Embed Size (px)

Citation preview

Approaching Destination

Approaching waters

Our Vision 03

Year at a Glance 05

Board of Directors 07

Chairman’s Letter to the Shareholders 09

Business Segments 11

Directors' Report 13

Corporate Governance Report 21

Management Discussion & Analysis Report 35

Auditors' Report 43

The Financials

Balance Sheet 46

Profit & Loss Account 47

Cash Flow Statement 48

Schedules 49

Consolidated Financials 79

Financial Data Analysis 99

CONTENTS

Seeing Beyond Boundaries

Seeking Horizon

OUR CORE VALUES

OUR CORE PURPOSE

OUR GOAL

Honouring Commitments towards all the stake holders.

Consistent growth.

Ensuring that every employee feels pride in being called a

“Mercatorian”.

Innovation... We believe in doing things differently.

Giving the best solutions and offering outstanding value

and service to our customers.

To become a dominant player in the international shipping

and offshore

OUR VISION

ANNUAL REPORT 2007-2008

2

Fostering Teamwork

Forcing Migration ON BOARD

Mr. H. K. Mittal - Executive Chairman

Mr. Atul J. Agarwal - Managing Director

Mr. Manohar Bidaye - Director

Mr. H. K. Mittal, aged 58 years, the Executive Chairman of the

company. Having received masters from Indian Institute of

Technology (IIT), Roorkee; he started his tryst with enterprise

by forming a proprietorship firm; way back 1975, which was

later converted into a limited company. This Company was

primarily into the manufacturing of Sulphuric Acid and

Ferric Alum. Expansion of businesses both vertically and horizontally; soon became his

passion that still continues to be a major driving force backed up by more than three

decades of entrepreneurial experience.

Mr. Mittal acquired Mercator Lines Ltd. in 1988 and with his vision and keen insight has

brought the Company to where it is today.

Mr. Atul J. Agarwal, aged 50 years, the Managing Director of

the Company, is a Chartered Accountant, with 27 years of

professional experience. He has been associated with the

Company since its inception.

As a Chartered Accountant, Mr. Agarwal specializes in the

financial aspects of business. He looks after day - to - day

management and financial matters of the Company. He also has a strong expertise in

financial and strategic planning and execution. Mr. Agarwal has been accredited with

memberships of various committees formed by the Government for shipping reforms.

He has been instrumental in the successful implementation of many of the

Company's projects.

He is also member of the Board of Trustees of Mumbai Port Trust and is on the Board of

Directors of various organizations such as Indian National Ship-owners' Association

(INSA); Thirumalai Chemicals Ltd., and Mercator Healthcare Ltd.

Mr. Manohar Bidaye, aged 45 years, has Masters in

Commerce (M.Com) from the University of Mumbai, and has

a general Degree in Law (LLB - Gen.). He is also an Associate

Member of The Institute of Company Secretaries of India

(ACS).

He has been a practicing Company Secretary since 1989 and

has a broad based experience in corporate advisory and counseling. He also brings

expertise in corporate and taxation laws to the board.

Mr. Bidaye is the Promoter and Chairman of Zicom Electronic Security Systems Limited,

where he's involved with the overall Corporate Planning, Strategy and

Implementation, Financial Management, Banking, Accounts, Taxation and Legal

aspects.

He joined the board of Mercator Lines Limited in May 1994.

Mr. Anil Khanna - Director

Mr. M. G. Ramkrishna - Director

Mr. K. R. Bharat - Director

Mr. Anil Khanna aged 49 years, a

Fellow Chartered Accountant, is a

practicing professional specializing

in business management, joint

ventures and auditing. He has been

on the Board of Directors of several

Indian and multinational companies. Mr. Khanna has over 10

years of experience in consultancy.

He joined Mercator Lines Limited in May 1994.

M. G. Ramkrishna, aged 64 years, an

M. A., L. L. B. & CAIIB, has over 35 years

of experience in handling treasury,

financial and banking matters.

During the span of his service, he has

worked with reputed national and

international Companies and banks, in various capacities and

is on the Board of many companies.

He joined Mercator Lines Limited in January 2003.

Mr. K. R. Bharat, aged 46 years is MBA

f r o m I n d i a n I n s t i t u t e o f

Management . He has been

associated with Capital Market for

more than 25 years in various

segments like Merchant Banking,

Equities and Investment banking; Risk Management, research

etc. He is on the Board of many companies. He worked as

Managing Director at Credit Suisse First Boston Securities

(CSFB) India and Pregrine Securities (India). Before that he had

a successful stint of 10 yrs with Citi Bank. He was also member

of Market Advisory Committee of Bombay Stock Exchange.

He joined Mercator Lines Limited in July 2007

ANNUAL REPORT 2007-2008

6

Instilling Stability

Installing Anchor

Dear Shareholders,

At the outset; it has been yet another eventful year at

Mercator; fast tracking growth and sustain ability by exigent

expansions and prudent diversifications. Your company

undertook expansion to broad base offerings to the

customers; and diversification to take on newer opportunities

on the horizon.

May I share with you the firsts, Mercator embarked upon this year. Your company forayed into Dredging – another highly promising sector;

and integrated backwards by diversifying into coal mining. Opportunities in these areas are infinite; will ensure growth over medium to

even long term. The offshore segment appears firmer, having employed one jack-up rig already.

In shipping segment, the fleet expansion continued this year as well keeping the tradition of growth. Our consolidated capacity increased

by 15% to 2.34 Million DWT. In addition to the capacity; the type and age of vessels were once again rationalized to improve market access.

Your company demonstrated a solid all round performance; top line growth being 39% and bottom line grew by about 196%.

Mercator Lines (Singapore) Ltd – the Singapore based subsidiary got listed on main board of Singapore Stock Exchange successfully this

year after maiden IPO, raising USD 143 million. It is already the second largest shipping company in Singapore now; obviously the numbers

are simply indicative.

Our customer base has been growing continually. Several names of international repute find mention on our order books; such as Arcelor

Mittal; Cosco and Petronas to name but a few.

Your company continued its pursuit to continually improve and remain a world class organization by recognizing human capital as its real

assets. A holistic and systemic approach has been taken to spearhead sustainability initiatives towards ensuring safety, quality, our

responsibility towards environment and society at large.

We shall continue to endeavor, in all possible ways, to constantly and consistently return long term value to you, our shareholders. We truly

realize the enormity of responsibility arising out of your unwavering support and confidence bestowed on us. We are sure of the path and

the direction your company is headed towards.

Thank You,

Yours sincerely,

H. K. Mittal

Mumbai June 29, 2007

ANNUAL REPORT 2007-2008

8

Unearthing Opportunities

Exploring Natural

Resources

BUSINESS SEGMENTS

ANNUAL REPORT 2007-2008

10

SHIPPING

u

u

u

u

u

u

u

u

u

u

OFFSHORE

u

u

LOGISTIC SOLUTIONS

u

MINING

u

Tankers (Wet Bulk)

Dry Bulk Carriers

Dredgers

VLCC's

Suezmax

Aframax

Product Carriers

Chemical Carriers

Panamax – Geared

Panamx – Geareless

Post Panamax

Kamsarmax

Trailer Hopper Suction Dredgers (THSD's)

Premium Jack-Up Rigs

Oil and Gas Exploration

Coal Handling

Coal Mining

Sustaining GrowthSustaining Growth

Sustaining Energy

DIRECTORS’ REPORT

To

The Members,

Mercator Lines Limited

thWe take great pleasure in presenting the 24

annual report of your Company for the year ended

on March 31, 2008.

ANNUAL REPORT 2007-2008

12

FINANCIAL HIGHLIGHTS:

Particulars Year ended

31.03.2007

Standalone

Year ended

31.03.2008

Standalone

Year ended

31.03.2008

Consolidated

Year ended

31.03.2007

Consolidated

Income from operations

Total Income

Operating Profit

Interest

Depreciation

Profit before Tax & Minority Interest

Minority Interest

Taxes

-Current Year

-Fringe Benefit Tax

Net Profit After Tax & Minority Interest

Balance brought forward from last year

Prior Period Adjustments

Short provision for tax of earlier years

Profit available for appropriations:

Less: Appropriations:

Transfers to Reserves

-Tonnage Tax Reserve

-General Reserve

Interim Dividend on Preference shares

Dividend on Equity Shares of previous yr

Provision for final Dividend on Equity

Shares

Tax on Dividend

Balance carried to Balance Sheet

1,122.76

1142.69

322.91

80.77

103.80

138.34

(0.08)

(3.27)

(0.13)

134.86

150.99

(0.43)

Nil

285.42

16.00

7.50

3.20

Nil

18.92

3.67

236.13

781.14

863.07

339.14

58.56

103.83

176.75

N.A.

(7.70)

(0.21)

168.84

153.06

(1.20)

(1.30)

319.41

33.00

17.70

3.08

0.80

25.84

5.05

233.94

1454.87

1588.98

721.48

144.64

167.49

409.35

(29.89)

(8.81)

(0.21)

370.44

236.13

(41.49)

(1.30)

563.79

33.00

17.70

3.08

0.80

25.84

5.05

478.32

783.26

801.15

235.78

63.38

97.54

74.86

N.A.

(3.10)

(0.13)

71.63

131.15

(0.43)

Nil

202.35

16.00

7.50

3.20

Nil

18.92

3.67

153.06

Amount Rs. in Crores

ANNUAL REPORT 2007-2008

13

contracted to acquire one more dredger at a cost of about Rs.

57.60 crore which was proposed to be financed through mix of

internal accruals and debt. The Company through its subsidiary

Mercator Lines (Singapore) Ltd. (MLS), acquired five Kamsarmax

vessels; thereby adding a total tonnage of 387,265 MT, during the

year under review. The total cost of acquisitions was Rs. 1048.26

crores which was financed by a mix of internal accruals and debt.

Subsequent to the year end, MLS also contracted to acquire two

Panamax vessels of 1,38,442 DWT in aggregate, at a cost of about

Rs. 522 crores, equivalent to USD 131 million. These are proposed

to be financed by its IPO proceeds.

In December 2007, MLS successfully concluded its maiden IPO for

an amount of about Rs. 568.56 crores, which is equivalent of USD

142.80 million. MLS also issued shares arising upon conversion of

FCCB Series A of USD 35mn which is about Rs. 139 crores (together

with an interest amount of USD 4mn (about Rs. 16 crores ) accrued

thereon) as per the terms of the issue. The shares of this subsidiary

are listed on the main board of the Singapore Stock Exchange.

With a foray into dredging during the year, your Company has

added one more segment under its fold in addition to its existing

range of segments of Bulk Carriers, Tankers and Offshore.

The global demand for commodities still continues to be mainly

driven by India and China. India expects the rate of growth to be

around 8-9% per annum. With a consolidation in double hulls

taking place at faster pace; the tanker market is expected to

remain firm in near future.

All major Indian ports are presently working at 100% capacity,

whereas India further expects 8 to 9% growth rate. This would

translate into a meteoric rise in seaborne trade from current levels

of about 400mn tons to 900mn tones by the year 2013. The Indian

Government plans to develop new ports, as well as deepen the

existing ports to absorb additional requirements. In addition to

this is the “Sethusamduram” project that promises to provide

tremendous opportunities in dredging.

In the offshore services; the delivery of the jack-up rig is expected

as scheduled during the quarter of Jan-March 2009. Subsequent

to the year end; this rig has been contracted for deployment with

effect from date of its delivery. With the demand overhang from

the year 2008; the business prospects of further acquisitions and

the deployment of rigs appears good. Your Company is also

equipped to take up Exploration and Production (E&P) activities in

the Oil & Gas sector. With forthcoming NELP VII by the Government

of India; your Company foresees good opportunities in this sector

too.

BUSINESS OPERATIONS & FUTURE OUTLOOK:

The consolidated turnover for the year under review was

significantly higher at Rs. 1588.98 crores as against Rs. 1142.69

crores in the previous year; registering a substantial growth of

39%. The operating profit for the year of Rs. 721.48 crores was

higher by 123% over previous year of Rs. 322.91 crores.

Inspite of 79% higher interest costs amounting to Rs. 144.64 crores

(previous year Rs. 80.77 crores); and 61% higher depreciation to the

tune of Rs. 167.49 crores (The previous year Rs. 103.80 crores). The

Profit Before Tax (PBT) almost tripled this year; precisely an increase

of 196% to Rs. 409.35 crores as against Rs. 138.34 crores in the

previous year. Profit After Tax (PAT) also grew correspondingly by

197% to Rs. 400.33 crores as against Rs. 134.93 crores for the

previous year in spite of the higher tax outgo of Rs. 9.02 crores

against Rs. 3.41 crores in the previous year; increase of 165%. After

providing for the minority interest of Rs. 29.89 crores (Rs. 0.08 crore,

previous year) the net profit was recorded at Rs. 370.44 crores

(Rs. 134.86 crore); an increase of 175%.

The key driver of this exciting consolidated performance of the

Company was timely expansion of the fleet, culminating in

achievement of 99% fleet utilization.

On a standalone basis, the turnover of the Company for the year

under review was Rs. 863.07 crores as against Rs. 801.15 crores in

the previous year, registering a growth of 8% for the year. The

operating profit for the year under review at Rs. 339.14 crores was

higher by 44% as against Rs. 235.78 crores of the previous year. The

Profit Before Tax increased by 136% to Rs. 176.75 crores as against

Rs. 74.86 crores in the previous year. Profit after Tax also grew by

136% to Rs. 168.84 crores as against Rs. 71.63 crores for the

previous year. Better utilization of the fleet and the profits due to

sale of vessels have contributed to register a remarkable growth in

the bottom line of the Company.

A few more feathers to our cap were added this year too.

Mr. H. K. Mittal, the Executive Chairman of the Company was

awarded the “Newsmaker of the Year 2007” by Lloyd's List Middle

East and India Subcontinent and “Outstanding Achievement

Innovation” by Shipping & Marine Leadership & Excellence Awards

2008.

During the year under review, the Company continued its

expansion-cum diversification drive, and forayed into Dredging by

acquiring three dredgers of 24,153 DWT at a total cost of about Rs.

240.23cr. Two of these dredgers were financed by internal accruals

and one with a mix of internal accruals and financial assistance

from the banks. Subsequent to the year end, the Company

AWARDS AND RECOGNITIONS

EXPANSION AND FINANCE

ANNUAL REPORT 2007-2008

14

Being one of the largest carriers of coal into the country; one of the

strategic fit was to integrate the company backwards. Your

company has therefore, forayed into coal mining through its

subsidiaries. Two coal licenses in Indonesia and one in

Mozambique have already been granted to the said subsidiaries.

Both the projects are progressing well in terms of timelines and

operational milestones. The company expects revenues from

these projects in the current year.

In view of the global trade in commodities continuing to be

growing at a higher rate, the future outlook of industry in general,

and that for your Company in particular, appears to be bright,

barring unforeseen circumstances.

During the year, the Company allotted 3,76,52,887 equity shares of

Rs. 1/- each on the conversion of 5,150 FCCB's of an aggregate

amount of USD 51,500,000 at a price of Rs. 59/812 per share at a

fixed exchange rate of Rs. 43/73 per USD. The Company also issued

and allotted 32,00,000 equity shares of Re. 1/- each at a price of Rs.

137/50 along with the entitlement of 48,00,000 equity shares as

bonus shares to the promoter's group Company in exchange of

warrants allotted to them, pursuant to the resolution passed by

the shareholders of the Company at their EOGM held on January 17,

2006. Subsequent to the year end, further 10,96,686 equity shares

of Re. 1/- each were issued and allotted in lieu of surrender of 150

FCCB for conversion out of the abovementioned FCCB issue.

Further during the year 285,00,000 warrants carrying an option to

apply and subscribe for an equivalent number of shares at a price

not less than Rs. 58/50 per share to one of promoters on

preferential basis in accordance with SEBI Guidelines pursuant to

the resolution passed by shareholders of the Company at their

EOGM held on October 11, 2007.

During the last quarter of the financial year; the Company

redeemed its 8% Preference Share capital aggregating Rs. 40

crores on maturity.

The Board of Directors are pleased to recommend a 110% dividend

i.e. Rs. 1.10 per equity share of Re. 1/- each for the financial year

2007-08 on the enlarged capital base post issue of shares on

conversion of FCCBs; for your approval. The previous year total

dividend was 100% i.e. Re.1 per share aggregating Rs. 19.72 crores

on 19,72,42,500 shares. The aggregate amount of the dividend on

equity shares for the financial year 2007-08 would be Rs. 30.23

crores including corporate tax & surcharge thereon (as against Rs.

22.14 crores in the previous year). The dividend pay out has

therefore increased significantly in absolute value i.e. by 37%.

SHARE CAPITAL:

DIVIDEND:

Further during the year; the Directors declared and paid pro-rata

dividend of 8% on the Redeemable Cumulative Preference shares

of Rs. 4000 lacs, amounting to Rs. 3.60 crores (as against the

previous year at Rs. 3.65 crores) inclusive of the Corporate Tax &

surcharge thereon amounting to Rs. 0.52 crore (as against Rs. 0.45

crore in the previous year).

In accordance with the provisions of the Companies Act, 1956 and

the Articles of Association of the Company, Anil Khanna is the

Director liable to retire by rotation at the ensuing Annual General

Meeting and being eligible, has offered himself for re-

appointment. The brief resume of Anil Khanna is included under

the Corporate Governance section of this report.

Your Directors recommend for your approval the re-appointment

of Anil Khanna at the ensuing Annual General Meeting.

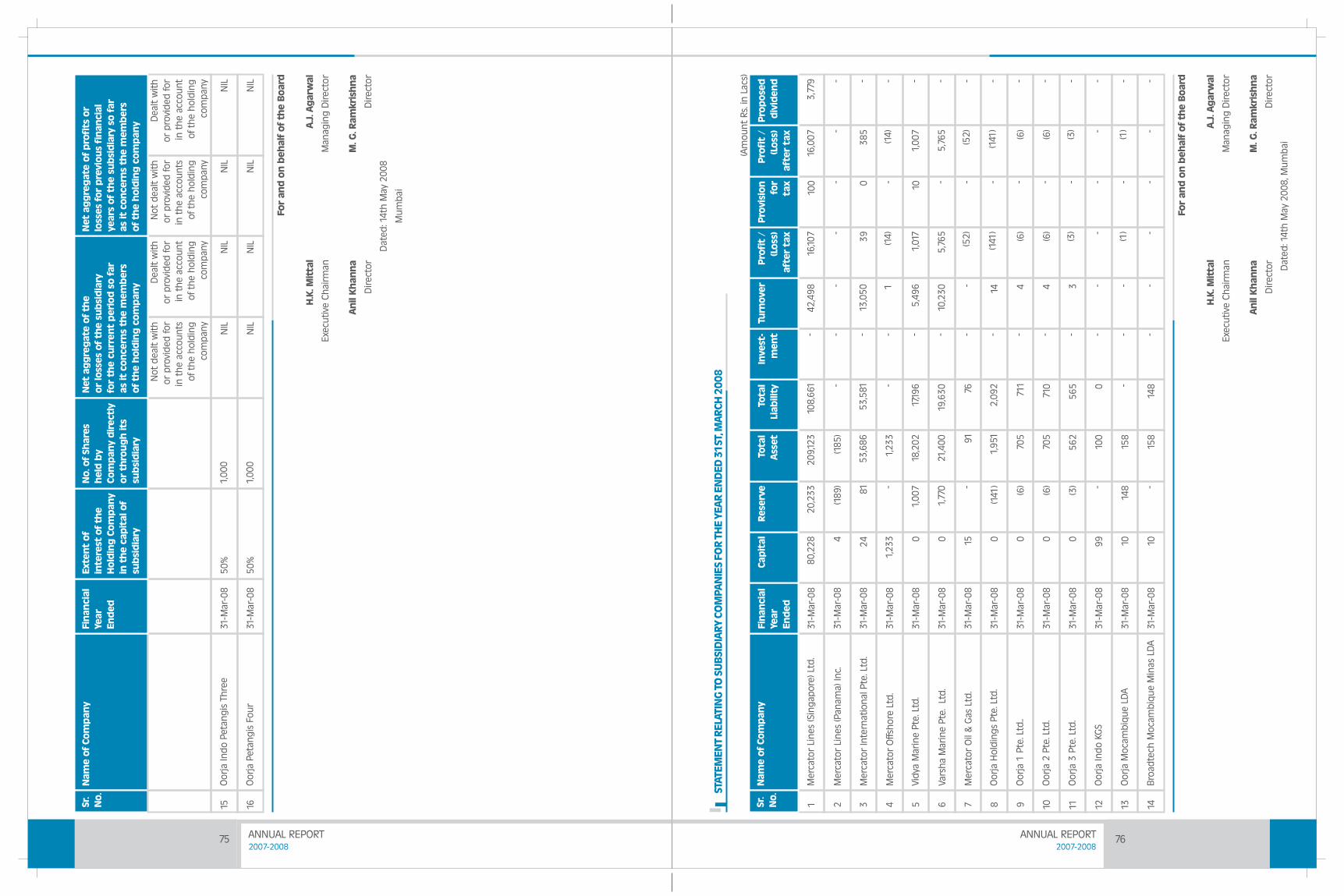

Your company has following subsidiaries/fellow subsidiaries:

DIRECTORS:

SUBSIDIARY COMPANIES:

Sl No. Name Country of

Incorporation

Mercator International Pte. Ltd. Singapore

Singapore

Singapore

Singapore

Singapore

Singapore

Singapore

Singapore

Singapore

Mercator Offshore Ltd.

Mercator Lines (Singapore) Ltd.

Varsha Marine Pte. Ltd.

Vidya Marine Pte. Ltd.

Mercator Lines (Panama) Inc.

Mercator Oil & Gas Ltd.

Oorja Holdings Pte. Ltd.

Oorja 1 Pte. Ltd.

Oorja 2 Pte. Ltd.

Oorja 3 Pte. Ltd.

Oorja Indo KGS.

Oorja Mozambique Lda.

Broadtec Mozambique Minas Lda.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

Panama

India

Indonesia

Mocambique

Mocambique

Pursuant to Accounting Standard (AS 21) issued by the Institute of

Chartered Accountants of India, consolidated financial statements

presented by the Company include financial information of its

subsidiaries.

ANNUAL REPORT 2007-2008

15

Your Company has not imported any technology during the year. It

has earned foreign exchange of Rs. 269.00 crores (as against the

previous year earnings of Rs. 201.73 crores) and spent Rs. 602.12

crores (as against Rs. 751.75 crores for the previous year) in foreign

exchange on account of acquisition of vessels, charter hire & other

vessel expenses and interest etc.

Your Company complies with the provisions laid down in

Corporate Governance laws. It believes in and practices good

corporate governance. Mercator maintains transparency, creates

value and wealth for its shareholders and also enhances corporate

accountability.

A separate report on the Corporate Governance, along with the

requisite certificate from the Auditors of the Company is annexed

herewith as part of this Annual Report.

Your company is a responsible corporate citizen, both in letter and

in spirit. Mercator therefore is always keen to discharge its social

responsibility towards the society it operates within. The company

has several such initiatives; mainly focused on education sector.

Your company has increased its amount of donations by about 9%

during the year to Rs. 32 lacs.

All properties of the Company are adequately insured.

Pursuant to the provisions of section 217(2AA) of the Companies

Act, 1956, the Directors hereby confirm that:

(I) In preparation of the annual accounts, the applicable

accounting standards have been followed along with proper

explanation relating to material departures;

(ii) They have selected such accounting policies and applied

them consistently and made judgments and estimates that

are reasonable and prudent, so as to give a true and fair view

of the state of affairs of the Company at the end of the

financial year and of the profit for the year under review;

CORPORATE GOVERNANCE:

OUR SOCIAL RESPONSIBILITY:

INSURANCE:

DIRECTORS' RESPONSIBILITY STATEMENT:

A statement in respect of the said subsidiaries pursuant to Section

212 of the Companies Act, 1956 is enclosed herewith as required.

The Company has received an exemption from the Government of

India u/s 212(8) of the Companies Act 1956 from attachment of the

documents of above subsidiaries for the year ended on March 31,

2008. The annual reports and accounts of subsidiaries will be kept

for inspection at the registered office of the Company and also of

the subsidiary companies concerned; and the same along with

related detailed information will be made available to the

investors of the Company, as well as, subsidiaries at any point of

time. Investors desirous of obtaining annual accounts of the

Company's subsidiaries may obtain the same on request.

The Auditors of your Company, M/s. Contractor, Nayak &

Kishnadwala, Chartered Accountants, retire at the ensuing Annual

General Meeting and have confirmed their eligibility for re-

appointment under Section 224 (1-B) of the Companies Act, 1956.

The Directors recommend their re-appointment for approval of

the members.

At Mercator, we believe that our employees are our partners in our

success and hence our partners in rewards. It is nothing but their

dedication, hard work and inimitable team spirit that has enabled

the Company to achieve new milestones in business.

As required under provisions of Section 217(2A) of the Companies

Act, 1956, read with the Companies (Particulars of Employees)

Rules 1975 as amended, the requisite particulars in respect of the

employees of the Company, who were in receipt of remuneration

in excess of the limits specified under the said section are set out in

the annexure forming part of this report.

The Conservation of Energy and Technology Absorption under the

Companies (Disclosure of Particulars in the Report of the Board of

Directors) Rules, 1988 are not applicable to your Company. All the

same, the Directors would like to assure you that every measure is

taken to save and conserve energy at all the stages of our

operation of the vessels, as well as, in our shore activities.

In its endeavor of the development of the export market, the

Company has formed new subsidiaries during the year.

AUDITORS:

PARTICULARS OF EMPLOYEES:

CONSERVATION OF ENERGY, TECHNOLOGY ABSORPTION;

EXPORT MARKET DEVELOPMENT AND FOREIGN EXCHANGE

EARNINGS & OUTGO:

ANNUAL REPORT 2007-2008

16

(iii) They have taken proper and sufficient care for the

maintenance of adequate accounting records in accordance

with the provision of the Companies Act 1956, for

safeguarding the assets of the Company and for preventing

and detecting fraud and other irregularities;

(iv) They have prepared the annual accounts on a going concern

basis.

As required under clause 3(1) (e) of the Securities and Exchange

Board of India (Substantial Acquisition of Shares and Takeovers)

Regulations, 1997 persons constituting “Group” (within the

meaning as defined in the Monopolies and Restrictive Trade

Practices act, 1969) for the purpose of availing exemption from

applicability of the provisions of Regulation 10 to 12 of the aforesaid

Regulations, are given in the annexure B attached herewith and

forms part of this Annual Report.

GROUP FOR TRANSFER OF SHARES:INTERSE

ACKNOWLEDGMENTS:

The Directors' would like to take this opportunity to thank the

Ministry of Shipping, M/s. Transchart, the Directorate General of

Shipping and other statutory authorities for their continual

support and encouragement.

We would also like to express our gratitude towards our bankers;

all the stakeholders and employees for their unflinching support

and faith in the Company.

For and on behalf of the Board

H. K. MITTAL

Executive Chairman

Regd. Office:rd3 Floor, Mittal Tower,

B-wing, Nariman Point,

Mumbai - 400021

Dtd: May 14, 2008

ANNUAL REPORT 2007-2008

ANNEXURE - A TO THE DIRECTORS' REPORT

Information as per Section 217(2-A) of the Companies Act, 1956 read with Companies (Particulars of Employees) Rules, 1975 and forming

part of the Report of the Board of Directors for the year ended on March 31, 2008.

17

NOTES

1. The employment at 1& 2 above are on contractual basis. All others are on non-contractual basis.

2. Gross Remuneration includes salary, commission, reimbursement of medical expenses and all other monetary benefits.

3. None of the above is relative of any Director of the Company.

4. *indicates the employees employed for part of the financial year.

Name Nature Of

Duties

Gross

Remune-

ration

(Rs. In Lacs)

Qualification Experience

(Yrs.)

Date of

Commen-

cement of

Employment

Age

Yrs.

Particulars of Previous

Employment

H. K. Mittal Executive

Chairman

800.29 M. Tech

(IIT - Roorkee)

32 Yrs Managing Director with

Natraj Organic Ltd for

17 Yrs.

59

Atul J.

Agarwal

Managing

Director

805.49 B. Com, F.C.A. 27 Yrs 01/01/1990

01/01/1990

Proprietor of A.J Agarwal &

Co. Chartered Accountant

for 7 Yrs

49

Atul M.

Malhotra

General Manager

- Logistic

34.45 B. Com 14 Yrs 22/09/1996 35

Kowshik

Kuchroo

Vice President -

Strategy

39.90 HND (Nautical

Science) MICS

14 Yrs 43

T. V.

Shanbhag

Advisor- Shipping 34.91 MA (Economics),

F.I.C.S (London),

A.I.I.I.

36 Yrs 18/04/2005 Chief Controller of

Chartering GOI for 10 Yrs

61

F. X. Chacko* Marine

Superintendent

22.44 B. Sc, Master -

Foreign Going

40 Yrs 11/01/2006 K Steamship Agencies Ltd.

for 2 years

53

Valentine

Dias*

Marine

Superintendent

8.52 Master - Foreign

Going

26 Yrs 01/02/2006 Wallem Ship Management

Hongkong for 7 Yrs

44

Ranjan

Agarawal

C.E.O.- Oil and

Gas

42.28 B. Tech (Chemical

Engg.) PGDBM

24 Yrs 10/07/2006 Reliance Industries Ltd for

2.5 Yrs

47

S. M. Rai Technical Head 29.46 B. E. 40 Yrs 16/08/2006 Shipping Corporation of

India for 37 years

61

Arun Nanda Vice President -

Tankers

Operations

42.07 Master - Foreign

Going

35 Yrs 28/08/2006 Marshall Produce Ship

Brokers, Mumbai for

6 Months

53

Joshua

Kandula

Vice President -

Offshore

69.46 B. Tec (Electrical)

MBA - IIMS

24 Yrs 21/08/2006 The Great Eastern Shipping

Co of India for 9 Yrs

48

Nitin

Kolhatkar*

Vice President -

Finance and

Accounts

22.86 M. Com, AICWA 19 Yrs 06/08/2007 United Phosphorous Ltd

for 14 years

44

Madhusudhan

Thayi*

General Manager

- Dredging

Operation

6.34 B. E (Civil) 30 yrs. 01/12/2007 Dredging Corporation of

India for 29 years

51

K. S. Raheja General Manager

- Projects

5.61 B. Tech (IIT), MBA

(XLRI)

03/01/2007 Tata Steel for 13 years 38

Jayesh Doshi* Chief Financial

Officer

8.56 F. C. A.; L.L.B 13/06/2006 Gujarat Ambuja Cement

Ltd. for 15 years

43

Mundo Gas for 7 Years01/04/2005

NA

21 yrs.

14 yrs.

ANNUAL REPORT 2007-2008

18

ANNEXURE – B TO THE DIRECTORS' REPORT

For the purpose of transfer of shares under Regulation 3 (1) (e) of the Securities and Exchange board of India

(Substantial Acquisition of Shares and Takeovers) Regulations, 1997, the following person constitute “Group” as defined in the

Monopolistic & Restrictive Trade Practices, 1969, (54 of 1969):

1. Mercator Healthcare Ltd.

2. MLL Logistics Pvt. Ltd.

3. AHM Investments Pvt. Ltd.

4. Mercator Mechmarine Ltd.

5. Ankur Fertilizers Pvt. Ltd.

6. Rishi Holdings Pvt. Ltd.

7. AAAM Properties Private Ltd.

8. Mercator International Pte. Ltd.

9. Mercator Offshore Ltd.

10. Mercator Oil & Gas Ltd.

11. Mercator Petroleum Pvt. Ltd.

12. Mercator Lines (Singapore) Ltd.

13. Mercator Lines (Panama) Inc

14. Varsha Marine Pte. Ltd.

15. Vidya Marine Pte. Ltd.

16. Oorja Holdings Pte. Ltd.

17. Oorja 1 Pte. Ltd.

18. Oorja 2 Pte. Ltd.

19. Oorja 3 Pte. Ltd.

20. Oorja Indo KGS

21. Oorja Mocambique Minas Limitada

22. Broadtec Mocambique Minas Limitada

23. Oorja Indo Pentangis Three

24. Oorja Indo Pentangis Four

25. H. K. Mittal

26. Archna Mittal

27. Atul J. Agarwal

28. Manjuli Agarwal

29. Shalabh Mittal

30. Shruti Mittal

31. Adip Mittal

32. Aayush Agarwal

33. Arooshi Agarwal

inter se

Building Future

Cultivating Industry

COMPANY'S PHILOSOPHY:

I. BOARD OF DIRECTORS:

The Company strongly believes in ethical way of

conducting business. The Company upholds its

relationship with the society and hence its social

responsibility of environmental safety and human

welfare.

Corporate governance to us is not just a compliance

issue but central guiding principle for everything it

does. It’s a way of thinking, way of conducting business

and a way to steer the organization to take on

challenges for now and for the future.

The Company recognizes its responsibility towards its

shareholders and therefore constantly endeavors to

create and enhance shareholder's wealth and value

by implementing its business plans at appropriate

times and thus taking maximum advantage of

available opportunities to benefit the Company, its

shareholders and the society at large. The Company

believes in monitoring its performance regularly and

with utmost transparency to ensure ethical

governance at all levels within the organization.

The Board of Directors of the Company comprises of

six Directors with a combination of two Executive

Directors and four Non-executive Independent

Directors. Among the two Executive Directors one is

Executive Chairman and the other is Managing

Director. The Company is in compliance with the

requirement of at least half of the Board comprising of

Independent Directors as the Chairman of the Board

is an Executive Director.

None of the Independent Directors:

a. apart from receiving director's remuneration, does not have any

material pecuniary relationships or transactions with the

company, its promoters, its directors, its senior management or

its holding company, its subsidiaries and associates which may

affect independence of the director;

b. is not related to promoters or persons occupying management

positions at the board level or at one level below the board;

c. has not been an executive of the company in the immediately

preceding three financial years;

d. is not a partner or an executive or was not partner or an executive

during the preceding three years, of any of the following:

i) the statutory audit firm or the internal audit firm that is

associated with the company, and

ii) the legal firm(s) and consulting firm(s) that have a material

association with the company.

e. is not a material supplier, service provider or customer or a lessor

or lessee of the company, which may affect independence of the

director;

f. is not less than 21 years of age

g. is not a substantial shareholder of the company i.e. owning two

percent or more of the block of voting shares.

There is no Nominee Director on the Board of the Company.

REPORT ON CORPORATE

GOVERNANCE

(Forming part of Directors' report for the year stended on 31 March 2008)

ANNUAL REPORT 2007-2008

20

ANNUAL REPORT 2007-2008

21

No Director of the Company is either member in more than ten

committees and/or Chairman of more than five committees

across all Companies in which he is Director and necessary

disclosures to this effect has been received by the Company from

all the Directors.

During the year, in all Eight Board meetings were held i.e. on May

28, 2007; June 29, 2007; July 30, 2007, September 13, 2007;

October 24, 2007; December 26, 2007; January 28, 2008; and

March 13, 2008. The time gap between any two meetings was not

more than 4 months.

The details of Directors and their attendance record at Board

Meetings held during the year, at last Annual General Meeting and

number of other Directorships and Chairmanships/ membership

of Committees is given below:

Sr.

No.

Name of Director Category No. of Board

Meetings

Attended

Attendance

at last AGM

No. of other

Directorship

No. of

committee

membership

in other

Companies*

No. of

committee

Chairmanship

in other

Companies *

H. K. Mittal Chairman & Managing

Director-Executive-Promoter

8 Yes Nil1

2 A. J. Agarwal Joint Managing Director,

Executive-Promoter

8

8

Yes

3 Manohar Bidaye Non-Executive

Independent Director

5 Yes

4 Anil Khanna Non-Executive

Independent Director

Yes

5 M. G. Ramkrishna Non-Executive

Independent Director

Yes

5

7

6 K. R. Bharat Non-Executive

Independent Director

Yes

5

8

11

8

2

2

1

2

1

2

Nil

Nil

Nil

1

Nil

1

Nil

*In accordance with Clause 49 of the Listing Agreement, Memberships / Chairmanships of only the Audit Committees and Shareholders'/ Investors' Grievance Committees of all Public Limited Companies have been considered.

II. AUDIT COMMITTEE:

Composition:

Pursuant to the provisions of Section 292(A) of the Companies Act,

1956 and Clause 49 of the Listing Agreements, the Company has a

qualified and independent Audit Committee comprising of three

Independent Non-executive Directors. Anil Khanna, a senior

member of Institute of Chartered Accountants of India, having a

sound accounting and financial background, is the Chairman of

the Committee with the other members being Manohar Bidaye, a

senior member of Institute of Company Secretaries of India and M.

G. Ramkrishna, a veteran from the banking & finance industry. The

Managing Director, Head of Finance Department along with the

Internal Auditors and Statutory Auditors are always invitees to the

Audit Committee Meeting. All other Functional Managers are

invited to attend the meeting, as and when necessary. The

Committee is vested, inter alia, with following powers and terms of

references as prescribed under relevant provisions of the

Companies Act, 1956 and Stock Exchanges Listing Agreement:

None of the independent directors had resigned nor removed for

the Board of the Company during the year and hence compliance

in respect of replacement thereof did not arise.

All the information required to be furnished to the Board was

made available to them along with detailed agenda notes.

The Board reviews compliance reports of all laws applicable to the

Company, presented by Managing Director at the meeting.

Code of Conduct:

The Board has laid down a Code of Conduct for all Board members

and senior management personnel of the Company, which has

been posted on the website of the Company www.mercator.in

All Board members and senior management personnel have

affirmed compliance with the code for the year ended on March

31, 2008. Declaration to this effect signed by the Chief Executive

Officer for the year ended on March 31, 2008 has been included

elsewhere in this report.

ANNUAL REPORT 2007-2008

22

Powers:

a) To investigate any activity within its terms of reference.

b) To seek information from any employee.

c) To obtain outside legal or other professional advice.

d) To secure attendance of outsiders with relevant expertise, if it

considers necessary.

Terms of Reference:

The Audit committee reviews the reports of the Internal Auditors

and the Statutory Auditors periodically and discuss their findings

and suggest the corrective measures. The role of the Audit

Committee is as follows: -

1. Oversight of the company's financial reporting process and

the disclosure of its financial information to ensure that the

financial statement is correct, sufficient and credible.

2. Recommending to the Board, the appointment, re-

appointment and, if required, the replacement or removal of

the statutory auditor and the fixation of audit fees.

3. Approval of payment to statutory auditors for any other

services rendered by the statutory auditors.

4. Reviewing, with the management, the annual financial

statements before submission to the board for approval, with

particular reference to:

a. Matters required to be included in the Director's

Responsibility Statement to be included in the Board's

Report in terms of clause (2AA) of Section 217 of the

Companies Act, 1956.

b. Changes, if any, in accounting policies and practices and

reasons for the same.

c. Major accounting entries involving estimates based on

the exercise of judgment by the management.

d. Significant adjustments made in the financial statements

arising out of the audit findings.

e. Compliance with listing and other legal requirements

relating to financial statements.

f. Disclosure of any related party transactions.

g. Qualifications in the draft audit report.

5. Reviewing, with the management, the quarterly financial

statements before submission to the board for approval.

5A. Reviewing, with the management, the statement of uses /

application of funds raised through an issue (public issue,

rights issue, preferential issue, etc.), the statement of funds

utilized for purposes other than those stated in the offer

document/prospectus/notice and the report submitted by

the monitoring agency monitoring the utilisation of proceeds

of a public or rights issue, and making appropriate

recommendations to the Board to take up steps in this

matter.

6. Reviewing, with the management, performance of statutory

and internal auditors and adequacy of the internal control

systems.

7. Reviewing the adequacy of internal audit function, if any,

including the structure of the internal audit department,

staffing and seniority of the official heading the department,

reporting structure coverage and frequency of internal audit.

8. Discussion with internal auditors any significant findings and

follow up there on.

9. Reviewing the findings of any internal investigations by the

internal auditors into matters where there is suspected fraud

or irregularity or a failure of internal control systems of a

material nature and reporting the matter to the board.

10. Discussion with statutory auditors before the audit

commences, about the nature and scope of audit, as well as,

post-audit discussion to ascertain any area of concern.

11. To look into the reasons for substantial defaults in the

payment to the depositors, debenture holders, shareholders

(in case of non payment of declared dividends) and creditors.

12. To review the functioning of the Whistle Blower mechanism, in

case the same is existing.

13. Carrying out any other function as is mentioned in the terms

of reference of the Audit Committee.

Meetings:

During the year, in all five meetings of the Committee were held i.e.

on May 28, 2007; June 29, 2007; July 30, 2007; October 24, 2007

and January 28, 2008. The time interval between two meetings of

the Committee was not more than four months.

ANNUAL REPORT 2007-2008

23

ESPS COMMITTEE:

III. SUBSIDIARY COMPANIES:

The Company has Employee Stock Purchase Committee (ESPS) of

Directors comprising of two Executive Directors viz. H. K. Mittal & A.

J. Agarwal and three Non-executive Independent Directors viz.

Manohar Bidaye; Anil Khanna & M. G. Ramkrishna, to implement the

Employee Stock Purchase Scheme of the Company.

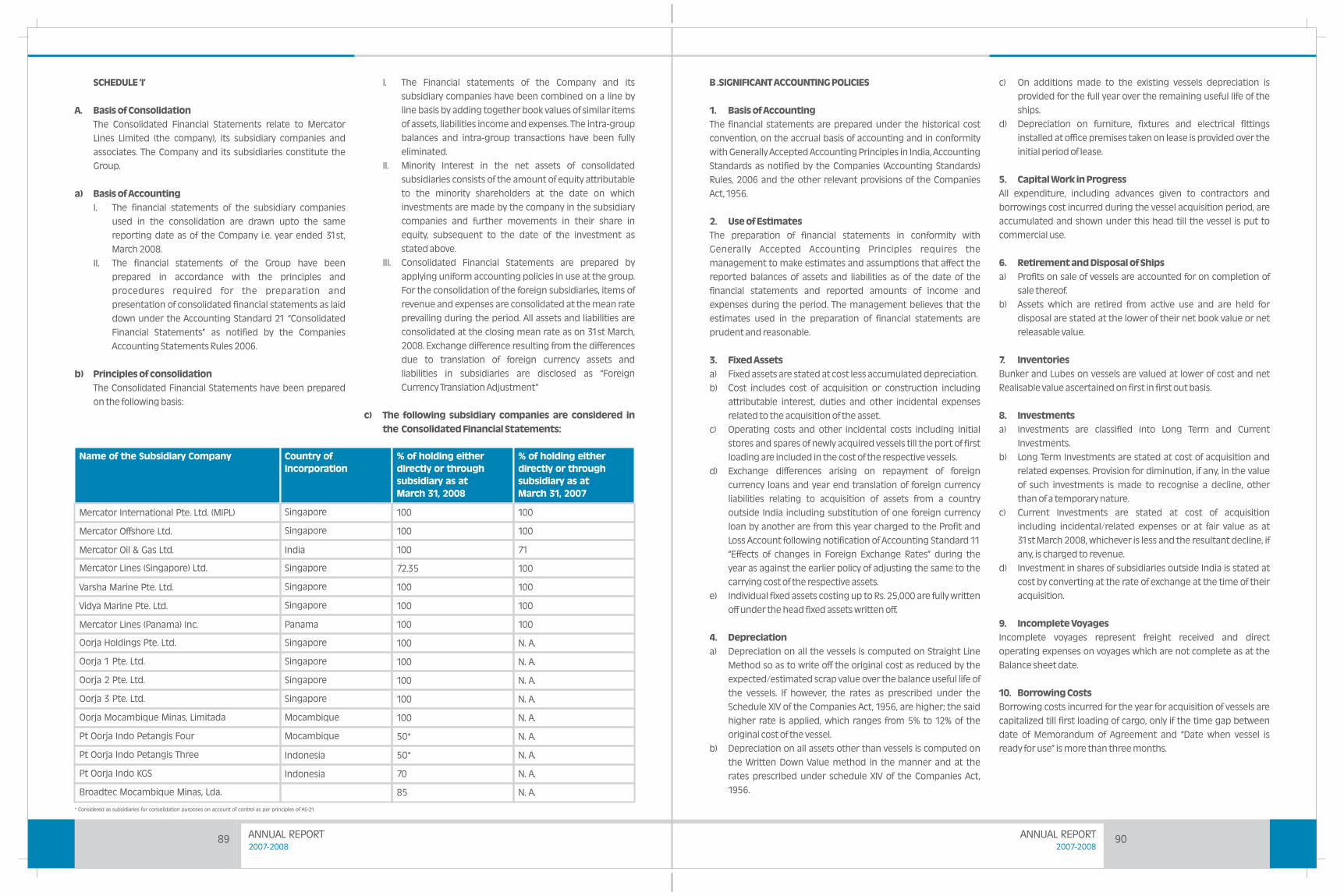

As at March 31, 2008 the Company had following subsidiaries:

No. of Audit Committee

Meetings attended

Name of Director

5

5

5

H. K. Mittal

Atul J. Agarwal

Anil Khanna

3K.R. Bharat

No. of Audit Committee

Meetings attended

Name of Director

5

4

5

Anil Khanna

Manohar Bidaye

M. G. Ramkrishna

The Managing Director, as a head of the Finance Department;

Statutory Auditors and Internal Auditors attended all the four

meetings. The Company Secretary acted as the Secretary to the

committee.

Review of Information:

The Audit committee was presented with and reviewed following

information:

1. Management discussion and analysis of financial condition

and results of operations;

2. Statement of significant related party transactions (as defined

by the audit committee), submitted by management.

3. Management letters/letters of internal control weaknesses

issued by the statutory auditors, if any.

4. Internal audit reports related to internal control weaknesses;

and

5. The appointment, removal and terms of remuneration of the

Internal Auditor. Presently the Company has independent

Chartered Accountant's firm as its Internal Auditor

There was no instance of management letter/letter of internal

control weaknesses issued by the Statutory Auditors during the

financial year 2007-08.

The Company has Expansion Committee comprising of two

Executive Directors viz. H. K. Mittal & A. J. Agarwal and two Non-

executive Independent Directors viz. Anil Khanna & K.R. Bharat. The

Committee is authorized to assess the business opportunities and

take the decisions from time to time on expansion projects; means

of finance and other related matters, within the limits sanctioned

by the Board. During the year five meetings were held.

Attendance of each member at the audit Committee Meetings:

EXPANSION COMMITTEE:

Sl

No.

Name

1

Incorporated

in

Mercator International

Pte. Ltd. (MIPL)

Remark

Singapore Wholly Owned

Subsidiary (WOS)

2 Mercator Offshore Ltd. Singapore Wholly Owned

Subsidiary

3 Mercator Oil & Gas Ltd. India Wholly Owned

Subsidiary

5 Varsha Marine Pte. Ltd. Singapore Step down

subsidiary

(WOS of MLS)

4 Mercator Lines

(Singapore) Ltd.(MLS)

Singapore Step down

Subsidiary

(Subsidiary of

MIPL with

71.35% holding)

6 Vidya Marine Pte. Ltd. Singapore Step down

subsidiary

(WOS of MLS)

7 Mercator Lines

(Panama) Inc

Panama Step down

subsidiary

(WOS of MLS)

8 Oorja Holdings Pte.

Ltd.(OHPL)

Singapore Step down

Subsidiary

(WOS of MIPL)

9 Oorja 1 Pte. Ltd. Singapore Step down

Subsidiary

(WOS of OHPL)

10 Oorja 2 Pte. Ltd. Singapore Step down

Subsidiary

(WOS of OHPL)

11 Oorja 3 Pte. Ltd. Singapore Step down

Subsidiary

(WOS of OHPL)

ANNUAL REPORT 2007-2008

24

12 Oorja Mocambique

Lda (OML)

Mocambique Step down

Subsidiary

(WOS of OHPL)

13 Broadtec Mocambique

Lda

Mocambique Step down

subsidiary

(Subsidiary of

OML with 85%

holding)

14 Oorja Indo KGS Indonesia Step down

subsidiary

(Subsidiary of

Oorja 3 wih 70%

holding)

Sl

No.

Name Incorporated

in

Remark

The Indian Subsidiary Mercator Oil & Gas Ltd., was neither listed nor

material as at March 31, 2008.

Mercator Lines (Singapore) Ltd., a then wholly owned subsidiary of

Mercator International Pte. Ltd., (MIPL) completed its IPO during

the year. Consequently, holding of MIPL reduced to 72.35%. The

shares of Mercator Lines (Singapore) Ltd. are listed on the main

Board of Singapore Stock Exchange.

Mercator Lines (Panama) Inc is dormant company.

Oorja 1 Pte. Ltd. has 50% joint venture Company Oorja Indo

Pentagis Four in Indonesia.

Oorja 2 Pte. Ltd. has 50% joint venture Company Oorja Indo

Pentagis Three in Indonesia

Subsequent to year end; Mercator Petroleum Private Ltd., was

taken over as 100%WOS by the Company.

The Audit Committee reviews the financial statements of all the

subsidiary companies including the investment made by the

Company.

The Minutes/resolutions of the Board Meetings of all the subsidiary

companies (including the step down subsidiary Companies) are

placed before the Board periodically.

The management periodically reviews a statement of all

significant transactions, if any, entered into by all the subsidiary

companies.

IV. DISCLOSURES:

(A) Basis of related party transactions:

i. A statement in summary form of transactions with related

parties in the ordinary course of business are placed

periodically before the audit committee.

ii. Details of material individual transaction with related parties,

which are not in the normal course of business, are placed

before the audit committee, whenever applicable.

iii. During the year, there was no material individual transaction

with related parties or others, which was not on an arm's

length basis.

(B) Disclosure of Accounting Treatment:

In the preparation of financial statements for the year ended on

March 31, 2008; there was no treatment different from that

prescribed in an accounting standard had been followed.

(C) Board Disclosures-Risk Management:

The Company has laid down procedures to inform Board members

about the risk assessment and minimization procedures. These

procedures are periodically reviewed to ensure that executive

management controls risk through means of properly defined

framework.

(D) Proceeds from public issues, rights issues, preferential

issues etc.

During the year, the Company raised an amount of Rs. 56.27 crores

through two separate preferential issues on private placement

basis, the uses/application of funds of which were disclosed to the

Audit Committee as a part of their quarterly declaration of

financial results. The funds were utilized for their intended

purposes as disclosed in the respective notices calling general

meeting seeking shareholders for such issues. All such disclosures

were duly certified by the statutory auditors.

(E) Remuneration cum Selection Committee &

Remuneration of Directors:

The Company has Remuneration Committee comprising of three

Non-executive Independent Directors. Manohar Bidaye is the

Chairman of the Committee with Anil Khanna and M. G.

Ramkrishna being other members. The committee, on behalf of

the Board and the shareholders, determines, with agreed terms of

reference, the Company's policy on specific remuneration

packages for Executive Directors and senior management people

including pension rights and any compensation payment.

ANNUAL REPORT 2007-2008

25

Non-executive Directors:

During the year, non-executive Directors were paid following

remuneration for the financial year 2007-08:

No other convertible instrument was held by any of the above

Non-executive Directors.

No stock options were issued to the Non-executive Directors

during the year.

Anil Khanna, the Non-Executive Director retiring by rotation at the

ensuing Annual General Meeting has declared his shareholding in

the Company and the same has been disclosed in the notice of the

Annual General Meeting.

(F) Management

A Management Discussion and Analysis report forming part of this

Directors' report is attached herewith.

During the year, there was no material financial and commercial

transaction by senior management that may have a potential

conflict with the interest of the Company at large.

The Board decided the payment of commission to Non-executive

directors within the limits approved by members of the Company

in their Annual General Meeting held on September 26, 2007.

Presently the Company pays remuneration to Non-executive

Directors by way of commission not exceeding 1% of its net profit

being distributed among themselves equally. No sitting fees are

being paid to non-executive Directors.

All the Non-executive Directors have disclosed their

shareholdings to the Company, which is as under:

Manohar Bidaye

Anil Khanna

M. G. Ramkrishna

Name No of equity shares held

as on 31/03/2008

K. R. Bharat

97,500

2,51,120

17,000

Nil

Name Commission

Amount Rs in Lacs

Manohar Bidaye

Anil Khanna

M. G. Ramkrishna

K. R. Bharat

2.50

2.50

2.50

2.50

The remuneration to the Executive Directors is governed by the

agreements executed with them as approved by the members of

the Company in their General Meeting. As per the agreement,

salary and perquisites are a fixed component and the commission

is based on the performance of the Company, i.e. on the net profit

of the year, calculated as per the provisions of the Companies Act,

1956. The present terms & conditions of appointment agreements

of both the Executive Directors were approved by the shareholders

at the Annual General Meeting of the Company held on September

26, 2007. As per the terms of respective agreements, the

appointments of Executive Chairman and Managing Director are

valid upto July 31, 2012 and can be terminated by either party by

giving six month's notice in writing. There is no severance fees

payable. The Executive Directors were not issued any Stock Options

during the year.

H. K. Mittal

Executive Chairman

Name Salary Commission Perquisites

A. J. Agarwal

Managing Director

Amount Rs in Lacs

48.00

48.00

746.25

746.25

6.04

11.24

This Committee also acts as a Remuneration Committee under

Schedule XIII and as Selection Committee under Section 314 of the

Companies Act, 1956.

Two meetings of Remuneration Committee were held during the

year. Except M.G. Ramkrishna, who attended one meeting; all other

members attended both the meetings.

The remuneration of non-executive Directors is decided by the

Board/Shareholders.

The Company did not have any pecuniary relationship or

transaction with the Non-executive Directors during the year

other than those disclosed elsewhere in this report. Except

commission on net profits for the year ended on March 31, 2008 as

fixed by the Board of Directors and approved by the shareholder's

resolution; no Non-Executive Director was paid any

fees/compensation.

Details of remuneration paid to Directors for the financial

year ended March 31, 2008:

Executive Directors:

ANNUAL REPORT 2007-2008

26

(G) Shareholders

Details of General Meetings held during last three years are given

below:

(i) GENERAL BODY MEETINGS:

No special resolution through postal ballot was passed last year nor proposed at the ensuing Annual General Meeting.

(ii) DISCLOSURES:

During the year, there were no transactions of materially

significant nature with the Promoters or Directors or the

Management or their subsidiaries or relatives etc. that had

potential conflict with the interest of the Company. However, the

transactions entered into with the related parties as per

Accounting Standard 18 are reported at Note No. 20 of Notes

forming part of the Accounts under Schedule I (B) annexed to the

Accounts for the year under review.

There were no instances of non-compliance on any matter related

to the capital market during the past three years and that no

penalties or strictures were imposed on the Company by any Stock

Exchange or SEBI.

Presently the Company does not have any Whistle Blower Policy.

Financial

Year

Date VenueTime Special Resolution(s)

11/10/20072007-08

(E.G.M)

Y. B. Chavan Centre,

General Jagannath Bhosle

Marg, Nariman Point,

Mumbai-400021

11.00 A.M. 1. Issue of warrants on preferential basis to

promoter.

31/07/20062006-07

(A.G.M.)

C. K. Nayudu Hall,

Brabourne Stadium,

Churchgate,

Mumbai-400020

12.00 Noon 1. Alteration of Object Clause of Memorandum

of Association.

2. Approval for commencing new business

activity set out in the object clause of

Memorandum of Association.

28/09/20052005-06

(A.G.M.)

C. K. Nayudu Hall,

Brabourne Stadium,

Churchgate,

4.00 P.M. 1. Approval to payment of sitting fees to

Non- Executive Directors.

2. Appointment of Whole-time Director

26/09/20072007-08

(A.G.M.)

Y. B. Chavan Centre,

General Jagannath Bhosle

Marg, Nariman Point,

Mumbai-400021

3.30 P.M. 1. Appointment of Mr. H. K. Mittal as

Executive Chairman of the Company and

remuneration thereof.

2. Appointment of Mr. A.J. Agarwal as

Managing Director of the Company and

remuneration thereof.

3. Appointment of Mr. Adip Mittal, a relative

of Director to hold the office or place

of profit of the Company.

4. Delisting of equity shares from Ahmedabad

Stock Exchange

17/01/20062005-06

(E.G.M.)

C. K. Nayudu Hall,

Brabourne Stadium,

Churchgate,

Mumbai-400020

4.30 P.M. 1. Increase in Authorised Share Capital and

amendments to the capital clauses of

Memorandum and Articles of Association

of the Company.

2. Issue of Bonus shares

3. Issue of warrants on preferential basis to

Promoter's group Company.

4. Increase in the limit of investments by FIIs

in the capital of the Company.

ANNUAL REPORT 2007-2008

29

Shareholding of nominal

value of

No. of

Shareholders

% to total

Shareholders

No. of Shares % to total Capital

UPTO 5000 60,093 97.59 2,49,93,106 10.64

5001 10000 627 1.02 47,66,971 2.03

10001 20000 397 0.64 56,05,668 2.38

10001 20000 397 0.64 56,05,668 2.38

20001 30000 158 0.26 39,42,353 1.68

30001 40000 63 0.10 22,06,319 0.94

40001 50000 41 0.07 18,83,606 0.80

50001 100000 84 0.13 60,07,575 2.56

100001 AND ABOVE 116 0.19 18,54,89,789 78.97

TOTAL 61,579 100.00 23,48,95,387 100.00

SHARE TRANSFER:

SHAREHOLDERS'/ INVESTORS' GRIEVANCES COMMITTEE:

The Company has Shareholders'/Investors' Grievances Committee

comprising of one Executive Director and two Non-executive

Directors to look after share transfer and other related matters,

including the shareholders' grievances. Manohar Bidaye, a senior

member of Institute of Company Secretaries of India, is the

Chairman of the Committee with the other members being, A. J.

Agarwal and Anil Khanna, both senior members of Institute of

Chartered Accountants of India. The Committee normally meets

fortnightly and looks into the shareholder & investor grievances

that are not settled at the level of the Company

Secretary/Compliance Officer and helps to expedite share

transfers & related matters.

Twenty three Meetings of the Committee were held during the

year. All the members attended all the meetings except one such

meeting by Manohar Bidaye.

Supriya Joshi, who was appointed as Company Secretary (under

the designation of Dy. Company Secretary) within the meaning of

the Companies Act, 1956 w.e.f. March 7, 2007 resigned w.e.f.

January 28, 2008. As at March 31, 2008, Deepak Dalvi, Manager

Secretarial was acting as Compliance officer. During the year, the

Company received 78 complaints from the shareholders and

which were duly resolved. Further, during the year requests for

transfer of 1,39,750 equity shares; and for demat of 87,30,547

equity shares were received and processed.

Registrar and Transfer Agents and Share Transfer System:

Intime Spectrum Registry Ltd., having their office at C-13, Pannalal

Silk Mills Compound, LBS Road, Bhandup (W), Mumbai - 400 078 (Tel

No.91-22-25963838) and branch office at 203, Dawer House,

197/199, D.N. Road, Mumbai - 400 001 (Tel No. 91-22-22694127) are

the Registrar and Transfer Agents (RTA) as also the registrar for

electronic connectivity. Entire functions of Share Registry, both for

physical transfer as well as dematerialisation/rematerialisation of

shares, issue of duplicate/split/consolidation of shares is being

carried out by the RTA at their above address.

The correspondence regarding query of dividends shall be

addressed to Compliance Officer at the registered office of the

Company.

(xiii)DISTRIBUTION OF SHAREHOLDING AS ON MARCH 31,

2008

0

Ap

ril 2007

Marc

h 2

008

Sh

are

Pri

ce (Ru

pees)

30

50

70

90

110

130

150

170

190

Feb

ruary

2008

Sep

tem

ber2

007

Oct

ob

er

2007

Nove

mb

er

2007

Dece

mb

er

2007

Jan

uary

2008

May

2007

Jun

e 2

007

July

2007

Au

gu

st 2

007

High

Low

ANNUAL REPORT 2007-2008

30

(xiv)SHAREHOLDING PATTERN AS ON MARCH 31, 2008:

Series No Category % to Capital No. of Holders

1 Promoters / Directors and their Relatives

Mutual Funds / UTI

38.11

12.13

10

38

No. of Shares

8,95,23,975

2,85,03,5322

Banks 0.47 211,12,8003

FIIs / Foreign Companies/foreign Banks 22.24 325,22,30,0224

Private Corporate Bodies 6.66 1,2771,56,35,1945

Indian Public 18.74 58,7294,40,23,2236

NRIs / OCBs 0.71 1,08116,69,7317

Non-promoter Independent Directors and their relatives 0.20 74,80,5958

Clearing members 0.73 40317,16,3159

Total 100.00 61,57923,48,95,387

(xv) DEMATERIALISATION OF SECURITIES:

The equity shares of the Company are under compulsory trading in de-mat form. Out of total capital of 23,48,95,387 equity shares;

23,03,69,303 equity shares representing 98.07% were held in de-mat form and balance 45,26,084 equity shares representing 1.93% were

in physical form as on March 31, 2008. The ISIN of the equity shares of the Company is INE934B01028.

The shares are actively traded on BSE and NSE and the turnover data during the financial year 2007-08; was as under:

Particulars

No of shares 24,35,37,639

228,611.85

29,13,43,341

284,112.88

53,49,00,980

512,724.73Value (Rs. In lacs)

BSE NSE Total

Promoters / Directors and

their Relatives - 38.11%

Mutual Funds /

UTI - 12.13%

Banks -

0.47%

FIIs / Foreign Companies /

foreign Banks - 22.24%

Private Corporate

Bodies - 6.66%

Indian Public - 18.74%

NRIs / OCBs -

0.71%

Non-promoter Independent

Directors and their

relatives - 0.2%

Clearing members - 0.73%

ANNUAL REPORT 2007-2008

31

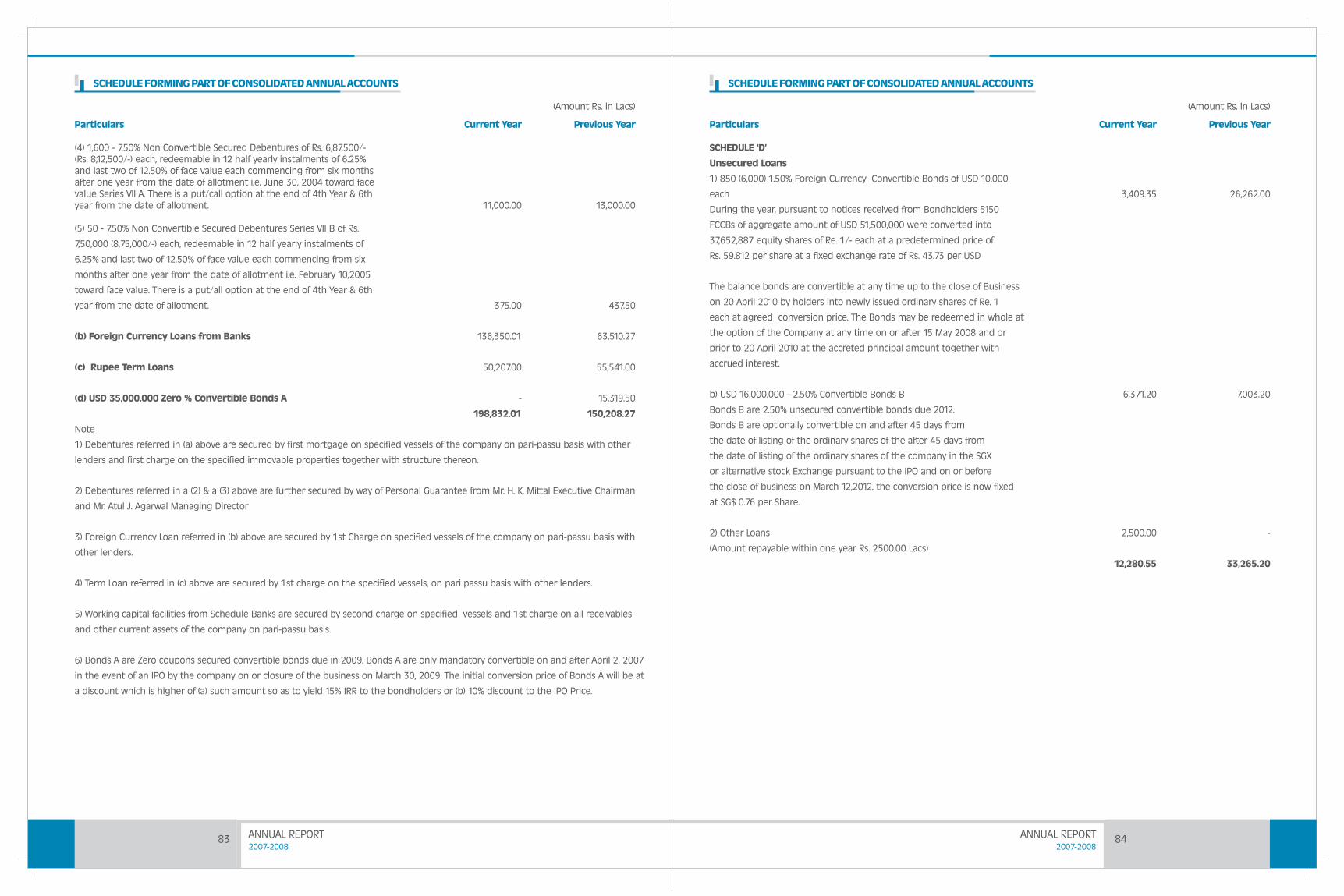

Series No No. of NCDs Coupon rate O/s. Face value

As on 31/03/08

Outstanding

Amount

ISIN

IV 30,00,000 10.00% Rs. 10/- each Rs. 3.00 crores INE934B07033

V 30,00,000 10.00% Rs. 20/- each Rs. 6.00 crores INE934B07041

VII-A 1600 7.50% Rs. 6,87,500/- each Rs. 110.00 crores INE934B07066

VII-B 50 7.50% Rs. 7,50,000/- each Rs. 3.75 crores INE934B07074

2,85,00,000 Warrants carrying an option to apply for equivalent

number of equity shares of Re. 1/- each in the Company; were

issued to a promoter on October 25, 2008, on preferential basis in

accordance with SEBI Guidelines on Preferential Issue, as approved

by shareholders in their meeting held on October 11, 2008; and the

same were outstanding as on March 31, 2008.

Further, out of 10,000 1.50% Foreign Currency Convertible Bonds of

USD 10,000 each aggregating USD 60 millions; 850 FCCBs of an

aggregate amount of USD 8.50 mn were outstanding as at March

31, 2008 consequent upon surrender of 9,150 FCCBs for conversion

by the Bondholders during the year. The conversion price of

the Bonds is fixed at Rs. 59.812 (ex-bonus) per share with a fixed

rate of exchange on conversion of Rs. 43.73= USD 1.00 with

maturity date as April 27, 2010.

Subsequent to year end, further 10,96,686 equity shares of Re. 1/-

each were issued and allotted in lieu of surrender of 150 FCCBs for

conversion out of the said issue. Consequently, there were 700

outstanding FCCBs of aggregate amount of USD 7 million.

If all the FCCB holders exercise their rights to convert FCCB into

equity shares then the paid up equity capital of the Company

would increase by 51,17,869 shares of Re. 1/- each.

'Mercator Lines (Singapore) Ltd', a step-down subsidiary of the

company, had issued Convertible Bonds aggregating USD 51

million, consisting of Bonds-A of USD 35 Million and Bonds-B of USD

16 Million, during last financial year. Consequent to the IPO by the

said subsidiary in the month of October 2007; Bonds-A were

converted into shares pursuant to the terms of the issue. However,

these conversion of bonds had no impact on equity capital of the

Company.

Other than above, there was no outstanding GDRs/ADRs or

warrants or any other convertible instruments.

(xvi)OUTSTANDING GDRs/ADRs OR WARRANTS OR ANY

CONVERTIBLE INSTRUMENTS, CONVERSION DATE AND

LIKELY IMPACT ON EQUITY

(V) CEO/CFO CERTIFICATION:

VI) COMPLIANCE:

VII) PLANT LOCATIONS:

The necessary certification from Chief Executive Officer H. K. Mittal

and Chief Financial Officer Atul J. Agarwal in respect of the financial

year ended on March 31, 2008 has been annexed to this report.

The Company has complied with all the mandatory requirements

of Corporate Governance Clause 49 of the Listing Agreement with

Stock Exchanges. Further, the Company has also adopted

Remuneration committee requirements out of Non-mandatory

requirements of the Clause.

A certificate from the Auditors of the Company regarding

compliance of conditions of corporate governance is annexed to

the Directors' Report.

The Company does not have any plant.

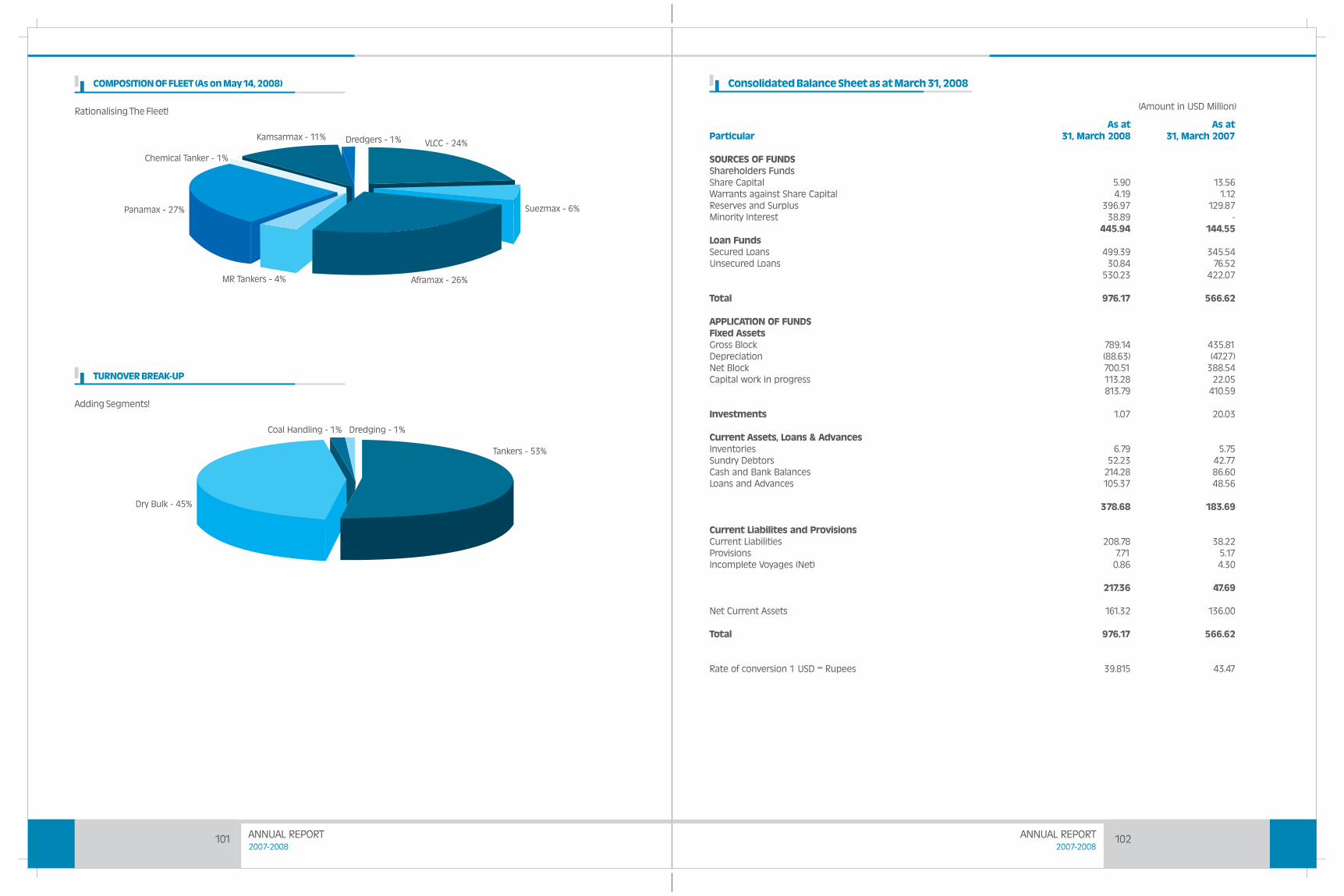

As at March 31, 2008, the Company owns total thirteen vessels of

aggregate tonnage of 1,137,712 DWT consisting of a Very Large

Crude Carrier (VLCC); a Suezmax tanker; five Aframax tankers; two

MR Tankers; a Panamax and three dredgers. Seven vessels of

aggregate tonnage of 543,105 MT were owned by Subsidiary of the

Company consisting of four panamax and three Kansarmax

vessels. Further, as at March 31, 2008; the Company alongwith its

subsidiaries also had seven chartered vessels of aggregate

tonnage of 660,021 DWT comprising of four panamax; a VLCC;

an aframax and a chemical tanker. The consolidated capacity was

27 vessels of 2,340,838 DWT. All the vessels are deployed on various

sea-route.

Address for correspondence:

Mercator Lines Limited

3rd Floor, Mittal Tower, B-wing,

Nariman Point, Mumbai-400 021

Tel Nos: 91-22-66373333

Fax Nos: 91-22-66373344

E-mail:[email protected] / [email protected]

Besides LOA for debentures amounting Rs. 25 crores issued during the year under ISIN INE934B08064; the Company has following series

of listed Redeemable Non-Convertible Debentures on private placement basis in dematerialized form:

ANNUAL REPORT 2007-2008

32

Whistle blower policy

The Company does not have any formal whistle blower policy.

However, the employees are welcomed to report to the

management, their concerns about unethical behaviour, actual

or suspected fraud or violation of the company's code of

conduct and they are provided direct access to the Chairman

of the Audit Committee of Board of Directors of the Company.

For and on behalf of the Board

H. K. MITTAL

Executive Chairman

Regd. Office:rd3 Floor, Mittal Tower,

B-wing, Nariman Point,

Mumbai - 400021

Dtd: May 14, 2008

Compliance with Non-Mandatory Requirement

Company continuously strives for improving its Corporate

Governance practices. Besides following mandatory requirements;

the Company follows non-mandatory requirements also as under:

Office Space for Non-Executive Chairman

The Company's Chairman is an Executive Chairman and hence the

issue of providing office space for Non-executive Chairman is not

applicable.

There is no specific tenure specified for Independent Directors.

But, some of Independent Directors' tenure exceeds the period of

9 years. All the independent Directors have requisite qualifications

and experience which has been of use to the Company and which

enables them to contribute effectively to the Company in their

capacity as an independent Directors.

Remuneration Committee

The Company's Remuneration Committee details have already

been mentioned earlier in this Annual Report.

Rights of Shareholders to receive financial results

The Company's financial results for every quarter are published in

the newspapers and are put on the Company's website as well,

besides being made available on the SEBI website

www.sebiedifar.nic.in.

Audit Qualifications

There was no audit qualification in the Company's financial

statements during the year under review. The company continues

to adopt best practices to ensure the regime of unqualified

financial statements.

Board Members Training

The management and the working Directors give extensive

briefings to the Board members on the business scenario of the

company and factors affecting the business during the Audit and

Board meetings.

Evaluating Performance of non-executive Board Members

Based on the criteria of attendance at the Board / Committee

meetings as also the contributions made at the said meetings, the

performance evaluation of the non executive Board members is

done by the Board annually.

Paving the Ways

Dredging the Ways

(Forming part of Directors' report for

the year ended on 31st March 2008)

THE SHIPPING INDUSTRY

Shipping is a primary means of international transportation of

many essential commodities. In Indian context, it is all about

maritime transport as our country's international trade;

approximately 95% by volume and 70% by value is sea-borne.

Shipping as industry, though a component of service industry;

plays a pivotal role in shaping economy by facilitating international

trade. It is therefore an ideal candidate to enjoy the status of a

mother industry. The industry is classified globally in several ways;

such as capacity specific to route specific; however, in general it is

broadly classified into Wet bulk; Dry bulk and Liners. Sub sets of wet

bulk are Tankers and offshore; whereas Dry Bulk is mainly further

classified based on carrying capacities. Under Liners, it has

Containers, MPP and Ro-Ros type of vessels.

The Offshore Industry is a logical offshoot of the Shipping Industry.

The Offshore sector is further segmented into drilling, exploration

and production, development and maintenance of floating

production systems etc; essentially based on the services offered

to petroleum sector.

As with any other industry, the sub sectors are driven by a

combination of demand and supply with pricing and services

offered, being the key. The underlying trend for demand in

shipping is mainly driven by the strength of the global economy

and global trade. The tanker segment or even the offshore

segment, for example, is further driven by oil demand, while the

Dry Bulk segment is influenced by the commodity demand,

primarily iron ore and coal. In each segment; the freight rates and

consequently vessel values have exhibited volatility in varying

degrees at various points in time. These fluctuations have been

primarily due to changes in the level and pattern of global

economic growth, trade balance or trade deficits. The degree of

competition within the global shipping industry largely depends

on the changes in the availability of vessels.

RECENT DEVELOPMENTS

SHIPPING:

Tanker Markets (Wet Bulk):

All the segments of the tanker market were very stable for most

part of the year. In the last quarter of the financial year, a sudden

spurt in the tanker demand sent the VLCC freight rates soaring.

The Suezmax segment also enjoyed a boost in their earnings, as

charterers made efforts to control the VLCC rates by splitting the

parcel sizes. The demand was created by the flurry of cargos fixed

by the charterers before the Christmas holidays. However, the

Aframax segment did not see any increase in demand with the

year ending on a soft note. The last quarter ended very well, giving

the much required boost to the tanker earnings, which ensured

that tanker owners continued being bullish about this segment in

medium to even long term.

Dry Bulk Markets:

It was a historical year for bulk carriers with Baltic Dry Index (BDI)

touching an all time high of 11,039 points in November 2007. The

dry bulk market which has seen firm earnings over the last three

years is likely to continue to do so in future. The strength of the dry

bulk market is due to the large import of coal into India and iron

ore into China. Chinese economic progress; particularly

unprecedented growth in infrastructure sector; have given a fresh

impetus to steel production; therefore iron ore imports into China

and record steel exports from China have pushed the momentum

in dry bulk market. The foregoing commodity aspects, when

coupled with marine infrastructural limitations and ageing fleets,

slower deliveries of the new builts led to the above historical high

indices.

MANAGEMENT DISCUSSION &

ANALYSIS REPORT

ANNUAL REPORT 2007-2008

34

ANNUAL REPORT 2007-2008

This increased prices and the steady rising demand gave impetus

to exploration activities, resulting in greater demand for offshore

services like Seismic, Drilling Rigs etc. To bridge the increasing

'demand - supply' gap, there is an increased thrust on the

'Development and Production' from the existing fields which

further increases demand for 'versatile' and 'improved' technology

based Jack-Up Rigs. Also Oil companies revised their basis for

exploration & production cost from a level of USD 45 to an amount

in excess of USD 65-70 per barrel thereby becoming a driver for

increased drilling activity backed by an increased demand and

improved remunerative rates for service providers. Consequently

the offshore segment shall continue to remain bullish over

medium to even long term.

The company is into shipping operations, with its own fleet of

Tankers, Bulk Carriers and Dredgers. The consolidated income

from our shipping operations was Rs. 1,477 crores for the year

under review as compared to Rs. 1,138 crores in the previous year,

recording top line growth of about 30% year on year.

The company's tanker fleet consists of VLCC, Suezmaz, Aframax,

Product Tankers and Chemical Tankers. Within the tanker segment,

the Company had ten tankers owned by it totaling a capacity of

11,44,761 DWT at the beginning of the year. During the year, the

Company sold one of its tankers of 1,00,488 DWT; therefore, at the

end of the year, the Company had 9 tankers owned by it; with an

aggregate tonnage of 10,44,273 DWT. Further, during the year the

Company chartered in two tankers and one chemical tanker with

an aggregate capacity of 3,74,337 DWT through its subsidiary.