Embed Size (px)

Citation preview

May 2009 Examinations Strategic Level Paper P3 – Management Accounting – Risk and Control Strategy Question Paper 2 Examiner’s Brief Guide to the Paper 22 Examiner’s Answers 24 The answers published here have been written by the Examiner and should provide a helpful guide for both tutors and students. Published separately on the CIMA website (www.cimaglobal.com/students) from August is a Post Examination Guide for the paper which provides much valuable and complementary material including indicative mark information. © The Chartered Institute of Management Accountants. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recorded or otherwise, without the written permission of the publisher.

© The Chartered Institute of Management Accountants 2009

Management Accounting Pillar

Strategic Level Paper

P3 – Management Accounting – Risk and Control Strategy

21 May 2009 – Thursday Morning Session Instructions to candidates

You are allowed three hours to answer this question paper.

You are allowed 20 minutes reading time before the examination begins during which you should read the question paper and, if you wish, highlight and/or make notes on the question paper. However, you will not be allowed, under any circumstances, to open the answer book and start writing or use your calculator during the reading time.

You are strongly advised to carefully read ALL the question requirements before attempting the question concerned (that is, all parts and/or sub-questions). The question requirements are contained in a dotted box.

ALL answers must be written in the answer book. Answers or notes written on the question paper will not be submitted for marking.

Answer the ONE compulsory question in Section A on pages 2 to 3. The question requirements are on page 3, which is detachable for ease of reference.

Answer TWO questions only from Section B on pages 5 to 9.

Maths Tables and Formulae are provided on pages 11 to 14. These pages are detachable for ease of reference.

The list of verbs as published in the syllabus is given for reference on the inside back cover of this question paper.

Write your candidate number, the paper number and examination subject title in the spaces provided on the front of the answer book. Also write your contact ID and name in the space provided in the right hand margin and seal to close.

Tick the appropriate boxes on the front of the answer book to indicate which questions you have answered.

P3 –

Ris

k an

d C

ontr

ol S

trat

egy

TURN OVER

P3 2 May 2009

SECTION A – 50 MARKS

[the indicative time for answering this Section is 90 minutes]

ANSWER THIS QUESTION. Question One LLL is a major quoted company. It owns three of the major airports in its home country, including Eastfield which is the main airport serving the capital city. Eastfield is one of Europe’s main airports. It attracts passengers who wish to travel to or from the capital city for business or leisure purposes as well as passengers from intercontinental flights who wish to transfer to short flights to other destinations in Europe. The airport is becoming increasingly congested because the airport’s two runways are operating at close to full capacity. LLL has applied for permission to build a third runway that would increase the number of flights that it could handle. It would also ensure that the airport could service the new generation of very large aircraft that will soon come into service. The total cost of this new runway is likely to exceed €0·5 billion. LLL’s market capitalisation is €6 billion. Planning the new runway has been a major project for LLL. The government demanded very detailed plans before granting initial permission to proceed with the project. LLL has had to spend €50m on feasibility studies, architects’ plans and on marketing the proposal just to get to the stage of obtaining permission to proceed. The airline operators which use Eastfield have had to make major commitments to expand their services in order to utilise the potential new capacity. The company has reached the stage where it is about to buy the necessary land on which to build the new runway. It has, however, encountered two major problems. Firstly, the proposed construction of a third runway has upset a large number of environmental campaigners. They say that the new runway will lead to a massive increase in air travel and that the project should be stopped immediately. They have protested by buying a small field in the middle of the land that LLL will have to buy in order to build the runway. They say that they will not sell this field under any circumstances. There is no other site suitable for the runway. LLL’s lawyers are confident that they can take legal action to force the environmental campaigners to sell the land, although that will lead to a major delay in commencing the project. It would be possible to start work in the meantime, although that would risk wasting the cost of doing so if the courts do not force the sale of the field. It is thought the environmental campaigners may also lobby the government to reconsider its decision. Secondly, the global economy has gone into recession and that has reduced the demand for business and leisure travel. LLL’s economists have forecast a recovery over the next few years. It will take at least five years to build the runway. The airline operators have reacted to these problems in different ways. Some, mainly the smaller airline operators, have written to the Chief Executive of LLL and have asked for the building of the new runway to be postponed. They are concerned that LLL will be forced to increase the charges to the airline operator for using the airport and, as a result of the recession, there will be a lower volume of passengers to cover these additional costs. Furthermore, they feel that environmental concerns will encourage passengers to use alternative forms of transport such as high-speed rail links for journeys within Europe, which will take business away from the short flights that they provide. In contrast, the larger airline operators have written to express concern that the new runway may be delayed. They have already spent a great deal of money on planning new routes which will become operational only when the new runway is completed. One of these airline operators has paid €30m for options to take delivery of new aircraft to use on these new routes. These options give the airline operator guaranteed delivery dates for the aircraft at a fixed price

May 2009 3 P3

denominated in US dollars if firm orders are placed. However, the option will lapse and become worthless if an order is not placed within four years. Airline operators often take out options such as this because aircraft manufacturers often struggle to keep up with demand and so it can be difficult to ensure that new aircraft are available as and when they are required. The larger airline operators have warned that they will seek compensation from LLL if the new runway is not completed within the next seven years. LLL’s lawyers have advised that the airline operators would have a strong case. The Chairman of LLL met with the Chief Executive and asked why the company had not planned ahead in order to deal with risks such as the difficulty of obtaining the land and the unexpected decline in the demand for air travel. The Chief Executive responded that it would have been very expensive for LLL to have purchased the land before obtaining permission to build the runway and that the company would have had no use for that land if the government had refused permission for the runway. In any case, the environmental campaigners who purchased the field would almost certainly have found some other way to delay the project if LLL had secured the land sooner. The Chief Executive does not believe that there will be significant, long-term decline in demand for air travel. He believes economic downturns happen from time to time and are generally short-lived. The runway is a project that should be viewed as an investment in the company’s future for the next fifty years and demand for air travel is likely to remain robust over most of that longer-term period. The Chairman has decided to call an immediate meeting of the non-executive directors. After the non-executive directors have been briefed, there will be a meeting of the full board.

Required:

(a) Compare and contrast the responsibilities of LLL’s executive directors and non-executive directors for the management of the risks associated with this project.

(10 marks)

(b) “Managing long-term strategic risks should always take priority over the management of short-term risks”. Discuss the above statement using examples from the scenario.

(14 marks)

(c) Explain the political and reputational risks, and the associated commercial implications, that might arise from the activities of the environmental campaigners.

(13 marks)

(d) Discuss the benefits and risks associated with the initial purchase of an option to buy an aircraft and the possible subsequent exercise of that option, as described in the scenario.

(13 marks)

(Total for Question One = 50 marks)

(Total for Section A = 50 marks)

Section B begins on page 5

TURN OVER

P3 4 May 2009

[this page is blank]

May 2009 5 P3

SECTION B – 50 MARKS

[the indicative time for answering this section is 90 minutes]

ANSWER TWO QUESTIONS ONLY Question Two AFC is a global engineering business with a $1 billion turnover, employing 5,000 people in 15 countries. It is listed on stock exchanges in New York and London. AFC carries out major construction projects that typically take several years to complete. Examples of the kinds of projects carried out by AFC are power stations, dams and bridges. Most of AFC’s customers are governments. Negotiations leading to the winning of tenders are extensive and the terms and conditions of the resulting contracts are very comprehensive. The negotiated price is most often a fixed price contract. Subsequent variations requested by the customer are invoiced to the customer at cost plus a 20% profit margin for AFC. The major risks faced by AFC could arise from: • Professional indemnity claims arising from technical errors that have caused faulty work

and/or rectification. AFC’s insurance premiums for professional indemnity are several million dollars each year.

• Downturns in business due mainly to the reductions in government funding of large construction projects.

• Cost over-runs, which erode profit (however, cost increases that result from specification changes requested by customers are invoiced to them as contract variations).

• Penalties that apply under the contract for late completion of the project.

Required: Recommend the controls that AFC should implement in order to minimise the risks identified in the scenario. You should consider separately each of the four major risks faced by AFC, and for each risk recommend controls in each of the following categories: • financial

• non-financial quantitative

• qualitative

There are approximately 2 marks available for each risk/control combination.

(Total for Question Two = 25 marks)

Section B continues on the next page

TURN OVER

P3 6 May 2009

Question Three CM is an owner-managed restaurant in a student area of a university city. The menu lists a wide range of dishes, which are individually priced. The restaurant also offers, at certain times, a fixed price “eat as much as you like” buffet. The opening times for the restaurant and the times for the “all you can eat” buffet are shown below:

CM Opening Hours “Eat as Much as You Like” opening hours

Monday – Friday Noon – 11pm 5pm – 8pm Saturday Noon – Midnight 1pm – 3pm

6pm – 8pm Sunday Noon – 7pm 1pm – 6pm

When the “eat as much as you like” buffet is closed, customers can choose individually priced dishes from an extensive menu. The owner thinks that about 85% of CM’s customers come for the buffet. CM offers free jugs of water but also sells a wide range of alcoholic and non-alcoholic drinks, which carry a high mark up on delivered cost. In an effort to keep operating costs as low as possible, the restaurant employs only part-time staff aged under 21, who are paid the national minimum wage. Their terms of employment require them to be willing to work on any of a range of tasks including preparation and cooking in the kitchen, serving on tables, replenishing the buffet, and working on the reception and payment desk. Staff turnover rates are very high, with the average employee only working two months for CM. The provision of a daily free meal for each member of staff plus a friend has recently been introduced in an attempt to reduce high staff turnover. No records are kept of the number of free meals provided. The restaurant manager has nationally recognised qualifications in catering and food hygiene. Externally accredited courses in food hygiene for employees are available at local colleges. However, the manager considers them to be too expensive in view of the high staff turnover. Consequently, he takes sole responsibility for training new staff. The restaurant accepts only cash from its customers. Customers pay on departure, giving cash to whoever is working the payment desk at the time. The cash is not processed through a till and receipts are not issued.

Required:

(a) Identify the potential risks in the current operation of CM and recommend appropriate control measures to reduce those risks in each of the following areas of CM’s operations:

• Record keeping; • Working capital management; • Human resource policy.

(19 marks)

(b) Explain three possible reasons why the manager of CM may choose not to implement any controls.

(6 marks)

(Total for Question Three = 25 marks)

May 2009 7 P3

Question Four

Required:

(a) Explain why organisations need to formulate an information technology strategy.

(6 marks) (b) Discuss the risks which may be faced by an organisation that is dependent on

computerised information systems (excluding systems development risks).

(7 marks)

(c) (i) Explain three disadvantages of outsourcing information technology.

(6 marks)

(ii) Recommend ways in which the risks associated with outsourcing information technology may be controlled.

(6 marks)

(Total for requirement (c) = 12 marks)

(Total for Question Four = 25 marks)

Section B continues on the next page

TURN OVER

P3 8 May 2009

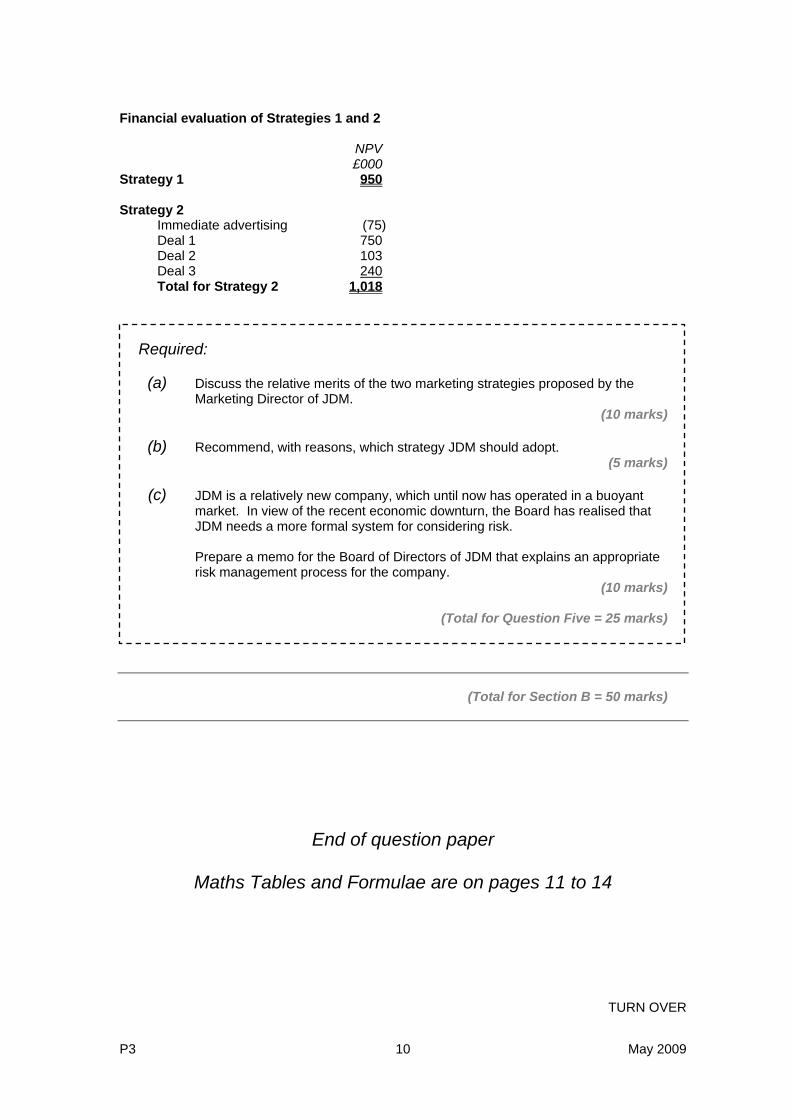

Question Five JDM Construction is a UK-based construction company. The company completed the building of 30 apartments in December 2008 and immediately sold 15 of them for £125,000 each. However, no apartments have been sold since that date. The total cost of building the apartments was £75,000 each. It is thought that the only additional cash flows that will arise will be for marketing and selling the remaining 15 apartments. The Marketing Director of JDM has forecast the following changes in property prices during the next five years: Market Forecast 2009 10% decrease 2010 2% decrease 2011 5% increase 2012 8% increase 2013 5% increase In response to the declining market, the Marketing Director has proposed and financially evaluated the two possible alternative marketing strategies shown below. Marketing Strategy 1 Sell the properties at a discounted price of £115,000 each. This would require a marketing campaign that involves spending £210,000. Market research suggests that there is a 70% chance that all of the apartments would be sold within six months but a 30% chance that none will be sold. Under this strategy all money will be paid and received by 31 December 2009. Marketing Strategy 2 This strategy requires spending £75,000 on advertising. The Marketing Director expects that all the remaining 15 apartments will be sold under this strategy. Marketing Strategy 2 involves offering potential buyers the choice of three different deals, as detailed below:

Deal 1 Customers can buy an apartment at a reduced price of £95,000, if they agree to a rapid transfer of ownership. A 10% deposit is payable immediately, and the remaining balance is payable in eight weeks’ time. The Marketing Director expects that eight apartments will be sold under this arrangement. Deal 2 Purchasers will be given the opportunity to purchase an apartment for £110,000, with a guarantee that if they wish to sell at any time during the next five years, JDM will purchase the property back at this initial price. Under this deal all sales receipts will be received within the next three months. The marketing director expects to sell five apartments under this arrangement and that they will all be repurchased by 2012. Deal 3 Customers will be given the opportunity to purchase an apartment for £105,000, payable in three months’ time, plus a further payment of £25,000 payable after 10 years, or when the customer sells the apartment, whichever occurs first. The Marketing Director expects that two apartments will be sold under this arrangement.

May 2009 9 P3

Financial evaluation of Strategies 1 and 2 NPV

£000 Strategy 1

950

Strategy 2 Immediate advertising (75) Deal 1 750 Deal 2 103 Deal 3 240 Total for Strategy 2 1,018

Required:

(a) Discuss the relative merits of the two marketing strategies proposed by the Marketing Director of JDM.

(10 marks)

(b) Recommend, with reasons, which strategy JDM should adopt. (5 marks)

(c) JDM is a relatively new company, which until now has operated in a buoyant

market. In view of the recent economic downturn, the Board has realised that JDM needs a more formal system for considering risk.

Prepare a memo for the Board of Directors of JDM that explains an appropriate risk management process for the company.

(10 marks)

(Total for Question Five = 25 marks)

(Total for Section B = 50 marks)

End of question paper

Maths Tables and Formulae are on pages 11 to 14

TURN OVER

P3 10 May 2009

[this page is blank]

May 2009 11 P3

P3 12 May 2009 P3 12 May 2009

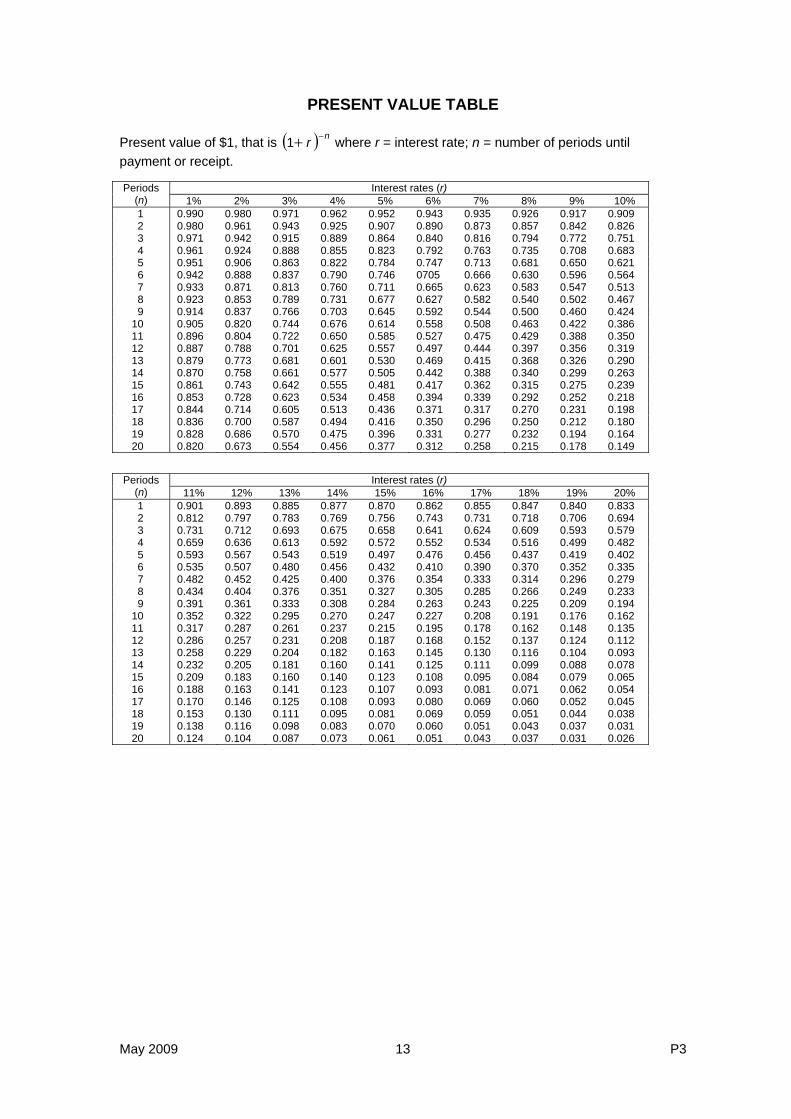

PRESENT VALUE TABLE

Present value of $1, that is where r = interest rate; n = number of periods until payment or receipt.

( ) nr −+1

Interest rates (r) Periods

(n) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 1 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909 2 0.980 0.961 0.943 0.925 0.907 0.890 0.873 0.857 0.842 0.826 3 0.971 0.942 0.915 0.889 0.864 0.840 0.816 0.794 0.772 0.751 4 0.961 0.924 0.888 0.855 0.823 0.792 0.763 0.735 0.708 0.683 5 0.951 0.906 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621 6 0.942 0.888 0.837 0.790 0.746 0705 0.666 0.630 0.596 0.564 7 0.933 0.871 0.813 0.760 0.711 0.665 0.623 0.583 0.547 0.513 8 0.923 0.853 0.789 0.731 0.677 0.627 0.582 0.540 0.502 0.467 9 0.914 0.837 0.766 0.703 0.645 0.592 0.544 0.500 0.460 0.424 10 0.905 0.820 0.744 0.676 0.614 0.558 0.508 0.463 0.422 0.386 11 0.896 0.804 0.722 0.650 0.585 0.527 0.475 0.429 0.388 0.350 12 0.887 0.788 0.701 0.625 0.557 0.497 0.444 0.397 0.356 0.319 13 0.879 0.773 0.681 0.601 0.530 0.469 0.415 0.368 0.326 0.290 14 0.870 0.758 0.661 0.577 0.505 0.442 0.388 0.340 0.299 0.263 15 0.861 0.743 0.642 0.555 0.481 0.417 0.362 0.315 0.275 0.239 16 0.853 0.728 0.623 0.534 0.458 0.394 0.339 0.292 0.252 0.218 17 0.844 0.714 0.605 0.513 0.436 0.371 0.317 0.270 0.231 0.198 18 0.836 0.700 0.587 0.494 0.416 0.350 0.296 0.250 0.212 0.180 19 0.828 0.686 0.570 0.475 0.396 0.331 0.277 0.232 0.194 0.164 20 0.820 0.673 0.554 0.456 0.377 0.312 0.258 0.215 0.178 0.149

Interest rates (r) Periods

(n) 11% 12% 13% 14% 15% 16% 17% 18% 19% 20% 1 0.901 0.893 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 2 0.812 0.797 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694 3 0.731 0.712 0.693 0.675 0.658 0.641 0.624 0.609 0.593 0.579 4 0.659 0.636 0.613 0.592 0.572 0.552 0.534 0.516 0.499 0.482 5 0.593 0.567 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402 6 0.535 0.507 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335 7 0.482 0.452 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279 8 0.434 0.404 0.376 0.351 0.327 0.305 0.285 0.266 0.249 0.233 9 0.391 0.361 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194 10 0.352 0.322 0.295 0.270 0.247 0.227 0.208 0.191 0.176 0.162 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0.148 0.135 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 0.112 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 0.116 0.104 0.093 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 0.099 0.088 0.078 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 0.084 0.079 0.065 16 0.188 0.163 0.141 0.123 0.107 0.093 0.081 0.071 0.062 0.054 17 0.170 0.146 0.125 0.108 0.093 0.080 0.069 0.060 0.052 0.045 18 0.153 0.130 0.111 0.095 0.081 0.069 0.059 0.051 0.044 0.038 19 0.138 0.116 0.098 0.083 0.070 0.060 0.051 0.043 0.037 0.031 20 0.124 0.104 0.087 0.073 0.061 0.051 0.043 0.037 0.031 0.026

May 2009 13 P3

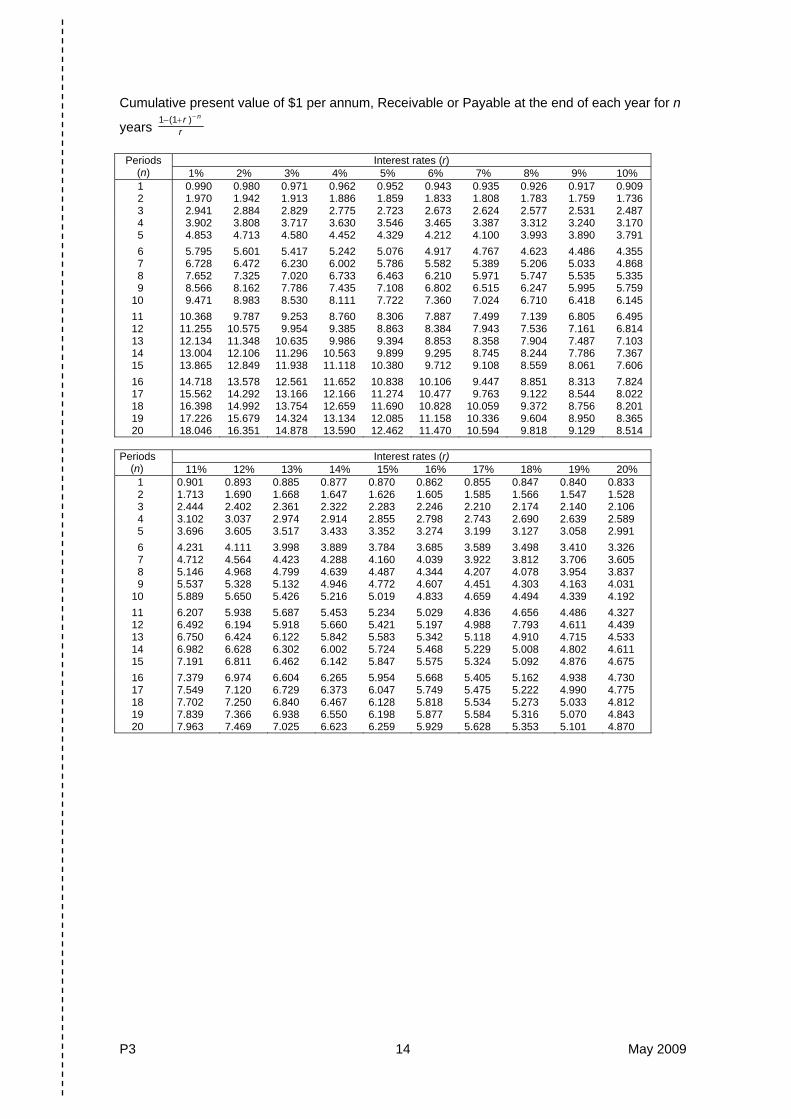

Cumulative present value of $1 per annum, Receivable or Payable at the end of each year for n

years rr n−+− )(11

Interest rates (r) Periods

(n) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 1 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909 2 1.970 1.942 1.913 1.886 1.859 1.833 1.808 1.783 1.759 1.736 3 2.941 2.884 2.829 2.775 2.723 2.673 2.624 2.577 2.531 2.487 4 3.902 3.808 3.717 3.630 3.546 3.465 3.387 3.312 3.240 3.170 5 4.853 4.713 4.580 4.452 4.329 4.212 4.100 3.993 3.890 3.791 6 5.795 5.601 5.417 5.242 5.076 4.917 4.767 4.623 4.486 4.355 7 6.728 6.472 6.230 6.002 5.786 5.582 5.389 5.206 5.033 4.868 8 7.652 7.325 7.020 6.733 6.463 6.210 5.971 5.747 5.535 5.335 9 8.566 8.162 7.786 7.435 7.108 6.802 6.515 6.247 5.995 5.759 10 9.471 8.983 8.530 8.111 7.722 7.360 7.024 6.710 6.418 6.145 11 10.368 9.787 9.253 8.760 8.306 7.887 7.499 7.139 6.805 6.495 12 11.255 10.575 9.954 9.385 8.863 8.384 7.943 7.536 7.161 6.814 13 12.134 11.348 10.635 9.986 9.394 8.853 8.358 7.904 7.487 7.103 14 13.004 12.106 11.296 10.563 9.899 9.295 8.745 8.244 7.786 7.367 15 13.865 12.849 11.938 11.118 10.380 9.712 9.108 8.559 8.061 7.606 16 14.718 13.578 12.561 11.652 10.838 10.106 9.447 8.851 8.313 7.824 17 15.562 14.292 13.166 12.166 11.274 10.477 9.763 9.122 8.544 8.022 18 16.398 14.992 13.754 12.659 11.690 10.828 10.059 9.372 8.756 8.201 19 17.226 15.679 14.324 13.134 12.085 11.158 10.336 9.604 8.950 8.365 20 18.046 16.351 14.878 13.590 12.462 11.470 10.594 9.818 9.129 8.514

Interest rates (r) Periods

(n) 11% 12% 13% 14% 15% 16% 17% 18% 19% 20% 1 0.901 0.893 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 2 1.713 1.690 1.668 1.647 1.626 1.605 1.585 1.566 1.547 1.528 3 2.444 2.402 2.361 2.322 2.283 2.246 2.210 2.174 2.140 2.106 4 3.102 3.037 2.974 2.914 2.855 2.798 2.743 2.690 2.639 2.589 5 3.696 3.605 3.517 3.433 3.352 3.274 3.199 3.127 3.058 2.991 6 4.231 4.111 3.998 3.889 3.784 3.685 3.589 3.498 3.410 3.326 7 4.712 4.564 4.423 4.288 4.160 4.039 3.922 3.812 3.706 3.605 8 5.146 4.968 4.799 4.639 4.487 4.344 4.207 4.078 3.954 3.837 9 5.537 5.328 5.132 4.946 4.772 4.607 4.451 4.303 4.163 4.031 10 5.889 5.650 5.426 5.216 5.019 4.833 4.659 4.494 4.339 4.192 11 6.207 5.938 5.687 5.453 5.234 5.029 4.836 4.656 4.486 4.327 12 6.492 6.194 5.918 5.660 5.421 5.197 4.988 7.793 4.611 4.439 13 6.750 6.424 6.122 5.842 5.583 5.342 5.118 4.910 4.715 4.533 14 6.982 6.628 6.302 6.002 5.724 5.468 5.229 5.008 4.802 4.611 15 7.191 6.811 6.462 6.142 5.847 5.575 5.324 5.092 4.876 4.675 16 7.379 6.974 6.604 6.265 5.954 5.668 5.405 5.162 4.938 4.730 17 7.549 7.120 6.729 6.373 6.047 5.749 5.475 5.222 4.990 4.775 18 7.702 7.250 6.840 6.467 6.128 5.818 5.534 5.273 5.033 4.812 19 7.839 7.366 6.938 6.550 6.198 5.877 5.584 5.316 5.070 4.843 20 7.963 7.469 7.025 6.623 6.259 5.929 5.628 5.353 5.101 4.870

P3 14 May 2009

FORMULAE Annuity Present value of an annuity of £1 per annum receivable or payable for n years, commencing in one year, discounted at r% per annum:

PV = ⎥⎥⎦

⎤

⎢⎢⎣

⎡

+−

nrr ]1[111

Perpetuity Present value of £1 per annum, payable or receivable in perpetuity, commencing in one year, discounted at r% per annum:

PV = r1

Growing Perpetuity Present value of £1 per annum, receivable or payable, commencing in one year, growing in perpetuity at a constant rate of g% per annum, discounted at r% per annum:

PV = gr −

1

May 2009 15 P3

[this page is blank]

P3 16 May 2009

[this page is blank]

May 2009 17 P3

[this page is blank]

P3 18 May 2009

[this page is blank]

May 2009 19 P3

LIST OF VERBS USED IN THE QUESTION REQUIREMENTS A list of the learning objectives and verbs that appear in the syllabus and in the question requirements for each question in this paper. It is important that you answer the question according to the definition of the verb.

LEARNING OBJECTIVE VERBS USED DEFINITION

1 KNOWLEDGE

What you are expected to know. List Make a list of State Express, fully or clearly, the details of/facts of Define Give the exact meaning of

2 COMPREHENSION What you are expected to understand. Describe Communicate the key features

Distinguish Highlight the differences between Explain Make clear or intelligible/State the meaning of Identify Recognise, establish or select after consideration Illustrate Use an example to describe or explain something

3 APPLICATION How you are expected to apply your knowledge. Apply

Calculate/compute To put to practical use To ascertain or reckon mathematically

Demonstrate To prove with certainty or to exhibit by practical means

Prepare To make or get ready for use Reconcile To make or prove consistent/compatible Solve Find an answer to Tabulate Arrange in a table

4 ANALYSIS How are you expected to analyse the detail of what you have learned.

Analyse Categorise

Examine in detail the structure of Place into a defined class or division

Compare and contrast Show the similarities and/or differences between Construct To build up or compile Discuss To examine in detail by argument Interpret To translate into intelligible or familiar terms Produce To create or bring into existence

5 EVALUATION How are you expected to use your learning to evaluate, make decisions or recommendations.

Advise Evaluate Recommend

To counsel, inform or notify To appraise or assess the value of To advise on a course of action

P3 20 May 2009

Management Accounting Pillar Strategic Level Paper

P3 – Management Accounting – Risk and Control Strategy

May 2009

Thursday Morning Session

May 2009 21 P3

The Examiners for Management Accounting – Risk and Control Strategy offer to future candidates and to tutors using this booklet for study purposes, the

following background and guidance on the questions included in this examination paper.

Section A – Question One – Compulsory Question One The case study involves LLL a large company who owns several airports. One of the main hub airports in Europe is investigating building a new, very large runway which would be able to be used by the latest large aircraft. The new large aircraft can be ordered in advance by taking out an option with the aircraft builders for the purchase of the aircraft at some future date. One of the many issues holding up the decision to proceed with the new runway are the environmental protesters, who have bought a small but essential piece of land, right in the middle of the proposed site. Another major issue is the economic downturn and the possible decrease in air travel over the next few years. The chairman of LLL has decided to hold a meeting of non-executive directors prior to holding a meeting with the executive directors to discuss the situation. The first part of the question asks candidates to compare and contrast the role of executive and non-executive directors a specific answer relating to the scenario is required. The question then goes on to ask about prioritising long or short term risks, this is followed by a question about political and reputational risk that could arise from the activities of the environmental campaigners and finally candidates are asked to discuss the benefits and risks of the initial purchase and exercise of the option to purchase the aircraft.

The syllabus areas covered are B(i) Define and identify risks facing an organization, B(iv) Evaluate risk management strategies, Bvii) Discuss the principles of good corporate governance for listed companies, particularly as regards the need for internal controls and D(iii) Evaluate the effects of alternative methods of risk management and make recommendations accordingly.

Section B – answer two of four questions Question Two provides the scenario of an engineering business involved in long-term contracting based largely on government tenders. The scenario identifies four key risks facing the company: professional indemnity claims, economic downturn, cost over-runs, and contractual penalties. For each risk, candidates are asked to recommend controls which are financial, non-financial quantitative, and qualitative. This results in a 4x3 matrix (of four risks and three categories of control for each risk).

Candidates are expected to be able to consider controls beyond the traditional accounting controls. In answering this question, candidates need to consider a wide range of possible controls including contract profitability and insurance (financial); measurement/investigation of variances and portfolio approaches (non-financial quantitative); and policies and procedures for human resources, relationship management and project management (qualitative), etc. Importantly, each control recommended needs to be appropriate to the risks identified in the scenario.

The syllabus areas covered are B (iv) evaluation of risk management strategies; and B (v) evaluation of the essential features of internal control systems for identifying, assessing and managing risks.

Question Three requires candidates to identify the risks faced by a restaurant. The scenario is of an owner-managed business with a high staff turnover and a ‘relaxed’ attitude to internal control. Candidates are also required to identify appropriate controls to reduce risks in three aspects of the restaurant’s operation: record keeping; working capital management; and human resources. In the second part of the question, candidates are expected to provide reasons why an owner-manager may prefer not to implement the appropriate controls.

P3 22 May 2009

In each of the three aspects of the restaurant’s operations, candidates need to both identify the risks that emerge from the scenario, and recommend appropriate controls in relation to those risks. However, candidates are not penalised for using examples of risks and controls under different aspects than are listed in the suggested solution. In answering the second part of the question, candidates should be able to recognise the financial constraints that may prevent controls from being implemented and the practical constraints that controls will impose on the owner. The syllabus areas covered are B (i) define and identify risks facing an organisation; A (ii) evaluate the control of activities and resources within the organisation; and A (iv) evaluate the appropriateness of an organisation’s management accounting control systems and make recommendations for improvements. Question Four is a question without a scenario and has three parts. In part (a) candidates need to explain why organisations have information technology strategies. In part (b) candidates need to identify the risks where an organisation is dependent on computerised information systems. Part (c) requires candidates to explain the disadvantages of outsourcing IT and how the risks of outsourcing might be controlled. The question explicitly excludes system development risks. In the first part, candidates need to distinguish between IT and IS strategies and explain the importance of an IT strategy in the context of overall strategy. In the second part, candidates should be able to identify a variety of risks including data entry errors, breaches of security and business continuity issues. Candidates should note that the requirement in all three parts of the question to ‘explain’, ‘discuss’ and ‘recommend’ means that it is not sufficient to merely provide a list. Reasons need to be provided to support the candidate’s answer. The syllabus areas covered are mainly E (i) evaluate and advise managers on the development of IM, IS and IT strategies that support management and internal control requirements; and E (iii) evaluate benefits and risks in the structuring and organisation of the IS/IT function and its integration with the rest of the business. Question Five is the scenario of a construction company facing alternative marketing strategies to sell apartments that have been built but remain unsold in a declining market. The question requires candidates to discuss the relative merits of the alternative marketing strategies, and recommend (with supporting reasons) the strategy the business should adopt. The final part of the question asks candidates to explain to a Board how it should adopt a more formal risk management process. There is no right and wrong answer in relation to the preferred marketing strategy, but candidates are expected to provide well considered reasons to support their recommendation. In their approach to answering the question, candidates should identify the relative importance of financial & non-financial criteria and the risk appetite of the business. In answering the final part of the question, candidates should be able to make recommendations that address the particular needs of the industry. The syllabus areas covered are D (i) identify and evaluate financial risks facing an organisation; D (ii) identify and evaluate appropriate methods for managing financial risks; and D (iii) evaluate the effects of alternative methods of risk management and make recommendations accordingly.

May 2009 23 P3

Strategic Level Paper

P3 – Management Accounting – Risk and Control Strategy

Examiner’s Answers

The answers that follow are fuller and more comprehensive than would have been expected from a well-prepared candidate. They have been written in this way to aid teaching, study and revision for tutors and candidates alike.

SECTION A Answer to Question One

(a) The entire board is responsible for the leadership of the company, including the assessment and management of risks. All directors are responsible for selecting projects that offer an acceptable relationship between risk and return.

The non-executive directors have a specific duty under the Combined Code to challenge the major strategies that the executive directors propose. Any major proposals for strategic changes should be reviewed by the non-executives to ensure that they are genuinely in the company’s best interests. The shareholders and executive directors will have different attitudes towards risk because each party has a different interest in the company. The shareholders can diversify their investment portfolio whereas the directors can have only one full-time job and so the executive board might be unduly risk-averse. The executive directors are not investing their own cash and so any failed investments might have a limited downside risk for the directors but not for the shareholders and so the executives might take excessive risks in cases where their bonuses might be enhanced if the gamble pays off. The non-executive directors can review the risk profile of the business in a more dispassionate and objective manner.

In this case the project involves massive amounts of investment, amounting to €0·5bn / €6·0bn = 8·3% of the company’s capitalisation. The potential impact is so large that it really requires the “creative tension” associated with the detailed scrutiny of the non-executives seeking some assurance from the executive directors that this proposal is in the company’s best interests.

The project also involves risks that are very difficult to quantify and manage. The non-executive directors may have a role to play in mitigating the political implications of proceeding with this project. For example, one factor in appointing non-executives is their contacts in government and the media. The non-executive directors may also tend to have a broader range of experience than their executive counterparts and be able to identify risk factors that might otherwise be overlooked.

P3 24 May 2009

(b) Risk management should always be considered in terms of the implications for the company and for shareholders’ wealth. The distinction between long-term and short-term risk factors is important, but is of a secondary importance. The board should prioritise risks in terms of severity and likelihood.

In general, long-term risks arise at the strategic level. In the case of LLL, the decision to proceed with the new runway is partly about balancing the risks associated with investing a massive amount of money in a new runway against the risks of being hampered by a lack of capacity. Such major risks must be kept under regular review, although they are unlikely to require constant attention.

Short-term risks tend to arise at the tactical level associated with implementing strategic plans. For example, the matter of the risks of delays and costs arising from the activities of the environmentalists should be managed on an ongoing basis because that is an area that will change over time, but is clearly both potentially serious and likely. Similarly, the concerns raised by the smaller airlines are really a short-term risk. Provided they can be supported through the recession, demand for their services will recover and they will continue to trade with LLL.

Arguably, both long-term and short-term risk should be reviewed and managed in an appropriate manner. While long-term strategic risks may not require constant management, the board should briefly consider the possibility that work is required in that area at every meeting. This may amount to little more than the board being aware of the key areas where strategic risks arise in their business or industry and reacting to any threats or opportunities that arise. Short-term risks may not have the same potential relevance to the company’s inherent value, but they could easily be sufficient to cause serious or even irreparable harm. For example, the economic downturn may well be a fairly short-lived cycle that will reverse in the medium term, but the directors will have to implement a response to safeguard the company’s cash flows during that period.

The immediate and pressing nature of short-term risks may be a dangerous distraction for companies. For example, changes in consumer attitudes to short-haul air travel or improvements in alternative technologies such as high speed rail links could render the third runway obsolete before it is built. Such threats may well be overlooked if managers focus their attention on immediate problems such as the public relations problems created by the protests.

Decisions taken at the strategic level will tend to have an impact on subsequent short-term risks. For example, the decision to proceed with the third runway will expose LLL to a series of political and financial risks throughout the whole process of planning and building. The long-term strategic matters may not necessarily be more important, but they may have to be considered first because they will then change the shape of the immediate short-term risks faced by the company.

(c) There is a danger that the government will reverse its decision if the actions of the environmentalists create sufficient public sympathy. Politicians must always be aware of the effects of public sympathy and the possible loss of votes. If the expansion does not go ahead then LLL may be held liable for the costs borne to date by the larger airlines if they feel that LLL has not taken sufficient care in managing the planning and approval process.

The fact that LLL will have to take the environmentalists to court will cause a great deal of bad publicity. This will look as if a large corporation is bullying a small group of committed campaigners. It will be worse if the campaigners suffer significant costs in defending the action because that may create even further bad publicity for LLL.

There is always a possibility that LLL will lose the court action, thereby threatening the project. There is also a possibility that it will win the case but be forced to delay if the activists decide to appeal the decision. Even if the environmentalists know that they will lose eventually, they can impose significant harm on LLL by delaying the project.

May 2009 25 P3

These uncertainties will make it far more difficult to plan the project. The undertaking is far too large to delay work until the case is resolved and yet any initial work that is undertaken will create costs for LLL.

The bad publicity could have a particularly bad effect on demand for short flights within Europe. That could lead to some of the smaller airlines going out of business or moving to a different airport. The potential loss of business for LLL will be particularly damaging for LLL because many passengers use the airport to connect from one flight to another. The fewer connecting flights, the less attractive the services provided by the larger airlines.

(d) Purchasing this option gives the airline far more flexibility in terms of budgeting and planning. It need not commit itself to buying aircraft to meet its planned services until much later in the budgeting cycle, so it might avoid the cost of buying an aircraft that will prove to be surplus to requirements. Taking out this option will also make it more difficult for competitors to buy aircraft in order to compete. This is particularly beneficial when a new type of aircraft is developed, such as the Airbus A380, which captures the public’s attention.

The downside is that the airline has to commit a significant amount of cash in paying for the option. Quite apart from the cash flow implications, the whole sum may be lost if the airline decides not to proceed with the purchase. If the option is allowed to lapse then the shareholders may feel that their money has been wasted, despite the economic arguments that the €30m is a sunk cost. The directors might feel pressured into buying the aircraft anyway in order to escape criticism.

Exercising the option creates further risks. Presumably the airline will make assumptions about the likelihood of an option being exercised. There may be cases where more options are taken up than expected and that could delay the completion of the order. In that case, the airline will lose the benefits of buying the option and will have had a significant amount of cash tied up for no reason? There is also a risk that the manufacturer will fail before the airline has the opportunity to exercise the option. This is a very competitive industry and so the advance might be lost.

In the example given in the scenario, the options do not seem to guarantee anything other than an advanced delivery date. Even if the price is fixed, it is set in terms of $US and currency fluctuations will affect the final purchase cost in €.

That could be a problem because the airline is not certain that it will purchase the airliners and so it would not be appropriate to buy $ forward or hedge this potential position. It would, however, be worth considering the merits of buying an option to buy $ at a fixed price on or before the likely date that a final decision would be made to buy the airliner. This could prove expensive, although the large amounts involved in the transaction may mean that it would be a sensible precaution against currency risks.

Exercising the option means that the airline has now committed itself to purchasing a very expensive asset. Once the airline is committed to taking delivery of the airliner then it will be unable to sell it in response to any downturn in demand. The unexpected global recession and LLL’s difficulties in completing its third runway both indicate that an additional airliner could become surplus to requirements at very short notice.

P3 26 May 2009

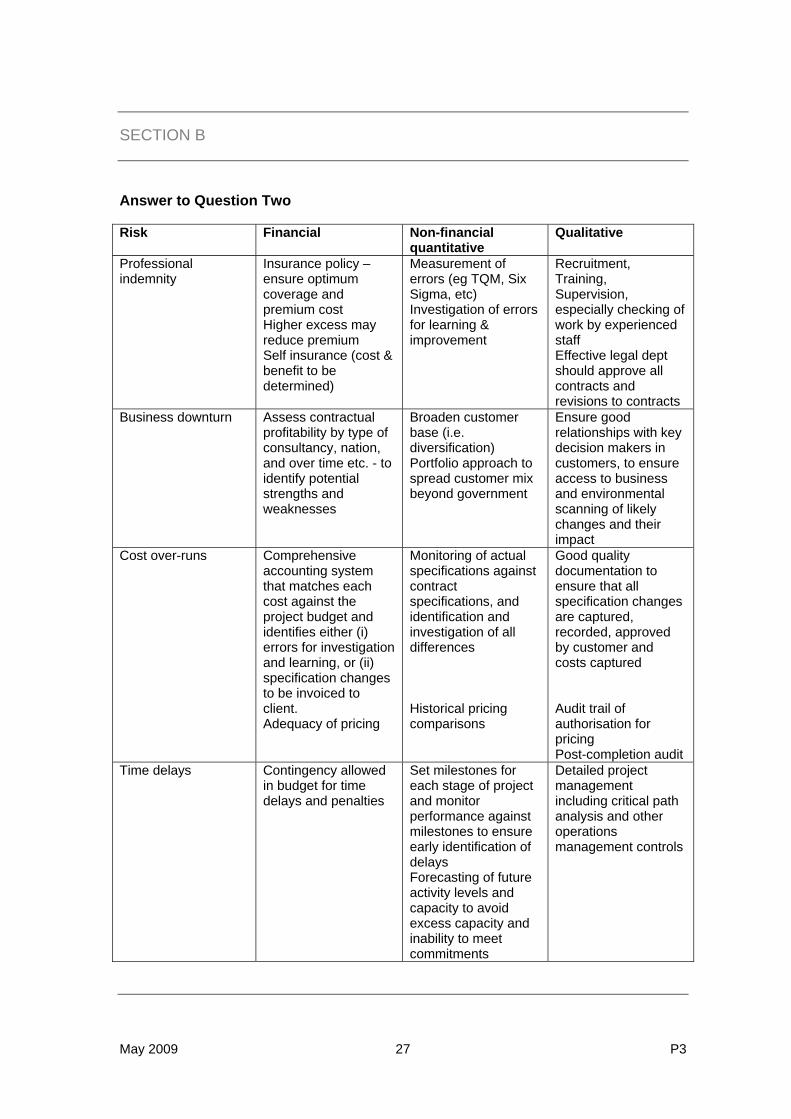

SECTION B Answer to Question Two Risk Financial Non-financial

quantitative Qualitative

Professional indemnity

Insurance policy – ensure optimum coverage and premium cost Higher excess may reduce premium Self insurance (cost & benefit to be determined)

Measurement of errors (eg TQM, Six Sigma, etc) Investigation of errors for learning & improvement

Recruitment, Training, Supervision, especially checking of work by experienced staff Effective legal dept should approve all contracts and revisions to contracts

Business downturn Assess contractual profitability by type of consultancy, nation, and over time etc. - to identify potential strengths and weaknesses

Broaden customer base (i.e. diversification) Portfolio approach to spread customer mix beyond government

Ensure good relationships with key decision makers in customers, to ensure access to business and environmental scanning of likely changes and their impact

Cost over-runs Comprehensive accounting system that matches each cost against the project budget and identifies either (i) errors for investigation and learning, or (ii) specification changes to be invoiced to client. Adequacy of pricing

Monitoring of actual specifications against contract specifications, and identification and investigation of all differences Historical pricing comparisons

Good quality documentation to ensure that all specification changes are captured, recorded, approved by customer and costs captured Audit trail of authorisation for pricing Post-completion audit

Time delays Contingency allowed in budget for time delays and penalties

Set milestones for each stage of project and monitor performance against milestones to ensure early identification of delays Forecasting of future activity levels and capacity to avoid excess capacity and inability to meet commitments

Detailed project management including critical path analysis and other operations management controls

May 2009 27 P3

Answer to Question Three

(a) Potential risks and recommended controls

Record Keeping CM operates on a cash basis, but the use of a cash box rather than an electronic till system, combined with no provision of receipts for customers, means that formal records of transactions are non-existent. The absence of information about the number and type of meals being served creates huge risks for the business, as it makes it very difficult, if not impossible, to measure profitability. In addition, it exposes the business owner to risks in relation to the provision of evidence in support of tax returns for the payment of income tax and sales taxes (such as VAT). More specifically, record keeping is inadequate in each of the following areas: (a) Customer spending on food versus drink. The suggestion is that drink sales carry a high

mark up of 60% on delivered cost, but no record is kept of what drinks are sold and so it is impossible to know whether this mark up is being achieved.

(b) There is no system for recording either the number of free meals provided or the extent to which staff take up the opportunity offered under the terms of employment of providing a friend with a free meal. This makes it impossible to measure the total number of meals served daily.

(c) The failure to use a till to record the takings means that there are no records of total customer numbers.

(d) No information is given about record keeping in respect of food stocks or orders, but it appears likely that controls in this area are also very poor. Physical as well are paper or electronic records of both food and drink stocks are required to control risks.

Poor record keeping creates a variety of risks. Overall, it makes it very difficult to evaluate the profitability of the business except at the most basic level of cash receipts less running costs. In order to manage the business more effectively, it would be helpful to have information to enable the profit from different product groups to be calculated and compared. For example, the profit from buffet food sales versus individually ordered meals, or from drinks versus food and alcoholic versus non alcoholic drink sales.

Suggested Controls 1. A simple EPOS system should be introduced that is specially designed for the hospitality

industry. EPOS, or Electronic Point of Sales systems can be used either as a stand alone till or for a broader range of purposes, depending upon individual business requirements. The primary purpose of such a system is to manage the collection of data through the use of a computer, and the user defines the type and volume of data to be collected. At its simplest, a cash register could be programmed with a list of codes to identify different meal types and drinks, for example, buffet or special order, beer, cola, sparkling water etc and the respective price of each item. Using a touch pad, the waiter could record customer orders and the resulting bill would then be automatically printed for each customer. Analysis of the resulting records would facilitate a better understanding of sales patterns on different days of the week and at different times of day. This information could then be used in planning staffing requirements and food preparation, as well as budgeting and profitability analysis.

2. Record keeping for free meals could be controlled via the introduction of an authorisation system that requires staff members to request and sign for their free meal(s) through the restaurant manager. Such a system will ensure that records are kept not only of the number of meals taken, but also the type of food that is consumed. When such records are combined with customer records, a full profile of meal types and consumption levels will be achievable. In the restaurant business, portion control is vital to ensuring profitability and without such records, it is impossible to monitor portion sizes.

3. Once records are available, performance and risk exposure can be monitored using measures such as:

P3 28 May 2009

• Average spend per customer on food and drink both separately and in combination

• Number of covers served per day

• Ratio of customers: members of staff

• Level of food wastage

Working capital management If staff are disillusioned and lack commitment to a business then they are possibly more tempted to commit fraud or steal cash. The use of a solely cash based system increases the risk of theft or fraud, which is compounded by the lack of record keeping. It would appear to be very easy for a member of staff to simply keep for themselves some of the cash received from a customer and with no checks in place, such theft would not be noticed, especially as the multi-skilling approach means that any number of staff could accept cash. The acceptance of cash only for restaurant sales risks losing considerable business from potential customers who prefer to pay by credit card. Stock losses could also easily take place, by taking either food or drinks from the restaurant without payment. This would extend to the fraudulent provision of additional free meals by staff to their friends which is also easy to achieve in the absence of record keeping. Suggested Controls 1. The restaurant could also invest in an EFTPOS (Electronic funds transfer point of sale)

system, which would enable customers to pay for their meals with either a debit or credit card instead of just cash. This would help to control the risk of theft of cash, as well as improving record keeping. EFTPOS records could be reconciled with the EPOS till records on a regular basis, to ensure that all sales are being formally recorded, and to monitor the ratio of cash to credit based sales. The use of EFTPOS could also potentially increase the number of customers because it offers an alternative payment facility.

2. To further improve controls and record keeping in relation to purchases, the EPOS system suggested above could be linked to inventory records for certain items such as bottles of drink, or high priced special order food items such as lobster. Linking inventory to sales records not only improves overall business control, but also further reduces the opportunity and incentive for fraud or theft.

Human resource policy The employment of only part-time staff creates a problem in relation to staff turnover, planning for absences, lack of consistency in service delivery, staff training, supervision, etc. The need for training and supervision is particularly important when staff members are multi-skilled and paid a minimum wage. Whilst this strategy is low cost it does risk providing poor customer service, bypassing health and safety and food hygiene practices, and theft of cash and/or stock, especially when outside training is not used and the owner/manager assumes all responsibility for training.

May 2009 29 P3

The risks that arise from existing staffing policies are as follows: (a) The majority of staff are on low rates of pay and employed on a part time basis. This means

that their reliability and commitment may be limited, so they may not be especially polite to customers, or may not worry about turning up late (or not at all) for a shift. The risk is that the business will lose customers as a result.

(b) Staff roles are not well defined, and this can lead to confusion about lines of responsibility. Who is supposed to be clearing tables or preparing food at any given time? A lack of segregation of duties makes it impossible to identify lines of responsibility and hence make staff accountable for errors or problems. At the same time it also makes it impossible to know whom to praise if a job has been done particularly well. The risk is that members of staff are unsure of their role and as a result they operate in a reactive way to problems, dealing with them after the event rather than taking the initiative to anticipate and plan for them. This can be bad for staff morale but most importantly it can reduce the overall level of service in the restaurant.

(c) There is minimal evidence of investment in staff training, which is assigned to the restaurant manager, as the only person with a nationally accredited catering and food hygiene qualification.

Lack of training in food preparation and basic hygiene creates risks in terms of health and safety. Breaches of such regulations could, in extreme circumstances, result in the restaurant being closed down. In addition, lack of training could also result in high levels of food wastage which would reduce profits. Lastly, poor training results in staff members who lack a real understanding of the business requirements, and are therefore more likely to be less efficient in their work. For example, a failure to train staff in how to allocate tables to customer groups of different sizes may lead to some customers being turned away as there is not the space to accommodate them. This translates into lost profit. The business appears to suffer from low staff morale which results in high staff turnover levels, and this exposes CM to potential theft and fraud risk (see above).

Suggested Controls 1. The simplest form of control would be to maintain a small core of fully trained and full time

staff, who could support the manager in providing a high level of reliable customer service. Their commitment to the business could be increased via the introduction of performance related pay, perhaps in the form of a share of the restaurant takings. This would encourage them to persuade customers to spend more and the better levels of customer service may also increase customer loyalty. Monitoring the level and frequency of customer return visits would be one way of measuring this.

2. The core of full time staff could be allocated specific responsibility for different aspects of the business, for example front of house manager; food ordering; food preparation etc. All part time staff should be allocated to a particular area and be answerable to a named full time staff member. In this way clear lines of responsibility are established for all aspects of the restaurant’s operations. The controls could be supplemented by performance measures linked to bonus systems, so that if planned targets are achieved in a given area, then all staff within that area receive monetary benefit. This will help to motivate the part time staff who receive relatively low wages.

3. A training budget should be established, and clear targets set for the proportion of staff that should be fully trained in certain skills. Salary levels should be adjusted to reward those who have received formal training.

4. Certain tasks, for example those which carry potential health and safety risks, should only be carried out by staff who have received the appropriate formal training. Penalties should be laid down and clearly imposed for any breach of such controls.

P3 30 May 2009

Examiner’s note: Under record keeping or working capital management, candidates may raise the following additional issues.

Business strategy and product mix The business is selling low priced buffet food within a restaurant that also sells individually prepared and priced meals. There is a danger that this mix is serving two different customer types which do not fit well together. The risks arising from the business strategy are as follows:

(a) It is not clear that the business actually has a clearly defined strategy, but if it does not, then

it will find it difficult to evaluate its own success and identify the risks that may impede the achievement of objectives.

(b) Risks are created by the lack of clarification of the target market. Is it students, families or

whom? Menus and the choice of foods cannot be refined to meet customer requirements if the designated customer group is not defined, and this may increase the risk of wastage.

(c) There is no information about how the buffet selection is planned, but careful choice of the

mix is vital to ensuring costs are effectively controlled.

Suggested Controls 1. The introduction of occasional customer satisfaction surveys, to maintain a check on which

dishes have either broad or narrow appeal.

2. Staff monitoring of customer patterns – estimated age, group sizes, type of customer to begin to develop a “typical” customer profile. This will ensure future strategies have a closer match to customer needs.

3. Detailed recording of costs and consumption levels of the dishes served in the buffet. Recipes can then be varied to cut costs if necessary.

4. Monitoring of wastage – if customers are leaving food on their plates, the range of choice may be too broad, and costs could be saved via some reduction in choices.

5. Regular staff and management meetings to ensure that strategies are known and shared.

(b) The manager of CM may choose not to implement controls because:

• he has considerable scope for control, and may not want to be constrained by systems and procedures, but prefers to control all aspects of the restaurant him/herself.

• he may wish to avoid taxation (VAT and income tax) and by having minimal records, may believe that he is less likely to be caught by a tax audit. Cash takings may be pocketed by the owner/manager without them being processed through the books of the business.

• he may not have either time or experience to implement controls and/or may be unwilling or unable to pay for someone to implement controls for the business.

• he may not have the funds or access to credit facilities to acquire EPOS or EFTPOS facilities.

• he may not be willing to make a long-term commitment to employ staff for personal reasons.

May 2009 31 P3

Answer to Question Four

(a) An information technology (IT) strategy is important because it defines the particular hardware, software and operating systems that an organisation needs to carry out its business. The hardware, software and operating systems must be capable of collecting, analysing and reporting the data required by the business, which represents a considerable investment.

The IT strategy is directly associated with the organisation’s information systems (IS) strategy which establishes the long-term information requirements of the organisation and provides an ‘umbrella’ for the different information technologies that may be used within the organisation (for example, separate systems may exist for accounting, customer relationship management, and supplier data). The IS strategy is linked closely to the organisation’s overall strategic plans. Within the umbrella of the IS strategy, IT strategy is important because:

• It will result in an appropriate budgetary allocation and budgetary control given the

high investment involved in IT purchasing. • information technology is critical to business success and the hardware, software

and operating systems acquired must be reliable as failure can affect the day to day conduct of the business as well as internal control.

• to build and retain competitive advantage, information technology is critical e.g. by satisfying customer demand better than competitors, by managing supply chains more effectively than competitors.

• It is important to maximise cost reductions in operations, e.g. the use of EDI technology to communicate between suppliers in the supply chain to achieve JIT deliveries and reduce inventory.

The IT strategy may define hardware requirements as mainframe computers, networked or stand-alone PCs. Appropriate operating systems may range from Windows to Linux, Unix or more sophisticated customised products. Software may be off-the-shelf products e.g. Microsoft Office or accounting packages (e.g. MYOB, Sage, Pegasus, Quicken); to customised management information systems or Enterprise Resource Planning (ERP) systems such as those by SAP or Oracle.

(b) Information is also an essential tool of management control but it is also a critical part of

the business process for many organisations (e.g. systems may be essential for customer order processing, purchasing, invoicing, supplier payments, etc.). A computer systems failure may therefore not only affect management information but may also prevent the business from operating. Information systems enable distributed processing, often PC-based using an intranet, which has led to the decentralisation of data processing and consequently to greater control risks. For example, transactions are often processed in real-time, with the production of documents (e.g. invoices, cheques) as a by-product of data entry. There is also a frequent need for quick systems change as a result of sophisticated programming tools and the availability of relational database systems and data warehousing. Program changes without adequate planning and testing can result in unforeseen impacts on information and business processes.

P3 32 May 2009

Risks in IS/IT systems include: • lack of availability of the system or application • erroneous data entry • unauthorised usage and fraudulent data entry • failure in the integrity of information managed by the application, such as

calculation accuracy, and completeness. • virus infection, • unlicensed use of software, • theft of hardware or software, • corruption of software, • implementation of an unapproved change • business interruption through fire or flood, etc.

and these risks may be exacerbated where customers are allowed access to an organisation’s systems, e.g. to order goods or services through the Internet. (c) (i)

Examiner’s note: Candidates were required to provide full explanations of three disadvantages of outsourcing IT. The following are examples of disadvantages which candidates could have chosen to explain. • The difficulty of agreeing on a service level agreement (SLA) that clearly identifies

the obligations of each party • The loss of flexibility and inability to quickly respond to changing circumstances as

the outsourced service is no longer under the control of the organisation • Risk of unsatisfactory quality and service, or even failure of supplier • Short-term cost-savings focus at expense of long-term strategy considerations • Ignoring unchanged overhead burden • Poor management of the changeover • Poor management of outsource supplier • Increasing costs of outsource provision and difficulty of changing the outsourced

supplier or of returning to an in-house provision. (ii) The risks associated with outsourcing IT can be controlled by

• Establishing a comprehensive information systems development process including

a feasibility study, systems design, testing and implementation • Applying project management techniques • Establishing oversight by a steering committee. • Carrying out a competitive bidding process • Building a long-term partnership or joint venture between both companies. • Retaining a small group of IT specialists in-house to monitor and work with the

outsource supplier. • Arranging an outsourcing contract such that a member of the supplier’s staff is

permanently located at the organisation’s premises to act as liaison between client and contractor.

May 2009 33 P3

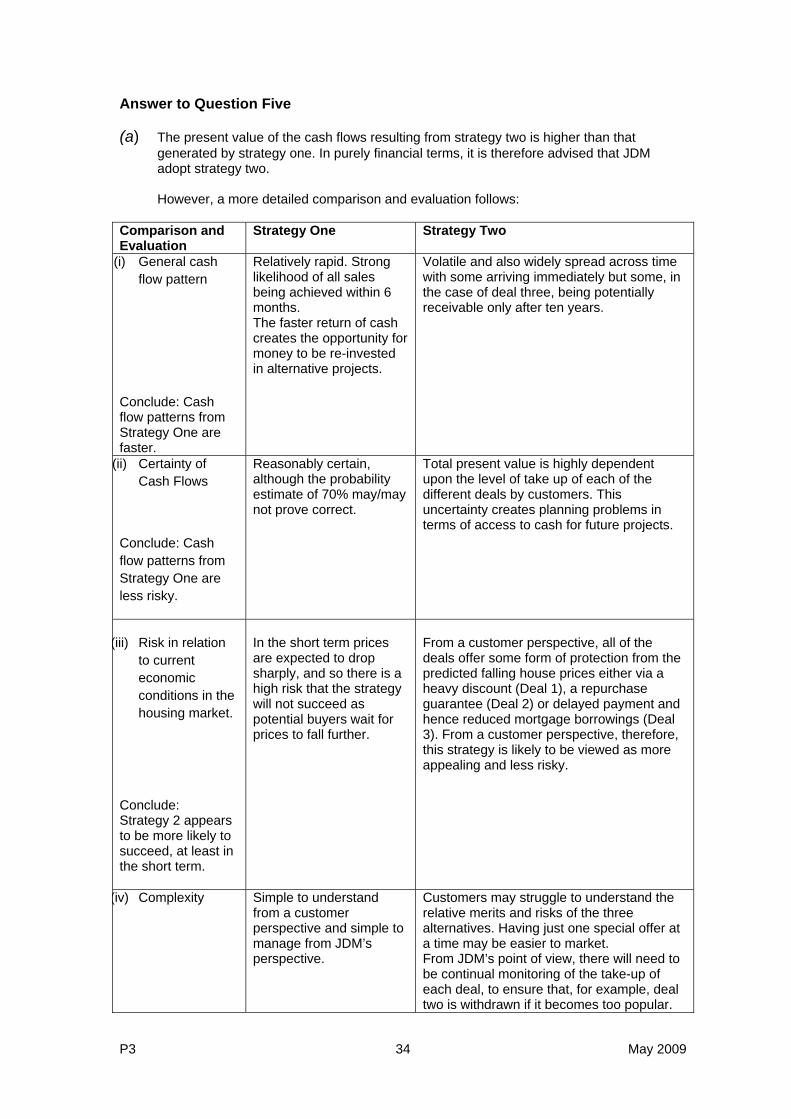

Answer to Question Five (a) The present value of the cash flows resulting from strategy two is higher than that

generated by strategy one. In purely financial terms, it is therefore advised that JDM adopt strategy two.

However, a more detailed comparison and evaluation follows:

Comparison and Evaluation

Strategy One Strategy Two

(i) General cash flow pattern

Conclude: Cash flow patterns from Strategy One are faster.

Relatively rapid. Strong likelihood of all sales being achieved within 6 months. The faster return of cash creates the opportunity for money to be re-invested in alternative projects.

Volatile and also widely spread across time with some arriving immediately but some, in the case of deal three, being potentially receivable only after ten years.

(ii) Certainty of Cash Flows

Conclude: Cash flow patterns from Strategy One are less risky.

Reasonably certain, although the probability estimate of 70% may/may not prove correct.

Total present value is highly dependent upon the level of take up of each of the different deals by customers. This uncertainty creates planning problems in terms of access to cash for future projects.

(iii) Risk in relation

to current economic conditions in the housing market.

Conclude: Strategy 2 appears to be more likely to succeed, at least in the short term.

In the short term prices are expected to drop sharply, and so there is a high risk that the strategy will not succeed as potential buyers wait for prices to fall further.

From a customer perspective, all of the deals offer some form of protection from the predicted falling house prices either via a heavy discount (Deal 1), a repurchase guarantee (Deal 2) or delayed payment and hence reduced mortgage borrowings (Deal 3). From a customer perspective, therefore, this strategy is likely to be viewed as more appealing and less risky.

(iv) Complexity

Simple to understand from a customer perspective and simple to manage from JDM’s perspective.

Customers may struggle to understand the relative merits and risks of the three alternatives. Having just one special offer at a time may be easier to market. From JDM’s point of view, there will need to be continual monitoring of the take-up of each deal, to ensure that, for example, deal two is withdrawn if it becomes too popular.

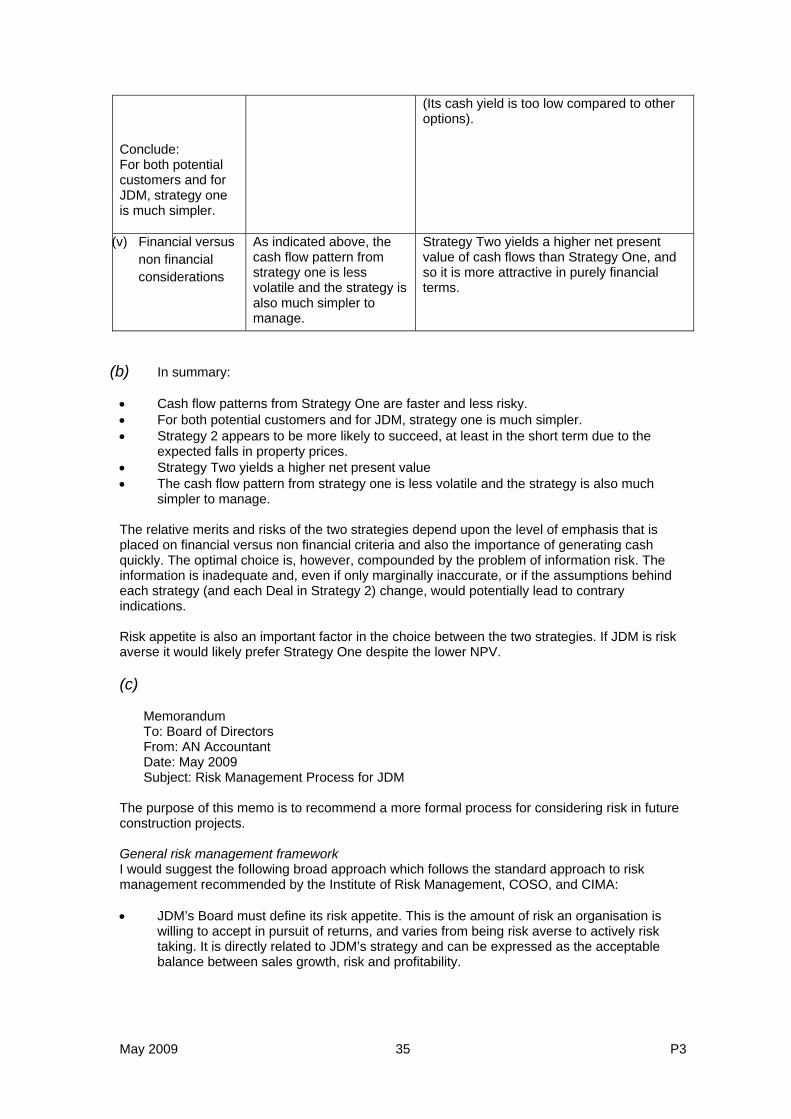

P3 34 May 2009

Conclude: For both potential customers and for JDM, strategy one is much simpler.

(Its cash yield is too low compared to other options).

(v) Financial versus non financial considerations

As indicated above, the cash flow pattern from strategy one is less volatile and the strategy is also much simpler to manage.

Strategy Two yields a higher net present value of cash flows than Strategy One, and so it is more attractive in purely financial terms.

(b) In summary:

• Cash flow patterns from Strategy One are faster and less risky. • For both potential customers and for JDM, strategy one is much simpler. • Strategy 2 appears to be more likely to succeed, at least in the short term due to the

expected falls in property prices. • Strategy Two yields a higher net present value • The cash flow pattern from strategy one is less volatile and the strategy is also much

simpler to manage. The relative merits and risks of the two strategies depend upon the level of emphasis that is placed on financial versus non financial criteria and also the importance of generating cash quickly. The optimal choice is, however, compounded by the problem of information risk. The information is inadequate and, even if only marginally inaccurate, or if the assumptions behind each strategy (and each Deal in Strategy 2) change, would potentially lead to contrary indications. Risk appetite is also an important factor in the choice between the two strategies. If JDM is risk averse it would likely prefer Strategy One despite the lower NPV. (c)

Memorandum To: Board of Directors From: AN Accountant Date: May 2009 Subject: Risk Management Process for JDM

The purpose of this memo is to recommend a more formal process for considering risk in future construction projects. General risk management framework I would suggest the following broad approach which follows the standard approach to risk management recommended by the Institute of Risk Management, COSO, and CIMA: • JDM’s Board must define its risk appetite. This is the amount of risk an organisation is

willing to accept in pursuit of returns, and varies from being risk averse to actively risk taking. It is directly related to JDM’s strategy and can be expressed as the acceptable balance between sales growth, risk and profitability.

May 2009 35 P3

• JDM should then establish a risk management policy which sets out its approach to and appetite for risk and its approach to risk management. The policy should also set out responsibilities for risk management throughout the organisation.

• A Chief Risk Officer (CRO) should be appointed to act as the champion of risk management throughout the organisation (although s/he may not have this as a full-time role). A Risk Management Group comprising the CRO and representative operational managers will advise the Board (and/or audit and risk committees) on risk management strategy and processes and will be the body which implements the Board’s strategies and policies.

• Risk assessment needs to take place on an ongoing basis. This comprises the analysis and evaluation of risk through processes of identification, description and estimation. This would involve assessing economic and market conditions, competition, likely customer demand, etc. The most common way of assessing risks is through the likelihood/impact matrix, or risk mapping. Risks should be recorded in a risk register.

• Risk evaluation is used to make decisions about the significance of risks to the organisation, given its risk appetite, and whether each specific risk should be accepted or treated.

• Each risk needs to be considered in terms of the management response, including risk control/mitigation activity, risk avoidance by abandoning the events that give rise to risks, risk transfer (e.g. hedging, insurance), or accepting a risk.

• Risk reporting should take place on a regular basis to review risks, review management responses to risks, take corrective action where necessary, and provide early warning of changes in risks or weaknesses in controls or other risk responses.

Conclusion Overall, I believe that a generally accepted risk management approach applied to each investment decision will reduce the risks faced by JDM and improve its ability to respond to those risks that do arise. Yours sincerely, AN Accountant.

P3 36 May 2009