Embed Size (px)

Citation preview

1

Market Discipline in the Secondary Bond Market:

The Case of Systemically Important Banks

Elyas Elyasiani

Fox School of Business and Management

Temple University

Jason M. Keegan*

Supervision, Regulation, and Credit

The Federal Reserve Bank of Philadelphia

This Version:

January 17, 2017

JEL Classification: G01, G2, G21, G28

Keywords: Bank Risk; Financial Crisis; U.S. Bank Holding Companies; Risk Management;

Market Discipline

*The views expressed here are those of the authors and do not necessarily reflect those of the

Federal Reserve Bank of Philadelphia, the Board of Governors of the Federal Reserve System, or

the Federal Reserve System.

2

Abstract

We investigate the association between the yields on debt issued by U.S. Systemically Important

Banks (SIBs) and their idiosyncratic risk factors, macroeconomic factors, and bond features in

the secondary market. Although greater SIB risk-levels are expected to increase debt yields

(Evanoff and Wall, 2000), prevalence of government safety nets complicates the market

discipline mechanism, rendering the issue an empirical exercise. Our main objectives are

twofold. First, we study how bond-buyers reacted to elevation of SIB and macroeconomic risk

factors over the recent business cycle. Second, we investigate the degree to which the

proportions of the variance in yields explained by these two risk categories changed across the

phases of the cycle. Our data include over 8 million bond trades across 26 SIBs. We divide our

sample period into the pre-crisis (2003:Q1 to 2007:Q3), crisis (2007:Q4 to 2009:Q2), and post-

crisis (2009:Q3 to 2014:Q3) sub-periods to contrast the findings. We obtain several results. First,

bond-buyers do react to changes in the SIB risk factors (leverage, credit risk, inefficiency, lack of

profitability, illiquidity, and interest rate risk) by demanding higher yields. Second, bond

buyers’ responses to risk factors are sensitive to the phase of the business cycle. Third, the

proportion of variance in yields driven by SIB-specific and bond-specific risk factors increased

from 23% in the pre-crisis period to 47% and 73% during the crisis and post-crisis periods,

respectively. These findings indicate that the force of market discipline improved greatly during

the crisis and post-crisis periods, at the expense of the macroeconomic factors. The

strengthening of market discipline in the crisis and post-crisis periods, despite the

unprecendented regulatory intervention in the form of quantitative easing (QE), troubled asset

relief program (TARP), large bail outs and generally accomodative fiscal and monetary policies

adopted during these periods, demonstrates that regulatory intervention and market discipline can

work in tandem.

3

1. Introduction

We investigate how the yield-spreads1 on the debt issued by U.S. Systemically Important

Banks (SIBs) in the secondary market are associated with their idiosyncratic risk,

macroeconomic factors, and bond-specific features across the pre-crisis (2003:Q1 to 2007:Q3),

crisis (2007:Q4 to 2009:Q2), and post-crisis (2009:Q3 to 2014:Q3) phases of the recent business

cycle.2 We focus on the SIB population because, if mandatory debt issuance were to become a

part of the regulatory framework, as recommended e.g., by the joint report submitted to Congress

by the Board of Governors of the Federal Reserve System and the Treasury Secretary (Board and

Treasury, 2000), and by Lang and Robertson (2002), it would likely impact this group of bank

holding companies (BHCs) to the greatest extent. The SIB designation is an indication that the

failure of these institutions could have serious adverse effects on the global financial markets

and, thus, could elevate systemic risk.

Appendix A provides a list of the current SIBs, broken out by global (G-SIBs) and

domestic (D-SIBs) designations. G-SIB is an official designation by the Financial Stability

Board (FSB) and the Basel Committee on Banking Supervision (BCBS) based on a framework

that accounts for the contribution to systemic risk. The methodology equally weights each of the

five categories of systemic importance: [1] size, [2] cross-jurisdictional activity, [3]

interconnectedness, [4] substitutability/financial institution infrastructure, and [5] complexity.3

1 The yield spread is the difference between the yield to maturity on a bond and the rate on a Treasury security with

an identical maturity and similar other features.

2 According to the NBER, the 2001 recession reached its trough in November 2001, and the business cycle reference

dates indicate that the peak and trough of the most recent business cycle are December 2007 and June 2009,

respectively. The NBER list of U.S. business cycle expansions and contractions can be found at:

http://www.nber.org/cycles.html

3 See the updated assessment methodology and the higher loss absorbency requirements at

http://www.bis.org/publ/bcbs255.pdf

4

D-SIB is not an official designation by the FSB or BCBS, yet it is implicitly assumed that these

other large U.S.-based BHCs that participate in the Dodd-Frank Act Stress Test (DFAST) and

Comprehensive Capital Analysis and Review (CCAR) are systemically important within the

U.S., if not globally. Thus, we include these institutions in our analysis.

The crux of this paper, from a policy perspective, is to examine the level, as well as the

change, in the explained variation of the SIB debt yields attributed to SIB risk factors, versus that

driven by the macroeconomic factors, across the phases of the business cycle. The fundamental

question we seek to answer is: Do bond investors respond to SIB-specific risk factors, and, if so,

to what extent are these factors responsible for bond yield movements, compared to

macroeconomic factors? The relative power of SIB-specific and macroeconomic risk factors is

important because, even if bond-buyers do show sensitivity to firm risk characteristics, when the

market-wide factors largely dominate the yield-spread behavior, the role of market discipline

will be diminished. By examining the proportions of explained variance in yield-spreads

attributed to macroeconomic and idiosyncratic risk factors, we also shed light on the extent of

complementarity versus substitutability of regulation and market discipline. Our findings help

policy makers and regulators in understanding bond investor behavior in response to increased

SIB-specific and macroeconomic risks in an environment similar to that of the recent business

cycle.

The question of whether, and to what extent, bond investors respond to SIB-specific risks

is an important empirical issue because, if it is shown that bond traders do respond to bank risk

levels, then yield-spreads of bank debt could help the regulators, bank managers, and investors in

the bond market understand how markets react to changes in risk and help them with their

decisions. From a policy perspective, regulators could use yield-spreads on bank debt as an early

5

warning sign and could set thresholds for yield-spreads as a trigger for regulatory action.

Investors and bank managers could also use the information in their choice of a portfolio

composition and the timing of, and yield offering on, debt issuance. The bank-specific risk

measures used here are CAMELS proxies, described in more detail in section 3. CAMELS

ratings, designed and monitored by the Federal Reserve and other banking regulators,

characterize Capital adequacy, Asset quality, Management, Earnings, Liquidity, and Sensitivity

to interest rate risk. This rating system provides a holistic assessment of a bank’s financial

conditions and level of risk. It is used by regulators to form a composite rating indicating the

overall performance and risk management practices of a financial institution.4

We obtain data on all SIB trades from 2003:Q1 through 2014:Q3. We begin the analysis

in 2003 because our interest lies in the most recent business cycle. In this way, we also avoid the

impact of the 2001 recession, such as the market disturbances and systemic shocks associated

with the 911 terrorist attacks, as well as the changes in accounting rules associated with The

Sarbanes-Oxley Act (2002). We segment the data into subordinated notes and debentures (SND)

and senior bonds (non-SND). It is necessary to separate the two bond types due to the junior

rank of SND compared to senior debt with respect to repayment status in the case of BHC

failure.

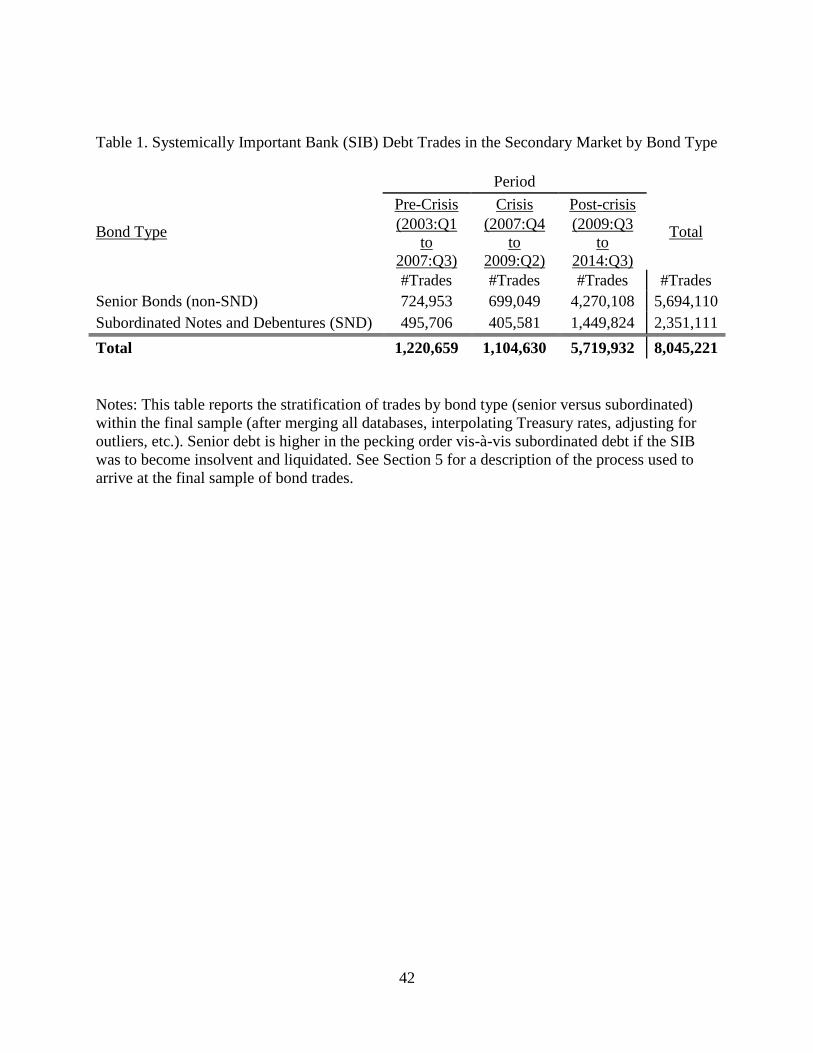

Table 1 reports the number of trades in the sample by bond type.5

We focus on the secondary bond market because the high volume of transactions in this

market (liquidity) provides extensive variation and allows us to determine whether secondary

4 DeYoung et al. (2001) establish the link between CAMEL ratings and market prices of subordinated notes and

debentures. Since CAMEL(S) ratings are private information produced by bank examiners, one would expect that

bond traders would proxy for CAMEL(S) ratings using publically available information.

5 We exclude Junior (and Junior Subordinate) debt as well as Senior Secured debt due to low levels of liquidity

compared to the other categories (together, the categories comprise less than 0.01% of all secondary market trades

over the period of study).

6

market participants behaved “rationally” during the sample period, in response to change in SIB-

specific and macroeconomic risk factors. The choice of the 2003:Q1-2014:Q3 sample period

allows us to determine the proportion of explained variance in yield-spreads that can be

attributed to macroeconomic factors versus the proportion driven by SIB-specific and bond-

specific features, and to investigate how this proportion changed over the pre-crisis, crisis, and

post-crisis periods. This variance decomposition is of special interest to regulators because the

greater the force of the SIB-specific factors and market discipline, which is beyond the

regulators’ control, the less powerful they will be in influencing bond yields. Moreover, if yield-

spreads are used as an early warning indicator of SIB risk, the thresholds that trigger regulatory

action will need to be tailored to the phase of the business cycle.

[Insert Table 1 Here]

We obtain a number of results. First, we find strong evidence of market discipline with

respect to SIB-specific risks in the secondary bond market. This finding is important because of

its policy implications on mandatory SND issuance by banks. Second, we find that the strength

of market discipline varied considerably across the phases of the business cycle. Specifically,

market discipline in the form of sensitivity of debt yields to bond-specific and SIB-specific risk,

was at a relatively low scale during the pre-crisis period, compared to the crisis and post-crisis

periods. This finding indicates a greater level of risk sensitivity and a lower degree of risk-

tolerance (greater risk aversion) on the part of bond investors during the latter two phases of the

cycle.6 In other words, in the latter two periods, bond investors either made a more accurate

assessment of risks in the U.S. financial markets and/or they demanded a greater risk premium

6 Alternatively, this result could indicate that bond holders had a false sense of security during the pre-crisis period

(mismeasurement error), rather than failing to react to risk.

7

per unit of additional risk due to their elevated risk aversion, at least for some risk measures.

Third, in terms of the magnitude of the effects (economic significance), the impact on

yield-spreads due to a one standard deviation increase in leverage, credit risk, and liquidity

measures are the largest during the crisis period, reflecting greater risk premiums per unit of risk.

This is likely to be due to investors’ better risk assessment or greater risk aversion owing to fear

and pessimism. Fourth, macroeconomic factors drive a smaller proportion of the explained yield

variance during the crisis and post-crisis periods, compared to the pre-crisis period. In fact, the

percentage of variance in yield-spreads explained by SIB and bond-specific factors climbs from

23% in the pre-crisis period, to 47%, and then to 73%, across the crisis, and post-crisis periods.

This implies a considerable strengthening of market discipline with respect to idiosyncratic vis-a-

vis macroeconomic factors, in particular in the post-crisis period.

Our finding that bond-specific and SIB-specific attributes are major drivers of yield-

spreads, provides support for the proposal of mandatory issuance of bank debt and the use of

yield-spreads as “early warning” indicators in regulatory policies that leverage market discipline.

This policy has received interest both in academic (for e.g., Evanoff et al., 2007; Nguyen, 2013)

and regulatory circles (Lang and Robertson, 2002). With our results, policy makers will be able

to identify the risk factors to which bond investors are likely to respond, and the extent of their

sensitivity. They can then leverage this effect when formulating policies, procedures, and

guidelines for bank regulation.

The rest of the paper proceeds as follows. In Section 2, we review the literature. In

Section 3, we describe the econometric model and introduce the variables in the model. In

Sections 4 and 5 we outline the hypotheses, describe the data sources and discuss descriptive

statistics. In Sections 6 and 7, we review the methodology and report results. Section 8

8

concludes.

2. Literature Review

The concept of how the behavior of market participants can serve as a check on firm risk-

taking is broadly referred to as market discipline. As Flannery (2001) explains, market discipline

requires two “distinct components:” [1] market monitoring, which suggests that market

participants obtain transparent and accurate data on the health of the monitored institution, and

[2] market activism and influence, suggesting that, once investors become privy of a firm’s

financial health, they do act on the information and, in turn, their actions do exert a significant

impact on the behavior (i.e., risk taking) of the monitored institutions. The U.S. banking

industry provides an attractive setting for testing the impact of market discipline due to the

extensive and standardized reporting requirements on this industry set forth by the Federal

Financial Examination Council (FFIEC). Bank regulators, investors, researchers, and various

other stakeholders can use the information available through these regulatory required reports to

learn about the banks and react accordingly. Bond-investors tend to use the financial statement

information supplied by the banks, in conjunction with macroeconomic and bond-specific

information, to determine the overall level of risk embodied in the bond; the riskier a bond is, the

larger the risk premium demanded by bond-holders is expected to be. Assuming transparency,

reactions of market participants would serve to limit the riskiness of BHCs. However,

government assurances, such as “too big to fail” (TBTF) policy, bail outs, emergency lending

facilities (the discount window, Term Auction Facility, Primary Dealer Credit Facility, Term

Securities Lending Facility, the Troubled Asset Relief Program (TARP)), and other explicit and

implicit safety-nets can weaken, if not eliminate, the impact of market discipline since market

participants will be less vigilant when their investment is guaranteed, regardless of bank

9

solvency status (Flannery, 1998).

The stakeholders in market discipline include shareholders (in particular institutional),

bond holders, depositors, counterparties in derivative positions, and bank auditors, among others.

In this study, we focus on bank debtholders as enforcers of market discipline. Bank debtholders

have been the focus of several prior studies.7

Flannery and Sorescu (1996) use data on SND spreads for BHCs from 1983 to 1991 and

breakout the SND data into three separate sub-samples with different degrees of government

protection. The authors find that the bank’s accounting ratios have little to no effect on SND

spreads during the earliest two subperiods of: [1] 1983-1985, during which time the “TBTF

doctrine was most credible;” and [2] 1986-1988, when the regulators began to reduce implicit

protection of SND holders. However, they find a change in investor behavior during the 1989-

1991 sub-period, when conjectural government guarantees were no longer present, and SND

holders at failed financial insitutions were realizing losses. Specifically, the authors find that

bond investors do account for bank risk increases in the form of lower asset quality and greater

leverage, by demanding higher yeild spreads, during this last sub-period.

Morgan and Stiroh (1999) examine nearly 600 fixed-rate bond issuances by banks and

BHCs from 1993 to 1998. They include bond ratings, time effects (to control for

macroeconomic factors), and a litany of BHC-specific factors including asset and liability

characteristics, as explanatory variables in their model. They obtain several results. First, the

banking industry prices debt similarly to non-bank industries in the sense that the impact of

7 There have also been studies that empirically estimate the risk-spread relationship for non-U.S. banks, including

Canadian (Caldwell, 2007), Japanese (Imai, 2007), Swiss (Birchler and Facchinetti, 2007), and European (Bruni and

Paterno, 1995; Sironi, 2003) banks. Zhang et al. (2014) provide a good overview of the international evidence and

perform a study of yield spreads of 631 sub-debt issuances in UK’s primary market between 1997 and 2009. These

authors find that the yield spreads on this sub-debt do vary with the ratings assigned by traditional rating agencies.

Despite this relationship, they find that some accounting measures, such as bank leverage, net loans to total assets,

and liquidity ratio, among others, do not hold significant explanatory power for yield spreads.

10

credit ratings on bond spreads are virtually identical between the two industries, despite major

dissimilarities in terms of regulation, leverage, and the uniqueness of bank assets and liabilities.

Second, market participants do account for bank-specific risk factors when pricing debt. Third,

larger banks experience market discipline to a lesser degree, than the smaller banks. The

rationales offered for this finding is that large banks considered to be too-big-to-fail (TBTF)

benefit from implicit deposit insurance, which counterbalances some of their risk, and/or market

participants fail to properly gauge bank risk due to opacity of bond issuances.

Jagtiani et al. (1999) study the relationship between the risk levels and the return of bonds

issued by some of the largest U.S. commercial banks. Their sample period runs from 1992

through 1997, where they study year-end secondary market observations of subordinated debt for

19 large commercial banks and 39 BHCs. They find that risk is similarly priced for BHCs and

banks, in the sense that bond holders respond to risk characteristics of the issuers in an equally

potent manner for the two groups.

Balasubramnian and Cyree (2011) use secondary market transactions of SNDs during the

1994 to 1999 period8 and find two main results. First, a decrease in the sensitivity of SND yield-

spreads to bank risk factors such as loans to assets, non-performing loans to total loans, net

charge-offs, etc., following the issuance of trust-preferred securities (TPSs)9 in 1996. This result

8 They end the sample in 1999 to remain consistent with some prior studies, to avoid possible data issues related to

the enactment of the Financial Services Modernization (The Gramm-Leach-Bliley) Act in 1999, the Regulation Fair

Disclosure (Reg FD) in 2000, and the Sarbanes-Oxley Act in 2002, and to avoid the internet bubble, Enron failure,

and the 911 terrorist attacks.

9 Trust preferred securities are securities issued from a trust set up by a BHC. The trust generally makes quarterly

distributions to the TPS holders. TPSs are subordinated to other debt, but are senior to preferred and common

stocks. On October 21, 1996 the Board of Governors of the Federal Reserve System issued a press release

approving the capital treatment of TPSs as Tier 1 capital for BHCs, subject to a 25% limit (together with other

cumulative preferred stock). Due to the capital treatment, dividend deferral rights (allows deferral for 20 quarters),

and favorable tax treatment (dividends are tax deductible for the BHC), the issuance of TPSs was an attractive way

for BHCs to raise capital without stock dilution. For a high level overview of TPSs, see “A Guide to Trust Preferred

Securities” by Alan Faircloth (Federal Reserve Bank of Atlanta) available through the following link:

11

is partially due to the tax shield and flexibility in meeting capital regulatory requirements

associated with TPS, which provide an additional buffer to SNDs from default risk. Second, a

paradigm shift occurred after the bail-out of Long Term Capital Management (LTCM) in 1998 in

the sense that off-balance sheet exposure became a determinant of SND yield-spreads, because

bond market participants became more cognizant of banks’ “hidden leverage.”

Balasubramnian and Cyree (2014) use daily data for SND transactions in the secondary

market, and firm-specific, market-level, and bond-specific variables to examine the impact of the

Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA) of 2010 on market

discipline. They find that the passage of the Act decreased the size-discount on yield-spreads for

the TBTF and systemically important financial institutions (SIFI). The rationale is that the

DFA’s intention to end TBTF policies (e.g., a living will), resulted in a decrease in the size-

discount for the large BHCs for which the Federal Reserve Board conducts stress tests. In terms

of magnitude, they find a 94% decrease in the size-discount associated with TBTF institutions

along with a 47% discount in the size discount across all banks. They attribute the increase in

yield-spreads after the passage of the DFA (i.e., reduction in the size discount) to an

improvement in market discipline due to the policy of reduced support for TBTF banks.

We follow the Balasubramnian and Cyree (2014) empirical methodology to an extent, but

introduce several important differences. First, our objective is to create an industry benchmark

for SIB bond trades, while their focus is on the change in the size-discount associated with the

passage of the Dodd-Frank Act (DFA). Second, our sample covers over 8 million bond trades,

spanning from January 2003 through September 2014, while their work is based on a smaller

sample of around 17,000 observations from June 2009 to December 2011. Third, we include all

https://www.frbatlanta.org/banking/publications/financial-update/2014/q1/viewpoint/spotlight-guide-trust-preferred-

securities.aspx

12

daily bond trades as separate observations, indirectly weighting each firm’s debt to the extent to

which it is traded in the market. In contrast, they use an equal-weighting scheme of bond trades,

regardless of intra-day trade frequency, as they calculate the daily average yield-spread when

they have multiple transactions for the same bond. Fourth, keeping our goal of creating an

industry benchmark model in mind, we include multiple bond types, including subordinate

(SND) and senior (non-SND) whereas Balasubramnian and Cyree focus solely on SNDs.

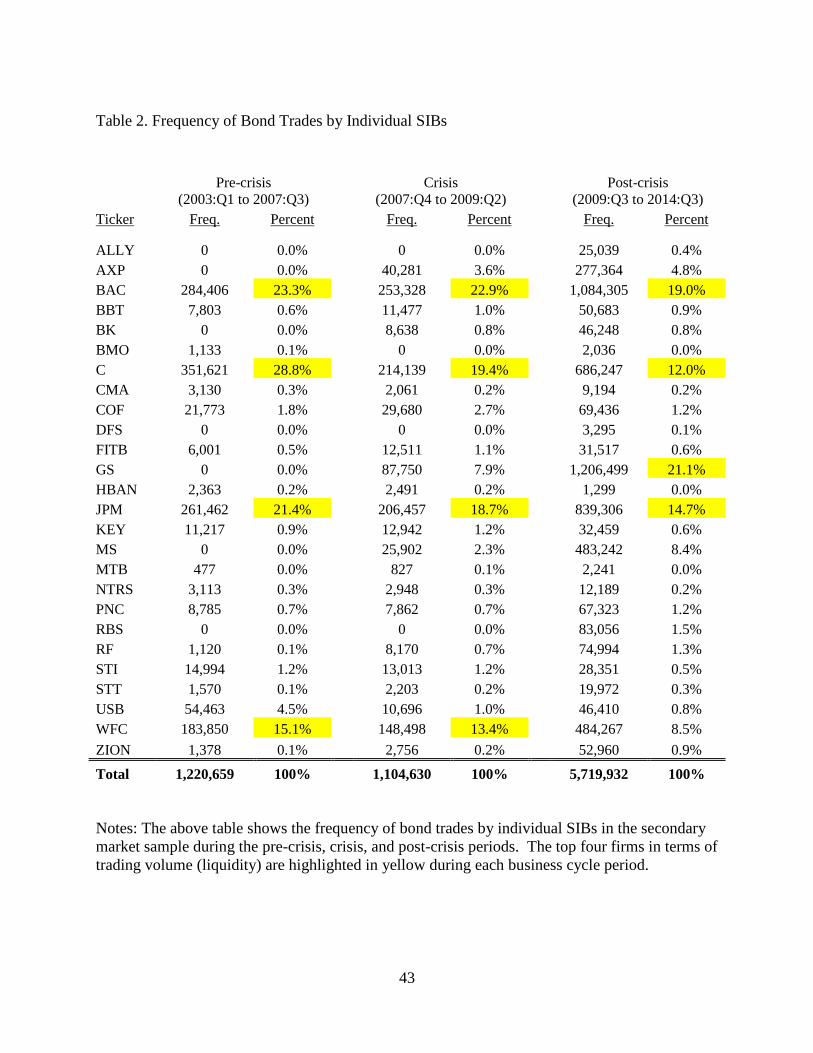

The frequency of bond trades by SIBs across our pre-crisis, crisis, and post-crisis sub-

samples are reported in Table 2. In this table, the top four firms in term of trading volume are

highlighted.

[Insert Table 2 Here]

The area of market discipline that we focus on is the pricing of BHC debt in the

secondary market. The notion of financial regulators using mandatory issuance of bank debt to

mitigate risk-taking at these institutions has been investigated e.g., by Jagtiani et al., 1999; Bliss

and Flannery, 2002; and Lang and Robertson, 2002, though the findings remain in dispute. The

mandatory issuance of BHC debt can mitigate risk taking through two channels: [1] market cost

on the debt-issuing institution through the primary issuance, and [2] greater debt yields in the

secondary market in response to increased riskiness of the issuing bank and the use of it by

regulators as a risk indicator for regulatory action, as detailed below. The focus of this paper is

on the second channel. According to Lang and Robertson (2002), this channel can “become an

extremely useful tool in the regulatory effort to increase market discipline in the banking

industry.” The rationale is that, as risk-taking at a BHC increases, bond traders will demand a

greater risk premium when purchasing the debt in the secondary market. Since the bond yields

are indicative of the overall risk levels of the issuing institution, regulators can flag elevated

13

yields as an “early warning” sign and subsequently take regulatory action.

Our research is timely because, given the recent financial crisis, innovative methods to

regulate SIBs have garnered even greater attention. Also, the size and the trading volume of the

overall bond market have increased tremendously. According to the Securities Industry and

Financial Markets Association (SIFMA), the amount of outstanding corporate debt and average

daily trading volume have grown from $4.3 trillion and $18 billion in 2003, to over $7.8 trillion

and $26.7 billion, respectively, by 2014. The growth in size and liquidity of the corporate bond

market is partly due to advancements in technology, such as the advent of high frequency trading

(HFT), which has increased the transparency of the bond market. In fact, in 2014, bank debt

reached all-time highs and global banks more than doubled debt issuance, from the prior year, to

nearly $275 billion primarily due to the Basel III requirement of increased bank capital in the

form of both debt and equity (Thompson, 2015). Changes in the regulatory landscape from

Basel III, coupled with greater transparency in the market for corporate debt, make our study

even timelier as bank regulators attempt to find the optimal shares of debt and equity capital to

be held by large institutions.

The aforementioned studies have some common themes. In general, these studies use

yield-spreads of bonds to measure market discipline and include some combination of institution,

security, and macroeconomic-specific risk factors as determinants of yield-spreads. They also

study the impact of bank risk measures on yield-spreads within the context of the broader

regulatory environment. For example, when the government safety net expands (as in the case of

bailouts), or new hybrid securities are introduced (as in the case of TPSs), interpretation of bank

risk measures can be impacted. Unusual volatility during and after the financial crisis in the

macroeconomic realm, and the keen focus by regulators, investors, and other stakeholders on

14

idiosyncratic risk makes it theoretically unclear which countervailing force is the primary driver

of yield-spreads in the secondary market. We develop our econometric model with these

elements in mind.

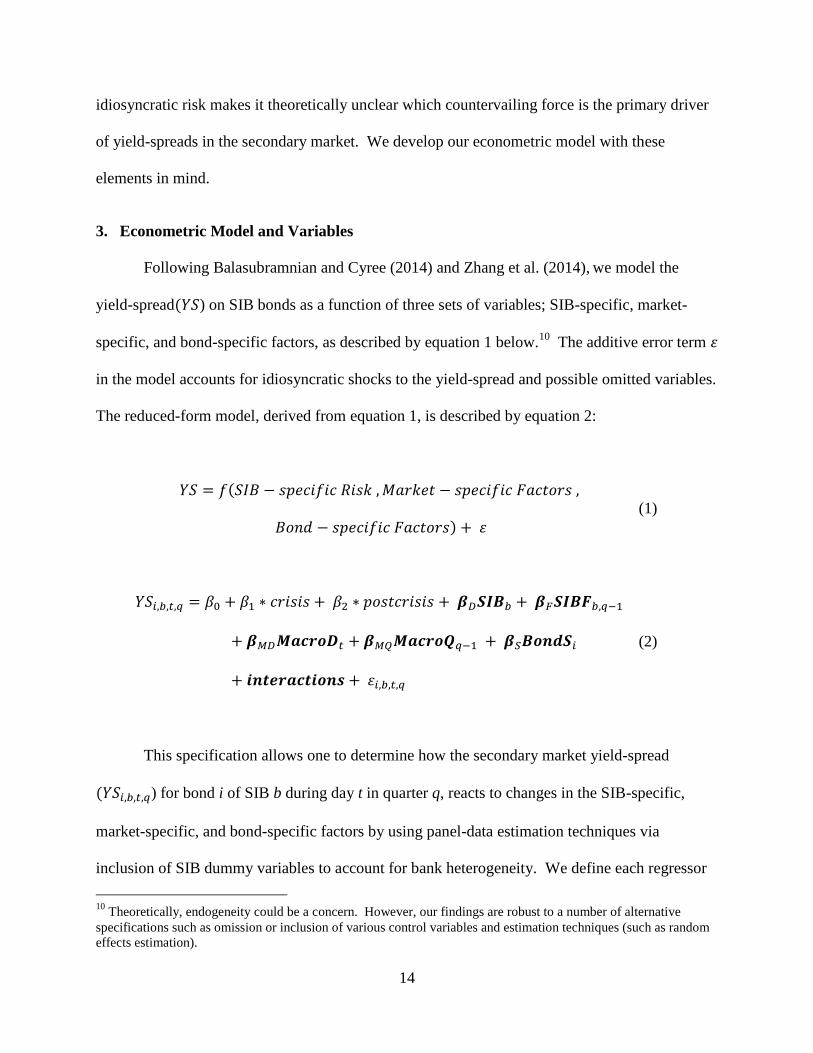

3. Econometric Model and Variables

Following Balasubramnian and Cyree (2014) and Zhang et al. (2014), we model the

yield-spread(𝑌𝑆) on SIB bonds as a function of three sets of variables; SIB-specific, market-

specific, and bond-specific factors, as described by equation 1 below.10

The additive error term 𝜀

in the model accounts for idiosyncratic shocks to the yield-spread and possible omitted variables.

The reduced-form model, derived from equation 1, is described by equation 2:

𝑌𝑆 = 𝑓(𝑆𝐼𝐵 − 𝑠𝑝𝑒𝑐𝑖𝑓𝑖𝑐 𝑅𝑖𝑠𝑘 , 𝑀𝑎𝑟𝑘𝑒𝑡 − 𝑠𝑝𝑒𝑐𝑖𝑓𝑖𝑐 𝐹𝑎𝑐𝑡𝑜𝑟𝑠 ,

𝐵𝑜𝑛𝑑 − 𝑠𝑝𝑒𝑐𝑖𝑓𝑖𝑐 𝐹𝑎𝑐𝑡𝑜𝑟𝑠) + 𝜀 (1)

𝑌𝑆𝑖,𝑏,𝑡,𝑞 = 𝛽0 + 𝛽1 ∗ 𝑐𝑟𝑖𝑠𝑖𝑠 + 𝛽2 ∗ 𝑝𝑜𝑠𝑡𝑐𝑟𝑖𝑠𝑖𝑠 + 𝜷𝐷𝑺𝑰𝑩𝑏 + 𝜷𝐹𝑺𝑰𝑩𝑭𝑏,𝑞−1

+ 𝜷𝑀𝐷𝑴𝒂𝒄𝒓𝒐𝑫𝑡 + 𝜷𝑀𝑄𝑴𝒂𝒄𝒓𝒐𝑸𝑞−1 + 𝜷𝑆𝑩𝒐𝒏𝒅𝑺𝑖

+ 𝒊𝒏𝒕𝒆𝒓𝒂𝒄𝒕𝒊𝒐𝒏𝒔 + 𝜀𝑖,𝑏,𝑡,𝑞

(2)

This specification allows one to determine how the secondary market yield-spread

(𝑌𝑆𝑖,𝑏,𝑡,𝑞) for bond i of SIB b during day t in quarter q, reacts to changes in the SIB-specific,

market-specific, and bond-specific factors by using panel-data estimation techniques via

inclusion of SIB dummy variables to account for bank heterogeneity. We define each regressor

10

Theoretically, endogeneity could be a concern. However, our findings are robust to a number of alternative

specifications such as omission or inclusion of various control variables and estimation techniques (such as random

effects estimation).

15

in what follows. The data include the secondary market bond trades across the 26 designated

SIBs. After merging databases from seven different sources11 (Section 5) and adjusting for

outlier treatment, our sample includes over 8 million trades. The intercept 𝛽0 in the model is

allowed to shift over time across the three sub-periods and across the 26 SIBs by introducing the

following dummy variables: [1] the crisis dummy (𝑐𝑟𝑖𝑠𝑖𝑠); [2] the post-crisis dummy

(𝑝𝑜𝑠𝑡𝑐𝑟𝑖𝑠𝑖𝑠); and [3] the SIB dummies (𝑺𝑰𝑩𝑏). The crisis and post-crisis dummies serve as a

catch-all for macroeconomic factors that are shared across all SIBs during the respective

business cycle phases but are not explicitly included in the specification. The pre-crisis period

serves as the base period. The SIB dummies capture all firm-specific factors not accounted for

in the model, including unobserved heterogeneity such as firm culture, information technology

(IT) infrastructure, management skills, cyber-security, etc.

The model variables are outlined in Table 3. Vector 𝑺𝑰𝑩𝑭𝑏,𝑞−1, includes all SIB-specific

risk factors lagged by one-quarter. These variables are stratified across the CAMELS stripes,12

and are lagged by one quarter since consolidated financial statements for BHCs (FR Y-9C forms)

are made public 45 days after the end of each quarter. The Tier 1 leverage ratio at the BHC

consolidated level represents Capital adequacy. Bank capital serves as a cushion that can be

used to charge-off bad loans and other non-performing investments once the allowances for loan

losses are depleted. However, one can also view excess bank capital as costly since these funds

11

The seven database sources used in the analysis are: [1] TRACE, [2] Mergent FISD, [3] Y9-C reports, [4] Bank

Holding Company Performance Report (BHCPR), [5] Yahoo! Finance, [6] Board of Governors, and [7] U.S. Bureau

of Labor Statistics.

12 Since CAMELS ratings are not publically disclosed, bondholders are not privy to these ratings. Thus, we proxy

for the categories. See Appendix A of the Comptroller’s Handbook: Bank Supervision Process for more information

regarding the Uniform Financial Institutions Rating System (UFIRS) or CAMELS rating system. It can be accessed

at: http://www.occ.treas.gov/publications/publications-by-type/comptrollers-handbook/pub-ch-ep-bsp.pdf. The

CAMELS rating system has evolved over time: from the Uniform Financial Institutions Rating System (UFIRS),

originally adopted by the Federal Financial Examination Council (FFIEC) in 1979, which included five components,

to include the sixth component (sensitivity to market risks) in 1997.

16

are not lent out or invested through other means. Net charge-offs to average loans serves as our

Asset quality measure and can be viewed as credit risk at a SIB. Bank inefficiency, calculated as

non-interest expense (salaries and employee benefits, expenses of premises and fixed assets, etc.)

less amortization of intangible assets divided by average assets, relates to Management

inefficiency since it measures how much management spent on overhead for every dollar of

assets. Return on average assets (ROAA) is a standard measure for Earnings and is calculated as

net income divided by average total assets. Our Liquidity measure is the liquidity ratio. It is

calculated as short-term investments (the sum of interest-bearing bank balances, federal funds

sold and securities purchased under agreements to resell, and debt securities with a remaining

maturity of one year or less), divided by total assets. The last component, Sensitivity to interest

rate risk, is measured by the funding gap defined as the difference between short term assets and

short term liabilities (i.e., those that mature or re-price within one year) divided by total assets.

In addition to these risk measures, we also include the lag of the natural log of BHC total assets

(in real terms13

) to account for variation in institution size.

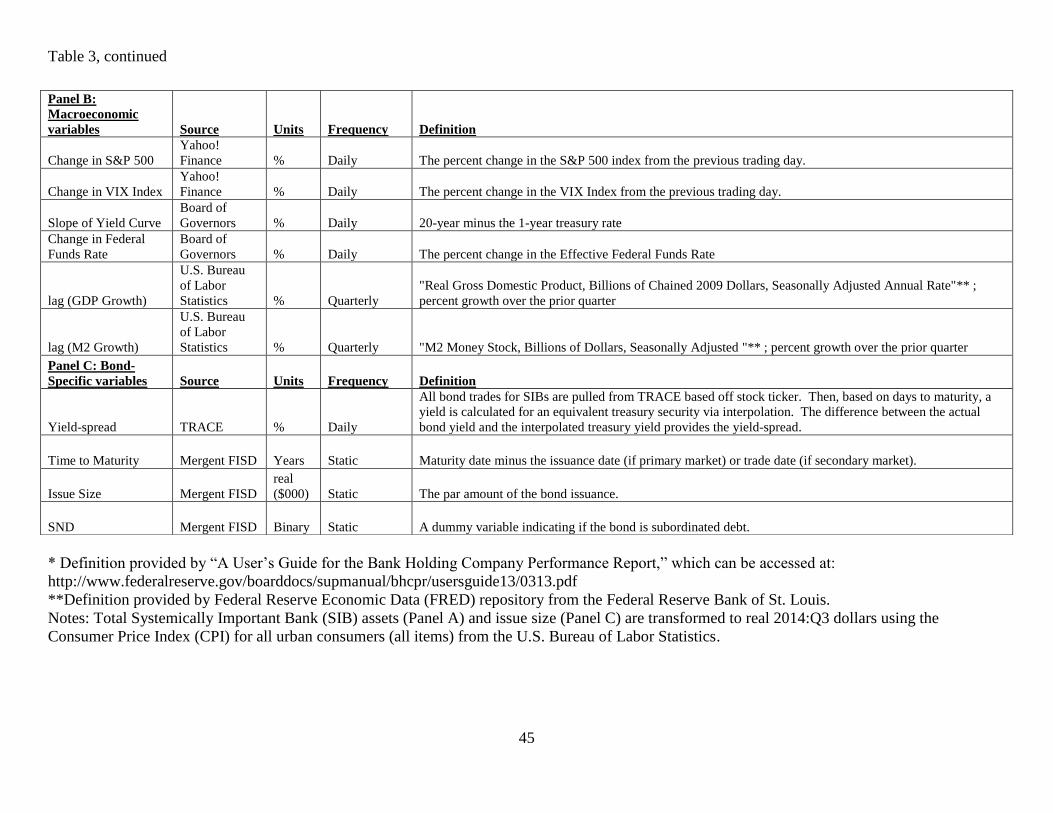

[Insert Table 3 Here]

We include both daily and quarterly14

macroeconomic control variables in vectors

𝑴𝒂𝒄𝒓𝒐𝑫𝑡 and 𝑴𝒂𝒄𝒓𝒐𝑸𝑞−1, respectively, to capture the daily trading environment within the

context of the broader economy. The daily variables included are the percentage change in S&P

500 based on the daily closing value of the index, change in the Chicago Board Options

Exchange Market Volatility Index (VIX), the slope of the yield curve, and the change in the

13

All variables reported in real terms reflect 2014:Q3 dollars based off the Consumer Price Index (CPI) for all urban

consumers (all items) from the U.S. Bureau of Labor Statistics.

14 We do not see an issue including quarterly macroeconomic control variables to model daily yield spreads. Bond

traders would account for the daily trading environment within the context of the broader economic trends.

Econometrically, we are not concerned with multicollinearty between the daily and quarterly market variables due to

the relatively low correlations shown in rows 12 and 13 of Appendix B and given the large number of observations.

17

federal funds rate.15 The slope of the yield curve is calculated as the 20-year minus the 1-year

treasury rate. In “normal” times one expects the yield curve to be upward sloping. However,

prior to, and during recessions, an inverted yield curve is not uncommon. The quarterly

macroeconomic variables are quarterly lags of GDP and M2 growth, which capture the broader

health of the economy (including the demand for money) and available liquidity, respectively.

The last vector 𝑩𝒐𝒏𝒅𝑺𝑖 contains the bond-specific features. The variable time to

maturity reflects the number of years until the bond matures. Log of the issue size relates to the

log of the total dollar amount (in real terms) of the debt issuance in the primary market. The last

variable is a dummy variable for SND; it takes the unit value for SND and zero for senior debt,

rendering the latter the control group. One would expect a discount on senior debt when

compared to SND since senior bondholders are higher in the pecking order if the SIB were to

liquidate its assets. Thus, the coefficient of the SND dummy is expected to be positive.

Lastly, the vector 𝒊𝒏𝒕𝒆𝒓𝒂𝒄𝒕𝒊𝒐𝒏𝒔 includes the interaction terms between the crisis and

post-crisis dummy variables and the SIB-specific, bond-specific, and macroeconomic risk

factors. The coefficient estimates on the interaction terms (with continuous variables) are

interpreted as changes in the slopes during the crisis and post-crisis periods, respectively.

Economically, the interaction terms represent the possible change in bond investor behavior with

respect to SIB, bank, and macroeconomic factors during the crisis and post-crisis phases of the

business cycle.

4. Hypotheses

As a risk factor increases in magnitude at a given bank, one would expect the bank’s

bond yield-spreads to increase (i.e., bond prices to decrease). This increase in risk premium in

15

Our choice of daily macroeconomic variables is similar to those in Balasubramnian and Cyree (2014).

18

the secondary market would be indicative of market discipline by bond traders. That is, the

investor selling the bond will be disciplined by being forced to accept a lower price on the debt

security as the risk level of the issuing SIB increases. As an analogy, one can think of bond

yields as the barometer for market discipline, and bank-specific risks as levers which raise or

lower the barometer, depending on the level of risk. We propose four hypotheses concerning the

association between SIB debt yield-spread and various risk measures across the business cycle.

The first hypothesis is standard in the market discipline literature on bond yields (Section 2).

The question is if, how, and to what extent each risk factor impacts the yield-spread. We

formulate this hypothesis as:

H1: An increase in SIB risk is associated with market discipline in the form of a higher

yield-spread.

Once the relationship between the yield-spread and risk measures is established, we ask

more penetrating questions that are not standard in the literature. These hypotheses examine how

market discipline in bond yields could be used as a viable option for policy makers to leverage.

For example, we trust that an increase in a risk metric will engender different responses

depending on the phase of the business cycle. This differential is due to varying levels of

sensitivity to risk and risk tolerance on the part of the bond market participants, over the phases

of the business cycle. In the extreme case, there could be a reversal of a marginal effect, namely

that what is viewed as a viable risk-return trade-off in one phase could be perceived as

disadvantageous in another phase. We propose hypothesis H2 as:

H2: The sensitivity of the yield-spread to an increase in SIB risk measures is business-

cycle phase dependent (i.e., the slope of a risk factor (its marginal impact) will change during the

crisis and post-crisis periods (slope shifts), compared to the pre-crisis period).

19

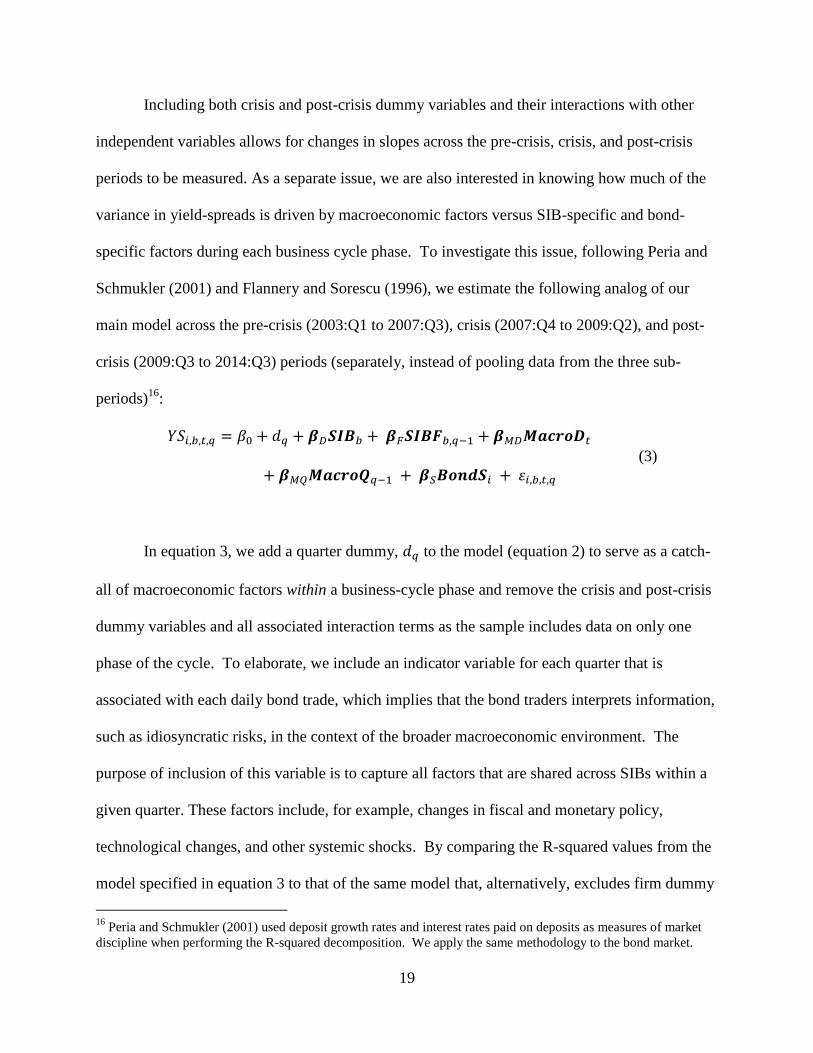

Including both crisis and post-crisis dummy variables and their interactions with other

independent variables allows for changes in slopes across the pre-crisis, crisis, and post-crisis

periods to be measured. As a separate issue, we are also interested in knowing how much of the

variance in yield-spreads is driven by macroeconomic factors versus SIB-specific and bond-

specific factors during each business cycle phase. To investigate this issue, following Peria and

Schmukler (2001) and Flannery and Sorescu (1996), we estimate the following analog of our

main model across the pre-crisis (2003:Q1 to 2007:Q3), crisis (2007:Q4 to 2009:Q2), and post-

crisis (2009:Q3 to 2014:Q3) periods (separately, instead of pooling data from the three sub-

periods)16

:

𝑌𝑆𝑖,𝑏,𝑡,𝑞 = 𝛽0 + 𝑑𝑞 + 𝜷𝐷𝑺𝑰𝑩𝑏 + 𝜷𝐹𝑺𝑰𝑩𝑭𝑏,𝑞−1 + 𝜷𝑀𝐷𝑴𝒂𝒄𝒓𝒐𝑫𝑡

+ 𝜷𝑀𝑄𝑴𝒂𝒄𝒓𝒐𝑸𝑞−1 + 𝜷𝑆𝑩𝒐𝒏𝒅𝑺𝑖 + 𝜀𝑖,𝑏,𝑡,𝑞 (3)

In equation 3, we add a quarter dummy, 𝑑𝑞 to the model (equation 2) to serve as a catch-

all of macroeconomic factors within a business-cycle phase and remove the crisis and post-crisis

dummy variables and all associated interaction terms as the sample includes data on only one

phase of the cycle. To elaborate, we include an indicator variable for each quarter that is

associated with each daily bond trade, which implies that the bond traders interprets information,

such as idiosyncratic risks, in the context of the broader macroeconomic environment. The

purpose of inclusion of this variable is to capture all factors that are shared across SIBs within a

given quarter. These factors include, for example, changes in fiscal and monetary policy,

technological changes, and other systemic shocks. By comparing the R-squared values from the

model specified in equation 3 to that of the same model that, alternatively, excludes firm dummy

16

Peria and Schmukler (2001) used deposit growth rates and interest rates paid on deposits as measures of market

discipline when performing the R-squared decomposition. We apply the same methodology to the bond market.

20

variables, SIB risk factors, or bond-specific variables, we can estimate the proportion of

explained variation that is driven by macroeconomic factors vis-à-vis firm-specific and bond-

specific factors. From a policy perspective, this is a crucial test because if macroeconomic

conditions are the primary drivers of yield-spreads, bond investors are demanding higher risk

premia mostly due to systematic, rather than idiosyncratic, factors. Under these circumstances,

bond investor behavior is largely a reflection of the macro environment, and a policy of

mandatory debt issuance by the largest BHCs could not succeed because bond-specific and SIB-

specific risk factors do not exert a significant influence on yields. To elaborate, if policy makers

were to implement the mandatory issuance of subordinated debt and monitor yields on that debt

in the secondary market as an “early warning” sign, they would do so with the assumption that

bond investors are responding to bank risks through the price they are willing to pay on the debt.

If instead, bond investors of SIB debt are simply reacting to the economy at large, then the bond

yields will not be reflective of inherent risk at the issuing institution, market discipline will be

greatly diminished since there is less sensitivity to the firm’s idiosyncratic risks, and the

responsibility of policy makers in curtailing SIB risk would become more challenging. Thus, we

propose our third hypothesis as:

H3: SIB and bond-specific factors drive the majority (greater than 50%) of the explained

variance in yield-spreads (i.e., play a dominant role in market discipline) across all phases of the

business cycle.

A pertinent question is how the proportions of variation in yield-spread due to SIB-

specific and bond-specific risk factors change across the phases of the business cycle. Two

scenarios are possible here. First, one might expect that bond-holders become more attentive to

idiosyncratic factors during the turbulent crisis times (more sensitive to SIB and bond-specific

21

risks), especially because the banking industry was experiencing arguably the most severe

liquidity and solvency issues since the Great Depression. Under these conditions, the proportion

of variance driven by macroeconomic factors could be smaller during the crisis, compared to the

pre and post-crisis periods. Second, it is possible that during the crisis period macroeconomic

factors dominate all institution-specific risk measures because systemic shocks could dominate

bond trader psychology and bond trader behavior, sidelining the idiosyncratic factors. Thus,

determining which forces prevail is rendered an empirical exercise. This leads us to our fourth

hypothesis:

H4: The proportion of explained variation in market discipline driven by SIB and bond-

specific factors increases during the crisis period (2007:Q4 to 2009:Q2), compared to the pre-

crisis (2003:Q1 to 2007:Q3) and post-crisis (2009:Q3 to 2014:Q3) periods.

5. Data Sources and Descriptive Statistics

5.1. Data Sources

Using the stock tickers of the 26 SIBs, we extract the yields and dates of all secondary

market trades for these SIBs that are available in TRACE, from 2003:Q1 through 2014:Q3.

Then, using the daily Treasury constant maturity rates provided by the Board of Governors of the

Federal Reserve System17

we interpolate (or extrapolate, where necessary) the risk-free rate

associated with each trade based upon the number of days remaining until the debt matures. This

procedure helps us to calculate the yield-spread for every trade.18

Next, we merge in all bond-

17

Daily Treasury rates are available for 1, 3, and 6-month periods and 1, 2, 3, 5, 7, 10, 20, and 30-year periods.

Rates can be accessed through the Treasury Department’s Resource Center.

18 An example: Suppose a trade takes place on January 5, 2004 with a yield of 5.0%, the bond has 1 ½ years to

maturity, the daily Treasury yields for the same day are 1.35% and 1.95% for the 1 year and 2 year Treasury bonds,

respectively. Linear interpolation would provide a risk-free rate of: 𝑦 =𝑦1−𝑦0

𝑥1−𝑥0(𝑥 − 𝑥0) + 𝑦0 =

1.95−1.35

2−1(1.5 − 1) +

1.35 = 1.65%.

22

specific information from the Mergent Fixed Income Securities Databases (FISD). Using the

unique Committee on Uniform Securities Identification Procedures (CUSIP) number for each

bond, we match the bond-specific variables available in the Mergent database, such as callable,

putable, time to maturity, issue size, and type (SND, Non-SND), with the individual bond trades.

We then drop the callable and putable bonds from our dataset because the option of the firm to

buy the bond from the investor or the investor to demand principal repayment would complicate

the market discipline mechanism.19

This process generates a dataset of daily yield-spreads with bond-specific information.

In the next step, we use the stock ticker and quarter identifiers to match the dataset with SIB-

specific data from FR Y-9C reports and BHC Performance Reports (BHCPRs). Then, using the

trade date, we merge in the macro variables for the specific day (or quarter) during which the

trade took place.20

Lastly, we remove all observations with bond or daily macro variables that lie

above the 99th

or below the 1st percentile as outliers, separately across the pre-crisis, crisis, and

post-crisis periods. The process described provides observations for 8,045,221 trades of bank

debt across all 26 SIBs from 2003:Q1 through 2014:Q3.

5.2. Descriptive Statistics

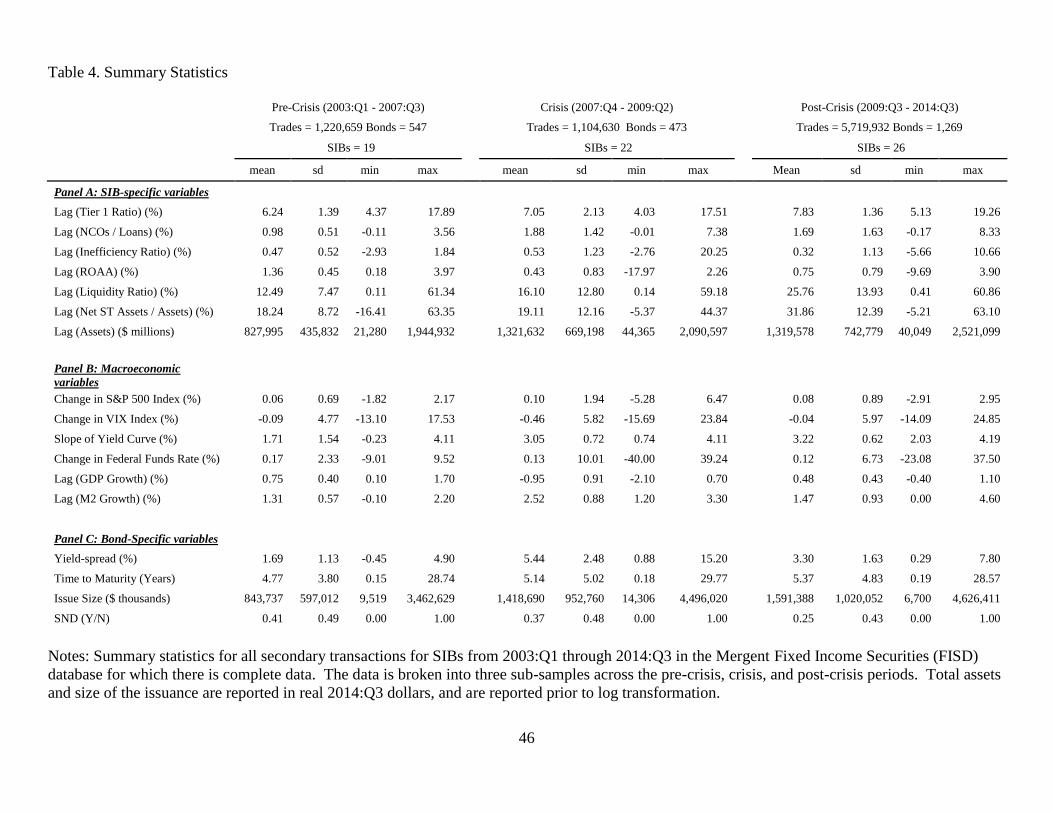

The summary statistics stratified across the pre-crisis, crisis, and post-crisis periods are

shown in Table 4. Panels A, B, and C, include SIB, macroeconomic, and bond-specific

variables, respectively. Note that the debt sample changes over the business cycle. For example,

only during the crisis period are the bonds of all 26 SIBs traded, and liquidity is greatest during

the post-crisis period. The daily mean yield-spread for SIB debt traded across the pre-crisis,

19

Our main conclusions still hold with the inclusion of callable and putable bonds.

20 For data sources of the macroeconomic variables, see the Source column of Table 3.

23

crisis, and post-crisis periods are 1.69%, 5.44%, and 3.30%, respectively, demonstrating a big

contrast. The increases in yields during the crisis and post-crisis periods, relative to the pre-crisis

period, are consistent with increased market volatility, greater risk aversion, and longer maturity

of the bonds (4.77, 5.14, and 5.37 years, respectively) traded during these periods (consistent

with Guidolin and Tam, 2013).

[Insert Table 4 Here]

The average issue size in the primary market has also increased in real terms over the

business cycle, peaking in the post-crisis era at around $1.6 billion, with a minimum value of

$6.7 million and a maximum value of $4.6 billion during that same period. This could reflect the

increase in bond liquidity due to advancement in electronic trading technology (e.g., trading

algorithms), and declining transaction costs. Furthermore, there are new capital requirements in

the pipeline surrounding SND with the implementation of Basel III reforms. According to the

final rule,21

the Basel III Capital Framework lists criteria that a financial instrument must meet in

order to be considered as regulatory capital, which would presumably apply to all firms

considered in this study. We include a number of firm-specific, bond-specific, and

macroeconomic-specific control variables, consistent with Balasubramnian and Cyree (2011 and

2014). The correlation matrix of all continuous variables included in the model is shown in

Appendix B.22

6. Empirical Results

21

A description of the final rule can be accessed through the OCC website: http://www.occ.gov/news-

issuances/news-releases/2013/2013-110a.pdf

22 The correlations between inefficiency ratio (variable #3) and the ROAA (variable #4) and between the daily

change in S&P 500 (variable #8) and the VIX index (variable #9) stand at -0.62 and -0.73, respectively, raise

concerns about collinearity. However, removal of the liquidity ratio and/or daily change in the VIX index from the

model does not significantly impact the results or the conclusions. Furthermore, we believe the strong correlations

between the quarterly risk measures (i.e., CAMELS proxies) and daily yields indicates robustness of the model.

24

6.1. Methodology

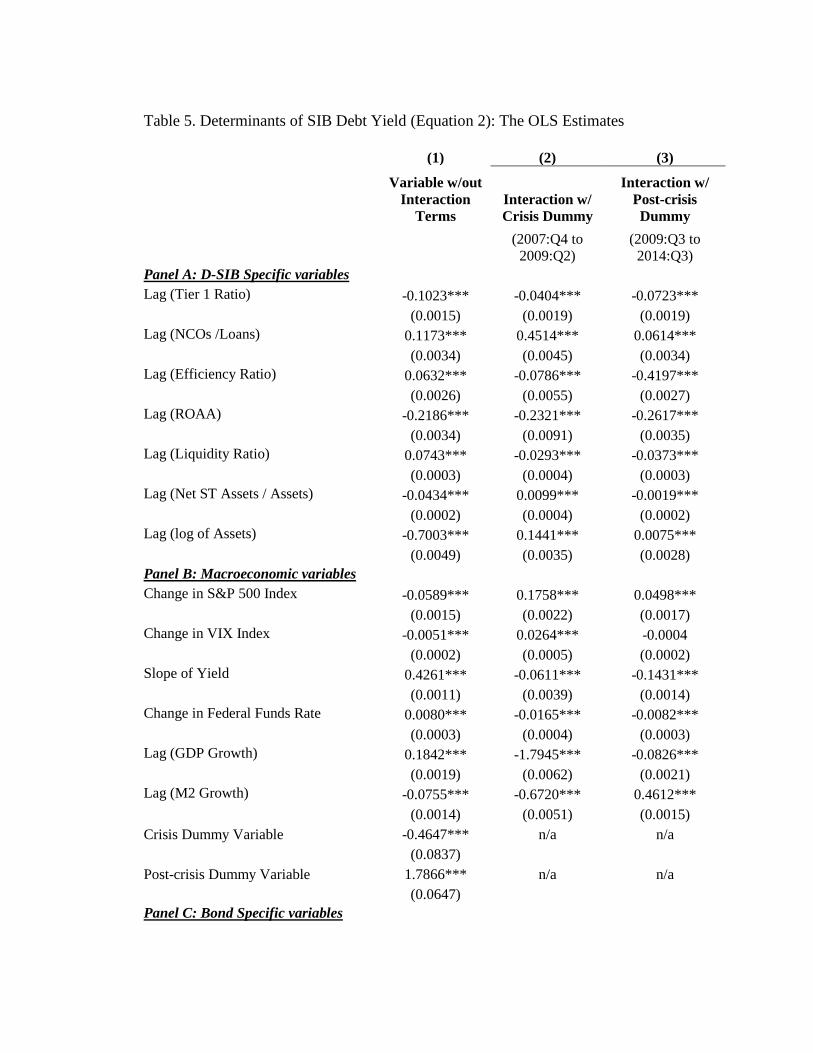

The model (equation 2) is estimated via the ordinary least squares (OLS) technique with

heteroscedasticity-robust errors. Results are presented in Table 5. Column 1, 2, and 3 of this

table display the coefficient estimates for the risk measures during the pre-crisis period, and their

changes during the crisis and post-crisis periods, respectively. The coefficient changes refer to

changes in slopes (intercepts) demonstrated by interactions of the crisis or post-crisis dummy

variable with a continuous (dummy) variable. Column 1 also includes the intercept shifts due to

the latter two phases of the business cycle (last two rows of Panel B of Table 5). To calculate the

overall effect, which we refer to as a marginal impact, of an increase in each risk measure on

yields during the crisis or post-crisis periods, we add the coefficient estimate in column 2 (for the

crisis) or column 3 (for the post-crisis) to the coefficient estimate in column 1. Panels A-C in

this table contain the SIB-specific, macroeconomic, and bond-specific variables, respectively.

The SIB fixed effects and the constant term, all significant at the1% level, are not reported to

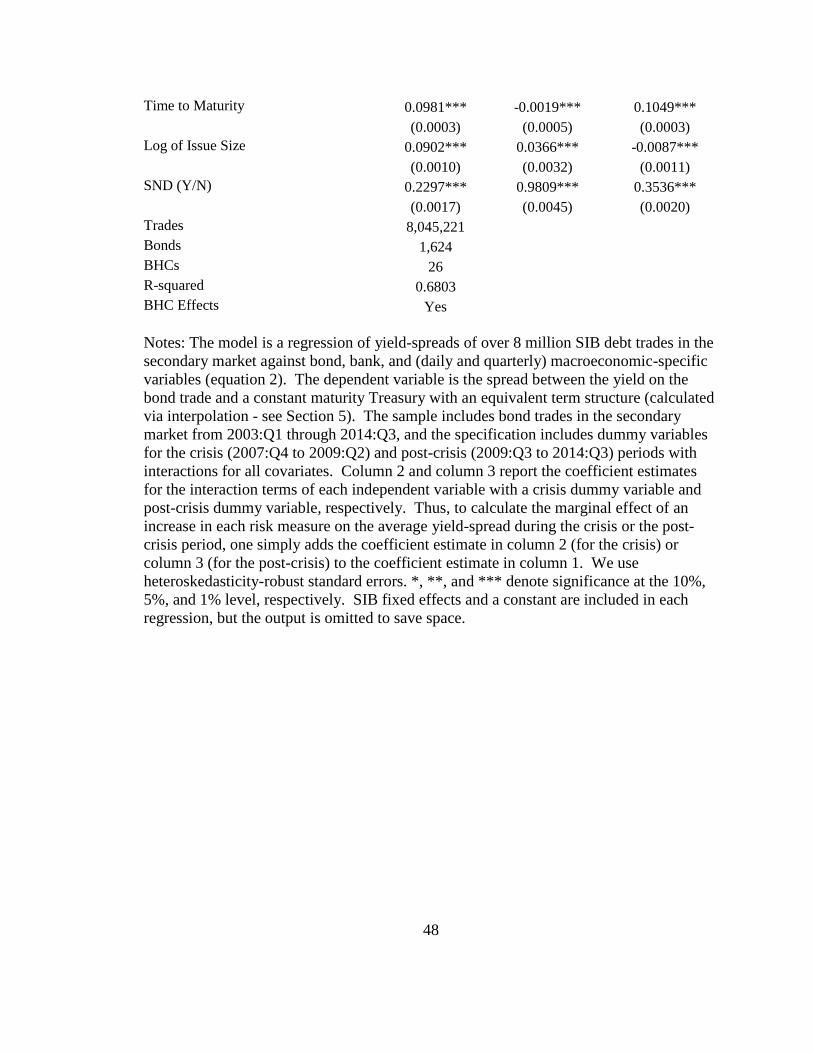

save space. The economic effects, reported in Table 6, measure the change in the yields in basis-

points (bps) attributable to a one standard deviation change in the pertinent independent variable

(economic effect).

[Insert Table 5 Here]

[Insert Table 6 Here]

A main question of interest is whether yields increase in the secondary market as SIB

riskiness rises. From a policy standpoint, if regulators were to require regular issuance of debt,

such as SNDs, by banks, it would be with the assumption that primary and secondary market

participants would demand a higher rate for both new and outstanding debt (primary and

secondary markets) in response to increased risk, thereby placing pressure on the BHC to

25

mitigate it.

It is reasonable to presume that bond traders will react to an increase in SIB risk

differently depending on the phase of the business cycle, reflected in the interactions terms for

the crisis and post-crisis periods (Flannery and Sorescu, 1996). For example, secondary market

participants may find an increase in credit risk for a SIB to be less problematic during the pre-

crisis period, when the economy is experiencing an up-swing, because credit issues may be

easier to remediate. However, during the crisis, when the flow of credit was tight and there were

numerous bank solvency issues, additional credit risk could be seen as more de-stabilizing, than

in the pre-crisis period, further strengthening the impact on yields.

6.2. Results for SIB-Specific Variables

The coefficient estimates and the economic effects of the SIB-specific risk measures are

shown in Table 5 (Panel A) and Table 6, respectively, for the three sub-periods. We discuss these

effects below.

Capital Adequacy (leverage): The marginal effect of the capital ratio on the yield-spread is

found to be negative and highly significant, with the magnitude of the effect varying across the

three sub-periods. During the pre-crisis period, the marginal impact takes the value of -0.1023,

while, accounting for the interaction effects, it increases in magnitude to -0.1427 during the crisis

and then it increases further to -0.1746 during the post crisis period (Table 6). These incremental

effects are statistically different because the interaction terms between capital and the crisis and

post-crisis dummy variables, respectively, are negative and statistically significant, as shown in

Table 5. The negative capital ratio effects imply that bond traders view an increase in SIB

capital as a force to reduce bank risk, and, thus, they lower their required yield on SIB debt.

These results confirm that there exists a shift between business cycle phases regarding the extent

26

to which market participants react to changes in risk measures. The economic effects show that

a one standard deviation increase in Tier 1 capital will decrease the yield on the SIB debt by 14,

30, and 24 bps in the pre-crisis, crisis, and post-crisis eras, respectively. The greater sensitivity

of bond buyers to changes in bank capital during the crisis could possibly be related to the

distribution of TARP capital infusions. In fact, the largest capital infusions under the Capital

Purchase Program (CPP) were given to the SIBs including Citigroup and Bank of America ($45

billion infusions each) and JP Morgan and Wells Fargo ($25 billion infusions each), who

together comprise nearly 75% of the bond trades during the crisis period (Table 2). Since the

CPP purchases injected additional capital into the firms during a time when their probability of

failure was heightened, bond traders reacted more strongly to an additional buffer of capital

support, which could be viewed as a mitigating factor. Moreover, the capital injections could

have provided a signaling effect to the market that there were underlying issues that could

potentially impact bank solvency at these large BHCs that the regulators were aware of via

confidential information, which could partially explain the greater sensitivity of bond traders to

bank capital. Put simply, if market participants believed that the SIBs required TARP funds to

prevent insolvency, then this could explain the greater sensitivity of market participants to bank

capital levels.

Asset Quality: The coefficient of credit risk, measured by net charge-offs (loan and lease losses)

to total loans ratio, is positive and significant across the three sub-periods indicating that bond

traders raise their yield requirement when bank asset quality declines. The marginal and

economic effects of asset quality are reported in Table 6. According to the figures in this table,

the magnitude of the marginal impact of credit risk on SIB debt yields increases substantially,

27

from 11.73 to 56.87, and then declines back to 17.87 basis points (Table 6) from the pre-crisis to

the crisis and post-crisis periods, indicating that bond investors do account for credit risk

exposure of the SIB across all three phases of the business cycle but much more so during the

crisis. It is also notable that increased sensitivity of the bond traders to credit risk during the

crisis did not move back to the pre-crisis period in the post-crisis period, demonstrating

persistence of fear and risk aversion.

According to the figures in Table 6, the magnitudes of economic effects of asset quality

changes are 6, 81, and 29 basis points, reflecting heightened sensitivity of the market participants

in the crisis and post-crisis periods, compared to the pre-crisis period when markets were clam.

The crisis period, by far, displays the strongest effect. The greater impact of asset quality on risk

premium during the crisis period implies that during times of economic expansion, as in the pre-

crisis period, bond investors are less sensitive to changes in credit risk, likely a reflection of the

robust economy and positive psychology. According to figures reported in Table 6, during the

crisis, the bond traders reacted to changes in credit risk to a much greater extent than to all other

bank-specific risk measures included in the model, likely a symptom of the turbulent recession

leading to investor fear and pessimism and over-reaction due to deeper opacity and complexity

of the banks during this period.

Management: The coefficient for the inefficiency ratio, the proxy for bank management quality,

is significant across the three sub-periods but changes in terms of the direction of the effect

(sign). The positive effect of increased inefficiency during the pre-crisis period indicates that

bond traders treated the debt issued by less efficient SIBs as riskier and demanded a higher yield-

spread on it. The magnitude of the effect was small; a one standard deviation increase in the

28

inefficiency ratio increased the yield by only 3 bps in this period.

During the crisis and post-crisis periods, the marginal impacts stood at -0.0154 and

-0.3565, respectively, suggesting that, unlike the first sub-period, during the latter two phases of

the business cycle, bond traders viewed SIB expenses on areas such as salaries, employee

benefits, and premises as risk mitigating factors. The change in bond investor behavior could

reflect a shift from the cost-cutting culture of the pre-crisis era to focus on hiring more skilled

managers and building more attractive buildings to compete away customers from other banks,

or it could imply that SIBs that had the ability to invest in their employees and infrastructure

during and after the crisis were perceived to be safer and more stable. For example, during the

crisis, when the solvency of SIBs was in doubt and TBTF policies were being implemented by

policy authorities, SIBs’ ability to pay expenses such as salaries, employee benefits, and

operating expenses, would send a message to investors that it is strong enough to continue

business as usual.

Earnings (ROAA): For the profitability measure, return on assets (ROAA), the effects are

negative and significant at the 1% level for all three sub-periods, as expected, indicating that an

increase in SIB profitability is perceived by bond-traders as decreasing the chances of default on

SIB bonds. The marginal impacts take values of -0.2186, -0.4507, and -0.4803 during the pre-

crisis, crisis, and post-crisis periods, respectively, indicating a decrease of 10, 37, and 38 bps in

the yield for a one standard deviation positive profitability shock during each respective business

cycle phase. As was the case with the credit risk measure, there is more sensitivity to changes in

bank profitability during the crisis compared to the pre-crisis period, suggesting that, during

periods of greater macroeconomic uncertainty, each unit of profitability translates into a greater

29

risk premium by bond traders, than in calmer sub-periods. The stronger effect observed during

the crisis seems to have sustained itself even in the post-crisis period as the shift in psychology

of the traders in more highly valuing bank profitability was persistent, rather than short-lived.

Liquidity: The effect of the liquidity ratio (short-term (<1 year)) assets divided by consolidated

assets) is positive and significant across the three sub-periods but weaker during the post-crisis

phase. As Berrospide (2012) explains, during the summer of 2007 at the onset of the mortgage

crisis, short term funding had dried up and securitization markets were headed for collapse. As a

result, SIBs became concerned about counterparty, liquidity, and portfolio risks, in particular

regarding the size of their exposures related to sub-prime assets, the interbank market froze, and

banks began to “hoard liquid buffers.” Figures in Panel A of Table 4 reflect this hoarding of

liquidity at the SIBs, as we see the liquidity ratio increase from 12.49% to 16.10% to 25.76%

across the pre-crisis, crisis, and post-crisis periods. The results in Table 6 convey that holding

excess liquidity was seen as costly to the SIB, and, thus, increased the SIB yields. That is,

excessive cash holding was viewed by traders as a suboptimal and costly allocation of resources.

In terms of magnitude, a one standard deviation increase in the liquidity ratio translated into a

yield-spread increase of 56, 58, and 52 bps across the three sub-periods, respectively. The

interpretation of these findings is that SIBs holding high levels of liquid assets, relative to total

assets, to prepare for negative shocks in the near term were perceived as distressed because it

was assumed that such banks were unable to rely on liability management sources of liquidity,

and were holding excessive liquidity to counter that.

Interest Rate Risk: Interest rate risk is measured by the funding gap ratio (short-term (<1

30

year) assets less short-term (<1 year) liabilities to total assets). Since SIBs included in our

sample held, on average, more short-term assets than liabilities (they have positive funding

gaps), during the sample period, they were protected from the anticipated rise in interest rates,

especially during the post-crisis period.23

Thus, wider positive gaps corresponded to greater

profits and lower yield on their debt. Specifically, the funding gap marginal impacts are all

negative and highly significant (-0.0434, -0.0335, and -0.0453, respectively, for the three sub-

periods) (Table 6). Figures reported in Table 4 show that the average SIB increased its funding

gap ratio from 18.24 to 19.11 to 31.86 percent of total assets across the pre-crisis, crisis, and

post-crisis quarters, respectively. In terms of economic effects, the gap coefficients translate to a

decrease in the SIB yields of 38, 41, and 56 bps, for each respective phase of the business cycle,

when SIBs benefit from a one standard deviation increase in the positive funding gap.

6.3. Pertinent Hypotheses

The results displayed in column one in Table 5, Panel A, resolutely fail to reject

hypothesis H1, purporting that an increase in SIB risk measures results in market discipline in the

form of higher yields for SIB bonds traded in the secondary market. Results displayed in

columns two and three also fail to reject hypothesis H2, proposing that secondary bond market

participants’ sensitivity to an increase in risk is dependent upon the phase of the business cycle.

Two main implications can be drawn here. First, researchers and policy makers should both

account for the phase of the business cycle and sensitivities of the market players when studying

market discipline. Specifically, policy makers need to stay cognizant of how the behavior of

market participants can change within the context of the business cycle. If regulators were to use

23

The Fed was expected to raise rates in 2015 (See the Federal Reserve Bank of San Francisco Economic Letter,

November 18, 2013 titled: “Expectations for Monetary Policy Liftoff”).

31

SIB yields as an early warning indicator, they would need to adjust the thresholds for policy

shifts based on the state of the macroeconomic environment. Second, our results support the

mandatory issuance of SIB debt as a method of market discipline, since we find that bond traders

do respond to increased bank risk by demanding higher yields on SIB debt in every phase of the

business cycle. Thus, fluctuations in yield-spreads for SIB debt can serve as a barometer to

gauge overall risk levels and regulators could utilize this mechanism to curtail risk. U.S. banking

regulators had monitored the yield spreads of large banking institutions in the past, but, post

financial crisis, the focus has shifted away from market discipline and towards the regulatory

components of the Dodd-Frank Act, such as the DFAST and CCAR exercises. With that said,

the difficulty with monitoring yield spreads in the past was the thinness of the market, which is

why required issuance of debt would be a necessary component if the monitoring of yield

spreads were to be implemented within the current regulatory framework.

In general, regulators and policy makers should account for the effect of market

discipline in formulation and implementation of their monetary and fiscal policies designed to

achieve specific risk targets because, otherwise, they may miss the targets. Put simply, market

dicsipline via the monitoring of yield spreads provides an avenue for regulators to curtail SIB

risk to desired levels. Moreover, yield-spread thresholds should be business cycle phase

dependent since their sensitivity to SIB risks change within the context of the macroeconomic

cycle. Besides policy makers, managers of bank risk and investors should also account for the

sensitivity of bond yields to the phases of the business cycle, including the stance of monetary

and fiscal policies in issuing or purchasing bonds because bond yields contain current

information on the health of the banking institutions.

32

6.4. Results for Macroeconomic and Bond-Specific Variables

We report the results associated with macroeconomic and bond-specific variables in

Panels B and C of Table 5, respectively. The daily macroeconomic variables (and their

interaction terms), which include the change in the S&P 500 index, the change in the VIX market

volatility index, slope of the yield curve, and the change in the fed funds rate, are found to be

significant at the 1% level. The sole exception is the VIX interaction term during the post-crisis

period. Similarly, the quarterly measures used including the GDP and M2 growth rates are

significant at the 1% level. As expected, the former results confirm that bond-traders do account

for the daily trading environment within the context of the economy at large.

An interesting issue is how the effect of a given macro variable changes across the phases

of the business cycle. For example, the daily change in the S&P 500 index has a negative

coefficient estimate of -0.0589 during the pre-crisis quarters, indicating that S&P 500 returns and

SIB debt yields, on average, move in opposite directions (or the daily change in the S&P 500 and

SIB debt returns move in the same direction) during this period. The finding supports the

generally positive correlation between daily stock and bond price movements during the pre-

crisis quarters, reflecting investor confidence and an increasing demand for both debt and equity

securities in the secondary market during this time span. However, during the latter two phases

of the business cycle, the effect for the broad market index switches to a positive sign, indicative

of a negative correlation between SIB debt prices and the broad equity market.24

24

These results reflect the mechanism studied by Baele et al. (2010). They examine stock and bond return co-

movements with a focus on their time variation. They find that fundamental factors play a relatively large role for

bond returns, while liquidity factors and variance premium matter to a greater extent for stocks. Some studies (e.g.,

Connolly et al., 2005) attribute the negative correlation of the stock-bond returns to “flight-to-safety” in response to

large negative shocks such as those of 1997 and 1998. They find that the negative co-movement between stock and

bond returns is related to investor uncertatinty. Specficially, they find that the lagged and contemporaenous VIX

index have a negative relation with the stock-bond return. However, Campbell et al. (2009) create a pricing model

for stock and bond returns where the real economy “enables the model to fit the changing covariance of bond and

stock returns,” which opens the door for additional drivers.

33

We report the coefficient estimates for the bond-specific variables in Panel C of Table 5.

The reference group for the bond type is senior debt (non-SND). The positive and significant

coefficients for the subordinate notes and debenture (SND) dummy variables suggest that these

junior riskier bonds trade at a higher yield than the benchmark senior debt (non-SND). The

estimates for time to maturity coefficients are all positive and significant at the 1% level across

all three sub-periods, as implied by the liquidity premium hypothesis of term structure. The

marginal impacts are 0.0981, 0.0962 (0.0981 - 0.0019), and 0.2030 (0.0981 + 0.1049),

respectively, implying that for each additional year of remaining term to maturity the yield will

increase by approximately, 9.8, 9.6, and 20.3 bps , during the three sub-periods, respectively.

The greater premium observed for the pre and post-crisis periods may be reflective of stronger

expectations of rate increases during these two periods than during the crisis. Lastly, during all

three sub-periods, an increase in the size of the bond issuance in the primary market positively

impacts yield-spreads. In other words, the issuing banks will have to pay a higher yield to be

able to sell a bigger volume.

7. The Relative Share of Macroeconomic and Bank-specific Factors in Driving Yields

In this section, we investigate the relative power of bank-specific and bond-specific

factors versus the macroeconomic variables in driving the changes in SIB bond yields. This

issue is critical from a policy perspective because market discipline relies on the premise that

market participants do react to all publically available information, which in turn keeps a check

on the SIB risk-levels. If bond market participants are reacting mostly to the overall economic

environment, in lieu of SIB-specific risks, this will pose an impediment for relying on market

discipline because the magnitude of its effect will be slight.

34

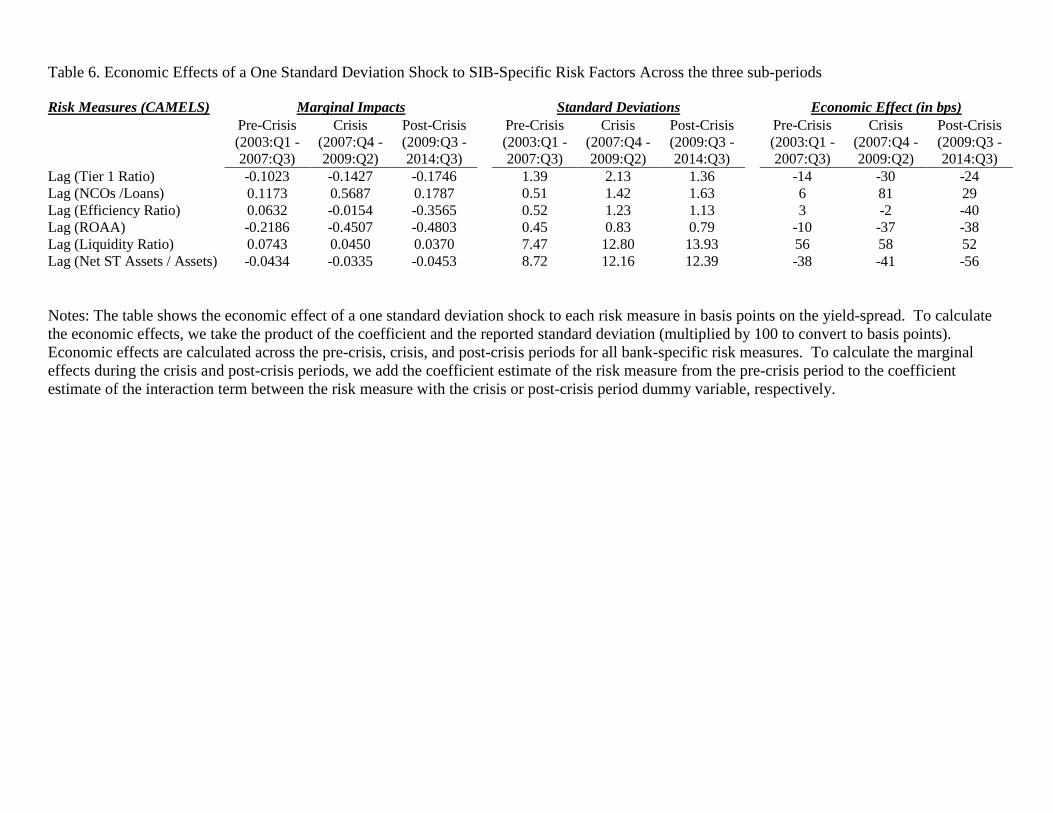

To test the proportion of explained variation in yield-spreads driven by SIB-specific

factors, versus the macro environment, we re-run the model (equation 3) including only the

macroeconomic factors and quarter time dummies for each of the three sub-periods. Then, we

obtain the R-squared from each of the three separate regressions following the method used by

Peria and Schmukler (2001). Theoretically, the “macro-only” specification would capture all

explained variation that arises from macroeconomic factors because the quarter time dummies

would serve as a catch-all for factors that are shared across all SIBs during the pertinent phase of

the business cycle. We then determine the percent of the R-squared from the fully specified

regression that is comprised by the R-squared from the specification that includes only

macroeconomic factors. The incremental R-squared reveals the extent to which market

participants are reacting to the overall economic environment versus the SIB and bond-specific

risks. Results are shown in Table 7.

[Insert Table 7 here]

Hypothesis H3 states that SIB-specific and bond-specific factors drive the majority of

variation seen in yield-spreads. Per Table 7, the percentage of variance in yield-spreads

attributable to macroeconomic factors is 77%, 53%, and 27% across the pre-crisis, crisis, and

post-crisis periods, respectively. Given these percentages, we reject hypothesis H3 during the

pre-crisis and crisis periods since only 23% and 47% of the variation in yield-spreads is

attributable to SIB and bond-specific risks, respectively. Notably, the latter figure (47%), though

falls short of constituting the majority share of the yield-spread variance, is still very

considerable and may offer a tool to the policy makers to rely on. The more interesting result,

however, is that, we cannot reject the hypothesis for the post-crisis period considering that 73%

of the R-squared is attributable to institution-specific and security-specific risk. This indicates

35

that in the post-crisis period, market discipline has considerably strengthened in controlling bond

yield variations and can be effectively used by policy makers to achieve their targets in terms of

bank risk levels. Furthermore, we reject hypothesis H4, postulating that the proportion of

variance in yields comprised of SIB-specific and bond-specific factors peaks during the crisis

period since the aforementioned results show that such factors dominate in the post-crisis period.

These findings beg the fundamental question: Why do bond-traders react much less to

macroeconomic factors during and since the financial crisis? We believe a major contributing

factor is the implementation of the unconventional fiscal and monetary policies during and after

the crisis. These include the introduction of the Troubled Asset Relief Program (TARP),

establishment of emergency lending facilities (e.g., Term Auction Facility, Primary Dealer

Credit Facility, Term Securities Lending Facility, etc.), bailouts of AIG and Bear Stearns, and

macroeconomic interventions by the Federal Reserve that remained in effect through the

specified post-crisis period, most notably quantitative easing programs (QE). These heavy and

unusual regulatory interventions in the markets likely broadened the explicit and implicit safety-

nets, and consequently dampened the proportion of variation in yields attributable to

macroeconomic shocks and rendering these forces secondary factors.25

Other possible reasons

that contribute to the bond-investor shift from macroeconomic to bank-specific factors could be

the calm environment prevailing during the pre-crisis phase, the (intended) end of TBTF policies

with the passage of Dodd-Frank Act (July 2010), as well as changes in bond-trading technology,

25

The mechanism at work is the financial accelerator, which characterizes how business cycles can impact financial

factors. Gertler and Lown (1999) show that the high-yield bond spread reflects information about aggregate

economic activity. However, the authors note that “the informativeness of any financial indicator is sensitive to the

nature of the business cycle and, relatedly, to the conduct of monetary policy.” This finding relates to the analysis at

hand because monetary and fiscal policy attempts to dampen the financial accelerator mechanism with respect to

negative shocks during the crisis and post-crisis periods. Thus, bond investors become less concerned with the

macroeconomic factors and focus more on the institution specific risks.

36

especially during the post-crisis phase, such as more accurate and timely bond pricing software.26

8. Conclusion

We pursue three objectives. First, we investigate whether market participants in the

secondary bond market for SIB debt react to SIB-specific, macroeconomic, and bond-specific

features via movements in yield-spreads. Second, we study how the behavior of bond-traders

changed in terms of reaction to variations in risk factors across various phases of the recent

business cycle. Third, we investigate the relative force of SIB-specific and bond-specific versus

the macroeconomic factors in driving SIB bond yields. Market discipline on SIBs in the market

for debt is important to study because there has been renewed interest in unorthodox regulation

as policy makers have been attempting to identify the gaps in the existing laws27

and to

implement new regulations to prevent similar crises in the future. One such regulation would be

the mandatory issuance of SIB subordinated debt according to which regulators would monitor

yield-spreads on SIB debt as an early warning indicator for regulatory actions. If regulators plan

on implementing compulsory SIB debt issuance with the expectation that bond investors would

keep risk in check, it is imperative to study the behavior of these stakeholders to examine if they

indeed respond to changes in bank-specific factors with significant strength.

Several interesting results are obtained. First, bond-traders do account for firm,