Embed Size (px)

Citation preview

MARSHALL OF CAMBRIDGE (HOLDINGS) LIMITED

Report & Accounts 2006

2

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

Chairman’s Statement 3

Operating Reviews

Marshall Aerospace 5

Marshall Motor Holdings:

Marshall Motor Group 9

Marshall Leasing 11

Marshall Thermo King 13

Marshall Specialist Vehicles 15

Property Review 16

Corporate Responsibility 17

Financial Review 18

Corporate Governance 20

The Board 23

Directors’ Report 24

Statement of Directors’ Responsibilities 27

Group Profit and Loss Account 28

Group Statement of Total Recognised Gains and Losses 28

Group Statement of Cash Flows 29

Group Balance Sheet 30

Company Balance Sheet 31

Notes to the Financial Statements 32

Report of the Auditors 50

Recent Financial History 51

Notice of AGM 52

AGM Agenda 53

Sir Arthur Marshall OBE DL 54

Key Group Personnel 56

C o n t e n t s

3

I cannot begin my Statement this year

without a reference to the death of our

Honorary Life President, my father Sir

Arthur Marshall, who after an

incredible 103 year innings finally

folded his wings and died peacefully at home early in

the morning of March 16th. The tributes to him have

been pouring in from all over the world and from

some 500 kind colleagues, friends and acquaintances,

to whom we in the Company are all most grateful.

There have also been amazing obituaries in the

national press. Although my father had ‘retired’ in

1989, it was good that we were able to persuade him

to write the history of the wonderful story of the life

of his family and the development of Marshall of

Cambridge in his much sought-after book ‘The

Marshall Story’. We must all be grateful to him for

what he has bequeathed to us in this Company, some

highlights of which are recorded on pages 54-55 of

this report, and it is in our hands to continue to build

further on his legacy.

2006 has been an excellent year for the Group, thanks to the hard work

of our dedicated management and staff.

Our Aerospace activities have continued to grow on the back of the

important HIOS contract which gives such critical support to the Royal

Air Force on its C-130 fleet. Our work in Canada has already resulted in

a sharp reduction in turnaround time for the RCAF C-130 fleet. We are

delighted that our Dutch company has been established to carry out

engineering work in support of our C-130 digitisation and modernisation

programme for the C-130s of the Royal Netherlands Air Force. Our

manufacturing of Airbus wing stringers for the A320 and A330

programmes is exceeding expectations, as is our work for Boeing on

long range integral fuel tanks.

As I write this, we anticipate soon taking delivery of an A400M engine

from Airbus for us to mount and test-fly on a C-130 Hercules which has

been substantially modified for this important task. I was also delighted

that in July we were able to celebrate with Lockheed Martin and

the Royal Air Force the fortieth anniversary of our support for the

C-130, which has been such a success story for all of us and the nation.

At Cambridge Airport we have seen a major increase in the number of

executive jets and are ourselves participating in the rapid growth of this

sector with our work for NetJets on Citations.

Michael Marshall

Chairman and Chief Executive

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

C h a i r m a n ’ s S t a t e m e n t

Our Motor Group has had a further tough year but has maintained its

sales penetration levels. The prime focus has been on continuing to

provide our customers with a service second to none. We are pleased to

have reached agreement with the HM Revenue and Customs on the

repayment to us of VAT on demonstrator vehicles.

Specialist Vehicles is now building up its production of the bodies for the

MoD Support Vehicle contract with MAN at our new facility at

Mildenhall, close to the RAF Station which is used by the USAF. We are

involved in a number of important MoD manufacturing and logistics

support programmes.

Marshall Thermo King and VTR, now under the Chairmanship of my son

Robert and led by Nigel Faben, have consolidated their headquarters in

the Quorum building next to Cambridge Airport, from which, with their

twelve depots and one hundred mobile workshops, we are positioning to

provide a first rate service to our customers.

As a result of the increase in profits and reserves, the Board recommends

that the final dividend should be increased to 14p, thereby making a

total payment for the year of 19p.

We have built further on our strong links with the community and have

continued to support many local activities and schools. We have also

maintained our participation in national organisations and charities in the

industries of which we are a part.

Our staff continue to work enthusiastically and I am grateful for all their

support. I was very pleased that John Lander was awarded the MBE in

the New Year’s Honours List for his splendid work in training and leading

apprentices working on our aircraft modernisation programmes.

I am sad, that after almost 52 years work with the Company and 42 years

on the Board of our Group, Peter Hedderwick has finally decided to

retire from the Board at the AGM, at the end of his current term. Peter

has enjoyed the trust of all of us, including my father, and provided a

vital link during the years of transition to me and the next generation of

management. His wise contributions to the development of the business,

and particularly the Aerospace business in which he spent the major part

of his career, will be greatly missed. We are enormously grateful to him

for all that he has done for our Group.

I would again like to thank our shareholders for their encouragement,

our non-executive directors for their support and guidance, and above all

our executive directors, management and staff who continue to ensure

that, whenever possible, we exceed our customers’ expectations. As

always, delighted customers underpin all our endeavours.

5

M a r s h a l l A e r o s p a c e

Turnover was up by 61% on 2005 and the company returned to profit,

recording by far its best result for several years. The most important

element underpinning this growth and improvement was the securing

of a contract with the UK MoD, at the end of May 2006, to provide

enhanced levels of service in support of the Royal Air Force fleet of

C-130 Hercules aircraft.

This programme known as Hercules Integrated Operational Support

(HIOS) tasks Marshall Aerospace to provide support through to the

planned retirement date for the C-130J aircraft (currently 2030) and

requires the company to deliver maintenance, logistic and technical

services sufficient to ensure a set level of daily availability. In

delivering these services the company is partnered with Lockheed

Martin, Rolls-Royce and the MoD Hercules Integrated Project Team,

with Marshall Aerospace taking the lead management role.

Personnel from all the organisations are centred at Cambridge and

new office facilities have been built to cater for the joint working

teams. The contract has a headline value for Marshall Aerospace of

£1.4bn and will save MoD some £171m, over the life of the contract,

as compared with the pre-existing arrangements. HIOS represents a

ground breaking way of working between Industry and Government

and the reputation of Marshall Aerospace has been greatly enhanced

through this innovative approach to partnership.

The company believes that there will be extensive opportunities to

extend the concept of integrated operational support to new and

existing customers and this forms one of the three legs to our

strategy going forward.

The second leg is based on the provision of technology services.

During the course of the last year we have made considerable

progress, in particular in developing our business of providing

specialist fuel tanks. We are now the selected supplier to Boeing on

the 777-200 LR Civil airliner and on the US Navy P8A Multi-

Mission military aircraft. In addition we are undertaking

preliminary design work on tanks for the next generation 737-900

and Boeing Business Jet aircraft. Further opportunities exist to

become a supplier on the US Air Force KC767 military tanker

aircraft. Whilst all these programmes are in the preliminary phases

MARSHALL AVIATION SERVICES

CAMBRIDGE

AERO CLUB

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

2006 was a year of significant growth and improvement for Marshall Aerospace.

M a r s h a l l A e r o s p a c e

the potential for high volumes of production orders is good. We are

considering developing a US presence to facilitate the ongoing

delivery of these and similar programmes. Equally encouraging is the

development of our Test Business where enquiries and orders are

growing on a monthly basis.

The third leg of our strategy is based on People Services and I am

pleased to report that Aeropeople has made further strides during the

course of the last year. Of particular significance was the completion

of the acquisition of the Acetech business from Babcock plc.

This acquisition has given a boost to our customer base and the

integrated company now has an average of 400 engineers on contract

at any one time. We will look to supplement this business through

further acquisitions this year. We have also started up an Airfield

Services arm providing air traffic control, fire and airfield

management personnel.

The thrust of Marshall Aerospace strategy is to move the company over

time away from its traditional reliance on runway related volume

towards a broader range of services many of which may not be

delivered from Cambridge. In this respect, we were pleased to open

our Netherlands Design Office, based in Leiden. It is planned that

Marshall Aerospace Netherlands B.V. will be staffed by the end of 2007

with some twenty engineers. They will be carrying out tasks in support

of the Royal Netherlands Air Force and other customers in the region.

In the short to medium term, however, it is essential that Marshall

Aerospace maintains its core strength and the expansion of military

work for a wide range of customers over the past year has been helpful

in this respect. We have progressively effected an exit

from large civil aircraft maintenance where low

margins and lack of consistency of work had led

to this stream of activity

becoming unviable. We do,

however, see real prospects for expanding our Business Jet service and

maintenance business both at Cambridge and at other locations. We

are building a relationship with NetJets the world’s largest operator and

we expect to see our work on Citation aircraft more than double over

the course of the next year.

6

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

7

M a r s h a l l A e r o s p a c e

In order to focus the organisation better on delivery, the company

has undertaken a major re-organisation. We have broken down our

traditional functional organisation and created a series of business

streams focused on specific markets, each with a designated Head of

Business Unit specifically tasked with developing and growing their

area. These key positions have been staffed through a combination

of internal promotion and external recruitment. As a service

business, it is essential that we put our customers at the heart of our

approach and we continue to count customer service satisfaction as

the single most important non-financial key performance indicator

that we measure. Our customer satisfaction index score continued

to show improvement during 2006.

The expansion of business over the past year, taken together with the

efforts to develop and implement the diversification strategy, has placed

intense pressure on resource but the company has managed to cope

remarkably well despite running

below target personnel numbers

throughout the period. We have

strengthened our Human

Resources team both to help manage

the pressures and to bring all our HR processes into

line with best practice. The emphasis that the company has placed on

training over the past years is certainly standing us in good stead and,

whilst we have made a number of outside appointments during the

year, we have also been in a good position to promote internally.

In summary, Marshall Aerospace has had an extremely busy and

exciting year during which we established a more predictable

throughput of work and created a platform from which we can start to

reshape the business for the medium to long term. This will involve

significant challenges particularly in terms of resource but we are

seeing progress in a number of key areas which is encouraging.

As ever, it will be the company’s service ethic and open approach to

partnership working which will underpin these developments.

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

Martin Broadhurst

Chief Executive

9

Following a year of relocations and refurbishments, we focused during 2006 on the capabilities of our people, with a

particular emphasis on the operation and the structure of our management team in the Motor Group.

M a r s h a l l M o t o r H o l d i n g s

Our aim is to ensure that our staff have the necessary skills to move the

business forward in a demanding environment over the next decade. In

Marshall Leasing, we completed an acquisition to strengthen this

successful business.

MARSHALL MOTOR GROUP

The Motor Group is positioned as a

regional force in the retail car market. We

also successfully operate in the truck and

commercial vehicle market, but we are

particularly influenced by the

performance of the new car market.

The decline in the new car market

seen in 2005 continued into

2006, yet despite this we

achieved a number of

significant highlights during

the year, spearheaded by

the performance of our

Land Rover dealerships. The

introduction of Discovery 3 and

Range Rover Sport helped our Land Rover

branches perform above expectations. We were particularly pleased to

be rated as the number one Land Rover Dealer Group on performance

during the year in the UK.

Our Vauxhall franchises in the Group also performed well during the

year, especially the Leicester Vauxhall dealership which was the

Group’s top performing branch in 2006. The Vauxhall franchise, which

in recent years has been refocused on retail sales, has performed well

within the Group. Strong performances were also seen from our

Honda, Toyota and Nissan car operations, three brands with which we

are keen to grow our representation.

Our used car performance during the year did not quite reach the level

we had planned, with a sales shortfall in the nearly new market caused,

in our view, by extremely competitive new car pricing.

The new year has started well for our new and used car businesses

throughout the Group despite signs of upward pressure on interest

rates in early 2007. However, we are

susceptible to pressures

both on consumer

spending power and

also long term

environmental issues.

Clearly those

manufacturers involved

in producing large

prestige vehicles are continuing to work very

hard to ensure that their products lose their perception of causing

environmental damage. We have already seen a number of new

products coming through specifically designed to avoid the increasing

costs of high emissions and congestion charges.

One priority during 2006 was reinforcing the capabilities of our

management team. The management structure within head office and

R

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

10

M a r s h a l l M o t o r H o l d i n g s

the regions was reorganised during the summer, focusing on

streamlining the communication between the Motor Holdings Board

and the branch network. The subsequent performance of the Motor

Group has confirmed that these actions were timely and appropriate.

All of the senior management of the Group have embarked on a

Leadership Development programme specifically designed to help those

managers develop and bring out the best in their dealership teams. In

addition to this training, a robust system of performance reviews has

been introduced throughout the Group. We are intending to develop

further our work with Loughborough University Automotive Academy,

expanding the intake of young people to the Group, who are supported

by Marshall through their BSc degree course in Automotive Retailing.

We are continuing to measure performance of the key elements of our

business to ensure that our performance is in line with our

expectations. We have focused in particular on our market share of the

new vehicle franchises, together with measurement of our stock turns

on used vehicles based on the available display spaces, and

improvements in stock management and sales performance within our

parts business. Our two large parts wholesale operations are now

managed jointly within the Group. Our service departments are

measured on capacity utilisation and growth in labour sales and

associated products, and we appointed a Group Service Development

Manager during the year to ensure that this vital area of our business

continues to prosper. We have seen some tremendous success in the

sale of service plans, add-on products and, in particular, the

development of tyre sales across the Group.

All these key performance indicators are relevant to the business but

without customer feedback they only tell part of the story. During the

last 12 months we have sought and received feedback from 16,000

customers, a number well in excess of anything achieved by the

manufacturers. Encouragingly, when asked the key question of

whether they would recommend us to family and friends, 95% of our

customers said "yes". Whilst pleased with this result, we are not

complacent, and have worked hard to understand the reasoning

behind those who said "no".

The scale of our activity on CSI or customer research resulted in our

winning an Automotive Management award for Excellence in Customer

Service during 2006. We are currently reviewing the whole area of

communication with our customers to ensure that our contact with

them is timely and appropriate. This includes the use of email, SMS text

and the internet. We firmly believe that retention of customers and the

provision to them of a more competitive range of products and services

is the key to the future of this business.

Into 2007, we are continuing to focus sharply on the growth of our

used car business and our after sales operations. We are particularly

working on the development of "all makes servicing" plans to ensure

that capacity in our workshops is fully utilised. The issue of available

land and property to develop further businesses continues to be a

challenge. We are fortunate to have property in key locations in

many of the towns in which we operate, but further

growth and development is

certainly affected by

alternative use values

of suitable sites.

The importance of

good relationships with

our stakeholders in the

business, particularly our

customers, our suppliers and our staff, will

continue to be high on the agenda over the next few

years. We will continue to work hard to attract and retain customers,

and to ensure regular communication with them. Good relationships

with our manufacturing suppliers, together with suppliers of finance, oil,

fuel, etc, will continue to be key to the success of our business. RE

PO

RT

&

AC

CO

UN

TS

2

00

6

11

M a r s h a l l M o t o r H o l d i n g s

The relationships with our staff are crucial to our success and as the

competitive business environment puts increasing demands on them,

we endeavour to ensure that they feel valued and recognised in their

jobs. Staff retention and long service is valued in the business, and we

will continue to recognise long service and exceptional job performance

across the Group.

Marshall Leasing had another excellent year in 2006, delivering a

profit of £1.1m. This represents a 15% increase over 2005, and

shows the continued strength of the business.

During the course of the year, we acquired the vehicle assets and

staff of Gates Contract Hire. This business, a long established and

respected company, shares our focus on customer satisfaction and

retention through high service levels. Indeed, the philosophies of

both companies are remarkably similar. As a result, we are confident

that the combined business will flourish, with the Gates brand being

retained with its own market positioning. The acquisition has added

20% to our funded fleet size, and has been profitable from day one.

This growth has been particularly welcome, as the competitive

environment has remained extremely tough, with the result that

our like-for-like fleet size would otherwise have

diminished slightly.

We have seen some success in new

account opening, and are confident that

we can build on this with further new

clients throughout 2007. Meanwhile, our

focus has been placed strongly on existing

client retention. To this end, we have

developed and launched a number of new products within the year,

thereby enabling us to offer a compelling proposition to both existing

and new clients.

Amongst these, a dramatically improved short term vehicle rental service

has been introduced, and has already been widely welcomed amongst

our client base. Further developments are planned, reflecting our

determination to remain at the leading edge of our industry.

In 2007, the sales environment remains competitive. We will meet the

challenge with confidence, however, knowing that we offer a unique

combination of small company service and large corporation stability.

MARSHALL MOTOR HOLDINGS SUMMARY

Following a testing year in 2006, we have approached 2007 with a

leaner, more focused business. We will continue to look to grow our new

vehicle activities, both within the Motor Group and the Leasing business.

The success of our business however, will increasingly be underpinned

by the continued growth of our aftersales, used car, leasing and

contract hire operations and particularly by the ability of our staff to

offer exceptional customer service in every one of our locations.

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

Roger Knight

Chief Executive

13

M a r s h a l l T h e r m o K i n g

Marshall Thermo King is working hard with Thermo King to re-establish the pre-eminence of their product in the UK.

2006 saw the first significant increase in sales of Thermo King

refrigeration products in the UK for several years, following an

extended period of falling market share. This has come about as a result

of renewed support of the dealer network and improved

competitiveness of the product line. However, this increase in new unit

sales takes time to filter through to aftersales support where Marshall

Thermo King achieves most of its sales and gross margin. The result for

the year was, therefore, disappointing.

The main emphases of the year have been to: strengthen the management

team; complete the process of centralisation of business processes and

the national call centre to the new Cambridge headquarters office; and to

build the relationship with Thermo King so that we can both capitalise on

the increasing unit sales and improving market share. The ultimate aim

of this effort is, of course, to provide the customer with best in class sales

and aftersales support of the best refrigeration products in the market.

TEAM WORK

I was delighted that Nigel Faben transferred

from the Motor Group to become

Managing Director. His

experience as Financial

Director and Aftersales

Director of the Motor

Group has been ideal for

ensuring a disciplined

and spirited approach

to establishing the

Cambridge headquarters.

This included integrating all

back office systems and sales

and aftersales work scheduling

systems with the engineer field communication equipment. One of his

initial tasks was to complete and consolidate the centralisation of our Call

Centre and back office systems.

The result of this integration is a cost effective one-stop-shop service for

our refrigeration customers, for whom speed of repair and minimum

downtime of their refrigerated fleet are of paramount importance.

Over the course of the year, we have seen continuous improvement in

sales, service performance and back office efficiencies. Great credit

must go to all the team for making these difficult changes and

maintaining their focus on the customer throughout.

VTR

VTR has franchise agencies with many tail lift manufacturers, and there

are good opportunities for future expansion. In 2006 VTR improved

sales and gross profit but overall profits were depressed due to the

move at the start of the year to a new headquarters at Aldridge. We

have capacity for higher volumes of work and our efforts are being

concentrated on winning that business in 2007 and improving our

outlook as a result.

CUSTOMER SERVICE

At MTK and VTR we acknowledge that the success of our business is

directly related to the quality of service which we give to our

customers. Every effort is being made to ensure that interaction with our

customers is prompt, courteous and efficient. We can now measure

our response times, monitor periods of down time and record our "first

time fix rates" as well as providing our customers with this information

in a prompt and professional manner.

OUTLOOK

In 2007 we have the opportunity to increase sales through a

resurgence in the competitiveness of the

Thermo King product, better partnership

with Thermo King, greater emphasis on

aftersales, and through a relentless focus

on satisfying our customers’ needs.

As sales develop, we aim to increase the

numbers of tail lifts and refrigeration units

being looked after by our aftersales departments. Our ability to

provide first class support to our customers through our reinvigorated

central support and local teams will strongly affect our performance in

2007. We are determined to improve our relationships with our

customers and Thermo King which should, in turn, translate into an

improved financial performance.

Robert MarshallChairman R

EP

OR

T

& A

CC

OU

NT

S

20

06

15

M a r s h a l l S p e c i a l i s t V e h i c l e s

MSV is currently enjoying a strong order book of long term

design and production contracts for the British Army’s Support

Vehicles and the Watchkeeper aerial surveillance programme.

On the back of a stable order bank, MSV has focused on its military

customers, concentrating on the delivery and support of mission

critical systems. The company has undergone a major management

overhaul to enable employees at all levels to improve project

management controls and business systems. We have also made the

decision to locate the production of the Support Vehicles at a new

facility in Mildenhall equipped with automated welding equipment

and a state-of-the-art metal surface treatment plant. This is the most

significant investment in the company for many years and we look

forward to reaping the rewards over the 10 year life of the contract.

INVESTING IN PEOPLE

Following a comprehensive business review in early 2006, the company

has decided to concentrate on a limited number of core military and

government markets. To facilitate this, the business has been restructured

into a number of streams. Since the start of 2007, the Support Vehicle at

Mildenhall and our unmanned aerial vehicle activities at Cambridge have

been managed as separate subsidiary companies, Marshall Vehicle

Engineering Ltd and Marshall UAV Ltd respectively.

The success of these entities is dependent on the good governance of

the company as a whole and, more importantly, the people that run

them. People are at the heart of MSV’s capability. During the year

considerable progress was made in encouraging project teams to take

full responsibility for project delivery. Training has focused on

increasing cross department co-operation and project management.

A philosophy of continuous improvement is now an accepted part of

the MSV culture, and through this approach significant improvements

have been realised in the company’s bid process, procurement and

IT systems.

VEHICLE ENGINEERING

The ability to manage complex projects, delivering on time and to cost

is key to our future success. Over the past year increased emphasis has

been placed on developing our teams by way of establishing dedicated

project rooms and processes. An example of progress has been on the

design, testing and manufacture of the load beds for the Army’s Support

Vehicle Programme. This has been managed in conjunction with the

establishment of the new 120,000 square feet factory at Mildenhall,

housing one of the largest electro-phosphating plants within the UK

and state-of-the-art robotic welding equipment. This new facility has

been brought in on time and to budget.

MILITARY ENGINEERING

In our traditional markets of providing military customers with shelter

based systems and vehicle engineering, it has been a busy time with a

broad workload. We progressed well into the design and prototype phase

of the ground systems for the Watchkeeper aerial surveillance programme.

The company completed the design and manufacture of the prototype

stretcher handling system for the Boxer armoured vehicle being procured

for the Dutch Army. Other specialist shelter systems were designed and

manufactured for Sweden, reviving a long-standing relationship.

In addition to MSV’s traditionally recognised capabilities in the design

and manufacture of shelters and specialist vehicles, the company has also

demonstrated the ability to provide valuable assistance to prime

contractors in the field of human factors and safety engineering. This has

enabled MSV to engage with customers on a broad front from an early

stage in major programmes. In this respect, our specialist engineering

department at Petersfield has had a good year and has fulfilled customer

expectations and its prime role within MSV with enthusiasm and aplomb.

SUMMARY

In 2006, we used the stable order bank to restructure and rationalise the

company. We invested in our people and built up our capability to

manage large complex projects within budget and to the satisfaction of

our customers. We invested heavily in our new factory at Mildenhall

which will be unique in scale and capability in the UK. The company

has developed well in the year and is starting to meet expectations.

For 2007 the priorities will be to ensure that the investment in the Support

Vehicle at Mildenhall starts making the expected return, the continuation

of the development of our people together with the enhancement of our

project management capabilities, and the building of the long term order

bank in our key military markets.

Robert MarshallChairman

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

P r o p e r t y R e v i e w

The Carter Group has built a number of major buildings for the Group andthe most recent result of this successful relationship is Phase II of the AircraftSupport Centre which has been completed on time and within budget. TheCarter Group is another very large East Anglian family-owned business whichalso believes in the benefits of developing long term relationships.

In the summer of 2006 the multi-million pound programme to replace theAirport Works oil fired heating system with a much more efficient localisedgas fired heating plant was completed. The improvement to the local airquality around Cambridge Airport has been welcomed by the local councils.

In the summer of 2006 the Cambridge City Local Plan was adopted and thishas confirmed that the 115 hectares of Cambridge Airport that lie within theCity boundaries should be removed from the Green Belt and allocated forhousing if the flying activities of Marshall Aerospace can be relocated.

The remainder of Cambridge Airport falls within the South CambridgeshireDistrict Council area and a Public Inquiry is due to take place in the summerof 2007 to consider the removal of the remainder of the Airport from theGreen Belt and its allocation for housing. The Council’s draft Cambridge EastArea Action Plan, which will be considered at this Public Inquiry, proposesthe building of about 10,000 houses on Marshall-owned land.

Marshall has confirmed that if the Cambridge East Area Action Plan isapproved then it will be willing to release its land for housing, providing thatsuitable alternative sites can be found for the Marshall businesses which

would need to be relocated, and that the development is of a high qualitythat enhances the City.

In 2006, Marshall Specialist Vehicles won a major contract with partners toprovide support vehicles to the British Army. To provide state-of-the-artfacilities for this important contract, MSV has established a newmanufacturing facility in Mildenhall.

This development has been enthusiastically supported by Forest HeathDistrict Council, which is also encouraging Marshall Aerospace to relocatesome of its aviation activities to land adjacent to RAF Mildenhall rather thanan alternative possible relocation site in Wyton.

We have been working in partnership with a local housing developer toredevelop a two acre site in Cambridge. In December 2006, Marshall andthe developer received planning permission for the construction of 113apartments on this site. Work is underway to refurbish and extend existingpremises on Marshall-owned land north of Newmarket Road in Cambridge toprovide space for the relocation of the businesses which are currentlyoperating from this site.

During the year the Motor Group sold surplus premises in Spalding andPeterborough which generated an exceptional profit of £153,000. Itcontinues to invest in refurbishing its premises and there was a majorrefurbishment of its Vauxhall franchise in Peterborough, which wascompleted in early 2007.

The Cambridge office and housing markets have continued to improve and asa result the directors have incorporated a revaluation increase of our propertyassets of £1.35m into the financial statements.

Jonathan Barker

Company Secretary

2006 was a year during which the property interest of the Marshall Group continued to benefit from a number

of important long term relationships.

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

16

17

C o r p o r a t e R e s p o n s i b i l i t y

The Marshall Group of Companies values its important relationships with its staff,

customers, suppliers and the local communities in which it operates.

SKILLS DEVELOPMENT

The Company’s commitment to the ongoing development of employee skills continues, recognising that

continued investment in this important area strengthens individuals and the Group’s future.

The range of skills development programmes running throughout the Company continues to extend from full

apprenticeships and induction for new starters to the honing of advanced leadership skills for senior managers

and includes the ongoing development of product, technical and management skills in all areas of the

businesses, including the BSc Degree in Automotive Retailing which the Motor Group is supporting at

Loughborough University.

Recognition on a local, national, or even international level encourages individuals and businesses to strive

for ever greater challenges and we continue to be delighted by the number of awards that recognise

individual or business success.

Our active Human Resources teams work alongside our operational management teams to help ensure

that we continue to attract, recruit and retain the very best people in the business. We seek to employ

people who reflect the diverse nature of society and we value our people and their contribution,

irrespective of their age, gender, disability, sexual orientation, race, colour, religion or ethnic origin.

COMMUNITY

Most of the Company’s employees are drawn from the local communities within which our businesses are

based. For the Motor Group, these communities are also our customers. The Group, therefore, remains

committed to the development and maintenance of close relationships with the local community at all

levels from local charitable projects to district or regional initiatives.

Marshall employees from across the Group continue to be actively involved in many aspects of local

community life in a variety of largely voluntary roles, including as school governors, magistrates, youth

organisation leader and as charity volunteers. The Group also continues to encourage employees to

support a number of national charities and events such as: the Macmillan Cancer Relief Biggest Coffee

Morning; the Red Nose Day in aid of Comic Relief; and the BBC’s Children in Need.

HEALTH, SAFETY & ENVIRONMENT

Maintaining high standards in the area of Health & Safety and the Environment remains a high priority.

We continue to invest significantly in new and revised systems and processes to ensure that we

consistently meet our obligations in each of these areas.

Globally, concern for the environment is gaining momentum; in particular regarding the impact that

mankind is having on climate change. As part of good business practice and our commitment to understand

better our role in managing our own impact on the environment, the Marshall Group continues to invest in

new initiatives to reduce the emissions generated by the Company in the course of our business. This has

included the complete upgrade of our heating systems at the Cambridge Airport site to modern, highly

efficient gas-fired boiler systems with state-of-the-art computerised thermostatic control systems.

We are very proud that Marshall Aerospace has been awarded, for the second consecutive year, a Gold

Medal by RoSPA, recognising five years of continuous improvement.

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

18

F i n a n c i a l R e v i e w

The profit before tax for the Group for 2006 was a record £18.5m.

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

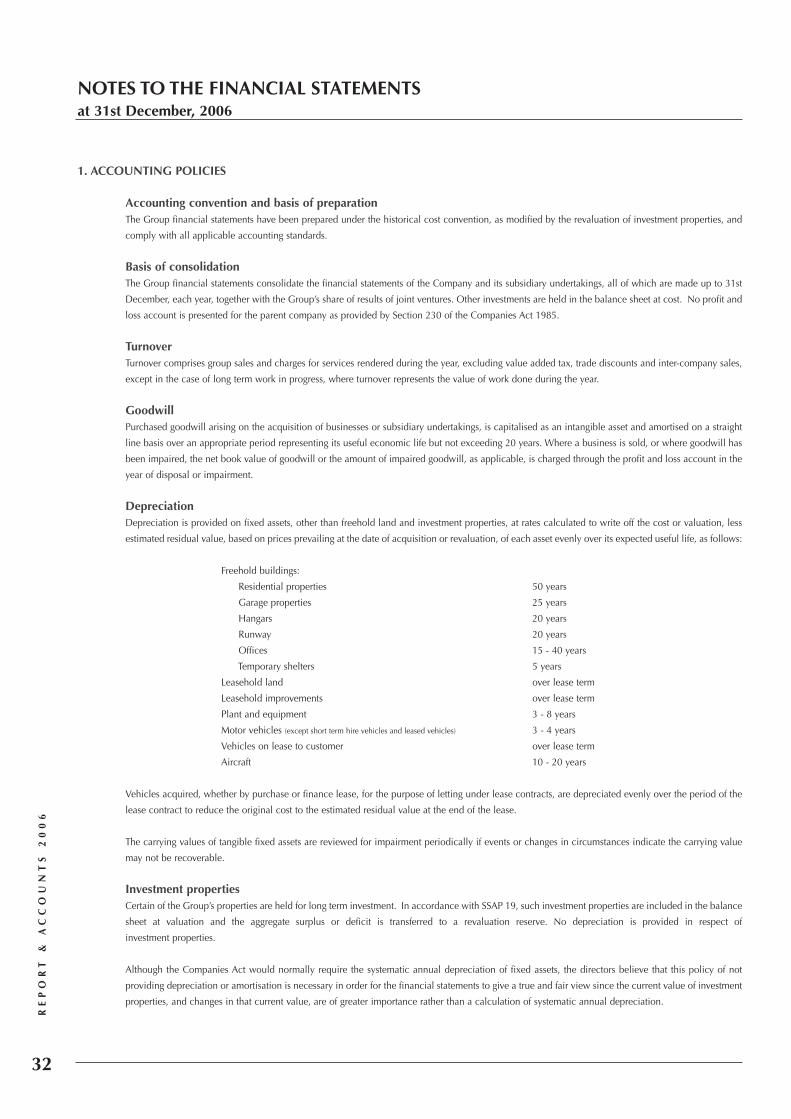

RESULTSGroup sales increased over 10% to £633m following the award of theHIOS contract to Marshall Aerospace and a general increase in activitylevels for the engineering companies, although the climate for motorretail sales remained challenging.

Gross profits increased by nearly 19% to £142m representing a returnof 22.4% on sales, well up on the 20.8% achieved in 2005. MarshallAerospace was the catalyst for this improvement, although MarshallSpecialist Vehicles saw an increase here too.

Exceptional property profits, principally on the sale of the formerVolvo premises in Peterborough and Spalding, were only £153,000but the main exceptional item, included in cost of sales, was the VATrecovery of £1.8m in respect of two claims against HMRC togetherwith interest of £2m.

The pre tax profit of £18.5m is the highest profit the Group has everreported and has been achieved with trading conditions still difficult forsome subsidiaries.

DIVIDENDSPreference dividends amounting to £744,000 were paid to preferenceshareholders during the year. The directors increased the interimdividend to ordinary shareholders in respect of 2006’s results to 5pper share and this was paid out in January, 2007. In view of the results,the Board is recommending a final dividend of 14p. This wouldrepresent a total dividend on ordinary shares of 19p in respect of 2006.If the final dividend is approved by shareholders at the AGM, it wouldbe the intention to pay this on 29th June 2007.

It is important to reiterate that, as a private company, we have limitedaccess to external funds, other than by way of borrowing or loans,generally from the banks. Accordingly, the Group has to generate andretain sufficient post-tax profits to fund future investments, as well asgrowth in the business. It is, therefore, the Group’s policy to try toensure that dividends are well covered by post tax earnings.

GROUP ACCOUNTING POLICIESThere have been no new Financial Reporting Standards to adopt in2006 so the Group’s financial statements have been drawn up on abasis consistent with previous years and in accordance with the latestrequirements applicable to us.

Shareholders will be aware from last year’s report that for the UK, and,for that matter, the rest of the EC, International Accounting Standards

(IAS) and International Financial Reporting Standards (IFRS) becamemandatory for all listed or quoted companies from 2005. Although theGroup is not required to comply, we have evaluated the implications forthe Group of adopting these Standards. No decision has, as yet, beenmade to change but the Board continues to keep this issue under review.

TAXATIONThe Group tax charge at 34.9% is above the statutory rate of 30%,principally because of certain expenses not allowed for tax and also theeffect of there being restricted allowances on the purchase of land andbuildings. The Group has been able to utilise in 2006 certain taxationlosses brought forward from 2005. A full analysis and reconciliation ofthe tax charges is given in Note 8 on page 36.

In accordance with FRS 19, the deferred tax accounting standard, wecontinue to recognise deferred tax in the financial statements. This can besimply explained as taxation charges, reliefs or benefits which will beincluded in future years’ financial statements. Where recovery is notassured, such as Industrial Building Allowances which the Government hasrecently indicated will now be phased out by 2011, an asset is not booked.

GOODWILLIntangible assets acquired in the year amounted to £0.4m as a result ofthe purchase of Acetech by Aeropeople. The policy for goodwill is tocapitalise and then write-down the assets over the years in which it isexpected results will benefit.

NET ASSETSThe Group net assets were increased to nearly £138m at the end of2006. The carrying value of the Group’s principal investmentproperty, the Quorum, rose from £9.0m to £9.5m following animprovement in the Cambridge commercial property market and therevaluation surplus of £1.3m on this, and the other investmentproperties, was credited to the revaluation reserve thereby increasingnet assets.

Group total reserves are now over £122m of which only £5.3mrepresents revaluation surpluses or capital profits.

Net current assets, namely our net working capital and cash balances,increased during the year, as the increase in profitability outstrippedcash being invested in fixed assets, which, nevertheless, increased to£113.5m (2005 - £105.5m) reflecting the continued commitment toinvest for the future.

PENSIONSThe Group’s defined benefit scheme, the “Plan” had shown a funding

4002002

£490m

£536m

£605m

£574m

£633m

2003 2004 2005 2006

450

500

550

600

650

Turnover (£m)

110

115

120

125

130

135

140

2002 2003 2004 2005 2006

Net assets (£m)

19

F i n a n c i a l R e v i e w

deficit of £2.4m in April 2005. Since then, the Group has invested afurther £0.75m and there has been an improvement in the marketssuch that at 5th April, 2006 there was a surplus of £0.8m.

For accounting purposes, however, the above valuation which informsthe Company and the Trustees of the recommended funding position,is no longer the relevant valuation methodology. FRS 17, which wasadopted fully for the first time in 2005, mandates that all liabilitiesshould be valued by reference to the yield attainable on AA ratedCorporate Bonds. This valuation takes no account of where the assetsof the pension fund are actually invested, or of the yields currently andprospectively to be earned on those assets. On this basis, the deficit at31st December 2006 (not April 2006) was estimated at £1.96m beforetax (and £1.4m after tax relief). The improvement from the £4m deficitin 2005, arose from the additional contributions and the improvementin the markets although the increase in yield on corporate bonds from4.74% in 2005, to 5.16% had a smaller impact than would beexpected. The Board and the Pension Fund Trustees are very closelyaligned in addressing and continuing to monitor and manage thefunding challenges as well as taking account of the best interests of the employees.

CASH FLOWThe Group ended 2006 with cash balances of just over £23m, anincrease of £8.5m over 2005 and a sound position. This cashimprovement was achieved without restricting any essential investmentfor the future. Rigorous reviews, however, of the return or pay back arecarried out for all capital projects, other than those deemed essential inorder to comply with operating regulations or legislative requirements.

The investment in fixed assets amounted to £29.9m compared with£31.7m in 2005. Only £1.8m of this was on property developmentswith a further £8.2m on equipment and technological improvementsand a continuing spend of £18.4m gross (£13.6m net) on the Leasingfleet including the acquisition of the Gates fleet which increased thefleet size to 3,598.

TREASURY MANAGEMENTThe Group Finance function continues to manage, centrally, our mainGroup banking relationships. It is also responsible for monitoring,controlling and reviewing the management of the Group’s loans, cash,currency and interest risk for the benefit of the Group and subsidiarycompanies. The function is not set up as a profit centre but one whichis meant to mitigate cost and risk for the benefit of the tradingsubsidiaries in the Group.

The Group, once again, became a net receiver of interest reflecting thehigher level of cash balances throughout the year, as well as interestrelating to the tax rebate.

Group borrowings were largely stable in the year, reducing slightlyfrom £25.6m to £24.8m. The main movements were in Leasing loans,whilst a further £1m was repaid on the loan taken out in 2003 to helpfund the purchase of the TMS assets. Notes 19 and 28 give furtheranalysis of loans and cash flow.

The Group trades not only in Sterling but in a number of othercurrencies, principally US Dollars and the Euro. Managementendeavours to identify, monitor, measure and control likely currencyexposures within the Group’s trading operations. Where it is possibleto protect trading margins against the adverse impact of currencymovements, forward exchange cover is considered.

KEY PERFORMANCE INDICATORSThere are a number of Key Performance Indicators ("KPIs") bothfinancial and non-financial used by the individual companies to gaugeperformance. The diversity of the nature of the Group’s businessesmeans that few are applicable for every company. Accordingly, as aGroup, we set a number of specific KPIs against which we canmonitor individual or Group performance in the monthly managementaccounts. These are measured and reported on monthly to the Board.

The principal measures used to monitor the Group’s results areachieving a minimum return on capital employed of 12.5% and areturn on sales of at least 2% which were both accomplished in 2006.At company level, the former remains a target but the latter is too higha threshold for the motor retail businesses and too low a target for theengineering companies and therefore only works as an amalgam forthe Group.

There are also two primary cash measures. The first is for the Group tobe cash generative in any three year period after allowing for normalcapital expenditure but excluding acquisitions or major developments.The second target is to ensure that available cash and borrowingfacilities are at least 5% of turnover. Again, in 2006 both of thesewere achieved. All subsidiary companies are monitored on their cashgenerative performance and use of Group facilities.

Non-financial KPIs, particularly customer satisfaction measures, arereferred to in the various subsidiary operating reviews.

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

Bill Dastur

Group Financial Director

28%3%(4%)

(45%)

(27%)

(24%)

62%

Land & buildings

Plant & machinery

Motor vehicles

Hire & Leasing fleet

7%

2006 (2005) Capital expenditure analysis

15

20

25

30

35

2002 2003 2004 2005 2006

Gross capital expenditure (£m)

CORPORATE GOVERNANCE

The Combined Code on Corporate Governance applies only to those

companies listed on the London Stock Exchange which are obliged to

implement the various guidelines. However, the Group continues to

endeavour to apply the highest standards of corporate governance and

has implemented the recommendations, where it is considered both

practical and appropriate for a private company.

Set out below are the arrangements which have applied during 2006.

THE WORKINGS OF THE BOARD

Eleven directors served during the year, ten at the year end, including

five experienced non-executive directors. The Board has overall

responsibility for the Group; it is responsible for setting the Group’s

strategic aims, ensuring that sufficient resources are available for the

Group to meet its objectives as well as monitoring executive

management. The Board is accountable to the shareholders for the

performance and activities of the Group.

The Board has a formal schedule of matters required to be brought to

it for its decision. Such matters include: monitoring the Group’s

businesses and their performance; developing strategy; approval of

major investments, acquisitions and disposals; approval of major

contracts, board and senior management appointments; corporate

governance; dividend policy; and the endorsement of Group policy in

important areas.

The Board delegates executive responsibility to management for the

Group’s performance in order to ensure that the business is managed

in a fit and proper manner in keeping with its values and business

principles. The Board has put in place an organisational structure with

formally defined lines of responsibility and there are clear limits on the

authority, which the Group’s businesses and individuals have, to make

financial commitments. Directors receive detailed briefing papers,

including monthly management accounts prior to each meeting to

enable them to perform their role effectively.

The Board and its principal committees met regularly during the year.

The timetable is set at the beginning of the year so as to ensure that

sufficient regular meetings are scheduled and other meetings held, as

required, in order for the Board and the committees to discharge their

respective duties sufficiently. In 2006, in addition to the AGM, the

Board held ten regular meetings.

The Board has established procedures to allow individual directors to

seek independent professional advice at the Company’s expense for

the furtherance of their duties. All directors have access to the services

of the Company Secretary who is responsible for ensuring compliance

with relevant procedures, rules and regulations. There are also

procedures in place for the induction and training of new directors.

BOARD INDEPENDENCE

The non-executives bring a wide range of experience to the Board and

participate fully in key decisions facing the Group. They are all

considered by the Board to be independent of management and free

from any business, or other relationship, which could materially

interfere with the exercise of independent judgement.

PDN Hedderwick and JCG Stancliffe were appointed to the Board in

1965 and 1992 respectively. Their length of service exceeds the nine

years referred to in the Combined Code. The Board considers,

however, that the experience and long association of both the

directors with the Group provide a valuable contribution to the

Board, given the long term nature of the business. In particular, they

have both continued to demonstrate a strong independence of

management in the manner in which they discharge their

responsibilities as directors. Accordingly, the Board has decided that,

in the absence of any other relevant factors, both should be

considered independent non-executive directors.

In the few instances where a director has not been able to attend a

Board or committee meeting, this has been due to a prior commitment

or for reason of illness. In such circumstances, it has been the normal

practice for his/her comments on the papers to be relayed to the

chairman in advance. The number of meetings of the Board and the

Audit Committee, held during the year, and directors’ attendance

thereat, is given below:

DIRECTORS’ ATTENDANCE AT MEETINGS OF THE BOARD AND

AUDIT COMMITTEE DURING 2006

20

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

C o r p o r a t e G o v e r n a n c e

Meetings Holdings Board Audit Committee Attended Held* Attended Held*

MJ Marshall 10 10NV Barber 9 10MT Broadhurst 10 10WCM Dastur 10 10PDN Hedderwick 10 10RM Knight 10 10RD Marshall 8 10Sir Ralph Robins 8 10 4 4FAL Robinson 4 5 2 2SJ Sillars 10 10JCG Stancliffe 10 10 4 4

*During the period a director was in office or a member of the audit committee

21

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

C o r p o r a t e G o v e r n a n c e

DIRECTORS’ AND OFFICERS’ LIABILITY INSURANCE

The company purchased and maintained a directors’ and officers’

liability insurance policy throughout 2006. Although a director’s

defence costs may be met, neither the company’s indemnity nor

insurance provides cover in the event that he or she is proved to have

acted fraudulently or dishonestly.

BOARD COMMITTEES

In accordance with the principles of good corporate governance, the

following committees, all of which have written terms of reference,

have been established by the Board.

AUDIT COMMITTEE

The Audit Committee met four times during 2006. Its members are

independent, non-executive directors under the chairmanship of JCG

Stancliffe. While the audit committee members are not considered to

have "recent" financial experience, as recommended by the Combined

Code, in common with all the non-executive directors, the members

of the Audit Committee are experienced individuals, and the Board

considers that they have the requisite skills and attributes to enable the

Audit Committee to properly discharge its responsibilities.

A key function of the Audit Committee is to monitor the control

environment through reports to it from the Group Finance function

and the internal and external auditors. Its responsibilities include

advising and reporting to the Board after each meeting on its review of

the internal and external audit processes, presentation of the financial

results, the review of the success of any major capital acquisition or

capital expenditure, the review of progress on major contracts and

reviewing the performance, independence and objectivity of the

external auditors.

The Group Financial Director, the external audit partner and the

internal auditor attend each meeting at the request of the committee

chairman. The committee also met with the external auditor, without

the executive management being present.

The committee received reports from the Group Financial Director

concerning the Group’s accounting treatment of various issues

including provisions, pensions and the revaluation of fixed assets. The

committee were satisfied that such liabilities and contingencies were

appropriately reflected in the financial results.

The committee evaluated the performance of the external auditors and

enquired into their independence and objectivity. The external auditors

are engaged to express an opinion on the financial statements. They

review and test the systems of internal financial control and the data

contained in the financial statements to the extent necessary to express

their audit opinion. They discuss with management the reporting of

operational results and the financial position of the Group and present

their findings to the Audit Committee. The auditors regularly rotate the

partners assigned to the audit. In 2007, the Group has been advised

that the current engagement partner who has completed six years on

the audit will be replaced. After review, the Audit Committee has

recommended to the Board that the re-appointment of the auditors be

proposed to shareholders at the Annual General Meeting to be held in

2007. Internal audit’s work is focused on areas of priority as identified

by the risk profiles. During the year, internal audit has, in conjunction

with the management teams of each of the subsidiaries, continued to

develop the risk profiles for those operating subsidiaries, together with

a group level risk assessment. These assessments have enabled the

Audit Committee to review the effectiveness of the system of internal

control in operation for managing significant risks throughout the year.

The reports describe the significant risks identified together with an

assessment of the effectiveness of management’s controls. The

continuing development of the systems and processes to identify,

manage and address these risks is also covered.

The committee approved the annual internal audit plan to be

undertaken during the year. Regular reports of audit findings and

management responses were reviewed in detail. Discussions of these

reports contributed to the committee’s view of the effectiveness of

company’s internal control framework.

NOMINATIONS COMMITTEE

The Nominations Committee which met twice during the year has

responsibility for overseeing that appropriate procedures are in place

for the nomination, selection and training of directors as well as

ensuring the right balance between executive and non-executive

directors with an appropriate blend of skills and training. All new

appointments to the board are based on the recommendation of the

Chairman and Nominations Committee and approved by the entire

board. There are also procedures in place for the proper induction and

training of new directors.

EXECUTIVE REMUNERATION

The Chairman has a Remuneration Committee to advise him in the

process of setting and reviewing executive remuneration. This met on

two occasions during 2006. Operating subsidiary Chief Executives and

the Group Financial Director have service contracts, which are

terminable by no longer than twelve months’ notice given by either

party thereto.

22

C o r p o r a t e G o v e r n a n c e

AGM

The Chairman, the executive directors and board committee chairmen

were present at the 2006 AGM and available to answer shareholders’

questions or to hear their views.

INTERNAL CONTROL

The Board has established what it believes is an appropriate control

environment through the definition of the organisational structure and

authority levels.

The key features of the Group’s internal control system are: an

organisational structure at head office and at subsidiary level which

clearly defines responsibilities; an annual budgeting process,

supported by regular forecasts; monthly detailed management

accounts with a report to the Board; an internal audit function; control

of capital expenditure through budgets and authorisation levels;

defined procedures for investment and treasury management; detailed

matrix levels of authority; Board approval of significant investments,

acquisitions and disposals; and policies for health, safety and

environment which are applicable to the whole Group.

During the year, the Audit Committee received and reviewed reports

from both the internal and external auditors. In the Board’s view, the

information the Board received was sufficient to enable it to review the

effectiveness of the systems of internal control.

GOING CONCERN

In accordance with the Combined Code, the directors, having made

appropriate enquiries, consider that adequate resources exist for the

Group to continue in operational existence for the foreseeable future

and that, therefore, it is appropriate to adopt the going concern basis

in preparing the financial statements.

ETHICS POLICY

In 2006, the Board approved and issued a Code of Business Ethics to

all employees of the Group. This document sought to encapsulate and

combine in one document the various Group policies and guidelines

in place. It seeks to ensure the Group’s commitment to the highest

ethical standards in all its dealings and provides a framework and

decision tree to guide members of staff. There is also a confidential

disclosure mechanism for reporting serious breaches of this code.

HEALTH & SAFETY POLICY

The Group is committed to safeguarding the health and safety of its

employees, customers, contractors and visitors to the Group’s premises,

and the community. Subsidiaries employ health and safety advisers for

the implementation of the Group’s health and safety policies. The

Group’s policies are kept under review and include procedures that:

• Ensure that all sites meet all legal and company health and

safety requirement;

• Strive to eliminate unsafe practices at all locations;

• Promote high standards of safety awareness through

employee involvement and management commitment at

each location;

• Minimise danger to local communities; and

• Provide an immediate and effective response in the event of

accidents and emergencies.

THE ENVIRONMENT

All Marshall operating companies are required to conform to the

relevant legislation and codes of practice. In addition, companies

adopt integrated environmental management systems which

specifically focus on minimising pollution by:

• Controlling emissions to air, land and water;

• Reducing the consumption of energy;

• Managing waste to maximise re-cycling;

• Improving the awareness of, and training to, employees in

environmental best practice.

ADVISERS

AUDITORS Ernst & Young LLP SOLICITORS Greenwoods / Rustons & Lloyd / Eversheds / Bird & Bird BANKERS Barclays Bank PLC

PROPERTY ADVISERS Bidwells PENSION AND ACTUARIAL ADVISERS Buck Consultants INSURANCE BROKERS Willis

REGISTERED OFFICE Airport House Newmarket Road Cambridge CB5 8RY REGISTERED NUMBER 2051460

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

EXECUTIVE DIRECTORS NON-EXECUTIVE DIRECTORS

M.J. MARSHALL CBE DL * o

Appointed to main Board in 1960

Having joined the Group in 1955, he was appointed aDirector in 1957. In 1963 he was appointed ManagingDirector of the Motor Group. In 1990, he became Chairmanand Chief Executive of the whole Group. He is a DeputyLieutenant of Cambridgeshire, Honorary Air Commodore ofNo 2623 (East Anglian) Squadron RAuxAF, President of TheAir League, a Fellow of the Royal Aeronautical Society, aCompanion of the Institute of Management and a VicePresident of the Institute of the Motor Industry and of theEngineering Employers’ Federation, and President of theFund for Addenbrooke’s. Aged 75.

M.T. BROADHURST OBE FRAeS C.Dir Appointed 1996

Having joined the Group in 1975, he was appointedManaging Director of Marshall Aerospace in 1996 and ChiefExecutive in 1999. He is also Chairman of Connexions forCambridgeshire and Peterborough. Aged 53.

W.C.M. DASTUR FCA Appointed 1996

Formerly a partner with Ernst & Young, he joined theGroup and the Board in 1996 as Group FinancialDirector. He acts as Chairman of the Trustees for theGroup’s various pension funds. He is also Chairman ofEly Cathedral Finance Investment Advisory Committeeand a Fellow of the Royal Society for the Encouragementof Arts, Manufactures and Commerce. Aged 54.

R.M. KNIGHT Appointed 1996

He has over 30 years of motor industry experience,working for both manufacturers and retailers, includingVolvo Concessionaires, Rover Group and Henlys. Hejoined the Group in 1989 as Regional Director, waspromoted to Managing Director of Marshall MotorHoldings in 1995 and is now Chief Executive. He sits onthe National Franchised Dealer Association StrategyCommittee and the DTI-sponsored Retail Motor StrategyGroup. Aged 58.

R.D. MARSHALL Appointed 2000

He joined Marshall Aerospace in 1995 and wasappointed a Director in 1999 before moving to MarshallSpecialist Vehicles as Chief Executive in 2000. He wasappointed Chairman of Marshall Specialist Vehicles fromJanuary 2006 and Chairman of Marshall Thermo Kingfrom January 2007. Aged 44.

COMPANY SECRETARYJ.D. BARKER AIB ACIS

Formerly with Lloyds Bank plc before joining the MarshallGroup in 1976. He is a member of the Institute of Bankersand the Institute of Chartered Secretaries andAdministrators and was appointed Company Secretary ofthe Group in 1993. He is Company Secretary of allprincipal Group companies and the Audit Committee.Aged 56.

P.D.N. HEDDERWICK CBE FRAeS Appointed 1965

Formerly Managing Director of Marshall Aerospace. Hewas appointed CBE in 1989 and elected a Fellow of theRoyal Aeronautical Society in 1995. Aged 74.

J.C.G. STANCLIFFE * ✝ Appointed 1992

Deputy Chairman of Marshall of Cambridge (Holdings)Limited and Chairman of the Audit Committee. Formerly aDirector of S. G. Warburg Group and Mercury AssetManagement Group. Aged 75.

N.V. BARBER * Appointed 2000

Formerly an Executive Director of Smiths Industries,responsible for their aerospace activities and prior to thatsuccessively Managing Director of the Weapons Systemsand Military Aircraft divisions of British Aerospace. PastPresident of the SBAC. Aged 67.

S.J. SILLARS Appointed 2004

Sarah has been the Chief Executive of The Institute ofMotor Industry since 2002. Prior to this appointment shewas the Operations Director of Anne Gray Associates aleading Management Consultancy to the Motor Industry.She is a member of the DTI's Retail Motor Strategy Group,Fellow of the IMI and a Freeman of the City of London. Aged 48.

23

T h e B o a r d

✝ Member of the Audit Committee

* Nomination Committee

oRemuneration Advisory Committee

SIR RALPH ROBINS DL FREng FRAeS ✝ oAppointed 2004

He retired as Chairman of Rolls-Royce plc in January2003, and is a former Chairman of Cable & Wireless plcand the Defence Industries Council. He is also a formerPresident of the Society of British Aerospace Companiesand Director of several international companies. He is aDeputy Lieutenant of Derbyshire and a Freeman of theCity of London. Aged 74.

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

24

DIRECTORS’ REPORT

The directors present their report and financial statements for the year ended 31st December, 2006.

RESULTS AND DIVIDENDSThe Group recorded a profit after tax and minority interests for the year of £12,060,000 (2005 - £1,816,000). An interim dividend of 5.0p was paid on 15th January, 2007and the directors recommend a final ordinary dividend in respect of the year of 14p per share, which, in accordance with FRS 21, is not shown as a liability in the financialstatements as it has been proposed after the balance sheet date and will be included in the financial statements for 2007. Preference dividends on the ‘A’ and ‘B’ preferenceshares amounting to £744,000 were accrued and paid during the year.

PRINCIPAL ACTIVITIESThe activities of the Group consist principally of the business of car and commercial vehicle sales, distribution, service, hire and associated activities, together with generalengineering connected with aircraft and military systems.

REVIEW OF THE BUSINESS AND FUTURE DEVELOPMENTSIn contrast with 2005, 2006 was a record year for the Group. The Group produced the highest pre-tax profit in its 98 year history on the back of a strong set of results fromMarshall Aerospace. Improvement in the order take position for the engineering companies in 2006 contributed to higher levels of activity and, coupled with the benefit ofcontracts won towards the end of 2005, contributed to a much improved performance. The motor retail market, nationally, fell again which was reflected in low operatingprofitability in the Motor Group, although the Leasing operations held up well and produced another good set of results. Marshall Thermo King had a difficult year withsignificant restructuring at senior management level, operations and in the administrative areas. These changes should provide a platform for a better performance in 2007.VTR fell back slightly in 2006 as it moved its headquarters into new premises and upgraded its computer support systems. Exceptional property profits were low although theresults for the Motor Group were boosted by a settlement with HMRC on a long running VAT claim in respect of demonstrator bonuses.

The Group entered 2007 with an improved long term order book for its engineering businesses, although the prospects for the motor retail market continue to remain mixedwhilst vehicle and refrigeration support activities also face a challenging and competitive environment. The Group remains focused on structuring its cost base to match currentactivity levels as well as ensuring the appropriate amounts of investment are made in its businesses, facilities and people to provide a solid base for future success. This isreinforced by the commitment to balance short term performance with long term sustainability through capital expenditure on property and infrastructure improvements aswell as a profit improvement and enhancement initiatives.

The Group uses a series of Key Performance Indicators to measure performance both at a Group and company level. These include returns on sales, return on capital employed,interest cover and cash generation measures as well as order intake, unit sales, service absorption and utilisation measures. These are explained further in the individualoperating and financial reviews earlier in this report. However, a principal measure of improving customer service and satisfaction remains paramount to all our business andunderpins the ongoing business ethos of the Group.

The Group undertakes an annual assessment of the risks and uncertainties facing the Group as a whole and each of its principal trading subsidiaries. This is carried out byoperational management and a summary of the main risks is set out below.

Further details on the Group’s principal businesses and their prospects for the future can be found in the operational reviews of the subsidiaries included earlier in this report.

RISK ASSESSMENTThe risk management process is designed to identify, manage and mitigate business risk. Regular reporting of these risks and the monitoring of actions and controls is conductedby the Audit Committee, which reports its findings to the Board. This process is described in the Corporate Governance section on pages 20 to 22.

The factors described below highlight risks and uncertainties which affect the Group but are not intended to be an exhaustive analysis of all the potential risks which may arisein the ordinary course of business or otherwise. Some risks may be unknown to the Group and other risks, currently regarded as immaterial, could turn out to be material.

Business conditions, general economy and Government policyThe profitability of the Group’s businesses could be adversely affected by a worsening of general economic conditions in the UK. Factors such as unemployment, the level ofvolatility of equity markets, interest rates, exchange rates, and inflation could all impact the markets in which we operate and reduce demand whilst action taken by the UKgovernment relating to the taxation of private cars and the availability and cost of credit could significantly affect the market for the sale of new and used motor cars. In thecase of new car sales during a period of economic downturn, there is likely to be an oversupply of vehicles leading to reduced margins. Whilst a short term worsening ineconomic conditions in the UK should not significantly adversely impact in our various aftersales business, a sustained downturn over a number of years would be likely tolead to reduced profits in these businesses. Equally, a reduction in defence spending by the Government or a change in procurement policy would have a marked impact onthe engineering businesses which could lead to reduced orders, activities and, thus, our ability to absorb fully current levels of overheads. Over a prolonged period this wouldhave a detrimental effect on performance, profitability and, possibly, employment levels.

Complexity of major projectsMarshall Aerospace and Marshall Specialist Vehicles undertake highly complex projects involving design, development and integration of major aircraft systems and military systemsrespectively. Underestimation of the technical content and requirements could lead to cost and schedule overruns impacting both financial performance and customer confidence.

Labour marketThe UK aerospace skills base is under pressure with falling numbers available in the engineering resource pool. Aerospace is a highly labour intensive industry and Marshallcontinues to invest strongly in training to protect itself from this threat to its business.

Franchises and agreementsWe operate motor car franchises as well as refrigeration and tail lift franchises and aircraft servicing agreements. Franchises are awarded to us and the failure to continue to

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

RE

PO

RT

&

AC

CO

UN

TS

2

00

6

25

DIRECTORS’ REPORT

hold franchises could result in a significant reduction in the profits of the Group due to our inability then to source new car stock to sell, perform warranty repairs or carry outmaintenance activity.

Vehicle manufacturer dependenciesWe depend on the vehicle manufacturers’ financial condition, marketing, vehicle design, production capabilities, reputation, management and industrial relations. Althoughwe do not depend on any single vehicle manufacturer, a failure by a manufacturer, as with MG Rover a few years ago, could lead to significant losses. Vehicle manufacturersprovide sales incentive, warranty and other programmes that are intended to promote new vehicle sales. A withdrawal or reduction in these programmes would have anadverse impact on our business.