Embed Size (px)

Citation preview

Chapter 224: Payment Reform What it means going forward?

Since Passing Health Care Reform in 2006

• Good news is that in over 6 years, 98% of residents now have coverage.

• Bad news is that employers and consumers find health care coverage too expensive – Despite slowing somewhat in more recent years,

mostly due to decreases in utilization, MA premiums grew 18-19% (between 2006-2010);

– Per capita health spending is 15% higher than the national average;

– Massachusetts has the highest individual market premiums in the country.

Key Elements • Benchmarks health care cost growth against the state’s overall

economic growth – a system-wide measure – For years 2013 – 2017: PGSP

– For years 2018-2022 - PGSP -.5%

– For years 2023 and beyond – the PGSP

• Builds off current effort to transition away from FFS to alternative payment methods (APM); doesn’t mandate a specific way to pay

• Estimated to save $200BB in health care expenses over the next 15 years

• On or before 7/1/14, requires GIC, MassHealth and any other state funded insurance program to the maximum extent feasible implement APM

Chapter 224

Medicaid • Required to transition payment for health care services using ACOs or

patient-centered medical home models as follows:

– By July 1, 2013: at least 25% of its enrollees,

– By July 1, 2014: at least 50% of its enrollees,

– By July 1, 2015: at least 80% of its enrollees, or the maximum percentage feasible.

• To achieve these benchmarks, MassHealth is working on a proposal to transition its PCC plan and the MCO program into alternative payments beginning July 1, 2013.

GIC • Increase the number of GIC employees in Integrated Risk-Bearing

Organizations (IRBO): 15% by 1/31/14 to 75% by 3/31/16 • Costs to rise slightly, flatten and then decrease • Target PMPY

Chapter 224 – State Activities

FY14 FY15 FY16 FY17 FY18

2% 2% 0% –2% –2%

Other Key Elements • 266 new appointees & 25 new boards, task forces, and

commissions including the Health Policy Commission to monitor and enforce spending caps, oversee provider performance, certify ACOs and delivery system changes

• Oversight by DOI of providers taking risk • MLR standards of 90% in 2013, 89% in 2014 and 88% thereafter;

ACA MLR standards: 85% large employers, 80% individual/small group

• Assessment on health plans to fund HIT, Wellness of $160MM • Establishes a Health Planning Council that is charged with

identifying the Commonwealth’s health care service needs, providers, programs and facilities, the resources available to meet those needs, and the priorities for addressing those needs.

Chapter 224

Nationally • Massachusetts viewed as the “de-facto” national leader on

health care access and may now be the leader on “how to bend the health care cost curve”

• If the ACA remains in effect, affordability will be a major conversation in the coming years

• Key elements of Chapter 224 were developed with national policy experts involved in the development of the ACA

• Potential for GSP to emigrate to other states

Implications of Chapter 224

Implications for the Health Care Sector?

Health Plans • How will we be held accountable for GSP?

• Is it safe to assume that provider contracts will not go up by no more than the PGSP target? How will this deal with provider price disparities?

• Will health plans use Chapter 224 to move to new payment methods like global payments, will FFS remain?

• Will we see greater provider integration – will it lead to higher or lower prices? Better quality?

• Will providers look to become insurers without all the regulatory hurdles?

• How will plans change product design?

– Limited/Tiered Network plans at a 14% discount

– Increased disclosure of consumer costs

• Will health plans look to implement APMs given current market realities?

– ½ Massachusetts market is self insured; What do those employers want?

– For fully insured: HMO- 50%; PPO-50%

Implications for the Health Care Sector?

Hospitals & Physicians • Will we see a massive move to integration of providers/ACOs?

• Will such integration lead to higher or lower provider prices?

• How can sole practitioners survive in a world of integration?

• Can providers, large and small, live with new spending targets?

• How can lower paid hospitals survive if everyone is paid about the same?

• Can larger organizations squeeze out waste and inefficiencies?

• How will PGSP target impact purchasing decisions within the organization?

• Will PGSP targets lead to more medical management within a system?

• Will hospitals and physicians want to take on insurance risk?

Implications for the Health Care Sector?

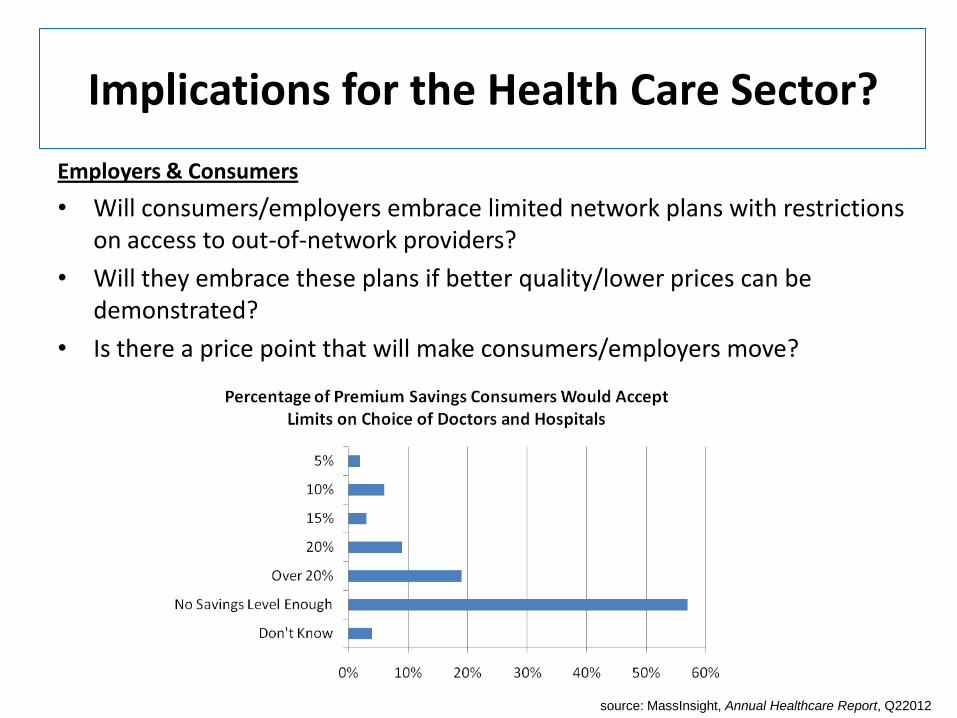

Employers & Consumers

• Will consumers/employers embrace limited network plans with restrictions on access to out-of-network providers?

• Will they embrace these plans if better quality/lower prices can be demonstrated?

• Is there a price point that will make consumers/employers move?

source: MassInsight, Annual Healthcare Report, Q22012

Implications for the Health Care Sector?

Employers & Consumers • What will make employers and self insured employers move from PPOs to

closed network plans?

• What is the future of product design? Tiered, select/limited network products (ACO), HDHPs

• Can we move populations and make them participate in wellness programs?

• Will state Exchanges take off and supplant the carrier/broker relationship with the consumer/employer?

Implications for the Health Care Sector?

Medical Device & Pharmaceutical Companies

• How will spending targets influence provider purchasing practices? Will state cost targets having a “chilling effect” on spending on the latest new thing?

• As providers consolidate, will each individual practices have a need for a technology or diagnostic device, or is it enough to have it somewhere in the system?

• Will brand reputation be enough to succeed or will you need to now solely focus on price/quality distinctions?

Implications for the Health Care Sector?

Medical Device & Pharmaceutical Companies

How will new state planning & transparency impact new technologies and devices?

“…Dichter, a 59-year-old local consultant who started asking questions after his insurance company was charged

$83 for a sling. Dichter’s co-pay was only $25, but he still thought the price seemed stiff — especially when he learned that a comparable sling cost a mere $7 online.…he launched a barrage of complaints from government agencies down to his health insurance company and the Waltham medical equipment supplier that provided this $83 sling. Dichter got his charge forgiven, but, more important, he brought new scrutiny to the way in which unjustifiable costs are simply passed along

$83 sling shows power of consumer scrutiny

Editorial – September 3, 2012

Lessons Learned

• If you do universal access, cost containment is likely to follow…if individuals will be required to have insurance, they need to be able to afford it.

• Greater scrutiny of health plans to drive down costs in provider contracting, which will drive down their purchasing ability.

• For health plans, what regulatory requirements should be in place for ACOs to protect consumers and ensure a level playing field? Oppose broad waivers to Stark!

• If Massachusetts is the incubator for reform, GSP targets will be exported.