Embed Size (px)

Citation preview

Global Outlook 2012-2014 Applied Portfolio Management

O c t o b e r 9 t h , 2 0 1 3 B e n L i n

Materials Sector Report

Metals & Mining Industr

y

Chemicals Industry

Table of Content

Ø RECOMMENDATION 2

Ø ECONOMIC OUTLOOK 2

Ø SECTOR OVERVIEW 3 - 7

Ø BUSINESS ANALYSIS 8 - 27

Ø Financial ANALYSIS 28 - 38

Ø Valuation ANALYSIS 39 - 41

Ø Conclusion 42

Ø References 43 - 44

Economic Outlook

Recommendation

I recommend overweighting our holdings in the materials sector from its current 1.7 percent to 4.46

percent, 1.01 percent higher relative to the weight of S&P 500, by primarily focusing on the

chemicals industry because the increasing volume and decreasing price of domestic natural gas, as

well as the maturing GTL technology will significantly reduce chemicals production cost on the top

of the industry’s strong cost control system. In addition, the solid growth of the product line in the

chemicals industry has strengthened by the decline in the mining industry, the government’s support

in the chemicals new technology development, and the increasing demand for alternative materials

such as plastics will send the chemicals industry to a new level.

I anticipate an optimistic outlook for the U.S. economy moving forward in 1 to 1.5-‐year

horizon. The lower growth of consumer spending reinforces the stock market as more capital flows

into it. According to a research done by University of Michigan, Consumer Sentiment reading is

only 76.8, lowest since this April. The bad mortgages are the lowest since the 4th quarter of 2007,

works out of labor force are the lowest since the 4th quarter of 2008, stock market capitalization is at

all time high, assets held by the Fed are at all time high; In addition, research has shown that the

corporate earnings gap between Europe and the U.S. just reached 25-year high in September as the

U.S. outperformed Europe by 20 percent; also, the U.S. aging population is the lowest among the top

5 countries by economic scale, which provides U.S. comparative advantage in working capital in the

future; making the U.S. investment opportunities more attractive to foreign investors. Domestically,

tapering is not going to effect therefore short-term interest rates will stay low into the future. The

Fed had debt outstanding of $3.72 trillion as of the first week of September. Prior to the FOMC

meeting, analysts of major banks expected that the Fed would start tapering once the amount of debt

reaches $4.06 trillion. The figure was reassessed right after the FOMC meeting and raised up to

$4.27 trillion, which implies that the potential tapering may come 2.5 months later than the original

estimate. The rule of thumb shows that every $100 billion assets the Fed adds to its balance sheet

will decrease the 10-year bond interest rates by 0.03 percentage points. Consequently, 2.5 months no

tapering will ultimately result in additional $213 billion on the Fed’s balance sheet, therefore 0.0639

percentage points decrease in interests rates if the estimate comes out true.

Sector Overview

Overview

The Materials Sector is the third smallest sector of the ten S&P 500 sectors, which makes up

3.45 percent of the S&P 500 with a market capitalization of $1.82 trillion. Consisting of five

industries, the materials sector is heavily weighted in the chemicals industry with the weight

of 68.76 percent; Metals and mining, containers and packaging, paper and forest products, and

construction materials are weighted 15.65 percent, 6.31 percent, 4.71 percent, and 1.32

percent respectively. The sector beta of 1.3 defines its offensive nature, which usually puts the

sector in trouble when the market is in downturn. However, the precious examination of the

optimistic economic outlook moving forward in the next 1 to 1.5-‐year horizon indicates that

the sector is worth overweighting relative to the market.

1-1. S&P 500 Sector Breakdown [As of Sep-20-2013]

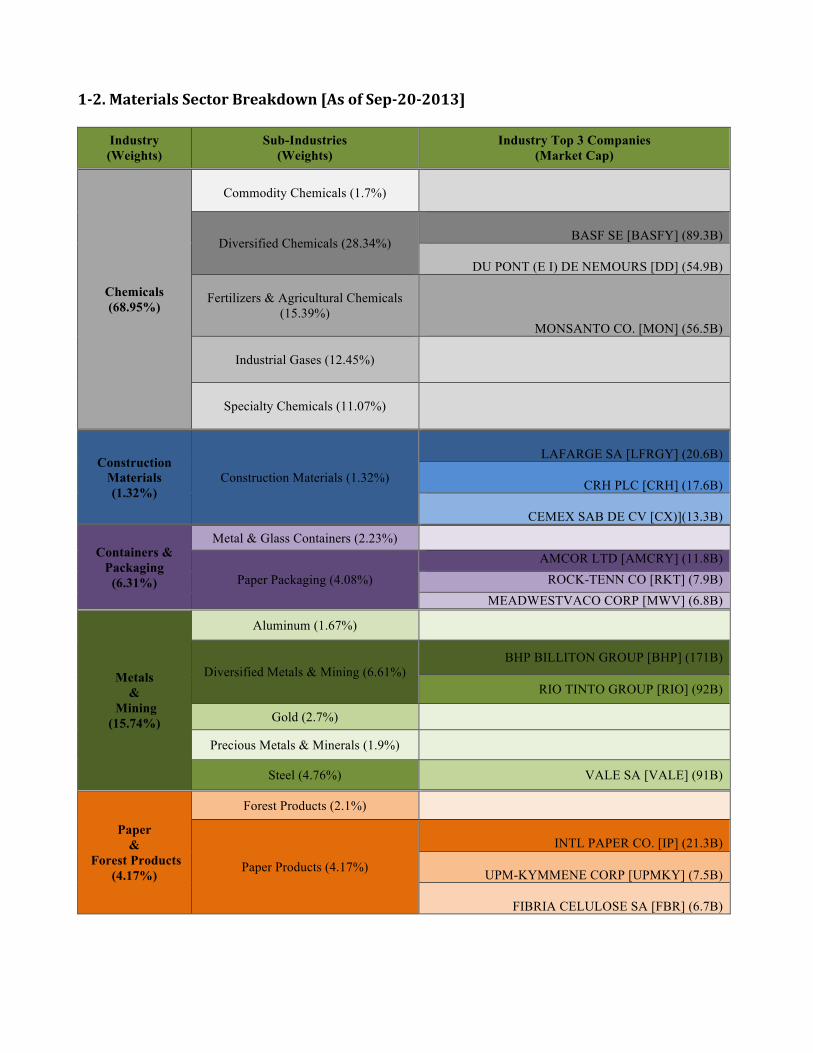

1-‐2. Materials Sector Breakdown [As of Sep-‐20-‐2013]

Industry (Weights)

Sub-Industries (Weights)

Industry Top 3 Companies (Market Cap)

Chemicals (68.95%)

Commodity Chemicals (1.7%)

Diversified Chemicals (28.34%)

BASF SE [BASFY] (89.3B)

DU PONT (E I) DE NEMOURS [DD] (54.9B)

Fertilizers & Agricultural Chemicals

(15.39%)

MONSANTO CO. [MON] (56.5B)

Industrial Gases (12.45%)

Specialty Chemicals (11.07%)

Construction Materials (1.32%)

Construction Materials (1.32%)

LAFARGE SA [LFRGY] (20.6B)

CRH PLC [CRH] (17.6B)

CEMEX SAB DE CV [CX)](13.3B)

Containers & Packaging

(6.31%)

Metal & Glass Containers (2.23%)

Paper Packaging (4.08%) AMCOR LTD [AMCRY] (11.8B)

ROCK-TENN CO [RKT] (7.9B) MEADWESTVACO CORP [MWV] (6.8B)

Metals &

Mining (15.74%)

Aluminum (1.67%)

Diversified Metals & Mining (6.61%) BHP BILLITON GROUP [BHP] (171B)

RIO TINTO GROUP [RIO] (92B)

Gold (2.7%)

Precious Metals & Minerals (1.9%)

Steel (4.76%) VALE SA [VALE] (91B)

Paper &

Forest Products (4.17%)

Forest Products (2.1%)

Paper Products (4.17%)

INTL PAPER CO. [IP] (21.3B)

UPM-KYMMENE CORP [UPMKY] (7.5B)

FIBRIA CELULOSE SA [FBR] (6.7B)

Table 1-2 gives a clear breakdown of the materials sector. Although the chemicals industry makes

up the majority market capitalization of the materials sector, the three largest companies are from the

metals and mining industry. With the total market cap of $354 Billion combined, the three largest

companies in the mining industry are larger than all the 12 largest companies in the other four

industries combined. The capital-intensive nature of their business implies that a solid financial

fundamental is required to support their massive supplies and ongoing projects.

The metals and mining industry provides the building blocks for economic development, meanwhile,

the chemicals industry possesses the potential reserves for materials sector’s turnaround. The

relationship between two industries is quite complicated in terms of they naturally against each other

by consuming the same natural resources and supplying almost the same industries, automotive and

construction industries in particular. On the other hand, they intimately support each other by

hedging against the decline in commodity price and the necessity of importing foreign products.

However, environmental restrictions have put more pressure on the mining industry over the

chemicals industry, shifting its energy consumption from coal to oil, then to natural gas. Cheap

access to steel and other major metals products have worsen the needs of precious metals, making

diversified miners give up their poor performance operations and focus on popular metals such as

steel and aluminum, therefore exaggerating the supply of certain metals, steel in particular. On the

contrary, chemicals products such as plastics are becoming more attainable because of higher cost

efficiency and lower transportation and carrying cost. In addition, return is rewarding for those who

can allocate assets accordingly and maintain operational stability in response to the downturn of the

global economy.

At last, focusing on the APM portfolio’s weight and performance, the materials sector is only

weighted 1.6% of the overall portfolio. Comparing to the other two underweighted sectors, the

utilities sector and the telecom sector, weighted 4% and 4.2% respectively. The materials sector has

delivered over 34% rate of return since November last year, compares to 10 percent from the utilities

sector and 20 percent from the telecom sector. And it has outperformed some highly weighted

sectors such as the consumer staples sector, which has only contributed 10.1% of return to the

portfolio with the weight of 13.5%. All of this real data further proves that the materials sector has

been underweighted. Due to the upcoming great prospects for the chemicals industry, increasing the

weight of the materials sector becomes more valuable and credible. The following two graphs

further demonstrate the strong historical performance of the chemicals industry.

Up close examination, from the beginning of 2012 to August 2013, the performances of industries

within the materials sector has been fluctuated as the poor performance from the metals and mining

industry, and the momentum performance from the chemicals industry. Although the prospect of the

materials sector as a whole is valued underwater, I anticipate the materials sector is in recovery, with

the continuing momentum growth from the chemicals industry and gradual rebound from the metals

and mining industry. I believe the performance of the materials sector will be reshaped in the next 1

to 1.5 year horizon.

Rate of return is the most convincing evidence of companies’ performances over a specific period of

time. Following table shows the best performing companies by total return in 1-year and 3-year

horizon, selected from 100 largest companies within the materials sector. As shown, 80 percent of

the best performing companies in 1-year horizon come from the chemicals industry, and 100 percent

of the best performing companies in 3-year horizon come from the chemicals industry. (Morningstar,

2013) To better compare the performances of these the industries, following business analysis will

focus on both the metals and mining industry and chemicals industry.

1-3. Top Five Performing Companies By Total Return Of 100 Largest Companies By

Market Capitalization In The Materials Sector [As of Oct 04th, 2013]

1-Year 3-Year

Company Name

(Ticker) Industry Return

Company Name

(Ticker) Industry Return

Alfa, S.A.B. de

C.V.

(ALFFF)

Chemicals 267.32%

Alfa, S.A.B. de

C.V.

(ALFFF)

Chemicals 54.66%

Nippon Steel &

Sumitomo Metal

Corporation ADR

(NSSMY)

Steel 68.85%

LyondellBasell

Industries NV

(LYB)

Specialty

Chemicals 52.86%

Mexichem,

S.A.B. de C.V.

(MXCHF)

Chemicals 59.08%

Sherwin-Williams

Company

(SHW)

Specialty

Chemicals 37.44%

Koninklijke

DSM NV ADR

(RDSMY)

Specialty

Chemicals 55.59%

PPG Industries,

Inc.

(PPG)

Specialty

Chemicals 35.03%

Ecolab, Inc.

(ECL)

Specialty

Chemicals 54.48%

CF Industries

Holding, Inc.

(CF)

Agricultural

Chemicals

32.77%

Business Analysis

Metals and mining Industry Life/Business Cycle

Metals and mining industry is highly cyclical in terms of its performance is highly correlated with

the demand and supply of the raw materials, the commodity price cycle as well as the discovery of

substitutes. Exposing to the fact that resources are scarce, poor demand or oversupply usually leads

to a rapid decline in the industry. I infer that the metals and mining industry is in a mature lifecycle,

because of the rising business risk and cost inflation, driven by a number of factors such as global

economic uncertainties, softening commodity prices and the emergence of substitutes.

2-1. Business Risk of The Materials Sector Compares to 2012

According to Ernst and Young’s business risk analysis on metals and mining industry, industry’s top

two risks have shifted relative to 2012. The risk of capital allocation and access indicates

that the rampant cost inflation and falling returns due to the rapid decline in commodity prices have

created a mismatch between miners’ long-term investment horizons and investors’ short-term return

horizons. In the other words, the conflicts between short-term investors’ incentives, and the sector’s

longer-term return horizon due to its cyclical nature are very likely to influence miners’ decisions

therefore damaging their growth prospects. The risk of margin protection and

productivity improvement on the other hand, indicates that productivity in the sector has been

declining for nearly a decade, while most miners haven’t realized the directional change from

growth prospect towards long-term capital allocation and operating costs optimization. The long-

term value is rewarding for those who keep their input-to-output ratio in order by optimizing

productivity through their capital structure, on the contrary, expanding territory and taking over

more product lines will result in larger business write-downs. (Mike Elliott, 2013)

The competition within the metals and mining industry is fierce, table 2-2 shows that in 2012,

there were approximately 5,500 junior producers with assets less than $1billion, and 500

intermediate and senior producers with assets exceeding $1 billion within the industry, making

competition on price and quality extremely intense, especially for the small size miners.

2.2 Profile for the formal mining industry [As of the end of 2012]

Fierce competition and oversupply empower huge bargaining power to customers because

miners all over the world can adjust their price accordingly based on geographical or quantity supply

advantages.

On the other hand, the bargaining power from suppliers is low. First, large volume of

M&As within the mining industry over the past two years have concentrated the mining power

therefore crossing a number of small or medium size customers off of mining equipment suppliers

and energy suppliers’ lists. Second, historical low prices of coal and natural gas have offered miners

an advantage to switch from one to another in order to find the most cost efficient and sustainable

energy product. At last, due to three major oil fields under development in the US: Texas, North

Dakota and California. Oil industry is facing all-time high competition due to the diversification of

the sources of supply, and the threats from substitutes such as LNG, liquefied natural gas, driving

down the price therefore guaranteeing miners lower transportation costs. Studies have shown that the

United States will overtake Saudi Arabia as the world leading oil producer by the year of 2017.

(Elisabeth Rosenthal, 2013)

However, cheap energy price also benefits chemicals industry as the largest energy consumer in the

materials sector. Indicating that the threat of substitute products for metals is emerging as

a large volume of ultra-high strength, temperature resistant and cost-efficient products are being

used in the range from automotive to energy industry. Currently, approximately 16% weight in a

vehicle is plastic, with a growth trend to possibly reach 25% in the next 5 years. At last, internal

rivalry is fierce in terms of aluminum intends to overtake steel to become the most important

metal by volume.

The government’s regulations on emission put high pressure on miners as their profits

squeeze. For example, the Obama administration and the Environmental Protection Agency (EPA)

have introduced strict legislation targeted at the coal industry in an effort to curb harmful emissions

and reduce greenhouse gases. Meanwhile, coal also suffers from multiple secular headwinds,

particularly from competing fuels such as natural gas. With abundant supplies and historically low

prices for U.S. natural gas, many utilities are switching to this cleaner-burning commodity and no

longer using coal. Chemicals industry on the other hand, is benefited from the government by

enjoying lower tax rate and subsidies for new product and technology development. Finally, the

threat of new entrants is minimized since metals and mining industry is very capital

intensive in terms of high cost of patent, low machinery useful life, heavy transportation cost and

increasing labor cost. On the other hand, the decline in metals prices and low equity financings have

given entrepreneurs less incentives to seek the profitable opportunities within the mining industry.

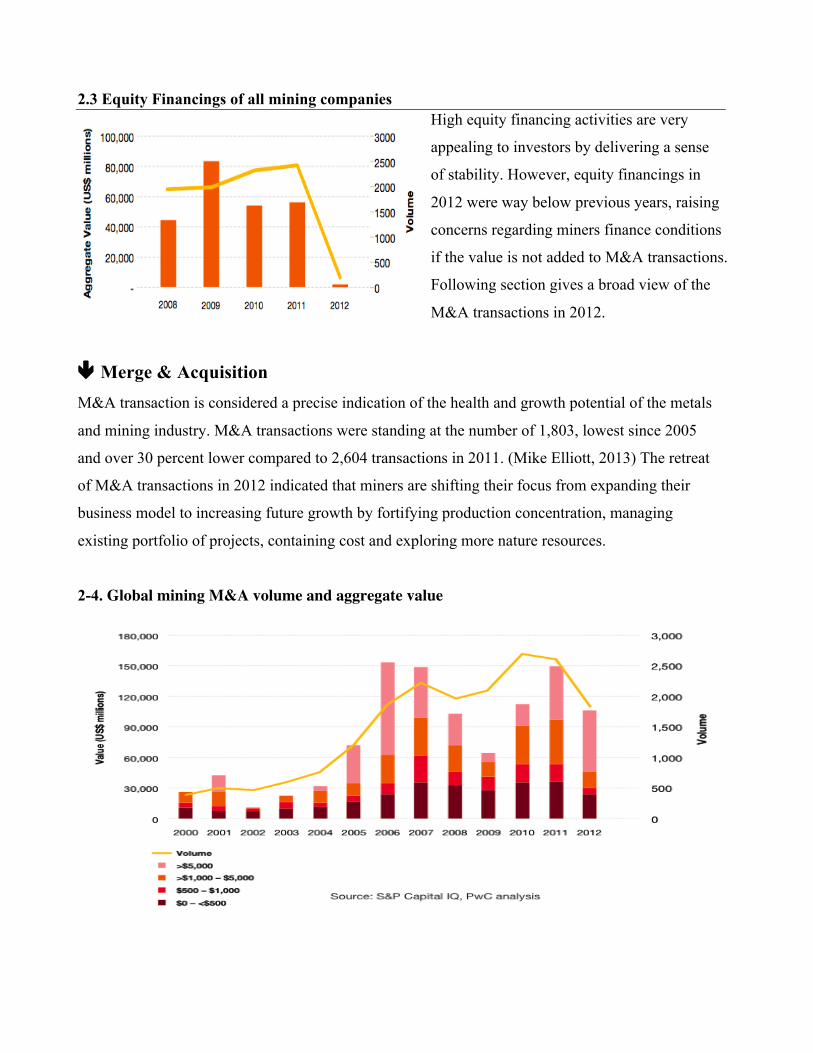

2.3 Equity Financings of all mining companies High equity financing activities are very

appealing to investors by delivering a sense

of stability. However, equity financings in

2012 were way below previous years, raising

concerns regarding miners finance conditions

if the value is not added to M&A transactions.

Following section gives a broad view of the

M&A transactions in 2012.

ê Merge & Acquisition M&A transaction is considered a precise indication of the health and growth potential of the metals

and mining industry. M&A transactions were standing at the number of 1,803, lowest since 2005

and over 30 percent lower compared to 2,604 transactions in 2011. (Mike Elliott, 2013) The retreat

of M&A transactions in 2012 indicated that miners are shifting their focus from expanding their

business model to increasing future growth by fortifying production concentration, managing

existing portfolio of projects, containing cost and exploring more nature resources.

2-4. Global mining M&A volume and aggregate value

Lower M&A transactions once again verifies the mature stage of metals and mining

industry, forcing miners to aggregate their resources and reserve capitals in the effort of lowering

operational cost. In this stage, massive pricing competition raises as the large miners acquire most of

the resources, smaller miners become less likely to survive under both pricing and business scale

pressures, but have to be taken over or recognize losses.

With mega-mergers out of the way and the importance of the bottom-line front and centre, 2014 will

be all about asset rationalization. “Deal activity will be driven mainly by two things: senior miners

looking to divest non-core assets and seniors looking to de-risk projects through joint-ventures.”

(Jason Burkitt, 2013) While asset rationalization usually takes a long period of time until it starts

showing profitability to the miners. As for junior miners, it will be extremely hard for them to raise

capital or look for potential buyout opportunities, which may force junior mining executives to

handover their companies at low valuations. To conclude, I expect a slow year for mining M&A

deals in 2014, well below last year’s reduced numbers. Next part elaborates the mining deals in 2012

for comparison.

In 2012, the value of mining deals totaled $110 billion, including the Glencore-Xstrata’s $54 billion

deal in Switzerland. Without this mega-merger deal, total merger value was only $56 billion,

comparing to a total merge value close to $150 billion in 2011.

2-5. The Value of the deals in 2012 (Includes Glencore-Xstrata deal)

All the deals in 2012 were settled as 56

percent of them fell in the diversified

metals. However, Glencore-Xstrata deal

accounted for a large percentage in

diversified metals with total gross

transaction value of $54,000 million. On

the other hand, Iron Ore deals were flat as

its price slumped from $147.65 in April

2012 to $99.47 in September 2012. Steep decline in the price is majorly caused by a large volume of

substitutes and the slowing down demand from its biggest consumers such as China.

2-6. The Value of the deals in 2012 (Exclude Glencore-Xstrata deal)

ê Transportation Cost

Vessel price has dropped over the course of months since the beginning this year, which is a strong

indicator for the health of the shipping industry. “Over the past two months (July and August),

we’ve seen Capesize prices fall from $14.5 million $14 million. Supramax and Panamax had both

pulled back from $10 million to $9 million.” According to a Chinese shipping industry expert.

Lower vessel price is usually caused by the decline in the shipping cost, implying that importing

materials overseas becomes more attractive. Which is harmful for the domestic production as the

price of raw materials such as crude steel and coal has already showed large decline over the past six

months. Evidence can be found that the production of the steel in China has declined due to an

increase demand of international steel. “China’s iron ore imports reached a new high in July,

shipments totaled 73.1 million metric tons — a record monthly volume that was 26% higher than a

year earlier and 17% higher from June”. (Chuin-Wei Yap, 2013) Chinese government is expected to

take some actions by demanding steel overseas therefore driving up the international steel price and

making domestic steel supply more attractive.

Excluding Glencore-Xstrata deal, copper

and gold deals make up the majority part of

the M&A deals, with 30 percent and 27

percent respectively of the total gross

transaction value compares to 12 percent of

Iron Ore. These two metals together

accounted for half of the top 20 deals in

2012, even before considering their mix in

diversified metal mergers.

Gold is used as a hedge against the economic uncertainty. Copper, on the other hand,

reflects the future health of the global economy. However, both gold and copper prices

rose in 2012 and declined in the first half of 2013 implied that the oversupply problem in

the materials sector has distorted the relationship between gold and copper, changing

their 5-‐year correlation coefficient of 0.19 to 1-‐year correlation coefficient of 0.77.

ê Steel Steel as the most important product in the materials sector by volume, touching every aspect of

human lives. The steel industry directly employs more than 2 million people worldwide, and spends

more than $15 billion per year on process improvements, new product development and future

breakdown technology. However, the massive capital expenditures on innovation are not in line with

the growth rate of the production. Although the amount of energy required to produce a tonne of

steel has been reduced by 50%, the growth rate of the production is slowing down. While the total

steel produced still exceeded the total steel demanded. I assess the life cycle of steel industry is in

the decline phase, and anticipate continuing poor performance in the following 1 to 1.5 year horizon.

2-7. Average growth rates of steel production [As of December, 2012]

The steel industry has steadily recovered from the global economic downturn, which reduced the

production of crude steel by 9% in 2009. World Crude steel production hit the record of 1,548 Mt in

2012, 1.2% higher than the record in 2011, which is mostly driven by the growth of production in

Asia and North America. During 2012, crude steel Production in Asia increased 2.7% to 1,012 Mt as

China once again leaded the production by yielding over 46% of the global output, up 3.1% year

over year. The United States produced 88.6 Mt of crude steel, up 2.5% year over year, which

accounted for 6% of the global output and hold the third position in 2012. On the contrary,

Production in Japan remained flat, Euro and South America declined 2.7% and 3.1% respectively.

Higher production didn’t harvest more appealing profits. On the contrary, profits in the steel industry

slumped when the price of iron ore was hammered due to the lower demand from big consumers

such as China, and higher competition stemming from substitutes such as copper, aluminum and

chemical products. However, China continues its momentum on consuming commodity and basic

materials even as the economic growth has dropped over the past year.

2-8. Distribution of Crude Steel Production (As of 2012)

The world steel supply distribution has

shifted to the Asian market dominance

as over 64% of total steel production

comes from Asia. However, Japan

capacity has declined 5% since 2002,

meanwhile, EU, NAFTA and CIS

capacities have declined 10%, 5%, 4%

respectively.

2-9. Distribution of Apparent Steel Use (As of 2012)

As far as demand for crude steel goes,

China sufficiently absorbs resources

domestically and maintains appealing

net exports to the world. While NAFTA

and other Asian countries except China

and Japan have to consume a large

amount of crude steel oversea because of

their increasing demands.

2-10. World Exports in Steel Products

The percentage of crude steel exports has gone down

from 39.2% in 2000 to 28.7% in 2012, implying that

the biggest steel consumption countries such as China

have found ways out to satisfy themselves. Despite the

slump in production resulted from the financial crisis

in 2009, the production level has quickly picked up to

its pre-crisis level in 2010. However, the exports of

steel stayed low. A steep decline in exports of an

industry can be considered the process of getting to the

mature stage. In which the gap between production

supply and demand are widen, leads to the loom of

oversupply thus price meltdown. Worst scenario can

be found in Europe as its demand for steel declined

another 9% in 2012 as a major downturn in its heavily

dependent automotive sector. Europe’s demand for

steel is currently 29% blow its pre-crisis level.

2-11. World Volume Of Trade (Quantum indices 2000=100, 2000 – 2012)

In the course of 10 years, the

volume of trades among steel,

steel containing manufactured

goods and commodities have

differed as commodities volume

continued spiking, steel

containing manufactured goods

started moving in the opposite

direction aginst steel in response

to the rise of other substitutes in

the late 2011.

The automotive and construction sectors, two biggest markets for steel consumption showed

opposite result in 2012. The automotive sector in the US hit the record in five years as auto sales

shot up 13% to 14.5 million vehicles in 2012, driving up a strong demand for steel, mostly

influenced by cheap financing, cheap gas and the launch of fuel-efficient vehicle. However,

intelligent materials concepts are increasingly required in order to achieve energy efficiency and

sustainability. To be specific, lightweight construction is increasingly adopted: according to Green

Car Congress, in March this year, the Advanced Research Project Agency-Energy (ARPA-E)

rewarded 18 projects that could recycle metals to the construction of lightweight cars. Which implies

the likelihood that the steel will be taken over by chemical plastic in the future.

On the other hand, the construction market delivered a sign of slowdown. Globally, according to the

Wall Street Journal, Chinese economy sluggish has over as industrial output accelerated to 10.4%

year-to-year growth in august, up from 9.7% in July, which built up the market confidence regarding

the demand of steel. However, an up close examination indicates that the total social financing

(broad measure of new credit in the economy) in China was 1.6 trillion yuan in August, nearly

doubled the amount of 808 billion yuan in July, raising doubts regarding if the growth in

construction built on debts could truly reflect a comeback of the economic growth.

China’s September HSBC Flash Manufacturing PMI, which is largely viewed as a leading

indicator of the strength of China’s economic activity, rose and beat estimates. More iron ore is

needed to support Chinese growing manufacturing activities, while cheap Iron ore price induces

Chinese corporations to import iron ore overseas instead of absorbing domestically. Due to the

nature of Mixed Capitalist

economic system in China, the

Chinese government is

expected to step up by

demanding iron ore overseas

to increase international steel

price therefore increasing

domestic steel profit, which

may create continuous tension

in global steel competition.

(HSBC, 2013)

2-12. New Housing Units Started in the United States

(U.S. Department of Commerce, 2013)

Since iron and steel make up a majority of the volume in the materials sector, followed by

aluminum, copper and gold. After picking steel industry as a falling sub-industry, following section

introduces gold and copper sub-industries as comparative rising sub-industries to further analyze the

future outlook of the materials industry.

éGold & Copper Gold and copper on the other hand, have shown solid prospects regarding their future demand and

production. I assess both gold and copper industries are in the recovery phase of their lifecycles, and

anticipate steady growth in the following 1 to 1.5 year horizon majorly due to the raising economic

uncertainties and increasing M&A transactions.

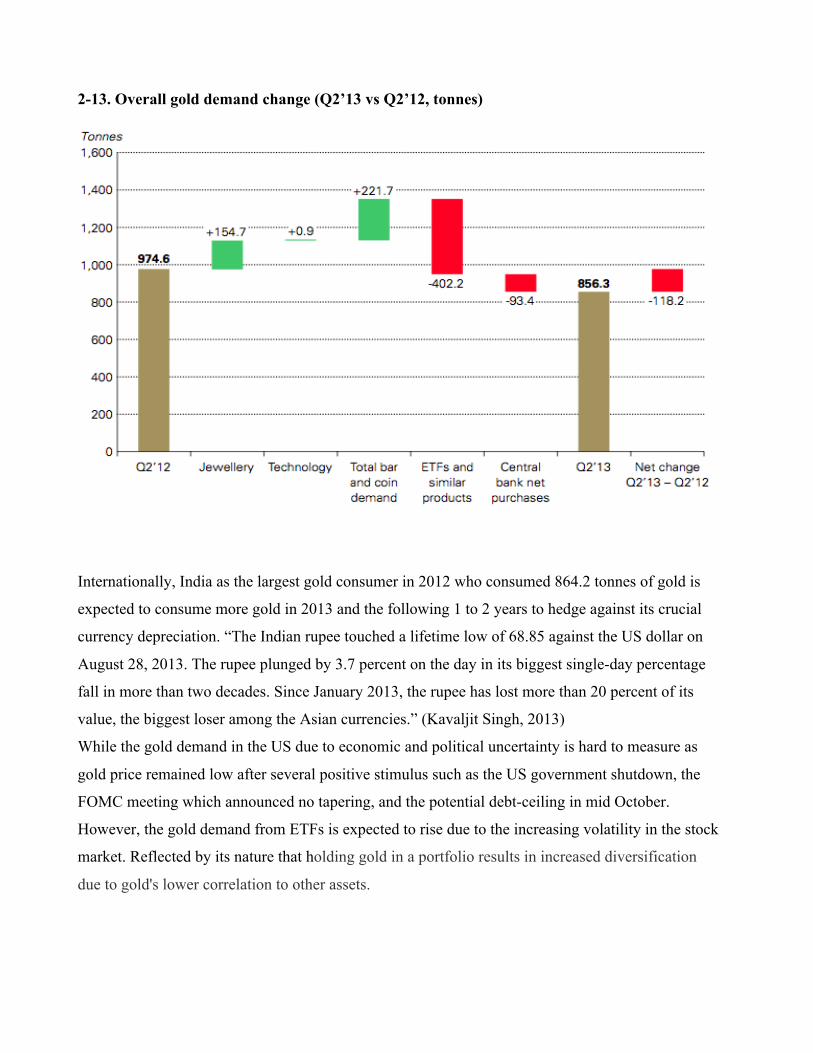

The demand of gold has fallen 118.2 tonnes in the second quarter of 2013 compares to the second

quarter of 2012, mostly reflected by a rapid decline in the ETFs and the central bank net purchases.

However, the decline of demand from ETFs and Central bank was mitigated by the large growth of

demand from jewelry, as well as bar and coin. Which delivered an optimistic perspective regarding

the growth of the global economy going forward, driving gold price to the lowest point since the end

of 2010. On the other hand, the abnormal optimism provides more downside risk as the economic

uncertainty rises, which gives gold more upward opportunities.

Demand from technology applications is also promising as the price correction of gold provided a

much needed boost to the sector as manufacturers took advantage of lower prices to replenish

previously liquidated assets.

Domestically, US Construction

sector haven’t seen significant

growth since 2009. With

approximately 891,000 total new

housing units under construction

by September this year. New

construction activities are still

below its pre-‐crisis level.

2-13. Overall gold demand change (Q2’13 vs Q2’12, tonnes)

Internationally, India as the largest gold consumer in 2012 who consumed 864.2 tonnes of gold is

expected to consume more gold in 2013 and the following 1 to 2 years to hedge against its crucial

currency depreciation. “The Indian rupee touched a lifetime low of 68.85 against the US dollar on

August 28, 2013. The rupee plunged by 3.7 percent on the day in its biggest single-day percentage

fall in more than two decades. Since January 2013, the rupee has lost more than 20 percent of its

value, the biggest loser among the Asian currencies.” (Kavaljit Singh, 2013)

While the gold demand in the US due to economic and political uncertainty is hard to measure as

gold price remained low after several positive stimulus such as the US government shutdown, the

FOMC meeting which announced no tapering, and the potential debt-ceiling in mid October.

However, the gold demand from ETFs is expected to rise due to the increasing volatility in the stock

market. Reflected by its nature that holding gold in a portfolio results in increased diversification

due to gold's lower correlation to other assets.

2-14. Investment demand of gold by category

Copper holds the third place after iron and aluminum in terms of consumption, due to its high

ductility highlighting its popularity in industrial usage. The world witnessed the record high levels of

copper prices from 2006 to 2008 because of limited supplies, and growing demands from emerging

markets such as China. However, due to a slowdown in the Chinese economy, Europe’s sovereign

debt crisis, and a slowing US economy, the copper price has dipped 10 percent in 2012. While I

believe the long-term stance for copper is still bullish, in terms of a large volume of M&A

transactions further limited the supplies of copper from existing mines, suppliers shut down or

divested their high-cost or non-profitable business has improved their concentration, and the demand

from the emerging markets is promising. One interesting fact from M&A transactions in 2012 is that

copper related transactions were valued $112 million in average, standing in the middle of $60

million gold related transactions and $137 million iron ore related transactions. While copper related

transactions delivered 62% average deal premium, comparing to 47% average deal premium of gold

and 18% average deal premium of iron ore. (Amy Hogan) Observation can be made that copper is

expected to deliver a comparatively higher value in the future than its peers due to its widespread use

and absence of significant new development projects.

Chemical Industry Life/Business Cycle

The technological advancements in horizontal drilling and fractionation have guaranteed the US to

obtain natural gas from shale domestically. With the increase in natural gas production, the price of

US natural gas has declined from $12.50/MBTU in 2008 to approximately $3.49/MBTU in 2013 (As

of Sep 27). Consequently, chemicals industry will be able to take advantage of low-cost chemicals to

create chemical-based substitutes against other materials such as metal, glass and wood. The

chemicals industry has invested $15 billion in ethylene production, increasing capacity by 33%.

(Anthony, 2012) This estimate is expected to continue growing next year.

Meanwhile, the revolutionary gas to liquid (GAL) enables monetization of remote natural gas by

converting them into sulfur-free crude oil that can be easily transported by tanker. The GTL products

can then be used as-is or blended with diesel oils as a fuel with lower environmental impact for

transportation and power plants. This emerging technology has become a very cost efficient way for

major oil/fuel consumers.

Liquefied natural gas, as a clear

burning, and less expensive

resource for vessels, sells for about

$1.7 a gallon, about half the cost of

diesel. About 50% fuel cost saving

will allow companies to attract new

customers and negotiate longer

contracts.

BTU, British thermal unit, is a basic measure of heat energy. One BTU is the amount of energy

needed to raise the temperature of 1 pound of water by 1 Fahrenheit. Despite its name, BTU is rarely

used in British, but in countries such as the US and Canada as the standard measurement of heat

output for fuels such as coal, oil and natural gas. (WiseGeek, 2013) The new natural gas is

anticipated to produce 20 BTU per unit compares to its 7 times BTU per unit a few years ago,

making it more attainable than the other fuel.

3-2. Trends In Natural Gas Prices Across The World ($ per million BTUs)

Due to demographic advantage, the US is able to expand its natural gas drilling at major fields

such as Texas, North Dakota and California. Chart 3-2 shows that the US has dominated the natural

gas market by keeping its price below $4 per million BTUs, giving domestic consumers more

incentives to take the advantages of low price and transportation cost, meanwhile, accelerating

natural gas export as foreign natural gas prices stay high.

3.3. Industrial energy consumption by fuel

Much of the growth of industrial energy

consumption is accounted for natural gas use. And

it is anticipated to increase 18 percent by the year

of 2025 according to the US energy information

administration. Energy intensive industries such as

metals and mining industry, as well as chemicals

industry will be more dependent on natural gas

resources than ever before. (Adam, 2013)

3-3. Natural Gas Cost As A Percent Cost Of Total Cost

The NGL from shale gas production���

is used by the chemicals industry to

produce a variety of derivatives and

products that ultimately become raw

materials for multiple

manufacturing sectors. (Anthony,

2012) Chart 3-3 shows that most of

chemical products are made of a

large percentage weight of NGL.

Notably, Polyethylene, the No.1

plastic by volume and value

produced by converting ethylene

into long-chain polymers, is highly

dependent on the use of natural gas

in which natural gas represents 85%

of its total production costs.

The cheap, domestic natural gas

empowers chemicals industry enormous growth potential and huge competitive advantage. To

elaborate, ethylene, a building block chemical used in thousands of products such as plastics and

tires, is produced by ethane and propane derived from NGL in the US. However, the nature of

ethane indicates that it’s extremely difficult to transport, therefore is unlikely to be exported out of

the US. As a result, chemical producers in the US are expected to consume additional ethane

domestically, therefore increasing the bargaining power from suppliers. Which can easily be

offset by the low bargaining power from consumers due to the overall high cost efficiency of

chemical producers in the US.

Increased ethane production is already occurring as gas processors build the infrastructure to process

and distribute production from shale gas formations. Chemical producers are starting to take

advantage of these new ethane supplies with crackers running at 95% of capacity, and several large

chemical companies have announced plans to build additional capacity. And because the price of

ethane is low relative to oil-based feedstocks used in other parts of the world, US-based chemical

manufacturers are contributing to strong exports of petrochemical derivatives and plastics. (shale-

gas-full-study)

3-4. Economic cost model of natural gas-ethane-ethylene

3-5. Economic cost model of ethane-ethylene

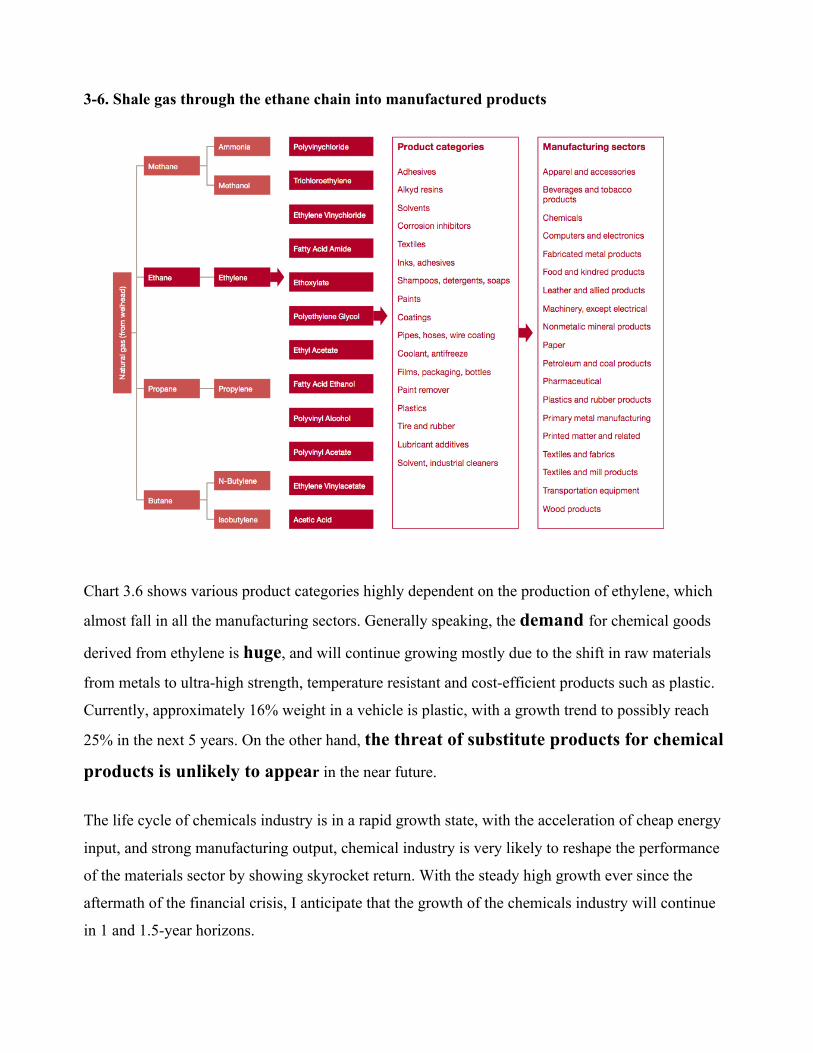

3-6. Shale gas through the ethane chain into manufactured products

Chart 3.6 shows various product categories highly dependent on the production of ethylene, which

almost fall in all the manufacturing sectors. Generally speaking, the demand for chemical goods

derived from ethylene is huge, and will continue growing mostly due to the shift in raw materials

from metals to ultra-high strength, temperature resistant and cost-efficient products such as plastic.

Currently, approximately 16% weight in a vehicle is plastic, with a growth trend to possibly reach

25% in the next 5 years. On the other hand, the threat of substitute products for chemical

products is unlikely to appear in the near future.

The life cycle of chemicals industry is in a rapid growth state, with the acceleration of cheap energy

input, and strong manufacturing output, chemical industry is very likely to reshape the performance

of the materials sector by showing skyrocket return. With the steady high growth ever since the

aftermath of the financial crisis, I anticipate that the growth of the chemicals industry will continue

in 1 and 1.5-year horizons.

3-7. Composition of new capital investment by chemical industry segment

Most of the new projects in the chemicals

industry announced so far have been heavily

weighted in bulk petrochemicals. Which is

anticipated to pay off by the time they are under

operations. Chart 3-7 shows the estimate of

incremental capital expenditures by chemical

industry segment. Those shares will likely evolve

over time as future investment announcements

expand capacity for downstream petrochemical

derivatives such as plastic resins.

3-8. Incremental Shale-related US chemical Industry Capital Expenditure in 10-year horizon (Billions of Dollars)

As a result, the composition of actual

investment will increase in response to

greater shares in downstream, therefore

higher value added products. Moreover,

greater production of chemical products will

generate larger demand for other chemistry,

boosting the growth of the industry as a

whole.

Chart 3-8 shows the possible incremental growth of the shale-related chemical industry capital

expenditure in 10 years. Of which the most rapid growth of capital expenditure falls between 2013

and 2015, facilitating the production of chemical products and attracting new investors with more

capital flows into the chemicals industry. The prospect for the chemicals industry in the 2-year

horizon is therefore bright.

Government’ support on energy projects is a major push of chemicals production. According to

Green Car Congress, on September 19th, the Advanced Research Project Agency-Energy (ARPA-E)

awarded $33 million to 15 projects to find advanced technologies that can convert natural gas to

liquid fuel for transportation in the effort of making the transport of ethane possible.

3-9 States Covered By CAIR limits on emissions of sulfur dioxide and nitrogen oxides

Graph 3-9 shows that within all the major natural gas fields in the US, only Texas is controlled for

annual SO2 AND NOx emission. Other major fields such as North Dakota, Alaska and California are

not under regulations yet. Moreover, the majority of reactors in the US are holding the operating

licenses that won’t be expired until 2020. In this case, the suspend actions related to issuance of

operating licenses and license renewals issued by NRC in August 2012 will not come into affect in

the short-term. (Adam, 2013)

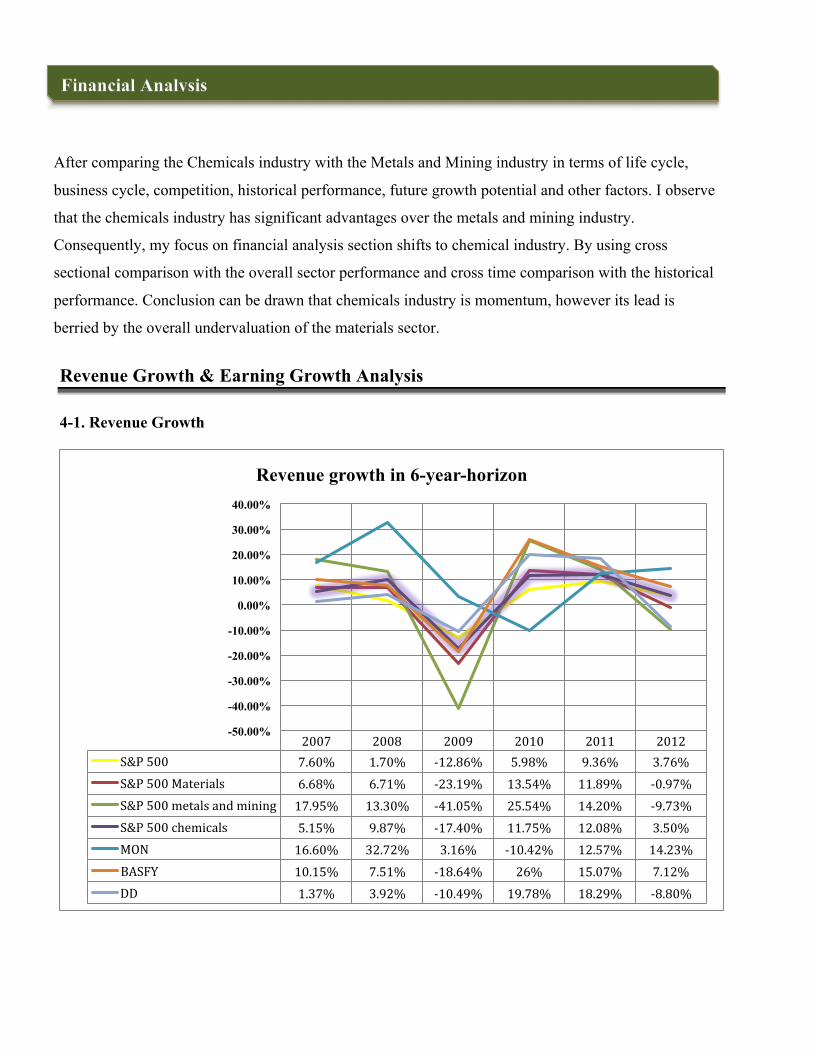

Financial Analysis

After comparing the Chemicals industry with the Metals and Mining industry in terms of life cycle,

business cycle, competition, historical performance, future growth potential and other factors. I observe

that the chemicals industry has significant advantages over the metals and mining industry.

Consequently, my focus on financial analysis section shifts to chemical industry. By using cross

sectional comparison with the overall sector performance and cross time comparison with the historical

performance. Conclusion can be drawn that chemicals industry is momentum, however its lead is

berried by the overall undervaluation of the materials sector.

Revenue Growth & Earning Growth Analysis

4-1. Revenue Growth

2007 2008 2009 2010 2011 2012 S&P 500 7.60% 1.70% -‐12.86% 5.98% 9.36% 3.76% S&P 500 Materials 6.68% 6.71% -‐23.19% 13.54% 11.89% -‐0.97% S&P 500 metals and mining 17.95% 13.30% -‐41.05% 25.54% 14.20% -‐9.73% S&P 500 chemicals 5.15% 9.87% -‐17.40% 11.75% 12.08% 3.50% MON 16.60% 32.72% 3.16% -‐10.42% 12.57% 14.23% BASFY 10.15% 7.51% -‐18.64% 26% 15.07% 7.12% DD 1.37% 3.92% -‐10.49% 19.78% 18.29% -‐8.80%

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

Revenue growth in 6-year-horizon

4-2. Earning Growth

Chart 4-1 shows that the materials sector’s revenue growth was hammered in 2009, mostly reflected

by a free fall of the metals and mining industry. The revenue growth of the chemicals industry on the

other hand outperformed the sector, but was still outpaced by the market. Although the chemicals

industry’s revenue growth didn’t pickup as rapid as the metals and mining industry nor the materials

sector in 2010, it maintained in a very sustainable level and was able to keep up with the market even

when the materials sector was down one percent in 2012 due to the decline in the commodity prices

and the oversupply from metals and mining industry. Chart 4-2 further elaborates that the chemicals

industry was able to keep its earning in a good shape when the earnings of the materials sector

declined over 86 percent in 2008. Similarly, the chemicals industry’s earning growth didn’t have any

rapid ups and downs over the past 6 years while the materials sector was extremely volatile, showing

its strong cost control and rational assets allocation. More importantly, the chemicals industry as a

whole focuses on free cash flow financing instead of high growth, which gives it more flexibility in

times of crisis. Following margin analysis and ROE analysis deliver a better idea of how the chemicals

industry keeps its growth rate stable.

2007 2008 2009 2010 2011 2012 S&P 500 -‐17.41% -‐69.71% 172.46% 43.60% 10.86% -‐0.93% S&P 500 Materials -‐12.84% -‐86.09% 256.47% 89.28% 16.39% -‐25.77% S&P Metals and Mining -‐17.76% -‐138.10% -‐172.32% 194.31% 6.11% -‐44.46% S&P 500 Chemicals 13.21% 0.49% -‐20.98% -‐12.57% 43.44% 34.59% BASFY 26.47% -‐28.38% -‐51.58% 223.19% 35.79% -‐21.15% MON 44.12% 103.83% 4.20% -‐47.42% 44.91% 27.26% DD -‐5.08% -‐32.83% -‐12.56% 72.71% 14.62% -‐19.75%

-200.00% -150.00% -100.00%

-50.00% 0.00%

50.00% 100.00% 150.00% 200.00% 250.00% 300.00%

Earning Growth in 6-year-horizon

Margin Analysis

4-3. Gross Margin

Gross margin is extremely important for the materials sector due to its capital-intensive nature. And it

is mainly supported by steady demand, stable price and strong cost control. The materials sector hasn’t

been able to follow up with the market since pre-crisis, mostly influenced by the imparity of the supply

and demand, and the low cost efficiency from the metals and mining industry. The chemicals industry

is an outlier in the materials sector, which could keep its gross margin close to 30% during the financial

crisis, and quickly sent its gross margin to the level even one percent higher than the market in 2009.

Currently, chemicals industry and the market are standing at the same gross margin level.

Operating margin, return on sales, shows how much an industry makes on each dollar of sales. The

metals and mining industry, driven by its cyclical nature, has shown very volatile operating margin

over the course of six years, as some extreme changes can be found between 2007 and 2009. Chemicals

industry on the other hand, was more affected by the overall economic trend, as it has been moving

along with the market, and consistently beating the performance of the materials sector. Net margin

shows similar result because two industries generally share the same low leverage trait, however,

chemicals industry has more tax advantages and endures less government restrictions over the metals

and mining’s industry.

2007 2008 2009 2010 2011 2012 S&P 500 36.09% 31.39% 34.40% 36.11% 35.14% 35.76% S&P 500 Materials 27.50% 22.08% 29.35% 29.22% 29.41% 29.84% S&P 500 Metals & Mining 26.88% 13.11% 21.82% 26.50% 25.14% 22.59% S&P 500 Chmicals 29.55% 28.50% 35.73% 33.46% 33.92% 34.90%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

Gross Margin

4-4. Operating Margin (ROS)

4-5. Net Margin

2007 2008 2009 2010 2011 2012 S&P 500 16.02% 8.28% 11.21% 14.10% 14.03% 13.65% S&P 500 Materials 13.07% 3.65% 9.35% 12.80% 13.53% 10.84% S&P 500 Metals & Mining 17.98% -‐2.11% 9.73% 16.55% 15.62% 10.78% S&P 500 Chemicals 11.93% 9.18% 10.01% 12.43% 14.29% 12.86%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

ROS

2007 2008 2009 2010 2011 2012 S&P 500 6.83% 2.04% 6.37% 8.62% 8.74% 8.35% S&P 500 Materials 7.87% 1.03% 4.76% 7.94% 8.26% 6.19% S&P 500 Metals & Mining 10.38% -‐3.49% 4.28% 10.04% 9.33% 5.74% S&P 500 Chemicals 7.92% 5.70% 6.03% 7.74% 9.29% 8.15%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Net Margin

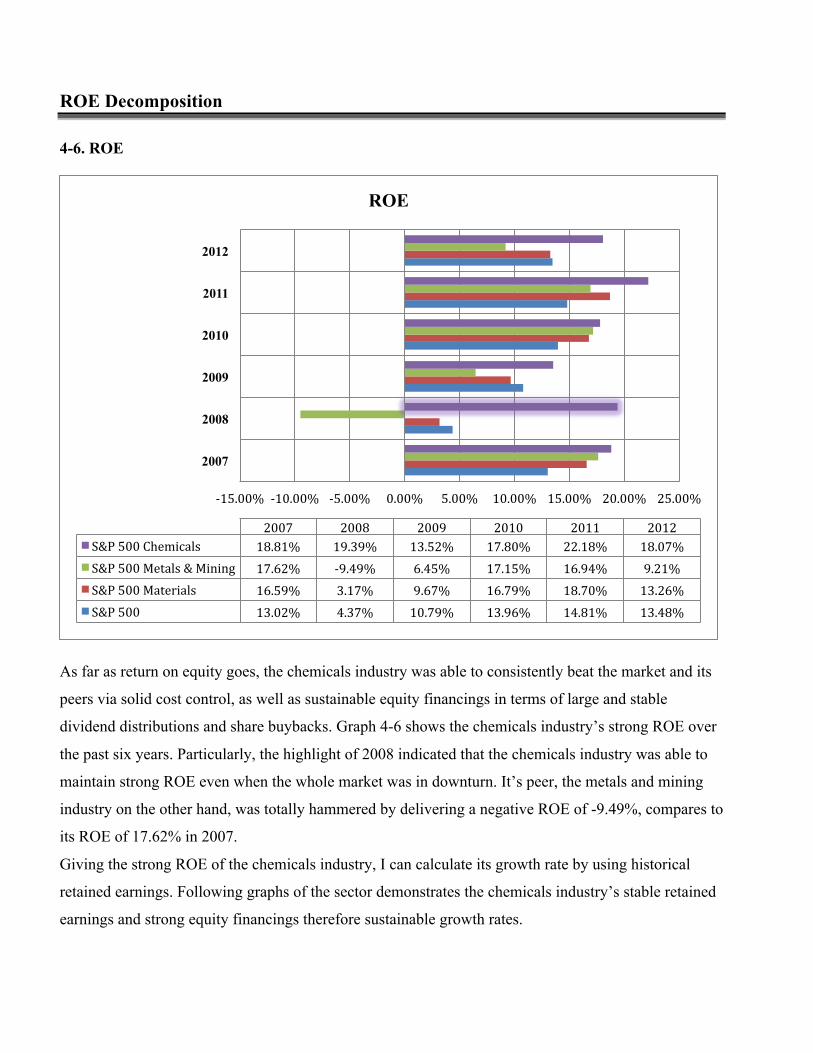

ROE Decomposition 4-6. ROE

As far as return on equity goes, the chemicals industry was able to consistently beat the market and its

peers via solid cost control, as well as sustainable equity financings in terms of large and stable

dividend distributions and share buybacks. Graph 4-6 shows the chemicals industry’s strong ROE over

the past six years. Particularly, the highlight of 2008 indicated that the chemicals industry was able to

maintain strong ROE even when the whole market was in downturn. It’s peer, the metals and mining

industry on the other hand, was totally hammered by delivering a negative ROE of -9.49%, compares to

its ROE of 17.62% in 2007.

Giving the strong ROE of the chemicals industry, I can calculate its growth rate by using historical

retained earnings. Following graphs of the sector demonstrates the chemicals industry’s stable retained

earnings and strong equity financings therefore sustainable growth rates.

-‐15.00% -‐10.00% -‐5.00% 0.00% 5.00% 10.00% 15.00% 20.00% 25.00%

2007

2008

2009

2010

2011

2012

2007 2008 2009 2010 2011 2012 S&P 500 Chemicals 18.81% 19.39% 13.52% 17.80% 22.18% 18.07% S&P 500 Metals & Mining 17.62% -‐9.49% 6.45% 17.15% 16.94% 9.21% S&P 500 Materials 16.59% 3.17% 9.67% 16.79% 18.70% 13.26% S&P 500 13.02% 4.37% 10.79% 13.96% 14.81% 13.48%

ROE

4-7. Retained Earnings [1 – Dividend Payout Ratio]

Abnormal retained earning of the materials sector can be explained by the earning of the whole sector

slumped further from -12.84% in 2007 to -86.09% in 2008, while the whole sector has decided to keep

its dividends as the highest level since 2006, creating large negative retained earnings. The metals and

mining industry followed the sector’s track and showed large negative retained earnings. Despite the

rapid drop of retained earnings in the materials sector and the metals and mining industry, the

chemicals industry was able to keep its retained earning positive without cutting too much dividends

payout as graph 4-9 shows. However, the nature of large dividend payback and shares buyback

activities of the chemicals industry implies its retained earnings were outpaced by the materials sector

as well as the metals and mining industry most of the time. But the key of keeping sustainable retained

earnings makes chemicals industry one step ahead of its peers. Following graphs further elaborates

how the chemicals industry utilizes its net financing cash flow, and distribute dividends to the

investors.

-‐200% -‐150% -‐100% -‐50% 0% 50% 100%

2007

2008

2009

2010

2011

2012

2007 2008 2009 2010 2011 2012 S&P 500 Chemicals 60.16% 44.84% 42.67% 59.48% 68.25% 51.20% S&P 500 Metals & Minings 76.60% -‐167.97% 59.44% 79.68% 73.87% 51.12% S&P 500 Materials 62.20% -‐169.01% 47.65% 67.62% 69.08% 47.78% S&P 500 68.08% -‐11.84% 61.50% 74.54% 74.23% 69.03%

Retained Earnings

4-8. Net Financing Cash Flow, Percentage Change

4-9. Historical dividend Growth Rate [ROE * Retained Earnings]

2007 2008 2009 2010 2011 2012 S&P 500 -‐38.01% -‐235.22% -‐70.47% -‐26.08% 5.08% 15.81% S&P 500 Materials 102.88% -‐472.63% 439.28% -‐222.39% 45.67% -‐150.03% S&P 500 Mtl&Mining 298.90% -‐91.09% 129.00% -‐221.62% 61.46% -‐160.56% S&P 500 Chemicals 22.87% 40.51% 324.94% -‐143.36% -‐38.07% -‐32.25%

-‐600.00%

-‐400.00%

-‐200.00%

0.00%

200.00%

400.00%

600.00%

Net Financing Cash Flow

2007 2008 2009 2010 2011 2012 S&P 500 8.86% -‐0.52% 6.64% 10.41% 10.99% 9.30% S&P 500 Materials 10.82% -‐5.36% 4.61% 11.36% 12.92% 6.34% S&P 500 Metals & Mining 13.50% 15.94% 3.83% 13.66% 12.51% 4.71% S&P 500 Chemicals 11.32% 8.69% 5.77% 10.59% 15.13% 9.25%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Growth Rate

As graphs 4-8 and 4-9 have shown, the chemicals industry could keep its net financing cash flow grow

at a faster and more stable rate than the market at the most of the time, and was able to keep its growth

rate close to the market when the materials sector as a whole was taken a large decline. Dividend

growth rate further demonstrates that the chemicals industry could adjust its dividends payout

accordingly without having large fluctuations in its net financing cash flows at the most of the time.

The materials sector and the metals and mining industry on the other hand were extremely volatile. It is

well known that industries able to keep sustainable dividend growth rates without hurting its net

financing cash flow always outpace those who have big up and downs over time.

However, special case can be found between 2009 and 2010, as the whole materials sector just

recovered from the financial crisis, dividend payout and share payback activities were almost doubled

in order to attract more capitals to flow into the sector. The chemicals industry responded by launching

its largest dividend payout and share buyback program in the past 6 years. Consequently, corresponding

large capitals inflow has enabled the chemicals industry to gradually keep its net financing cash flows

in order while maintain strong dividend payout. On the contrary, the materials sector and the metals and

mining industry’s net financing cash flows fell off the cliff after a temporary celebration in 2011,

therefore dragging down their growth. In next section, I will introduce the decomposition of the return

on equity of the materials sector, metals and mining industry, as well as chemicals industry comparing

to the market.

ROE as shown in the last section, is the most important element in comparing the profitability across

sectors and industries, which can be calculated by using Leverage ratio times Asset turnover

ratio times ROS times Interest burden times Tax burden. The ROE of the market was

averaged 11.7% over the past 6 years, relatively, the chemicals industry delivered an average of 18.3%

ROE over the same period, beating the market by 56%. And each of the ROE compositions of the

chemicals industry is significantly superior over its peers’. Given ROS (Operating Margin) in the

margin analysis section, following two sections further breakdown the other four variables into

turnover analysis and leverage analysis to elaborate how the strong ROE of the chemicals industry is

formed.

ROE Decomposition - Turnover Analysis

Materials Industry as a whole is very capital intensive, therefore one firm’s ability to allocate resources

accordingly is the key to maximize their profit and future growth. Comparing to S&P 500 index, the

materials sector has a much higher asset turnover due to widespread demands from all the other sectors,

and its limited ability of preserving its assets. While the Chemicals industry has relative higher asset

turnover compares to the Metals and mining industry and the sector as a whole. However, we can

observe that the asset turnover of the materials sector is in decline. Which is actually due to the

increasing profit margin and the oversupply issue.

4-10. Asset Turnover

2007 2008 2009 2010 2011 2012 S&P 500 30.73% 37.60% 33.93% 33.83% 36.02% 34.80% S&P 500 Materials 83.94% 96.15% 69.59% 75.99% 79.36% 74.96% S&P 500 Metals & Mining 74.83% 95.42% 58.83% 69.84% 74.49% 65.19% S&P 500 Chemicals 92.19% 104.77% 74.29% 78.26% 81.09% 77.85%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

Asset Turnover

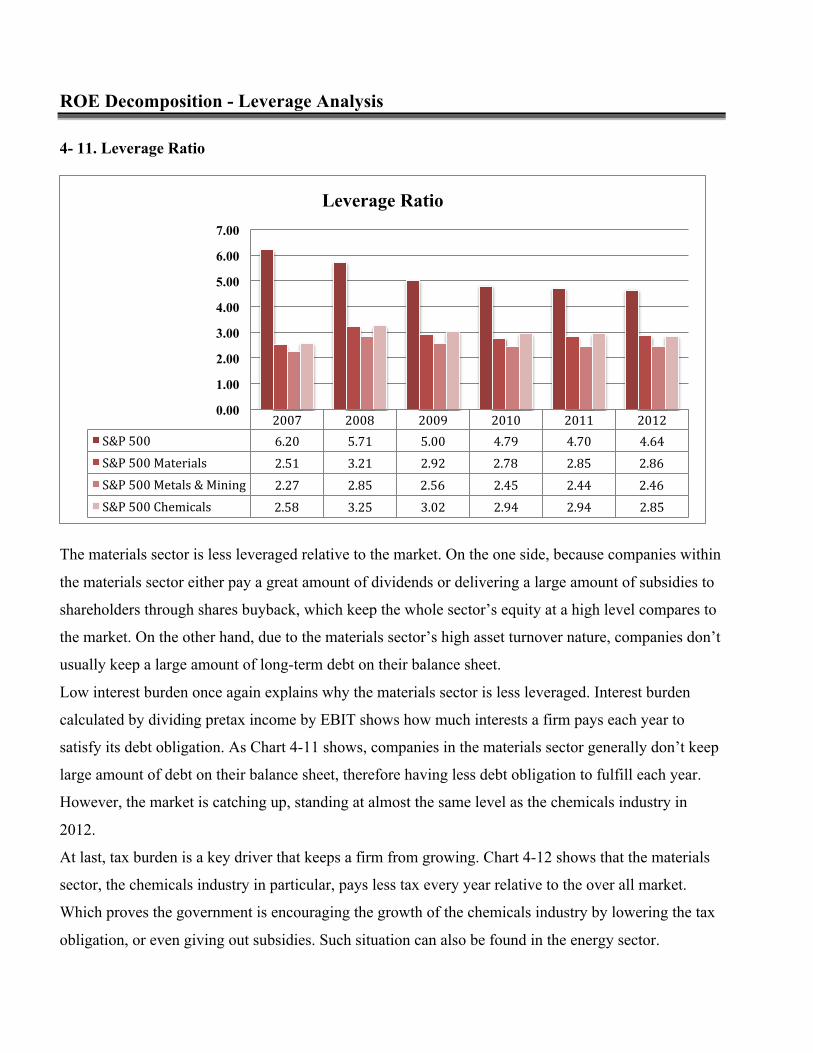

ROE Decomposition - Leverage Analysis 4- 11. Leverage Ratio

The materials sector is less leveraged relative to the market. On the one side, because companies within

the materials sector either pay a great amount of dividends or delivering a large amount of subsidies to

shareholders through shares buyback, which keep the whole sector’s equity at a high level compares to

the market. On the other hand, due to the materials sector’s high asset turnover nature, companies don’t

usually keep a large amount of long-term debt on their balance sheet.

Low interest burden once again explains why the materials sector is less leveraged. Interest burden

calculated by dividing pretax income by EBIT shows how much interests a firm pays each year to

satisfy its debt obligation. As Chart 4-11 shows, companies in the materials sector generally don’t keep

large amount of debt on their balance sheet, therefore having less debt obligation to fulfill each year.

However, the market is catching up, standing at almost the same level as the chemicals industry in

2012.

At last, tax burden is a key driver that keeps a firm from growing. Chart 4-12 shows that the materials

sector, the chemicals industry in particular, pays less tax every year relative to the over all market.

Which proves the government is encouraging the growth of the chemicals industry by lowering the tax

obligation, or even giving out subsidies. Such situation can also be found in the energy sector.

2007 2008 2009 2010 2011 2012 S&P 500 6.20 5.71 5.00 4.79 4.70 4.64 S&P 500 Materials 2.51 3.21 2.92 2.78 2.85 2.86 S&P 500 Metals & Mining 2.27 2.85 2.56 2.45 2.44 2.46 S&P 500 Chemicals 2.58 3.25 3.02 2.94 2.94 2.85

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Leverage Ratio

4-12. Interest Burden

4-13. Tax Burden

2007 2008 2009 2010 2011 2012 S&P 500 66.46% 51.69% 79.39% 85.62% 86.84% 87.05% S&P 500 Materials 86.86% 52.55% 71.79% 82.86% 86.18% 82.27% S&P 500 Metals and Mining 91.29% 178.49% 71.64% 88.03% 88.64% 83.21% S&P 500 Chemicals 89.38% 85.66% 78.15% 84.36% 88.63% 87.43%

0.00% 20.00% 40.00% 60.00% 80.00%

100.00% 120.00% 140.00% 160.00% 180.00% 200.00%

Interest Burden

2007 2008 2009 2010 2011 2012 S&P 500 64.18% 47.55% 71.53% 71.43% 71.75% 70.25% S&P 500 Materials 69.35% 53.52% 70.77% 74.82% 70.82% 69.43% S&P 500 Metals & Mining 63.24% 92.74% 61.44% 68.88% 67.35% 63.94% S&P 500 Chemicals 74.31% 72.43% 77.07% 73.83% 73.40% 72.50%

0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00% 70.00% 80.00% 90.00%

100.00%

Tax Burden

Valuation Analysis

Valuation analysis draws a clear picture of the performances of the sector and its underlying industries

relative to the market and each other. Here I mainly focus on three basic valuation multiples, price to

book, price to sale, price to earning. Following valuation analysis uses diversified metals and mining

sub-industry, as well as the diversified chemicals sub-industry to represent their industry groups.

Price to Book

An industry’s price to book ratio is closely related to its ROE. Although the metals and mining industry

has shown momentum P/B after the financial crisis, it was outpaced by the chemicals industry since

2011 due to its low ROE nature. And the gap is expected to widen in the next 1.5 year. The metals and

mining industry’s temporary high P/B can be explained by large stock buybacks using free financing

cash flows, which could not sustain due to the falling profit margin and raising liabilities. The

continuing underperformances are expected to see in the metals and mining industry in the next 5 to 10-

year horizon. The chemicals industry on the other hand, is expected to maintain sustainable growth in

the P/B ratios mostly reflected by large dividend payouts and sustainable earning growth.

2009 2010 2011 2012 2013(f) 2014(f) S&P 500 2.08 2.11 2.02 2.11 2.14 2.19 S&P 500 Materials 2.58 2.84 2.40 2.57 2.83 2.88 S&P 500 Deversibied Mtl&Mining 3.69 4.43 2.23 1.85 1.66 2.13 S&P 500 Deversibied Chemicals 2.35 2.95 2.70 3.04 3.24 3.57

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

P/B

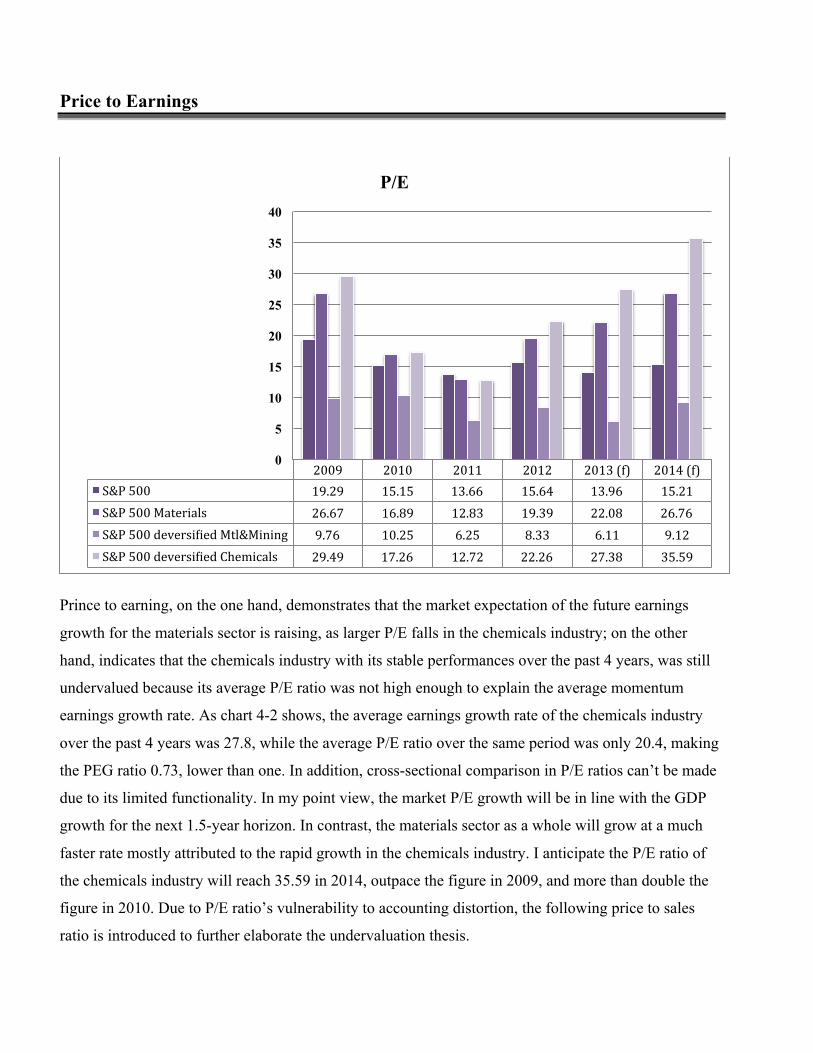

Price to Earnings

Prince to earning, on the one hand, demonstrates that the market expectation of the future earnings

growth for the materials sector is raising, as larger P/E falls in the chemicals industry; on the other

hand, indicates that the chemicals industry with its stable performances over the past 4 years, was still

undervalued because its average P/E ratio was not high enough to explain the average momentum

earnings growth rate. As chart 4-2 shows, the average earnings growth rate of the chemicals industry

over the past 4 years was 27.8, while the average P/E ratio over the same period was only 20.4, making

the PEG ratio 0.73, lower than one. In addition, cross-sectional comparison in P/E ratios can’t be made

due to its limited functionality. In my point view, the market P/E growth will be in line with the GDP

growth for the next 1.5-year horizon. In contrast, the materials sector as a whole will grow at a much

faster rate mostly attributed to the rapid growth in the chemicals industry. I anticipate the P/E ratio of

the chemicals industry will reach 35.59 in 2014, outpace the figure in 2009, and more than double the

figure in 2010. Due to P/E ratio’s vulnerability to accounting distortion, the following price to sales

ratio is introduced to further elaborate the undervaluation thesis.

2009 2010 2011 2012 2013 (f) 2014 (f) S&P 500 19.29 15.15 13.66 15.64 13.96 15.21 S&P 500 Materials 26.67 16.89 12.83 19.39 22.08 26.76 S&P 500 deversibied Mtl&Mining 9.76 10.25 6.25 8.33 6.11 9.12 S&P 500 deversibied Chemicals 29.49 17.26 12.72 22.26 27.38 35.59

0

5

10

15

20

25

30

35

40

P/E

Price to Sales

The low P/S of the chemicals industry delivers a potent message in telling the attractiveness and the

growth nature of the industry. The chemicals industry’s low leverage nature makes it more attainable

because P/S ratios don’t tell anything about a company’s debt obligation. In contrast, the metals and

mining’s high P/S ratios up until recent resulted from the falling prices have proven the fact that the

industry has been overvalued after the financial crisis. This is extremely true for highly cyclical

industries such as metals and mining industry, because there are years when only a handful of

companies in the industry produce any earnings. I believe P/S is a better measure than P/E to determine

how much investors were paying for a dollar of the industry’s sales rather than its earnings. For the P/S

ratios moving forward in the next 1.5 year, I believe the metals and mining industry will repeat its

cyclical nature with lower P/S in 2013 and higher P/S in 2014. The chemicals industry on the other

hand, I anticipate it to show continuing super-low P/S due to its sustainable cost control and enormous

future profit potential.

2009 2010 2011 2012 2013(f) 2014(f) S&P 500 1.23 1.31 1.19 1.31 1.19 1.12 S&P 500 Materials 1.27 1.34 1.06 1.20 1.09 1.24 S&P 500 Diversibied Mtl & Mining 2.24 2.95 1.69 1.82 1.71 2.01 S&P 500 diversibied Chemicals 0.82 1.02 0.82 0.99 0.94 0.84

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

P/S

Conclusion

To conclude, I recommend overweighting our holdings in the materials sector from its current 1.7

percent to 4.46 percent, 1.01 percent higher relative to the weight of S&P 500, by focusing on the

chemicals industry primarily because the increasing volume and decreasing price of the domestic

natural gas, as well as the maturing GTL technology will significantly reduce chemicals production

cost on the top of the industry’s strong cost control system. In addition, the solid growth of the product

line in the chemicals industry has strengthened by the decline in the mining industry, the government’s

support in the chemicals new technology development, and the increasing demand for alternative

materials such as plastics will send chemicals industry to a new level. Financial analysis further

demonstrates that the chemicals industry possesses strong gross margin and asset turnover to support

their high equity financing activities in terms of dividend payouts and share buybacks. Meanwhile, the

chemicals industry has maintained solid cost control and kept its revenue growth in line with the

market, which has given the industry the ability to sustain its growth rate and keep its net financing

cash flows in order. This is the key driver makes the chemicals industry superior than its peers within

the materials sector. Moreover, the chemicals industry could consistently beat the market was mostly

attribute to its strong balance sheet driven by low leverage ratio, low long term debt, as well as tax

advantages and subsidies from the government. Valuation analysis verifies the financial sustainability

of the chemicals industry, and examines that the chemicals industry has been undervalued although it

has outperformed its peers ever since the financial crisis. Given the chemicals industry’s sustainable

price to book, volatile price to earning, as well as low price to sale in the past four years, I expect price

to earning to increase dramatically next year, price to sale to slowly adjust to its fair value, and price to

book to stay high into the future.

References

John J. Conti, 2013, Annual Energy Outlook 2013 with projections to 2040, U.S. Energy Information

Administration

Mike Elliott, 2013, Business risks facing mining and metals, Ernst & Young

Mehdi Miremadi, 2013, Chemical innovation: An investment for the ages, Mckinsey on chemicals

Anthony Scamuffa, 2012, Shale gas reshaping the US chemicals industry, PWC

Jason Burkitt, 2013, What do investment professionals need from mining company reporting, PWC

Amy Hogan, 2013, Global mining deals 2012 review and 2013 outlook, PWC

Edwin Basson, 2013, World Steel in figures 2013, World Steel Association

Tobias Welo, 2012, 2013 Outlook: Materials, Fidelity

ICMM, 2012, Trends in the mining and metals industry, International Council on Mining & Metals

Louise Street, 2013, Gold Demand Trends, World Gold Council

Economics & Statistics Department, 2013, Shale Gas, Competitiveness, and New US Chemical

Industry Investment: An Analysis Based On Announced Projects, American Chemistry Council

Hongbin Qu, 2013, HSBC China Manufacturing PMI, HSBC

Adam Sieminski, 2013, International Energy Outlook 2013, U.S. Energy Information Administration

Dr. Edward Yardeni, 2013, Performance 2013 S&P 500 Sector & Industries, Yardeni Research

Elisabeth Rosenthal, 2013, U.S. to Be World’s Top Oil Producer in 5 Years, Report Says, The New

York Times

Zacks.com, 2013, Metals & Mining Stock Outlook – Industry Outlook, Nasdaq.com

Housley Carr, 2013, Industrials Say, “I’m a Believer,” But Will They Still Love the U.S. Tomorrow,

RBN Energy LLC

Russell Gold, 2013, U.S. Is Overtaking Russia as Largest Oil-and-Gas Producer, Wall Street Journal

Yajun Zhang, 2013, China’s Steel Industry Gains Steam, Wall Street Journal

Bob Tita, 2013, Natural Gas Powered Ships Arrive, Wall Street Journal

Chuin-Wei Yap, 2013, China’s Iron Ore Imports Surge to Record High, Wall Street Journal

WiseGeek, 2013, What is BTU? Wisegeek.org

U.S. Department of Commerce, 2013, New Housing Units Started in the United States, Census.gov

Kavaljit Singh, 2013, Collapsing Asian Currencies? Why is the Indian Rupee Depreciating, Global

Research

Morningstar, 2013, Stock Returns, Morningstar.com