Embed Size (px)

Citation preview

Investment products are: NOT FDIC INSURED – NO BANK GUARANTEE – MAY LOSE VALUE

May 7, 2014

BMO Economy and MarketsRetrospective and Perspective

BMO Economy and Markets: Retrospective and Perspective • May 7, 20141

Retrospective and PerspectiveApril – Post weather beating, economic data improves

Review

TOTAL RETURNS (as of 04/30/2014) April YTD 2014 2013

S&P 500® Index 0.74 2.56 32.38

STOXX Europe 600 Index 1.64 4.28 21.56

MSCI Emerging Markets Index 0.33 -0.10 -2.60

U.S. 10-Yr Treasury 0.88 4.29 -7.84

Sources: Bloomberg L.P., BMO Global Asset Management

April wiped some sweat off investors’ brows as weather did appear to be the culpritbehind weaker economic results in the first two to three months of 2014. April datatook some pressure off, as a number of key economic readings improved.U.S.: Perhaps the most encouraging numbers came from the two most recent jobsreports, as non-farm payrolls rose 203,000 in March and in April jumped to 288,000.There was also broad participation in hiring across sectors including constructionand manufacturing, not just the usual hospitality and retail components. Reportsalso indicated that earned income and hours worked inched higher.Outside of hiring, there were other positives of note. Manufacturing activity stayed inpositive territory, and durable goods orders and industrial production also improved.Companies like Boeing, Caterpillar and General Electric each posted profit andsales results that bettered expectations. Auto sales jumped back from a 15.3 millionannual rate to over 16 million.Two-thirds of S&P 500® Index companies that have reported earnings for the firstquarter exceeded expectations, even though 40% of S&P companies reported theirbusiness was negatively affected by weather.Housing continued to show a mixed bag of results and some metrics here may alsobe weather related. Existing home sales slowed for the third month in a row. But onthe other hand, building permits and housing starts improved. So stay tuned.With this economic reassurance, large cap stocks did well, but mid and small capstocks struggled. Biotech and social media really suffered; stocks may also havebeen spooked by the geopolitics of Ukraine/Russia, etc. Investment grade bondsand Treasuries did well for the month, as yields lowered.Europe: On balance, better news came out of Europe during the month. The EUreported both manufacturing and service results that continue to stay above aneutral reading of 50. Germany in particular came in with improved numbers forservices and manufacturing, including gains in industrial production, which nowstands at a three-year high. Retail sales also moved up nicely in Germany. TheUnited Kingdom continues to post improved results across both the retail andindustrial components of their economy, too.Perhaps one of the big shockers in Europe for the month was Greece, whichbrought a five-year sovereign bond to market; and it was priced to yield 4.95%, a farcry from the 37% rate peak of just a few years ago; and the bond was over-subscribed.

The European Central Bank kept rates unchanged at 0.25%. While on hold for sometime, they continue to watch and hope for sign of some increase in inflation andupticks in growth. In spite of the proximity to the Ukraine and the reliance on energysupplies from Russia which run through Ukraine, EU stocks ended up 1.6% for themonth.Emerging Markets (EM): The MSCI Emerging Market Index, which is dominated bythe BRIC countries, was up only 0.3% in April. While China reported better-than-expected GDP growth at 7.4% and retail sales grew 12% year-over-year, concernsremain regarding China’s long-term growth rate and the rapid expansion of credit thathas occurred.In Russia, the conflict over Ukraine clobbered Russian equities and the ruble. Theeconomy, which was slowing already, is now near recession. The central bankraised rates from 5.5% to 7.25% in an attempt to buttress the currency, etc. ─ afurther drag on EM performance.Brazil raised interest rates again and inflation finally started to ease a bit. In addition,their index of economic activity posted a modest gain. In India, national electionsloom; an effective pro-reform platform could be a tailwind for India.Japan: Value-added sales tax went from 5 to 8% on April 1. It will take a few monthsto judge its impact, but it’s a critical watch point.

Important forward-looking issues:• Progress on resolving Ukraine conflict• India’ s election results• Second quarter GDP in U.S. and interest rate direction

BMO Economy and Markets: Retrospective and Perspective • May 7, 20142

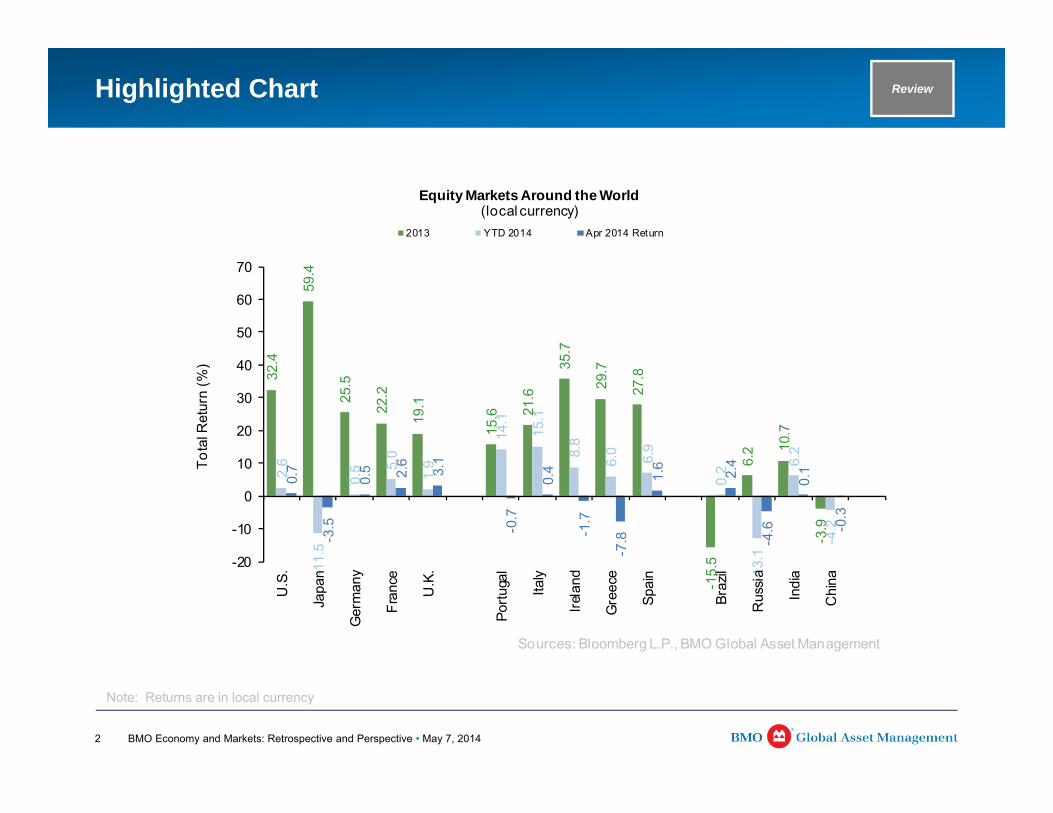

Highlighted Chart

32.4

59.4

25.5

22.2

19.1

15.6 21

.6

35.7

29.7

27.8

-15.

5

6.2 10

.7

-3.9

2.6

-11.

5

0.5 5.

0

1.9

14.1

15.1

8.8

6.0 6.9

0.2

-13.

1

6.2

-4.2

0.7

-3.5

0.5 2.6

3.1

-0.7

0.4

-1.7

-7.8

1.6 2.4

-4.6

0.1

-0.3

-20

-10

0

10

20

30

40

50

60

70U

.S.

Japa

n

Ger

man

y

Fran

ce

U.K

.

Portu

gal

Italy

Irela

nd

Gre

ece

Spai

n

Braz

il

Rus

sia

Indi

a

Chi

na

Tota

l Ret

urn

(%)

Equity Markets Around the World(local currency)

2013 YTD 2014 Apr 2014 Return

Sources: Bloomberg L.P., BMO Global Asset Management

Review

Note: Returns are in local currency

BMO Economy and Markets: Retrospective and Perspective • May 7, 20143

Highlighted items represent either the best- or worst-performing equity sector for the period. Total returns for periods of one year or more are annualized. MSCI indices performance is net of foreign taxes on dividends. Sources: Bloomberg L.P., FactSet, BMO Global Asset Management

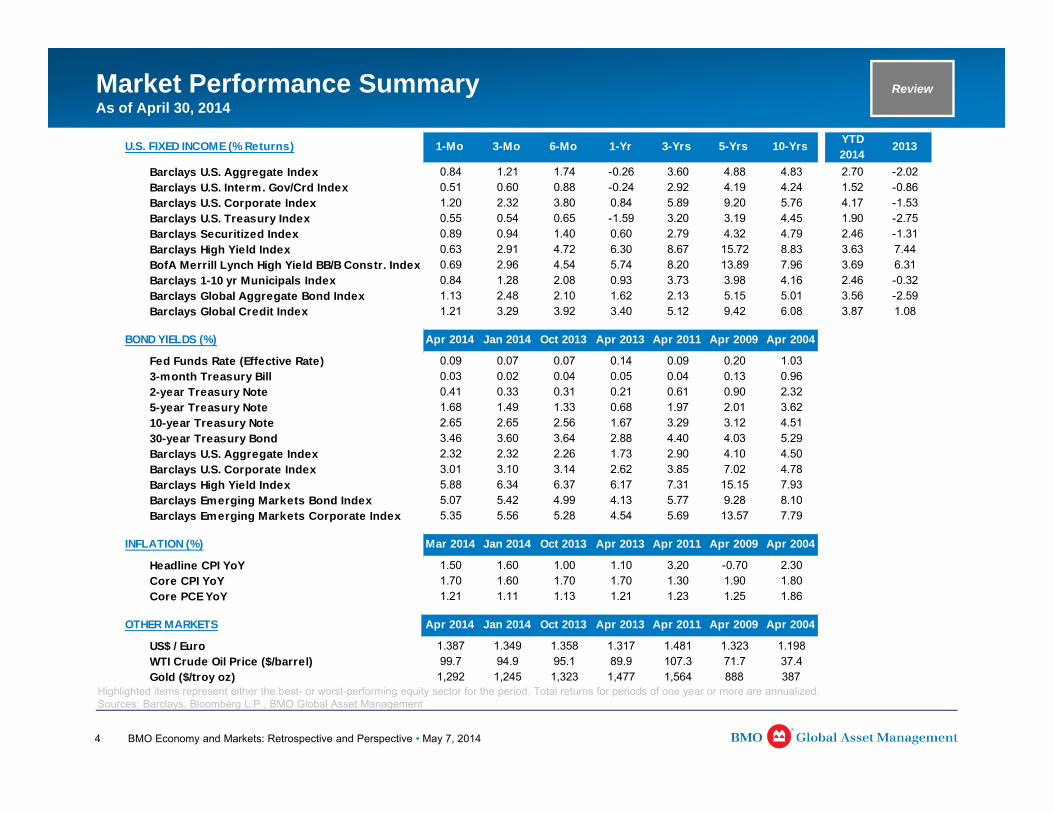

Market Performance SummaryAs of April 30, 2014

Review

EQUITIES (% Returns) 1-Mo 3-Mo 6-Mo 1-Yr 3-Yrs 5-Yrs 10-Yrs YTD 2014 2013

U.S. Large Cap EquitiesS&P 500® Index 0.74 6.23 8.35 20.43 13.82 19.13 7.67 2.56 32.38Dow Jones Industrial Average Index 0.87 6.22 7.90 14.44 11.85 18.32 7.68 0.72 29.65Russell 1000® Index 0.47 5.91 8.25 20.81 13.80 19.52 8.05 2.53 33.11Russell 1000® Growth Index 0.00 4.09 6.95 20.66 13.37 19.47 7.99 1.12 33.48Russell 1000® Value Index 0.95 7.83 9.61 20.90 14.16 19.52 7.95 4.00 32.53

U.S. Mid Cap EquitiesRussell Midcap® Index -0.57 4.98 7.76 21.25 13.05 21.87 10.40 2.93 34.76Russell Midcap® Growth Index -1.47 2.78 6.04 20.62 11.63 21.10 9.63 0.55 35.74Russell Midcap® Value Index 0.41 7.47 9.69 22.10 14.41 22.61 10.77 5.66 33.46

U.S. Small-Mid Cap Equities (SMID)Russell 2500TM Index -2.31 2.27 5.20 20.78 12.00 21.22 9.71 -0.06 36.80

U.S. Small Cap EquitiesRussell 2000® Index -3.88 -0.04 3.08 20.50 10.74 19.84 8.67 -2.80 38.82Russell 2000® Growth Index -5.13 -3.00 1.27 21.46 10.33 20.50 8.85 -4.67 43.30Russell 2000® Value Index -2.57 3.15 4.97 19.61 11.16 19.13 8.37 -0.84 34.52

International EquitiesMSCI ACWI ex USA Index (Devlp. & EM) 1.58 6.64 4.51 13.14 4.96 13.45 7.16 2.34 21.02MSCI EAFE Index (Developed Markets) 1.45 6.40 4.44 13.35 5.66 13.58 6.93 2.12 22.78MSCI European Monetary Union Index (in €) 0.99 6.37 6.10 21.45 6.52 11.06 5.32 3.93 23.40MSCI AC Asia Pacific Index -0.39 2.58 -2.55 -0.95 2.09 11.30 6.44 -2.12 11.97MSCI Emerging Markets Index 0.33 6.84 -2.98 -1.84 -3.74 11.08 11.09 -0.10 -2.60

Technology and Growth StocksNASDAQ Composite Index -1.96 0.56 5.66 25.26 14.24 20.53 9.16 -1.14 40.17

ALTERNATIVES (% Returns) 1-Mo 3-Mo 6-Mo 1-Yr 3-Yrs 5-Yrs 10-Yrs YTD 2014 2013

DJ UBS Commodity Index 2.44 9.27 10.07 3.17 -7.68 4.59 0.85 9.60 -9.52MSCI ACWI Commodity Producers Index 3.92 10.27 3.82 8.23 -6.76 6.33 7.03 3.40 0.63Wilshire U.S. REIT Index 3.41 8.78 6.67 -2.20 5.81 18.49 5.60 12.86 -1.74S&P Global REIT Index 3.64 9.32 6.32 -0.12 6.63 17.58 4.96 11.21 2.91S&P Global Infrastructure Index 1.96 10.01 9.91 14.00 8.19 16.23 12.12 9.18 15.03

BMO Economy and Markets: Retrospective and Perspective • May 7, 20144

Highlighted items represent either the best- or worst-performing equity sector for the period. Total returns for periods of one year or more are annualized. Sources: Barclays, Bloomberg L.P., BMO Global Asset Management

ReviewMarket Performance SummaryAs of April 30, 2014

U.S. FIXED INCOME (% Returns) 1-Mo 3-Mo 6-Mo 1-Yr 3-Yrs 5-Yrs 10-Yrs YTD 2014

2013

Barclays U.S. Aggregate Index 0.84 1.21 1.74 -0.26 3.60 4.88 4.83 2.70 -2.02Barclays U.S. Interm. Gov/Crd Index 0.51 0.60 0.88 -0.24 2.92 4.19 4.24 1.52 -0.86Barclays U.S. Corporate Index 1.20 2.32 3.80 0.84 5.89 9.20 5.76 4.17 -1.53Barclays U.S. Treasury Index 0.55 0.54 0.65 -1.59 3.20 3.19 4.45 1.90 -2.75Barclays Securitized Index 0.89 0.94 1.40 0.60 2.79 4.32 4.79 2.46 -1.31Barclays High Yield Index 0.63 2.91 4.72 6.30 8.67 15.72 8.83 3.63 7.44BofA Merrill Lynch High Yield BB/B Constr. Index 0.69 2.96 4.54 5.74 8.20 13.89 7.96 3.69 6.31Barclays 1-10 yr Municipals Index 0.84 1.28 2.08 0.93 3.73 3.98 4.16 2.46 -0.32Barclays Global Aggregate Bond Index 1.13 2.48 2.10 1.62 2.13 5.15 5.01 3.56 -2.59Barclays Global Credit Index 1.21 3.29 3.92 3.40 5.12 9.42 6.08 3.87 1.08

BOND YIELDS (%) Apr 2014 Jan 2014 Oct 2013 Apr 2013 Apr 2011 Apr 2009 Apr 2004

Fed Funds Rate (Effective Rate) 0.09 0.07 0.07 0.14 0.09 0.20 1.033-month Treasury Bill 0.03 0.02 0.04 0.05 0.04 0.13 0.962-year Treasury Note 0.41 0.33 0.31 0.21 0.61 0.90 2.325-year Treasury Note 1.68 1.49 1.33 0.68 1.97 2.01 3.6210-year Treasury Note 2.65 2.65 2.56 1.67 3.29 3.12 4.5130-year Treasury Bond 3.46 3.60 3.64 2.88 4.40 4.03 5.29Barclays U.S. Aggregate Index 2.32 2.32 2.26 1.73 2.90 4.10 4.50Barclays U.S. Corporate Index 3.01 3.10 3.14 2.62 3.85 7.02 4.78Barclays High Yield Index 5.88 6.34 6.37 6.17 7.31 15.15 7.93Barclays Emerging Markets Bond Index 5.07 5.42 4.99 4.13 5.77 9.28 8.10Barclays Emerging Markets Corporate Index 5.35 5.56 5.28 4.54 5.69 13.57 7.79

INFLATION (%) Mar 2014 Jan 2014 Oct 2013 Apr 2013 Apr 2011 Apr 2009 Apr 2004

Headline CPI YoY 1.50 1.60 1.00 1.10 3.20 -0.70 2.30Core CPI YoY 1.70 1.60 1.70 1.70 1.30 1.90 1.80Core PCE YoY 1.21 1.11 1.13 1.21 1.23 1.25 1.86

OTHER MARKETS Apr 2014 Jan 2014 Oct 2013 Apr 2013 Apr 2011 Apr 2009 Apr 2004

US$ / Euro 1.387 1.349 1.358 1.317 1.481 1.323 1.198WTI Crude Oil Price ($/barrel) 99.7 94.9 95.1 89.9 107.3 71.7 37.4Gold ($/troy oz) 1,292 1,245 1,323 1,477 1,564 888 387

BMO Economy and Markets: Retrospective and Perspective • May 7, 20145

0.1

2.0

-0.1

-0.8

-0.2

-0.8

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5

Real GDP QoQ Growth

Personal Consumption Contribution

Government Spending Contribution

Investment (ex. Housing) Contribution

Housing Investment Contribution

Net Exports Contribution

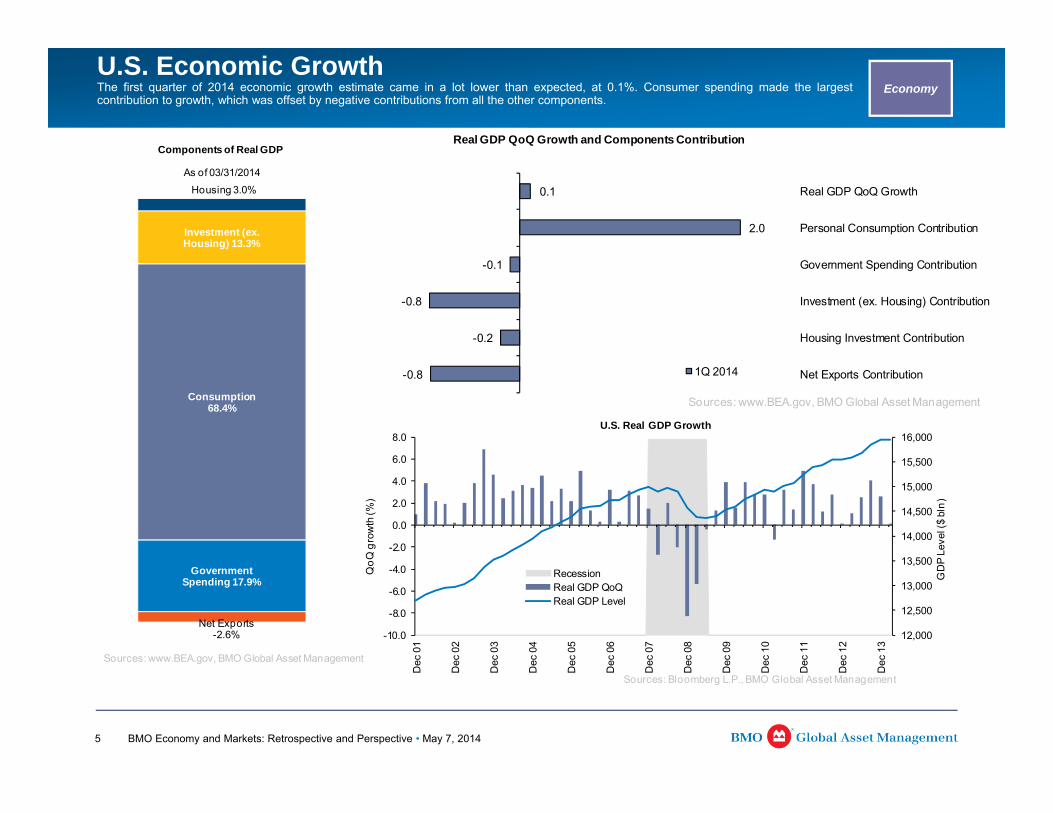

Real GDP QoQ Growth and Components Contribution

1Q 2014

Sources: www.BEA.gov, BMO Global Asset Management

Government Spending 17.9%

Consumption 68.4%

Investment (ex. Housing) 13.3%

Housing 3.0%

Net Exports-2.6%

Components of Real GDP

Sources: www.BEA.gov, BMO Global Asset Management

As of 03/31/2014

12,000

12,500

13,000

13,500

14,000

14,500

15,000

15,500

16,000

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

Dec

01

Dec

02

Dec

03

Dec

04

Dec

05

Dec

06

Dec

07

Dec

08

Dec

09

Dec

10

Dec

11

Dec

12

Dec

13

GD

P Le

vel (

$ bl

n)

QoQ

gro

wth

(%)

U.S. Real GDP Growth

RecessionReal GDP QoQReal GDP Level

Sources: Bloomberg L.P., BMO Global Asset Management

U.S. Economic GrowthThe first quarter of 2014 economic growth estimate came in a lot lower than expected, at 0.1%. Consumer spending made the largestcontribution to growth, which was offset by negative contributions from all the other components.

Economy

BMO Economy and Markets: Retrospective and Perspective • May 7, 20146

-10-9-8-7-6-5-4-3-2-10

-1,100

-900

-700

-500

-300

-100

100

300

500

700D

ec 0

6

Jun

07

Dec

07

Jun

08

Dec

08

Jun

09

Dec

09

Jun

10

Dec

10

Jun

11

Dec

11

Jun

12

Dec

12

Jun

13

Dec

13

Cum

ulat

ive

(mill

jobs

)

Mon

thly

(thou

sand

jobs

)

Job Gain/Losses

MonthlyCumulative

Sources: Bloomberg L.P., BMO Global Asset Management

5%

28%

15%

11%

10%

7%

5%

4%

3%

1%

1%

-2%

-3%

-4%

-6%

2%

6%

4%

3%

2%

2%

2%

2%

1%

1%

1%

0%

3%

0%

-1%

Total Non-Farm Payrolls

Natural Res./Mining

Professional and Business Services

Leisure and Hospitality

Education and Health Services

Transportation and Warehousing

Retail

Wholesale

Other Services

Manufacturing

Finance, Insurance, and Real Estate

Utilities

Construction

Govt Payrolls

Information

Payrolls Change by Industry

5-Yr Payroll Change

1-Yr Payroll Change

Sources: Bloomberg L.P., BMO Global Asset Management

As of 04/30/2014

250300

350400

450

500550

600650

700

2.02.53.03.54.04.55.05.56.06.57.0

Dec

06

Dec

07

Dec

08

Dec

09

Dec

10

Dec

11

Dec

12

Dec

13

Initi

al C

laim

s (4

wee

k av

g, in

thou

sand

s)

Con

tinui

ng C

laim

s (th

ousa

nds)

Jobless Claims

Continuing ClaimsInitial Jobless Claims

Sources: Bloomberg L.P., BMO Global Asset Management

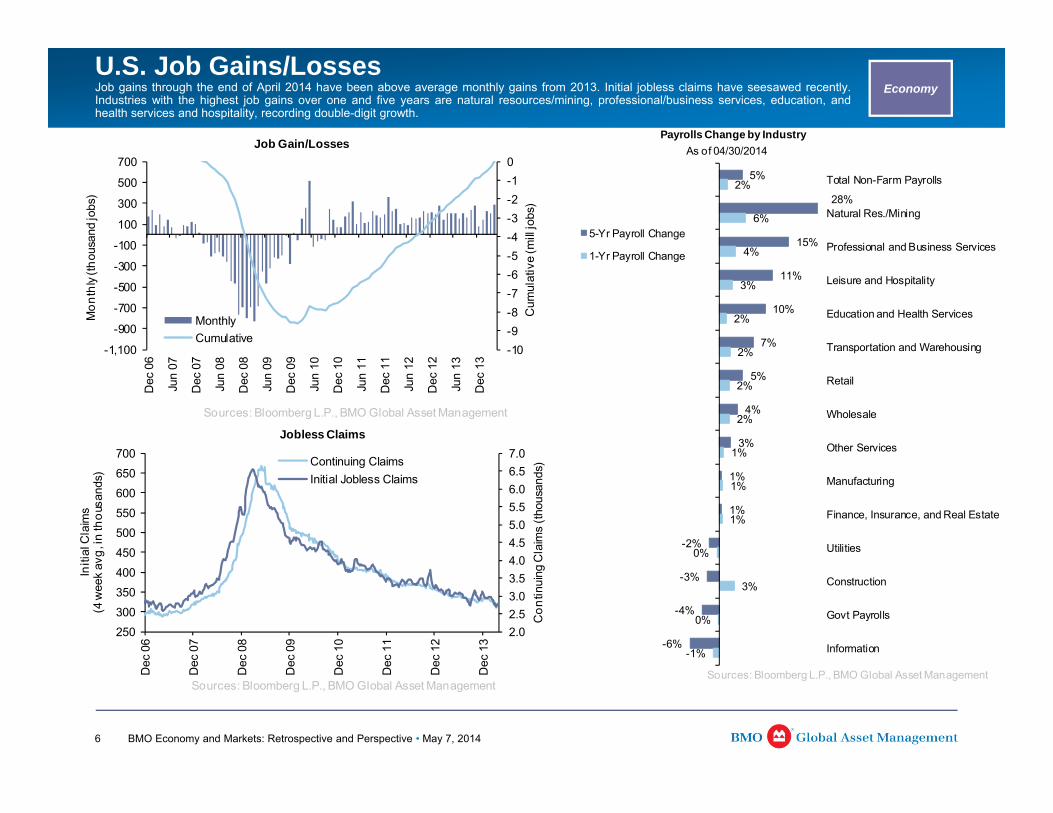

EconomyU.S. Job Gains/LossesJob gains through the end of April 2014 have been above average monthly gains from 2013. Initial jobless claims have seesawed recently.Industries with the highest job gains over one and five years are natural resources/mining, professional/business services, education, andhealth services and hospitality, recording double-digit growth.

BMO Economy and Markets: Retrospective and Perspective • May 7, 20147

-4.0

0.0

4.0

8.0

12.0

16.0

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Developed Countries CPI (YoY %)

World EuropeG10 Countries U.S.

Sources: Bloomberg L.P., BMO Global Asset Management

World Economic Growth and InflationYear-over-year Eurozone economic growth crossed into positive territory in fourth quarter 2013, after seven straight quarters of economiccontraction. China’s GDP growth in first quarter 2014 was 7.4%, slightly below the prior quarter growth of 7.7%. While world inflation has beendeclining slightly since the end of third quarter 2011, Japan, India and even China have seen higher inflation.

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

2006

2007

2008

2009

2010

2011

2012

2013

YoY

GD

P G

row

th (%

)

Real GDP Growth for Developed Countries

Eurozone Germany France Japan

Sources: Bloomberg L.P., BMO Global Asset Management

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

2006

2007

2008

2009

2010

2011

2012

2013

YoY

GD

P G

row

th (%

)

Real GDP Growth for BRIC Countries

Brazil Russia India China

Sources: Bloomberg L.P., BMO Global Asset Management

Economy

-4.0

0.0

4.0

8.0

12.0

16.0

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Emerging Markets CPI (YoY %)

WorldBRICU.S.ChinaIndia

Sources: Bloomberg L.P., BMO Global Asset Management

BMO Economy and Markets: Retrospective and Perspective • May 7, 20148

Total returns are based on Russell-style indicesperformance and include dividends. Graphs depictprice levels only. Sources: Bloomberg L.P., BMOGlobal Asset Management.

550

650

750

850

950

1,050

1,150

Dec 11 Mar 12 Jun 12 Sep 12 Dec 12 Mar 13 Jun 13 Sep 13 Dec 13 Mar 14

Inde

x Le

vel

Large Cap Stocks

Russell 1000® Index2012:

16.4% TR

2013 : 33.1% TR

Sources: Bloomberg L.P., BMO Global Asset Management

YTD 2014 : 2.5% TR

600

700

800

900

1,000

1,100

1,200

1,300

Dec 11 Mar 12 Jun 12 Sep 12 Dec 12 Mar 13 Jun 13 Sep 13 Dec 13 Mar 14

Inde

x Le

vel

Small Cap Stocks

Russell 2000® Index

Sources: Bloomberg L.P., BMO Global Asset Management

2012: 16.4% TR

2013 : 38.8% TR

YTD 2014 : -2.8% TR

YTD4/30/2014

Value Blend Grow th

Larg

e

4.0 2.5 1.1

Mid 5.7 2.9 0.5

Smal

l

-0.8 -2.8 -4.7

Total Returns (%)

2013Value Blend Grow th

Larg

e

32.5 33.1 33.5

Mid 33.5 34.8 35.7

Smal

l

34.5 38.8 43.3

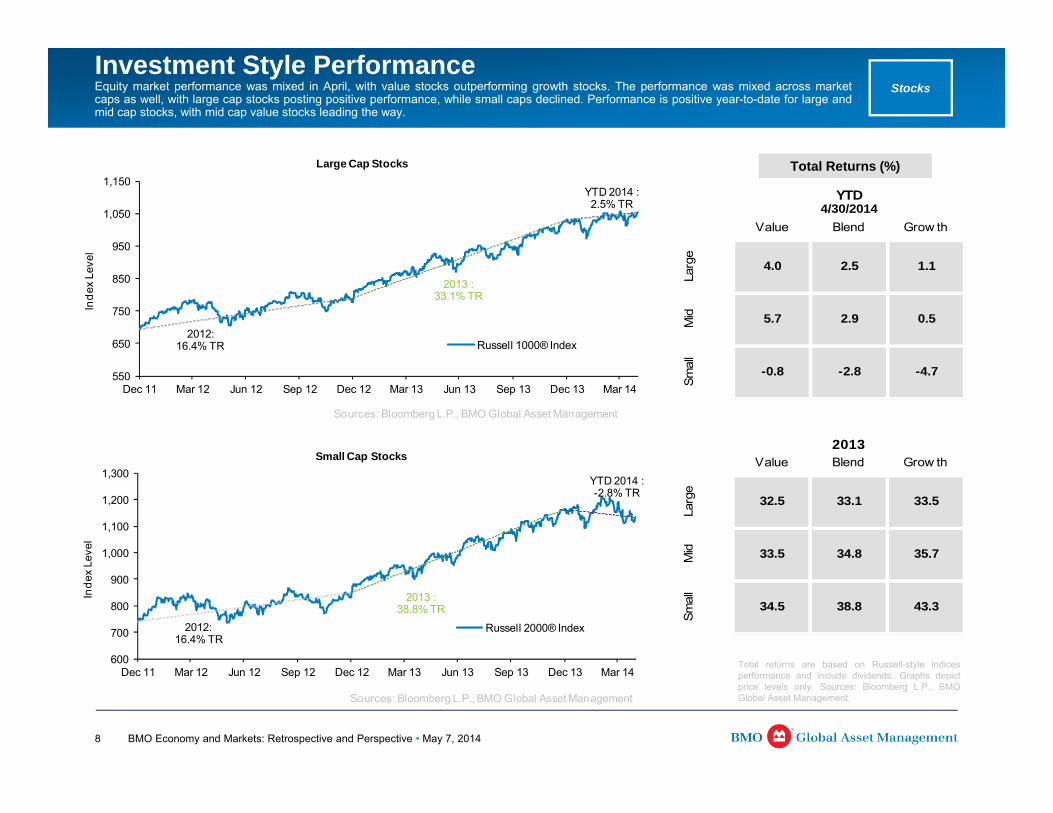

StocksInvestment Style PerformanceEquity market performance was mixed in April, with value stocks outperforming growth stocks. The performance was mixed across marketcaps as well, with large cap stocks posting positive performance, while small caps declined. Performance is positive year-to-date for large andmid cap stocks, with mid cap value stocks leading the way.

BMO Economy and Markets: Retrospective and Perspective • May 7, 20149

*Data begins in June 1988. Data based onRussell-style indices. Earnings are estimatedearnings for the next 12 months (NTM).Sources: FactSet, BMO Global AssetManagement.

0.30x

0.40x

0.50x

0.60x

0.70x

0.80x

0.90x

1.00x

1.10x

Jun 88 Jun 90 Jun 92 Jun 94 Jun 96 Jun 98 Jun 00 Jun 02 Jun 04 Jun 06 Jun 08 Jun 10 Jun 12

Valu

e PE

/ G

row

th P

E

Value vs. Growth Price to NTM Earnings

Russell 1000® Value PE / Russell 1000® Growth PE

Value / Growth Avg. since Jun '88 Growth Cheaper

Value Cheaper

Sources: FactSet, BMO Global Asset Management

0.40x

0.50x

0.60x

0.70x

0.80x

0.90x

1.00x

1.10x

1.20x

1.30x

1.40x

Jun 88 Jun 90 Jun 92 Jun 94 Jun 96 Jun 98 Jun 00 Jun 02 Jun 04 Jun 06 Jun 08 Jun 10 Jun 12

Smal

l Cap

PE

/ Lar

ge C

ap P

E .

Small vs. Large Price to NTM Earnings

Russell 2000® PE / Russell 1000® PE

Small / Large Avg. since Jun '88

Sources: FactSet, BMO Global Asset Management

Large Cap Cheaper

Small Cap Cheaper

Current P/E (Avg. P/E)

Value Blend Grow th

Larg

e 14.3 (13.5)

15.6 (15.9)

17.2 (19.7)

Mid 16.1

(13.8)17.3

(15.6)18.7

(19.5)

Smal

l 16.4 (13.7)

17.9 (15.5)

19.7 (18.0)

Current PE as % of Avg PE

Value Blend Grow th

Larg

e

106.3% 98.0% 87.2%

Mid 116.8% 110.9% 95.9%

Smal

l

119.1% 115.1% 109.6%

P/E vs. Long Term Average* As of 4/30/2014

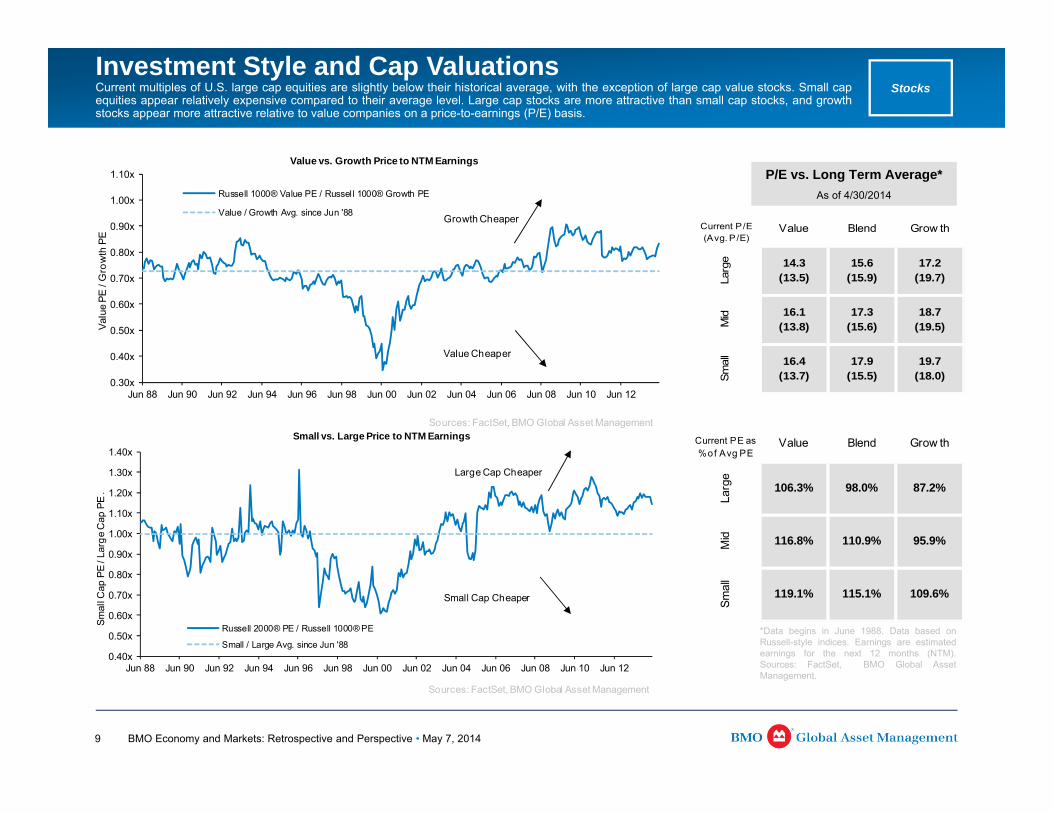

StocksInvestment Style and Cap ValuationsCurrent multiples of U.S. large cap equities are slightly below their historical average, with the exception of large cap value stocks. Small capequities appear relatively expensive compared to their average level. Large cap stocks are more attractive than small cap stocks, and growthstocks appear more attractive relative to value companies on a price-to-earnings (P/E) basis.

BMO Economy and Markets: Retrospective and Perspective • May 7, 201410

As of 04/30/2014 Russell Index Materials and

Processing Utilities Consumer Staples Energy Producer

Durables Health Care Consumer Discretionary Financials Technology

MTD 0.5% 0.5% 2.8% 2.6% 5.2% 1.2% -0.8% -1.2% -1.5% 0.1%

YTD 2014 2.5% 3.0% 8.9% 4.1% 6.7% 1.8% 5.1% -3.2% 0.7% 3.3%

2013 33.1% 25.2% 15.2% 27.7% 25.5% 41.9% 42.3% 41.9% 34.8% 27.6%

MTD -3.9% -2.6% -0.5% -0.2% 3.3% -3.3% -8.5% -3.9% -2.9% -7.0%

YTD 2014 -2.8% -1.9% 3.7% 2.8% 10.4% -2.2% -5.0% -7.2% -2.1% -6.6%

2013 38.8% 28.0% 21.8% 47.7% 35.0% 43.5% 51.7% 44.9% 31.4% 41.3%

LARG

E CA

P E

QUI

TIES

SMAL

L CA

P E

QUI

TIES

4.4%5.6%

7.9%

10.0%

11.3%

12.3%16.2%

18.1%

15.6%

Russell 1000® Index Composition

7.1%3.7%

3.9%

6.5%

14.7%

13.5%17.9%

24.1%

13.9%

Russell 2000® Index Composition

Sources: Bloomberg L.P., BMO Global Asset Management. Sector break-down based on Russell categories.

Materials and Processing

Utilities

Consumer Staples

Energy

Producer Durables

Health Care

Consumer Discretionary

Financials

Technology

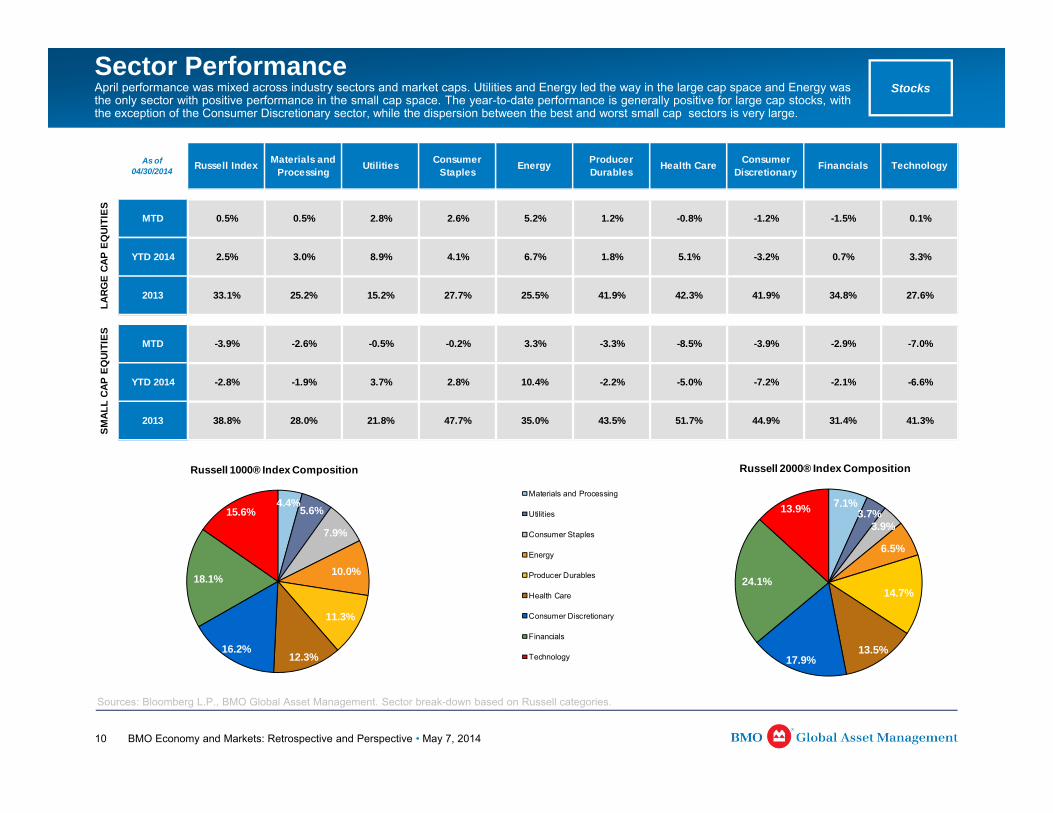

StocksSector PerformanceApril performance was mixed across industry sectors and market caps. Utilities and Energy led the way in the large cap space and Energy wasthe only sector with positive performance in the small cap space. The year-to-date performance is generally positive for large cap stocks, withthe exception of the Consumer Discretionary sector, while the dispersion between the best and worst small cap sectors is very large.

BMO Economy and Markets: Retrospective and Perspective • May 7, 201411

0.60.8

0.50.3 0.5

0.91.2 1.2

0.60.5

1.2

0.70.4

0.9 0.9

2.3

2.8 2.9

1.9

2.7

1.6

0.9

1.8

2.5

4.2 4.03.6

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50U.S. Treasury U.S. Agg. Agencies ABS CMBS MBS Corporates Non-Corp HY

Bon

ds T

otal

Ret

urns

(%) 1-Mo 3-Mo YTD (04/30/2014)

Sources: Barclays, BMO Global Asset Management

Bonds

23 17 14 1733 41 48

22NA

5235 30

69

25

135

195

261

40 37 33

83

9

113142

223

0

50

100

150

200

250

300

U.S. Treasury U.S. Agg. Agencies ABS CMBS MBS Corporates Non-Corp HYBon

ds E

xces

s R

etur

ns v

s. T

reas

ury

Bon

ds W

ith S

imila

r Dur

atio

n (b

ps)

1-Mo 3-Mo YTD (04/30/2014)

Sources: Barclays, BMO Global Asset Management

U.S. Bond Market PerformanceBond performance was positive in April and year-to-date due to tighter spreads and lower yields. Compared to U.S. Treasury bonds with similar durations, all bond sectors posted positive performance in April and year-to-date.

BMO Economy and Markets: Retrospective and Perspective • May 7, 201412

U.S. BondsU.S. Treasury yields declined slightly in April. The 10-year U.S. Treasury yield decreased 38 basis points (bps) in 2014 and posted a strong return of 4.29% year-to-date. The tax-exempt market continues to benefit from light new issuance supply and little investor selling activity. Demand remains strong as the taxable equivalent yield on municipal bonds looks especially attractive .

Bonds

2.132.88

3.76

5.16

3.29

4.14

5.22

7.17

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Aaa Aa A Baa

(%)

Total Returns of the Taxable and Non-Taxable Bonds

U.S. Aggregate Bond Index (Taxable)

Municipals Index (Non-Taxable)

Sources: Barclays, BMO Global Asset Management

YTD (04/30/2014)

300

400

500

600

700

800

900

1,000

100

150

200

250

300

350

400

Mar

10

Jun

10

Sep

10

Dec

10

Mar

11

Jun

11

Sep

11

Dec

11

Mar

12

Jun

12

Sep

12

Dec

12

Mar

13

Jun

13

Sep

13

Dec

13

Hig

h Yi

eld

OAS

(bps

)

Inve

stm

ent G

rade

OAS

(bps

)

Corporate Bonds OAS Level

CorporatesFinancialsHY

Sources: Barclays, BMO Global Asset Management

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

3 m

o6

mo

2 yr

5 yr

10 y

r

20 y

r

30 y

r

Yiel

d (%

)

AAA Municipals and Treasury Yield Curves

Municipals Curve on 04/30/2014

Treasury Curve on 04/30/2014

Sources: Bloomberg L.P., BMO Global Asset Management

0.0

1.5

3.0

4.5

6.0

Dec

05

Jun

06

Dec

06

Jun

07

Dec

07

Jun

08

Dec

08

Jun

09

Dec

09

Jun

10

Dec

10

Jun

11

Dec

11

Jun

12

Dec

12

Jun

13

Dec

13

(%)U.S. Treasury Yields

3-Mo T-Bill2-Yr Tsy Note10-Yr Tsy Note

Sources: Bloomberg L.P., BMO Global Asset Management

BMO Economy and Markets: Retrospective and Perspective • May 7, 201413

Alternative Assets

0

500

1,000

1,500

2,000

0

50

100

150

200

250

Dec

91

Dec

92

Dec

93

Dec

94

Dec

95

Dec

96

Dec

97

Dec

98

Dec

99

Dec

00

Dec

01

Dec

02

Dec

03

Dec

04

Dec

05

Dec

06

Dec

07

Dec

08

Dec

09

Dec

10

Dec

11

Dec

12

Dec

13

Stoc

k In

dex

Leve

l

Com

mod

ities

Inde

x Lev

ell

Commodities and Stocks

DJ UBS Commodity Index

S&P 500® Index

Sources: Bloomberg L.P., BMO Global Asset Management

As of 04/30/2014

DJ UBS Agriculture Subindex

DJ UBS Livestock Subindex

DJ UBS Grains Subindex

DJ UBS Energy Subindex

DJ UBS Precious Metals

Subindex

DJ UBS Industrial

Metals Subindex

DJ UBS Commodity

IndexS&P 500® Index

MTD 3.5 -1.6 3.2 3.0 -0.1 3.0 2.4 0.7

YTD 2014 20.6 14.5 19.8 7.3 5.3 -1.7 9.6 2.6

2013 -14.3 -3.6 -16.9 5.1 -30.8 -13.7 -9.5 32.4

Sources: Bloomberg L.P., BMO Global Asset Management

CommoditiesThe DJ UBS Commodity Index has outperformed the S&P 500® Index year-to-date and posted slightly positive returns in April, but performance was mixed across the sub-sectors. The decoupling trend against equities, which began in 2011, has continued.

BMO Economy and Markets: Retrospective and Perspective • May 7, 201414

0

500

1,000

1,500

2,000

0

50

100

150

200

250

300

Dec

99

Dec

00

Dec

01

Dec

02

Dec

03

Dec

04

Dec

05

Dec

06

Dec

07

Dec

08

Dec

09

Dec

10

Dec

11

Dec

12

Dec

13

Stoc

k In

dex

Leve

l

REI

T In

dex

Leve

l .

REITS and Stocks

Wilshire U.S. REIT Index

S&P 500® Index

Sources: Bloomberg L.P., BMO Global Asset Management

0

500

1,000

1,500

2,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Dec

99

Dec

00

Dec

01

Dec

02

Dec

03

Dec

04

Dec

05

Dec

06

Dec

07

Dec

08

Dec

09

Dec

10

Dec

11

Dec

12

Dec

13

Stoc

k In

dex

Leve

l

Infra

stru

ctur

e In

dex

Leve

l

Global Infrastructure and Stocks

S&P Global Infrastructure Index

S&P 500® Index

Sources: Bloomberg L.P., BMO Global Asset Management

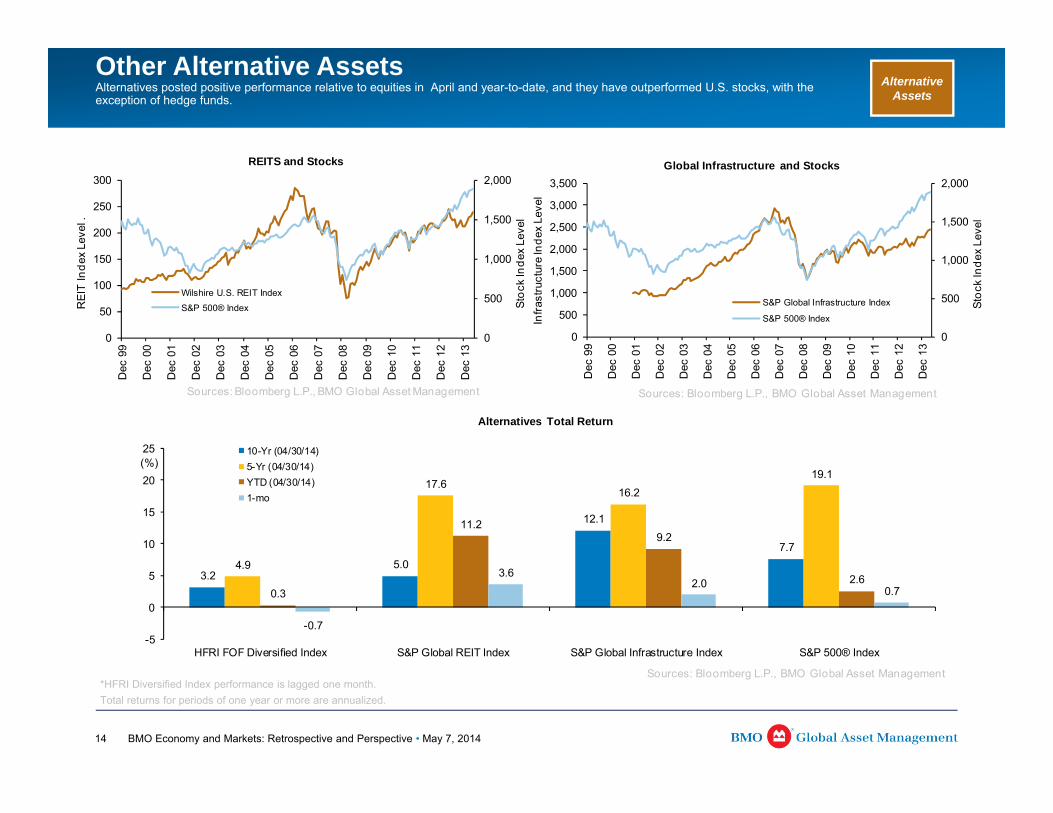

3.25.0

12.1

7.74.9

17.616.2

19.1

0.3

11.29.2

2.6

-0.7

3.62.0

0.7

-5

0

5

10

15

20

25

HFRI FOF Diversified Index S&P Global REIT Index S&P Global Infrastructure Index S&P 500® Index

(%)

Alternatives Total Return

10-Yr (04/30/14)5-Yr (04/30/14)YTD (04/30/14)1-mo

Sources: Bloomberg L.P., BMO Global Asset Management*HFRI Diversified Index performance is lagged one month. Total returns for periods of one year or more are annualized.

Alternative Assets

Other Alternative AssetsAlternatives posted positive performance relative to equities in April and year-to-date, and they have outperformed U.S. stocks, with the exception of hedge funds.

BMO Economy and Markets: Retrospective and Perspective • May 7, 201415

Sandy Lincoln Chief Market Strategist

Bob Decker, CFA Director, Quantitative Strategies

Irina Pacheco, CFA Vice President, Quantitative Strategies

Investment Strategy Group

BMO Economy and Markets: Retrospective and Perspective • May 7, 201416

Index Definitions

Equity IndicesS&P 500® IndexThe S&P 500® Index is an unmanaged index of large-cap common stocks.Dow Jones Industrial AverageThe Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on theNew York Stock Exchange and the Nasdaq.Russell 1000® IndexRussell 1000® Index consists of approximately 1,000 of the largest companies in the U.S. equitymarkets.Russell 1000® Growth IndexRussell 1000® Growth Index measures the performance of those Russell 1000 Companies with higherprice-to-book ratios and higher forecasted growth values.Russell 1000® Value IndexRussell 1000® Value Index measures the performance of those Russell 1000 Companies with lowerprice-to-book ratios and lower forecasted growth values.Russell Midcap® IndexRussell Midcap® Index measures the performance of the smallest 800 U.S. companies in the Russell1000 Index.Russell Midcap® Growth IndexRussell Midcap® Growth Index measures the performance of those Russell Midcap companies withhigher price-to-book ratios and higher forecasted growth values.Russell Midcap® Value IndexRussell Midcap® Value Index measures the performance of those Russell Midcap companies withlower price-to-book ratios and lower forecasted growth values.Russell 2500TM IndexThe Russell 2500TM Index measures the performance of the small to mid-cap segment of the U.S.equity universe. It is a subset of the Russell 3000® Index.Russell 2000® IndexRussell 2000® Index is an unmanaged index that measures the performance of the smallest 2000U.S. companies in the Russell 3000® Index.Russell 2000® Growth IndexRussell 2000® Growth Index measures the performance of those Russell 2000 Companies with higherprice-to-book ratios and higher forecasted growth values.Russell 2000® Value IndexRussell 2000® Value Index measures the performance of those Russell 2000 Companies with lowerprice-to-book ratios and lower forecasted growth values.MSCI ACWI ex USA IndexThe MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed tomeasure the equity market performance of developed and emerging markets.

Investments cannot be made in an index.

MSCI EAFE Index (Developed Markets)The MSCI EAFE Index Europe, Australasia, and Far East Index (EAFE) is a standard unmanagedforeign securities index representing major non-U.S. stock markets, as monitored by Morgan StanleyCapital International.MSCI European Monetary Union IndexThe MSCI EMU (European Economic and Monetary Union) Index is a free float-adjusted marketcapitalization weighted index that is designed to measure the equity market performance of countrieswithin EMU.MSCI AC Asia Pacific IndexThe MSCI AC Asia Pacific Index is a free float-adjusted market capitalization weighted index that isdesigned to measure the equity market performance of Asia and Pacific region.MSCI Emerging Markets IndexThe MSCI Emerging Markets Index is a market capitalization weighted index comprised of over 800companies representative of the market structure of the emerging countries in Europe, Latin America,Africa, Middle East and Asia. Prior to January 1, 2002, the returns of the MSCI Emerging MarketsIndex were presented before application of withholding taxes.NASDAQ Composite IndexThe NASDAQ Composite Index is a market-cap weighted index of the more than 3,000 commonequities listed on the Nasdaq stock exchange.STOXX Europe 600 IndexThe STOXX Europe Index represents 600 large, mid, and small capitalization companies across 18countries of the European Region.Deutsche Borse AG German Stock IndexThe Deutsche Borse AG German Stock Index (DAX) is a total return index of 30 selected Germanblue chip stocks traded on the Frankfurt Stock Exchange. The equities use free float shares in theindex calculation.CAC 40 IndexCAC 40 Index is a modified cap-weighted index of 40 companies on the Paris Bourse.Shanghai Stock IndexShanghai Stock Exchange Composite Index is a capitalization-weighted index. The index tracks thedaily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange.Hang Seng IndexThe Hang Seng Index is a free-float capitalization-weighted index of selection of companies from theStock Exchange of Hong Kong. The components of the index are divided into four sub-indexes:Commerce and Industry, Finance, Utilities, and Properties. The index was developed with a base levelof 100 as of July 31, 1964NIKKEI 225 IndexThe Nikkei-225 Stock Average is a price-weighted average of 225 top-rated Japanese companieslisted in the First Section of the Tokyo Stock Exchange.

BMO Economy and Markets: Retrospective and Perspective • May 7, 201417

Fixed Income IndicesBarclays U.S. Aggregate IndexBarclays U.S. Aggregate Bond Index is an unmanaged index that covers theU.S. investment-grade fixed-rate bond market, including government and creditsecurities, agency mortgage pass-through securities, asset-backed securitiesand commercial mortgage-based securities.Barclays U.S. Interm. Gov/Crd IndexBarclays Intermediate U.S. Government/Credit Index (Barclays Int Gov’t/Credit)is an unmanaged index comprised of government and corporate bonds ratedBBB or higher with maturities between 1-10 years.Barclays U.S. Corporate IndexThe Barclays U.S. Corporate Bond Index is designed to measure theperformance of the U.S. corporate bond market.Barclays U.S. Treasury IndexThe Barclays U.S. Treasury Index is an unmanaged index that includes a broadrange of U.S. Treasury obligations and is considered representative of U.S.Treasury bond performance overall.Barclays Securitized IndexThe Barclays U.S. Securitized Bond Index is an unmanaged index of asset-backed securities, collateralized mortgage-backed securities (ERISA-eligible),and fixed-rate mortgage-backed securities.Barclays High Yield IndexThe Barclays U.S. Corporate High-Yield Bond Index is an unmanaged indexthat covers the USD-denominated, non-investment-grade, fixed-rate, taxablecorporate bond market.BofA Merrill Lynch High Yield BB/B Constr. IndexThe BofA Merrill Lynch BB-B Global High Yield Index is a subset of The BofAMerrill Lynch Global High Yield Index including all securities rated BB1 throughB3, inclusive.

Barclays 1-10 yr Municipals IndexThe Barclays 1-10 Year Municipal Blend Index is a market value-weightedindex which covers the short and intermediate components of the BarclaysMunicipal Bond Index—an unmanaged, market value-weighted index whichcovers the U.S. investment-grade tax-exempt bond market.Investments cannot be made in an index.

Barclays Global Aggregate Bond IndexThe Barclays Global Aggregate Bond Index is an index of global government,government-related agencies, corporate and securitized fixed-incomeinvestments.Barclays Global Credit IndexThe Barclays Global Credit Index is the credit component of the Barclays GlobalAggregate Index, an index of global government, government-related agencies,corporate and securitized fixed-income investments.

Index Definitions

BMO Economy and Markets: Retrospective and Perspective • May 7, 201418

Alternative Investments IndicesDJ UBS Commodity IndexThe Dow Jones-UBS Commodity Index is composed of commodities traded onU.S. exchanges.MSCI ACWI Commodity Producers IndexThe MSCI ACWI Commodity Producers Index is a component of the broaderMSCI Commodity Producers Indices and covers large, mid and small capcompanies across 45 Developed and Emerging Markets.Wilshire US REIT IndexThe Wilshire US REIT Index measures U.S. publicly traded Real EstateInvestment Trusts. It is a subset of the Wilshire US Real Estate SecuritiesIndex.S&P Global REIT IndexThe S&P Global REIT Index measures the performance of real estateinvestment trusts in both developed and emerging markets.S&P Global Infrastructure IndexThe S&P Global Infrastructure Index provides liquid and tradable exposure to75 companies from around the world that represent the listed infrastructureuniverse including utilities, transportation and energy.

Other IndicesS&P/Case-Shiller 20-City IndexThe S&P/Case-Shiller 20-City Index is a composite index of the home priceindex for 20 major metropolitan statistical areas in the U.S.CPI IndexThe Consumer Price Index is a measure that examines the weighted average ofprices of a basket of consumer goods and services, such as transportation,food and medical care.HFRI FOF Diversified IndexThe Hedge Fund Research Diversified Index invests in a variety of strategiesamong multiple hedge funds managers. A fund in the HFRI FOF DiversifiedIndex tends to show minimal loss in down markets while achieving superiorreturns in up markets.Investments cannot be made in an index.

Index Definitions

BMO Economy and Markets: Retrospective and Perspective • May 7, 201419

Disclosures

For further information, please visit our website at www.bmogam.com

This is not intended to serve as a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect ourjudgment at this date and are subject to change. Information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy.This publication is prepared for general information only. This material does not constitute investment advice and is not intended as an endorsement of any specificinvestment. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive thisreport. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this reportand should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. Thevalue of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.Investments cannot be made in an index. Past performance is not necessarily a guide to future performance.

BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management, retirement, and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

Investment products are: NOT FDIC INSURED – NO BANK GUARANTEE – MAY LOSE VALUE

©2014 BMO Financial Corp.