Embed Size (px)

Citation preview

17 March 2021 | Evolution of raw material selection for Refractory Materials 1

Phil Edwards Chris Parr Marketing Director - Refractory VP Science and Technology

Evolution of raw material selection for refractory applications

17 March 2021 | Evolution of raw material selection for Refractory Materials 2

Evolution of Raw Material Selection

Applications & Material Selection

External market forces and impact

The next lines of raw materials

Applications & Material Selection

17 March 2021 | Evolution of raw material selection for Refractory Materials 3

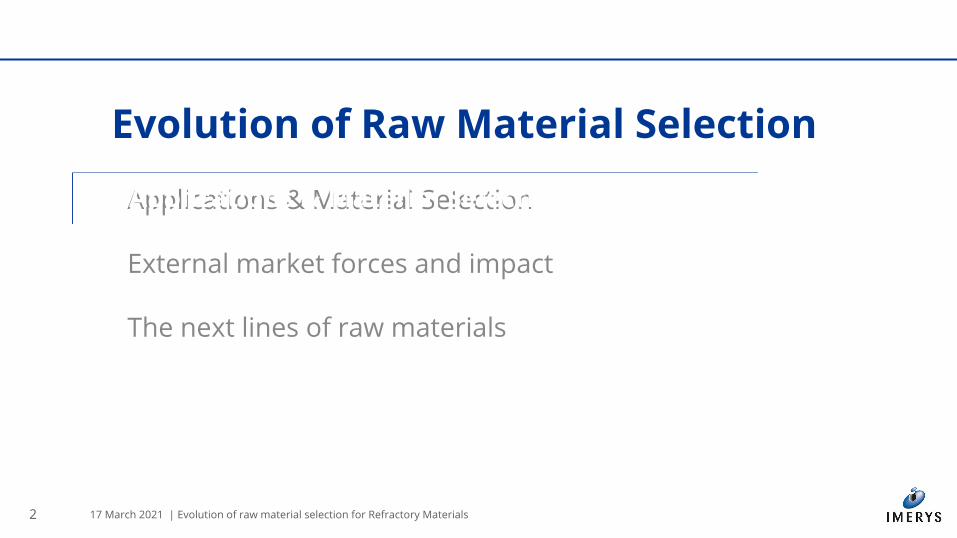

● Refractory markets estimated to have declined by around 8%

○ Strong variance globally ○ Covid related drop in EU/Americas ≈20%○ China rebound in Q3/Q4

● The two sides to the Refractory market

○ Acid v Basic minerals ○ Monolithic v Shaped products○ China production v ROW

● Production linked to value & usage○ Long shelf life items more likely to travel ○ Repairs & maintenance more likely to be

sourced locally ○ Ability to solve customers problems

drives local solutions

Refractory Market was impacted heavily across 2020 with COVID striking consumers forcing a reduction in non-critical activities

With plants forced to reduce both production and repairs & maintenance activities, with onsite personnel limited, the typical day to day activities have been reduced across the board

Basic : Acid materials (55/45)

Brick : Monolithics (57/43)

China : ROW production (60/40)

≈37 MMT

17 March 2021 | Evolution of raw material selection for Refractory Materials 4

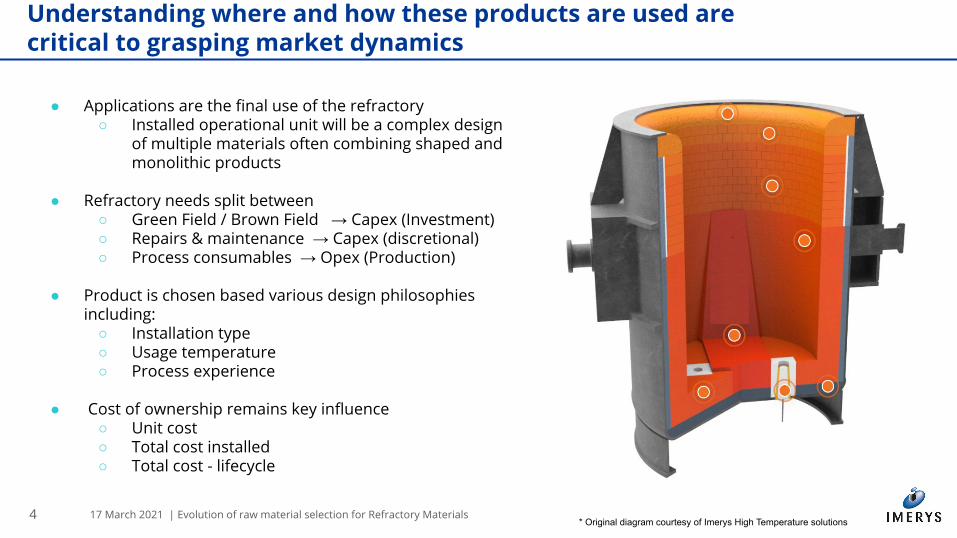

● Applications are the final use of the refractory○ Installed operational unit will be a complex design

of multiple materials often combining shaped and monolithic products

● Refractory needs split between ○ Green Field / Brown Field → Capex (Investment) ○ Repairs & maintenance → Capex (discretional) ○ Process consumables → Opex (Production)

● Product is chosen based various design philosophies

including: ○ Installation type ○ Usage temperature ○ Process experience

● Cost of ownership remains key influence ○ Unit cost ○ Total cost installed ○ Total cost - lifecycle

Understanding where and how these products are used are critical to grasping market dynamics

* Original diagram courtesy of Imerys High Temperature solutions

17 March 2021 | Evolution of raw material selection for Refractory Materials 5

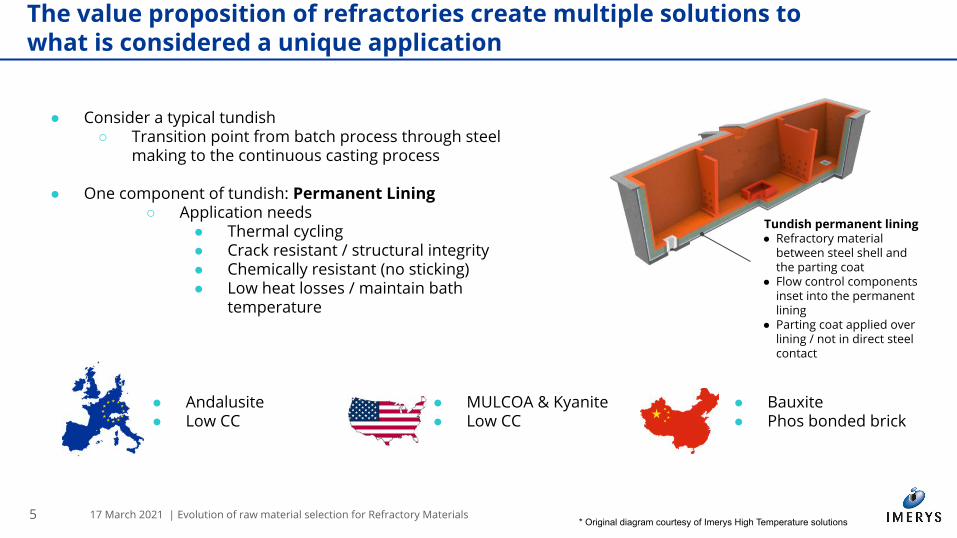

The value proposition of refractories create multiple solutions to what is considered a unique application

● Consider a typical tundish○ Transition point from batch process through steel

making to the continuous casting process

● One component of tundish: Permanent Lining ○ Application needs

● Thermal cycling ● Crack resistant / structural integrity ● Chemically resistant (no sticking) ● Low heat losses / maintain bath

temperature

* Original diagram courtesy of Imerys High Temperature solutions

● Andalusite ● Low CC

● MULCOA & Kyanite● Low CC

● Bauxite ● Phos bonded brick

Tundish permanent lining● Refractory material

between steel shell and the parting coat

● Flow control components inset into the permanent lining

● Parting coat applied over lining / not in direct steel contact

17 March 2021 | Evolution of raw material selection for Refractory Materials 6

Depends on industry & type of job

○ Refractory producers will produce and recommend products based on knowledge of application within cost to serve expectations

○ Steel repairs and maintenance■ Internal refractory stewards■ Mix of internal / external workforce

→ Reduce operational costs

○ Cement kiln annual repairs ■ Maintenance contractor in place■ Refractory recommended by suppliers

→ Meet ‘ontime’ unit start up

○ Greenfield processing units■ Signed off and specified by ‘OEM’ ■ Technology providers / designers

Pechiney & Aluminium → Target to meet ‘warranty’ timeline

How do these decisions get made? By who and why?

17 March 2021 | Evolution of raw material selection for Refractory Materials 7

Evolution of Raw Material Selection

Applications & Material Selection

External market forces and impact

The next lines of raw materials

External Market forces and impact

17 March 2021 | Evolution of raw material selection for Refractory Materials 8

● Products are designed to contain high temperature processes in a safe manner

● No easy way to say this, failures can result in fatalities. This is unacceptable on any level

● Consequently, by its nature you have a relatively conservative decision making approach wrapped in data & experience

● Change has to be to create value & the value creation has to be validated.

● Only 3 ways to create value ○ Reduce risk ○ Reduce time ○ Reduce cost

Refractories are about creating a safe working environment

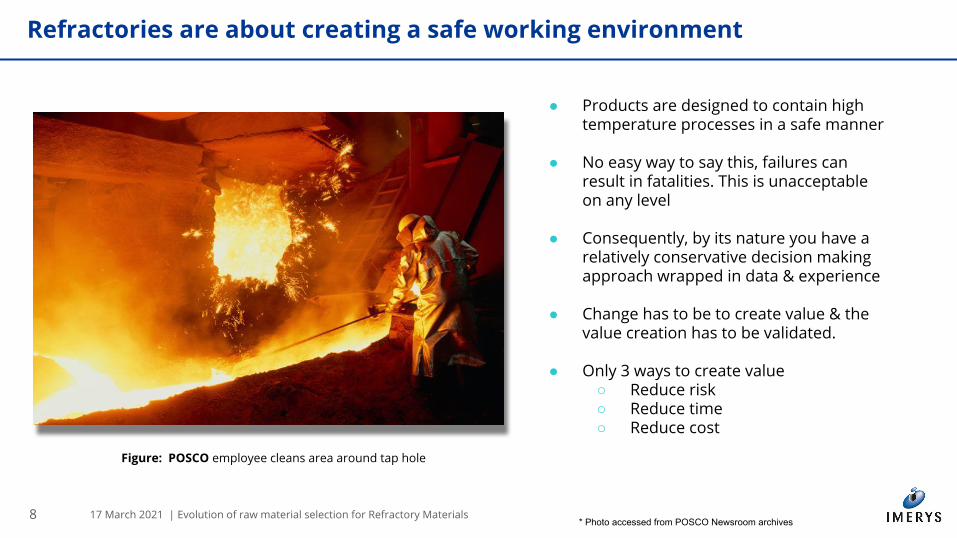

* Photo accessed from POSCO Newsroom archives

Figure: POSCO employee cleans area around tap hole

17 March 2021 | Evolution of raw material selection for Refractory Materials 9

● Refractories are a High Visibility cost

○ Refractories represent a relatively low portion of plant production costs

○ But represent high proportion of ‘impactable’ costs that the local teams can have on the total running costs.

● Optimal solutions targeting specific needs of the decision maker

○ Innovator: Reduce down-time / faster return to service■ Brick > Casting > Dry Gunning > Wet Shotcreting ■ Time to install / return to service / economies of scale

○ Curator: Managing price & risk ■ Better matching of available reserves with applications■ Upgrading of downgrading RM necessary when

adapting solutions■ Inclusion of recycled materials / balancing cost & usage

Refractory solutions have been driven to create value through understanding of customer needs

17 March 2021 | Evolution of raw material selection for Refractory Materials 10

● Cannot replace a bauxite brick with bauxite castable ○ Monolithic binders increase shrinkage○ Require compensation aggregate or upgrade material

● Shortage of bauxite combined with upgrade necessary has

seen an significant increase in Tabular Alumina capacity○ Flow on into global markets for WFA & Tabular

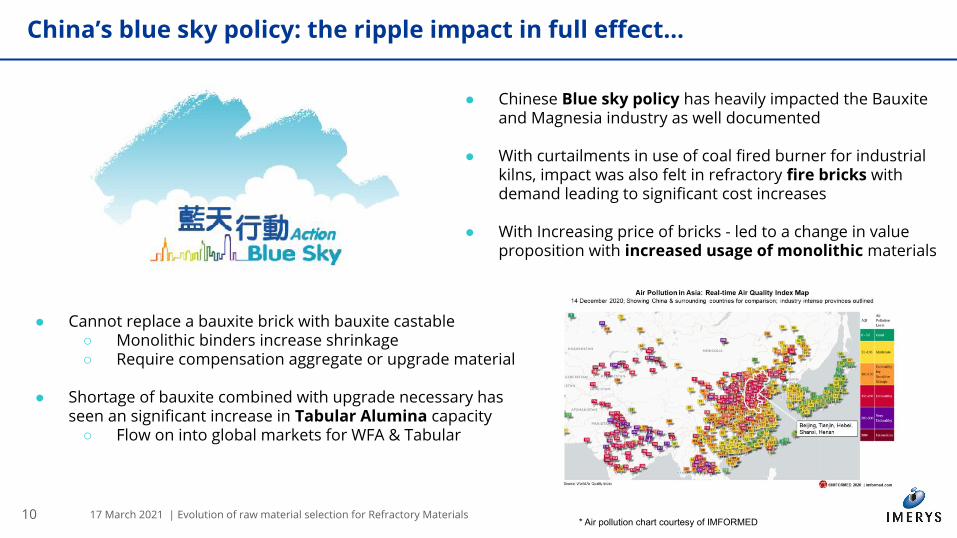

China’s blue sky policy: the ripple impact in full effect...

● Chinese Blue sky policy has heavily impacted the Bauxite and Magnesia industry as well documented

● With curtailments in use of coal fired burner for industrial kilns, impact was also felt in refractory fire bricks with demand leading to significant cost increases

● With Increasing price of bricks - led to a change in value proposition with increased usage of monolithic materials

* Air pollution chart courtesy of IMFORMED

17 March 2021 | Evolution of raw material selection for Refractory Materials 11

Potential external influences on the ‘optimal solution’ for refractories are widespread & considerable

● The committed road map of global steel makers to ‘net zero’ or similar targets as announced by ArcelorMittal

○ Move to EAF furnaces away from traditional Blast Furnace○ Return of DRI processes with hydrogen / alternate fuels

● Electrification of Vehicles industry with targets in China & EU○ Reduced dependence on Internal combustion engines ○ Flow on to sub-segments (investment casting) for

turbo-chargers and other specialty products.

● Portland Cement targets to reduce emissions○ Alternative fuels / hydrogen mix ○ Electrification of kilns and processes

17 March 2021 | Evolution of raw material selection for Refractory Materials 12

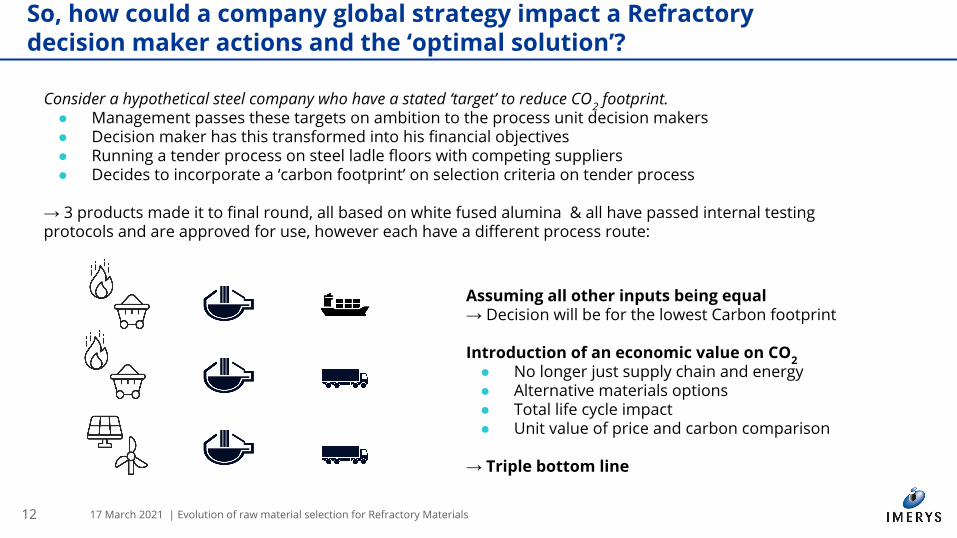

So, how could a company global strategy impact a Refractory decision maker actions and the ‘optimal solution’?

Consider a hypothetical steel company who have a stated ‘target’ to reduce CO2 footprint. ● Management passes these targets on ambition to the process unit decision makers ● Decision maker has this transformed into his financial objectives ● Running a tender process on steel ladle floors with competing suppliers● Decides to incorporate a ‘carbon footprint’ on selection criteria on tender process

→ 3 products made it to final round, all based on white fused alumina & all have passed internal testing protocols and are approved for use, however each have a different process route:

Assuming all other inputs being equal → Decision will be for the lowest Carbon footprint

Introduction of an economic value on CO2 ● No longer just supply chain and energy ● Alternative materials options ● Total life cycle impact ● Unit value of price and carbon comparison

→ Triple bottom line

17 March 2021 | Evolution of raw material selection for Refractory Materials 13

Evolution of Raw Material Selection

Applications & Material Selection

External market forces and impact

The next lines of raw materials The next lines of raw materials

17 March 2021 | Evolution of raw material selection for Refractory Materials 14

Our ambition is simple: we want to unlock the sustainable potential of minerals

As the world’s leading supplier of mineral-based specialty solutions, the technical expertise and innovative mindset of our people enable us to extract and transform minerals responsibly and in a sustainable way over the long term.

In full alignment with the UN Global Compact Principles and contributing concretely to 9 of the UN Sustainable Development Goals.

3 GOOD HEALTH AND WELL-BEING 5 GENDER

EQUALITY 4 QUALITY EDUCATION 6 CLEAN WATER

AND SANITATION 8 DECENT WORK AND ECONOMIC GROWTH

12 RESPONSIBLE CONSUMPTION AND PRODUCTION

13 CLIMATE ACTION 15 LIFE

ON LAND 16 PEACE JUSTICE AND STRONG INSTITUTIONS

17 March 2021 | Evolution of raw material selection for Refractory Materials 15

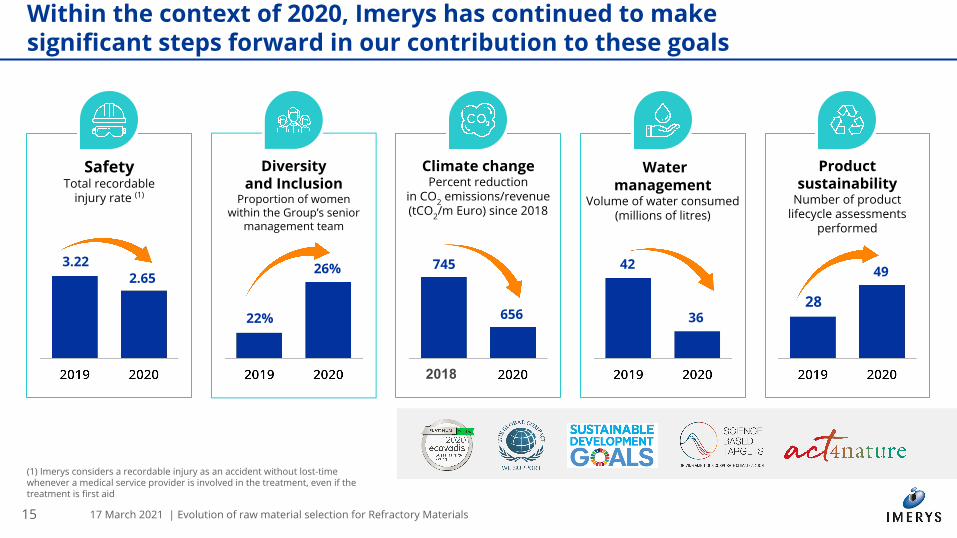

Within the context of 2020, Imerys has continued to make significant steps forward in our contribution to these goals

(1) Imerys considers a recordable injury as an accident without lost-time whenever a medical service provider is involved in the treatment, even if the treatment is first aid

SafetyTotal recordable

injury rate (1)

Diversity and Inclusion

Proportion of women within the Group’s senior

management team

Climate changePercent reduction

in CO2 emissions/revenue (tCO2/m Euro) since 2018

Water management

Volume of water consumed (millions of litres)

Product sustainability

Number of product lifecycle assessments

performed

3.222.65

22%

26% 745

656

42

3628

49

2018

17 March 2021 | Evolution of raw material selection for Refractory Materials 16

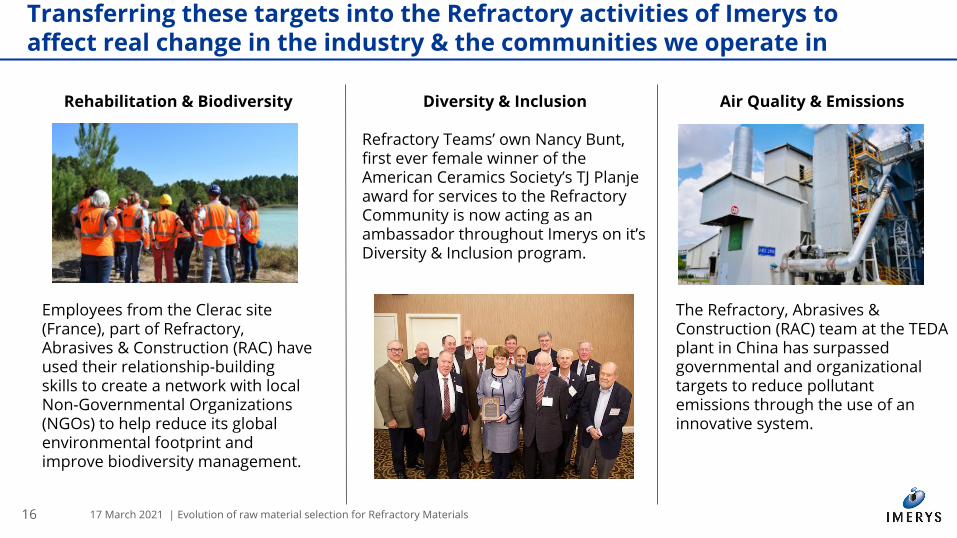

Rehabilitation & Biodiversity

Employees from the Clerac site (France), part of Refractory, Abrasives & Construction (RAC) have used their relationship-building skills to create a network with local Non-Governmental Organizations (NGOs) to help reduce its global environmental footprint and improve biodiversity management.

Transferring these targets into the Refractory activities of Imerys to affect real change in the industry & the communities we operate in

Air Quality & Emissions

The Refractory, Abrasives & Construction (RAC) team at the TEDA plant in China has surpassed governmental and organizational targets to reduce pollutant emissions through the use of an innovative system.

Diversity & Inclusion

Refractory Teams’ own Nancy Bunt, first ever female winner of the American Ceramics Society’s TJ Planje award for services to the Refractory Community is now acting as an ambassador throughout Imerys on it’s Diversity & Inclusion program.

17 March 2021 | Evolution of raw material selection for Refractory Materials 17

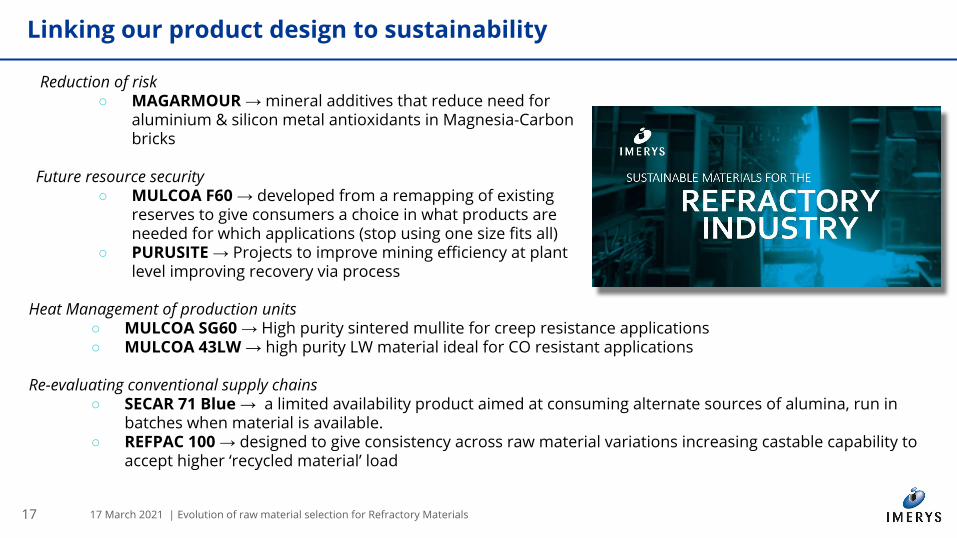

Reduction of risk ○ MAGARMOUR → mineral additives that reduce need for

aluminium & silicon metal antioxidants in Magnesia-Carbon bricks

Future resource security ○ MULCOA F60 → developed from a remapping of existing

reserves to give consumers a choice in what products are needed for which applications (stop using one size fits all)

○ PURUSITE → Projects to improve mining efficiency at plant level improving recovery via process

Linking our product design to sustainability

Heat Management of production units ○ MULCOA SG60 → High purity sintered mullite for creep resistance applications○ MULCOA 43LW → high purity LW material ideal for CO resistant applications

Re-evaluating conventional supply chains○ SECAR 71 Blue → a limited availability product aimed at consuming alternate sources of alumina, run in

batches when material is available. ○ REFPAC 100 → designed to give consistency across raw material variations increasing castable capability to

accept higher ‘recycled material’ load

17 March 2021 | Evolution of raw material selection for Refractory Materials 18

Continue to invest our reserves and operations to push the transition to a low carbon future

● Business Group road map introduced in 2020 targeting a 36% reduction in CO2

footprint across Fused, Sintering & Calcination assets by 2030.

● Have 6 active projects across multiple regions in Solar Energy that are due for commissioning in 2022, targeting reduction of 7.4 kt /CO2 per annum

● Have invested over 10M USD in process technologies for alternative energy burners for rotary kilns allowing for variable energy mix

● Long term innovation projects to remap refractory binders to zero emission processes

“We must relook at our CAPEX projects and re-evaluate based on metrics that include reducing our CO2

Footprint” Alessandro Dazza

17 March 2021 | Evolution of raw material selection for Refractory Materials 19

Continue to invest our operations to push the transition to a low carbon future

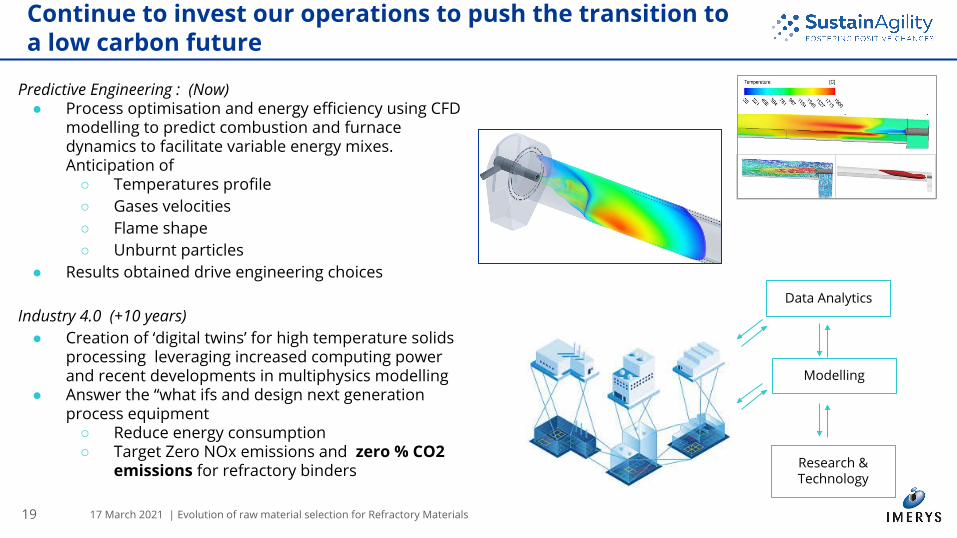

Predictive Engineering : (Now)● Process optimisation and energy efficiency using CFD

modelling to predict combustion and furnace dynamics to facilitate variable energy mixes. Anticipation of

○ Temperatures profile○ Gases velocities○ Flame shape○ Unburnt particles

● Results obtained drive engineering choices

Industry 4.0 (+10 years)● Creation of ‘digital twins’ for high temperature solids

processing leveraging increased computing power and recent developments in multiphysics modelling

● Answer the “what ifs and design next generation process equipment

○ Reduce energy consumption○ Target Zero NOx emissions and zero % CO2

emissions for refractory binders

Data Analytics

Research & Technology

Modelling

17 March 2021 | Evolution of raw material selection for Refractory Materials 20

Summary & Conclusions

17 March 2021 | Evolution of raw material selection for Refractory Materials 21

● Refractory customers have in a way by necessity been the first adopters of the circular economy, with efforts to reuse and consume less, this has been at the heart of the ‘optimal solution’ in terms of economic value before it became more broadly known.

● Refractory Producers, as solution providers that tailor their offer to their customers needs, are seeing increasing consumer awareness and targets for the whole value chain around CO2 footprints, creating a new variable to the evaluation process.

● History has proven that changes in political & social landscape impact the value proposition for refractory products and will have an impact on the ‘optimal solution’

○ Historically with labour costs & Installation methodology ○ How raw materials are used and consumed geographically; and now ○ Supply chain and process methodology of those raw materials

● As a company, and specifically within the Refractory team, Imerys are aligning our innovation efforts within our plants, processes and products to meet the challenges of our broader society. To deliver refractory raw materials that are sustainable and offer the most flexibility to our customers to achieve the ‘optimal solution’

Summary & Conclusion

17 March 2021 | Evolution of raw material selection for Refractory Materials 22

Thank you for your attention

@imerys

Visit www.imerys.com for more information.

Or connect with us:

www.linkedin.com/company/imerys/

www.facebook.com/imerysgroup/