Embed Size (px)

Citation preview

ON

ECOMPANY

BRUSH ENGINEERED MATERIALS INC.

ACADEMY CORPORATION

BARR ASSOCIATES, INC.

BRUSH CERAMIC PRODUCTS INC.

BRUSH WELLMAN ALLOY PRODUCTS

BRUSH WELLMAN BERYLLIUM PRODUCTS

CERAC, INCORPORATED

TECHNI-MET, LLC

TECHNICAL MATERIALS, INC.

THIN FILM TECHNOLOGY, INC.

WILLIAMS ADVANCED MATERIALS INC.

2010 ANNUAL REPORT

ON

ECONTENTSAbout the Company, Financial Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Inside front Introduction to Materion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1Letter to Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6One Company: Financial Data and Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10One Name: Our New Name and Unified Brand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12One Goal: New Collaboration and Synergies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14One Focus: Fast-growing Market Niches . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Operating Summary and Shareholder Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182010 Form 10-K . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Directors, Officers and Facilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122Corporate Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

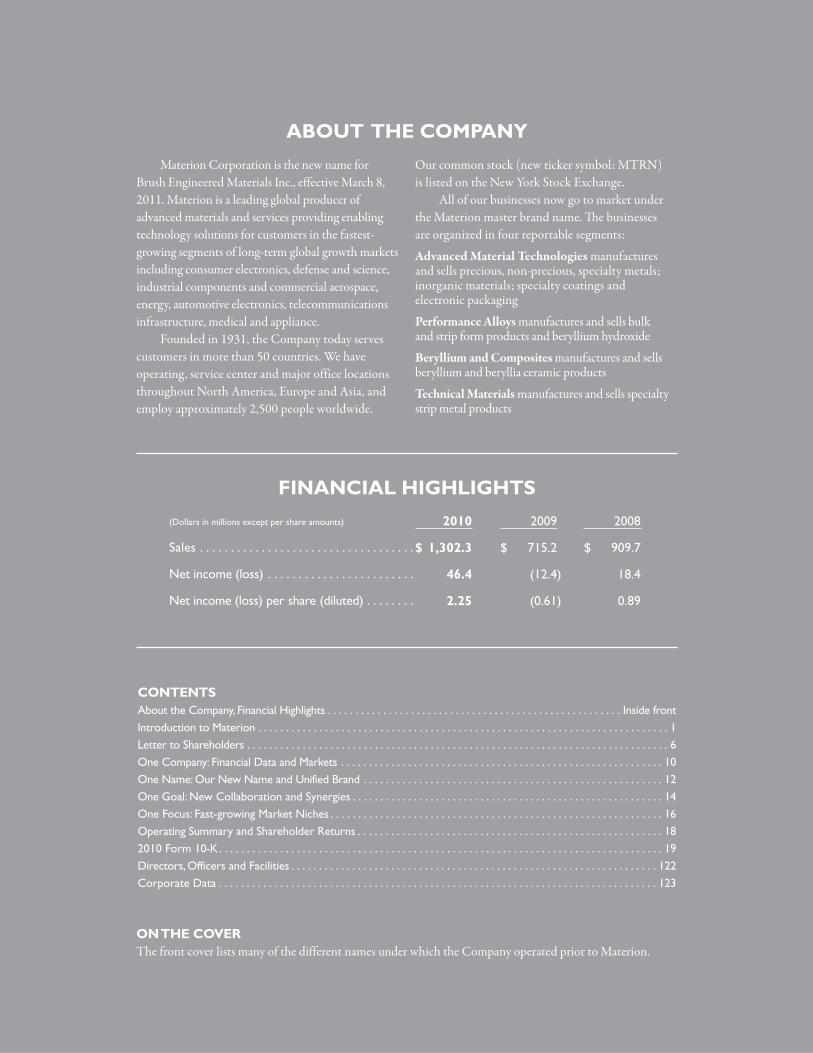

Materion Corporation is the new name forBrush Engineered Materials Inc., effective March 8,2011. Materion is a leading global producer of advanced materials and services providing enablingtechnology solutions for customers in the fastest-growing segments of long-term global growth marketsincluding consumer electronics, defense and science,industrial components and commercial aerospace, energy, automotive electronics, telecommunicationsinfrastructure, medical and appliance.

Founded in 1931, the Company today servescustomers in more than 50 countries. We haveoperating, service center and major office locationsthroughout North America, Europe and Asia, andemploy approximately 2,500 people worldwide.

Our common stock (new ticker symbol: MTRN) is listed on the New York Stock Exchange.

All of our businesses now go to market underthe Materion master brand name. The businesses are organized in four reportable segments:

Advanced Material Technologies manufactures and sells precious, non-precious, specialty metals; inorganic materials; specialty coatings and electronic packaging

Performance Alloys manufactures and sells bulk and strip form products and beryllium hydroxide

Beryllium and Composites manufactures and sellsberyllium and beryllia ceramic products

Technical Materials manufactures and sells specialtystrip metal products

ABOUT THE COMPANY

FINANCIAL HIGHLIGHTS

2009

$ 715.2

(12.4)

(0.61)

2008

$ 909.7

18.4

0.89

2010

$ 1,302.3

46.4

2.25

(Dollars in millions except per share amounts)

Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Net income (loss) . . . . . . . . . . . . . . . . . . . . . . . .

Net income (loss) per share (diluted) . . . . . . . .

ON THE COVER The front cover lists many of the different names under which the Company operated prior to Materion.

ON

ENAME

One Company. One Name. Transformative initiatives, organic growth and

strategic acquisitions dramatically broadened our productportfolio and worldwide footprint. Yet with many

loosely connected brands we lacked the strong brandrecognition appropriate for our size and scale. Many

customers were served by more than one of ourbusinesses without realizing it. Others didn’t fullyperceive all the ways we might help them. Today,

rebranded and unified, we bring those issues to a close.One company. One name. Materion.

ON

EGOAL

One Goal…To be our customers’ first choice. And why not?

We form deep bonds with our customers by helping them conceive and design technical and performanceadvantages. Our advanced materials solutions make

products higher performing: Lighter. Stronger. Smaller.Thinner. Exceptionally precise. Optically superior.

Remarkably resistant to vibration, corrosion ortemperature extremes. It’s no wonder customers chooseMaterion, we help achieve goals. And our goal – to be

their first choice – is now more broadly achievable sinceexpected synergies from unifying our businesses will

facilitate additionally comprehensive solutions.

One Focus…Just imagine; a company founded eight decades agoremains a leader today in fast-growing segments of fast-growing global markets. In fact, that’s the case.

Materion’s relentless focus – on long-term growth marketswith compelling demand drivers, strong margins and

differentiated technologies – largely explains our success.That focus also explains our optimism for the future.

As the world demands ever-more advanced technologiesin markets like consumer electronics, defense and science,commercial aerospace, telecommunications infrastructure,

medical and energy, Materion stands ready – on ourcustomers’ behalf – to continue innovating for the future. ON

EFOCUS

To Our Shareholders:

Today, it is our great pleasure to introduce you toMaterion. We hope you come to know the name well.

Investors have known us for many years as Brush

Engineered Materials. Customers, on the other hand, have

known us by one or more of many different names and

brands built and acquired over eight decades in business.

Those who have followed the Company’s transformation

from a specialty metals business to an advanced materials

company will certainly recognize why a unified name and

brand structure is the next logical step in our evolution. To

increase global awareness and leverage worldwide capabilities,

facilitate synergies, efficiencies and cross-selling opportunities,

our businesses are now unified under one name and one

brand – Materion.

What a Difference a Year MakesWhile our new name and structure provide a solid

platform for future growth, you likely are more interested in

hearing about our financial performance in 2010. As is often

said, what a difference a year makes! Like so many companies

at this time last year, Materion was responding to the

profoundly adverse effects from tough economic conditions

around the world. In 2010, however, we more than over-

came those challenges. Coming out of recessionary

challenges, we posted record sales, strong margins

and important gains in market penetration.

Driving Sales to a Record $1.3 BillionFor the first time in Company history,

revenues in 2010 exceeded $1 billion. Sales

climbed 82% from 2009 to $1.3 billion.

Revenue gains were driven first and fore-

most by healthy, broad-based increases in

demand across most of our key markets, ON

ECOMPANY

7

beginning with robust restored demand in consumer

electronics early in the year. Following this, we saw demand

return in the telecommunications infrastructure market.

As the year progressed, we experienced stronger demand

from customers in industrial and commercial aerospace,

energy (especially oil and gas) and in high performance

optical applications. Demand was also strong in defense

and automotive electronics.

In addition to strong organic growth, our two most

recent acquisitions – Barr Associates (October 2009) and

Academy Corporation (January 2010) – added approxi-

mately $233 million to sales and were accretive to earnings

by approximately $0.30 per share. Metal price increases

passed along to customers accounted for approximately

$103 million of sales growth. The precious metal content of

our sales has increased significantly due to growth, acquisi-

tions and metal price increases. Sales growth net of metal

price inflation was approximately 68% in 2010, and excluding

acquisitions, our organic growth was 35% for the year.

Higher Value Mix Yields Profitability Gains Profitability improved notably throughout the year.

We posted near-record earnings of $46.4 million, or $2.25

per share, an extraordinary turnaround from a 2009 loss

of $12.4 million, or $0.61 per share. Reported operating

margins showed substantial improvement, particularly in

view of the dilutive effect of higher pass-through metal

pricing and higher precious metal volumes in our sales mix.

In addition to viewing our margins on a GAAP basis, we

also measure margins internally on a “value-added” basis;

that is, with metal costs excluded from revenues, because

we believe that provides a better measure of our operating

performance. On this basis, our 2010 gross profit margin

is above 40%, compared to the reported 17%. Similarly,

operating margin is in the mid-teens as opposed to the

reported 6%. These value-added-basis margins improved

substantially in 2010.

Improved profitability benefited from ongoing strategic

initiatives to both broaden and diversify our market base

and to shift our mix toward faster-growing, higher-value

materials and less cyclical market sectors. Expanded well

beyond integrated and specialty metals, our product portfolio

and distinctive competencies encompass precision optical

filters, specialty inorganic chemical powders and evaporative

materials, precious metals refining and management, large

“Coming out of recessionary challenges, we postedrecord sales, strong margins and important gainsin market penetration.”

$1,302$763 $956 $910 $715

Total Sales(in millions)

$0

$400

$200

$800

$600

$1,200

$1,000

$1,400

Gross Margin(in millions)

$162 $197 $152 $91 $223

Average Sales per Employee(in thousands)

$524$349 $434 $407 $326

06 07 08 09 10 06 07 08 09 1006 07 08 09 10

$150

$100

$50

$200

$250

$0

$200

$400

$600

$0

and small area thin film deposition, electronic packaging

materials, and engineered clad and plated metal systems.

With this unmatched offering of related materials and

capabilities, we focus on the fastest-growing, technology-

driven segments of sustainable global growth markets.

Today, we primarily produce high-value, innovative

and technologically advanced materials that customers

$70 million at year end. Our ratio of debt-to-debt-plus-

equity was approximately 18% at year end. A healthy

balance sheet, coupled with ongoing positive cash flows

from operations, gives us the financial flexibility to make

important investments in the business and to continue to

evaluate complementary acquisitions or other strategic

growth initiatives.

8

“We look ahead with confidence and optimism. OurCompany’s sales have been growing at a compoundannual rate of 17% since 2002.”

Debt-to-Debt-Plus-EquityNet Cash Provided from

Operating Activities(in millions)

Earnings Before Interest, Taxes, Depreciation and

Amortization (EBITDA)*(in millions)

$20

$40

$60

$80

5%

15%

10%

20%$68 $108 $62 $12 $109 15% 9% 11% 16% 18% $39 $51 $77 $42 $31

06 07 08 09 10 06 07 08 09 10 06 07 08 09 10

$40

$80

$120

$0 0% $0

need to achieve differentiating designs and engineering

characteristics essential to stay at the forefront of rapidly

changing markets. As a result, we rarely compete in

commoditized spaces.

Profitability gains were also aided by significant

improvements in our cost structure, principally due to

a lowered breakeven point for our Performance Alloys

business and through the ongoing success of our lean sigma

programs throughout the Company, as well as by enhanced

pricing models.

At the same time, we continue enjoying organic and

acquisition growth in our businesses which generally have

lower infrastructure and capital costs. The Company

entered and exited 2010 with a very strong balance sheet.

Even with more than $76 million invested in the Barr

Associates and Academy acquisitions, debt net of cash was

Rapid Recovery Affirms Transformative Strategy We’d likely be proud to report results like these most

any year. We’d be remiss, however, if we didn’t underscore

how rewarding it is to report them for 2010.

The challenging economic conditions putting most

businesses and industries to the test during this time are

well known. Simply put, our Company, our team, recovered

quickly and convincingly. And, we recovered quicker and

stronger than in the last recession, while in an indisputably

tougher environment. During the last recession, we posted

losses for three years. Following this recession, we turned

the corner after just two quarters and drove record sales

coming out.

Diversifying our portfolio. Focusing on high-growth

market niches and high-value products. Reducing risk

and cyclicality. These transformative measures have been

*A non-GAAP measure used as an indicator of cash generation,EBITDA is operating profit plus depreciation and amortization.

implemented consistently. Our evolved business model is

primed for capitalizing on market growth opportunities

while also providing resiliency against market turbulence.

Investing to Capitalize on Future OpportunitiesWhile our multi-year transformation strategy is

credibly paying off, we remain focused on investing in

our business to be our customers’ first choice, driving

their and our future success. In early 2011, we completed

construction of a new state-of-the-art primary beryllium

manufacturing facility in Elmore, Ohio, and are now

ramping up production. This flagship plant resulted from

a $94 million public-private partnership between our

Company and the U.S. Department of Defense, built to

secure a sustainable domestic supply of beryllium and

beryllium products for our country’s national defense.

Demand for beryllium products continues to expand for

optics, satellite structures, medical imaging, and for critical

components in aircraft and missile defense.

Unifying and branding our businesses as Materion

is another long-term investment in our future. While

reaping many benefits from our transformation, we have

not achieved our full business potential. Positioning

Materion as a single, unified organization will broaden

our customers’ awareness of the total scope of our offerings

and enable us to better compete for business, acquisitions

and talent globally.

Global Market Trends Point to Favorable OutlookToday, we look ahead with confidence and optimism.

Our Company’s sales have been growing at a compound

annual rate of 17% since 2002 – 10% organic growth.

Our goal is to continue delivering double digit organic

growth, on average over time, and augment that with

strategic and manageable acquisitions.

We believe we are entering an exciting period of

accelerated and sustainable growth driven by strong secular

trends and by our market and product positioning. Overall

market conditions are continuing to improve. Our position

in faster-growing overseas markets is also strengthening.

Our transformation strategy is yielding good results.

Customers count on us to deliver innovative, technologically

advanced material solutions for their critical applications.

We have demonstrated our ability to identify and succeed

in high-growth niche markets with promising futures.

Demand for high-end, more sophisticated electronics in

both consumer products and automotive applications is

expected to continue to expand, as will requirements for

new materials-based technology solutions in high-growth

segments of energy, medical and defense.

As a result of focused product development, organic

growth and good acquisitions, our portfolio today is signifi-

cantly more diverse, less cyclical and more robust than in years

past. We have become leaner and faster-growing, with a

higher-value business model in terms of growth potential,

margins, cash flow, balance sheet and capital structure.

Our new and unified name reflects the new and

unified Company we have become, and provides a common

platform for future growth.

In closing, we thank our employees for their hard work

and dedication in making 2010 so successful, and for their

outstanding execution of our strategies. We also thank you,

our shareholders, for your past investment and continued

confidence in our Company, our team and our future as a

brand new Materion.

Richard J. HippleChairman, President and Chief Executive Officer

9

ON

ECOMPANY

‘‘Our portfolio today is significantly more diverse,less cyclical and more robust than in years past.’’

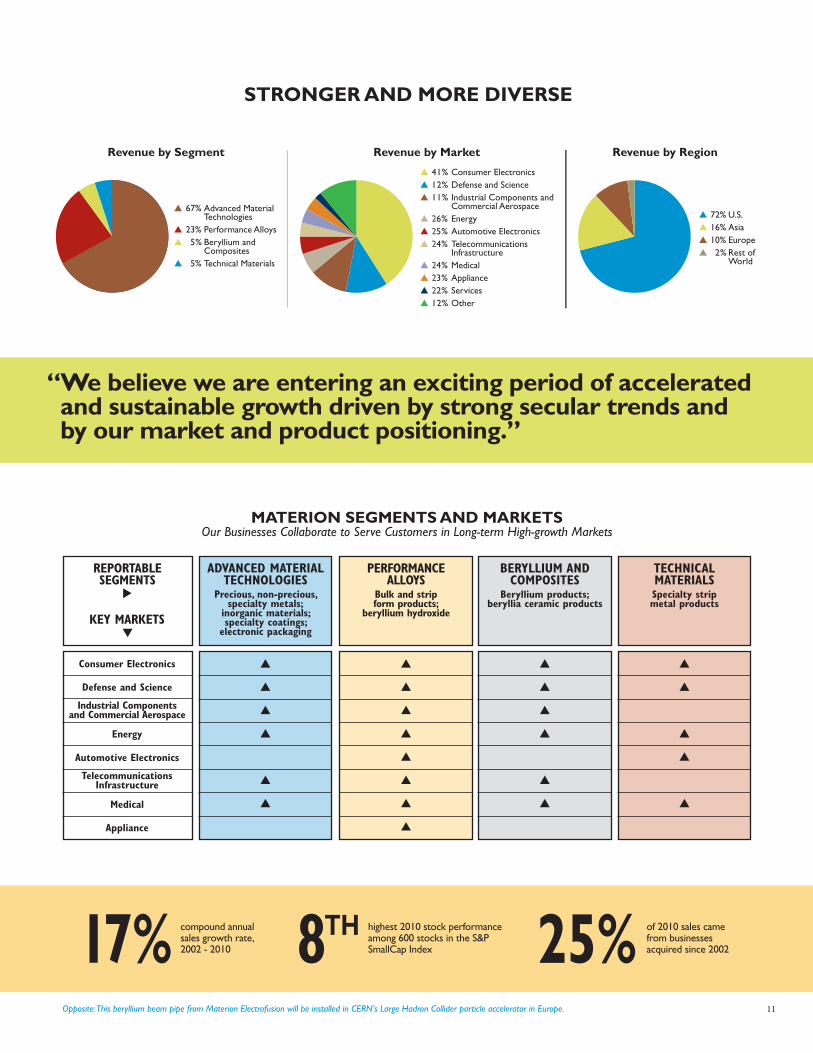

One Company... that has become leaner, faster-growing, more diversified and less cyclical.

The success of our transformation strategy is reflected in record revenues, better margins andstronger market penetration achieved in 2010.Today, we have a higher-value business model in terms of capital intensity, growth potential,

margins, cash flow, balance sheet and capital structure. And our businesses are now

structured to collaborate in new andmeaningful ways across fast-growing

segments of fast-growing markets.

BERYLLIUM AND COMPOSITES

Beryllium products;beryllia ceramic products

11

17% compound annualsales growth rate,2002 - 2010 8TH highest 2010 stock performance

among 600 stocks in the S&PSmallCap Index 25% of 2010 sales came

from businesses acquired since 2002

STRONGER AND MORE DIVERSE

▲ 72% U.S.

▲ 16% Asia

▲ 10% Europe

▲ 222% Rest of World

▲ 41% Consumer Electronics

▲ 12% Defense and Science

▲ 11% Industrial Components and Commercial Aerospace

▲ 26% Energy

▲ 25% Automotive Electronics

▲ 24% Telecommunications Infrastructure

▲ 24% Medical

▲ 23% Appliance

▲ 22% Services

▲ 12% Other

▲ 67% Advanced Material Technologies

▲ 23% Performance Alloys

▲ 225% Beryllium and Composites

▲ 225% Technical Materials

Revenue by Segment Revenue by Market Revenue by Region

MATERION SEGMENTS AND MARKETSOur Businesses Collaborate to Serve Customers in Long-term High-growth Markets

KEY MARKETS

REPORTABLE SEGMENTS▲

▲

ADVANCED MATERIALTECHNOLOGIES

Precious, non-precious, specialty metals;

inorganic materials; specialty coatings;

electronic packaging

▲

▲

▲

▲

▲

▲

PERFORMANCEALLOYS

Bulk and strip form products;

beryllium hydroxide

TECHNICALMATERIALSSpecialty stripmetal products

Consumer Electronics

Defense and Science

Industrial Components and Commercial Aerospace

Energy

Automotive Electronics

TelecommunicationsInfrastructure

Medical

Appliance

▲

▲

▲

▲

▲

▲

▲

▲

▲

▲

▲

▲

▲

▲

▲

▲

▲

▲

▲

“We believe we are entering an exciting period of acceleratedand sustainable growth driven by strong secular trends and by our market and product positioning.”

Opposite:This beryllium beam pipe from Materion Electrofusion will be installed in CERN’s Large Hadron Collider particle accelerator in Europe.

ON

ENAME

“Those who have followed the Company’s transformation…will certainly recognize why a unified name brand… is the next logical step in our evolution.”

One Name... One brand new name for an 80-year-old company. What’s behind the name? With Materion, it was a deliberate, logical and evolutionary step following significant growth,

a series of successful acquisitions, and numerous internal and external initiatives that fundamentally

changed our organization. We completed the transformation into a global advanced materials company with expertise in metallurgy, chemistry,

thin film deposition, specialty coatings and optical filter technology from our origins

as a North American metals business.

Investing in One Name for the FutureThe enterprise we are today, with sales beyond

$1 billion, a dramatically broadened geographic footprintand a product portfolio serving fast-growing sectors of expanding global markets, is what we proudly call Materion.

We believe this investment in strategic rebranding –unifying us as one company with one name – is in the bestinterests of customers, shareholders and employees. It unitesa complicated assortment of brands, each with its own nameand visual identity. Most investors knew our former corporatename: Brush Engineered Materials. Yet customers knew usby up to a dozen different names. In fact, we serve a numberof customers from two or more of our businesses.

In addition to being less confusing, a single masterbrand accelerates greater appreciation for our full scope of product and service solutions. We have the resources to compete effectively. Greater global awareness enhancesour competitive edge going forward.

One Name for One CompanyWith technology the lifeblood of our customers, it

was appropriate to adopt a name with updated appeal andwider relevance, one that accurately reflects our business.

To enhance collaboration and cross-selling, we recastall of our businesses as Materion. One name is simpler for customers. One name builds internal teamwork. Onename brings consistency and focus. One name maximizesmarketing resources and provides a range of possibilities fornew synergies benefitting customers. One name acceleratesglobal awareness. Most of all, one name is a long-term invest-ment in Materion, a company with a proud heritage and afuture filled with promising opportunities.

13

2,500 Materion employees work at our 30 facilities in 11 countries 50 countries are home to more than

9,000 Materion customers, using oursolutions in their products worldwide 1company with one name; all our

businesses are now unified underMaterion as a single master brand

Clockwise: Loading electronic package componentsfor brazing in Newburyport, Massachusetts; rollingspecialty metals in Lincoln, Rhode Island; metaland ceramic brazing operations in Newburyport,and monitoring our new primary beryllium facility in Elmore, Ohio.

Opposite: Visi-Lid™ optical window assemblies prepared in a cleanroom in Buffalo, New York.

ON

EGOAL

One Goal… Rebranding and unifying Materion is fundamentally about further achieving

our number one goal: to become and remain our customers’ first choice as a trusted partner

for whatever comes next in their world. In our world, it is about capturing synergies, enhancing collaboration, reducing costs and

building a more powerful marketplace position.

‘‘We focus on the fastest-growing, technology-drivensegments of sustainable global growth markets.’’

Emphasizing Our One GoalWe are proud of our deep customer bonds. Materion

has helped innovate and improve everything from medicaldevices to smart phones; solar photovoltaic cells to deepwater drilling; commercial airliners to unmanned militaryaircraft. Customers depend on us to solve problems, providedifferentiating ideas and help them meet ever-advancingtechnology demands.

Years of innovation go a long way toward making us afirst choice, but we challenge ourselves to continuously offermore. In the past, a solution inside our organization to a customer’s engineering challenge may have never been consid-ered because of how we were structured. As one companywith one name, we increasingly collaborate on innovation to leverage combined capabilities across our businesses.

The Power of CollaborationCollaborative opportunities capitalizing on the breadth

of our portfolio are energizing because many of our businessessupply related materials and services to complementaryindustries and sectors. For example, Materion Electrofusionand Materion Barr Precision Optics & Thin Film Coatings arecollaborating to apply specialty vapor deposition coating ontoberyllium metal x-ray windows, helping customers producecompact x-ray tubes that verify purity and safety of food,toys and metals. Elsewhere, Materion Advanced Chemicalsand Materion Ceramics are helping customers produce thelatest-generation of thin film solar cells by teaming up to useceramic and powder metallurgical engineering for highlycompact vapor deposition targets.

For the rapidly growing energy management market,Materion Technical Materials and Materion Brush Performance Alloys have partnered to produce electron beamwelded composite alloys in rod, wire and strip form for largehigh-power shunt resistors. Shunt resistors are used in smartmeters for monitoring real-time power grid energy usage andfor hybrid and electric vehicle battery management. Andnearly all our businesses have capabilities serving the growingLED (light-emitting diode) market to help manufacturersand material suppliers produce energy-saving LED wafers,lenses, reflectors, dies, phosphors, connectors, substrates,thin film deposition and packaging.

Customers know we will help develop solutions for tomorrow’s still-undiscovered challenges. Now, we offermore resources and share in the benefits of deeper, moremeaningful partnerships.

Internal SynergiesOur new structure and unified brand is expected to

yield other synergies that deepen customer relationships and drive earnings. We expect increased buying leverage and a more efficient customer supply chain. Concentratedmarketing resources present another promising area. Seventeen websites have been consolidated as one. Greaterawareness of our size and scope helps us attract and retaintop talent, and will strengthen future negotiations withbanks, landlords or even acquisition targets. Further, onebrand provides a platform that will simplify integration of future acquisitions.

15

6 different Materion businesses areactive in the alternative energymarkets 17 websites formerly represented our

many businesses; today customers canfind all our solutions in one unified place at www.materion.com

#1our goal is to be the first choice amongour customers; a trusted partner they recommend to others for a wide rangeof solutions

Clockwise: Refining silver for vapordeposition targets in Albuquerque,New Mexico; electron beam weldedresistor materials in Lincoln, RhodeIsland; processing precision microslitfilms in Bloomfield, Connecticut, and inspecting window lid components inBuffalo, New York destined for our Singapore assembly facility.

Opposite: Loading x-ray tube windows from Fremont, California into tooling for magnetron sputter coating in Buellton, California.

ON

EFOCUS

One Focus… Our company has a long history ofbeing on the leading edge of technology and today

remains at the forefront of fast-growing segments within high-growth markets,

precisely where our customers need us most. We succeed where premium performance is

demanded and margins can be protected. This strategy enabled our strong 2010 performance and gives us confidence

in our future. We believe we are entering a period of sustainable growth driven

by secular trends and strong positioning in important market segments.

“Customers count on us to deliver innovative, technologically advanced material solutions for critical applications.”

Our High-growth, High-value MarketsConsumer Electronics – Portability, multi-functionality, increased storage, next-generation LED lighting – are alltrends enabled by our advanced materials. To be essential in tomorrow’s electronics breakthroughs, we support early stageproduct development with customer design centers aroundthe world. Rapid innovation, compressed product life cyclesand fierce competition mean customers depend on us for solutions for the latest devices including smart phones, tabletcomputers, flat-screen TVs, and high-end home audio andtheater systems.

Defense and Science – Sophisticated imaging, surveillanceand targeting technologies are critical to defense, science andsecurity. Our materials are in satellite components, infraredsensors, radar navigation, night vision optics, laser-guidedweapons and other end uses. Because our materials are light,strong and stiff, vibration resistant, manage light at all wave-lengths and handle temperature extremes, they are selectedfor space probes, scientific particle colliders, reconnaissancesatellites, submarine mechanisms, targeting systems and military aircraft.

Industrial Components and Commercial Aerospace – Ouralloys and beryllium materials offer superior strength, weightsavings, corrosion resistance, high thermal and electricalconductivity, and anti-galling characteristics. Bushings andbearings made from our materials have greater load-bearingcapabilities and in-service life than alternatives, increasinguptime and fuel savings. These benefits provide a rapid returnon investment in applications like mining and off-highwayequipment, and commercial aircraft.

Automotive Electronics – Evolving technology in cars andtrucks increases demand for higher reliability and higherperforming materials. Airbag crash sensors, anti-lock braking,electrical steering, engine and stability control systems must allperform unfailingly. Growing demand for alternative energyvehicles is driving new technological challenges met by thecollective properties of our clad and multi-metal systems, andcopper beryllium and ToughMet® copper-nickel-tin alloys.

Telecommunications Infrastructure – A robust telecommuni-cations infrastructure calls for higher component connectivitybetween satellite, cable, fiber optics and wireless broadbandincluding 3G, 4G/LTE, and WiFi. Our materials improve

coaxial connector terminals, dense wavelength optical systemsand thermally optimized packaging for semiconductors inhigh power amplifiers at base stations and undersea cable repeater housings. Elsewhere, we enable integrated circuitchip interconnects, strengthen router/server connections,improve local area network reliability and provide digitalTV broadcasting packaging solutions.

Medical – Medical advances, longer life expectancies and agrowing global population are increasing demand for highperforming medical devices and equipment that work safelyin and around the human body. Our materials are found indiabetes blood glucose test strips and meters, implanted insulin pumps, CT imaging and mammography x-ray systems,cancer radiation therapy, blood and DNA analysis, surgicalinstruments and pacemakers.

Energy – Rising worldwide consumption, higher adoption of alternative energy and harsh drilling environments are expanding our opportunities in this market. Our highstrength, low friction, non-magnetic, non-sparking, anti-corrosive materials are widely used throughout the oil andgas sector, even in curtailing the 2010 Gulf of Mexico oilspill. Polycrystalline silicon thin film, concentrator photo-voltaic technologies and innovative flexible solar technologyintegrated into building components all depend on our materials. You’ll also find us in nuclear and wind power systems, and fuel cells.

Our advanced chemicals, ceramics and thin film materialsare helping to increase solar cell efficiency and lower costs. Heavy equipment makers specify our ToughMet® copper-nickel-tin alloys for bearings and other critical components. Materion’s specialty alloys, ceramics and electronic packagingmaterials help the telecommunications infrastructure supportrising traffic volumes.

17

99% of the world’s cell phonesare estimated to containcomponents made fromour materials 75% of 2010 sales came

from advancedmaterials comparedwith 47% in 2002

$1.3 billion – for the first time inCompany history revenues surpassed$1 billion in 2010 driven by strongdemand in fast-growing markets

Opposite: Portable electronic devices are increasingly utilized in the workplace to gather, manage and transmit information.

18

OPERATING SUMMARY

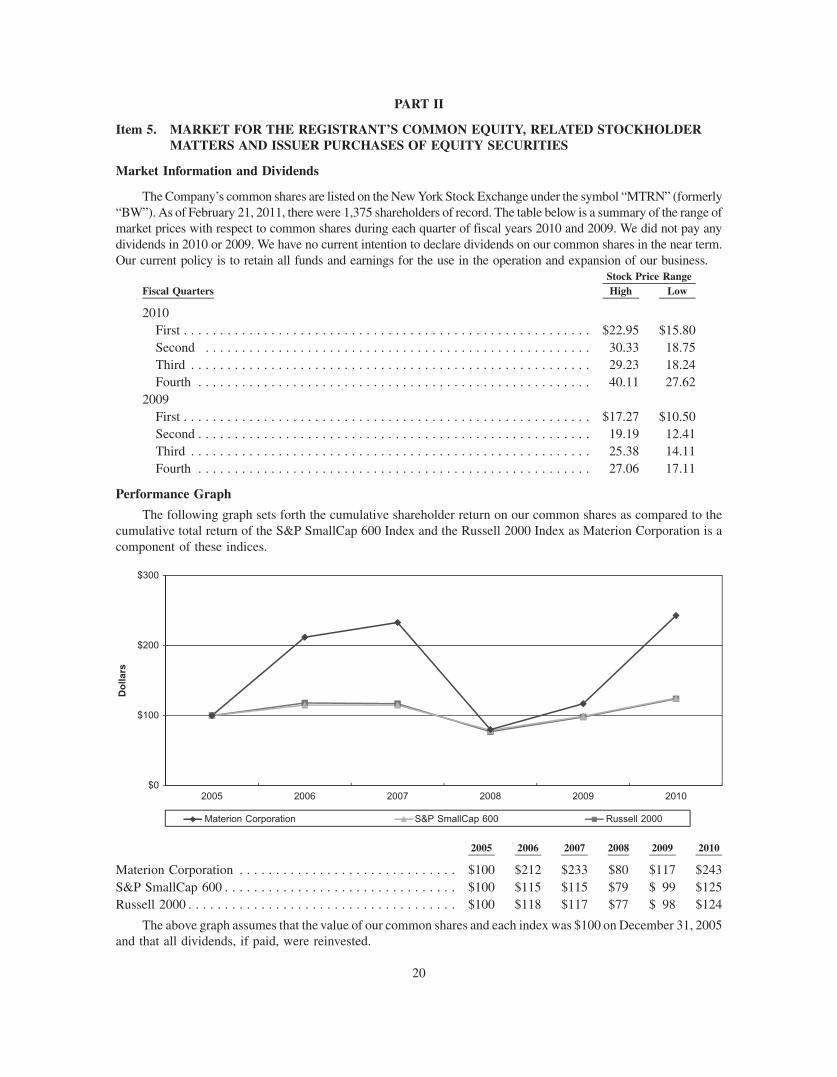

The following graph sets forth the cumulative shareholder return on our common shares as compared to the cumulative total return of the S&P SmallCap 600 Index and the Russell 2000Index. Materion Corporation is a component company of theS&P SmallCap 600 Index and the Russell 2000 Index.

Performance Comparison

2005 2006 2007 2008 2009 2010

Materion Corporation $100 $212 $233 $80 $117 $243

S&P SmallCap 600 $100 $115 $115 $79 $99 $125

Russell 2000 $100 $118 $117 $77 $98 $124

Assumes that the value of our common shares and each index was $100 on December 31, 2005 and that all applicable dividends were reinvested.

$50

$100

$150

$200

$250

2006 2007 2008 2009 2010$0

S&P SmallCap 600 Russell 2000 Materion Corporation

For the Years Ended December 31,

* Return on invested capital = operating profit/(average debt + average equity – average cash)

** Non-GAAP operating run rate is computed by excluding or adjusting from operating profit derivative ineffectiveness expense of $4.9 million on a copper derivative embedded in a debt obligationsecured during 2009, lower of cost or market inventory charges of $0.7 million in 2009 and $15.2 million in 2008, a 2007 accounts receivable correction of $2.6 million recorded in 2008 andother non-operating expenses of $2.9 million in 2009 and $0.6 million in 2008, and excluding from net income discrete tax items of $1.0 million in both 2009 and 2008. Managementbelieves that the non-GAAP run rate is more reflective of the earnings or loss directly attributable to the investments in our operating businesses.

2010

$ 1,302,314 73,633 70,968 46,427 31,041 (14,938) (31,581) 19,820

$ 2.25 20,590$ 38.64 18.67

5.7% 17.4% 18%

$ 73,633 2.25 17.4%

2,484$ 524

2009

$ 715,186 (19,485) (20,784) (12,355) 41,643 (54,107) (16,703) 23,117

$ (0.61) 20,191$ 18.54 16.83

(2.7%) (5.1%) 16%

$ (10,985) (0.38) (2.9%)

2,196$ 326

2008

$ 909,711 28,071 26,076 18,357 76,877 (63,137) (27,853) 752

$ 0.89 20,543$ 12.72 16.90

3.1% 7.7% 11%

$ 46,471 1.44 12.8%

2,235$ 407

(Dollars in thousands except per share amounts)

Operating DataNet sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Operating profit (loss) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Income (loss) before income taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Net income (loss) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Net cash provided from operating activities . . . . . . . . . . . . . . . . . . . . . . . Net cash used for the purchase of businesses . . . . . . . . . . . . . . . . . . . . . . Net cash used in other investing activities . . . . . . . . . . . . . . . . . . . . . . . . . Net cash provided from financing activities . . . . . . . . . . . . . . . . . . . . . . . .

Per Share Data (Diluted)Earnings per share . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Shares outstanding (weighted-average, in thousands) . . . . . . . . . . . . . . . . Closing price of common shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Book value per share . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

RatiosReturn on sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Return on invested capital*. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Debt-to-debt-plus-equity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Non-GAAP Operating Run Rate Data**Run rate operating profit (loss) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Run rate earnings per share (diluted) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Run rate return on invested capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

OtherNumber of employees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Average sales per employee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

SHAREHOLDER RETURNS

UNITED STATES SECURITIES AND EXCHANGE COMMISSIONWashington, D.C. 20549

Form 10-K(Mark One)

¥ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)OF THE SECURITIES EXCHANGE ACT OF 1934For the Fiscal Year Ended December 31, 2010

OR

n TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)OF THE SECURITIES EXCHANGE ACT OF 1934For the Transition Period from to

Commission File Number 1-15885

MATERION CORPORATION(Exact name of Registrant as specified in its charter)

Ohio 34-1919973(State or other jurisdiction ofincorporation or organization)

(I.R.S. EmployerIdentification No.)

6070 Parkland Blvd., Mayfield Heights, Ohio 44124(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code216-486-4200

Securities registered pursuant to Section 12(b) of the Act:Title of Each Class Name of Each Exchange on Which Registered

Common Stock, no par value New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the SecuritiesAct. Yes ¥ No n

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes n No ¥

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the SecuritiesExchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and(2) has been subject to such filing requirements for the past 90 days. Yes ¥ No n

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, everyInteractive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during thepreceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes n No n

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is notcontained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statementsincorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. n

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smallerreporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 ofthe Exchange Act. (Check one):Large accelerated filer n Accelerated filer ¥ Non-accelerated filer n

(Do not check if a smaller reporting company)Smaller reporting company n

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes n No ¥

The aggregate market value of Common Stock, no par value, held by non-affiliates of the registrant (based upon the closing saleprice on the New York Stock Exchange) on July 2, 2010 was $387,244,077.

As of February 21, 2011, there were 20,357,787 common shares, no par value, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement for the annual meeting of shareholders to be held on or about May 4, 2011 are incorporated byreference into Part III.

MATERION CORPORATION

Index to Annual ReportOn Form 10-K for

Year Ended December 31, 2010

PART IItem 1. Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Item 1A. Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Item 1B. Unresolved Staff Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Item 2. Properties. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Item 3. Legal Proceedings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Item 4. (Removed and Reserved) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

PART IIItem 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases

of Equity Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Item 6. Selected Financial Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations . . . 22

Item 7A. Quantitative and Qualitative Disclosures About Market Risk . . . . . . . . . . . . . . . . . . . . . . . . . 47

Item 8. Financial Statements and Supplementary Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure . . 90

Item 9A. Controls and Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

Item 9B. Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

PART IIIItem 10. Directors, Executive Officers and Corporate Governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

Item 11. Executive Compensation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related StockholderMatters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

Item 13. Certain Relationships and Related Transactions, and Director Independence . . . . . . . . . . . . . . 93

Item 14. Principal Accountant Fees and Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

PART IVItem 15. Exhibits and Financial Statement Schedules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

Signatures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

Forward-looking Statements

Portions of the narrative set forth in this document that are not statements of historical or current facts areforward-looking statements. Our actual future performance may materially differ from that contemplated by theforward-looking statements as a result of a variety of factors. These factors include, in addition to those mentionedelsewhere herein:

• The global economy;

• The condition of the markets which we serve, whether defined geographically or by segment, with the majormarket segments being: consumer electronics, defense and science, industrial components and commercialaerospace, energy, automotive electronics, telecommunications infrastructure, medical and appliance;

• Changes in product mix and the financial condition of customers;

• Actual sales, operating rates and margins for 2011;

• Our success in developing and introducing new products and new product ramp-up rates;

• Our success in passing through the costs of raw materials to customers or otherwise mitigating fluctuatingprices for those materials, including the impact of fluctuating prices on inventory values;

• Our success in integrating newly acquired businesses, including the acquisitions of Materion PrecisionOptics and Thin Film Coatings Inc. (formerly known as Barr Associates, Inc.) and Materion AdvancedMaterials Technologies and Services Corp. (formerly known as Academy Corporation);

• The impact of the results of Materion Precision Optics and Thin Film Coatings Inc. and Materion AdvancedMaterials Technologies and Services Corp. on our ability to achieve fully the strategic and financialobjectives related to these acquisitions;

• Our success in implementing our strategic plans and the timely and successful completion and start-up ofany capital projects, including the new primary beryllium facility in Elmore, Ohio;

• The availability of adequate lines of credit and the associated interest rates;

• Other financial factors, including the cost and availability of raw materials (both base and precious metals),metal financing fees, tax rates, exchange rates, pension costs and required cash contributions and otheremployee benefit costs, energy costs, regulatory compliance costs, the cost and availability of insurance, andthe impact of our stock price on the cost of incentive compensation plans;

• The uncertainties related to the impact of war and terrorist activities;

• Changes in government regulatory requirements and the enactment of new legislation that impacts ourobligations and operations;

• The conclusion of pending litigation matters in accordance with our expectation that there will be nomaterial adverse effects;

• The amount and timing of repurchases of our Common Stock, if any;

• The timing and ability to achieve further efficiencies and synergies resulting from our name change, fromBrush Engineered Materials Inc. to Materion Corporation, and product line alignment under the Materionname and Materion brand; and

• The risk factors set forth elsewhere in Part I, Item 1A of this Form 10-K.

1

Item 1. BUSINESS

Materion Corporation (formerly known as Brush Engineered Materials Inc.), through its wholly ownedsubsidiaries, is an integrated producer of high performance advanced engineered materials used in a variety ofelectrical, electronic, thermal and structural applications. Our products are sold into numerous markets, includingconsumer electronics, defense and science, industrial components and commercial aerospace, energy, automotiveelectronics, telecommunications infrastructure, medical and appliance. As of December 31, 2010, we had2,484 employees.

In the first quarter 2011, we announced the change of our name from Brush Engineered Materials Inc. toMaterion Corporation. The names of all of our active subsidiaries are changing as well and each subsidiary will haveMaterion as part of their name. The legal and ownership structure of our subsidiaries will remain unchanged.

This name change did not alter our senior management structure or how the chief decision maker evaluates theperformance of our businesses. We continue to have the same four reportable segments as we had previously with nochange in their make up, although the names of those segments have changed. Advanced Material Technologies andServices has been renamed as Advanced Material Technologies; Specialty Engineered Alloys is now known asPerformance Alloys; Beryllium and Beryllium Composites has been shortened to Beryllium and Composites; andEngineered Material Systems has been changed to Technical Materials.

All Other includes our parent company expenses, other corporate charges and the operating results of MaterionServices Inc., a wholly owned subsidiary that provides administrative and financial oversight services to our otherbusinesses on a cost-plus basis. Corporate employees not included in a reportable segment totaled 92 as ofDecember 31, 2010.

We use our web site, www.materion.com, as a channel for routine distribution of important information,including news releases, analyst presentations, and financial information. We post filings as soon as reasonablypracticable after they are electronically filed with, or furnished to, the SEC, including our annual, quarterly, andcurrent reports on Forms 10-K, 10-Q, and 8-K; our proxy statements; and any amendments to those reports orstatements. All such postings and filings are available on our web site free of charge. In addition, this web site allowsinvestors and other interested persons to sign up to automatically receive e-mail alerts when we post news releasesand financial information on our web site. The SEC also maintains a web site, www.sec.gov, that contains reports,proxy and information statements, and other information regarding issuers who file electronically with the SEC.The content on any web site referred to in this Annual Report on Form 10-K is not incorporated by reference intothis annual report unless expressly noted.

ADVANCED MATERIAL TECHNOLOGIES

Sales for this segment were $879.0 million, or 67% of total sales, in 2010; $460.8 million, or 64% of total sales,in 2009; and $480.3 million, or 53% of total sales, in 2008. As of December 31, 2010, Advanced MaterialTechnologies had 1,089 employees.

Advanced Material Technologies manufactures precious, non-precious and specialty metal products,including vapor deposition targets, frame lid assemblies, clad and precious metal preforms, high temperaturebraze materials, ultra-fine wire, advanced chemicals, optics, performance coatings and microelectronic packages.These products are used in wireless, semiconductor, photonic, hybrid and other microelectronic applications withinthe consumer electronics and telecommunications infrastructure markets. Other key markets for these productsinclude medical, defense and science, energy and industrial components. Advanced Material Technologies also hasmetal cleaning operations and in-house refineries that allow for the reclaim of precious metals from internallygenerated or customers’ scrap.

Advanced Material Technologies’ products are sold directly from its facilities throughout the U.S., Asia andEurope, as well as through direct sales offices and independent sales representatives throughout the world. Principalcompetition includes companies such as Sumitomo Metals, Heraeus Inc., Praxair, Inc., Honeywell InternationalInc., Solar Applied Materials Technology Corp. and a number of smaller regional and national suppliers.

2

Advanced Material Technologies — Sales and Backlog

The backlog of unshipped orders for Advanced Material Technologies as of December 31, 2010, 2009 and2008 was $55.4 million, $51.3 million and $34.6 million, respectively. Backlog is generally represented bypurchase orders that may be terminated under certain conditions. We expect that substantially all of our backlog oforders for this segment at December 31, 2010 will be filled during 2011.

Sales are made to over 7,100 customers. Government sales accounted for less than 1% of the sales volume in2010, 2009 and 2008. Sales outside the United States, principally to Europe and Asia, accounted for approximately19% of sales in 2010, 29% of sales in 2009 and 28% of sales in 2008. Other segment reporting and geographicinformation is contained in Note M of Notes to Consolidated Financial Statements, which can be found in Part II,Item 8 of this Form 10-K and which is incorporated herein by reference.

Advanced Material Technologies — Research and Development

Active research and development programs seek new product compositions and designs as well as processinnovations. Expenditures for research and development for Advanced Material Technologies amounted to$4.0 million in 2010, $3.2 million in 2009 and $2.9 million in 2008. A staff of 22 scientists, engineers andtechnicians was employed in this effort as of year-end 2010.

PERFORMANCE ALLOYS

Sales for this segment were $293.8 million, or 23% of total sales, in 2010; $172.5 million, or 24% of total sales,in 2009; and $299.9 million, or 33% of total sales, in 2008. As of December 31, 2010, Performance Alloys had893 employees.

Performance Alloys manufactures and sells three main product families: strip products, bulk products andberyllium hydroxide. Strip products, the larger of the product families, include thin gauge precision strip and thindiameter rod and wire. These copper and nickel alloys provide a combination of high conductivity, high reliabilityand formability for use as connectors, contacts, switches, relays and shielding. Major markets for strip productsinclude consumer electronics, telecommunications infrastructure, automotive electronics, appliance and medical.Performance Alloys’ primary direct competitor in strip form beryllium alloys is NGK Insulators, Ltd. of Nagoya,Japan, with subsidiaries in the United States and Europe. Performance Alloys also competes with alloy systemsmanufactured by Global Brass and Copper, Inc., Wieland Electric, Inc., Stolberger Metallwerke GmbH, NipponMining, PMX Industries, Inc. and also with other generally less expensive materials, including phosphor bronze,stainless steel and other specialty copper and nickel alloys which are produced by a variety of companies around theworld.

Bulk products are copper and nickel-based alloys manufactured in plate, rod, bar, tube and other customizedforms that, depending upon the application, may provide superior strength, corrosion or wear resistance, thermalconductivity or lubricity. While the majority of bulk products contain beryllium, a growing portion of bulkproducts’ sales is from non-beryllium-containing alloys as a result of product diversification efforts. Applicationsfor bulk products include oil and gas drilling components, bearings, bushings, welding rods, plastic mold tooling,and undersea telecommunications housing equipment. In the area of bulk products, in addition to NGK Insulators,Ltd., Performance Alloys competes with several smaller regional producers such as International Beryllium Corp.,Ningxia Orient Tantalum in China and LeBronze Industriel in Europe.

Beryllium hydroxide is produced at our milling operations in Utah from our bertrandite mine and purchasedberyl ore. The hydroxide is used primarily as a raw material input for strip and bulk products and, to a lesser extent,by the Beryllium and Composites segment. External sales of hydroxide from the Utah operations were less than 4%of Performance Alloys’ total sales in each of the three most recent years. We also sell beryllium hydroxideexternally to NGK Insulators, Ltd.

Strip and bulk products are manufactured at facilities in Ohio and Pennsylvania and are distributedinternationally through a network of company-owned service centers and outside distributors and agents.

3

Performance Alloys — Sales and Backlog

The backlog of unshipped orders for Performance Alloys as of December 31, 2010, 2009 and 2008 was$98.9 million, $68.6 million and $55.5 million, respectively. Backlog is generally represented by purchase ordersthat may be terminated under certain conditions. We expect that substantially all the backlog of orders for thissegment as of December 31, 2010 will be filled during 2011.

Sales are made to over 1,700 customers. Performance Alloys had government sales accounting for less than1% of segment sales in 2010 and 2009 and none in 2008. Sales outside the United States, principally to Europe andAsia, accounted for approximately 58% of sales in 2010 and 57% of sales in 2009 and 2008. Other segmentreporting and geographic information is contained in Note M of Notes to Consolidated Financial Statements, whichcan be found in Part II, Item 8 of this Form 10-K and which is incorporated herein by reference.

Performance Alloys — Research and Development

Active research and development programs seek new product compositions and designs as well as processinnovations. Expenditures for research and development amounted to $1.8 million in 2010, $2.2 million in 2009 and$2.3 million in 2008. A staff of seven scientists, engineers and technicians was employed in this effort as of year-end2010.

BERYLLIUM AND COMPOSITES

Sales for this segment were $61.9 million, or 5% of total sales, in 2010; $47.0 million, or 7% of total sales, in2009; and $63.6 million, or 7% of total sales, in 2008. As of December 31, 2010, Beryllium and Composites had226 employees.

Beryllium and Composites manufactures beryllium-based metals and metal matrix composites in rod, sheet, foiland a variety of customized forms at our Elmore, Ohio and Fremont, California facilities. These materials are used inapplications that require high stiffness and/or low density and they tend to be premium-priced due to their uniquecombination of properties. This segment also manufactures beryllia ceramics produced at our Tucson, Arizonafacility. Defense and science is the largest market for Beryllium and Composites, while other markets served includeindustrial components and commercial aerospace, medical, energy and telecommunications infrastructure. Productsare also sold for acoustics and optical scanning applications. A majority of defense sales are made to contractors andsubcontractors instead of directly to government entities. In June 2008, we announced that Materion Brush Inc.(formerly known as Brush Wellman Inc.), a wholly owned subsidiary, had entered into an agreement with theDepartment of Defense to construct a $93.6 million primary beryllium facility. This facility will produce primaryberyllium, the feedstock material used to produce beryllium metal products. Construction of this facility wascompleted in 2011, and the start-up is underway. Beryllium-containing products are sold throughout the world througha direct sales organization and through company-owned and independent distribution centers. While Beryllium andComposites is the only domestic producer of metallic beryllium, it competes primarily with designs utilizing othermaterials including metals, metal matrix and organic composites. Electronic components utilizing beryllia are used inthe telecommunications infrastructure, medical, industrial components and commercial aerospace, and defense andscience markets. These products are distributed through direct sales and independent sales agents. Direct competitorsinclude American Beryllia Inc. and CBL Ceramics Limited.

Beryllium and Composites — Sales and Backlog

The backlog of unshipped orders for Beryllium and Composites as of December 31, 2010, 2009 and 2008 was$26.1 million, $38.1 million and $28.7 million, respectively. Backlog is generally represented by purchase ordersthat may be terminated under certain conditions. We expect that substantially all of our backlog of orders for thissegment at December 31, 2010 will be filled during 2011.

Sales are made to over 300 customers. Government sales accounted for less than 2% of Beryllium andComposites’ sales in 2010 and 2009, and less than 1% of segment sales in 2008. Sales outside the United States,principally to Europe and Asia, accounted for approximately 22% of sales in each of 2010 and 2009, and 23% of salesin 2008. Other segment reporting and geographic information is contained in Note M of Notes to ConsolidatedFinancial Statements, which can be found in Part II, Item 8 of this Form 10-K and which is incorporated herein byreference.

4

Beryllium and Composites — Research and Development

Active research and development programs seek new product compositions and designs as well as processinnovations. Expenditures for research and development amounted to $1.3 million in 2010, $1.4 million in 2009 and$1.3 million in 2008. A staff of seven scientists, engineers and technicians was employed in this effort as of year-end 2010.Some research and development projects, expenditures for which are not material, were externally sponsored and funded.

TECHNICAL MATERIALS

Sales for this segment were $67.5 million, or 5% of total sales, in 2010; $34.7 million, or 5% of total sales, in2009; and $65.9 million, or 7% of total sales, in 2008. As of December 31, 2010, Technical Materials had184 employees.

Technical Materials manufactures clad inlay and overlay metals, precious and base metal electroplatedsystems, electron beam welded systems, contour profiled systems and solder-coated metal systems. These specialtystrip metal products provide a variety of thermal, electrical or mechanical properties from a surface area orparticular section of the material. Our cladding and plating capabilities allow for a precious metal or brazing alloy tobe applied to a base metal only where it is needed, reducing the material cost to the customer as well as providingdesign flexibility. Major applications for these products include connectors, contacts and semiconductors while thelargest markets are automotive electronics and consumer electronics. The defense and science, energy and medicalmarkets are smaller, but offer further growth opportunities. Technical Materials’ products are manufactured at ourLincoln, Rhode Island facility and sold directly and through its sales representatives. Technical Materials’ majorcompetitors include Umicore S.A., Heraeus Inc. and Doduco, Inc.

Technical Materials — Sales and Backlog

The backlog of unshipped orders for Technical Materials as of December 31, 2010, 2009 and 2008 was$16.3 million, $7.6 million and $7.6 million, respectively. Backlog is generally represented by purchase orders thatmay be terminated under certain conditions. We expect that substantially all of our backlog of orders for thissegment at December 31, 2010 will be filled during 2011.

Sales are made to over 200 customers. Technical Materials did not have any sales to the government for 2010,2009 or 2008. Sales outside the United States, principally to Europe and Asia, accounted for approximately 26% ofTechnical Materials’ sales in 2010, 21% of sales in 2009 and 17% of sales in 2008. Other segment reporting andgeographic information is contained in Note M of Notes to Consolidated Financial Statements, which can be foundin Part II, Item 8 of this Form 10-K and which is incorporated herein by reference.

Technical Materials — Research and Development

Active research and development programs seek new product compositions and designs as well as processinnovations. Expenditures for research and development for Technical Materials were nominal in 2010, 2009 and 2008.

GENERAL

Availability of Raw Materials

The principal raw materials we use are aluminum, beryllium, cobalt, copper, gold, nickel, palladium, platinum,ruthenium, silver and tin. Ore reserve data can be found in Part II, Item 7 of this Form 10-K. The availability of theseraw materials, as well as other materials used by us, is adequate and generally not dependent on any one supplier.

Patents and Licenses

We own patents, patent applications and licenses relating to certain of our products and processes. While ourrights under the patents and licenses are of some importance to our operations, our business is not materiallydependent on any one patent or license or on all of our patents and licenses as a group.

Regulatory Matters

We are subject to a variety of laws which regulate the manufacture, processing, use, handling, storage,transport, treatment, emission, release and disposal of substances and wastes used or generated in manufacturing.For decades we have operated our facilities under applicable standards of inplant and outplant emissions andreleases. The inhalation of airborne beryllium particulate may present a health hazard to certain individuals.

5

Standards for exposure to beryllium are under review by the U.S. Occupational Safety and HealthAdministration (OSHA) and by other governmental and private standard-setting organizations. One result ofthese reviews will likely be more stringent worker safety standards. Some organizations, such as the CaliforniaOccupational Health and Safety Administration and the American Conference of Governmental IndustrialHygienists, have adopted standards that are more stringent than the current standards of OSHA. Thedevelopment, proposal or adoption of more stringent standards may affect buying decisions by the users ofberyllium-containing products. If the standards are made more stringent and/or our customers or other downstreamusers decide to reduce their use of beryllium-containing products, our results of operations, liquidity and financialcondition could be materially adversely affected. The impact of this potential adverse effect would depend on thenature and extent of the changes to the standards, the cost and ability to meet the new standards, the extent of anyreduction in customer use and other factors. The magnitude of this potential adverse effect cannot be estimated.

Executive Officers of the Registrant

Name Age Positions and Offices

Richard J. Hipple 58 Chairman of the Board, President and Chief Executive Officer. InMay 2006, Mr. Hipple was named Chairman of the Board and ChiefExecutive Officer of Materion Corporation. He had served asPresident since May 2005. He was Chief Operating Officer fromMay 2005 until May 2006. Mr. Hipple served as President ofPerformance Alloys from May 2002 until May 2005. He joinedthe Company in July 2001 as Vice President of Strip Products andserved in that position until May 2002. Prior to joining Materion,Mr. Hipple was President of LTV Steel Company, a business unit ofthe LTV Corporation (integrated steel producer and metal fabricator).Prior to running LTV’s steel business, Mr. Hipple held numerousleadership positions in engineering, operations, strategic planning,sales and marketing and procurement since 1975 at LTV. Mr. Hipplehas served on the Board of Directors of Ferro Corporation since 2007and as its Lead Director since April 2010.

John D. Grampa 63 Senior Vice President Finance and Chief Financial Officer.Mr. Grampa was named Senior Vice President Finance and ChiefFinancial Officer in December 2006. Prior to that, he had served asVice President Finance and Chief Financial Officer since November1999 and as Vice President Finance since October 1998. Prior tothat, he had served as Vice President, Finance for the WorldwideMaterials Business of Avery Dennison Corporation since March1994 and held other various positions at Avery DennisonCorporation (producer of pressure sensitive materials, officeproducts, labels and other converted products) from 1984.

Daniel A. Skoch 61 Senior Vice President Administration. Mr. Skoch was namedSenior Vice President Administration in July 2000. Prior to thattime, he had served as Vice President Administration and HumanResources since March 1996. He had served as Vice PresidentHuman Resources since July 1991 and prior to that time, he wasCorporate Director – Personnel.

Item 1A. RISK FACTORS

Our business, financial condition, results of operations and cash flows can be affected by a number of factors,including, but not limited to, those set forth below and elsewhere in this Annual Report on Form 10-K, any one ofwhich could cause our actual results to vary materially from recent results or from our anticipated future results.Therefore, an investment in us involves some risks, including the risks described below. The risks discussed beloware not the only risks that we may experience. If any of the following risks occur, our business, results of operationsor financial condition could be negatively impacted.

6

The businesses of many of our customers are subject to significant fluctuations as a result of the cyclical natureof their industries and their sensitivity to general economic conditions, which could adversely affect the demandfor our products and reduce our sales and profitability.

A substantial number of our customers are in the consumer electronics, telecommunications infrastructure,defense and science, industrial components and commercial aerospace, automotive electronics and applianceindustries. Each of these industries is cyclical in nature, influenced by a combination of factors that could have anegative impact on our business, including, among other things, periods of economic growth or recession, strengthor weakness of the U.S. dollar, the strength of the consumer electronics, automotive electronics and computerindustries and the rate of construction of telecommunications infrastructure equipment and government spendingon defense.

Also, in times when growth rates in our markets slow down, there may be temporary inventory adjustments byour customers that may negatively affect our business.

The recent global economic crisis had, and any additional negative or uncertain worldwide economic conditionsmay have, a negative impact on our financial performance.

The recent global economic crisis adversely affected the global economy. Some customers experienceddifficulty in obtaining adequate financing due to the disruption in the credit markets, which has impacted our sales.Our exposure to bad debt losses may also increase if customers are unable to pay for products previously ordered.The severe recession has also caused higher unemployment rates globally which could have an adverse effect ondemand for consumer electronics, which comprised 41% of our sales in 2010. Any additional negative or uncertainfinancial and macroeconomic conditions may have a significant adverse effect on our sales, profitability and resultsof operations.

We may not be able to execute our acquisition strategy or successfully integrate acquired businesses.

We have been active over the last several years in pursuing niche acquisitions. For example, during 2010 wecompleted the acquisition of Materion Advanced Materials Technologies and Services Corp. (formerly known asAcademy Corporation). We intend to continue to consider further growth opportunities through the acquisition ofassets or companies and routinely review acquisition opportunities. We cannot predict whether we will besuccessful in pursuing any acquisition opportunities or what the consequences of any acquisition would be.Future acquisitions may involve the expenditure of significant funds and management time. Depending upon thenature, size and timing of future acquisitions, we may be required to raise additional financing, which may not beavailable to us on acceptable terms. Further, we may not be able to successfully integrate any acquired business withour existing businesses or recognize any expected advantages from any completed acquisition.

In addition, there may be liabilities that we fail, or are unable, to discover in the course of performing duediligence investigations on the assets or companies we have already acquired or may acquire in the future. Wecannot assure that rights to indemnification by the sellers of these assets or companies to us, even if obtained, will beenforceable, collectible or sufficient in amount, scope or duration to fully offset the possible liabilities associatedwith the business or property acquired. Any such liabilities, individually or in the aggregate, could have a materiallyadverse effect on our business, financial condition and results of operations.

The markets for our products are experiencing rapid changes in technology.

We operate in markets characterized by rapidly changing technology and evolving customer specifications andindustry standards. New products may quickly render an existing product obsolete and unmarketable. For example,copper beryllium has long been used for high reliability contacts in mobile handheld devices. Mobile devicedesigners may justify using lower-performance materials in some of the less-critical components of mobile phones.Our growth and future results of operations depend in part upon our ability to enhance existing products andintroduce newly developed products on a timely basis that conform to prevailing and evolving industry standards,meet or exceed technological advances in the marketplace, meet changing customer specifications, achieve marketacceptance and respond to our competitors’ products.

7

The process of developing new products can be technologically challenging and requires the accurateanticipation of technological and market trends. We may not be able to introduce new products successfully ordo so on a timely basis. If we fail to develop new products that are appealing to our customers or fail to developproducts on time and within budgeted amounts, we may be unable to recover our research and development costs,which could adversely affect our margins and profitability.

A portion of our revenue is derived from the sale of defense-related products through various contracts andsubcontracts. These contracts may be suspended or canceled, which could have an adverse impact on ourrevenue.

In 2010, 12% of our revenue was derived from sales to customers in the defense and science market. A portionof these customers operate under contracts with the U.S. government, which are vulnerable to termination at anytime, for convenience or default. Some of the reasons for cancellation include, but are not limited to, budgetaryconstraints or re-appropriation of government funds, timing of contract awards, violations of legal or regulatoryrequirements, and changes in political agenda. If these cancellations were to occur, it would result in a reduction onour revenue. For example, various projects, including the F-22 fighter aircraft, have been canceled, which had, andwill have, a negative impact on our revenue.

Our products are deployed in complex applications and may have errors or defects that we find only afterdeployment.

Our products are highly complex, designed to be deployed in complicated applications and may containundetected defects, errors or failures. Although our products are generally tested during manufacturing, prior todeployment, they can only be fully tested when deployed in specific applications. For example, we sell beryllium-copper alloy strip products in a coil form to some customers, who then stamp the alloy for its specific purpose. Onoccasion, it is not until such customer stamps the alloy that a defect in the alloy is detected. Consequently, ourcustomers may discover errors after the products have been deployed. The occurrence of any defects, errors, orfailures could result in installation delays, product returns, termination of contracts with our customers, diversion ofour resources, increased service and warranty costs and other losses to our customers, end users or to us. Any ofthese occurrences could also result in the loss of or delay in market acceptance of our products and could damageour reputation, which could reduce our sales.

The terms of our indebtedness may restrict our operations, including our ability to pursue our growth andacquisition strategies.

The terms of our credit facilities contain a number of restrictive covenants, including restrictions in our abilityto, among other things, borrow and make investments, acquire other businesses and consign additional preciousmetals. These covenants could adversely affect us by limiting our ability to plan for or react to market conditions orto meet our capital needs, as well as adversely affect our ability to pursue our growth, acquisition strategies andother strategic initiatives.

Our failure to comply with the covenants contained in the terms of our indebtedness could result in an event ofdefault, which could materially and adversely affect our operating results and our financial condition.

The terms of our credit facilities require us to comply with various covenants, including financial covenants. Ifthe recent global economic downturn returns, it could have a material adverse impact on our earnings and cash flow,which could adversely affect our ability to comply with our financial covenants and could limit our borrowingcapacity. Our ability to comply with these covenants depends, in part, on factors over which we may have nocontrol. A breach of any of these covenants could result in an event of default under one or more of the agreementsgoverning our indebtedness that, if not cured or waived, could give the holders of the defaulted indebtedness theright to terminate commitments to lend and cause all amounts outstanding with respect to the indebtedness to be dueand payable immediately. Acceleration of any of our indebtedness could result in cross defaults under our other debtinstruments. Our assets and cash flow may be insufficient to fully repay borrowings under all of our outstandingdebt instruments if some or all of these instruments are accelerated upon an event of default, in which case we maybe required to seek legal protection from our creditors.

8

We conduct our sales and distribution operations on a worldwide basis and are subject to the risks associated withdoing business outside the United States.