Embed Size (px)

Citation preview

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

Previous Page Home Next Page

MARKET INSIGHTCENTRAL MIDWEST MULTIFAMILY REPORT | THIRD QUARTER 2017

CUSHMAN & WAKEFIELD CENTRAL MIDWEST MULTIFAMILY RESEARCH

The Cushman & Wakefield Central Midwest Multifamily Research Team provides in-depth coverage of primary, secondary, and tertiary cities across the Midwest. In addition to analyzing multifamily rent and sales trends, these reports examine employment data, job growth trends, key economic announcements, and development pipeline news.

CINCINNATI/DAYTON INDIANAPOLIS

MINNEAPOLIS

IN THIS EDITION

Effective as of third quarter 2017, multifamily trends included in this and future reports reflect a shift in data sources. Therefore, trends in prior reports will not match going forward.

RESEARCH TEAM

COLUMBUS KANSAS CITY

OMAHA

BRENDAN DUNBARST. LOUIS [email protected]

JARRETT HICKSCINCINNATI/DAYTON, COLUMBUS, [email protected]

MATTHEW NEVINGERKANSAS [email protected]

MATT NIEHOFFINDIANAPOLIS [email protected]

SARA [email protected]

SHARON [email protected]

ST. LOUIS TOLEDO

Don MurphySenior Director +1 513 763 [email protected]

Scott PollomDirector+1 317 639 [email protected]

Phillip BrimbleManaging Director+1 816 412 [email protected]

Mike HanrahanExecutive Director+1 314 746 [email protected]

Scott KoetheDirector +1 402 548 [email protected]

Lance SteigerSenior Director+1 952 893 [email protected]

Don MurphySenior Director +1 513 763 [email protected]

Don MurphySenior Director +1 513 763 [email protected]

INTERACTIVE CONTENT

CINCINNATI/DAYTON

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

1CI N CI N N AT I / DAY TONMARKET INSIGHTThird Quarter 2017

The following are select announcements from the third quarter of 2017:

• According to the U.S. Bureau of Economic Analysis (BEA), Greater Cincinnati is now the largest metropolitan economy in Ohio, with a GMP of $132 billion. Nationally, Greater Cincinnati is the 28th largest local economy, followed by Columbus (29th) and Cleveland (30th).

• At 4.7%, unemployment in the combined Cincinnati/Dayton market is now slightly higher than the national average.

• Multifamily vacancy should remain between 5.5% and 6.0% with effective rent rates continuing to grow steadily.

Average Q3 employment increased by 25,000 jobs.

Average Q3 unemployment increased to 4.7%.

+2.0 +37% Y O Y B P S Y O Y

ECONOMIC EXPANSION

OUTLOOKJOB GROWTH & UNEMPLOYMENT RATE

Paycor is planning to double the size of its Norwood corporate headquarters, as it adds 1,064 new jobs.

In Monroe, a 1.3 million-square-foot fulfillment center is being built for Amazon, which will result in the creation of more than 1,000 full-time jobs.

UPS Supply Chain Solutions will add 130 jobs at a new West Chester facility by the end of 2020.

Automotive manufacturer Hematite is constructing a 106,000-square-foot U.S. headquarters / manufacturing facility in Englewood, which will create 100 jobs.

As part of its expansion, East Price Hill-based Q Laboratories is planning to add 90 new jobs.

Dayton-based manufacturer Composite Advantage LLC is looking to double its area workforce, by adding 90 new jobs.

a

a

a

a

a

The combined Cincinnati/Dayton region added more than 25,000 net jobs year-over-year per the Bureau of Labor Statistics’ (BLS) total employment average for the third quarter of 2017. The 25,000 new jobs represent a job growth rate of 2.0%, which is slightly higher than the growth rates from the prior three quarters. Industries that led job growth in the third quarter were Leisure & Hospitality (+9,800 net jobs), Professional & Business Services (+6,300 net jobs), and Trade/Transportation & Utilities (+5,500 net jobs).

EMPLOYMENT & UNEMPLOYMENT TRENDS

CINCINNATI/DAYTON JOB GROWTH TRENDS

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

1.42

1.43

1.44

1.45

1.46

1.47

1.48

1.49

1.50

1.51

Q4 Q1 Q2 Q3

CINCINNATI/DAYTON JOB GROWTH TRENDSEMPLOYMENT IN MILLIONS

2015-2016 2016-2017 YOY % Job Growth

CINCINNATI/DAYTON, OH

Q3 2015 Q3 2016 Q3 2017 FORECAST

U.S. UNEMPLOYMENT RATE 5.1% 4.9% 4.4%

EMPLOYMENT (% Change) 2.1% 1.5% 2.0%

LOCAL UNEMPLOYMENT RATE 4.4% 4.4% 4.7%

a

Forecast is 12-month outlook

EMPLOYMENT IN MILLIONS & JOB GROWTH (%)

Source: Moody’s Analytics

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

2CI N CI N N AT I / DAY TONMARKET INSIGHTThird Quarter 2017

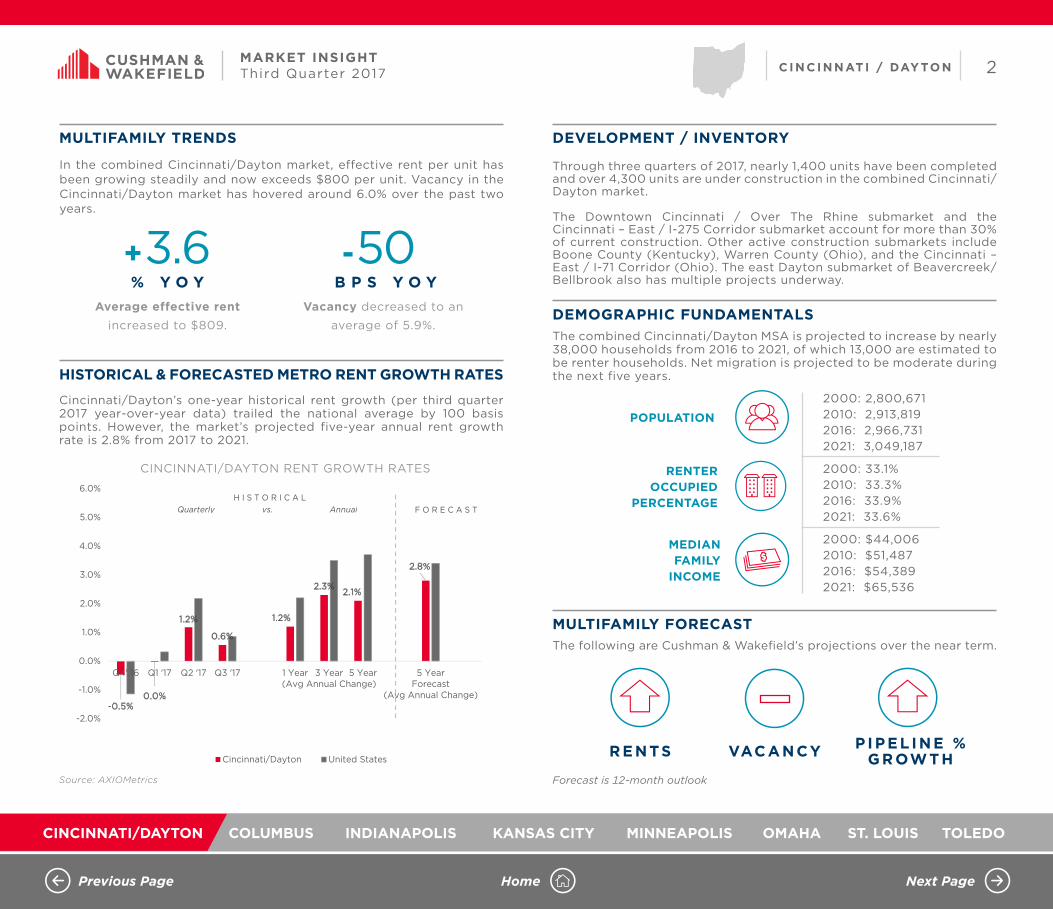

In the combined Cincinnati/Dayton market, effective rent per unit has been growing steadily and now exceeds $800 per unit. Vacancy in the Cincinnati/Dayton market has hovered around 6.0% over the past two years.

Cincinnati/Dayton’s one-year historical rent growth (per third quarter 2017 year-over-year data) trailed the national average by 100 basis points. However, the market’s projected five-year annual rent growth rate is 2.8% from 2017 to 2021.

Through three quarters of 2017, nearly 1,400 units have been completed and over 4,300 units are under construction in the combined Cincinnati/Dayton market.

The Downtown Cincinnati / Over The Rhine submarket and the Cincinnati – East / I-275 Corridor submarket account for more than 30% of current construction. Other active construction submarkets include Boone County (Kentucky), Warren County (Ohio), and the Cincinnati – East / I-71 Corridor (Ohio). The east Dayton submarket of Beavercreek/Bellbrook also has multiple projects underway.

The combined Cincinnati/Dayton MSA is projected to increase by nearly 38,000 households from 2016 to 2021, of which 13,000 are estimated to be renter households. Net migration is projected to be moderate during the next five years.

The following are Cushman & Wakefield’s projections over the near term.

MULTIFAMILY TRENDS

HISTORICAL & FORECASTED METRO RENT GROWTH RATES

DEVELOPMENT / INVENTORY

DEMOGRAPHIC FUNDAMENTALSAverage effective rentincreased to $809.

Vacancy decreased to an

average of 5.9%.

-0.5%0.0%

1.2%

0.6%

1.2%

2.3%2.1%

2.8%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Q4' 16 Q1 '17 Q2 '17 Q3 '17 1 Year 3 Year(Avg Annual Change)

5 Year 5 YearForecast

(Avg Annual Change)

CINCINNATI/DAYTON RENT GROWTH RATESHISTORICAL AND FORECAST

Cincinnati/Dayton United States

Quarterly vs. AnnualH I S T O R I C A L

F O R E C A S T

CINCINNATI/DAYTON RENT GROWTH RATES

+3.6 -50% Y O Y B P S Y O Y

2000: 2,800,6712010: 2,913,8192016: 2,966,7312021: 3,049,187

2000: 33.1%2010: 33.3%2016: 33.9%2021: 33.6%

2000: $44,0062010: $51,4872016: $54,3892021: $65,536

MULTIFAMILY FORECAST

VACANCYREN TS P IP EL INE % G ROWTH

Source: AXIOMetrics Forecast is 12-month outlook

POPULATION

MEDIANFAMILY

INCOME

RENTER OCCUPIED

PERCENTAGE

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

3CI N CI N N AT I / DAY TONMARKET INSIGHTThird Quarter 2017

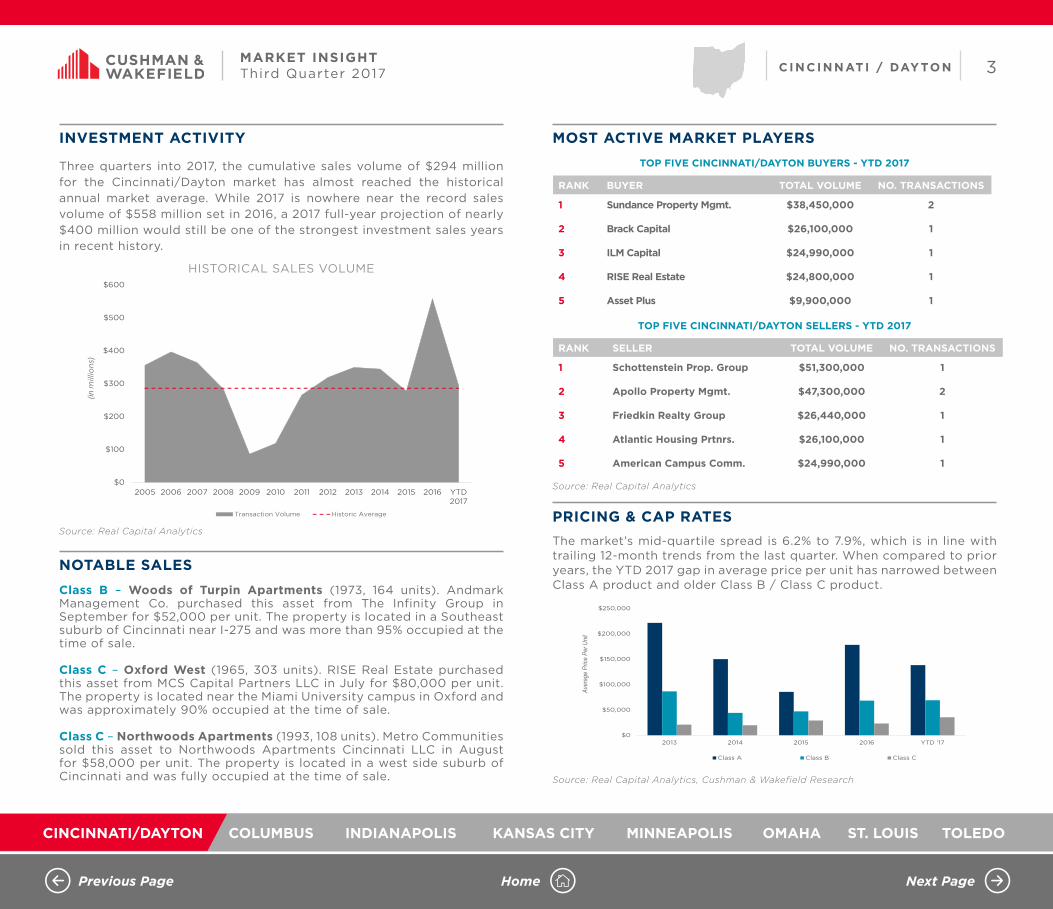

Three quarters into 2017, the cumulative sales volume of $294 million for the Cincinnati/Dayton market has almost reached the historical annual market average. While 2017 is nowhere near the record sales volume of $558 million set in 2016, a 2017 full-year projection of nearly $400 million would still be one of the strongest investment sales years in recent history.

Class B – Woods of Turpin Apartments (1973, 164 units). Andmark Management Co. purchased this asset from The Infinity Group in September for $52,000 per unit. The property is located in a Southeast suburb of Cincinnati near I-275 and was more than 95% occupied at the time of sale.

Class C – Oxford West (1965, 303 units). RISE Real Estate purchased this asset from MCS Capital Partners LLC in July for $80,000 per unit. The property is located near the Miami University campus in Oxford and was approximately 90% occupied at the time of sale.

Class C – Northwoods Apartments (1993, 108 units). Metro Communities sold this asset to Northwoods Apartments Cincinnati LLC in August for $58,000 per unit. The property is located in a west side suburb of Cincinnati and was fully occupied at the time of sale.

The market’s mid-quartile spread is 6.2% to 7.9%, which is in line with trailing 12-month trends from the last quarter. When compared to prior years, the YTD 2017 gap in average price per unit has narrowed between Class A product and older Class B / Class C product.

INVESTMENT ACTIVITY

NOTABLE SALES

MOST ACTIVE MARKET PLAYERS

PRICING & CAP RATES

$0

$100

$200

$300

$400

$500

$600

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 YTD2017

CINCINNATI/DAYTON ANNUAL SALES VOLUMEANNUAL SALES VOLUME ($ MILLIONS)

Transaction Volume Historic Average

(inm

illio

ns)

$0

$50,000

$100,000

$150,000

$200,000

$250,000

2013 2014 2015 2016 YTD '17

Class A Class B Class C

CINCINNATI/DAYTON PRICING TRENDSPRICE / UNIT & CAP RATE

Aver

age

Price

Per

Uni

t

TOP FIVE CINCINNATI/DAYTON BUYERS - YTD 2017

Source: Real Capital Analytics

TOP FIVE CINCINNATI/DAYTON SELLERS - YTD 2017

HISTORICAL SALES VOLUME

RANK BUYER TOTAL VOLUME NO. TRANSACTIONS

1 Sundance Property Mgmt. $38,450,000 2

2 Brack Capital $26,100,000 1

3 ILM Capital $24,990,000 1

4 RISE Real Estate $24,800,000 1

5 Asset Plus $9,900,000 1

RANK SELLER TOTAL VOLUME NO. TRANSACTIONS

1 Schottenstein Prop. Group $51,300,000 1

2 Apollo Property Mgmt. $47,300,000 2

3 Friedkin Realty Group $26,440,000 1

4 Atlantic Housing Prtnrs. $26,100,000 1

5 American Campus Comm. $24,990,000 1

Source: Real Capital Analytics, Cushman & Wakefield Research

Source: Real Capital Analytics

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

4CI N CI N N AT I / DAY TONMARKET INSIGHTThird Quarter 2017

Clifton/Corryville

• Developer Trinitas Ventures, along with Harrison Street Real Estate Capital, has purchased multiple properties near the University of Cincinnati campus, including the former Deaconess Hospital. A mixed-used development is being planned for the area, including a 357-unit apartment complex called the Collegiate. This complex will feature fully-furnished units and is scheduled to be complete in the fall of 2019.

Oakley

• To meet growing multifamily demand, Nashville-based Hickory Capital Group is building an 82,000-square foot indoor self-storage facility on the site of a former restaurant on Madison Road. CubeSmart will be three stories tall and climate-controlled. The project is expected to be complete in April of 2018.

Covington

• Following the demolition of a former bank building, construction will begin on a 187-unit luxury apartment complex called River Haus. The $40 million project is being built on Fifth Street in Covington’s MainStrasse Village and is being developed by Flaherty & Collins Properties.

Downtown Dayton

• In the mixed-use Water Street District, Crawford Hoying and Woodard Development are in the early stages of developing a 100-unit apartment complex. The project would be located on the site of a soon-to-be demolished industrial building on East First Street. The complex is expected to be complete in 2019.

SUBMARKET OVERVIEW SELECT SUBMARKET NEWS

RENTS & VACANCY BY SUBMARKET

$969

$781

$733

$736

$694

$1,007

$1,355

$619

$576

$628

$996

$623

$664

$810

$946

$835

$761

$888

$832

$824

$974

Warren County

Miamisburg/Moraine

Miami County

Kenton County

Fairborn/WPAFB

Downtown Dayton/Oregon Dist.

Downtown Cincinnati/O-T-R

Dayton - North/West

Dayton - East

Dayton - Central/West

Clifton/Corryville

Clark County

Cincinnati - West

Cincinnati - North

Cincinnati - East / I-71 Corr.

Cincinnati - East / I-275 Corr.

Centerville/Kettering

Campbell County

Butler County

Boone County

Beavercreek/Bellbrook

CINCINNATI/DAYTON SUBMARKET TRENDSRENTS & VACANCY

5.0%

7.4%

5.5%

4.1%

4.6%

10.0%

7.1%

5.1%

4.7%

9.3%

4.7%

3.9%

5.8%

4.4%

5.1%

3.9%

6.1%

4.7%

6.0%

6.3%

6.7%

Warren County

Miamisburg/Moraine

Miami County

Kenton County

Fairborn/WPAFB

Downtown Dayton/Oregon…

Downtown Cincinnati/O-T-R

Dayton - North/West

Dayton - East

Dayton - Central/West

Clifton/Corryville

Clark County

Cincinnati - West

Cincinnati - North

Cincinnati - East / I-71 Corr.

Cincinnati - East / I-275 Corr.

Centerville/Kettering

Campbell County

Butler County

Boone County

Beavercreek/Bellbrook

RENTS & VACANCY BY SUBMARKET

356

528

218

76

355

700

406

114

804

11058

226

428

0

100

200

300

400

500

600

700

800

900

CINCINNATI/DAYTON SUBMARKET TRENDSUnder ConstructionUNDER CONSTRUCTION BY SUBMARKET

Source: CoStar, Cushman & Wakefield ResearchNote: Submarkets are defined by Cushman & Wakefield Research

COLUMBUS

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

1COLUMB USMARKET INSIGHTThird Quarter 2017

The following are select announcements from the third quarter of 2017:

• Greater Columbus was one of North America’s “most competitive cities” in both automotive and logistics by a recent Site Selection magazine report

• At 4.4%, unemployment in the Columbus area remains on-par with the national average.

• Columbus is the largest multifamily market in Ohio with more than 7,600 apartment units under construction and increasing effective rental rates.

Average Q3 employment increased by 13,000 jobs.

Average Q3 unemployment increased to 4.4%.

+2.0 +27% Y O Y B P S Y O Y

ECONOMIC EXPANSION

OUTLOOKJOB GROWTH & UNEMPLOYMENT RATE

Honda is adding 300 new jobs between its manufacturing plants in Marysville and Anna.

Meijer is hiring 300 new employees across 13 of its Central Ohio area stores.

Housing developer Woda Group is relocating its Central Ohio office to the Brewery District and plans to add 100 new jobs.

Facebook will be building a new 900,000-square-foot data center in New Albany that will create 100 jobs.

Ascena Retail Group, the parent company of Catherines stores, will add 100 jobs in Central Ohio, as it relocates operations from Philadelphia.

Fluvitex USA, an Ikea bedding supplier, is planning to add 80 full-time equivalent jobs to its Groveport facility.

a

a

a

a

a

The Columbus market added more than 13,000 net jobs year-over-year per the Bureau of Labor Statistics’ (BLS) total employment average for the third quarter of 2017. The 13,000 new jobs represent a job growth rate of 2.0%, which is similar to the growth rates from each the prior three quarters. Industries that led job growth in the third quarter were Mining/Logging/Construction (+5,800 net jobs), Manufacturing (+5,600 net jobs), and Government (+3,600 net jobs).

EMPLOYMENT & UNEMPLOYMENT TRENDS

COLUMBUS JOB GROWTH TRENDS

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

1.02

1.03

1.04

1.05

1.06

1.07

1.08

1.09

1.10

Q4 Q1 Q2 Q3

COLUMBUS JOB GROWTH TRENDSEMPLOYMENT IN MILLIONS

2015-2016 2016-2017 YOY % Job Growth

COLUMBUS, OH

Q3 2015 Q3 2016 Q3 2017 FORECAST

U.S. UNEMPLOYMENT RATE 5.1% 4.9% 4.4%

EMPLOYMENT (% Change) 2.2% 2.3% 2.0%

LOCAL UNEMPLOYMENT RATE 4.0% 4.1% 4.4%

a

Forecast is 12-month outlook

EMPLOYMENT IN MILLIONS & JOB GROWTH (%)

Source: Moody’s Analytics

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

2COLUMB USMARKET INSIGHTThird Quarter 2017

Effective rent per unit has been growing significantly in the Columbus market over the past few years. For the first time ever, effective rent now exceeds $860 per unit. Vacancy in the Columbus market has ranged between 5.0% and 6.0% over the past two years.

Columbus’ one-year historical rent growth (per third quarter 2017 year-over-year data) was ahead of the national average by 50 basis points. Furthermore, the market’s projected five-year annual rent growth rate is 3.0% from 2017 to 2021.

Through three quarters of 2017, nearly 2,600 units have been completed and more than 7,600 units are under construction in the eight-county Columbus Metro Area.

Downtown Columbus is currently the most active development submarket. Activity is also strong in the northern Dublin/Hilliard submarket and the New Albany submarket, along with the far northern counties of Delaware, Morrow and Union.

The Columbus MSA is projected to increase by more than 43,000 households from 2016 to 2021, of which 16,000 are estimated to be renter households. Net migration is projected to accelerate during the next five years.

The following are Cushman & Wakefield’s projections over the near term.

MULTIFAMILY TRENDS

HISTORICAL & FORECASTED METRO RENT GROWTH RATES

DEVELOPMENT / INVENTORY

DEMOGRAPHIC FUNDAMENTALSAverage effective rentincreased to $864.

Vacancy decreased to an

average of 5.3%.

-0.6%

0.3%

2.5%

1.4%

3.5% 3.4%3.2% 3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Q4' 16 Q1 '17 Q2 '17 Q3 '17 1 Year 3 Year(Avg Annual Change)

5 Year 5 YearForecast

(Avg Annual Change)

COLUMBUS RENT GROWTH RATESHISTORICAL AND FORECAST

Columbus United States

Quarterly vs. AnnualH I S T O R I C A L

F O R E C A S T

COLUMBUS RENT GROWTH RATES

+5.1 -20% Y O Y B P S Y O Y

2000: 1,674,6532010: 1,901,9792016: 2,022,1052021: 2,122,571

2000: 36.1%2010: 37.1%2016: 37.7%2021: 37.2%

2000: $44,4452010: $51,1882016: $56,6652021: $67,923

MULTIFAMILY FORECAST

VACANCYREN TS P IP EL INE % G ROWTH

Source: AXIOMetrics Forecast is 12-month outlook

POPULATION

MEDIANFAMILY

INCOME

RENTER OCCUPIED

PERCENTAGE

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

3COLUMB USMARKET INSIGHTThird Quarter 2017

Three quarters into 2017, the cumulative sales volume of $280 million for the Columbus market is on-pace to reach nearly $375 million for the year. The 2017 projection would fall short of the record-breaking multifamily investment sales years of 2014, 2015, and 2016, which were $861 million, $702 million and $448 milion respectively.

Class B – Sterling Place (1990, 300 units). Connor Group purchased this asset from CORE Realty Holdings in September for $108,000 per unit. The property is located in Northwest Columbus and was almost fully occupied at the time of sale.

Class B – Alkire Glen (2000, 252 units). Crawford Hoying sold this asset to RealSource Management LLC in July for $79,000 per unit. The property is located near I-270 in Southeast Columbus and was over 95% occupied at the time of sale.

Class C – Creekside at Taylor Square (2001, 532 units). Crawford Hoying sold this asset to Monarch Investments in August for $97,000 per unit. The property is located in the eastern suburb of Reynoldsburg and was 100% occupied at the time of sale.

The market’s mid-quartile spread is 5.9% to 7.3%, which is similar to the trailing 12-month trend from the last quarter.

INVESTMENT ACTIVITY

NOTABLE SALES

MOST ACTIVE MARKET PLAYERS

PRICING & CAP RATES

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 YTD2017

COLUMBUS ANNUAL SALES VOLUMEANNUAL SALES VOLUME ($ MILLIONS)

Transaction Volume Historic Average

(inm

illio

ns)

$0

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

2013 2014 2015 2016 YTD '17

Class A Class B Class C

COLUMBUS PRICING TRENDSPRICE / UNIT & CAP RATE

Aver

age

Pric

e Pe

r Uni

t

TOP FIVE COLUMBUS BUYERS - YTD 2017

Source: Real Capital Analytics

TOP FIVE COLUMBUS SELLERS - YTD 2017

HISTORICAL SALES VOLUME

RANK BUYER TOTAL VOLUME NO. TRANSACTIONS

1 Albion Residential $55,450,000 1

2 Independence Realty Trust $50,900,000 2

3 Cortland Partners $49,000,000 1

4 Connor Group $32,500,000 1

5 CDEC $30,000,000 1

RANK SELLER TOTAL VOLUME NO. TRANSACTIONS

1 Connor Group $55,450,000 1

2 Hamilton Point Investments $50,900,000 2

3 Crawford Hoying $49,000,000 1

4 CORE Realty Holdings $32,500,000 1

5 UBS $30,000,000 1

Source: Real Capital Analytics, Cushman & Wakefield Research

Source: Real Capital Analytics

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

4COLUMB USMARKET INSIGHTThird Quarter 2017

SUBMARKET OVERVIEW SELECT SUBMARKET NEWS

RENTS & VACANCY BY SUBMARKET

Italian Village

• Dublin-based Borror Properties is close to breaking ground on an unnamed multi-story apartment complex on East Fifth Street. The 89-unit complex will be built on the site of the former Acme Taxi building and is expected to be complete by the Spring of 2019.

Grandview Heights

• Plans are underway to redevelop the current White Castle corporate headquarters into a $65 million mixed-use complex, located west of downtown. In addition to new offices, the project will include 270 new housing units and a community center.

Downtown

• Denver-based Charles Street Investment Partners LLC is proposing a six story mixed-used development on East Long Street, with a unique block-O structure. The project would include 225 apartment units.

Short North

• A 100-unit apartment complex is being planned by Columbus-based Pizzuti Companies on a West First Avenue site. The six-story complex will be located adjacent to another new Pizzuti office and retail development project.

Westerville

• The Fenimore will be a 180-unit apartment complex which soon begin construction on Hamilton Road. The project will be built on an 11-acre site adjacent to a number of other multifamily complexes by developers Robert Weiler Co. and Donald W. Kelley & Associates.

$988

$753

$756

$728

$994

$747

$813

$965

$1,270

$945

$732

Upper Arlington/OSU

Southwest Columbus /Madison Co.

Southeast Columbus

Northeast Columbus

New Albany

Licking Co.

Fairfield Co. / Pickaway Co.

Dublin/Hilliard

Downtown/ShortNorth/Brewery

Delaware Co. / Morrow Co. /Union Co.

Bexley/Whitehall

COLUMBUS SUBMARKET TRENDSRENTS & VACANCY

4.8%

5.3%

8.0%

4.9%

4.8%

5.0%

3.4%

5.2%

3.7%

6.1%

5.2%

Upper Arlington/OSU

Southwest Columbus /Madison Co.

Southeast Columbus

Northeast Columbus

New Albany

Licking Co.

Fairfield Co. /Pickaway Co.

Dublin/Hilliard

Downtown/ShortNorth/Brewery

Delaware Co. / MorrowCo. / Union Co.

Bexley/Whitehall

RENTS & VACANCY BY SUBMARKET

199

1,011

2,242

2,001

53

1,314

136

665

0

500

1,000

1,500

2,000

2,500

COLUMBUS SUBMARKET TRENDSUnder ConstructionUNDER CONSTRUCTION BY SUBMARKET

Source: CoStar, Cushman & Wakefield ResearchNote: Submarkets are defined by Cushman & Wakefield Research

INDIANAPOLIS

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

MARKET INSIGHTINDIANAPOLIS MULTIFAMILY REPORT | THIRD QUARTER 2017

CUSHMAN & WAKEFIELD INDIANAPOLIS MULTIFAMILY RESEARCH

The Cushman & Wakefield Multifamily Research Team provides in-depth coverage of the Indianapolis Metropolitan Statistical Area. In addition to analyzing multifamily rent and sale trends, these reports examine employment data, key economic announcements, and development pipeline news.

RESEARCH TEAM

IN THIS EDITION

32

32

32

36

38

9

9

9

9

9

9

9

9

9

44

44

44

44

37

37

37

37

67

6739

39

39

39

39

39

4747

38

38

38

38

19

19

3232

32

42

42

75

75

75

75

42

42

67

67

44

67

67

37

37

36

36

36

36

40

40

4040

40

52

52

31

31

31

31

31

31

31

31

31

52

4040

13

38

128

213

109

234

135

144

144

142

135

135

135

252252

267

267

267

267

236

234

236

252

234

109

28

37

9

37

36

52

52

52

52

52

136

421

421

421

421

421

136

36

Greenfield

Anderson

Pendleton

Elwood

Bud

Edinburgh

Martinsville

Franklin

Whiteland

Greenwood

IMS

IndianapolisInternational

Airport

Mooresville

Plainfield

DanvilleAvon

Brownsburg

Zionsville

MeridianHills

Lawrence

Beech Grove

Indianapolis

Southport

Fairland

Shelbyville

Fishers

Carmel

Noblesville

Lebanon

Speedway

69

69

69

70

70

70

70

74

74

74

74

74

74

74

65

65

65

65

65

65

65

65

74

465

465

465

465

865465

465

70

Bud

CARMEL

NORTHWEST

NORTHEAST

DOWNTOWNWEST

CARMELZIONSVILLEZIONSVILLE

NORTHNORTH

FISHERSFISHERS

NORTHWEST

NORTHEAST

SOUTHSOUTH

SOUTHWESTSOUTHWEST

SOUTHEASTSOUTHEAST

GREENWOODGREENWOOD

DOWNTOWN

CENTERCENTER

EASTEASTWEST

Downtown

Center

North

Northeast

East

Southeast

South

Southwest

West

Northwest

Zionsville

Carmel

Fishers

Greenwood

SCOTT POLLOM, CCIMDIRECTOR, CAPITAL [email protected]

MATT NIEHOFFRESEARCH [email protected]

MITCH OSTROWSKIRESEARCH [email protected]

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

2I N DI A N A POL I SMARKET INSIGHTThird Quarter 2017

+1.5% Y O Y

Average Q3 employment increased by 19,200.

-80B P S Y O Y

Average Q3 unemployment decreased to 3.2%.

ECONOMIC EXPANSIONThe following are select announcements from third quarter 2017:

OUTLOOK• The industrial market inventory continues to expand. By year-end,

construction deliveries are expected to set a new market high.• Construction (+7.3% YOY), Financial Activities (+6.5% YOY) and Trade

(+2.0% YOY) jobs all grew at above-average rates.• Job growth in Indianapolis will slow in the short-term as its current

expansion cycle matures, with Manufacturing employment staying steady and Technology jobs continuing to grow.

JOB GROWTH & UNEMPLOYMENT RATE

EMPLOYMENT & UNEMPLOYMENT TRENDSThe Indianapolis market added 19,200 net jobs year-over-year for third quarter 2017. The 19,200 new jobs represent a job growth rate of 1.5%, which is 70 basis points less than the growth rate from the prior quarter. The top sectors leading the way were Financial Activities (+4,300 net jobs), Education and Health Services (+4,000 net jobs), Construction (+3,700 net jobs), Government (+3,300 net jobs).

INDIANAPOLIS JOB GROWTH TRENDSEMPLOYMENT IN MILLIONS & JOB GROWTH (%)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

Q4 Q1 Q2 Q3

INDIANAPOLIS JOB GROWTH TRENDSEMPLOYMENT IN MILLIONS

2015-2016 2016-2017 YOY % Job Growth

INDIANAPOLIS

Q3 2015 Q3 2016 Q3 2017 FORECAST

NATIONAL UNEMPLOYMENT 5.1% 4.9% 4.4%

EMPLOYMENT (% Change) 2.9% 2.3% 1.5%

UNEMPLOYMENT RATE (%) 4.4% 4.4% 3.2%

Forecast is 12-month outlook

Source: Moody’s Analytics

a Amazon expects to hire more than 120,000 holiday jobs in 33 states, 7,000 jobs will be added locally.

a KAR Auction Services announced plans to build an $80-mil-lion corporate campus which will add 400 jobs.

a FedEx Corporation will build a $259-million distribution center in Greenwood and expects to hire 450 employees.

a Clean Slate Technology Group expects to invest $1 million to expand which will add 50 jobs by 2020.

aFuzic will add 250 jobs when it completes the build-out of just under 12,000-square-foot space in the newly constructed Braden Building.

a TechPoint received a $5.7-million grant to expand its tech- focused talent acquisition programs locally.

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

3I N DI A N A POL I SMARKET INSIGHTThird Quarter 2017

0.9% 0.9% 1.3% 0.0%

3.2%

10.6%

15.8%

22.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Q4' 16 Q1 '17 Q2 '17 Q3 '17 1 Year(YOY)

3 Year(Total

Change)

5 Year(Total

Change)

5 YearForecast

(TotalChange)

INDIANAPOLIS RENT GROWTH RATES HISTORICAL AND FORECAST

Indianapolis United States

H I S T O R I C A L

F O R E C A S T

INDIANAPOLIS RENT GROWTH RATES

Forecast is 12-month outlook

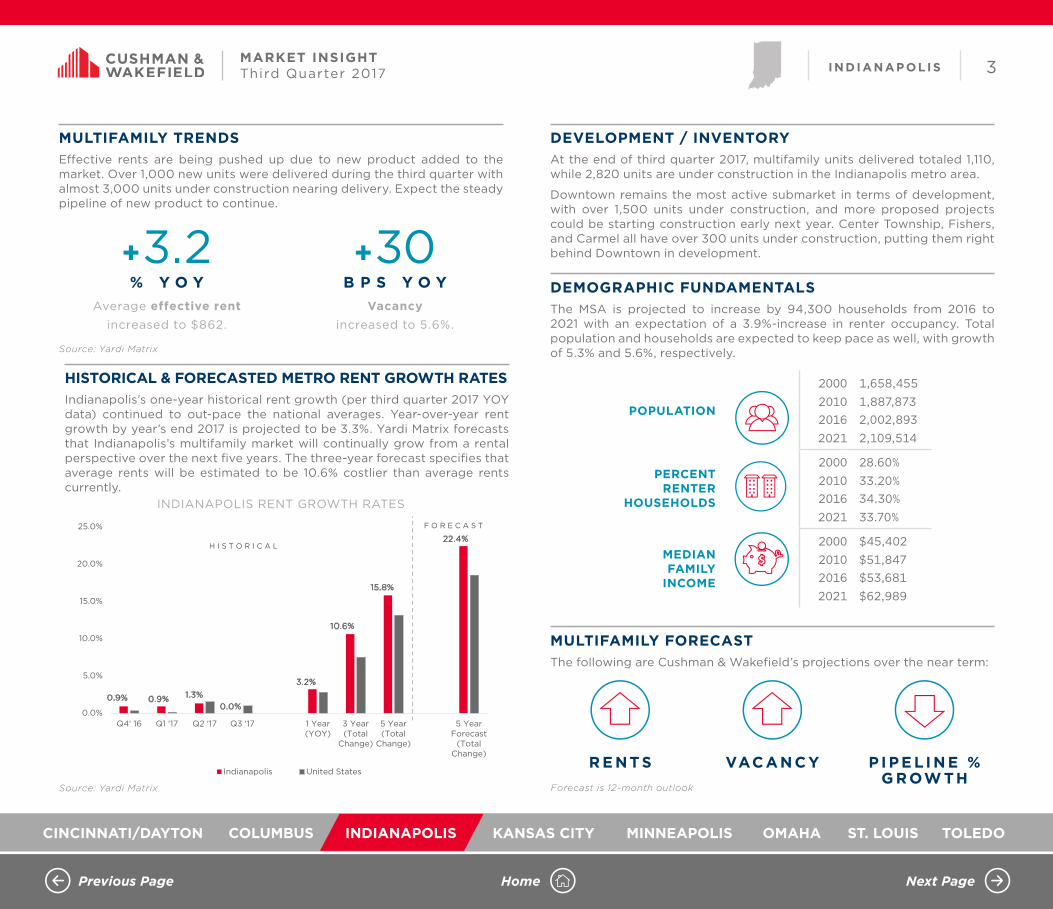

MULTIFAMILY TRENDSEffective rents are being pushed up due to new product added to the market. Over 1,000 new units were delivered during the third quarter with almost 3,000 units under construction nearing delivery. Expect the steady pipeline of new product to continue.

DEVELOPMENT / INVENTORYAt the end of third quarter 2017, multifamily units delivered totaled 1,110, while 2,820 units are under construction in the Indianapolis metro area.

Downtown remains the most active submarket in terms of development, with over 1,500 units under construction, and more proposed projects could be starting construction early next year. Center Township, Fishers, and Carmel all have over 300 units under construction, putting them right behind Downtown in development.

DEMOGRAPHIC FUNDAMENTALSThe MSA is projected to increase by 94,300 households from 2016 to 2021 with an expectation of a 3.9%-increase in renter occupancy. Total population and households are expected to keep pace as well, with growth of 5.3% and 5.6%, respectively.

MULTIFAMILY FORECASTThe following are Cushman & Wakefield’s projections over the near term:

HISTORICAL & FORECASTED METRO RENT GROWTH RATESIndianapolis’s one-year historical rent growth (per third quarter 2017 YOY data) continued to out-pace the national averages. Year-over-year rent growth by year’s end 2017 is projected to be 3.3%. Yardi Matrix forecasts that Indianapolis’s multifamily market will continually grow from a rental perspective over the next five years. The three-year forecast specifies that average rents will be estimated to be 10.6% costlier than average rents currently.

+3.2% Y O Y

Average effective rent increased to $862.

+30B P S Y O Y

Vacancy

increased to 5.6%.

R E NT S

VAC A N C Y P I P E L I N E % G ROW TH

POPULATION

2000 1,658,4552010 1,887,8732016 2,002,8932021 2,109,514

PERCENTRENTER

HOUSEHOLDS

2000 28.60%2010 33.20%2016 34.30%2021 33.70%

MEDIAN FAMILY

INCOME

2000 $45,4022010 $51,8472016 $53,6812021 $62,989

Source: Yardi Matrix

Source: Yardi Matrix

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

4I N DI A N A POL I SMARKET INSIGHTThird Quarter 2017

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 YTD2017

INDIANAPOLIS ANNUAL SALES VOLUMEANNUAL SALES VOLUME ($ MILLIONS)

Transaction Volume Historic Average

(in m

illio

ns)

INDIANAPOLIS PRICING TRENDSPRICE / UNIT & CAP RATE

$0

$50,000

$100,000

$150,000

$200,000

2013 2014 2015 2016 YTD '17

Class A Class B Class C

TOP FIVE INDIANAPOLIS BUYERS - YTD 2017

Source: Real Capital Analytics

TOP FIVE INDIANAPOLIS SELLERS - YTD 2017

HISTORICAL SALES VOLUME

RANK BUYER TOTAL VOLUME NO. TRANSACTIONS

1 Sterling Group/Virtus RE Capital $98,119,702 1

2 Pedcor Management $88,050,000 2

3 Birge & Held $60,693,750 2

4 Covenant Capital Group $52,900,000 2

5 Lighthouse Group $52,500,000 3

RANK SELLER TOTAL VOLUME NO. TRANSACTIONS

1 Harbor Group Int'l. $117,250,000 2

2Bluestone Holdings / QVT Mount

Auburn Cap$98,119,702 1

3 Meridian Realty $74,300,000 2

4 Sinclair Broadcast Group $72,250,000 1

5 Sheehan Development $56,900,000 2

Source: Real Capital Analytics, Cushman & Wakefield Research

Source: Real Capital Analytics

INVESTMENT ACTIVITYThrough the third quarter, YTD investment activity is tracking over $200 million above the historical average. Nearly $150 million was invested during the third quarter.

Investment activity already outpaces the total market investment in 2015 and is nearing levels seen in 2016. With announcements of additional technology and warehouse jobs coming to the market, investor dollars should continue to steadily pour into the market due to demand of space by the millennial workforce.

PRICING & CAP RATESIn 2017, the average cap rate for Class A product is up from 5.6% in 2016 to 6.2% in 2017. Conversely, average Class B cap rate declined to 5.9% proving favorable for landlords. The following graph reflects price per unit trends by asset class.

MOST ACTIVE MARKET PLAYERS

NOTABLE SALES

• Milhaus Development sold Mozzo Apartments (2013, 65 units, $215,385 per unit) and The Maxwell (2008, 105 units, $190,476 per unit) to Birge & Held for a total of $34 million. Both are Class A assets.

• Samuel Geltman & Co. sold Columns of Castleton (1969, 398 units) for $76,000 per unit to Covenant Capital Group. The asset is located in the Northeast submarket.

• Domo Development Company sold Eaglepoint Apartments (2015, 240 units) in July to AR Building Co. for $28 million at nearly $117,000 per unit.

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

5I N DI A N A POL I SMARKET INSIGHTThird Quarter 2017

SUBMARKET OVERVIEW SELECT SUBMARKET NEWS

Downtown

• Flaherty & Collins’ 28-story, 292-unit, luxury mixed-use development, 360 Market Square Apartments, is under construction and is expected to be finished in the early part of 2018.

North

• Requests For Qualifications (RFQs) for the potential White River Development Plan are now being considered for the Broad Ripple area.

• TWG Development received approvals to build a $27.1-million, 186-unit complex despite opposition from the Nora community. The “Notch at Nora” includes 18 studio, 98 one-bedroom, and 70 two-bedroom units.

Carmel

• Midtown Carmel announced plans to widen the Monon Trail to accommodate the $210-million mixed-use investment being made in the area. The Midtown development will include office, retail and multifamily developments clustered within a 17-acre area.

Fishers

• IKEA and Topgolf have officially opened in Fishers. IKEA is expected to average $90-million in annual revenue while Topgolf is projected to average $24.5 million.

Zionsville

• Anson in Whitestown—a $1-billion commercial, retail and housing development—just announced the Shoppes at Whitestown. The $50-million project is expected to feature 275,000 square feet of retail, services, and restaurants.

$1,058

$692

$813

$907

$734

$736

$721

$853

$815

$1,138

$640

$1,423

$932

$1,128

Zionsville

West

Southwest

Southeast

South

Northwest

Northeast

North

Greenwood

Fishers

East

Downtown

Center

Carmel

INDIANAPOLIS SUBMARKET TRENDSRENTS & VACANCY

3.5%

7.5%

5.4%

7.2%

5.8%

6.0%

7.6%

5.2%

5.1%

8.5%

6.2%

4.8%

7.5%

6.7%

Zionsville

West

Southwest

Southeast

South

Northwest

Northeast

North

Greenwood

Fishers

East

Downtown

Center

Carmel

305343

1,515

354

194110

0

200

400

600

800

1,000

1,200

1,400

1,600

Carmel Center Downtown Fishers North Southeast

INDIANAPOLIS SUBMARKET TRENDSUnder Construction

RENTS & VACANCY BY SUBMARKET

UNDER CONSTRUCTION BY SUBMARKET

Source: Yardi Matrix, Cushman & Wakefield ResearchNote: Submarkets are defined by Cushman & Wakefield Research

KANSAS CITY

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

1KA N SAS C I T YMARKET INSIGHTThird Quarter 2017

The following are select announcements from third quarter 2017:

• Demand for residential space continued to outpace supply as the combined inventory of homes for sale in the Kansas City metro area has fallen 16.7% over the past twelve months.

• Johnson County, KS has the highest percentage of residents ages 25 and over with at least a Bachelor’s degree of any county in the United States with a population of at least 250,000.

• There are 3,704 units under construction in Downtown Kansas City as development in the area remains at a record high.

Kansas City has averaged 1,800

new jobs per month since Q3 2014.

Kansas City’s unemployment rate

reamains below the US level.

+1.3 -30% Y O Y B P S Y O Y

ECONOMIC EXPANSION

OUTLOOKJOB GROWTH & UNEMPLOYMENT RATE

Creative Planning is hoping to double employment to 400 in their new headquarters.

Horizons Global will create 150 jobs at their new distribution facility at Logistics Park Kansas City.

Cerner continues to add hundreds of jobs as it moves forward with its contract for the Department of Defense.

Amazon continues to hire for at least 1,000 full-time jobs at their new fulfillment center near I-70 and the Turner Diagonal, in addition to seasonal workers.

Sioux Chief is aiming to create 100 additional jobs at their new headquarters in the Centerpoint Intermodal.

Spring Venture Group will be initiating the hiring of 1,000 employees as the move into their new offices.

a

a

a

a

a

The Kansas City job market remains in robust health, with an umemployment rate of just 4.1%. More importantly, job growth remains strong with a 3.6% increase in the seasonally adjusted number of non-farm payroll over the past 24 months. The biggest constraint on job growth in Kansas City has been the low unemployment rate, although an increase in total population is helping in that area. According to estimates by the United States Census, the total population for Kansas City increased 2.4% from 2015 to 2016, the latest timeframe for which numbers are available.

EMPLOYMENT & UNEMPLOYMENT TRENDS

KANSAS CITY

Q3 2015 Q3 2016 Q3 2017 FORECAST

NATIONAL UNEMPLOYMENT 5.1% 4.9% 4.4%

EMPLOYMENT (% Change) 2.1% 2.3% 1.3%

UNEMPLOYMENT RATE (%) 4.7% 4.4% 4.1%

a

Forecast is 12-month outlook

Source: Bureau of Labor Statistics

KANSAS CITY JOB GROWTH TRENDSEMPLOYMENT IN MILLIONS & JOB GROWTH (%)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1,020

1,030

1,040

1,050

1,060

1,070

1,080

1,090

Q4 Q1 Q2 Q3

2015-2016 2016-2017 YOY % Job Growth

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

2KA N SAS C I T YMARKET INSIGHTThird Quarter 2017

-0.4%

-0.1%

1.4%

0.5%

1.4%

7.0%

13.1%13.9%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

Q4'16 Q1'17 Q2'17 Q3'17 1 Year(YOY)

3 Year 5 Year 5 YearForecast

Kansas City U.S.

H I S T O R I C A L F O R E C A S T

Effective rents moved slightly higher, driven in large part by the continued development of new, higher-priced units Downtown. Developments in the Central Business District, Crossroads, and the River Market should drive rates higher over the next 12 months.

The rate of growth for rent rates in Kansas City has been slowing. Over the past 12 months the growth rate in Kansas City was only 60.5% of the national average, while over the last five years Kansas City’s growth rate has been 74.4% of the national average. Forecasts show that over the next five years Kansas City growth rates should accelerate and come more in line with national trends.

For the 12-month period ending September 30, 2017, 8,660 units were completed and approximately 6,300 were under construction at the time. These rates are at all-time highs, but the overall rate of development has remained steady for at least 24 months.

The downtown urban revival remains the focus of new development, with over 3,700 units currently under construction in and around the area.

Kansas City’s population is projected to increase by almost 100,000 people over the next five years, while the percentage of renters is expected to remain steady at just over one-third of the total population.

The following are Cushman & Wakefield’s projections over the near term.

MULTIFAMILY TRENDS

HISTORICAL & FORECASTED METRO RENT GROWTH RATES

DEVELOPMENT / INVENTORY

DEMOGRAPHIC FUNDAMENTALSAverage effective rentincreased to $961.

Vacancy decreased to an

average of 4.2%.

+1.4 -118% Y O Y B P S Y O Y

2000: 1,811,2082010: 2,009,3402016: 2,093,4382021: 2,188,903

2010: 32.8% 2016: 34.0% 2021: 33.8%

2000: $45,9312010: $54,8752016: $58,5212021: $68,965

POPULATION

RENTER OCCUPIED

PERCENTAGE

MEDIAN FAMILY

INCOME

MULTIFAMILY FORECAST

VACANCYREN TS P IP EL INE % G ROWTH

Forecast is 12-month outlookSource: AXIOMetrics

KANSAS CITY RENT GROWTH RATES

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

3KA N SAS C I T YMARKET INSIGHTThird Quarter 2017

The volume of investment activity in the Kansas City market was strong through the first six months of the year, but the pace slowed in the third quarter. Year-to-date there has been $426.6 million in total transactions, which puts the market behind pace to match the five-year average of $639.3 million. However there were some encouraging signs during the third quarter.

The per-unit-price jumped up significantly in the third quarter, and three-quarters of the way through 2017, Class A and Class B transactions have accounted for 84.3% of the total number of units transacted. Increased investment in higher-end properties could quickly bring volume back in line with historical averages.

Class A – The most significant Class transaction of the third quarter was the Province of Briarcliff, which was purchased by Forum Real Estate Group for $18.8 million, or $156,000 per unit. A few years ago Northland Apartments trading at those values would have been a major surprise, but the last few years have seen a drastic increase in the value of apartments north of the river, especially those around Briarcliff.

Class B – A local partnership led by Jones Development Co. purchased a total of 588 units spread across five different complexes in Prairie Village, KS. The group now owns 73% of all apartments in the Kansas City suburb.

The spread of cap rates for the middle fifty percent of transactions was 5.8% to 6.6% for the twelve months ending September 30, 2017. The median cap rate during that period of time was 6.0%.

INVESTMENT ACTIVITY

NOTABLE SALES

MOST ACTIVE MARKET PLAYERS

PRICING & CAP RATES

TOP FIVE KANSAS CITY BUYERS - YTD 2017

Source: Real Capital Analytics

TOP FIVE KANSAS CITY SELLERS - YTD 2017

RANK BUYER TOTAL VOLUME NO. TRANSACTIONS

1 CRES Management $70,083,000 1

2 PRG Managment $58,250,000 1

3 BH Managment Services, LLC $55,550,000 2

4 Fogelman Management Group $48,100,000 1

5 Starwood Capital $42,800,000 1

RANK SELLER TOTAL VOLUME NO. TRANSACTIONS

1 MAA REIT $70,083,000 1

2 Somerset Partners $58,250,000 1

3 Preferred Apartment Comm. $48,100,000 1

4 Milestone Apartments REIT $42,800,000 1

5 Banner Apartments $28,000,000 1

Source: Real Capital Analytics

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2011 2012 2013 2014 2015 2016 YTD 2017

Transaction Volume Historic Average

(in m

illio

ns)

$221

,495

$150

,210

$85,

558

$178

,247

$171

,247

$ 86,

624

$44,

317

$47,

201

$68,

464

$79,

372

$ 21,1

79

$19,

928

$29,

251

$23,

177

$22,

875

$0

$50,000

$100,000

$150,000

$200,000

$250,000

2013 2014 2015 2016 YTD '17

Class A Class B Class C

Source: Real Capital Analytics, Cushman & Wakefield Research

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

4KA N SAS C I T YMARKET INSIGHTThird Quarter 2017

SUBMARKET OVERVIEW SELECT SUBMARKET NEWS

Downtown Area

• Work is now getting started on new apartments near the Berkley Riverfront. Additionally, plans are moving forward on an extension for the KC Streetcar to serve the area, which could accelerate even more development.

Plaza & Midtown

• Renovations have been completed at Plaza Club City Apartments near the Country Club Plaza. The total investment in upgrading the complex was over $7 million and included substantial upgrades to the common space amenities along with improvements to the units.

North Johnson County

• Jones Development Co. led a group of investors that purchased a total of 588 units at Kenilworth Apartments, Corinth Place, Corinth Paddock, Corinth Gardens, and Corith Mission Valley. The price has not yet been disclosed and upgrades and rebranding are planned for the near future, but the group now owns 73% of all the apartments in Prairie Village.

South Johnson County

• After suffering a construction fire earlier this year, work is continuing on the mixed-use development at CityPlace. The fire has not caused any significant setbacks and residents are continuing to move into the 205-unit Royale View.

East & Southeast Jackson County

• The Manor Homes of Arborwalk were part of a national portfolio purchase by Starwood Capital. The 280-unit Lee’s Summit property was valued at $42.8 million.

RENTS & VACANCY BY SUBMARKET

UNDER CONSTRUCTION BY SUBMARKET

Source: AXIOMetrics, Cushman & Wakefield ResearchNote: Submarkets are defined by Cushman & Wakefield Research

$804

$977

$832

$1,125

$1,490

$959

$909

$865

$956

$803

$830

$963

$709

$1,107

$1,237

$877

$695

Wyandotte County

Western 435

South Kansas City

South Johnson County

Plaza

Olathe

North Kansas City

North Johnson County

Midtown

Independence

I-35 Northland

I-29 Northland

Eastern 435

East & SE Jackson County

Downtown

College Boulevard

Brookside & Waldo

7.8%

4.6%

5.8%

5.2%

8.5%

3.6%

5.3%

3.8%

4.0%

5.4%

6.0%

8.0%

6.5%

2.5%

6.6%

4.6%

7.9%

Wyandotte County

Western 435

South Kansas City

South Johnson County

Plaza

Olathe

North Kansas City

North Johnson County

Midtown

Independence

I-35 Northland

I-29 Northland

Eastern 435

East & SE Jackson County

Downtown

College Boulevard

Brookside & Waldo

1,026

3,704

646

315 292 337

1,168

547

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Overland ParkNorth

Downtown East & SEJacksonCounty

I-29 NorthlandI-35 Northland Plaza & SouthKC

Western 435 Plaza

MINNEAPOLIS

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

MARKET INSIGHTMINNEAPOLIS MULTIFAMILY REPORT | THIRD QUARTER 2017

CUSHMAN & WAKEFIELD MINNEAPOLIS MULTIFAMILY RESEARCH

The Cushman & Wakefield Multifamily Research Team provides in-depth coverage of the Minneapolis Metropolitan Statistical Area. In addition to analyzing multifamily rent and sale trends, these reports examine employment data, key economic announcements, and development pipeline news.

MARKET TEAM

IN THIS EDITION

ROBERT DULINSENIOR ASSOCIATE, CAPITAL [email protected]

LANCE STEIGERSENIOR DIRECTOR, CAPITAL [email protected]

SouthwestSouthwest

NorthwestNorthwest

SoutheastSoutheast

NortheastNortheast

SouthSouthCentralCentral

NorthNorthCentralCentral

MinneapolisMinneapolis

MinneapolisMinneapolisCBDCBD Saint PaulSaint Paul

Saint PaulSaint PaulCBDCBD

!"b$

!"b$

%&h(

%&h(

%&f(

%&f(

%&f(

%&f(

%&e(

!"b$ !"b$!"b$

%&d(

%&d(

%&d(

%&d(

%&c(

%&c(

%&c(

%&c(

)y

)y

)y

)y

!"�$

)n

)z

?�A@

?�A@

?�A@

)m

?�A@

?�A@

?�A@

?�A@

?�A@

?ØA@

?�A@

)p

)s

)p

)s

?'A@

?�A@

)s?�A@

?�A@

!"b$

S�

► Minneapolis

► Minneapolis - DT

► St. Paul

► St. Paul - DT

► North Central

► South Central

► Northwest Metro

► Southwest Metro

► Northeast Metro

► Southeast Metro

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

1MINNEAPOLISMARKET INSIGHTThird Quarter 2017

The following are select announcements from third quarter 2017:

• Minneapolis is in an economic expansion phase with job growth rates projected at 1.1% to 1.6% annually through 2019.

• Fortune 500 companies are expected to continue to fuel in-migration, attracting candidates from other markets such as Chicago, St. Cloud, and Duluth due to the metro’s tight labor market.

• In addition to healthcare and technology, the logistics sector is projected to drive future growth with Amazon’s growing presence.

Average Q3 employment increased by 39,450 jobs.

Average Q3 unemployment decreased to 3.5%.

+2.0 -10% Y O Y B P S Y O Y

ECONOMIC EXPANSION

OUTLOOKJOB GROWTH & UNEMPLOYMENT RATE

St. Paul City Council approved the master plan and zoning layout for the 135-acre former Ford Assembly Plant. The redevelopment is expected to provide 1,500 jobs.

Minnesota United FC, a North America Soccer League team, broke ground on the 20,000 seat Allianz field at I-94 and Snelling Avenue in St. Paul. The stadium is the beginning of a 34.5 acre urban village redevelopment that includes retail, residential and open space.

Emerson Automated Solutions recently completed a $10 million renovation in Shakopee, adding 100 jobs. They also announced a $14 million conversion project in Chanhassen, adding another 80 jobs.

Calyxt broke ground on a new 40,000 square foot headquarters in Roseville and expect to add 100 jobs.

The Minneapolis MSA added more than 39,450 net jobs year-over-year per BLS’ third quarter 2017 average. . The Education & Health Services sector led job growth with a 4.4% increase from September 2016 to September 2017. The unemployment rate in Minneapolis continues to trend well below the U.S. rate due to the market’s highly educated workforce and the presence of corporate headquarters such as UnitedHealth Group, Target, Best Buy, and 3M.

EMPLOYMENT & UNEMPLOYMENT TRENDS

MINNEAPOLIS JOB GROWTH TRENDS

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1.90

1.92

1.94

1.96

1.98

2.00

2.02

Q4 Q1 Q2 Q3

2015-2016 2016-2017 YOY % Job Growth

MINNEAPOLIS, MN

Q3 2015 Q3 2016 Q3 2017 FORECAST

NATIONAL UNEMPLOYMENT 5.1% 4.9% 4.4%

EMPLOYMENT (% Change) 1.6% 2.0% 2.0%

UNEMPLOYMENT RATE (%) 3.5% 3.6% 3.5%

Forecast is 12-month outlook

EMPLOYMENT IN MILLIONS & JOB GROWTH (%)

Source: Moody’s Analytics

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

3MINNEAPOLISMARKET INSIGHTThird Quarter 2017

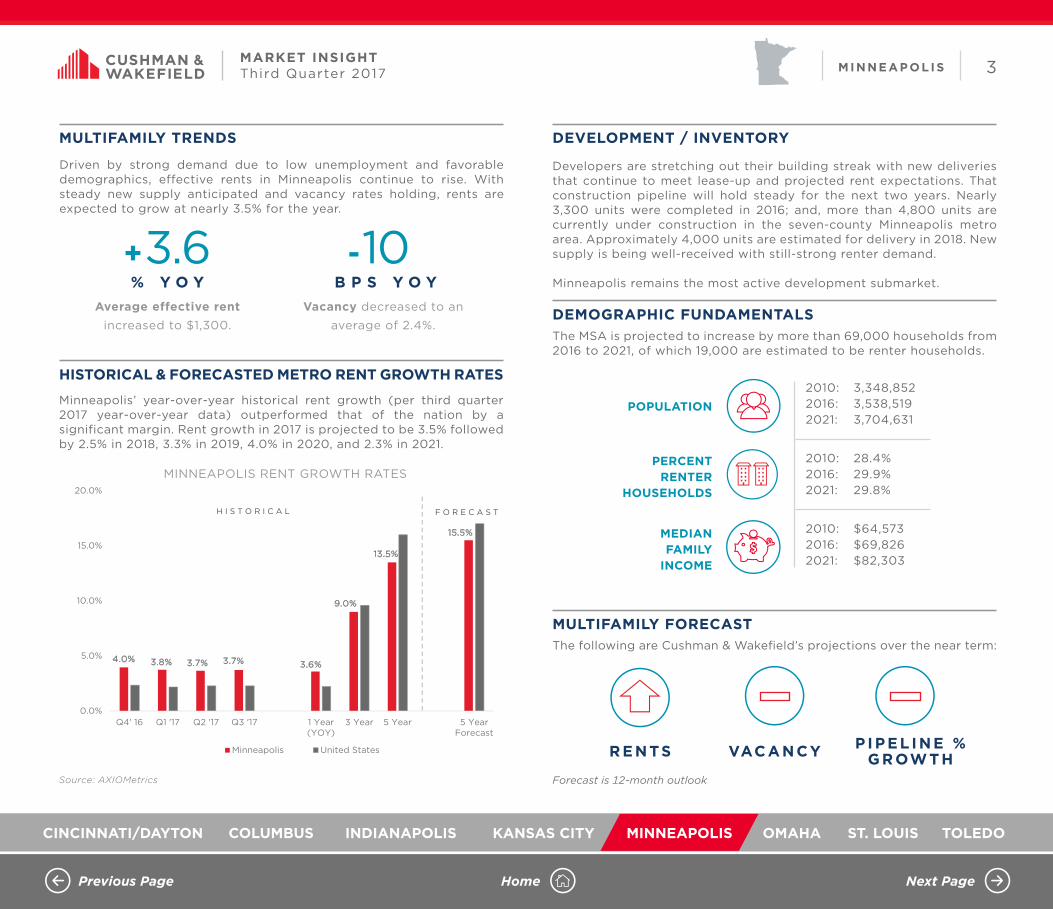

Driven by strong demand due to low unemployment and favorable demographics, effective rents in Minneapolis continue to rise. With steady new supply anticipated and vacancy rates holding, rents are expected to grow at nearly 3.5% for the year.

Minneapolis’ year-over-year historical rent growth (per third quarter 2017 year-over-year data) outperformed that of the nation by a significant margin. Rent growth in 2017 is projected to be 3.5% followed by 2.5% in 2018, 3.3% in 2019, 4.0% in 2020, and 2.3% in 2021.

Developers are stretching out their building streak with new deliveries that continue to meet lease-up and projected rent expectations. That construction pipeline will hold steady for the next two years. Nearly 3,300 units were completed in 2016; and, more than 4,800 units are currently under construction in the seven-county Minneapolis metro area. Approximately 4,000 units are estimated for delivery in 2018. New supply is being well-received with still-strong renter demand.

Minneapolis remains the most active development submarket.

The MSA is projected to increase by more than 69,000 households from 2016 to 2021, of which 19,000 are estimated to be renter households.

The following are Cushman & Wakefi eld’s projections over the near term:

MULTIFAMILY TRENDS

HISTORICAL & FORECASTED METRO RENT GROWTH RATES

DEVELOPMENT / INVENTORY

DEMOGRAPHIC FUNDAMENTALSAverage effective rentincreased to $1,300.

Vacancy decreased to an

average of 2.4%.

4.0% 3.8% 3.7% 3.7% 3.6%

9.0%

13.5%

15.5%

0.0%

5.0%

10.0%

15.0%

20.0%

Q4' 16 Q1 '17 Q2 '17 Q3 '17 1 Year(YOY)

3 Year 5 Year 5 YearForecast

Minneapolis United States

H I S T O R I C A L F O R E C A S T

MINNEAPOLIS RENT GROWTH RATES

+3.6 -10% Y O Y B P S Y O Y

2010: 3,348,8522016: 3,538,5192021: 3,704,631

2010: 28.4%2016: 29.9%2021: 29.8%

2010: $64,5732016: $69,8262021: $82,303

POPULATION

PERCENTRENTER

HOUSEHOLDS

MEDIANFAMILY

INCOME

MULTIFAMILY FORECAST

VAC ANCYRENTS PI PEL I NE % G ROW T H

Source: AXIOMetrics Forecast is 12-month outlook

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

4MINNEAPOLISMARKET INSIGHTThird Quarter 2017

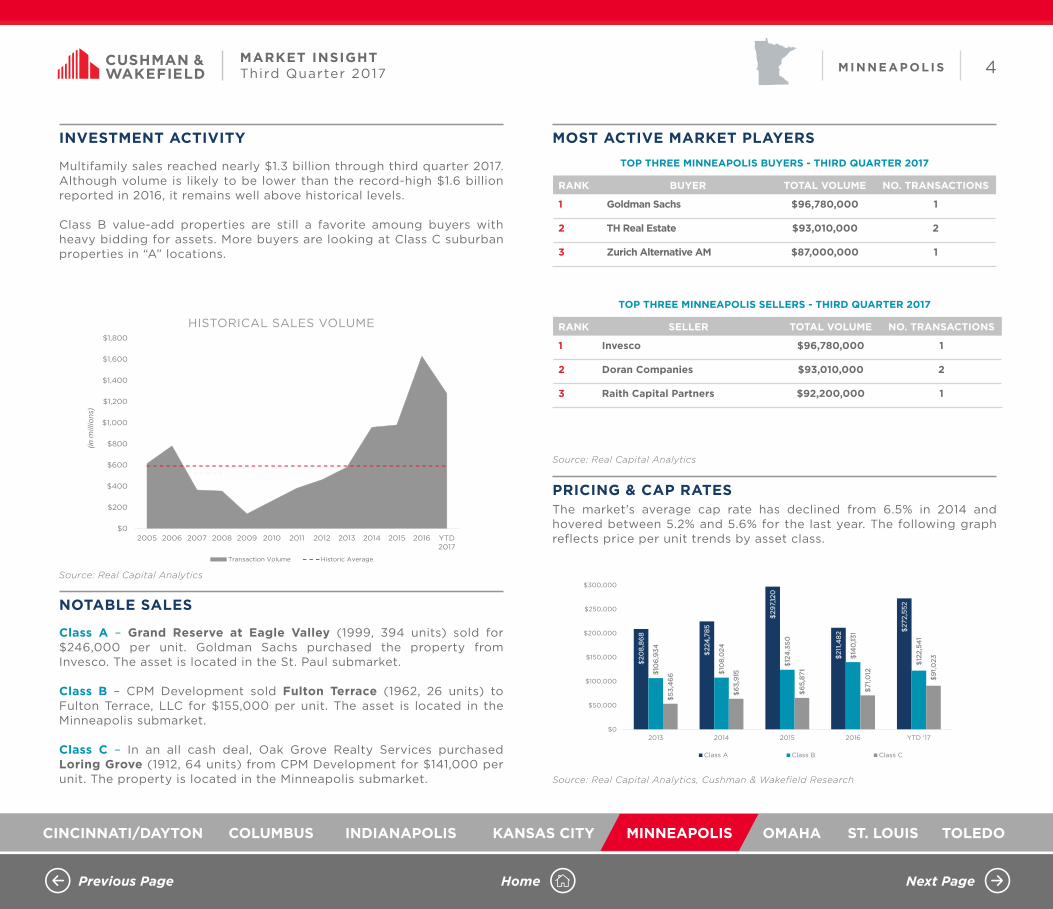

Multifamily sales reached nearly $1.3 billion through third quarter 2017. Although volume is likely to be lower than the record-high $1.6 billion reported in 2016, it remains well above historical levels.

Class B value-add properties are still a favorite amoung buyers with heavy bidding for assets. More buyers are looking at Class C suburban properties in “A” locations.

Class A – Grand Reserve at Eagle Valley (1999, 394 units) sold for $246,000 per unit. Goldman Sachs purchased the property from Invesco. The asset is located in the St. Paul submarket.

Class B – CPM Development sold Fulton Terrace (1962, 26 units) to Fulton Terrace, LLC for $155,000 per unit. The asset is located in the Minneapolis submarket.

Class C – In an all cash deal, Oak Grove Realty Services purchased Loring Grove (1912, 64 units) from CPM Development for $141,000 per unit. The property is located in the Minneapolis submarket.

The market’s average cap rate has declined from 6.5% in 2014 and hovered between 5.2% and 5.6% for the last year. The following graph reflects price per unit trends by asset class.

INVESTMENT ACTIVITY

NOTABLE SALES

MOST ACTIVE MARKET PLAYERS

PRICING & CAP RATES

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 YTD2017

Transaction Volume Historic Average

(inm

illio

ns)

$2

08

,86

8

$22

4,7

85

$29

7,12

0

$21

1,4

82

$27

2,5

52

$10

6,9

34

$10

8,0

24

$12

4,3

50

$14

0,13

1

$12

2,5

41

$5

3,4

66

$6

3,9

15

$6

5,8

71

$7

1,0

12

$9

1,0

23

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

2013 2014 2015 2016 YTD '17

Class A Class B Class C

TOP THREE MINNEAPOLIS BUYERS - THIRD QUARTER 2017

Source: Real Capital Analytics

TOP THREE MINNEAPOLIS SELLERS - THIRD QUARTER 2017

HISTORICAL SALES VOLUME

RANK BUYER TOTAL VOLUME NO. TRANSACTIONS

1 Goldman Sachs $96,780,000 1

2 TH Real Estate $93,010,000 2

3 Zurich Alternative AM $87,000,000 1

RANK SELLER TOTAL VOLUME NO. TRANSACTIONS

1 Invesco $96,780,000 1

2 Doran Companies $93,010,000 2

3 Raith Capital Partners $92,200,000 1

Source: Real Capital Analytics, Cushman & Wakefield Research

Source: Real Capital Analytics

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

5MINNEAPOLISMARKET INSIGHTThird Quarter 2017

SUBMARKET OVERVIEW SELECT SUBMARKET NEWS

RENTS & VACANCY BY SUBMARKET

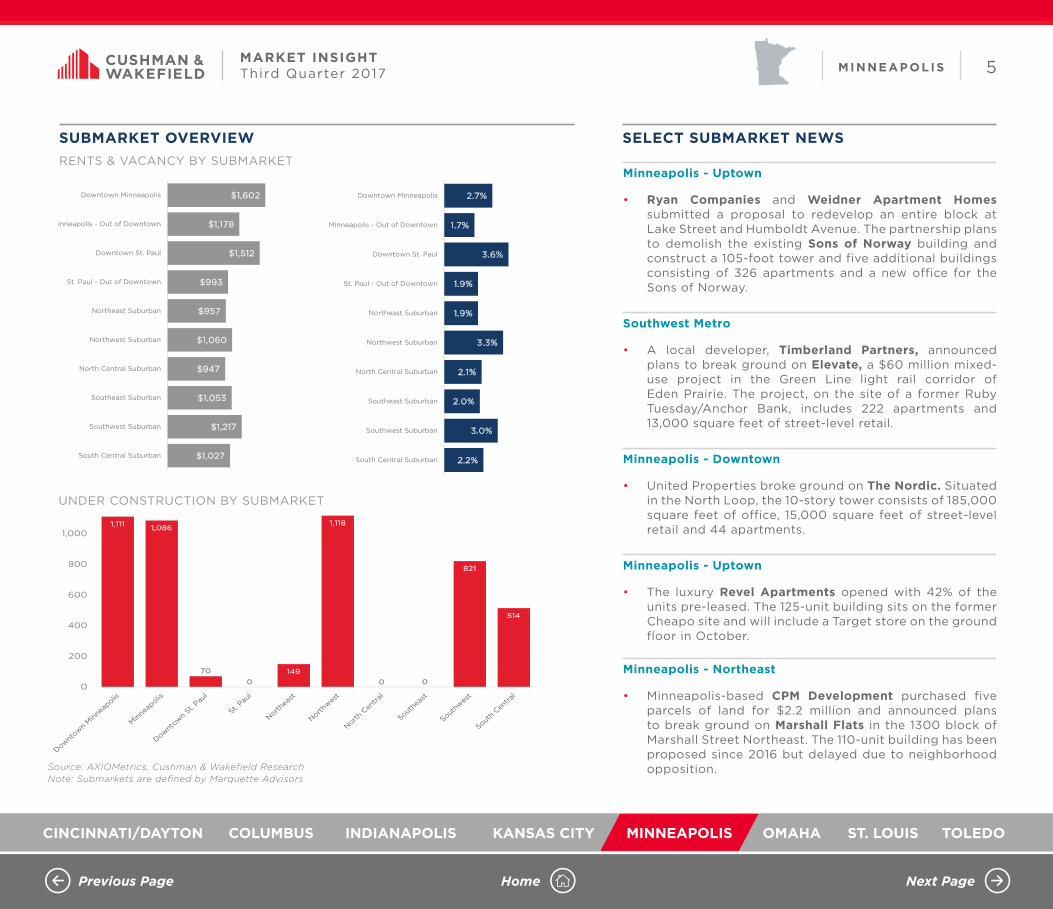

Minneapolis - Uptown

• Ryan Companies and Weidner Apartment Homes submitted a proposal to redevelop an entire block at Lake Street and Humboldt Avenue. The partnership plans to demolish the existing Sons of Norway building and construct a 105-foot tower and five additional buildings consisting of 326 apartments and a new office for the Sons of Norway.

Southwest Metro

• A local developer, Timberland Partners, announced plans to break ground on Elevate, a $60 million mixed-use project in the Green Line light rail corridor of Eden Prairie. The project, on the site of a former Ruby Tuesday/Anchor Bank, includes 222 apartments and 13,000 square feet of street-level retail.

Minneapolis - Downtown

• United Properties broke ground on The Nordic. Situated in the North Loop, the 10-story tower consists of 185,000 square feet of office, 15,000 square feet of street-level retail and 44 apartments.

Minneapolis - Uptown

• The luxury Revel Apartments opened with 42% of the units pre-leased. The 125-unit building sits on the former Cheapo site and will include a Target store on the ground floor in October.

Minneapolis - Northeast

• Minneapolis-based CPM Development purchased five parcels of land for $2.2 million and announced plans to break ground on Marshall Flats in the 1300 block of Marshall Street Northeast. The 110-unit building has been proposed since 2016 but delayed due to neighborhood opposition.

$1,027

$1,217

$1,053

$947

$1,060

$957

$993

$1,512

$1,178

$1,602

South Central Suburban

Southwest Suburban

Southeast Suburban

North Central Suburban

Northwest Suburban

Northeast Suburban

St. Paul - Out of Downtown

Downtown St. Paul

inneapolis - Out of Downtown

Downtown Minneapolis

2.2%

3.0%

2.0%

2.1%

3.3%

1.9%

1.9%

3.6%

1.7%

2.7%

South Central Suburban

Southwest Suburban

Southeast Suburban

North Central Suburban

Northwest Suburban

Northeast Suburban

St. Paul - Out of Downtown

Downtown St. Paul

Minneapolis - Out of Downtown

Downtown Minneapolis

RENTS & VACANCY BY SUBMARKET

1,111 1,086

70

0149

1,118

0 0

821

514

0

200

400

600

800

1,000

UNDER CONSTRUCTION BY SUBMARKET

Source: AXIOMetrics, Cushman & Wakefield ResearchNote: Submarkets are defined by Marquette Advisors

OMAHA METRO

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

1MARKET INSIGHTThird Quarter 2017 OMA HA MET RO

The following are metro area expansion announcements as of third quarter 2017:

Average Q3 employment increased by 8,800 jobs.

Average Q3 unemployment decreased to 2.9%.

ECONOMIC EXPANSION

JOB GROWTH & UNEMPLOYMENT RATE

Work began on the initial stages of a $1.2 billion Boys Town development that will eventually feature 2.3 million square feet of commercial space, 2,000 residences, and a food, dining and retail area. The property includes land formerly occupied by a Boys Town farm near 144th Street and West Dodge. As planned, the nearly 500 acres of undeveloped land west of historic Boys Town would showcase a food and dining plaza, a retail center and an entertainment hub for live bands and festivals. The $370 million Buffett Cancer Center opened in June 2017 as part of the Nebraska Medicine campus is adding 4,657 new jobs. The 615,000-square-foot facility is a joint venture between the University of Nebraska Medical Center and clinical partner Nebraska Medicine that will pull all cancer-related functions — research, outpatient and inpatient — together under one roof.

The $205 million Capital District is Omaha’s newest downtown entertainment district. The District surrounds a technology-smart, modern town square and will feature a 218-unit high rise apartment tower, a full-service 333-room Marriott hotel, Class A office space, plenty of adjacent parking and over 20 diverse restaurants and bars – all within walking distance of Omaha’s best civic, cultural and entertainment venues and the Riverfront.

a

a

a

Average effective rent growth year-over-year as of the third quarter slowed a bit to the 1.6% range. Vacancy increased by a nominal amount year-over-year and remained below 5.0% as of the third quarter. Rents are projected to increase by 13.3% from 2017 to 2022 per AXIOMetrics, with an average annual rate of 2.7%. This trend is in line with current rent growth trends in the market.

MULTIFAMILY TRENDS

Average effective rentincreased to $884.

Vacancy decreased to an

average of 4.0%.

+1.6 +.68% Y O Y B P S Y O Y

The Omaha–Council Bluffs Metro added approximately 8,800 new jobs from third quarter 2016 to third quarter 2017. The major job producers as of September 2017 are Professional & Business Services and Education & Health Services. Omaha’s unemployment rate is very low at 2.9% - 150 basis points below that of the nation - indicating that the metro is experiencing a tight labor market.

EMPLOYMENT & UNEMPLOYMENT TRENDS

OMAHA JOB GROWTH TRENDS

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

400

420

440

460

480

500

520

540

Q4 Q1 Q2 Q3

OMAHA/COUNCIL BLUFFS JOB GROWTH TRENDSEMPLOYMENT IN THOUSANDS

2015-2016 2016-2017 YOY % Job Growth

+1.8 -50% Y O Y B P S Y O Y

OMAHA - COUNCIL BLUFFS

Source: U.S. Bureau of Labor Statistics (BLS)

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

2MARKET INSIGHTThird Quarter 2017 OMA HA MET RO

The Omaha Market has continued to heat up through the third quarter. Transaction volume on a unit basis is up substantially over 2016, with a 2017 year-to-date total of 2,120 units compared to just over 1,200 units in 2016. A total of 882 units traded in the third quarter alone. The pipeline of product under contract, on the market, and coming to the market has the Omaha MSA tracking toward a 3,000-unit year. Cap rates have remained low despite the increased supply, hovering between 6.0% and 7.0% depending upon the class, condition, and age of the asset. Notably, Willow Creek (1998, 156 units) had the low trailing cap of the third quarter at 6.38%, and Fox Ridge (1988, 120 units) had the high trailing cap of the third quarter at 7.42%.

There are six notable properties under construction or in lease up competing for tenants in the downtown market, totaling more than 1,000 total new units: Capital District (218 units), The Breakers (214 units), Zag Apartments (193 units), The Conrad (153 units), The Triangle (134 units), The Yard (101 units). Suburban Omaha has fewer but larger projects, with 752 units under construction in two projects. Andover Pointe is finishing up Phase II, adding 390 units to the southwest Omaha market near 132nd and Chandler. The Lumberyard in Millard is finishing up its 346 units, completing the mixed-use redevelopment project.

INVESTMENT ACTIVITY & CAP RATES

DEVELOPMENT / INVENTORY NOTABLE SALES

REGIONAL SALES VOLUME / CAP RATES

The following are Cushman & Wakefield’s projections for the near term.

DEMOGRAPHIC FUNDAMENTALS

2000: 767,0522010: 865,3542017: 917,5172022: 960,358

2010: 33.2%2016: 33.9%2021: 33.4%

2000: $44,6742010: $55,4072016: $56,9592021: $68,079

POPULATION

RENTER OCCUPIED

PERCENTAGE

MEDIAN HOUSEHOLD

INCOME

MULTIFAMILY FORECAST

VACANCYREN TS P IP EL INE % G ROWTH

Forecast is 12-month outlook

PricePerUnit(avg.)CapRate(avg.)2010 $47,312 6.46% The Region is experiencing a cultural shift , where people are moving to revitalized downtown areas that offer live/work/play environments not typically seen in smaller Midwest metros.2011 $53,135 8.96% Market Velocity is up and transaction volume in units sold for 2017 YTD (2,120) has surpassed 2016 (1,200), with an additional 1,271+ units under contract and set to close in Q4 20172012 $53,814 7.18% Absorption remains steady, but concessions are up in the downtown areas due the amount of new product delivered and under construction, suburban rents remain steady and strong2013 $49,643 7.63%2014 $57,596 7.40%2015 $65,068 7.99%2016 $80,377 7.03%

2017 YTD $72,376 6.63%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

2010 2011 2012 2013 2014 2015 2016 2017 YTD

Regional Sale Price Per Unit / Cap Rate

Price Per Unit (avg.) Cap Rate (avg.)

The Region is experiencing a cultural shift , where people are moving to revitalized downtown areas that offer live/work/play environments not typically seen in smaller Midwest metros.Market Velocity is up and transaction volume in units sold for 2017 YTD (2,120) has surpassed 2016 (1,200), with an additional 1,271+ units under contract and set to close in Q4 2017Absorption remains steady, but concessions are up in the downtown areas due the amount of new product delivered and under construction, suburban rents remain steady and strong

PROPERTY YEAR BUILT

BUYER SELLER # OF UNITS

PURCHASE PRICE

PRICE PER UNIT

Maple View 1991 Briar Capital Maxx 108 $6,270,000 $58,056

Fox Valley 1997 Briar Capital Maxx 228 $14,980,000 $65,702

Willow Creek 1998 Briar Capital Maxx 156 $8,420,000 $53,974

Edgewater Court 1975 Briar Capital Maxx 108 $6,270,000 $58,056

Fox Ridge 1988 Briar Capital Maxx 120 $6,175,000 $51,458

Howard Street 1986 Briar Capital Maxx 90 $4,659,000 $51,767

Briar Hills 1999 JB Group NewStreet 72 $6,550,000 $90,972

Median household income rose by 24.0% from 2000 to 2010. It is projected to increase by another 19.5% from 2016 to 2021, thereby fueling future rent growth in the market.

Source: CoStar

Source: Site To Do Business

ST. LOUIS

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

MARKET INSIGHTST. LOUIS MULTIFAMILY REPORT | THIRD QUARTER 2017

CUSHMAN & WAKEFIELD ST. LOUIS MULTIFAMILY RESEARCH

The Cushman & Wakefield Multifamily Research Team provides in-depth coverage of the St. Louis Metropolitan Statistical Area. In addition to analyzing multifamily rent and sale trends, these reports examine employment data, key economic announcements, and development pipeline news.

MARKET TEAM

IN THIS EDITION

NORTH COUNTY

67

67

67

67

61

61

61

94

94

94

94

94

47

47

47

100

100

50

94

141

141

141

141

364

364

141

ST. CHARLES COUNTY

JEFFERSON COUNTY

CHESTERFIELD

MARYLAND HEIGHTS / CREVE COEUR

BALLWIN

KIRKWOODSOUTH

SOUTH ST. LOUIS CITY

RICHMOND HEIGHTS

CLAYTONCBD

CENTRAL WEST END DOWNTOWNCBD

NORTHST. LOUIS CITY

UNIVERSITY CITY

OLIVETTE

METROEAST

170

270

270

70

70

70

270

64

64

70

270

70

44

44

44

44

64

44

44

270270

55

70 55

64

64

255

255

255

255

255

170

70

370

370

21

55

55

55

64

64

64

70

70

Downton Clayton

Downtown CBD

St. Louis City

Mid County

West County

St. Charles County

North County

South County

Metro East

BOBBY MILLSASSOCIATE, CAPITAL [email protected]

PAUL HILTONEXECUTIVE DIRECTOR, CAPITAL [email protected]

MICHAEL HANRAHANEXECUTIVE DIRECTOR, CAPITAL [email protected]

BRENDAN DUNBARST. LOUIS RESEARCH [email protected]

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

2MARKET INSIGHTThird Quarter 2017 ST. LOUI S

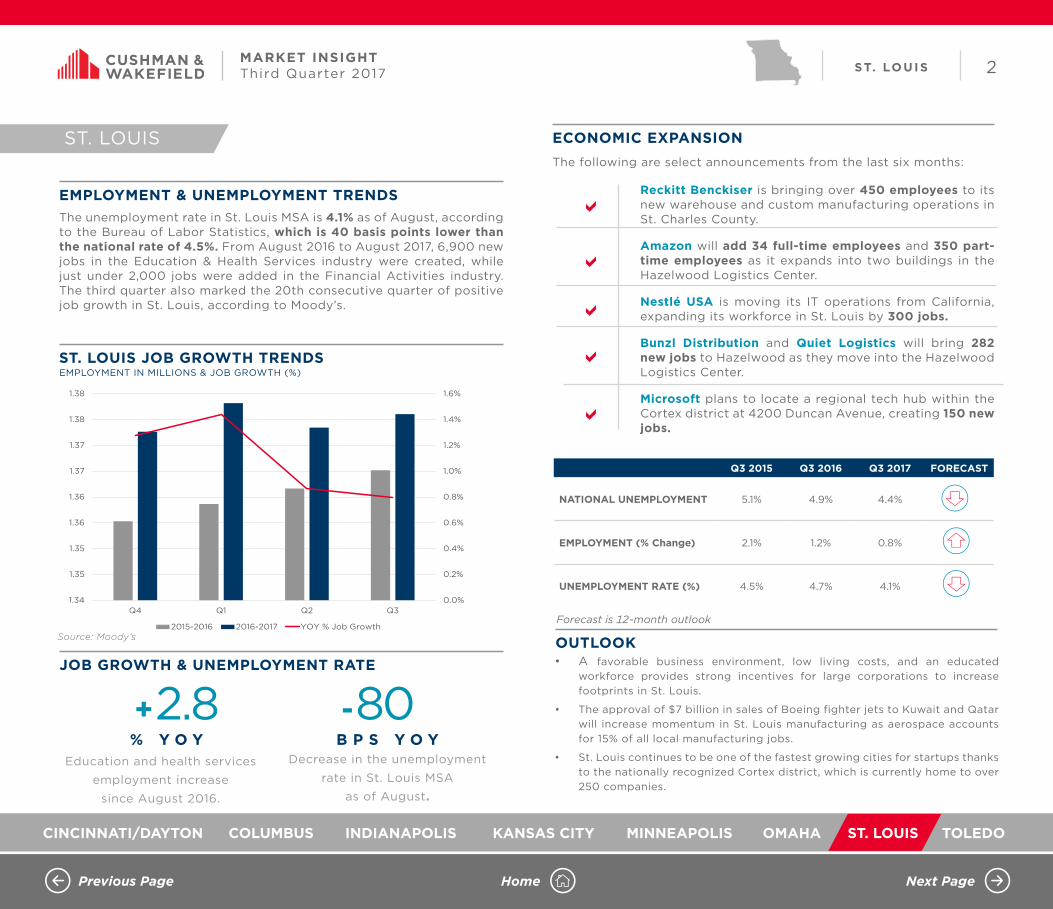

The following are select announcements from the last six months:

• A favorable business environment, low living costs, and an educated workforce provides strong incentives for large corporations to increase footprints in St. Louis.

• The approval of $7 billion in sales of Boeing fighter jets to Kuwait and Qatar will increase momentum in St. Louis manufacturing as aerospace accounts for 15% of all local manufacturing jobs.

• St. Louis continues to be one of the fastest growing cities for startups thanks to the nationally recognized Cortex district, which is currently home to over 250 companies.

Education and health services

employment increase

since August 2016.

Decrease in the unemployment

rate in St. Louis MSA

as of August.

+2.8 -80% Y O Y B P S Y O Y

ECONOMIC EXPANSION

OUTLOOKJOB GROWTH & UNEMPLOYMENT RATE

Reckitt Benckiser is bringing over 450 employees to its new warehouse and custom manufacturing operations in St. Charles County.

Amazon will add 34 full-time employees and 350 part-time employees as it expands into two buildings in the Hazelwood Logistics Center.

Nestlé USA is moving its IT operations from California, expanding its workforce in St. Louis by 300 jobs.

Bunzl Distribution and Quiet Logistics will bring 282 new jobs to Hazelwood as they move into the Hazelwood Logistics Center.

Microsoft plans to locate a regional tech hub within the Cortex district at 4200 Duncan Avenue, creating 150 new jobs.

a

a

a

a

The unemployment rate in St. Louis MSA is 4.1% as of August, according to the Bureau of Labor Statistics, which is 40 basis points lower than the national rate of 4.5%. From August 2016 to August 2017, 6,900 new jobs in the Education & Health Services industry were created, while just under 2,000 jobs were added in the Financial Activities industry. The third quarter also marked the 20th consecutive quarter of positive job growth in St. Louis, according to Moody’s.

EMPLOYMENT & UNEMPLOYMENT TRENDS

ST. LOUIS JOB GROWTH TRENDS

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.34

1.35

1.35

1.36

1.36

1.37

1.37

1.38

1.38

Q4 Q1 Q2 Q3

ST. LOUIS JOB GROWTH TRENDS EMPLOYMENT IN MILLIONS

2015-2016 2016-2017 YOY % Job Growth

ST. LOUIS

Q3 2015 Q3 2016 Q3 2017 FORECAST

NATIONAL UNEMPLOYMENT 5.1% 4.9% 4.4%

EMPLOYMENT (% Change) 2.1% 1.2% 0.8%

UNEMPLOYMENT RATE (%) 4.5% 4.7% 4.1%

a

Forecast is 12-month outlook

EMPLOYMENT IN MILLIONS & JOB GROWTH (%)

Source: Moody’s

Previous Page Home Next Page

CINCINNATI/DAYTON COLUMBUS INDIANAPOLIS KANSAS CITY MINNEAPOLIS OMAHA ST. LOUIS TOLEDO

3MARKET INSIGHTThird Quarter 2017 ST. LOUI S

Effective rents in the third quarter reached $959, a 7.0% increase over the last two years. The third quarter marks the 30th consecutive quarter of positive effective rent growth according to AXIOMetrics.

The St. Louis market experienced strong rent growth over the last three years with an average annual increase in rates of 2.6%. Over the next five years, rates are expected to grow around 2.7% annually on average. This is slightly higher than average annual growth over the previous five years of 2.6%.

More than 3,700 units are under construction in the St. Louis Area, led by the Central West End with over 1,300 units under construction. Other strong submarkets include Downtown Clayton and Chesterfield, with 349 and 345 units under construction, respectively. Close to 2,000 deliveries are expected by the end of the year, according to CoStar. While new construction, such as the development at 32 N. Euclid Ave, dominates the Central West End, the redevelopment of aging office buildings in Downtown St. Louis has increased considerably in the past few years. This redevelopment activity is heavily reliant on favorable tax incentives offered by the city.

The St. Louis Area continues to be an attractive market for residents as it ranks as the 37th most afforable single family market out of 211 markets.

The following are Cushman & Wakefield’s projections over the near term.

MULTIFAMILY TRENDS

HISTORICAL & FORECASTED METRO RENT GROWTH RATES

DEVELOPMENT / INVENTORY

DEMOGRAPHIC FUNDAMENTALSEffective rate growth from 3Q

2015 to 3Q 2017.

Vacancy decreased since the

beginning of 2016.

1.9% 1.9%

1.1% 1.1% 1.5%

2.6% 2.6% 2.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Q4 '16 Q1 '17 Q2 '17 Q3 '17 1 Year 3 Year(Avg Annual Change)

5 Year 5 YearForecast

(Avg Annual Change)

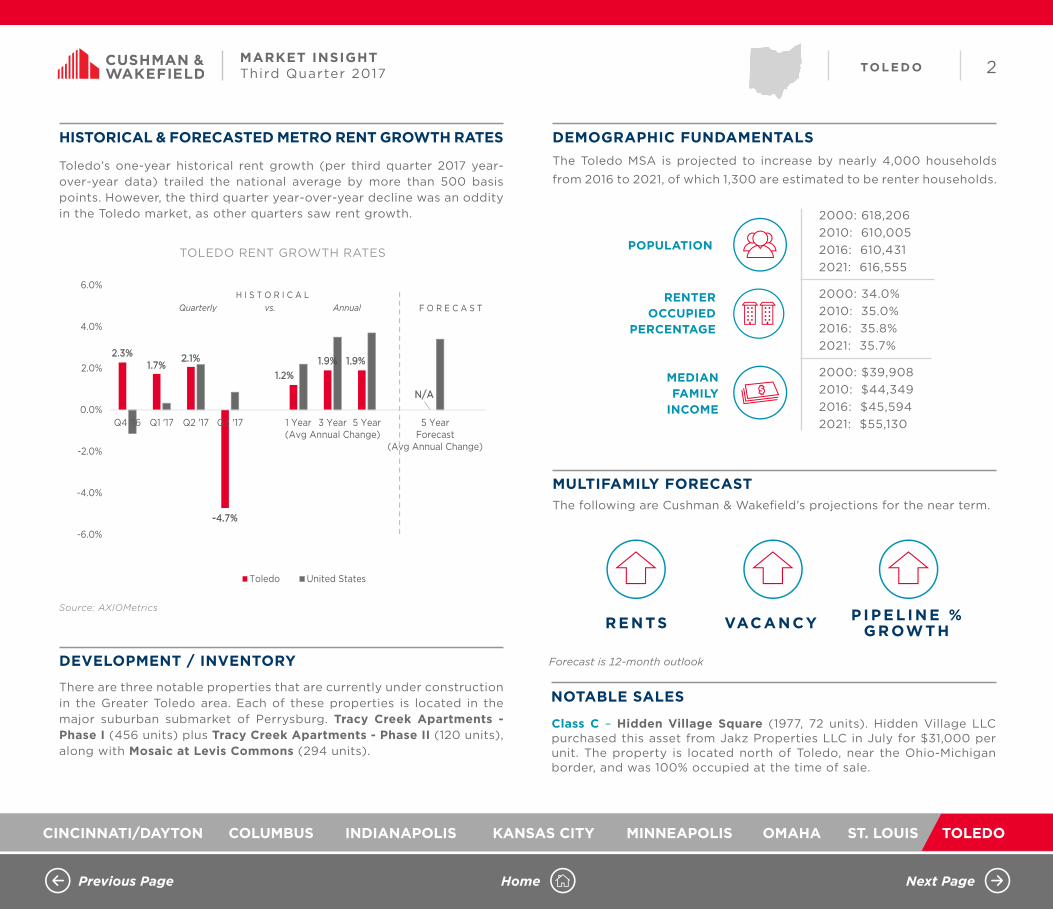

ST. LOUIS RENT GROWTH RATES HISTORICAL AND FORECAST