Embed Size (px)

Citation preview

The second quarter of 2017/18 (ended 30 September 2017) 1

VGi GLOBAL MEDIA PLC MANAGEMENT DISCUSSION & ANALYSIS 2Q 2017/18 30 OCT 2017

MEDIA INDUSTRY AND BUSINESS IMPACT ANALYSIS

Thailand's advertising industry remains sluggish as evident from the contraction of overall advertising expenditures by 11.4% YoY to 26,351mn in 2Q 2017/18. Advertising expenditures in the TV sector having the highest market share at 65.4% fell 12.8% YoY to THB 17,226mn and Traditional media (Newspaper, Magazines and Radio) with a 13.8% market share, declined by 22.7% YoY to THB 3,629mn. Out-of-Home media (OOH), which includes Transit, Outdoor and In-store media with a market share of 12.9%, resiliently increased by 2.6% YoY to THB 3,394mn. OOH media continues to benefit from the structural shift in the media industry, the ongoing trend of people spending more time outdoors and its strength as being a medium that reaches consumers when they are on the go to create brand awareness. For Online media, Digital Advertising Association Thailand (“DAAT”) revised up the advertising expenditures to THB 12,000mn, or an expected growth of 29% in 2017 (prior forecast: 24% growth in 2017), mainly driven by the acceleration of internet access and the ubiquity of mobile phones.

VGI once again outperformed the overall market posting significant revenue growth of 23.5% YoY to THB 978mn, driven by the healthy performance of all business units. Adjusted net profit grew by 10.3% YoY to THB 228mn. Please find more details of the Company performance in performance analysis 2Q 2017/18.

During Royal Cremation Ceremonies for the late King in October 2017, VGI, as an OOH media operator, has cooperated with advertising guidelines released by Media Agency Association Thailand (MAAT) and DAAT by adjusting all digital screens to display in grayscale for one month. The Company expects that there will be minimal impact of around 1-2% to the full-year performance. This impact has already been factored into our full-year forecast.

Having already seen signs of improvement in overall advertising sentiment in the remaining months of our fiscal year, we reiterate our target of THB 4,000mn in revenue in 2017/18.

IMPORTANT EVENTS IN 2Q 2017/18

Transit in Thailand

Launched 3 station sponsorship campaigns on BTS Skytrain network with AEON at Asok station, COMICO at Victory Monument station and Aquarius at Chong Nonsi station.

AEON – Asok station

COMICO – Victory Monument station

Aquarius – Chong Nonsi station

The second quarter of 2017/18 (ended 30 September 2017) 2

VGi GLOBAL MEDIA PLC MANAGEMENT DISCUSSION & ANALYSIS 2Q 2017/18 30 OCT 2017

Transit in Malaysia

Currently, Titanium Compass Sdn Bhd (“TCSB”) managed advertising on 2 stations and 15 trains, while the SBK Line recorded ridership of more than 200,000 trips, having fully operated since July 2017.

TCSB – on station advertising

Office

During the 6 months of 2017, the Company added 8 new contracts into its office building portfolio, in line with our target of 10 additional office contracts by year end 2017. With a total of 170 buildings under management (1,309 digital screens), VGI is currently the largest office building media provider in Thailand capturing most of the market share in Grade A & B office buildings.

Digital Services

As of 30 September 2017, under VGI’s offline payment channel, over 8.1mn Rabbit cards were issued with more than 133 brand partners and over 4,400 retail points of acceptance. Under VGI’s online payment channel, Rabbit LinePay has over 2.4mn users with more than 425 brand partners.

The second quarter of 2017/18 (ended 30 September 2017) 3

VGi GLOBAL MEDIA PLC MANAGEMENT DISCUSSION & ANALYSIS 2Q 2017/18 30 OCT 2017

2Q 2017/18 SNAPSHOT & ANALYSIS

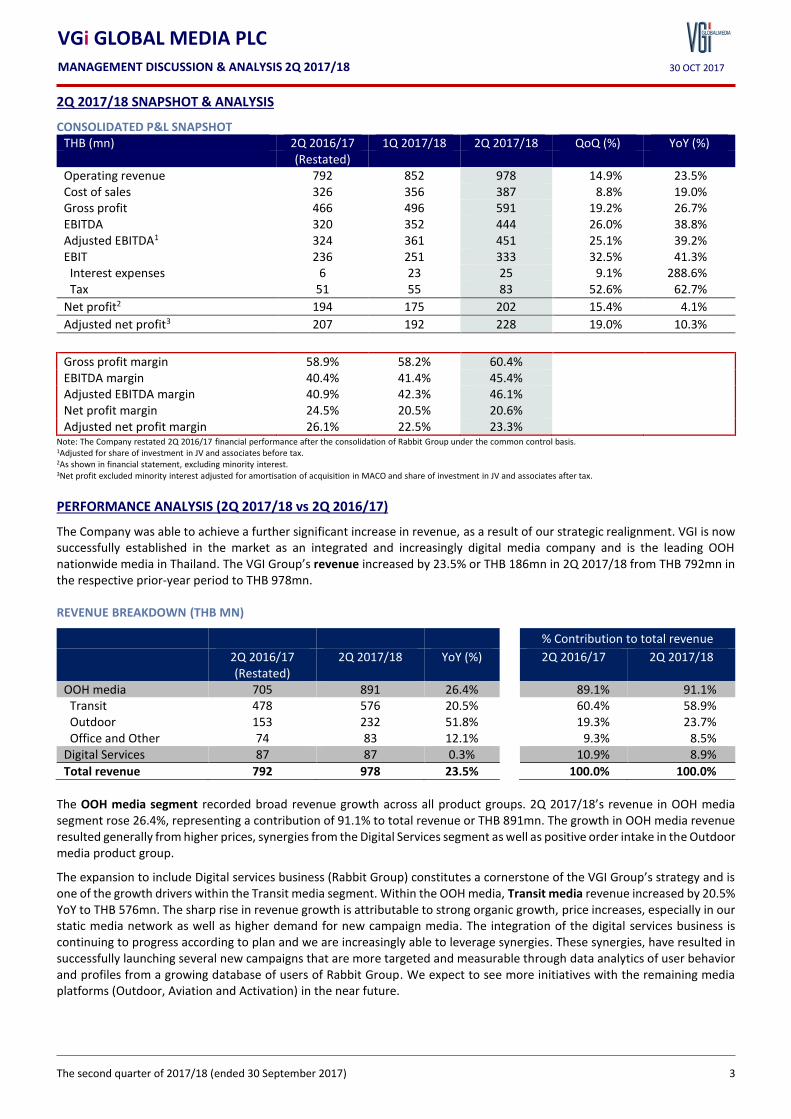

CONSOLIDATED P&L SNAPSHOT THB (mn) 2Q 2016/17 1Q 2017/18 2Q 2017/18 QoQ (%) YoY (%) (Restated) Operating revenue 792 852 978 14.9% 23.5% Cost of sales 326 356 387 8.8% 19.0% Gross profit 466 496 591 19.2% 26.7% EBITDA 320 352 444 26.0% 38.8% Adjusted EBITDA1 324 361 451 25.1% 39.2% EBIT 236 251 333 32.5% 41.3% Interest expenses 6 23 25 9.1% 288.6% Tax 51 55 83 52.6% 62.7%

Net profit2 194 175 202 15.4% 4.1%

Adjusted net profit3 207 192 228 19.0% 10.3%

Gross profit margin 58.9% 58.2% 60.4%

EBITDA margin 40.4% 41.4% 45.4%

Adjusted EBITDA margin 40.9% 42.3% 46.1%

Net profit margin 24.5% 20.5% 20.6%

Adjusted net profit margin 26.1% 22.5% 23.3% Note: The Company restated 2Q 2016/17 financial performance after the consolidation of Rabbit Group under the common control basis. 1Adjusted for share of investment in JV and associates before tax. 2As shown in financial statement, excluding minority interest. 3Net profit excluded minority interest adjusted for amortisation of acquisition in MACO and share of investment in JV and associates after tax.

PERFORMANCE ANALYSIS (2Q 2017/18 vs 2Q 2016/17)

The Company was able to achieve a further significant increase in revenue, as a result of our strategic realignment. VGI is now successfully established in the market as an integrated and increasingly digital media company and is the leading OOH nationwide media in Thailand. The VGI Group’s revenue increased by 23.5% or THB 186mn in 2Q 2017/18 from THB 792mn in the respective prior-year period to THB 978mn.

REVENUE BREAKDOWN (THB MN)

% Contribution to total revenue

2Q 2016/17 (Restated)

2Q 2017/18 YoY (%) 2Q 2016/17 2Q 2017/18

OOH media 705 891 26.4% 89.1% 91.1% Transit 478 576 20.5% 60.4% 58.9% Outdoor 153 232 51.8% 19.3% 23.7% Office and Other 74 83 12.1% 9.3% 8.5% Digital Services 87 87 0.3% 10.9% 8.9%

Total revenue 792 978 23.5% 100.0% 100.0%

The OOH media segment recorded broad revenue growth across all product groups. 2Q 2017/18’s revenue in OOH media segment rose 26.4%, representing a contribution of 91.1% to total revenue or THB 891mn. The growth in OOH media revenue resulted generally from higher prices, synergies from the Digital Services segment as well as positive order intake in the Outdoor media product group.

The expansion to include Digital services business (Rabbit Group) constitutes a cornerstone of the VGI Group’s strategy and is one of the growth drivers within the Transit media segment. Within the OOH media, Transit media revenue increased by 20.5% YoY to THB 576mn. The sharp rise in revenue growth is attributable to strong organic growth, price increases, especially in our static media network as well as higher demand for new campaign media. The integration of the digital services business is continuing to progress according to plan and we are increasingly able to leverage synergies. These synergies, have resulted in successfully launching several new campaigns that are more targeted and measurable through data analytics of user behavior and profiles from a growing database of users of Rabbit Group. We expect to see more initiatives with the remaining media platforms (Outdoor, Aviation and Activation) in the near future.

The second quarter of 2017/18 (ended 30 September 2017) 4

VGi GLOBAL MEDIA PLC MANAGEMENT DISCUSSION & ANALYSIS 2Q 2017/18 30 OCT 2017

Meanwhile, our Office Building and Other media segment revenue recorded a solid performance, increasing by 12.1% to THB 83mn. Revenue growth in 2Q 2017/18 was mainly driven by the expansion of the office building media network and price increase. During the first half of 2017/18, we successfully added 8 new contracts to the office building portfolio. The performance of this business is expected to improve in the remaining quarters in line with the continuous increase in the number of office buildings.

The Group also benefited from the ongoing momentum in Outdoor media segment, which saw growth of 51.8%, or THB 79mn reaching THB 232mn in 2Q 2017/18. The increase was mainly due to the rolling out of new digital media, which consists of 21 LED billboards across 19 provinces. In the same period, this business segment also benefitted from the consolidation of Multi Sign Co. Ltd., (“Multi Sign”) and COMASS Co. Ltd., (“COMASS”) which was acquired in October 2016 and July 2017, respectively. The consolidation has expanded MACO’s nationwide footprints and increased MACO revenue capacity to THB 1,400mn. (Please find more details of Outdoor media segment in 3Q 2017 MACO’s management discussion and analysis http://maco.listedcompany.com/misc/mdna/20171020-maco-mdna-3q2017-en.pdf)

Digital Services business contributed 8.9% of total revenue or THB 87mn, slightly increased by 0.3% to THB 87mn mainly due to higher revenue from Bangkok Smartcard System Co., Ltd.’s project management fee.

The growth in the operating business is also reflected in cost of sales which came to THB 387mn, an increase of THB 62mn or 19.0% YoY, primarily from higher sales, an increase of Transit media concession fee from 5% to 10% (revenue sharing scheme which increases by 5% every 5 years since May 2015), full quarter consolidation of newly acquired companies Multi Sign and COMASS by MACO. Cost-to-sales ratio, however, decreased from 41.1% to 39.6% primarily as a result of improved operational efficiency and cost management especially in Outdoor media business. Consequently, the gross profit was up 26.7% from THB 466mn to THB 591mn.

Selling, General and Administrative expenses (“SG&A”) increased slightly by 9.2% from THB 245mn to THB 267mn, mainly due to the newly acquired businesses (Outdoor and Digital Services). The increase in SG&A from the Outdoor segment was mainly due to the full quarter consolidation of Muti Sign as well as the consolidation of COMASS. The increase in SG&A from Digital Services is mainly due to Rabbit Group’s expanded headcount, which is rapidly developing and investing in its burgeoning data acquisition and analytics capabilities to uncover opportunities to enhance customers and shareholder return. Nevertheless, the ratio of SG&A to revenue decreased to 27.3% (prior year: 30.9%), from higher revenue growth. The Company expects that the ratio should be maintained at no more than 30% going forward and the ratio should gradually decline as a result of cost synergies in through restructuring, in particular in digital operations.

In light of tangible improvement in gross profit, VGI Group’s positive momentum is also reflected in its EBIT of THB 333mn (prior year: THB 236mn) and EBITDA increased by 38.8% from THB 320mn to THB 444mn.

Interest expenses increased by THB 19mn from THB 6mn to THB 25mn in this quarter. The increase was as a result of an increase of loan for financing the Rabbit Group acquisition in March 2017.

Given this further improvement in operating activities, the Group’s tax base also increased. The Company also recorded a higher tax expense in the separate financial statements this quarter from capital gains from the sale of MACO’s shares, which rose substantially year on year to THB 83mn (THB 51mn in the previous year). Hence, our effective tax rate at consolidated level this quarter stood at 27% - higher than usual corporate tax rate of 20%.

Bolstered by the improved operating performance, VGI Group generated total net profit of THB 202mn (prior year: THB 194mn), an increase by 4.1% YoY. At the same time, adjusted net profit climbed 10.3% from THB 207mn to THB 228mn.

The second quarter of 2017/18 (ended 30 September 2017) 5

VGi GLOBAL MEDIA PLC MANAGEMENT DISCUSSION & ANALYSIS 2Q 2017/18 30 OCT 2017

FINANCIAL POSITION

ASSETS

ASSETS BREAKDOWN 31 MARCH 2017 30 SEPTEMBER 2017 (Restated)

(THB mn) % out of total (THB mn) % out of total

Cash & cash equivalents and short-term investments 1,210 15.2% 624 7.8% Trade & other receivables 763 9.6% 851 10.6% Equipment – net 1,503 18.8% 1,620 20.2% Investment in JVs, associates and other long-term investments 1,373 17.2% 1,349 16.8% Goodwill and excess of acquisition costs and net assets 1,487 18.6% 1,768 22.0%

Other assets 1,649 20.6% 1,810 22.6%

Total assets 7,985 100.0% 8,023 100.0%

Total assets as of 30 September 2017 stood at THB 8,023mn, an increase of THB 38mn or 0.5% from THB 7,985mn as of 31 March 2017. Total current assets were THB 2,171mn, decreasing by 16.9% or THB 441mn, primarily due to 1) a decrease in cash & cash equivalents and short-term investments of THB 587mn mainly from cash used for MACO’s investment in COMASS and BSSH’s loan to Rabbit Internet. However, the decrease was partially offset by 2) an increase in trade and other receivables of THB 88mn (see further details in trade and other receivable section) and 3) an increase bank account for advance received from Rabbit cardholders of THB 22mn.

Total non-current assets stood at THB 5,851mn, an increase of 8.9% or THB 479mn due to an increase of 1) an estimated amount by which costs of the acquisition of investment in subsidiary exceed identifiable net assets of the acquiree of THB 282mn from acquisition in COMASS by MACO, 2) equipment –net of THB 118mn and 3) advance payments for purchase of assets of THB 85mn.

Trade and other receivables were THB 851mn, an increase of THB 88mn. The increase was in-line with higher sales in 2Q 2017/18. The Company gives 60 – 90 days credit terms to customers. For accounts receivables of more than 120 days, the Company has a policy for allowance for doubtful accounts, which also considers the customers’ payment history and credit-worthiness. As of 30 September 2017, the allowance for doubtful accounts was THB 33mn.

AGEING OF TRADE RECEIVABLES (THB mn) 31 MARCH 2017 (Restated)

30 SEPTEMBER 2017

Not yet due 577 585 Up to 6 months 93 99 Over 6 months 39 47

Total 709 731 % of total receivables 93.0% 85.9%

Allowance for doubtful debt 34 33 % of total receivables 4.5% 3.9%

LIABILITIES AND SHAREHOLDERS’ EQUITY

LIABILITIES AND EQUITY BREAKDOWN 31 MARCH 2017 30 SEPTEMBER 2017 (Restated)

(THB mn) % out of total (THB mn) % out of total

Short term loans 778 9.7% 655 8.2% Trade & other payables 536 6.7% 242 3.0% Accrued expenses 400 5.0% 513 6.4% Current portion of long-term loans from financial institutions 246 3.1% 242 3.0% Other current liabilities 848 10.6% 874 10.9% Long term loan 1,933 24.2% 1,912 23.8% Other non-current liabilities 139 1.7% 145 1.8%

Total liabilities 4,880 61.1% 4,584 57.1%

Shareholders’ equity 3,105 38.9% 3,438 42.9%

Total liabilities and equity 7,985 100.0% 8,023 100.0%

Total liabilities were THB 4,584mn, a decrease of THB 295mn or 6.1% from THB 4,880mn as of 31 March 2017 mainly from decrease in 1) trade and other payables of THB 294mn mainly from other payables for purchases of investment in Multi Sign by Green Ad Co., Ltd., a subsidiary of MACO, of THB 175mn, dividend payable to Multi Sign’s shareholders of THB 21mn as well as trade payables of THB 98mn and 2) short term loans of THB 123mn. The decrease was partially offset by an increase in 3) accrued expenses of THB 114mn.

The second quarter of 2017/18 (ended 30 September 2017) 6

VGi GLOBAL MEDIA PLC MANAGEMENT DISCUSSION & ANALYSIS 2Q 2017/18 30 OCT 2017

Total equity was THB 3,438mn increasing by THB 333mn or 10.7%, which was attributed to an increase in retained earnings from the 3-month operating performance. Return on equity for 2Q 2017/18 was 34.7%.

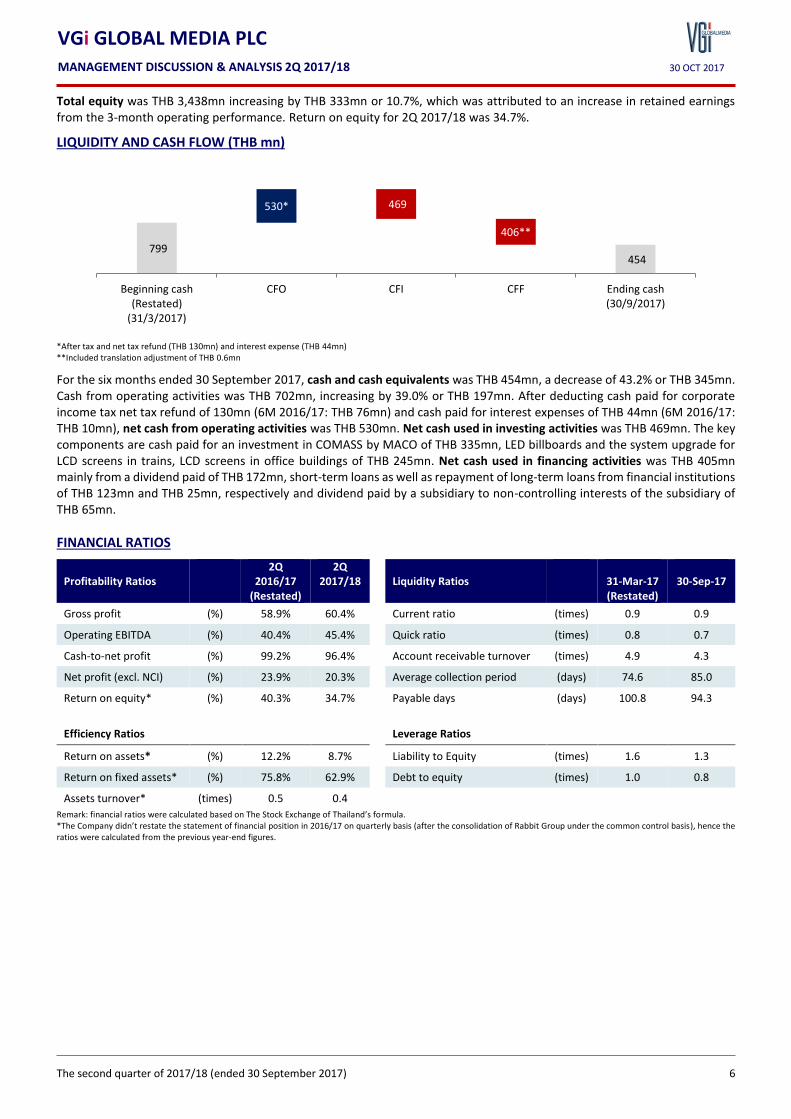

LIQUIDITY AND CASH FLOW (THB mn)

*After tax and net tax refund (THB 130mn) and interest expense (THB 44mn) **Included translation adjustment of THB 0.6mn

For the six months ended 30 September 2017, cash and cash equivalents was THB 454mn, a decrease of 43.2% or THB 345mn. Cash from operating activities was THB 702mn, increasing by 39.0% or THB 197mn. After deducting cash paid for corporate income tax net tax refund of 130mn (6M 2016/17: THB 76mn) and cash paid for interest expenses of THB 44mn (6M 2016/17: THB 10mn), net cash from operating activities was THB 530mn. Net cash used in investing activities was THB 469mn. The key components are cash paid for an investment in COMASS by MACO of THB 335mn, LED billboards and the system upgrade for LCD screens in trains, LCD screens in office buildings of THB 245mn. Net cash used in financing activities was THB 405mn mainly from a dividend paid of THB 172mn, short-term loans as well as repayment of long-term loans from financial institutions of THB 123mn and THB 25mn, respectively and dividend paid by a subsidiary to non-controlling interests of the subsidiary of THB 65mn.

FINANCIAL RATIOS

Profitability Ratios 2Q

2016/17 (Restated)

2Q 2017/18

Liquidity Ratios

31-Mar-17 (Restated)

30-Sep-17

Gross profit (%) 58.9% 60.4% Current ratio (times) 0.9 0.9

Operating EBITDA (%) 40.4% 45.4% Quick ratio (times) 0.8 0.7

Cash-to-net profit (%) 99.2% 96.4% Account receivable turnover (times) 4.9 4.3

Net profit (excl. NCI) (%) 23.9% 20.3% Average collection period (days) 74.6 85.0

Return on equity* (%) 40.3% 34.7% Payable days (days) 100.8 94.3

Efficiency Ratios Leverage Ratios

Return on assets* (%) 12.2% 8.7% Liability to Equity (times) 1.6 1.3

Return on fixed assets* (%) 75.8% 62.9% Debt to equity (times) 1.0 0.8

Assets turnover* (times) 0.5 0.4

Remark: financial ratios were calculated based on The Stock Exchange of Thailand’s formula. *The Company didn’t restate the statement of financial position in 2016/17 on quarterly basis (after the consolidation of Rabbit Group under the common control basis), hence the ratios were calculated from the previous year-end figures.

799 454

530* 469

406**

Beginning cash(Restated)

(31/3/2017)

CFO CFI CFF Ending cash(30/9/2017)

The second quarter of 2017/18 (ended 30 September 2017) 7

VGi GLOBAL MEDIA PLC MANAGEMENT DISCUSSION & ANALYSIS 2Q 2017/18 30 OCT 2017

MANAGEMENT OUTLOOK

Revenue growth in OOH advertising is subject to generally similar seasonal fluctuations as the rest of the media industry. While

the fourth quarter (October – December) historically generates higher revenue and earnings contribution to VGI Group, the

mourning period is expected to impact the digital media segment by approximately 1 month in 3Q 2017/18. This impact is

expected to be around 1-2% to the full-year performance, which has already been factored into our full-year forecast. We

expect that the advertising segment will rebound after the mourning period as well as the expected boost from spending

leading up to the elections slated in 2018. For 2017/18 as a whole, we reiterate our revenue forecast for the VGI Group at THB

4,000mn.

…………………………………..

Chitkasem Moo-Ming

(Chief Financial Officer)