Embed Size (px)

Citation preview

Maximize Financial Services KPIs with Connected Customer Data:The Road to Success in Advisory, Banking, Insurance, Mutual Funds & Wealth Management

Licensed for Distribution By

av

July 2020 Omer Minkara VP & Principal Analyst Contact Center & Customer Experience Management LinkedIn, Twitter

RR

MAXIMIZE FINANCIAL SERVICES KPIS WITH CONNECTED CUSTOMER DATA: THE ROAD TO SUCCESS IN ADVISORY, BANKING, INSURANCE, MUTUAL FUNDS & WEALTH MANAGEMENT

2

2

This report highlights how connecting customer data captured across all sources enables financial firms to hyper-personalize their CX activities while maximizing client satisfaction and spend.

Poor Data Management Impacts CX Results for Financial Services Firms

The financial services industry has a long and rich heritage. It’s also very diverse, comprised of firms ranging from private banks and commercial banks to firms providing wealth management, brokerage, mortgage origination, and insurance services. One of the elements that unites companies with such diverse activities is their struggle to use data to manage customer engagement.

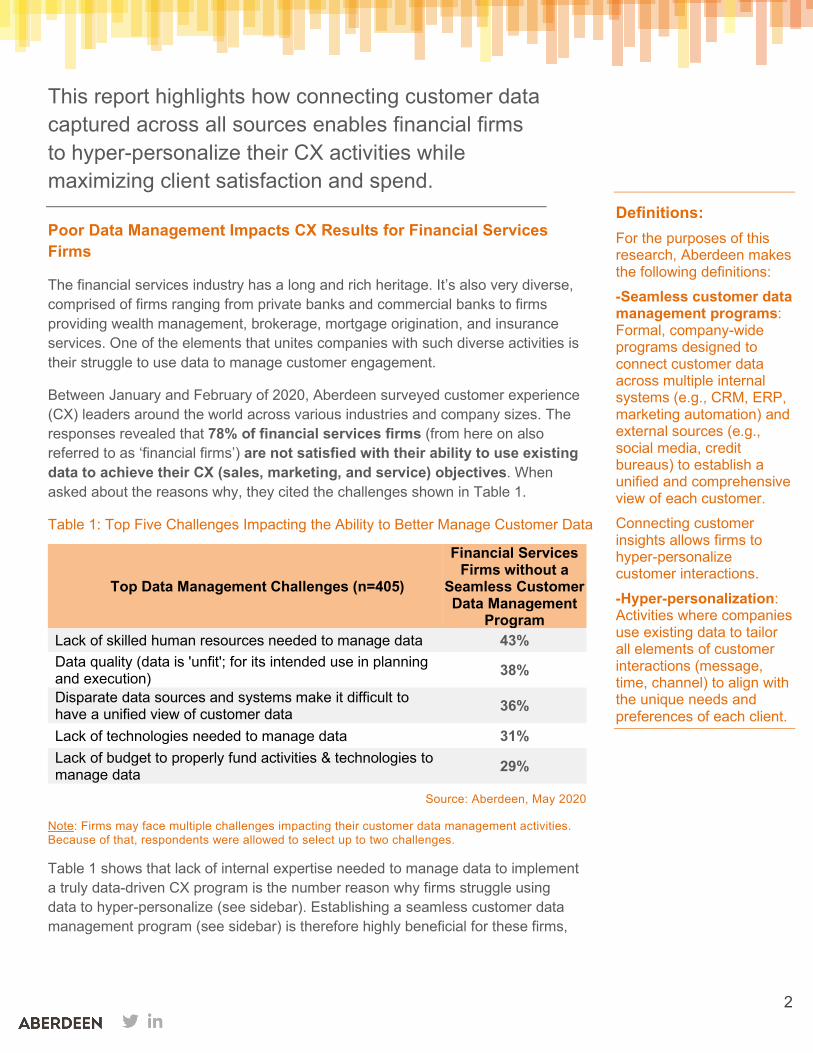

Between January and February of 2020, Aberdeen surveyed customer experience (CX) leaders around the world across various industries and company sizes. The responses revealed that 78% of financial services firms (from here on also referred to as ‘financial firms’) are not satisfied with their ability to use existing data to achieve their CX (sales, marketing, and service) objectives. When asked about the reasons why, they cited the challenges shown in Table 1.

Table 1: Top Five Challenges Impacting the Ability to Better Manage Customer Data

Source: Aberdeen, May 2020

Note: Firms may face multiple challenges impacting their customer data management activities. Because of that, respondents were allowed to select up to two challenges.

Table 1 shows that lack of internal expertise needed to manage data to implement a truly data-driven CX program is the number reason why firms struggle using data to hyper-personalize (see sidebar). Establishing a seamless customer data management program (see sidebar) is therefore highly beneficial for these firms,

Top Data Management Challenges (n=405)

Financial Services Firms without a

Seamless Customer Data Management

Program Lack of skilled human resources needed to manage data 43% Data quality (data is 'unfit'; for its intended use in planning and execution) 38%

Disparate data sources and systems make it difficult to have a unified view of customer data 36%

Lack of technologies needed to manage data 31% Lack of budget to properly fund activities & technologies to manage data 29%

Definitions: For the purposes of this research, Aberdeen makes the following definitions: -Seamless customer data management programs: Formal, company-wide programs designed to connect customer data across multiple internal systems (e.g., CRM, ERP, marketing automation) and external sources (e.g., social media, credit bureaus) to establish a unified and comprehensive view of each customer. Connecting customer insights allows firms to hyper-personalize customer interactions. -Hyper-personalization: Activities where companies use existing data to tailor all elements of customer interactions (message, time, channel) to align with the unique needs and preferences of each client.

3

3

as it helps simplify the use of data so employees can easily tailor customer conversations. A (modern) responsive data platform (see sidebar) that makes it easier to connect customer data across multiple systems — while ensuring compliance — therefore helps firms alleviate the challenge of lack of internal expertise while simultaneously helping firms improve the quality (accuracy and relevancy) of data used in CX activities.

Table 1 reveals that poor data quality and lack of a unified view of customer data across disparate sources are, in order, the second and third top CX data management challenges impacting financial firms. Therefore, using a platform that helps seamlessly connect customer data collected from all channels (and through multiple systems) helps financial firms alleviate those challenges getting in the way of hyper-personalization.

Other top challenges cited by financial firms as the reasons why they struggle using data to achieve their CX goals include lack of relevant technologies needed to manage customer data and lack of budget to invest in these technologies. The next section will shed light on how enriching the technology toolbox with a modern data platform helps service organizations reduce unnecessary costs and grow revenue, while also boosting CX results.

The ROI of Unifying Customer Data for Hyper-personalization

Successful CX programs don’t just help companies acquire and retain clients. They also help deliver shareholder value by enhancing the overall financial health of the business. Figure 1 provides a comparison of the year-over-year performance gains observed by financial firms using a modern data platform for seamless customer data management to those without it. Data shows that firms in the former category excel in year-over-year improvement of both CX and financial key performance indicators (KPIs).

Figure 1: Effective Data Management Maximizes CX Results Across Financial Firms

Customer retention is a strong indicator of organizations’ ability to meet and exceed client needs. Firms that struggle keeping up with the changing needs of their buyers are more likely to see their clients leave for competitors that understand and cater to those needs. Retaining an existing account and

23.4%

11.5% 11.3%8.7%8.9%

3.8% 4.6% 4.8%

0%

5%

10%

15%

20%

25%

Customer retention Customer lifetime value Improvement incustomer effort score

Average profit marginper customer

Financial Services Firms with a Seamless Customer Data Management Program

Financial Services Firms without a Seamless Customer Data Management Program

Source: Aberdeen, May 2020

Year

-ove

r-ye

ar p

erce

ntch

ange

, n=4

05

Definition: Responsive Data Management For the purposes of this research, Aberdeen defines responsive data management as a framework designed to enable companies to integrate relevant insights across a variety of internal and external sources to build a 360-degree view of each customer. Firms with this capability don’t just aim to have a holistic view of customer insights. They also use it to be more responsive to the continuously changing needs of their clients through hyper-personalizing their activities.

4

4

growing that account (especially high-value ones) is often far more cost-effective and efficient for financial firms than finding net-new clients. While the latter is still necessary and important, the long-term success of many financial firms is closely associated with retaining their clientele and growing their lifetime value over time. Customer lifetime value is an indicator of the total spend a client makes with the business through the duration of their relationship. As such, high-value clients for financial services firms are often those accounts who not only have a long-standing relationship with the company, but also those that continue to increase their spend / investment with the business.

Figure 1 shows that financial firms with a seamless customer data management program achieve 2.6x greater annual increase in retention rates (23.4% vs. 8.9%) and 3.0x greater annual growth in average customer lifetime value (11.5% vs. 3.8%). Those findings validate that effective use of data is crucial for financial firms to earn customer loyalty.

Analyzing other performance results depicted in Figure 1 tells us how data-savvy firms boost customer satisfaction. Data shows that they improve customer effort scores (see sidebar) by 2.5x more year-over-year, compared to competitors that struggle using data in their CX programs (11.3% vs. 4.6%). Customer effort score is an emerging measure that’s becoming increasingly popular across CX leaders within all industries. Measuring this metric is important, as customers today expect their interactions with all companies to be convenient. This means hyper-personalizing interactions across all channels so each interaction is truly contextual at every moment of engagement and across every channel. Effort scores are a direct indicator of customer convenience — the effort customers perceive to put into their interactions with financial firms is their perception of how easy these firms are to do business with.

Figure 1 also reveals that when financial firms connect customer data, they gain 81% greater annual growth in average profit margin per client. While growth in customer spend / investment is one reason driving this growth, reduction in cost is another. To this point, Figure 2 shows that financial firms with savvy data management activities enjoy 2.5x greater annual improvement (decrease) in service costs (38.3% vs. 15.2%).

Figure 2: Financial Firms Minimize Cost by Making Better Use of Customer Data

Definition: Customer Effort For the purposes of this research, Aberdeen defines customer effort score as a performance measure reflecting the perceived effort clients put into certain activities (e.g., email, phone conversation, website visit, branch visit) when interacting with a firm. It’s a subjective measure based on the unique expectations of each client. Improving it means that the company has made it easier for its customers to do business. Companies measure effort in various ways. The most widely used method is a numeric scale (1: minimal effort, 5: significant effort). These scales can be in different ranges, including 1-5, 1-10, 1-100. The second most popular way firms use to measure client effort is observing customer behavioral data such as number of repeat contacts, account termination, or steady decline in investment balance. Firms also use mixed metrics blending various data points such as responses to numeric scale questions and behavioral data analysis

38.3%

28.0%

18.4%15.2%

20.5%

11.1%

0%

10%

20%

30%

40%

Improvement in annual customerservice cost

Improvement in average responsetime to customer requests

Improvement in average handletime in the contact center

Financial Services Firms with a Seamless Customer Data Management Program

Financial Services Firms without a Seamless Customer Data Management Program

Source: Aberdeen, May 2020

Year

-ove

r-ye

ar p

erce

nt c

hang

e, n

=405

5

5

Data-savvy financial firms enjoy superior cost decrease because a modern and responsive platform used to manage data helps them ensure data quality. Using analytics to analyze customer data ultimately allows firms to reveal the precise impact of their marketing, sales, and service activities on KPIs such as customer satisfaction and average client value. This, in turn, makes it easier to avoid and address inefficiencies which are among the main the culprits of unnecessary costs.

Figure 2 validates the above assertion on efficiency gains. It shows that firms with a seamless customer data management program improve (decrease) the average response time to customer requests across the whole organization by 37% more year-over-year (28.0% vs. 20.5%). That’s because they reduce inefficiencies leading to delays to requests such as commercial loan applications, insurance claims, or transfers between accounts.

When customers have issues and seek support through the contact center, research also shows that financial firms with prowess in managing CX data once again outperform their competitors. They enjoy 66% greater annual improvement (decrease) in average handle times addressing support requests in the contact center (18.4% vs. 11.1%). Such reduction in handle times is achieved because using truly holistic and accurate data — in combination with analytics — allows service leaders to reveal and address the reasons why it takes longer than necessary for the firm to address client needs.

Key Activities to Hyper-personalize Customer Interactions through Better, More Complete Data

To reveal the core competencies companies need to ensure success through effective use of customer data, Aberdeen compared the capabilities adopted by financial firms that mastered managing CX insights to those adopted by others. The findings revealed that firms with seamless customer data management programs have two core competencies which they support through the adoption of several key capabilities.

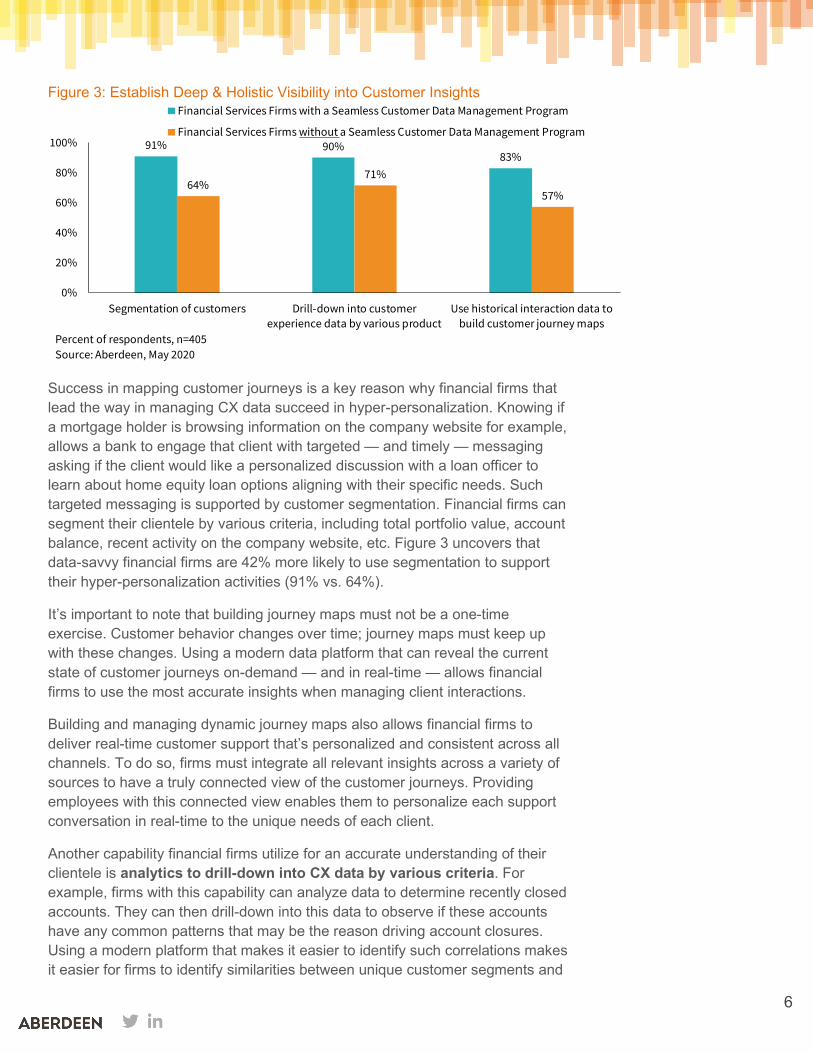

The first of those two core competencies is establishing deep and holistic visibility into customer insights. Data shows that once financial firms use a modern data platform to connect the internal and external data stored across multiple sources, they then leverage these connected insights to build detailed journey maps for each account. This refers to mapping the interactions of each client by context (e.g., opening a new checking account for a net-new account, loan request by an existing account with an active mortgage balance). It also includes mapping interactions by channel, business department, etc. Journey maps serve as an illustration of the overall relationship a client has with the company from the very beginning to retention, loyalty, and where applicable, churn. Figure 3 reveals that data-savvy financial firms are 46% more likely to have such detailed journey maps that provide them with contextual visibility into the relationship with each client (83% vs. 57%).

Incumbents vs. Challengers The financial services sector is transforming rapidly through innovation. Greater adoption of digital channels, changes in tecnology adoption, and market trends are bringing challengers into the sector. These challengers try to position themselves by focusing on the innovation they bring to the market. The change in market dynamics create different priorities for incumbents and challengers. For incumbents, they must focus on ways to catch-up with the innovation driven by challengers while finding ways to effectively meet the needs of their clientele with their current capabilities. For challengers, they must scale their activities effectively and ensure that the innovation they bring to the market is valued by customers to expand their market share. Despite their competing priorities, firms in both category share a common objective. They must ensure that their activities align with the needs of their current and potential customers — that’s where hyper-personalization comes in. Establishing a seamless customer data management program is crucial for incumbents and challengers to achieve their short-term and long-term objectives.

6

6

Figure 3: Establish Deep & Holistic Visibility into Customer Insights

Success in mapping customer journeys is a key reason why financial firms that lead the way in managing CX data succeed in hyper-personalization. Knowing if a mortgage holder is browsing information on the company website for example, allows a bank to engage that client with targeted — and timely — messaging asking if the client would like a personalized discussion with a loan officer to learn about home equity loan options aligning with their specific needs. Such targeted messaging is supported by customer segmentation. Financial firms can segment their clientele by various criteria, including total portfolio value, account balance, recent activity on the company website, etc. Figure 3 uncovers that data-savvy financial firms are 42% more likely to use segmentation to support their hyper-personalization activities (91% vs. 64%).

It’s important to note that building journey maps must not be a one-time exercise. Customer behavior changes over time; journey maps must keep up with these changes. Using a modern data platform that can reveal the current state of customer journeys on-demand — and in real-time — allows financial firms to use the most accurate insights when managing client interactions.

Building and managing dynamic journey maps also allows financial firms to deliver real-time customer support that’s personalized and consistent across all channels. To do so, firms must integrate all relevant insights across a variety of sources to have a truly connected view of the customer journeys. Providing employees with this connected view enables them to personalize each support conversation in real-time to the unique needs of each client.

Another capability financial firms utilize for an accurate understanding of their clientele is analytics to drill-down into CX data by various criteria. For example, firms with this capability can analyze data to determine recently closed accounts. They can then drill-down into this data to observe if these accounts have any common patterns that may be the reason driving account closures. Using a modern platform that makes it easier to identify such correlations makes it easier for firms to identify similarities between unique customer segments and

91% 90%83%

64%71%

57%

0%

20%

40%

60%

80%

100%

Segmentation of customers Drill-down into customerexperience data by various product

Use historical interaction data tobuild customer journey maps

Financial Services Firms with a Seamless Customer Data Management Program

Financial Services Firms without a Seamless Customer Data Management Program

Source: Aberdeen, May 2020Percent of respondents, n=405

7

7

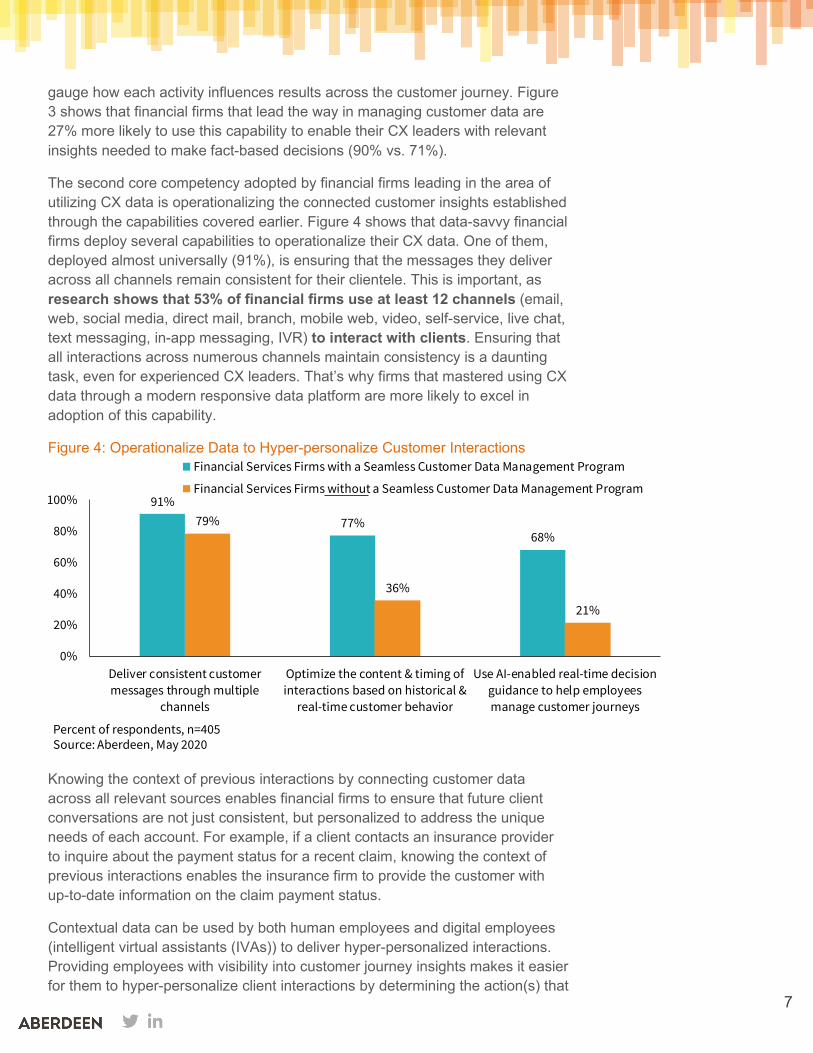

gauge how each activity influences results across the customer journey. Figure 3 shows that financial firms that lead the way in managing customer data are 27% more likely to use this capability to enable their CX leaders with relevant insights needed to make fact-based decisions (90% vs. 71%).

The second core competency adopted by financial firms leading in the area of utilizing CX data is operationalizing the connected customer insights established through the capabilities covered earlier. Figure 4 shows that data-savvy financial firms deploy several capabilities to operationalize their CX data. One of them, deployed almost universally (91%), is ensuring that the messages they deliver across all channels remain consistent for their clientele. This is important, as research shows that 53% of financial firms use at least 12 channels (email, web, social media, direct mail, branch, mobile web, video, self-service, live chat, text messaging, in-app messaging, IVR) to interact with clients. Ensuring that all interactions across numerous channels maintain consistency is a daunting task, even for experienced CX leaders. That’s why firms that mastered using CX data through a modern responsive data platform are more likely to excel in adoption of this capability.

Figure 4: Operationalize Data to Hyper-personalize Customer Interactions

Knowing the context of previous interactions by connecting customer data across all relevant sources enables financial firms to ensure that future client conversations are not just consistent, but personalized to address the unique needs of each account. For example, if a client contacts an insurance provider to inquire about the payment status for a recent claim, knowing the context of previous interactions enables the insurance firm to provide the customer with up-to-date information on the claim payment status.

Contextual data can be used by both human employees and digital employees (intelligent virtual assistants (IVAs)) to deliver hyper-personalized interactions. Providing employees with visibility into customer journey insights makes it easier for them to hyper-personalize client interactions by determining the action(s) that

91%

77%68%

79%

36%

21%

0%

20%

40%

60%

80%

100%

Deliver consistent customermessages through multiple

channels

Optimize the content & timing ofinteractions based on historical &

real-time customer behavior

Use AI-enabled real-time decisionguidance to help employeesmanage customer journeys

Financial Services Firms with a Seamless Customer Data Management Program

Financial Services Firms without a Seamless Customer Data Management Program

Source: Aberdeen, May 2020Percent of respondents, n=405

8

8

will address the unique needs of each account. Indeed, Figure 4 shows that data-savvy financial firms are 2.1x more likely to have this capability (77% vs. 36%).

Having established accurate and comprehensive insights into the customer journey, savvy financial firms also use machine learning algorithms to analyze which customer interactions are more likely to yield desired outcomes, such as opening a new credit line, for an existing account so they can implement those activities to achieve desired results. Data shows that financial firms with a seamless customer data management program are 3.2x more likely to build automated processes through which they provide employees next-best-action-guidance to hyper-personalize by using insights gleaned through machine learning (68% vs. 21%).

Firms using self-service tools such as IVAs can also improve the effectiveness of these tools by incorporating the aforementioned AI capability, where the insights gleaned through machine learning are used to adjust how the IVA responds to client needs. For example, customers seeking to use self-service to request an auto loan can interact with an IVA to make a request. However, the company may observe an uptick in in-person conversations for auto loans, and use of analytics may reveal that most of these added requests are associated with clients who also previously interacted with an IVA. Use of machine learning to analyze relevant insights will make it easier for the firm to determine the cause(s) of why clients struggle using the IVA for auto loan requests. This, in turn, offers visibility into necessary adjustments that need to be made so customers can use the IVA to get their auto loan requests addressed without repeated contact with the business.

Key Takeaways

Customers are the lifeline of financial services firms. Those that earn customer trust and loyalty succeed, and those that don’t struggle and fall behind. Effective use of data is in the heart of successful CX programs deployed by financial firms — yet, 78% of financial firms struggle using data to achieve their sales, marketing, and service goals.

When we examine the reasons why financial firms struggle using CX data, we uncovered several challenges. Among the most common were lack of internal resources needed to manage existing data, poor data quality, disparate data sources, and technologies that aren’t sufficient in helping financial firms address their CX data management needs. When we compare the performance of financial firms using a (modern) responsive data management platform to those that don’t, the findings revealed that firms that mastered using CX data have found ways to mitigate the challenges impacting their activities.

By connecting customer data across all sources to build a truly unified and accurate view of customers, financial firms distinguish themselves in improving customer satisfaction rates, growing net client value, and reducing cost of

Knowing the context of previous interactions by connecting customer data across all relevant sources enables financial firms to ensure that future conversations with clients are not just consistent, but personalized to address the unique needs of each account.

9

9

servicing clients. Aberdeen’s research showed that these firms have two core competencies that allow them to maximize their results and achieve long-term success.

First, they establish deep and holistic visibility into customer journeys by building journey maps, segmenting clients, and analyzing root-causes of what drives customer behavior across all stages of the customer journey. Second, they operationalize those insights to hyper-personalize client interactions. This means ensuring that all conversations taking place across all channels are consistent and personalized for each account. It also means using capabilities such as analytics and AI to support hyper-personalization efforts, so regardless of the changes in customer behavior, the company can find continue to use data to meet and exceed client needs.

If you don’t yet have a truly connected view of customer insights and currently struggle using data to achieve your CX goals, we recommend considering how a responsive data platform can help you transform your CX program to align with that of industry-leading financial firms. If you’re satisfied with your ability to use data, we still highly recommend you to observe which of the key capabilities outlined across Figures 3 and 4 you currently have, and if you’re missing any, to prioritize incorporating them within your activities to ensure you can continue using data to achieve desired results.

10

10

Related Research

Customer Experience Executive’s Agenda 2020; February 2020

Customer Engagement Analytics: Demystify the Customer Journey to Maximize Results; December 2019

The Role of Hyper-personalization in Today’s Customer Service, June 2019

CRM in Credit Unions: Better Member Insights Lead to Better Business Results; May 2019

About Aberdeen

Since 1988, Aberdeen has published research that helps businesses worldwide to improve their performance. Our analysts derive fact-based, vendor-neutral insights from a proprietary analytical framework, which identifies Best-in-Class organizations from primary research conducted with industry practitioners. The resulting research content is used by hundreds of thousands of business professionals to drive smarter decision-making and improve business strategies. Aberdeen is headquartered in Waltham, Massachusetts, USA.

This document is the result of primary research performed by Aberdeen and represents the best analysis available at the time of publication. Unless otherwise noted, the entire contents of this publication are copyrighted by Aberdeen and may not be reproduced, distributed, archived, or transmitted in any form or by any means without prior written consent by Aberdeen.

18149