Embed Size (px)

Citation preview

Market Outlook

Sao Paulo, Brazil

October, 2005

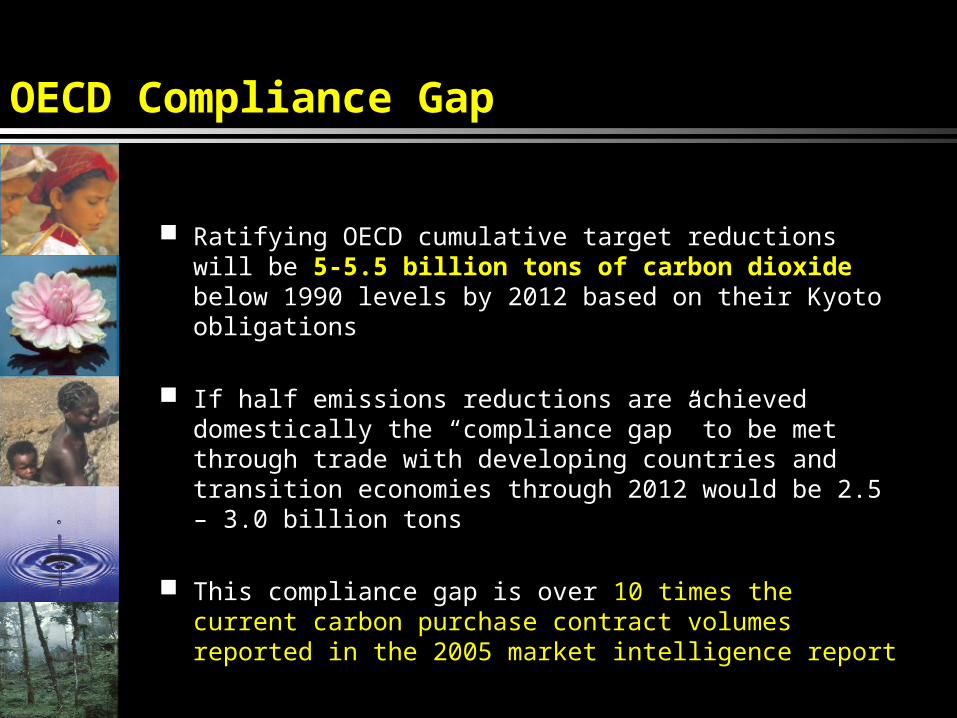

OECD Compliance Gap

Ratifying OECD cumulative target reductions will be 5-5.5 billion tons of carbon dioxide below 1990 levels by 2012 based on their Kyoto obligations

If half emissions reductions are achieved domestically the “compliance gap” to be met through trade with developing countries and transition economies through 2012 would be 2.5 – 3.0 billion tons

This compliance gap is over 10 times the current carbon purchase contract volumes reported in the 2005 market intelligence report

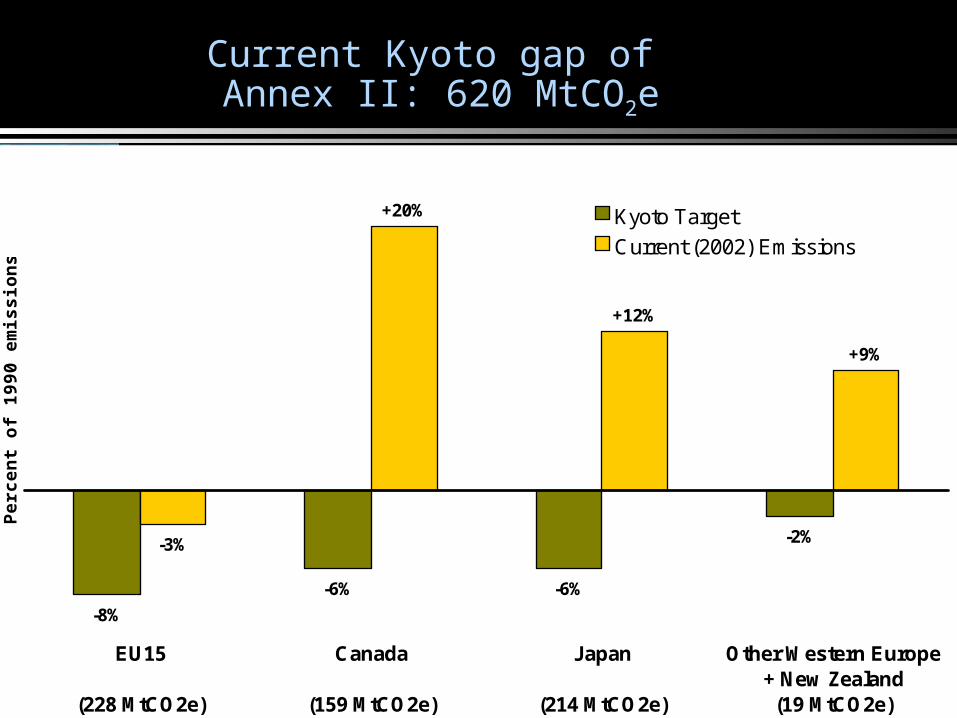

Current Kyoto gap of Annex II: 620 MtCO2e

-8%

-6% -6%

-2%-3%

+20%

+12%

+9%

EU15

(228 MtCO2e)

Canada

(159 MtCO2e)

Japan

(214 MtCO2e)

Other Western Europe+ New Zealand

(19 MtCO2e)

Pe

rce

nt

of

19

90

em

iss

ion

s l

ev

el

Kyoto Target

Current (2002) Emissions

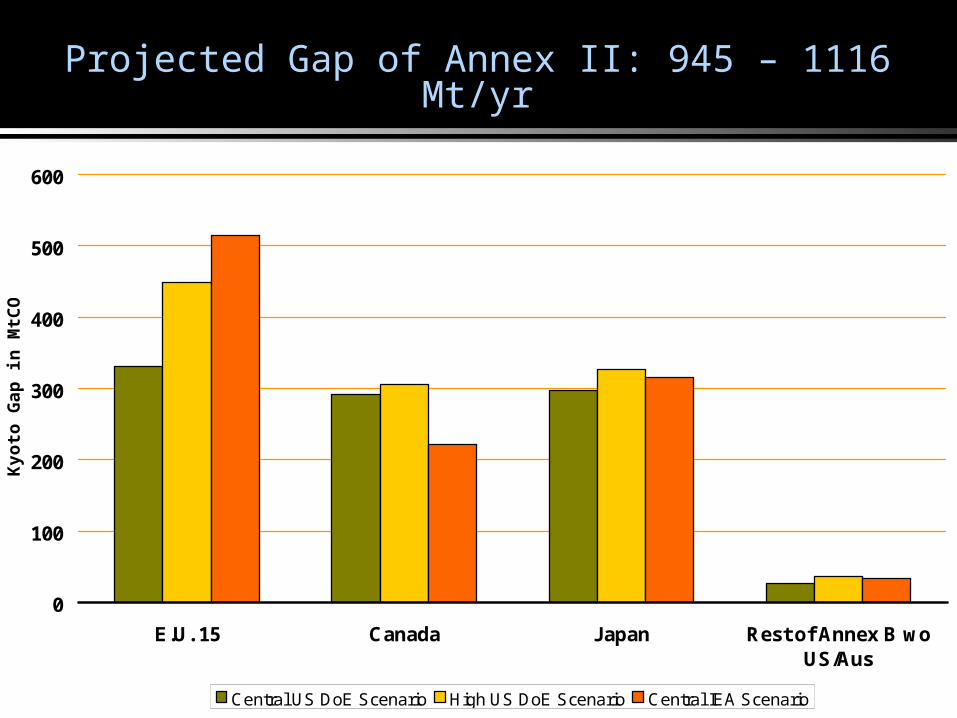

Projected Gap of Annex II: 945 – 1116 Mt/yr

0

100

200

300

400

500

600

E.U. 15 Canada Japan Rest of Annex B woUS/Aus

Ky

oto

Ga

p in

MtC

O2e

Central US DoE Scenario High US DoE Scenario Central IEA Scenario

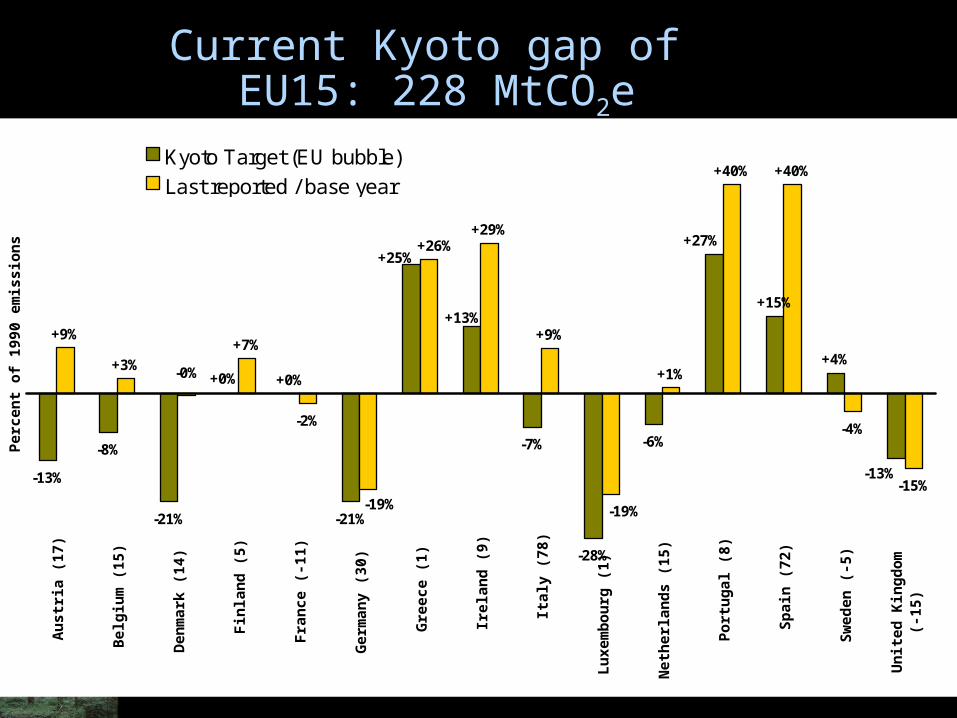

Current Kyoto gap of EU15: 228 MtCO2e

-13%

-8%

-21%

+0%

-21%

-7%

-28%

-6%

+15%

+4%

+9%

+3%+7%

-2%

+29%

+9%

+1%

+40% +40%

-4%

-15%-13%

+27%

+13%

+25%

+0%

-19%

-0%

+26%

-19%

Au

stri

a (1

7)

Bel

giu

m (

15)

Den

mar

k (1

4)

Fin

lan

d (

5)

Fra

nce

(-1

1)

Ger

man

y (3

0)

Gre

ece

(1)

Irel

and

(9)

Ital

y (7

8)

Lu

xem

bo

urg

(1)

Net

her

lan

ds

(15)

Po

rtu

gal

(8)

Sp

ain

(72

)

Sw

eden

(-5

)

Un

ited

Kin

gd

om

(-15

)

Per

cen

t o

f 19

90 e

mis

sio

ns

leve

l

Kyoto Target (EU bubble)

Last reported / base year

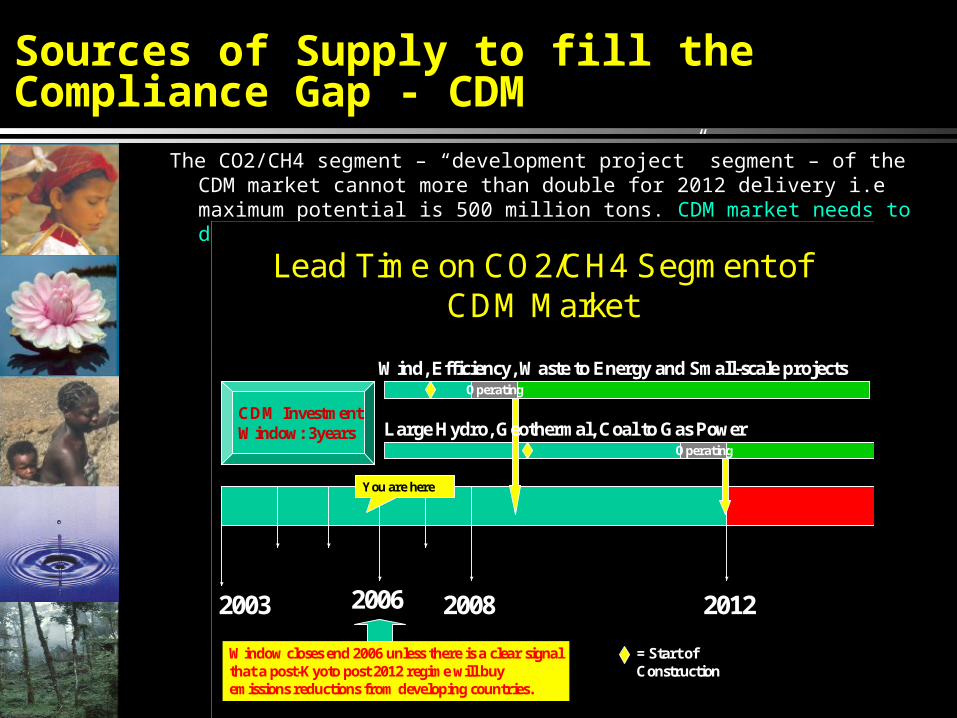

Sources of Supply to fill the Compliance Gap - CDM

The CO2/CH4 segment – “development project” segment – of the CDM market cannot more than double for 2012 delivery i.e maximum potential is 500 million tons. CDM market needs to deliver at least 1.5 billion tons

Lead Time on CO2/CH4 Segment of CDM Market

2006 20082003 2012

Operating

Wind, Efficiency, Waste to Energy and Small-scale projects

Large Hydro, Geothermal, Coal to Gas PowerCDM Investment Window: 3years

Window closes end 2006 unless there is a clear signal that a post-Kyoto post 2012 regime will buy emissions reductions from developing countries.

Operating

= Start of Construction

You are here

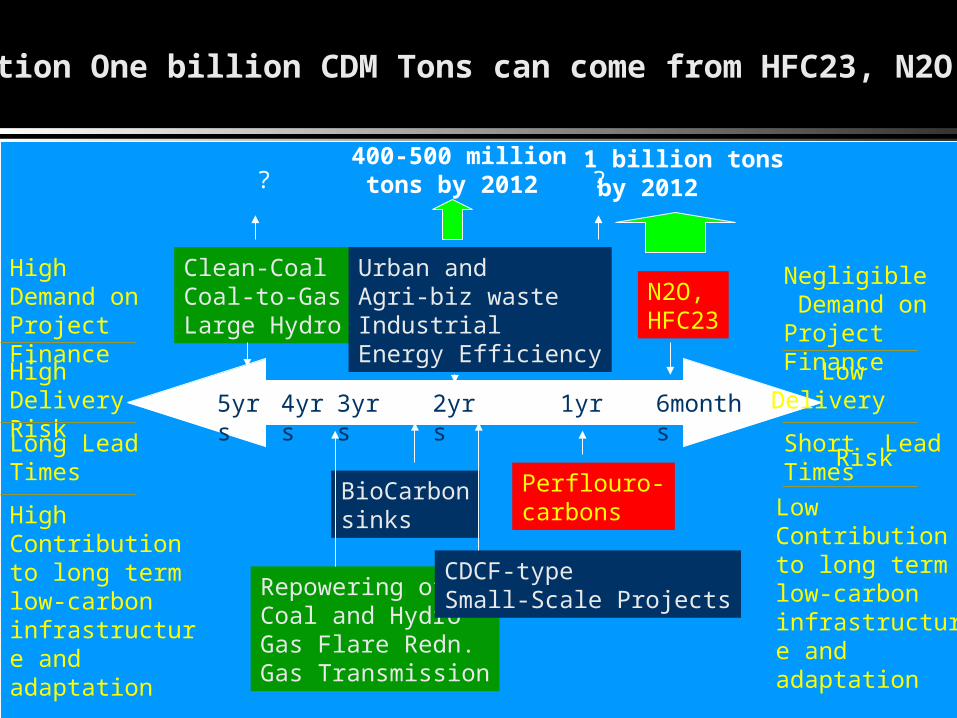

High Demand on Project Finance

Negligible Demand on Project Finance

High Delivery Risk

Low Delivery Risk

Long Lead Times

Short Lead Times

High Contribution to long term low-carbon infrastructure and adaptation

Low Contribution to long term low-carbon infrastructure and adaptation

Clean-CoalCoal-to-GasLarge Hydro

Repowering ofCoal and HydroGas Flare Redn.Gas Transmission

BioCarbonsinks

Urban and Agri-biz wasteIndustrialEnergy Efficiency

CDCF-typeSmall-Scale Projects

Perflouro-carbons

N2O, HFC23

5yrs 6months2yrs 1yr4yrs 3yrs

400-500 million tons by 2012

1 billion tons by 2012??

Addition One billion CDM Tons can come from HFC23, N2O, PF6

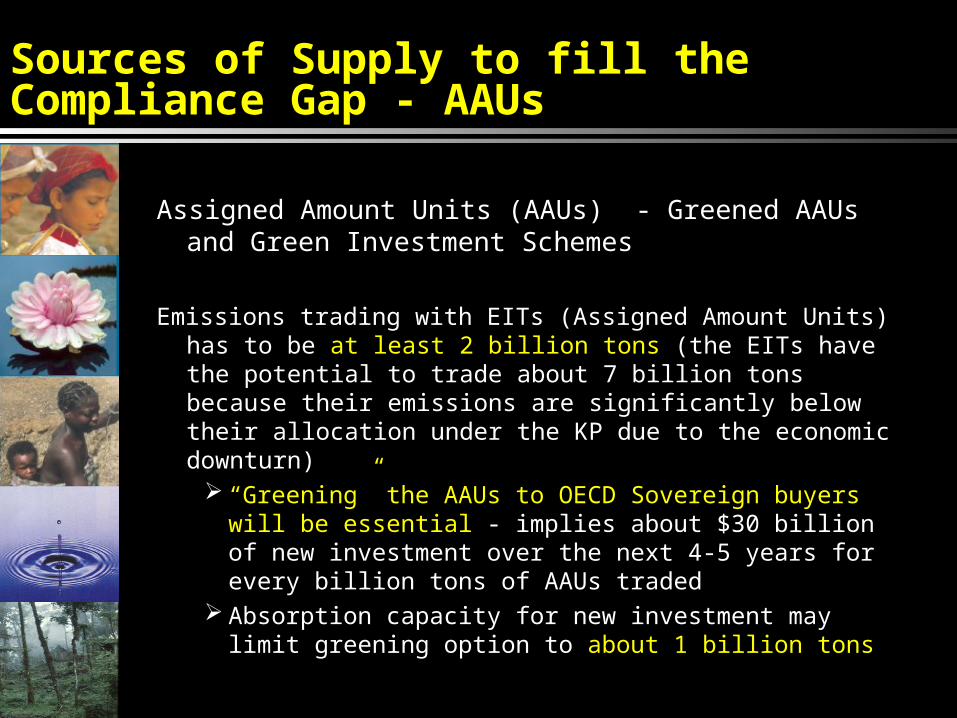

Sources of Supply to fill the Compliance Gap - AAUs

Assigned Amount Units (AAUs) - Greened AAUs and Green Investment Schemes

Emissions trading with EITs (Assigned Amount Units) has to be at least 2 billion tons (the EITs have the potential to trade about 7 billion tons because their emissions are significantly below their allocation under the KP due to the economic downturn)

“Greening” the AAUs to OECD Sovereign buyers will be essential - implies about $30 billion of new investment over the next 4-5 years for every billion tons of AAUs traded

Absorption capacity for new investment may limit greening option to about 1 billion tons

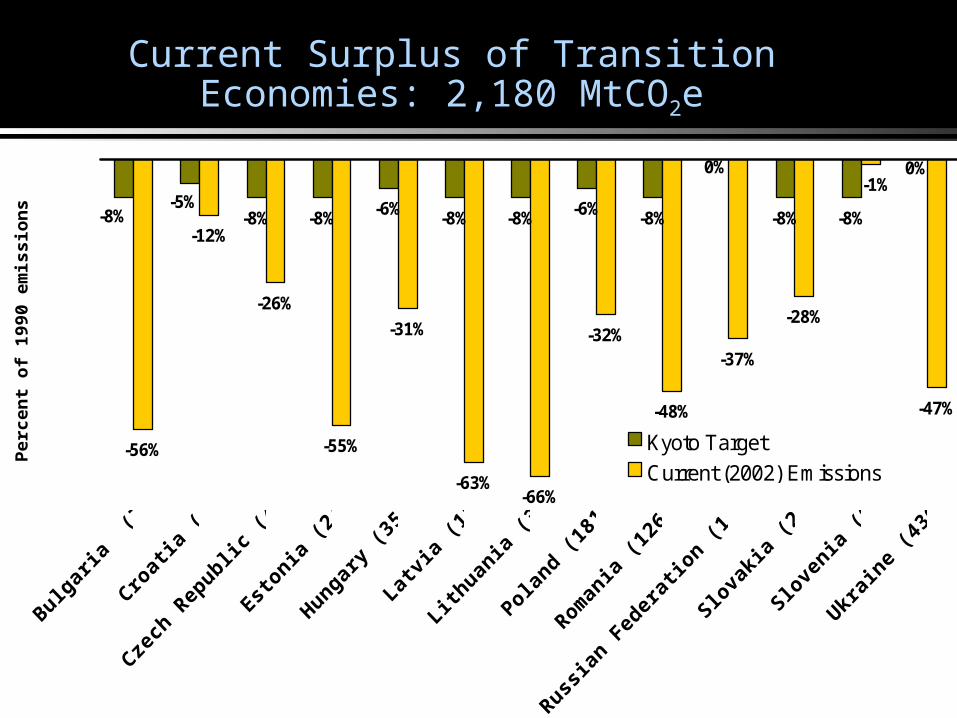

Current Surplus of Transition Economies: 2,180 MtCO2e

-8% -8% -6% -8% -8% -6% -8% -8% -8%

-56%

-12%

-26%

-55%

-31%

-63%-66%

-32%

-48%

-37%

-28%

-47%

0%0%

-5%-8%

-1%

Per

cen

t o

f 19

90 e

mis

sio

ns

leve

l

Kyoto Target

Current (2002) Emissions

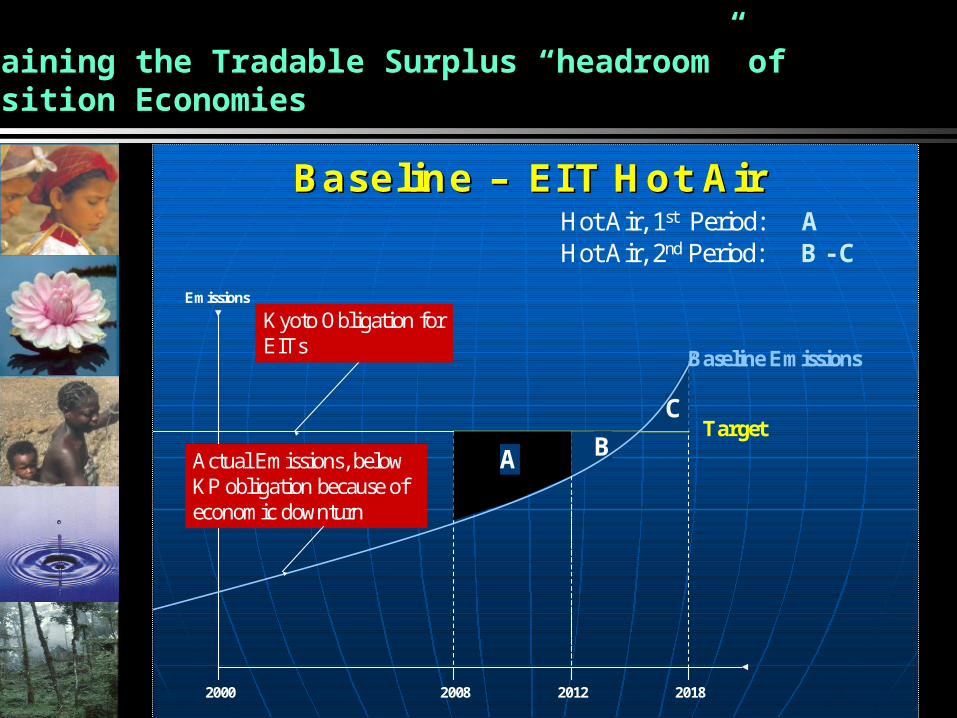

Baseline Baseline –– EIT Hot AirEIT Hot Air

2000 2008 2012 2018

Emissions

Target

Baseline Emissions

Hot Air, 1st Period: A

A

Hot Air, 2nd Period: B - C

B

C

Kyoto Obligation for EITs

Actual Emissions, below KP obligation because of economic downturn

Explaining the Tradable Surplus “headroom” of Transition Economies

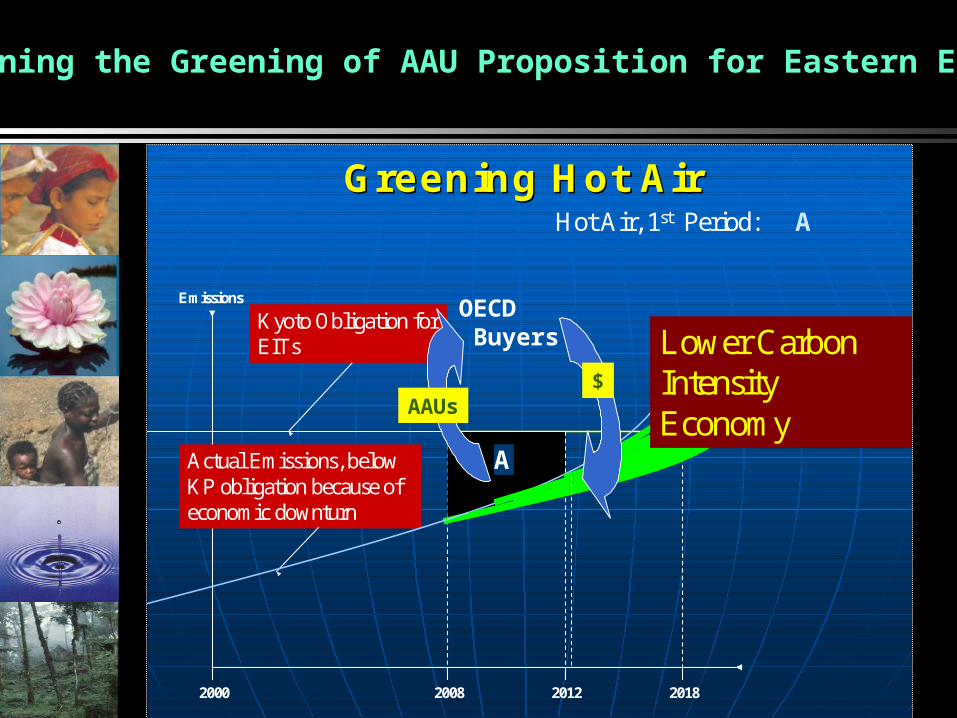

Greening Hot AirGreening Hot Air

2000 2008 2012 2018

Emissions

Target

Baseline Emissions

Hot Air, 1st Period: A

A

Kyoto Obligation for EITs

Actual Emissions, below KP obligation because of economic downturn

Lower Carbon Intensity Economy

Explaining the Greening of AAU Proposition for Eastern Europe

OECD Buyers

AAUs$

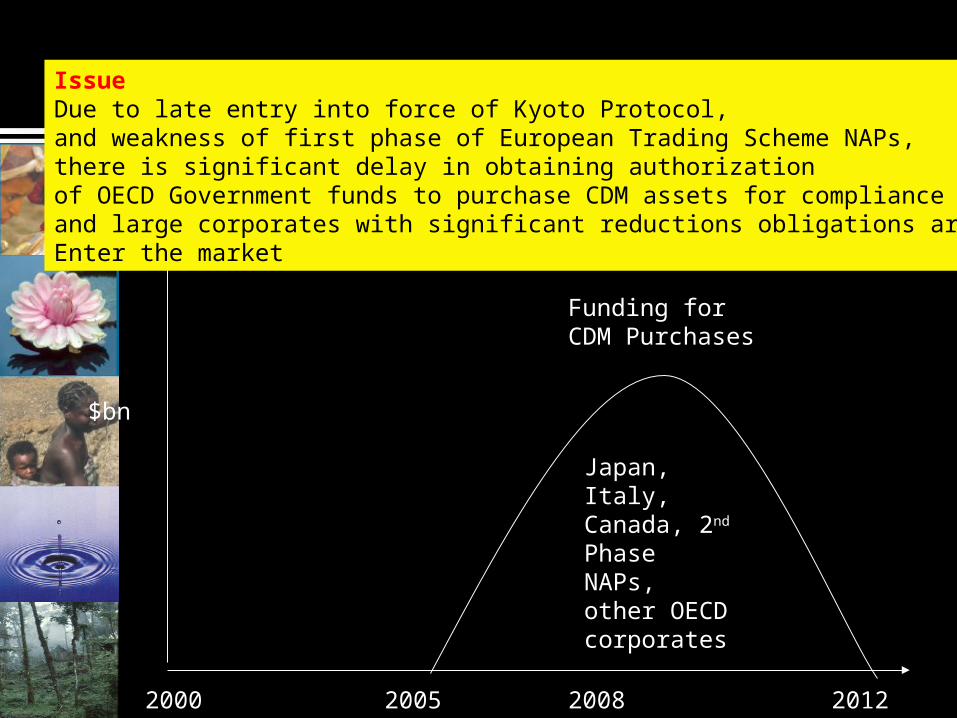

Funding for CDM Purchases

2000 2005 2008 2012

Japan, Italy, Canada, 2nd Phase NAPs, other OECD corporates

IssueDue to late entry into force of Kyoto Protocol, and weakness of first phase of European Trading Scheme NAPs,there is significant delay in obtaining authorization of OECD Government funds to purchase CDM assets for compliance and large corporates with significant reductions obligations are late to Enter the market

$bn

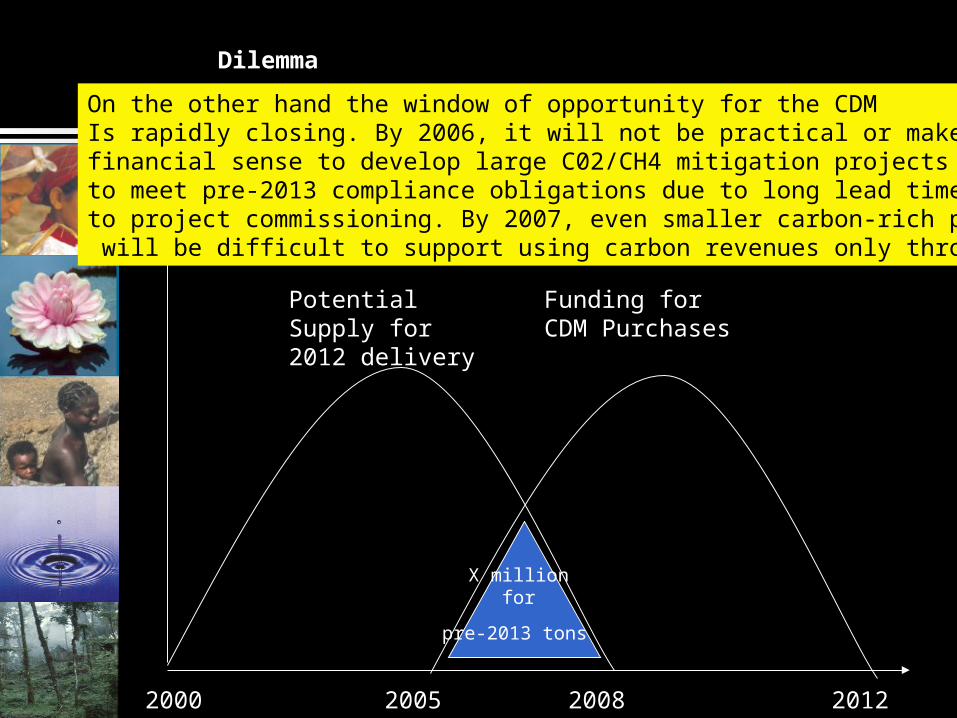

Potential Supply for 2012 delivery

Funding for CDM Purchases

2000 2005 2008 2012

On the other hand the window of opportunity for the CDM Is rapidly closing. By 2006, it will not be practical or make financial sense to develop large C02/CH4 mitigation projects to meet pre-2013 compliance obligations due to long lead times to project commissioning. By 2007, even smaller carbon-rich projects will be difficult to support using carbon revenues only through 2012

Dilemma

X million for

pre-2013 tons

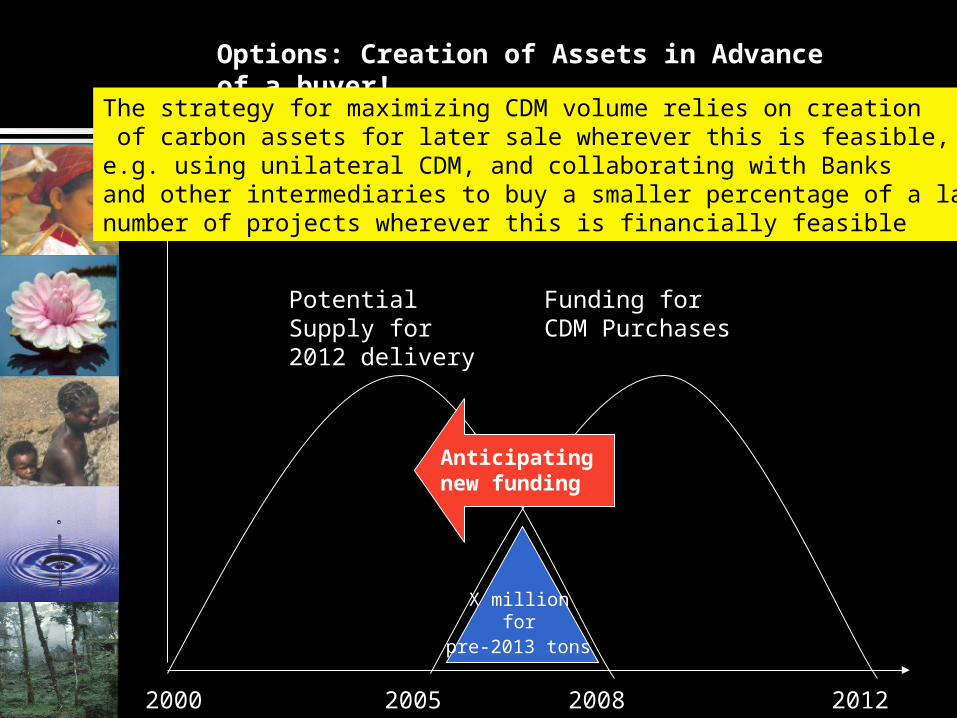

Potential Supply for 2012 delivery

Funding for CDM Purchases

2000 2005 2008 2012

Anticipating new funding

Options: Creation of Assets in Advance of a buyer!

The strategy for maximizing CDM volume relies on creation of carbon assets for later sale wherever this is feasible, e.g. using unilateral CDM, and collaborating with Banks and other intermediaries to buy a smaller percentage of a largernumber of projects wherever this is financially feasible

X million for

pre-2013 tons

Potential Supply for 2012 delivery

Funding for CDM Purchases

2000 2005 2008 2012

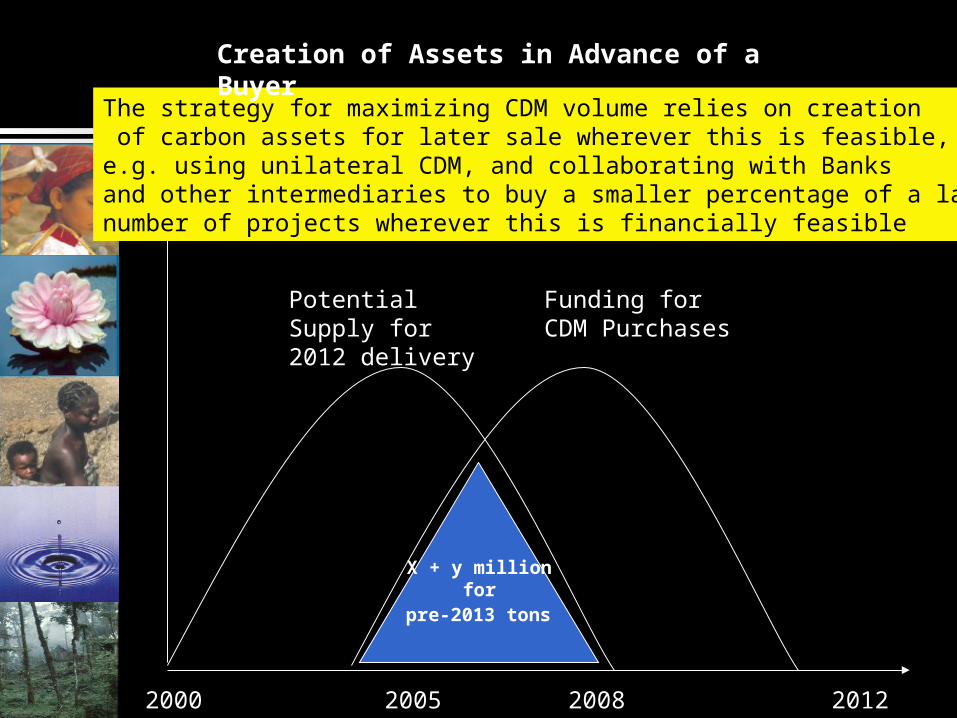

The strategy for maximizing CDM volume relies on creation of carbon assets for later sale wherever this is feasible, e.g. using unilateral CDM, and collaborating with Banks and other intermediaries to buy a smaller percentage of a largernumber of projects wherever this is financially feasible

X + y million for

pre-2013 tons

Creation of Assets in Advance of a Buyer

A Cautionary Note

To avoid a collapse in the CO2/CH4 segment of the carbon market (and continued stagnation in investment in low carbon climate friendly energy and infrastructure) we need:• Immediately implemented CDM Reform embracing

capacity enhancement, process streamlining and “technology additionality” agreed in CoP/MoP

• A CDM Market Continuity Facility to buy post-2012 vintage CERs to guarantee 10-year contracts, combined with a

• OECD Commitment to grandfather CDM assets into the post-2012 era

“Technology Additionality” Proposal

48(c ) approach: “The average emissions of similar project activities undertaken in the previous five years, in similar social, economic, environmental and technological circumstances, and whose performance is among the top 20 per cent of their category.”

(so far no approved CDM methodology using 48c) Flexible interpretation of 48 (c) provides an opportunity for radical

reduction in CDM transaction costs and the needed regulatory certainty for developers and financiers

Parallel to pre-defined baselines for small-scale projects Parties could approve in December a positive list of “additional”

technologies up to an initial penetration rate.• e.g. up to an agreed market penetration rate, all renewables, all demand

side management efficiency activities, all landfill gas capture and composting et etc is additional…

CDM’s Contribution to Post-2012 Climate Management Regime

CDM’s track record demonstrates that project-by-project approaches are incompatible with future carbon market needs of large industrializing developing countries.

A future market-based mechanism for carbon trade should ensure:• Very low transactions costs• High transparency and simplicity in regulations defining a compliance grade

carbon asset• Low regulatory risk that carbon assets contracted will have compliance

value, allowing forward carbon contracts to be monetized and financiers to accept carbon revenues as a real contribution to project viability and bankabiity

These are pre-conditions to catalyze high volumes of transactions and investment resource flows and technology transfer

These conditions would allow carbon revenues to cover the incremental cost and incremental risk of much low carbon development

Project-based vs Sectoral Mechanisms in the post-2012 era

Both will be required• Sectoral approaches for larger energy using economies -

the only means of generating the resource and technology flows on the needed scale

• Project-based approaches - for smaller less industrialized countries, or for low volume sectors not amenable to sectoral approaches

Neither the sectoral nor project-based approaches of the future has yet been demonstrated!

This the opportunity for Technology Additionality and CDM Reform

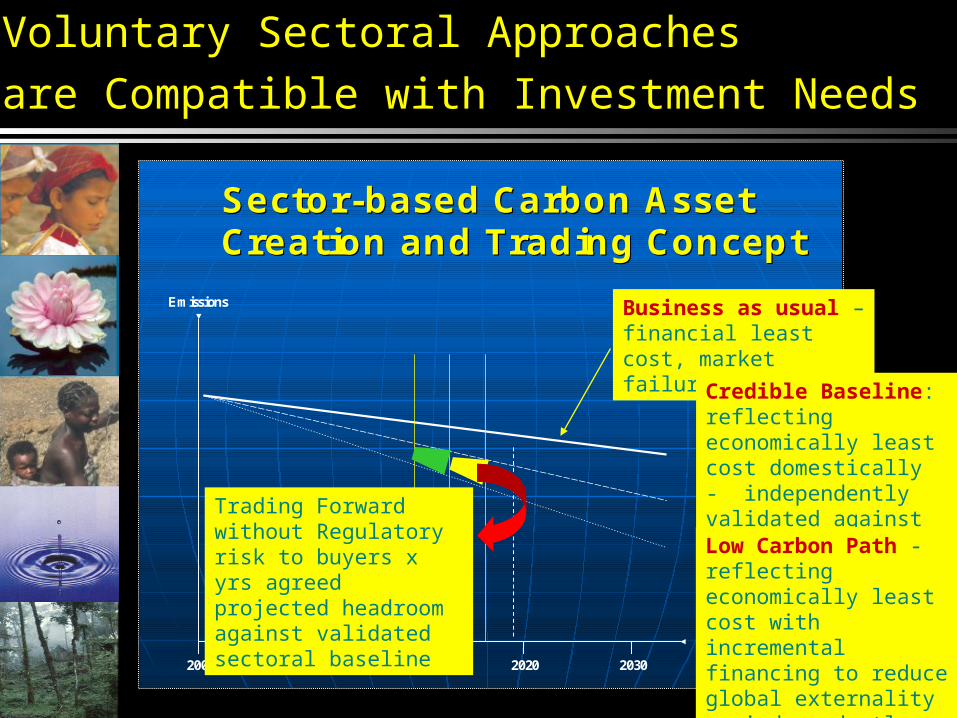

SectorSector--based Carbon Asset based Carbon Asset Creation and Trading ConceptCreation and Trading Concept

2000 2010 2020 2030

Emissions

Trading Forward without Regulatory risk to buyers x yrs agreed projected headroom against validated sectoral baseline

Voluntary Sectoral Approaches

are Compatible with Investment Needs

Business as usual – financial least cost, market failures

Credible Baseline: reflecting economically least cost domestically - independently validated against policies and measuresLow Carbon Path - reflecting economically least cost with incremental financing to reduce global externality - independently validated against policies and measures