Embed Size (px)

Citation preview

MARKETPLACE HOUSING and COMMERCIAL IMPACT ASSESSMENT

City of Wyoming Village of Lockland

April 2008

by

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 2

INTRODUCTION

The following is a comprehensive Commercial Impact and Marketplace Housing Assessment compiled for the marketplace surrounding the City of Wyoming and the Village of Lockland. The market-based analysis was conducted utilizing com-mercial data gathered on competitive projects in the proposed trade area, recorded commercial inventory and activity,

and specific household demographics, residential transfers, and expenditure data to estimate future space demands, po-tential for development, and trends in the marketplace.

Scope of Assessment Page 3 Definitions Page 4

City of Wyoming Master Plan Page 5 Professional Observations Page 6

Commercial Impact Analysis Page 7 Commercial Trade Areas Page 8

Retail Trade Area Overview Page 9-11 Office Market Assessment Page 12-14 Retail and Office Findings Page 15

Marketplace Housing Assessment Page 16 Marketplace Search Areas Page 17-18 Household Demographic Data Page 19-24

Housing Market Performance Page 25-27 Professional Recommendations Page 28-31

Confidentiality and Disclaimers Page 32

TABLE of CONTENTS

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 3

SCOPE OF ASSESSMENT

The Village of Lockland and the City of Wyoming have joined forces to better understand their development potential. Both municipalities share Business Districts located along Wyoming Avenue and extending from State Route 4 in Wyo-ming eastward into Lockland, past Interstate 75 and beyond. With a desire to fully understand the current residential

and commercial real estate market conditions, Wyoming and Lockland have engaged Property Advisors to provide the Scope of Services outlined below:

Marketplace Housing Study. The Marketplace Housing Study will identify and measure the household profiles, consumer buying

power and market depth of the City of Wyoming, Village of Lockland and surrounding housing markets (Demographic Areas) based upon 2007 U.S. Census data. Consultant will also gather information on recorded housing transfers of all types within the same competitive housing market (Search Area) over the last three years. The analysis intends to reveal specific housing trends,

unserved housing needs and development or redevelopment opportunities.

� Current year household demographic data within the Demographic Areas and select surrounding cities, as agreed by Client

and Consultant, in both tabular form and then geographically mapped for relevant metrics by US Census block group.

� Current year psychographic lifestyle segmentation data within the same Demographic Areas and the same select sur-

rounding cities in both tabular form and then mapped for dominant segments by US Census block group.

� Trends and analyses of all recorded housing transfer activity within the Search Area for the prior three years, sorted by

major neighborhood or subdivisions, home product type, sales price and sales date. Professional and market-comparative conclusions into the Search Area’s depth and character of current housing stock, housing performance, and expected

housing market potential.

� Professional recommendations on any and all unserved and underserved housing market positions by product and mix,

with suggested price points. Executive Summary of these findings.

Commercial Impact Study. To optimize these preparations and launch a positive economic spiral for the City and Village, Con-sultant will conduct a feasibility study of each commercial property type and incorporate the impact of additional residential devel-

opment for the City and Village, plus its surrounding communities. In addition, Consultant will conduct an overall competitive analysis to optimize the overall redevelopment strategy.

� Supply and demand analysis of all retail, office and restaurant product within identified, relevant trade areas.

� Professional recommendations on market absorption of retail, office and restaurant product, including recommended lease

rates and tenant finish allowances.

� Identification of retail and office shortfalls by category in the same relevant trade areas, taking into account the concentra-

tion of current year psychographic lifestyle segments found in the Marketplace Housing Study.

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 4

Housing Search Area Housing activity and housing demand were analyzed within the Search Area by collecting housing transfer data of

the surrounding the cities, or areas of Wyoming, Lockland, Finneytown, Woodlawn, and Lincoln Heights.

Immediate Trade Area (ITA) The ITA was used for the Commercial Impact Analysis and encompasses a 1-mile radius around the center point

(CP) of Oak and Wyoming Avenues. This considers the supply and potential demand within the trade area, and

encompasses both Wyoming’s and Lockland’s Business Districts. Primary Trade Area (PTA):

The PTA encompasses a 3-mile radius around the CP. This area inventories competitive supply and commercial demand potentially captured by the Wyoming and Lockland primary market area.

Secondary Trade Area (STA):

The STA was also captured for purposes of commercial supply and demand, which encompasses the PTA and ITA in their entirety, and extends further to include a 6-mile radius from the CP.

Cincinnati-Middletown Metropolitan Statistical Area (MSA):

The MSA represents the larger regional population, and contains the following counties: Butler, Warren, Hamilton, Clermont, and Brown (Ohio); Boone, Kenton, Campbell, Gallatin, Grant, Pendleton, and Bracken (Kentucky); Franklin, Dearborn, and Ohio (Indiana).

Mixed-Use: A development, within one or several buildings, that combines at least three significant revenue-producing uses

that are physically and functionally integrated and developed in conformance with a coherent plan.

The following product types are analyzed within this report:

Residential: Property used primarily as a place to live. Retail: Property used by a retail business for the sale of merchandise or services.

Restaurant: Place where meals are served to the public. Office: Building used exclusively or primarily for office use, as opposed to manufacturing, warehousing, or other uses.

ASSESSMENT DEFINITIONS

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 5

The market “canvas” for our analyses was the established and progressive City of Wyoming Master Plan, an elegant concentration of real estate

assets that was launched by the City to establish Zones of Potential Change, preservation, and conservation.

North Pike Zone is home to the Wyoming Recreation Center, and also hosts the retail and grocery destinations where many Wyoming residents shop

and bank. Many of the retail choices are actually located in Woodlawn. There are few retail shops in Wyoming in the North Pike Zone, one that may come available for redevelopment in the future.

The Promenade is a small strip of retail stores and cafes at the corner of Wyoming Avenue and Springfield Pike. It serves as the entryway into the

Business District located in the City Center. South Pike Zone is located in Springfield Township.

This zone boasts retail and consumer service centers that cater to Wyoming residents as well as those from Springfield Township.

The City Center is a mixed-use area of town that affords boutique retail and restaurants, homes on smaller lots and apartment buildings atop retail in

both Wyoming and Lockland. Lockland’s street layout and zoning is very similar to that of Wyoming’s, however, property owners have not maintained the buildings over the years, creating a visually eroded

look of Lockland’s share of the Business District. As noted by the green boundaries at left, some of the

Zones of Potential Change are located outside Wyoming City limits. Purposefully drawn in this manner, Wyoming realizes

that initial investment in the neighboring areas would likely sustain their community health for years to come.

City of Wyoming Master Plan—Zones of Potential Change

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 6

� There is today a high concentration of affluent and lifestyle driven households in the City of Wyoming,

characterized by larger homes and families, higher-paying jobs in more distant employment centers with longer com-mutes, and overall superior household buying power for a range of goods, services and experiences.

� The housing market in Wyoming remains strong, but is lacking single-family attached product at the en-

try-level, upscale price range of $200,000 to $300,000. For-sale attached housing product is vital to creating a vibrant mixed-use town center, although there remains a paucity of attached housing choices. From our experience, we believe that sustainable town centers are driven by the diversity of their residential components and choices be-cause they help to attract diverse residents that will sustain a community’s health over time.

� The Village of Lockland shows high-earning residents seemingly unserved by Lockland’s current housing stock. This

demonstrates that Lockland has potential to offer new and higher valued housing stock to cater to these households, and potentially attract more to the area.

� Lockland has the potential to offer neighborhood serving retail that would cater to the needs of residents

near its Business District. Lockland’s challenge lies within its ability to offer a genuine “place” that provides the quality of lifestyle many contributing households seek. Without this, their current residents must travel outside the Village to find this experience in other communities.

� Both the Village of Lockland and the City of Wyoming offer very limited retail options. Because of this, we see a

strong amount of retail leakage into surrounding communities. Retail dollars spent by residents from Wyo-ming and Lockland are spent in communities such as Finneytown (Springfield Township), Woodlawn and Hartwell. Wyoming and Lockland should collaborate in thought and resources to provide options that cater to their residents

needs and allow them to invest into their own communities.

� Our Commercial Impact Analysis has found that the immediate submarkets of Wyoming and Lockland

currently have the demand necessary to support new office and retail commercial space. Household demo-graphic and other commercial market factors reveal that 200,000 SF of office, and 250,000 SF of retail could be ab-

sorbed by Lockland and Wyoming over the next five years. With the proper development design and strategy, these commercial offerings would not only cater to the household consumers looking for convenient shopping options, but also to the consumers looking for a shopping and entertainment lifestyle experience.

� This additional commercial demand within Wyoming and Lockland must be strategically located within the community.

A development strategy should be launched through the combined efforts of Lockland and Wyoming in order to balance and maximize community impact and spur additional economic activity.

Property Advisors believes a strong market understanding combined with traditional planning and physical analysis will lead to powerful, economically driven and sustainable development strategies.

PROFESSIONAL MARKET OBSERVATIONS

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 7

COMMERCIAL IMPACT ASSESSMENT City of Wyoming

Village of Lockland

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 8

The City of Wyoming and Village of Lockland’s com-mercial environment is impacted by activity beyond their boundaries. To capture the data that represents

those areas, Property Advisors selected the intersec-tion of Oak and Wyoming Avenues as this assess-ment’s center point (CP) shown as the red star at left. Also shown in color shades are Wyoming, Lockland,

Woodlawn, Lincoln Heights and Finneytown. From the CP, three distinct Trade Areas were established as the Immediate, Primary and Secondary Trade Areas.

These areas are defined as follows: IMMEDIATE TRADE AREA (ITA) The Immediate Trade Area represents a one-mile ra-

dius from the center point and incorporates the most relevant demand for the City of Wyoming and Village of Lockland, shown in dark blue.

PRIMARY TRADE AREA (PTA) The Primary Trade Area encompasses the ITA and ex-tends the radius three miles from the center point. The

PTA includes the additional Villages of Woodlawn and Glendale, plus a large portion of Springfield Township, shown in blue.

SECONDARY TRADE AREA (STA) The Secondary Trade Area encompasses both the ITA

and STA, extending six miles form the center point. This STA captures the majority of the commercial in-ventory in the Cincinnati MSA, including the submar-kets of Kenwood, Blue Ash, Tri County and Norwood,

shown in light blue.

Property Advisors examined the commercial inventory, competitive projects, and other relevant market fac-tors within these Areas to measure the possible com-

mercial space that could be supported in the combined Wyoming and Lockland community. By examining the commer-cial environments of the ITA, PTA, and STA, Property Advisors is better able to gauge the impact of new commercial de-velopment and the potential market demand in the City of Wyoming and Village of Lockland.

COMMERCIAL TRADE AREA OVERVIEW

Wyoming-Lockland CP

Cincinnati cityCincinnati cityCincinnati cityCincinnati cityCincinnati city

Amberley villageAmberley villageAmberley villageAmberley villageAmberley village

Arlington Heights villageArlington Heights villageArlington Heights villageArlington Heights villageArlington Heights village

Blue Ash cityBlue Ash cityBlue Ash cityBlue Ash cityBlue Ash city

Deer Park cityDeer Park cityDeer Park cityDeer Park cityDeer Park city

Dillonvale CDPDillonvale CDPDillonvale CDPDillonvale CDPDillonvale CDP

Elmwood Place villageElmwood Place villageElmwood Place villageElmwood Place villageElmwood Place village

Evendale villageEvendale villageEvendale villageEvendale villageEvendale village

Fairfax villageFairfax villageFairfax villageFairfax villageFairfax village

Finneytown CDPFinney town CDPFinneytown CDPFinneytown CDPFinneytown CDP

Forest Park cityForest Park cityForest Park cityForest Park cityForest Park city

Glendale villageGlendale villageGlendale villageGlendale villageGlendale village

Golf M anor villageGolf M anor villageGolf M anor villageGolf M anor villageGolf M anor village

Greenhills villageGreenhills villageGreenhills villageGreenhills villageGreenhills village

Groesbeck CDPGroesbeck CDPGroesbeck CDPGroesbeck CDPGroesbeck CDP

Kenwood CDPKenwood CDPKenwood CDPKenwood CDPKenwood CDP

Lincoln Heights villageLincoln Heights villageLincoln Heights villageLincoln Heights villageLincoln Heights village

M adeira cityM adeira cityM adeira cityM adeira cityM adeira cityM onfort Heights East CDPM onfort Heights East CDPM onfort Heights East CDPM onfort Heights East CDPM onfort Heights East CDP

M onfort Heights South CDPM onfort Heights South CDPM onfort Heights South CDPM onfort Heights South CDPM onfort Heights South CDP

M ount Healthy cityM ount Healthy cityM ount Healthy cityM ount Healthy cityM ount Healthy city

M ount Healthy Heights CDPM ount Healthy Heights CDPM ount Healthy Heights CDPM ount Healthy Heights CDPM ount Healthy Heights CDP

Northbrook CDPNorthbrook CDPNorthbrook CDPNorthbrook CDPNorthbrook CDP

North College Hill cityNorth College Hill cityNorth College Hill cityNorth College Hill cityNorth College Hill city

Northgate CDPNorthgate CDPNorthgate CDPNorthgate CDPNorthgate CDP

Norwood cityNorwood cityNorwood cityNorwood cityNorwood city

Pleasant Run CDPPleasant Run CDPPleasant Run CDPPleasant Run CDPPleasant Run CDP

Pleasant Run Farm CDPPleasant Run Farm CDPPleasant Run Farm CDPPleasant Run Farm CDPPleasant Run Farm CDP

Reading cityReading cityReading cityReading cityReading city

St. Bernard citySt. Bernard citySt. Bernard citySt. Bernard citySt. Bernard city

Sharonville citySharonville citySharonville citySharonville citySharonville city

Silverton citySilverton citySilverton citySilverton citySilverton city

Sp ringdale citySpringdale citySp ringdale citySp ringdale citySp ringdale city

White Oak CDPWhite Oak CDPWhite Oak CDPWhite Oak CDPWhite Oak CDP

White Oak East CDPWhite Oak East CDPWhite Oak East CDPWhite Oak East CDPWhite Oak East CDP

Woodlawn villageWoodlawn villageWoodlawn villageWoodlawn villageWoodlawn village

Wyoming cityWy oming cityWy oming cityWy oming cityWy oming city

Bu t

ler

Wa

r re n

Rd

But

ler

Wa

rren

Rd

Bu t

ler

Wa r

r en

Rd

Bu

tler

Wa

rren

Rd

Bu t

ler

Wa

rren

Rd

North Bend RdNorth Bend RdNorth Bend RdNorth Bend RdNorth Bend Rd

E Fork Ave

E Fork Ave

E Fork Ave

E Fork Ave

E Fork AveHopkins Ave

Hopkins Ave

Hopkins Ave

Hopkins Ave

Hopkins Ave

Del

ta A

veD

elta

Av e

Del

t a A

veD

elt a

Ave

Del

t a A

ve

Edw

ard

s R

dE

dwa

rds

Rd

Edw

ard

s R

dE

dw

ard

s R

dE

dwa

rds

Rd

Fleming RdFleming RdFleming RdFleming RdFleming RdSmalley RdSmalley RdSmalley Rd

Smalley RdSmalley Rd

Compton RdCompton RdCompton RdCompton RdCompton Rd Spooky H

ollow Rd

Spooky Hollow Rd

Spooky Hollow R

d

Spooky Hollow Rd

Spooky Hollow Rd

W Galbraith RdW Galbraith RdW Galbraith RdW Galbraith RdW Galbraith Rd

Blo

me

Rd

Blo

me

Rd

Blo

me

Rd

Blo

me

Rd

Blo

me

Rd

Section RdSection RdSection RdSection RdSection Rd Section RdSection RdSection RdSection RdSection Rd

Center H

ill Ave

Center H

ill Ave

Center H

ill Ave

Center H

ill Ave

Center H

ill Ave

Car

thag

e A

veC

arth

age

Ave

Car

thag

e A

veC

arth

age

Ave

Car

thag

e A

ve

Spring Grove Ave

Spring Grove Ave

Spring Grove Ave

Spring Grove Ave

Spring Grove Ave

E Mitchell Ave

E Mitchell Ave

E Mitchell Ave

E Mitchell Ave

E Mitchell AveWoolper AveWoolper AveWoolper AveWoolper AveWoolper Ave

Murray Ave

Murray AveMurray Ave

Murray Ave

Murray AveWasson RdWasson RdWasson RdWasson RdWasson Rd

Chu

rch

St

Chu

rch

St

Chu

rch

St

Chu

rch

St

Chu

rch

St

W Crescentville RdW Crescentville RdW Crescentville RdW Crescentville RdW Crescentville Rd

Crescentville RdCrescentville RdCrescentville RdCrescentville RdCrescentville RdFields Ertel RdFields Ertel RdFields Ertel RdFields Ertel RdFields Ertel Rd

W Sharon RdW Sharon RdW Sharon RdW Sharon RdW Sharon Rd

Woodford RdWoodford RdWoodford RdWoodford RdWoodford Rd

Woodridge Blvd

Woodridge Blvd

Woodridge BlvdWoodridge Blvd

Woodridge BlvdRo s

s R

dR

oss

Rd

Ros

s R

dR

oss

Rd

Ros

s R

d

Dimmick RdDimmick RdDimmick RdDimmick RdDimmick Rd

W North Bend RdW North Bend RdW North Bend RdW North Bend RdW North Bend Rd

Resor RdResor RdResor RdResor RdResor Rd

Clif

t on

Ave

Cli f

ton

Ave

Clif

t on

Ave

Clif

t on

Ave

Clif

t on

Ave Erie

Ave

Erie

Ave

Erie

Ave

Erie

Ave

Erie

Ave

Mill

Rd

Mil l

Rd

Mill

Rd

Mill

Rd

Mill

Rd

W Kemper RdW Kemper RdW Kemper Rd

W Kemper RdW Kemper Rd

Re a

din

g R

dR

ead

ing

Rd

Rea

din

g R

dR

ead i

ng

Rd

Rea

din

g R

d

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Glendale Milford RdGlendale Milford RdGlendale Milford RdGlendale Milford RdGlendale Milford Rd

Summ

it Rd

Summ

it Rd

Summ

it Rd

Summ

it Rd

Summ

it Rd

Euclid AveEuclid AveEuclid AveEuclid AveEuclid Ave

Highland AveHighland AveHighland AveHighland Ave

Highland Ave

Putz PlPutz PlPutz PlPutz PlPutz Pl

Montana Ave

Montana Ave

Montana Ave

Montana Ave

Montana Ave

Dana AveDana AveDana AveDana AveDana Ave

Hopple StHopple StHopple StHopple StHopple St

Pla

infie

ld R

dP

lain

field

Rd

Pla

infie

ld R

dP

lain

field

Rd

Pla

infie

ld R

d

E Galbraith Rd

E Galbraith Rd

E Galbraith Rd

E Galbraith Rd

E Galbraith Rd

Madison Rd

Madison R

d

Madison Rd

Madison Rd

Madison Rd

Beekm

an St

Beekm

an St

Beekm

an St

Beekm

an St

Beekm

an St

Struble RdStruble RdStruble RdStruble RdStruble Rd

Win

ton

Rd

Win

ton

Rd

Win

ton

Rd

Win

ton

Rd

Win

ton

Rd

Losantiville AveLosantiville AveLosantiville AveLosantiville AveLosantiville Ave

Euclid RdEuclid RdEuclid RdEuclid RdEuclid Rd

ITA

PTA

STA

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 9

TRADE AREA RETAIL INVENTORY The Retail Assessment was conducted by analyzing these three Trade Areas, with a summary of the Trade Area inven-

tory listed below. Unless considered significant, retail projects under 5,000 SF and those built before 1980 were not considered in the inventory*.

* A list of the Retail inventory within the Trade Areas will be found in the Addendum of a full Assessment Report upon request.

ITA Inventory Summary: Retail

� Total Space: 150,000 SF

� Majority of space is located on

Wyoming Avenue

� Current Vacancy: 14%

Restaurant

� Total Space: 32,000 SF

� Current Vacancy: 11%

� Planned Space: none

PTA Inventory Summary: Retail

� Total Space: 2,495,000 SF

� Current Vacancy: 10%

� Majority of space is located along

Reading Road/Winton Road

Restaurant

� Total Space: 110,000 SF

� Current Vacancy: 8%

� Planned Space: none

STA Inventory Summary: Retail

� Total Space: 9,620,000 SF

� Current Vacancy: 12%

� Comprises the commercial submar-

kets of Kenwood, Blue Ash, Tri

County and Norwood.

COMMERCIAL IMPACT ANALYSIS — RETAIL MARKET ASSESSMENT, continued.

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 10

GREATER CINCINNATI RETAIL MARKET OVERVIEW The findings and conclusions of our supply and demand analysis within the Primary and Secondary Trade Areas are

shown in the next few pages. Beginning with a review of the Retail Market Assessment, we examined the Greater Cincin-nati Submarket Statistics found in the graph below.

Greater Cincinnati Market Retail vacancy in Greater Cincinnati was at 10% with an average lease rate of $12.29/SF per year at mid-year 2007. The retail market for the entire metropolitan area has been solid and we believe the demand sustained should keep the

region relatively healthy for the foreseeable future. Tri-County Submarket The Immediate, Primary, and Secondary Trade Areas are a part of the submarket listed above as the Tri-County submar-

ket. This submarket is inline with the overall Greater Cincinnati Market with respect to vacancy and performs slightly better than the overall market in lease rates. The Tri-County vacancy rates fall just above 10% and the net lease rates reach $13.63.

Source: CB Richard Ellis Marketview Mid-year 2007

COMMERCIAL IMPACT ANALYSIS — RETAIL MARKET ASSESSMENT, continued.

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 11

DETERMINANTS OF RETAIL DEMAND: Property Advisors considers key market, demographic, and sales factors when conducting a Supply and Demand Analysis

for Retail. Key factors that help to determine demand are listed below. Household Income:

� Immediate Trade Area Average household income: $64,314

� Primary Trade Area Average household income: $60,334

� Secondary Trade Area Average household income: $54,142

Household Growth:

� ITA expected growth over the next 5 years -6.13%

� PTA expected growth over the next 5 years -4.43%

� STA expected growth over the next 5 years -4.49%

Spending Habits:

� Average household income spent on Retail items 36%

� Retail dollars spent in shopping centers 85%

� Retail dollars spent in community shopping centers 54%

� Average household income spent on Food Outside of the Home 15%

Sale per Square Foot:

� Average sales per square foot for neighborhood shopping retail $275—$375

� Average sales per square foot for restaurant space $200—$350

Frictional Vacancy:

� A healthy frictional vacancy is estimated as 10% of the current vacancy that will be filled from new demand.

� Current space and planned competitive space are also considered.

Capture Rate:

� A Capture Rate, subjective to market conditions, is used to determine the estimated percentage of total de-

mand within a targeted market segment that a proposed project would be expected to attract.

COMMERCIAL IMPACT ANALYSIS — RETAIL MARKET ASSESSMENT

The supply and de-mand analysis was

conducted for all three of the trade areas and

based upon a five year model.

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 12

TRADE AREA OFFICE INVENTORY The Retail Assessment was conducted by analyzing these same three Trade Areas, with a summary of the Trade Area in-

ventory listed below. Unless considered significant, retail projects under 5,000 SF and those built before 1980 were not considered in the inventory*.

* A list of the Office inventory within the Trade Areas will be found in the Addendum of a full Assessment Report upon request.

ITA Inventory Summary: Office

� Total space: 115,000 SF

� Current vacancy: 10%

� The majority of the projects are lo-

cated within the Springfield Pike

corridor

PTA Inventory Summary: Office

� Total Space: 2,140,000 SF

� Current vacancy: 18%

� The majority of the projects are un-

der 10,000 SF

STA Inventory Summary: Office

� Total Space: 13,150,000 SF

� Current vacancy: 23%

� Over 300,000 SF currently under

construction

COMMERCIAL IMPACT ANALYSIS — OFFICE MARKET ASSESSMENT, continued.

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 13

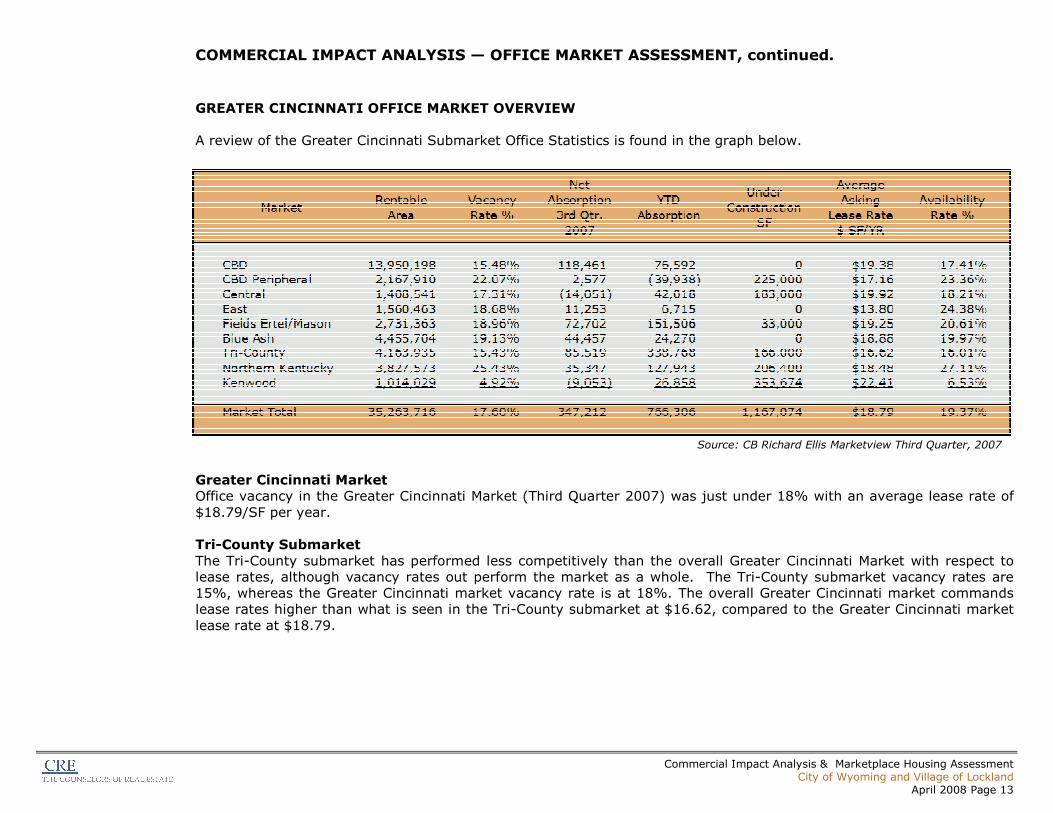

GREATER CINCINNATI OFFICE MARKET OVERVIEW A review of the Greater Cincinnati Submarket Office Statistics is found in the graph below.

Greater Cincinnati Market Office vacancy in the Greater Cincinnati Market (Third Quarter 2007) was just under 18% with an average lease rate of

$18.79/SF per year. Tri-County Submarket

The Tri-County submarket has performed less competitively than the overall Greater Cincinnati Market with respect to lease rates, although vacancy rates out perform the market as a whole. The Tri-County submarket vacancy rates are 15%, whereas the Greater Cincinnati market vacancy rate is at 18%. The overall Greater Cincinnati market commands lease rates higher than what is seen in the Tri-County submarket at $16.62, compared to the Greater Cincinnati market

lease rate at $18.79.

Source: CB Richard Ellis Marketview Third Quarter, 2007

COMMERCIAL IMPACT ANALYSIS — OFFICE MARKET ASSESSMENT, continued.

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 14

DETERMINANTS OF OFFICE DEMAND: Property Advisors considers key market, demographic and employment factors when conducting a Supply and Demand

Analysis for office development. Key office demand is driven by: Total Employment Growth:

The Cincinnati-Middletown MSA is forecasted to grow by approximately 50,000 jobs (2007-2012), according to the

Bureau of Labor Statistics.

Office Employment: Based on the Bureau of Labor Statistics Standard Occupation Classification (SOC) categories, the percentage of office employment in the Cincinnati-Middletown MSA is estimated at 45%.

Space per Worker:

The amount of space per office worker varies according to industry. For our analysis, the amount of space is esti-mated at 150—250 SF per employee. This estimate is based upon employment and current available office space

within Trade Areas.

Trade Area Capture Rate: The Trade Areas are estimated to capture 5% to 50% of space required by new Office workers within the Cincin-nati-Middletown MSA. This estimate is based on the total jobs within the Cincinnati-Middletown MSA currently be-ing captured by the Trade Areas.

Existing Vacant Space:

The office market assessment assumes that only a portion, 10% of the current vacant office space, will be filled from new demand.

Planned Space: The majority of planned competitive office space is assumed to be occupied.

COMMERCIAL IMPACT ANALYSIS — OFFICE MARKET ASSESSMENT

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 15

After considering the relevant market and demographic factors that help to determine supply and demand, a forecast of Trade Area market absorption can be found below:

SUMMARY OF COMMERCIAL DEMAND: With an assessment of the determinants of demand, 525,000 to 725,000 square feet of commercial space could be absorbed over the next five years by the City of Wyoming and Village Of Lockland, an average of 105,000-145,000

square feet per year.

In this analysis, the largest amount of demand in each product is found within the Secondary Trade Area. The lowest amount of commercial demanded is found within the Immediate area of Wyoming and Lockland.

Given the number of affluent households within the trade areas, the significant demand for commercial space is not un-expected. The lack of viable commercial space within the Immediate Trade Area, in addition to residents’ high disposable incomes, have generated “leakage” of retail dollars spent in outside communities. The City of Wyoming and Village of

Lockland have an opportunity to recapture a share of this “leakage” through sustainable commercial development oppor-tunities which exist in both of the communities. There is potential for developments outside of the City of Wyoming and Village of Lockland to also capture this same de-

mand. It is crucial for Wyoming and Lockland to collaborate in order to capture this demand before surrounding areas seize the opportunity themselves, thus contributing further to the “leakage” of expenditures spent by Wyoming and Lock-land residents.

COMMERCIAL IMPACT ANALYSIS — COMBINED RETAIL and OFFICE MARKET FINDINGS

Trade

AreaOffice Retail Restaurant

ITA Annual

Absorption40,000 - 50,000 50,000 - 70,000 15,000 - 25,000

5 Year

Total200,000 - 250,000 SF 250,000 - 350,000 SF 75,000 -125,000 SF

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 16

MARKETPLACE HOUSING ASSESSMENT City of Wyoming

Village of Lockland

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 17

Our look into the surrounding mar-ketplace begins with carefully se-lected trade areas to gauge house-

hold depth and relative housing mar-ket performance, as shown in the map at left. The tan shaded areas denote the corporate boundaries of

either cities or Census defined places (CDP). Shown in colored shades are Wyoming, Lockland, Woodlawn, Lin-

coln Heights and Finneytown. Key household demographics were also measured in drive times from

the center point, shown as irregular 8- and 15-minute Drive Areas. The core 8-minute Area under normal traffic conditions and speed limits is

shown in dark violet, while a more regional 15-minute Area is shown in violet, each from the previous

center point (CP) of Oak Avenue and Wyoming Avenue. For this Assessment, we will concen-

trate on the households within the limits of Wyoming and Lockland and then reference their demograph-

ics against the surrounding commu-nities of Woodlawn, Lincoln Heights, and Finneytown and also within the adjacent 8-minute Area.

Later, for recent housing market ac-tivity and sales performance, we will examine the recorded residential

transfers in the same areas above. The following page provides a detail of the map above within the 8-minute Drive Area.

HOUSEHOLD DEMOGRAPHIC DATA and TRENDS

Wyom ing-Lockland CP

Cincinnati cityCincinnati cityCincinnati cityCincinnati cityCincinnati city

Amberley villageAmberley villageAmberley villageAmberley villageAmberley village

Arlington Heights villageArlington Heights villageArlington Heights villageArlington Heights villageArlington Heights village

Blue Ash cityBlue Ash cityBlue Ash cityBlue Ash cityBlue Ash city

Bridgetown North CDPBridgetown North CDPBridgetown North CDPBridgetown North CDPBridgetown North CDPCheviot cityCheviot cityCheviot cityCheviot cityCheviot city

Deer Park cityDeer Park cityDeer Park cityDeer Park cityDeer Park city

Dillonvale CDPDillonvale CDPDillonvale CDPDillonvale CDPDillonvale CDP

Elmwood Place villageElmwood Place villageElmwood Place villageElmwood Place villageElmwood Place village

Evendale villageEvendale villageEvendale villageEvendale villageEvendale village

Fairfax villageFairfax villageFairfax villageFairfax villageFairfax village

Finney town CDPFinney town CDPFinney town CDPFinney town CDPFinney town CDP

Forest Park cityForest Park cityForest Park cityForest Park cityForest Park city

Glendale villageGlendale villageGlendale villageGlendale villageGlendale village

Golf M anor villageGolf M anor villageGolf M anor villageGolf M anor villageGolf M anor village

Greenhills villageGreenhills villageGreenhills villageGreenhills villageGreenhills village

Groesbeck CDPGroesbeck CDPGroesbeck CDPGroesbeck CDPGroesbeck CDP

Kenwood CDPKenwood CDPKenwood CDPKenwood CDPKenwood CDP

Lincoln Heights villageLincoln Heights villageLincoln Heights villageLincoln Heights villageLincoln Heights village

M adeira cityM adeira cityM adeira cityM adeira cityM adeira cityM onfort Heights East CDPM onfort Heights East CDPM onfort Heights East CDPM onfort Heights East CDPM onfort Heights East CDP

M onfort Heights South CDPM onfort Heights South CDPM onfort Heights South CDPM onfort Heights South CDPM onfort Heights South CDP

M ontgomery cityM ontgomery cityM ontgomery cityM ontgomery cityM ontgomery city

M ount Healthy cityM ount Healthy cityM ount Healthy cityM ount Healthy cityM ount Healthy city

M ount Healthy Heights CDPM ount Healthy Heights CDPM ount Healthy Heights CDPM ount Healthy Heights CDPM ount Healthy Heights CDP

Northbrook CDPNorthbrook CDPNorthbrook CDPNorthbrook CDPNorthbrook CDP

North College Hill cityNorth College Hill cityNorth College Hill cityNorth College Hill cityNorth College Hill city

Northgate CDPNorthgate CDPNorthgate CDPNorthgate CDPNorthgate CDP

Norwood cityNorwood cityNorwood cityNorwood cityNorwood city

Pleasant Run CDPPleasant Run CDPPleasant Run CDPPleasant Run CDPPleasant Run CDP

Pleasant Run Farm CDPPleasant Run Farm CDPPleasant Run Farm CDPPleasant Run Farm CDPPleasant Run Farm CDP

Reading cityReading cityReading cityReading cityReading city

St. Bernard citySt. Bernard citySt. Bernard citySt. Bernard citySt. Bernard city

Sharonville citySharonville citySharonville citySharonville citySharonville city

Silverton citySilverton citySilverton citySilverton citySilverton city

Springdale citySp ringdale citySpringdale citySpringdale citySpringdale city

The Village of Indian Hill cityThe Village of Indian Hill cityThe Village of Indian Hill cityThe Village of Indian Hill cityThe Village of Indian Hill city

White Oak CDPWhite Oak CDPWhite Oak CDPWhite Oak CDPWhite Oak CDP

White Oak East CDPWhite Oak East CDPWhite Oak East CDPWhite Oak East CDPWhite Oak East CDP

Woodlawn villageWoodlawn villageWoodlawn villageWoodlawn villageWoodlawn village

Wy oming cityWyoming cityWyoming cityWyoming cityWyoming city

Bu t

ler

Wa

r ren

Rd

But

ler

Wa

rren

Rd

Bu t

ler

War

ren

Rd

Bu

tler

Wa

r re n

Rd

Bu t

ler

Wa

r re n

Rd

Mai

n A

veM

a in

Ave

Mai

n A

veM

ain

Ave

Mai

n A

ve

North Bend RdNorth Bend RdNorth Bend RdNorth Bend RdNorth Bend Rd

E Fork Ave

E Fork Ave

E Fork Ave

E Fork Ave

E Fork AveHopkins Ave

Hopkins Ave

Hopkins Ave

Hopkins Ave

Hopkins Ave

Westbrook DrWestbrook DrWestbrook DrWestbrook DrWestbrook Dr

De l

ta A

veD

elta

Ave

Del

ta A

veD

elta

Ave

Del

ta A

ve

Edw

ard

s R

dE

dwa

rds

Rd

Edw

a rd

s R

dE

dw

ard

s R

dE

dwa

rds

Rd

Sn i

der R

dS

nide

r Rd

Sn

ide r

Rd

Sni

der R

dS

nide

r Rd

Colerain A

ve

Colerain A

ve

Colerain A

ve

Colerain A

ve

Colerain A

ve

Fleming RdFleming RdFleming RdFleming RdFleming RdSmalley RdSmalley RdSmalley Rd

Smalley RdSmalley Rd

Compton RdCompton RdCompton RdCompton RdCompton Rd Spooky H

ollow Rd

Spooky Hollow Rd

Spooky Hollow R

d

Spooky Hollow

Rd

Spooky Hollow Rd

W Galbraith RdW Galbraith RdW Galbraith RdW Galbraith RdW Galbraith Rd

Blo

me

Rd

Blo

me

Rd

Blo

me

Rd

Blo

me

Rd

Blo

me

Rd

Section RdSection RdSection RdSection RdSection Rd Section RdSection RdSection RdSection RdSection Rd

Che

viot

Rd

Che

viot

Rd

Che

viot

Rd

Che

viot

Rd

Che

viot

Rd C

enter Hill Ave

Center H

ill Ave

Center H

ill Ave

Center H

ill Ave

Center H

ill Ave

Car

thag

e A

veC

arth

age

Ave

Car

thag

e A

veC

arth

age

Ave

Car

thag

e A

ve

Spring Grove Ave

Spring Grove Ave

Spring Grove Ave

Spring Grove Ave

Spring Grove Ave

E Mitchell Ave

E Mitchell Ave

E Mitchell Ave

E Mitchell Ave

E Mitchell AveWoolper AveWoolper AveWoolper AveWoolper AveWoolper Ave

Murray Ave

Murray AveMurray Ave

Murray Ave

Murray AveWasson RdWasson RdWasson RdWasson RdWasson Rd

Chu

rch

St

Chu

rch

St

Chu

rch

St

Chu

rch

St

Chu

rch

St

W Crescentville RdW Crescentville RdW Crescentville RdW Crescentville RdW Crescentville Rd

Crescentville RdCrescentville RdCrescentville RdCrescentville RdCrescentville RdFields Ertel RdFields Ertel RdFields Ertel RdFields Ertel RdFields Ertel Rd

W Sharon RdW Sharon RdW Sharon RdW Sharon RdW Sharon Rd

Woodford RdWoodford RdWoodford RdWoodford RdWoodford Rd

Shawnee Run RdShawnee Run RdShawnee Run RdShawnee Run RdShawnee Run Rd

Woodridge Blvd

Woodridge Blvd

Woodridge BlvdWoodridge Blvd

Woodridge BlvdRos

s R

dR

o ss

Rd

Ros

s R

dR

oss

Rd

Ros

s R

d

Dimmick RdDimmick RdDimmick RdDimmick RdDimmick Rd

W North Bend RdW North Bend RdW North Bend RdW North Bend RdW North Bend Rd

Resor RdResor RdResor RdResor RdResor Rd

Clif

ton

Ave

Clif

t on

Ave

Clif

ton

Av e

Clif

ton

Av e

Clif

ton

Av e Erie

Ave

Erie

Ave

Erie

Ave

Erie

Ave

Erie

Ave

Rou

nd B

otto

m R

d

Rou

nd B

otto

m R

d

Rou

nd B

otto

m R

d

Rou

nd B

otto

m R

d

Rou

nd B

otto

m R

d

Mil l

Rd

Mil l

Rd

Mil l

Rd

Mil l

Rd

Mil l

Rd

W Kemper RdW Kemper RdW Kemper Rd

W Kemper RdW Kemper Rd

Rea

din

g R

dR

ead

ing

Rd

Rea

din

g R

dR

eadi

ng

Rd

Rea

din

g R

d

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Sn i

der R

dS

n ide

r Rd

Sn

ide r

Rd

Sn i

der R

dS

n ide

r Rd

Glendale Milford RdGlendale Milford RdGlendale Milford RdGlendale Milford RdGlendale Milford Rd

Summ

it Rd

Summ

it Rd

Summ

it Rd

Summ

it Rd

Summ

it Rd

Euclid AveEuclid AveEuclid AveEuclid AveEuclid Ave

Highland AveHighland AveHighland AveHighland Ave

Highland Ave

Putz PlPutz PlPutz PlPutz PlPutz Pl

Montana Ave

Montana Ave

Montana Ave

Montana Ave

Montana Ave

Dana AveDana AveDana AveDana AveDana Ave

Hopple StHopple StHopple StHopple StHopple St

Pla

infie

ld R

dP

lain

field

Rd

Pla

i nfie

ld R

dP

lai n

field

Rd

Pla

i nfie

ld R

d

E Galbraith Rd

E Galbraith Rd

E Galbraith Rd

E Galbraith Rd

E Galbraith Rd

Madison Rd

Madison Rd

Madison Rd

Madison Rd

Madison Rd

Westwood Northern BlvdWestwood Northern BlvdWestwood Northern BlvdWestwood Northern BlvdWestwood Northern Blvd

Beekm

an St

Beekm

an St

Beekm

an St

Beekm

an St

Beekm

an St

Struble RdStruble RdStruble RdStruble RdStruble Rd

Win

ton

Rd

Win

ton

Rd

Win

ton

Rd

Win

ton

Rd

Win

ton

Rd

Losantiville AveLosantiville AveLosantiville AveLosantiville AveLosantiville Ave

Euclid RdEuclid RdEuclid RdEuclid RdEuclid Rd

Covedale CDPCovedale CDPCovedale CDPCovedale CDPCovedale CDP

8 min

15 min

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 18

Wyom ing-Lockland CP

Amberley villageAmberley villageAmberley villageAmberley villageAmberley village

Arlington Heights villageArlington Heights villageArlington Heights villageArlington Heights villageArlington Heights village

Blue Ash cityBlue Ash cityBlue Ash cityBlue Ash cityBlue Ash city

Deer Park cityDeer Park cityDeer Park cityDeer Park cityDeer Park city

Dillonvale CDPDillonvale CDPDillonvale CDPDillonvale CDPDillonvale CDP

Elmwood Place villageElmwood Place villageElmwood Place villageElmwood Place villageElmwood Place village

Evendale villageEvendale villageEvendale villageEvendale villageEvendale village

Finney town CDPFinney town CDPFinney town CDPFinney town CDPFinney town CDP

Glendale villageGlendale villageGlendale villageGlendale villageGlendale village

Golf M anor villageGolf M anor villageGolf M anor villageGolf M anor villageGolf M anor village

Greenhills villageGreenhills villageGreenhills villageGreenhills villageGreenhills village

Lincoln Heights villageLincoln Heights villageLincoln Heights villageLincoln Heights villageLincoln Heights village

M ount Healthy cityM ount Healthy cityM ount Healthy cityM ount Healthy cityM ount Healthy city

North College Hill cityNorth College Hill cityNorth College Hill cityNorth College Hill cityNorth College Hill city

Reading cityReading cityReading cityReading cityReading city

Silverton citySilverton citySilverton citySilverton citySilverton city

Woodlawn villageWoodlawn villageWoodlawn villageWoodlawn villageWoodlawn village

Wy oming cityWyoming cityWyoming cityWyoming cityWyoming city

Damon Rd

Damon Rd

Damon Rd

Damon Rd

Damon Rd

Knoll

Rd

Knoll

Rd

Knoll

Rd

Knoll

Rd

Knoll

Rd

Wa

ycro

ss R

dW

ayc

ross

Rd

Wa

ycro

ss R

dW

ayc

ross

Rd

Wa

ycro

ss R

dFleming RdFleming RdFleming RdFleming RdFleming Rd

Smalley RdSmalley RdSmalley Rd

Smalley RdSmalley Rd

Compton RdCompton RdCompton RdCompton RdCompton Rd

N W

ayne

Ave

N W

ayne

Ave

N W

ayn

e A

veN

Wa

yne

Ave

N W

ayne

Ave

Section RdSection RdSection RdSection RdSection Rd

Center H

ill Ave

Center H

ill Ave

Center H

ill Ave

Center H

ill Ave

Center H

ill Ave

Sprin

g G

rove

Ave

Sprin

g G

rove

Ave

Sprin

g G

rove

Ave

Sprin

g G

rove

Ave

Sprin

g G

rove

Ave

W Sharon Rd

Woodford RdWoodford RdWoodford RdWoodford RdWoodford Rd

Cam

argo

Rd

Cam

argo

Rd

Cam

argo

Rd

Cam

argo

Rd

Cam

argo

Rd

Sycamore RdSycamore RdSycamore RdSycamore RdSycamore Rd

W North Bend RdW North Bend RdW North Bend RdW North Bend RdW North Bend Rd

Mile

s R

dM

iles

Rd

Mi le

s R

dM

i les

Rd

Mi le

s R

dM

ill R

dM

ill R

dM

ill R

dM

ill R

dM

ill R

d

Rea

din

g R

dR

ead

ing

Rd

Rea

din

g R

dR

ead

ing

Rd

Rea

din

g R

d

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Cornell RdCornell RdCornell RdCornell RdCornell Rd

Glendale Milford RdGlendale Milford RdGlendale Milford RdGlendale Milford RdGlendale Milford Rd

Springdale Rd

Springdale Rd

Springdale Rd

Springdale Rd

Springdale Rd

Cooper RdCooper RdCooper RdCooper RdCooper Rd

Hunt RdHunt RdHunt RdHunt RdHunt Rd

Dal

y R

dD

aly

Rd

Dal

y R

dD

aly

Rd

Dal

y R

d

W Galbraith RdW Galbraith RdW Galbraith RdW Galbraith RdW Galbraith Rd

An

thon

y W

ayne

Ave

An

thon

y W

ayne

Ave

Ant

hon

y W

ayne

Ave

Ant

hony

Way

ne A

ve

An

thon

y W

ayne

Ave

Summ

it Rd

Summ

it Rd

Summ

it Rd

Summ

it Rd

Summ

it Rd

Euclid AveEuclid AveEuclid AveEuclid AveEuclid Ave

Ridge Ave

Ridge Ave

Ridge A

ve

Ridge A

ve

Ridge Ave

Pfeiffer RdPfeiffer RdPfeiffer RdPfeiffer RdPfeiffer Rd

Pla

i nf ie

ld R

dP

lain

fi eld

Rd

Pla

infie

ld R

dP

lain

field

Rd

Pla

infie

ld R

d

E Sharon RdE Sharon RdE Sharon RdE Sharon RdE Sharon Rd

E Sharon RdE Sharon RdE Sharon RdE Sharon RdE Sharon Rd

Pla

infie

ld R

dP

lai n

f iel d

Rd

Pl a

infi e

ld R

dP

l ain

fi eld

Rd

Pl a

infi e

ld R

d

Losantiville AveLosantiville AveLosantiville AveLosantiville AveLosantiville Ave

Ke

nwo

od R

dK

enw

ood

Rd

Ke

nwo

od R

dK

enw

ood

Rd

Ke

nwo

od R

d

E Galbraith RdE Galbraith RdE Galbraith RdE Galbraith RdE Galbraith Rd

Blue Ash cityBlue Ash cityBlue Ash cityBlue Ash cityBlue Ash city

Madeira cityMadeira cityMadeira cityMadeira cityMadeira city

S haronville cityS haronville cityS haronville cityS haronville cityS haronville city

S pringdale city

HOUSEHOLD DEMOGRAPHIC DATA and TRENDS, continued.

8 min

15 min

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 19

This Assessment relies upon the updated 2007 US Census estimates collected during the initial analyses last December. Provided

by AGS, the data was then categorized into columnar household Demographic Areas of interest, as shown at left.

These tables, with the complete set provided in the full Report, offer key insights into the character, and makeup of the following char-

acteristics of the surrounding marketplace:

� Household growth & size

� Incomes by age group

� Household net worth

� Ownership and renters

� Education level

� Racial background

� Household familial status

� Housing units & style

� Year housing units built

� Occupation and job sector

� Commute mode & times

To better locate the relative concentrations of

any typical household metric or trend, we have also created color-gradient maps plotted by Census block group, with an exam-

ple on the following page. Here, the esti-mated 2007 median household incomes are

graphically plotted by block group in ranges by color. Please see the accompanying key legend.

We note that the City of Wyoming has challenged the US Census estimates in recent years. The following US Census in-formation does not reflect all of the City’s suggested population, household, and housing unit counts as requested in the Census Challenge. Although we fully consider the suggested counts from the City of Wyoming in our final conclusions

and recommendations, the following pages reflect trends and metrics identified from the greater pool of demographic in-formation provided by the Census.

HOUSEHOLD DEMOGRAPHIC DATA and TRENDS, continued.

2007 Estimates Finneytown Woodlawn Wyoming

Lincoln

Heights Lockland 8-Minute 15-Minute

Marital Status:

Age 15 + Population 10,074 2,200 5,829 2,771 2,671 37,861 233,376

Divorced 9.0% 12.3% 7.4% 13.1% 15.0% 12.2% 11.6%

Never Married 24.1% 32.6% 19.5% 39.2% 33.2% 27.8% 32.0%

Now Married 56.3% 42.0% 64.9% 26.4% 36.9% 47.1% 43.4%

Separated 3.3% 4.5% 3.1% 11.7% 6.2% 4.9% 5.0%

Widowed 7.4% 8.5% 5.1% 9.6% 8.7% 8.0% 8.1%

Educational Attainment:

Age 25 + Population 8,583 1,854 5,079 2,194 2,227 32,140 193,986

Grade K - 8 1.9% 1.7% 0.7% 4.4% 6.7% 3.1% 3.0%

Grade 9 - 12 5.6% 4.6% 2.2% 17.4% 11.9% 9.6% 9.7%

High School Graduate 27.2% 29.6% 13.0% 41.4% 45.8% 32.4% 32.2%

Some College, No Degree 17.7% 19.9% 12.4% 20.2% 17.0% 17.4% 18.1%

College Degree 47.6% 44.2% 71.7% 16.7% 18.7% 37.6% 37.0%

Household Income

Income $ 0 - $9,999 5.3% 4.5% 1.7% 21.8% 13.8% 8.1% 10.1%

Income $ 10,000 - $14,999 3.5% 4.0% 1.1% 10.4% 6.5% 4.5% 5.0%

Income $ 15,000 - $24,999 7.2% 11.0% 5.2% 21.5% 16.8% 12.4% 11.8%

Income $ 25,000 - $34,999 8.0% 11.1% 7.0% 12.0% 13.9% 12.7% 12.2%

Income $ 35,000 - $49,999 12.9% 14.3% 10.5% 7.2% 17.5% 14.2% 14.8%

Income $ 50,000 - $74,999 23.7% 18.7% 13.4% 13.1% 17.3% 18.1% 18.4%

Income $ 75,000 - $99,999 17.5% 15.5% 10.4% 7.7% 8.4% 10.9% 11.4%

Income $100,000 - $124,999 9.8% 8.1% 10.1% 3.5% 2.2% 6.1% 6.2%

Income $125,000 - $149,999 4.0% 3.4% 10.9% 0.8% 1.5% 3.9% 3.3%

Income $150,000 + 8.2% 9.5% 29.8% 2.0% 2.1% 9.1% 6.7%

Average Household Income $60,924 $72,121 $111,002 $33,347 $32,719 $57,691 $52,555

Median Household Income $63,260 $55,859 $101,982 $23,207 $33,811 $47,703 $45,591

Per Capita Income $24,046 $32,311 $42,485 $13,252 $14,652 $25,777 $23,454

Vehicles Available

0 Vehicles Available 5.4% 5.4% 4.1% 21.1% 18.7% 11.6% 13.0%

1 Vehicle Available 29.9% 40.7% 24.0% 44.0% 38.3% 36.7% 37.1%

2+ Vehicles Available 64.7% 54.0% 72.0% 34.9% 42.9% 51.7% 50.0%

Average Vehicles Per Household 1.90 1.70 2.00 1.30 1.40 1.60 1.60

Total Vehicles Available 9,666 2,090 5,739 1,923 2,148 33,428 201,696

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 20

HOUSEHOLD DEMOGRAPHIC DATA and TRENDS, continued.

Wyom ing-Lockland CP

Amberley villageAmberley villageAmberley villageAmberley villageAmberley village

Arlington Heights villageArlington Heights villageArlington Heights villageArlington Heights villageArlington Heights village

Blue Ash cityBlue Ash cityBlue Ash cityBlue Ash cityBlue Ash city

Deer Park cityDeer Park cityDeer Park cityDeer Park cityDeer Park city

Dillonvale CDPDillonvale CDPDillonvale CDPDillonvale CDPDillonvale CDP

Elmwood Place villageElmwood Place villageElmwood Place villageElmwood Place villageElmwood Place village

Evendale villageEvendale villageEvendale villageEvendale villageEvendale village

Finney town CDPFinney town CDPFinney town CDPFinney town CDPFinney town CDP

Forest Park cityForest Park cityForest Park cityForest Park cityForest Park city

Glendale villageGlendale villageGlendale villageGlendale villageGlendale village

Golf M anor villageGolf M anor villageGolf M anor villageGolf M anor villageGolf M anor village

Greenhills villageGreenhills villageGreenhills villageGreenhills villageGreenhills village

Groesbeck CDPGroesbeck CDPGroesbeck CDPGroesbeck CDPGroesbeck CDP

Kenwood CDPKenwood CDPKenwood CDPKenwood CDPKenwood CDP

Lincoln Heights villageLincoln Heights villageLincoln Heights villageLincoln Heights villageLincoln Heights village

M adeira cityM adeira cityM adeira cityM adeira cityM adeira cityM onfort Heights East CDPM onfort Heights East CDPM onfort Heights East CDPM onfort Heights East CDPM onfort Heights East CDP

M ontgomery cityM ontgomery cityM ontgomery cityM ontgomery cityM ontgomery city

M ount Healthy cityM ount Healthy cityM ount Healthy cityM ount Healthy cityM ount Healthy city

M ount Healthy Heights CDPM ount Healthy Heights CDPM ount Healthy Heights CDPM ount Healthy Heights CDPM ount Healthy Heights CDP

Northbrook CDPNorthbrook CDPNorthbrook CDPNorthbrook CDPNorthbrook CDP

North College Hill cityNorth College Hill cityNorth College Hill cityNorth College Hill cityNorth College Hill city

Northgate CDPNorthgate CDPNorthgate CDPNorthgate CDPNorthgate CDP

Norwood cityNorwood cityNorwood cityNorwood cityNorwood city

Pleasant Run CDPPleasant Run CDPPleasant Run CDPPleasant Run CDPPleasant Run CDP

Reading cityReading cityReading cityReading cityReading city

St. Bernard citySt. Bernard citySt. Bernard citySt. Bernard citySt. Bernard city

Sharonville citySharonville citySharonville citySharonville citySharonville city

Silverton citySilverton citySilverton citySilverton citySilverton city

Springdale citySp ringdale citySpringdale citySpringdale citySpringdale city

The Village of Indian Hill cityThe Village of Indian Hill cityThe Village of Indian Hill cityThe Village of Indian Hill cityThe Village of Indian Hill city

White Oak CDPWhite Oak CDPWhite Oak CDPWhite Oak CDPWhite Oak CDP

White Oak East CDPWhite Oak East CDPWhite Oak East CDPWhite Oak East CDPWhite Oak East CDP

Woodlawn villageWoodlawn villageWoodlawn villageWoodlawn villageWoodlawn village

Wyoming cityWyoming cityWy oming cityWy oming cityWy oming city

Knoll

Rd

Knoll

Rd

Knoll

Rd

Knoll

Rd

Knoll

Rd

North Bend RdNorth Bend RdNorth Bend RdNorth Bend RdNorth Bend Rd

E Fork Ave

E Fork Ave

E Fork Ave

E Fork Ave

E Fork AveHopkins Ave

Hopkins Ave

Hopkins Ave

Hopkins Ave

Hopkins Ave

Appleton St

Appleton St

Appleton St

Appleton St

Appleton St

Sn

ide

r R

dS

nid

er

Rd

Sn

ide

r R

dS

nid

er

Rd

Sn

ide

r R

d

Waycross R

d

Waycross R

d

Waycross R

d

Waycross R

d

Waycross R

d

Col e

rai n A

veC

ol erai n

Av e

Co le

rain A

veC

o lerain

Ave

Co le

rain A

ve

Fleming RdFleming RdFleming RdFleming RdFleming RdSmalley RdSmalley RdSmalley Rd

Smalley RdSmalley Rd

Compton RdCompton RdCompton RdCompton RdCompton Rd

Spooky Hollow

Rd

Spooky Hollow

Rd

Spooky Hollow

Rd

Spooky Hollow

Rd

Spooky Hollow

Rd

W Galbraith RdW Galbraith RdW Galbraith RdW Galbraith RdW Galbraith Rd

Blo

me

Rd

Blo

me

Rd

Bl o

me

Rd

Bl o

me

Rd

Bl o

me

Rd

Section RdSection RdSection RdSection RdSection Rd

Che

viot

Rd

Che

viot

Rd

Che

vio t

Rd

Che

vio t

Rd

Che

vio t

Rd C

enter Hill Ave

Center H

ill Ave

Center H

ill Ave

Center H

ill Ave

Center H

ill Ave

Car

tha

ge

Ave

Car

tha

ge

Ave

Car

tha

ge

Ave

Car

tha

ge

Ave

Car

tha

ge

Ave

Indian Hill RdIndian Hill RdIndian Hill RdIndian Hill RdIndian Hill Rd

Spring G

rove Ave

Spring G

rove Ave

Spring G

rove Ave

Spring G

rove Ave

Spring G

rove AveE Mitchell Ave

E Mitchell Ave

E Mitchell Ave

E Mitchell Ave

E Mitchell Ave

Fields Ertel RdFields Ertel RdFields Ertel RdFields Ertel RdFields Ertel Rd

Bo

udi n

ot

Ave

Bo

udin

ot

Ave

Bo

udin

ot

Ave

Bo

udin

ot

Ave

Bo

udin

ot

Ave

W Sharon RdW Sharon RdW Sharon RdW Sharon RdW Sharon Rd

Red

Ba

nk Rd

Red

Ba

nk Rd

Red

Ba

nk R

dR

ed B

an

k Rd

Red

Ba

nk Rd

Woodford RdWoodford RdWoodford RdWoodford RdWoodford Rd Shawnee Run Rd

Shawnee Run RdShawnee Run RdShawnee Run RdShawnee Run Rd

Hopewell LnHopewell LnHopewell LnHopewell LnHopewell Ln

W North Bend RdW North Bend RdW North Bend RdW North Bend RdW North Bend Rd

Mile

s R

dM

iles

Rd

Mi le

s R

dM

i les

Rd

Mi le

s R

dM

ill R

dM

ill R

dM

ill R

dM

ill R

dM

ill R

d

Win

ton R

dW

into

n Rd

Win

ton R

dW

inton R

dW

into

n Rd

W Kemper RdW Kemper RdW Kemper Rd

W Kemper RdW Kemper Rd

Rea

din

g R

dR

ead

ing

Rd

Rea

din

g R

dR

ead

ing

Rd

Rea

din

g R

d

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Ree

d H

artm

an H

wy

Sn

ide

r R

dS

nid

er

Rd

Sn

ide

r R

dS

nid

er

Rd

Sn

ide

r R

d

Cornell Rd

Cornell RdCornell Rd

Cornell RdCornell Rd

Glendale Milford RdGlendale Milford RdGlendale Milford RdGlendale Milford RdGlendale Milford Rd

Pfeiffer RdPfeiffer RdPfeiffer RdPfeiffer RdPfeiffer Rd

Hunt RdHunt RdHunt RdHunt RdHunt Rd

Dal

y R

dD

aly

Rd

Dal

y R

dD

aly

Rd

Dal

y R

d

Ant

hony

Way

ne A

ve

Ant

hony

Way

ne A

ve

An

thon

y W

ayn

e A

ve

Ant

hon

y W

ayne

Ave

Ant

hony

Way

ne A

ve

Summ

it Rd

Summ

it Rd

Summ

it Rd

Summ

it Rd

Summ

it Rd

Euclid AveEuclid AveEuclid AveEuclid AveEuclid Ave

Vine

St

Vine

St

Vin

e S

t

Vine

St

Vine

St

Highland AveHighland AveHighland AveHighland AveHighland Ave

Duck Creek RdDuck Creek RdDuck Creek RdDuck Creek RdDuck Creek Rd

Putz PlPutz PlPutz PlPutz PlPutz Pl

Sp

ring Grove

Ave

Sp

ring Grove

Ave

Sprin

g Grove A

ve

Spring

Grove A

ve

Sp

ring Grove

Ave

Pla

infie

ld R

dP

lain

fiel d

Rd

Pla

infi e

ld R

dP

lain

fi eld

Rd

Pla

infi e

ld R

d

E Sharon RdE Sharon RdE Sharon RdE Sharon RdE Sharon Rd

E Sharon RdE Sharon RdE Sharon RdE Sharon RdE Sharon Rd

Beekm

an St

Beekm

an St

Beekm

an St

Beekm

an St

Beekm

an St

Struble RdStruble RdStruble RdStruble RdStruble Rd

Pla

infi e

ld R

dP

lain

field

Rd

Pla

infie

ld R

dP

lain

field

Rd

Pla

infie

ld R

d

Losantiville AveLosantiville AveLosantiville AveLosantiville AveLosantiville Ave

Euclid RdEuclid RdEuclid RdEuclid RdEuclid Rd

Median Household Income By US Census Block Group Dk Blue over $75,000 Blue $50,000-$75,000 Green $35,000-$50,000 Tan $25,000-$35,000 Blush under $25,000

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 21

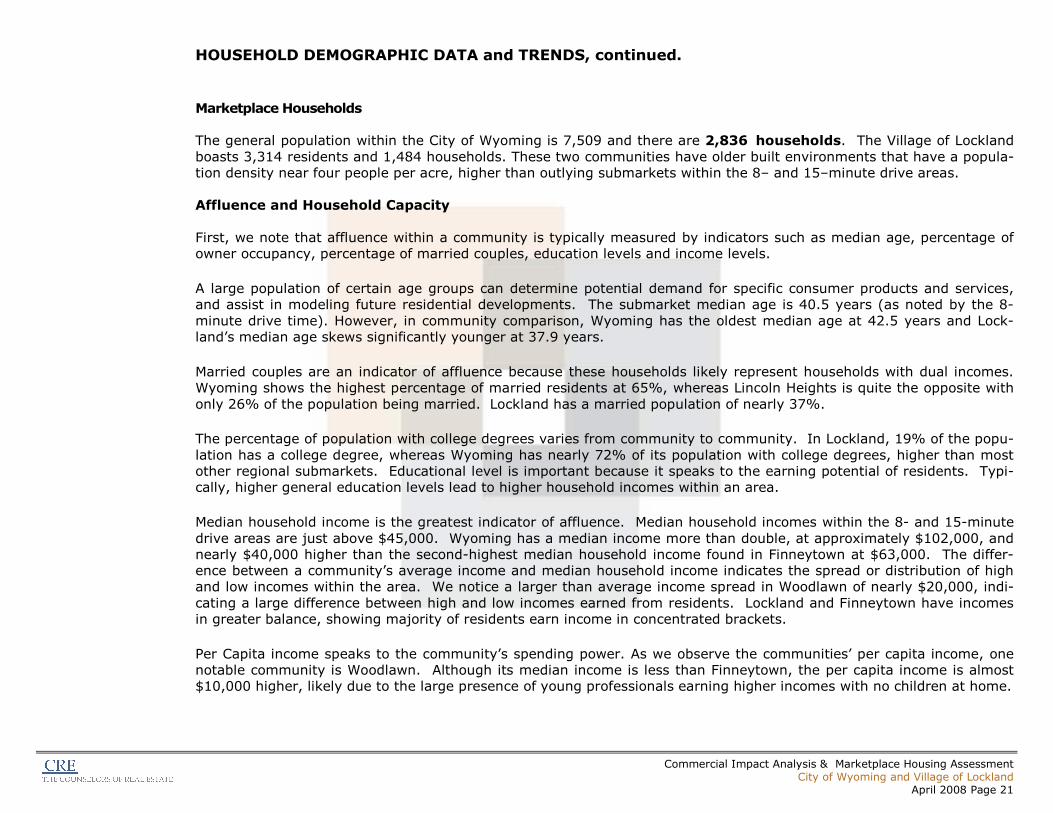

Marketplace Households The general population within the City of Wyoming is 7,509 and there are 2,836 households. The Village of Lockland

boasts 3,314 residents and 1,484 households. These two communities have older built environments that have a popula-tion density near four people per acre, higher than outlying submarkets within the 8– and 15–minute drive areas. Affluence and Household Capacity

First, we note that affluence within a community is typically measured by indicators such as median age, percentage of owner occupancy, percentage of married couples, education levels and income levels.

A large population of certain age groups can determine potential demand for specific consumer products and services, and assist in modeling future residential developments. The submarket median age is 40.5 years (as noted by the 8-

minute drive time). However, in community comparison, Wyoming has the oldest median age at 42.5 years and Lock-land’s median age skews significantly younger at 37.9 years.

Married couples are an indicator of affluence because these households likely represent households with dual incomes. Wyoming shows the highest percentage of married residents at 65%, whereas Lincoln Heights is quite the opposite with

only 26% of the population being married. Lockland has a married population of nearly 37%.

The percentage of population with college degrees varies from community to community. In Lockland, 19% of the popu-

lation has a college degree, whereas Wyoming has nearly 72% of its population with college degrees, higher than most other regional submarkets. Educational level is important because it speaks to the earning potential of residents. Typi-cally, higher general education levels lead to higher household incomes within an area.

Median household income is the greatest indicator of affluence. Median household incomes within the 8- and 15-minute

drive areas are just above $45,000. Wyoming has a median income more than double, at approximately $102,000, and nearly $40,000 higher than the second-highest median household income found in Finneytown at $63,000. The differ-ence between a community’s average income and median household income indicates the spread or distribution of high and low incomes within the area. We notice a larger than average income spread in Woodlawn of nearly $20,000, indi-

cating a large difference between high and low incomes earned from residents. Lockland and Finneytown have incomes in greater balance, showing majority of residents earn income in concentrated brackets.

Per Capita income speaks to the community’s spending power. As we observe the communities’ per capita income, one notable community is Woodlawn. Although its median income is less than Finneytown, the per capita income is almost $10,000 higher, likely due to the large presence of young professionals earning higher incomes with no children at home.

HOUSEHOLD DEMOGRAPHIC DATA and TRENDS, continued.

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 22

Affluence and Household Capacity, continued. Census growth data from 2000 to 2007 shows the region declined in households, and therefore shows declines in Wyo-

ming and Lockland. We note that Wyoming has challenged the Census households count with positive results. However, there is evidence of an aging population and diminishing household size. This is typical of many communities that experienced growth 10 to

15 years ago and now have grown children moving away to college or other communities. A city like Wyoming is consid-ered a great place to raise a family and young families no doubt consider Wyoming for the schools and quality of life. After their children leave, many parents stay and increase the ranks of empty-nesters and smaller household sizes.

These smaller family stakeholders are key assets to any community, yet sustained community health comes from a bal-ance of downsizing households and additional growing families. In Wyoming, nearly 52% of households have lived in their home for more than five years, noted as “stability” by the

Census. This is a higher share than what is found within other regional submarkets. Typically, there is a direct correla-tion between the average household size and the share of stability rate, that the larger the household size, the higher the stability. Wyoming 2007 Census estimates show this relationship.

In contrast to stability, “turnover” represents that percentage of households that have historically moved in the last year. Turnover typically correlates with the amount of renter-occupied housing due to annual leases seen in multi-family hous-ing. Woodlawn and Lockland have the highest percentages of renter-occupied housing and also have the largest percent-

ages of turnover, indicating a stronger presence of transient households. Wyoming has low representation of transient households. Unserved Households

In Lockland, we also note a strong percentage of households living in their residence for more than five years. Lockland experiences loyalty from residents that can afford to live in homes of higher value, yet choose to live in Lockland despite

its scarcity of higher valued homes. In Lockland, some 30% of households earn more than $50,000 a year, although there is no comparable housing stock valued to match that income level. There is a clear opportunity to provide housing options to cater to the more affluent underserved households within Lockland.

In Wyoming, we also notice a number of unserved households. Much of Wyoming’s housing activity occurs in the higher priced homes. However, there are few choices for move-down couples with no children, or for young families looking to move to Wyoming in the price range of $200,000 to $300,000.

The following chart helps to estimate the number of unserved households that the City of Wyoming and Village of Lock-land could potentially serve through more diverse housing options:

HOUSEHOLD DEMOGRAPHIC DATA and TRENDS, continued.

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 23

HOUSEHOLD DEMOGRAPHIC DATA and TRENDS, continued.

Source: Demographics Now, 2007 City of Wyoming estimates

Unserved Households, continued.

For the total household counts in Wyoming and Lockland, we separate those households with combined incomes of $50,000 or more per year. These households are the most likely to have a

penchant for new housing above $200,000 or apartments with rents above $900. Our analysis over the past three years in the

relevant Housing Search Area of all communities studied demonstrates that 5% of all households purchase a new home priced over $200,000

each year and another 5% lease in rental units with contract rents over $900 per month. When combined, these households reflect a po-

tential 10% of qualified households that would consider a new residence of $200,000 or more each year. After subtracting the average his-

torical activity of 150 competitive units seen an-nually, we net some 140 households each year that remain unserved by current housing options within Wyoming or Lockland.

We believe the City of Wyoming and Village of Lockland can conservatively capture 20-25% of these unserved households with new or revi-

talized residential product. This creates additional housing demand of 25-35

units per year, or 125-175 units over the next five years, that could be offered by the City of Wyoming or Village of Lockland to cap-ture unserved households.

Households within Wyoming & Lockland = 4,800

Total Qualified Households = 2,900

Annual households expected to

enter market (10%) = 290

less Annual activity

=150 units 140 Unmet

Annual House-hold Demand

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 24

Psychographics Property Advisors uses a psychographic household profile set known as MOSAIC Market Segmentation.

Those MOSAIC segments most viable for new housing product and commercial goods are normally found in Groups A, B, H and cluster F01 Steadfast Conservatives because these households have median incomes greater than $50,000. A02 Dream Weavers are home to well-off families living an affluent, ranked second in terms of wealth, they live in

new-money subdivisions, possess high incomes, have college degrees and median household incomes near $113,000. And with a median age of 38.5 years, these well-educated late Baby Boomers strive to own the trappings of success. They drive at least one luxury vehicle such as Mercedes Benz, BMW 7 or 5 Series, or top-of-the line Audi and Lexus mod-els. They also have premium SUVs, Saabs, Volvos and Volkswagens in their multi-driver households.

A06 Small-Town Success households are white-collar, college educated, middle-aged working couples. Though the median household income is $75,000, about a third bring home more than $100,000 annually. Predominantly married,

nearly 40% have children at home. Over 90% own single detached homes with a median value of $175,000. The median age is 39, though a third of the crowd is age 50 plus. B06 Affluent Urban Professionals are mostly wealthy singles and couples owning swank condos and apartments val-

ued at twice the national average. Most residents are in their twenties and thirties, hold college degrees and have jobs as executives and white-collar professionals. 20% reside in housing with median home values about $300,000. Median household income is $74,950. They drive luxury cars such as Land Rovers, Mercedes, and Audis. The Gen X crowd pre-

fers trendier models such as the Audi TT, Mini-Cooper and even hybrids. H02 Minority Metro Communities are made up of households concentrated in inner-ring suburbs, these households earn above-average incomes from a mix of service Industry and white-collar jobs in transportation, health care, educa-

tion and public administration. Many have settled into older homes and semi-detached houses built in the 1960s. The median household income is $55,000 and median Age: 37.9 years. F01 Steadfast Conservatives boasts mature singles and couples living in midscale urban neighborhoods. Households

tend to be white, high school-educated and middle class. Many have begun to empty-nest or filled with young couples and singles. The seniority of many residents does have benefits in the workplace. They earn middle class incomes from skilled jobs in manufacturing, retail and health care. Their median income near $50,600 goes far, allowing residents to

own older homes and multiple cars and trucks at higher than average rates.

MOSAIC segmenta-tion was created by Experian and sorts

each household into 12 household

groups, each group with 3-7 clusters for a total of 62 individual market segmentation

clusters.

Segmentation data considers demograph-ics and overlays it with purchasing data from credit bureaus, insur-ance agencies, banks,

and more.

Segmentation provides insight into each

household’s lifestyle and their penchant

toward products rang-ing from housing, in-vestments, and media subscriptions, to en-

tertainment interests, leisure activities and types of vehicles they

are likely to own.

HOUSEHOLD DEMOGRAPHIC DATA and TRENDS, continued.

MOSAIC segments most prevalent within Wyoming: Group A06 Small Town Success (15%)

Group A02 Dream Weavers (43%) Group B02 Affluent Urban Professionals (22%) Group H02 Minority Metro Communities (13%)

MOSAIC segments most prevalent within Lockland: Group D04: Small-town Endeavors (25%)

Group F01: Steadfast Conservatives (29%) Group J03: Struggling City Centers (32%)

Commercial Impact Analysis & Marketplace Housing Assessment City of Wyoming and Village of Lockland

April 2008 Page 25

Market Performance Seen in Recent Home Closings We believe that housing market performance is best tracked and analyzed based upon the closings of all residential

properties within a defined Housing Search Area. For this assessment, we electronically collected all of the actual resi-dential transfers in a select Search Area around the City of Wyoming and Village of Lockland over the last three years. We then sorted and categorized each transfer by its inherent original community or legal subdivision. In this way, the homes as product and as community are grouped by like lot size, original builder and relative year built.