Embed Size (px)

DESCRIPTION

MBA

Citation preview

UNIT - I

INTRODUCTION TO ACCOUNTING

CONCEPTS

Synopsis:

1. Introduction

2. Objectives and Principles

3. Accounting Concepts and conventions

4. Principles of accountancy according to GAAP

5. Double entry system

6. Classification of accounts

7. Accounting cycle

8.

1. INTRODUCITON

FINANCIAL ACCOUNTING

The main object of any business is to make profits. It is may be a business

engaged in the purchase and sales of goods or it may be engaged in the production of

goods or provision of services whatever be it’s nature, the main object is to earn

profits.

A businessman enters into business in order to earn profits. in the

businessman wishes to find out how much profit he has made during a given period, he

must be able to remember all the transactions that have taken place in his business. But

it is not possible for any businessman to remember all the transactions that have takes

place in his business. So he has to record them in his books of accounts.

History of Accounting:

Accounting is as old as civilization itself. From the ancient relics of Babylon, it

can be will proved that accounting did exist as long as 2600 B.C. However, in modern

form accounting based on the principles of Double Entry System came into existence

in 17th Century. Fra Luka Paciolo, a Fransiscan monk and mathematician published

a book De computic et scripturies in 1494 at Venice in Italyl. This book was translated into

English in 1543. In this book he covered a brief section on ‘book-keeping’.

Accounting in India is now a fast developing discipline. The two premier

Accounting Institutes in India viz., chartered Accountants of India and the Institute of

Cost and Works Accountants of India are making continuous and substantial

contributions. The international Accounts Standards Committee (IASC) was

established as on 29th June. In India the ‘Accounting Standards Board (ASB) is

formulating ‘Accounting Standards’ on the lines of standards framed by International

Accounting Standards Committee.

Book-keeping is the art of recording all business transactions in the books of

account maintained by businessman for that purpose.

Keeping a separate book to recording all the business transaction by using

principle of accounting is also called Book-keeping.

Accounting is an art as well as sciences of identifying, analyzing, recording,

classifying and summarizing of business transactions which are of a financial character

and are expressed in terms of money. It also includes interpretation aspect of the

recorded information.

American Institute of Certified Public Accountants (AICPA): “The art of

recording, classifying and summarizing in a significant manner and in terms of money

transactions and events, which are in part at least, of a financial character and

interpreting the results thereof.”

Thus, accounting is an art of identifying, recording, summarizing and

interpreting business transactions of financial nature. Hence accounting is the

Language of Business.

OBJECTIVES OF BOOK KEEPING & ACCOUNTANCY

To ascertainment of financial position of the business organization.

To determine the profit and loss of organization

To knowing the information about capital employed in the business.

To know the value of asset of the organization

To Calculation of amounts due to and due by others.

To know how much tax to pay to the government

To comparison between the current year and the previous year’s records.

To plan the organization

To know the financial information of the other organization

To preparation of financial statements

BASIC ACCOUNTING CONCEPTS

Accounting is a system evolved to achieve a set of objectives. In order to

achieve the goals, we need a set of rules or guidelines. These guidelines are termed here

as “BASIC ACCOUNTING CONCEPTS”. The term concept means an idea or

thought. Basic accounting concepts are the fundamental ideas or basic assumptions

underlying the theory and profit of FINANCIAL ACCOUNTING. These concepts

help in bringing about uniformity in the practice of accounting. In accountancy

following concepts are quite popular.

1. Business Entity Conept: In this concept “Business is treated as separate from the

proprietor”. All the Transactions recorded in the book of Business and not in the

books of proprietor. The proprietor is also treated as a creditor for the Business.

2. Going Concern Concept: This concept relates with the long life of Business. The

assumption is that business will continue to exist for unlimited period unless it is

dissolved due to some reasons or the other.

3. Money Measurement Concept: In this concept “Only those transactions are

recorded in accounting which can be expressed in terms of money, those transactions

which cannot be expressed in terms of money are not recorded in the books of

accounting”.

4. Cost Concept: Accounting to this concept, can asset is recorded at its cost in the

books of account. i.e., the price, which is paid at the time of acquiring it. In balance

sheet, these assets appear not at cost price every year, but depreciation is deducted and

they appear at the amount, which is cost, less classification.

5. Accounting Period Concept: every Businessman wants to know the result of his

investment and efforts after a certain period. Usually one-year period is regarded as an

ideal for this purpose. This period is called Accounting Period. It depends on the

nature of the business and object of the proprietor of business.

6. Dual Ascept Concept: According to this concept “Every business transactions has

two aspects”, one is the receiving benefit aspect another one is giving benefit aspect.

The receiving benefit aspect is termed as“DEBIT”, where as the giving benefit aspect

is termed as “CREDIT”. Therefore, for every debit, there will be corresponding credit.

7. Matching Cost Concept: According to this concept “The expenses incurred during

an accounting period, e.g., if revenue is recognized on all goods sold during a period,

cost of those good sole should also Be charged to that period.

8. Realisation Concept: According to this concept revenue is recognized when a sale

is made. Sale is Considered to be made at the point when the property in goods posses

to the buyer and he becomes legally liable to pay.

ACCOUNTING CONVENTIONS

Accounting is based on some customs or usages. Naturally accountants here to adopt

that usage or custom.They are termed as convert conventions in accounting. The

following are some of the important accounting conventions.

1. Full Disclosure: According to this convention accounting reports should disclose

fully and fairly the information. They purport to represent. They should be prepared

honestly and sufficiently disclose information which is if material interest to

proprietors, present and potential creditors and investors. The companies ACT, 1956

makes it compulsory to provide all the information in the prescribed form.

2.Materiality: Under this convention the trader records important factor about the

commercial activities. In the form of financial statements if any unimportant

information is to be given for the sake of clarity it will be given as footnotes.

3.Consistency: It means that accounting method adopted should not be changed from

year to year. It means that there should be consistent in the methods or principles

followed. Or else the results of a year Cannot be conveniently compared with that of

another.

4. Conservatism: This convention warns the trader not to take unrealized income in to

account. That is why the practice of valuing stock at cost or market price, which ever is

lower is in vague. This is the policy of “playing safe”; it takes in to consideration all

prospective losses but leaves all prospective profits.

DOUBLE ACCOUNTING SYSTEM

Double entry system of Book-keeping is simple and universal in its application.

It has the test of four hundred years continuous use. It may be claimed that it is the

only system worthy of adoption by the practical businessman. To understand the

system of double entry system of book-keeping all that we need to remember is the

fundamental rule:

“Debit the account which receives the benefit.”

“Credit the account which gives the benefit”

Types of account

1) Personal Account

2) Real Account

3) Nominal Account

RULES FOR DEBIT & CREDIT.

1) Personal Account: - This account deals with the individuals of the organization

these includes accounts of natural persons in varied capacities likes suppliers

and buyers of goods, lenders and borrowers of loans etc.

“Debit the receiver”

“Credit the giver”

2) Real Account: - This account deals with the group of individuals of the

organization these include combinations of the properties or assets are known as real

account.

“Debit what comes in”

“Credit what goes out”

3) Nominal Account: - Nominal accounts relate to such items which exist in name

only. These items pertain to expenses and gains like interest, rent, commission,

discount, salary etc,

“Debit all expenses and losses”

“Credit all incomes and gains”

Branches/classification of Accounting:

The important branches of accounting are:

1. Financial Accounting: The purpose of Accounting is to ascertain the

financial results i.e. profit or loass in the operations during a specific period. It

is also aimed at knowing the financial position, i.e. assets, liabilities and equity

position at the end of the period. It also provides other relevant information

to the management as a basic for decision-making for planning and controlling

the operations of the business.

2. Cost Accounting: The purpose of this branch of accounting is to ascertain

the cost of a product / operation / project and the costs incurred for carrying

out various activities. It also assist the management in controlling the costs.

The necessary data and information are gatherr4ed form financial and other

sources.

3. Management Accounting: Its aim to assist the management in taking

correct policy decision and to evaluate the impact of its decisions and actions.

The data required for this purpose are drawn accounting and cost-accounting.

UNIT - II

INTRODUCTION TO ACCOUNTING VALUATION OF FIXED ASSETS & INVENTORY

CONCEPTS

1. Introduction Journal

2. Journal Entries

3. Ledgers

4. Cash book

5. Trial Balance

6. Final Accounts With adjustments

7. Tangible Vs Intangible Asset

8. Reasons for Depreciation

9. provision for depreciation

10. Methods of Depreciation

11. Inventory valuation

12. Methods of inventory valuation

13. Problems on Depreciation & Inventory

JOURNAL

In the early evaluation of book-keeping traders used to record the business

transactions in a simple manner in the Waste book or Rough book. The waste book

is a book in which a businessman briefly notes down each transaction as soon as it

takes place. Transaction is writing in this very first so it is also called Book of Prime or

First Entry Book The Proforma of Journal is given below.

Date Date Particulars L.F. no Debit

RS.

Credit

RS.

LEDGER

Ledger is the secondary book of accounts all business transactions are

recorded in the first instance in the journal, but they must find their place ultimately in

the accounts in the ledger in a duly classified form. This ledger are also called final

entry book. OR Transferring of all journals in to accounts by using accounting

principles is called ledger.

CASH BOOK

Cash book plays an important role in accounting. Whether transactions made are in the

form of cash or credit, final statement will be in the form of receipt or payment of

cash. So, every transaction finds place in the cash book finally.

Cash book is a principal book as well as the subsidiary book. It is a book of original

entry since the transactions are recorded for the first time from the source of

documents. It is a ledger in a sense it is designed in the form of cash account and

records cash receipts on the debit side and the cash payments on the credit side. Thus,

a cash book fulfils the functions of both a ledger account and a journal.

Cash book is divided into two sides. Receipt side (debit side) and payment side (credit

side). The method of recording cash sample is very simple. All cash receipts will be

posted on the debit side and all the payments will be recorded on the credit side.

Types of cash book: cash book may be of the following types according to the needs of

the business.

Simple cash book

Double column or two column cash book

Three column cash book

SINGLE COLUMN CASH BOOK: The simple cash book is a record of only cash

transactions. The model of the cash book is given below.

Date Particulars Lf no Amount Date Particulars Lf no Amount

CASH BOOK

TWO COLUMN CASH BOOK: This book has two columns on each side one for

discount and the other for cash. Discount column on debit side represents loss being

discount allowed to customers. Similarly, discount column on credit side represents

gain being discount received.

Discount may be two types.

(i)Trade discount

(ii)cash discount

TRADE DISCOUNT: when a retailer purchases goods from the wholesaler, he allows

some discount on the catalogue price. This discount is called as Trade discount. Trade

discount is adjusted in the invoice and the net amount is recorded in the purchase

book. As such it will not appear in the book of accounts.

CASH DISCOUNT: When the goods are purchased on credit, payment will be made in

the future as agreed by the parties. If the amount is paid early as promptly a discount by

a way of incentive will be allowed by the seller to the buyer. This discount is called as

cash discount. So cash discount is the discount allowed by the seller to encourage

prompt payment from the buyer. Cash discount is entered in the discount column of

the cash book. The discount recorded in the debit side of the cash book is discount

allowed. The discount recorded in the credit side of the cash book is discount received.

CASH DISCOUNT COLUMN CASH BOOK

Date particulars Lf

no

Disc.

Allo

wed

cash Date Particulars Lf

No

Disc

Recei

Ved.

cash

Date Partic

ulars

Lf no Amount Date Particulars Lf no Amo

unt

THREE COLUMN CASH BOOK: This book has three columns on each side one for

discount, cash and the other for bank. Discount column on debit side represents loss

being discount allowed to customers. Similarly, discount column on credit side

represents gain being discount received.

CASH DISCOUNT COLUMN CASH BOOK

TRAIL BALANCE

The first step in the preparation of final accounts is the preparation of trail balance. In

the double entry system of book keeping, there will be credit for every debit and there

will not be any debit without credit. When this principle is followed in writing journal

entries, the total amount of all debits is equal to the total amount all credits.

A trail balance is a statement of debit and credit balances. It is prepared on a particular

date with the object of checking the accuracy of the books of accounts. It indicates that

all the transactions for a particular period have been duly entered in the book, properly

posted and balanced. The trail balance doesn’t include stock in hand at the end of the

period. All adjustments required to be done at the end of the period including closing

stock are generally given under the trail balance.

Characteristic of a Trial Balance:

1. It is a statement prepared in tabular form.

2. Trial balance is a statement of closing balance but it is not an account. It is prepared to verify the arithmetical accuracy.

3. Preparation of trial balance will leads to preparation of final accounts.

PROFORMA FOR TRAIL BALANCE:

Trail balance for MR…………………………………… as on …………

Date particulars Lf

no

Disc.

Allo

wed

Cash Bank Date Particulars Lf

No

Disc

Recei

Ved.

Cash Bank

NAME OF ACCOUNT

(PARTICULARS)

DEBIT

AMOUNT(RS.)

CREDIT

AMOUNT(RS.)

Debit Balances Purchases

XXXX

Carriage inwards wages All factory & manufacturing exp (factory rent factory Insurance factory lighting.) Oil, water. Gas. Coal. Fuel, power excise duty.octroi trade expenses Salaries Rent rates & taxes Advertising Audit fees, legal charges Insurance Bad debts Repairs Discount allowed Printing& stationary Postage& telegrams Commission paid (dr) Interest on capital Interest on loan Carriage outwards All depreciations All management exp All office exp General exp Discount on debtors Selling exp Cash in hand Cash at bank Debtors Furniture Buildings Good will patents Copy rights. Bills receivable Machinery Motor car Freehold premises All fixed variable assets Credit balances Sales Commission receive bad debts reserve interest received commission receiv interest on drawing discount on creditors Capital Bank loan Bank overdraft

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

Classification of capital and revenue expenses

1 Capital Credit Loan

2 Opening stock Debit Asset

3 Purchases Debit Expense

4 Sales Credit Gain

5 Returns inwards Debit Loss

6 Returns outwards Debit Gain

7 Wages Debit Expense

8 Freight Debit Expense

9 Transport expenses Debit Expense

10 Royalities on production Debit Expense

11 Gas, fuel Debit Expense

12 Discount received Credit Revenue

13 Discount allowed Debit Loss

14 Bas debts Debit Loss

15 Dab debts reserve Credit Gain

16 Commission received Credit Revenue

17 Repairs Debit Expense

18 Rent Debit Expense

19 Salaries Debit Expense

20 Loan Taken Credit Loan

21 Interest received Credit Revenue

22 Interest paid Debit Expense

23 Insurance Debit Expense

24 Carriage outwards Debit Expense

25 Advertisements Debit Expense

26 Petty expenses Debit Expense

27 Trade expenses Debit Expense

28 Petty receipts Credit Revenue

29 Income tax Debit Drawings

30 Office expenses Debit Expense

31 Customs duty Debit Expense

32 Sales tax Debit Expense

Income received in advance Creditors Bills payable All other loans

XXXX

XXXX

XXXX

XXXX

TOTAL XXXX XXXX

33 Provision for discount on debtors Debit Liability

34 Provision for discount on creditors Debit Asset

35 Debtors Debit Asset

36 Creditors Credit Liability

37 Goodwill Debit Asset

38 Plant, machinery Debit Asset

39 Land, buildings Debit Asset

40 Furniture, fittings Debit Asset

41 Investments Debit Asset

42 Cash in hand Debit Asset

43 Cash at bank Debit Asset

44 Reserve fund Credit Liability

45 Loan advances Debit Asset

46 Horse, carts Debit Asset

47 Excise duty Debit Expense

48 General reserve Credit Liability

49 Provision for depreciation Credit Liability

50 Bills receivable Debit Asset

51 Bills payable Credit Liability

52 Depreciation Debit Loss

53 Bank overdraft Credit Liability

54 Outstanding salaries Credit Liability

55 Prepaid insurance Debit Asset

56 Bad debt reserve Credit Revenue

57 Patents & Trademarks Debit Asset

58 Motor vehicle Debit Asset

59 Outstanding rent Credit Revenue

FINAL ACCOUNTS In every business, the business man is interested in knowing whether the

business has resulted in profit or loss and what the financial position of the business is

at a given time. In brief, he wants to know (i)The profitability of the business and (ii)

The soundness of the business.

The trader can ascertain this by preparing the final accounts. The final accounts

are prepared from the trial balance. Hence the trial balance is said to be the link

between the ledger accounts and the final accounts. The final accounts of a firm can be

divided into two stages. The first stage is preparing the trading and profit and loss

account and the second stage is preparing the balance sheet.

TRADING ACCOUNT

The first step in the preparation of final account is the preparation of trading

account. The main purpose of preparing the trading account is to ascertain gross profit

or gross loss as a result of buying and selling the goods.

PROFIT AND LOSS ACCOUNT

The business man is always interested in knowing his net income or net profit.Net

profit represents the excess of gross profit plus the other revenue incomes over

administrative, sales, Financial and other expenses. The debit side of profit and loss

account shows the expenses and the credit side the incomes. If the total of the credit

side is more, it will be the net profit. And if the debit side is more, it will be net loss. PROFORMA OF TRADING AND PROFIT & LOSS A/C

As on …………………………in the books of Mrs. ………………………….

Trading and Profit & Loss A/C Dr Cr

Particulars Amount Particulars Amount

To Opening stock

To Purchases

Less: Pur. Returns

To Carriage inwards

To Wages

Add. Out standings

To All factory & manufacturing

exp (factory rent factory

insurance factory lighting.)

To Oil, water. Gas.

To Freight

To Coal. Fuel, power

To Excise duty.octroi

To Trade expenses

To Gross profit (transfer to

P & L A/C Cr side)

To Gross Loss

To Salaries

Add: outstanding

To Rent rates & Taxes

To Advertising

To Audit fees, legal charges

To Insurance

Less: prepaid insurance

By Sales

Less: Sales returns

By Stolen goods

By Closing stock

By Gross loss (Transfer

to P & L A/C Dr side)

By Gross Profit

By commission received

By bad debts reserve

By interest received

By commission received

By interest on drawings

By discount on creditors

To Bad debts

To Repairs

To Discount allowed

To Printing& Stationary

To Postage& Telegrams

To Commission paid (Dr)

To Interest on capital

To Interest on loan

To Carriage outwards

To All depreciations

To All management exp

To All office exp

To General exp

To Discount on debtors

To Selling exp

To Net profit (transfer to

capital A/C)

By Net loss (transfer to capital

A/C)

BALANCE SHEET The second point of final accounts is the preparation of balance sheet. It is

prepared often in the trading and profit, loss accounts have been compiled and closed.

A balance sheet may be considered as a statement of the financial position of the

concern at a given date.

Thus, Balance sheet is defined as a statement which sets out the assets and liabilities of

a business firm and which serves to as certain the financial position of the same on any

particular date. On the left-hand side of this statement, the liabilities and the capital are

shown. On the right-hand side all the assets are shown. Therefore, the two sides of the

balance sheet should be equal. Otherwise, there is an error somewhere. PROFORMA OF BALANCE SHEET

As on …………………………in the books of Mrs. ………………………….

Balance Sheet

Liabilities Amouts Assets Amounts

Capital

Add :Int on cap

Add :Net profit

or

Less: Net loss

Less: drawings

Less: Int on drawings

Bank loan

Bank overdraft

Income received in

advance

Creditors

Less Discount on

creditors

Bills payable

All other loans

Outstanding wages,

salaries

Cash in hand

Cash at bank

Debtors

Less Bad debts

Furniture

Less depreciation

Buildings

Less depreciation

Good will patents

Copy rights.

Bills receivable

Machinery

Less Depreciation

Motor car

Less depreciation

Prepaid expenses(insurance)

Freehold premises

All fixed variable assets

Closing stock

FINAL ACCOUNTS -- ADJUSTMENTS

We know that business is a going concern. It has to be carried on indefinitely.

At the end of every accounting year. The trader prepares the trading and profit and loss

account and balance sheet. While preparing these financial statements, sometimes the

trader may come across certain problems .The expenses of the current year may be still

payable or the expenses of the next year have been prepaid during the current year. In

the same way, the income of the current year still receivable and the income of the next

year have been received during the current year. Without these adjustments, the profit

figures arrived at or the financial position of the concern may not be correct. As such

these adjustments are to be made while preparing the final accounts.

The adjustments to be made to final accounts will be given under the Trial Balance.

While making the adjustment in the final accounts, the student should remember that

“every adjustment is to be made in the final accounts twice i.e. once in trading, profit

and loss account and later in balance sheet generally”. The following are some of the

important adjustments to be made at the time of preparing of final accounts:-

1. CLOSING STOCK :-

(i)If closing stock is given in Trail Balance: It should be shown only in the balance sheet

“Assets Side”.

(ii)If closing stock is given as adjustment :

1. First, it should be posted at the credit side of “Trading Account”.

2. Next, shown at the asset side of the “Balance Sheet”.

2. OUTSTANDING EXPENSES:-

(i)If outstanding expenses given in Trail Balance: It should be only on the liability side of

Balance Sheet.

(ii)If outstanding expenses given as adjustment :

1. First, it should be added to the concerned expense at the

debit side of profit and loss account or Trading Account.

2. Next, it should be added at the liabilities side of the Balance Sheet.

3.PREAPID EXPENSES :-

(i)If prepaid expenses given in Trial Balance: It should be shown only in assets side of the

Balance Sheet.

(ii)If prepaid expense given as adjustment :

1. First, it should be deducted from the concerned expenses at the debit side of profit

and loss account or Trading Account.

2. Next, it should be shown at the assets side of the Balance Sheet.

4.INCOME EARNED BUT NOT RECEIVED [OR] OUTSTANDING INCOME [OR]

ACCURED INCOME :-

(i)If incomes given in Trial Balance: It should be shown only on the assets side of the Balance

Sheet.

(ii)If incomes outstanding given as adjustment:

1. First, it should be added to the concerned income at the credit side of profit and loss

account.

2. Next, it should be shown at the assets side of the Balance sheet.

5. INCOME RECEIVED IN ADVANCE: UNEARNED INCOME:-

(i)If unearned incomes given in Trail Balance : It should be shown only on the liabilities side of

the Balance Sheet.

(ii)If unearned income given as adjustment :

1. First, it should be deducted from the concerned income in the credit side of the profit

and loss account.

2. Secondly, it should be shown in the liabilities side of the

Balance Sheet.

6.DEPRECIATION:-

(i)If Depreciation given in Trail Balance: It should be shown only on the debit side of the

profit and loss account.

(ii)If Depreciation given as adjustment

1. First, it should be shown on the debit side of the profit and loss account.

2. Secondly, it should be deduced from the concerned asset in the Balance sheet assets

side.

7.INTEREST ON LOAN [OR] CAPITAL :-

(i)If interest on loan (or) capital given in Trail balance :It should be shown only on debit side

of the profit and loss account.

(ii)If interest on loan (or)capital given as adjustment :

1. First, it should be shown on debit side of the profit and loss account.

2. Secondly, it should added to the loan or capital in

the liabilities side of the Balance Sheet.

8. BAD DEBTS:-

(i)If bad debts given in Trail balance :It should be shown on the debit side of the profit and

loss account.

(ii)If bad debts given as adjustment:

1. First, it should be shown on the debit side of the profit and loss account.

2. Secondly, it should be deducted from debtors in the assets side of the Balance Sheet.

9.INTEREST ON DRAWINGS :-

(i)If interest on drawings given in Trail balance: It should be shown on the credit side of the

profit and loss account.

(ii)If interest on drawings given as adjustments :

1. First, it should be shown on the credit side of the profit and loss account.

2. Secondly, it should be deducted from capital on liabilities

side of the Balance Sheet.

10.INTEREST ON INVESTMENTS :-

(i)If interest on the investments given in Trail balance :It should be shown on the credit side of

the profit and loss account.

(ii)If interest on investments given as adjustments :

1. First, it should be shown on the credit side of the profit and loss account.

2. Secondly, it should be added to the investments on assets side of the Balance Sheet

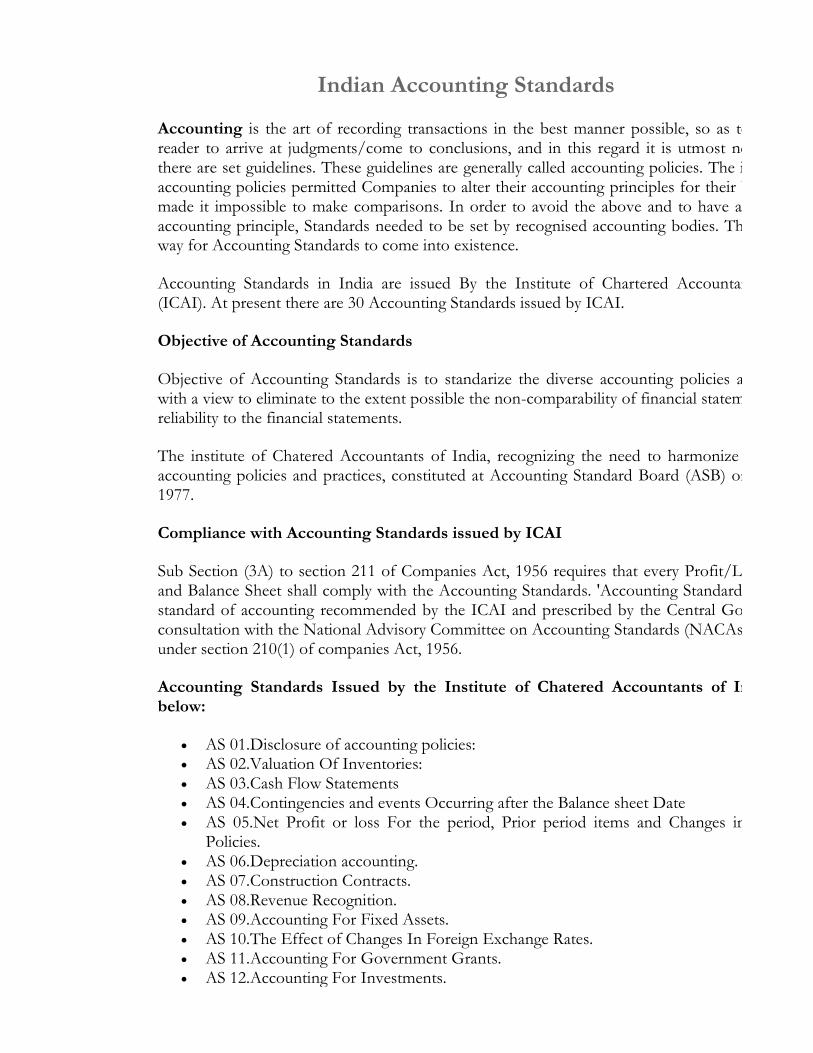

Indian Accounting Standards

Accounting is the art of recording transactions in the best manner possible, so as to enable the reader to arrive at judgments/come to conclusions, and in this regard it is utmost necessary that there are set guidelines. These guidelines are generally called accounting policies. The intricacies of accounting policies permitted Companies to alter their accounting principles for their benefit. This made it impossible to make comparisons. In order to avoid the above and to have a harmonised accounting principle, Standards needed to be set by recognised accounting bodies. This paved the way for Accounting Standards to come into existence.

Accounting Standards in India are issued By the Institute of Chartered Accountanst of India (ICAI). At present there are 30 Accounting Standards issued by ICAI.

Objective of Accounting Standards

Objective of Accounting Standards is to standarize the diverse accounting policies and practices with a view to eliminate to the extent possible the non-comparability of financial statements and the reliability to the financial statements.

The institute of Chatered Accountants of India, recognizing the need to harmonize the diversre accounting policies and practices, constituted at Accounting Standard Board (ASB) on 21st April, 1977.

Compliance with Accounting Standards issued by ICAI

Sub Section (3A) to section 211 of Companies Act, 1956 requires that every Profit/Loss Account and Balance Sheet shall comply with the Accounting Standards. 'Accounting Standards' means the standard of accounting recommended by the ICAI and prescribed by the Central Government in consultation with the National Advisory Committee on Accounting Standards (NACAs) constituted under section 210(1) of companies Act, 1956.

Accounting Standards Issued by the Institute of Chatered Accountants of India are as below:

AS 01.Disclosure of accounting policies: AS 02.Valuation Of Inventories: AS 03.Cash Flow Statements AS 04.Contingencies and events Occurring after the Balance sheet Date AS 05.Net Profit or loss For the period, Prior period items and Changes in accounting

Policies. AS 06.Depreciation accounting. AS 07.Construction Contracts. AS 08.Revenue Recognition. AS 09.Accounting For Fixed Assets. AS 10.The Effect of Changes In Foreign Exchange Rates. AS 11.Accounting For Government Grants. AS 12.Accounting For Investments.

AS 13.Accounting For Amalgamation. AS 14.Employee Benefits. AS 15.Borrowing Cost. AS 16.Segment Reporting. AS 17.Related Party Disclosures. AS 18.Accounting For Leases. AS 19.Earning Per Share. AS 20.Consolidated Financial Statement. AS 21.Accounting For Taxes on Income. AS 22.Accounting for Investment in associates in Consolidated Financial Statement. AS 23.Discontinuing Operation. AS 24.Interim Financial Reporting. AS 25.Intangible assets. AS 26.Financial Reporting on Interest in joint Ventures. AS 27.Impairment Of assets. AS 28.Provisions, Contingent, liabilities and Contingent assets. AS 29.Financial instrument. AS 30.Financial Instrument: presentation. AS 31.Financial Instruments, Disclosures and Limited revision to accounting standards.

Disclosure of Accounting Policies: Accounting Policies refer to specific accounting principles and the method of applying those principles adopted by the enterprises in preparation and presentation of the financial statements.

Valuation of Inventories: The objective of this standard is to formulate the method of computation of cost of inventories / stock, determine the value of closing stock / inventory at which the inventory is to be shown in balance sheet till it is not sold and recognized as revenue.

Cash Flow Statements: Cash flow statement is additional information to user of financial statement. This statement exhibits the flow of incoming and outgoing cash. This statement assesses the ability of the enterprise to generate cash and to utilize the cash. This statement is one of the tools for assessing the liquidity and solvency of the enterprise.

Contigencies and Events occuring after the balance sheet date: In preparing financial statement of a particular enterprise, accounting is done by following accrual basis of accounting and prudent accounting policies to calculate the profit or loss for the year and to recognize assets and liabilities in balance sheet. While following the prudent accounting policies, the provision is made for all known liabilities and losses even for those liabilities / events, which are probable. Professional judgement is required to classify the likehood of the future events occuring and, therefore, the question of contingencies and their accounting arises.Objective of this standard is to prescribe the accounting of contigencies and the events, which take place after the balance sheet date but before approval of balance sheet by Board of Directors. The Accounting Standard deals with Contingencies and Events occuring after the balance sheet date.

Net Profit or Loss for the Period, Prior Period Items and change in Accounting Policies : The objective of this accounting standard is to prescribe the criteria for certain items in the profit and loss account so that comparability of the financial statement can be enhanced. Profit and loss account being a period statement covers the items of the income and expenditure of the particular period. This accounting standard also deals with change in accounting policy, accounting estimates and extraordinary items.

Depreciation Accounting : It is a measure of wearing out, consumption or other loss of value of a depreciable asset arising from use, passage of time. Depreciation is nothing but distribution of total cost of asset over its useful life.

Construction Contracts : Accounting for long term construction contracts involves question as to when revenue should be recognized and how to measure the revenue in the books of contractor. As the period of construction contract is long, work of construction starts in one year and is completed in another year or after 4-5 years or so. Therefore question arises how the profit or loss of construction contract by contractor should be determined. There may be following two ways to determine profit or loss: On year-to-year basis based on percentage of completion or On cpmpletion of the contract.

Revenue Recognition : The standard explains as to when the revenue should be recognized in profit and loss account and also states the circumstances in which revenue recognition can be postponed. Revenue means gross inflow of cash, receivable or other consideration arising in the course of ordinary activities of an enterprise such as:- The sale of goods, Rendering of Services, and Use of enterprises resources by other yeilding interest, dividend and royalties. In other words, revenue is a charge made to customers / clients for goods supplied and services rendered.

Accounting for Fixed Assets : It is an asset, which is:- Held with intention of being used for the purpose of producing or providing goods and services. Not held for sale in the normal course of business. Expected to be used for more than one accounting period.

The Effects of changes in Foreign Exchange Rates : Effect of Changes in Foreign Exchange Rate shall be applicable in Respect of Accounting Period commencing on or after 01-04-2004 and is mandatory in nature. This accounting Standard applicable to accounting for transaction in Foreign currencies in translating in the Financial Statement Of foreign operation Integral as well as non- integral and also accounting for For forward exchange.Effect of Changes in Foreign Exchange Rate, an enterprises should disclose following aspects:

Amount Exchange Difference included in Net profit or Loss; Amount accumulated in foreign exchange translation reserve; Reconciliation of opening and closing balance of Foreign Exchange translation reserve

Accounting for Government Grants : Governement Grants are assistance by the Govt. in the form of cash or kind to an enterprise in return for past or future compliance with certain conditions. Government assistance, which cannot be valued reasonably, is excluded from Govt.

grants,. Those transactions with Governement, which cannot be distinguished from the normal trading transactions of the enterprise, are not considered as Government grants.

Accounting for Investments : It is the assets held for earning income by way of dividend, interest and rentals, for capital appreciation or for other benefits.

Accounting for Amalgamation : This accounting standard deals with accounting to be made in books of Transferee company in case of amalgamtion. This accounting standard is not applicable to cases of acquisition of shares when one company acquires / purcahses the share of another company and the acquired company is not dissolved and its seperate entity continues to exist. The standard is applicable when acquired company is dissolved and seperate entity ceased exist and purchasing company continues with the business of acquired company

Employee Benefits : Accounting Standard has been revised by ICAI and is applicable in respect of accounting periods commencing on or after 1st April 2006. the scope of the accounting standard has been enlarged, to include accounting for short-term employee benefits and termination benefits.

Borrowing Costs : Enterprises are borrowing the funds to acquire, build and install the fixed assets and other assets, these assets take time to make them useable or saleable, therefore the enterprises incur the interest (cost on borrowing) to acquire and build these assets. The objective of the Accounting Standard is to prescribe the treatment of borrowing cost (interest + other cost) in accounting, whether the cost of borrowing should be included in the cost of assets or not.

Segment Reporting : An enterprise needs in multiple products/services and operates in different geographical areas. Multiple products / services and their operations in different geographical areas are exposed to different risks and returns. Information about multiple products / services and their operation in different geographical areas are called segment information. Such information is used to assess the risk and return of multiple products/services and their operation in different geographical areas. Disclosure of such information is called segment reporting.

Related Paty Disclosure : Sometimes business transactions between related parties lose the feature and character of the arms length transactions. Related party relationship affects the volume and decision of business of one enterprise for the benefit of the other enterprise. Hence disclosure of related party transaction is essential for proper understanding of financial performance and financial position of enterprise.

Accounting for leases : Lease is an arrangement by which the lesser gives the right to use an asset for given period of time to the lessee on rent. It involves two parties, a lessor and a lessee and an asset which is to be leased. The lessor who owns the asset agrees to allow the lessee to use it for a specified period of time in return of periodic rent payments.

Earning Per Share :Earning per share (EPS)is a financial ratio that gives the information regarding earning available to each equiy share. It is very important financial ratio for assessing the state of market price of share. This accounting standard gives computational methodology for the

determination and presentation of earning per share, which will improve the comparison of EPS. The statement is applicable to the enterprise whose equity shares or potential equity shares are listed in stock exchange.

Consolidated Financial Statements : The objective of this statement is to present financial statements of a parent and its subsidiary (ies) as a single economic entity. In other words the holding company and its subsidiary (ies) are treated as one entity for the preparation of these consolidated financial statements. Consolidated profit/loss account and consolidated balance sheet are prepared for disclosing the total profit/loss of the group and total assets and liabilities of the group. As per this accounting standard, the conslidated balance sheet if prepared should be prepared in the manner prescribed by this statement.

Accounting for Taxes on Income : This accounting standard prescribes the accounting treatment for taxes on income. Traditionally, amount of tax payable is determined on the profit/loss computed as per income tax laws. According to this accounting standard, tax on income is determined on the principle of accrual concept. According to this concept, tax should be accounted in the period in which corresponding revenue and expenses are accounted. In simple words tax shall be accounted on accrual basis; not on liability to pay basis.

Accounting for Investments in Associates in consolidated financial statements : The accounting standard was formulated with the objective to set out the principles and procedures for recognizing the investment in associates in the cosolidated financial statements of the investor, so that the effect of investment in associates on the financial position of the group is indicated.

Discontinuing Operations : The objective of this standard is to establish principles for reporting information about discontinuing operations. This standard covers "discontinuing operations" rather than "discontinued operation". The focus of the disclosure of the Information is about the operations which the enterprise plans to discontinue rather than dsclosing on the operations which are already discontinued. However, the disclosure about discontinued operation is also covered by this standard.

Interim Financial Reporting (IFR) : Interim financial reporting is the reporting for periods of less than a year generally for a period of 3 months. As per clause 41 of listing agreement the companies are required to publish the financial results on a quarterly basis.

Intangible Assets : An Intangible Asset is an Identifiable non-monetary Asset without physical substance held for use in the production or supplying of goods or services for rentals to others or for administrative purpose

Financial Reporting of Interest in joint ventures : Joint Venture is defined as a contractual arrangement whereby two or more parties carry on an economic activity under 'joint control'. Control is the power to govern the financial and operating policies of an economic activity so as to obtain benefit from it. 'Joint control' is the contractually agreed sharing of control over economic activity.

Impairment of Assets : The dictionary meanong of 'impairment of asset' is weakening in value of asset. In other words when the value of asset decreases, it may be called impairment of an asset. As per AS-28 asset is said to be impaired when carrying amount of asset is more than its recoverable amount.

Provisions, Contingent Liabilities And Contingent Assets : Objective of this standard is to prescribe the accounting for Provisions, Contingent Liabilitites, Contingent Assets, Provision for restructuring cost.Provision: It is a liability, which can be measured only by using a substantial degree of estimation.Liability: A liability is present obligation of the enterprise arising from past events the settlement of which is expected to result in an outflow from the enterprise of resources embodying economic benefits.

Financial Instrument: Recognition and Measurement, issued by The Council of the Institute of Chartered Accountants of India, comes into effect in respect of Accounting periods commencing on or after 1-4-2009 and will be recommendatory in nature for An initial period of two years. This Accounting Standard will become mandatory in respect of Accounting periods commencing on or after 1-4-2011 for all commercial, industrial and business Entities except to a Small and Medium-sized Entity. The objective of this Standard is to establish principles for recognizing and measuring Financial assets, financial liabilities and some contracts to buy or sell non-financial items. Requirements for presenting information about financial instruments are in Accounting Standard.

Financial Instrument: presentation : The objective of this Standard is to establish principles for presenting financial instruments as liabilities or equity and for offsetting financial assets and financial liabilities. It applies to the classification of financial instruments, from the perspective of the issuer, into financial assets, financial liabilities and equity instruments; the classification of related interest, dividends, losses and gains; and the circumstances in which financial assets and financial liabilities should be offset. The principles in this Standard complement the principles for recognising and measuring financial assets and financial liabilities in Accounting Standard Financial Instruments:

Financial Instruments, Disclosures and Limited revision to accounting standards: The objective of this Standard is to require entities to provide disclosures in their financial statements that enable users to evaluate:

the significance of financial instruments for the entity’s financial position and performance; and

the nature and extent of risks arising from financial instruments to which the entity is exposed during the period and at the reporting date, and how the entity manages those risks.

DEPRECIATION The depreciation accounting is mainly based on the concept of income. The

concept of income is matching of revenues with expenses. The goods purchased are

frequently matched through immediate sale or within a year. The crux of the concept

of income is that the expenses are to be matched against the revenues. The ultimate

aim of matching is done in order to determine the volume of profit or loss of the

transaction. If the assets are nothing but long term assets procured by the enterprise

should be matched against the revenues of them. The matching of expenditure of the

assets incurred by the firm at the time of purchase against the revenues is the hard core

task of the firm. Why it is being considered as a cumbersome task in matching ? The

benefits/revenues of the fixed assets expected to accrue for many number of years but

not within a year. The

initial investment on the assets at the time of purchase should be matched against the

revenue pattern of the same year after year in order to find out the profitability of the

long term investment. To have an effective matching against the revenues on every

year, the amount of purchase has to be stretched. The stretching of expenses into many

years is known as depreciation.

The ultimate purpose of the depreciation is to replace the fixed assets only at the

moment of becoming useless through the current revenues.

According to Dickens, “depreciation is the permanent and continuous diminution in

the quality /quantity / value of the asset. ”

In simple words to understand the terminology depreciation is the permanent decrease

in the value of the fixed assets.

4.3.1 Reasons for Depreciation

(1) Wear and Tear of the Asset: The long term assets are becoming less efficient and

poor quality in operations due to the continuous usage of the asset.

(2) Exhaustion: Nothing will be remaining due to the continuous extraction of

resources. The resources in the oil wells, mine fields will become nothing due to

continuous extraction should be replaced by new exploration. To invest on the new

exploration in order to have continuous exploration which requires the depreciation as

a charge against the revenues of the fields?

Example, Oil & Natural Gas Corporation Ltd. (ONGC) indulges in the process of new

oil exploration projects through research projects. Then the new projects should be

identified and invested by huge initial investment outlay through the current revenues

out of the existing projects on account of replacement due to depletion of resources..

(3) To Face Technological Obsolescence: To replace the old machinery with new

machinery before the expiry of the economic life period of the asset in order to

maintain the efficiency and economy of the asset. The type writer was replaced by the

electronic typewriter during the yester periods of office automation. To replace the old

type writer which is not efficient as well as economical, should be replaced by the new

electronic typewriter through the depreciation charge on the old one.

(4) Accident: The value of the asset mainly depends upon the efficiency and

economy;which gets affected due to the accident.

(5) To Implementing New Technology in the Business Organization

(6) Passage of time:Some assets diminish in value on account of sheer passage of time,

even though they are not used e.g. lease hold property, patent rights, copy rights etc.

(7) Depletion: Some assets decline in value proportionate to the quantum of

production, e.g. mines, quarry etc. With the raising of coal etc. from coal mine, the total

deposit reduces gradually and after some time it will be fully exhausted. Then its value

will be nil.

The need for provision for depreciation arises for the following reasons:

(1) Ascertainment of true profit or loss-Depreciation is a loss. So unless it is

considered like all other expenses and losses, true profit/loss cannot be ascertained. In

other words, depreciation must be considered in order to find out true profit/loss of a

business.

(2) Ascertainment of true cost of production-Goods are produced with the help of

plant and machinery which incurs depreciation in the process of production. This

depreciation must be considered as a part of the cost of production of goods.

Otherwise, the cost of production would be shown less than the true cost. Sale price is

normally fixed on the basis of cost of production. So, if the cost of production is

shown less by ignoring depreciation, the sale price will also be fixed at a low level

resulting in loss to the business;

(3) Actual Value of Assets-Value of assets gradually decreases on account of

depreciation. If depreciation is not taken into account, the value of asset will be shown

in the books at a figure higher than its true value and hence the true financial position

of the business will not be disclosed through Balance Sheet.

(4) Replacement of Assets-After some time an asset will be completely exhausted on

account of use. A new asset then be purchased requiring large sum of money. If the

whole amount of profit is withdrawn from business each year without considering the

loss on account of depreciation, necessary sum may not be available for. buying the

new assets. In such a case the required money is to be collected by introducing fresh

capital or by obtaining loan by selling some other assets. This is contrary &0sound

commercial policy.

(5) To Implementing New Technology in the Business Organization

(6) Keeping Capital' Intact-Capital invested in buying an asset, gradually diminishes

on

account of depreciation. If loss on account of depreciation is not considered in

determining profit/ loss at the year end, profit will be shown more. If the excess profit

is withdrawn, the working capital will gradually reduce, the business will become weak

and its profit earning

capacity will also fall.

(7) Legal Restriction-According to Sec. 205 of the Companies Act, 1956 dividend

cannot be declared without charging depreciation on fixed assets. Thus in "Case of

joint stock companies charging of depreciation is compulsory.

METHODS OF DEPRECIATION

Straight line method

Diminishing Balance or Written down method

Annuity method

Depletion or Output method

Machine hour rate method

Sum of digits method

Sinking fund method

Insurance policy method

ACCOUNTING ENTRIES FOR DEPRECIATION 1) Purchasing of assets Asset A/c ……………. Dr To Bank A/c (Being the furniture is purchased) 2) Providing depreciation for asset Depreciation A/c ……….Dr To Asset A/c (Being Depreciation provided) 3) Sale of Asset (loss) Profit& Loss A/c……….Dr To Asset A/c (Being Loss on Asset) 4) Sale of Asset (Profit) Asset A/c …………..Dr To Profit& Loss A/c (Being Profit on Asset) STRAIGHT LINE METHOD/FIXED INSTALLMENT METHOD

This method, depreciation is calculated as a fixed proportion on the original

value of the asset. The depreciation is charged as fixed in volume on the original value

of the asset at which it was purchased. The original value of the asset is nothing but the

purchase value of the asset.

DIMINISHING BALANCE/WRITTEN DOWN VALUE METHOD

This method also having the same methodology in charging depreciation on the

fixed assets like fixed percentage Though it is bearing similar approach in charging

depreciation but different in application from the straight line method. Under this

method, the depreciation is charged on the value of the asset available at the beginning

of the year.

ANNUITY METHOD:-

The annuity method of depreciation is also commonly referred to as the

compound interest method of depreciation. If the cash flow of the asset being

depreciated is constant over the life of the asset, then this method is called the

annuity method.

A method of depreciation centered on cost recovery and a constant rate of

return upon any asset that is being depreciated. This method requires the

determination of the internal rate of return (IRR) on the cash inflows and

outflows of the asset. The IRR is then multiplied by the initial book value of the

asset, and the result is subtracted from the cash flow for the period in order to

find the actual amount of depreciation that can be taken.

DEPRECIATION FUND METHOD:-

A method of depreciation under which the depreciation expense is an

amount of an Annuity so that the amount of the annuity at the end of the useful

life would equal the Acquisition Cost of the asset. Theoretically, the depreciation

charge should include interest on accumulated depreciation at the beginning of

the period. This method is rarely used in practice.

INVENTORY

The raw materials, work-in-process goods and completely finished goods that

are considered to be the portion of a business's assets that is ready or will be ready for

sale. Inventory represents one of the most important assets that most businesses

possess, because the turnover of inventory represents one of the primary sources

of revenue generation and subsequent earnings for the company's

shareholders/owners.

METHODS OF INVENTORY MANAGEMENTS:

First In First Out (FIFO) Method

Last In First Out (LIFO) Method

Average Cost (AC)Method

1)FIRST IN FIRST OUT (FIFO) METHOD:

The first in first out (FIFO) method of costing is used to

introduce the subject of materials costing. The FIFO method of costing issued

materials follows the principle that materials used should carry the actual experienced

cost of the specific units used. The methods assumes that materials are issued from the

oldest supply in stock and that the cost of those units when placed in stock is the cost

of those same units when issued. However, FIFO costing may be used even though

physical withdrawal is in a different order.

Advantages claimed for first in first (FIFO) out costing method are:

1. Materials used are drawn from the cost record in a logical and systematic

manner.

2. Movement of materials in a continuous, orderly, single file manner represents a

condition necessary to and consistent with efficient materials control,

particularly for materials subject to deterioration, decay and quality are style

changes.

Limitations of FIFO Method

FIFO method is definitely awkward if frequent purchases are made at different prices

and if units from several purchases are on hand at the same time. Added costing

difficulties arise when returns to vendors or to the storeroom occur.

2) LAST IN FIRST OUT (LIFO) METHOD:-

The last in first out (LIFO) method of costing materials

issued is based on the premise that materials units issued should carry the cost of the

most recent purchase, although the physical flow may actually be different. The method

assumes that the most recent cost (the approximate cost to replace the consumed units)

is most significant in matching cost with revenue in the income determination

procedure.

Under LIFO procedures, the objective is to charge the cost of current

purchases to work in process or other operating expenses and to leave the oldest costs

in the inventory. Several alternatives can be used to apply the LIFO method. Each

procedure results in different costs for materials issued and the ending inventory, and

consequently in a different profit. It is mandatory, therefore, to follow the chosen

procedure consistently.

The advantages of the last in first out method are: Materials consumed are priced

in a systematic and realistic manner. It is argued that current acquisition costs are

incurred for the purpose of meeting current production and sales requirements;

therefore, the most recent costs should be charged against current production and

sales.

Unrealized inventory gains and losses are minimized, and reported operating profits are

stabilized in industries subject to sharp materials price fluctuations.

Inflationary prices of recent purchases are charged to operations in periods of rising

prices, Thus reducing profits, resulting in a tax saving, and therewith providing a cash

advantage through deferral of income tax payments. The tax deferral creates additional

working capital as long as the economy continues to experience an annual inflation rate

increase.

The disadvantages or limitations of the last in first out costing method are:

1. The election of last in first out for income tax purposes is binding for all

subsequent years unless a change is authorized or required by the Internal

Revenue Service (IRS)

2. This is a "cost only" method with no right down to the lower of cost or market

allowed for income tax purposes.

3. LIFO must be used in financial statements if it is elected for income tax

purposes. However, for financial reporting purposes, the lower of LIFO cost or

market can be used without violating IRS LIFO conformity rules.

4. Record keeping requirements under this method, as well as FIFO, are

substantially greater than those under alternative costing and pricing methods.

5. Inventories may be depleted due to unavailability of materials to the point of

consuming inventories costed at older or perhaps the oldest prices. This

situation will create a miss matching of current revenue and cost,

6. In standard number 411 "accounting for acquisition costs of materials, " the

cost accounting standards board "CASB" precludes the use of LIFO except

when applied currently on a specific identification basis. As a result, the use of

this method, when an annual LIFO adjustment is made, is ruled out for

government contracts to which CASB regulations apply.

3) AVERAGE COSTING METHOD:-

Issuing materials at an average cost assumes that each

batch taken from the storeroom is composed of uniform quantities from each

shipment in stock at the date of issue. Often it is not feasible to mark or label each

materials item with an invoice price in order to identify the used units with its

acquisition cost. It may be reasoned that units are issued more or less at random as for

as the specific units and the specific costs are concerned and that an average cost of all

units in stock at the time of issue is satisfactory measure of materials cost. However,

average costing may be used even though the physical withdrawal is an identifiable

order. If materials tend to be made up of numerous small items low in unit cost and

especially if prices are subject to frequent changes.

Advantages of Average Costing Method:

Average costing method has the following main advantages:

1. It is a realistic costing method useful to management in analyzing operating

results and appraising future production.

2. It minimizes the effect of unusually high or low materials prices, thereby making

possible more stable cost estimates for future work.

3. It is practical and less expensive perpetual inventory system.

The average costing method divides the total cost of all materials of a particular class

by the number of units on hand to find the average price. The cost of new invoices are

added to the total in the balance column; the units are added to the existing quantity;

and the new total cost is divided by the new quantity to arrive at the new average cost.

Materials are issued at the established average cost until a new purchase is recorded.

Although a new average cost may be computed when materials are returned to vendors

and when excess issues are returned to the storeroom, for practical purposes, it seems

sufficient to reduce or increase the total quantity and cost, allowing the unit price to

remain unchanged. When a new purchase is made and a new average is computed, the

discrepancy created by the returns will be absorbed.

a)Simple Average Method, issue price of materials are fixed at average unit price.

Simple average is an average of price without considering the quantities involved. The

average price is calculated by dividing the total of the rates of the materials in the stores

by the number of rates of prices.

Advantages Of Simple Average Method

Main advantages of simple average method are as follows:

1. Simple average method is very suitable when materials are received in uniform lot

quantities.

2. Simple average method is very easy to operate.

3. Simple average method reduces clerical work.

Disadvantages Of Simple Average Method

Major disadvantages of simple average method are as follows:

1. If the quantity in each lot varies widely, the average price will lead to erroneous costs.

2. Costs are not fully recovered.

3. Closing stock is not valued at the current assets.

b)Weighted Average Method:- The final method is called weighted average. This is a

"method in calculation in which the weighted average cost per unit for the period is the

cost of the goods available for sale divided by the number of units available for sale"

(Barron Education System). In this method, the order in which goods are purchased

does not matter. The costs of the goods are averaged at the end of the year to find your

cost of goods sold. The weighted average cost method is most commonly used in

manufacturing businesses where inventories are piled or mixed together and cannot be

differentiated, such as chemicals, oils, etc. Chemicals bought two months ago cannot

be differentiated from those bought yesterday, as they are all mixed together.

Main Reports:-

Materials ledger cards commonly show the account number, description or type of

material, location, unit measurement, and maximum and minimum quantities to carry.

These cards are the materials ledger with new cards prepared and old ones discarded as

changes occur in the types of materials carried in stock. The ledger card arrangement is

basically the familiar debit, credit, and balance columns under the description of

received, issued, and balance. Following is an example of material ledger card:

Example | Sample of materials ledger card:

Piece or Part No.____________________ Reorder

Point___________________

Description________________________ Reorder

Quantity_________________

Maximum Quantity__________________

Received Issue Balance

Date Res.

No Qty Amount Date

Res.

No Qty Amount Qty Unit cost Amount

Bin cards or stock cards are effective ready references that may be attached to

storage bins, shelves, racks, or other containers. Bin cards usually show quantities of

each type of materials received, issued, and on hand. They are not a part of the

accounting records as such, but they show the quantities on hand in the storeroom at

all times and should agree with the quantities on the materials ledger cards in the

accounting department.

Illustration: I Journalize the following transactions and prepare a cash ledger.

1. Ram invests Rs. 10, 000 in cash. 2. He bought goods worth Rs. 2000 from shyam. 3. He bought a machine for Rs. 5000 from Lakshman on account. 4. He paid to Lakshman Rs. 2000

5. He sold goods for cash Rs.3000 6. He sold goods to A on account Rs. 4000 7. He paid to Shyam Rs. 1000 8. He received amount from A Rs. 2000

Illustration II Journalize the following transactions and post them into Ledgers Jan 1. Commenced business with a capital of Rs. 10000 ,, 2. Bought Furniture for cash Rs. 3000 ,, 3. Bought goods for cash from ‘B’ Rs. 500 ,, 4. Sold goods for cash to A Rs. 1000 ,, 5. Purchased goods from C on credit Rs.2000 ,, 6. Goods sold to D on credit Rs. 1500 ,, 8. Bought machinery for Rs. 3000 paying Cash ,, 12. Paid trade expenses Rs. 50 ,, 18. Paid for Advertising to Apple Advertising Ltd. Rs. 1000 ,, 19. Cash deposited into bank Rs. 500 ,, 20. Received interest Rs. 500 ,, 24. Paid insurance premium Rs. 200 ,, 30. Paid rent Rs. 500 ,, 30. Paid salary to P Rs.1000 Illustration-III During January 2003 Narayan transacted the following business.

Date Transactions Amount

2003 Jan.1 ,, 2 ,, 3 ,, 4 ,, 5 ,, 6 ,, 7 ,, 8 ,, 9 , 10 , 11 , 12

Commenced business with cash Purchased goods on credit from Shyam Received goods from Murthy as advance for goods ordered by him Paid Wages Goods returned to shyam Goods sold to Kamal Goods returned by Kamal Paid into Bank Goods sold for Cash Bought goods for cash Paid salaries

40000 30000 3000 500 200 10000

500 500 750

1000. 700

1000

Journalize the above transactions and prepare cash Account

Illustration IV:

From the following list of balances prepare a Trial Balance as on 30-6-2003

i Opening Stock 1800 xiii Plant 750

ii Wages 1000 xiv Machinery tools 180

Illustration V Prepare a Trial Balance from the following Data for the year 2003.

Rs. Rs.

Freehold property 10800 Discount received 150

Capital 40000 Returns inwards 1590

Returns outwards 2520 Office expenses 5100

Sales 80410 Bad debts 1310

Purchases 67350 Carriage outwards(sales exp) 1590

Depreciation on furniture 1200 Carriage inwards 1450

Insurance 3300 Salaries 4950

Opening stock 14360 Book debts 11070

Creditors for expenses 400 Cash at bank 2610

Creditors 4700

Illustration: VI The following is the Trial Balance of Abhiram, was prepared on 31st March 2006. Prepare Trading and Profit& Loss Account and Balance Sheet.

Debit Rs. Credit Rs.

Capital

------ 22000

Opening stock 10000 ------

Debtors and Creditors 8000 12000

Machinery 20000 -------

Cash at Bank 2000 -------

Bank overdraft ------ 14000

Sales returns and Purchases returns 4000 8000

Trade expenses 12000 -------

Purchases and Sales 26000 44000

Wages 10000 -------

Salaries 12000 -------

Bills payable ------- 10600

Bank deposits 6600 -------

TOTAL Closing Stock was valued at Rs.60, 000

110600 110600

Illustration VII Prepare Trading and Profit &Loss A/C for the year ended 31.12.2001 and a Balance Sheet as on that date from the following Trial Balance.

iii Sales 12000 xv Lighting 230

iv Bank loan 440 xvi Creditors 800

v Coal coke 300 xvii Capital 4000

vi Purchases 7500 xviii Misc. receipts 60

vii Repairs 200 xix Office salaries 250

viii Carriage 150 xx Office furniture 60

ix Income tax 150 xxi Patents 100

x Debtors 2000 xxii Goodwill 1500

xi Leasehold premises 600 xxiii Cash at bank 510

xii Cash in hand 20

Dr, Rs. Cr, Rs.

Furniture 6500

Plant and machinery 60000

Buildings 75000

Capital 125000

Bad debts 1750

Reserve for bad debts 3000

Sundry debtors 40000

Sundry creditors 24000

Stock(1.1.2001) 34600

Purchases 54750

Sales 154500

Bank over draft 28500

Sales returns 2000

Purchase returns 1250

Advertising 4500

Interest 1180

Commission received 3750

Cash in hand 6500

Salaries 33000

General expenses 7820

Car expenses 9000

Taxes and insurance 3500

340000 340000

Closing stock valued at Rs. 50000 Illustration VIII The following figures have been extracted from the records of Fancy Stores a proprietary concern as on 31.12.2003.

Rs. Rs.

Furniture 15000 Insurance 6000

Capital A/C 54000 Rent 22000

Cash in hand 3000 Sundry debtors 60000

Opening stock 50000 Sales 600000

Fixed deposits 134600 Advertisement 10000

Drawings 5000 Postages & Telephone 3400

Provision for bad debts

3000 Bad debts 2000

Cash at Bank 10000 Printing and stationary 9000

Purchases 300000 General charges 13000

Salaries 19000 Sundry creditors 40000

Carriage inwards 41000 Deposit from customers 6000

Illustration IX

Prepare Trading, Profit and loss account and Balance sheet after taking into

consideration the following information.

a) Closing stock as on 31st March was Rs. 10000.

b) Salary of Rs. 2000 is yet to be paid to an employee.

Prepare Trading and Profit &Loss A/C for the year ended 31.12.2001 and a Balance Sheet as on that date from the following Trial Balance.

Debit Rs. Credit Rs.

Purchases 45000

Debtors 60000

Interest earned 1200

Salaries 9000

Sales 96300

Purchase returns 1500

Wages 6000

Rent 4500

Sales returns 3000

Bad debts return off 2100

Creditors 36600

Capital 31800

Drawings 7200

Printing and stationary 2400

Insurance 3600

Opening stock 15000

Office expenses 3600

Furniture and fittings 6000

GRAND TOTAL 167400 167400

Adjust the following a) Closing stock Rs.20000 b) Write off furniture @ 15% per annum.

UN IT – III

ISSUE OF SHARES AND DEBENTURES

CONCEPTS

Introduction

Company meaning, characteristics types

Share valuation, Issue of shares

Issue of shares premium & discount

Share forfeiture

Debenture valuation, Issue of Debenture

Issue of Debenture Premium & Discount

A company is a voluntary association of individuals formed to carry on business

to earn profits or for non profit purposes. These persons contribute towards the capital

by buying its shares in which it is divided. A company is an association of individuals

incorporated as a company possessing a common capital i.e. share capital contributed

by the members comprising it for the purpose of employing it in some business to earn

profit.

As per Companies Act 1956, a company is formed and registered under the

Companies Act or an existing company registered under any other Act”.

Characteristics of a Company

Following are the main characteristics of a company:

1) Artificial legal person

A company is an artficial person as it is created by law. It has almost all the

rights and powers of a natural person. It can enter into contract. It can sue in its own

name and can be sued.

2) Incorporated body

A company must be registered under Companies Act. By virtue of this, it is

vested with corporate personality. It has an identity of its own. Although the capital is

contributed by its members called shareholders yet the property purchased out of the

capital belongs to the company and not to its shareholders.

3)Capital divisible into shares

The capital of the company is divided into shares. A share is an indivisible unit

of capital. The face value of a share is generally of a small denomination which may be

of Rs 10, Rs 25 or Rs 100.

4) Transferability of shares

The shares of the company are easily transferable. The shares can be bought and sold

in the stock market.

5) Perpetual existence

A company has an independent and separate existence distinct from its share holders.

Changes in its membership due to death, insolvency etc. does not affect its existence

and its continuity.

6) Limited Liability

The liability of the shareholders of a company is limited to the extent of face value of

shares held by them. No shareholder can be called upon to pay more than the face

value of the shares held by them. At the most the shareholders may be asked to pay the

unpaid value of shares.

7) Representative Management

The number of shareholders is so large and scattered that they cannot manage the

affairs of the company collectively. Therefore they elect some persons among

themselves to manage and administer the company. These elected representatives of

shareholders are individually called the ‘directors’ of the company and collectively the

Board of Directors.

8) Common seal

A common seal is the official signature of the company. Any document bearing the

common seal of the company is legally binding on the company.

On the basis of ownership

On the basis of ownership, companies can be catagorised as :

(a) Private Company

A private company is one which by its Articles of Association :

(i) restricts the right of members to transfer its shares;

(ii) limits the number of its members to fifty (excluding its past and present employees);

(iii) prohibits any invitation to the public to subscribe to its shares, debentures.

(iv) The minimum paid up value of the company is one lakh rupees (Rs 100000).

The minimum number of shareholders in such a company is two and the company is

to add the words ‘private limited’ at the end of its name. Private companies do not

involve participation of public in general.

(b) Public Copmpany

A company which is not a private company is a public company. Its Articles of

association does not contain the above mentioned restrictions.

Main features of a public company are :

(i) The minimum number of members is seven.

(ii) There is no restriction on the maximum number of members.

(iii) It can invite public for subscription to its shares.

(iv) Its shares are freely tansferable.

(v) It has to add the word ‘Limited’ at the end of its name.

(vi) Its minimum paid up capital is five lakhs rupees (Rs 500,000).

SHARE VALUATION

A joint stock company divides its capital into units of equal denomination. Each

unit is called a share. These units i.e. shares are offered for sale to raise capital. This is

termed as issuing shares. A person who buys share/ shares of the company is called a