Embed Size (px)

Citation preview

Zamira Simkins, Richard Stewart 1

Measuring a Port’s Performance Using the Real Economic Value of 1

Commodities 2

3

4

Re-submission date: November 15, 2012 5

Word count: 7,454 (including 5 figures and 2 tables) 6

7

8

Zamira Simkins, Ph.D. 9

Assistant Professor of Economics 10

Department of Business and Economics 11

University of Wisconsin Superior 12

Belknap & Catlin 13

PO Box 2000 14

Superior, WI 54880 15

Tel: (715) 394-8360 16

Fax: (715) 394-8180 17

E-mail: [email protected] 18

19

Richard Stewart, Ph.D, CTL* 20

Director, Transportation and Logistics Research Center 21

Professor, Department of Business and Economics 22

University of Wisconsin-Superior 23

Belknap & Catlin 24

PO Box 2000 25

Superior, WI 54880 26

Tel: (715) 394-8547 27

Fax: (715) 394-8180 28

E-mail: [email protected] 29

30

* Corresponding author 31

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 2

Measuring a Port’s Performance Using the Real Economic Value of 1

Commodities 2

3

The marine transportation system plays a significant role in many economies, and ports serve as 4

gateways to economic activities. Ports ability to provide services depends on their facilities, but 5

ports typically have to compete for federal, state, local and private funding. To allocate scarce 6

resources efficiently and effectively, decision-makers must be able to assess ports performance 7

over time and relative to other ports. Conventionally, tonnage or ton-miles statistics are used in 8

bulk port evaluations. These indicators, however, do not reflect the heterogeneity of ports cargo 9

or the economic value of their service, which makes ports performance comparison difficult. To 10

address these issues, we propose three economic port performance measures that add new 11

information decision-makers can use in bulk port assessments: total real value of commodities, 12

average real value per ton, and real value index of a port. Container ports already collect similar 13

data in nominal terms, but bulk ports typically do not. Economists, however, track the real value 14

of commodities when measuring economic performance. Hence, the proposed methodology can 15

be applied to all, container and bulk, ports. Further, total real value and average real value per 16

ton can be used to compare the economic performance of different ports, and real value index of 17

a port can help assess the economic performance of a given port over time. To illustrate how 18

these economic port performance measures can be calculated, we use the Port of Duluth-Superior 19

as a case study and produce three series of annual indicators based on publicly available data. 20

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 3

INTRODUCTION 1

The marine transportation system plays a significant role in many countries’ economies. In the 2

US, for example, in 2010, 80 percent of all freight tonnage in foreign trade was moved by water 3

(1, p. 13). Ports play a vital role in this system by serving as gateways to economic activities. 4

Ports are not alike, however; some mostly handle containerized cargo, others – bulk cargo, or a 5

combination of cargoes, which range from basic primary commodities to high-tech manufactured 6

goods. The importance of all of these ports is undisputable, but their ability to provide services 7

often depends on the state of their facilities and ability to obtain resources to support them. In 8

the United States, all ports compete for federal, state, local and private resources. To allocate 9

scarce resources efficiently and effectively, decision-makers must be able to assess a port’s 10

performance not only over time but also relative to other ports. Conventionally, TEU’s tonnage 11

or ton-miles statistics are used in evaluating ports performance in terms of cargo shipped. These 12

indicators, however, do not reflect the heterogeneity of ports cargo, the monetary value ports 13

helps create, or the economic significance of their service. When using the tonnage indicator, 14

decision-makers essentially weigh one ton of coal, for instance, equally to one ton of wheat. 15

Markets, however, weigh one ton of wheat as more valuable than one ton of coal. In the US, for 16

example, in 2010, hard red winter wheat was worth $246 per net ton (1 short ton = 2,000 pounds) 17

and subbituminous coal was only $14 per net ton (2, 3). 18

To capture the heterogeneity of ports cargo and the economic role of ports, we propose 19

using the economic value of cargo as one of the criteria for assessing bulk ports’ economic 20

performance. In fact, container ports already collect similar data, but bulk ports typically do not. 21

The collected data, however, is tracked in nominal terms, or using prices not adjusted for 22

inflation (i.e., current prices). Then, the nominal value of a port’s cargo can increase over time 23

either because a port transports more tonnage or because cargo prices increase over time. If a 24

port’s tonnage increases over time, it typically reflects an increasing demand for the port’s 25

services; whereas higher current prices of commodities are usually associated with inflation. 26

Since inflation raises all prices, using the nominal value of cargo can mislead decision-makers, 27

particularly during periods of high inflation. To separate the effect of inflation from the 28

changing demand for port’s services, it is necessary to use the real economic value of cargo to 29

measure the economic performance of a port, where the real value of commodities is calculated 30

by adjusting the nominal market prices for inflation (or by using constant prices). 31

Given the above discussion and to enable decision-makers to compare the performance of 32

different ports, as well as assess a given port’s performance over time, we propose three new 33

economic port performance measures: the total real value of commodities, the average real value 34

per ton, and the real value index of a port. The total real value and the average real value per ton 35

measures can be used to compare the economic performance of different ports, whereas the real 36

value index of a port can help assess the economic performance of a given port over time. The 37

methodology behind these three measures is similar to how economists measure the economic 38

productivity and performance of a country (i.e., real gross domestic product). 39

In overall, tracking the real value of a port’s cargo is useful because it can: (i) offer an 40

economic justification for resource allocation decisions, (ii) help reveal the trends in the demand 41

for a given port’s services, (iii) be used in developing economic impact studies, (iv) be used by 42

the port and the waterway navigational authorities in port development planning, and (v) be used 43

in pricing of port’s services based on the value of service approach. It must be acknowledged, 44

however, that knowing the economic value of the cargo alone does not provide decision-makers 45

with complete information sufficient to allocate scarce resources efficiently and effectively. 46

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 4

Other indicators, such as the operational and financial port performance metrics and port 1

customers’ perspectives (4), need to be considered as well. 2

Given the fact that there are currently no universally accepted standard methods of 3

measuring a port’s economic performance (5), the primary goal of this paper is to propose a set 4

of enhanced practical economic port performance measures that policy-makers, port-authorities, 5

and other decision-makers and interested parties can try out in various suggested applications. 6

To illustrate how the proposed economic port performance measures can be calculated, we use 7

the Port of Duluth-Superior as a case study and produce three series of annual indicators using 8

publicly available data. The methodology used in the project can be potentially replicated for all 9

ports. 10

11

PORT PERFORMANCE INDICATORS 12

The efforts to develop formal port performance indicators can be traced back to the 1976 United 13

Nations Conference on Trade and Development, which produced a report containing a set of 14

operational and financial port performance indicators aimed at improving ports operations and 15

port development plans (6). Table 1 provides a summary of these UNCTAD-proposed port 16

performance measures, out of which the only indicators that all ports, container and bulk cargo, 17

currently publicly report on a consistent basis are the ships arrival rate and the total tonnage 18

worked. 19

20

TABLE 1 UNCTAD Financial and Operational Port Performance Indicators 21

Indicator Measurement unit

Operational indicators

Ships arrival rate (average daily ship arrivals) Ships/day

Berthing ship waiting time (average wait between arrival and berthing) Hours/ship

Ship service time (average time between ship berthing and departure) Hours/ship

Ship turnaround time (average time between ship arrival and departure) Hours/ship

Total tonnage worked/Total number of ships Tons/ship

Total time berthed ships worked/Total ships turnaround time Ratio

Total gross gang time/Total time berthed ships worked Ratio

Total tonnage worked/Total ships turnaround time Tons/hour

Total tonnage worked/Total ships service time Tons/hour

Total tonnage worked/Total gross gang time Tons/gang-hour

Total idle gang time/Total gross gang time Ratio

Financial indicators

Total tonnage worked Tons

Total revenue from berth occupancy/Total tonnage worked $/ton

Total revenue from handling cargo/Total tonnage worked $/ton

Labor expenditures from handling cargo/Total tonnage worked $/ton

Capital equipment expenditures/Total tonnage worked $/ton

Total contribution = Revenues from berth occupancy and handling cargo

– Labor and capital expenditures (i.e., profit)

$

Total contribution/Total tonnage worked (i.e. profit per ton) $/ton

22

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 5

Since the UNCTAD report, many studies were published on different aspects of ports 1

performance. In 1997-2008, there were 395 port-related studies published in 51 different 2

journals, which Pallis, Vitsounis, De Langen and Notteboom classified into seven research 3

themes (7). Terminal studies examined the port terminals’ performance as measured by terminal 4

operational productivity, which over time changed from partial productivity measures (e.g. 5

vessel turnaround time, yard productivity, crane productivity, labor productivity, etc.) to more 6

comprehensive, overall terminal efficiency assessments (based on Data Envelopment Analysis 7

and Stochastic Frontier Models). Port governance studies focused on improving ports operations 8

via governance reforms: for example, studies assessing a port’s performances before and after 9

privatization largely focused on a port’s financial performance indicators. Studies related to port 10

planning and development mainly assessed the economic impact of ports and ports’ future 11

development plans. Empirical data used in these various studies was essentially based on 12

different port performance indicators, ranging from ports contribution to local, national, and 13

regional development to port operational efficiency, maritime costs, terminal utilization, vessel 14

in-port time, and so on. Further, according to their classification, port competition and 15

competitiveness was the most popular port research theme. Several interesting studies included 16

in this theme were by De and Ghosh (8) and Haezendock, Coeck and Verbeke (9). The former 17

combined the port’s financial, operational, and assets management performance indicators into a 18

composite port performance index and found that more efficient ports tend to have a higher 19

traffic volume. The latter proposed a port’s performance indicator based on differences in 20

creating the value-added among traffic categories and suggested that their indicator can be used 21

to identify future port market niches. 22

Conceptually, modern port performance indicators can be distinguished from an 23

engineering and an economic perspective (10). The engineering port performance evaluation 24

approach involves comparing the actual physical port throughput (e.g., tonnage or number of 25

containers) to some engineering optimum level of throughput. The economic port performance 26

evaluation follows the microeconomic approach of maximizing port’s profits. To a large extent, 27

these indicators continue to follow the operational and financial port performance classifications 28

developed earlier by UNCTAD. When it comes to resources allocation, in theory, “in an 29

environment in which ports have natural hinterlands and are not in competition with one another, 30

an engineering performance evaluation…may be appropriate…In an environment in which ports 31

are in competition with one another…an economic optimum…should be utilized” (10, p. 500). 32

Since nearly all domestic ports face competition, if not with each other then with other modes of 33

transportation (e.g., bulk ports compete with railroads in transporting coal), economic port 34

performance evaluation is just as appropriate for bulk ports as for container ports, especially 35

when it comes to resource allocation decisions. 36

The in-field port performance measurements have been studied by the Port Performance 37

Research Network, which in 2004-2005 surveyed 42 port authorities about which port 38

performance metrics the ports in fact collected (11). The results of this survey are presented in 39

Table 2. Further, according to de Langen, Nijdam and van der Horst (12) survey, the most 40

common port performance metrics used today are the throughput volume, port-related 41

employment, and value added. 42

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 6

TABLE 2 Main Port Performance Indicators Collected by Ports (11) 1

Performance indicator Number of ports

collecting data

Financial measures (N = 30)

Growth rate of profit (before taxes) 25

Debt to equity ratio 23

Ancillary revenue as % of gross revenue 22

Interest coverage ratio 21

Return on capital employed 21

Average days accounts receivable 19

Port related profit as % of port related revenue 19

Terminal charges as % of gross revenue 19

Capital expenditure as % of gross revenue 13

Vessel operations (N = 34)

Average vessel calls per week 29

Average hours of turnaround time per vessel 24

Average waiting time at anchor 22

Length of quay in meters 22

Revenue per ton handled 19

Hours of equipment downtime per month 14

Container operations (N = 30)

Growth in TEU throughput 19

Container port throughput (TEU/meter of quay per

year)

18

Import containers as % of total containers 17

20’ TEU as % of total TEY per year 17

Lifts per crane per hour 12

Average yard dwell time in hours 10

Average revenue per TEU 9

Other indicators (N = 34)

Destinations served in the current year 21

Number of customers served 18

Overall customer satisfaction 15

Customer complaints per month 15

Employee turnover rate 14

2

Most of the reviewed literature suggests that port authorities can effectively control the 3

port’s financial performance by controlling the port’s operational performance and port 4

customers’ satisfaction levels. This explains why ports collect ample data on their operational 5

performance. At the same time, ports seem to have little power over the demand for their 6

services, which primarily depends on external to port factors, such as fluctuations in the world 7

commodity prices and pace of regional development. Therefore, in addition to assessing the port 8

internal (operational and financial) indicators, port authorities and decision-makers should assess 9

external to port factors as well (e.g., demand for port’s services). 10

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 7

To help approximate the trends in the demand for port’s services, it is often useful to 1

track the changes in the real value of commodities shipped through a port. As will be 2

demonstrated in the methodological section, real value of commodities, as opposed to nominal, 3

separates the effects of inflation from the value of commodities and reveals the changes in the 4

demand for port’s services. Conceptually, as the real value of transported cargo increases, 5

ceteris paribus, the demand for port’s services tends to increase as well, and more cargo can be 6

expected to pass through a port. This information then can be used for port development 7

planning purposes, resource allocation decisions, economic impact studies, value of service 8

pricing, and so on. 9

Using the value of commodities as an economic port performance measure is not a new 10

concept, but most of the reviewed literature uses the nominal value of commodities as opposed to 11

real, or at least does not explicitly state that the cargo value is measured in real terms. All major 12

US container ports, for example, track the overall value of the cargo that goes through them and 13

use this data to showcase their performance. Port of Los-Angeles, for instance, reported that in 14

2007 it was the #1 port in the US in terms of the cargo value and container volume (13). 15

Similarly, the Port of Baltimore reported that in 2011 it ranked 11th

among 360 US ports in terms 16

of the cargo value and 12th

for tonnage (14). On an aggregate level, in 2009, US container ports 17

handled about $474 billion of containerized cargo (15). At a national level, the value of cargo 18

moving by mode is tracked by the US Bureau of Transportation Statistics. Further, private firms 19

in the US, such as Martin and Associates, and other researchers worldwide assess the value of 20

ports cargo to determine the economic impact of ports (16, 17, 18). The US Maritime 21

Administration has long used the value of sales revenue and value added to calculate their 22

multipliers of the economic impact of ports (19). The US Army Corps of Engineers also 23

publishes data on the value of cargo moving through the Great Lakes system, but the data is not 24

broken down to individual port level (20). Such a system-wide view may provide an excellent 25

oversight; however, funding for dredging, port development and terminals is done at a port level. 26

On rare occasions, when the USACE reports the value of cargo shipped by an individual port, 27

such data is often difficult to use in decision-making situations. For example, in the Great Lakes 28

Fact sheets, USACE listed the value of cargo shipped through the Port of Duluth-Superior at $2 29

billion (20). It is not clear, however, which year was evaluated or what estimation methodology 30

was used. For comparison, when we estimated the total nominal value of the Port of Duluth-31

Superior cargo, it was $2.2 billion in 2006 and $2.8 billion in 2007. Hence, clear methodology 32

and periodic timely reporting of port-level economic indicators are necessary. Further, if the 33

value of cargo is used as an economic port performance measure, it needs to be reported in real 34

terms, or adjusted for inflation. 35

36

REAL ECONOMIC VALUE OF COMMODITIES: METHODOLOGY 37

This paper proposes three economic port performance indicators that can be applied to both bulk 38

and container cargo-handling ports: total real value (TRV) of cargo moved through a port, 39

average real value (ARV) per ton moved, and real value index (RVI) of a port. The design of the 40

first two indicators allows comparing the economic performance of different ports relative to 41

each other, whereas the third indicator can help assess a given port’s economic performance 42

relative to itself over time. The total real value of cargo moved through a port can also be used 43

as a tool to help forecast the demand for port’s services, which then can be used to rationalize the 44

port funding decisions, development plans, and other port capacity-related proposals. 45

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 8

The methodology behind the proposed total real value of cargo indicator is similar to that 1

of the real gross domestic product (GDP). By definition, real GDP is the total market value of all 2

final goods and services produced in an economy during a given year and calculated using 3

constant prices. Economists use real GDP as a standard statistic to measure the aggregate 4

economic performance of a country. Similarly, we propose using the total real value of cargo 5

moved through a port as an aggregate economic performance measure of a port. The total value 6

of bulk cargo shipped through a port can help address the heterogeneous cargo issue discussed 7

earlier. Market prices are initially used to estimate the nominal value of commodities because 8

they represent the value of cargo to transacting parties. The higher the value of cargo the more 9

parties value such cargo and, hence, port’s services. Tracking the value of cargo can then also be 10

useful in developing the value of service pricing strategies. The real value of cargo is calculated 11

by adjusting the nominal market prices for inflation; so, the indicator would capture only an 12

increase in the value of commodities to transacting parties, not the effect of a rise in the general 13

level of prices (graphically, the pure inflationary effect can be pictured in figure 1, panel A as a 14

shift from equilibrium E2 to E3, with the equilibrium quantity of commodities remaining 15

essentially constant at Q2 level but the equilibrium price level rising above P2). Then, similar to 16

real GDP, when the total real value of cargo transported through a port increases, it can be 17

explained as a result of the increasing demand for such commodities, as current market 18

commodity prices get adjusted for inflation. Higher demand for commodities in turn means 19

higher demand for port’s services. These linkages between the commodity market and the 20

market for port services are illustrated in figure 1. 21

22

23 Panel A shows the commodity market and panel B shows the market for port’s services. 24

In panel A, blue line denoted Demand1 illustrates the initial demand for a commodity; orange 25

line denoted Supply illustrates the commodity supply. When the demand for a commodity 26

Transp. cost Price

Welfare

loss

C

Revenue

loss

Q2 Q1

P2

P1

Demand1

Demand2

Supply

Quantity Q2 Q1 = T

Demand1

Demand2

Supply

Quantity

Panel (a) Commodity market

FIGURE 1 Commodity market and port services.

E2

E3

E1

E1 E2

Not feasible

Panel (b) Port services

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 9

increases, the demand curve shifts to the right from Demand1 to Demand2. As a result, the 1

equilibrium market price of a commodity increases, and suppliers respond to the higher price by 2

increasing the quantity of the commodity supplied to the market. Consequently, the equilibrium 3

price and quantity increase from P1 to P2 and from Q1 to Q2 respectively. Higher equilibrium 4

quantities in a commodity market means more tonnage needs to be transported, so the demand 5

for port’s services would increase. This creates a link between the commodity market and the 6

port’s services market. 7

In panel B, blue line denoted Demand1 illustrates the initial demand for port’s services, 8

and orange line denoted Supply illustrates the supply of port’s services. The supply of port’s 9

services is drawn as a vertical line because at any given point in time a port’s operating capacity 10

is limited, as it takes time and resources to expand ports facilities. Further, to simplify the 11

analysis, we assume that the illustrated port’s operating capacity, T, is equal to the initial 12

commodity tonnage, Q1. This assumption allows us to easily illustrate that an increase in the 13

demand for the port’s services may not be feasible given the current supply of port’s services. 14

Of course, the exact extent to which the demand for port’s services would increase depends on 15

how competitive a port is in comparison to other local modes of transportation. This competitive 16

relationship can be potentially measured by conducting a more comprehensive study, which is 17

beyond the scope of this paper, but presents opportunities for future research. Further, for 18

practical purposes, the assumption that a port operates at a full operating capacity should not be 19

automatic. It is made here merely to ease the illustration of how the real economic value of 20

commodities can help track the changes in the demand for port’s services. 21

After the demand for a commodity increases in panel A, the demand for port’s services 22

increases as well, causing a shift in panel B from Demand1 to Demand2. However, given the 23

port’s current operating capacity, T, transporting higher quantities such as Q2 is not feasible. 24

Then, unless the commodity suppliers find other ways to transport their products, they will face 25

lost revenue opportunities, which are represented by the grid-like fill-pattern area of a 26

rectangular shape in panel A (orange-filled grid area). In turn, the society will face a welfare 27

loss represented by the diagonal-line fill-pattern area of a triangular shape in panel A (blue 28

diagonally lined area). The economic inefficiency associated with this welfare loss and foregone 29

revenues can be prevented if the supply of port’s services can be increased to Q2 level, but this 30

will depend on the port’s ability to obtain resources. Since ports are vital for regional 31

economies, tracking and analyzing changes like these then becomes critical in ensuring that the 32

supply of port’s services can keep up with the demand. 33

The mathematical formula for calculating the proposed total real value (TRV) of a port’s 34

cargo is presented below, where P stands for the market price of a commodity, Q stands for the 35

commodity’s tonnage moved through a port, PPI stands for a producer price index, i indices all 36

transported commodities, and t indices years: 37

1 100

Nit

t it it

i

PPITRV P Q

38

One drawback of the total real value of the cargo indicator is that being an aggregate 39

measure it does not explicitly reflect how many tons were actually moved or how valuable a ton 40

of cargo is. Therefore, to improve the allocation of resources, we suggest considering the 41

following measure of the average real value per ton moved, which is just the total real value of 42

the port’s cargo divided by the total tonnage: 43

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 10

1

tt N

it

i

TRVARV

Q

1

Neither of the above two measures should be considered as the only relevant measures of 2

a port’s performance. Rather, we recommend using them in combination with other port 3

performance indicators, the exact set of which will depend on the ultimate purpose of the port’s 4

performance assessment. Theoretically, however, the above two measures could be potentially 5

applied as follows: if two ports ship the same tonnage but different total real values of the cargo 6

and are otherwise equivalent in all other port performance measurement aspects, the port with a 7

higher average real value per ton should receive more funding. 8

The above two indicators can help decision-makers compare the performance of different 9

ports to each other. The real value index of a port is an indicator that can track a given port’s 10

performance over time or relative to itself at a given point in time. The formula for calculating 11

the proposed real value index of a port is presented below: 12

2005

100tt

TRVRVI

TRV

13

This index essentially compares the total real value of the port’s cargo in a given year to a 14

base year of 2005 in percentage terms. The choice of such reference point is critical. In 15

economic literature, it is usually a time period when the economy is neither in a recession nor 16

booming. Since the Bureau of Economic Analysis currently uses 2005 as a base year, we chose 17

to do the same. Alternatively, the base year could also represent a time period when a port 18

receives public funds, and then statistical analysis could be performed to examine the economic 19

effect of funding on the port’s performance. 20

21

PORT OF DULUTH-SUPERIOR: DATA 22

The Port of Duluth-Superior is located at the western end of the Great Lakes St. Lawrence 23

Seaway System. It is the US farthest inland freshwater seaport and accommodates both domestic 24

and international trade. Based on 2009 data, it ranks as the second largest dry cargo bulk port in 25

the US and #1 volume port on the Great Lakes. According to the port’s facts sheet, over 90 26

percent of the port’s cargo tonnage is composed of dry bulk cargo: taconite pellets, 27

subbituminous coal, and grain. Among other transported cargo are cement, fertilizers, salt, scrap 28

metal, wind turbine components, and so on. The port annually handles about 42 million short 29

(net) tons of cargo and over 1,000 vessels calls per year (21). 30

As stated earlier, data on the Port of Duluth-Superior cargo value is very limited, which 31

reduces the amount of information decision-makers can use in assessing its economic 32

performance. This case study will help fill this data gap. Further, using the Port of Duluth-33

Superior as a case study will allow us to illustrate how the proposed economic port performance 34

measures can be calculated. Practitioners then can use this example to apply the proposed 35

economic port performance measurement methodology to other ports. 36

To calculate the proposed economic port performance indicators, we started by collecting 37

the following statistical data on the Port of Duluth-Superior: (i) cargo tonnage, (ii) market prices 38

of commodities shipped through the port, and (iii) producer price indices of the transported 39

commodities (2, 3, 22, 23, 24). All data was collected from publicly available sources and 40

converted into uniform units of measurement. Particularly, we made sure that all cargo tonnage 41

was measured in net tons, and all commodity prices were in dollars per net ton. 42

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 11

1 FIGURE 2 Port of Duluth-Superior commodities tonnage. 2

3

4 FIGURE 3 Nominal market prices of commodities. 5

6

0

5

10

15

20

25

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Mil

lio

n N

et T

on

s

Taconite Grain Coal

0

50

100

150

200

250

300

350

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

$ p

er n

et t

on

Hard red winter wheat Subbituminous coal (Vale) Iron Ore Pellets

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 12

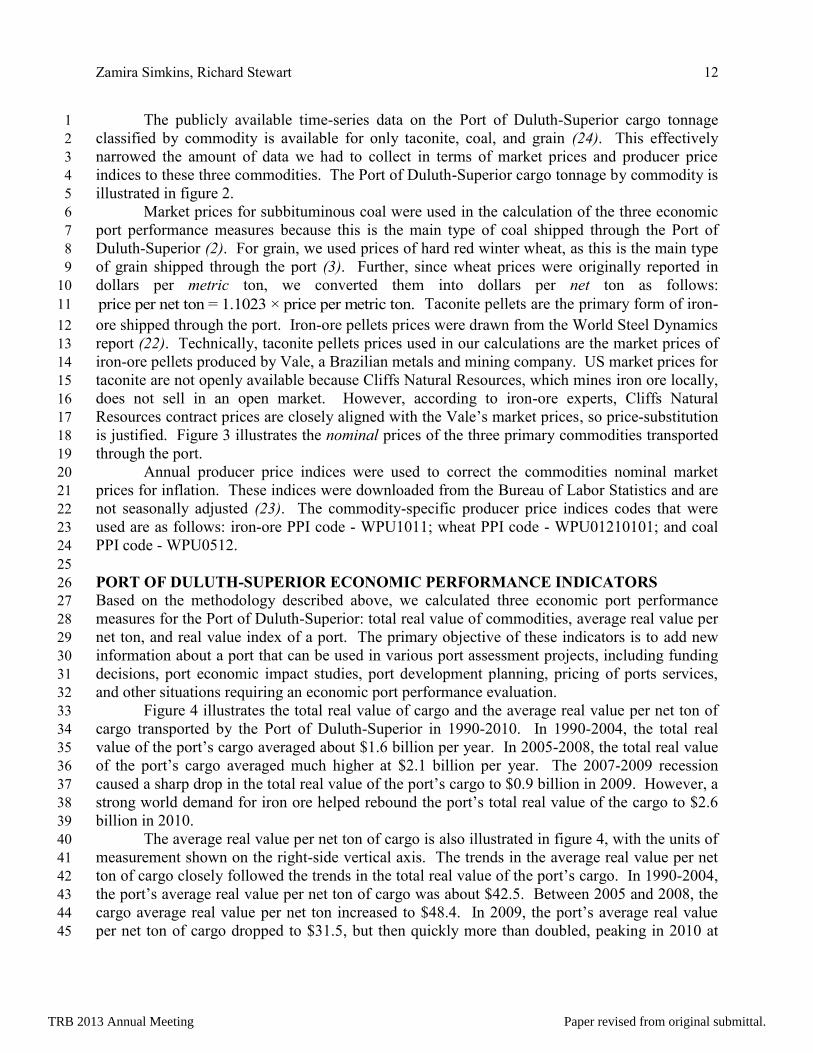

The publicly available time-series data on the Port of Duluth-Superior cargo tonnage 1

classified by commodity is available for only taconite, coal, and grain (24). This effectively 2

narrowed the amount of data we had to collect in terms of market prices and producer price 3

indices to these three commodities. The Port of Duluth-Superior cargo tonnage by commodity is 4

illustrated in figure 2. 5

Market prices for subbituminous coal were used in the calculation of the three economic 6

port performance measures because this is the main type of coal shipped through the Port of 7

Duluth-Superior (2). For grain, we used prices of hard red winter wheat, as this is the main type 8

of grain shipped through the port (3). Further, since wheat prices were originally reported in 9

dollars per metric ton, we converted them into dollars per net ton as follows: 10

price per net ton = 1.1023 × price per metric ton. Taconite pellets are the primary form of iron-11

ore shipped through the port. Iron-ore pellets prices were drawn from the World Steel Dynamics 12

report (22). Technically, taconite pellets prices used in our calculations are the market prices of 13

iron-ore pellets produced by Vale, a Brazilian metals and mining company. US market prices for 14

taconite are not openly available because Cliffs Natural Resources, which mines iron ore locally, 15

does not sell in an open market. However, according to iron-ore experts, Cliffs Natural 16

Resources contract prices are closely aligned with the Vale’s market prices, so price-substitution 17

is justified. Figure 3 illustrates the nominal prices of the three primary commodities transported 18

through the port. 19

Annual producer price indices were used to correct the commodities nominal market 20

prices for inflation. These indices were downloaded from the Bureau of Labor Statistics and are 21

not seasonally adjusted (23). The commodity-specific producer price indices codes that were 22

used are as follows: iron-ore PPI code - WPU1011; wheat PPI code - WPU01210101; and coal 23

PPI code - WPU0512. 24

25

PORT OF DULUTH-SUPERIOR ECONOMIC PERFORMANCE INDICATORS 26

Based on the methodology described above, we calculated three economic port performance 27

measures for the Port of Duluth-Superior: total real value of commodities, average real value per 28

net ton, and real value index of a port. The primary objective of these indicators is to add new 29

information about a port that can be used in various port assessment projects, including funding 30

decisions, port economic impact studies, port development planning, pricing of ports services, 31

and other situations requiring an economic port performance evaluation. 32

Figure 4 illustrates the total real value of cargo and the average real value per net ton of 33

cargo transported by the Port of Duluth-Superior in 1990-2010. In 1990-2004, the total real 34

value of the port’s cargo averaged about $1.6 billion per year. In 2005-2008, the total real value 35

of the port’s cargo averaged much higher at $2.1 billion per year. The 2007-2009 recession 36

caused a sharp drop in the total real value of the port’s cargo to $0.9 billion in 2009. However, a 37

strong world demand for iron ore helped rebound the port’s total real value of the cargo to $2.6 38

billion in 2010. 39

The average real value per net ton of cargo is also illustrated in figure 4, with the units of 40

measurement shown on the right-side vertical axis. The trends in the average real value per net 41

ton of cargo closely followed the trends in the total real value of the port’s cargo. In 1990-2004, 42

the port’s average real value per net ton of cargo was about $42.5. Between 2005 and 2008, the 43

cargo average real value per net ton increased to $48.4. In 2009, the port’s average real value 44

per net ton of cargo dropped to $31.5, but then quickly more than doubled, peaking in 2010 at 45

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 13

$72.2 per net ton. Again, strong world demand for iron ore explains the swift recovery in the 1

average real value per ton of the port’s cargo. 2

3

4 FIGURE 4 Port of Duluth-Superior total real value of cargo and average real value per 5

net ton of cargo. 6

7

8 FIGURE 5 Port of Duluth-Superior real value index, 2005 = 100. 9

30

35

40

45

50

55

60

65

70

75

0.5

1

1.5

2

2.5

3

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

$ p

er n

et t

on

Bil

lion $

Total real value Average real value per ton

40

50

60

70

80

90

100

110

120

130

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 14

Figure 5 illustrates the real value index of the Port of Duluth-Superior. As described in 1

the methodology section, 2005 was selected as a base year. Then obtaining a port real value 2

index below the 100-percent reference line prior to 2005 is normal. In 2006, the real value index 3

of the Port of Duluth-Superior fell below the reference line, as the port transported only 87 4

percent of the benchmark (2005) total real value of cargo. Thus, in 2006 the port’s economic 5

performance was not as good as in 2005. In 2007-2008, however, the port of Duluth-Superior 6

performed better than in 2005, but then the index dropped to 44% in 2009. By 2010, the real 7

value index of the port rebounded to 129%. 8

Given the severity of the 2007-2009 recession, it is remarkable that the Port of Duluth-9

Superior’s economic performance indicators have dropped for only one year. This suggests that 10

there exists a strong demand for the commodities transported by the port and, hence, port’s 11

services. Theoretically, this relationship between the commodity markets and the market for 12

ports services has been established in the methodology section. Empirical evidence supports this 13

relationship as well, as we found a fairly strong positive correlation between the total cargo 14

tonnage and the total real value of the port’s cargo. Hence, tracking the total real value of a 15

port’s cargo can be useful not only for measuring the economic performance of a port but also to 16

help predict the future demand for port’s services, which by itself then can be used in port 17

planning and other decisions. 18

19

CONCLUSION 20

This paper proposes three innovative economic port performance measures: the total real value 21

of cargo, the average real value per ton of cargo, and the real value index of a port. The primary 22

objective of these indicators is to add new information about ports that previously has not been 23

collected on a regular, uniform basis but which can be invaluable in various port assessments, 24

including funding decisions, port economic impact studies, port development planning, pricing 25

of ports services, and so on. The methodological approach behind these indicators was drawn 26

from the field of economics and is based on the real economic value of commodities, which 27

improves on the current container ports practice of tracking the nominal value of their cargo. 28

Economists track the real value of commodities when measuring the economic performance 29

because it is adjusted for inflation. Further, the design of the first two indicators allows 30

comparing the performance of different ports to each other; whereas the real value index of a 31

port can help uncover the economic performance of a port over time, which can be particularly 32

useful in assessing the impact of funding or some policy on port’s performance. 33

Using the Port of Duluth-Superior as a case study, we calculated the three proposed 34

indicators. In the process of data collection we were limited to publicly available sources of 35

data, which presented several difficulties and most likely resulted in the underestimation of the 36

Port of Duluth-Superior economic performance. Specifically, the data source we used for our 37

cargo tonnage variable reported detailed tonnage data for only three commodities, the rest were 38

aggregated into a category of “miscellaneous” and therefore their value could not be estimated. 39

When we attempted to download more detailed cargo tonnage data from the U.S. Army Corps of 40

Engineers Navigation Data Center website, we found it very difficult to navigate and were 41

unable to compile the desired length of time-series data. The port performance evaluation 42

process could then be potentially improved if port cargo tonnage data is reported in a more user-43

accessible manner. 44

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 15

ACKNOWLEDGEMENTS 1

Authors would like to thank Amarachi Okorigbo and Sarah Nabiddo for research assistance. We 2

are also grateful to Peter Clevenstine from the Minnesota Department of Natural Resources and 3

Adolph Ojard, Executive Director of the Duluth Seaway Port Authority, for sharing their 4

expertise and data. 5

6

7

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 16

REFERENCES 1

1. U.S. Department of Transportation, Federal Highway Administration. Freight Facts and 2

Figures. Washington, DC: Office of Freight Management and Operations, 2011. 3

2. U.S. Energy Information Administration. Coal Prices, 1949-2010. 4

http://www.eia.gov/totalenergy/data/annual/index.cfm#coal (accessed May 20, 2012). 5

3. World Bank. Commodity Price Data (Pink Sheet). 6

http://econ.worldbank.org/WBSITE/EXTERNAL/EXTDEC/EXTDECPROSPECTS/0,,c7

ontentMDK:21574907~menuPK:7859231~pagePK:64165401~piPK:64165026~theSiteP8

K:476883,00.html (accessed May 27, 2012). 9

4. Brooks, M., D. Schellinck, A. Pallis. "Port Effectiveness: Users' Pesrpectives in North 10

America." Transportation Research Record: Journal of the Transportation Research 11

Board , 2011: 34-42. 12

5. Tsamboulas, D., P. Moraiti, A. Lekka. "Port Performance Evaluation for Port Community 13

System Implementation." Transportation Research Board Annual Meeting 2012. 14

Washington, DC., 2012. 15

6. UNCTAD. "Port Performance Indicators." United Nations Conference on Trade and 16

Development. New York, 1976. 17

7. Pallis, A., T. Vitsounis, P. De Langen, T. Notteboom. "Port Economics, Policy and 18

Management: Content Classification and Survey." Transport Reviews, 31(4), 2011: 445-19

471. 20

8. De, P., B. Ghosh. "Causality Between Performance and Traffic: An Investigation with 21

Indian Ports." Maritime Policy and Management, (30)1, 2003: 5-27. 22

9. Haezendock, E., C. Coeck, A. Verbeke. "The Competitive Position of Seaports: 23

Introduction of the Value Added Concept." Maritime Economics and Logistics, 2(2), 24

2000: 107-118. 25

10. Talley, W. "Port Performance: An Economics Perspective ." In Devolution, Port 26

Governance and Port Performance Research in Transportation Economics, by M. 27

Brooks and K. Cullinane, 499-516. London: Elsevier, 2007. 28

11. Brooks, M. "Issues in Measuring Port Performance Devolution Program Performance: A 29

Managerial Perspective." In Devolution, Port Governance and Performance, by M. 30

Brooks and K. Cullinane, 599-631. London: Elsevier, 2007. 31

12. De Langen, P., M. Nijdam and M. van der Horst. "New Indicators to Measure Port 32

Performance." Journal of Maritime Research, 4(1), 2007: 23-36. 33

13. Port of Los Angeles Press Release. 2007. 34

http://atwww.portoflosangeles.org/newsroom/2007_releases/news_120607econ.htm 35

(accessed May 25, 2012). 36

14. Port of Baltimore Press Release. 2012. http://mpa.maryland.gov/_media/client/News-37

Publications/2012/press/082912press.pdf (accessed August 30, 2012). 38

15. Research and Innovative Technology Administration. America’s Container Ports: 39

Linking Markets at Home and Abroad. Washington, DC: US Department of 40

Transportation, 2011. 41

16. Martin and Associates. "Economic Impact Study of the Great Lakes and St. Lawrence 42

Seaway System." Lancaster, PA, 2001. 43

17. Martin and Associates. "The Economic Impacts of the Great Lakes and St. Lawrence 44

Seaway System." Lancaster, PA, 2011. 45

TRB 2013 Annual Meeting Paper revised from original submittal.

Zamira Simkins, Richard Stewart 17

18. Coto-Millan, P., I. Mateo-Mantecon, J. Castro. “The Economic Impact of Ports: Its 1

Importance for the Region and Also the Hinterland.” In Essays on Port Economics, by P. 2

Coto-Millan, M. Pesquera and J. Castanedo, 167-200. Berlin: Springer-Verlag, 2010. 3

19. US Maritime Administration. Public Port Financing in the United States. Washington, 4

DC: US Department of Transportation, 1994. 5

20. U.S. Army Corps of Engineers . "Great Lakes Navigation System Five Year 6

Development Plan Fact Sheets." Washington, DC, 2008. 7

21. Port of Duluth-Superior. http://www.duluthport.com/port.php (accessed May 27, 2012). 8

22. World Steel Dynamics. "Iron Ore Price History and Forecast." 2011. 9

23. Bureau of Labor Statistics. Producer Price Indices . 2011. 10

http://data.bls.gov/pdq/querytool.jsp?survey=wp (accessed May 20, 2012). 11

24. U.S. Army Corps of Engineers. Duluth-Superior Harbor Statistics. 2011. 12

http://www.duluthport.com/uploads/Tonnage_Totals_History_Grand_Totals_thru_2010.p13

df (accessed May 10, 2012). 14

TRB 2013 Annual Meeting Paper revised from original submittal.