Embed Size (px)

Citation preview

Published by

Indo – German Energy Programme

Green Energy Corridors

Market Design for an Electricity

System with higher share of RE

Energy Sources

Consortium Partners

Ernst & Young LLP, India

Fraunhofer IWES, Germany

University of Oldenburg, Germany

FICHTNER GmbH & Co. KG, Germany

Contents

1 Problem Statement 1

1.1 High Delivered Cost of RE Power 1

1.2 Burden on DISCOMs on Purchase of RE power 1

1.3 Deviation from RE Schedule 2

1.4 Non Uniform Distribution of RE potential 3

2 Current Indian power market 4

2.1 Introduction 4

2.2 Structure of Indian Electricity Market 5

2.3 Transactions in the Market 6

3 German Electricity Market 14

3.1 Regulatory Framework 14

3.2 Introductive example 15

3.3 Balancing groups 17

3.4 Market based balancing 18

3.4.1 Scheduling 19

3.4.2 Spot market 20

3.5 Product specifications 21

3.5.1 Day-ahead auctions 21

3.5.2 Orders 21

3.5.3 Price determination 24

3.5.4 Post trading period 24

3.5.5 15-min. intraday auction 25

3.5.6 Intraday continuous trading 25

3.6 Control energy or reserves for imbalances 27

3.6.1 Pricing, remuneration and settlement 27

3.7 Cross-border trading 28

3.8 Market coupling 30

3.8.1 Cross border capacity allocation 31

3.9 Network tariffs 32

3.10 Renewable Energies within the set-up of regulation and mechanisms 33

3.10.1 Funding and refinancing 33

3.10.2 Marketing of RE and conformity with balancing group concept 34

3.10.3 Impact on short-term markets and consequences 35

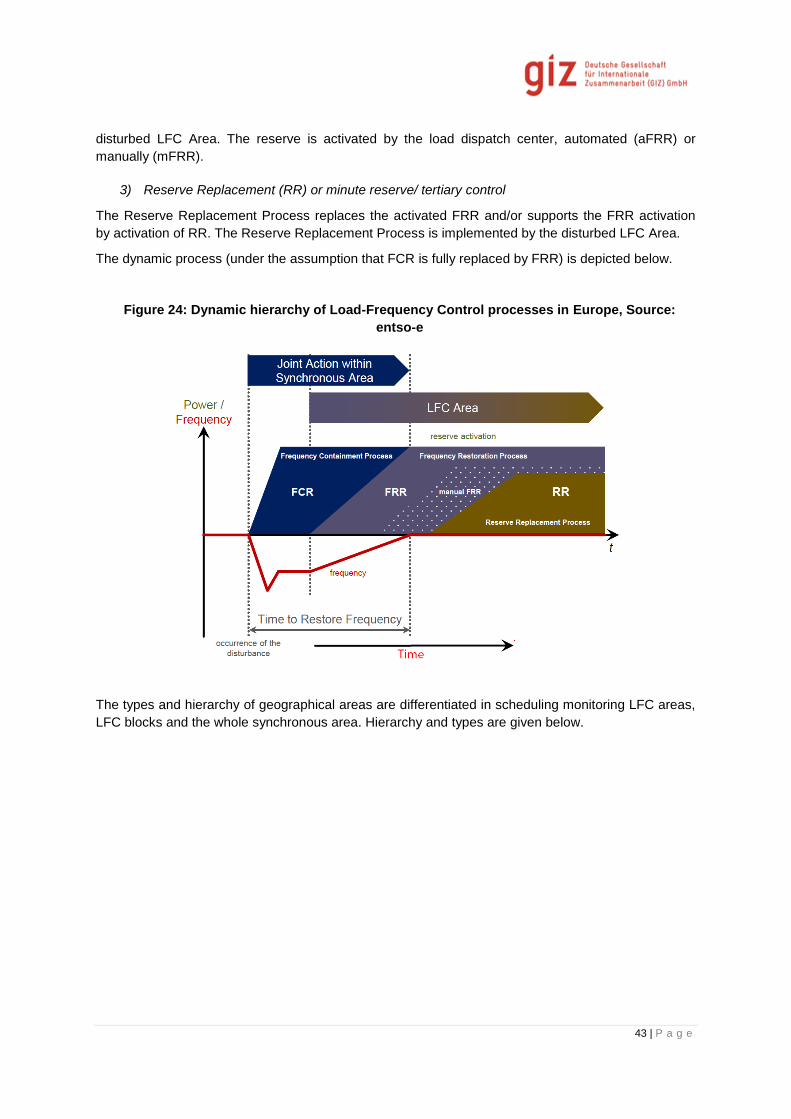

4 Ancillary Services (AS) 40

4.1 Development of joint operational procedures 41

4.2 Organizational Implementation of the Frequency Control 42

4.2.1 Control activities 42

4.2.2 Assessment of balancing needs and level of responsibility 45

4.3 Methodology of reserve dimensioning 53

4.3.1 Primary reserve 54

4.3.2 Secondary and minute reserve 55

4.4 Specification of reserves 58

4.4.1 Prequalification 58

4.4.2 Product specifications 59

4.4.3 Recommendation for the introduction of restoration reserve as ancillary

service 61

4.4.4 Implementation of grid control cooperation 62

4.5 Voltage control 64

4.5.1 Market design for voltage support 65

4.5.2 Examples of current approaches to contract voltage support in Europe 65

4.5.3 Voltage support by RES 66

4.6 Black start 67

4.7 RES capabilities to provide ancillary services 67

4.8 German Scenario 71

4.8.1 Primary control reserve 71

4.8.2 Secondary control reserve 71

4.8.3 Tertiary control reserve 71

4.8.4 Grid control cooperation 72

4.9 Status of ancillary services in India 73

4.9.1 Definition and Scope 73

4.9.2 CERC Draft Regulation on Ancillary Services Operation, May 2015 74

4.9.3 Petition on the inadequate response of FGMO, February 2015 74

5 Market Options 75

5.1 Market Models 75

5.2 Pricing Models 77

6 Balancing Group Concept 79

6.1 Formation of balancing groups 79

6.2 Balance Responsible Party 80

6.3 Cost of Ancillary Services and Reserves 80

6.4 Timeline of rollout 80

6.5 Participants and Roles 80

6.5.1 System Operators 80

6.5.2 BRPs 82

6.6 Demand Response in Balancing Groups 83

7 Transition to Proposed Market Design 85

7.1 Phase 1 86

7.1.1 Modifications to regulations related to Power Purchase Agreements 86

7.1.2 New Products in the market 87

7.1.3 Introduction of Generator only Balancing Groups & Reserve Products 87

7.1.4 Introduction of Generator Only Balancing Groups 88

7.1.5 Congestion Management 89

7.1.6 Flexible Generation 89

90

7.2 Phase 2 90

7.3 Required Legislative and Regulatory Changes 90

7.3.1 Introduction of Consumers in Balancing Groups 91

7.3.2 Introduction of Demand Side Products 91

7.3.3 Load Forecasting 91

7.3.4 Review of Balancing Group Regional Restrictions 91

7.3.5 Migration of PPAs 91

7.4 Phase 3 93

7.4.1 Modification of Products on PXs 93

7.4.2 Migration of PPAs 93

7.4.3 Review of RPO/REC 93

7.5 Proposed Market Design for India 95

7.5.1 Market Design 95

7.6 Deviation and mechanism of settlement 98

Management of Schedule Deviations due to RE 98

Remuneration to RE Generators and Aggregators 98

7.7 Control Reserves (Ancillary Services and Balancing) 99

7.7.1 Contracting of reserves 99

7.7.2 Scheduling of reserves 99

7.7.3 Activation of Reserves 100

7.7.4 Infrastructure for Deployment of Reserves 100

7.7.5 Payment to reserve service providers 101

7.7.6 Reserve service providers 101

7.7.7 Penalty for defaulting reserve providers 102

8 Roadmap and Summary of Recommendations 103

8.1 Immediate Steps – Over the next 5 years (Phase 1 of transition) 103

8.2 Steps to be taken after 5 years up to 10 years (Phase 2 of transition) 103

8.3 Steps to be taken after 10 years up to 15 years (Phase 3 of transition) 104

9 Bibliography 105

Annexure 1 110

Annexure 2 1

Annexure 3 7

Annexure 4 11

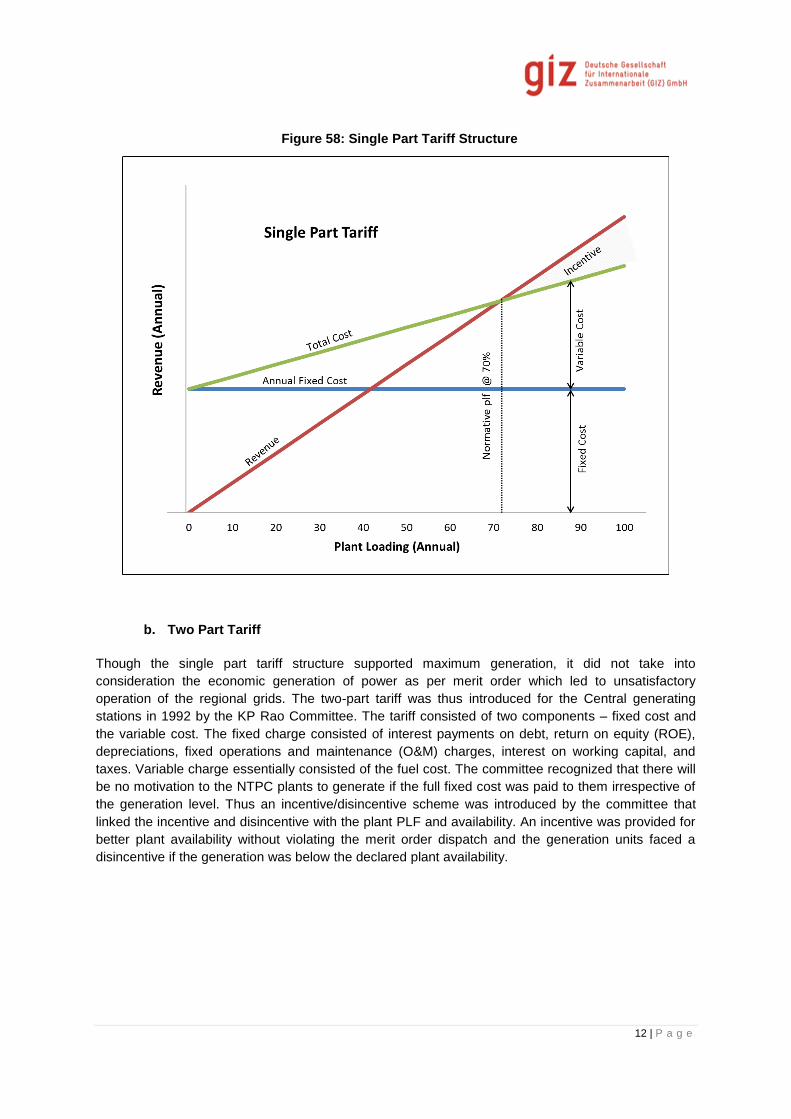

a. Single Part Tariff 11

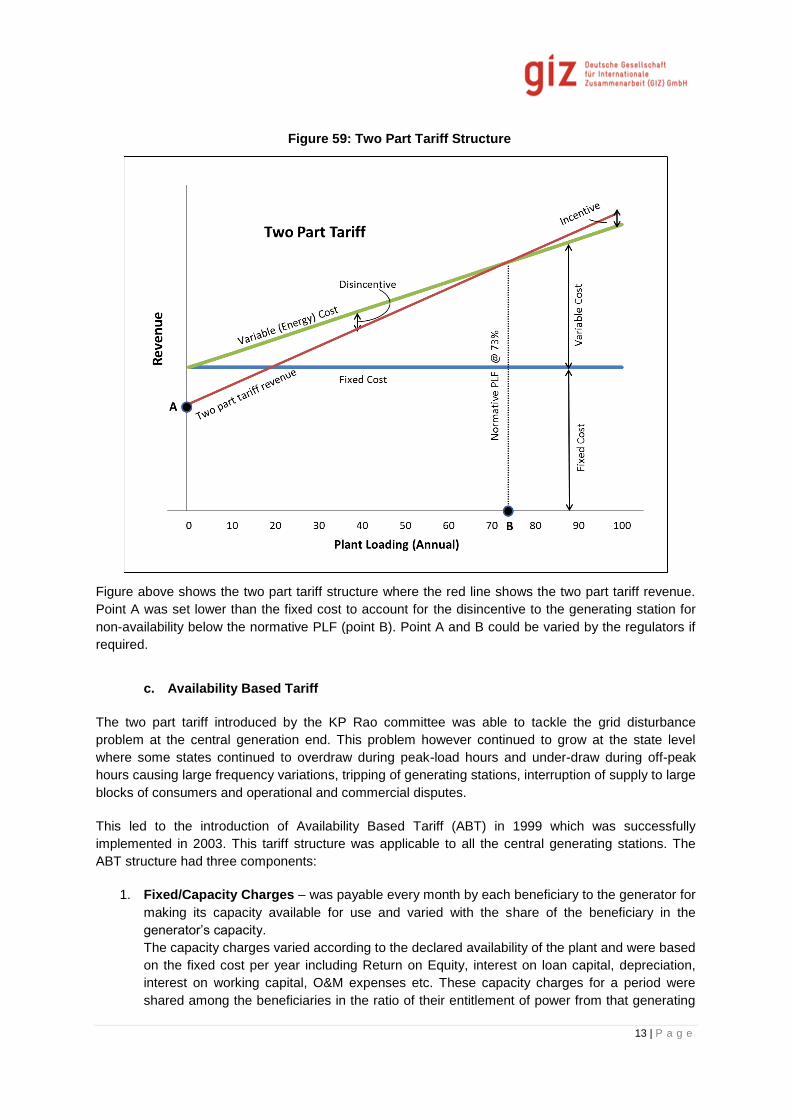

b. Two Part Tariff 12

c. Availability Based Tariff 13

List of Figures

Figure 1: Wind and Solar Generation Gujarat 2014 and 2022 (projected) ............................................. 2

Figure 2: Variation of Wind and Solar potential in India .......................................................................... 3

Figure 3: Segments of Indian Power Sector ........................................................................................... 4

Figure 4: Structure of Indian Power Market ............................................................................................ 5

Figure 5: Classification of Indian Power Market...................................................................................... 7

Figure 6: Transactions in Indian Power Market ...................................................................................... 8

Figure 7: Regulatory Transition of Indian Power Market ........................................................................ 9

Figure 8: Percentage Distribution of Contracts in the Market ................................................................. 9

Figure 9: Functioning of Day Ahead Markets ........................................................................................ 10

Figure 10: Timeline of trades on the IEX under 24 hour operations ..................................................... 11

Figure 11: German electricity markets. (Fraunhofer IWES based on (Judith et al. 2011)) ................... 14

Figure 12 Interaction of two BRPs and a TSO in a control zone regarding scheduling and imbalance

settlement .............................................................................................................................................. 16

Figure 13: Estimated marginal cost based merit-order for all German power plants ........................... 19

Figure 14: Share of trading volume of national EPEX SPOT market in annual national (EPEX SPOT

2014f) .................................................................................................................................................... 20

Figure 15: Example of an individual offer curve at EPEX SPOT representing the up to 256 possible

price-quantity combinations .................................................................................................................. 21

Figure 16: Possible block orders of the day-ahead auction at EPEX SPOT (EPEX SPOT 2014b) ..... 22

Figure 17: Principles of price convergence in coupled electricity markets (PCR 2014b) ..................... 30

Figure 18: Concept of direct marketing & refinancing RE ..................................................................... 33

Figure 19: Portfolio size of 30 selected direct marketing companies ................................................... 35

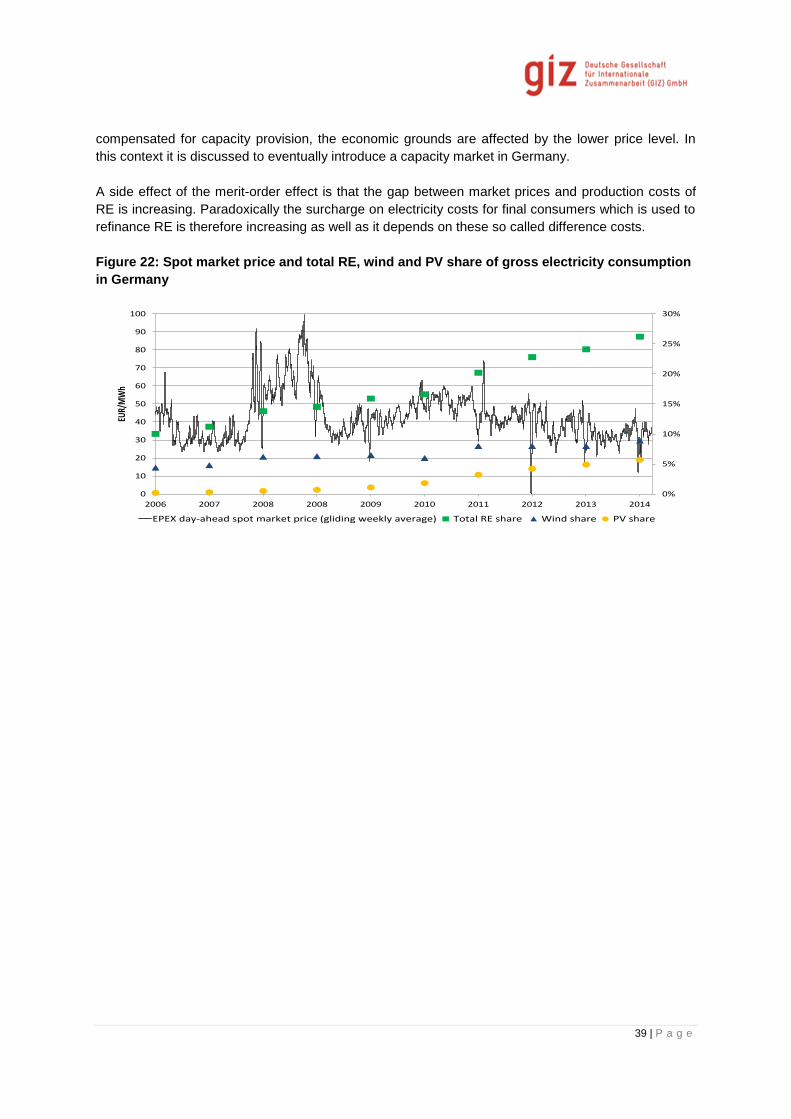

Figure 20: Electricity production by source and price development at EPEX spot markets ................. 37

Figure 21: Illustrative example: Marginal cost pricing mechanism and merit-order effect of RE .......... 38

Figure 22: Spot market price and total RE, wind and PV share of gross electricity consumption in

Germany................................................................................................................................................ 39

Figure 23: Survey of important system characteristics and services .................................................... 40

Figure 24: Dynamic hierarchy of Load-Frequency Control processes in Europe, Source: entso-e ..... 43

Figure 25: Types and hierarchy of geographical areas in Load-Frequency Control processes in

Europe and a possible configuration of a synchronous area, Source: entso-e .................................... 44

Figure 26: Current status of Synchronous Areas, LFC Blocks and LFC Areas in Europe, Source:

entso-e .................................................................................................................................................. 44

Figure 27: Load Frequency Control Block Diagram with Input ∆PL and Output ∆f .............................. 46

Figure 28: Steady state frequency deviation for different shares of RE - no speed regulation ............ 47

Figure 29: Steady state frequency deviation for different shares of RE – 50% conventional generation

with speed regulation R =5% ................................................................................................................ 48

Figure 30: Steady state frequency deviation for different shares of RE – 100% conventional

generation with speed regulation R=5% ............................................................................................... 49

Figure 31: Steady state frequency deviation for different shares of RE – 50% conventional and 100%

RE generation with speed regulation R=5% ......................................................................................... 49

Figure 32: Steady state frequency deviation for different shares of RE - all generation with speed

regulation R=5% .................................................................................................................................... 50

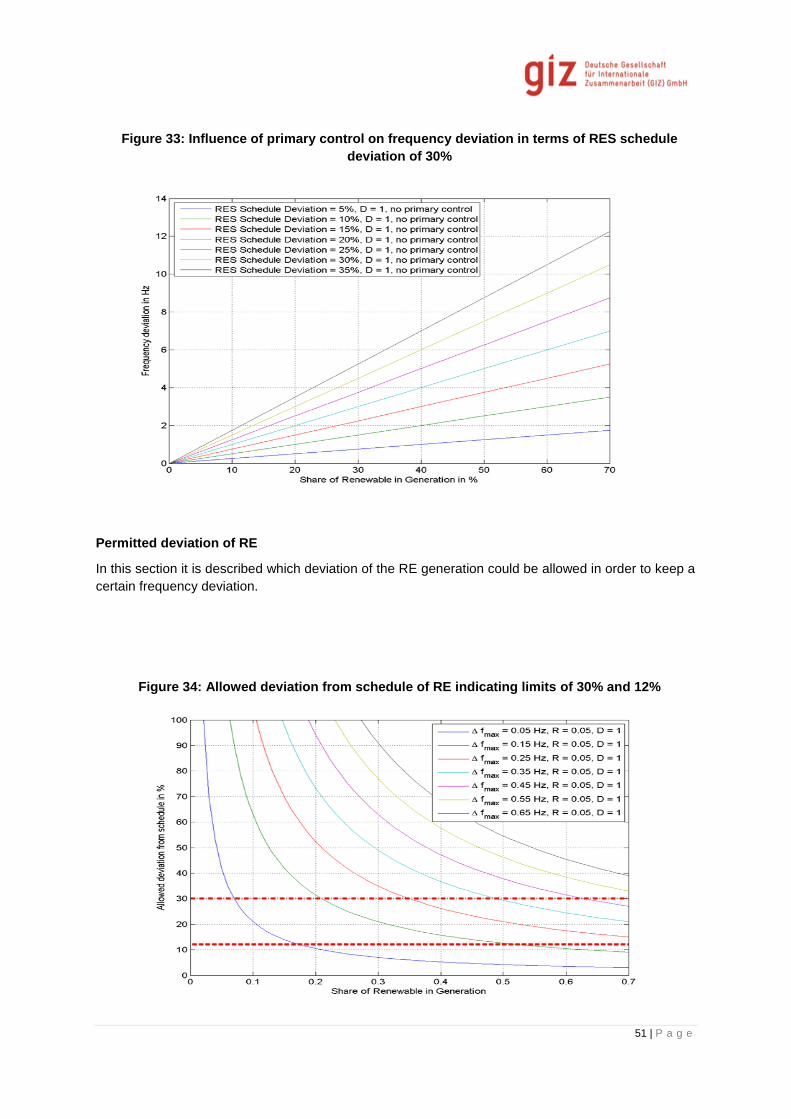

Figure 33: Influence of primary control on frequency deviation in terms of RES schedule deviation of

30% ....................................................................................................................................................... 51

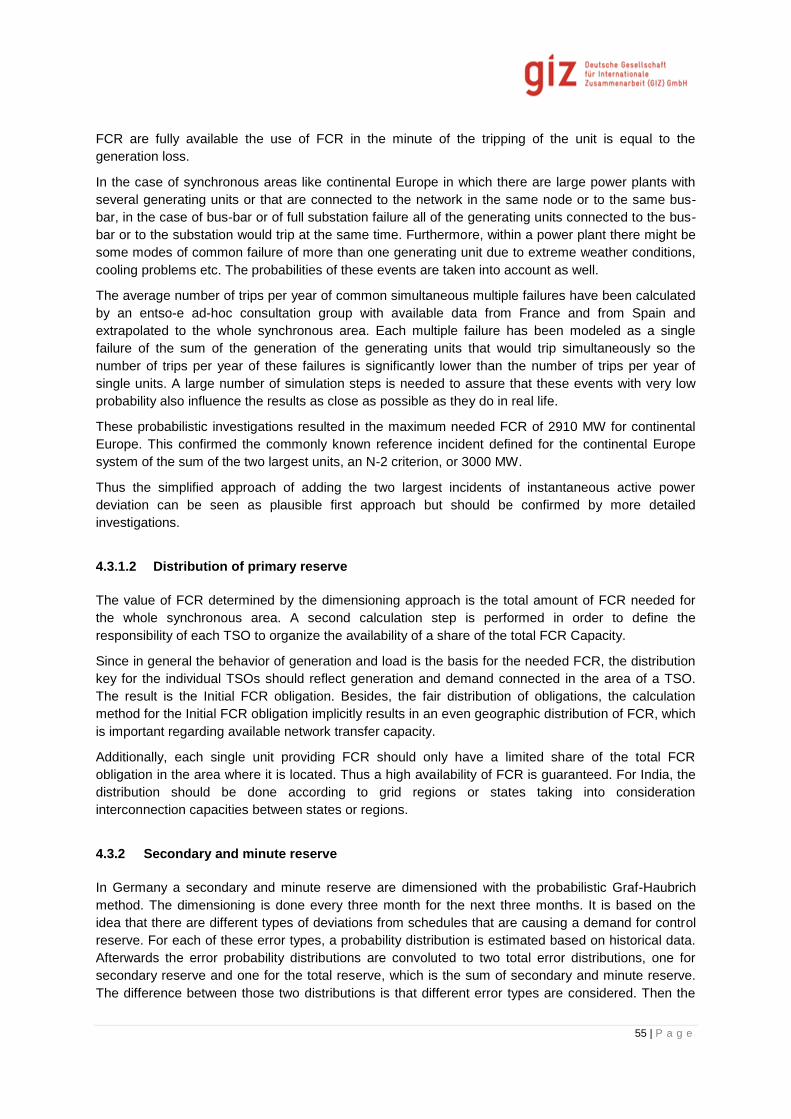

Figure 34: Allowed deviation from schedule of RE indicating limits of 30% and 12% .......................... 51

Figure 35: Allowed deviation from schedule of RE indicating limits of 30% and 12% with variable

primary control provision. ...................................................................................................................... 52

Figure 36: Simplified illustration of imbalance types (source: entso-e) ................................................ 53

Figure 37: Schematic representation of the Graf-Haubrich method ..................................................... 56

Figure 38: Procured secondary reserve capacity in Germany for each quarter of the year ................. 57

Figure 39: Procured minute reserve capacity in Germany for each quarter of the year ....................... 57

Figure 40: Model protocol for the prequalification of a technical unit for positive primary control ........ 59

Figure 41: Technical implementation of Imbalance Netting in IGCC .................................................... 63

Figure 42: Example of pro-rata distribution of netting potential with congestion correction ................. 63

Figure 43: Value of netted imbalances per country .............................................................................. 64

Figure 44 - Market Options ................................................................................................................... 75

Figure 45 - Types of electricity pool options ......................................................................................... 76

Figure 51: Organization of Intra state balancing groups ....................................................................... 81

Figure 52: Organization of Inter-state Balancing Groups ..................................................................... 82

Figure 53 - Demand Response ............................................................................................................. 84

Figure 46: Current Power Market .......................................................................................................... 86

Figure 47: Market on complete implementation of phase 1 .................................................................. 90

Figure 48: Market structure after complete implementation of Phase 2 ............................................... 92

Figure 49: Market on Completion of Phase 3 ....................................................................................... 94

Figure 50 - Proposed Market Design .................................................................................................... 96

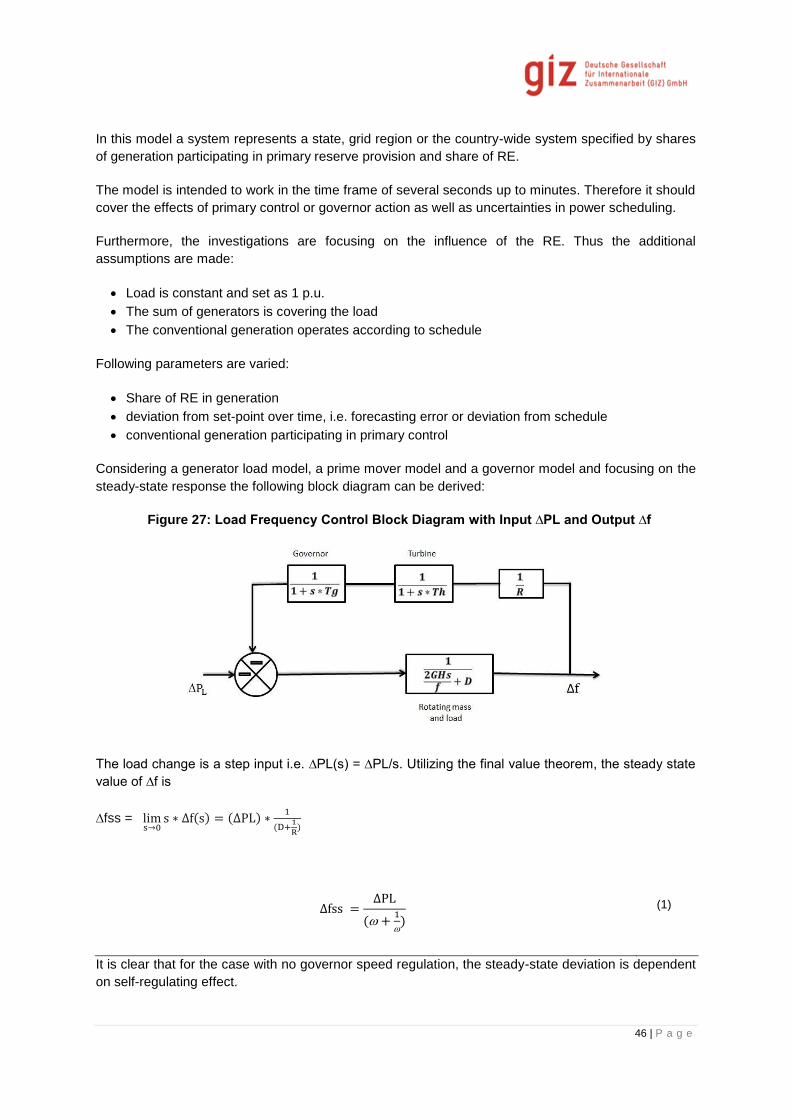

Figure 54: Block diagram of a generator-load model (Kundur, 1994) .................................................... 3

Figure 55: Governor Steady-State Speed Characteristics (Saadat) ....................................................... 4

Figure 56: Block Diagram of Governor with Frequency Control Loops for Steam Generator Unit

(Saadat)................................................................................................................................................... 5

Figure 57: Load Frequency Control Block Diagram with Input ∆PL and Output ∆f ................................ 6

Figure 58: Single Part Tariff Structure .................................................................................................. 12

Figure 59: Two Part Tariff Structure ...................................................................................................... 13

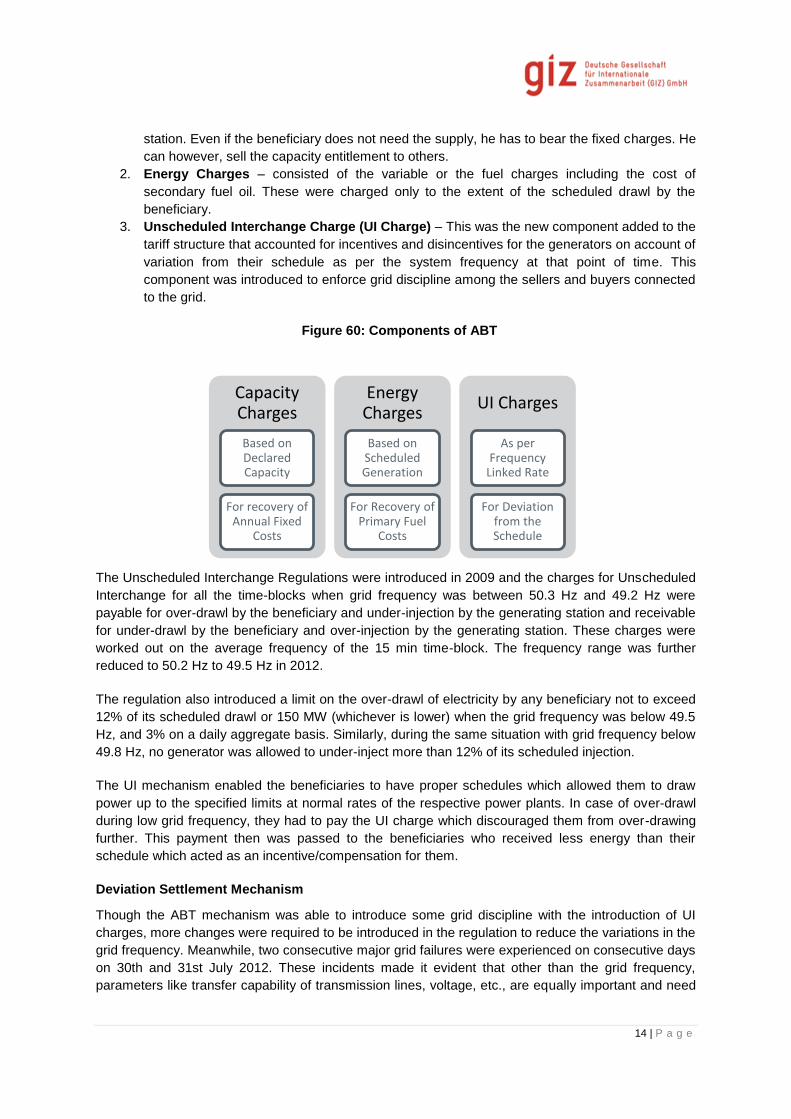

Figure 60: Components of ABT ............................................................................................................ 14

Figure 61: Gujarat Load Demand - 2014 and 2022 .............................................................................. 16

Figure 62: Gujarat Solar Generation for July 2014 and July 2022........................................................ 16

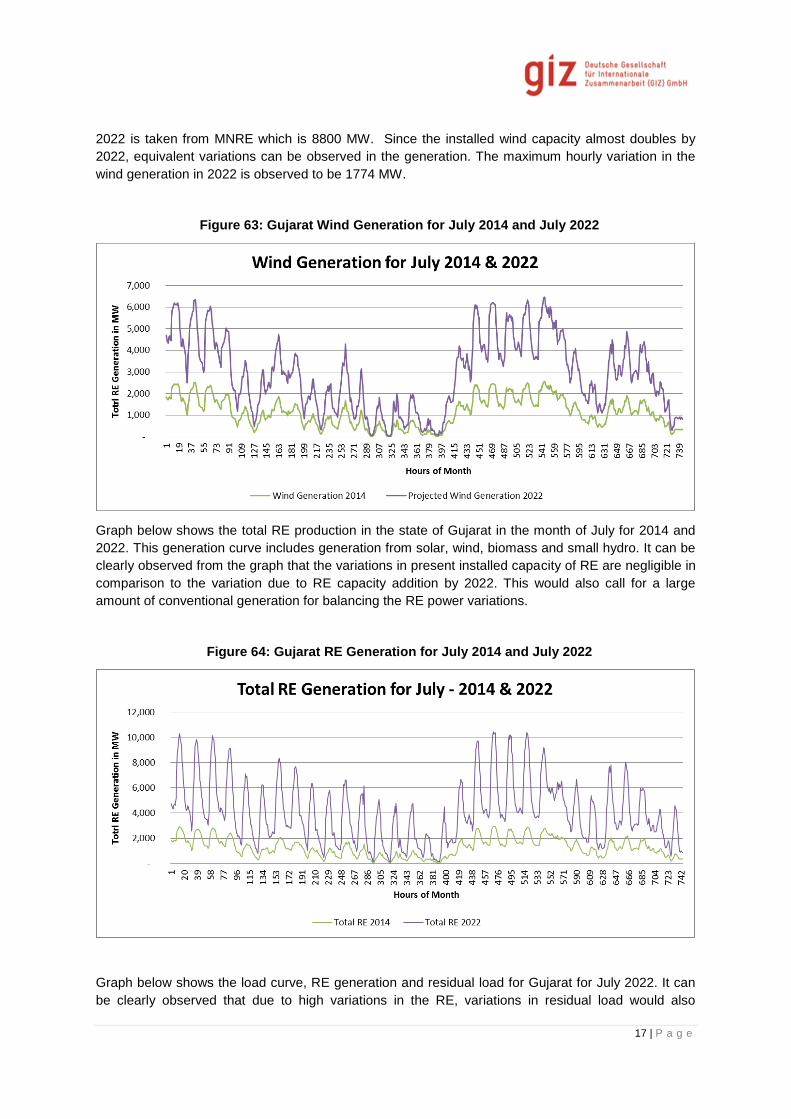

Figure 63: Gujarat Wind Generation for July 2014 and July 2022 ........................................................ 17

Figure 64: Gujarat RE Generation for July 2014 and July 2022 ........................................................... 17

Figure 65: Gujarat Load Demand v/s RE Generation & Residual Load for July 2022.......................... 18

Figure 66: Frequency Deviation for Different Shares of RE ................................................................. 19

Figure 67 - Forecasted GHI series ........................................................................................................ 28

Figure 68 - IFS gridded map of Rajasthan ............................................................................................ 29

Figure 69: Change in Forecast Error for a Regional and Single Site Forecast .................................... 30

Figure 70: Accuracy of forecast for different Prediction Horizons......................................................... 31

Figure 71: Scatter plot linking forecast error to actual generation in % of total installed capacity ........ 32

List of Tables

Table 1: Type of Contracts in Term-Ahead Market ............................................................................... 11

Table 2: Difference between Day Ahead Contingency and Day Ahead Spot Contracts ...................... 12

Table 3: Summary of Term-Ahead Market ............................................................................................ 13

Table 4: EPEX SPOT day-ahead auction contracts specifications (EPEX SPOT 2015) ..................... 23

Table 5: EPEX SPOT 15-min. intraday auction contracts specifications (EPEX SPOT 2015) ............. 25

Table 6: EPEX SPOT intraday continuous trading one hour contracts specifications (EPEX SPOT

2014e) ................................................................................................................................................... 29

Table 7: Classification of ancillary and operational services in Germany ............................................. 41

Table 8: SOC and Regional group activities ......................................................................................... 42

Table 9: Error types considered in the Graf-Haubrich method (CONSENTEC 2010) .......................... 56

Table 10: Parameterization of the Graf-Haubrich method (CONSENTEC 2010) ................................. 56

Table 11: Reserve product specifications ............................................................................................. 60

Table 12 - Factors influencing demand and supply of the control reserve market in Germany ........... 61

Table 13: Wind and Solar PV Technology Capabilities for Gas Provision ........................................... 68

Table 14: Explanations and References for Wind and Solar Technology Capabilities ........................ 70

Table 15: Requirements of the different types of control reserves ....................................................... 73

Table 16 - Comparison of Market Options ............................................................................................ 77

Table 17: Proposed Products on the Power Exchange ........................................................................ 87

Table 18: Requirement of Different types of control reserves ............................................................ 102

Table 22: Proposed Deviation Settlement for RE Generators .............................................................. 22

Table 23: Analysis of RRF and Proposed DSM for RE Generators ..................................................... 24

Table 24: Per Unit Charges for a Wind Generator as per Proposed DSM Mechanism ....................... 25

Table 25: Analysis of RRF and Proposed DSM for RE Generators for deviation within ±12% ............ 26

Table 26: Impact of Proposed DSM Mechanism due to different PPA Rates ...................................... 32

1 | P a g e

1 Problem Statement

Large scale integration of Renewable Energy (RE) into a power system poses multiple technical and

commercial challenges to the stake holders of the system. It is critical to address these challenges for

large scale integration of RE into the power system. This section of the report describes the major

techno-commercial challenges faced by RE grid integration.

1.1 High Delivered Cost of RE Power

The delivered cost of power refers to the actual expense incurred for the total quantity of power

delivered at the metering point. The overall high delivered cost of RE power is a major deterrent in the

large scale adoption of RE.

Cost of Interstate Transfer of RE

The delivered cost of RE power increases in the case of an interstate transfer of power. This increase

is the result of addition of charges linked to wheeling, transmission and losses. RE power therefore

becomes uncompetitive in the power market, leading to the requirement of Renewable Purchase

Obligations (RPOs) to ensure it’s off take.

Cost of RE above APPC

The cost of RE power to DISCOMS is higher than APPC in all states. This makes the purchase of RE

power a loss making business decision to DISCOMS.

To bridge the gap between delivered cost of RE power and delivered cost of conventional generation,

many states have introduced exemptions by policy on cost of transmission of RE power. Since wind

energy is more mature and intensively promoted (especially over the past 2 decades), it has lower

tariffs in comparison to solar power. It is estimated that solar PV is expected to achieve parity with

conventional power in the in the coming years with falling price of PV systems and rising price of retail

electricity. Till RE power becomes competitive in the market, there is a need to incentivise the sale of

RE power to make the upcoming capacity addition economically viable.

1.2 Burden on DISCOMs on Purchase of RE power

DISCOMs’ debt burden was INR 3.04 lakh crore and accumulated loss was INR 2.52 lakh crore

adding up to a total of INR 5.56 lakh crores as of June 2015. Most DISCOMS in India are operating in

losses, primarily due to inefficient revenue recovery systems. According to the UP electricity regulator,

of 3.54 crore households in the state, only 1.14 crore have registered electricity connections. Out of

these registered connections, only 70.67 lakh are metered connections. This implies that out of every

100 users only 35 were paying1.

There is unwilling to raise power tariffs to recover the cost and therefore DISCOMs are unable to buy

the quantum of power they need. The provision of subsidised electricity to farmers and residential

consumers further increases this burden.

Sale of RE power in India is mainly driven by obligation enforced through regulation. DISCOMs are

one of the largest consumers of RE power in the country. Purchase of RE power is an additional

financial burden on the DISCOMs that are already financially stressed. Owing to the cost implications

of buying expensive RE power, DISCOMs fail to meet RPO targets. This increases investment risk of

RE power and is therefore a major deterrent to RE developers. In certain cases the DISCOMs are

liable to pay a penalty for failure to meet RPO targets. However these penalties are not strictly

1 http://www.assocham.org/newsdetail.php?id=5003

2 | P a g e

enforced across all states. There is therefore an imminent need to develop a market mechanism for

the sale of RE power that reduces the burden on DISCOMs.

1.3 Deviation from RE Schedule

The deviation from RE schedule is due to the error in forecast of RE power generation. The error in

RE power forecast occurs because actual RE power generation depends on fluctuating weather

conditions. This variable nature of RE power is represented by the following plots of actual wind and

solar generation in Gujarat over the period of a month in 2014 and 2022(projected).

Figure 1: Wind and Solar Generation Gujarat 2014 and 2022 (projected)

There is an urgent need for Ancillary Services (AS) to support the power system when large quantities

of RE is integrated into the grid. Forecasting RE generation and estimating balancing requirement

would help manage the overall variability in the system. However the error in forecasting leading to

deviation from schedule would requires AS for mitigation. The cost of provisioning AS would be a

financial burden on the central and state governments.

In the current market scenario the cost of AS cannot be loaded onto RE generators because:

a) Additional costs would reduce the economic viability and competitiveness of RE generators

and would deter investors.

b) All disturbances in the power system do not originate from RE sources. There is also a

requirement of Ancillary Services to manage the variability of the power system due to

conventional generation as well as consumers deviating from schedule.

There is therefore a need to develop a market mechanism to meet the requirement of introducing AS

in the Indian power system.

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1

69

13

7

20

5

27

3

34

1

40

9

47

7

54

5

61

3

68

1

Totr

l RE

Ge

ne

rati

on

in M

W

Hours of Month

Wind Generation for July 2014 & 2022

Wind Generation 2014

Projected Wind Generation 2022

-

1,000

2,000

3,000

4,000

5,000

6,000

1

69

13

7

20

5

27

3

34

1

40

9

47

7

54

5

61

3

68

1

Totr

l RE

Ge

ne

rati

on

in M

W

Hours of Month

Solar Generation for July 2014 & 2022

Solar Generation 2014

Projected Solar Generation 2022

3 | P a g e

1.4 Non Uniform Distribution of RE potential

RE potential of a region is based on its geographical features which vary significantly across the

country. The state wise estimated wind and solar power potential are depicted in the figures below.

Figure 2: Variation of Wind and Solar potential in India

Source: MNRE 2014, NIWE 2014

The uneven spread of RE potential across different states would create a disparity in the

RE/Conventional generation mix in different parts of the country. This would necessitate evacuation of

RE power out of the RE rich states. Profitable interstate trade of RE power is therefore needed to

ensure offtake of upcoming RE capacity and optimal utilisation of India’s RE potential.

0 20000 40000

Uttarakhand

Kerala

Uttar Pradesh

Orissa

MadhyaPradesh

Rajasthan

Jammu &Kashmir

Maharashtra

Karnataka

Tamil Nadu

AndhraPradesh

Gujarat

Wind Potential (MW) @ 80m

Estimated Potential (MW) @ 80m0 50 100 150

Goa

Tripura

Haryana

Meghalaya

Nagaland

Mizoram

Bihar

Uttarakhand

Jharkhand

Telangana

Karnataka

Himachal…

Andhra Pradesh

Maharashtra

Rajasthan

Solar Potential (GWp)

Solar Potential (GWp)

4 | P a g e

2 Current Indian power market

2.1 Introduction

Source: CEA report, March 2015 http://www.cea.nic.in/reports/planning/dmlf/growth_2015.pdf2

The state electricity boards (SEBs) and central utilities have maximum market share in the

transmission and distribution segments of the Indian power market. In the generation space, out of

the overall capacity of 271GW, the share of central, private and state utilities stand at 72GW, 104GW

and 95GW, respectively. The recent emphasis of policy and regulatory framework, as guided by the

provisions of the Electricity Act, 2003, is on bringing in competition, private sector participation and

independent regulation.

The main enablers for competition are as follows:

Generation is de-licensed (except large hydro and nuclear projects) and now all new

generation in the private sector has to be contracted through the competitive bidding route.

Open access on common carrier principle is allowed on transmission networks and is soon to

be phased in on distribution networks as well.

Provisions for parallel distribution networks in existing areas are made. This would create a

competitive environment in distribution.

Prior to 2003 and prior EA 2003, power exchanges between states/vertically integrated utilities

were majorly of small or intermittent volumes. Transactions were predominantly in nature of

emergency support. The exchanges were majorly limited due to lack of transmission inter

connections. There had been sustained shortages both in energy and peak demand which

discourages initiatives and for long there had been scepticism about success of trading.

2 http://powermin.nic.in/JSP_SERVLETS/internal.jsp

Figure 3: Segments of Indian Power Sector

5 | P a g e

2.2 Structure of Indian Electricity Market

The present electricity market is governed by the Power Market Regulation Act 2010. Below

mentioned is the synopsis of the regulation.

Indian electricity market predominantly follows a wholesale decentralized model. In this model, the

generation, transmission and distribution companies are unbundled. Transmission Company controls

the system operation and schedules the generation over 96 time blocks in a day. Multiple generators,

including Independent power producers and public sector generation companies, are allowed to

participate in the supply of electricity. This ensures supply security and removes monopoly on the

prices. The generators are allowed to openly compete, which enables system operators to schedule

& dispatch the power based on the different contracted prices and also the distribution companies to

procure power at the competitive prices. However, in this model choice available to all the retailers

and consumers to procure power in the open market besides their DISCOM is restricted. Open

access is available for consumers above 1MW of requirement as per the Open Access Regulation.

There is a power exchange available in the country, which allows the consumers to bypass DISCOM

and procure power at the spot market. Power exchange has been introduced to offer a nation-wide

voluntary access, e-trading, no counter party risk, robust platforms and deliver based contracts.

However, due to volatility/uncertainty in prices and higher liquidity is required; the percentage of

power traded in the exchange is very low in the country.

Generator

Organized Inter- State Power Market as Follows:

Over the Counter (OTC) Market.

Power Exchange Market.

Other Exchange Market.

OTC Market:

Buyer and Seller Transact Directly or Through Trader.

Price Set by Negotiations or Bidding.

Risk Managed by Parties/Trader.

Power Exchange:

Transactions on Standard Platform.

Price Set by Market Rules.

Other Exchange Market:

Derivative Product.

Figure 4: Structure of Indian Power Market

Generator Generator Generator

Distribution Company Distribution Company

Retailer Retailer

Transmission and System Operation

6 | P a g e

The above mentioned summarizes broadly a market model followed in the country. The power can

either be directly sold by the generation companies to the distribution companies or through an

intermediary i.e. an independent body who can purchase power in bulk. However there can be

change in orientation of the above model from state to state which is discussed as under.

In Rajasthan, the DISCOMs are purchasing power directly from RVUNL, which is the generation

company responsible for the development, operation and maintenance of state owned power stations.

Rajasthan DISCOM Power Procurement Centre (RDPPC) has been established for purchase of

power on behalf of the DISCOMs. The 3 DISCOMs in Rajasthan are Jaipur Vidyut Nigam Ltd, Ajmer

Vidyut Vitran Nigam Ltd and Jodhpur Vidyut Vitran Nigam Ltd.

In Gujarat, the Gujarat State Electricity Corporation Ltd. (GSECL) is the power generation company.

The vertically integrated GEB was unbundled into seven companies one each for generation and

transmission, four distribution companies (DISCOMs) and a holding company known as Gujarat Urja

Vikas Nigam Limited (GUVNL). The generation, transmission and distribution companies have been

structured as subsidiaries of GUVNL. GUVNL acted as the planning and coordinating agency in the

sector when reforms were undertaken. It is now the single bulk buyer in the state as well as the bulk

supplier to distribution companies. It also carries out the function of power trading in the state.

Presently, there are four DISCOMs in Gujarat; UGVCL, DGVCL, MGVCL and PGVSL.

In Andhra Pradesh, the generation company is Andhra Pradesh Power Generation Corporation

(APGENCO). Post the state bifurcation and as per the AP Reorganization Act 2014, the NPDCL,

CPDCL, EPDCL, SPDCL have become TGNPDCL, TGSPDCL, APNPDCL and APSPDCL. The

DISCOMs in Andhra Pradesh are Southern Power Distribution Company (APSPDCL) and Northern

Power Distribution Company (APNPDCL). These DISCOMs directly purchase power from the

generating companies through PPAs.

In Karnataka, there exist PPA’s between the generation company i.e. Karnataka Power Corporation

Limited (KPCL) and Power Company of Karnataka Limited (PCKL) which is a body established to

purchase power on behalf of the five DISCOMS. The five DISCOMS in Karnataka are BESCOM,

HESCOM, MESCOM, GESCOM and CESC.

In Tamil Nadu, no independent body exists and power is purchased directly from the generation

companies. Tamil Nadu Generation and Distribution Corporation (TANGEDCO) is the only DISCOM

present and responsible for power generation and procurement.

In Himachal Pradesh, the Himachal Pradesh State Electricity Board, having its registered office in

Vidyut Bhawan, Shimla is responsible for supply of quality power to all categories of consumers’ at

most economic rates. It’s the only body responsible for power generation and supply.

2.3 Transactions in the Market

The overall market transaction comprises of Long term, Medium Term and Short term transactions.

The country has an overall peak demand of 140GW as on 2015. The demand of the country is

managed by the system operator by allocating the market transacted contracts such that it optimally

and efficiently manages the load curve. In order to manage the demand in the country, the market

transactions are scheduled such that

Base and Intermittent load- Managed by Long Term PPAs

Seasonal Variations – Managed through Short Term trades, by Traders, Bilateral Contracts or

Banking Arrangements

Daily Variations – Managed through Day ahead Power Exchange or DSM Balancing

7 | P a g e

Figure 5: Classification of Indian Power Market

In Indian electricity market, bulk power supply is tied up with Long Term (LT) agreements/contracts

which have long time period. The bulk power suppliers include predominantly the central generating

stations, state generating stations and few IPPs. DISCOMs who are obligated to supply electricity to

their consumers prefer and predominantly rely upon the long term contracts. Long term contracts

secure a base load electricity supply in the country. Moreover, it is not economically feasible for the

DISCOMs to purchase short contracts to meet the seasonal variations. It can be observed that in the

Indian electricity market, nearly 89% of power purchase agreements fall in the category of Long Term

contracts.

8 | P a g e

Figure 6: Transactions in Indian Power Market

Short Term (ST) contracts in the electricity market majorly refer to contracts less than one year period.

The contracts include electricity transactions through

Bilateral transactions through interstate trading licensees

Bilateral transactions directly by Distribution Licensees (DISCOMs)

Power Exchanges (IEX and PXIL)

Unscheduled interchange

Several regulatory interventions have enabled the successful creation and operation of Power

Exchange market. This market provides a platform on which power can be transacted in shorter time

duration/period. Two exchanges namely Power Exchange India Limited (PXIL), Indian Electricity

Exchange (IEX) are fully operation from 2008. This representation is primarily with respect to IEX as it

hosts 96% of the total volume traded on the exchanges. As per the CERC order dated 8.4.2015 on

extended market sessions. The power exchanges in India now operate for 24 hours; this however

does not mean that all products are traded for all 24 hours. Different products have different trade

windows as explained in this section.

These short term contracts cater to just 5% of the existing electricity market structure. However, these

contracts play a very crucial role in managing the peak demand and handling the intraday

imbalances.

9 | P a g e

Figure 7: Regulatory Transition of Indian Power Market

Several different contracts are executed in the power exchange market which includes namely

Intraday, Day Ahead Market (DAM), Day Ahead Contingency (DAC) contracts, daily contracts and

weekly.

Figure 8: Percentage Distribution of Contracts in the Market

Two power exchanges work in tandem and handle same or at times different electricity

contracts/products. Nevertheless, both the exchanges offer Day-ahead products.

Day-ahead Services

10 | P a g e

This service facilitates the electricity to be procured and to be scheduled for one day ahead (d) in

every 15 minutes time block. Physical electricity trading market which facilities contract for deliveries

for any/some/all 15 minute time blocks in 24 hours of next day starts from midnight. Prices of

electricity traded are determined using double sided auction bidding. The procedures are guided by

CERC- Open Access Inter-state transmission regulations, 2008.

Typical order types are:

Hourly orders

Block orders

Consecutive orders

Minimum size of the contract to be traded should be 0.1MW and the minimum quotation step is Rs. 1

per MWh. Power exchanges at 15:00hr on the present day (d-1) calculates the area clearing price

based on the transmission network availability and send the scheduling request to NLDC. Periphery

of the regional transmission in which grid entity is connected will be the delivery point. Settlement

mechanism occurs on a daily basis and is calculated based on the formula of Area Clearing Price

(ACP) X Traded volume.

Detailed procedures for day-ahead services have been provided in the form of functional diagram

below.

Day Ahead markets

The Day Ahead Markets open at 10:00 hrs every trading day, Trading days are as defined by the IEX

trading calendar. The DAM functions from 10:00 hrs to 12:00 hrs every day. Till 12:00 market players

are allowed to bid for the buying or selling of power. Between 12:00 to 13:00 the bids are matched

and the market clearing price (MCP) as well as the market clearing volume (MCV) re calculated. This

data is then sent to the respective dispatch centres for checking availability of corridors. The

availability of funds is also verified in this period. At the 15:00 hours the actual clearing price (ACP) as

well as the actual clearing volume (ACV) is published and this data is forwarded to the respective

SLDCs for verification. Market is split if there are transmission constraints; this creates different

clearing prices and volumes for different market regions. At 17:30 the NLDC clears the final schedule

and forwards it to the respective SLDCs for incorporation into despatch schedule. The illustration

below graphically depicts the operation of the Day-Ahead markets.

Figure 9: Functioning of Day Ahead Markets

Source: IEX

CERC in August 2009 allowed a Term Ahead/Additional Contracts to be traded through power

exchange. Both the exchanges commenced their operations since September 2009.

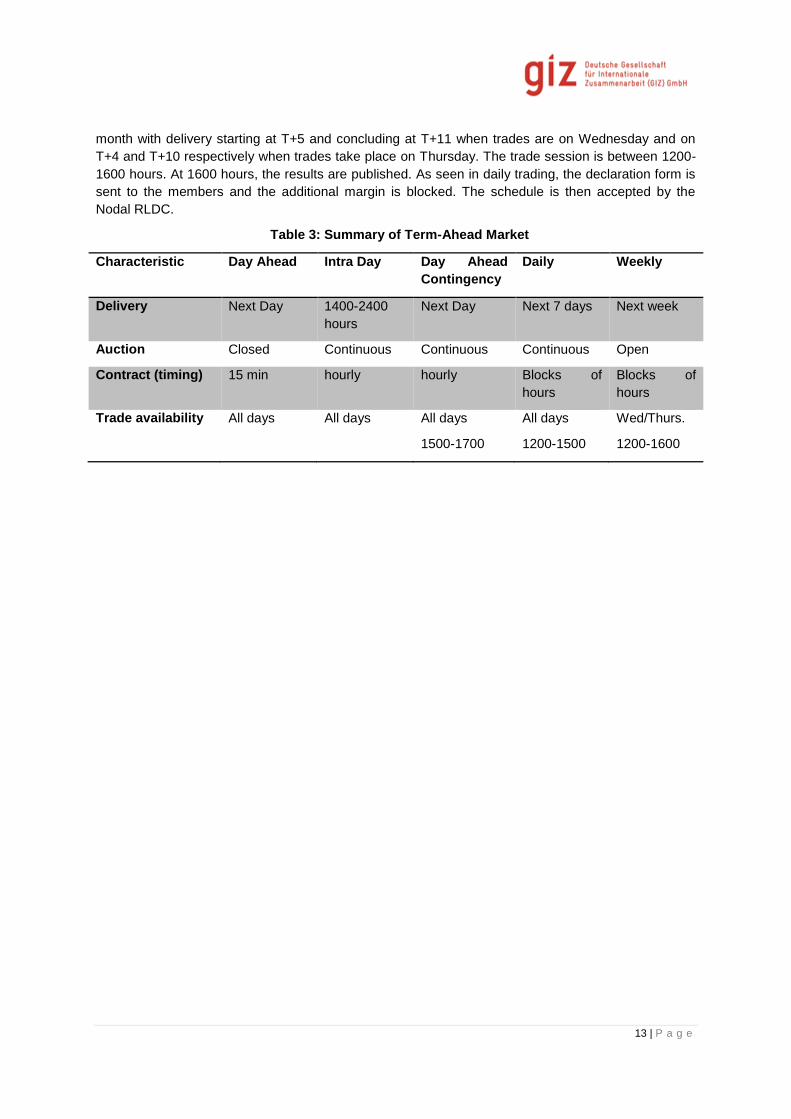

Term-Ahead Market (TAM)

11 | P a g e

TAM provides a range of products allowing the participants to buy/sell electricity for contracts beyond

day-ahead market besides intraday contracts. Four different services under TAM are tabulated

below:

Table 1: Type of Contracts in Term-Ahead Market

S.No. Contract Trading

1. Intra Day contract Trading on delivery day few hours before delivery.

3. Day Ahead contingency contract Trading to a day before delivery and after DAM

auction.

4. Daily contract Trading up to 1 Week in advance for any calendar

day starting from the 4th day of the month

5. Weekly contract Trading up to 11 days in advance

In Term Ahead Markets, the price of electricity between the producer and consumer is estimated

through way of a double sided auction. This begins with a Bid Entry where the buyers and sellers bid

their maximum and minimum prices respectively. Under this mechanism, buy trades are settled at or

below the quoted price and sell trades are settled at or above the quoted price. Based on this a

matching price is established, ensuring maximum benefits to both buyers and sellers of electricity.

This is then included in the day-ahead schedules. This is a bilateral contract between the buyer and

the seller and there is complete anonymity of the bids between them. Clearing is then done by the

SLDC and exchange and final settlement is done when the clearance is accepted by the RLDC.

The services under TAM can be further explained as follows, Timelines of products are illustrated

below:

Figure 10: Timeline of trades on the IEX under 24 hour operations

12 | P a g e

Source: IEX

1. Intra Day Contracts

The Indian power markets now operate for 24 hours, in the past the seller could only submit bids from

his own region, whereas a buyer can buy any regional contract. These contracts are available for

trading from 10:00 hrs To 20:00 hrs. on a daily basis through continuous trading process. By 20:30,

all funds are blocked including transmission and operating charges. After blocking the funds, pay-out

is done on the T or T+2 basis and the nodal RLDC is also paid its charges on T+2 basis (where T is

trading day).

In the current organisation of the power markets, the trading of products timelines is as below.

2. Day Ahead Contingency Contracts

In these contracts, for the first hour, selling bids are allowed region wise, followed by buy bids. Buyers

are allowed to see the price and region of the seller but the seller’s identity is not revealed and the

same auction mechanism with differential pricing issued. These contracts auction for all the 24 hours,

subdivided into hourly contracts and the pay-in and pay-out is on T+1 basis.

Though the Day Ahead Contingency Contracts Market appears similar to Day Ahead Spot Contracts

Market, there are subtle differences in the functioning of both. Some noticeable differences being:

Table 2: Difference between Day Ahead Contingency and Day Ahead Spot Contracts

Day Ahead Contingency Day Ahead Spot

Uses Differential Price Mechanism Uses Uniform Clearing Price

Congestion managed by curtailing trade/re-

routing as per Nodal RLDC/SLDC

Congestion managed by Market Splitting

Members aware of counterparty, as it’s a

Bilateral transaction

Members not aware of counterparty

Scheduling procedure is handled by Nodal

RLDC

Scheduling procedure is handled by NLDC

Supersedes DAS Precedes DAC

Comes under the Bilateral Transactions Comes under Collective transactions

3. Daily Contracts

In this type of contract, the minimum trading volume is 1 MW and trading is done in different blocks.

As far as the delivery process goes, the delivery point is at Seller’s Regional Periphery. Up to the

delivery point, Transmission, Scheduling & Operating charges and Transmission Losses are borne by

the seller. Post that, up to the point of drawl, charges is borne by the buyer. These contracts are

available for trading from 12:00 hrs to 15:00 hrs through a continuous trading cycle. By 15:30, a

declaration form is sent to the members after getting clearance from SLDC. The addition of the

buyer’s member is then calculated and blocked and Nodal RLDC is paid its charges. Pay in is on D-1

basis and pay-out is on D+1 basis.

4. Weekly Contracts

Delivery for whole week traded on the preceding Wednesday & Thursday of the week. Trading

Calendar is declared by the IEX through circulars and bidding and matching is done on a similar basis

as above. Also, trading is done through open auction on every Wednesday and Thursday of the

13 | P a g e

month with delivery starting at T+5 and concluding at T+11 when trades are on Wednesday and on

T+4 and T+10 respectively when trades take place on Thursday. The trade session is between 1200-

1600 hours. At 1600 hours, the results are published. As seen in daily trading, the declaration form is

sent to the members and the additional margin is blocked. The schedule is then accepted by the

Nodal RLDC.

Table 3: Summary of Term-Ahead Market

Characteristic Day Ahead Intra Day Day Ahead

Contingency

Daily Weekly

Delivery Next Day 1400-2400

hours

Next Day Next 7 days Next week

Auction Closed Continuous Continuous Continuous Open

Contract (timing) 15 min hourly hourly Blocks of

hours

Blocks of

hours

Trade availability All days All days All days

1500-1700

All days

1200-1500

Wed/Thurs.

1200-1600

14 | P a g e

3 German Electricity Market

The set-up of the German electricity wholesale market and the developments to deal with the

integration of RES are described in this section. To integrate high shares of RES more flexibility is

needed in power systems. In a liberalized electricity market, the incentives to develop and operate

plants in a flexible way should be delivered by market signals. The design of wholesale electricity

markets therefor plays a key-role. Negative prices can signal a surplus of electricity better than a

zero-price, while low price-caps will give fewer incentives to players to operate when most needed.

Moreover, as forecasts improve significantly when calculated closer to the generation horizon, market

participants should be given an opportunity to manage their bids close to real-time. Intraday markets

could reduce the costs of balancing and help the integration of intermittent RES.

Figure 11: German electricity markets. (Fraunhofer IWES based on (Judith et al. 2011))

3.1 Regulatory Framework

The wholesale market in Germany is organized using balancing groups. Each group is a Balancing

Responsible Party (BRP) and can be responsible for the scheduling of generation and load, or traded

15 | P a g e

energy, or a combination of them. There are overall about 5000 BRPs in Germany including some

special BRPs used by grid operators summarizing renewable generation or grid losses.

In this section an introductive example is followed by a detailed description of the obligations and

market design regarding the balancing group concept. Please note: Power generation, transmission

and distribution, and retail is unbundled in Germany, with minor exemptions for very small utilities.

The imbalance settlement has some similarities to the settlement mechanisms used in India. But the

concept of reserve energy markets is (so far) not introduced in India.

In Germany all power producers and commercial consumers (i.e. distribution companies or industrial

companies) are obliged to forecast their energy consumption or production day-ahead and report their

quarter-hourly schedules to the responsible TSO. To do so, consumers and producers are organized

in balancing groups. Small power producers or consumers are able to cluster their activity in a

balancing group. In this case their total production and consumption is made accountable and

managed by one responsible representative. This is especially the case for distributed generation

such as renewable energies where hundreds and thousands of individual producers make up one

portfolio. Over- or under drawl in respect to the schedule is accounted by the TSO only balancing

group wise. Internal costs distribution is not regulated and settlement is done by the balancing group

members on an individual, contractual basis.

Activation of reserve power is only necessary if there is a net deviation in respect to the total schedule

of a control zone (sum of all balancing group schedules). Over- or under drawl of different balancing

groups may cancel each other out in case of opposite direction of deviation.

The imbalance price is calculated by dividing the sum of costs for reserve power activation by the total

reserve power delivered. If the control area is in a deficit situation (i.e. less production or more

consumption than scheduled) balancing groups which deviate from their schedules and contribute to

the situation (increase deficit) have to pay the imbalance price. Balancing groups which reduce the

deficit (more production or less consumption than scheduled) receive the imbalance price. In times of

surplus situation within the control zone it is the reverse case. This means one part of the total

balancing price charged is circulating between contributing and compensating balancing groups and

one part is used to refinance the activated control reserve.

3.2 Introductive example

To give a first impression of the balancing group concept the figure below describes the interaction of

two BRPs within the control area of a TSO for a fictive example of a deficit situation in a control zone

with two balancing groups and resulting money flows.

16 | P a g e

Figure 12 Interaction of two BRPs and a TSO in a control zone regarding scheduling and imbalance

settlement

Source: Fraunhofer IWES

BRPs are scheduling generation, consumption and exchange for every quarter hour in their own

responsibility. Also forecast of consumption and generation (including renewables) is the

responsibility of the BRP. The schedules have to be balanced. But the actual will deviate from

schedule. In the example the consumption of BRP1 is 10 MWh lower and the generation of BRP2 is

40 MWh lower than scheduled. The resulting imbalance of 30 MWh is handled by the TSO. For this

the TSO is contracting primary, secondary and tertiary reserves on the power reserve market

exchange. The costs for the contracted power are remunerated by the grid usage fees. The costs of

the actual utilized energy of secondary and tertiary reserves are remunerated by the BRP responsible

for the imbalance. (For primary reserves only power is contracted.)

In the example costs of 900 € occur for a specific quarter hour. Now these costs are divided by the

actual imbalance of the control zone which is 30 MWh leading to a reserve energy price of 30 €/MWh.

BRP1 is supporting the balancing of the TSO control zone with 10 MWh and receives 300 € from the

TSO. 40 MWh have to be utilized for the balancing of the schedule of BRP2 and for this the TSO

receives 1,200 € from BRP2. If surplus arises, like in the given example, this is used to cover the

power costs of the reserve contracting.

The imbalance price is supposed to incentivize balancing groups to comply with their schedules. As

the resulting control area situation at any moment of time is unknown and unpredictable for the

balancing group, the best strategy is to avoid deviation from schedule. However in the recent past,

additional rules have been introduced in order to increase the imbalance price if more than 80% of

procured control reserve has been activated. The imbalance price is than increased about 50%, but is

at least 100 EUR/MWh. Higher prices should increase the effort of a balancing group to predict

production or consumption adequately and avoid schedule deviations.

17 | P a g e

Beside the general balancing groups, a number of special balancing groups exist. The most important

types are:

Balancing group for residual deviations (DSOs):

o Is responsible for all imbalances within the DSO‘s grid which cannot be assigned to

any other balancing group due to quarter hour data which is not available

o Imbalance costs are split to grid usage fees

Balancing group for grid losses (DSOs and TSOs):

o Grid operators are responsible for buying energy to cover their grid losses; this is

done via this balancing group.

Balancing group for EEG-Trading (TSOs):

o The German TSOs are responsible to trade the energy that is subsidized due to the

EEG and that is not marketed by direct marketers

o Forecast is in the responsibility of the TSO

o They sell the energy only to the Spot Market

Balancing groups for direct marketing of renewables (renewable generators or aggregators):

o Forecast is in the responsibility of the generator or aggregator

Balancing groups of power exchange (power exchange):

o Traders at the power exchange do not trade directly which each other but via the

exchange

o Balancing groups of the power exchange are the counterparts of the trader’s

balancing groups

o As they are only trading balancing groups (they do not have any generation or

consumption points) they do not have any imbalances

3.3 Balancing groups

The commercial transfer of electrical energy in Germany is processed through balancing groups. A

balancing group accounts traded volumes and generation as well as consumption of measurement

points for every quarter of an hour. Every grid connection point has to be allocated to a balancing

group within a transmission system operator’s (TSO’s) control area (Electricity grid access regulation

Stromnetzzugangsverordnung (StromNZV) § 4 (3)). In a balancing group the power trades, electricity

generation and electricity consumption of a player or a group of players in the energy market are

pooled.

The balancing group contract is a standard contract which is prescribed by formal definitions of the

Federal Network Agency (Bundesnetzagentur 2011)3. It is concluded between the BRP and the

operator of the control area. The BRP needs balancing groups and according balancing group

contracts in every control area where he is trading or where he is responsible for measurement

points. In Germany, there are four control areas operated by the four TSOs TransnetBW, 50Hertz,

Tennet and Amprion.

A balancing group is created for diverse purposes by utilities, traders, large consumers, distribution

system operators or TSOs. A list of balancing groups is published regularly4. A distribution system

operator e.g. operates several balancing groups for the accounting of grid losses, the feed-in of

3 An English version of this contract can be found here:

http://www.tennet.eu/de/index.php?eID=pmkfdl&file=fileadmin%2Fdownloads%2FKunden%2FBNetzA-

BKC_englisch.pdf&ck=48c0a802ea08e09a09d442421b76ecf4&forcedl=1&pageid=324.

4 http://www.bdew.de/internet.nsf/id/DE_EIC-Codes-und-VNB-Bilanzkreise,

http://www.bdew.de/internet.nsf/id/205ED10B9209489EC1257D570040F5EC/$file/ENTSO-Code_EIC.pdf

18 | P a g e

renewable energy sources or the differences of household power purchase and consumption. In the

following the main aspects of the balancing group contract are explained5.

As a precondition for the conclusion of a balancing group contract for a balancing group with physical

grid connection the grid usage has to be agreed with the responsible distribution grid operator in

whose grid the connection points of the balancing group are located.

The balancing group contract enables both the feed-in and draw-off of electrical energy within the

TSO’s control area as well as the exchange of electrical energy with other balancing groups. The

exchange with other balancing groups can be a trade between two different companies within the

TSO's control area or a delivery to a balancing group of the same company in another TSO's control

area. The BRP has to inform the TSO immediately of the identity of the traders and suppliers who are

allocated to its balancing group. The BRP also has to make sure that it is reachable to the extent

required for a proper compliance with its contractual duties.

3.4 Market based balancing

As in India, power generators in Germany have different options for selling their production. These are

basically bilateral trade (over-the-counter, OTC) and trade over power exchange trade. Since the

liberalization in Germany the trade over the European Power Exchange has become more and more

important. While future products are used for price risk mitigation of the market participants short-term

markets have a direct impact on the physical balancing of demand and supply as power producer

decided upon their price signals weather production takes place or not. If prices are below the

marginal production costs power plants shut-down or decrease their power output and vice versa.

Today power trade is done on the day-ahead and intra-day market. The day-ahead auction ends at

12:00 p.m. (noon) and power for the following day (hours 0-24) can be traded in form of single hour or

block bids. In addition to this, it is possible to continuously trade for the next day in a separate auction.

Single hours and blocks can be traded continuously starting from 3 p.m. for the same or next day.

Quarterly-hour is possible starting from 4 p.m. This auction complements the quarter-hourly intra-day

trade which ends at 3 p.m. where power is exchanged for the next day in 96 intervals (hours 0-24).

At the moment the European Energy Exchange has three market regions (France, Germany/Austria

and Swiss). The market region Germany/Austria includes the area of the four German transmission

system operators (TSOs: Amprion GmbH, transpower GmbH, 50Hz, TransnetBW) and the Austrian

TSO (Austrian Power Grid). Compared to India the trading volume of the short-term markets in this

area is significant. In 2014 it has reached 263 TWh in the day-ahead market and 17 TWh hours in the

intra-day market. Trade on the day-ahead market was strongly influenced by the renewable

penetration which was around 150 TWh and has been sold to the power exchange. For comparison

the net electricity consumption in Germany in the same year has reached 512 TWh. Thus, around

51.4% of the physically delivered energy has been traded via the power exchange. In India in 2013-

2014 only 3% (30 TWh) of the generation has been sold via the power exchange as most of it is

bounded in long-term power purchase agreement (PPA) [EEX 2014, EMI 2014]. Consequently there

is a great difference between the role and impact of short-term markets in India and Germany.

However, trading volume at the power exchange in India has increased with a growth rate of 22% p.a.

in the last years.

5 The balancing group contract may be changed in the near future by the Federal Network Agency

(Bundesnetzagentur 2014a)

19 | P a g e

Price settlement at the EPEX spot market is based on the bids of market participants. The uniform

price results from the individual demand and supply curves resulting from these bids for each time

interval. The supply curve is influenced by the structure of the marginal production costs bidding

power plants. Real marginal production costs are not known, but can be estimated based on fuel and

plant type. A typical merit-order of all conventional power plants in Germany is depicted in Figure 13.

The marginal production costs especially depend on the fuel type and costs. Nuclear plants and

lignite plants are in general the cheapest plants followed by coal and natural gas power plants. Fuel

oil plants are rarely used due to very high costs. Combined heat and power (CHP) plants are able to

bid lower prices in the market as non-CHP plants of the same fuel type. This is because they can take

into account revenues from their heat production. Some plants with very high heat production

compared to their electricity production may even be able to bid with negative marginal costs. Power

plants with marginal costs below the current market price gain money. The uniform settlement price is

based on the marginal production costs of the most expensive power plant which is necessary to

cover the total demand.

Figure 13: Estimated marginal cost based merit-order for all German power plants

Source: Fraunhofer IWES

Every utility or large scale consumer can procure and every producer can sell its’ power in this

market. The market mechanism is thus responsible for balancing the demand and supply side on a

day-ahead or hour(s)-ahead base. Unexpected or unpredictable occurrences inflicting with load and

generation balance are settled in Germany by the control reserve of the system operator (explanation

in section .These are for example forecasting errors for RE production and load which are not known

before trading gate closure, power plant outages or unexpected unavailability. Accountability for not

complying with production and consumption schedules is enforced by the imbalance pricing

mechanism.

3.4.1 Scheduling

Schedules have to be transmitted from the BRP to the TSO until 14:30 of the previous day and have

to contain a balanced quarter hour performance for each quarter hour. Schedules within the German

control areas may be changed with minimum advance notice of one quarter hour to each quarter hour

0 10 20 30 40 50 60 70 80-100

-50

0

50

100

150

200

Installed capacity [GW]

Ma

rgin

al C

osts

[E

uro

/MW

h]

Merit-Order of capacity in Germany

Lignite

Coal

Natural Gas

Uran

Oil

20 | P a g e

of each day. Additionally, schedules within the control area of one TSO can be changed subsequently

until 4:00 of the following working day. Schedules can be transferred by File Transfer Protocol (FTP)

or via ISDN or by email. For the verification of the grid safety the TSO requires the schedule of every

power plant unit with a physical electrical capacity more than 100 MW until 14:30 at the previous day.

3.4.2 Spot market

Trading on the exchange spot market enables market participants to sell and buy electricity in a non-

discriminatory and anonymous environment and ensures the maximization of the social welfare

through merit-order dispatch (Jiang Wu et al.). Electricity can be traded in standardized contracts on a

day-ahead auction and a continuous intraday trading at the EPEX SPOT.

Energy traded in the power exchange markets accounted for 40% of the national electricity

consumption in the year 2013 with an increasing trend. The increase in the share can be explained

with the increase in generation from renewable energy sources and their need for day-ahead

settlement (EPEX SPOT 2014f).

Figure 14: Share of trading volume of national EPEX SPOT market in annual national (EPEX SPOT 2014f)

There are three exchange regulations, the code of conduct, the market rules and the operational

rules. This set of rules is agreed upon between the exchange operator and the market participants

and are uniformly applied to all market participants through contracts (EPEX SPOT 2014g).

The market rules organize the general exchange organization and operations procedures. They

contain information about the exchange operator, the purpose of the markets as well any fundamental

information about the exchange. The operational rules organize the details of the trading systems and

the traded products. The operational rules define e.g. tradable contracts, gate-closure-times, price

limits, order quantity, block types and further information to trade a product on the exchange. A fair

and transparent market operation is ensured by the code of conduct which regulates the behavior of

the exchange members. It also regulates the consequences when the rules are violated.

2009 2010 2011 2012 20130

10

20

30

40

50

Year

Perc

enta

ge

Percentage of annual consumpt ion

21 | P a g e

3.5 Product specifications

The sections below introduces to product details and the way of transaction and price determination

of the day-ahead auction market and the continuous intraday market at EPEX SPOT.

3.5.1 Day-ahead auctions

In a daily auction power contracts for every single hour of the next day are traded. An individual price

for every hour is determined in this auction. The sections below point out orders, product details and

the price determination.

3.5.2 Orders

Orders are submitted by exchange members via the ETS client. The orders placed in the trading

system need to fulfill specified conditions. Traders in the EPEX SPOT day-ahead market can place

single-contract orders or block orders. All orders and transactions are anonymous. The order book is

closed each day at noon, from when on orders cannot be changed and are binding. Single-contract

orders are only valid for one of the 24 hours and block orders for a defined combination of hours

(EPEX SPOT 2014b). Every hour that is intended to be traded individually needs an own single

contract order.

Single contract orders are placed as a monotonous demand curve with up to 256 price-quantity

combinations that limit the volume at a specific price. The curve is interpolated linearly between the

entered price-quantity combinations as in the following graph. It shows a generic offer curve with it’s

up to 256 price-quantity combinations.

Figure 15: Example of an individual offer curve at EPEX SPOT representing the up to 256 possible price-

quantity combinations

Buy volumes have no sign, sell volumes are signed with a minus. A monotonous curve means that an

increasing amount to buy must be entered with a decreasing price and an increasing amount to sell

must be entered with an increasing price. Prices are specified in steps of 0.1 EUR/MWh and volumes

in steps of 0.1 MW. Negative prices must be indicated with a minus. The entered prices must lie in-

P1

P2

P3

P256

P255

P254

Q1 Q2 Q3 Q254 Q255 Q256

…

22 | P a g e

between the minimum and the maximum price of the exchange market (table product details below)

(EPEX SPOT 2014b).

Different types of order can be placed in the market for different types of orders (EPEX SPOT 2014b):

Unlimited orders (single-contract or block) also called market orders or price-independent

orders. They must contain equal quantities for the minimum and the maximum order price

boundaries. These orders are fulfilled at any price.

Limited order (single-contract or block) have a price limit and are only executed if the market

prices matches the specified price or is better for the trader

All or none block orders are only executed if the market price for the entire volume matches

the specified price or is better for the trader. Otherwise the order would be rejected

Price-independent orders are placed e.g. by the TSO for the renewable energy feed-in in their own

balancing group6 or by market participants who aim towards a physical fulfillment of financial futures7

(EPEX SPOT 2014b),(EEX 2012).

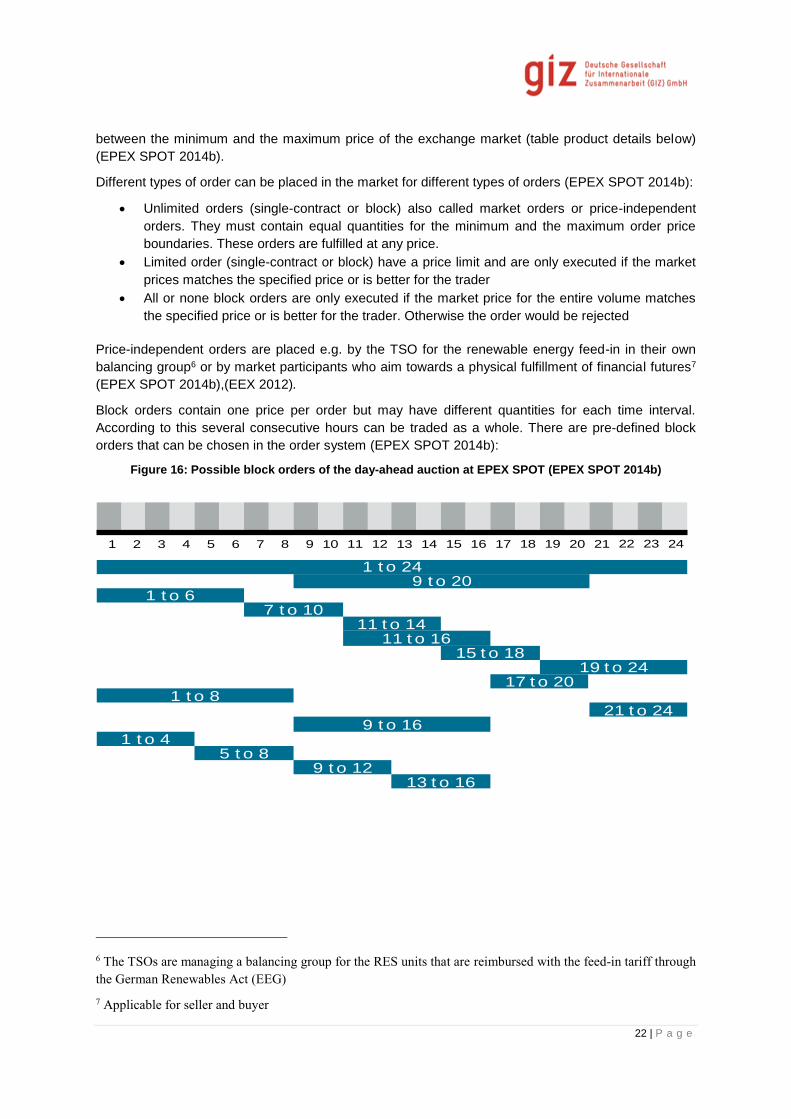

Block orders contain one price per order but may have different quantities for each time interval.

According to this several consecutive hours can be traded as a whole. There are pre-defined block

orders that can be chosen in the order system (EPEX SPOT 2014b):

Figure 16: Possible block orders of the day-ahead auction at EPEX SPOT (EPEX SPOT 2014b)

6 The TSOs are managing a balancing group for the RES units that are reimbursed with the feed-in tariff through

the German Renewables Act (EEG)

7 Applicable for seller and buyer

1 t o 249 t o 20

1 t o 67 t o 10

11 t o 1411 t o 16

15 t o 1819 t o 24

17 t o 201 t o 8

21 t o 249 t o 16

1 t o 45 t o 8

9 t o 1213 t o 16

1 3 4 5 6 72 8 10 11 12 13 149 15 17 18 19 20 2116 22 23 24

23 | P a g e

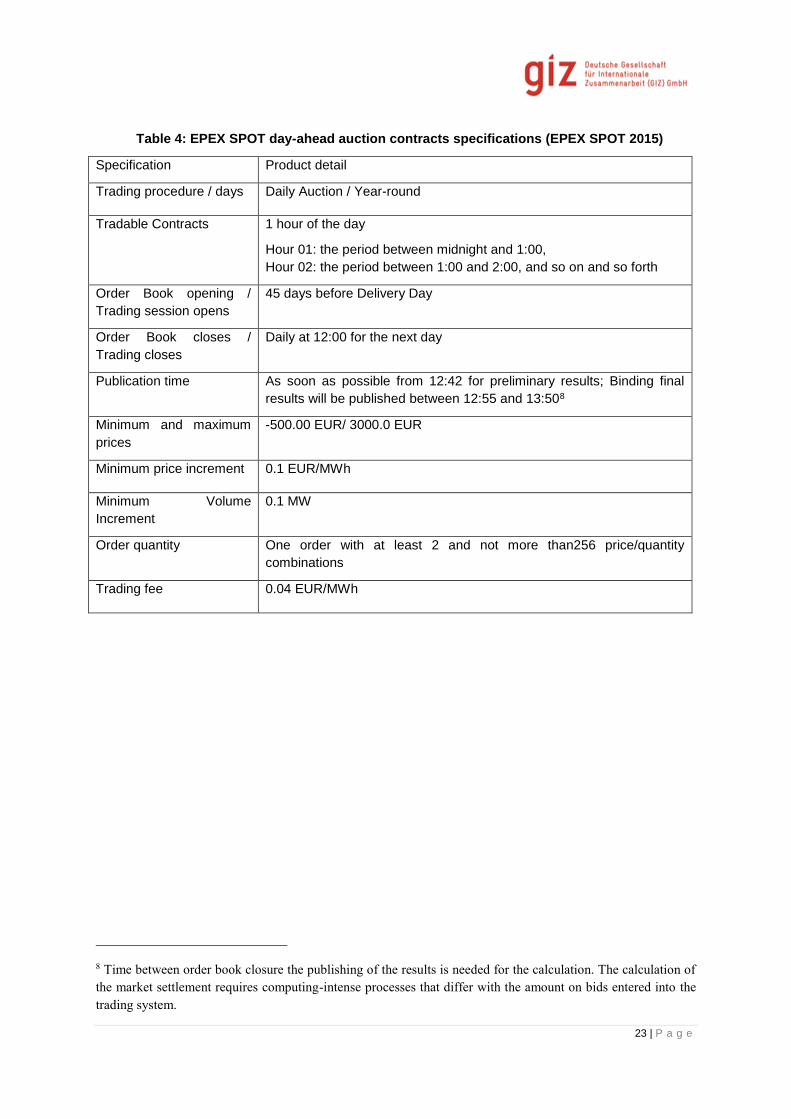

Table 4: EPEX SPOT day-ahead auction contracts specifications (EPEX SPOT 2015)

Specification Product detail

Trading procedure / days Daily Auction / Year-round

Tradable Contracts 1 hour of the day

Hour 01: the period between midnight and 1:00,

Hour 02: the period between 1:00 and 2:00, and so on and so forth

Order Book opening /

Trading session opens

45 days before Delivery Day

Order Book closes /

Trading closes

Daily at 12:00 for the next day

Publication time As soon as possible from 12:42 for preliminary results; Binding final

results will be published between 12:55 and 13:508

Minimum and maximum

prices

-500.00 EUR/ 3000.0 EUR

Minimum price increment 0.1 EUR/MWh

Minimum Volume

Increment

0.1 MW

Order quantity One order with at least 2 and not more than256 price/quantity

combinations

Trading fee 0.04 EUR/MWh

8 Time between order book closure the publishing of the results is needed for the calculation. The calculation of

the market settlement requires computing-intense processes that differ with the amount on bids entered into the

trading system.

24 | P a g e

3.5.3 Price determination

The orders are auctioned daily after the closure of the order book. The price is determined through

matching of the exchange members' aggregated supply and demand curves9 for each time interval

consisting of single orders and block orders. Block orders are only considered to be part of the

aggregated demand and supply curves if they can be executed completely. The price determined by

the trading system is the price at which the highest volume will be executed, the so-called market

clearing price. Afterwards, the price is determined considering the market-coupling with other spot

market auctions. The consideration of all constraints can lead to a different market price since the

aggregated demand and supply curves may differ from the initial solution. The market clearing price

will be set where both curves intersect. In this point the traded volume will be the highest, which is

also called quantity allocation. This entire process of price determination is called market clearing

(EPEX SPOT 2014b).

The market price and all order prices after price matching and quantity allocation are rounded to

0.01 EUR/MWh. For that purpose the exchange member's interest is assumed to be linear between

two price-quantity combinations. The matching algorithm also matches the prices with other market

areas, including network constraints on subsea cables. The matching algorithm executes sell orders

that are lower or equal to the market price and buy orders above or equal the market price. Orders

equal to the market price may be partially executed or not at all. If the matching algorithm does not

generate a valid market price (e.g. insufficient liquidity) a second auction is performed. This should

give the exchange members the chance to change their orders to improve the situation10. The results

of the joint German/Austrian market area shall be published and validated not later than 14:0011

(EPEX SPOT 2014b).

3.5.4 Post trading period

In the post trading period the market participants receive notice from the exchange operator about the

traded amounts. The exchange members are responsible for transferring the market results into

schedules for the TSO themselves. The exchange members forward the results to the corresponding

BRP for the creation of schedules. BRPs have to fill in the form for the schedule using the exchange

operator as a counterpart to balance positions. The energy exchange is a balancing group itself. The

traded amount on the exchange has to match the amounts in the exchange schedule of the BRP. If

the schedules are not balanced, they are rejected by the TSO, preventing imbalances prior to

production.

The BRP’s equilibrium of physical production, consumption and trading is covered by the balancing

group contract. Ultimately, trading on the exchange is a separate process to the obligations from the

balancing group contract.

9 Aggregated curves are the sum of all individual curves (demand or supply). Each one of them can consist of up

256 price-quantity combinations

10 The second auction is performed after the publishing of the results before the start of the intraday trading.

Second auctions for EPEX SPOT day-ahead markets are not happening often. In fact, the requirement of a

second auction is a sign of illiquidity of the markets which is not the case in the EPEX SPOT day-ahead market.

11 Including the second auction and before the start of the intraday trading.

25 | P a g e

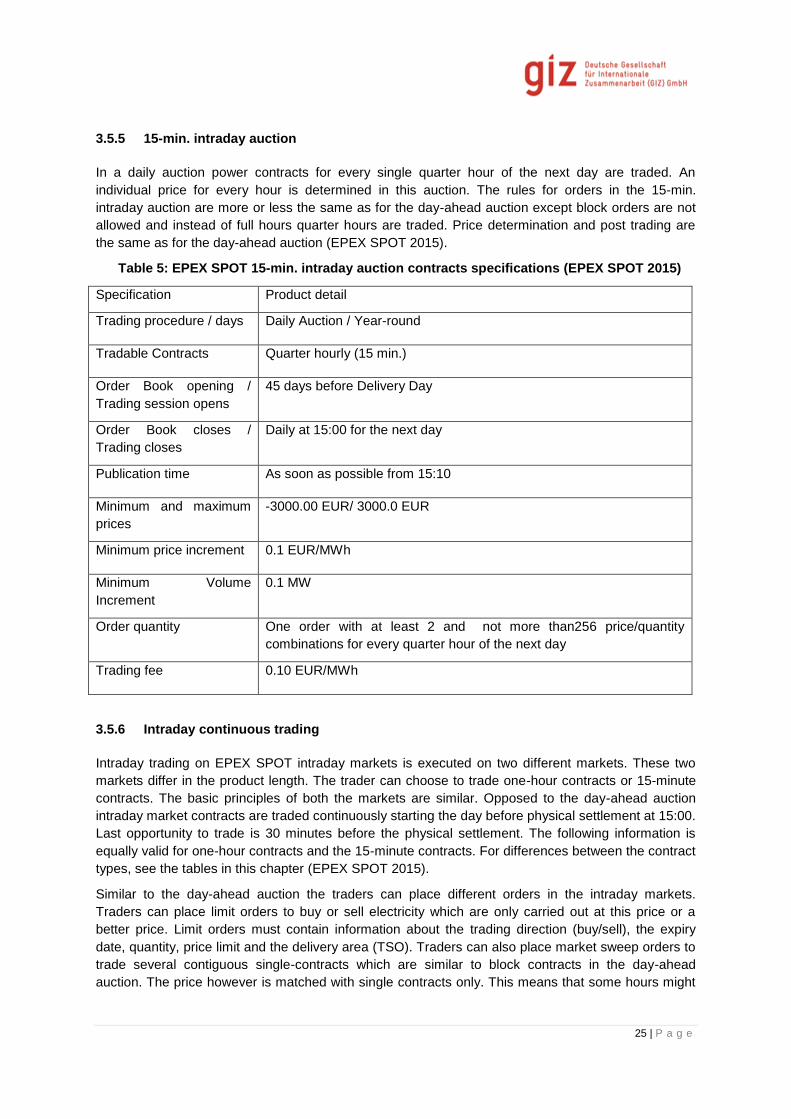

3.5.5 15-min. intraday auction

In a daily auction power contracts for every single quarter hour of the next day are traded. An

individual price for every hour is determined in this auction. The rules for orders in the 15-min.

intraday auction are more or less the same as for the day-ahead auction except block orders are not

allowed and instead of full hours quarter hours are traded. Price determination and post trading are

the same as for the day-ahead auction (EPEX SPOT 2015).

Table 5: EPEX SPOT 15-min. intraday auction contracts specifications (EPEX SPOT 2015)

Specification Product detail

Trading procedure / days Daily Auction / Year-round

Tradable Contracts Quarter hourly (15 min.)

Order Book opening /

Trading session opens

45 days before Delivery Day

Order Book closes /

Trading closes

Daily at 15:00 for the next day

Publication time As soon as possible from 15:10

Minimum and maximum

prices

-3000.00 EUR/ 3000.0 EUR

Minimum price increment 0.1 EUR/MWh

Minimum Volume

Increment

0.1 MW

Order quantity One order with at least 2 and not more than256 price/quantity

combinations for every quarter hour of the next day

Trading fee 0.10 EUR/MWh

3.5.6 Intraday continuous trading

Intraday trading on EPEX SPOT intraday markets is executed on two different markets. These two

markets differ in the product length. The trader can choose to trade one-hour contracts or 15-minute

contracts. The basic principles of both the markets are similar. Opposed to the day-ahead auction

intraday market contracts are traded continuously starting the day before physical settlement at 15:00.

Last opportunity to trade is 30 minutes before the physical settlement. The following information is

equally valid for one-hour contracts and the 15-minute contracts. For differences between the contract

types, see the tables in this chapter (EPEX SPOT 2015).

Similar to the day-ahead auction the traders can place different orders in the intraday markets.

Traders can place limit orders to buy or sell electricity which are only carried out at this price or a

better price. Limit orders must contain information about the trading direction (buy/sell), the expiry

date, quantity, price limit and the delivery area (TSO). Traders can also place market sweep orders to

trade several contiguous single-contracts which are similar to block contracts in the day-ahead

auction. The price however is matched with single contracts only. This means that some hours might

26 | P a g e

be executed and some are not12. Limit orders must contain information about the trading direction

(buy/sell), the expiry date, quantity, price limit and the delivery area (TSO). In addition to sweep

orders, pre-defined block orders can be placed (EPEX SPOT 2014b):

Block Base load covering hours 1 to 24

Block Peak load covering hours 9 to 20

The order book is open twenty-four hours a day throughout the year. EPEX SPOT however has the

right to close the order at any time. The information from the order book communicated from the

exchange to the exchange members for each contract during the trading session. This includes all

bids and ask limit order, details of the last trade, price, quantity and the time of execution. The single

contract orders (including sweep orders) are entered in a central open and anonymous order book.

Block order are handled in a separate order book. Orders are submitted electronically to the trading

system (EPEX SPOT 2014b).

Depending on the order’s price limit and quantity and on the order book configuration, any single

contract within the time range may not be executed since it cannot be matched with a counter

position. This means that contracts in some hours are executed where others are not. In addition to

this the executed volume may vary for each individual single contract since it can be possible that the

counter position does not have the matching volume. The orders placed in the trading system need to

fulfill specified conditions. Prices in limit orders must lie in-between the minimum and the maximum

price of the exchange market (see tables lower in this chapter). Negative prices must be indicated

with a “-“. Prices must be rounded to 0.01 EUR/MWh. Orders can be entered with the following