Embed Size (px)

Citation preview

MB0050 –Research MethodologyQ1

a) Differentiate between nominal, ordinal, interval and ratio scales, with an example of each.

b) What are the purposes of measurement in social science research?Answer:a. There are four types of data that may be gathered in social research, each one adding

more to the next. Thus ordinal data is also nominal, and so on.NominalThe name 'Nominal' comes from the Latin nomen, meaning 'name' and nominal data are items which are differentiated by a simple naming system. The only thing a nominal scale does is to say that items being measured have something in common, although this may not be described. Nominal items may have numbers assigned to them. This may appear ordinal but is not -- these are used to simplify capture and referencing. Nominal items are usually categorical, in that they belong to a definable category, such as 'employees'.Example

The number pinned on a sports person.A set of countries.

OrdinalItems on an ordinal scale are set into some kind of order by their position on the scale. This may indicate such as temporal position, superiority, etc. The order of items is often defined by assigning numbers to them to show their relative position. Letters or other sequential symbols may also be used as appropriate. Ordinal items are usually categorical, in that they belong to a definable category, such as '1956 marathon runners'. You cannot do arithmetic with ordinal numbers -- they show sequence only.Example

The first, third and fifth person in a race.Pay bands in an organization, as denoted by A, B, C and D.

IntervalInterval data (also sometimes called integer) is measured along a scale in which each position is equidistant from one another. This allows for the distance between two pairs to be equivalent in some way. This is often used in psychological experiments that measure attributes along an arbitrary scale between two extremes. Interval data cannot be multiplied or divided.Example

My level of happiness, rated from 1 to 10.Temperature, in degrees Fahrenheit.

RatioIn a ratio scale, numbers can be compared as multiples of one another. Thus one person can be twice as tall as another person. Important also, the number zero has meaning.Thus the difference between a person of 35 and a person 38 is the same as the difference between people who are 12 and 15. A person can also have an age of zero.Ratio data can be multiplied and divided because not only is the difference between 1 and 2 the same as between 3 and 4, but also that 4 is twice as much as 2.Interval and ratio data measure quantities and hence are quantitative. Because they can be measured on a scale, they are also called scale data.

1

ExampleA person's weightThe number of pizzas I can eat before fainting

b. Purpose of measurement in social science.One of the primary purposes of classifying variables according to their level or scale of measurement is to facilitate the choice of a statistical test used to analyze the data. There are certain statistical analyses which are only meaningful for data which are measured at certain measurement scales. For example, it is generally inappropriate to compute the mean for Nominal variables. Suppose you had 20 subjects, 12 of which were male, and 8 of which were female. If you assigned males a value of '1' and females a value of '2', could you compute the mean sex of subjects in your sample? It is possible to compute a mean value, but how meaningful would that be? How would you interpret a mean sex of 1.4? When you are examining a Nominal variable such as sex, it is more appropriate to compute a statistic such as a percentage (60% of the sample was male).

When a research wishes to examine the relationship or association between two variables, there are also guidelines concerning which statistical tests are appropriate. For example, let's say a University administrator was interested in the relationship between student gender (a Nominal variable) and major field of study (another Nominal variable). In this case, the most appropriate measure of association between gender and major would be a Chi-Square test. Let's say our University administrator was interested in the relationship between undergraduate major and starting salary of students' first job after graduation. In this case, salary is not a Nominal variable; it is a ratio level variable. The appropriate test of association between undergraduate major and salary would be a one-way Analysis of Variance (ANOVA), to see if the mean starting salary is related to undergraduate major. Finally, suppose we were interested in the relationship between undergraduate grade point average and starting salary. In this case, both grade point average and starting salary are ratio level variables. Now, neither Chi-square nor ANOVA would be appropriate; instead, we would look at the relationship between these two variables using the Pearson correlation coefficient.

2

Q2

a) What are the sources from which one may be able to identify research problems?b) Why literature survey is important in research?

Answer:

a. Identifying research ProblemThis involves the identification of a general topic and formulating it into a specific research problem. It requires thorough understanding of the problem and rephrasing it in meaningful terms from an analytical point of view.Types of Research Projects

Those that relate to states of nature Those which relate to relationships between variables

In understanding the problem, it is helpful to discuss it with colleagues or experts in the field. It is also necessary to examine conceptual and empirical literature on the subject. After the literature review, the researcher is able to focus on the problem and phrase it in analytical or operational terms. The task of defining the research problem is of greatest importance in the entire research process. Being able to define the problem unambiguously helps the researcher in discriminating relevant data from irrelevant ones.Extensive literature reviewReview of literature is a systematic process that requires careful and perceptive reading and attention to detail. In the review of the literature, the researcher attempts to determine what others have learned about similar research problems. It is important in the following ways:

Specifically limiting and identifying the research problem and possible hypothesis or research questions i.e. sharpening the focus of the research.

Informing the researcher of what has already been done in the area. This helps to avoid exact duplication.

“If one had the literature and exercised enough patience and industry in reviewing available literature, it may well be that his problem has already been solved by someone somewhere some time ago and he will save himself the trouble.” Nwana (1982).

Providing insights into possible research designs and methods of conducting the research and interpreting the results.

Providing suggestions for possible modifications in the research to avoid unanticipated difficulties.

The library is the most likely physical location for the research literature. Within the library there is access to books, periodicals, technical reports and academic theses. Other sources are the Education Index and the Educational Resources information centre (ERIC). Computer-assisted searchers of literature have become very common today. They have the advantage of comprehensiveness and speed. They are also very cost-effective in terms of time and effort although access to some of the databases requires payment. Irrespective of the sources of the literature, ethics of research require that the source is acknowledged through a clear system of referencing.

b. Doing a literature survey before you begin your investigation enables you to take advantage of the unique human capacity to pass on detailed written information from one generation to another. Reading all the knowledge that's accumulated so far on the problem you want to study can be time-consuming and even tedious. But careful evaluation of that material helps make your investigation worthwhile by alerting you to knowledge already gained and problems already encountered in your areas of interest.

3

A literature survey amounts to reading available material on a given topic, analyzing and organizing findings, and producing a summary. There are many sources for literature reviews, including journals of general interest in each discipline, such as the American Political Science Review. There are also journals for specific topics such as the Leadership and Organization Development Journal. Governments publish great quantities of data on many topics. The United Nations and the United States Government Printing Office are two major sources. In addition, businesses and private organizations gather and publish information you might find useful. For certain problems you may want to search through popular or non-scholarly periodicals as well. While it's customary to include only data from sources that actually research the problem in a precise fashion, articles in more popular sources may provide interesting insight or orientations. Talking to knowledgeable people may also give you information that helps you formulate your problem.

Thoroughness is the key. Most libraries have staff trained in information retrieval who can help find sources and suggest strategies to review the literature. The Internet, of course, now allows easy access to limitless information on given topics. Thoroughness in your review means not only finding all current publications on a topic but locating earlier writing as well. There's no easy rule for how long ago literature was published on your topic. The time varies from problem to problem. A useful way to locate past as well as current writing is to begin with the most current sources likely to contain relevant material. Then, follow these authors' footnotes and bibliographies. At some point in this search you'll find the material is beginning to be only peripherally related to your current interest or that authors claim originality for their work.Of course, doing a good literature survey is easier when you know a great deal about the subject already. In such a case you'd probably be familiar with publications and even other people who do research in your area of interest. But for the novice, efficient use of library/Internet services and organizing how they check sources are especially important skills.Having located literature, keeping a checklist of useful information will help you read each source. You might ask yourself, particularly for research articles:

1. What was the exact problem studied?2. How were the topics of interest defined?3. What did the authors expect to find?4. How were things measured?5. What research did this author cite? Have you read it?6. Who were the subjects of study?7. What do the results show?8. Do the data presented agree with the written conclusions?9. What were the limitations of the study?

A thorough literature survey should demonstrate that you've carefully read and evaluated each article or book. Because research reports can be tedious and difficult to understand for new researchers, many tend to read others' conclusions or summaries and take the author's word that the data actually support the conclusions. Careful reading of both tables and text for awhile will convince you they don't always agree. Sometimes data are grossly misinterpreted in the text, but on other occasions authors are more subtle. Consider, for example, the following statements:

Fully 30 percent of the sample said they did not vote. Only 30 percent of the sample said they did not vote.

4

The percentage is the same, but the impression conveyed is decidedly different. Reading the actual data before accepting the author's conclusions will help prevent some of these errors of interpretation from creeping into your own research. It's important that after you finish your reading, you're able to write your literature survey in a way that's clear, organizing what you know about the content and methods used to study your problem. You may find it helpful to record information about each source on a separate card or piece of paper so that information can later be reshuffled, compared, and otherwise reorganized. Note in most journal articles that what probably began as a long literature survey is usually condensed on the first few pages of the research report, explaining previous research on the problem and how the current study will contribute. You, too, want to add to this growing body of knowledge we call social science by a creative summary of what's been accomplished by others as well as by your own research.

5

Q3a) What are the characteristics of a good research design? b) What are the components of a research design?

Answer:a)A research design is the arrangement of conditions for collection and analysis of data in a manner that aims to combine relevance to the research purpose with economy in procedure” Is the conceptual structure within which research is conducted; it constitutes the blueprint for the collection, measurement and analysis of data more explicitly:

1. It is a series of guide posts to keep one going in the right direction. 2. It reduces wastage of time and cost. 3. It encourages co-ordination and effective organization.4. It is a tentative plan which undergoes modifications, as circumstances demand, when

the study progresses, new aspects, new conditions and new relationships come to light and insight into the study deepens.

5. It has to be geared to the availability of data and the cooperation of the informants.6. It has also to be kept within the manageable limits

b. Components of Research Design It is important to be familiar with the important concepts relating to research design. They are:

1. Dependent and Independent variables: A magnitude that varies is known as a variable. The concept may assume different quantitative values, like height, weight, income, etc. Qualitative variables are not quantifiable in the strictest sense of objectivity. However, the qualitative phenomena may also be quantified in terms of the presence or absence of the attribute considered. Phenomena that assume different values quantitatively even in decimal points are known as „continuous variables‟. But, all variables need not be continuous. Values that can be expressed only in integer values are called „non-continuous variables‟. In statistical term, they are also known as „discrete variable‟. For example, age is a continuous variable; where as the number of children is a non-continuous variable. When changes in one variable depends upon the changes in one or more other variables, it is known as a dependent or endogenous variable, and the variables that cause the changes in the dependent variable are known as the independent or explanatory or exogenous variables. For example, if demand depends upon price, then demand is a dependent variable, while price is the independent variable.

2. Extraneous variable: The independent variables which are not directly related to the purpose of the study but affect the dependent variable are known as extraneous variables. For instance, assume that a researcher wants to test the hypothesis that there is relationship between children‟s school performance and their self-concepts, in which case the latter is an independent variable and the former, the dependent variable. In this context, intelligence may also influence the school performance. However, since it is not directly related to the purpose of the study undertaken by the researcher, it would be known as an extraneous variable. The influence caused by the extraneous variable on the dependent variable is technically called as an „experimental error‟. Therefore, a research study should always be framed in such a manner that the dependent variable completely influences the change in the independent variable and any other extraneous variable or variables.

3. Control: One of the most important features of a good research design is to minimize the effect of extraneous variable. Technically, the term control is used when a researcher designs the study in such a manner that it minimizes the effects of

6

extraneous independent variables. The term control is used in experimental research to reflect the restrain in experimental conditions.

4. Confounded relationship: The relationship between dependent and independent variables is said to be confounded by an extraneous variable, when the dependent variable is not free from its effects.

5. Research hypothesis: When a prediction or a hypothesized relationship is tested by adopting scientific methods, it is known as research hypothesis. The research hypothesis is a predictive statement which relates a dependent variable and an independent variable. Generally, a research hypothesis must consist of at least one dependent variable and one independent variable. Whereas, the relationships that are assumed but not be tested are predictive statements that are not to be objectively verified are not classified as research hypothesis.

6. Experimental and control groups: When a group is exposed to usual conditions in an experimental hypothesis-testing research, it is known as „control group‟. On the other hand, when the group is exposed to certain new or special condition, it is known as an „experimental group‟. In the afore-mentioned example, the Group A can be called a control group and the Group B an experimental one. If both the groups A and B are exposed to some special feature, then both the groups may be called as „experimental groups‟. A research design may include only the experimental group or the both experimental and control groups together.

7. Treatments: Treatments are referred to the different conditions to which the experimental and control groups are subject to. In the example considered, the two treatments are the parents with regular earnings and those with no regular earnings. Likewise, if a research study attempts to examine through an experiment regarding the comparative impacts of three different types of fertilizers on the yield of rice crop, then the three types of fertilizers would be treated as the three treatments.

8. Experiment: An experiment refers to the process of verifying the truth of a statistical hypothesis relating to a given research problem. For instance, experiment may be conducted to examine the yield of a certain new variety of rice crop developed. Further, Experiments may be categorized into two types namely, absolute experiment and comparative experiment. If a researcher wishes to determine the impact of a chemical fertilizer on the yield of a particular variety of rice crop, then it is known as absolute experiment. Meanwhile, if the researcher wishes to determine the impact of chemical fertilizer as compared to the impact of bio-fertilizer, then the experiment is known as a comparative experiment.

9. Experiment unit: Experimental units refer to the predetermined plots, characteristics or the blocks, to which the different treatments are applied. It is worth mentioning here that such experimental units must be selected with great caution.

10. Experimental and Non-Experimental Hypothesis Testing Research When the objective of a research is to test a research hypothesis, it is known as a hypothesis-testing research. Such research may be in the nature of experimental design or non-experimental design. A research in which the independent variable is manipulated is known as „experimental hypothesis-testing research‟, where as a research in which the independent variable is not manipulated is termed as „non-experimental hypothesis-testing research‟. E.g., assume that a researcher wants to examine whether family income influences the social attendance of a group of students, by calculating the coefficient of correlation between the two variables. Such an example is known as a non-experimental hypothesis-testing research, because the independent variable family income is not manipulated. Again assume that the researcher randomly selects 150 students from a group of students who pay their school fees regularly and them classifies them into tow sub-groups by randomly including 75 in Group A, whose parents have regular earning, and 75 in group B, whose parents do not have regular earning. And that at the end of the study, the researcher conducts a test on each group in order to examine the effects of regular

7

earnings of the parents on the school attendance of the student. Such a study is an example of experimental hypothesis-testing research, because in this particular study the independent variable regular earnings of the parents have been manipulated

8

Q4

a) Distinguish between Doubles sampling and multiphase sampling.b) What is replicated or interpenetrating sampling?

Answer:a. Double Sampling: Sample size calculations for a continuous outcome require specification of the anticipated variance; inaccurate specification can result in an underpowered or overpowered study. For this reason, adaptive methods whereby sample size is recalculated using the variance of a subsample have become increasingly popular. The first proposal of this type (Stein, 1945, Annals of Mathematical Statistics 16, 243-258) used all of the data to estimate the mean difference but only the first stage data to estimate the variance. Stein's procedure is not commonly used because many people perceive it as ignoring relevant data. This is especially problematic when the first stage sample size is small, as would be the case if the anticipated total sample size were small. A more naive approach uses in the denominator of the final test statistic the variance estimate based on all of the data. Applying the Helmert transformation, we show why this naive approach underestimates the true variance and how to construct an unbiased estimate that uses all of the data. We prove that the type I error rate of our procedure cannot exceed alpha.Double sampling refers to the subsection of the final sample form a pre-selected larger sample that provided information for improving the final selection. When the procedure is extended to more than two phases of selection, it is then, called multi-phase sampling. This is also known as sequential sampling, as sub-sampling is done from a main sample in phases. Double sampling or multiphase sampling is a compromise solution for a dilemma posed by undesirable extremes. “The statistics based on the sample of ‘n’ can be improved by using ancillary information from a wide base: but this is too costly to obtain from the entire population of N-elements. Instead, information is obtained from a larger preliminary sample n which includes the final sample n. extraneous Double sampling refers to the subsection of the final sample form a pre-selected larger sample that provided information for improving the final selection. When the procedure is extended to more than two phases of selection, it is then, called multi-phase sampling. This is also known as sequential sampling, as sub-sampling is done from a main sample in phases. Double sampling or multiphase sampling is a compromise solution for a dilemma posed by undesirable extremes. “The statistics based on the sample of ‘n’ can be improved by using ancillary information from a wide base: but this is too costly to obtain from the entire population of N elements. Instead, information is obtained from a larger preliminary sample n L which includes the final sample n.

Multistage sampling is a complex form of cluster sampling.

Advantages

cost and speed that the survey can be done in convenience of finding the survey sample normally more accurate than cluster sampling for the same size sample

Disadvantages

Is not as accurate as SRS if the sample is the same size More testing is difficult to do

Using all the sample elements in all the selected clusters may be prohibitively expensive or not necessary. Under these circumstances, multistage cluster sampling becomes useful.

9

Instead of using all the elements contained in the selected clusters, the researcher randomly selects elements from each cluster. Constructing the clusters is the first stage. Deciding what elements within the cluster to use is the second stage. The technique is used frequently when a complete list of all members of the population does not exist and is inappropriate.In some cases, several levels of cluster selection may be applied before the final sample elements are reached. For example, household surveys conducted by the Australian Bureau of Statistics begin by dividing metropolitan regions into 'collection districts', and selecting some of these collection districts (first stage). The selected collection districts are then divided into blocks, and blocks are chosen from within each selected collection district (second stage). Next, dwellings are listed within each selected block, and some of these dwellings are selected (third stage). This method means that it is not necessary to create a list of every dwelling in the region, only for selected blocks. In remote areas, an additional stage of clustering is used, in order to reduce travel requirements.Although cluster sampling and stratified sampling bear some superficial similarities, they are substantially different. In stratified sampling, a random sample is drawn from all the strata, where in cluster sampling only the selected clusters are studied, either in single stage or multi stage.

b. Replicated or Interpenetrating SamplingIt involves selection of a certain number of sub-samples rather than one full sample from a population. All the sub-samples should be drawn using the same sampling technique and each is a self-contained and adequate sample of the population. Replicated sampling can be used with any basic sampling technique: simple or stratified, single or multi-stage or single or multiphase sampling. It provides a simple means of calculating the sampling error. It is practical. The replicated samples can throw light on variable non-sampling errors. But disadvantage is that it limits the amount of stratification that can be employed.

10

Q5 a. How is secondary data useful to researcher? b. What are the criteria used for evaluation of secondary data?

Answer:a.Secondary Sources of Data These are sources containing data which have been collected and compiled for another purpose. The secondary sources consists of readily compendia and already compiled statistical statements and reports whose data may be used by researchers for their studies e.g., census reports , annual reports and financial statements of companies, Statistical statement, Reports of Government Departments, Annual reports of currency and finance published by the Reserve Bank of India, Statistical statements relating to Co-operatives and Regional Banks, published by the NABARD, Reports of the National sample survey Organization, Reports of trade associations, publications of international organizations such as UNO, IMF, World Bank, ILO, WHO, etc., Trade and Financial journals newspapers etc. Secondary sources consist of not only published records and reports, but also unpublished records. The latter category includes various records and registers maintained by the firms and organizations, e.g., accounting and financial records, personnel records, register of members, minutes of meetings, inventory records etc.

Features of Secondary Sources Though secondary sources are diverse and consist of all sorts of materials, they have certain common characteristics. First, they are readymade and readily available, and do not require the trouble of constructing tools and administering them. Second, they consist of data which a researcher has no original control over collection and classification. Both the form and the content of secondary sources are shaped by others. Clearly, this is a feature which can limit the research value of secondary sources.Finally, secondary sources are not limited in time and space. That is, the researcher using them need not have been present when and where they were gathered.

Use of Secondary Data The second data may be used in three ways by a researcher. First, some specific information from secondary sources may be used for reference purpose. For example, the general statistical information in the number of co-operative credit societies in the country, their coverage of villages, their capital structure, volume of business etc., may be taken from published reports and quoted as background information in a study on the evaluation of performance of cooperative credit societies in a selected district/state. Second, secondary data may be used as bench marks against which the findings of research may be tested, e.g., the findings of a local or regional survey may be compared with the national averages; the performance indicators of a particular bank may be tested against the corresponding indicators of the banking industry as a whole; and so on. Finally, secondary data may be used as the sole source of information for a research project. Such studies as securities Market Behaviour, Financial Analysis of companies, Trade in credit allocation in commercial banks, sociological studies on crimes, historical studies, and the like, depend primarily on secondary data. Year books, statistical reports of government departments, report of public organizations of Bureau of Public Enterprises, Censes Reports etc, serve as major data sources for such research studies.

11

Advantages of Secondary Data Secondary sources have some advantages:

1. Secondary data, if available can be secured quickly and cheaply. Once their source of documents and reports are located, collection of data is just matter of desk work. Even the tediousness of copying the data from the source can now be avoided, thanks to Xeroxing facilities.

2. Wider geographical area and longer reference period may be covered without much cost. Thus, the use of secondary data extends the researcher’s space and time reach.

3. The use of secondary data broadens the data base from which scientific generalizations can be made.

4. Environmental and cultural settings are required for the study. 5. The use of secondary data enables a researcher to verify the findings bases on

primary data. It readily meets the need for additional empirical support. The researcher need not wait the time when additional primary data can be collected.

b.Evaluation of Secondary Data :When a researcher wants to use secondary data for his research, he should evaluate them before deciding to use them. 1. Data Pertinence The first consideration in evaluation is to examine the pertinence of the available secondary data to the research problem under study. The following questions should be considered.

1. What are the definitions and classifications employed? 2. Are they consistent ? 3. What are the measurements of variables used? 4. What is the degree to which they conform to the requirements of our research? 5. What is the coverage of the secondary data in terms of topic and time?6. Does this coverage fit the needs of our research?

On the basis of above consideration, the pertinence of the secondary data to the research on hand should be determined, as a researcher who is imaginative and flexible may be able to redefine his research problem so as to make use of otherwise unusable available data.

2. Data Quality If the researcher is convinced about the available secondary data for his needs, the next step is to examine the quality of the data. The quality of data refers to their accuracy, reliability and completeness. The assurance and reliability of the available secondary data depends on the organization which collected them and the purpose for which they were collected. What is the authority and prestige of the organization? Is it well recognized? Is it noted for reliability? It is capable of collecting reliable data? Does it use trained and well qualified investigators? The answers to these questions determine the degree of confidence we can have in the data and their accuracy. It is important to go to the original source of the secondary data rather than to use an immediate source which has quoted from the original. Then only, the researcher can review the cautionary and other comments that were made in the original source.

3. Data Completeness The completeness refers to the actual coverage of the published data. This depends on the methodology and sampling design adopted by the original organization. Is the methodology sound? Is the sample size small or large? Is the sampling method appropriate? Answers to these questions may indicate the appropriateness and adequacy of the data for the problem under study. The question of possible bias should also be examined. Whether the purpose for which the original organization collected the data had a particular orientation? Has the study been made to promote the organization’s own interest? How the study was

12

conducted? These are important clues. The researcher must be on guard when the source does not report the methodology and sampling design. Then it is not possible to determine the adequacy of the secondary data for the researcher’s study.

13

Q6 What are the differences between observation and interviewing as methods of data collection? Give two specific examples of situations where either observation or interviewing would be more appropriate.Answer:

Observation vs interviewing as Methods of Data Collection

Collection of data is the most crucial part of any research project as the success or failure of the project is dependent upon the accuracy of the data. Use of wrong methods of data collection or any inaccuracy in collecting data can have significant impact on the results of a study and may lead to results that are not valid. There are many techniques of data collection along a continuum and observation and interviewing are two of the popular methods on this continuum that has quantitative methods at one end while qualitative methods at the other end. Though there are many similarities in these two methods and they serve the same basic purpose, there are differences that will be highlighted in this article.

ObservationObservation, as the name implies refers to situations where participants are observed from a safe distance and their activities are recorded minutely. It is a time consuming method of data collection as you may not get the desired conditions that are required for your research and you may have to wait till participants are in the situation you want them to be in. Classic examples of observation are wild life researchers who wait for the animals of birds to be in a natural habitat and behave in situations that they want to focus upon. As a method of data collection, observation has limitations but produces accurate results as participants are unaware of being closely inspected and behave naturally. Interviewing Interviewing is another great technique of data collection and it involves asking questions to get direct answers. These interviews could be either one to one, in the form of questionnaires, or the more recent form of asking opinions through internet. However, there are limitations of interviewing as participants may not come up with true or honest answers depending upon privacy level of the questions. Though they try to be honest, there is an element of lie in answers that can distort results of the project.Though both observation and interviewing are great techniques of data collection, they have their own strengths and weaknesses. It is important to keep in mind which one of the two will produce desired results before finalizing.

Observation vs Interviewing • Data collection is an integral part of any research and various techniques are employed for this purpose.• Observation requires precise analysis by the researcher and often produces most accurate results although it is very time consuming• Interviewing is easier but suffers from the fact that participants may not come up with honest replies. Interview format: Interviews take many different forms. It is a good idea to ask the organization in advance what format the interview will take.

14

Competency/criteria based interviews:

These are structured to reflect the competencies or qualities that an employer is seeking for a particular job, which will usually have been detailed in the job specification or advert. The interviewer is looking for evidence of your skills and may ask such things as: Give an example of a time you worked as part of a team to achieve a common goal.Technical interviews: If you have applied for a job or course that requires technical knowledge, it is likely that you will be asked technical questions or has a separate technical interview. Questions may focus on your final year project or on real or hypothetical technical problems. You should be prepared to prove yourself, but also to admit to what you do not know and stress that you are keen to learn. Do not worry if you do not know the exact answer - interviewers are interested in your thought process and logic. The Screening Interview: Companies use screening tools to ensure that candidates meet minimum qualification requirements. Computer programs are among the tools used to weed out unqualified candidates. (This is why you need a digital resume that is screening-friendly. See our resume centre for help.) Sometimes human professionals are the gatekeepers. Screening interviewers often have honed skills to determine whether there is anything that might disqualify you for the position. Remember they do not need to know whether you are the best fit for the position, only whether you are not a match. For this reason, screeners tend to dig for dirt. Screeners will hone in on gaps in your employment history or pieces of information that look inconsistent. They also will want to know from the outset whether you will be too expensive for the company. The Informational Interview: On the opposite end of the stress spectrum from screening interviews is the informational interview. A meeting that you initiate, the informational interview is underutilized by job-seekers who might otherwise consider themselves savvy to the merits of networking. Jobseekers ostensibly secure informational meetings in order to seek the advice of someone in their current or desired field as well as to gain further references to people who can lend insight. Employers that like to stay apprised of available talent even when they do not have current job openings, are often open to informational interviews, especially if they like to share their knowledge, feel flattered by your interest, or esteem the mutual friend that connected you to them. During an informational interview, the jobseeker and employer exchange information and get to know one another better without reference to specific job opening.

15

MB0051 – Legal Aspects of Business

Q.1 Distinguish between fraud and misrepresentation. Answer:

Meaning of fraud:Fraud means and includes any of the following acts committed by a party to a contractwith an intent to deceive the other party thereto or to induce him to enter into a contract: (i) the suggestion as a fact of that which is not true by one who does not believe it to be true; (ii) active concealment of a fact by one having knowledge or belief of the fact; (iii)promise made without any intention of performing it; (iv) any other act fitted to deceive;(v) any such act or omission as the law specifically declares to be fraudulent.

Meaning of misrepresentation:Misrepresentation is also known as simple misrepresentation whereas fraud is known as fraudulent misrepresentation. Like fraud, misrepresentation is an incorrect or falsestatement but the falsity or inaccuracy is not due to any desire to deceive or defraud theother party. Such a statement is made innocently. The party making it believes it to betrue. In this way, fraud is different from misrepresentation.

Difference between fraud and misinterpretation:- In misrepresentation the person making the false statement believes it to be true.

In fraud the false statement is person who knows that it is false or he does not care to know whether it is true or false.

There is no intention to deceive the other party when there is misrepresentation of fact. The very purpose of the fraud is to deceive the other party to the contract.

Misrepresentation renders the contract voidable at the option of the party whoseconsent was obtained by misrepresentation. In the case of fraud the contract isvoidable It also gives rise to an independent action in tort for damages.

Misrepresentation is not an offence under Indian penal code and hence not punishable. Fraud, In certain cases is a punishable offence under Indian penal code.

Generally, silence is not fraud except where there is a duty to speak or the relations between parties is fiduciary. Under no circumstances can silence be considered as misrepresentation.

The party complaining of misrepresentation can’t avoid the contract if he had themeans to discover the truth with ordinary deligance. But in the case of fraud, Theparty making a false statement cannot say that the other party had the means todiscover the truth with ordinary deligance.

16

Q.2 What are the remedies for breach of contract.Answer:

Remedies for Breach of ContractWhen someone breaches a contract, the other party is no longer obligated to keep its end of the bargain. From there, that party may proceed in several ways: (i) the other party may urge the breaching party to reconsider the breach; (ii) if it is a contract with a merchant, the other party may get help from consumers’ associations; (iii) the other party may bring the breaching party to an agency for alternative dispute resolution; (iv) the other party may sue for damages; or (v) the other party may sue for other remedies.

Rescission of the contract: When a breach of contract is committed by one party, the other party may treat the contract as rescinded. In such a case the aggrieved party is freed from all his obligations under the contract.

Damages: Another relief or remedy available to the promisee in the event of a breach of promise by the promisor is to claim damages or loss arising to him there from. Damages under Sec.75 are awarded according to certain rules as laid down in Secs.73-74. Sec.73 contains three important rules: (i) Compensation as general damages will be awarded only for those losses that directly and naturally result from the breach of the contract. (ii) Compensation for losses indirectly caused by breach may be paid as special damages if the party in breach had knowledge that such losses would also follow from such act of breach. (iii) The aggrieved party is required to take reasonable steps to keep his losses to the minimum.

The most common remedy for breach of contracts: The usual remedy for breach of contracts is suit for damages. The main kinds of damages awarded in a contract suit are ordinary damages. This is the amount of money it would take to put the aggrieved party in as good a position as if there had not been a breach of contract. The idea is to compensate the aggrieved party for the loss he has suffered as a result of the breach of the contract.

In addition to the rights of a seller against goods provided in Secs.47 to 54, the seller has the following remedies against the buyer personally. (i) suit for price (Sec.55); (ii) damages for non-acceptance of goods (Sec.56); (iii) suit for interest (Sec.56).

Suit for price (Sec.55): Where under a contract of sale the property in the goods has passed to the buyer and the buyer wrongfully neglects or refuses to pay the price, the seller can sue the buyer for the price of the goods. Where the property in goods has not passed to the buyer, as a rule, the seller cannot file a suit for the price; his only remedy is to claim damages.

Suit for damages for non-acceptance (Sec.56): Where the buyer wrongfully neglects or refuses to accept and pay for the goods, the seller may sue him for damages for non-acceptance. Where the property in the goods has not passed to the buyer and the price was not payable without passing of property, the seller can only sue for damages and not for the price. The amount of damages is to be determined in accordance with the provisions laid down in Sec.73 of the Indian Contract Act, 1872. Thus, where there is an available market for the goods prima facie, the difference between the market price and the contract price can be recovered.

17

Suit for interest (Sec.61): When under a contract of sale, the seller tenders the goods to the buyer and the buyer wrongfully refuses or neglects to accept and pay the price, the seller has a further right to claim interest on the amount of the price. In the absence of a contract to the contrary, the court may award interest at such rate as it thinks fit on the amount of the price. The interest may be calculated from the date of the tender of the goods or from the date on which the price was payable. It is obvious that the unpaid seller can claim interest only when he can recover the price, i.e., if the seller’s remedy is to claim damages only, then he cannot claim interest.

Buyer’s remedies against seller: The buyer has the following rights against the seller for breach of contract: (i) damages for non-delivery (Sec.57); (ii) right of recovery of the price; (iii) specific performance (Sec.58); (iv) suit for breach of condition; (v) suit for breach of warranty (Sec.59); (vi) anticipatory breach (Sec.60); (vii) recovery of interest (Sec.61).)

18

Q.3 Distinguish between indemnity and guarantee.Answer:

Distinction between a contract of guarantee and a contract of indemnity. L.C. Mather in his book “Securities Acceptable to the Lending Banker” has very briefly, but excellently, brought out the distinction between indemnity and guarantee by the following illustration. A contract in which A says to B, ‘If you lend £20 to C, I will see that your money comes back’ is an indemnity. On the other hand undertaking in these words, “If you lend £20 to C and he does not pay you, I will is a guarantee. Thus, in a contract of indemnity, there are only two parties, indemnifier and indemnified. In case of a guarantee, on the other hand, there are three parties, the ‘principal debtor’, the ‘creditor’ and the ‘surety’. Other points of difference are:

1. The liability of a promissory is primary and independent in a contract of indemnity. In a contract of guarantee, the liability of the surety is secondary, the primary liability being that of the principal debtor.

2. In the case of guarantee, there is an existing debt or obligation, the performance of which is guaranteed by the surety. In case of indemnity the possibility of any loss happening is a contingency against which the indemnifier undertakes to indemnify.

3. In a contract of guarantee, after discharging the debt, the surety is entitled to proceed against the principal debtor in his own name while in case of indemnity, the indemnifier cannot proceed against third parties in his own name, unless there is an assignment in his favour.

19

Q.4 What is the distinction between cheque and bill of exchange.Answer:

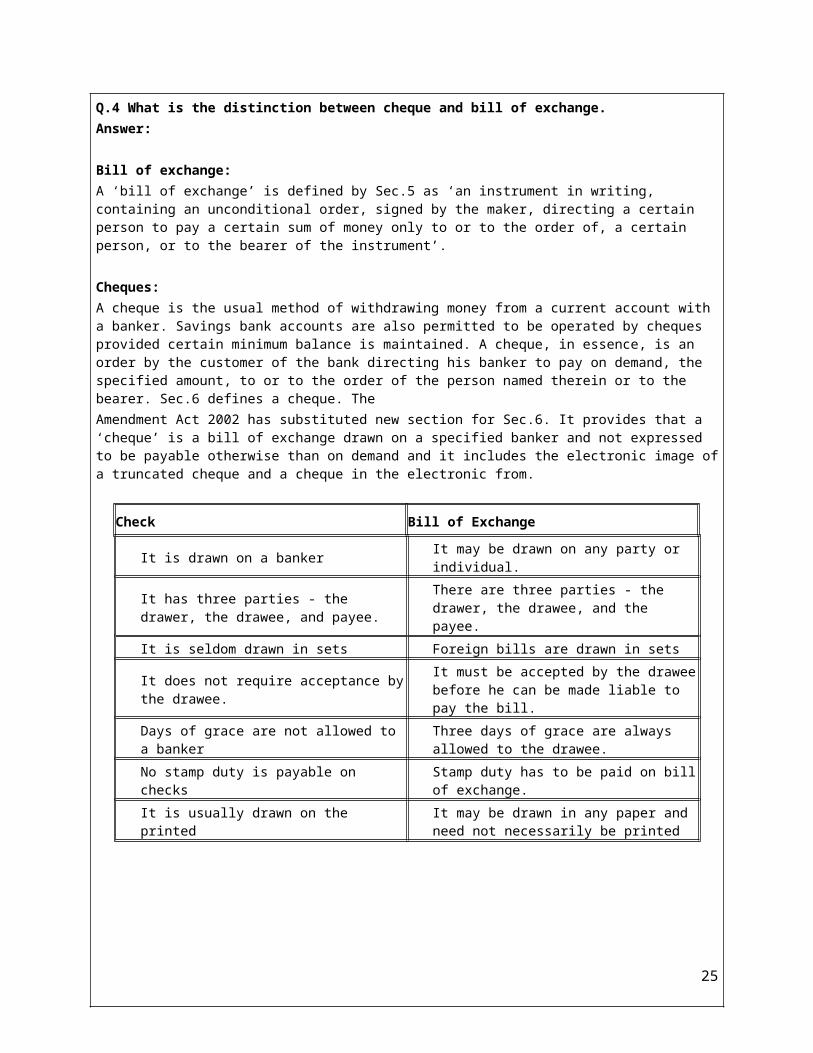

Bill of exchange:A ‘bill of exchange’ is defined by Sec.5 as ‘an instrument in writing, containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to or to the order of, a certain person, or to the bearer of the instrument’.

Cheques: A cheque is the usual method of withdrawing money from a current account with a banker. Savings bank accounts are also permitted to be operated by cheques provided certain minimum balance is maintained. A cheque, in essence, is an order by the customer of the bank directing his banker to pay on demand, the specified amount, to or to the order of the person named therein or to the bearer. Sec.6 defines a cheque. TheAmendment Act 2002 has substituted new section for Sec.6. It provides that a ‘cheque’ is a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand and it includes the electronic image of a truncated cheque and a cheque in the electronic from.

Check Bill of Exchange

It is drawn on a banker It may be drawn on any party or individual.

It has three parties - the drawer, the drawee, and payee.

There are three parties - the drawer, the drawee, and the payee.

It is seldom drawn in sets Foreign bills are drawn in sets

It does not require acceptance by the drawee.

It must be accepted by the drawee before he can be made liable to pay the bill.

Days of grace are not allowed to a banker

Three days of grace are always allowed to the drawee.

No stamp duty is payable on checks Stamp duty has to be paid on bill of exchange.

It is usually drawn on the printed It may be drawn in any paper and need not necessarily be printed

20

Q.5. Distinguish between companies limited by shares and companies limited by guarantee.Answer:

The Companies Act, 1956 defines the word “company as a company formed and registered under the Act or an existing company formed and registered under any of the previous company laws (Sec.3)”. This definition does not bring out the meaning and nature of the company into a clear perspective. Also Sec.12 permits the formation of different types of companies. These may be:

1. Companies limited by shares 2. Companies limited by guarantee and 3. Unlimited companies.

The vast majority of companies in India are with limited liability by shares. Distinction between Cheque and bill of exchange

Companies limited by shares Companies limited by guarantee

A company limited by guarantee is normally incorporated for nonprofit making functions. The company has no share capital. A company limited by guarantee has members rather than shareholders. The members of the company guarantee/undertake to contribute a predetermined sum to the liabilities of the company which becomes due in the event of the company being wound up. The Memorandum normally includes a non-profit distribution clause and these companies are usually formed by clubs, professional, trade or research associations.

Limited by shares is defined by: a company that has shareholders, and that the financial obligation of the shareholders to creditors of the company is restricted to the capital invested in the first place (i.e. the specified value of the shares and any premium paid off in exchange for the issue of the shares by the company). Shareholder's individual’s assets are there by secured in the case of the company's insolvency, but revenues invested in the company will be unrecoverable. Limited companies could be either private or public. A private Ltd. (limited company disclosure) involves are less demanding, but for this reason its shares might NOT be provided to the general public (and consequently can't be listed on a national stock market exchange). This is the well-known distinctive characteristic between a private limited company and a public limited company. The absolute majority of trading corporations are private companies limited by shares

.Companies limited by shares are more popular

Companies limited by guarantee are less popular than companies limited by shares.

Companies limited by shares are profit making companies.

Companies limited by guarantee are non-profit making. In case of companies limited by shares, there are shareholders.

21

Companies limited by guarantee have members, and not share holders

Companies limited by shares can engage in legal trades and have general clauses. There is no share capital in case of companies limited by guarantee and it also has self-imposed restrictions

22

Q6. What are the various categories of Cybercrimes?Answer:

Introduction: Crime and criminality have been associated with man since his fall. Crime remains elusive and ever strives to hide itself in the face of development. Different nations have adopted different strategies to contend with crime depending on their nature and extent. One thing is certain, it is that a nation with high incidence of crime cannot grow or develop. That is so because crime is the direct opposite of development. It leaves a negative social and economic consequence. Cybercrime: Cybercrime is defined as crimes committed on the internet using the computer as either a tool or a targeted victim. It is very difficult to classify crimes in general into distinct groups as many crimes evolve on a daily basis. Even in the real world, crimes like rape, murder or theft need not necessarily be separate. However, all cyber crimes involve both the computer and the person behind it as victims; it just depends on which of the two is the main target. Hence, the computer will be looked at as either a target or tool for simplicity’s sake. For example, hacking involves attacking the computer’s information and other resources. It is important to take note that overlapping occurs in many cases and it is impossible to have a perfect classification system. Computer as a tool: When the individual is the main target of Cybercrime, the computer can be considered as the tool rather than the target. These crimes generally involve less technical expertise as the damage done manifests itself in the real world. Human weaknesses are generally exploited. The damage dealt is largely psych logical and intangible, making legal action against the variants more difficult. These are the crimes which have existed for centuries int he offline. Scams, theft, and the likes have existed even before the development in high-tech equipment. The same criminal has simply been given a tool which increases his potential pool of victims and makes him all the harder to trace and apprehend.

Computer as a target: These crimes are committed by a selected group of criminals. Unlike crimes using he computer as a tool, these crimes requires the technical knowledge of the perpetrators. These crimes are relatively new, having been inexistence for only as long as computers have - which explains how unprepared society and the world in general is towards combating these crimes. There are numerous crimes of this nature committed daily on the internet. But it is worth knowing that Africans and indeed Nigerians are yet to develop their technical knowledge to accommodate and perpetrate this kind of crime. The internet in India is growing rapidly. It has given rise to new opportunities in every field we can think of – be it entertainment, business, sports or education. There are two sides to a coin. Internet also has its own disadvantages. One of the major disadvantages is Cybercrime – illegal activity committed on the internet. The internet, along with its advantages, has also exposed us to security risks that come with connecting to a large network. Computers today are being misused for illegal activities like e-mail espionage, credit car fraud, spams, and software piracy and so on, which invade our privacy and offend our senses. Criminal activities in the cyberspace are on the rise. Here we publish an article by Nandini Ram prasad in series for the benefit of our netizens.

23

Cybercrimes can be basically divided into 3 major categories: 1) Cybercrimes against persons2) Cybercrimes against property. 3) Cybercrimes against government. Cybercrimes committed against persons include various crimes like transmission of child-pornography, harassment of any one with the use of a computer such as e-mail. The trafficking, distribution, posting, and dissemination of obscene material including pornography and indecent exposure, constitutes one of the most important Cybercrimes known today. The potential harm of such a crime to humanity can hardly be amplified. This is one Cybercrime which threatens to undermine the growth of the younger generation as also leave irreparable scars and injury on the younger generation, if not controlled. In the United States alone, the virus made its way through 1.2 million computers in one-fifth of the country's largest businesses. David Smith pleaded guilty on Dec. 9, 1999 to state and federal charges associated with his creation of the Melissa virus. There are numerous examples of such computer viruses few of them being "Melissa" and "love bug". A Mumbai-based upstart engineering company lost a say and much money in the business when the rival company, an industry major, stole the technical database from their computers with the help of a corporate cyber spy. Unauthorized access: Using one's own programming abilities as also various programs with malicious intent to gain unauthorized access to a computer or network are very serious crimes. Similarly, the creation and dissemination of harmful computer programs which do irreparable damage to computer systems is another kind of Cybercrime. Software piracy is also another distinct kind of Cybercrime which is perpetuated by many people online who distribute illegal and unauthorized pirated copies of software. Professionals who involve in these cybercrimes are called crackers and it is found that many of such professionals are still in their teens. A report written near the start of the Information Age warned that America's computers were at risk from crackers. It said that computers that "control (our) power delivery, communications, aviation and financial services (and) store vital information, from medical re-cords to business plans, to criminal records", were vulnerable from many sources, including deliberate attacks

24

MF0010– Security Analysis and Portfolio Management

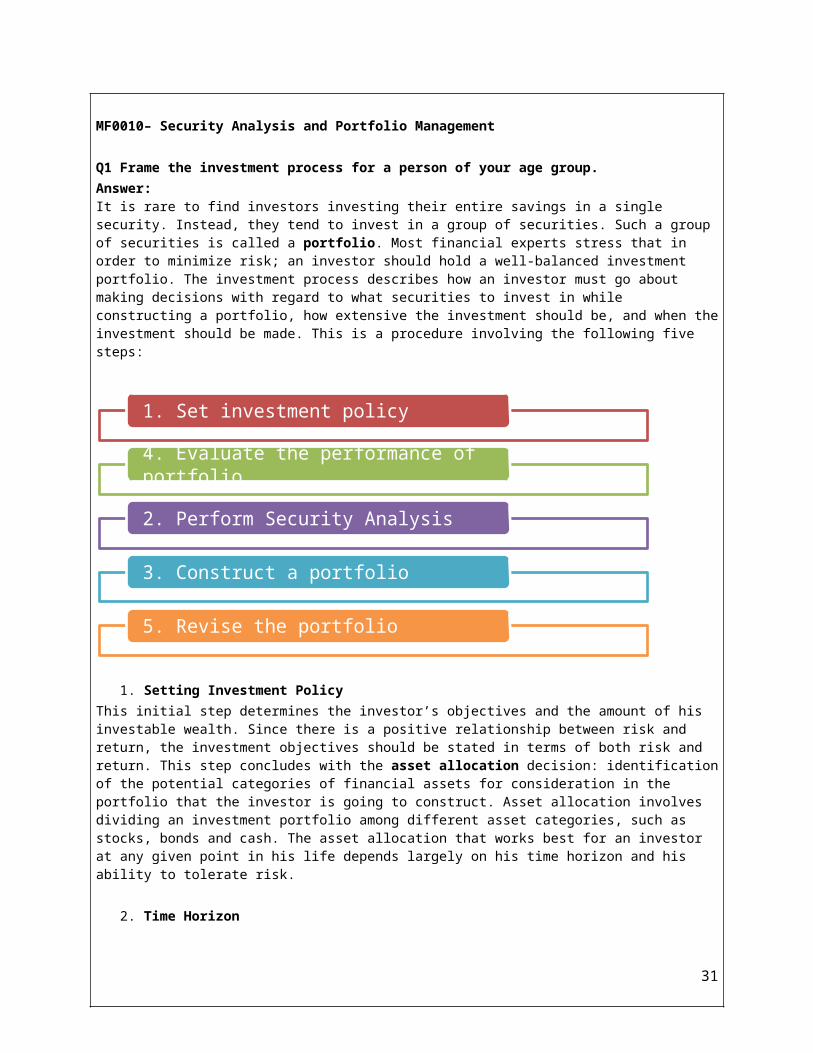

Q1 Frame the investment process for a person of your age group. Answer:It is rare to find investors investing their entire savings in a single security. Instead, they tend to invest in a group of securities. Such a group of securities is called a portfolio. Most financial experts stress that in order to minimize risk; an investor should hold a well-balanced investment portfolio. The investment process describes how an investor must go about making decisions with regard to what securities to invest in while constructing a portfolio, how extensive the investment should be, and when the investment should be made. This is a procedure involving the following five steps:

1. Setting Investment Policy This initial step determines the investor’s objectives and the amount of his investable wealth. Since there is a positive relationship between risk and return, the investment objectives should be stated in terms of both risk and return. This step concludes with the asset allocation decision: identification of the potential categories of financial assets for consideration in the portfolio that the investor is going to construct. Asset allocation involves dividing an investment portfolio among different asset categories, such as stocks, bonds and cash. The asset allocation that works best for an investor at any given point in his life depends largely on his time horizon and his ability to tolerate risk.

2. Time Horizon The time horizon is the expected number of months, years, or decades that an investor will be investing his money to achieve a particular financial goal. An investor with a longer time horizon may feel more comfortable with a riskier or more volatile investment because he can ride out the slow economic cycles and the inevitable ups and downs of the markets. By contrast, an investor who is saving for his teen-aged daughter’s college education would be less likely to take a large risk because he has a shorter time horizon.

3. Risk Tolerance Risk tolerance is an investor’s ability and willingness to lose some or all of his original investment in exchange for greater potential returns. An aggressive investor, or one with a

25

1. Set investment policy

4. Evaluate the performance of portfolio

2. Perform Security Analysis

3. Construct a portfolio

5. Revise the portfolio

high-risk tolerance, is more likely to risk losing money in order to get better results. A conservative investor, or one with a low-risk tolerance, tends to favor investments that will preserve his or her original investment. The conservative investors keep a "bird in the hand," while aggressive investors seek "two in the bush." While setting the investment policy, the investor also selects the portfolio management style (active vs. passive management).

Active Management is the process of managing investment portfolios by attempting to time the market and/or select „undervalued‟ stocks to buy and „overvalued‟ stocks to sell, based upon research, investigation and analysis.

Passive Management is the process of managing investment portfolios by trying to match the performance of an index (such as a stock market index) or asset class of securities as closely as possible, by holding all or a representative sample of the securities in the index or asset class. This portfolio management style does not use market timing or stock selection strategies.

2. Performing Security Analysis This step is the security selection decision: Within each asset type, identified in the asset allocation decision, how does an investor select which securities to purchase. Security analysis involves examining a number of individual securities within the broad categories of financial assets identified in the previous step. One purpose of this exercise is to identify those securities that currently appear to be mispriced. Security analysis is done either using Fundamental or Technical analysis (both have been discussed in subsequent units). Fundamental analysis is a method used to evaluate the worth of a security by studying the financial data of the issuer. It scrutinizes the issuer's income and expenses, assets and liabilities, management, and position in its industry. In other words, it focuses on the „basics‟ of the business. Technical analysis is a method used to evaluate the worth of a security by studying market statistics. Unlike fundamental analysis, technical analysis disregards an issuer's financial statements. Instead, it relies upon market trends to ascertain investor sentiment to predict how a security will perform. 3. Portfolio Construction This step identifies those specific assets in which to invest, as well as determining the proportion of the investors wealth to put into each one. Here selectivity, timing and diversification issues are addressed. Selectivity refers to security analysis and focuses on price movements of individual securities. Timing involves forecasting of price movement of stocks relative to price movements of fixed income securities (such as bonds). Diversification aims at constructing a portfolio in such a way that the investor‟s risk is minimized.

The following table summarizes how the portfolio is constructed for an active and a passive investor. Asset Allocation

Security Selection

Active investor Market timing Stock picking Passive investor Maintain pre-

determined selections

Try to track a well-known market index like Nifty, Sensex

4. Portfolio Revision This step is the repetition of the three previous steps, as objectives might change and previously held portfolio might not be the optimal one. 5. Portfolio performance evaluation

26

This step involves determining periodically how the portfolio has performed over some time period (returns earned vs. risks incurred).

Q2 From the website of BSE India, explain how the BSE Sensex is calculated. Answer:An index is a statistical indicator providing a representation of the value of the securities which constitute it. Indexes often serve as barometers for a given market or industry and benchmarks against which financial or economic performance is measured. A stock index reflects the price movement of shares while a bond index captures the manner in which bond prices go up and down. For more than hundred years, people have tracked the market’s daily ups and downs using various indices of overall market performance. There are currently thousands of indices calculated by various information providers. Internationally, the best known indices are provided by Dow Jones & Co, S & P, Morgan Stanley Capital Markets (MSCI), Lehman Brothers (bond indices). Dow Jones alone currently publishes more than 3,000 indices. Some of the well-known indices are Dow Jones Industrial Average (DJIA), Standard & Poor‟s 500 Index (S&P 500), Nasdaq Composite, Nasdaq 100, Financial Times-Stock Exchange 100 (FTSE 100), Nikkei 225 Stock Average, Hang Seng Index, Deutscher Aktienindex (DAX). In India the best known indices are Sensex and Nifty. Sensex is the stock market index for BSE. It was first compiled in 1986. It is made of 30 stocks representing a sample of large, liquid and representative companies. The base year of SENSEX is 1978-79 and the base value is 100. Sensex till August 31, 2003 was constructed on the basis of full market capitalization. A need was felt to switch over to free float wherein non-promoter and non-strategic shareholdings are eliminated and only those outstanding shares that are available for trading are included. Sensex since 31st September, 2003, is being constructed on free float market capitalization.

Free Float Market CapitalizationCurrently all equity indices in India, except the BSE-TECk Index and BANKEX, are calculated using the 'full-market capitalization' methodology. Under the 'full-market capitalization' methodology, the total market capitalization of a company, irrespective of who is holding the shares, is taken into consideration for computation of an index. However, if instead of taking the total market capitalization, only the Free-float market capitalization of a company is considered for index calculation, it is called the Free-float methodology. Free-float market capitalization is defined as that proportion of total shares issued by the company, which are readily available for trading in the market. It generally excludes promoters' holding, government holding, strategic holding and other locked-in shares, which will not come to the market for trading in the normal course. Thus, the market capitalization of each company in a Free-float index is reduced to the extent of its Free-float available in the market. A Free-float based index is regarded as a better benchmark in comparison to a full market capitalization weighted index. It not only reflects the market trends in a more rational manner, but also aids both active and passive investing styles. It aids active managers by enabling them to benchmark their fund returns vis-à-vis an investable index. This enables an apple-to-apple comparison thereby facilitating better evaluation of performance of active managers. Being a perfectly replicable portfolio of stocks, a Free-float adjusted index is best suited for the passive managers as it enables them to track the index with the least tracking error. Advantages of Free float Market Capitalization: A Free-float Index reflects the market movements better. It aids passive investment because a Free-float index is easily replicable It improves index flexibility and the resultant market coverage and sector coverage

27

It avoids the undue influence of any closely-held large-capitalization stock on the index movement

It is considered as a global best practice in index construction.

How does BSE determine the Free-float factor for each Index Company?

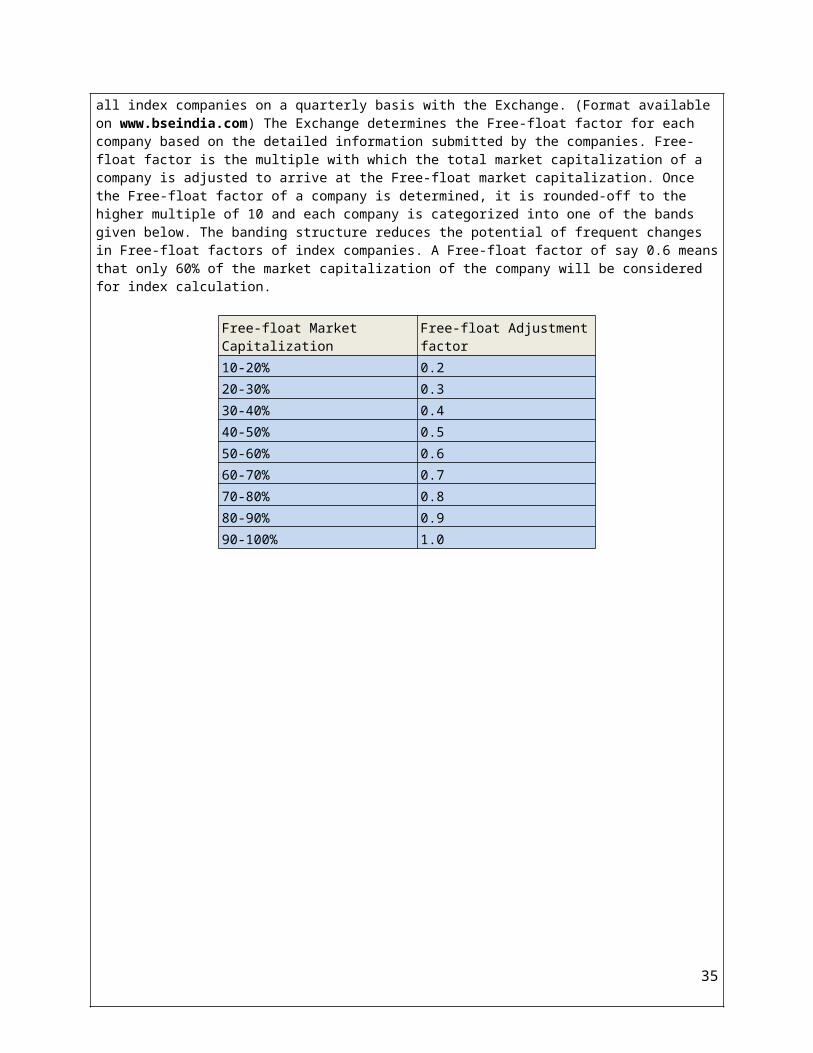

BSE has designed a detailed Free-float format to be filled and submitted by all index companies on a quarterly basis with the Exchange. (Format available on www.bseindia.com) The Exchange determines the Free-float factor for each company based on the detailed information submitted by the companies. Free-float factor is the multiple with which the total market capitalization of a company is adjusted to arrive at the Free-float market capitalization. Once the Free-float factor of a company is determined, it is rounded-off to the higher multiple of 10 and each company is categorized into one of the bands given below. The banding structure reduces the potential of frequent changes in Free-float factors of index companies. A Free-float factor of say 0.6 means that only 60% of the market capitalization of the company will be considered for index calculation.

Free-float Market Capitalization

Free-float Adjustment factor

10-20% 0.220-30% 0.330-40% 0.440-50% 0.550-60% 0.660-70% 0.770-80% 0.880-90% 0.990-100% 1.0

28

29

30

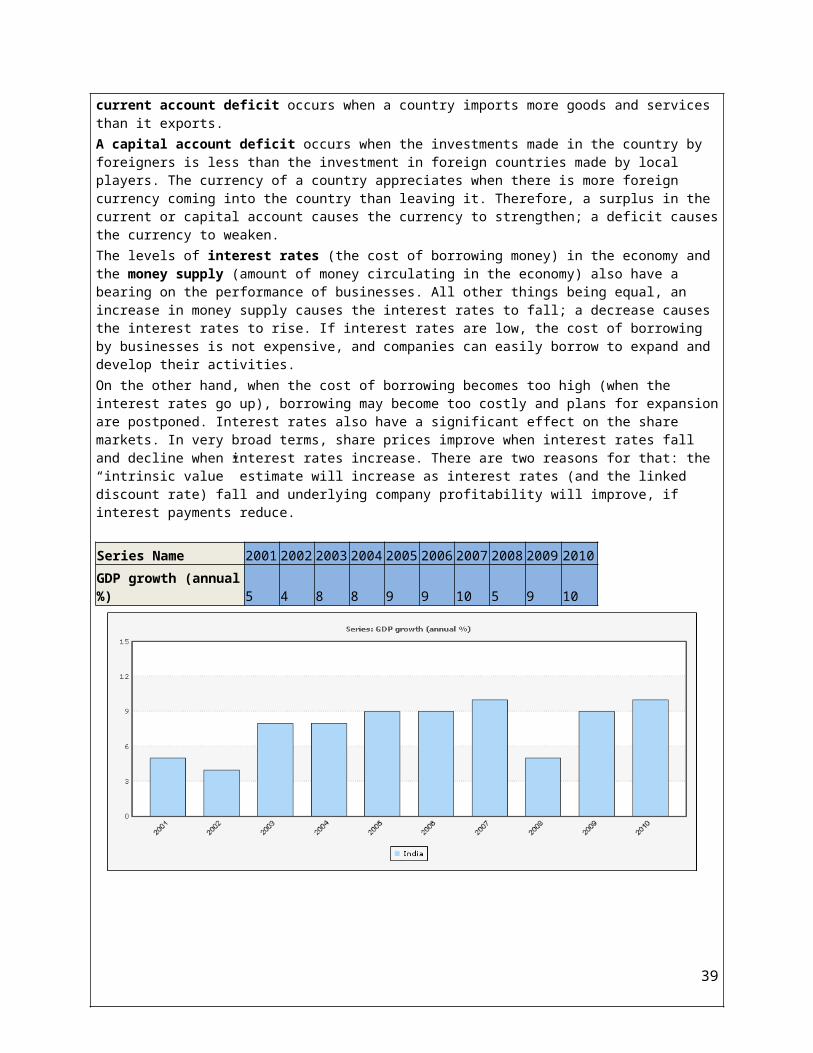

Q4 Perform an economy analysis on Indian economy in the current situation.Answer:Economy analysis investors determine whether the economic climate offers a positive and encouraging investing environment. Economic analysis is done for two reasons: first, a company‟s growth prospects are, ultimately, dependent on the economy in which it operates; second, share price performance is generally tied to economic fundamentals, as most companies generally perform well when the economy is doing the same. Factors to be considered in economy analysis The economic variables that are considered in economic analysis are:

1. gross domestic product (GDP) growth rate, 2. exchange rates, 3. the balance of payments (BOP), 4. the current account deficit, 5. government policy (fiscal and monetary policy), 6. domestic legislation (laws and regulations), 7. unemployment (the percent of the population that wants to work and is currently not

working), 8. public attitude (consumer confidence) 9. inflation (a general increase in the price of goods and services), interest rates, 10. productivity (output per worker), 11. Capacity utilization (output by the firm) etc.

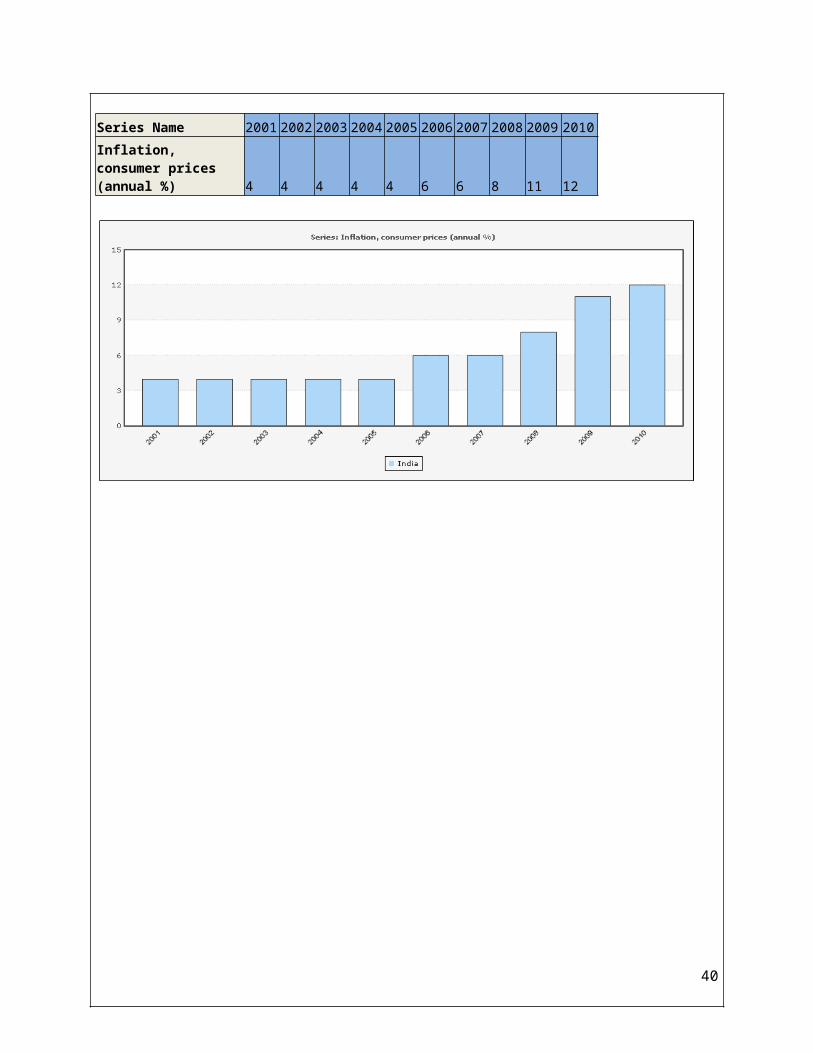

GDP is the total income earned by a country. GDP growth rate shows how fast the economy is growing. Investors know that strong economic growth is good for companies and recessions or full-blown depressions cause share prices to decline, all other things being equal. Inflation is important for investors, as excessive inflation undermines consumer spending power (prices increase) and so can cause economic stagnation. However, deflation (negative inflation) can also hurt the economy, as it encourages consumers to postpone spending (as they wait for cheaper prices). The exchange rate affects the broad economy and companies in a number of ways. First, changes in the exchange rate affect the exports and imports. If exchange rate strengthens, exports are hit; if the exchange rate weakens, imports are affected. The BOP affects the exchange rate through supply and demand for the foreign currency. BOP reflects a country’s international monetary transactions for a specific time period. It consists of the current account and the capital account. The current account is an account of the trade in goods and services. The capital account is an account of the cross-border transactions in financial assets. A current account deficit occurs when a country imports more goods and services than it exports. A capital account deficit occurs when the investments made in the country by foreigners is less than the investment in foreign countries made by local players. The currency of a country appreciates when there is more foreign currency coming into the country than leaving it. Therefore, a surplus in the current or capital account causes the currency to strengthen; a deficit causes the currency to weaken. The levels of interest rates (the cost of borrowing money) in the economy and the money supply (amount of money circulating in the economy) also have a bearing on the performance of businesses. All other things being equal, an increase in money supply causes the interest rates to fall; a decrease causes the interest rates to rise. If interest rates are low, the cost of borrowing by businesses is not expensive, and companies can easily borrow to expand and develop their activities.

31

On the other hand, when the cost of borrowing becomes too high (when the interest rates go up), borrowing may become too costly and plans for expansion are postponed. Interest rates also have a significant effect on the share markets. In very broad terms, share prices improve when interest rates fall and decline when interest rates increase. There are two reasons for that: the “intrinsic value” estimate will increase as interest rates (and the linked discount rate) fall and underlying company profitability will improve, if interest payments reduce.

Series Name2001

2002

2003

2004

2005

2006

2007

2008 2009 2010

GDP growth (annual %) 5 4 8 8 9 9 10 5 9 10

Series Name2001

2002

2003

2004

2005

2006

2007

2008 2009 2010

Inflation, consumer prices (annual %) 4 4 4 4 4 6 6 8 11 12

32

33

Series Name2001

2002

2003

2004

2005

2006

2007

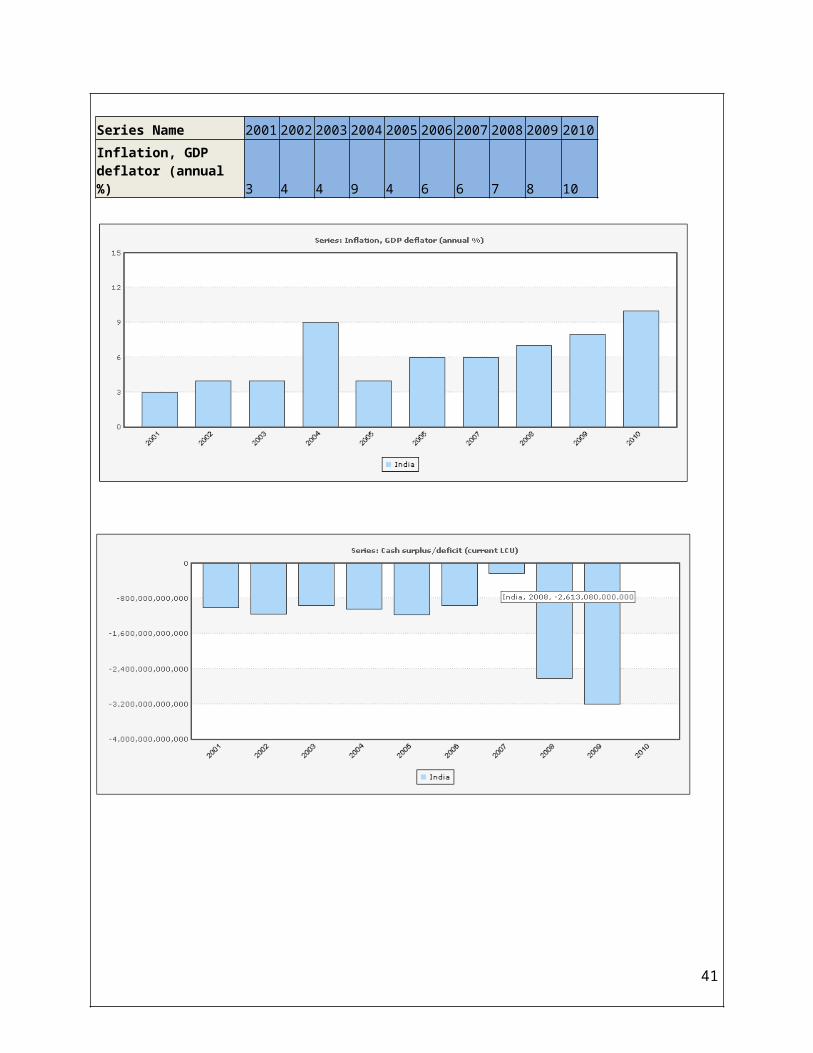

2008 2009 2010

Inflation, GDP deflator (annual %) 3 4 4 9 4 6 6 7 8 10

34

Q4 Identify some technical indicators and explain how they can be used to decide purchase of a company’s stock. Answer:

Technical Indicators: The technical approach to investment is essentially a reflection of the idea that prices move in trends that are determined by the changing attitudes of investors toward a variety of economic, monetary, political and psychological forces. The art of technical analysis, for it is an art, is to identify a trend reversal at a relatively early stage and ride on that trend until the weight of the evidence shows or proves that the trend has reversed. The evidence in this case is represented by the numerous scientifically derived indicators described in this book.

Human nature remains more or less constant and tends to react to similar situations in consistent ways. By studying the nature of previous market turning points, it is possible to develop some characteristics that can help to identify market tops and bottoms. Therefore, technical analysis is based on the assumption that people will continue to make the same mistakes they have made in the past. Sentiment indicators are intended to measure the expectations of various groups of investors, for example, mutual fund investors, and corporate insiders. Sentiment or expectational indicators monitor the actions of different market participants, such as insiders, mutual funds managers and investors, and floor specialists. Just as the pendulum of a clock continually moves from one extreme to another, so the sentiment indexes (which monitor the emotions of investors) move from one extreme at a bear market bottom to another a at bull market top. The assumption on which these indicators are based is that different groups of investors are consistent in their actions at major market turning points. For example, insiders (that is, key employees or major stockholders of a company) and New York Stock Exchange (NYSE) members as a group have a tendency to be correct at market turning points; in aggregate, their transactions are on the buy side toward market bottoms and the sell side toward tops.

Conversely, advisory services as a group are often wrong at market turning points, since they consistently become bullish at market tops and bearish at market troughs. Indexes derived from such data show that certain readings have historically corresponded to market tops, while others have been associated with market bottoms. Since the consensus or majority opinion is normally wrong at market turning points, these indicators of market psychology are a useful basis from which to form a contrary opinion.

Flow of funds indicators are intended to measure the potential for various investor groups to buy or sell stocks, in order to predict the price pressure from those actions. The area of technical analysis that involves what are loosely termed flow-of-funds indicators analyzes the financial position of various investor groups in an attempt to measure their potential capacity for buying or selling stocks. Since there has to be a purchase for each sales, the ex post, or actual dollar balance between supply and demand for stock, must always be equal. The price at which a stock transaction takes place has to be the same for the buyer and the seller, so naturally the amount of money flowing out of the marketing must equal that put in. The flow-of-funds approach is therefore concerned with the before-the-fact balance between supply and demand, known as the ex ante relationship. If at a given price there is a preponderance of buyers over sellers on an ex ante basis, it follows that the actual (ex post) price will have to rise to bring buyers and sellers into balance.

35

Flow-of-funds analysis is concerned, for example, with trends in mutual fund cash positions and those of other major institutions, such as pension funds, insurance companies, foreign investors, bank trust accounts, and customers' free balances, which are normally a source of cash on the buy side. On the supply side, flow-of-funds analysis is concerned with new equity offerings, secondary offerings, and margin debt.

This money flow analysis also suffers from disadvantages. Although the data measure the availability of money for the stock market (for example, mutual fund cash position or pension fund cash flow), they give no indication of the inclination of market participants to use this money for the purchase of stock, or of their elasticity or willingness to sell at a given price on the sell side. The data for the major institutions and foreign investors are not sufficiently detailed to be of much use, and in addition they are reported well after the face. In spite of these drawbacks, flow-of-funds statistics may be used as background material.

Market structure indicators monitor price trends and cycles. This area of technical analysis is the main concern of this book, embracing market structure or the character of the market indicators. These indicators monitor the trend of various price indexes, market breadth, cycles, volume, and so on in order to evaluate the health of the prevailing trend.

Indicators that monitor the trend of a price include moving averages, peak-and-trough analysis, price patterns, and trendlines. Such techniques can also be applied to the sentiment and flow-of-funds indicators discussed previously. This is because these indicators also move in trends. When the trend of psychology, as reflected in these series, reverses, prices are also likely to change direction.