a feasible option for the collection of premiums due to its low usage.

Retail spaces are also viewed as potential distribution channels, but some challenges exist:

The stores are not allowed to promote the insurance product unless it is one of the top ten products sold or if there is a special promotion.

Giving a commission to the stores for selling the product is not allowed. Competitions between stores for a prize may be used, but is not believed to be effective.

Marketing costs will be expensive. While the costs can be shared with the insurance company, it is an investment deemed too costly.

The minimart personnel are not fully knowledgeable about the product and are not capable to explain properly to customers.

Data entry for registering the product takes too long.

Connection to the internet across Indonesia is still not stable. The instability could affect the Internet-linked registration system.

The Islamic Council of Indonesia (MUI) has recently been reinvigorating the religious practices in the country, requesting Muslim citizens to prioritize and choose Shariah compliant entities, products and services, wherever possible. Hence, the preference should be for Islamic banks and halal minimarts, as an example. With this revival and the growth of crucial channels as BMTs, the future seems to hold great opportunities for microtakaful distribution channels.

6.3 Partnership arrangements

The largest distribution channel for Takaful motor in Indonesia is through multi-finance companies. Although this is not termed micro, almost everyone in the FGDs and interviews mentioned this because most low-income Muslims in Indonesia have purchased motorcycles with credit. Banks and direct selling to bank members through telemarketing is also practiced.

During the launching of the Microinsurance Grand Design, many organizations signed an MoU with the industry. Those participating in the informal agreement include the Indonesian Post Office, PNM (Permodalan Nasional Madani) which includes both MFIs and IMFIs, Pawnshops, Bank BNI, Bank BTN, Bank BRI, Bank Mandiri, and Indomaret. The strong role of cooperatives and the MFIs and IMFIs in providing financing for business and assets, rural banks and also state banks are seen as the best outlets for microtakaful in Indonesia. A variety of channels have been identified and practiced also in other countries. For a comparison, see Table 5.

Probably the most common practice for microtakaful is that of partnering with MFIs & IMFIs (partner-agent model).The benefits of this arrangement are twofold. First, the MFI has proven to be a great distribution channel to gain access to the low-income segment. Second, MFIs undertake several tasks on behalf of the insurer such as marketing the microtakaful product, explaining it to MFI clients, and helping in claims processing. This saves the insurer a lot of time and money besides raising awareness on microtakaful.

Subsidies from Zakat funds have also played a role in partnership between Takaful providers and the low income segment. For example, when TAKMIN started its pilot project in 2006-2007, the first year’s credit life premiums for their pilot partner’s members were paid for by the Tazkia Zakat fund.

15

Partnerships among insurance companies, insurance companies with Takaful provider, and Takaful provider with Takaful Broker (e.g. ASyKi) exist. This partnership models has proven to be the most useful, given the vast low income population of Indonesia and the wide outreach.

Given the landscape of microtakaful in Indonesia, the providers have to deal with high distribution and acquisition costs due to the inaccessibility of potential customers. Penetrating the rural market has obvious obstacles, but reaching the urban customers is also not easy due to the lack of infrastructure. In both cases, their lack of awareness and understanding of microtakaful, the shortage of facilitating services and capacity gaps will impede acquisition and may contribute to attrition. Therefore, it seems in line with this reasoning, the best option available to enable this industry to take off despite various setbacks is to create partnerships with organizations that are already available and in which the market is already familiar with.

Based on experiences and the remarks learned from various industry stakeholders such as the BMT Sidogiri, NGO TAKMIN, the Takaful Broker ASyKi as well as the current microtakaful provider providers (Allianz and etc.), it seems the best would be to create partnerships with existing entities in which the market are already in relationship with potential microtakaful clients or subscribers. This will automatically provide the industry with a database to promote their products. Besides providing the database for potential clients, the cooperatives (LKS, LKM or MFIs and IMFIs) can be the marketing arm for the microtakaful providers, in return saving them costs, be their information disseminator (provide training and brochures etc.) creating microtakaful awareness and in the long run, enhancing their financial and takaful literacy. The acquisition cost (of clients) is borne by the microtakaful partner while the administrative and other costs will be borne by the microtakaful provider. This relationship will facilitate and at the same time speed up the process of formalizing the current arrangements.

16

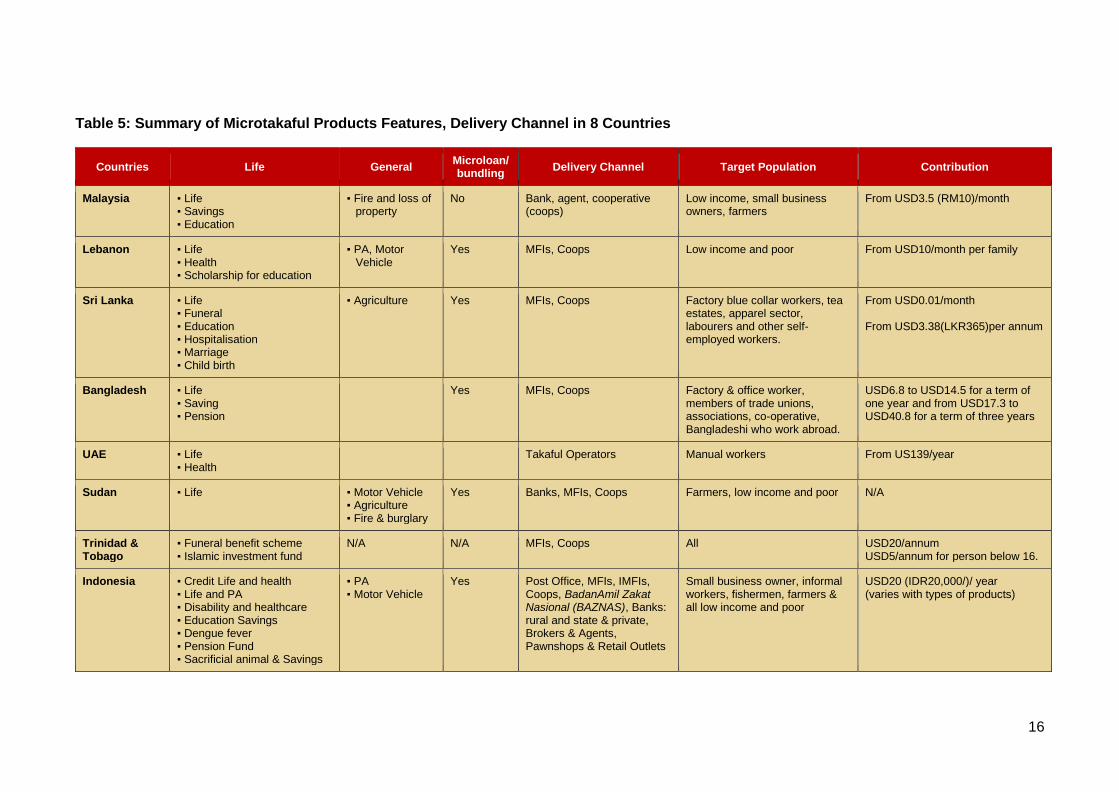

Table 5: Summary of Microtakaful Products Features, Delivery Channel in 8 Countries

Countries Life General Microloan/ bundling

Delivery Channel Target Population Contribution

Malaysia ▪ Life ▪ Savings ▪ Education

▪ Fire and loss of property

No Bank, agent, cooperative (coops)

Low income, small business owners, farmers

From USD3.5 (RM10)/month

Lebanon ▪ Life ▪ Health ▪ Scholarship for education

▪ PA, Motor Vehicle

Yes MFIs, Coops Low income and poor From USD10/month per family

Sri Lanka ▪ Life ▪ Funeral ▪ Education ▪ Hospitalisation ▪ Marriage ▪ Child birth

▪ Agriculture Yes MFIs, Coops Factory blue collar workers, tea estates, apparel sector, labourers and other self-employed workers.

From USD0.01/month From USD3.38(LKR365)per annum

Bangladesh ▪ Life ▪ Saving ▪ Pension

Yes MFIs, Coops Factory & office worker, members of trade unions, associations, co-operative, Bangladeshi who work abroad.

USD6.8 to USD14.5 for a term of one year and from USD17.3 to USD40.8 for a term of three years

UAE ▪ Life ▪ Health

Takaful Operators Manual workers From US139/year

Sudan ▪ Life ▪ Motor Vehicle ▪ Agriculture ▪ Fire & burglary

Yes Banks, MFIs, Coops Farmers, low income and poor N/A

Trinidad & Tobago

▪ Funeral benefit scheme ▪ Islamic investment fund

N/A N/A MFIs, Coops All USD20/annum USD5/annum for person below 16.

Indonesia ▪ Credit Life and health ▪ Life and PA ▪ Disability and healthcare ▪ Education Savings ▪ Dengue fever ▪ Pension Fund ▪ Sacrificial animal & Savings

▪ PA ▪ Motor Vehicle

Yes Post Office, MFIs, IMFIs, Coops, BadanAmil Zakat Nasional (BAZNAS), Banks: rural and state & private, Brokers & Agents, Pawnshops & Retail Outlets

Small business owner, informal workers, fishermen, farmers & all low income and poor

USD20 (IDR20,000/)/ year (varies with types of products)

17

7 MICROTAKAFUL PRODUCTS: FEATURES AND ISSUES

At present, there are some 14 microtakaful products in the market which range from credit life, personal accident, motor, disability, education, some medical and hospitalization to dengue takaful products. The market survey participants expressly mentioned their risk priorities are those pertaining to illness, death (bundled with microloans), accident, education and business risk due to loss of assets (motorcycles and other properties). Most of the products currently offered are those demanded by the market with few exceptions, such as Tabung Qurban designed specifically to pay for a goat/cow for sacrificial purposes and Demam Berdarah Syariah (Dengue fever). While Table 5 presents a selection of microtakaful products offered in 8 different countries, Table 6 provides an overview of the products currently available in Indonesia.

The sums insured are small (Tabung Khairat) which refers to mainly funeral benefits with some cash assistance, ranging between IDR 1 to 5 million [USD 103 to USD 516]) and the perils covered are standard, e.g. life microtakaful, natural death, disability due to accidents (>IDR 5 – 7.5 million [USD 516 to USD 773]). Depending on the type of coverage and frequency of payment, contributions are equally small ranging from IDR 20,000 to IDR 200,000 month/year (USD 1.88 / USD 18.8).

Microtakaful products offered by the industry are registered with the regulators. However, those offered under the cooperatives, e.g. BMT Sidogiri, are not under the purview of the regulator since the cooperatives are regulated by a different government agency.

18

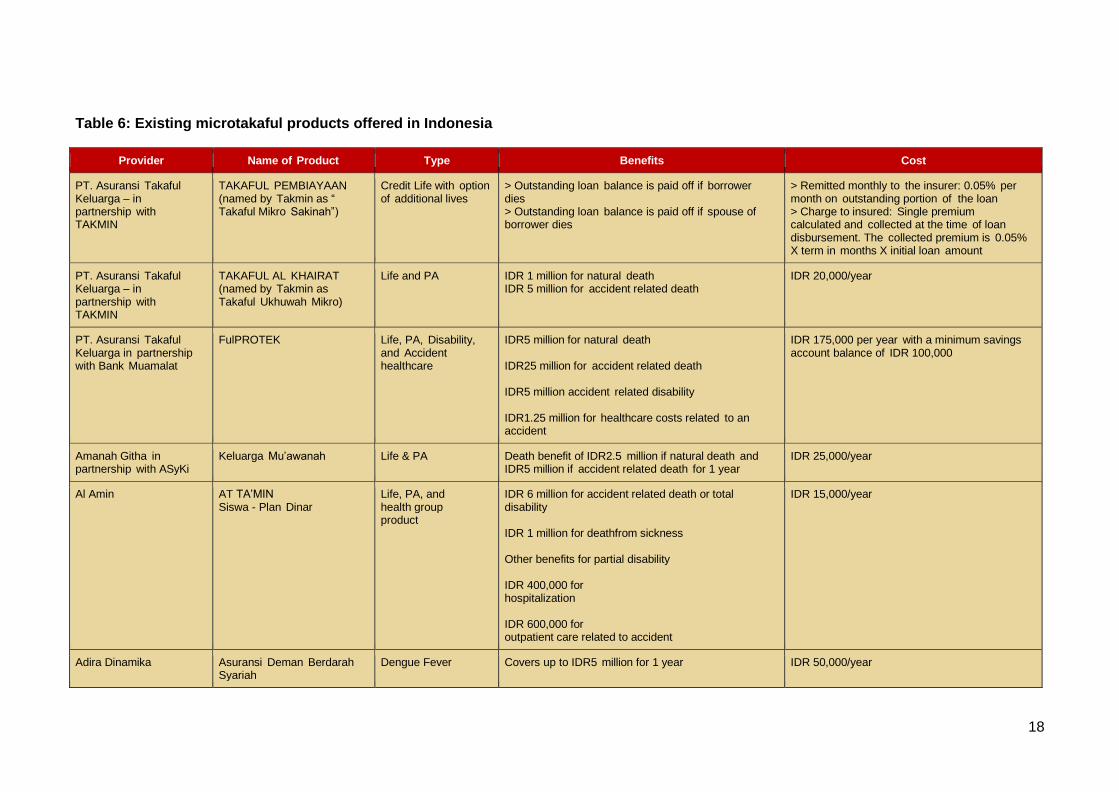

Table 6: Existing microtakaful products offered in Indonesia

Provider Name of Product Type Benefits Cost

PT. Asuransi Takaful Keluarga – in partnership with TAKMIN

TAKAFUL PEMBIAYAAN (named by Takmin as “ Takaful Mikro Sakinah”)

Credit Life with option of additional lives

> Outstanding loan balance is paid off if borrower dies > Outstanding loan balance is paid off if spouse of borrower dies

> Remitted monthly to the insurer: 0.05% per month on outstanding portion of the loan > Charge to insured: Single premium calculated and collected at the time of loan disbursement. The collected premium is 0.05% X term in months X initial loan amount

PT. Asuransi Takaful Keluarga – in partnership with TAKMIN

TAKAFUL AL KHAIRAT (named by Takmin as Takaful Ukhuwah Mikro)

Life and PA IDR 1 million for natural death IDR 5 million for accident related death

IDR 20,000/year

PT. Asuransi Takaful Keluarga in partnership with Bank Muamalat

FulPROTEK Life, PA, Disability, and Accident healthcare

IDR5 million for natural death IDR25 million for accident related death IDR5 million accident related disability IDR1.25 million for healthcare costs related to an accident

IDR 175,000 per year with a minimum savings account balance of IDR 100,000

Amanah Githa in partnership with ASyKi

Keluarga Mu’awanah Life & PA Death benefit of IDR2.5 million if natural death and IDR5 million if accident related death for 1 year

IDR 25,000/year

Al Amin AT TA’MIN Siswa - Plan Dinar

Life, PA, and health group product

IDR 6 million for accident related death or total disability IDR 1 million for deathfrom sickness Other benefits for partial disability IDR 400,000 for hospitalization IDR 600,000 for outpatient care related to accident

IDR 15,000/year

Adira Dinamika Asuransi Deman Berdarah Syariah

Dengue Fever Covers up to IDR5 million for 1 year IDR 50,000/year

19

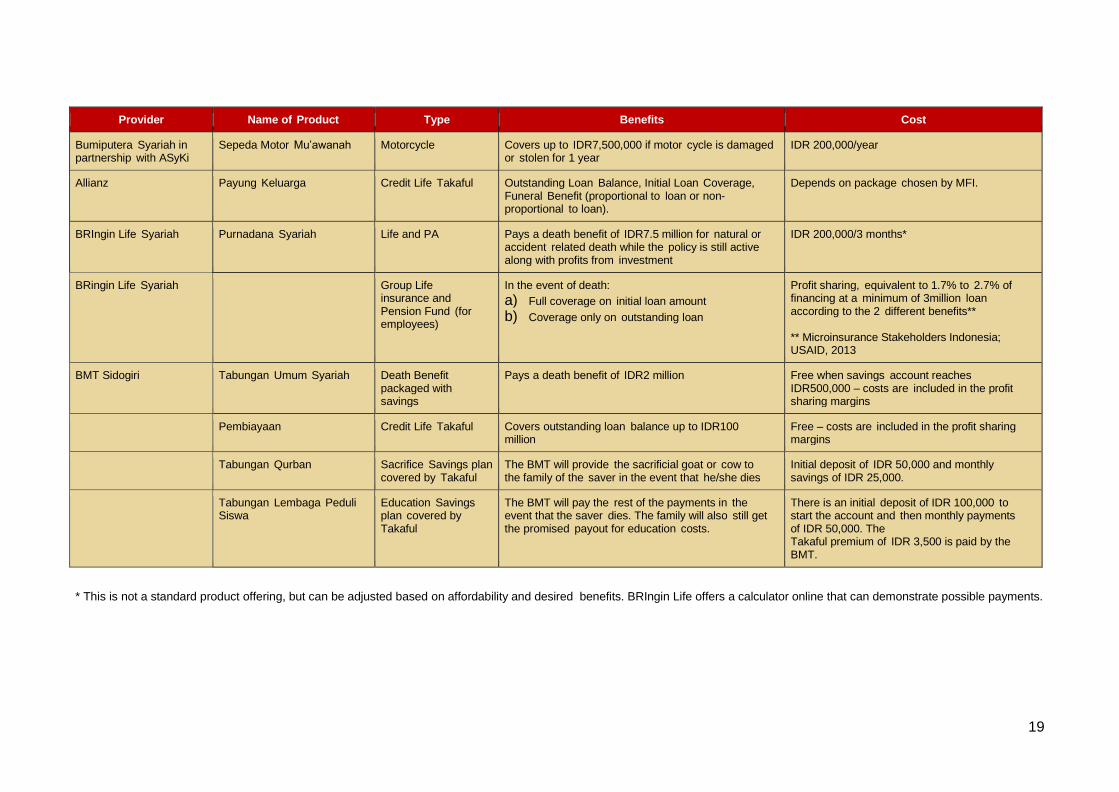

Provider Name of Product Type Benefits Cost

Bumiputera Syariah in partnership with ASyKi

Sepeda Motor Mu’awanah Motorcycle Covers up to IDR7,500,000 if motor cycle is damaged or stolen for 1 year

IDR 200,000/year

Allianz Payung Keluarga Credit Life Takaful Outstanding Loan Balance, Initial Loan Coverage, Funeral Benefit (proportional to loan or non-proportional to loan).

Depends on package chosen by MFI.

BRIngin Life Syariah Purnadana Syariah Life and PA Pays a death benefit of IDR7.5 million for natural or accident related death while the policy is still active along with profits from investment

IDR 200,000/3 months*

BRingin Life Syariah Group Life insurance and Pension Fund (for employees)

In the event of death:

a) Full coverage on initial loan amount

b) Coverage only on outstanding loan

Profit sharing, equivalent to 1.7% to 2.7% of financing at a minimum of 3million loan according to the 2 different benefits** ** Microinsurance Stakeholders Indonesia; USAID, 2013

BMT Sidogiri

Tabungan Umum Syariah Death Benefit packaged with savings

Pays a death benefit of IDR2 million Free when savings account reaches IDR500,000 – costs are included in the profit sharing margins

Pembiayaan Credit Life Takaful Covers outstanding loan balance up to IDR100 million

Free – costs are included in the profit sharing margins

Tabungan Qurban Sacrifice Savings plan covered by Takaful

The BMT will provide the sacrificial goat or cow to the family of the saver in the event that he/she dies

Initial deposit of IDR 50,000 and monthly savings of IDR 25,000.

Tabungan Lembaga Peduli Siswa

Education Savings plan covered by Takaful

The BMT will pay the rest of the payments in the event that the saver dies. The family will also still get the promised payout for education costs.

There is an initial deposit of IDR 100,000 to start the account and then monthly payments of IDR 50,000. The Takaful premium of IDR 3,500 is paid by the BMT.

* This is not a standard product offering, but can be adjusted based on affordability and desired benefits. BRIngin Life offers a calculator online that can demonstrate possible payments.

20

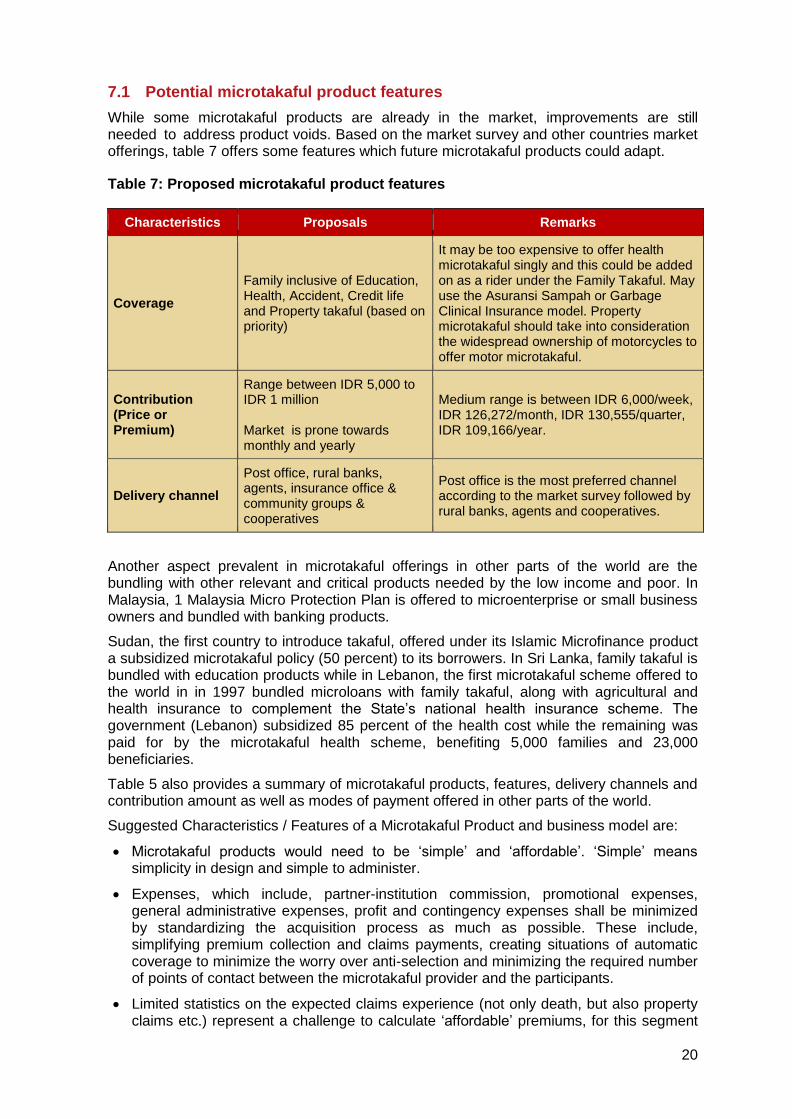

7.1 Potential microtakaful product features

While some microtakaful products are already in the market, improvements are still needed to address product voids. Based on the market survey and other countries market offerings, table 7 offers some features which future microtakaful products could adapt.

Table 7: Proposed microtakaful product features

Characteristics Proposals Remarks

Coverage

Family inclusive of Education, Health, Accident, Credit life and Property takaful (based on priority)

It may be too expensive to offer health microtakaful singly and this could be added on as a rider under the Family Takaful. May use the Asuransi Sampah or Garbage Clinical Insurance model. Property microtakaful should take into consideration the widespread ownership of motorcycles to offer motor microtakaful.

Contribution (Price or Premium)

Range between IDR 5,000 to IDR 1 million Market is prone towards monthly and yearly

Medium range is between IDR 6,000/week, IDR 126,272/month, IDR 130,555/quarter, IDR 109,166/year.

Delivery channel

Post office, rural banks, agents, insurance office & community groups & cooperatives

Post office is the most preferred channel according to the market survey followed by rural banks, agents and cooperatives.

Another aspect prevalent in microtakaful offerings in other parts of the world are the bundling with other relevant and critical products needed by the low income and poor. In Malaysia, 1 Malaysia Micro Protection Plan is offered to microenterprise or small business owners and bundled with banking products.

Sudan, the first country to introduce takaful, offered under its Islamic Microfinance product a subsidized microtakaful policy (50 percent) to its borrowers. In Sri Lanka, family takaful is bundled with education products while in Lebanon, the first microtakaful scheme offered to the world in in 1997 bundled microloans with family takaful, along with agricultural and health insurance to complement the State’s national health insurance scheme. The government (Lebanon) subsidized 85 percent of the health cost while the remaining was paid for by the microtakaful health scheme, benefiting 5,000 families and 23,000 beneficiaries.

Table 5 also provides a summary of microtakaful products, features, delivery channels and contribution amount as well as modes of payment offered in other parts of the world.

Suggested Characteristics / Features of a Microtakaful Product and business model are:

Microtakaful products would need to be ‘simple’ and ‘affordable’. ‘Simple’ means simplicity in design and simple to administer.

Expenses, which include, partner-institution commission, promotional expenses, general administrative expenses, profit and contingency expenses shall be minimized by standardizing the acquisition process as much as possible. These include, simplifying premium collection and claims payments, creating situations of automatic coverage to minimize the worry over anti-selection and minimizing the required number of points of contact between the microtakaful provider and the participants.

Limited statistics on the expected claims experience (not only death, but also property claims etc.) represent a challenge to calculate ‘affordable’ premiums, for this segment

21

of the market it is difficult to establish underwriting guidelines, but could be standardized using other countries experience.

Profit margins shall be built in but it should be allowed that any surplus to be distributed back to the participants in one way or another.

22

8 THE REGULATORY ENVIRONMENT FOR MICROTAKAFUL MARKET DEVELOPMENT

The Otoritas Jasa Keuangan (OJK) or Financial Services Authority of Indonesia is the government body that regulates and supervises the business of both conventional and Shariah insurance. There is no specific regulation yet for microtakaful, thus the business entity is regulated and supervised at the moment through the existing 18 PMK (Finance Ministry Rules or Peraturan Menteri Keuangan) and OJK Regulations (POJK) or OJK Circular Letters (SEOJK) binding for all Shariah insurance or Asuransi Shariah business. The current regulations defined that risk insurers in microinsurance are insurance companies, whereas microtakaful are takaful providers or insurance companies which operate all or part of its businesses in compliance with Shariah principles. Insurance and/or takaful companies can cooperate to produce microinsurance and or microtakaful products that provide protection over a combination of various risks in the form of ‘joint insurance/takaful product’. All regulated providers must clearly describe in the policy contracts which insurance or takaful companies act as the insurer, an address for claim submission and complaints, and information of the company that accepts premium from the customers. Insurance and takaful companies must evaluate microtakaful performance regularly and OJK will resolve guidance on microtakaful performance monitoring.

To be aligned to international practice, the Islamic Financial Services Board (IFSB) standards may also be consulted by OJK on commonality of issues pertaining to microtakaful business. These will include the definition of microtakaful, its characteristics, the type of stakeholders involved, and the challenges faced by this sector (Kartina Mohd. Ariffin, April 2014).

The standards already established by the IFSB on takaful and soon to be enacted for microtakaful should be able to solve technical and religious issues which have been deliberated on and subscribed to by more than 40 countries (refer to Box 3).

Box 3: Takaful Standards

• Corporate Governance not related to financial goals (shareholders) ONLY but to include stakeholders (suppliers, employees, consumers, MFIs, IMFIs, society); Shariah Governance to Shariah compliancy

• Prudential Requirements – microtakaful operations, multiple contractual relationship of Islamic finance transaction

• Business Conduct & Consumer Protection

• Operational & Reporting – accounting system could be guided by the AAOFI Standards

• Risk Management (systemic, market, liquidity, credit risks)

• Solvency – Shareholders’ Fund, Participants’ Risk Fund & Qard; tackling both the underwriting and claims settlement, reserves, retakaful, accounting, investment model, etc.

• Talent Development – various initiatives and measures need to be undertaken to create a pool of Shariah scholars and technical experts to drive the microtakaful industry

• Research – focus on applied Shariah research issues and to work with the support organizations to achieve a synergy where the regulators gain from experts output while institutions are engaged in providing the curriculum and training for these personnel

8.1 Prevailing regulatory issues

The development of the microtakaful market is consistent with the government’s Grand Design for Microinsurance, but specific regulatory issues need further elaboration and possible issuance of decrees.

Current regulatory practices on product registration are considered to be

23

conducive to the market, with the process of product registration made quicker and more efficient. Product evaluations by OJK are done on a quarterly basis and it is expected that once a product is registered, selling can already commence. While there are no specific decrees for the registration of microtakaful products, Decree No. 422/KMK.06/2003 on the Business Conduct of Insurance and Reinsurance Companies currently apply.

The absence of a specific regulation encouraging rural banks as microtakaful distribution channels is an issue needing further discussion. At present, the Bank of Indonesia only allows both conventional (BPR) and Islamic (BPRS) rural banks to participate in a reference business model, and providing their clients access to insurance can only be possible through partnership with an insurance company (Surat Edaran bank Indonesia Nomor 12/35/DPNP). However, no regulation exists either that prohibits them from selling insurance directly to their clients.

The OJK has clarified that the interpretation of the regulation on selling of insurance by banks is dependent on the regional authorities. This is still under discussion by authorities though no new regulation is being planned. As of January 2014, Indonesia has 163 Islamic banks with 402 branch offices and 1,636 conventional banks with 4,697 branch offices.

The regulatory environment also needs to consider what is called the “Shariah risk”, whereby existing insurance models and product structures could later be considered as no longer compliant with Shariah laws. This risk has implications on the competitiveness of products and services in the future, whereby, if some are deemed no longer compliant and are subsequently eliminated, only a few choices would be left for consumers which could dangerously lead to poor product quality and service.

Pawnshops, with its major potential for microtakaful distribution, are exposed to this Shariah risk, having only 637 Shariah compliant entities out of the total 4,000. Should the laws become more restrictive in the future and allow for only Shariah-compliant pawnshops to offer microtakaful, a significant number of channels will be lost. Minimarts are also exposed to this risk as these sell non-halal commodities, such as alcohol. Post offices, however, are safe because they do not sell anything non-halal.

No data currently exists to document the volume of informal risk sharing / takaful schemes being operated. Neither the Ministry of Cooperatives nor the OJK gathers information on this. It has been documented that some MFIs deduct 1% of member loans and allocates the money into a risk fund which then serves to repay a deceased member’s loan.

OJK has purposefully not made any restrictions on informal schemes to allow innovation and development within the cooperative segment. In the Grand Design for Microinsurance, informal schemes are not mentioned but it is understood from discussions that the regulatory body will oversee only those that sell and market registered microinsurance products. The aim is to prevent obstacles for cooperatives who can manage insurance/takaful programs on their own, leaving room for the growth of informal takaful schemes as ‘Takaful in its true essence is a cooperative’.

Other than regulatory matters, the Islamic finance and takaful industry suffers from lack of consistency in the interpretation of the Shariah rules.2 There are four main schools of Islamic jurisprudence and scholars may take a different view as to the compliance of an Islamic product. Although divergence of views can be considered as strength as it allows innovation when developing new products, it does not, however, provide a solution to the issue.

2 This issue was raised after the Microtakaful conference. For details, visit www.inclusiveinsuranceasia.com

24

Indonesia a vast nation with 27 provinces where Shariah rules are interpreted based on regional authority which may pose a problem to OJK regulation and supervision. OJK, therefore, is seeking for standardization for an enabling regulatory framework to survive the test of time. However, if rules are passed by an Act of Parliament then regional authorities must abide by the aspiration and prioritize based on national interest.

8.2 Considerations for the regulatory framework

The development of microtakaful market involves more than the development of new products and new institutions to deliver them. The government needs to establish the rules under which takaful companies and its intermediaries can operate in this market, and once these rules are set, to supervise these companies to make sure that they comply. The government may also need to regulate meso-level actors like actuaries or claims adjusters. They may also play a role in enhancing consumer protection through the funding of an ombudsman. Currently, Indonesia through OJK has equipped itself with a framework to regulate Microinsurance through its recently launched Microinsurance Grand Design. Microtakaful with its Shariah compliancy requirements needs to be enhanced with the appointment of a Shariah Advisory Council to ensure the Islamic laws are followed.

To preserve the financial stability of the takaful fund and to maintain public confidence, prudent undertaking on the part of the regulators requires the Takaful Company to adhere to professional ethics and business code of conduct to observe high standards of integrity, honesty and fair dealing. Hence an internal review mechanism must be in place and enforced compliance with the code, as in the establishment of an appropriate governance structure representing both the interest of the stakeholders, namely the shareholders and the participants. The Governance Committee can be formed from members of the Shariah Committee of the Takaful Company, an actuary, and an independent non-executive director from the Board of Directors appointed within the organization should be able to serve this purpose [Principle 2.1, Sub section 44-54 of IFSB Standards]. Indonesia’s regulation also has to give effect on the allowance for the accounting standards to take into account the contribution (premium) as a donation, a departure from the insurance accounting standards.

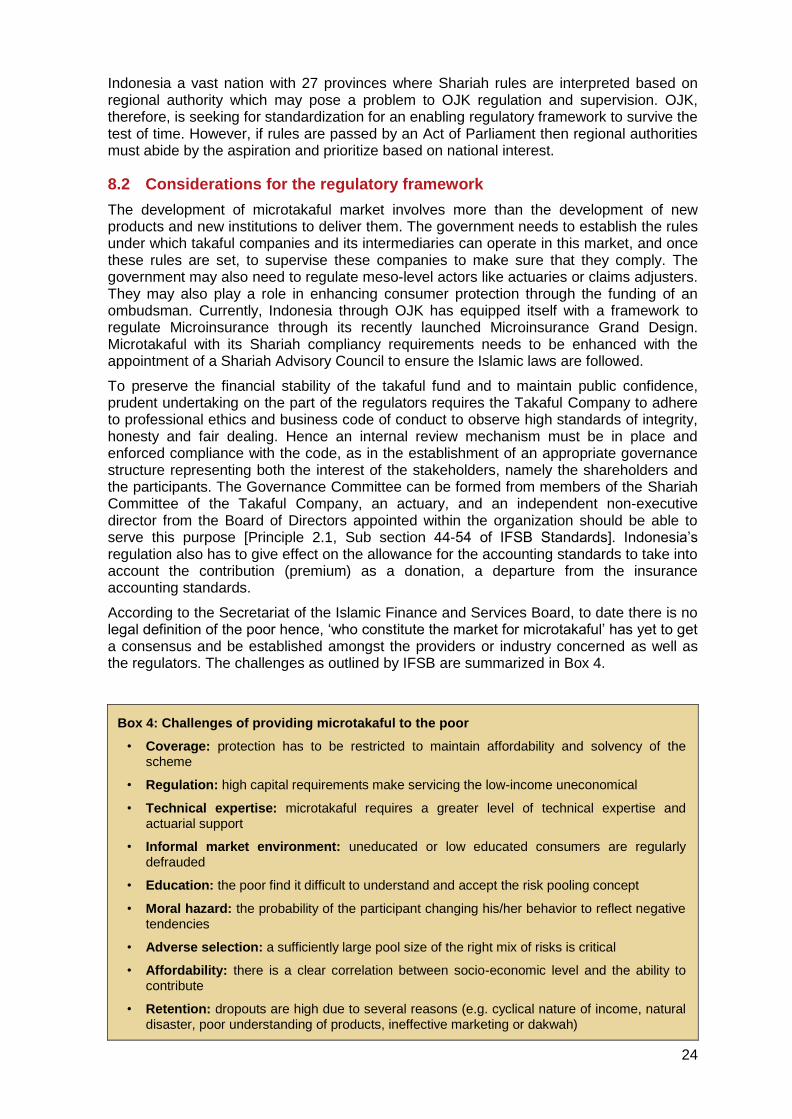

According to the Secretariat of the Islamic Finance and Services Board, to date there is no legal definition of the poor hence, ‘who constitute the market for microtakaful’ has yet to get a consensus and be established amongst the providers or industry concerned as well as the regulators. The challenges as outlined by IFSB are summarized in Box 4.

Box 4: Challenges of providing microtakaful to the poor

• Coverage: protection has to be restricted to maintain affordability and solvency of the scheme

• Regulation: high capital requirements make servicing the low-income uneconomical

• Technical expertise: microtakaful requires a greater level of technical expertise and actuarial support

• Informal market environment: uneducated or low educated consumers are regularly defrauded

• Education: the poor find it difficult to understand and accept the risk pooling concept

• Moral hazard: the probability of the participant changing his/her behavior to reflect negative tendencies

• Adverse selection: a sufficiently large pool size of the right mix of risks is critical

• Affordability: there is a clear correlation between socio-economic level and the ability to contribute

• Retention: dropouts are high due to several reasons (e.g. cyclical nature of income, natural disaster, poor understanding of products, ineffective marketing or dakwah)

25

• Flexibility: it is important to verify claims and process payments speedily

• Sustainability: in the initial years, most takaful providers after assertive consumer awareness and education promotional programs, finds that the market does not take up what is being made available due to consumer dissatisfaction, apathy or ignorance.

26

8.3 Industry perspectives on regulatory improvement needs

The following list is the suggestions gathered during the survey from leaders of the insurance industry in Indonesia.

i. Mandatory selling of insurance for low-income sector. All insurance companies should be required to sell a certain percentage of their portfolio as microinsurance. A portion of this would then be for microtakaful. For companies selling takaful, one out of ten of insurance policies sold should be mandated as a takaful product. Mandating insurance business, following the Indian industry experience, could be an approach to allow microtakaful to gain solid ground before it could transition into a voluntary business component. Of the total responses received from the market survey only 2 companies suggested this approach, which in itself reflected the sentiment of the industry which should be a voluntary business transaction.

ii. OJK should lead financial literacy. Industry representatives believe that the regulator should lead awareness-raising and promotions for insurance/takaful literacy. The regulator is perceived to be in the best position to address the challenge of socialization. Through the establishment of a government promotional agency called the Economic Shariah Committee Center, OJK has done a substantial part of educating the public on microtakaful, including: explaining OJK’s role as the regulator, informing the masses through its involvement in takaful with GRES! and other activities, providing a dedicated website for microtakaful, and promoting microtakaful through TV and other media.

iii. Comprehensive regulatory guidance on defining microinsurance should be developed. While the definition of microinsurance has been loosely defined based on the premium ceiling of IDR 50,000 and sum assured ceiling of IDR 50,000,000, industry representatives expressed the need still for additional criteria as guidance for product registration. Some products in their portfolio might be priced cheaply, but are not designed for the low-income groups. It would seem inaccurate to register these as microinsurance products. A more comprehensive set of criteria would also apparently help insurance providers differentiate between their activities for corporate social responsibilities and for microinsurance portfolio development.

iv. Future regulations on microtakaful should still be conducive to products designed and offered prior to the issuance of these regulations. Some insurance companies claim to have started offering microinsurance products even prior to the encouragement of the OJK. But with the heightened focus in its promotion, providers fear that the existing products will need to be redesigned or discouraged altogether. The industry representatives hope that any future microinsurance or microtakaful regulations will not deter products already on offer to the low-income sector. The OJK using the IFSB standards should be able to resolve this issue in the near future, partly and also with the establishment of a Shariah Committee and Shariah Advisory Council that will be able to provide advice and guidance to ensure Shariah compliancy.

v. Regulation should support the possible participation of banks as microtakaful distribution channels. As there are still no clear regulations on the participation of banks in insurance selling, industry representatives believe that issuing a regulation to permit banks to act as distribution channels will push market growth. Some expressed that the Islamic banking industry should be required to offer microtakaful products, especially if a standardized product is to be provided by AASI. To date only BPR and BPRS were given the permits to offer microtakaful products through their channel network. However, taking from the Malaysian experience, the regulator allowed only Islamic banks to offer takaful products while microtakaful products could also be promoted via conventional banks.

27

8.4 Financial literacy and consumer protection

According to the country’s insurance law (UU No. 21 Tahun 2011), the OJK has the responsibility and authority to conduct activities to educate and protect consumers regarding financial services, including financial and insurance literacy initiatives.

As provided for in the Grand Design for Microinsurance, and in line with the aforementioned insurance law, the OJK will be promoting microinsurance, including microtakaful, through the following avenues:

Designation of October 17 of every year as Microinsurance Day

Proposal of the creation of a microinsurance education curriculum

Creation of microinsurance motto, logo and jingle for public promotion use

Creation of a microinsurance website

Establishment of a service center or hotline for microinsurance

While no regulation is necessary to implement financial literacy for microinsurance, working agreements have been signed with organizations such as Kementerian Pembangunan Daerah Tertinggal (KPDT), Badan Nasional Penempatan dan Perlindungan Tenaga Kerja Indonesia (BNP2TKI) and Technology University of Sumbawa (UTS) to jointly increase the level of financial literacy and consumer protection for microinsurance.

Insurance literacy initiatives specifically designed for takaful are yet to be implemented. However, current initiatives of the Insurance Council of Indonesia (DAI) to promote insurance in general offer the opportunity for future integration of takaful and microtakaful themes. Some of these initiatives include:

Insurance Goes to Campus are visits to institutions to educate college student about insurance. It also includes an e-learning component.

The Grand Design for Insurance Education plans for activities as road shows, insurance expositions, insurance literacy surveys, talent competitions, and establishment of information centers, among others.