Embed Size (px)

Citation preview

1

M.Com. Fourth Semester Examination (Year 2016)

Advertising & Sales Management Subject Code: MCOM-401

Paper Code: TMT-291 Time : 20 Minutes

M.Marks : 10

Section A

[k.M v

(Objective Type Question)

¼oLrqfu"B Á’u½

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking the

correct answer.

lHkh iz’u vfuok;Z gSaA izR;sd iz’u gsrq 1 vad fu/kkZfjr gSA lgh mÙkj gsrq fn;s x;s ckDl esa () fpUg dk

iz;ksx djsaA

Q. No. I. Choose the correct answer-

lgh mÙkj pqfu,&

1- Which of the following is considered a non-personal form of any paid presentation

or promotion?

fuEufyf[kr esa ls D;k ,d iznÙk izdkj dh xSj&O;fDrxr izn'kZu ;k lao)Zu gS\

a) Direct Marketing b) Advertising

izR;{k foi.ku foKkiu

c) Personal Selling d) Sales Promotion

oS;fDrd foØ; foØ; lao)Zu

2. The _________ advertising objectives would be suggesting new uses of a product

and explaining how it works.

foKkiu ds -------------------- mís';] ,d oLrq ds uke mi;ksxksa ,oa mlds ladeksZa ds fy, lq>ko

iznku djrs gSA

a) Service b) Reminder

lsok vuqLekjd

c) Informative d) Persuasive

lwpukRed Bksl

3. The concept under which a company carefully integrates and coordinates its many

communication channels is called ________.

,d O;olk; ------------------------ vo/kkj.kk esa lko/kkuh ls dbZ lapkj pSuyksa dks ,dhd̀r ,oa

funsZf'kr djrk gSA

a) Non-personal communication

voSfDrd lapkj

b) Integrated marketing communication

laxfBr foi.ku lapkj

c) Hybrid communication

ladj lapkj

d) Parallel communication

lekUrj lapkj

Roll No.

Enrollment No. Enrollment No.

Invigilator’s Signature

2

4. The moral principles and values that govern actions and decisions are called

__________.

dk;Z ,oa fu.kZ;ksa dks izHkkfor djrs uSfrd fl)karksa ,oa ewY;ksa dks ------------------ dgrs gSA

a) Social responsibility

lkekftd ftEesnkjh

b) Macro-marketing problem

eSØks foi.ku leL;k

c) Micro-marketing problem

ekbØks foi.ku leL;k

d) Ethics

vkpkj uhfr

5. Which of the following media type has flexibility, good local market coverage and

broad acceptance as characteristics?

fuEufyf[kr esa ls fdl ehfM;k esa yphykiu] vPNh LFkkuh; cktkj dojst vkSj O;kid

Lohd`fr dh fo'ks"krk,¡ gS\

a) Television b) Newspaper

Vsyhfotu lekpkj i=

c) Radio d) Magazine

jsfM;ks if=dk

6. A message comes not only from a source, but also through some ___________

lans'k u dsoy ,d lzksr ls] cfYd ,d ------------------------ ds }kjk Hkh Hkstk tkrk gSA

a) Message media

lans'k ehfM;k

b) Communication channel

lapkj ek/;e

c) Message channel

lans'k ek/;e

d) None of these

mijksä esa ls dksbZ ugha

7. Which of the following is not one of the promotion jobs set forth in AIDA model?

AIDA ekWMy ds }kjk fu/kkZfjr lao)Zu dk;Z ds varjxr fuEufyf[kr ls dkSu ugha gS\

a) Attention b) Information

/;ku lwpuk

c) Desire d) Action

bPNk dk;Z

8. Among the following which does not promote the importance of media planning

function?

ehfM;k vk;kstu dk;Z dh fo'ks"krk dks fuEufyf[kr esa ls D;k c<+kok ugha nsrk\

a) Media fragmentation

ehfM;k fo[kaMu

b) Development of Internet

baVjusV dk fodkl

c) Soaring media cost

ehfM;k ds c<+rs ykxr

d) Focussed target Marketing strategies

y{; dsfUnzr foi.ku dk;Zuhfr

3

9. Which of the following budget methods ignores the effects of promotion on sales?

fuEufyf[kr esa ls dkSu esa ctV fof/k esa foØ; ij lao)Zu ds izHkkoksa ij /;ku ugha nsrk\

a) Affordable method

ogu fof/k

b) Percentage of sales method

foØ; izfr'krrk fof/k

c) Competitive parity method

Li/kkZRed lerk fof/k

d) Objective & Task method

mís'; ,oa dk;Z fof/k

10. In evaluating messages for advertising, telling how the product is better than

competing brands aims at making the ad:

foKkiu ds lans'kksa ds ewY;kadu esa] ftlesa foKkiu oLrq dk izfrLif/kZr czS.M ls mÙke

crkrk gS% a) Meaningful b) Distinctive

lkFkZdrk fo'ks"krk

c) Believable d) Remembered

eqefdu ;kn j[kus ;ksX;

-----------------------------

M.Com. Fourth Semester Examination (Year 2016)

Advertising & Sales Management Subject Code: MCOM-401

Paper Code: TMT-291 Time : 2:40 hours

M.Marks : 60

Section B

[k.M c (Short Answer Type Questions)

(y?kqmÙkjh; iz’u)

Attempt all questions. Each question carries 4 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 4 vad fu/kkZfjr g SA

Q.No.2. What is advertisement and state its objectives?

foKkiu D;k gS\ mlds mís';ksa dk mYys[k dhft,A

OR

Discuss the role of ethics in advertising.

foKkiu esa uSfrd ewY;ksa dh Hkwfedk ij fopkj dhft,A

Q.No.3. What do you mean by 'Novelty Advertisement'?

^vfHkuo foKkiu* ls vki D;k le>rs gSa\

OR

Write a short note on 'layout'.

Roll No.

4

^[kkdk fuekZ.k* ij laf{kIr fVIi.kh fyf[k,A

Q.No.4. What do you understand by client agency relationship?

DykbaV ,tsalh laca/k ls vki D;k le>rs gS\

OR

State the factors affecting advertising expenses.

foKkiu ds O;;ksa dks izHkkfor djus okys rRoksa dk mYys[k dhft,A

Q.No.5. Describe the limitations of 'sales promotion'.

^foØ; lao)Zu* dh lhekvksa dk o.kZu dhft,A

OR

Explain the mutual relations between 'advertising' and 'personal selling'.

^foKkiu* rFkk ^O;fDrxr foØ;* esa ikjEifjd laca/kksa dks Li"V dhft,A

Q.No.6. Explain in brief the functions of a salespersons or salesman.

foØ;drkZ ;k foØ;drkZvksa ds dk;Z dks laf{kIr esa le>kb,A

OR

What is the process of job analysis?

dk;Z fo'ys"k.k dh izfØ;k D;k gSa\

Section C

[k.M l (Long Answer Type Questions)

(nh?kZ mÙkjh; iz’u)

Attempt all questions. Each question carries 8 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 8 vad fu/kkZfjr gSA

Q.No.7. Examine carefully the principles of advertising.

,d izHkkoh foKkiu ds fl)karks dks Li"V dhft,A

OR

What is the stimulation process by advertising concept?

foKkiu ds fl)kar ls LVheqys'ku izfØ;k D;k gS\

Q.No.8. Write a critical note on the different media of advertisement and their proper

selection.

foKkiu ds fofHkUu ek/;eksa rFkk muds mfpr pquko ij ,d foospukRed fVIi.kh dhft,A

OR

What are the main elements of advertisement copy? At the time of building

advertisement copy what precautions are essential?

,d foKkiu izfr ds rRo dkSu ls gS\ foKkiu izfr;k¡ cukrs le; dkSu lh lko/kkfu;k¡

vko';d gS\

Q.No.9. "Advertising agency is an intermediate between corporate and client". How does

this role play an important factor for success of an advertising?

^^foKkiu ,tsalh dkWiksZjsV rFkk xzkgd ds chp ,d ek/;e gSA** ,d foKkiu ds fy, ,d

egRoiw.kZ dkjd ds :Ik esa ;g dSlh Hkwfedk fuHkkrk gS\

OR

What is the relevance of budgeting decisions in advertising?

5

foKkiu esa ctV ds fu.kZ; dh D;k izklafxdrk gS\

Q.No.10. What do you mean by 'Personal selling'? How does it differ from advertising?

O;fDrxr foØ; ls vki D;k le>rs gS\ ;g foKkiu ls fdl izdkj fHkUu gS\

OR

Discuss the merits and demerits of choosing a career in salesmanship.

foØ; dk;Z dks thou o`fÙk ds :Ik esa pquus ds ykHk ,oa nks"kksa dh foospuk dhft,A

Q.No.11. Discuss the supervision techniques in evaluating and controlling sales force.

foØ; cy dk ewY;kadu rFkk fu;a=.k djus esa i;ZosZ{k.k rduhd ij ppkZ dhft,A

OR

"Sales management is the management of sales force". How far do you agree with

this statement? Substantiate.

^^foØ; cy dk izca/ku gh foØ; izca/ku gS** vki bl dFku ls fdruk lger gS\ fl)

dhft,A

-----------------------------

M.Com. Fourth Semester Examination (Year 2016)

Consumer Behaviour Subject Code: MCOM-402

Paper Code: TMT-292 Time : 20 Minutes

M.Marks : 10

Section A

(Objective Type Questions)

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking the

correct answer.

Q. No. I. Fill in the blanks-

1. Random thoughts lead to a ……………… awareness of needs.

2. ………………. is responsible for those responses which are learnt from the

surrounding people.

Choose the correct answer-

3. Personality and attitude never change, they always remain same under each type of

circumstances.

a) True b) False

4. In an advertisement message is the ……………and creativity is ………..

a) Ground/Figure b) Figure, Ground

Roll No.

Enrollment No.

Invigilator’s Signature

6

c) Both (a) and (b) d) None of these

5. A group comprises of two or more people who are independent of each other.

a) True b) False

6. Formal groups arise spontaneously in the organization.

a) True b) False

7. Changes in consumer values have been recognized by many business firms that

have expanded their emphasis on _____________ products.

a) Latest Technology

b) Time saving, convenience-oriented

c) Health related

d) Communication

8. The middle class is differentiated from the working class in that the former tends to

emulate ……………..in their buying decisions.

a) Hollywood Stars b) Neighbours

c) Upper Americans d) popular leaders

9. ----------------------- are the groups that the individuals look to when forming

attitudes and opinions.

a) Reference groups b) Teenage groups

c) Religious Groups d) Adult groups

10. Secondary reference group include-

b) Family and close friends

c) Sports groups

c) Ethnic and religious groups

d) Fraternal organizations and professional associations

--------------------------------

7

M.Com. Fourth Semester Examination (Year 2016)

Consumer Behaviour Subject Code: MCOM-402

Paper Code: TMT-292 Time : 2:40 hours

M.Marks : 60

Section B (Short Answer Type Questions)

Attempt all questions. Each question carries 4 marks.

Q.No.2. Define the term ''Consumer Behaviour''.

OR

What refers to consumer as learner?

Q.No.3. What is the decision making process of an organization?

OR

Explain the characteristics of organizations buying behaviour?

Q.No.4. Explain the importance of motivation?

OR

What do you mean by dynamic nature of motivation?

Q.No.5. How does personality develops?

OR

What is the make-up of self image?

Q.No.6. ''In each class, life styles differ.'' Do you agree? Give reasons.

OR

Explain the nature of social-class.

Section C (Long Answer Type Questions)

Roll No.

8

Attempt all questions. Each question carries 8 marks.

Q.No.7. What are the factors which influence consumer behaviour? Explain them.

OR

What do you understand by attitude formation? Discuss the process of attitude

formation.

Q.No.8. Explain various stages of consumer behaviour?

OR

Differentiate between organizations and consumer buying behaviour?

Q.No.9. Discuss "Marketers don’t create needs, needs create the marketers."

OR

Discuss new approaches to motivation in organizations.

Q.No.10. Who are opinion leaders? Explain the qualities of an opinion leader.

OR

What is Jungian theory of personality and its application to marketing situations?

Q.No.11. Discuss the role of social class in formulation of consumer behaviour?

OR

Explain in detail the model of consumer decision.

-----------------------------

9

M.Com. Fourth Semester Examination (Year 2016)

Rural & Agricultural Marketing Subject Code: MCOM-403

Paper Code: TMT-293 Time : 10 Minutes

M. Marks: 10

Section A

[k.M v

(Objective Type Questions)

¼oLrqfu"B Á’u½

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking the

correct answer.

lHkh iz’u vfuok;Z gSaA izR;sd iz’u gsrq 1 vad fu/kkZfjr gSA lgh mÙkj gsrq fn;s x;s ckDl esa () fpUg dk

iz;ksx djsaA

Q.No.1. Choose the correct answer-

lgh mÙkj pqfu,&

1. Types of Rural Market are-

xzkeh.k cktkjksa ds izdkj gksrs gSa&

a) 2 b) 3

nks rhu

c) 4 d) 5

pkj ik¡p

2. "Product differentiation and market segmentation are alternative market strategies."

This statement is of-

**mRikn fofHkUuhdj.k rFkk cktkj foHkfädj.k oSdfYid foi.ku O;wg jpuk gS-** ;g dFku

gSa&

a) Kotler b) Smith

dksVyj fLeFk

c) Pearce d) Daver

ih;lZ Mkoj

3. Distribution of free sample is an example of-

Ukewuksa dk eq¶r forj.k mnkgj.k gS&

a) Dealer Promotion b) Consumer Promotion

O;kikjh laoa)Zu miHkksäk laoa)Zu

c) Both (a) and (b) d) None of these

nksuksa (a) ,oa (b) mijksDr esa ls dksbZ ugha

4. Kinds of future business is-

Hkkoh lkSnksa dk izdkj gS&

a) Speculative business b) Cash business

lêk lkSns udn lkSns

c) Ready business d) None of these

rS;kj lkSns mijksDr esa ls dksbZ ugha

Invigilator’s Signature

Roll No.

Enrollment No.

10

5. Kinds of speculator-

ifjdYid ds izdkj&

a) Two b) Three

nks rhu

c) Four d) Five

pkj ik¡p

6. Agricultural consumers goods is-

d`"kdh; miHkksäk eky gS&

a) Wheat b) Cotton

xsgw¡ dikl

c) Jute d) None of these

twV mijksDr esa ls dksbZ ugha

7. Agricultural Product Market Act in M.P. -

e/;izns'k esa d`f"k mit eaMh vf/kfu;e gS&

a) 1959 b) 1956

mUuhl lkS mulB mUuhl lkS NiUu

c) 1960 d) 1961

mUuhl lkS lkB mUuhl lkS bdlB

8. Regulated market expenditure is a burden-

fu;fer cktkj O;; Hkkj gS&

a) On consumers b) On Industries

miHkksäkvksa ij m|ksxksa ij

c) On Businessman d) None of these

O;kikfj;ksa ij mijksDr esa ls dksbZ ugha

9. Forms of specialization is-

fof'kf"Vdj.k dk Lo:Ik gS&

a) Labour b) Profession

Je is'kk

c) Industrial d) All of these

vkS|ksfxd mijksDr esa ls lHkh

10. Types of Labelling is-

yscfyax dk izdkj gS&

a) Brand b) Warranty

czkaM okjaVh

c) Packaging d) None of these

iSdsftax mijksDr esa ls dksbZ ugha

&&&&&&&&&&&&&&&&

11

M.Com. Fourth Semester Examination (Year 2016)

Rural & Agricultural Marketing Subject Code: MCOM-403

Paper Code: TMT-293 Time : 2 Hrs. 50 Mts.

M.Marks : 60

Section B

[k.M c (Short Answer Type Questions)

(y?kq mÙkjh; iz’u)

Attempt all questions. Each question carries 4 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 4 vad fu/kkZfjr gSA

Q.No.2. Discuss the characteristics of rural marketing?

xzkeh.k foi.ku dh fo'ks"krk,¡ fyf[k,\

OR What do you understand by visual communication? Explain.

n`"; lapkj ls vki D;k le>rs gSa\ le>kb,A

Q.No.3. Explain the process of agricultural marketing.

d`f"k foi.ku dh izfØ;k le>kb,A

OR

What is Agricultural Policy of India?

Hkkjr dh d`f"k uhfr D;k gS\

Q.No.4. Write a note on channel strategy?

Okkfgdk O;wg jpuk ij fVIi.kh fyf[k,A

OR Discuss the type of future Transactions.

Hkkoh lkSnksa ds izdkj le>kb,A

Q.No.5. Explain the present marketing regulation.

orZeku foi.ku fo;eu dks le>kb,A

OR

What do you understand by co-operative marketing?

Lkgdkjh foi.ku ls vki D;k le>rs gSa\

Q.No.6. Briefly discuss the factors affecting transportation cost.

Ikfjogu ykxr dks izHkkfor djus okys dkjdksa dks la{ksi esa crkb,A

OR

What are the advantages of processing?

izfØ;.k ls D;k ykHk gS\

Section C

[k.M l (Long Answer Type Questions)

(nh?kZ mÙkjh; iz’u)

Attempt all questions. Each question carries 8 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 8 vad fu/kkZfjr gSA

Roll No.

12

Q.No.7. Discuss in detail the factors affecting the selection of distribution channel.

forj.k okfgdk ds p;u dks izHkkfor djus okys dkjdksa dk lfoLrkj o.kZu dhft,A

OR

What do you understand by product line polices and strategies? Discuss.

mRikn iafä dh uhfr;ksa vkSj ;qfä;ksa ls vki D;k le>rs gSa\ lfoLrkj le>kb,A

Q.No.8. What is Agricultural Market? Describe various components of Agricultural Market.

d`f"k cktkj D;k gS\ d`f"k cktkj ds fofHkUu ?kVdksa dk o.kZu dhft,A

OR

Write a critical appraisal of Dynamics of Market structure.

cktkj lajpuk dh fØ;k'khyrk dh vkykspukRed O;k[;k dhft,A

Q.No.9. What are the fundamental concepts of modern marketing?

vk/kqfud foi.ku dh izeq[k vo/kkj.kk,a D;k gSa\

OR

What are the salient features of organized markets? Explain the difference between

organized and regulated markets.

LkaxfBr cktkj ds izeq[k rRo D;k gSa\ laxfBr cktkj vkSj fu;fer cktkj eas varj Li"V

dhft,A

Q.No.10. Giving an example, explain how regulated markets are organized?

fu;fer cktkjksa dks dSSls laxfBr fd;k tkrk gS\ ,d mnkgj.k nsdj le>kb,A

OR

Write an essay on co-operative marketing.

Lkgdkjh foi.ku ij ,d fuca/k fyf[k,A

Q.No.11. Define brand and trade mark. How they are different from each other? Enumerate

the characteristics of a good brand.

czkaM vkSj VsªM ekdZ dks ifjHkkf"kr dhft,A nksuksa ds varj dks Li"V dhft,A vPNs czkaM dh

fo'ks"krkvksa dk o.kZu dhft,A

OR

Critically examine the status of standardization and grading in India.

Hkkjr esa izek.khdj.k vkSj Js.kh;u dh fLFkfr dh vkykspukRed foospuk dhft,A

----------------------

13

M.Com. Fourth Semester Examination (Year 2016)

International Marketing Subject Code: MCOM-404

Paper Code: TMT-294

Time : 20 Minutes

M.Marks : 10

Section A

(Objective Type Questions)

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking the

correct answer.

Q. No. I. Choose the correct answer-

1. Ultimately ………………. was replaced by the …………… on 1st Jan 1995.

a) GATT, WTO b) WTO, GATT

c) GATS, WTO d) IMF, GATT

2. Which is the right sequence of a stages of Internationalization?

a) Domestic, Transnational, Global, International, Multinational

b) Domestic, International, Multinational, Global, Transnational

c) Domestic, Multinational, International, Transnational, Global

d) Domestic, International, Transnational, Multinational, Global

3. The tie up of Allianz Company with Bajaj is an example for-

a) Licensing b) Subcontracting

c) Joint Venture d) Subsidiaries

4. The primary focus of International Marketing is on-

a) Place b) Product

c) Price d) All of these

5. State one most important reason for the trade to become international.

Roll No.

Enrollment No.

Invigilator’s Signature

14

a) Technology

b) Improved Transportation

c) Communication

d) Warehouse

6. FII stands for-

a) Foreign Institutional Investors

b) Foreign Institutional Institutes

c) Foreign Institutions of India

d) Foreign Investment of India

7. When was EXIM Bank of India was established?

a) 1978 b) 1985

c) 1982 d) 1995

8. The four P's marketing includes-

a) Product b) Price

c) Place, Promotion d) All of these

9. Traders that handles their own exports are engaged in-

a) Direct Trading

b) Licensing

c) Indirect Trading

d) Contract Manufacturing

10. Trade Restrictions includes-

a) Legislation & Quotas b) Non tarrif barriers

c) Taxes & Tarrifs d) All of these

------------------------------

15

M.Com. Fourth Semester Examination (Year 2016)

International Marketing Subject Code: MCOM-404

Paper Code: TMT-294

Time : 2:40 hours

M.Marks : 60

Section B (Short Answer Type Questions)

Attempt all questions. Each question carries 4 marks.

Q.No.2. Throw a light on the significance of International marketing Environment.

OR

What are the various factors that affect the International marketing environment?

Q.No.3. What do you mean by Export organization. Describe the types of export

organization.

OR

What are the various factors that are stated in international price quotation?

Q.No.4. What is Indirect trading? Explain the various methods of payment in international

marketing.

OR

Write a note on foreign exchange bill. Explain the various features of it.

Q.No.5. Illustrate the role of EXIM Bank.

OR

Explain the various methods of Export credit.

Q.No.6. Write a short note on bilateral and multilateral trade agreement.

OR

Explain the role of SAARC in detail.

Section C (Long Answer Type Questions)

Roll No.

16

Attempt all questions. Each question carries 8 marks.

Q.No.7. What is International marketing? Discuss the external International marketing

environment forces and its effect.

OR

Bring out the important points that need to be considered while identifying and

selecting the foreign market.

Q.No.8. Discuss the factors that influence pricing.

OR

Briefly discuss the various methods of pricing.

Q.No.9. Write a note on direct trading describes the various methods of direct trading.

OR

List down the various methods adopted for making international payments and

explain all the methods in detail.

Q.No.10. Discuss in detail the role of Export-Import Bank in India in foreign trade.

OR

Write a detailed note on the various factors that have an impact on export credit.

Q.No.11. What are the benefits and limitations of direct exporting?

OR

Elaborate the various documents that are required in foreign trade.

-----------------------------

17

M.Com. Fourth Semester Examination (Year 2016)

Corporate Accounting Subject Code: MCOM-405

Paper Code: TMT-295 Time : 10 Minutes

M.Marks : 10

Section A

[k.M v (Objective Type Questions)

¼oLrqfu"B Á’u½

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking the

correct answer.

lHkh iz’u vfuok;Z gSaA izR;sd iz’u gsrq 1 vad fu/kkZfjr gSA lgh mÙkj gsrq fn;s x;s ckDl esa () fpUg dk

iz;ksx djsaA

Q. No. I. Choose the correct answer-

lgh mÙkj pqfu,&

1- The shares can be issued-

va'kksa dk fuxZeu fd;k tk ldrk gS%&

a) At face value b) At discount

vafdr ewY; ij cês ij

c) At premium d) All of these

izC;kft ij mijksä lHkh

2. Preference Shareholder's are-

iwokZf/kdkj va'k/kkjh gS&

a) Customers of the Company

dEiuh ds xzkgd

b) Creditors of the Company

dEiuh ds ysunkj

c) Owners of the Company

dEiuh ds Lokeh

d) All of these

mijksä lHkh

3. Discount on issue of debentures is-

_.ki=ksa ds fuxZeu ij cêk gS&

a) Fixed Assets b) Current Assets

LFkk;h lEifÙk pkyw lEifÙk

c) Real Assets d) Fictitious Assets

okLrfod lEifÙk cukoVh lEifÙk

4. The profit prior to incorporation of Company is-

dEiuh ds lekesyu ls iwoZ dk ykHk gksrk gS&

a) A revenue profit b) Capital profit

vk;xr ykHk iw¡thxr ykHk

c) Divisible profit d) None of these

Roll No.

Enrollment No. Enrollment No.

Invigilator’s Signature

18

foHkktu ;ksX; ykHk mijksDr esa ls dksbZ ugha

5. When shares are forfeited, the share capital account is debited by-

va'kksa ds gj.k ij va'k iw¡th ys[kk MsfcV gksxk&

a) Nominal value of shares b) Called up amount

va'kksa ds vafdr ewY; ij ek¡xh x;h jkf'k ls

c) Paid up amount d) All of these

pqdkbZ xbZ jkf'k ls mijksDr lHkh

6. Calls in arrears is shown in the Balance Sheet under the head.

vof'k"V ;kpuk fpës esa fuEu 'kh"kZd ds v/khu n'kkZ;h tkrh gSA

a) Share Capital

va'k iw¡th

b) Reserve and Surplus

lap; ,oa vfrjd

c) Current Liabilities and provisions

pkyw nkf;Ro ,oa izko/kku

d) Unsecured Loan

vlqjf{kr _.k

7. Dividends are usually paid on-

lkekU;r% ykHkka'k dk Hkqxrku fd;k tkrk gS&%

a) Authorized Capital b) Issued Capital

izkf/kd`r iw¡th ij fuxZfer iw¡th ij

c) Paid-up Capital d) Reserve Capital

pqdrk iw¡th ij lafpr iw¡th ij

8. When the proposed dividend is 16% of paid up capital, the percentage of profit

transferred to reserve should be-

;fn izLrkfor ykHkka'k pqdrk iw¡th ij 16% gS rks lap; esa vUrfjr ykHk dk izfr'kr

gksxkA

a) 2.5% b) 5%

2-5 izfr'kr~ 5 izfr'kr~

c) 7.5% d) 10%

7-5 izfr'kr~ 10 izfr'kr~

9. A new company pay's for the purchases consideration as under-

,d u;h dEiuh Ø; izfrQy dk Hkqxrku djrh gS&

a) In cash b) Through bank

jksdM+ esa cSad ds ek/;e ls

c) By shares d) By Debentures

va'kksa }kjk _.ki=ksa }kjk

10. When the expenses of liquidation are to be borne by the purchasing company then

the purchasing company debits:

tc lekiu O;;ksa dk ogu Øsrk dEiuh djrh gS] rc Øsrk dEiuh Msfcr djsxh&

a) Vendor Company's Account b) Bank Account

foØsrk dEiuh dk [kkrk cSad [kkrk

c) Goodwill Account d) None of these

[;kfr [kkrk mijksä esa ls dksbZ ugha

19

-----------------------------------

M.Com. Fourth Semester Examination (Year 2016)

Corporate Accounting Subject Code: MCOM-405

Paper Code: TMT-295 Time : 2 Hrs. 50 Mts.

M.Marks : 60

Section B

[k.M c (Short Answer Type Questions)

(y?kqmÙkjh; iz’u)

Attempt all questions. Each question carries 4 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 4 vad fu/kkZfjr gSA

Q.No.2. Give journal entries for the forfeiture of shares and its reissue at premium?

va'kksa ds gj.k ,oa izC;kft ij iqufuZxeu lEcU/kh tuZy izfof"V;k¡ nhft;sA

OR

A Company Ltd. made the following issue of 6% Debentures; a) For cash @ 90%,

6,000 Debentures of Rs. 100 each b) Vendor who supplied machinery costing Rs.

10,00,000, 11,000 Debentures of Rs. 100 each. Pass the necessary Journal Entries in

the book of A company.

A dEiuh fy- us 6% _.ki=ksa dk fuxZeu fuEu vuqlkj fd;k% a) :- 100 okys 6]000

_.ki=ksa dk 90% jksdM+ ij] b) ,d foØsrk ftlus 10]00]000 :Ik;s dh e'khu nh Fkh] :-

100 okys 11]000 _.ki=A A fy- dh iqLrdksa esa tuZy izfof"V;k¡ cukb,A

Q.No.3. Give a specimen of Company's Balance Sheet according to the Companies Act,

1956.

dEiuh vf/kfu;e] 1956 ds vuqlkj dEiuh ds fpës dk izk:i nhft;sA

OR

What accounting entries are passed at the time of declaration and payment of

dividend?

ykHkka'k dh ?kks"k.kk ,oa Hkqxrku ij dkSu dkSu lh ys[kkadu izfof"V;k¡ dh tkrh gS\

Q.No.4. Give the journal entries that are passed in the books of the purchasing company at

the time of merger.

,dhdj.k ds le; Øsrk dEiuh dh iqLrdksa esa gksus okyh tuZy izfof"V;ksa dks fyf[k,A

OR

What is purchase consideration? How is it computed?

Ø; izfrQy D;k gS\ bldh x.kuk dSls dh tkrh gS\

Q.No.5. What is meant by Reconstruction of a Company? Give Accounting Journal Entries

of internal reconstruction.

dEiuh ds iqufuZek.k ls D;k rkRi;Z gS\ vkUrfjd iqufuZek.k dh ys[kkadu tuZy izfof"V;k¡

nhft;sA

Roll No.

20

OR

Varoda Textiles Ltd. went into voluntary liquidation on 31st March 2014. Following

information is available:

Excess of capital and liabilities over assets Rs. 2,00,000 Net dividends declared

during the last two years Rs. 30,000 Loss on realization Rs. 50,000, Net trading

profit Rs. 15,000. Prepare Deficiency Account.

ojkSM+k VSDlVkby fy- dk 31 ekpZ 2014 dks ,sfPNd lekiu gqvkA fuEu lwpuk;sa miyC/k

gSa%&

iw¡th vkSj nkf;Roksa dk lEifÙk;ksa ij vkf/kD; 2]00]000 :-] xr nks o"kksZa esa ?kksf"kr fd;s x;s

ykHkka'k 30]000 :-] olwyh ij gkfu 50]000 :-] 'kq) O;kikfjd ykHk 15]000 :A U;wurk

[kkrk rS;kj dhft;sA

Q.No.6. What do you mean by goodwill? Explain any two methods of its valuation with

example.

[;kfr ls vki D;k le>rs gks\ blds ewY;kadu dh dksbZ nks fof/k;ksa dks mnkgj.k lfgr

le>kb,A

OR

Calculate the value of equity share by dividend yield method:

2,000 Equity Shares of Rs. 100 each; 1,000, 14% preference shares of Rs. 100 each;

Annual Profits Rs. 2,00,000, Rs. 2,05,000, Rs. 2,10,000 and Rs. 2,05,000

respectively in 2002, 2003, 2004 and 2005, Tax rate 50%, transfer to general reserve

20% of profit and normal rate of return 20%.

2]000 lerk va'k] izfr va'k 100 :i;s( 1]000] 14% vf/keku va'k izfr va'k 100 :Ik;s(

okf"kZd ykHk 2]00]000 :-] 2]05]000 :-] 2]10]000 :-] 2]05]000 :- Øe'k% o"kZ 2002] 2003]

2004 rFkk 2005 esa( dj dh nj 50% ykHk dk 20% lkekU; lap; esa vUrj.k rFkk izR;k;

dh lkekU; nj 20%A

Section C

[k.M l (Long Answer Type Questions)

(nh?kZ mÙkjh; iz’u)

Attempt all questions. Each question carries 8 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 8 vad fu/kkZfjr gSA

Q.No.7. A Company was incorporated on 1st August 2012 in order to purchase a running

business from 1st April 2012. Following particulars are available from its record:

Sales from 1st April 2012 to 31st July 2012 Rs. 1,50,000, Sales from 1st August,

2012 to 31st March 2013 Rs. 3,50,000, Gross profit for the whole year Rs. 1,55,000,

office expenses for the whole year Rs. 65,400, Advertisement expenses for the

whole year Rs. 18,500, Director's fees Rs. 11,100. Prepare profit and loss account

showing profits or loss prior to incorporation and after incorporation.

,d dEiuh dk lekesyu] ,d pkyw O;kikj dks 1 vizSy 2012 ls [kjhnus ds fy;s 1 vxLr

2012 dks gqvkA buds [kkrksa esa fuEukafdr rRo Kkr gq;s%

1 vizSy 2012 ls 31 tqykbZ 2012 rd dk foØ; 1]50]000 :-] 1 vxLr 2012 ls 31 ekpZ

2013 rd dk foØ; 3]50]000 :-] lEiw.kZ o"kZ dk ldy ykHk] 1]55]000 :-] lEiw.kZ o"kZ dk

dk;kZy; O;; 65]400 :-] lEiw.kZ o"kZ dk foKkiu O;; 18]500 :-] lapkydksa dk 'kqYd

21

11]100 :-A lekesyu ls iwoZ ,oa i'pkr+ ds ykHk ;k gkfu dks n'kkZrs gq;s ykHk&gkfu [kkrk

cukb;sA

OR

'A' limited issued 10,000 shares of Rs. 100 each at Rs. 120 payable as follows: Rs.

25 on application, Rs. 45 on allotment (including premium) Rs. 20 on first call and

Rs. 30 on final call.

9,000 shares were applied for and allotted. All money were received with exception

of first and final call on 200 shares held by Shyam. These shares were forfeited.

Give necessary Journal Entries and Balance Sheet.

'A' fyfeVsM us 100 :- okys 10]000 va'kksa :- 120 izfr va'k ij fuxZfer fd;s tks fuEu

izdkj ns; Fks% :- 25 vkosnu ij] :- 45 vkcaVu ij ¼izC;kft lfgr½ :- 20 izFke ;kpuk

ij ,oa :- 30 vafre ;kpuk ijA

9]000 va'kksa ds fy;s vkosnu tc izkIr gq;sA lHkh jkf'k;k¡ izkIr gks xbZ] flok; 200 va'kksa

ij izFke ,oa vfUre ;kpuk] tks ';ke ds ikl FksA bu va'kksa dk gj.k dj fy;k x;kA

tuZy esa vko';d izfof"V;k¡ dhft;s vkSj vkfFkZd fpëk cukb;sA

Q.No.8. Subhash Ltd. made a profit of Rs. 74,000 during the year 2013-14, while it carried

forward a balance of Rs. 15,000 in the Profit & Loss Appropriation Account from

the year ended 31st March 2013. It took the following decision:

i) Development Rebate Reserve Rs. 14,000.

ii) Dividend equalization fund Rs. 10,000.

iii) Dividend on 10% Preference Shares of Rs. 80,000.

iv) Dividend at 15% on 30,000 equity shares of Rs. 5 each fully paid

v) Transfer to General Reserve Rs. 20,000.

Prepare Profit and Loss Appropriation Account and give Journal Entries for payment

of dividend. Ignore Income Tax.

lqHkk"k fyfeVsM us 2013&14 esa 74]000 :- dk ykHk dek;k] tcfd 31 ekpZ 2013 dks

lekIr gksus okys o"kZ ls 15]000 :- dk 'ks"k blds ykHk&gkfu fofu;kstu [kkrk esa yk;k

x;kA blds fuEufyf[kr fu.kZ; fy;s%

i) fodkl NwV lap; 14]000 :-

ii) ykHkka'k lekuhdj.k dks"k 10]000 :-

iii) 80]000 ds 10% iwokZf/kdkj va'kksa ij ykHkka'k

iv) 5 :- okys iw.kZnÙk 30]000 va'kksa ij 15% ykHkka'k

v) lkekU; lap; esa vUrj.k 20]000 :-

ykHk&gkfu fofu;kstu [kkrk cukb, Hkqxrku ds fy;s tuZy izfof"V;k¡ nhft,A vk;dj ij

/;ku u nsaA

OR

What do you understand by Final Accounts of a company? Describe in brief the

various provisions of the Indian Company Act, 1956 regarding the preparation and

presentation of Final Accounts by the Company.

,d dEiuh ds vfUre [kkrksa ls vki D;k le>rs gks\ la{ksi esa] Hkkjrh; dEiuh vf/kfu;e]

1956 ds mu fofHkUu izko/kkuksa dk mYys[k dhft,] ftuds vuqlkj ,d dEiuh ds vfUre

[kkrs rS;kj rFkk izLrqr fd;s tkrs gSaA

22

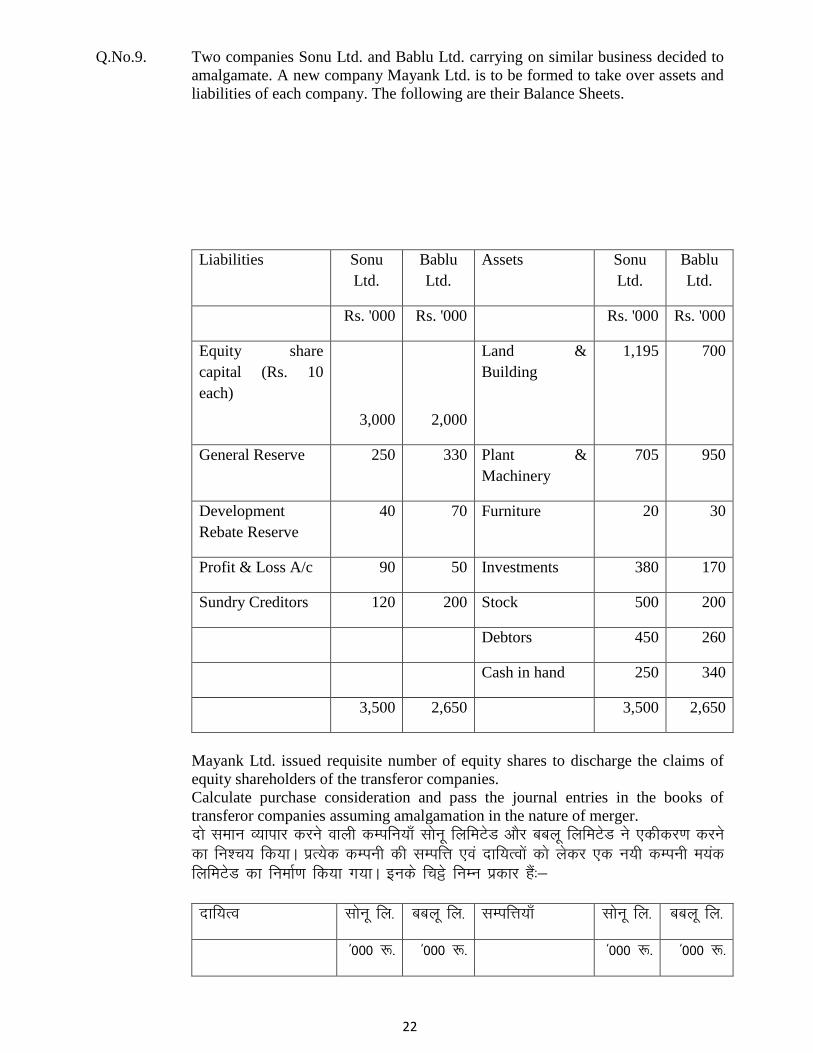

Q.No.9. Two companies Sonu Ltd. and Bablu Ltd. carrying on similar business decided to

amalgamate. A new company Mayank Ltd. is to be formed to take over assets and

liabilities of each company. The following are their Balance Sheets.

Liabilities Sonu

Ltd.

Bablu

Ltd.

Assets Sonu

Ltd.

Bablu

Ltd.

Rs. '000 Rs. '000 Rs. '000 Rs. '000

Equity share

capital (Rs. 10

each)

3,000

2,000

Land &

Building

1,195 700

General Reserve 250 330 Plant &

Machinery

705 950

Development

Rebate Reserve

40 70 Furniture 20 30

Profit & Loss A/c 90 50 Investments 380 170

Sundry Creditors 120 200 Stock 500 200

Debtors 450 260

Cash in hand 250 340

3,500 2,650 3,500 2,650

Mayank Ltd. issued requisite number of equity shares to discharge the claims of

equity shareholders of the transferor companies.

Calculate purchase consideration and pass the journal entries in the books of

transferor companies assuming amalgamation in the nature of merger.

nks leku O;kikj djus okyh dEifu;k¡ lksuw fyfeVsM vkSj ccyw fyfeVsM us ,dhdj.k djus

dk fu'p; fd;kA izR;sd dEiuh dh lEifÙk ,oa nkf;Roksa dks ysdj ,d u;h dEiuh e;ad

fyfeVsM dk fuekZ.k fd;k x;kA buds fpës fuEu izdkj gSa%&

nkf;Ro lksuw fy- ccyw fy- lEifÙk;k¡ lksuw fy- ccyw fy-

^000 :- ^000 :- ^000 :- ^000 :-

23

lerk va'k iw¡th ¼10

:- izfr½

3]000

2]000

Hkwfe ,oa Hkou 1]195 700

lkekU; lap; 250 330 la;U= ,oa

e'khujh

705 950

fodkl NwV lap; 40 70 QuhZpj 20 30

ykHk&gkfu [kkrk 90 50 fofu;ksx 380 170

fofo/k ysunkj 120 200 LdU/k 500 200

nsunkj 450 260

jksdM+ gkFk esa 250 340

3]500 2]650 3]500 2]650

e;ad fyfeVsM us gLrkUrjd dEifu;ksa ds lerk va'k/kkfj;ksa ds nkoksa dk Hkqxrku djus ds

fy;s vko';d la[;k esa lerk va'k fuxZfer fd;sA

Ø; izfrQy dh x.kuk dhft,] gLrkUrjd dEifu;ksa dh iqLrdksa esa vko';d tuZy

izfof"V;k¡ dhft,A ;g ekurs gq;s dh ,dhdj.k foy; dh izd`fr dk gSA

OR

What do you mean by 'Amalgamation in the nature of Merger'? Explain the

procedure of 'Amalgamation in the nature of Merger' according to Accounting

Standard-14.

^foy; ds izd`fr esa ,dhdj.k* ls vki D;k le>rs gks\ ys[kkadu ekud&14 ds vuqlkj]

^foy; dh izd`fr dk ,dhdj.k* dh izfØ;k dks le>kb;sA

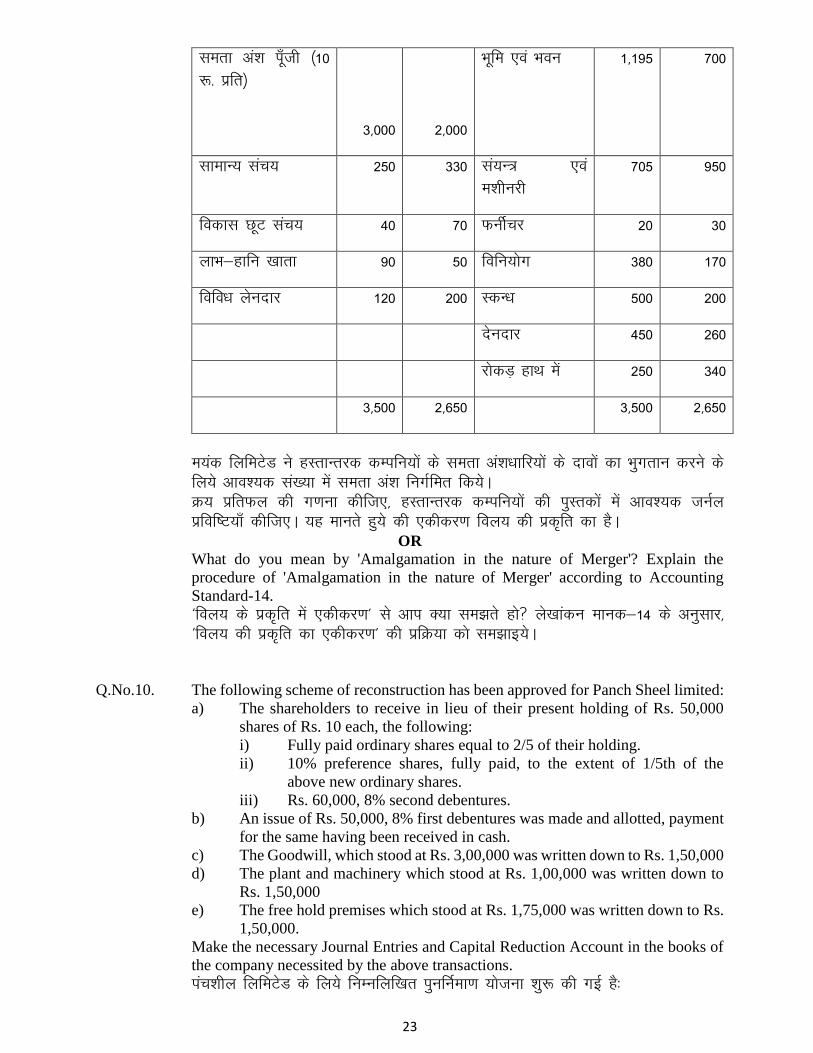

Q.No.10. The following scheme of reconstruction has been approved for Panch Sheel limited:

a) The shareholders to receive in lieu of their present holding of Rs. 50,000

shares of Rs. 10 each, the following:

i) Fully paid ordinary shares equal to 2/5 of their holding.

ii) 10% preference shares, fully paid, to the extent of 1/5th of the

above new ordinary shares.

iii) Rs. 60,000, 8% second debentures.

b) An issue of Rs. 50,000, 8% first debentures was made and allotted, payment

for the same having been received in cash.

c) The Goodwill, which stood at Rs. 3,00,000 was written down to Rs. 1,50,000

d) The plant and machinery which stood at Rs. 1,00,000 was written down to

Rs. 1,50,000

e) The free hold premises which stood at Rs. 1,75,000 was written down to Rs.

1,50,000.

Make the necessary Journal Entries and Capital Reduction Account in the books of

the company necessited by the above transactions.

iap'khy fyfeVsM ds fy;s fuEufyf[kr iqufuZek.k ;kstuk 'kq: dh xbZ gS%

24

d½ 10 :- okys 50]000 va'kksa ds va'k/kkfj;ksa dks muds va'kksa ds cnys fuEukafdr izkIr

gksxk%

i) vius orZeku va'kksa ds 2@5 ewY; ds cjkcj iw.kZ pqdrk lk/kkj.k va'kA

ii) mi;qZDr lk/kkj.k va'kksa 1@5 ewY; ds cjkcj 10% iwokZf/kdkj va'kA

iii) 60]000 ds 8% f}rh; _.ki=A

[k½ 50]000 :- ds 8% izFke _.ki= fuxZfer ,oa vkoafVr fd;s x;s rFkk mudk udnh

Hkqxrku izkIr gks pqdk gSA

x½ [;kfr dk ewY; 3]00]000 ls ?kVkdj 1]50]000 :- dj fn;k x;k gSA

?k½ la;U= ,oa e'khujh dk ewY; 1]00]000 :- ls ?kVkdj 75]000 :- dj fn;k x;k

gSA

³½ vkRe?k`r x`gkfj dk ewY; 1]75]000 :- ls ?kVkdj 1]50]000 :- dj fn;k x;k gSA

mi;qZDr O;ogkjksa ds vk/kkj ij dEiuh dh iqLrdksa esa vko';d tuZy izfof"V;k¡

,d iw¡th deh [kkrk cukb,A

OR

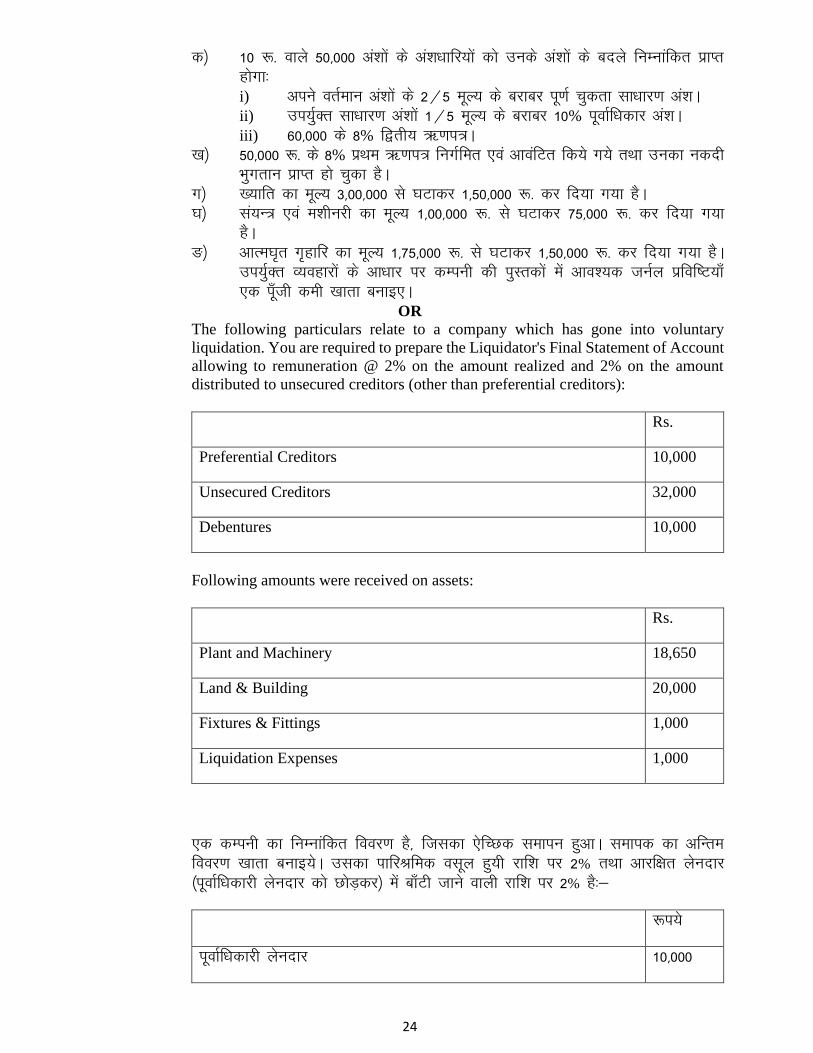

The following particulars relate to a company which has gone into voluntary

liquidation. You are required to prepare the Liquidator's Final Statement of Account

allowing to remuneration @ 2% on the amount realized and 2% on the amount

distributed to unsecured creditors (other than preferential creditors):

Rs.

Preferential Creditors 10,000

Unsecured Creditors 32,000

Debentures 10,000

Following amounts were received on assets:

Rs.

Plant and Machinery 18,650

Land & Building 20,000

Fixtures & Fittings 1,000

Liquidation Expenses 1,000

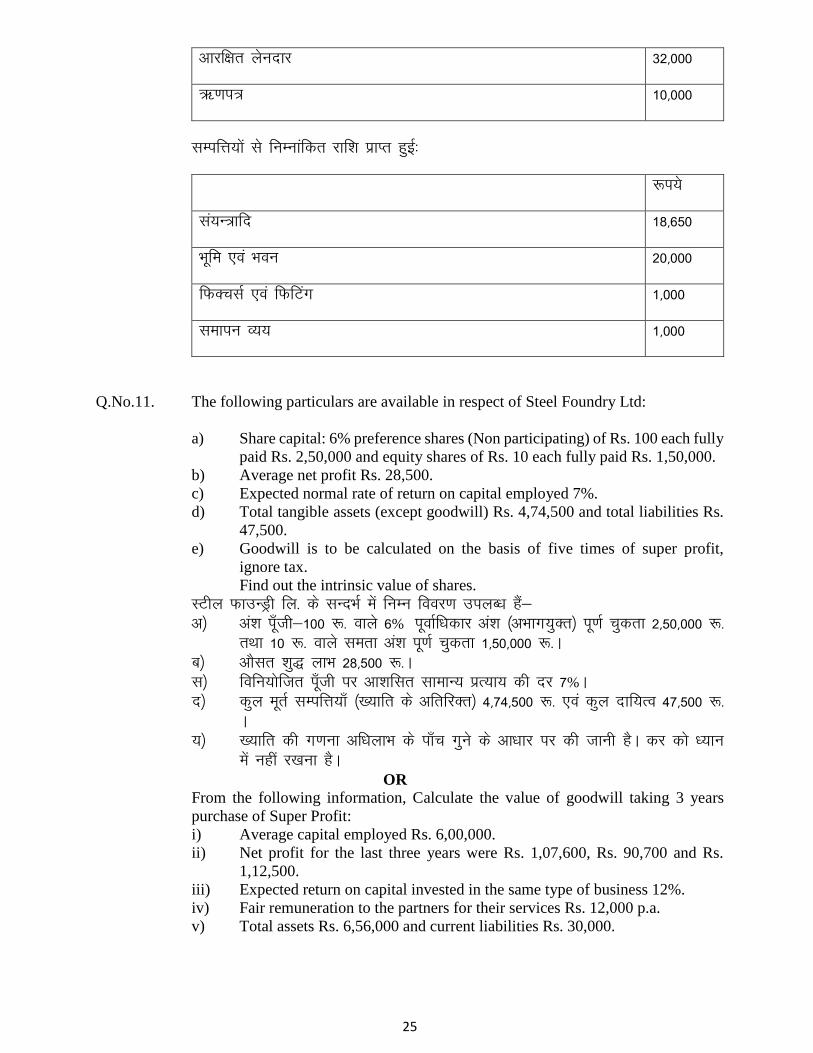

,d dEiuh dk fuEukafdr fooj.k gS] ftldk ,sfPNd lekiu gqvkA lekid dk vfUre

fooj.k [kkrk cukb;sA mldk ikfjJfed olwy gq;h jkf'k ij 2% rFkk vkjf{kr ysunkj

¼iwokZf/kdkjh ysunkj dks NksM+dj½ esa ck¡Vh tkus okyh jkf'k ij 2% gS%&

:i;s

iwokZf/kdkjh ysunkj 10]000

25

vkjf{kr ysunkj 32]000

_.ki= 10]000

lEifÙk;ksa ls fuEukafdr jkf'k izkIr gqbZ%

:i;s

la;U=kfn 18]650

Hkwfe ,oa Hkou 20]000

fQDplZ ,oa fQfVax 1]000

lekiu O;; 1]000

Q.No.11. The following particulars are available in respect of Steel Foundry Ltd:

a) Share capital: 6% preference shares (Non participating) of Rs. 100 each fully

paid Rs. 2,50,000 and equity shares of Rs. 10 each fully paid Rs. 1,50,000.

b) Average net profit Rs. 28,500.

c) Expected normal rate of return on capital employed 7%.

d) Total tangible assets (except goodwill) Rs. 4,74,500 and total liabilities Rs.

47,500.

e) Goodwill is to be calculated on the basis of five times of super profit,

ignore tax.

Find out the intrinsic value of shares.

LVhy QkmUMªh fy- ds lUnHkZ esa fuEu fooj.k miyC/k gSa&

v½ va'k iw¡th&100 :- okys 6% iwokZf/kdkj va'k ¼vHkkx;qDr½ iw.kZ pqdrk 2]50]000 :-

rFkk 10 :- okys lerk va'k iw.kZ pqdrk 1]50]000 :-A

c½ vkSlr 'kq) ykHk 28]500 :-A

l½ fofu;ksftr iw¡th ij vk'kflr lkekU; izR;k; dh nj 7%A

n½ dqy ewrZ lEifÙk;k¡ ¼[;kfr ds vfrfjDr½ 4]74]500 :- ,oa dqy nkf;Ro 47]500 :-

A

;½ [;kfr dh x.kuk vf/kykHk ds ik¡p xqus ds vk/kkj ij dh tkuh gSA dj dks /;ku

esa ugha j[kuk gSA

OR

From the following information, Calculate the value of goodwill taking 3 years

purchase of Super Profit:

i) Average capital employed Rs. 6,00,000.

ii) Net profit for the last three years were Rs. 1,07,600, Rs. 90,700 and Rs.

1,12,500.

iii) Expected return on capital invested in the same type of business 12%.

iv) Fair remuneration to the partners for their services Rs. 12,000 p.a.

v) Total assets Rs. 6,56,000 and current liabilities Rs. 30,000.

26

fuEufyf[kr lwpuk ls vf/kykHk dk rhu xquk ysrs gq;s [;kfr dk ewY; Kkr dhft;s%&

i) vkSlr fofu;ksftr iw¡th 6]00]000 :-

ii) xr rhu o"kksZa dk 'kq) ykHk % 1]07]600 :- 90]700 :- rFkk 1]12]500 :-

iii) blh izdkj ds O;olk; esa fofu;ksftr iw¡th ij vk'kaflr izR;; nj 12%

iv) lk>snkjksa dks mudh lsokvksa ds fy;s mfpr ikfjJfed 12]000 :- izfr o"kZA

v) dqy lEifÙk;k¡ 6]56]000 rFkk pkyw nkf;Ro 30]000 :-A

--------------------------------

M.Com. Fourth Semester Examination (Year 2016)

Cost Administration & Control Subject Code: MCOM-406

Paper Code: TMT-296 Time : 10 Minutes

M.Marks : 10

Section A

Objective Type Questions

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking the

correct answer.

Q. No. 1. Choose the correct answer-

1. If a firm has a negative Contribution margin to reach break even.

b) Sales volume increases b) Fixed cost decreases

c) Sales volume decreases d) Fixed cost increases

2. The break even point would be increased by-

a) A decrease in fixed cost

b) An increase in contribution margin ratio

c) Increase in Variable Cost

d) Decrease in Variable Cost

3. Ideal Standard means-

Invigilator’s Signature

Roll No.

Enrollment No.

27

a) Basic Standard b) Current Standard

b) Expected Standard d) Actual Standard

4. Main tools of planning a New Budgeting System is-

a) Programme Budget b) Multi year Costing

c) Zero Base Budget d) None of these

5. Under flexible budget what remains constant for all year-

a) Variable Expenses b) Semi Variable Expenses

c) Fixed Expenses d) All of these

6. The Cost of the product as determined under Standard Costing is-

a) Fixed Cost b) Direct Cost

c) Historical Cost d) Predetermined Cost

7. Standard costs are useful for except-

a) Reducing cost

b) Establishing records

c) Preparation of operating reports

d) Costing inventories

8. Which method of inventory valuation is most widely used in accounting?

a) Cost price

b) Cost on market price whichever is more

c) Market price

d) Cost on market price whichever is less

9. Revenue is generally recognized as being earned at that point of time when-

a) Sales is effected b) Production is completed

c) Cash is received d) Debts are collected

10. If profit is 25% of selling price what is the percentage of profit to cost?

28

d) 20% b) 25%

c) 30% d) 33.33%

-----------------------------

M.Com. Fourth Semester Examination (Year 2016)

Cost Administration & Control Subject Code: MCOM-406

Paper Code: TMT-296

Time : 2 Hrs. 50 Mts.

M.Marks : 60

Section B (Short Answer Type Questions)

Attempt all questions. Each question carries 4 marks.

Q.No.2. How is marginal costing useful in the decision making of a firm.

OR

What is ''Angle of Incidence''? Explain.

Q.No.3. Explain the concept of ''Zero Base Budget''

OR

What is Cost Plus Pricing?

Q.No.4. What do you mean by Transfer Pricing.

OR

Differentiate between standard and actual variance.

Q.No.5. Explain the term ''Value Analysis''.

OR

Explain cost reduction and cost control with examples.

Q.No.6. What do you mean by Benchmarking?

OR State the importance of planning in material requirement in an Industry.

Roll No.

29

Section C (Long Answer Type Questions)

Attempt all questions. Each question carries 8 marks.

Q.No.7. Define marginal costing. How does it differs from total costing.

OR

From the following information you are required to find out

a) Contribution

b) BEP in units

c) Margin of safety

d) Profit

Given-

Total fixed cost Rs. 4500

Total variable cost Rs. 7500

Total sales Rs. 15,000

Units sold 5,000

e) Also calculate the volume of sales to earn a profit of Rs. 6,000

Q.No.8. Elaborate the various factors influencing product pricing and pricing decision with

suitable examples.

OR

Define Budget and budgetary control. What are its components?

Q.No.9. A Factory works on the standard costing system. The standard estimates of materials

for the manufacture of 1,000 units of a commodity is 400 kg at Rs. 2.50 per kg.

When 2,000 units of a commodity are manufactured, it is found that 820 kg of

materials is consumed at Rs. 2.60 per Kg.

Calculate the material variances.

OR

Explain the influence of non financial factors of pricing in price discrimination.

Q.No.10. Elucidate the techniques used for cost control and reduction.

OR

You are given the following information.

Selling price Rs. 10 per unit

Variable cost Rs. 6 per unit

Fixed cost Rs. 10,000

Present production and sales 5000 units

30

The directors of the company propose to reduce the selling price by 20%. Find out

the additional number of units that should be sold to maintain the present profit.

Q.No.11. Explain the Concept and importance of Enterprises Resource Planning.

OR

How TQM is relevant in costing for manufacturing Resource Planning.

----------------------------------

M.Com. Fourth Semester Examination (Year 2016)

Accounting Theory Subject Code: MCOM-407

Paper Code: TMT-297 Time : 10 Minutes

M. Marks: 10

Section A

[k.M v

(Objective Type Questions)

¼oLrqfu"B Á’u½

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking the

correct answer.

lHkh iz’u vfuok;Z gSaA izR;sd iz’u gsrq 1 vad fu/kkZfjr gSA lgh mÙkj gsrq fn;s x;s ckDl esa () fpUg dk

iz;ksx djsaA

Q.No.1. Choose the correct answer-

lgh mÙkj pqfu,&

3. Which of the following jobs check accounting in ledgers and financial statements?

fuEufyf[kr ukSdfj;ksa esa ls dkSu [kkrksa vkSj foÙkh; fooj.k esa ys[kkadu dh tkap djrs gSA

a) Financial b) Audit

foÙkh; ys[kk ijh{kk

c) Management d) Budget Analysis

izca/k ctV fo'ys"k.k

2. The process of accounting is needed to-

ys[kkadu izfØ;k esa djus dh t:jr gSA

a) Take a holiday

,d vodk'k ys yks

b) Assist in decision making

gy fudkyus esa lgk;rk

c) Invest in startup of a business

,d O;olk; ds LVkVZvi ¼'kq:okr½ esa fuos'k

d) Track money spent

iSlk [kpZ djus dk rfjdk

Invigilator’s Signature

Roll No.

Enrollment No.

31

3. Accountants use Generally Accepted Accounting Principles (GAAP) to make the

financial information communicated.

,dkmVsaV ds }kjk vkerkSj ij Hksth foÙkh; tkudkjh cukus ds fy, ys[kkadu fl)karksa dks

Lohdkj djus esa mi;ksx djukA

a) Relevant b) Reliable

izklafxd fo'oluh;

c) Comparable d) Profitable

rqyuh; ykHknk;d

4. Dividends are paid by-

ykHkka'k }kjk Hkqxrku dj jgs gSA

a) Sole Trading Business b) Partnership Companies

,dy O;kikj ds dkjksckj lk>snkj daifu;k¡

c) Limited Liability Companies d) Co-operatives

lhfer ns;rk daifu;k¡ lgdkjh

5. The elements of the accounting equation are (i) Assets (ii) Liabilities (iii) Trial

Balance (iv) Capital -

ys[kkadu lehdj.k ds rRo gksrs gS (i) laifÙk (ii) nsunkfj;k¡ (iii) larqyu ijh{k.k (iv) iwath

a) (i), (ii) and (iii) b) (i) (ii) and (iv)

(i), (ii) vkSj (iii) (i) (ii) vkSj (iv)

c) (i), (iii) and (iv) d) (ii), (iii) and (iv)

(i), (iii) vkSj (iv) (ii), (iii) vkSj (iv)

6. Trading & Profit and Loss account is also called as: -

O;kikj vkSj ykHk vkSj gkfu [kkrs ds :i esa Hkh dgk tkrk gSA

a) Balance Sheet b) Cash Flow Statement

foÙkh; fLFkfr fooj.k udnh izokg fooj.k

c) Income Statement d) Trial Balance

vk; fooj.k larqyu ijh{k.k

7. Which of the following are asset?

fuEu esa ls tks laifÙk gS\

I Cash and Cash at Bank

udnh vkSj cSad esa udnh

II Land and Fixtures

Hkweh vkSj tqM+ukj

III Loans and Creditors

_.k vkSj ysunkjks

IV Mortgage Loans and Debtors

ca/kd _.k vkSj nsunkj

a) I and II b) I and III

I vkSj II I vkSj III

c) I and IV d) II and III

I vkSj IV II vkSj III

8. A debit note is a document made out when goods are: -

MsfcV uksV] ckgj dj fn;s eky dk ,d nLrkost gS&

a) Returned b) Over Charged

32

ykSVk gqvk vkjksi yxk gqvk

c) Sold d) Under Charged

fcdk gqvk vkjksi ds rgr

9. Which of the following books of original entry should be used to record credit soles?

fuEufyf[kr iqLrdksa esa ls dkSu lh iqLrdksa dh ewy izfof"V dk mi;ksx ØsfMV dh fcØh

fjdkMZ ds fy, fd;k tkuk pkfg,\

a) Sales Journal

fcØh if=dk

b) Returns Inwards Journal

fjVuZbuoMZ if=dk

c) Purchases Journal

[kjhn if=dk

d) Petty Cash Journal

QqVdj jksdM+ jk'kh if=dk

10. Which of the following items are used to prepare a balance sheet?

fuEufyf[kr enks essa ls fdls ,d csysal 'khV rS;kj djus ds fy, bLrseky djrs gSA

I The name of firm

QeZ dk uke

II The name of the financial statement

foÙkh; fooj.k dk uke

III The date it is being prepared

rS;kj djus dh fnukad

IV The style use for the preparation of statement

fooj.k dh rS;kjh ds fy, 'kSyh dk mi;ksx

a) I and II b) I and IV

I vkSj II I vkSj IV

c) II and III d) I, III and IV

II vkSj III I, III vkSj IV

&&&&&&&&&&&&&&&&

33

M.Com. Fourth Semester Examination (Year 2016)

Accounting Theory Subject Code: MCOM-407

Paper Code: TMT-297

Time : 2 Hrs. 50 Mts.

M. Marks: 60

Section B

[k.M c (Short Answer Type Questions)

(y?kq mÙkjh; iz’u)

Attempt all questions. Each question carries 4 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 4 vad fu/kkZfjr gSA

Q.No.2. Explain concept of Accounting Theory?

Yks[kk fl)kar dh vo/kkj.kk dh O;k[;k djsaA

OR Explain Accounting: as an Information System.

Yks[kkadu dh O;k[;k djsa % ,d lwpuk iz.kkyh ds :Ik esaA

Q.No.3. Write short notes on expenses, gain and loss.

Lkaf{kIr uksV~l fy[ks%& [kpsZ] ykHk ,oa gkfu ijA

OR A short note on GAAP: Explain.

Lkaf{kIr uksV fy[ksa % GAAP ijA

Q.No.4. Explain various concepts of Income.

vk; ds fofHkUu vo/kkj.kksa dh O;k[;k djsaA

OR Differentiate between Income Statement and Balance Sheet.

vk; LVsVesaV vkSj rqyd i= ds e/; varj Li"V djsaA

Q.No.5. What do you mean by Segment Reporting? Explain in brief.

[k.M fjiksfVZax ls vki D;k le>rs gSa\ laf{kIr esa O;k[;k djsaA

OR

Write a short note on conceptual study of Accounting for changing prices.

dherksa dks cnyus ds fy, ys[kkadu ds oSpkfjd v/;;u ij ,d laf{kIr uksV fy[ksaA

Q.No.6. What is interim Reporting? Explain with examples.

varfje fjiksfVZax D;k gS\ mnkgj.k ds lkFk le>kb,A

OR

Write short note on Environmental Accounting and Reporting.

Ik;kZoj.kh; ys[kk vkSj fjiksfVZax ij ,d laf{kIr ys[k fy[ksaA

Roll No.

34

Section C

[k.M l (Long Answer Type Questions)

(nh?kZ mÙkjh; iz’u)

Attempt all questions. Each question carries 8 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 8 vad fu/kkZfjr gSA

Q.No.7. What are different Approaches of Accounting Theory? Explain.

Yks[kkadu fl)kar ds vyx&vyx n`f"Vdks.k dh O;k[;k djsaA

OR

"Accounting is a major tool as an Information System."Kindly Explain.

**ys[kkadu lwpuk iz.kkyh ds :Ik esa ,d izeq[k midj.k gSA** Ñi;k foLrkj ls le>kb,A

Q.No.8. Explain Accounting Policies in detail.

foLrkj ls ys[kkadu uhfr;ksa dh O;k[;k djsaA

OR

Explain Accounting concepts and postulates in details.

ys[kkadu vo/kkj.kkvksa vkSj foLrkj esa rRoksa dh O;k[;k djsaA

Q.No.9. What do you mean by revenue measurement and its relevance with Accounting?

Kindly explain in detail.

jktLo eki vkSj ys[kkadu ds lkFk bldh izklafxdrk ls vki D;k le>rs gSa\ foLrkj iwoZd

crk,A OR Explain the concept of comprehensive income in relationship to earning, net

income and comprehensive income.

dekbZ ds laca/k esa O;kid vk;] fuoy vk; vkSj O;kid vk; dh vo/kkj.k dh foLrkj ls

O;k[;k djsaA

Q.No.10. Explain Social Accounting and its benefits to society as a business enterprise.

Lkkekftd ys[kkadu ds ykHk ,oa lekt esa ,d O;kolkf;d m|e ds :Ik esa blds mi;ksx

dh O;k[;k djsaA

OR

Kindly enumerate the conceptual study of Accounting for changing prices.

ÑIk;k dherksa dks cnyus ds fy, ys[kkadu ds oSpkfjd v/;;u dh x.kuk djsaA

Q.No.11. What is interim reporting and its utility for investors as well as share holders. Give

suitable examples.

varfje fjiksfVZax vkSj fuos'kdksa ds :Ik esa vPNh rjg ls 'ks;j /kkjdksa ds fy, bldh

mi;ksfxrk D;k gS\ mnkgj.k ds lkFk le>kb,A

OR

"Human Resource Accounting is the art of valuing, recording and presenting

systematically the worth of human resources in the books of account of

organization."Explain.

**ekuo lalk/ku ys[kkadu gS ckrksa dks egRo nsrh fjdkfMZax vkSj O;ofLFkr ewY; ekuo lalk/ku

dk ,d laxBu ds [kkrs dh iqLrdksa esa is'k djus dh dyk % O;k[;k djsaA

________________

35

M.Com. Fourth Semester Examination (Year 2016)

Institutional Accounting Subject Code: MCOM-408

Paper Code: TMT-298 Time : 10 Minutes

M. Marks: 10

Section A

(Objective Type Questions)

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking the

correct answer.

Q. No. I. Choose the correct answer-

4. The share of outsider in the net assets in subsidiary company is known as-

c) Outsider's liability b) Assets

c) Subsidiary company's liability d) Minority Interest

5. The Profit and Loss account under Double account system is termed as-

a) Revenue Account

b) Income and Expenditure account

c) Profit and Loss account

d) None of these

3. Preparation of consolidated statement as per AS-21 is-

a) Optional

b) Mandatory for listed companies

c) Mandatory for private limited

d) Companies limited partnership firm

4. Which of the following room rate plans includes a room only No meals?

a) American Plan b) Modified American Plan

c) European Plan d) Modified European Plan

Roll No.

Enrollment No. Enrollment No.

Invigilator’s Signature

36

5. If there exists some reserves and profits of the subsidiary company on the date of

acquisition of share of the subsidiary company, the outsider's share of such reserves

and profits is added to the-

a) Profit of the company b) Reserves of the company

c) Assets of the company d) Minority Interest

6. Any amount payable by the insurance company is called-

a) Premium b) Claim

c) Interest d) Dividend

7. Provision for taxation is charged to the P&L account under the heading-

a) Liabilities and Provisions

b) Provisions and Contingencies

c) Income and expenditure

d) None of these

8. ……………….. is uncollectable and is of such little value that it is not desirable to

show it as bank's asset though it may have some recovery value.

a) Loss asset b) Doubtful asset

c) Standard asset d) Substandard asset

9. Preliminary expenses account is shown on-

a) Assets side in General Balance Sheet

b) Debit side of the net revenue account

c) Debit side of the receipts and expenditure on capital account

d) It is not mentioned at all

10. Assets which have been classified as NPA for a period not exceeding two years are

termed as-

e) Standard assets b) Sub- Standard assets

c) Doubtful assets d) Loss assets

-------------------------------

37

M.Com. Fourth Semester Examination (Year 2016)

Institutional Accounting Subject Code: MCOM-408

Paper Code: TMT-298 Time : 2 Hrs. 50 Mts.

M. Marks: 60

Section B (Short Answer Type Questions)

Attempt all questions. Each question carries 4 marks.

Q.No.2. Define-

a) Standard assets

b) Sub-standard assets

c) Doubtful assets

d) Loss assets

OR

Give a proforma of Profit and Loss account of a Banking company.

Q.No.3. What is meant by reinsurance? How is it helpful to insurance companies?

OR

What is meant by Bonus in reduction of premium and how it is treated in Revenue

account?

Q.No.4. Write a note on Double accounting system with special reference to account of

Electricity Company.

OR

Explain the special features of preparing final accounts and Appropriation of profits

in case of electricity companies.

Q.No.5. A five star hotel in Delhi has 300 lettable rooms out of which 200 rooms are single

bed rooms and 100 rooms are double bed rooms. On 30th November, 2014, 160

single rooms and 80 double rooms are occupied by the guests. Calculate bed

occupancy rate for the day.

OR

'A' holds 10 share of Rs. 10 each in a cooperative society to which he is indebted for

Rs. 30. The debt has become overdue and he has applied for the refund of the amount

of his all the shares. The directors of the society have approved the refund subject to

the deduction of the amount of loan together with Rs. 2 on account of interest on

loan; if the condensed balance sheet of society is as follows, what amount will be

refunded to A?

Condensed balance sheet of society LTD as at 31 March, 2013

Rs. Rs.

Paid up Capital (Rs. 10) 5,000 Sundry Assets 6,000

Sundry Liabilities 2,000 P&L A/c 1,000

Roll No.

38

7,000 7,000

Q.No.6. A life insurance company gets its valuation made once in every two years. It's life

assurance fund on 31st March, 2000, amounted to Rs. 41,40,000 before providing

Rs. 30,000 for the shareholder's dividend for the year 1999-2000. Its actuarial

valuation due on 31st March, 2000 disclosed a net liability of Rs. 40,40,000 under

assurance annuity contract.

An interim bonus of Rs. 60,000 was paid to the policy holders during the two years

ending 31st March 2000.

Prepare a statement showing the amount now available as bonus to policy holders.

OR

Calculate rent to be charged per day per room from the following information for a

3 star hotel at Goa, if occupancy rate is (a) 100% (b) 80%

a. No. of rooms available for occupancy = 50.

b. Estimated total cost for April = Rs. 12,00,000.

c. Return expected = 50% on cost.

Section C (Long Answer Type Questions)

Attempt all questions. Each question carries 8 marks.

Q.No.7. The following balances relate to United India life assurance company Ltd. as on 31st

March, 2014.

Shareholders capital

(10,000 shares of Rs. 25

each Rs. 10 per share

paid-up)

1,00,000 Consideration for

annuities granted

25,250

Claims under policies

paid & outstanding less

received on re-assurance

22,50,000 Bonus in reduction of

premium

2,000

Life assurance fund on 1st

April 2013

2,40,00,000 Gain on redemption of

debentures (to be carried

to investment reserve

fund)

10,000

Investment reserve fund

on 1st April 2013

25,00,000 Interest, dividends &

rents received

16,00,168

Expenses of management 7,50,213 Interest accrued, but not

payable

1,58,500

Investments 2,55,00,000 Income tax paid 1,40,074

39

Freehold & leaseholds

property

12,50,000 Transfer & other fees 3,215

Unpaid dividend 25,895 Agents' balances

outstanding

72,952

Outstanding premiums 301,600 Furniture & Fittings 45,250

Claims admitted or

intimated, but not paid

15,00,000 Loans on the company's

policies within theirs

surrender Value

24,50,000

Outstanding interest 2,95,000 Cash in hand 1,82,000

Surrenders 1,79,475 Stamps in hand 3,661

Annuities 15,000 Cheques paid into bank &

in course of realization

24,500

Premiums less re-

assurance

37,50,000 Cheques issued but not

presented for payment

33,260

Sundry creditors 22,437

Premium received in

advance

50,000

You are required to prepare the revenue account for the year ended 31st March 2014

and a balance sheet at that date of United India Assurance Company Ltd.

OR

The following Balances are extracted from the books of Railway Company after

completion of the Revenue account for the year ended 31st March 2000. You are

required to prepare the Receipts & Expenditure on Capital account and the General

Balance sheet. Dr. (Rs.) Cr. (Rs.)

Equity Shares 10,00,000

6% preference shares 6,00,000

7.5% Debentures 4,00,000

Lines open for traffic 17,04,000

Lines in the course of construction 10,000

Working Stock 2,60,000

Lines leased 40,000

40

Lines jointly owned 1,00,000

Freehold land 25,000

Securities Premium A/c 55,000

Cash at bank 10,000

General Stores & Stocks 25,000

Net revenue A/c 32,000

Traffic accounts due to the company 20,000

Due from other companies 5,000

Sundry outstanding A/c 7,000

Due to other companies 4,000

Sundry Creditors 30,000

Fire insurance fund 5,000

General Reserve 65,000

Superannuation fund 15,000

22,06,000 22,06,000

During the year there was an issue of Rs. 1,50,000 6% preference shares at par and

this was fully subscribed. Equity shares of Rs. 2,00,000 were also issued at a

premium of 10%. Expenditure during the year made on lines open for traffic Rs.

40,000 and lines in the course of construction Rs. 3,000 were made and the

construction to lines jointly owned Rs. 20,000.

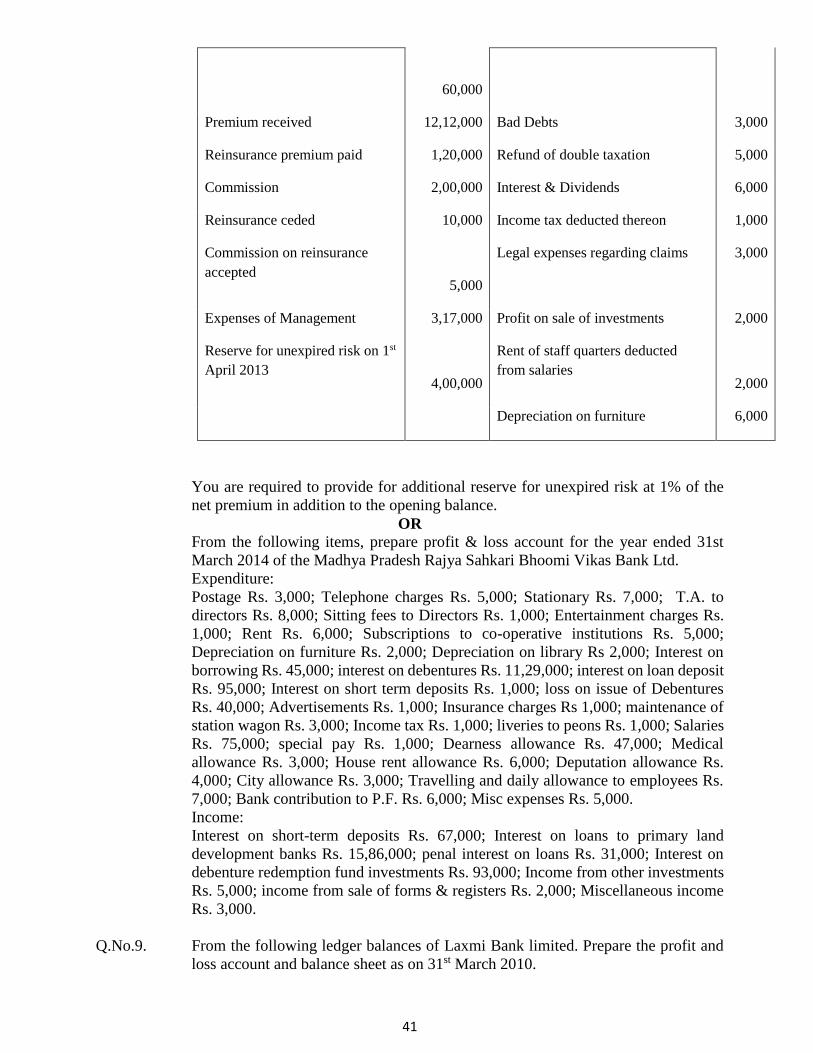

Q.No.8. From the following particulars you are required to prepare Fire Revenue account for

the year ended on 31st March 2014. Rs. Rs.

Claims paid 4,80,000 Additional reserve for unexpired

risk

20,000

Claims outstanding on 1st April

2013.

40,000

Reinsurance recoveries of claims 8,000

Claims intimated but not

accepted on 31st March 2014.

10,000

Sundry expenses regarding claims

5,000

Claims intimated & accepted but

not paid on 31st March 2014

Loss on sale of Car 5,000

41

60,000

Premium received 12,12,000 Bad Debts 3,000

Reinsurance premium paid 1,20,000 Refund of double taxation 5,000

Commission 2,00,000 Interest & Dividends 6,000

Reinsurance ceded 10,000 Income tax deducted thereon 1,000

Commission on reinsurance

accepted

5,000

Legal expenses regarding claims 3,000

Expenses of Management 3,17,000 Profit on sale of investments 2,000

Reserve for unexpired risk on 1st

April 2013

4,00,000

Rent of staff quarters deducted

from salaries

2,000

Depreciation on furniture 6,000

You are required to provide for additional reserve for unexpired risk at 1% of the

net premium in addition to the opening balance.

OR

From the following items, prepare profit & loss account for the year ended 31st

March 2014 of the Madhya Pradesh Rajya Sahkari Bhoomi Vikas Bank Ltd.

Expenditure:

Postage Rs. 3,000; Telephone charges Rs. 5,000; Stationary Rs. 7,000; T.A. to

directors Rs. 8,000; Sitting fees to Directors Rs. 1,000; Entertainment charges Rs.

1,000; Rent Rs. 6,000; Subscriptions to co-operative institutions Rs. 5,000;

Depreciation on furniture Rs. 2,000; Depreciation on library Rs 2,000; Interest on

borrowing Rs. 45,000; interest on debentures Rs. 11,29,000; interest on loan deposit

Rs. 95,000; Interest on short term deposits Rs. 1,000; loss on issue of Debentures

Rs. 40,000; Advertisements Rs. 1,000; Insurance charges Rs 1,000; maintenance of

station wagon Rs. 3,000; Income tax Rs. 1,000; liveries to peons Rs. 1,000; Salaries

Rs. 75,000; special pay Rs. 1,000; Dearness allowance Rs. 47,000; Medical

allowance Rs. 3,000; House rent allowance Rs. 6,000; Deputation allowance Rs.

4,000; City allowance Rs. 3,000; Travelling and daily allowance to employees Rs.

7,000; Bank contribution to P.F. Rs. 6,000; Misc expenses Rs. 5,000.

Income:

Interest on short-term deposits Rs. 67,000; Interest on loans to primary land

development banks Rs. 15,86,000; penal interest on loans Rs. 31,000; Interest on

debenture redemption fund investments Rs. 93,000; Income from other investments

Rs. 5,000; income from sale of forms & registers Rs. 2,000; Miscellaneous income

Rs. 3,000.

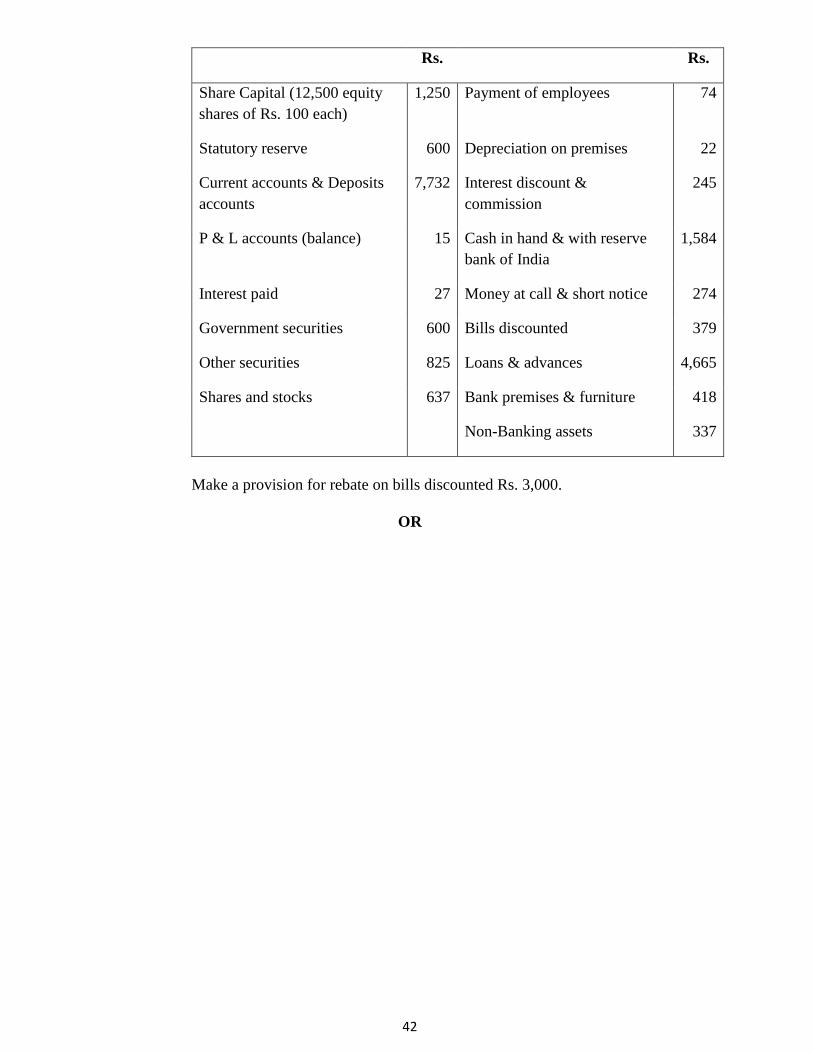

Q.No.9. From the following ledger balances of Laxmi Bank limited. Prepare the profit and

loss account and balance sheet as on 31st March 2010.

42

Rs. Rs.

Share Capital (12,500 equity

shares of Rs. 100 each)

1,250 Payment of employees 74

Statutory reserve 600 Depreciation on premises 22

Current accounts & Deposits

accounts

7,732 Interest discount &

commission

245

P & L accounts (balance) 15 Cash in hand & with reserve

bank of India

1,584

Interest paid 27 Money at call & short notice 274

Government securities 600 Bills discounted 379

Other securities 825 Loans & advances 4,665

Shares and stocks 637 Bank premises & furniture 418

Non-Banking assets 337

Make a provision for rebate on bills discounted Rs. 3,000.

OR

43

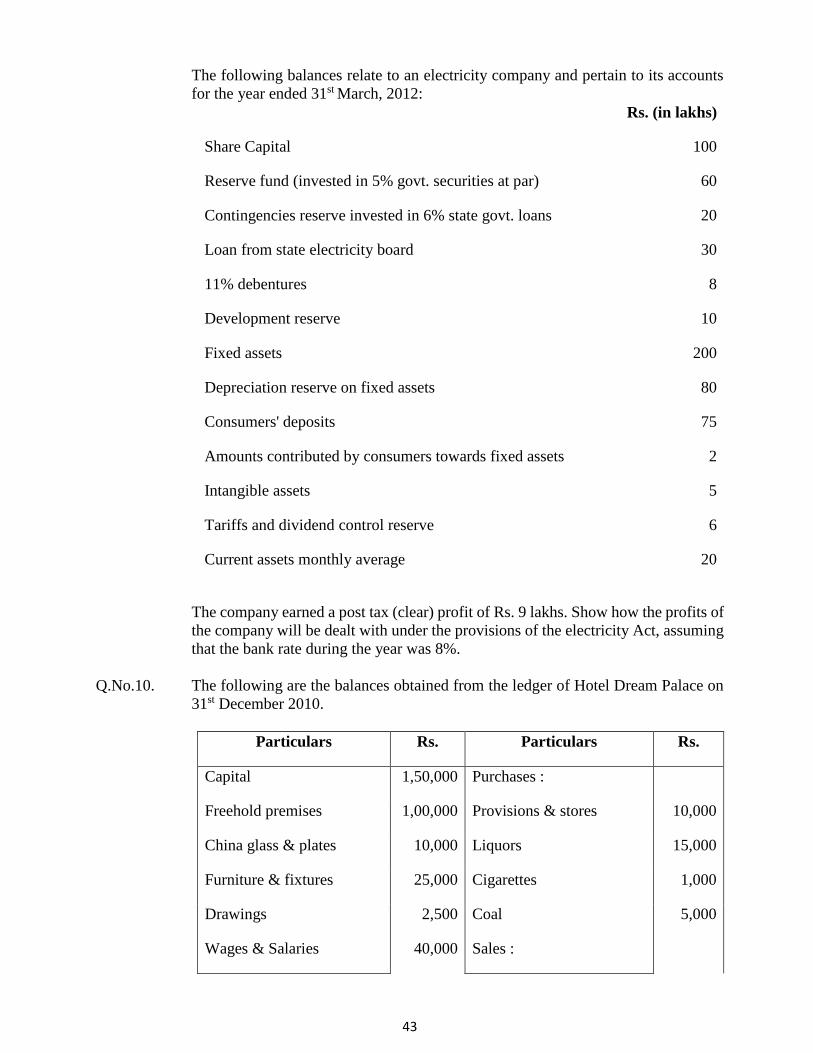

The following balances relate to an electricity company and pertain to its accounts

for the year ended 31st March, 2012:

Rs. (in lakhs)

Share Capital 100

Reserve fund (invested in 5% govt. securities at par) 60

Contingencies reserve invested in 6% state govt. loans 20

Loan from state electricity board 30

11% debentures 8

Development reserve 10

Fixed assets 200

Depreciation reserve on fixed assets 80

Consumers' deposits 75

Amounts contributed by consumers towards fixed assets 2

Intangible assets 5

Tariffs and dividend control reserve 6

Current assets monthly average 20

The company earned a post tax (clear) profit of Rs. 9 lakhs. Show how the profits of

the company will be dealt with under the provisions of the electricity Act, assuming

that the bank rate during the year was 8%.

Q.No.10. The following are the balances obtained from the ledger of Hotel Dream Palace on

31st December 2010.

Particulars Rs. Particulars Rs.

Capital 1,50,000 Purchases :

Freehold premises 1,00,000 Provisions & stores 10,000

China glass & plates 10,000 Liquors 15,000

Furniture & fixtures 25,000 Cigarettes 1,000

Drawings 2,500 Coal 5,000

Wages & Salaries 40,000 Sales :

44

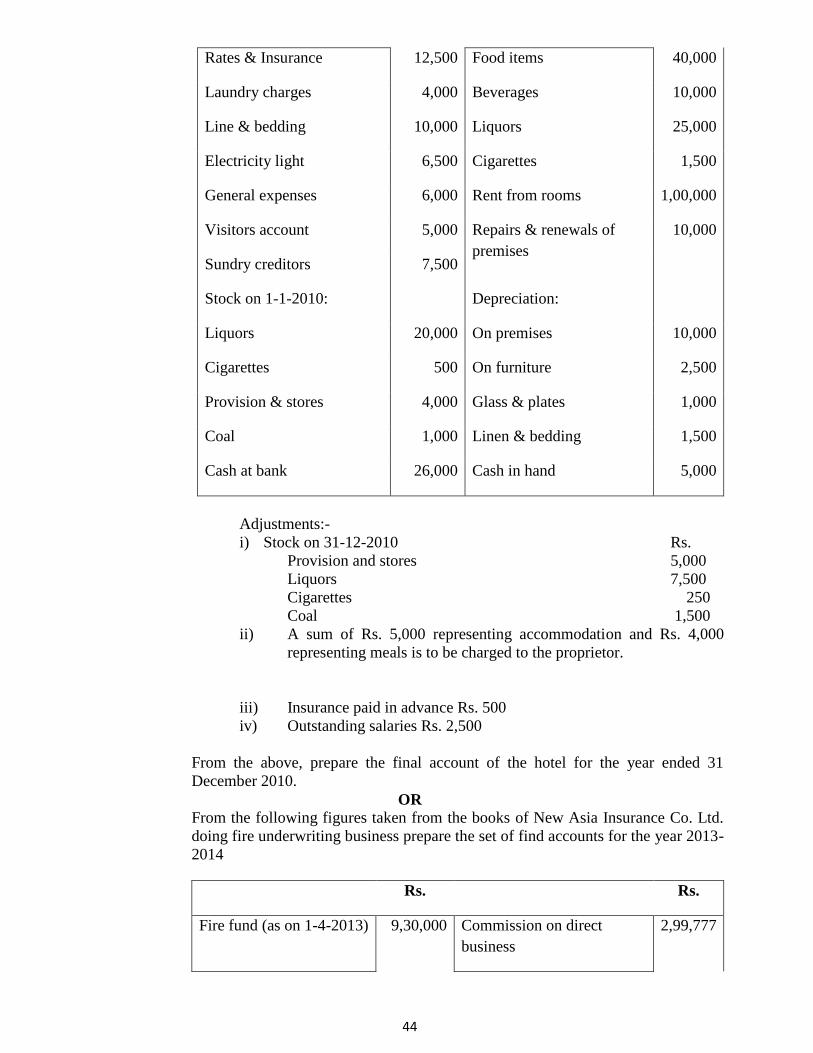

Rates & Insurance 12,500 Food items 40,000

Laundry charges 4,000 Beverages 10,000

Line & bedding 10,000 Liquors 25,000

Electricity light 6,500 Cigarettes 1,500

General expenses 6,000 Rent from rooms 1,00,000

Visitors account 5,000 Repairs & renewals of

premises

10,000

Sundry creditors 7,500

Stock on 1-1-2010: Depreciation:

Liquors 20,000 On premises 10,000

Cigarettes 500 On furniture 2,500

Provision & stores 4,000 Glass & plates 1,000

Coal 1,000 Linen & bedding 1,500

Cash at bank 26,000 Cash in hand 5,000

Adjustments:-

i) Stock on 31-12-2010 Rs.

Provision and stores 5,000

Liquors 7,500

Cigarettes 250

Coal 1,500

ii) A sum of Rs. 5,000 representing accommodation and Rs. 4,000

representing meals is to be charged to the proprietor.

iii) Insurance paid in advance Rs. 500

iv) Outstanding salaries Rs. 2,500

From the above, prepare the final account of the hotel for the year ended 31

December 2010.

OR

From the following figures taken from the books of New Asia Insurance Co. Ltd.

doing fire underwriting business prepare the set of find accounts for the year 2013-

2014

Rs. Rs.

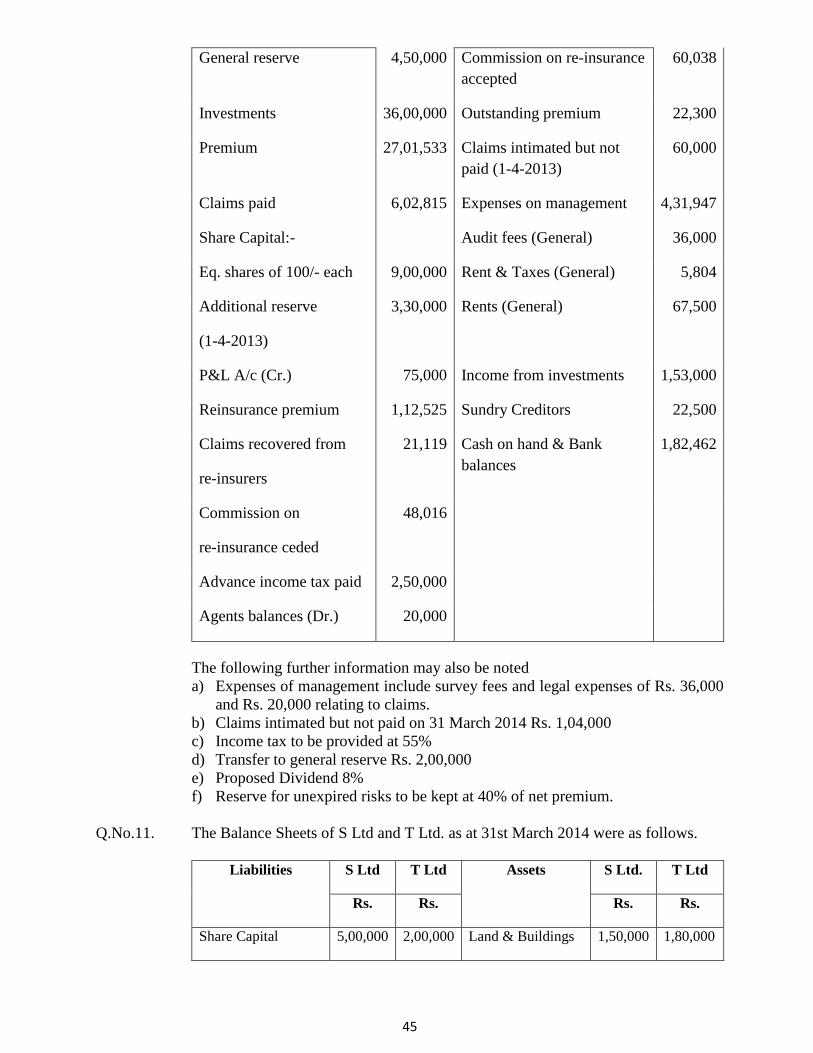

Fire fund (as on 1-4-2013) 9,30,000 Commission on direct

business

2,99,777

45

General reserve 4,50,000 Commission on re-insurance

accepted

60,038

Investments 36,00,000 Outstanding premium 22,300

Premium 27,01,533 Claims intimated but not

paid (1-4-2013)

60,000

Claims paid 6,02,815 Expenses on management 4,31,947

Share Capital:- Audit fees (General) 36,000

Eq. shares of 100/- each 9,00,000 Rent & Taxes (General) 5,804

Additional reserve

(1-4-2013)

3,30,000 Rents (General) 67,500

P&L A/c (Cr.) 75,000 Income from investments 1,53,000

Reinsurance premium 1,12,525 Sundry Creditors 22,500

Claims recovered from

re-insurers

21,119 Cash on hand & Bank

balances

1,82,462

Commission on

re-insurance ceded

48,016

Advance income tax paid 2,50,000

Agents balances (Dr.) 20,000

The following further information may also be noted

a) Expenses of management include survey fees and legal expenses of Rs. 36,000

and Rs. 20,000 relating to claims.

b) Claims intimated but not paid on 31 March 2014 Rs. 1,04,000

c) Income tax to be provided at 55%

d) Transfer to general reserve Rs. 2,00,000

e) Proposed Dividend 8%

f) Reserve for unexpired risks to be kept at 40% of net premium.

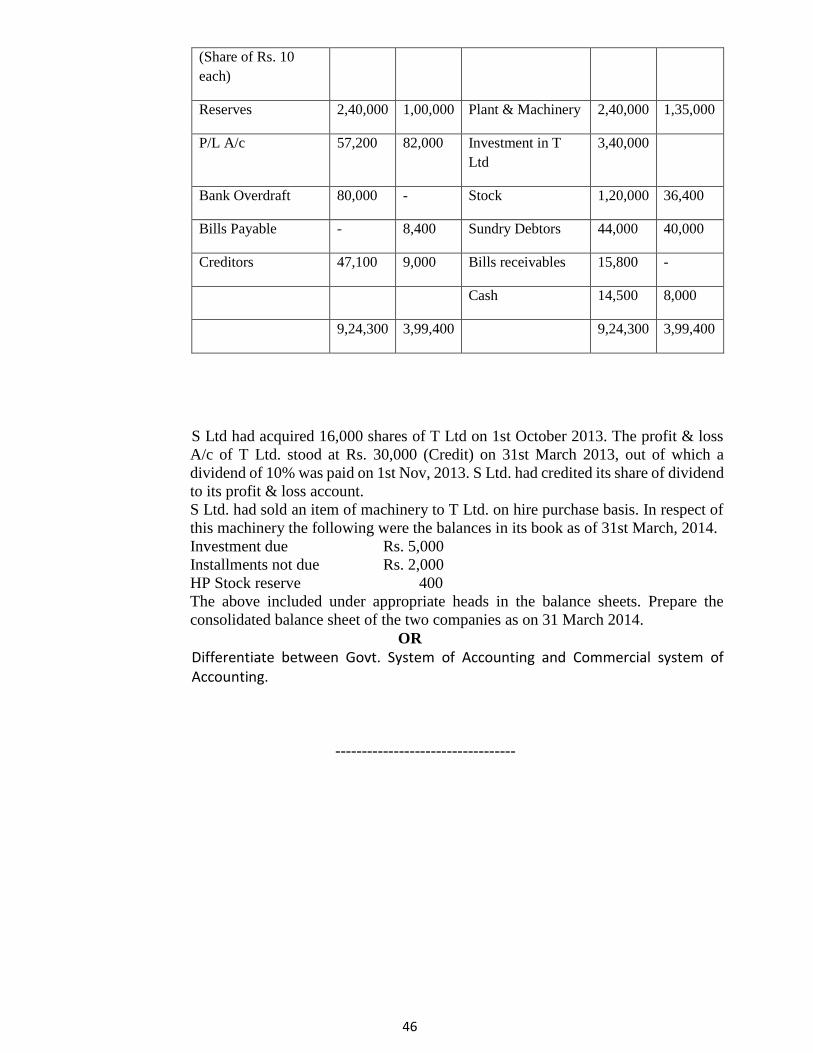

Q.No.11. The Balance Sheets of S Ltd and T Ltd. as at 31st March 2014 were as follows.

Liabilities S Ltd T Ltd Assets S Ltd. T Ltd

Rs. Rs. Rs. Rs.

Share Capital 5,00,000 2,00,000 Land & Buildings 1,50,000 1,80,000

46

(Share of Rs. 10

each)

Reserves 2,40,000 1,00,000 Plant & Machinery 2,40,000 1,35,000

P/L A/c 57,200 82,000 Investment in T

Ltd

3,40,000

Bank Overdraft 80,000 - Stock 1,20,000 36,400

Bills Payable - 8,400 Sundry Debtors 44,000 40,000

Creditors 47,100 9,000 Bills receivables 15,800 -

Cash 14,500 8,000

9,24,300 3,99,400 9,24,300 3,99,400

S Ltd had acquired 16,000 shares of T Ltd on 1st October 2013. The profit & loss

A/c of T Ltd. stood at Rs. 30,000 (Credit) on 31st March 2013, out of which a

dividend of 10% was paid on 1st Nov, 2013. S Ltd. had credited its share of dividend

to its profit & loss account.

S Ltd. had sold an item of machinery to T Ltd. on hire purchase basis. In respect of

this machinery the following were the balances in its book as of 31st March, 2014.

Investment due Rs. 5,000

Installments not due Rs. 2,000

HP Stock reserve 400

The above included under appropriate heads in the balance sheets. Prepare the

consolidated balance sheet of the two companies as on 31 March 2014.

OR

Differentiate between Govt. System of Accounting and Commercial system of Accounting.

----------------------------------

47

M.Com. Fourth Semester Examination (Year 2016)

Direct Taxes in India Subject Code: MCOM -409

Paper Code: TMT-299 Time : 10 Minutes

M.Marks : 10

Section A

[k.M v

(Objective Type Questions)

¼oLrqfu"B Á’u½

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking the

correct answer.

lHkh iz’u vfuok;Z gSaA izR;sd iz’u gsrq 1 vad fu/kkZfjr gSA lgh mÙkj gsrq fn;s x;s ckDl esa () fpUg dk

iz;ksx djsaA

Q. No. 1. Choose the correct answer-

lgh mÙkj pqfu,&

6. Income tax department works under-

vk;dj foHkkx fu;U=.k esa dk;Z djrk gS&

a) Central Government

dsUnzh; ljdkj

b) State Government

jkT; ljdkj

c) Central Board of Direct Taxes

izR;{k djksa dk dsUnzh; cksMZ

d) Chief Commissioner of Income Tax

eq[; vk;dj dfe'uj

2. Every year the residential status of an assessee-

djnkrk dh fuoklh; fLFkfr izR;sd o"kZ&

a) May change b) Will certainly change

cny ldrh gS fuf'pr cnysxh

c) Will not change d) None of these

ugha cnysxh mijksä esa ls dksbZ ugha

3. In which section of the Income-Tax Act exempted incomes have been mentioned?

dj&eqDr vk;ksa dk mYys[k vk;dj vf/kfu;e dh fdl /kkjk esa fd;k x;k gS\

a) Sec. 10 b) Sec. 80

/kkjk 10 /kkjk 80

c) Sec. 88 d) Sec. 2

/kkjk 88 /kkjk 2

4. Sections related to clubbing of income are-

vk; ds feyku ls lEcfU/kr /kkjk,a gSa&

a) Section 60 to 69 b) Section 60 to 64

Invigilator’s Signature

Roll No.

Enrollment No.

48

/kkjk 60 ls 69 /kkjk 60 ls 64

c) Section 60 to 67 d) Section 68 to 69

/kkjk 60 ls 67 /kkjk 68 ls 69

5. The rate of education cess is-

f'k{kk midj dh nj gS&

a) 2% b) 3%

nks izfr'kr~ rhu izfr'kr~

c) 4% d) 5%

pkj izfr'kr~ ik¡p izfr'kr~

6. Minimum age for being a senior citizen is-

ofj"B ukxfjd dgykus ds fy;s U;wure vk;q gS&

a) 60 Years b) 65 Years

60 o"kZ 65 o"kZ

c) 70 Years d) 75 Years

70 o"kZ 75 o"kZ

7. Items are taxed at special rates-

fof'k"V njksa ls dj yxus okyh ensa gSa&

a) Long term capital gain

nh?kZ dkyhu iw¡th ykHk

b) Short term capital gain on shares

va'kksa ij vYidkyhu iw¡th ykHk

c) Lottery and Horse race

ykWVjh ,oa ?kqMnkSM+

d) All of these

mijksä lHkh

8. Tax rate applicable u/s III (A) for short term capital gains on shares sold and

securities transaction tax paid-

izfrHkwfr dj pqdk;s x;s va'kksa ds vYidkyhu iw¡th ykHkksa ij /kkjk III (A) ds vUrxZr dj

dh nj gS&

a) 10% b) 15%

nl izfr'kr~ iUnzg izfr'kr~

c) 20% d) 30%

chl izfr'kr~ rhl izfr'kr~

9. Getting permanent account number is compulsory for-

LFkk;h [kkrk la[;k izkIr djuk vfuok;Z gS&

a) Income tax Assessee

vk;dj nkrk

b) Importer

vk;krd

c) Assessee under service tax

lsok 'kqYd ds vUrxZr djnkrk

d) All of these

mijksä lHkh

10. Section of best judgement assessment is-

49

loksZÙke fu.kZ; dj&fu/kkZj.k dh /kkjk gS& f) 143 b) 144

c) 147 d) 148

-------------------------

M.Com. Fourth Semester Examination (Year 2016)

Direct Taxes in India Subject Code: MCOM-409

Paper Code: TMT-299 Time : 2 Hrs. 50 Mts.

M.Marks : 60

Section B

[k.M c (Short Answer Type Questions)

(y?kqmÙkjh; iz’u)

Attempt all questions. Each question carries 4 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 4 vad fu/kkZfjr gSA

Q.No.2. In what circumstances is the income of one person treated as the income of other?

,d O;fDr dh vk; nwljs dh vk; fdu ifjfLFkfr;ksa esa ekuh tkrh gS\

OR

When will a person be treated as resident of India?

dksbZ O;fDr Hkkjr dk fuoklh dc ekuk tk;sxk\

Q.No.3. Mention the Income Tax rates applicable for individual assessee in respect of

Assessment Year 2015-2016.

dj&fu/kkZj.k o"kZ 2015&2016 ds fy;s O;fDr djnkrk ds fy;s izHkkoh vk;dj dh njksa dk

mYys[k dhft;sA

OR

Calculate the income tax payable by the following persons for the assessment year

2015-2016-

a) Total income of Anil is 4,75,000.

b) Total income of Pradeep is Rs. 10,60,000.

fuEufyf[kr O;fDr;ksa }kjk dj&fu/kkZj.k o"kZ 2015&2016 ds fy;s ns; vk;dj dh x.kuk

dhft,&

v½ vfuy dh dqy vk; 4]75]000 :Ik;s gSA

c½ iznhi dh dqy vk; 10]60]000 :Ik;s gSA

Q.No.4. Describe "Belated Return."

^^foyfEcr fooj.k** D;k gS& le>kb;sA

OR

What do you understand by Reassessment? In what circumstances is it done?

iqu% dj&fu/kkZj.k ls vki D;k le>rs gSa\ ;g fdu ifjfLFkfr;ksa esa fd;k tkrk gS\

Roll No.

50

Q.No.5. What are the payments on which tax is deducted at source?

os Hkqxrku dkSu&ls gSa ftuls mn~xe LFkku ij dj dkVk tkrk gS\

OR

State the penalty for concealment of income.

fNikbZ xbZ vk; ds lEcU/k esa vFkZn.M crkb;sA

Q.No.6. Write a note on appeal to a Supreme Court against the judgement of the High Court.

fVIi.kh fyf[k,&mPpre U;k;ky; esa mPp U;k;ky; ds vkns'k ds fo:) vihyA

OR

Describe the organization of the Income Tax Department.

vk; dj foHkkx ds laxBu dh O;k[;k dhft,A

Section C

[k.M l (Long Answer Type Questions)

(nh?kZ mÙkjh; iz’u)

Attempt all questions. Each question carries 8 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 8 vad fu/kkZfjr gSA

Q.No.7. Explain the deduction u/s 80 G.

/kkjk 80 G dh dVkSrh le>kb,A

OR

The following are the particulars of Income of Mr. Vikas for the Previous Year

2014-2015:-

1. Profit from business in Japan received in India Rs. 1,00,000

2. Income from house property in Bangladesh received in India Rs. 1,000

3. Income from house property in Srilanka, deposited in a bank

there

Rs. 2,000

4. Profit from business in Burma, deposited in a bank there. The

business is controlled from India

Rs.2,000

5. Accrued in India but received in Malaysia Rs.4,000

6. Profit from business in Indore Rs. 2,72,000

7. Past untaxed foreign income brought into India during the

previous year;

Rs.15,000

From the above particulars, compute the taxable income of Mr. Vikas for the

Assessment Year 2015-2016 if he is-