Embed Size (px)

Citation preview

Medicare Financial Management Manual Chapter 7 - Internal Control Requirements

Table of Contents

(Rev. 10614, 03-23-21)

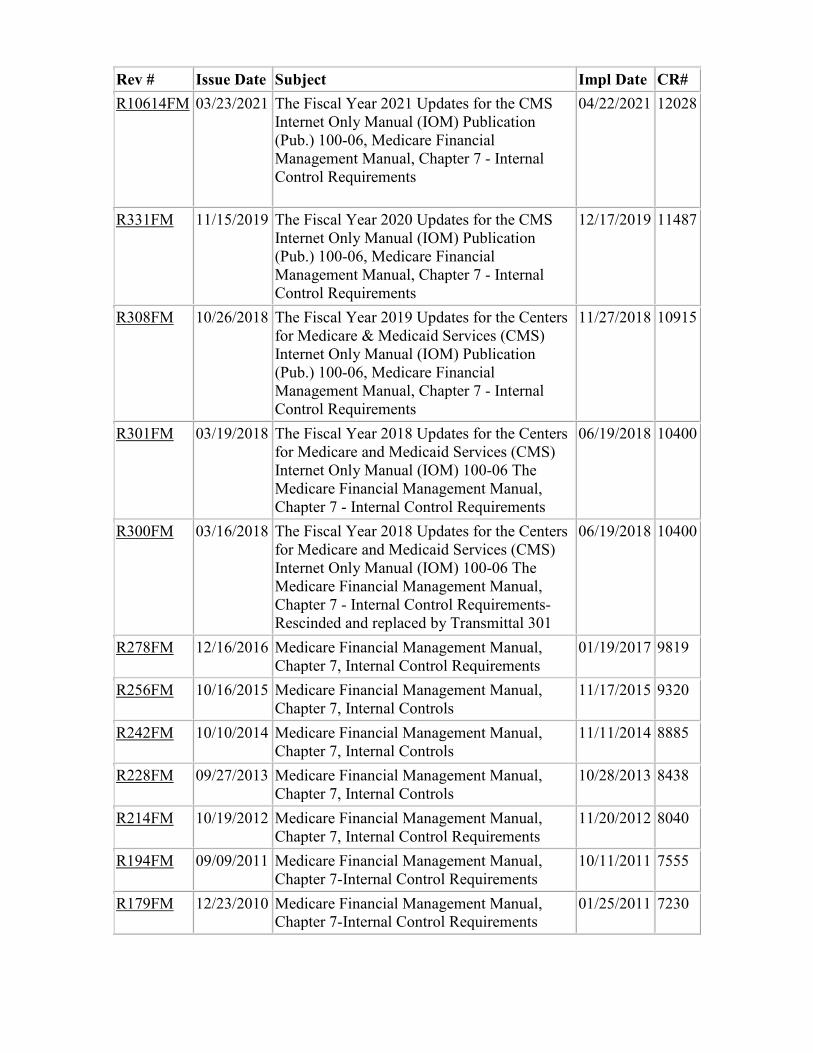

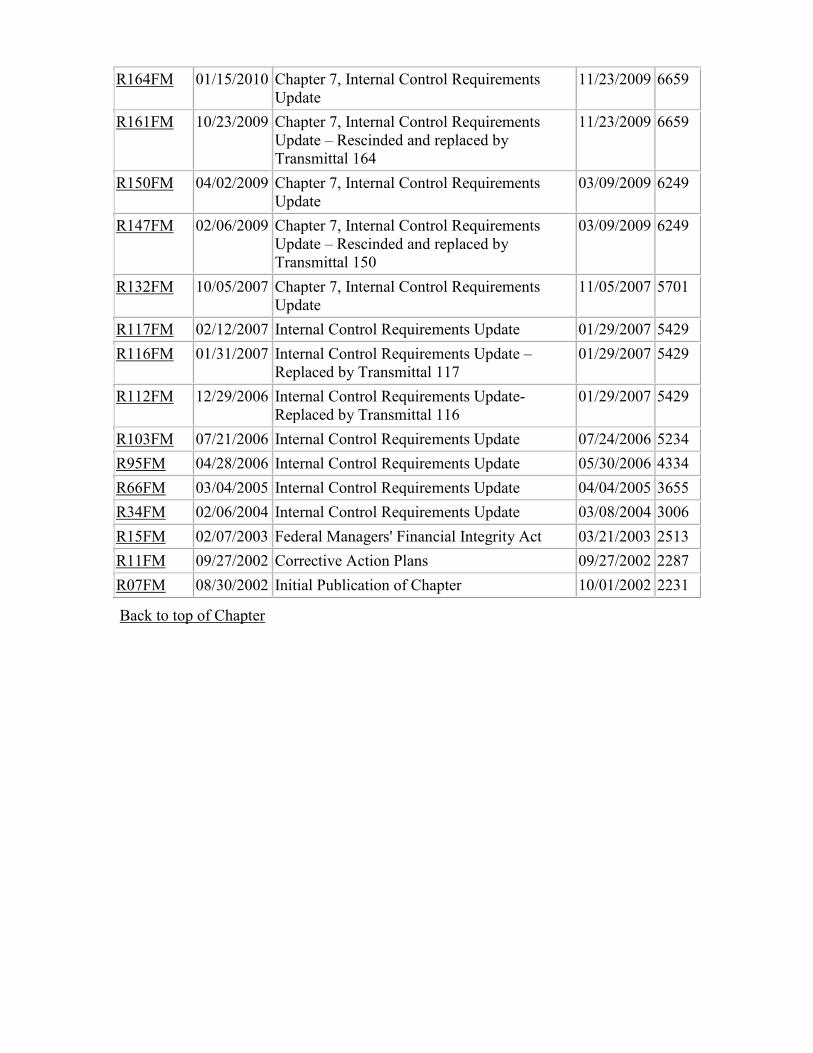

Transmittals for Chapter 7 10 – Introduction

10.1 – Authority 10.1.1– Federal Managers' Financial Integrity Act of 1982 (FMFIA) 10.1.2 – FMFIA and the CMS Medicare Contractor Contract 10.1.3 – Chief Financial Officers Act of 1990 (CFO) 10.1.4 – OMB Circular A-123 10.1.5 – GAO Standards for Internal Controls in the Federal Government

10.2 – GAO Standards in the Federal Government 10.2.1 – Definition and Objectives 10.2.2 – Fundamental Concepts 10.2.3 – Standards for Internal Control

10.2.3.1 – Control Environment 10.2.3.2 – Risk Assessment 10.2.3.3 – Control Activities 10.2.3.4 – Information and Communication 10.2.3.5 – Monitoring

20 – CMS Contractor Internal Control Review Process and Timeline 20.1 – Risk Assessment

20.1.1 – Risk Analysis Chart 20.2 – Internal Control Objectives

20.2.1 – CMS Contractor Control Objectives 20.3 – Policies and Procedures 20.4 – Testing Methods 20.5 – Documentation and Working Papers

30 - Internal Control Reporting Requirements 30.1 – Certification Package for Internal Controls (CPIC) Requirements

30.1.1 – OMB Circular A-123 Appendix A: Internal Control Over Financial Reporting (ICOFR)

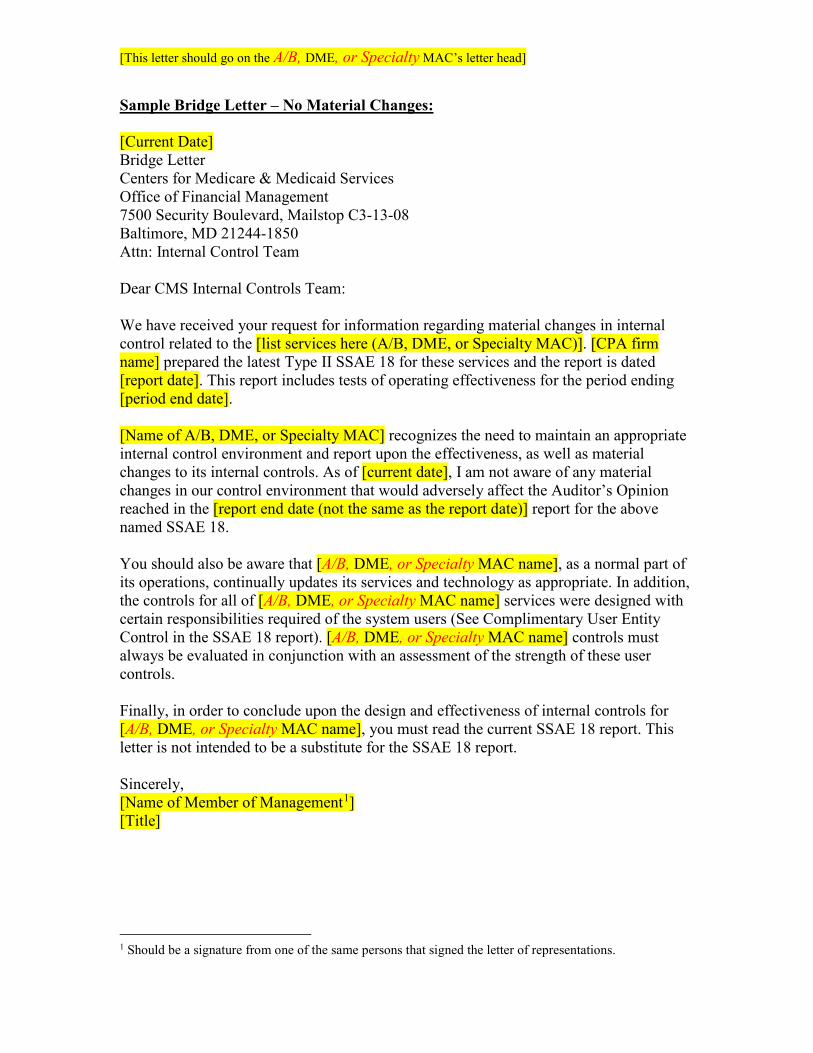

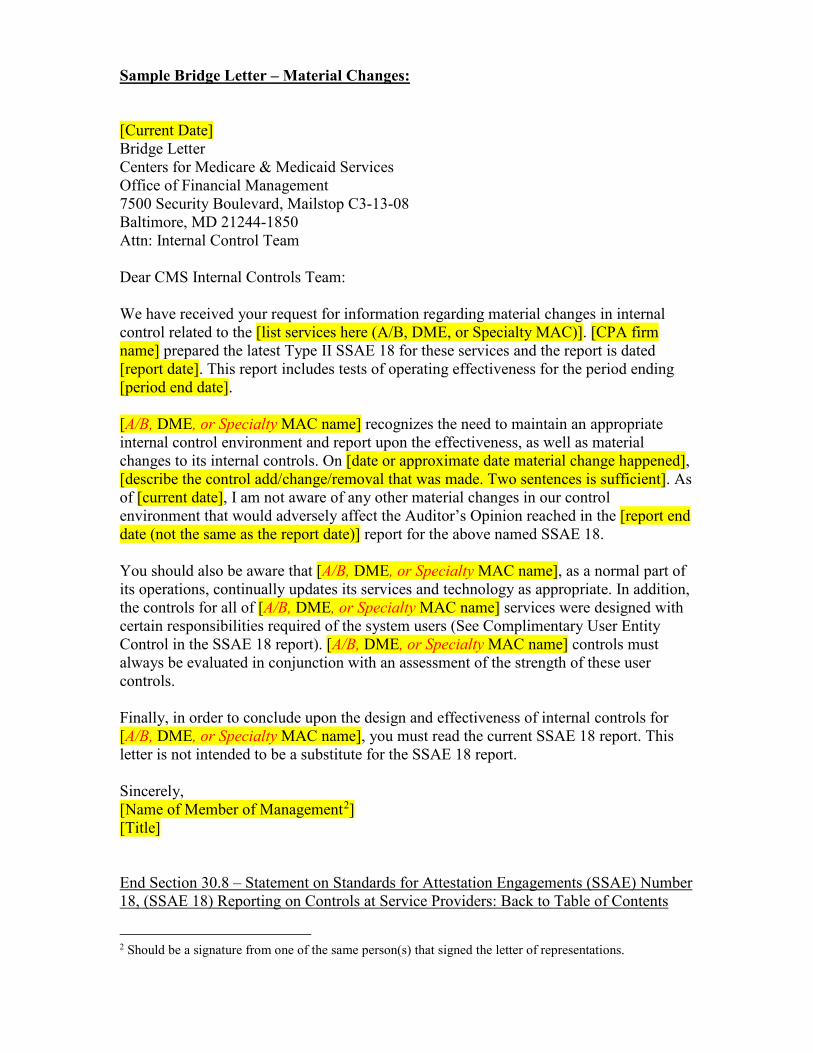

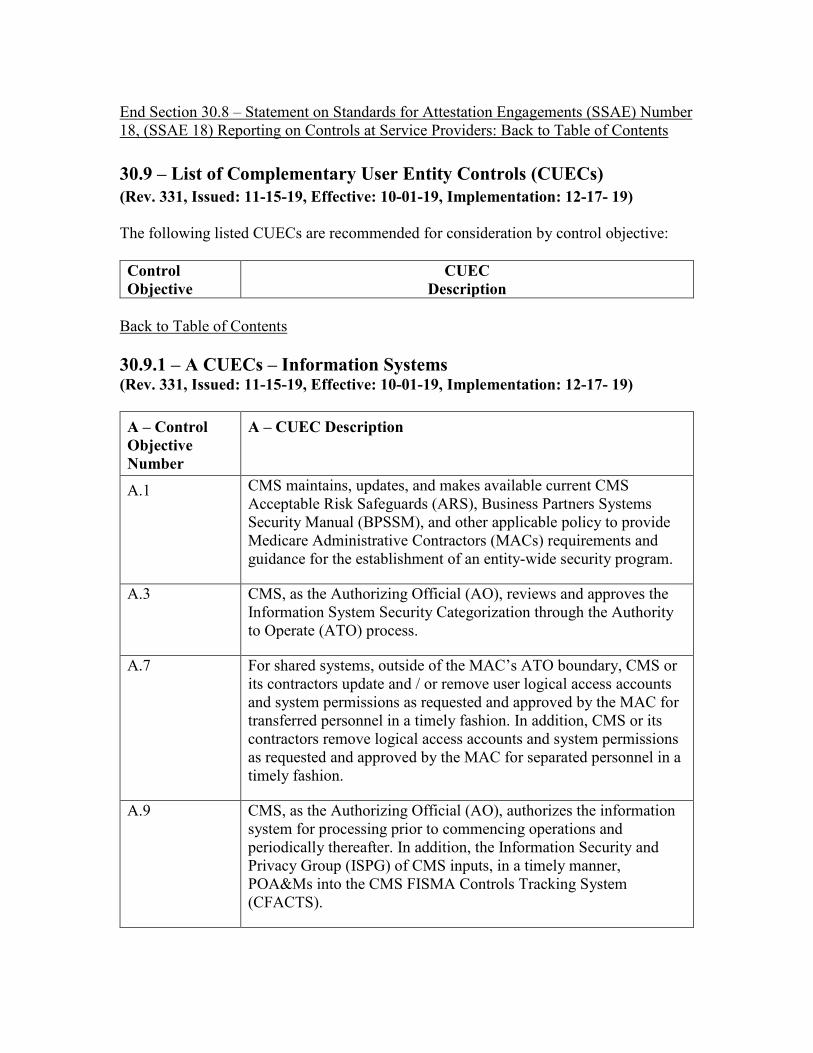

30.2 – Certification Statement 30.3 – Executive Summary 30.4 – CPIC - Report of Material Weaknesses 30.5 – CPIC- Report of Internal Control Deficiencies 30.6 – Definitions of Control Deficiency, Significant Deficiency, and Material Weaknesses 30.7 – Material Weaknesses Identified During the Reporting Period 30.8 – Statement on Standards for Attestation Engagements (SSAE) Number 18 (SSAE 18), Reporting on Controls at Service Providers 30.9 – List of Complementary User Entity Controls (CUECs)

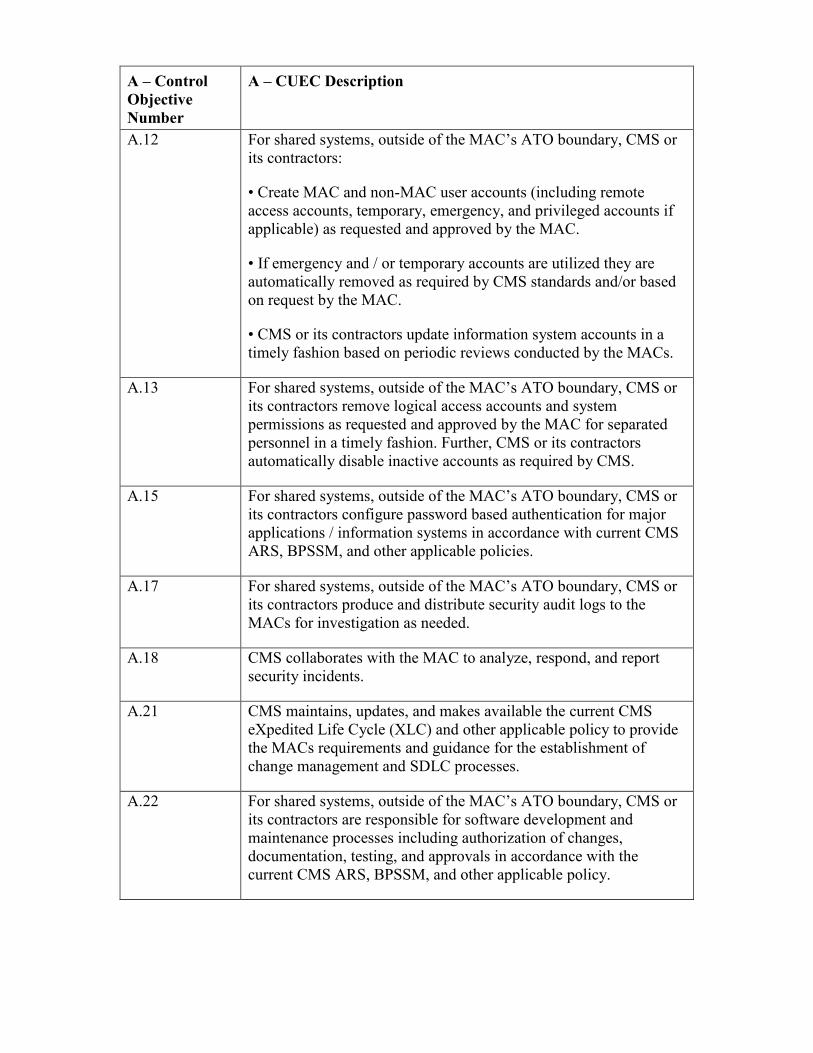

30.9.1 – A CUECs – Information Systems 30.9.2 – B CUECs – Claims Processing 30.9.3 – F CUECs – Medical Review (MR) 30.9.4 – G CUECs – Medicare Secondary Payer (MSP) 30.9.5 – I – CUECs Provider Audit 30.9.6 – J CUECs – Financial

30.9.6.1 – J CUECs – Financial (Non-HIGLAS) 30.9.6.2 – J CUECs – Financial (HIGLAS)

30.9.7 – K CUECs – Debt Referral (MSP and Non-MSP) 30.9.7.1 – K CUECs – Debt Referral (MSP and Non-MSP) (Non-HIGLAS) 30.9.7.2 – K CUECs – Debt Referral (MSP and Non-MSP) (HIGLAS)

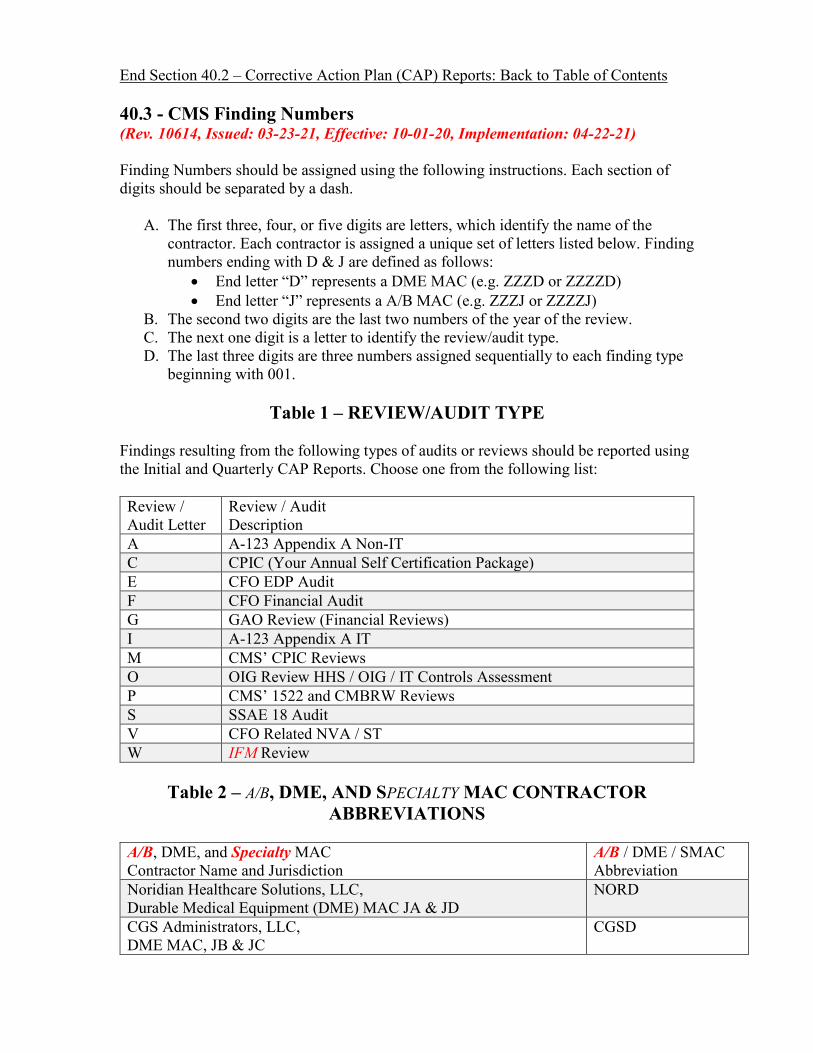

30.9.8 – L CUECs – Non-MSP Debt Collection 40 – Corrective Action Plans 40.1 – Submission, Review, and Approval of Corrective Action Plans 40.2 – Corrective Action Plan (CAP) Reports 40.3 – CMS Finding Numbers 40.4 – Initial CAP Report 40.5 – Quarterly CAP Report 40.6 – CMS CAP Report Template

50 – List of CMS Contractor Control Objectives 50.1 – A Controls – Information Systems 50.2 – B Controls – Claims Processing 50.3 – C Controls – Appeals 50.4 – D Controls – Beneficiary / Provider Services 50.5 – E Controls – Complementary Credits 50.6 – F Controls – Medical Review (MR) 50.7 – G Controls – Medicare Secondary Payer (MSP) 50.8 – H Controls – Administrative 50.9 – I Controls – Provider Audit 50.10 – J Controls – Financial Reporting Review Requirements 50.11 – K Controls – Debt Referral (MSP and Non-MSP) 50.12 – L Controls – Non-MSP Debt Collection 50.13 – M Controls – Provider Enrollment

60 – CMS Contractor Cycle Memo 60.1 – CMS Contractor Cycle Memo Outline

70 – List of Commonly Used Acronyms

10 - Introduction (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Chapter 7: Internal Control Requirements provides guidelines and policies to the CMS contractors in enabling them to strengthen their internal controls procedures. The CMS contracts with companies to administer the Medicare program under the Social Security Act and the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 (MMA). The contractors shall administer the Medicare program efficiently and economically in order to achieve the program objectives. Internal controls are an essential part of managing an organization. Additionally, internal controls also serves as the first line of defense in safeguarding assets and preventing and detecting errors and or fraud. In summary, internal controls assists government program managers in achieving desired results through effective stewardship of public resources. End Section 10 – Introduction: Back to Table of Contents 10.1 - Authority (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) The Federal Managers' Financial Integrity Act of 1982 (FMFIA) establishes internal control requirements that shall be met by CMS. For CMS to meet the requirements of FMFIA, CMS contractors shall demonstrate that they are in compliance with the FMFIA guidelines. End Section 10.1 – Authority: Back to Table of Contents 10.1.1 - Federal Managers' Financial Integrity Act of 1982 (FMFIA) (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) The FMFIA requires that internal accounting and administrative controls of each executive agency be established in accordance with the standards prescribed by the Comptroller General. Under FMFIA, the Office of Management and Budget (OMB) establishes guidelines for agencies to evaluate their systems of internal accounting and administrative control to determine such systems' compliance with the standards established by the Comptroller General. Under the prescribed standards of the FMFIA, agencies must provide reasonable assurance to the President and Congress on an annual basis that:

1. Obligations and costs are in compliance with applicable law; 2. Funds, property, and other assets are safeguarded against waste, loss, unauthorized use, or

misappropriation; and 3. Revenues and expenditures applicable to agency operations are properly recorded and accounted for

to permit the preparation of accounts, reliable financial and statistical reports, and to maintain accountability over the assets.

End Section 10.1.1 – Federal Managers' Financial Integrity Act of 1982 (FMFIA): Back to Table of Contents 10.1.2 - FMFIA and the CMS Medicare Contractor Contract (Rev. 331, Issued: 11-15-19, Effective: 10-01-19, Implementation: 12-17- 19) The CMS contract with its Medicare Title XVIII contractors includes an article titled FMFIA. In this article, the contractor agrees to cooperate with CMS in the development of procedures permitting CMS to comply with FMFIA and other related standards prescribed by the Comptroller General of the United States. The Medicare Part A and Part B (A/B) Medicare Administrative Contractor (MAC), Durable Medical Equipment (DME) MAC, and Specialty MAC (SMAC) (A/B, DME, & Specialty MACs) Statements of Work (SOW)

states that, “the contractor shall establish and maintain efficient and effective internal controls to perform the requirements of the contract in accordance with IOM Pub. 100-06, Chapter 7”. Under various provisions of the Social Security Act, and the Medicare Prescription Drug, Improvement Modernization Act of 2003 (MMA), contractors shall be evaluated by CMS on administrative service performance. The CMS evaluates contractor’s performance by various internal and external reviews. To further sensitize the contractors as to the importance of FMFIA compliance, CMS requires the contractors to annually provide assurance that internal controls are in place and to identify and correct any areas of weakness in their operations. The vehicle used by the contractors to provide this assurance is the Certification Package for Internal Controls (CPIC). The CPIC includes a self-certification representation that the contractor’s internal controls are in compliance with FMFIA expectations, that the contractor recognizes the importance of internal controls, and the contractor has provided required documentation in the package. End Section 10.1.2 – FMFIA and the CMS Medicare Contractor Contract: Back to Table of Contents 10.1.3 - Chief Financial Officers Act of 1990 (CFO) (Rev. 10614, Issued: 03-23-21, Effective: 10-01-20, Implementation: 04-22-21) The CFO Act of 1990 established a leadership structure, provided for long range planning, required audited financial statements, and strengthened accountability reporting. The aim of the CFO Act is to improve financial management systems and information. The CFO Act also requires the development and maintenance of agency financial management systems that comply with: applicable accounting principles, standards, and requirements; internal control standards; and requirements of OMB, the Department of the Treasury, and others. Under the CFO Act, CMS is subject to an annual financial statement audit. Contractors may be included in the annual financial statement audit and shall fully cooperate as needed with the audit. End Section 10.1.3 – Chief Financial Officers Act of 1990 (CFO): Back to Table of Contents 10.1.4 - OMB Circular A-123 (Rev. 10614, Issued: 03-23-21, Effective: 10-01-20, Implementation: 04-22-21) A revised OMB Circular A-123, Management’s Responsibility for Internal Control, issued in December 21, 2004 under the authority of FMFIA, provided specific requirements for assessing and reporting on internal controls. In July 2016, OMB Circular A-123 was again revised, and the title was changed to Management’s Responsibility for Enterprise Risk Management and Internal Control. This Circular defines management’s responsibilities for enterprise risk management (ERM) and internal control. The Circular provides updated implementation guidance to federal managers to improve accountability and effectiveness of federal programs as well as mission-support operations through implementation of ERM practices and by establishing, maintaining, and assessing internal control effectiveness. The Circular emphasizes the need to integrate and coordinate risk management and strong and effective internal control into existing business activities and as an integral part of managing an Agency. Pursuant to OMB Circular A-123, agencies are required to provide an annual assurance statement which represents the agency head’s informed judgment as to the overall adequacy and effectiveness of internal controls related to operations, reporting, and compliance. Appendix A to OMB, Internal Control Over Financial Reporting, was issued in 2004, which required the heads of certain federal agencies to annually document and assess internal controls over financial reporting and report the results in a management assurance statement. In June 2018, an updated version of Appendix A, Management of Reporting and Data Integrity Risk was issued, which among other changes, aligns Appendix A with the 2014 update to the Government Accountability Office (GAO) Green Book in part, by expanding the scope from ICOFR to include internal control over reporting (ICOR).

CMS conducts annual A-123 internal control reviews. Contractors will be subject to the annual A-123 internal control review. In lieu of an A-123 internal control review, contractors may be selected for a Statement on Standards for Attestation Engagements No. 18 (SSAE-18) internal control examination. End Section 10.1.4 – OMB Circular A-123: Back to Table of Contents 10.1.5 - GAO Standards for Internal Controls in the Federal Government (Rev. 10614, Issued: 03-23-21, Effective: 10-01-20, Implementation: 04-22-21) The FMFIA requires the GAO to prescribe standards for internal control in government, more commonly known as the Green Book. GAO's "Standards for Internal Controls in the Federal Government" were updated in September 2014. These standards provide the internal control framework and criteria for designing, implementing, and operating an effective system of internal control. The Green Book defines internal control as a process effected by an entity’s oversight body, management, and other personnel that provides reasonable assurance that the objectives of an entity are achieved. These are the internal control standards that CMS and its contractors must follow. See Section 10.2 for more information regarding GAO Standards for Internal Controls in the Federal Government. End Section 10.1.5 – GAO Standards for Internal Controls in the Federal Government: Back to Table of Contents 10.2 - GAO Standards in the Federal Government (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Back to Table of Contents 10.2.1 - Definition and Objectives (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Internal controls are the checks and balances that ensure that operational objectives are carried out as planned in the most effective and efficient manner possible. We should not look upon these controls as separate specialized systems, but as integral parts of each system that management uses to accomplish the objectives of the Medicare program. In this regard internal controls are not just financial tools that safeguard assets, but are tools that are of vital importance to day-to-day programmatic and administrative operations as well. Internal control should be the first thought in CMS' oversight process. That is, can we be sure that there are adequate internal controls in place and operating effectively for the process we are evaluating? Internal controls are an integral part of an organization's management to provide reasonable assurance that the following objectives are being achieved:

• Effectiveness and efficiency of operations; • Reliability of reporting; and • Compliance with applicable laws and regulations

Internal control also serves as the first line of defense in safeguarding assets and preventing and detecting errors and fraud. In short, internal control, which is synonymous with management control, helps program managers achieve desired results through effective stewardship of resources. End Section 10.2.1 – Definition and Objectives: Back to Table of Contents

10.2.2 - Fundamental Concepts (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Three fundamental concepts provide the underlying framework for designing and applying the internal control standards. A. A continuous built-in component of operations Internal control includes measures and practices that are used to mitigate risks and exposures that could potentially prevent an organization from achieving its goals and objectives. Internal control is not one event or circumstance, but a series of actions that permeate an organization's activities. These actions are pervasive and are inherent in the way management runs the organization. Internal controls involve an organization-wide commitment that defines and implements a continuous process of assessing, monitoring, and tracking activities and risks, through an integrated and effective communication mechanism. B. Are effected by people An organization's management directs internal control, which is carried out by the people within that organization. Management's commitment to establish strong internal control affects the organization's practices. Management sets goals and policies, provides resources, and monitors and evaluates the performance of the organization. The organization's internal control environment is established by these policies and is controlled by available resources. Although internal control begins with this established environment, the employees make it work and must be adequately trained. It is the manner in which the entire organization embraces the internal control that affects their accountability and operational results. C. Provide reasonable assurance, not absolute assurance Reasonable assurance indicates that an internal control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance regarding achievement of an entity's objectives, and further indicates that the likelihood of achievement of these objectives is affected by limitations inherent in all internal control systems. Examples of limitations are:

a. Judgment - the effectiveness of controls will be limited by decisions made by human judgment under pressures to conduct business based on information at hand;

b. Breakdowns - even well designed internal controls can break down. Employees sometimes

misunderstand instructions or simply make mistakes. Errors may also result from new technology and the complexity of computerized information systems;

c. Management Override - high-level personnel may be able to override prescribed policies and

procedures for personal gain or advantage. This should not be confused with management intervention, which represents management actions to depart from prescribed policies and procedures for legitimate purposes;

d. Collusion - control systems can be circumvented by employee collusion. Individuals acting

collectively can alter financial data or other management information in a manner that cannot be identified by control systems.

End Section 10.2.2 – Fundamental Concepts: Back to Table of Contents

10.2.3 - Standards for Internal Control (Rev. 331, Issued: 11-15-19, Effective: 10-01-19, Implementation: 12-17- 19) Internal control consists of five interrelated standards. The GAO "Standards for Internal Control in the Federal Government" describes these five standards:

A. Control environment; B. Risk assessment; C. Control activities; D. Information and communication; and E. Monitoring.

Each of these internal control standards plays an important role in the overall control environment of an organization. These standards define the minimum level of quality acceptable for internal control in government and provide the basis against which the internal control is to be evaluated. While each internal control standard is an integral part of the management process and plays a specific role, it is the combination of these standards that establishes internal control in an organization. The control environment provides the discipline and atmosphere in which the organization conducts its activities and carries out its control responsibilities. It also serves as the foundation for the other standards. Within this environment, management conducts risk assessments to assess the potential effect of internal and external risks in achieving the organization's objectives. Control activities are implemented to help ensure that management directives are carried out as planned. Relevant information is captured and communicated in a timely and effective manner throughout the organization on an ongoing basis. The organization's operations are continuously monitored as an integral part of the organization's performance evaluation. End Section 10.2.3 – Standards for Internal Control: Back to Table of Contents

10.2.3.1 - Control Environment (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Management and employees should establish and maintain an environment throughout the organization that sets a positive and supportive attitude toward internal control and conscientious management. The control environment of an organization sets the tone of an organization, influencing the internal control consciousness of its people. It is the foundation for all other standards of internal control, providing discipline and structure. Control environment factors include the integrity, ethical values, and competence of the organization's people; management's philosophy and operating style; and the way management assigns authority and responsibility and organizes and develops its human resources. End Section 10.2.3.1 – Control Environment: Back to Table of Contents 10.2.3.2 - Risk Assessment (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Every organization faces a variety of risks from external and internal sources that must be assessed. A precondition to risk assessment is establishment of control objectives, linked at different levels and internally consistent. Risk assessment is the identification and analysis of relevant risks to the achievement of established objectives. A key factor in the consideration of an internal control structure is the importance and risk associated with a program and its associated cost effectiveness. When determining whether a particular control objective should be established, the risk of failure and the potential affect must be considered along with the cost of establishing the control. End Section 10.2.3.2 – Risk Assessment: Back to Table of Contents 10.2.3.3 - Control Activities (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) The control activities help ensure that management's directives are carried out. The control activities should be effective and efficient in accomplishing the organization's control objectives. Control activities are the written activities used to support policies and procedures that help ensure management directives are carried out. Also see Section 20.3. They help ensure that necessary actions are taken to address potential risks that may affect the organization's objectives. Control activities occur throughout the organization, at all levels and in all functions. They include a range of activities as diverse as approvals, authorizations, verifications,

reconciliation, performance reviews, security of assets, and segregation of duties. For examples of Non-Information Systems and Information Systems control activities, please see the GAO – Internal Control Management and Evaluation Tool at the following hyperlink: Hyperlink: The USGAO-ICS: Internal Control Management and Evaluation Tool of August 2001 (GAO-01-1008G) [www.gao.gov/new.items/d011008g.pdf] End Section 10.2.3.3 – Control Activities: Back to Table of Contents

10.2.3.4 - Information and Communication (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Information should be recorded and communicated to management and others within the entity who need it and in a form and within a time frame that enables them to carry out their internal control and other responsibilities. Pertinent information shall be identified, captured, and communicated in a form and time frame that enables employees to carry out their responsibilities. Information systems produce reports containing operational, financial, and compliance related information that make it possible to control the organization. Information systems deal not only with internally generated data, but also information about external events, activities and conditions necessary for informed decision making and external reporting. Effective communication also must occur in a broader sense, flowing down, across, and up the organizational structure. All personnel must receive a clear message from top management that control responsibilities must be taken seriously. They must understand their own role in the internal control system, as well as how individual activities relate to the work of others. They must have a means of communicating significant information throughout the organization. The organization must also effectively communicate with external parties, such as customers, suppliers, state officials, and legislators. End Section 10.2.3.4 – Information and Communication: Back to Table of Contents 10.2.3.5 - Monitoring (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Internal control monitoring should assess the quality of performance over time and ensure that the observations and findings of audits and other reviews are promptly resolved.

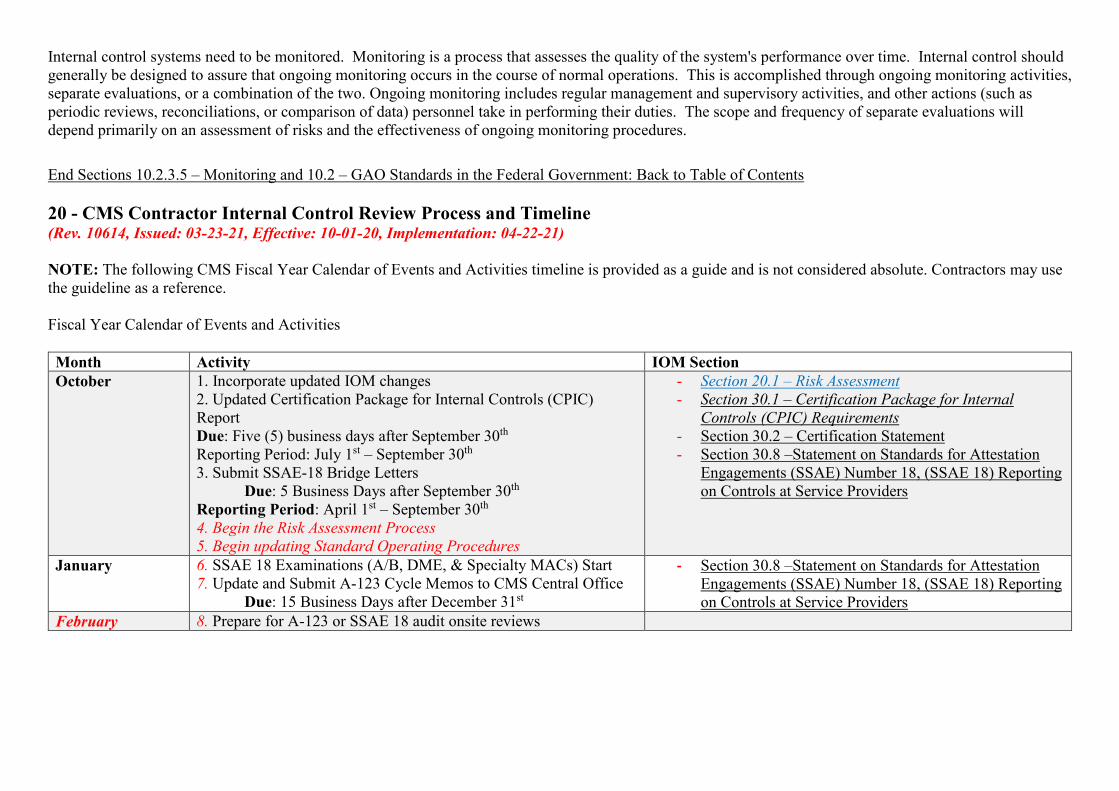

Internal control systems need to be monitored. Monitoring is a process that assesses the quality of the system's performance over time. Internal control should generally be designed to assure that ongoing monitoring occurs in the course of normal operations. This is accomplished through ongoing monitoring activities, separate evaluations, or a combination of the two. Ongoing monitoring includes regular management and supervisory activities, and other actions (such as periodic reviews, reconciliations, or comparison of data) personnel take in performing their duties. The scope and frequency of separate evaluations will depend primarily on an assessment of risks and the effectiveness of ongoing monitoring procedures. End Sections 10.2.3.5 – Monitoring and 10.2 – GAO Standards in the Federal Government: Back to Table of Contents 20 - CMS Contractor Internal Control Review Process and Timeline (Rev. 10614, Issued: 03-23-21, Effective: 10-01-20, Implementation: 04-22-21) NOTE: The following CMS Fiscal Year Calendar of Events and Activities timeline is provided as a guide and is not considered absolute. Contractors may use the guideline as a reference. Fiscal Year Calendar of Events and Activities Month Activity IOM Section October 1. Incorporate updated IOM changes

2. Updated Certification Package for Internal Controls (CPIC) Report Due: Five (5) business days after September 30th

Reporting Period: July 1st – September 30th 3. Submit SSAE-18 Bridge Letters

Due: 5 Business Days after September 30th Reporting Period: April 1st – September 30th

4. Begin the Risk Assessment Process 5. Begin updating Standard Operating Procedures

- Section 20.1 – Risk Assessment - Section 30.1 – Certification Package for Internal

Controls (CPIC) Requirements - Section 30.2 – Certification Statement - Section 30.8 –Statement on Standards for Attestation

Engagements (SSAE) Number 18, (SSAE 18) Reporting on Controls at Service Providers

January 6. SSAE 18 Examinations (A/B, DME, & Specialty MACs) Start 7. Update and Submit A-123 Cycle Memos to CMS Central Office

Due: 15 Business Days after December 31st

- Section 30.8 –Statement on Standards for Attestation Engagements (SSAE) Number 18, (SSAE 18) Reporting on Controls at Service Providers

February 8. Prepare for A-123 or SSAE 18 audit onsite reviews

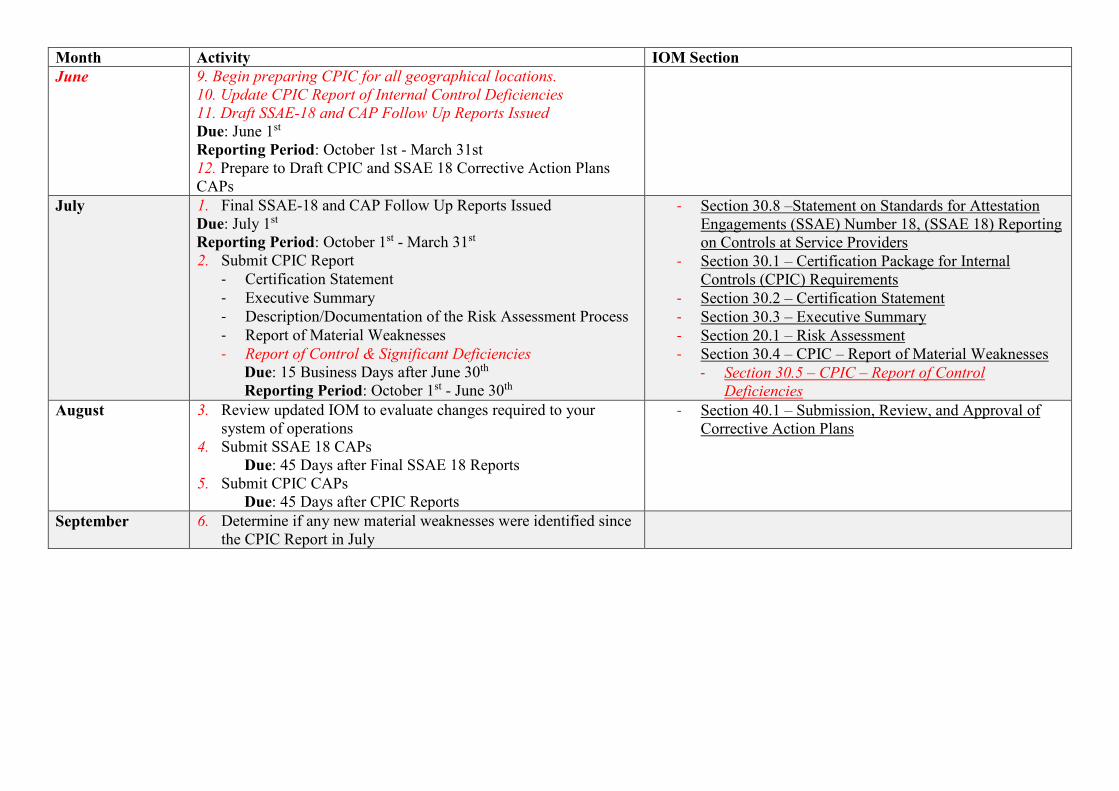

Month Activity IOM Section June 9. Begin preparing CPIC for all geographical locations.

10. Update CPIC Report of Internal Control Deficiencies 11. Draft SSAE-18 and CAP Follow Up Reports Issued Due: June 1st Reporting Period: October 1st - March 31st 12. Prepare to Draft CPIC and SSAE 18 Corrective Action Plans CAPs

July 1. Final SSAE-18 and CAP Follow Up Reports Issued Due: July 1st Reporting Period: October 1st - March 31st

2. Submit CPIC Report - Certification Statement - Executive Summary - Description/Documentation of the Risk Assessment Process - Report of Material Weaknesses - Report of Control & Significant Deficiencies

Due: 15 Business Days after June 30th Reporting Period: October 1st - June 30th

- Section 30.8 –Statement on Standards for Attestation Engagements (SSAE) Number 18, (SSAE 18) Reporting on Controls at Service Providers

- Section 30.1 – Certification Package for Internal Controls (CPIC) Requirements

- Section 30.2 – Certification Statement - Section 30.3 – Executive Summary - Section 20.1 – Risk Assessment - Section 30.4 – CPIC – Report of Material Weaknesses

- Section 30.5 – CPIC – Report of Control Deficiencies

August 3. Review updated IOM to evaluate changes required to your system of operations

4. Submit SSAE 18 CAPs Due: 45 Days after Final SSAE 18 Reports

5. Submit CPIC CAPs Due: 45 Days after CPIC Reports

- Section 40.1 – Submission, Review, and Approval of Corrective Action Plans

September 6. Determine if any new material weaknesses were identified since the CPIC Report in July

20.1 - Risk Assessment (Rev. 331, Issued: 11-15-19, Effective: 10-01-19, Implementation: 12-17- 19) Risk assessment identifies areas that should be reviewed to determine which components of an organization's operation present the highest probability of waste, loss, or misappropriation. The risk assessment process is the identification, measurement, prioritization, and mitigation of risks. This process is intended to provide the contractors with:

• Direction for what areas should get priority attention from management due to the nature, sensitivity, and importance of the area's operations;

• A preliminary judgment from managers about the adequacy of existing internal control policies and

procedures to minimize or detect problems; and • An early indication of where potential internal control weaknesses exist that should be corrected.

The CMS requires contractors to perform an annual risk assessment, to identify the most critical areas and areas of greatest risk to be subjected to a review. Operational managers with knowledge and experience in their particular business area shall perform risk assessments. Outside sources can assist with this process, but should not be solely relied upon (e.g., Internal Audit departments, SSAE 18 audits, OMB Circular A-123 Appendix A reviews, etc.). When performing your yearly risk assessment, you are to consider all results from final reports issued during the fiscal year from internal and external reviews including GAO, OIG, CFO audit, Contractor Performance Evaluation (CPE), CPIC, Contractor’s Monthly Bank Reconciliation Worksheet (CMBRW) and 1522 reviews, A-123 Appendix A reviews and results of your own or CMS-sponsored SSAE 18 audits. Any of these findings could impact your risk assessment and preparation of your certification statement. Your risk assessment process shall provide sufficient documentation to fully explain the reasoning behind and the planned testing methodology for each selected area. The contractor shall submit a description of the risk assessment process to CMS as an attachment with the annual CPIC and maintain sufficient documentation to support the risk assessment process. Examples of sufficient documentation are meeting agendas, meeting notes or minutes, and emails. The documentation should be readily available for CMS review. Below are the elements to include in the description or methodology of your risk assessment process:

• Who - List who is involved and state their roles and responsibilities. • Where - List the geographical location(s) for which the certification applies. For multi-site

contractors, review and explain the roles for all sites, i.e., do they do their own risk assessment and control objective testing. Describe the certification process for geographical locations.

• What – Describe the risk factors and the risk assessment process. • When - List when the risk assessment process was completed. • Why – Prioritize control objectives based upon their level of risk while ensuring high risk areas are

reviewed in accordance with the scoring criteria guidelines in Section 20.1.

NOTE: The A/B, DME, and Specialty MAC SOW may also include requirements regarding review of CMS control objectives.

• How – Describe the scoring methodology and provide a description and definition for each risk and

exposure factor. Include specific value ranges used in your scoring methodology.

The contractor is encouraged to exceed the risk assessment approach provided below based on its unique operations. The risk assessment process shall at a minimum include the following and shall be submitted as part of the CPIC package: Step 1 - Segment Operations Segment the contractor’s operation into common operational areas of activity that can be evaluated. List the primary components of the unit with consideration to the business purpose, objectives, or goals of the auditable unit. Limit the list to the primary activities designed to achieve the goals and objectives of the auditable unit. Include the CMS control objectives applicable to each auditable unit. Step 2 - Prioritize Risk and Exposure Factors Identify the primary risks and exposure factors that could jeopardize the achievement of the goals and objectives of the unit as well as the organization's ability to achieve the objectives of reliable financial reporting, safeguarding of assets, and compliance with budget, laws, regulations and instructions. Risk and exposure factors can arise due to both internal and external circumstances. Document the definitions and methodology of the risk and exposure factors used in the risk assessment process. Step 3 – Create a Matrix to Illustrate the Prioritization of Risk and Exposure Factors Create a matrix listing on the left axis by operational areas of activity (see Step 1 above). The top axis should list all the risk and exposure factors of concern and determine the weight each column should have. Some columns may weigh more than other columns. Develop a scoring methodology and provide a description and definitions of this methodology used for each risk or exposure factor. This methodology can use an absolute ranking or relative risk identification. Absolute ranking would assign predefined quantifiable measures such as dollars, volume, or some other factor in ranges that would equate to a ranking score such as high, medium or low. Relative risk ranking involves identifying the risk and exposure factors into natural clusters by definition and assigning values to these clusters. Include a legend with the score ranges representing high-risk, medium-risk, and low-risk on the risk matrix. Assign a score to each cell based on the methodology predetermined. Retain notes to support scoring of key risk factors such as “prior audits” and factors that are scored very high or very low. This will assist CMS in evaluating the reasonableness of your risk assessment results. Total the scores for each line item (control objective). The higher scores for each line item will prioritize the risk areas for consideration to be reviewed to support the CPIC. If a high risk control objective is included in a current year Type II SSAE 18 audit, or A-123 Appendix A review, you may rely on the SSAE 18 audit, or A-123 Appendix A review testing and document this as the rationale for excluding it from testing. The CMS considers system security to be a high risk area. Therefore, contractors shall include control objective A.1 in their CPIC each year. All contractors are required to certify their system security compliance. Contractors shall verify that a system's security plan meet CMS’ Minimum Security Requirements as defined by the Business Partners Systems Security Manual (BPSSM). Contractors should write a few paragraphs to self-certify that their organization has successfully completed all required security activities including the security self-assessment of their Medicare IT systems and associated software in accordance with the terms of their Contract. For more details, please see Section 3.4 – Certification of the BPSSM, which can be found at the following hyperlink: Hyperlink: CMS IOM Publication #: 100-17, CMS Business Partners Systems Security Manual, Revision #: 12, Issued: 11/15/2013 [https://www.cms.gov/Regulations-and-Guidance/Guidance/Manuals/Downloads/117_Systems_security.pdf] Also, include the results of the testing of A.1 in the Executive Summary. See Section 30.3.

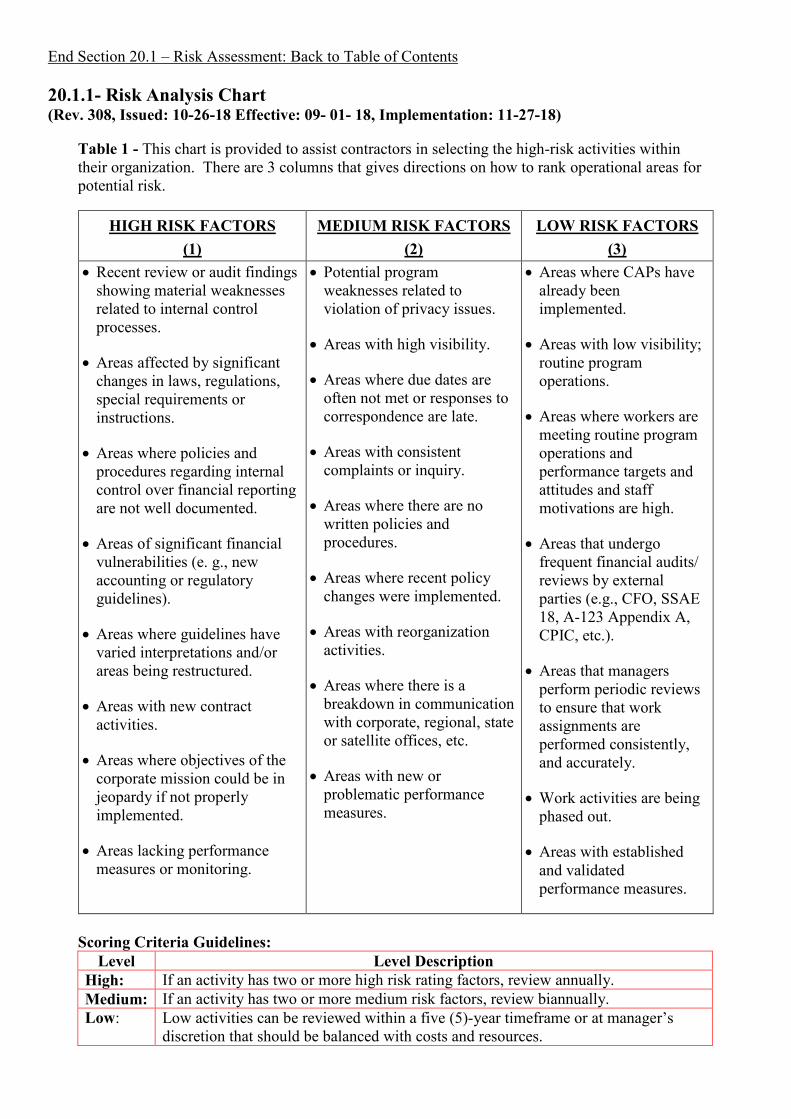

End Section 20.1 – Risk Assessment: Back to Table of Contents 20.1.1- Risk Analysis Chart (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18)

Table 1 - This chart is provided to assist contractors in selecting the high-risk activities within their organization. There are 3 columns that gives directions on how to rank operational areas for potential risk.

HIGH RISK FACTORS (1)

MEDIUM RISK FACTORS (2)

LOW RISK FACTORS (3)

• Recent review or audit findings showing material weaknesses related to internal control processes.

• Areas affected by significant changes in laws, regulations, special requirements or instructions.

• Areas where policies and procedures regarding internal control over financial reporting are not well documented.

• Areas of significant financial vulnerabilities (e. g., new accounting or regulatory guidelines).

• Areas where guidelines have varied interpretations and/or areas being restructured.

• Areas with new contract activities.

• Areas where objectives of the corporate mission could be in jeopardy if not properly implemented.

• Areas lacking performance measures or monitoring.

• Potential program weaknesses related to violation of privacy issues.

• Areas with high visibility.

• Areas where due dates are often not met or responses to correspondence are late.

• Areas with consistent complaints or inquiry.

• Areas where there are no written policies and procedures.

• Areas where recent policy changes were implemented.

• Areas with reorganization activities.

• Areas where there is a breakdown in communication with corporate, regional, state or satellite offices, etc.

• Areas with new or problematic performance measures.

• Areas where CAPs have already been implemented.

• Areas with low visibility; routine program operations.

• Areas where workers are meeting routine program operations and performance targets and attitudes and staff motivations are high.

• Areas that undergo frequent financial audits/ reviews by external parties (e.g., CFO, SSAE 18, A-123 Appendix A, CPIC, etc.).

• Areas that managers perform periodic reviews to ensure that work assignments are performed consistently, and accurately.

• Work activities are being phased out.

• Areas with established and validated performance measures.

Scoring Criteria Guidelines:

Level Level Description High: If an activity has two or more high risk rating factors, review annually. Medium: If an activity has two or more medium risk factors, review biannually. Low: Low activities can be reviewed within a five (5)-year timeframe or at manager’s

discretion that should be balanced with costs and resources.

End Section 20.1.1 – Risk Analysis Chart: Back to Table of Contents 20.2 - Internal Control Objectives (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Internal control objectives are established to identify risk and vulnerabilities. Control objectives may be set for an entity as a whole, or be targeted to specific activities within the entity. Generally, objectives fall into three categories:

1. Operations - relating to effective and efficient use of the organization's resources. 2. Financial Reporting - relating to preparation of reliable financial statements. 3. Compliance - relating to the organization's compliance with applicable laws and regulations.

An acceptable internal control system can be expected to provide reasonable assurance of achieving objectives relating to the reliability of operations, financial reporting and compliance. Achievement of those objectives depends on how activities within the organization's control are performed. Section 50 lists the minimum set of control objectives. The contractor may add to the CMS control objective list. For the respective operational areas selected for review in Step 2 of the Risk Assessment discussion, cross-reference the high risk operational areas to CMS' or the contractor’s unique control objectives on a work sheet. Some control objectives will apply to more than one operational area selected for review. The control objectives identified in this step shall be validated by documentation of the control activities (see Section 10.2.3.3) used as well as testing (see Section 20.4) that supports the control objectives. Reminder: Excessive control is costly and counterproductive. Too little control presents undue risk. There should be a conscious effort made to achieve an appropriate balance. End Section 20.2 – Internal Control Objectives: Back to Table of Contents 20.2.1 – CMS Contractor Control Objectives (Rev. 10614, Issued: 03-23-21, Effective: 10-01-20, Implementation: 04-22-21) CMS issues broad control objectives for which contractors shall develop control activities to ensure the objectives are met. The complete list of control objectives are in Section 50. If your risk assessment was completed prior to issuance of the current year CMS control objectives, ensure that any new or revised control objectives are assessed and the risk matrix is updated. In addition, control activities should be created or updated to support any new or revised control objectives as appropriate (see Section 10.2.3.3). Contractors shall also include in their risk assessment any significant or material areas not covered by a CMS control objective. End Section 20.2.1 – CMS Contractor Control Objectives: Back to Table of Contents 20.3 – Policies and Procedures (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Policies and procedures are a set of established guidelines or rules for conducting the affairs of a business. Good policies:

• Are written in clear, concise, and simple language. They are updated as necessary, signed and dated. • Address what the guideline or rule is; not how to implement the guideline or rule.

• Are readily available and properly communicated to staff.

Procedures are a set of steps in a plan intended to influence and determine decisions and actions. Good procedures are tied to policies and:

• Are written in clear, concise, and simple language. • Are tied to the policy. • Are developed and implemented with the user in mind. • Are readily available and properly communicated to staff.

Contractors shall have written policies and procedures to achieve their control objectives. These policies and procedures shall be updated in a timely manner to reflect changes in CMS instructions or your internal operations. Contractors shall demonstrate and document that its policies and procedures are actually being used as designed and are effectively and efficiently meeting the control objective, as described in Section 50. Evaluation and testing of the effectiveness of controls are important in determining if the major areas of risk have been properly mitigated. An example of a policy is, “an agency shall establish physical control to secure and safeguard vulnerable assets”. The specific control activities, or procedures, which support this policy may include: all doors to the facility have locks, the locks only have one key, all keys are held by security guards, security guards are stationed at every door. End Section 20.3 – Policies and Procedures: Back to Table of Contents 20.4 - Testing Methods (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) Testing the policies and procedures involves ensuring that the documented policies and procedures are actually being used as designed and are effective to meet a control objective. Evaluating and testing the effectiveness of policies and procedures is important to determine if the major areas of risks have been properly mitigated and provide reasonable assurance that the control objective is met. Testing and evaluating the policies and procedures consists of five (5) steps: Step 1: Select the policies or procedures to be tested It is both impractical and unnecessary to test all policies and procedures. The policies and procedures to be tested are those that primarily contribute to the achievement of the control objectives. A policy or procedure may be eliminated from testing when it does not meet the control objective to be tested due to being poorly designed, unnecessary or duplicative, or not performed in a timely manner. However, if this justification is invoked, other policies and procedures should be tested to validate meeting the control objective. Another justification for testing elimination is due to the cost of testing the policy or procedure exceeds the value of the control objective to be tested. If a policy or procedure is eliminated from testing, the reasoning should be documented. Step 2: Select test methods Once the policies and procedures to be tested are determined, test methods shall be determined. A combination of tests can be used depending on risk or type of activity. The following would be considered acceptable tests:

1. Inquiry: Asking responsible personnel if certain controls are functioning as intended (e.g., “Do you

reconcile your activity or do you review a certain report each month?”). 2. Inspection: Analyzing evidence of a given control procedure (e.g., searching for signatures of a

reviewing official or reviewing past reconciliations). 3. Observation: Observing actual controls in operation (e.g., observing a physical inventory or watching

a reconciliation occur). 4. Re-performance: Conducting a given control procedure more than once (e.g., recalculating an

estimate or re-performing a reconciliation). Observation and inquiry are less persuasive forms of evidence than inspection and re-performance. Step 3: Determine how much testing is needed The next sub-step is to determine the extent of the testing efforts. In most cases, it is unrealistic to observe each policy and procedure or to review 100 percent of all records. Instead, policies and procedures are tested by observing a selected number of controls performed or by reviewing a portion of the existing records. This selection process is called sampling. A representative sample provides confidence that the findings are not by chance by taking into account the factors of breadth and size.

1. Breadth: Breadth of the sample assures that the testing covers all bases and is a representative cross section of the universe being tested. This will provide confidence that the sample will lead to a conclusion about the situation as a whole.

2. Size: Size is the number of items sampled. The size should be large enough to allow a conclusion

that the findings have not happened by chance and provide confidence in the conclusion. The size of the sample should not be so large that testing becomes too costly. When selecting the size of the sample consider:

a. Experience: Reducing the size of the sample when controls have operated satisfactorily in the

past and no major changes have occurred. b. Margin of Error: Increase the size of the sample when only a small margin of error is acceptable. c. Importance: Increase the size of the sample when an important resource is at stake. d. Type: Increase the size of the sample when the control to be tested requires judgment calls.

Decrease the size of the sample when the control is routine. Step 4: Plan data collection The sampling plan gives an idea of the "who, where, what, when, why, and how" (see Section 20.1) aspect of the tests to be conducted. A data collection plan can be used to determine how the test results will be recorded. The accurate recording of test results is an extremely important part of the test documentation. Planning data collection prior to beginning the testing can be very helpful to ensure the information collected will provide conclusive data from which to evaluate the controls. Step 5: Conduct the tests The final step of testing and evaluating controls consists of actually effectuating the testing protocol and documenting the results.

At the conclusion of the testing, the results are analyzed and evaluated. Evaluating involves reviewing the information collected and making an overall judgment on the adequacy of the internal control system as a whole. Deficient areas are to be categorized into Control Deficiencies, Significant Deficiencies, and Material Weaknesses and should be considered for inclusion in the CPIC submission (see Section 30.6). End Section 20.4 – Testing Methods: Back to Table of Contents 20.5 - Documentation and Working Papers (Rev. 308, Issued: 10-26-18 Effective: 09- 01- 18, Implementation: 11-27-18) The contractor shall document through its working papers, the process it employed to support its internal control certification. This documentation shall include working papers so that a CMS reviewer can conclude that the Risk Assessment process as described in Section 20.1 follows or exceeds these guidelines, and that the Control Activities (Section 10.2.3.3) identified to support the high risk control objectives selected for review are current and clearly stated. Finally, the CPIC documentation shall demonstrate how the Testing Methods employed comply with the general parameters as described in Section 20.4 for the purpose of Control Activity validation. Working papers contain evidence accumulated throughout the review to support the work performed, the results of the review, including findings made, the judgment and/or conclusion of the reviewers. They are the records kept by the reviewer of the procedures applied, the tests performed, the information obtained, and the pertinent judgment and/or conclusions reached in the review process. Examples of working papers are review programs, analyses, memoranda, letters of confirmation and representation, abstracts of documents, and schedules or commentaries prepared or obtained by the reviewer. Working papers may be in the form of data stored on tapes, film, or other media. General Content of Working Papers - Working papers should ordinarily include documentation showing that:

• The work has been adequately planned and supervised. • The review evidence obtained, the reviewing procedures applied, and the testing performed has

provided sufficient, competent evidential matter to support the reviewer's judgments and/or conclusions.

Format of Working Papers - Working paper requirements should ensure that the working papers follow certain standards. As a whole, a good set of working papers should contain the following:

• The objectives, scope, methodology, and the results of the review. • Proper support for findings, judgments and/or conclusions, and to document the nature and scope of

the work conducted. • Sufficient information so that supplementary oral explanations are not required. • Adequate indexing and cross-referencing, and summaries and lead schedules, as appropriate. • Date and signature by the preparer and reviewer. • Evidence of supervisory review of the work.

• Proper heading should be given to the basic content of the working papers.

End Sections 20.5 – Documentation and Working Papers and 20 – CMS Contractor Internal Control Review Process and Timeline: Back to Table of Contents

30 - Internal Control Reporting Requirements (Rev. 10614, Issued: 03-23-21, Effective: 10-01-20, Implementation: 04-22-21) Several reporting methods are required for internal controls. Medicare Contractors shall use the following CPIC and SSAE 18 guidance to successfully meet them. Back to Table of Contents 30.1 – Certification Package for Internal Controls (CPIC) Requirements (Rev. 10614, Issued: 03-23-21, Effective: 10-01-20, Implementation: 04-22-21) NOTE: This section is only applicable to the following listed CMS Contractors: # Contractor Workload 1 DME MAC Jurisdiction A 2 DME MAC Jurisdiction B 3 DME MAC Jurisdiction C 4 DME MAC Jurisdiction D 5 Parts A & B MAC Jurisdiction 5 6 Parts A & B MAC Jurisdiction 6 7 Parts A & B MAC Jurisdiction 8 8 Parts A & B MAC Jurisdiction 15 9 Parts A & B MAC Jurisdiction E 10 Parts A & B MAC Jurisdiction F 11 Parts A & B MAC Jurisdiction H 12 Parts A & B MAC Jurisdiction J 13 Parts A & B MAC Jurisdiction K 14 Parts A & B MAC Jurisdiction L 15 Parts A & B MAC Jurisdiction M 16 Parts A & B MAC Jurisdiction N 17 Specialty MAC Railroad Board (RRB) 18 Pricing, Data Analysis, and Coding (PDAC) Contractor 19 Affordable Care Act Exchange Contractor 20 Benefits Coordination and Recovery Center (BCRC),

Medicare Secondary Payer Recovery Contractor (MSPRC) 21 Commercial Repayment Center (CRC), MSPRC 22 Retiree Drug Subsidy (RDS) Part D Contractor

The contractor certification process provides CMS with assurance that contractors are in compliance with the FMFIA, OMB Circular A-123, and CFO Act of 1990 by incorporating internal control standards into their operations. The contractor certification process supports the audit of CMS' financial statements by the Office of Inspector General (OIG) and the CMS Administrator's FMFIA assurance statement. This compliance is achieved by an annual certification statement included in its annual CPIC submission. CMS has required each contractor to certify that internal controls are in place to identify and correct areas of weakness in its operations. Contractors are expected to evaluate the effectiveness of their operations against CMS' control objectives discussed above. The control objectives represent the minimum expectations for contractor performance in the area of internal controls. Contractors shall have written policies and procedures regarding their annual CPIC preparation and submission process. Contractors shall also have written policies and procedures to address potential internal control deficiencies identified by employees and managers in the course of their daily operations. This includes the process for reporting issues upward through the appropriate levels of management, tracking and correcting deficiencies, and inclusion in the CPIC submission.

The CPIC represents a summary of your internal control environment for the period October 1st through June 30th (the CPIC period), as certified by your organization. It shall include an explicit conclusion as to whether the internal controls over financial reporting are effective (see Section 30.1.1). All material weaknesses identified during this period shall be included in the CPIC submission. Contractors should consider the results of internal and external audits and reviews, such as GAO, OIG, and CFO Act audits, consultant reviews, management control reviews, CPE reviews, SSAE 18 audits, A-123 Appendix A reviews, and other similar activities. These findings should be classified as control deficiencies, significant deficiencies, or material weaknesses based upon the definitions provided in Section 30.6. The contractor shall submit one CPIC report for each type of contract (i.e., A/B, DME, & Specialty MAC workloads, Retiree Drug Subsidy (RDS), and Medicare Secondary Payer Recovery Contractor (MSPRC) workloads). The contractor shall follow these guidelines when submitting the CPIC for A/B, DME, & Specialty MACs:

• Contractors with multiple A/B and DME MAC jurisdictions may submit a CPIC for each jurisdiction or may submit a combined CPIC as long as certification, test results, risk assessments, etc. are presented/distinguished for each jurisdiction.

• The Specialty MAC RRB shall submit a CPIC.

• Contractors that transitioned out of the program prior to June 30th, and are not assuming additional

workloads are not required to submit a CPIC. Electronic CPIC reports shall be received by CMS within fifteen (15) business days after June 30th. The contractor is not required to submit a hard copy report if it has the capability to insert electronic signatures or if the CPIC is sent from the VP of Operations’ email or the CFO’s email. An electronic version of all documents (including updates) submitted as part of your CPIC submission shall be sent to CMS’ Office of Financial Management (OFM) at [email protected] as Microsoft Excel or Word files. Electronic copies shall also be sent as follows:

• A/B, DME, and Specialty MACs shall send to the: o Director of the Office of Program Operations & Local Engagement (OPOLE) o IFM CFO Coordinator o Contracting Officer’s Representative (COR) of the A/B, DME, or Specialty MAC.

• RDS and MSPRC Contractors shall send to the CMS COR. A hard copy is not required to be submitted. The CPIC Report Package shall include:

• Certification Statement, see Section 30.2; • Executive Summary, see Section 30.3; • Description of your Risk Assessment Process, see Section 20.1. This should include a:

o Matrix to illustrate the prioritization of risk and exposure factors o Narrative or flowchart that outlines the risk assessment process

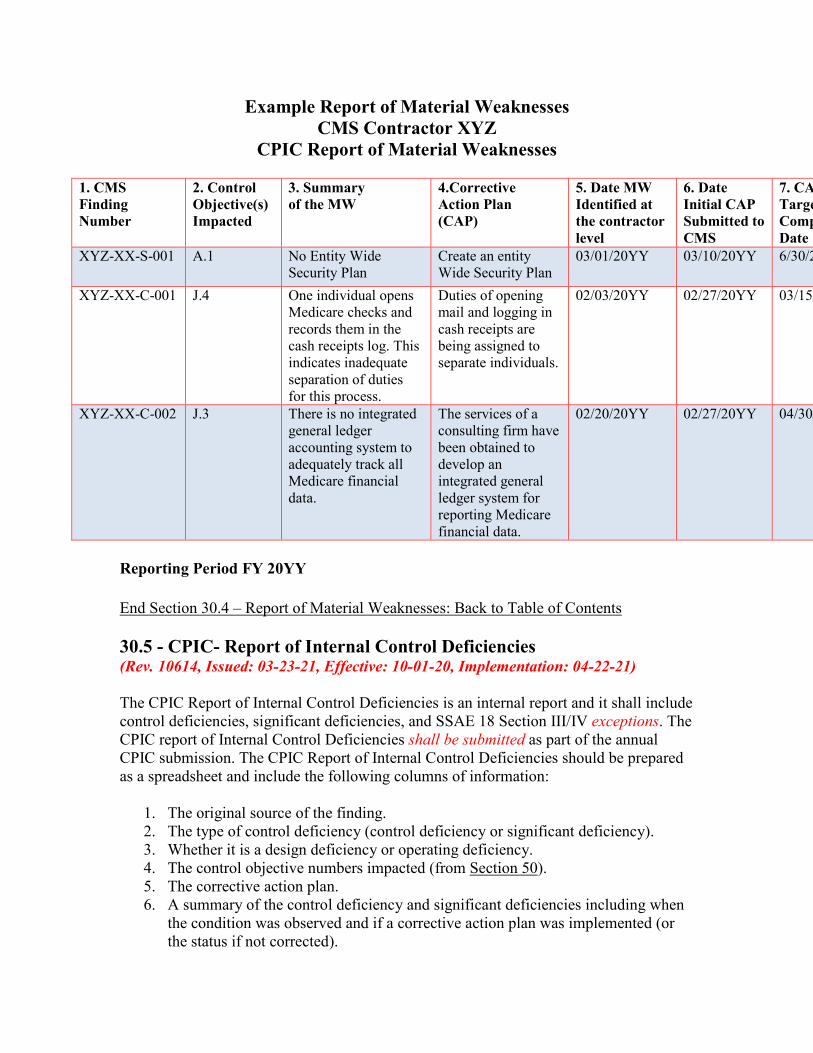

• CPIC Report of Material Weaknesses, see Section 30.4. • CPIC – Report of Internal Control Deficiencies, see Section 30.5.

Contractors shall submit an update for the period July 1st through September 30th to report any subsequently identified material weaknesses. The update shall be no more than a one page summary of any material weaknesses and the proposed corrective action. If no material weaknesses have been identified, the contractor shall submit the following for each jurisdiction or a combined statement for all jurisdictions: “As of September 30th, no material weaknesses (or no additional material weaknesses) have been identified during the period July 1 through September 30th for Fiscal Year 20XX”. The submission of the update

should follow the same guidelines as the initial CPIC. The CPIC update is due within five (5) business days after September 30th. If a material weakness is identified, then a CAP shall be completed in accordance to the guidelines shown at Section 40.1. The file names for all electronic files submitted, as part of your CPIC package should begin with the three, four, or five letter abbreviation assigned to each contractor in Section 40.3. Additionally, in the subject line of your email submission, you shall include the corporate name of the entity submitting the CPIC. Maintain the appropriate and necessary documents to support any assertions and conclusions made during the self-assessment process. In your working papers, you are required to document the respective policies and procedures for each control objective reviewed. These policies and procedures should be in writing, be updated to reflect any changes in operations, and be operating effectively and efficiently within your organization. The supporting documentation and rationale for your certification statement, whether prepared internally or by an external organization, shall be available for review and copying by CMS and its authorized representatives. End Section 30.1 – Certification Package for Internal Controls (CPIC) Requirements: Back to Table of Contents 30.1.1 - OMB Circular A-123, Appendix A: Internal Controls Over Financial Reporting (ICOFR) (Rev. 10614, Issued: 03-23-21, Effective: 10-01-20, Implementation: 04-22-21) CMS contractors, including A/B, DME, and Specialty MACs, MSPRC and RDS, shall use the five steps below to assess the effectiveness of its internal control over financial reporting. Documentation shall occur within each of the basic steps, whether documenting the assessment methodology during the planning phase or documenting key processes and test results during the evaluation and testing steps. 1) Plan and Scope the Evaluation During this phase, the CMS contractor shall leverage existing internal and external audits/reviews performed (Such as SSAE 18 audits, A-123 Appendix A Internal Control Reviews, CPIC, 912 Evaluations, Federal Information Security Management (FISMA), Contractor Performance Evaluations (CPE), etc.) when conducting its assessment of internal control over financial reporting. Management shall consider the results of these audits/reviews in order to identify gaps between current control activities and the documentation of them. The control objectives of A, B, F, G, I, J, K, and L shall be considered, if applicable. If a CMS contractor had an SSAE 18 audit, or an A-123 Appendix A Internal Control Review in the current or past two fiscal years, it shall be used as a basis for the statement of assurance combined with other audits and reviews as appropriate. The contractor shall conduct additional testing for Circular A-123 as deemed necessary (see A-123 Appendix A Internal Control Review/SSAE 18 Reliance Examples chart). For example, if the A-123 Appendix A assurance statement was unqualified, then the contractor is not required to conduct additional testing. Similarly, if the SSAE 18 audit report was unqualified (no findings in Section I (Opinion Letter)), then the contractor is not required to conduct additional testing. However, if the previous year’s A-123 Appendix A assurance statement is qualified, then the contractor shall conduct additional testing on the control deficiencies identified. Similarly if Section I of the prior year’s SSAE 18 audit report is qualified (one or more findings that have not been corrected and validated), then the contractor shall conduct additional testing on the findings identified in Section I and the exceptions identified in Section III (See A-123 Appendix A Internal Control Review Reliance Examples chart). If other audits and reviews contradict the SSAE 18 audit or A-123 Appendix A Internal Control Review, then that contradiction shall be addressed via testing if the issue has not already been corrected and validated.

2) Document Controls and Evaluate Design of Controls This step begins with the documentation and evaluation of entity-level controls. Consideration must be given to the five standards of internal control (control environment, risk assessment, control activities, information and communication, and monitoring) (see Section 10.2.3 – Standards for Internal Control) that can have a pervasive effect on the risk of error or fraud, and will aid in determining the nature and extent of internal control testing that may be required at the transaction or process level. The GAO issued an internal control evaluation tool (The GAO Internal Control Management and Evaluation Tool) to assess the effectiveness of internal control and identify important aspects of control in need of improvement. This tool shall be used in conducting your assessment. Contractors shall prepare cycle memos for financial reporting, accounts receivable, accounts payable, and claims expense (Note: Contractors may combine related cycles (e.g., accounts payable and claims expense). These major transaction cycles relate to significant line items on the financial reports. Cycle memos should identify the key control activities that are relied upon to assure the relevant financial statement assertions are met:

• Existence and Occurrence: All reported transactions actually occurred during the reporting period and all assets and liabilities exist as of the reporting date. Recorded transactions represent economic events that actually occurred during a stated period of time.

• Rights and Obligations: The entity legally owns all its assets collectively and all

liabilities are legal obligations of the entity. Assets and liabilities reported on the Balance Sheet are bona fide rights and obligations of the entity as of that point in time.

• Completeness: All assets, liabilities, and transactions that should be reported have

been included, and no unauthorized transactions or balances are included. All transactions during a specific period should have been recorded in that period. No unrecorded assets, liabilities, transactions or omitted disclosures.

• Valuation or Allocation: Assets, liabilities, revenue, and expenses have been

included in the financial statements at appropriate amounts. Where applicable, all costs have been properly allocated. Assets and liabilities are recorded at appropriate amounts in accordance with relevant accounting principles and policies.

• Presentation and Disclosure: The financial report is presented in the proper form

and any required disclosures are present. Financial statement items are properly described, classified and fairly presented.

Not all assertions will be significant to all accounts. A single key control will often not cover all assertions; which may necessitate several key controls to support the selected assertions for each line item. However, each assertion is applicable to every major transaction cycle and all associated assertions must be covered to avoid any control gaps. Documenting transaction flows accurately is one of the most important steps in the assessment process, as it provides a foundation for the A-123 assessment. Thorough, well-written documents and flowcharts can facilitate the review of key controls. The documentation should reflect an understanding, from beginning to end, of the underlying processes and document flows involved in each major transaction cycle. This would include the procedures for initiating, authorizing, recording, processing, and reporting accounts and transactions that affect the financial reports. The cycle memo shall include Information Technology (IT) key control activities pertinent to the transaction cycle.

The documentation should start with the collection and review of documentation that already exists. The following are examples of existing documentation that could be used:

• Existing policy and procedure manuals; • Existing forms and documents; • Documentation from independent auditors and the OIG; • Risk assessments; • Accounting manuals; • Memoranda; • Flowcharts; • Job descriptions; • Decision tables; • Procedural write-ups; and/or • Self-assessment reports.

Interviews should be conducted with personnel who have knowledge of the relevant operations to validate that manuals, policies, forms, and documents are accurate and being applied. A major transaction cycle narrative is a written summary of the transaction process. For each major transaction cycle, the narrative describes:

• The initiation point; • The processing type (e.g., automated versus manual, preventative versus detective); • The completion point; • Other data characteristics, such as source; receipt; processing; and transmission; • Key activities/class of transactions within the process; • Controls in place to mitigate the risk of financial statement errors; • Supervisor/manager review; process and calculations performed in preparation of

financial reporting; and process outputs; • Use of computer application controls and controls over spreadsheets used in the

preparation of financial reporting; • Identification of errors; types of errors found; reporting errors; and resolving errors;

and • Ability of personnel to override the process or controls.

Within the cycle memo, the key controls should be clearly identified by highlighting, bolding, or underlining. Contractors are responsible for reviewing and updating cycle memos to keep them current. Control activities are the specific policies, procedures, and activities that are established to manage or mitigate risks. Key controls are those controls designed to meet the control objectives and support management’s financial statement assertions. In other words, they are the controls that management relies upon to prevent and detect material errors and misstatements. For each key control activity, state: (a) the frequency of performance; (b) the specific steps performed; (c) how exceptions are resolved; and (d) how the performance of the control activity and related results/disposition are documented. Examples of control activities that may be identified include:

• Top-level reviews of actual performance; o Compare major achievements to plans, goals, and objectives

• Reviews by management at the functional or actual level; o Compare actual performance to planned or expected results

• Management of human capital; o Match skills to organizational goals o Manage staff to ensure internal control objectives are achieved

• Controls over information processing; o Edit checks of data o Control totals on data files o Access controls o Review of audit logs o Change controls o Disaster recovery

• Physical controls over vulnerable assets; o Access controls to equipment or other assets o Periodic inventory of assets and reconciliation to control records

• Establishment and review of performance measures and indicators; o Relationship monitoring of data

• Segregation of duties; • Proper execution of transactions and events

o Communicating names of authorizing officials o Proper signatures and authorizations

• Accurate and timely recording of transactions and events o Interfaces to record transactions o Regular review of financial reports

• Access restrictions to and accountability for resources and records; and o Periodic reviews of resources and job functions

• Appropriate documentation of transactions and internal control. o Clear documentation o Readily available for examination o Documentation should be included in management directives, policies, or operating manuals

To document management’s understanding of major transaction cycles, management should use a combination of the following:

• Narratives; • Flowcharts; and • Control matrices.

To illustrate this process, we have provided cycle memo guidelines in Section 60. Updated cycle memos shall be submitted to the CMS Internal Controls mailbox within fifteen business days after December 31. Note: The cycle memos must be 508 compliant when released to the Internal Controls mailbox. For information on 508 compliance, please visit the website at the following hyperlink: Hyperlink: The US Department of Health and Human Services (HHS) Section 508 Compliance Information In addition, the A/B, DME, and Specialty MAC contractors shall provide updated cycle memos to the SSAE 18 auditors. 3) Test Operating Effectiveness Testing of the operation of key controls shall be performed and documented (refer to “Plan and Scope the Evaluation” (above) as well as the chart below with regard to testing applicability), to determine whether the control is operating effectively, partially effectively, or not effectively. Testing shall address both manual and automated controls. Ideally, testing should be performed throughout the year. The results of testing completed prior to June 30th will form the basis of the June 30th assurance statement. As testing continues into the fourth quarter, the results of that testing, along with any items corrected since the June 30th assurance statement will be considered in the September 30th assurance statement update. The chart below is provided to assist contractors in determining when to conduct testing.

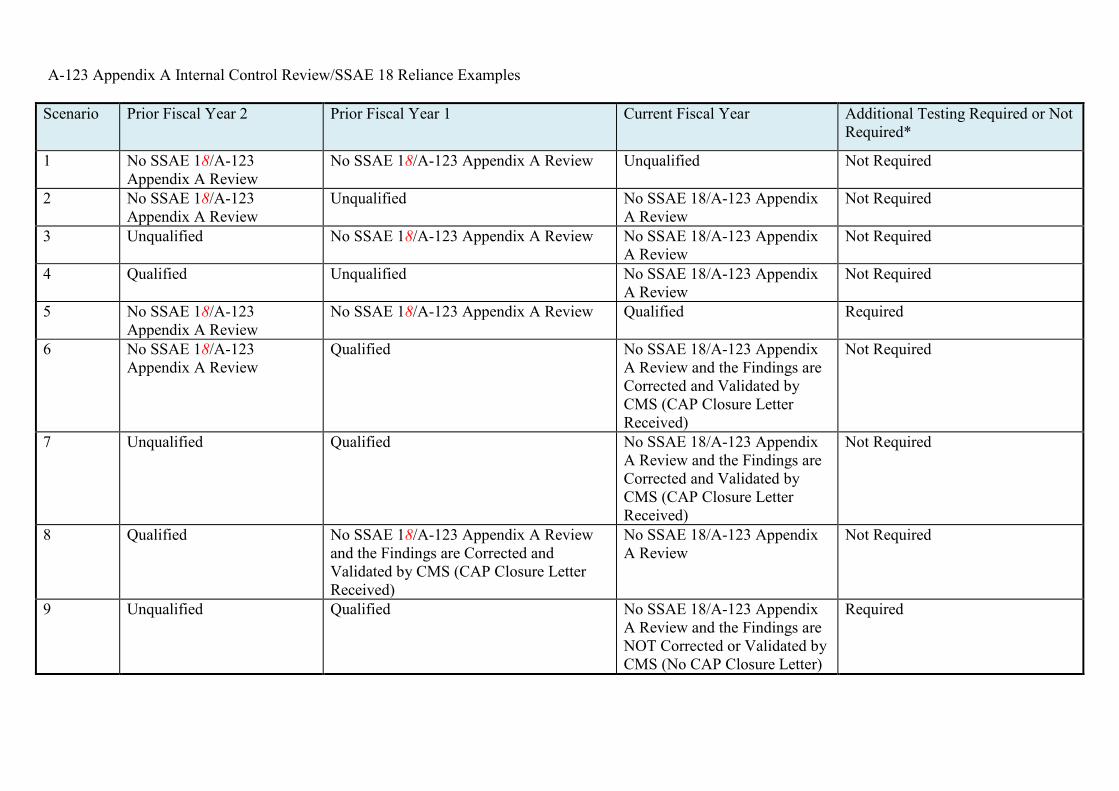

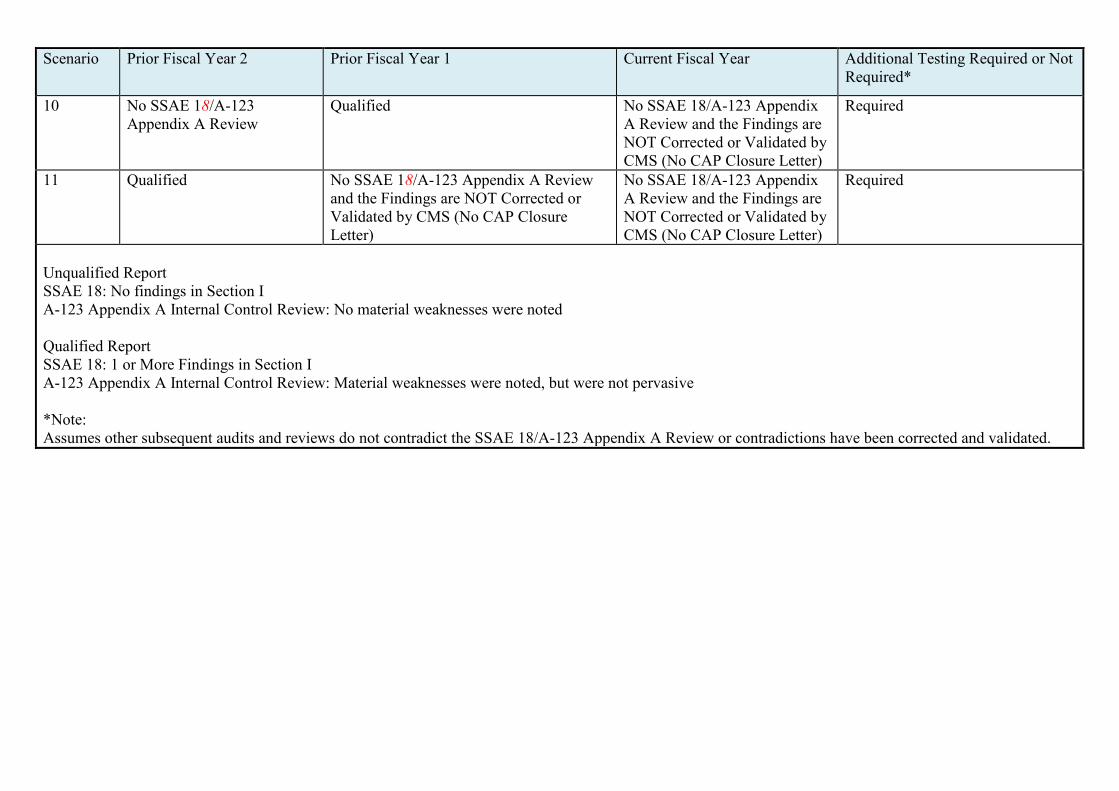

A-123 Appendix A Internal Control Review/SSAE 18 Reliance Examples

Scenario Prior Fiscal Year 2 Prior Fiscal Year 1 Current Fiscal Year Additional Testing Required or Not Required*

1 No SSAE 18/A-123 Appendix A Review

No SSAE 18/A-123 Appendix A Review Unqualified Not Required

2 No SSAE 18/A-123 Appendix A Review

Unqualified No SSAE 18/A-123 Appendix A Review

Not Required

3 Unqualified No SSAE 18/A-123 Appendix A Review No SSAE 18/A-123 Appendix A Review

Not Required

4 Qualified Unqualified No SSAE 18/A-123 Appendix A Review

Not Required

5 No SSAE 18/A-123 Appendix A Review

No SSAE 18/A-123 Appendix A Review Qualified Required

6 No SSAE 18/A-123 Appendix A Review

Qualified No SSAE 18/A-123 Appendix A Review and the Findings are Corrected and Validated by CMS (CAP Closure Letter Received)

Not Required

7 Unqualified Qualified No SSAE 18/A-123 Appendix A Review and the Findings are Corrected and Validated by CMS (CAP Closure Letter Received)

Not Required

8 Qualified No SSAE 18/A-123 Appendix A Review and the Findings are Corrected and Validated by CMS (CAP Closure Letter Received)

No SSAE 18/A-123 Appendix A Review

Not Required

9 Unqualified Qualified No SSAE 18/A-123 Appendix A Review and the Findings are NOT Corrected or Validated by CMS (No CAP Closure Letter)

Required

Scenario Prior Fiscal Year 2 Prior Fiscal Year 1 Current Fiscal Year Additional Testing Required or Not Required*

10 No SSAE 18/A-123 Appendix A Review

Qualified No SSAE 18/A-123 Appendix A Review and the Findings are NOT Corrected or Validated by CMS (No CAP Closure Letter)

Required

11 Qualified No SSAE 18/A-123 Appendix A Review and the Findings are NOT Corrected or Validated by CMS (No CAP Closure Letter)

No SSAE 18/A-123 Appendix A Review and the Findings are NOT Corrected or Validated by CMS (No CAP Closure Letter)

Required

Unqualified Report SSAE 18: No findings in Section I A-123 Appendix A Internal Control Review: No material weaknesses were noted Qualified Report SSAE 18: 1 or More Findings in Section I A-123 Appendix A Internal Control Review: Material weaknesses were noted, but were not pervasive *Note: Assumes other subsequent audits and reviews do not contradict the SSAE 18/A-123 Appendix A Review or contradictions have been corrected and validated.

4) Identify and Correct Deficiencies If design or operating deficiencies are noted, the potential impact of control gaps or deficiencies on financial reporting shall be discussed with management. The magnitude or significance of the deficiency will determine if it should be categorized as a control deficiency, a significant deficiency, or a material weakness (see Section 30.6). Corrective action plans (CAPs) shall be created and implemented to remediate identified deficiencies (see Section 40). The contractor shall submit corrective action plans for all deficiencies (control deficiencies, significant deficiencies, and material weaknesses) identified as a result of A-123 Appendix A reviews and SSAE 18 Section I findings. 5) Report on Internal Controls / Certification Statement The culmination of the contractor’s assessment will be the assurance statement regarding its internal control over financial reporting. The statement will be one of three types: 1) Unqualified Statement of Assurance Each contractor shall submit, as part of the CPIC report, an assurance statement for internal controls over financial reporting (ICOFR) stating: “… (Contractor) has effective internal controls over financial reporting (ICOFR) in compliance with OMB Circular A-123, Appendix A.” NOTE: The contractor’s statement of assurance should be unqualified if this is consistent with the A-123 Appendix A Internal Control Review statement per the CPA firm report (augmented by internal reviews, if necessary). Similarly, if the SSAE 18 audit (augmented by internal reviews, if necessary) did not result in any Section I findings or the contractor has not classified any findings as material weaknesses, then an unqualified statement of assurance would be applicable. 2) Qualified Statement of Assurance Each contractor shall submit, as part of the CPIC report, an assurance statement for internal controls over financial reporting stating: “…(Contractor) has effective internal controls over financial reporting in compliance with OMB Circular A-123, Appendix A, except for the SSAE 18 Section I finding(s) and/or material weakness(es) identified in the attached Report of Material Weaknesses.” Note: The contractor’s statement of assurance should be qualified if this is consistent with the A-123 Appendix A Internal Control Review statement per the CPA firm report (augmented by internal reviews, if necessary). Similarly, if a SSAE 18 audit disclosed at least one Section I finding and/or internal reviews in the current year disclosed a material weakness, then a qualified statement of assurance (see above) or a statement of no

assurance (see below) would be issued, depending on the pervasiveness of the Section I findings or material weakness. The results of work performed in other control-related activities may also be used to support your assertion as to the effectiveness of internal controls. 3) Statement of No Assurance Each contractor shall submit, as part of the CPIC report, an assurance statement for internal controls over financial reporting stating: “…(Contractor) is unable to provide assurance that its internal control over financial reporting was operating effectively due to the material weakness(es) identified in the attached Report of Material Weaknesses.” or “…(Contractor) did not fully implement the requirements included in OMB Circular A-123, Appendix A and therefore cannot provide assurance that its internal control over financial reporting was operating effectively.” End Section 30.1.1 – OMB Circular A-123, Appendix A: Internal Controls Over Financial Reporting (ICOFR): Back to Table of Contents 30.2 - Certification Statement (Rev. 10614, Issued: 03-23-21, Effective: 10-01-20, Implementation: 04-22-21) Contractors shall provide a certification statement to CMS pertaining to your internal controls. On the following page is a generic certification statement. This statement should be included as part of your CPIC. The statement is to be signed jointly by your Medicare CFO and Vice President (VP) for Medicare, RDS or MSPRC or the equivalent Senior Executive responsible for Medicare, RDS or MSPRC. The CPIC is due within fifteen (15) business days after June 30th and shall cover the period from October 1st through June 30th. An updated assurance statement for the period July 1st through September 30th is due to CMS within five (5) business days after September 30th. Your certification statement should follow this outline:

Sample Certification Statement: Chief Financial Officer Office of Financial Management Attn: Accounting Management Group, C3-13-08 Centers for Medicare & Medicaid Services 7500 Security Boulevard Baltimore, MD 21244-1850 Dear Chief Financial Officer: As the (Chief Financial Officer and Vice President of (contractor name), we are writing to provide certification of reasonable assurance for the period October 1 through June 30 that (contractor name) internal controls are in compliance with the Federal Managers' Financial Integrity Act (FMFIA) and Chief Financial Officers (CFO) Act by incorporating internal control standards into our operations. We are also providing an unqualified [or qualified] statement of assurance that (contractor name) has effective internal controls over financial reporting in compliance with revised OMB Circular A-123, Appendix A [except for the SSAE 18 Section I finding(s) and/or material weakness(es) identified in the attached Report of Material Weaknesses]. We are cognizant of the importance of internal controls. We have taken the necessary actions to assure that an evaluation of the system of internal controls and the inherent risks have been conducted and documented in a conscientious and thorough manner. Accordingly, we have included an assessment and testing of the programmatic, administrative, and financial controls for the (type of program) operations. In the enclosures to this letter, we have provided an executive summary that identifies a list of the minimum requirements. (See Section 30.3 - Executive Summary for the list of minimum requirements to be provided in your CPIC.) If material weaknesses have been identified, use the following language: "Material weaknesses have been reported to you and the appropriate Innovation & Financial Management (IFM) office, and/or COR. The respective Corrective Action Plans have been forwarded to your office." If no material weaknesses were identified, use the following language: "No material weaknesses have been identified during our review; therefore no material weaknesses have been reported." We have included a description of our risk assessment analysis and our CPIC Report of Material Weaknesses. This letter and attachments summarize the results of our review. We also understand that officials from the Centers for Medicare & Medicaid Services, Office of Inspector General, Government Accountability Office, or any other appropriate Government agency have authority to request and review the working papers from our evaluation. Sincerely,

______________________________________ [Chief Financial Officer Signature] ______________________________________ [Vice President for (type of program) Signature]