Embed Size (px)

Citation preview

September 22, 2011

2

Contents

Opportunities

Challenges

Indian Debt Market

3

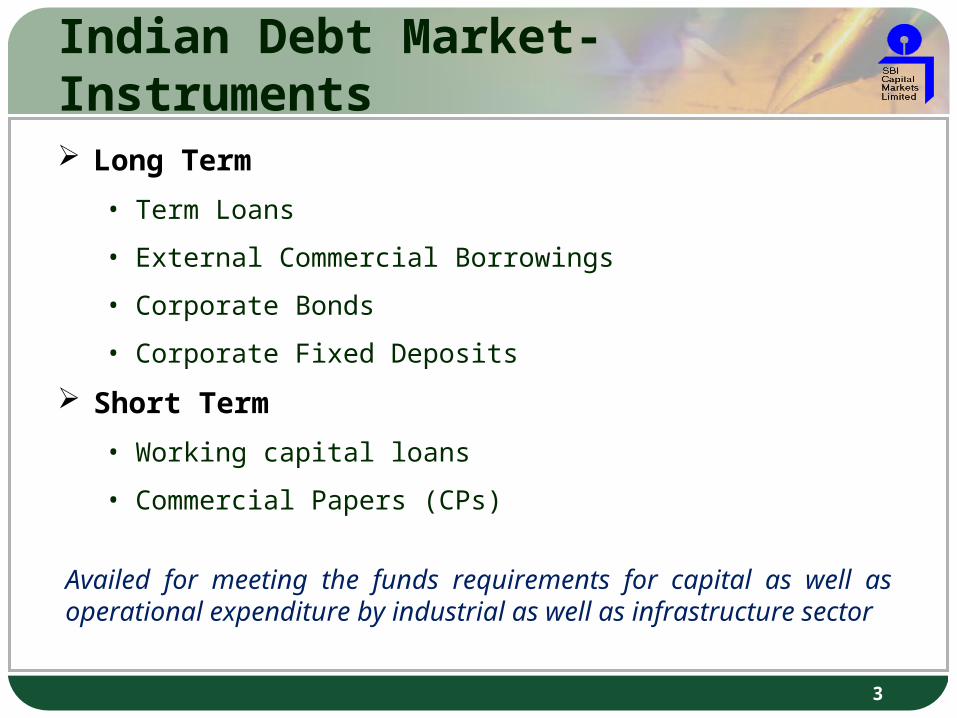

Indian Debt Market- Instruments Long Term

• Term Loans

• External Commercial Borrowings

• Corporate Bonds

• Corporate Fixed Deposits

Short Term• Working capital loans

• Commercial Papers (CPs)

Availed for meeting the funds requirements for capital as well as operational expenditure by industrial as well as infrastructure sector

4

Growth in Debt MarketParticulars July 2010

(Rs bn)July 2011

(Rs bn)YoY (%)

Growth in Bank CreditGross Bank Credit (Non Food)

32000 38000 19

-Industrial 14000 17000 21

-Infrastructure 4500 5500 22

Source: Research reports on www.securities.com, AsianBonds Online, *Source (Estimates): Based on Ministry of Finance, March 2010 report

Growth in Bond MarketBond Market 31,905 36,675 15

-Corporate 5,625 8,100 44

-Government 26,280 28,575 9

Growth in ECB/ External Debt* ECB/ External Debt 12250 14260 16

-Government 3400 4300 26

-Non Government 8850 9960 13

5

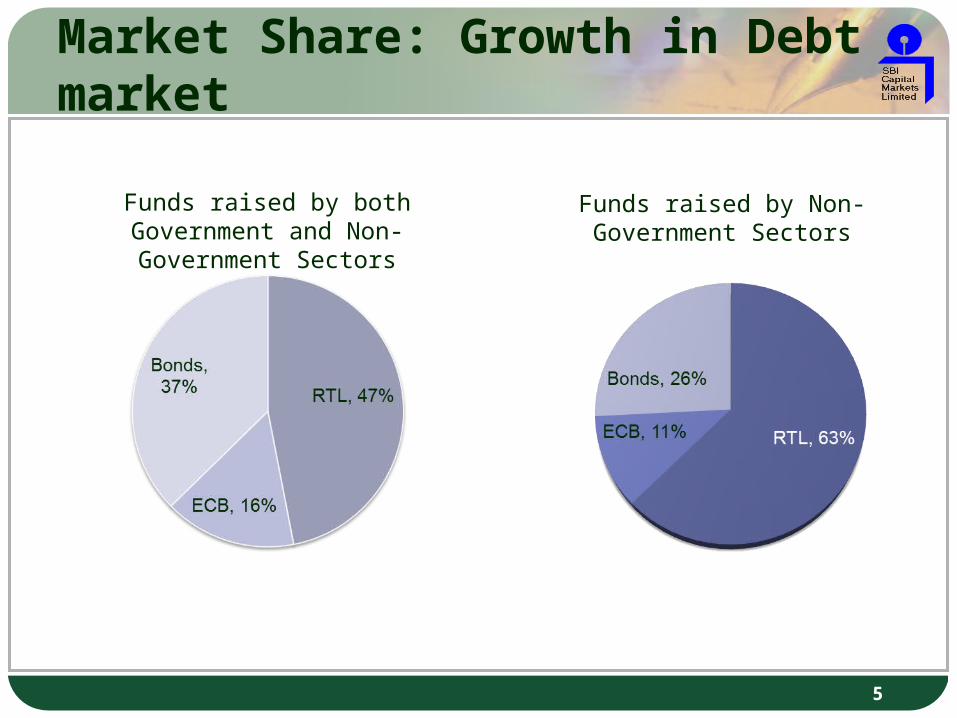

Market Share: Growth in Debt market

Funds raised by both Government and Non-Government Sectors

Funds raised by Non-Government Sectors

6

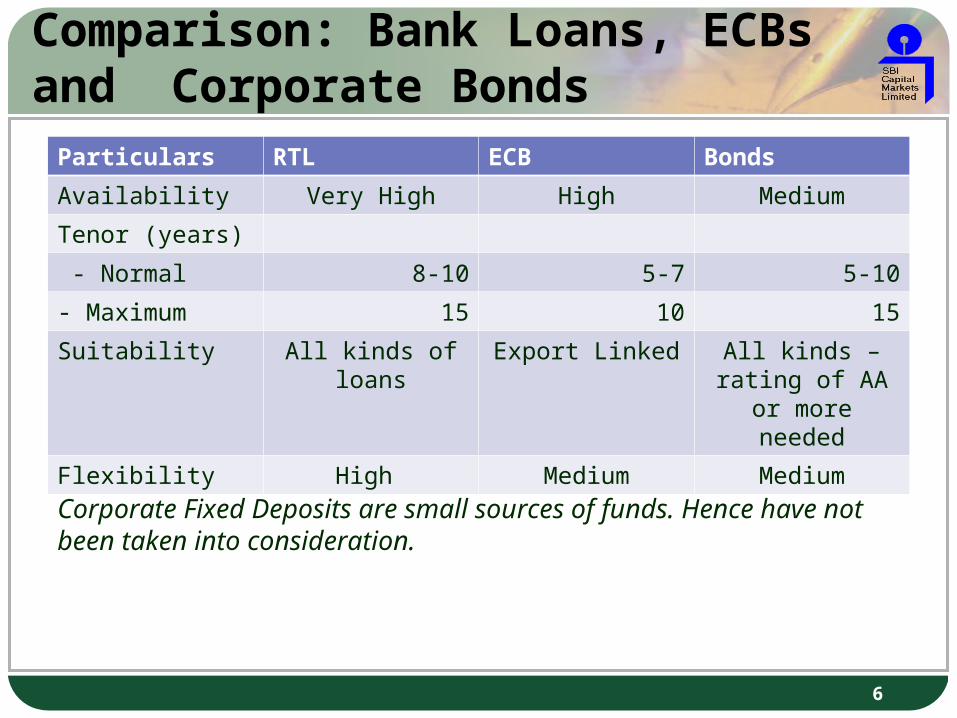

Comparison: Bank Loans, ECBs and Corporate Bonds

Particulars RTL ECB BondsAvailability Very High High Medium

Tenor (years)

- Normal 8-10 5-7 5-10- Maximum 15 10 15

Suitability All kinds of loans Export Linked All kinds – rating of AA or more

needed

Flexibility High Medium Medium

Corporate Fixed Deposits are small sources of funds. Hence have not been taken into consideration.

7

Contents

Challenges

Opportunities

Indian Debt Market

8

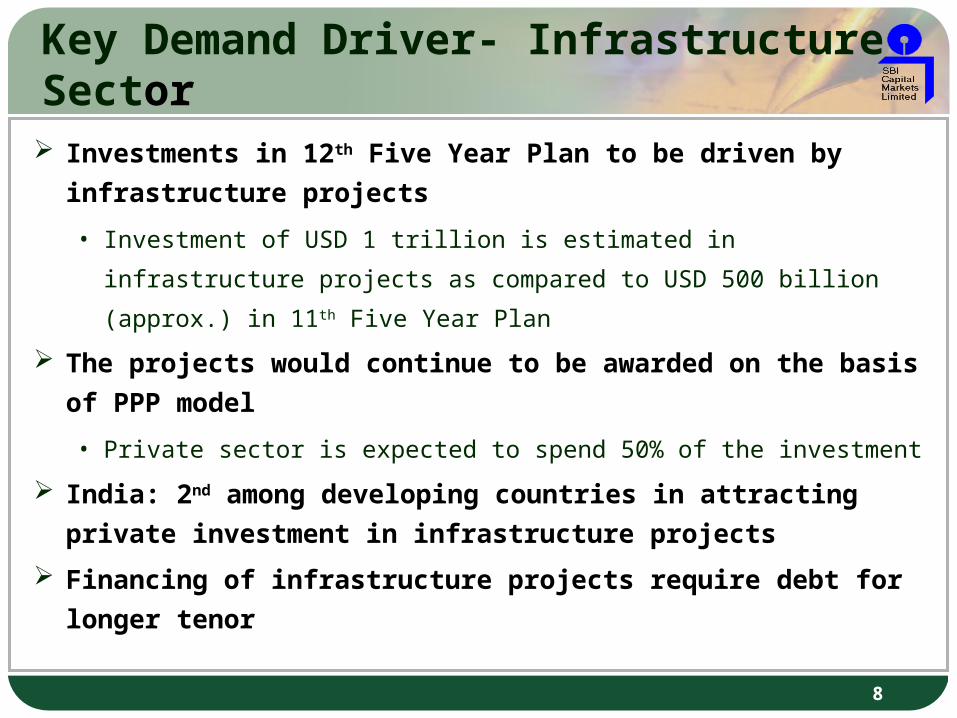

Key Demand Driver- Infrastructure Sector

Investments in 12th Five Year Plan to be driven by infrastructure projects• Investment of USD 1 trillion is estimated in infrastructure projects as

compared to USD 500 billion (approx.) in 11th Five Year Plan

The projects would continue to be awarded on the basis of PPP model• Private sector is expected to spend 50% of the investment

India: 2nd among developing countries in attracting private investment in infrastructure projects

Financing of infrastructure projects require debt for longer tenor

9

Contents

Opportunities

Challenges

Indian Debt Market

10

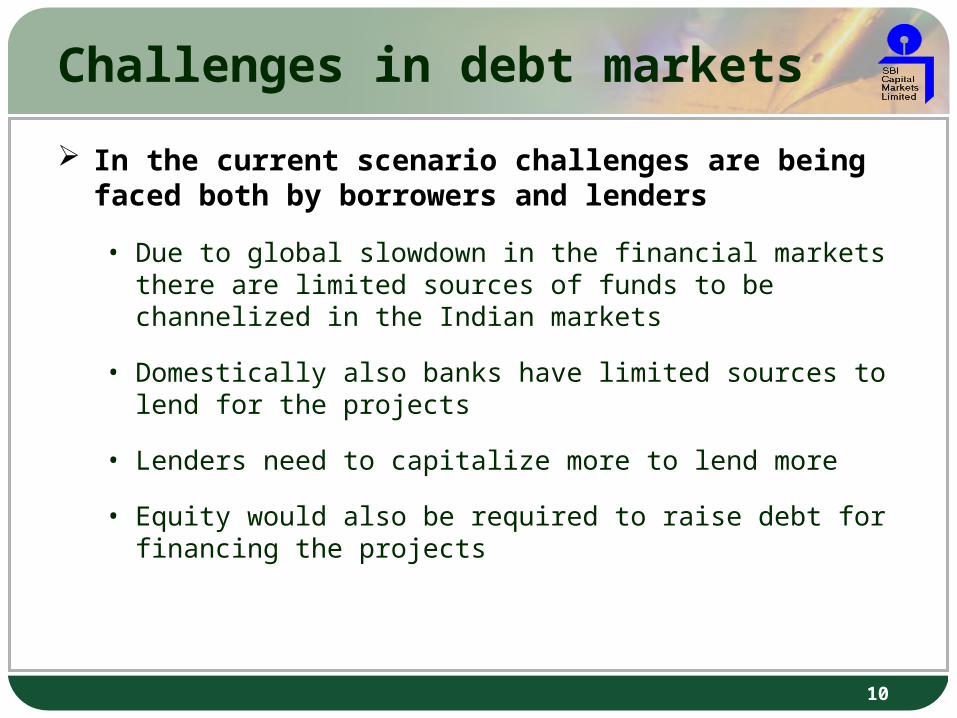

Challenges in debt markets In the current scenario challenges are being faced both

by borrowers and lenders

• Due to global slowdown in the financial markets there are limited sources of funds to be channelized in the Indian markets

• Domestically also banks have limited sources to lend for the projects

• Lenders need to capitalize more to lend more

• Equity would also be required to raise debt for financing the projects

11

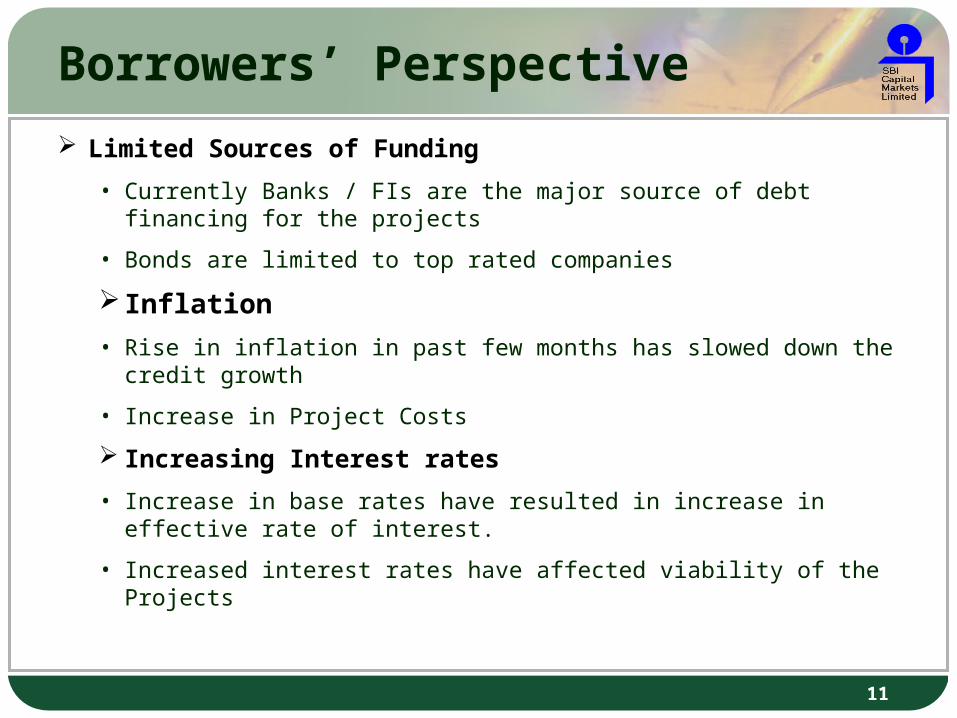

Borrowers’ Perspective Limited Sources of Funding

• Currently Banks / FIs are the major source of debt financing for the projects

• Bonds are limited to top rated companies

Inflation• Rise in inflation in past few months has slowed down the credit growth

• Increase in Project Costs

Increasing Interest rates• Increase in base rates have resulted in increase in effective rate of

interest.

• Increased interest rates have affected viability of the Projects

12

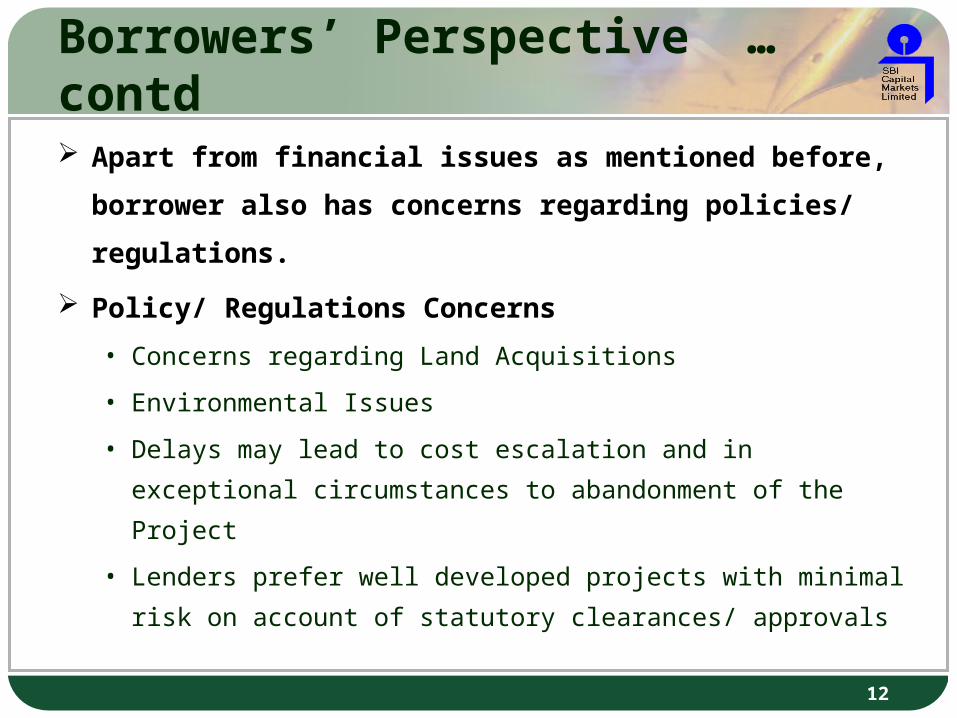

Borrowers’ Perspective …contd Apart from financial issues as mentioned before, borrower

also has concerns regarding policies/ regulations.

Policy/ Regulations Concerns• Concerns regarding Land Acquisitions

• Environmental Issues

• Delays may lead to cost escalation and in exceptional circumstances to abandonment of the Project

• Lenders prefer well developed projects with minimal risk on account of statutory clearances/ approvals

13

Term Lenders’ Perspective

Credit exposure limits • Close to being breached in infrastructure sectors esp. power

• Any future exposure seems to be severely constrained by balance sheet size and incremental credit growth

• Rising demands across all sectors

Increasing NPAs• RBI estimates NPAs to rise to 2.92% by March 31, 2012, an

increase by 25% (y-o-y), in the backdrop of global slowdown

Asset-Liability mismatch is also a concern for Lenders

14

Conclusion

Enablers for further borrowing

• More robust policy and regulatory regime

• Better capitalized banks

• New Instruments

Take – out financing

New Debt Instruments like Infrastructure Debt Fund, Clean Energy Funds etc

• Deepening of Insurance/Pension and bond markets

15

Thank You !!!