Embed Size (px)

Citation preview

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 1/110

A

SUMMER PROJECT REPORT

ON

“ AN ANALYSIS OF MARKETING STRATEIGES OF RELIANCE

LIFE INSURANCE CO. LTD.”

Submitted by :-

Masoom Raza

Roll no. 8551569

Submitted for partial fulfillment of

Fourth Semester Curriculum Requirement

For the Award of Degree

BACHELOR OF BUSINESS ADMINISTRATION

(SESSION 2007-2010)

SHRI RAM COLLEGE MUZAFFARNAGAR

1

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 2/110

ACKNOWLEDGEMENT

I was privileged to be associated with a reputed group, a company and a Brand, global presence. II was privileged to be associated with a reputed group, a company and a Brand, global presence. I

would like to express immense gratitude to RELIANCE LIFE INSURANCE CO. LTD. for would like to express immense gratitude to RELIANCE LIFE INSURANCE CO. LTD. for

providing me an opportunity to complete my summer internship. I would like to express immense providing me an opportunity to complete my summer internship. I would like to express immense

gratitude to RELIANCE LIFE INSURANCE CO. LTD. for providing me an opportunity togratitude to RELIANCE LIFE INSURANCE CO. LTD. for providing me an opportunity to

complete my summer internship.complete my summer internship.

I would like to extend deep sense of gratitude to Mr. Anil Kumar Gupta (Territory manager), WhoI would like to extend deep sense of gratitude to Mr. Anil Kumar Gupta (Territory manager), Who

guided me with his experience and knowledge throughout my endeavors to do quality work.guided me with his experience and knowledge throughout my endeavors to do quality work.

I would hereby, make most of the opportunity by expressing my sincerest thanks

to Mr. B.K TYAGI (principal sir) for providing me the information. I express my gratitude to Mr. SOURABH MITTAL (HOD) who provided me with thewho provided me with the

important inputs and suggestions.important inputs and suggestions.

I would like to extend deep sense of gratitude to Ms. SWATI UPADHAYAYA (project director)I would like to extend deep sense of gratitude to Ms. SWATI UPADHAYAYA (project director)

who teachings gave me conceptual understanding and clarity of comprehension, which

ultimately made my job more easy.

I would also like to thank all the faculty members who provided me with the importantI would also like to thank all the faculty members who provided me with the important

inputs and suggestions.inputs and suggestions.

Masoom Raza

2

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 3/110

BBA 5th sem.

PREFACEPREFACE

I, Masoom Raza, being a student of BBA, of SHRI RAM COLLEGE

MUZAFFARNAGAR

The project title “AN ANALYSIS OFMARKETING STRATEGIES OF RELIANCE LIFE

INSURANCE CO. LTD. ” is the analysis of the big scale sector of communication. This project

The survey was conducted so as to analyze the marketing strategies of reliance life insurance big

scale sector prevailing in the current industry

Market research study has been conducted in order to bring out the picture of big scale

sector that exists in this industry. The differences in service quality that exists in the

market.

3

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 4/110

TABLE OF CONTENTS

PART 1 1-75

• ABOUT RELIANCE LIFE INSURANCE 1

• HISTORY OF RELIANCE INS. 7

• PRODUCTS & SERVISES OF RELIANCE INS. 17

PART 2 76-100

• INTRODUCTION OF TOPIC 76

• RESEARCH METHODLOGY 78

• OBJECTIVE 80

• DATA ANALYSIS & INTERPRETATION 81

• CONCLUSION 92

• LIMITATIONS 93

• RECOMMENDATION 94

• BIBLIOGRAPHY 95

• QUESTIONNAIRE 96

4

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 5/110

LIST OF TABLE & FIGURSES

• RELIANCE AUTOMATIC PLANAT A GLANCE 35

• THE ASSEST ALLOCATION AND INVESTMENT OBJECTIVE OF

EACH OF THE PRE-PACKAGED FUNDS 41

• THE ASSEST ALLOCATION AND INVESTMENT OBJECTIVE

UNDER THE RETURN SHIELD FUND 42

• THE ASSEST ALLOCATION AND INVESTMENT OBJECTIVE

UNDER FUND C 43

• CONVENIENT PREMIUM PAYING OPTIONS 47

• WHEN & HOW MUCH OF FIXED BENEFITS PAID 67

5

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 6/110

PART 1

6

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 7/110

ABOUT RELIANCE LIFE INSURANCE

An Overview of Its origin

Reliance Life Insurance Company Limited is a part of Reliance Capital Ltd. of the Reliance - Anil

Dhirubhai Ambani Group. The company acquired 100 per cent shareholding in AMP Sanmar Life

Insurance Company in August 2005. Taking over AMP Sanmar Life provided Reliance Life

Insurance a readymade infrastructure and a portfolio. AMP Sanmar Life Insurance was a joint

venture between AMP, Australia and the Sanmar Group. Headquartered in Chennai, AMP Sanmar

had over 90 offices across the country, 9,000 agents, and more than 900 employees.

Reliance Life Insurance Company Limited is a part of Reliance

Capital Ltd. of the Reliance - Anil Dhirubhai Ambani Group. Reliance Capital is one of India’s

leading private sector financial services companies, and ranks among the top 3 private sector

financial services and banking companies, in terms of net worth. Reliance Capital has interests in

asset management and mutual funds, stock broking, life and general insurance, proprietary

investments, private equity and other activities in financial services.

Reliance Capital Limited (RCL) is a Non-Banking Financial Company (NBFC) registered with the

Reserve Bank of India under section 45-IA of the Reserve Bank of India Act, 1934.

7

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 8/110

Human Resources

“In my book, we have no greater asset than the quality of our intellectual capital, and no greater

priority than the growth and retention of our vast pool of talent” – Anil Dhirubhai Ambani

At Reliance - Anil Dhirubhai Amabani Group, we recognise the critical role that our people play in

the success and growth of each of our businesses. It is the skill and initiative of our workforce that

sets us apart from our peers in today’s knowledge-driven economy. It is their commitment and

dedication that lends us the competitive edge, and helps us stay ahead of the curve.

Its strong team of professionals is among the youngest in the country, and consists of some of the

most dynamic, motivated and qualified individuals to be found anywhere in the world. First-rate

management graduates, highly trained engineers, top-notch financial analysts and razor sharp

accountants—we have on our rolls some of the brightest minds in the business.

Mission

Its transparent HR policies and robust processes are driven by a single overarching objective:

To attract, nurture, grow and retain the best leadership talent in every sector and industry is

which we operate.

Vision

To build a global enterprise for all our stakeholders, and

A great future for our country,

To give millions of young Indians the power to shape their destiny,

Aim

To create a team of world beaters that is:

Committed to excellence in quality,

8

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 9/110

Focused on creation and enhancement of stakeholder value

Responsive to evolving business needs and challenges

Dedicated to uphold the core values of the Group

Promise

In order to achieve our objective, we offer our people...

Growth opportunities to expand leadership capabilities

True meritocracy and freedom to choose career paths

Opportunities to develop and hone leadership and functional capabilities

An entrepreneurial environment where people can pursue their dreams

Competitive compensation

In addition, we follow a well-defined Rewards & Recognitions programme that periodically

identifies exceptional individual and team achievers among the various business functions and

verticals in the Group.

Expectations

At Reliance - Anil Dhirubhai Ambani Group, we encourage our colleagues to take leadership, at

all levels of the organization, and participate in accelerating growth of our businesses to build a

formidable enterprise.

Leaders in Reliance - Anil Dhirubhai Ambani Group are expected to…

Always keep the customers’ needs in mind and constantly innovate

Execute flawlessly and with speed

9

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 10/110

Sustain and strengthen the group’s spirit of entrepreneurship—taking ownership and accountability

for their actions

Leverage synergies to learn and build on the diverse experiences and skill sets of our various

businesses and teams

Create a true meritocracy with a pervasive commitment to transparent systems and processes

Do all this with unquestionable Integrity to ensure total compliance with the laws of the land.

Core Values

Shareholder Interest

We value the trust of shareholders, and keep their interests paramount in every business decision

we make, every choice we exercise

People Care

We possess no greater asset than the quality of our human capital and no greater priority than the

retention, growth and well-being of our vast pool of human talent

Consumer Focus

We rethink every business process, product and service from the standpoint of the consumer – so

as to exceed expectations at every touch point

Excellence in Execution

We believe in excellence of execution – in large, complex projects as much as small everyday

tasks. If something is worth doing, it is worth doing well.

10

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 11/110

Team Work

The whole is greater than the sum of its parts; in our rapidly-changing knowledge economy,

organizations can prosper only by mobilizing diverse competencies, skill sets and expertise; by

imbibing the spirit of “thinking together” -- integration is the rule, escalation is an exception

Proactive Innovation

We nurture innovation by breaking silos, encouraging cross-fertilization of ideas & flexibility of

roles and functions. We create an environment of accountability, ownership and problem-solving –

based on participative work ethic and leading-edge research

Leadership by Empowerment

We believe leadership in the new economy is about consensus building, about giving up control;

about enabling and empowering people down the line to take decisions in their areas of operation

and competence…

Social Responsibility

We believe that organizations, like individuals, depend on the support of the community for their

survival and sustenance, and must repay this generosity in the best way they can

Respect for Competition

We respect competition – because there’s more than one way of doing things right. We can learn

as much from the success of others as from our own failures.

“In this Policy, the investment risk in investment portfolio is borne by the Policy holder”

Ensure a comfortable retirement for your corporate family.

11

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 12/110

INDUSTRY PROFILE

INSURANCE INDUSTRY AN OVERVIEW

Insurance may be described as a social device to reduce or eliminate risk of life and property.

Under the plan of insurance, a large number of people associate themselves by sharing risk,

attached to individual. The risk, which can be insured against include fire, the peril of sea, death,

incident, & burglary. Any risk contingent upon these may be insured against at a premium

commensurate with the risk involved.

Insurance is actually a contract between 2 parties whereby one party called insurer undertakes in

exchange for a fixed sum called premium to pay the other party happening of a certain event.

Insurance is a contract whereby, in return for the payment of premium by the insured, the insurers

pay the financial losses suffered by the insured as a result of the occurrence of unforeseen events.

With the help of insurance, large number of people exposed to a similar risk makes contributions

to a common fund out of which the losses suffered by the unfortunate few, due to accidental

events, are made good.

This is the current scenario of the global Insurance Industry and now, let us looks at the basic

functions of insurance. While conceding that insurance is a risk-transfer tool, corporate should be

made to understand that it does not suffice merely to transfer the risk but they have to participate in

the effort of loss prevention. New but they have to participate in the effort of loss prevention. New

techniques and technology have to be adopted from time to time in order to improve performance

and this has special significance to the order to improve performance and this has special

significance to the Indian Insurance Industry.

12

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 13/110

HISTORY OF RELIANCE INSURANCE

Reliance Insurance activity in India is going on for more than 20 years. In India, life insurance in

its modern form was brought for the first time by Britishers. The Oriental Life Insurance

Company started in 1818 in Calcutta was the first to be founded in India by Europeans to help the

widows of their community. The general insurance business in India, on the other hand, can trace

its roots in Triton Insurance Company Ltd., the first general insurance company established in

the year 1850 in Calcutta by the British. The year 1870, saw the birth of first Indian insurance

company namely, Bombay Mutual Life Assurance Society. The basic aim of this company was

to insure Indian lives at normal rate since in the earlier period. Indian lives were treated as

subnormal and loaded with an extra premium of fifteen to twenty percent. However, right up to the

end of 19th century, the foreign insurance companies in India had an upper hand in matters of

Insurance business. Insuring Indian lives with 10 percent of extra premium was a common practice

prevalent in those times. The Indian Life Assurance Companies were the first to regulate the life

insurance business in 1912. In 1928, the Indian Insurance companies act enabled the government

to collect statistical information about both life and non-life insurance business. Later, the

insurance Act of 1938 was passed and Department of Insurance under authority of superintendent of

insurance was established for the administration of the Act. Up to 1939, 199 companies were working

in India. However, the period 1939-55 was marked by:

13

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 14/110

World War II resulting in hasty premium adjustments by Indian companies.

Series of amendments to the insurance Act, 1938.

Appointment of a committee under the Chairmanship of Sir Cowasji Jehanger to enquire

into and to recommend measures to check certain trends and undesirable features in the

management of insurance companies.

The findings of the sub-committee on insurance under the National Planning Commission

headed by Pt. Jawaharlal Nehru.

Partition of India.

De-valuation of rupee on September 18, 1949.

The Insurance Amendment Act.

Interest yield sagging to the lowest lend of three per cent and remaining at that level over

1947-1949.

The rate war and cut throat competition between insurance companies.

The recommendation of the ruling political party, the Indian National Congress, to the

government that the life sector insurance be nationalized, and

The founding of the Jiwanlal Chimanlal Setawad Memorial-The Federation of Insurance

Institutes.

14

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 15/110

About IRDA

Structure

• The Life Insurance Council will have an Executive Committee of 16 members of which

2 will be from the IRDA and the rest from licensed life insurers

• The Committee will set up standards of conduct and practices for efficient customer

service, advise IRDA on controlling insurers’ expenses and serve as a forum that helps

maintain healthy market conduct

• It will create and manage a process for agent examination and certification

• The Life Insurance Council is funded by the Life Insurers in India

The Purpose

• The Life Insurance Council seeks to play a significant and complementary role in

transforming India’s life insurance industry into a vibrant, trustworthy and profitable

service, helping the people of India on their journey to prosperity.

Its mission:

• To function as an active forum to aid, advise and assist insurers in maintaining high

standards of conduct and service to policyholders

• Advise the supervisory authority in the matter of controlling expenses

• Interact with the Government and other bodies on policy matters

• Actively participate in spreading insurance awareness in India

• Take steps to develop education and research insurance

15

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 16/110

• Help bring to India the benefit of the best practices in the world

The Council will

• Strive for a positive image of the industry through media, forums and opinion- makers and

enhance consumer confidence in the industry

• Assist the industry in maintaining high standards of ethics and governance

• Promote awareness regarding the role and benefits of life insurance

• Organize structured, regular and proactive discussions with Government, lawmakers and

Regulators on matters relevant to the contribution by the life insurance industry and act as

an effective liaison between them

• Conduct research on operational, economic, legislative, regulatory and customer-oriented

issues in life insurance, publish monographs on current developments in life insurance and

contribute to the development of the sector

• Set up the Mortality and Morbidity Information Bureau (MMIB) and take an active role in

its functioning

• Set up similar organizations for the benefit of the life insurance industry

• Act as a forum of interaction with organizations in other segments of the financial services

sector

• Play a leading role in insurance education, research, training, discussion forums and

conferences

• Provide help and guidance to members when necessary

• Be an active link between the Indian life insurance industry and the global markets

16

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 17/110

Legislations & Control

• Address common issues in legislation and practice. Interface with the various other

regulatory bodies on behalf of the insurance industry.

• Identify regularly the important issues to be taken up with Government and/or IRDA &

PFRDA and make presentations on behalf of the industry

• Prepare benchmarks for the industry in all areas of operation and help maintain high

standards of conduct, ethics and governance

• Take measures to prevent practices that are detrimental to the interests of the policyholders

Training & Certification

• Take up the work relating to the training, examination and certification of Agents as

provided in the Insurance Act

• Play a positive role in establishing standards, training of officials and intermediaries not

only in products and sales but also other aspects relevant to the life insurance industry and

lift the level of professionalism

• Conduct professional development programs in collaboration with international councils

and life insurance institutes

Education & Awareness

• Launch regular insurance awareness programs

• Facilitate the conducting of Continuous Development Programs for intermediaries

17

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 18/110

• Provide structured regular information to the public about the industry

• Launch an interactive website/Life Insurance Journals/newsletters

• Organize / participate in major conferences, seminars, workshops and lectures by

Indian/visiting experts on insurance and related areas

• Facilitate knowledge-exchange programs (both in India and with Councils abroad) to

develop and upgrade the skills of local insurance professionals

• Co-ordinate with educational institutions in India and overseas to encourage research,

professional development courses etc.

• Elevate the profession of insurance selling and that of the Advisor, to that of financial

analysts and planners through certification programs developed in conjunction with Indian

and International institutions

• Establish a consumer relations cell

The Promise

Strengthening the role of the insurance sector in India and creating wealth for its people… The

Life Insurance Council. A three way interaction among the insurer, the insured and Regulatory

body. A convergence of interests… and the collective voice of life insurance.

In Perspective

Indian Life Insurance Industry

• More than a century in India

• Large mobilizations of savings next only to banks

• Significant participant in the Capital Markets

18

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 19/110

• Constitutes 15% of Gross Domestic Savings

• Assets under management - more than Rs. 4,00,000 Crores

• Invested in Infrastructure - Rs. 40,000 Crores

• Employment

Employs close to 2, 00,000. Retail customers: 92%

• Agency Force

1.5 million

• Policies in force

Nearly 20 crores

• Offices

Nearly 3000 offices across India and

growing

• Growth

Penetration grew from 1.2% to 2.2% of GDP

Insurance Density grew from Rs. 280 to Rs. 600 (per capita premium)

19

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 20/110

INSURANCE SECTOR REFORMS

The insurance sector began its reform process with the passage of the IRDA (the Insurance

Regulatory and Development Authority) bill in Parliament in December 1999. However with the

setting up of IRDA, the government has once again de-regulated the sector opening it for the

private players. The entry of private players has enabled the industry to look at alternative

distribution channels. To get the maximum pie of the premium, every insurance company is

adopting new distribution and marketing strategies. The transition of the insurance industry from a

public monopoly to a competitive environment now presents very interesting challenges both to

the new players and to the customer. Not only the new players have an opportunity to test out their

various hypotheses and apply learning’s from overseas markets, the customer will have a greater

choice when it comes to choosing a provider or a solution for their needs.

BENEFIT OF INSURANCE

Insurance can be seen as a hedge against the unexpected calamities like death, theft or damage of

property due to accidents, fire etc. The insurance potential untapped means human and physical

assets unprotected and their worth unpreserved. The sense of lost worth is relatively easy to

understand in the case property. But it is difficult to view human beings from this angle. When

these two things are appreciated in their right spirit, life insurance in India will not remain simply

as one more source or avenue of savings.

20

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 21/110

The most important benefit is the identification of unexpected losses. Restoring of losses

not only rebuilds the economic viability of an organization but also strengthens the society at large.

When the uncertainty gets reduced an insured person can spend more time and energy, work with

greater concentration, resulting in higher efficiency and better performance. From the management

point of view, it is accumulation of fund for investment in the field of national priority.

Accumulation of fund stems out of a gap in in-payment timings.

This means a large amount of money remaining under the disposal of insurer for

investment in a more productive way. The other major benefit arising out of insurance is the

strengthening of small business houses. Insurance can help a small unit to get involved with those

economic activities for which resource requirement is beyond its infernally accumulated fund

and/or mobilizing capacity. The biggest beneficiary of the incoming competition in insurance will

be Indian consumers. They will have more choice of insurance schemes. At present Indians are the

most deprived insurance customers in the world, out of about 150 general insurance schemes on

the global level, only 10 per cent of them are offered by the four subsidiaries of the GIC. So

through privation consumers will get wide range of insurance products. Also claims settlement will

be hassle free and customer friendly.

CHALLENGES FOR INSURANCE SECTOR

Insurance companies in India will have to develop appropriate channels to lap this huge

market as the core of insurance business hinges on an efficient distribution.

21

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 22/110

Direct marketing is one of the most successful channels of distribution in the developed

economics. It is a great way to reach a large population. So the product should be sold

through telemarketing or direct mail.

In the insurance business cost control and ability to service large number of customers are

crucial issues. So modern technology is to be adopted to handle both the services

effectively.

Today customers are well equipped with information, so insurance company should

reposition different product by changing customer attitudes.

The actuary should be required to attend minimum number of seminars called continuous

professional development courses for financial control of the organization.

Distribution of existing insurance products is the main course of worry for insurance

companies in India. The insurance companies are using WBFCS, banks and housing

finance.

Companies for distribution do not have much control on the agents and hence lose quality in the

distribution channel. So Bank’s advisory committee, representation of agency should be licensed.

22

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 23/110

RELIANCE LIFE PRODUCTS & SERVISES

It offers need based life insurance to solutions to individuals and corporate (Individual).

Employee Benefit

Reliance Group Gratuity policy

In this policy, the investment risk in investment portfolio is borne by the policy holder

The Indian Government introduced the Payment of Gratuity Act in 1972. Generally gratuity

accrues at a rate of 15 days last drawn salary per year of service for each employee or as defined

by the trust deeds. Gratuity is payable immediately on cessation of employment, provided the

employee has continuous service of at least five years. The five year provision does not apply on

death or disablement of the employee. Gratuity by nature is a medium- to long-term liability of the

employer and accordingly an appropriate medium- to long-term investment strategy should be

adopted by trustees to match assets and liabilities.

23

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 24/110

Liability for your employees’ gratuity is often the trickiest thing to forecast accurately and manage

well. While doing so you may come across some pertinent questions: What is my true liability for

employees’ gratuity? How do I manage this liability? Am I maximizing my potential tax benefit?

Am I rewarding my most valuable employees adequately? Am I matching long-term liabilities

under Gratuity with my investment strategy? Are my Gratuity assets professionally managed?

We at Reliance Life Insurance Company Limited can be of help to find answers to most of these

very relevant questions. We can assist you to meet your obligations under the Payment of Gratuity

Act while providing innovative solutions and delivering long-term results for your investment

through our Reliance Group Gratuity Plan. You can also transfer your existing gratuity liability

managed under some other funds to Reliance Life Insurance Company Limited.

Reliance Group Gratuity Plan

This is a unit linked group Gratuity product with three different fund options, namely Capital

Secure, Growth and Balanced Funds. It enables employers / trustees with more than 20 employees

to outsource the management of their employees’ Gratuity funds and the related administration to

Reliance Life Insurance Company Limited.

Policy Conditions

Minimum/Maximum annual past service gratuity contribution – Rs.200000/no limit

Minimum/Maximum Entry Age - 18 years last birthday/64 years last birthday

Maximum Maturity Age - 65 years last birthday

Minimum Policy Term - 1 year

24

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 25/110

Minimum/maximum Insured death benefit sum assured – Rs.1000 per member/no limits

The Reliance Group Gratuity Plan is a unit linked Plan where the employer can choose for each

member past service gratuity to be paid out to the employee and a level of insured death benefit,

subject to a minimum insured death benefit of Rs.1000 per member. This insurance premium will

be quoted by us and will be payable over and above the past service gratuity liability contributions.

Each past service gratuity liability contribution received will be utilized to purchase units in the

unit-linked funds chosen by the employer / trustees. The fund options have different time horizons,

risk profiles and return levels.

Capital Secure Fund: The investment objective of the Capital Secure fund is to maintain the value

of all past service gratuity liability contributions (net of charges). The current asset allocation

Limits are:

100% Government securities and bank deposits with duration of less than 180 days. Time horizon

– Short, Risk Level – Low, Level of expected returns – Low

The contributions in Capital Secure Fund must not exceed 20% of the total allocated contributions

at any time.

Balanced Fund:

The investment objective of the balanced fund is to provide policyholders with investment returns

which exceed the rate of inflation in the long term while maintaining a low probability of negative

investment returns. The current asset allocation limits are: 80% min Government securities and

25

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 26/110

corporate bonds & 20% max Equities. Time horizon – Medium, Risk Level – Low-medium, Level

of expected returns - Medium

Growth Fund:

The investment objective of the Growth fund is to provide policyholders with investment returns

which exceed the rate of inflation in the long term while maintaining a moderate probability of

negative investment returns. The current asset allocation limits are 60% min in Government

securities, corporate bonds and bank deposits & 40% max in Equities. Time horizon – Long, Risk

Level – Medium-High, Level of expected returns - Medium

Unit Pricing:

The unit price of each fund will be calculated on a daily basis. Unit Value = Total Market Value of

assets plus/less expenses incurred in the purchase/sale of assets plus Current Assets plus any

accrued income net of fund management charges less Current Liabilities less Provision

Total Number of units on issue (before any new units are allocated / redeemed)

The unit pricing shall be computed based on whether the company is purchasing (appropriation

price) or selling (expropriation price) the assets in order to meet the day to day transactions of unit

allocations and unit redemptions i.e. the company shall be required to sell/purchase the assets if

unit redemptions/allocations exceed unit allocations/redemptions at the valuation date.

The Appropriation price shall apply in a situation when the company is required to purchase the

assets to allocate the units at the valuation date as stated above. This shall be the amount of money

that the company should put into the fund in respect of each unit it allocates in order to preserve

the interests of the existing unit holders

26

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 27/110

The Expropriation price shall apply in a situation when the company is required to sell assets to

redeem the units at the valuation date as stated above. This shall be the amount of money that the

company should take out of the fund in respect of each unit it cancels in order to preserve the

interests of the continuing unit holders.

Allocation of units:

The company applies premiums to allocate units in one or more of the unit-linked funds in the

proportions which the policyholder specifies. In case of New Business, units shall only be

allocated on the day the proposal is completed and results into a policy by the application of

money towards premium. In the case of renewal premiums, the premium will be adjusted on the

due date, whether or not it has been received in advance. (This assumes that the full stipulated

premium is received on the due date.)

In respect of premiums received or funds switched up to 4.15 p.m. by the company along with a

local cheque or a demand draft payable at par at the place where the premium is received, the

closing NAV of the day on which the premium is received or funds switched, shall be applicable.

In respect of premiums received after 4.15 p.m. by the company along with a local cheque or a

demand draft payable at par at the place where the premium is received, the closing NAV of the

next business day shall be applicable.

27

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 28/110

In respect of premiums received with outstation cheques or demand drafts at the place where the

premium is received, the closing NAV of the day on which cheques / demand draft is realized shall

be applicable.

Redemptions

In respect of valid applications received (e.g. surrender, benefit payment, switch out etc) up to 4.15

p.m. by the insurer, the same day’s closing NAV shall be applicable. In respect of valid

applications received (e.g. surrender, benefit payment, switch out etc) after 4.15 p.m. by the

insurer, the closing NAV of the next business day shall be applicable. The NAV for each

segregated fund provided under this product shall be made available to the public in the print

media on a daily basis. The NAV will also be displayed in the web portal of the company.

Benefits under the Plan

The exact benefits for a scheme under this Plan will depend on the individual employer’s gratuity

scheme. Generally, the contingencies for benefit payment and the benefit level will be as given

below:

Death of employee in service– past service gratuity plus insured death benefit amount

Disability of employee in service - past service gratuity

Retirement of employee – past service gratuity

Resignation / early termination of service of the employee: past service gratuity

Surrender of Policy

28

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 29/110

If the employer / trustees decide to surrender their policy, Reliance Life Insurance Company Ltd.

will pay a surrender benefit equal to the fund value minus the surrender charges, if any.

All benefits, except for insured death benefit amount, shall be payable by canceling units at the

prevailing unit price. The liability of the insurer for a scheme will be limited to the fund value plus

the insured death benefit amount under the scheme.

Discontinuance of Insurance Premium payment

A policy shall lapse if insurance Premiums along with Gratuity Contributions are not paid within

the grace period of 30 days.Under a lapsed policy, the life cover will continue. The insurance

premium will be collected by canceling units. The policy will continue to participate in the

performance of unit funds chosen by the policyholder.

If the policy is not revived within the period of revival of 5 years from the due date of the first

unpaid premium, the surrender value, if any will be paid at the end of period allowed for revival

and the contract will be terminated.

Revival of discontinued policy

A policyholder may revive a policy by recommencing the payment of insurance premiums along

with Gratuity contributions at any time within a period of 5 years from the due date of first unpaid

insurance premium

29

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 30/110

Payment of gratuity liability contributions along with insurance premium

For a newly set up gratuity trust, the past service gratuity liability contribution can be paid either in

a lump sum or in installments spread over not more than 5 years. For an existing scheme, the

annual gratuity liability contributions along with insurance premium can be paid either in yearly or

half-yearly or quarterly or monthly installments.

Insurance Premium:

It means the amount payable to keep the insured death benefit in force. It will depend on the

attained age at start of policy year, the amount of insured death benefit and

Occupation class.

Grace Period

There is a grace period of 30 days from the due date for the payment of the insurance premium

along with gratuity contributions. If insurance premium along with gratuity contribution is payable

monthly, the grace period will be 15 days from the due date.

Switching & Contribution redirection:

Transferring (switching) assets from one investment fund to another can be done at any time. You

can make up to four switches free of charge each year. You may also redirect past service gratuity

liability contributions in future to a different asset mix. The flexibility is yours.

30

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 31/110

Charges

Fund Management Charges Fund Charge (% of funds under management)

Capital Secure Fund 0.75% per annum charged daily

Balanced Fund 0.75% per annum charged daily

Growth Fund 0.75% per annum charged daily

The fund management charges are not guaranteed. The Fund Management Charges under Capital

Secure Fund can be increased up to 2% per annum. The Fund Management Charges under

Balanced Fund and Growth Fund can be increased up to 2.5% per annum. However any changes to

the fund management charges shall be subject to Insurance Regulatory Development Authority

(IRDA) approval.

Switching charges

Transferring (switching) from one investment fund to another can be done at any time. You can

make up to four switches free of charge each year. Any switch above this will attract a charge of

0.1% of the switched amount subject to minimum of Rs.1000 per switch and maximum of Rs.5000

per switch. This charge is recovered by canceling units.

Surrender charges Year Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Onwards

Charge(% of fund value) 5% 4% 3% 2% 1% NIL

These charges are levied only if the employer / trustees decide to surrender the policy with

Reliance Life Insurance Company Limited.

Suicide Claim provisions

In case of a claim where a member has committed suicide within 12 months from the date of

inception of the scheme, whether sane or insane at that time, the company will limit the death

31

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 32/110

benefit to the past service gratuity benefit (which will be paid from the unit-linked fund of the

scheme), and will not pay any insured death benefit

Payment of taxes, stamp duties

We will deduct from benefits/insurance premium/contribution any taxes, duties or surcharges of

whatever description where levied by any statutory authority.

Reliance Group Term Assurance Policy

What is Reliance Group Term Assurance Policy?

Reliance Group Term Assurance Policy is a one year Renewable Term Assurance contract. The

benefit is payable on the happening of the contingency during one year. At the end of the year, the

contract may be renewed.

Who is Reliance Group Term Assurance Policy designed for?

Employers looking for a comprehensive professionally administered term assurance cover for their

employees. Subject to approval by the Provident Fund Commissioner, this Policy can be used as a

replacement for the Employees Deposit Linked Insurance Scheme under the Provident Fund Act.

What are the benefits provided?

A payment is made on the death of an employee. Cover can be:

Fixed multiple of salary

32

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 33/110

% of salary for each year of future service to normal retirement date

Fixed Rupee amount

Fixed Age-related scale

Formula based on designation / rank of employees in the group

If an employee becomes disabled, as defined by us, then the benefit above is accelerated and paid out

in 5 equal annual installments.

No further benefit is payable subsequently.

No benefits are payable on survival to the end of the year.

What options are available?

You can choose:

Whether or not to provide the benefit on disablement

Whether or not you wish to benefit from experience in your policy

Whether or not to give your employees the choice of continuing their cover with us under an

individual policy

What is the benefit from experience in the Policy?

At the end of every 3 policy periods, under the basis specified below, we will investigate the

claims experience under this policy. That investigation may lead us to decide that an experience

refund is due. If we declare that an experience refund is due, we will adjust it against the premium

due for the next policy period.

33

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 34/110

If it later turns out that an incorrect experience refund has been paid, the policy owner must pay

any amount owed to us. Also, we may reduce the amount we pay under any claim to reflect any

amount the policy owner owes.

Why take this policy?

Improved HR because the benefit has value to the employee

Replacement of lump sum payments with regular premiums accelerates tax relief

Statutory compliance if used to replace insurance cover under the Provident Fund Act

What do your employees get?

Coverage at rates lower than applicable to individual lives

Simplified procedures for insurability- limited or no medical tests

When benefits are not payable?

We do not pay the death benefit under this policy if the Insured Person, whether sane or insane,

dies by his or her own hand, within 12 months from the date on which his or her cover

commenced.

We do not pay the disability benefit under this policy which is caused, directly or indirectly, by:

Engaging in another occupation, unless the same has been agreed upon by us; or

Intentional self injury or illness (whether wholly or partly); or

Participation in any criminal or illegal act; or

34

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 35/110

Being under the influence of alcohol or drugs except under direction of a registered medical

practitioner; or

Racing or practicing racing of any kind other than on foot; or

flying or attempting to fly in, or using or attempting to use, an aerial device of any description,

other than as a fare paying passenger on a recognized airline or charter service; or

Participating in any riot, strike or civil commotion, active military, naval, air force, police or

similar service; or

War, invasion, act of foreign enemies, hostilities or war like operations (whether war be declared

or not), civil war, mutiny, military rising, insurrection, rebellion, military or usurped power or any

act of terrorism or violence.

Automatic Cover will apply to:

All Insured Persons who are At Work on the date of commencement of the policy; and

all of the Employer’s permanent employees who are first eligible to become an Insured Person on

or after the date of commencement of the policy and who apply to be an Insured Person within 3

months of first becoming eligible, and who are At Work on the date they first apply.

Provided that the persons in (a) and (b) above: are up to age 60;

have not been absent from work due to sickness or injury for more than 3 weeks in either of the 2

years prior to the date on which they are eligible to be insured under the Policy;

have joined the employer before attaining age 55.

Lives with cover above the automatic cover limits applicable to the group, will be underwritten

and substandard lives with medical conditions and other impairments will be underwritten as per

the underwriting manual. The basis of underwriting will be the full amount of cover, including up

to the automatic cover limit.

35

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 36/110

How will the plan be administered?

We will depend on you to provide us with details of the lives covered under the policy, in a

mutually agreeable format, showing for each member details like name, identity number, date of

birth, male / female, date of joining, salary, if absent from work, reason for the same, benefit

amount or formula for each type of benefit.

Reliance Group Superannuation Policy

“In this Policy, the investment risk in investment portfolio is borne by the Policy holder”

Ensure a comfortable retirement for your corporate family.

Why should you consider the Reliance Group Superannuation Policy?

As an employer you currently contribute 12% of each employee's salary into the Employees

Provident Fund Scheme. However, is this sufficient to provide for an adequate retirement income

for your employees?

The answer to this question is unfortunately, NO.

Firstly, your employees have the option to withdraw assets from the Provident Fund on a regular

basis to meet ongoing lifestyle expenses. Most of your employees will reach retirement age with

an inadequate balance to purchase an income stream to provide them a reasonable income on

retirement.The second reason is that employees are now retiring younger but are living longer.

36

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 37/110

Therefore the capital they need to buy an income stream is much greater than ever before, and this

increase in life expectancy will continue to grow making this gap even greater.

What does Reliance Group Superannuation Policy offer?

Superannuation is a tax effective way for employers to reward and recognize employee

performance. The Reliance Group Superannuation Policy provides you with the flexibility to

enable you to tailor your Superannuation Scheme to suit various groups of employees.

Employers can receive a full tax deduction for contributions up to 15% of an employee's salary

into the Reliance Group Superannuation Policy arrangement.

Our investment options are:

1. Capital Secure Fund:

The investment objective of the Capital Secure Fund is to maintain the value of all

contributions (net of charges) and all interest additions. The Policyholder may allocate up to

20% of their investment at any time under this fund. The asset allocation limits under this fund

are 100% Government Securities and Bank Deposits with duration of less than 180 days.

2. Balanced Fund:

The investment objective of the Balanced Fund is to provide Policyholders with investment

returns which exceed the rate of inflation in the long-term while maintaining a low probability

of negative investment returns. The asset allocation limits are: 80% minimum in Government

Securities and Corporate Bonds & 20% maximum in Equities.

37

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 38/110

3. Growth Fund:

The investment objective of the Growth Fund is to provide Policyholders with investment returns

which exceed the rate of inflation in the long-term while maintaining a moderate probability of

negative investment returns. The asset allocation limits under the fund are 60% minimum in

Government Securities, Corporate Bonds and Bank Deposits & 40% maximum in Equities.

Switching:

Transferring (switching) assets from one Investment Fund to another can be done at any time. You

can make up to four switches free of charge each year. You may redirect future contributions to a

different asset mix. The flexibility is yours.

Discontinuance of due contributions:

The contributions can be paid monthly, quarterly, half yearly or yearly. There is a grace period of

30 days (15 days if the contributions are paid monthly) for the payment of contributions.

If the payment of contributions is discontinued within 3 years from the inception of the Policy, the

Policyholder can revive the Policy within the period of revival allowed. The Policy will continue

to participate in the performance of the fund chosen by the Policyholder during this period. If the

Policy is not revived during the period of revival, the Policy will be terminated and the Surrender

Value if any shall be at the end of the allowed period of revival.

If the payment of contributions is discontinued after paying the contributions for at least three

consecutive years, the Policyholder can revive the Policy within the period of revival allowed. The

Policy will continue to participate in the performance of the fund chosen by the Policyholder. If

the Policy is not revived during the period of revival, the Policy will be terminated and the

38

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 39/110

Surrender Value, if any shall be paid at the end of the allowed period of revival. However, when

the Fund Value reaches an amount equal to

One full year’s contribution, the Contract shall be terminated by paying the Fund Value.

The Policyholder may revive the Policy at anytime during five years from the date of first unpaid

contribution by re-commencing the payment of contributions.

Individual’s plans

Reliance offers 16 individual’s plans. These are:

1. Reliance Automatic Investment Plan

2. Reliance Money Guarantee Plan

3. Reliance Endowment Plan

4. Reliance Special Endowment Plan

5. Reliance Cash Flow Plan

6. Reliance Child Plan

7. Reliance Whole Life Plan

8. Reliance Golden Years Plan

9. Reliance Golden Years Plan Value

10. Reliance Golden Years Plan Plus

11. Reliance Market Return Plan

39

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 40/110

12. Reliance Term Plan

13. Reliance Simple Term Plan

14. Reliance Special Term Plan

15. Reliance Credit Guardian Plan

16. Reliance Special Credit Guardian Plan

17. Reliance Connect To Life Plan

Details are given below of some individuals plan:-

Reliance Automatic Investment

The Key benefits of Reliance Automatic Investment Plan are as follows:

• A smart plan which adapts to your changing risk profile with increasing age

• Option to lower the average cost of units through systematic transfer of your funds

• Flexibility to switch between funds and plans

• Options for additional Insurance cover available through riders

Key Features Reliance Automatic Investment Plan

• Two plan options to choose from Ready-made and Tailor-made

• Life Stage asset allocation to ensure automatic change in investment patterns, under the

Ready-made Plan option

40

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 41/110

• Freedom to decide your own fund mix based on your risk profile under the Tailor-made

Plan

• Regular, limited, single premium paying options

• Unmatched flexibility through our ‘Exchange Option’

• Liquidity in the form of partial withdrawal

• Option to avail of Accidental Death Benefit, Accidental Total, Premium Disability and

Term Insurance riders

How does this Plan work?

As a customer you will have the liberty to choose between the Ready-made and Tailor-made Plan

options. The premium contributions made by you, net of Premium Allocation Charges and Sum

Assured Related Charges are invested in fund/funds of your choice and units are allocated

depending on the price of units for the fund/funds.

The Fund Value is the total value of units that you hold in the fund/ funds. The Mortality Charges

and Policy Administration Charges are deducted through cancellation of units, whereas the Fund

Management Charge is priced in the Unit Value.

Reliance Automatic Investment Plan at a glance

Basic Plan Minimum Maximum

Age at Entry 30 days 65 years last birthday

Age at Maturity 18 years last birthday 80 years last birthday

41

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 42/110

Premium Paying

Term

5 years 30 years

Min Sum Assured Regular / Limited Premium: Annualized Premium for 5 years or Annualised

Premium for half of the policy term, whichever higher

Single Premium 125% of the single premium amount

Max Sum Assured No Limit

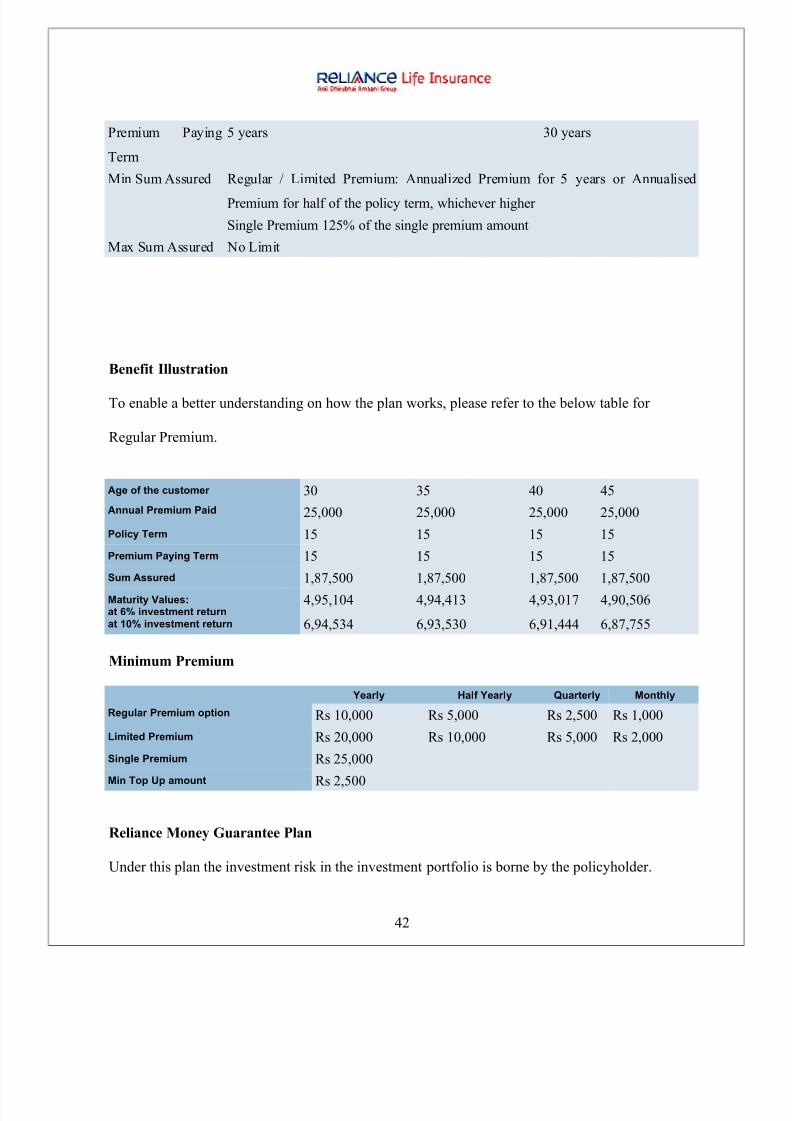

Benefit Illustration

To enable a better understanding on how the plan works, please refer to the below table for

Regular Premium.

Age of the customer 30 35 40 45

Annual Premium Paid 25,000 25,000 25,000 25,000

Policy Term 15 15 15 15

Premium Paying Term 15 15 15 15

Sum Assured 1,87,500 1,87,500 1,87,500 1,87,500

Maturity Values:at 6% investment returnat 10% investment return

4,95,104

6,94,534

4,94,413

6,93,530

4,93,017

6,91,444

4,90,506

6,87,755

Minimum Premium

Yearly Half Yearly Quarterly Monthly

Regular Premium option Rs 10,000 Rs 5,000 Rs 2,500 Rs 1,000

Limited Premium Rs 20,000 Rs 10,000 Rs 5,000 Rs 2,000

Single Premium Rs 25,000

Min Top Up amount Rs 2,500

Reliance Money Guarantee Plan

Under this plan the investment risk in the investment portfolio is borne by the policyholder.

42

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 43/110

Yes, it's a trio the pace setter plan, which promises Life Protection, an opportunity to gain control

over your investments along with protection of downside risk!

For the select few like you, the Reliance Money Guarantee Plan is a Unit Linked product

addressing comprehensive need to strike that perfect balance of Protection and Savings, that you

deserve as you grow successfully. The Reliance Money Guarantee Plan is a Regular Premium Unit

Linked Policy which guarantees the entire premium (including premiums for top- ups) paid by

you. This is a plan which helps you reap all the benefits of a rising market simultaneously

protecting you from the downside risk of the market.

Key Features

Capital Guarantee the sum of all premiums paid is guaranteed on maturity or on death before the

maturity.

Capital Guarantee is available on both the basic premiums as well as on top-up premiums

Unique Return Shield feature to protect your returns

Choice to invest from 3 pre-packaged investment fund options

Unmatched flexibility through our ‘Exchange Option’ to move between the Reliance Money

Guarantee suites of products offered, as you grow up the ladder

Liquidity in the form of partial withdrawals from top-up fund

Option to package with Accidental Death & Disability and Term Insurance riders

How does this Plan work?

The premium contributed by you net of Premium Allocation Charges and Miscellaneous Charge is

invested in fund option of your choice for a specified period of time as selected by you and units

43

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 44/110

are allocated depending on the price of units for the fund/funds. The Fund Value is the total value

of units that you hold in the fund. The Policy has a minimum Guaranteed Fund Value which is

equal to total of all premiums paid (excluding any additional and extra premiums if any), to be

payable on survival to maturity or earlier death. The amount of top-up premiums paid is also

guaranteed on death provided there is no partial withdrawal. The amount of top-ups premium is

guaranteed on maturity provided the top-ups premium was paid at least 10 years before the date of

maturity and there is no partial withdrawal. The Sum Assured under the Policy is fixed on the basis of

the selected annual premium and Policy Term.

The Mortality Charges and Policy Administration Charges are deducted through cancellation of

units whereas the Fund Management Charge is priced in the Unit Value. The premiums for riders,

if selected, are payable over and above the premium for the basic Policy .

Benefits in Details

Capital Guarantee: The plan offers Capital Guarantee provided the Policy is kept in full force by

payment of due premiums on time.

Capital Guarantee under the Basic Plan: Premiums paid under the Basic Plan are guaranteed on

the maturity of the Policy or on death during the Policy Term.

Capital Guarantee under the Top-Up premiums: Each top-up premium paid is guaranteed on

death during the Policy Term provided there are no partial withdrawals from that top-up.

Each top-up premium paid is guaranteed on maturity of the Policy provided the Policy Term is

greater than ten years, there are no partial withdrawals from that top-up and the top-up was paid

ten years before the maturity date.

44

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 45/110

Life Cover Benefit: The amount of Death Benefit depends on the age of the Life Assured at the

time of death

If the age of the Life Assured at the time of death is more than 12 years last birthday while the

Policy is in force, the Company will pay the sum of:

Higher of (Sum Assured, Fund Value as on date of intimation of death under Basic Plan,

Premiums paid under the Basic Plan excluding any extra or additional premiums paid.)

And

Higher of (Fund Value as on date of intimation of death under top- ups and top-up premium paid

provided no partial withdrawal is made from that top-up)

However if the Life Assured's age at the time of death is less than or equal to 12 years last birthday

while the Policy is in force, the Death Benefit will be the sum of:

Higher of (Fund Value as on date of intimation of death under Basic Plan and premiums paid

under the Basic Plan excluding any extra or additional premiums paid)

and

Higher of (Fund Value as on date of intimation of death under top- ups and top-up premium paid

provided no partial withdrawal is made from that top-up)

The Policy terminates on payment of the Death Benefit.

Maturity Benefit: The Maturity Benefit is the sum of Higher of (Fund Value under Basic Plan

and Premiums paid under Basic Plan excluding any extra or additional premiums paid) and

Maturity Benefit under Top-Up

If Policy Term is greater than ten years, the Maturity Benefit under top-up is the higher of ( Fund

Value under the top-up and top-up premium paid provided there is no partial withdrawal from that

top-up)If Policy Term is ten years, the Maturity Benefit under the top-up is the Fund Value under

45

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 46/110

the top-up. The Policy Terminates on payment of the Maturity Benefit. Sum assured

The fixed Sum Assured under the Basic Plan will be calculated as the amount of annual premiums

payable for half the Policy Term

Rider Benefit: You can add Accidental Death & Accidental Total and Permanent Disablement

Benefit Rider & Term Life Insurance Benefit Rider.

What are the different fund options?

Funds available in respect of Basic Plan and top-up premium

The plan offers three funds for Basic Plan and top-ups - Fund D, Fund E and Fund F. You have the

option to decide your own fund mix with respect to premiums under the Basic Plan and top-ups.

Funds available in respect of Return Shield Option

Return Shield Fund will be available if Return Shield Option is selected. The returns earned under

the Basic Plan and top-ups will be transferred to Return Shield Fund if Return Shield option is

selected.

Funds available during settlement period

If you have opted for the settlement option, then Fund C would apply by default during the

settlement period.

46

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 47/110

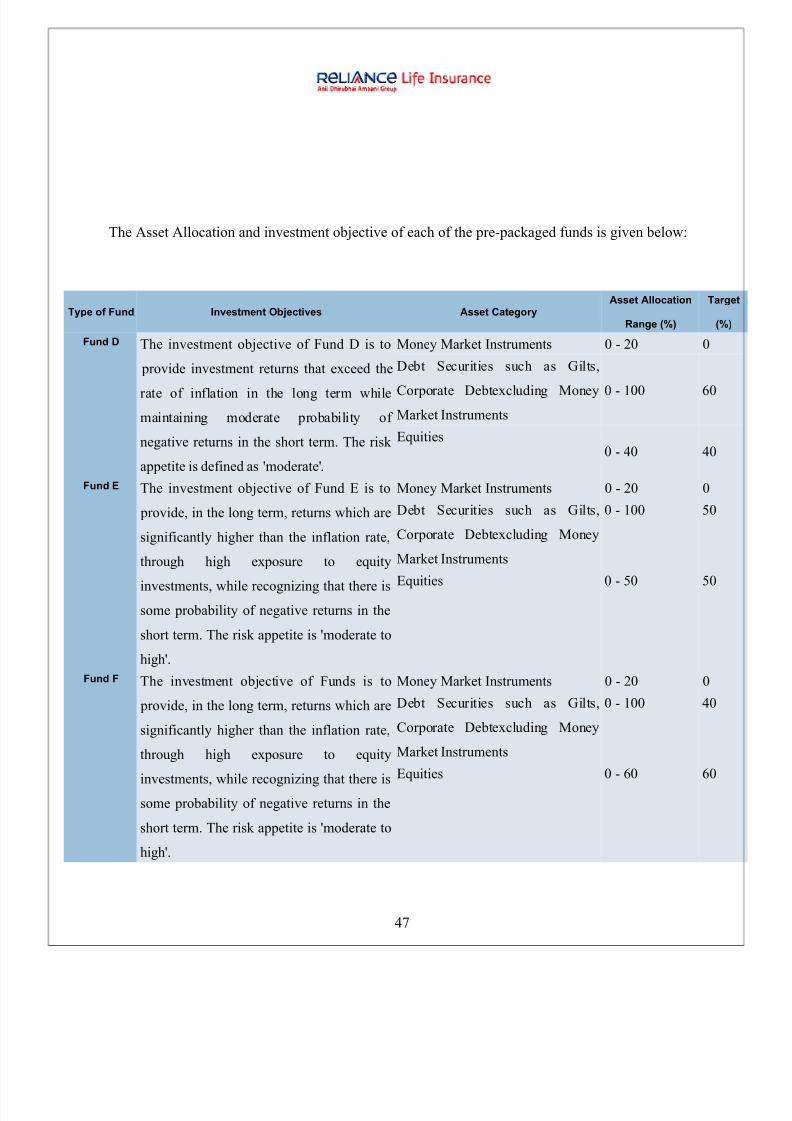

The Asset Allocation and investment objective of each of the pre-packaged funds is given below:

Type of Fund Investment Objectives Asset CategoryAsset Allocation

Range (%)

Targ

(%

Fund D The investment objective of Fund D is to

provide investment returns that exceed therate of inflation in the long term while

maintaining moderate probability of

negative returns in the short term. The risk

appetite is defined as 'moderate'.

Money Market Instruments 0 - 20 0

Debt Securities such as Gilts,

Corporate Debtexcluding Money

Market Instruments

0 - 100 60

Equities0 - 40 40

Fund E The investment objective of Fund E is to

provide, in the long term, returns which are

significantly higher than the inflation rate,

through high exposure to equity

investments, while recognizing that there is

some probability of negative returns in the

short term. The risk appetite is 'moderate to

high'.

Money Market Instruments 0 - 20 0

Debt Securities such as Gilts,

Corporate Debtexcluding Money

Market Instruments

0 - 100 50

Equities 0 - 50 50

Fund F The investment objective of Funds is to

provide, in the long term, returns which are

significantly higher than the inflation rate,

through high exposure to equity

investments, while recognizing that there is

some probability of negative returns in the

short term. The risk appetite is 'moderate to

high'.

Money Market Instruments 0 - 20 0

Debt Securities such as Gilts,

Corporate Debtexcluding Money

Market Instruments

0 - 100 40

Equities 0 - 60 60

47

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 48/110

The Asset allocation and Investment Objective under the Return Shield Fund is given below:

Type of Fund Investment Objectives Asset CategoryAsset

AllocationRange (%)

Target(%)

Return Shield The investment objective of the Return

Shield Fund is to provide steady

investment returns achieved through

100% investment in Debt Securities,

while maintaining moderate probability

of negative returns in the short term.

The risk appetite is defined as

'moderate'.

Money Market

Instruments

0 - 20 20

Government Securities

and’ approved securities0 - 100 40

Corporate Bonds and other

Debt Instruments0 - 60 40

The Asset Allocation and Investment Objective under Fund C is given below:

Type of Fund Investment Objectives Asset CategoryAsset

AllocationRange (%)

Target (%)

Fund C The investment objective of Fund C is

to provide investment returns that

exceedthe rate of inflation in the long

term while maintaining a low

probability of negative returnsin the

short term. The risk appetite is defined

as 'low to moderate'.

Money Market

Instruments

0 - 20 0

Debt Securities

such as Gilts,

Corporate

Debtexcluding

Money Market

Instruments.

0 - 100 80

Equities 0 - 20 20

Whilst, every attempt would be made to attain target levels prescribed above, it may not be

possible to maintain the prescribed “target” at all times owing to market volatility, availability of

market volumes and other related factors

48

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 49/110

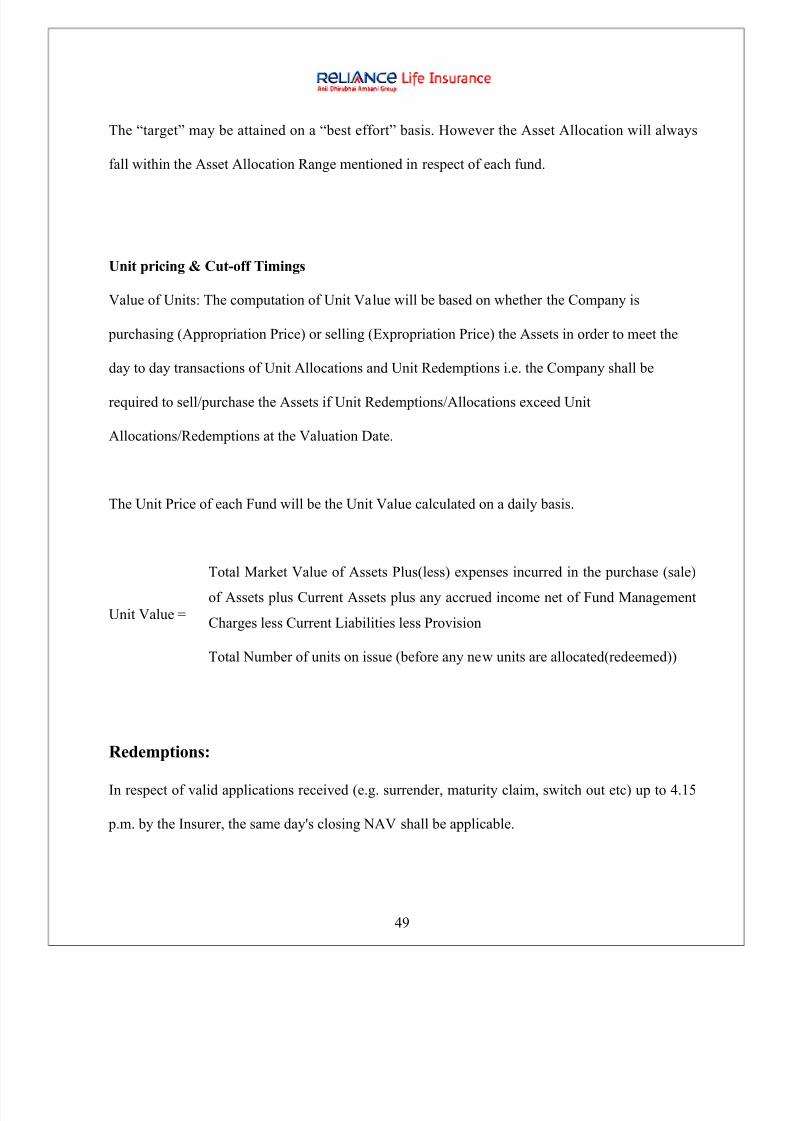

The “target” may be attained on a “best effort” basis. However the Asset Allocation will always

fall within the Asset Allocation Range mentioned in respect of each fund.

Unit pricing & Cut-off Timings

Value of Units: The computation of Unit Value will be based on whether the Company is

purchasing (Appropriation Price) or selling (Expropriation Price) the Assets in order to meet the

day to day transactions of Unit Allocations and Unit Redemptions i.e. the Company shall be

required to sell/purchase the Assets if Unit Redemptions/Allocations exceed Unit

Allocations/Redemptions at the Valuation Date.

The Unit Price of each Fund will be the Unit Value calculated on a daily basis.

Unit Value =

Total Market Value of Assets Plus(less) expenses incurred in the purchase (sale)

of Assets plus Current Assets plus any accrued income net of Fund Management

Charges less Current Liabilities less Provision

Total Number of units on issue (before any new units are allocated(redeemed))

Redemptions:

In respect of valid applications received (e.g. surrender, maturity claim, switch out etc) up to 4.15

p.m. by the Insurer, the same day's closing NAV shall be applicable.

49

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 50/110

In respect of valid applications received (e.g. surrender, maturity claim, switch etc) after 4.15 p.m.

by the Insurer, the closing NAV of the next business day shall be applicable.

Flexibility available under Reliance Money Guarantee Plan

Return Shield an innovative way to protect your returns

This option is available to you during the term of the Policy. You can select or delete this option at

any time during the term of the Policy.

There will not be any charge for the Return Shield option under following circumstances;

If the option is selected under Basic Plan on commencement of the plan

If the option is selected under top-up premium at the time of payment of top-up premium

Under all other circumstances, a fixed charge of Rs100 is payable every time the Return Shield

option is selected.

If this option is selected, the return earned on Basic Plan and Top-Ups during the month will be

transferred to Return Shield Fund at the end of the Policy month. The operation of Return Shield

option under Basic Plan is given below:

The amount of returns to be transferred to Return Shield Fund will be determined separately for

each Policyholder in respect of each of the tree funds D,E and F Fund The method used for

determining the return to be transferred is given below :

= Fund Value) on the last working day of the Policy month

Less Fund Value on last working day of the previous Policy month

Less amount of inflows during the month

The operation of Return Shield option under top-up premium(s) will be similar to that of Basic

Policy.

50

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 51/110

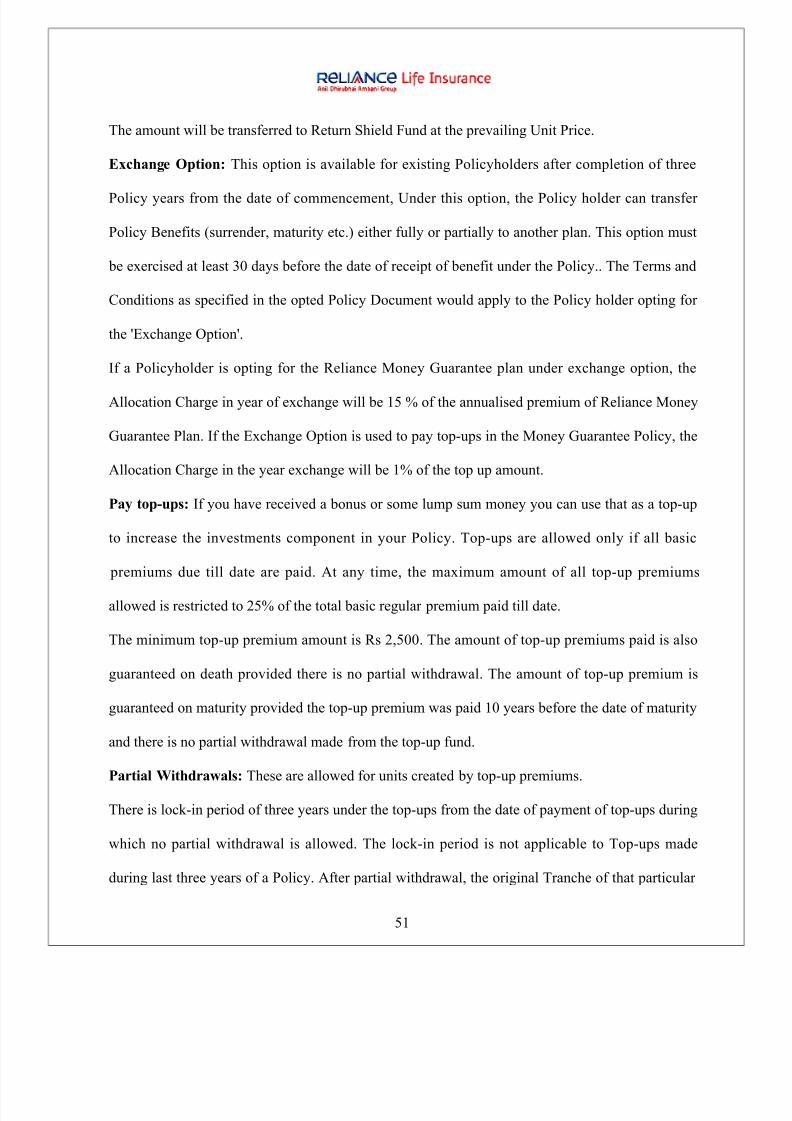

The amount will be transferred to Return Shield Fund at the prevailing Unit Price.

Exchange Option: This option is available for existing Policyholders after completion of three

Policy years from the date of commencement, Under this option, the Policy holder can transfer

Policy Benefits (surrender, maturity etc.) either fully or partially to another plan. This option must

be exercised at least 30 days before the date of receipt of benefit under the Policy.. The Terms and

Conditions as specified in the opted Policy Document would apply to the Policy holder opting for

the 'Exchange Option'.

If a Policyholder is opting for the Reliance Money Guarantee plan under exchange option, the

Allocation Charge in year of exchange will be 15 % of the annualised premium of Reliance Money

Guarantee Plan. If the Exchange Option is used to pay top-ups in the Money Guarantee Policy, the

Allocation Charge in the year exchange will be 1% of the top up amount.

Pay top-ups: If you have received a bonus or some lump sum money you can use that as a top-up

to increase the investments component in your Policy. Top-ups are allowed only if all basic

premiums due till date are paid. At any time, the maximum amount of all top-up premiums

allowed is restricted to 25% of the total basic regular premium paid till date.

The minimum top-up premium amount is Rs 2,500. The amount of top-up premiums paid is also

guaranteed on death provided there is no partial withdrawal. The amount of top-up premium is

guaranteed on maturity provided the top-up premium was paid 10 years before the date of maturity

and there is no partial withdrawal made from the top-up fund.

Partial Withdrawals: These are allowed for units created by top-up premiums.

There is lock-in period of three years under the top-ups from the date of payment of top-ups during

which no partial withdrawal is allowed. The lock-in period is not applicable to Top-ups made

during last three years of a Policy. After partial withdrawal, the original Tranche of that particular

51

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 52/110

top-up will lose the Capital Guarantee. Where Life Assured is minor, partial withdrawals will be

allowed only after completion of age 18 years.

No partial withdrawals are allowed for basic regular premium funds.

Switching Option: You can switch the whole or part of the funds between funds D, E, F at any

time during the Policy Term. You can also switch from Return Shield option to any one fund D, E

and F. First four switches in any Policy year are free.

If Return Shield option is selected switching from any of the funds D, E, F in to Return Shield

option will be done at the end of every Policy month. Such switches will not be counted as part of

the four free switches during the Policy year.

Premium Redirection: You may instruct us in writing to redirect all the future premiums under a

Policy in an alternative proportion to the various Unit Funds available. Redirection will not affect

the allocation of premium(s) paid prior to the request.

Settlement Options: This option enables you to take the maturity proceeds in the form of

periodical payments after the Maturity Date instead of a lump sum on the Maturity Date. You can

choose to redeem the units in your Unit Fund anytime up to 5 years from the date of maturity.

Capital Guarantee is not available during this period.

During this period, there will be no Life Cover. The only fund option available during the

settlement period is Fund C. The maturity proceeds will automatically be transferred in to Fund C

if settlement option is selected. The Policy will participate in the performance of units of Fund C.

The Company will deduct Policy Administration Charges by cancellation of units. The Fund

Management Charge will be priced in the Unit Value.

52

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 53/110

In the event of death during settlement period the Fund Value as on the date of intimation at the

office will be paid to the nominee. ?In order to opt for this option the customer has to give notice

of 30 days to the Company before the Maturity Date.

During the settlement period, the investments made in the Unit Funds are subject to investment

risks associated with Capital Markets and the Unit Prices may go up or down based on the

performance of the fund and the factors influencing the Capital Market, and the Policyholder is

responsible for his / her decisions. The investment risk during the settlement period will be borne

by the Policyholder.

Convenient Premium Paying options

you can pay the regular premiums in yearly, half yearly, quarterly and monthly mode and pay by

cash, cheque, debit/credit card, ECS & direct debit.

The minimum regular premium is Rs 10,000 for annual mode, Rs 5,000 for half-yearly, Rs 2,500

for quarterly and Rs 1,000 for monthly mode. The minimum top-up premium is Rs 2,500.

53

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 54/110

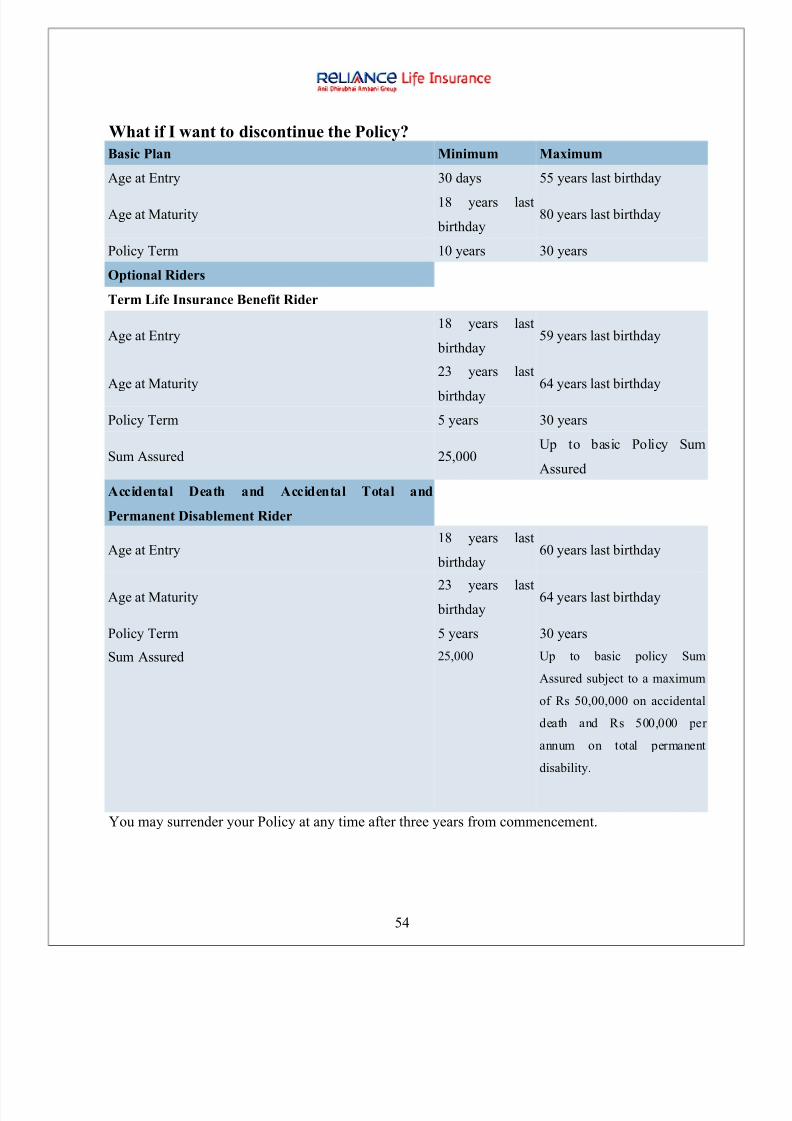

What if I want to discontinue the Policy?

You may surrender your Policy at any time after three years from commencement.

Basic Plan Minimum Maximum

Age at Entry 30 days 55 years last birthday

Age at Maturity18 years last

birthday80 years last birthday

Policy Term 10 years 30 years

Optional Riders

Term Life Insurance Benefit Rider

Age at Entry18 years last

birthday59 years last birthday

Age at Maturity 23 years last birthday

64 years last birthday

Policy Term 5 years 30 years

Sum Assured 25,000Up to basic Policy Sum

Assured

Accidental Death and Accidental Total and

Permanent Disablement Rider

Age at Entry18 years last

birthday

60 years last birthday

Age at Maturity23 years last

birthday64 years last birthday

Policy Term 5 years 30 years

Sum Assured 25,000 Up to basic policy Sum

Assured subject to a maximum

of Rs 50,00,000 on accidental

death and Rs 500,000 per

annum on total permanentdisability.

54

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 55/110

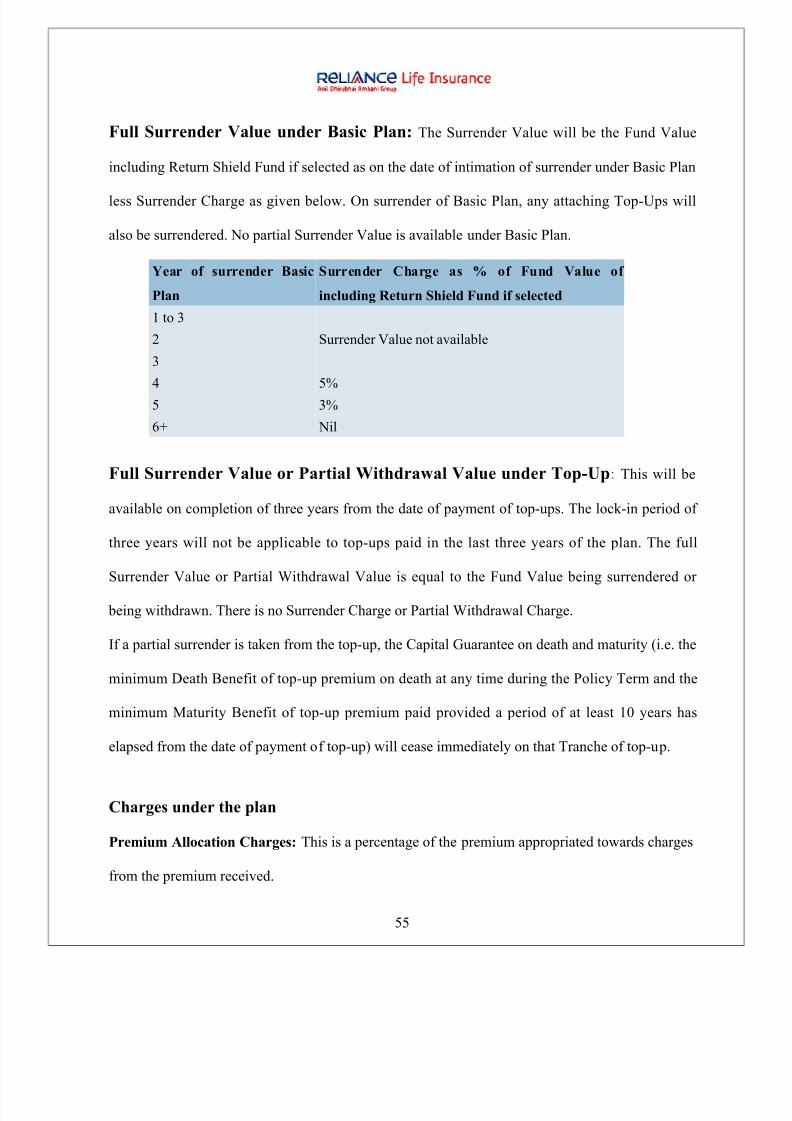

Full Surrender Value under Basic Plan: The Surrender Value will be the Fund Value

including Return Shield Fund if selected as on the date of intimation of surrender under Basic Plan

less Surrender Charge as given below. On surrender of Basic Plan, any attaching Top-Ups will

also be surrendered. No partial Surrender Value is available under Basic Plan.

Year of surrender Basic

Plan

Surrender Charge as % of Fund Value of

including Return Shield Fund if selected

1 to 3

Surrender Value not available2

3

4 5%

5 3%

6+ Nil

Full Surrender Value or Partial Withdrawal Value under Top-Up: This will be

available on completion of three years from the date of payment of top-ups. The lock-in period of

three years will not be applicable to top-ups paid in the last three years of the plan. The full

Surrender Value or Partial Withdrawal Value is equal to the Fund Value being surrendered or

being withdrawn. There is no Surrender Charge or Partial Withdrawal Charge.

If a partial surrender is taken from the top-up, the Capital Guarantee on death and maturity (i.e. the

minimum Death Benefit of top-up premium on death at any time during the Policy Term and the

minimum Maturity Benefit of top-up premium paid provided a period of at least 10 years has

elapsed from the date of payment of top-up) will cease immediately on that Tranche of top-up.

Charges under the plan

Premium Allocation Charges: This is a percentage of the premium appropriated towards charges

from the premium received.

55

8/4/2019 MASOOM RAZA

http://slidepdf.com/reader/full/masoom-raza 56/110

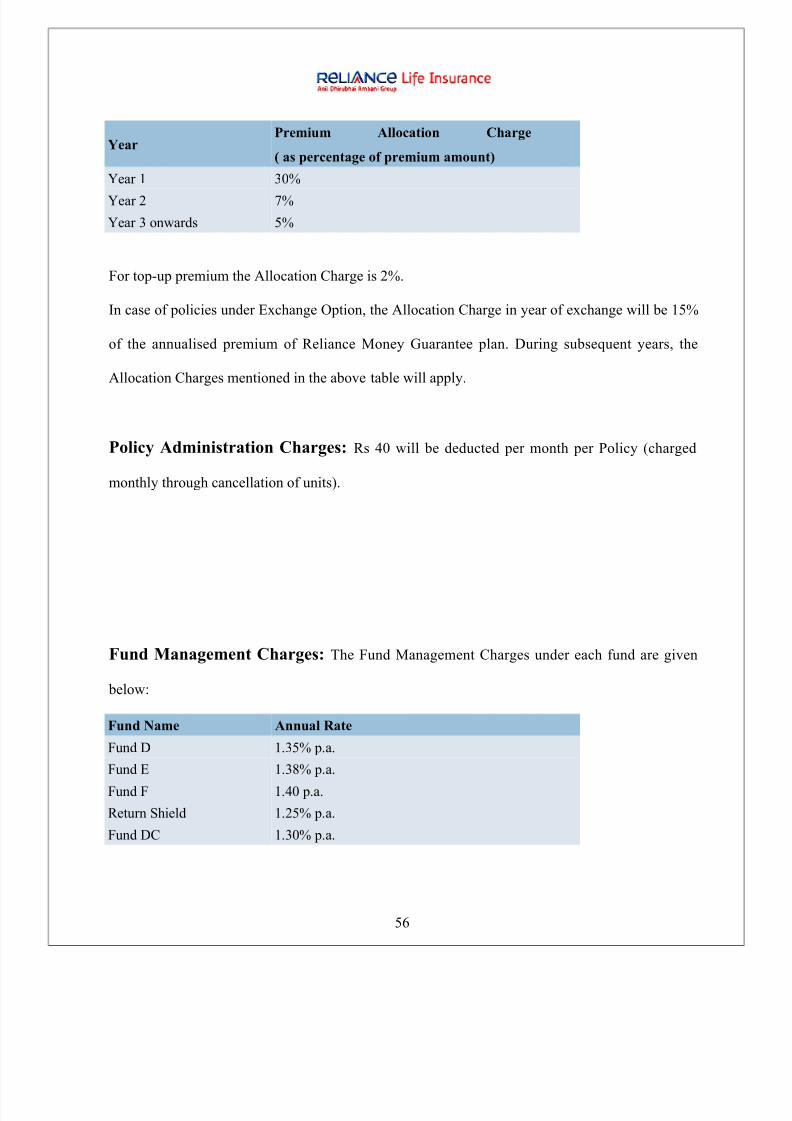

YearPremium Allocation Charge

( as percentage of premium amount)

Year 1 30%

Year 2 7%

Year 3 onwards 5%

For top-up premium the Allocation Charge is 2%.

In case of policies under Exchange Option, the Allocation Charge in year of exchange will be 15%

of the annualised premium of Reliance Money Guarantee plan. During subsequent years, the