Embed Size (px)

Citation preview

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 1/13

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539 1

Market OutlookIndia Research

November 11, 2011

Dealer’s Diary

Indian markets are expected to open sideways tracking mixed cues from the

markets worldwide. While the shift in epicenter of euro zone crisis from Greece toItaly have raised fresh concerns for investors and led to sharp fall in indices

worldwide on Wednesday, news of a successful bond auction in Italy pulling the

yield on Italy's ten-year bond back below 7% and election of former European

Central Bank Vice President Lucas Papademos as Greece's new prime minister

helped the markets relax and close mostly higher on Thursday.

The rebound in US stocks was also aided by better than expected economic data

from the US on Thursday. The jobless claims fell unexpectedly to 390,000 from

the previous week's revised figure of 400,000, while a separate report showed

that the U.S. trade deficit unexpectedly narrowed in September, as the value of

exports increased at a much faster rate than the value of imports.

Meanwhile, Indian investors will keenly watch out for the IIP and the weekly

inflation figures due today, which are expected to give more clarity to the

domestic markets in the coming days.

Markets Today The trend deciding level for the day is 17,451/5,250 levels. If NIFTY trades

above this level during the first half-an-hour of trade then we may witness a

further rally up to 17,570 – 17,778/5,288 – 5,356 levels. However, if NIFTY

trades below 17,451/ 5,250 levels for the first half-an-hour of trade then it may

correct up to 17,243– 17,123/5,183 – 5,144 levels.

Indices S2 S1 R1 R2

SENSEX 17,123 17,243 17,570 17,778

NIFTY 5,144 5,183 5,288 5,356

News Analysis

TCS bags US$2.2bn order

2QFY2012 Result Reviews – SBI, Tata Steel, DLF, Hindalco, Ranbaxy, Lupin, Mahindra Satyam, Bharat Forge, IRB, ITNL, CESC, Apollo Tyres, Godawari

Power, Ceat

2QFY2012 Result Previews – Coal India, NALCO, MOIL, Britannia, DISHRefer detailed news analysis on the following page

Net Inflows (November 08, 2011)

` cr Purch Sales Net MTD YTD

FII 2,269 2,053 216 521 1,037

MFs 589 439 151 (291) 4,844

FII Derivatives (November 09, 2011)

` cr Purch Sales Net Open Interest

Index Futures 2,085 1,550 535 14,497

Stock Futures 1,596 1,871 (275) 28,868

Gainers / Losers

Gainers Losers

Company Price (`) chg (%) Company Price (`) chg (%)

United Spirits 914 4.9 SBI 1,863 (6.8)

Ashok Leyland 28 3.5 Indiabulls Fin 143 (5.9)

Hindustan Unilever 391 2.9 BPCL 570 (5.5)

Manappuram Fin. 64 2.2 Voltas 102(5.2)

Wipro 377 2.1 HPCL 316 (4.9)

Domestic Indices Chg (%) (Pts) (Close)

BSE Sensex (1.2) (207.4) 17,362

Nifty (1.3) (68.3) 5,221MID CAP (1.3) (78.8) 6,233

SMALL CAP (1.1) (73.5) 6,873

BSE HC (1.7) (102.9) 6,036

BSE PSU (2.1) (157.1) 7,433

BANKEX (2.6) (297.0) 11,021

AUTO (1.7) (158.9) 9,082

METAL (2.5) (295.6) 11,539

OIL & GAS (2.3) (203.1) 8,841

BSE IT 0.4 24.0 5,793

Global Indices Chg (%) (Pts) (Close)

Dow Jones 1.0 112.9 11,894

NASDAQ 0.1 3.5 2,625

FTSE (0.3) (15.6) 5,445

Nikkei (2.9) (254.6) 8,501

Hang Seng (5.2) (1,051) 18,964

Straits Times (2.5) (71.8) 2,787

Shanghai Com (1.8) (45.4) 2,480

Indian ADRs Chg (%) (Pts) (Close)

Infosys (0.0) (0.0) $56.0

Wipro 0.7 0.1 $9.7

ICICI Bank 0.2 0.1 $33.3

HDFC Bank (1.3) (0.4) $29.1

Advances / Declines BSE NSE

Advances 991

Declines 1,879 1,124

Unchanged 104 48

Volumes (` cr)

BSE 2,576

NSE 11,024

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 2/13

Market Outlook | India Research

November 11, 2011 2

TCS bags US$2.2bn order

Diligenta, the business process outsourcing (BPO) provider in the UK and a

subsidiary of TCS, announced that it will assume administration responsibility for

3.2mn policies for Friends Life, a provider of pensions, investments and insurance.

The agreement, effective from March 1, 2012, is worth US$2.2bn (£1.37bn) over

15 years. This major business win will increase the total number of policies

administered by Diligenta to just under 8mn. Outsourcing much of its customer

service and IT functions for its UK heritage business will allow Friends Life to focus

on its new proposition developments, including its new corporate platform, in its

core markets of corporate benefits, protection and retirement income.

Diligenta will assume administration responsibility for much of Friends Life’s closed

book protection business and a significant part of its corporate benefits business.

Diligenta and TCS will deliver IT infrastructure and IT services with some policies

migrating to TCS BaNCS Insurance, a globally recognized industry-leading

insurance platform. As a result of this new arrangement, a total of approximately

1,900 Friends Life roles across a number of office locations in the UK will transfer

under their existing terms of employment to Diligenta. All those who will transfer

would continue to service Friends Life’s customers, ensuring both continuity of

service delivery and expertise. This is the second biggest order ever signed by TCS.

We continue to maintain our Accumulate recommendation on the stock with a

target price of `1,220.

Result Reviews

State Bank of India

For 2QFY2012, SBI’s standalone net profit increased by 12.4% yoy to ` 2,810cr,

in-line with our estimates. A strong sequential expansion in both domestic and

foreign NIM was the major positive from the result. However, fresh slippages of

` 8,000cr and lower recoveries and upgrades during the quarter led to gross NPAs

shooting up by 22.2% qoq. Gross NPA ratio as of 2QFY2012 stood at 4.2% and

net NPA ratio stood at 2.0%. Provisioning coverage ratio declined considerably by

375bp to 63.5%. The bank made counter-cyclical provisions of ` 550cr in2QFY2012 ( ` 1,100 for 1HFY2012) to meet the stipulated 70% provision coverage

to gross NPA ratio as of September 30, 2010. Non-interest income declined by

14.4% yoy on account of lower treasury gains and dividend income (no interim

dividend received from subsidiaries). Fee income also came in lower by 11.7% yoy

mainly on account of bulk upfront fees received from some large corporate deals

last year and lower cross-sell income.

The stock is trading at 1.2x FY2013E ABV (adjusting for value of subsidiaries).

We recommend a Buy rating on the stock with a target price of `2,194.

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 3/13

Market Outlook | India Research

November 11, 2011 3

Tata Steel

Tata Steel reported disappointing profitability for 2QFY2012. Consolidated net

sales increased by 14.5% yoy to ` 32,798cr (above our estimate of ` 30,936cr)

mainly on account of increased average realizations. Tata Steel India’s net sales

increased by 15.7% yoy to ` 81,42cr. Tata Steel India operations sales volumes

decreased by 0.7% yoy to 1.65mn tonnes, while Tata Steel Europe (TSE) operations

sales volumes decreased by 1.7% yoy to 3.48mn tonnes in 2QFY2012. Tata Steel

India’s average realization/tonne increased by 18.6% yoy to ` 46,402, while TSE’s

average realization/tonne decreased by 1.0% yoy to US$1,148 on account of

subdued demand in Europe. EBITDA/tonne decreased by 19.1% and 47.0% yoy to

US$365 and US$30 in Tata Steel India and TSE operations, respectively, as

increased realization (at India operations) was more than offset by higher raw-

material costs. Consolidated EBITDA decreased by 25.1% yoy to ` 2,750cr. Other

income decreased to ` 120cr compared to ` 814cr in 2QFY2011. The company reported exceptional forex loss of ` 150cr in 2QFY2012. Adjusting for exceptional

items, adjusted net profit decreased by 81.4% yoy to ` 362cr, significantly below

our estimate of ` 1,339cr. Consolidated reported net profit stood at ` 212cr

compared to ` 1,979cr in 2QFY2011. Standalone net profit decreased by 27.6%

yoy to ` 1,495cr. Consolidated net debt stood at US$8.4bn as on September 30,

2011. We maintain our Buy rating on the stock; our target price is under review.

DLF

DLF announced its 2QFY2012 numbers. The company’s net sales increased by 6.9% yoy to ` 2,532cr ( ` 2,369cr), below our estimate of ` 2,674cr. EBITDA came in

at ` 1,173cr, up 26.3% yoy, on the back of strong margin expansion. OPM

expanded by 711bp yoy to 46.3%, which was above our estimate of 43.0%. PAT

declined by 11.0% yoy to ` 372cr, which was slightly below our estimate of ` 399cr.

The decline in PAT was largely due to higher tax rate during the quarter, which

increased to 28.6% of PBT in 2QFY2012 vs. 14.9% of PBT in 2QFY2011. We

continue to maintain our Neutral recommendation on the stock. We may revise

our estimates and target price post management’s concall.

Hindalco

Hindalco and Novelis reported their 2QFY2012 results separately. Hindalco’s

standalone net sales increased by 7.2% yoy to ` 6,220cr, driven by increased

realization. However, EBITDA decreased by 4.2% yoy to ` 669cr on account of

rising costs of power, driven by increased coal prices. Power costs grew by 31.1%

yoy to ` 753cr. Thus, EBITDA margin slipped by 128bp yoy to 10.8% in

2QFY2012. Other income grew by 114.5% yoy to ` 176cr. Tax rate stood at 16.8%

compared to 22.0% in 2QFY2011. Consequently, net profit increased by 15.8%

yoy to ` 503cr. Hindalco has delayed its completion timeline of Mahan Aluminium

smelter to early CY2012 (CY2011-end earlier).

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 4/13

Market Outlook | India Research

November 11, 2011 4

Novelis' net sales grew by 14.1% yoy to US$2,880mn, driven by increased

realization. However, EBITDA decreased modestly by 0.9% yoy to US$228mn on

account of increased cost of goods sold, which grew by 16.5% yoy to

US$2,549mn. The company’s tax expense stood at US$(7)mn compared toUS$56mn in 2QFY2011. Consequently, net profit grew 140.0% yoy to US$120mn

in 2QFY2012.

We maintain our our Buy rating on Hindalco; our target is price under review.

Ranbaxy – 3QCY2011

For 3QCY2011, Ranbaxy reported net sales of ` 2,023cr, up 7.7% yoy. Gross

margin decreased by 65bp yoy for the quarter. OPM increased to 5.0% (4.7%)

during the quarter. The company reported loss of ` 465cr in earnings due to loss

on foreign exchange on foreign currency option derivatives (loss of ~ ` 400cr). Thestock is under review.

Lupin

For 2QFY2012, Lupin reported net sales of ` 1,742cr, up 23.6% yoy. Gross margin

increased by 465bp yoy for the quarter. OPM increased to 21.4% (19.4%) during

the quarter, despite higher manufacturing and other expenses (up 319bp yoy).

Adjusted net profit increased by 23.5% yoy to ` 267cr ( ` 216cr) despite higher

depreciation and tax rate. We maintain our Buy rating on the stock with a target

price of `593.

Mahindra Satyam

Mahindra Satyam (Satyam) announced its 2QFY2012 results, which were lower

than our expectations on the operating front. However, the company outperformed

on the PAT front. Dollar revenue came in at US$330mn, up 3.1% qoq, on the back

of 4.5% qoq volume growth. In rupee terms, the company’s revenue came in at

` 1,578cr, up by whopping 10.0% qoq. EBITDA margin expanded by 49bp qoq to

15.3%, lower than our expectation, due to higher operational expense because of

deployment of hardware and software licenses (25cr-30cr). PAT came in at

` 238cr, up 5.8% qoq. The stock is currently under review.

Bharat Forge

Bharat Forge (BFL) registered better-than-expected 26.6% yoy (6.1% qoq) jump in

its standalone revenue to ` 910cr, driven by robust 57.6% yoy (13.3% qoq) growth

in exports revenue. Strong growth in the CV segment and non auto segment in the

Europe and US benefitted the company’s exports performance. During 2QFY2012,

tonnage volume increased by 16.5% yoy (1.5% qoq) to 53,740MT on strongexport demand and increased average net realization increased (8.1% yoy, 4.7%

qoq). Domestic revenue growth was, however, sluggish as it grew modestly by

5.2% yoy (0.5% qoq) on account of slowdown in the automotive sector and

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 5/13

Market Outlook | India Research

November 11, 2011 5

industrial activity. On the operating front, the company's margin slipped by 56bp

yoy (63bp qoq) to 23.7%. While raw-material costs as a percentage of sales

remained stable, manufacturing expenses as a percentage of sales increased by

116bp yoy. Led by stable operating performance, a substantial increase in otherincome and lower tax rate, BFL's net profit jumped by 56.1% yoy (9.2% qoq)

to ` 106cr.

On a consolidated basis, BFL reported strong 25.3% yoy (flat qoq) growth in its top

line to ` 1,559cr. EBITDA margin came in slightly ahead of our estimates at 16.2%,

an increase of 50bp yoy (42bp qoq), resulting in a 55.2% yoy (1.2% qoq) increase

in PBT to ` 155cr. The stock rating is currently under review.

IRB

For 2QFY2012, IRB Infra reported a strong set of numbers, in-line with ourestimates. The company’s top line witnessed robust growth of 50.1% to ` 735.9cr

( ` 490.3cr), marginally ahead of our estimate of ` 687.0cr. On the EBITDAM front,

margin came at 43.7% (48.2%), slightly lower than our estimate of 45.2%. Interest

cost came in at ` 141.1cr ( ` 69.3cr), registering a jump of 103.7%/20.2% on a

yoy/qoq basis. At the earnings front as well, IRB Infra reported healthy growth of

22.1% to ` 147.6cr ( ` 120.9cr) and 11.1% to ` 110.1cr ( ` 99.1cr) on a yoy basis at

the PBT and PAT levels, respectively, against our estimate of ` 147.1cr and

` 107.3cr for PBT and PAT, respectively.

Our valuation of ` 193/share for the consolidated business uses NPV/EV/EBITDA-

based valuation for BOT assets and the C&EPC arm, respectively. We factor inCoE of 14% and a traffic growth rate of 5/6/7% for its BOT assets. We maintain

our view on the stock with a target price of `193.

ITNL

ITNL reported a good set of numbers for 2QFY2012. Revenue for the quarter

came in at ` 1,256cr ( ` 883cr), registering 42.1% yoy growth, primarily due to

higher revenue of the C&EPC segment. On a sequential basis as well, ITNL’s

revenue grew by 14.9%. EBITDA margin for the quarter stood at 28.4% vs. 29.6%

in 2QFY2011, down 120bp, mainly on account of increased contribution from the

relatively low-margin C&EPC segment, as expected. ITNL’s interest cost during the

quarter grew by 72.3%/18.8% yoy/qoq to ` 169.4cr ( ` 98.3cr). The bottom line

witnessed modest 8.2% yoy growth to ` 116.2cr ( ` 107.5cr), owing to lower

EBITDAM and higher interest cost during the quarter.

We have valued ITNL on an SOTP basis by assigning 6x EV/EBITDA to its

standalone business and have valued its investments on DCF/Mcap/BV basis

on FY2013E. We continue to maintain our Buy rating on the stock with a target

price of `260/share, implying an upside of 27.9% from current levels.

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 6/13

Market Outlook | India Research

November 11, 2011 6

CESC

During 2QFY2012, CESC reported 12.3% yoy growth in its standalone net sales to

` 1,241cr. Top-line growth was on account of better realization, as the volume of

power generated during the quarter was flat yoy at 2,355MU. Operating profit

during the quarter decreased by 18.2% yoy to ` 260cr. OPM for the quarter

declined by 783bp yoy to 21.0% on account of higher other expenses. Other

expenses during the quarter were higher on a yoy basis, at ` 195cr, on a low base

(CESC reported negative other expenses of ` 14cr in 2QFY2011). Other expenses

for the quarter included cost adjustments of ` 67cr as against negative ` 217cr in

2QFY2011. On the bottom-line front, net profit decreased by 26.5% yoy to

` 114cr. We maintain our Buy view on the stock; our target price is under review.

Apollo Tyres Apollo Tyres (APTY) reported a mixed set of results for 2QFY2012. While

standalone operating performance was subdued due to adverse product mix and

continued raw-material cost pressures, European operations posted strong results

led by robust demand for winter tyres ahead of the peak season.

For 2QFY2012, APTY registered 47.3% yoy (1.7% qoq) growth in its consolidated

net revenue to ` 2,871cr. Top-line growth was aided by 31.9% yoy (down 4% qoq)

growth in volumes to 120,000MT and 11.7% yoy (6% qoq) growth in average net

realization. On a low base of 2QFY2011 (lock-out at Cochin plant), standalone

volumes reported a 37% yoy jump, leading to 56.9% growth in revenue; however,

on a sequential basis, standalone volumes declined by ~10%. Europe and South

Africa operations registered strong revenue growth of 42.8% and 14.8% yoy,

respectively, during the quarter.

The company's operating margin declined by 148bp yoy (49bp qoq) to 8%, mainly

due to weak operating performance at the standalone level. While average rubber

cost declined by 4.1% sequentially, cost of other raw materials such as NTC and

carbon black moved up slightly due to depreciation of the INR. As a result,

consolidated raw material to net sales ratio stood at 67.5%, witnessing an increase

of 860bp yoy and 180bp qoq. EBIT margin at the European subsidiary expanded

by 240bp yoy (85bp qoq) to 10.6%, aided by price hike undertaken in June 2011.

Net profit grew by 46% yoy to ` 78cr. However, on a sequential basis, net profit

stood flat. A significant increase in other income and lower tax-rate benefited the

company's bottom-line performance during the quarter. We retain our Buy rating

on the stock with a target price of `74.

Godawari Power & Ispat

Godawari Power and Ispat reported its 2QFY2012 results. Consolidated net sales

increased by 190.0% yoy to ` 429cr, driven by increased volumes and realization.

However, EBITDA grew only by 73.2% yoy to ` 53cr on account of rising prices of

key inputs. Raw-material costs as a percentage of net sales stood at 65.8% in

2QFY2012, compared to 49.1% in 2QFY2011. Thus, EBITDA margin slipped by

828bp yoy to 12.3% in 2QFY2012. Interest costs and depreciation grew by

145.0% and 51.7% yoy to ` 25cr and ` 17cr, respectively. Consequently, net profit

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 7/13

Market Outlook | India Research

November 11, 2011 7

increased by 50.0% yoy to ` 11cr. We maintain our Buy rating on the stock; our

target price is under review.

Ceat

Ceat reported strong operating performance for 2QFY2012; however the bottom

line was severely impacted on account of high interest and depreciation expense

due to commissioning of the new facility at Halol. Ceat returned back to

profitability in 2QFY2012 after reporting losses at the operating as well as bottom-

line front in 1QFY2012.

Net sales grew strongly by 32.7% yoy (3.7% qoq) to ` 1,118cr on account of

availability of additional capacity at Halol plant and average price hike of ~10%

in 1QFY2012. Top-line growth also benefited from a 21.4% yoy increase in other

operating income. Operating margin improved by 27bp yoy to 5.5%, largely due

to ramp-up at Halol facility and price increases carried out in 1QFY2012. While

raw-material cost as a percentage of sales increased by 223bp yoy, the decline in

staff cost and other expenditure as a percentage of sales by 129bp and 132bp

yoy, respectively, helped Ceat maintain its margins. Net profit, however, fell

sharply by 63.3% yoy to ` 6cr due to a significant increase in depreciation (114%

yoy) and interest expense (170% yoy).

We expect the company to report continuous improvement in its operating

performance, led by improving utilization at Halol plant and a gradual decline in

raw-material prices. We maintain our Buy rating on the stock; however our target

price is under review.

Result Previews

Coal India

Coal India is slated to report its 2QFY2012 results tomorrow. We expect net sales

to increase by 18.2% yoy to ` 13,774cr mainly on account of increase in coal

prices. EBITDA margin is expected to expand 1,207bp yoy to 28.0% in 2QFY2012.

Net profit is expected to increase by 111.7% yoy to ` 3,164cr. We recommend

Accumulate on the stock.

Nalco

Nalco is slated to report its 2QFY2012 results. We expect net sales to decreaseby 1.0% yoy to ` 1,440cr despite higher realization on account of productioncuts during the quarter. EBITDA margin is expected to contract by 122bp yoy to 21.0% due to lower volumes and rise in prices of key inputs (primarily coal).Net profit is expected to increase by 6.2% yoy to ` 238cr. We maintain ourNeutral view on the stock.

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 8/13

Market Outlook | India Research

November 11, 2011 8

MOIL

MOIL is slated to report its 2QFY2012. We expect net sales to decline by 36.8%

yoy and 14.5% qoq to ` 180cr, mainly on account of a sharp decline in

manganese ore prices. Nevertheless, EBITDA margin is expected to improve by

1,967bp yoy, but decline by 430bp qoq, to 56.0% in 2QFY2012. Net profit is

expected to decrease by 70.2% yoy and 15.1% qoq to ` 93cr. We maintain our

Neutral view on the stock.

Britannia

Britannia is expected to announce its 2QFY2012 results. For the quarter, we expect

the company to report healthy revenue growth of 18% yoy to ` 1,291cr due to

improvement in sales mix. We expect the company to report a margin

improvement yoy for the quarter, despite high raw-material cost pressure. Earnings

for the quarter are expected to grow by 27% yoy to ` 42cr on the back of margin

expansion and healthy top-line growth. At the CMP, the stock is trading at 21.1x

F2013E EPS of `21.1. We recommend a Neutral rating on the stock.

Dishman Pharma

For 2QFY2012, Dishman Pharma (DISH) is expected to post net sales growth of

12.8% yoy. OPM for the quarter is likely to expand to 18.6%. However, the

company’s net profit is expected to come in at ` 16cr, reporting a dip of 43.1% yoy.

We maintain our Buy rating on the stock with a target price of `133.

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 9/13

Market Outlook | India Research

November 11, 2011 9

Quarterly Bloomberg Brokers’ Consensus Estimates

Mundra Port & SEZ Ltd. - (11/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 554 408 36.0 516 7.4

EBITDA 380 274 38.8 363 4.7

EBITDA margin (%) 69 67 70

Net profit 271 212 27.8 254 6.4

Source: Bloomberg

Tata Chemicals Ltd. - Consolidated - (11/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 2,950 2,935 0.5 2,924 0.9

EBITDA 556 418

33.1

527 5.6EBITDA margin (%) 19 14 18

Net profit 207 127 63.2 200 3.8

Source: Bloomberg

Adani Power Ltd. - (11/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 964 395 144.0 819 17.8

EBITDA 524 209 150.3 410 27.8

EBITDA margin (%) 54 53 50

Net profit 224 126 78.3 177 26.9

Source: Bloomberg

HDIL Ltd. - (11/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 491 373 31.7 502 (2.3)

EBITDA 251 367 (31.6) 266 (5.6)

EBITDA margin (%) 51 99 53

Net profit 192 214 (10.4) 209 (8.4)

Source: Bloomberg

Reliance Communication Ltd. - Consolidated (12/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 5,041 4,973 1.4 4,712 7.0

EBITDA 1,630 1,564 4.2 1,511 7.9

EBITDA margin (%) 32 31 32

Net profit 169 446 (62.1) 157 7.7

Source: Bloomberg

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 10/13

Market Outlook | India Research

November 11, 2011 10

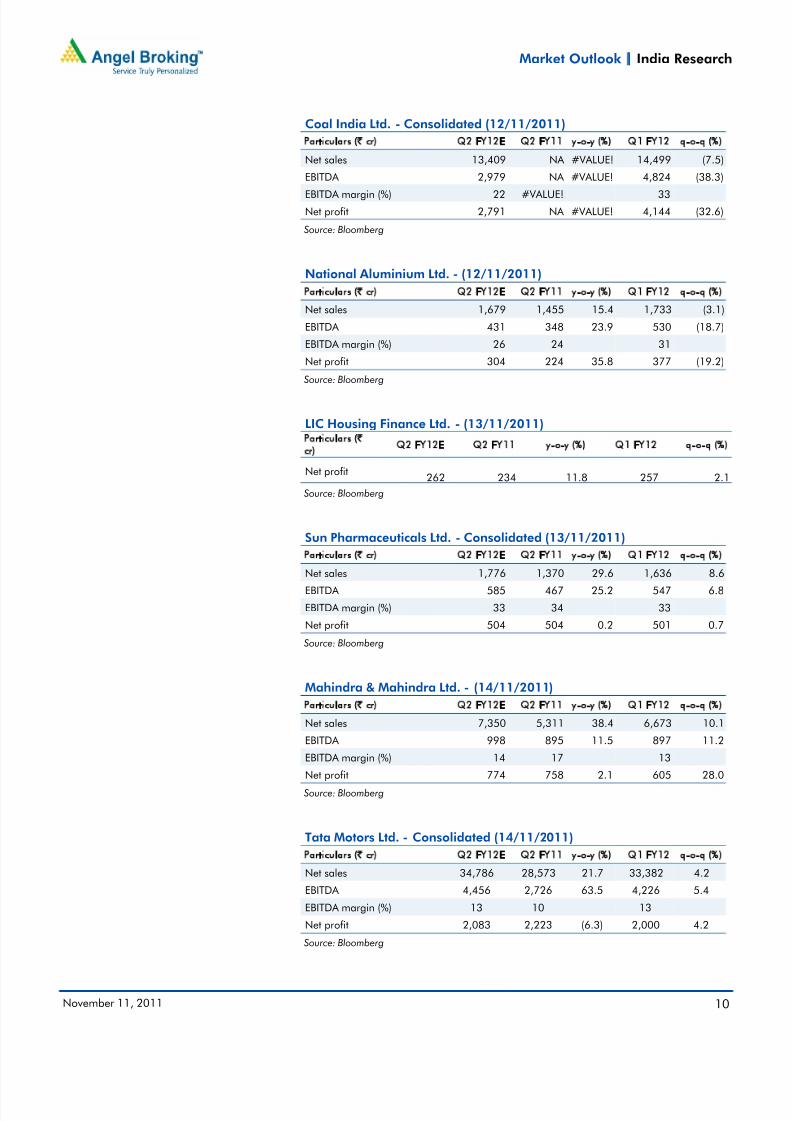

Coal India Ltd. - Consolidated (12/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 13,409 NA #VALUE! 14,499 (7.5)

EBITDA 2,979 NA #VALUE! 4,824 (38.3)

EBITDA margin (%) 22 #VALUE! 33

Net profit 2,791 NA #VALUE! 4,144 (32.6)

Source: Bloomberg

National Aluminium Ltd. - (12/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 1,679 1,455 15.4 1,733 (3.1)

EBITDA 431 348 23.9 530 (18.7)

EBITDA margin (%) 26 24 31

Net profit 304 224 35.8 377 (19.2) Source: Bloomberg

LIC Housing Finance Ltd. - (13/11/2011)Particulars (`cr)

Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net profit262 234 11.8 257 2.1

Source: Bloomberg

Sun Pharmaceuticals Ltd. - Consolidated (13/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 1,776 1,370 29.6 1,636 8.6

EBITDA 585 467 25.2 547 6.8

EBITDA margin (%) 33 34 33

Net profit 504 504 0.2 501 0.7

Source: Bloomberg

Mahindra & Mahindra Ltd. - (14/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 7,350 5,311 38.4 6,673 10.1

EBITDA 998 895 11.5 897 11.2

EBITDA margin (%) 14 17 13

Net profit 774 758 2.1 605 28.0

Source: Bloomberg

Tata Motors Ltd. - Consolidated (14/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 34,786 28,573 21.7 33,382 4.2

EBITDA 4,456 2,726 63.5 4,226 5.4

EBITDA margin (%) 13 10 13

Net profit 2,083 2,223 (6.3) 2,000 4.2

Source: Bloomberg

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 11/13

Market Outlook | India Research

November 11, 2011 11

Adani Enterprise Ltd. - Consolidated (14/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 8,120 5,750 41.2 9,596 (15.4)

EBITDA 1,349 726 85.9 1,168 15.5

EBITDA margin (%) 17 13 12

Net profit 515 509 1.1 570 (9.7)

Source: Bloomberg

Unitech Ltd. - Consolidated (14/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 660 645 2.3 596 10.7

EBITDA 172 253 (32.0) 120 43.5

EBITDA margin (%) 26 39 20

Net profit 115 174 (33.9) 98 16.9 Source: Bloomberg

Tata Power Company Ltd. - Consolidated (14/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 5,782 4,798 20.5 5,805 (0.4)

EBITDA 1,505 1,137 32.3 1,412 6.6

EBITDA margin (%) 26 24 24

Net profit 578 673 (14.0) 419 38.2

Source: Bloomberg

BHEL Ltd. - (14/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 9,716 8,328 16.7 7,126 36.3

EBITDA 1,810 1,632 10.9 1,113 62.6

EBITDA margin (%) 19 20 16

Net profit 1,275 1,142 11.6 816 56.4

Source: Bloomberg

Cipla Ltd. - (14/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 1,760 1,580 11.4 1,550 13.5

EBITDA 391 367 6.6 370 5.7

EBITDA margin (%) 22 23 24

Net profit 272 263 3.4 253 7.5

Source: Bloomberg

Jai Prakash Associates Ltd. - (14/11/2011)

Particulars (` cr) Q2 FY12E Q2 FY11 y-o-y (%) Q1 FY12 q-o-q (%)

Net sales 3,118 2,993 4.2 3,142 (0.8)

Net profit 117 116 1.1 107 9.2

Source: Bloomberg

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 12/13

Market Outlook | India Research

November 11, 2011 12

Economic and Political News

Domestic car sales dip by 24% yoy in October 2011

No automatic route for FDI into existing pharma firms

Agriculture sector growth of 4% will check inflation: Planning Commission

Corporate News

PFC gets nod to launch US$1bn private equity fund

EMC wins ` 776cr deal from PowerGrid Corp.

HCC’s arm Lavasa gets environment ministry's nod

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Results Calendar

11/11/2011 Mundra Port, Adani Power, Tata Chemicals, Reliance Capital, Britannia, MOIL, HDIL, Anant Raj, SpiceJet, Dishman Pharma

12/11/2011 Coal India, Nalco, Rcom, IVRCL Infra

13/11/2011 Sun Pharma, LIC Housing Fin.

14/11/2011BHEL, Tata Motors, Adani Enterp., M&M, Cipla, Jaiprakash Asso., JSW Steel , Unitech, Bhushan Steel, GSPL, Aventis, Areva, BGR Energy , India Cements, Amara Raja Batteries, Graphite India, Simplex Infra, Patel Engg., Madhucon Proj, JK Tyre

15/11/2011 Tech Mahindra

8/3/2019 Market Outlook 11th November 2011

http://slidepdf.com/reader/full/market-outlook-11th-november-2011 13/13

Market Outlook | India Research

N b 11 2011 13

Research Team Tel: 022 - 39357800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investmentdecision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliablesources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as thisdocument is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report .

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to thelatest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may haveinvestment positions in the stocks recommended in this report.