Embed Size (px)

Citation preview

© The Chartered Institute of Management Accountants 2001

POST EXAM GUIDE

May 2001 Exam

Management Accounting Fundamentals(FMAF)

CIMA publishes a Question and Answer booklet for each paperof the May 2001 exam which is essential reading for studentsand tutors. The published answers are written by the Examinerand should be read together with the post exam guide.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 2

Objective test questions are awarded 2 marks each. Explanations are provided foranswers to objective test questions involving calculations.

Question 1.1

XYZ Ltd operates an integrated accounting system. The material control account at 31 March2001 shows the following information:

Material control account£ £

Balance b/d 50,000 Production overhead controlaccount 10,000

Creditors 100,000 ? 125,000Bank 25,000 Balance c/d 40,000

175,000 175,000

The £125,000 credit entry represents the value of the transfer to the

A cost of sales account.B finished goods account.C profit and loss account.D work-in-progress account.

The answer is D.

Question 1.2

P Ltd is preparing the production budget for the next period. Based on previous experience, ithas found that there is a linear relationship between production volume and production costs.The following cost information has been collected in connection with production:

Volume Cost(units) £1,600 23,2002,500 25,000

What would be the production cost for a production volume of 2,700 units?

A £5,400 B £25,400 C £27,000 D £39,150

The answer is B.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 3

Workings for Question 1.2

Units £2,500 25,0001,600 23,200 900 1,800

Variable cost per unit = 900

800,1£ = £2

Substitute in high activity: £Total cost 25,000Variable cost = 2,500 units x £2 5,000Therefore fixed cost 20,000

Forecast for 2,700 units: £Fixed cost 20,000Variable cost 2,700 x £2 5,400Total cost 25,400

Question 1.3

ABC Ltd absorbs fixed production overheads in one of its departments on the basis ofmachine hours. There were 100,000 budgeted machine hours for the forthcoming period. Thefixed production overhead absorption rate was £2∙50 per machine hour.

During the period, the following actual results were recorded:

Standard machine hours 110,000Fixed production overheads £300,000

Which ONE of the following statements is correct?

A Overhead was £25,000 over-absorbed.B Overhead was £25,000 under-absorbed.C Overhead was £50,000 over-absorbed.D No under- or over-absorption occurred.

The answer is B.

Workings

£110,000 machine hours x £2∙50 275,000 absorbed

Actual incurred 300,000

Under absorbed 25,000

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 4

The following graph relates to questions 1.4 and 1.5

£ Profit

0 Level of activity

K

Question 1.4

Point K on the graph indicates the value of

A semi-variable cost.B total cost.C variable cost.D fixed cost.

The answer is D.

Question 1.5

This graph is known as a

A conventional breakeven chart.B contribution breakeven chart.C semi-variable cost chart.D profit volume chart.

The answer is D.

Paper 2 - Management Accounting Fundamentals

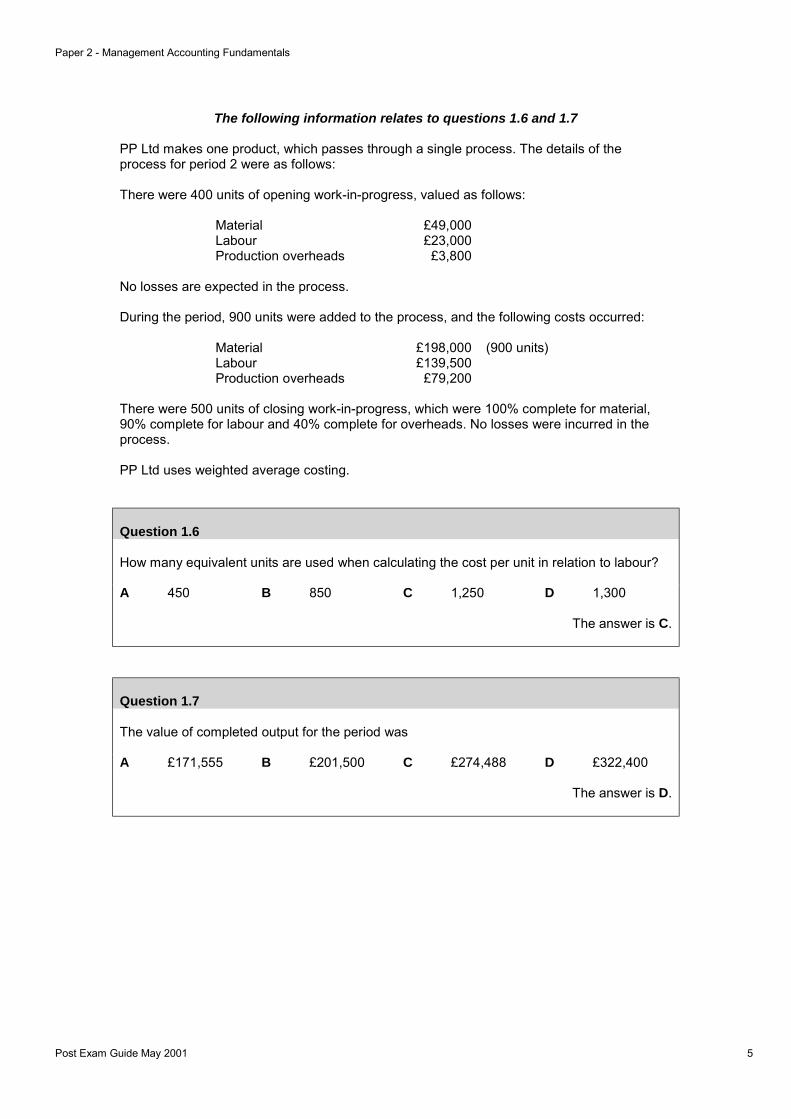

Post Exam Guide May 2001 5

The following information relates to questions 1.6 and 1.7

PP Ltd makes one product, which passes through a single process. The details of theprocess for period 2 were as follows:

There were 400 units of opening work-in-progress, valued as follows:

Material £49,000Labour £23,000Production overheads £3,800

No losses are expected in the process.

During the period, 900 units were added to the process, and the following costs occurred:

Material £198,000 (900 units)Labour £139,500Production overheads £79,200

There were 500 units of closing work-in-progress, which were 100% complete for material,90% complete for labour and 40% complete for overheads. No losses were incurred in theprocess.

PP Ltd uses weighted average costing.

Question 1.6

How many equivalent units are used when calculating the cost per unit in relation to labour?

A 450 B 850 C 1,250 D 1,300

The answer is C.

Question 1.7

The value of completed output for the period was

A £171,555 B £201,500 C £274,488 D £322,400

The answer is D.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 6

Workings for 1.6 and 1.7

Equivalent Unit Table

Description Units Materials Labour Productionoverheads

% eu % eu % euOutput 800 100 800 100 800 100 800CWIP 500 100 500 90 450 40 200EU’s 1,300 1,250 1,000

£ £ £Costs – Period 198,000 139,500 79,200

OWIP 49,000 23,000 3,800Total cost 247,000 162,500 83,000

Cost per equivalent unit £190 £130 £83

Value of completed output = 800 x (£190 + £130 + £83) = £322,400

Question 1.8

An engineering company has been offered the opportunity to bid for a contract which requiresa special component. Currently, the company has a component in stock, which has a netbook value of £250. This component could be used in the contract, but would requiremodification at a cost of £50. There is no other foreseeable use for the component held instock. Alternatively, the company could purchase a new specialist component for £280.What is the relevant cost of using the component currently held in stock for this contract?

A £50 B £250 C £280 D £300

The answer is A.

Workings

The £250 net book value is a sunk cost and therefore not relevant. Therefore the relevantcost is £50.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 7

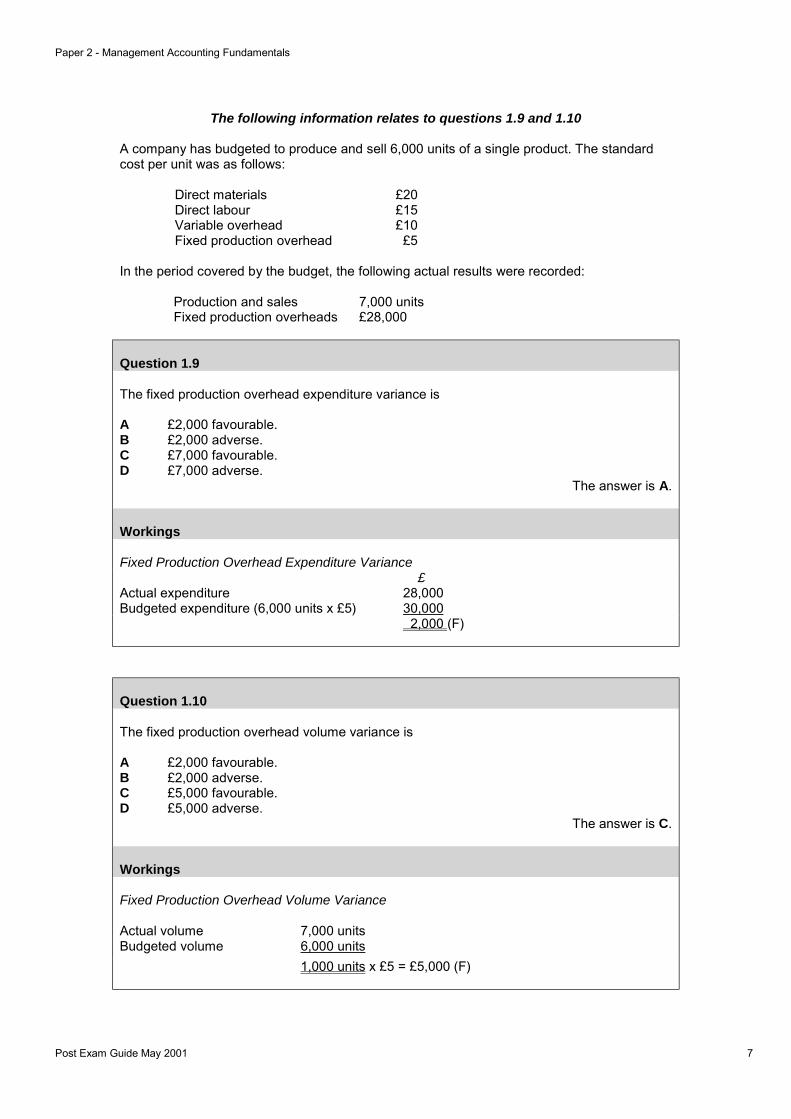

The following information relates to questions 1.9 and 1.10

A company has budgeted to produce and sell 6,000 units of a single product. The standardcost per unit was as follows:

Direct materials £20Direct labour £15Variable overhead £10Fixed production overhead £5

In the period covered by the budget, the following actual results were recorded:

Production and sales 7,000 unitsFixed production overheads £28,000

Question 1.9

The fixed production overhead expenditure variance is

A £2,000 favourable.B £2,000 adverse.C £7,000 favourable.D £7,000 adverse.

The answer is A.

Workings

Fixed Production Overhead Expenditure Variance £

Actual expenditure 28,000Budgeted expenditure (6,000 units x £5) 30,000

2,000 (F)

Question 1.10

The fixed production overhead volume variance is

A £2,000 favourable.B £2,000 adverse.C £5,000 favourable.D £5,000 adverse.

The answer is C.

Workings

Fixed Production Overhead Volume Variance

Actual volume 7,000 unitsBudgeted volume 6,000 units

1,000 units x £5 = £5,000 (F)

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 8

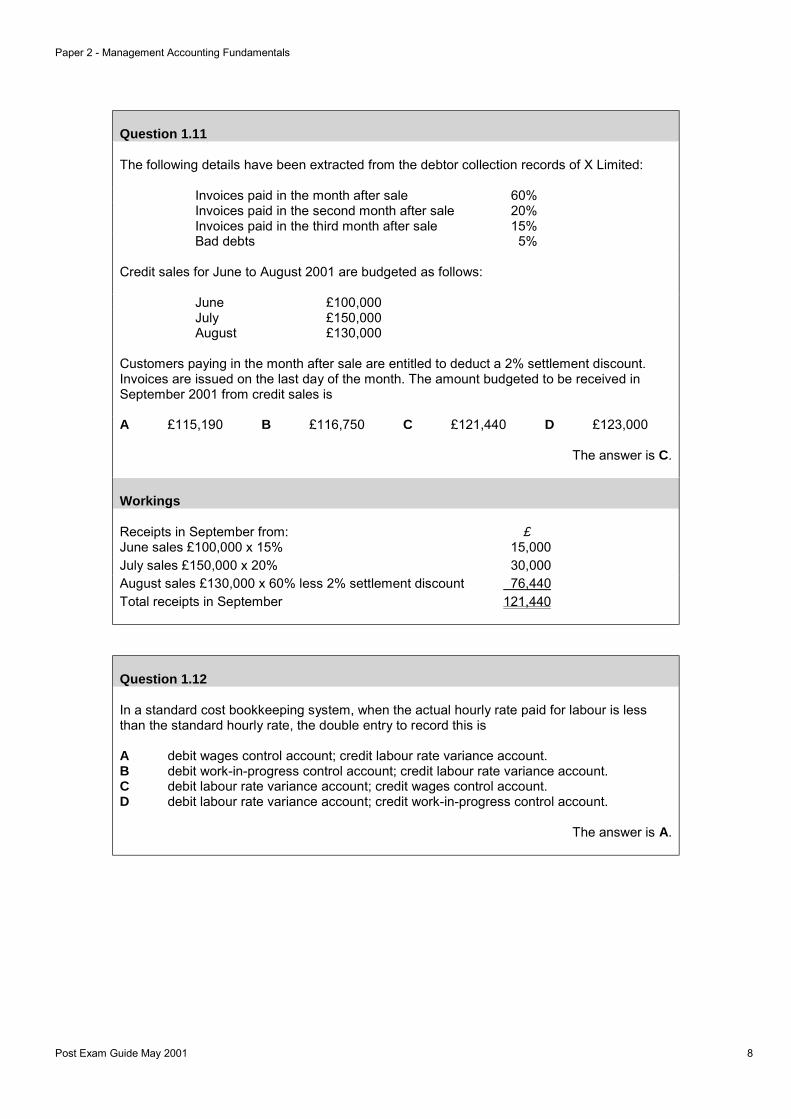

Question 1.11

The following details have been extracted from the debtor collection records of X Limited:

Invoices paid in the month after sale 60%Invoices paid in the second month after sale 20%Invoices paid in the third month after sale 15%Bad debts 5%

Credit sales for June to August 2001 are budgeted as follows:

June £100,000July £150,000August £130,000

Customers paying in the month after sale are entitled to deduct a 2% settlement discount.Invoices are issued on the last day of the month. The amount budgeted to be received inSeptember 2001 from credit sales is

A £115,190 B £116,750 C £121,440 D £123,000

The answer is C.

Workings

Receipts in September from: £June sales £100,000 x 15% 15,000July sales £150,000 x 20% 30,000August sales £130,000 x 60% less 2% settlement discount 76,440Total receipts in September 121,440

Question 1.12

In a standard cost bookkeeping system, when the actual hourly rate paid for labour is lessthan the standard hourly rate, the double entry to record this is

A debit wages control account; credit labour rate variance account.B debit work-in-progress control account; credit labour rate variance account.C debit labour rate variance account; credit wages control account.D debit labour rate variance account; credit work-in-progress control account.

The answer is A.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 9

Question 1.13

The labour cost graph below depicts

£

0 Output

A a piece rate scheme with a minimum guaranteed wage.B a straight piece rate scheme.C a straight time rate scheme.D a differential piece rate scheme.

The answer is A.

Question 1.14

X Ltd produces and sells a single product, which has a contribution to sales ratio of 30%.Fixed costs amount to £120,000 each year.

The number of units of sale required each year to break even

A is 156,000.B is 171,428.C is 400,000.D cannot be calculated from the data supplied.

The answer is D.

Workings

Breakeven point in terms of sales value = 0.3

£120,000 = £400,000

This must now be divided by the selling price.

The breakeven point in terms of units cannot be derived because we do not know the unitselling price.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 10

Question 1.15

P Ltd had an opening stock value of £2,640 (300 units valued at £8∙80 each) on 1 April. Thefollowing receipts and issues were recorded during April:

10 April Receipt 1,000 units £8∙60 per unit23 April Receipt 600 units £9∙00 per unit29 April Issues 1,700 units

Using the LIFO method, what was the total value of the issues on 29 April?

A £14,840 B £14,880 C £14,888 D £15,300

The answer is B.

Workings

The latest prices are used first:£

600 units from 23 April x £9∙00 per unit 5,4001,000 units from 10 April x £8∙60 per unit 8,600100 units from opening stock x £8∙80 per unit 880Total 14,880

Question 1.16

The following data relates to stock item A452:

Average usage 100 units per dayMinimum usage 60 units per dayMaximum usage 130 units per dayLead time 20-26 daysEOQ 4,000 units

The maximum stock level is

A 4,780 units. B 5,080 units. C 5,380 units. D 6,180 units.

The answer is D.

Workings

Maximum stock level = Reorder level (ROL) + EOQ – (Minimum rate of usage x minimum lead time)

ROL = Maximum usage x Maximum lead time= 130 x 26= 3,380 units

Maximum stock level = 3,380 + 4,000 – (60 x 20)= 6,180 units

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 11

Question 1.17

A company has been asked to quote for a job. The company aims to make a net profit of 30%on sales. The estimated cost for the job is as follows:

Direct materials 10 kg @ £10 per kgDirect labour 20 hours @ £5 per hourVariable production overheads are recovered at the rate of £2 per labour hour.

Fixed production overheads for the company are budgeted to be £100,000 each yearand are recovered on the basis of labour hours. There are 10,000 budgeted labourhours each year.

Other costs in relation to selling, distribution and administration are recovered at therate of £50 per job.

The company quote for the job should be

A £572. B £637. C £700. D £833.

The answer is C.

Workings

Direct materials 10 x £10 100Direct labour 20 x £5 100Prime cost 200Variable production overheads 20 x £2 40Fixed production overheads 20 x £10* 200Total production cost 440Other costs 50Total cost 490 = 70%Profit 210 = 30%Quote for the job 700 = 100%

* hours 10,000

overheads £100,000= £10 per hour

Question 1.18

The master budget comprises

A the budgeted profit and loss account, budgeted balance sheet and budgeted cashflow.

B the budgeted profit and loss account and budgeted balance sheet.C the budgeted profit and loss account.D the budgeted cash flow.

The answer is A.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 12

Question 1.19

RJD Ltd produces a single product. The managers currently use absorption costing, but areconsidering using marginal costing in future.

The fixed production overhead absorption rate is £68 per unit. There were 200 units ofopening stock for the period and 360 units of closing stock.

If marginal costing principles were applied, the profit for the period compared to theabsorption costing profit would be

A £6,800 lower.B £10,880 lower.C £10,880 higher.D £24,880 lower.

The answer is B.

Workings

Opening stock 200 unitsClosing stock 360 unitsStock increase 160 units x £68 = £10,880 (carried forward in stock under absorption

costing)

Under marginal costing the profit will be £10,880 lower than the absorption costing profit.

Question 1.20

A company is launching a new product. In order to manufacture this new product, two typesof labour are required – skilled and semi-skilled. The new product requires 5 hours of skilledlabour and 5 hours of semi-skilled labour.

A skilled employee is available and is currently paid £10 per hour. A replacement would,however, have to be obtained at a rate of £9 per hour, for the work which would otherwise bedone by the skilled employee. The current rate for semi-skilled workers is £5 per hour and anadditional employee would be appointed for this work.

The relevant cost of labour to be used in making one unit of the new product would be

A £25. B £70. C £75. D £120.

The answer is B.

Workings

£Skilled labour replacement 5 hours x £9 45

Semi-skilled labour 5 hours x £5 25

Relevant cost 70

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 13

Question 1.21

Cost centres are

A units of output or service for which costs are ascertained.B functions or locations for which costs are ascertained.C a segment of the organisation for which budgets are prepared.D amounts of expenditure attributable to various activities.

The answer is B.

Question 1.22

A company is currently preparing a material usage budget for the forthcoming year formaterial Z that will be used in product XX. The production director has confirmed that theproduction budget for product XX will be 10,000 units.

Each unit of product XX requires 4 kgs of material Z. Opening stock of material Z is budgetedto be 3,000 kgs and the company wishes to reduce stock at the end of the year by 25%.

What is the usage budget for material Z for the forthcoming year?

A 34,750 kgs B 39,250 kgs C 40,000 kgs D 40,750 kgs

The answer is C.

Workings

10,000 units produced x 4 kgs = 40,000 kgs

Question 1.23

Which of the following are characteristics of job costing?

(i) Customer-driven production(ii) Long production cycle(iii) Homogeneous products

A (i) only. B (i) and (ii) only. C (i) and (iii) only. D All of them.

The answer is A.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 14

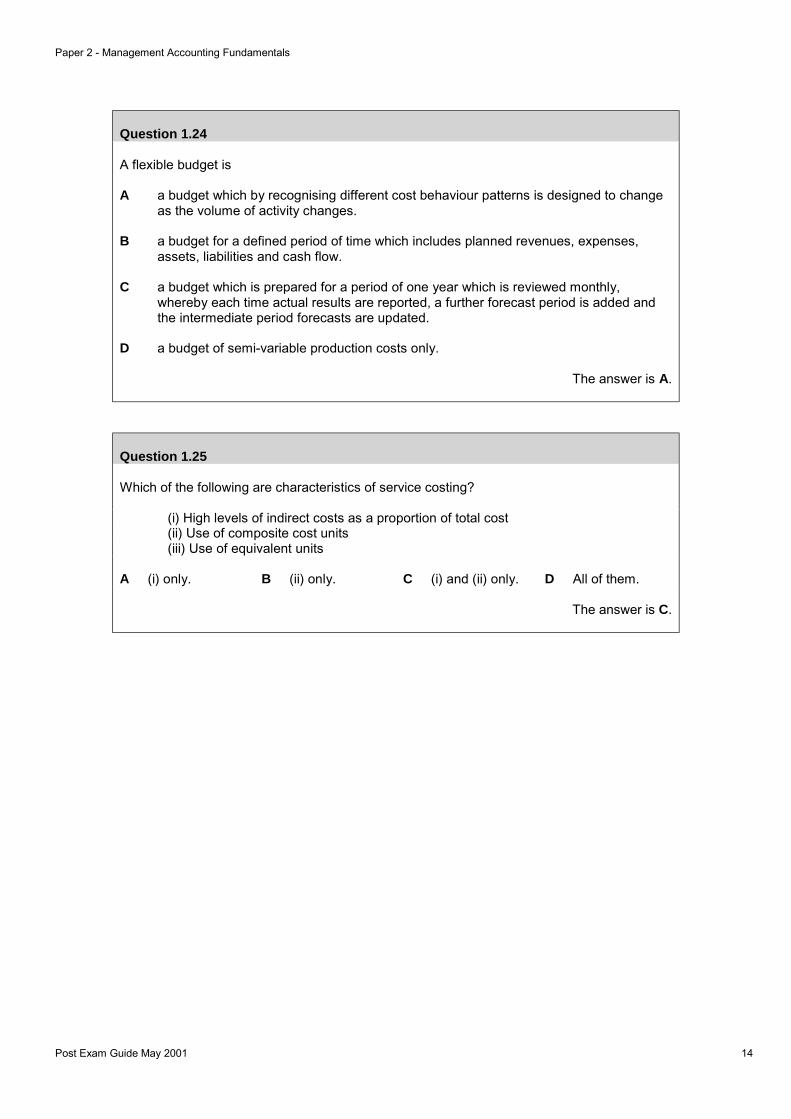

Question 1.24

A flexible budget is

A a budget which by recognising different cost behaviour patterns is designed to changeas the volume of activity changes.

B a budget for a defined period of time which includes planned revenues, expenses,assets, liabilities and cash flow.

C a budget which is prepared for a period of one year which is reviewed monthly,whereby each time actual results are reported, a further forecast period is added andthe intermediate period forecasts are updated.

D a budget of semi-variable production costs only.

The answer is A.

Question 1.25

Which of the following are characteristics of service costing?

(i) High levels of indirect costs as a proportion of total cost(ii) Use of composite cost units(iii) Use of equivalent units

A (i) only. B (ii) only. C (i) and (ii) only. D All of them.

The answer is C.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 15

Question 2

(a) Calculate the production plan that will maximise profit for the year ending 31 May 2002. (7 marks)

(b) Based on the production plan you have recommended in part (a), present a profitstatement for the year ending 31 May 2002 in a marginal costing format. (9 marks)

(c) Discuss two problems that may arise as a result of your recommended production plan. (4 marks)

(d) Explain why the contribution concept is used in limiting factor decisions. (5 marks)

Total marks = 25

Rationale

The question examines the application of marginal costing in a limiting factor decision-makingsituation. It is designed to encompass as many aspects as possible within this area. It isimportant that candidates have a good understanding of this topic as it forms the basis of theunderpinning knowledge required for decision making at the Intermediate level.

In part (a), candidates are asked to calculate the optimum production plan as a result of thelimiting factor and then in part (b) to calculate the profit derived from this plan. In part (c),candidates are then asked to discuss two problems which may arise as a result of thecompany not being in a position to fully satisfy demand. Part (d) of the question then askscandidates to comment on why the contribution concept is used in limiting factor decisions.Parts (c) and (d) require candidates to adopt a critical approach by asking them to discuss/comment on the methods and techniques used and any problems arising as a result of thelimiting factor.

Suggested Approach

Part (a)• Identify the limiting factor.• Calculate the contribution per unit.• Calculate the contribution per unit of limiting factor.• Rank the products in the order that maximises contribution per unit of limiting factor.• Allocate scarce resources according to the ranking.• Devise the production plan.

Part (b)• Calculate the profit generated by the plan using marginal costing principles.

Marking Guide Marks awarded

(a) Production plan 7(b) Marginal costing format & contribution calculation 9(c) Problems 4(d) Explanation 5

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 16

Examiner’s Comments

This question examined the application of marginal costing in a limiting factor decision -making situation in section (iv) of the syllabus.

Marginal costing is fundamental to candidates’ understanding of management accounting andtherefore it was surprising how poor the performance was on this question. Betterperformance would have been expected as a similar question appeared on the pilot paper.Disappointingly in a number of cases it was evident that some candidates had little or noknowledge of what a limiting factor was, or of how to deal with a limiting factor decision -making situation.

Part (a) asked for the production plan resulting from the limiting factor. Many candidatesderived the plan by incorrectly ranking on the basis of total profit, completely ignoring thelimiting factor. Other candidates incorrectly derived the plan on the basis of profit per unit oflimiting factor and only a small number of candidates correctly derived the plan on the basisof contribution per unit of limiting factor.

Part (b) asked for a marginal costing profit statement based on the plan recommended in part(a). Disappointingly a large number of candidates did not know how to calculate contributionor how to present the information in a marginal costing format. The most common error whencalculating contribution was to exclude the variable selling and distribution overheads fromvariable cost. A large number of candidates incorrectly adopted an absorption costingapproach and apportioned the common overheads between the two products. The commonoverheads should have been charged as a period cost in full against the contribution.

Part (c) was well answered with many candidates offering well thought out and structuredanswers to the problems associated with their recommended plans.

Part (d) was avoided by many candidates especially those who did not apply a marginalcosting approach in parts (a) and (b). Many candidates who attempted this part of thequestion correctly defined contribution and how the contribution concept is applied in limitingfactor decisions, yet their calculation of contribution and the application of the contributionconcept was incorrect in parts (a) and (b). This demonstrated that many candidates had rotelearned the definition of contribution and limiting factors but did not really understand theapplication of the contribution concept to limiting factor decisions.

Common Errors• Using absorption costing and ranking products on the basis of profit per unit of limiting

factor rather than contribution per unit of limiting factor.• Forgetting to include other variable costs, i.e. variable selling and distribution costs, in the

calculation of contribution.• Adjusting the fixed costs in line with the change in activity.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 17

Question 3

(a) Prepare the contract account in the books of SS Developments Ltd for the year ended 31December 2000. (8 marks)

(b) Calculate and explain the amount of profit (if any) to be recognised on the contract for theyear ended 31 December 2000. (8 marks)

(c) Explain why interim profits can be recognised on contracts. (5 marks)

(d) Explain briefly two non-financial factors which may arise as a result of the increase inresidential accommodation in Toyville. (4 marks)

Total marks = 25

Rationale

This question examines candidates’ understanding of contract costing. This is a new syllabusarea at the Foundation level and therefore the question is designed to encompass as manyaspects of contract costing as possible.

In part (a), candidates are asked to prepare a contract account for SS Developments Ltd.They are then asked in part (b) to calculate the amount of profit (if any) to be recognised onthe contract for the year. Part (c) asks the candidates to explain why interim profits arecalculated on contracts. It seeks to test the candidates’ understanding of the answer that theyhave calculated in part (b). Finally in part (d), candidates are asked to discuss non-financialfactors arising as a result of the contract. This part of the question requires candidates toapply some common sense.

Suggested Approach

Part (a)• Draw up the T account entering the various costs associated with the contract.• Enter the closing balances for stock of raw materials and the net book value (NBV) of

plant at the end of the period.• Close off the contract account, the balancing figure being the cost of work not yet

certified.

Part (b)• Calculate the profit expected from the contract.• Take a proportion of the profit expected according to the degree of completion to date;

this will then be the profit recognised for the contract.

Part (c)• In your own words explain why companies recognise interim profits on contracts.

Part (d)• Applying a common sense approach consider two non-financial implications of a

development of this nature.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 18

Marking Guide Marks awarded

Part (a)Entries into the contract accountAdjust for depreciation and the NBV of the plant

53

Part (b)Calculation of the expected profit and the profit recognisedExplanation of the calculation

53

Part (c)Provide an explanation incorporating the length of the contract, fluctuationin the reported results and prudence 5

Part (d)Two problems for Toyville associated with the residential development 4

Examiner’s Comments

This question examined candidates’ understanding of contract costing in section (iii) of thesyllabus. Performance was either very good or very poor. It was evident that a large numberof candidates had never studied contract costing but preferred to answer this question ratherthan the other optional question on standard costing and variance analysis.

In part (a) candidates were required to prepare a contract account. This was reasonably wellanswered but many candidates included non-cost items in the contract account e.g. value ofwork certified to date, cash receipts. Also many candidates correctly calculated annualdepreciation but did not charge the correct proportion (10/12ths) to the contract account.

In part (b) candidates were required to calculate and explain the amount of profit to berecognised on the contract. Many candidates correctly calculated the amount of profit to berecognised on the contract, but only a small number explained the result. Some candidatessimply calculated a profit as at 31 December 2000 and used this as the profit recognised forthe year. Candidates should have calculated the expected profit for the whole contract andthen taken a prudent proportion that represented the profit recognised as at 31 December2000.

Part (c), concerning the reasons why interim profits are recognised on contracts, was wellanswered by most candidates. Many earned full marks on this part of the question.

Part (d) was well answered. There were some well thought out and structured answers withmany candidates earning full marks.

Common Errors• Including non-cost items in the contract account e.g. value of work certified to date, cash

receipts.• Forgetting to adjust for depreciation and charging the contract with the full cost of the

plant.• Charging a full year’s depreciation when the contract only commenced on 1 March.• Not adjusting the final expected profit to recognise a profit at this stage in the contract.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 19

Question 4

(a) Calculate the standard costs of:(i) a general health assessment;(ii) a medical assessment. (5 marks)

(b) Prepare an operating statement for the period using detailed variance analysis toreconcile the standard cost of the new specialist unit with the actual cost of the newspecialist unit. (10 marks)

(c) Referring to your analysis in part (b):(i) for each of the variances calculated suggest one possible reason why it may have

occurred; (3 marks)(ii) discuss the possible difficulties of using standard costing in this type of

organisation. (7 marks)

Total marks = 25

Rationale

This question examines the application of standard costing in a service environment. Thequestion focuses on the labour and overhead cost variances. It is designed to encompass asmany aspects as possible within this area. It is important that candidates have a goodunderstanding of this topic as it forms the basis of the underpinning knowledge required forperformance measurement at the Intermediate level.

In part (a) candidates are required to calculate the standard cost for each type of assessment.This then forms the basis for calculating the labour and overhead cost variances in part (b).Candidates are also asked in part (b) to prepare an operating statement reconciling thestandard cost for the period with the actual cost. Part (c) asks candidates to give a reason foreach of the variances arising and to explain the possible difficulties that this type oforganisation may encounter when using standard costing. Candidates should apply acommon sense approach when answering this part of the question.

Suggested Approach

Part (a)• Identify the standard costs for a general health assessment and a medical assessment.

Part (b)• Draw up the pro-forma operating statement.• Using the standard cost for each assessment calculate the total standard cost and insert

the figure into the operating statement.• Calculate the actual cost and insert the figure into the operating statement.• Calculate and insert the variances.

Part (c)• Suggest some reasons why the variances calculated may have occurred.• Discuss the difficulties of using standard costing in this type of organisation.

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 20

Marking Guide Marks awarded

Part (a)Standard cost calculation 5

Part (b) Operating statement - formatActual cost and standard costVariances

136

Part (c)(i)One reason for each variance calculated 3

Part (c)(ii)Key points explaining the difficulties of using standard costing in thisorganisation 7

Examiner’s Comments

This question examined the application of standard costing in a service environment insection (ii) of the syllabus. It was reasonably well answered.

In part (a), candidates were required to calculate the standard costs of a general healthassessment and a medical assessment. Many candidates failed to earn marks because theyprepared the budgeted costs for each type of assessment rather than a unit standard cost foreach.

In part (b), the preparation of an operating statement was required. Many candidates failed toearn presentation marks because they were unable to produce such a statement. Only asmall number of candidates correctly calculated the standard cost for the new specialist unit.Many candidates incorrectly used the budgeted costs even though the question specificallyasked for the reconciliation of standard cost to actual cost. The labour efficiency and labourrate variances were well done by the majority of candidates. However, the majority wereunable to calculate the fixed overhead expenditure and fixed overhead volume variances, andtended to calculate only the total fixed overhead cost variance.

Part (c)(i) was generally well answered. However some candidates, when offering theirexplanations for the variances arising, tended not to make them specific to the variancescalculated in part (b) and simply offered a general explanation for variances occurring. Insome cases candidates wrote about the material usage variance and the material pricevariance even though there were no materials to consider in the question!

Part (c)(ii) required a general discussion of the possible difficulties of using standard costingin this type of organisation. Most candidates provided poor answers to this part of thequestion. Discussions were too general and in most cases too brief to warrant the award ofseven marks. Candidates failed to discuss the general problems associated with usingstandard costing in a service industry and in particular the problems encountered whensetting a standard time per assessment in relation to the specialist unit. Many candidatesbelieved that all organisations could easily use standard costing without any difficulties!

Paper 2 - Management Accounting Fundamentals

Post Exam Guide May 2001 21

Common Errors• Confusing standard cost with budgeted cost.• When explaining the reason for variances, failing to make the reasons specific to the

variances calculated in part (b) and instead giving general reasons for variancesoccurring.

• Believing that all organisations can easily use standard costing without any difficulties.