Embed Size (px)

Citation preview

H E A L T H W E A L T H C A R E E R

M E R C E R | C O M P T R Y X

H R ’ S R O L E I N S I T ES E L E C T I O N

© MERCER 2016 2

W E L C O M ET O D AY ’ S P R E S E N T E R S

AMY TILLESNA Solutions ConsultantWorkforce Metrics

[email protected] [email protected]

Patrick GutmannSector Leader Europe

© MERCER 2016 3

A G E N D A

S I T ES E L E C T I O NA P P R O A C H

W H YB U S I N E S S E S

E X P A N D

Q & AH O WM E R C E R |

C O M P T R Y XC A N H E L P

© MERCER 2016 4

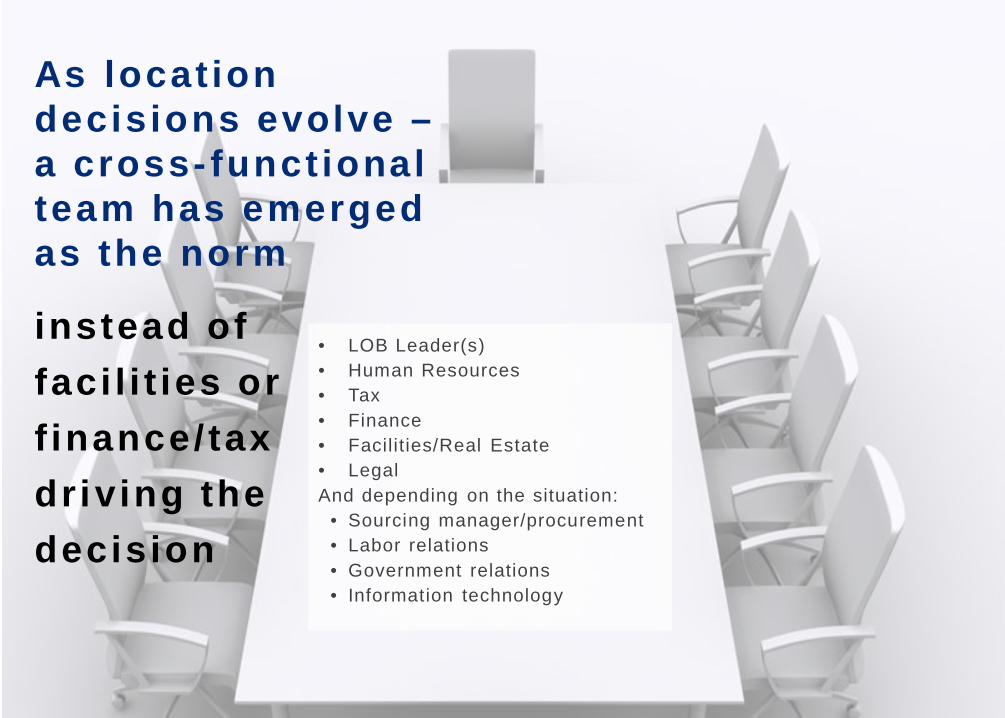

As locat iondecisions evolve –a cross- funct ionalteam has emergedas the norm

instead offaci l i t ies orf inance/taxdriving thedecision

• LOB Leader(s)• Human Resources• Tax• Finance• Facilities/Real Estate• LegalAnd depending on the situation:

• Sourcing manager/procurement• Labor relations• Government relations• Information technology

© MERCER 2016 5© MERCER 2016 5

WHY BUSINESSESEXPAND

© MERCER 2016 6

Why do companiesexplore new si telocat ion decisions?• G r o w t h• G e o g r ap h i c

e x p a n s i o n• Ac q u i s i t i o n

i n t e g r a t i o n• R e c r u i t i n g d i f f i c u l t i e s• To f i n d l o w e r c o s t

s t a f f• P ro x i m i t y t o

c u s t o m e r s

© MERCER 2016 7

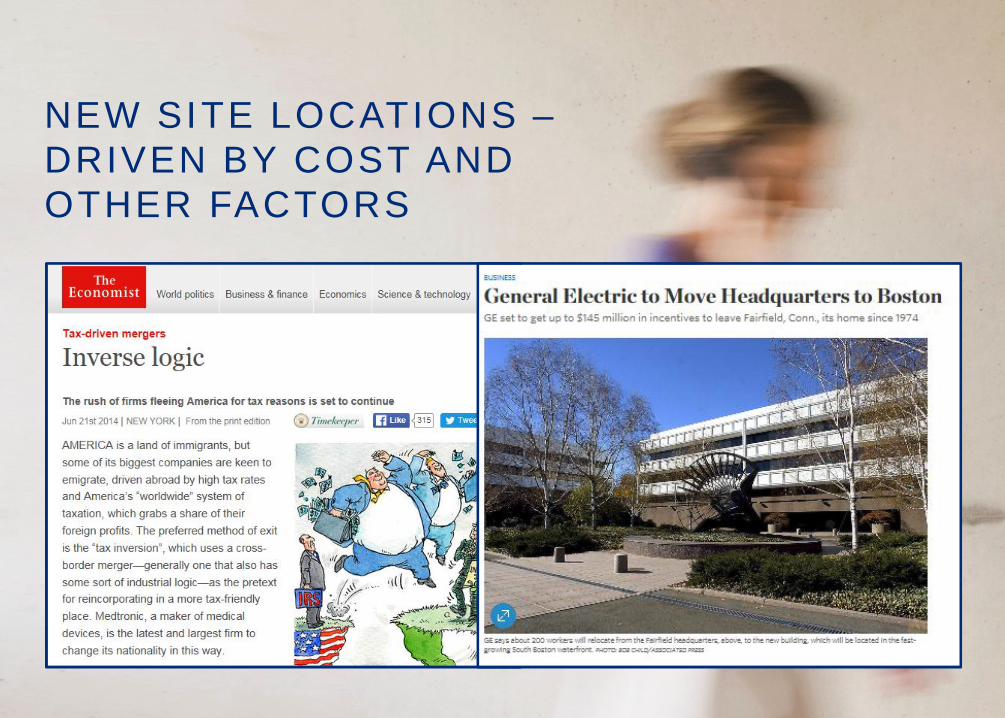

NEW SITE LOCATIONS –DRIVEN BY COST ANDOTHER FACTORS

© MERCER 2016 8© MERCER 2016 8

SITE SELECTIONAPPROACH

© MERCER 2016 9

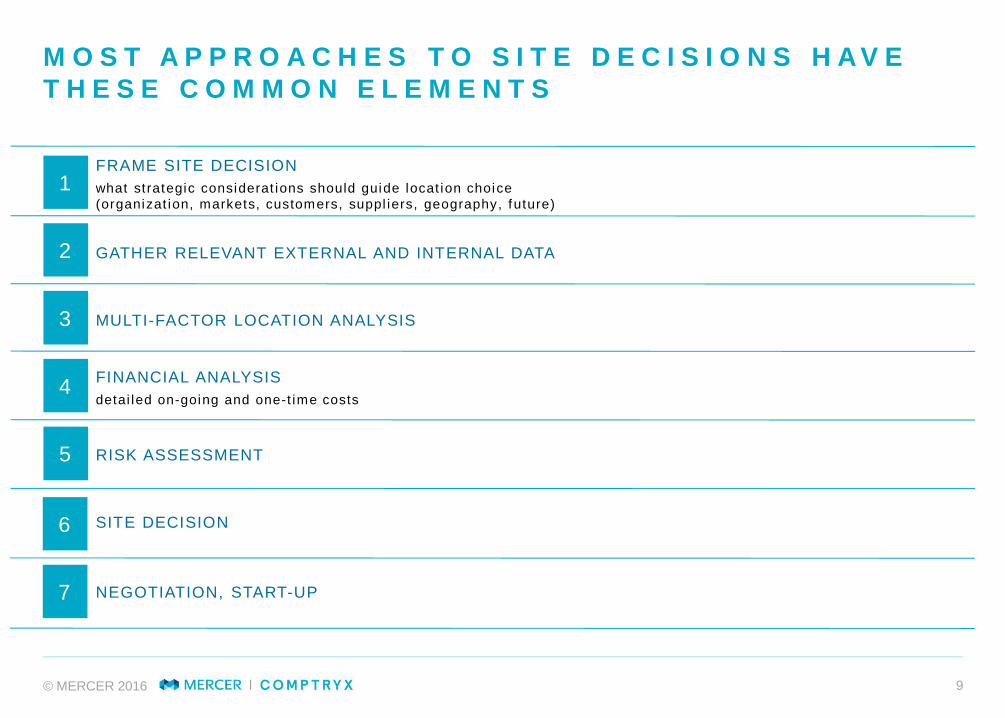

M O S T A P P R O A C H E S T O S I T E D E C I S I O N S H A V ET H E S E C O M M O N E L E M E N T S

1

2

3

4

5

6

7 NEGOTIATION, START-UP

FRAME SITE DECISIONwhat strategic considerat ions should guide locat ion choice(organizat ion, markets, customers, suppl iers, geography, future)

GATHER RELEVANT EXTERNAL AND INTERNAL DATA

MULTI-FACTOR LOCATION ANALYSIS

FINANCIAL ANALYSISdetai led on-going and one-t ime costs

RISK ASSESSMENT

SITE DECISION

© MERCER 2016 10

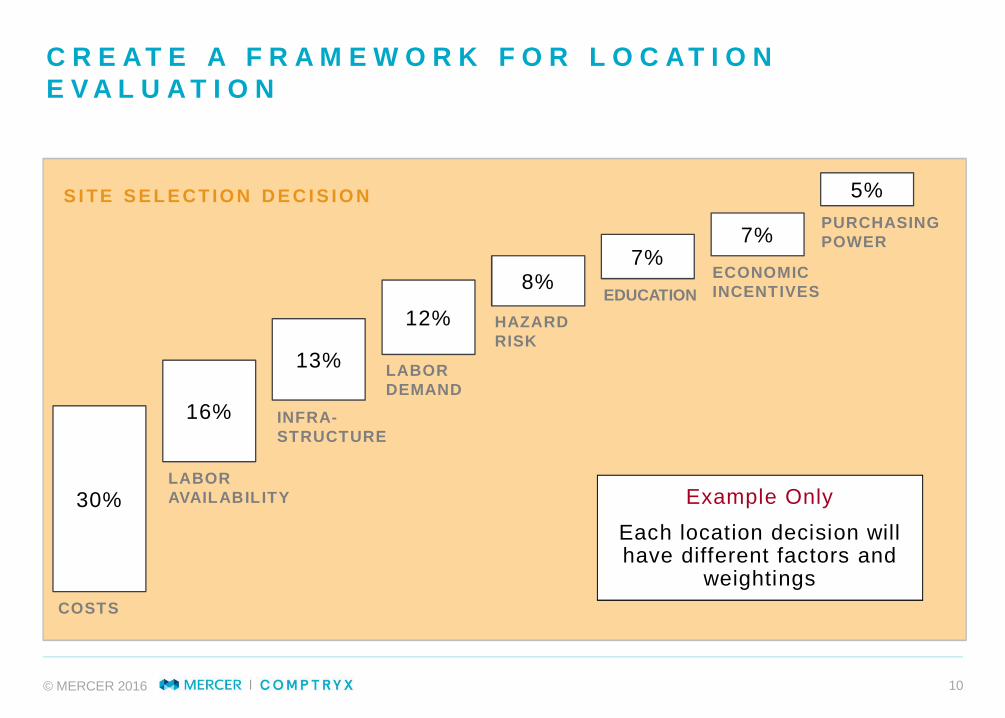

C R E AT E A F R A M E W O R K F O R L O C AT I O NE V A L U A T I O N

30%

16%

13%

12%

8%7%

7%

5%S I TE S E L E CT IO N D E C I S IO N

COSTS

LABORAVAILABILITY

INFRA-STRUCTURE

LABORDEMAND

HAZARDRISK

EDUCATIONECONOMICINCENTIVES

PURCHASINGPOWER

Example Only

Each location decision willhave different factors and

weightings

© MERCER 2016 11

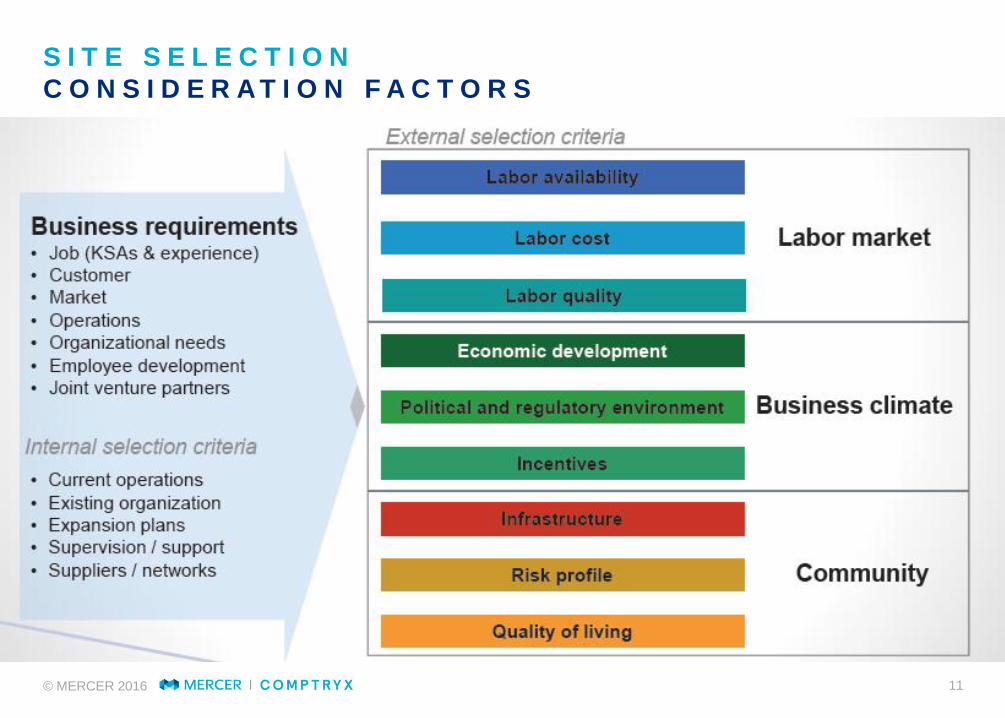

S I T E S E L E C T I O NC O N S I D E R A T I O N F A C T O R S

© MERCER 2016 12

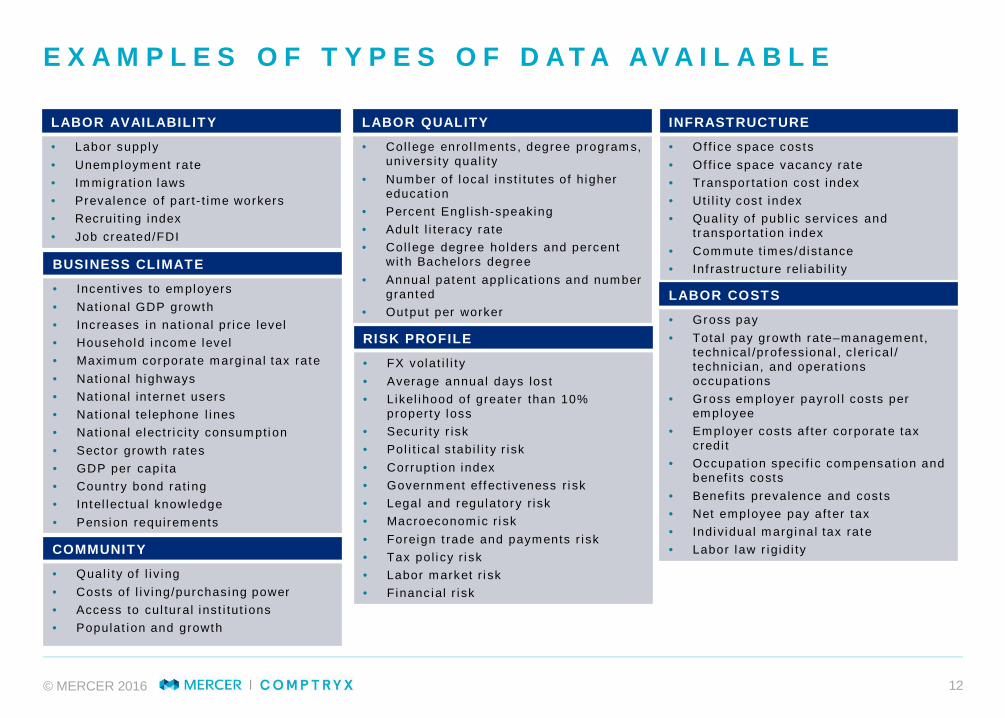

E X A M P L E S O F T Y P E S O F D A T A A V A I L A B L E

LABOR AVAILABILITY

• Labor supply• Unem ploym ent rate• Im migrat ion laws• Prevalence o f par t - t ime workers• Recrui t i ng index• Job created/FDI

LABOR COSTS

• Gross pay• Total pay growth rate–managem ent,

technical /professional , c ler i cal /technic ian, and operat ionsoccupat ions

• Gross em ployer payrol l costs perem ployee

• Employer costs af ter corporate taxcredi t

• Occupat ion speci f i c com pensat i on andbenef i ts costs

• Benef i ts prevalence and costs• Net employee pay af ter tax• Indi v idual m arginal tax rate• Labor law r ig id i ty

LABOR QUALITY

• Col l ege enrol lm ents , degree program s,univers i ty qual i ty

• Number of local inst i tutes of h ighereducat ion

• Percent Engl ish-speaking• Adul t l i teracy rate• Col lege degree holders and percent

wi th Bachelors degree• Annual patent appl icat ions and num ber

granted• Output per worker

INFRASTRUCTURE

• Of f ice space costs• Of f i ce space vacancy rate• Transpor tat ion cost index• Ut i l i t y cos t index• Qual i ty of publ i c serv i ces and

transpor tat ion index• Comm ute t im es/distance• Inf ras tructure rel iabi l i tyBUSINESS CLIMATE

• Incent i ves to em ployers• Nat ional GDP growth• Increases in nat ional pr i ce level• Household i ncom e level• Maxim um corporate m arginal tax rate• Nat ional h ighways• Nat ional internet users• Nat ional te lephone l ines• Nat ional elect r i c i ty consum pt i on• Sector growth rates• GDP per capi ta• Country bond rat i ng• Intel lectual knowledge• Pension requirem ents

RISK PROFILE

• FX volat i l i t y• Average annual days los t• Likel ihood of greater than 10%

property loss• Secur i ty r isk• Pol i t i cal s tabi l i t y r i sk• Corrupt i on index• Governm ent ef fect i veness r i sk• Legal and regulatory r i sk• Macroeconom ic r i sk• Foreign t rade and payments r i sk• Tax pol i cy r i sk• Labor m arket r i sk• Financ ial r i sk

COMMUNITY

• Qual i t y of l i v ing• Costs of l i v ing/purchasing power• Access to cul tural inst i tut ions• Populat ion and growth

© MERCER 2016 13

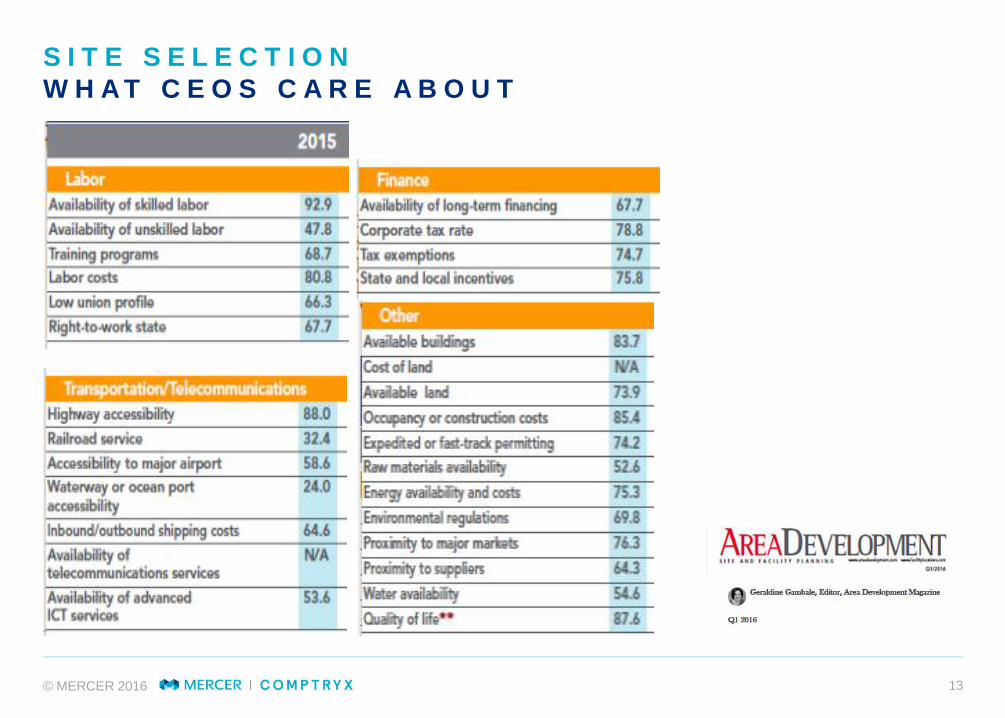

S I T E S E L E C T I O NW H A T C E O S C A R E A B O U T

© MERCER 2016 14

U N I T E D S T A T E SB E S T L O C A T I O N S F O R T E C H S T A R T U P S

Mark Schi l l , Research Di rector at Prax is Strategy Group Per Forbes Stat ista Report

© MERCER 2016 15

W H E R E D O M U L T I N A T I O N A L T E C H C O M P A N I E SO P E R A T E ? ( A C C O R D I N G T O M E R C E R | C O M P T R Y X )

VIRTUALLYEVERYONE

THE PIONEERS

U N I T E DS T A T E S

C A N A D A U N I T E DK I N G D O M

F R A N C E

I T A L Y

S W E D E NS W I T Z E R L A N DN E T H E R L A N D S

A U S T R A L I A

C H I N A

I N D I A

J A P A N

S I N G A P O R E

H O N G K O N G

B E L A R U S

A Z E R B A I J A N

M A C E D O N I A

G E R M A N Y

M A L T A

I V O R Y C O A S T

C A M E R O O N

T A N Z A N I A

M O Z A M B I Q U E

M Y A N M A RM A C A U

D O M I N I C A NR E P U B L I C

T R I N I D A D &T O B A G O

J A M A I C A

P A R A G U A Y

G H A N A

© MERCER 2016 16

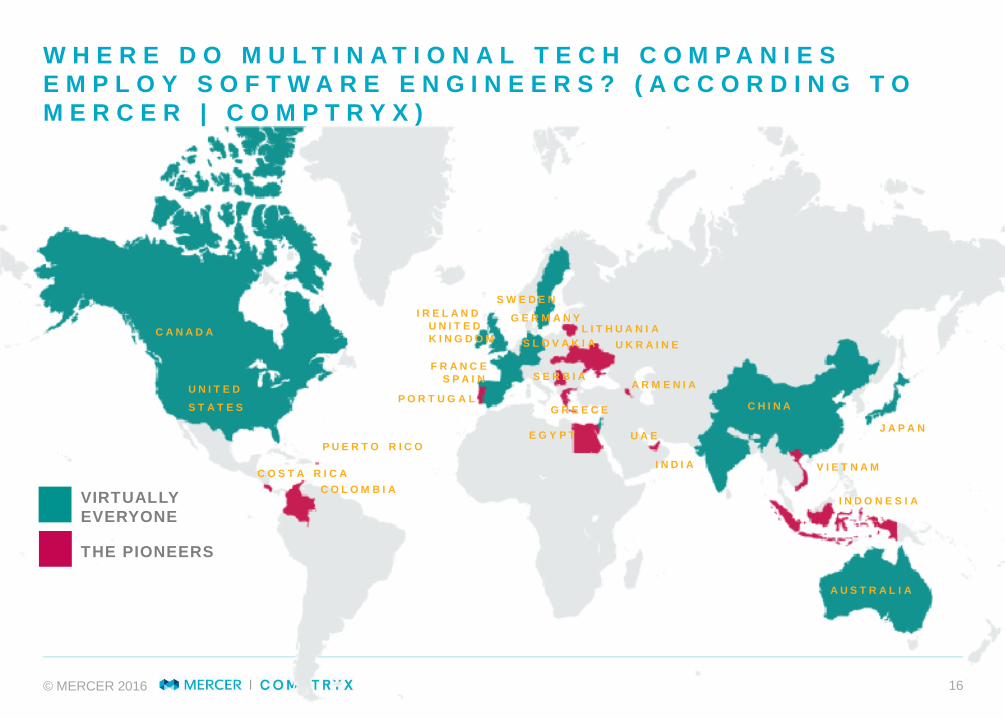

W H E R E D O M U L T I N A T I O N A L T E C H C O M P A N I E SE M P L O Y S O F T W A R E E N G I N E E R S ? ( A C C O R D I N G T OM E R C E R | C O M P T R Y X )

VIRTUALLYEVERYONE

THE PIONEERS

U N I T E DS T A T E S

C A N A D A

I R E L A N DU N I T E DK I N G D O M

F R A N C ES P A I N

S W E D E N

A U S T R A L I A

C H I N A

I N D I A

J A P A N

G E R M A N Y

U A EE G Y P TP U E R T O R I C O

C O L O M B I AC O S T A R I C A

P O R T U G A L

V I E T N A M

I N D O N E S I A

A R M E N I A

U K R A I N ES L O V A K I AL I T H U A N I A

G R E E C E

S E R B I A

© MERCER 2016 17© MERCER 2016 17

HOW MERCER |COMPTRYX CAN HELP

© MERCER 2016 18

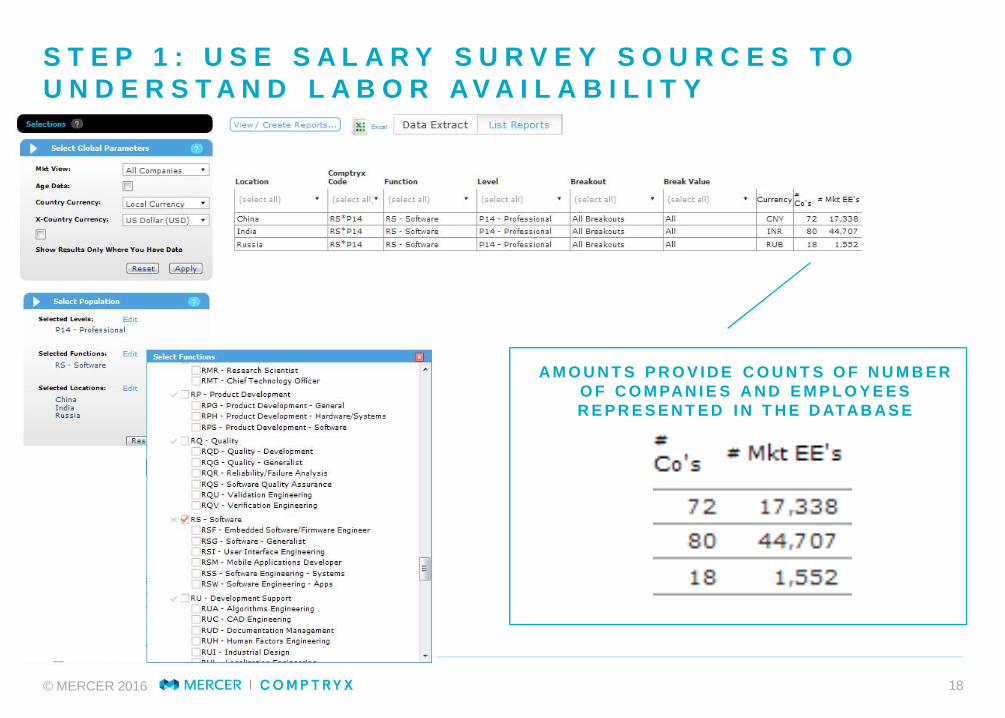

S T E P 1 : U S E S A L A R Y S U R V E Y S O U R C E S T OU N D E R S T A N D L A B O R A V A I L A B I L I T Y

AM O U N T S P R O V I D E C O U N T S O F N U M B E RO F C O M PAN I E S A N D E M P L O Y E E SR E P R E S E N T E D I N T H E D ATAB A S E

© MERCER 2016 19

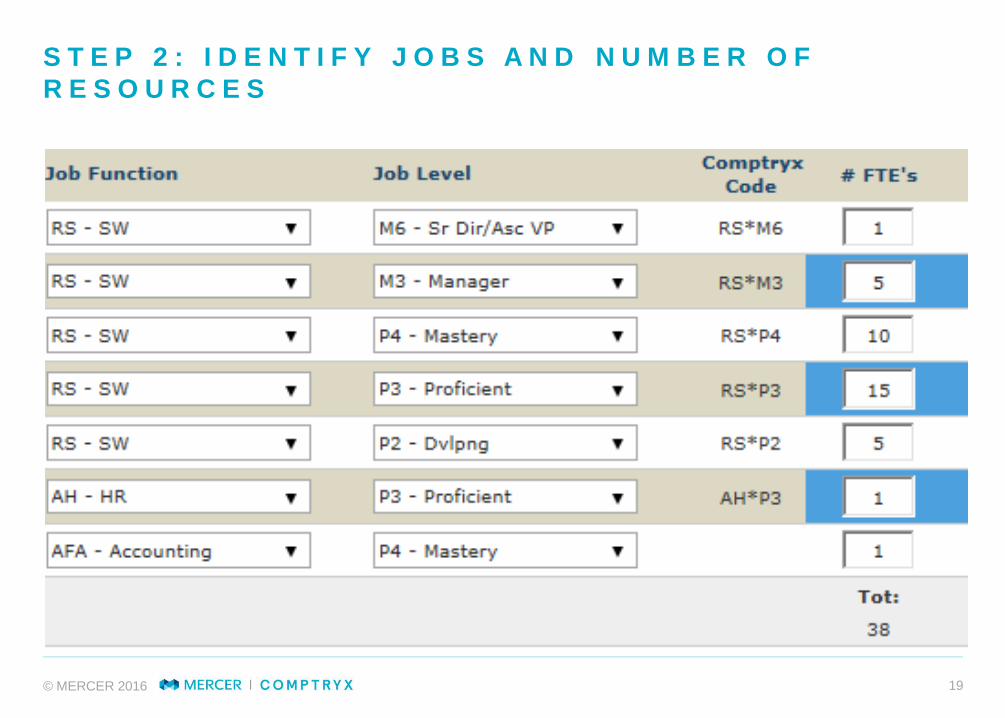

S T E P 2 : I D E N T I F Y J O B S A N D N U M B E R O FR E S O U R C E S

© MERCER 2016 20

S T E P 3 : S E L E C T L O C A T I O N S A N D I D E N T I F YC O S T S A N D V A R I A N C E

© MERCER 2016 21

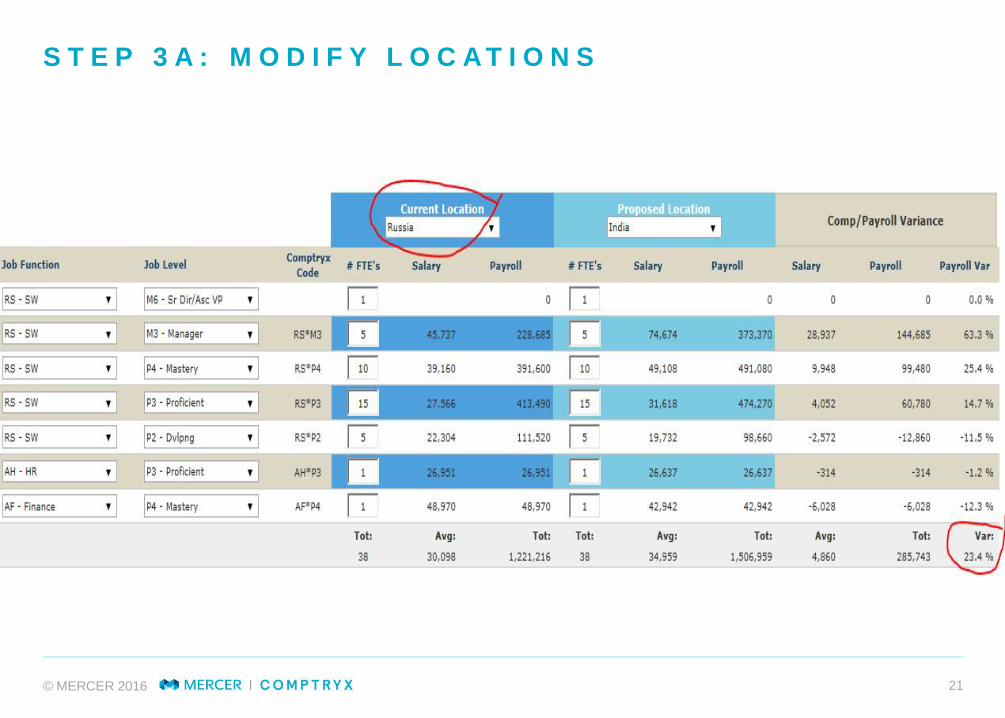

S T E P 3 A : M O D I F Y L O C A T I O N S

© MERCER 2016 22

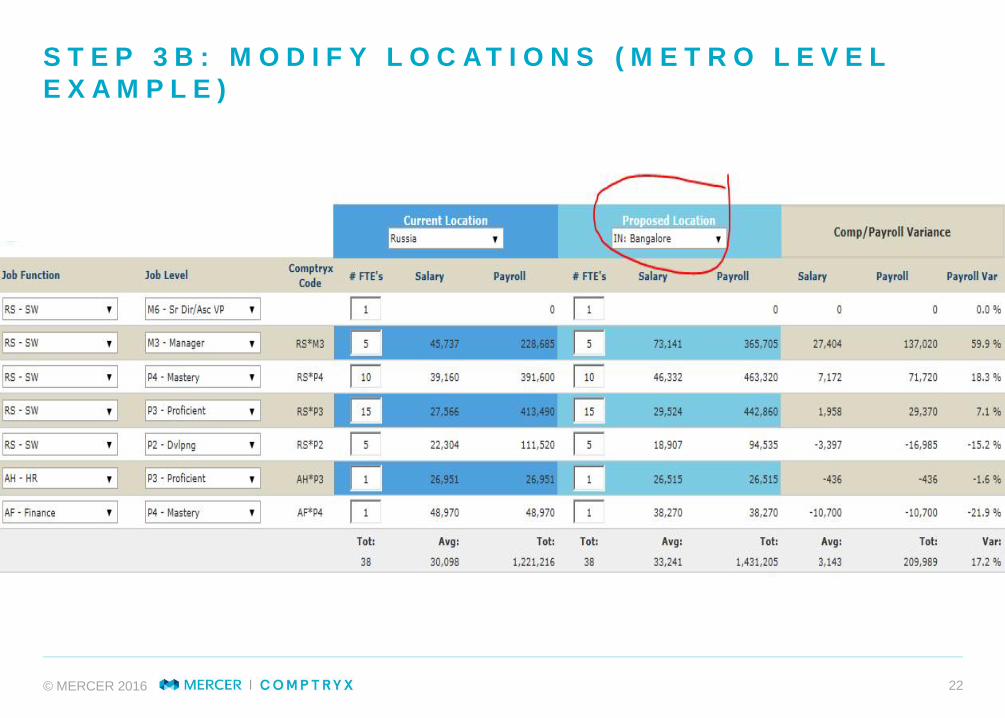

S T E P 3 B : M O D I F Y L O C A T I O N S ( M E T R O L E V E LE X A M P L E )

© MERCER 2016 23

1 . P R O J E C T IN G F U TU R E C O S TS

2 . COMPARING YOUR CURRENTLOCATION OR NEW LOCATIONS

3 . P R I C I NG AT U P P E R P E R C E N T IL E TOR E C R U I T S TAF F AWAY F R OM TH E I RC U R R E N T E M P L O YE R

4. BE NE FIT C OS TS

S E L E C T I N G L O C A T I O N S – O T H E R F A C T O R S T OC O N S I D E R

© MERCER 2016 24

LESSONSLEARNED

Successful decisions have all key stakeholdersRepresented—make decision criteria explicit, assessimpact to overall business, match what local labormarkets have to offer to workforce needs.

Focus only on factors that vary by Market—not on al lthe costs and quali ty ones.

Avoid original data collection, locationinformation—unless t iming is not an issue.

Perform due diligence—not just market’s but yourabi l i ty to manage within that environment.

Decisions based on costs alone often end indisappointment—be conservative in cost savings, stickto a short t ime-horizon.

Don’t ignore implications for your internal labormarket—understand balance between “bought” and“bui l t” talent needed for business success.

Know when it’s time to look across whole portfolioof businesses—don’t take each location decision asthey come.

Don’t copy others—f igure it out for yoursel f,uniqueness dominates, exploi t i t to create more lastingadvantage.

T H I S P R O C E S S O F F E R S I N S I G H T S B E Y O N DL O C AT I O N A N D S O U R C I N G S T R AT E G Y A N D H E L P S

I N R E C R U I T I N G , W O R K F O R C E P L A N N I N G ,G O V E R N M E N T R E L AT I O N S , I N C E N T I V E S ,

N E G O T I AT I O N S W I T H P A R T N E R S .

© MERCER 2016 25

W H A T ’ S C O M I N G ?

HTTPS://WWW.LINKEDIN.COM/GROUPS/4315619

TUESDAY

SEPTEMBER 27TH

HYATT REGENCY

SANTA CLARA

REGISTER NOW

M E R C E R | C O M P T R Y XD I S C U S S I O N G R O U P

M E R C E R | C O M P T R Y XA N N U A L C O N F E R E N C E

© MERCER 2016 26

A N Y Q U E S T I O N S ?

Q U E S T I O N S

Please type your questions in the Q&A section of the toolbarand we will do our best to answer as many questions as wehave time for.

To submit a question while in full screen mode, use the Q&Abutton, on the floating panel, on the top of your screen.

CLICK HERE TO ASK A QUESTIONTO “ALL PANELISTS”

F E E D B A C K

Please take the time to fill out thefeedback form at the end of thiswebcast so we can continue to improve.The feedback form will pop-up in a newwindow when the session ends.

© MERCER 2016 27