Embed Size (px)

Citation preview

METAL

JANUARY

METAL FORMING

JANUARY 2010

MACHINERY 2010 INDUSTRY

IN INDIAPRESSES SHEET METAL SECTIONS

IN INDIAPRESSES SHEET METAL SECTIONS

Indian Machine Tool Manufacturers’ Associationwww.imtma.in1

Forward by the President of IMTMA

• Metal forming plays a major role in the production of diverse products starting with large formed parts inthe automobile industry to high precision components for the instrumentation and electronics industries,and everywhere in-between. The defence and aerospace industries use formed parts in variousapplications from missile components to ordnance items. Progress in metal forming technologies haspp p g g gbeen rapid, keeping pace with the need to improve productivity, precision and volumes. Metal formingaccounts for nearly 40 percent of total machine tools consumption in India, pointing to its growingimportance.

• The metal forming machinery industry in India has been serving the need for formed parts through themanufacture of a variety of metal forming presses, sheet working machinery and others. However, theindustry has yet to meet the demand for higher technology machines. As a result the market share forIndian machines is low, and imports meet a large part of the demand for metal forming machines.

• IMTMA has commissioned this study of the metal forming machinery industry in India to gain anunderstanding of its potentials and prospects which will be valuable inputs for machinery manufacturersin developing new technologies, products and markets. The report brings out:

– The global and Indian position in metal forming machinesThe global and Indian position in metal forming machines– A profile of the metal forming machinery industry in India– Expectations of users in technology and product capabilities– Anticipated demand for metal forming machinery in India, by major product types and user

segmentssegments– User perceptions about Indian machines and areas requiring attention

2

Forward by the President of IMTMA

• The report has been developed for IMTMA by Feedback Business Consulting Services, Bangalore. I would like to thank their research team for their work in taking up and completing this report in time for its publication at IMTEX Forming 2010.

• IMTMA would like to acknowledge the suggestions and inputs received from the following in the course of preparing this report:

• Mr.Shailesh Sheth, Past President, IMTMA• Mr R D Madan President ISGEC YamunanagarMr.R.D.Madan, President, ISGEC, Yamunanagar• Ms.Ingrid Rasquinha, Director, Production, Electropneumatics and Hydraulics (India) Private Ltd., Pune• Mr.P.J.Mohanram, Senior Adviser (Technology), IMTMA, Bangalore

• This study report is a valuable reference work which can help manufacturers of metal forming machinesThis study report is a valuable reference work which can help manufacturers of metal forming machinesin India to develop strategies and plans to meet the potentially large requirement for such machines. Iam sure this report will be of use to the existing metal forming machinery manufacturers in guiding theirfurther expansion and development plans, as well as in attracting new investment to this growing field.

M.Lokeswara Rao

President

BangaloreJanuary 21, 2010

3

Table of Contents

Definitions

Approach & Methodology, Coverage

Objectives, Deliverables

BACKGROUNDI

Definitions

OVERVIEW OF INDIAN ECONOMYII

INDIAN MANUFACTURING SECTOR OVERVIEWIII

GLOBAL METAL FORMING INDUSTRY DETAILSIV

Global trends and markets – Production, consumption trends by country

Technology trends and developments

INDIAN METAL FORMING MACHINERY INDUSTRY V

Comparison of Indian and International machinery manufacturers

Industry structure, Products offered, Geographical clusters

Customer perceptions, Verbatim

INDIAN METAL FORMING MACHINERY MARKET ESTIMATES VI

Market estimates by type of Machinery, Segments

Approach and Methodology, Future market estimates

INDIAN METAL FORMING MACHINERY FUTURE ESTIMATES VII

Opportunity areas and Action points

OPPORTUNITY ASSESSMENT AND RECOMMENDATIONSVIII

4

Engagement backgroundEngagement background

5

Engagement background

IMTMA background Study objectives

IMTMA represents the machine toolindustry in India, comprising 370member organizations of large,medium and small categories

Estimate current industry size andstructure of metal forming machinesacross user industry segments

Understand the manufacturing andmedium and small categories

IMTMA proactively assists the machinetool industry to boost productivity andcompetitiveness in manufacturing

Understand the manufacturing andtechnology trends in the user segments

Likely changes in manufacturing practices

Impact on the type of machinesTowards this, IMTMA acts as an enablerthrough a range of value-addedinitiatives like training programs,industry studies and seminars and

Impact on the type of machines

Machine usage in the industrysegments

Imports Vs. Domestic, applicationsindustry studies and seminars andworkshops

IMTMA is working towards increasingthe presence of Indian metal forming

p , pp

Usage of imported machines

Future machine off take

Market/ Industry assessmentmanufacturers - a sector currentlygoverned by imports

Market estimation

Growth and future potential (5 years)6

Scope of the document (1/2)

All India market assessment from competition (Metal forming machines) Current market size and supply side estimates

All India market assessment

Supplier assessment

pp yPresence of major players (domestic & imported), their product offerings, marketing strategies Best practices & Business models of competition

Industry structure: Number of players and classification Comparison of Imports vs. Domestic scenario in IndiaProduct offerings – technology, product portfolio, pricing and commercial terms, range and specifications Key user segments catered Issues faced – range, quality, technology gaps

Future outlook

Challenges and key issues impacting the industry Emerging marketing trend that could significantly impact the industry

Demand driversFuture growth potential for next 5 years (order of magnitude) Future growth potential for next 5 years (order of magnitude) Role of domestic manufacturers

7

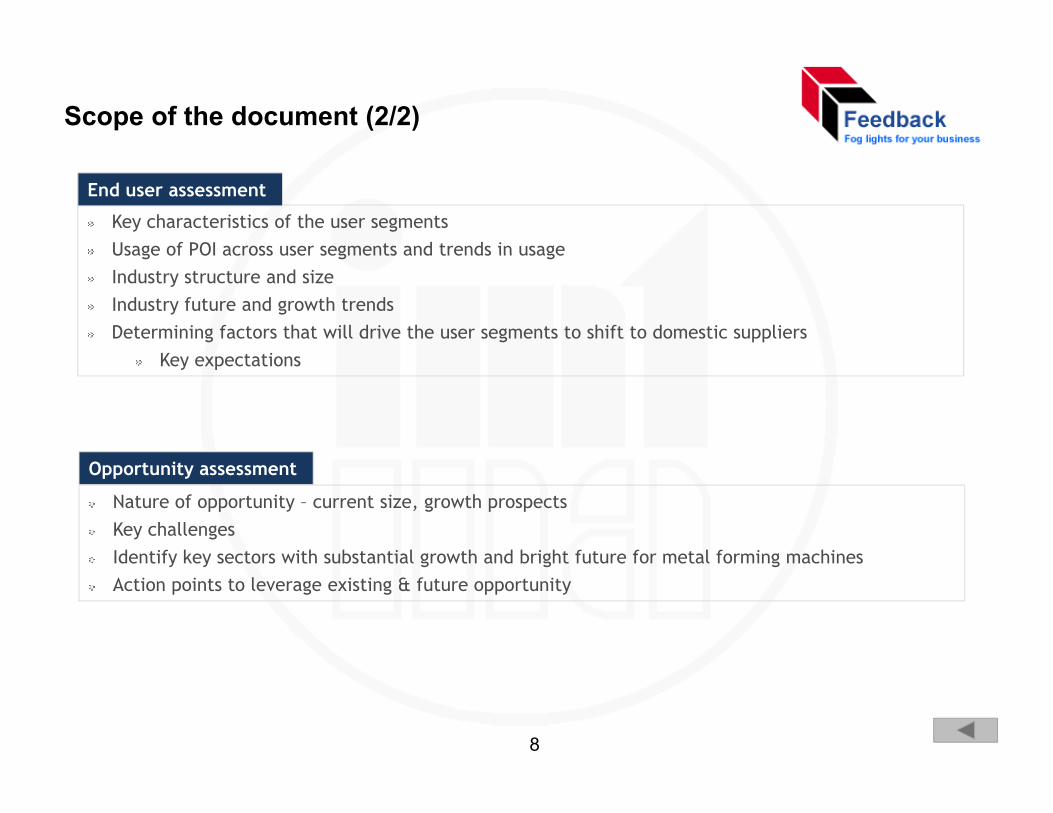

Scope of the document (2/2)

Key characteristics of the user segmentsUsage of POI across user segments and trends in usage

End user assessment

Usage of POI across user segments and trends in usage Industry structure and size Industry future and growth trends Determining factors that will drive the user segments to shift to domestic suppliers

K t ti Key expectations

Nature of opportunity – current size, growth prospectsKey challenges Identify key sectors with substantial growth and bright future for metal forming machines

Opportunity assessment

Identify key sectors with substantial growth and bright future for metal forming machines Action points to leverage existing & future opportunity

8

Overall approachFo

cus

Interviews with key stakeholders, the primary route to establish market dynamics and opportunity assessment

rces

Domestic user segments(12 segments and

corresponding sub-

Competition (Manufacturers,

Dealers Importers

Annual reports, Industry reports, Press releases,

Sou

Primary Secondary

corresponding sub-segments)

Dealers, Importers, Second hand dealers) publications and websites

dolo

gy

Respondent groups met were first identified based on market dynamics

Lists of respondents in each category were built through discussions with associations, Feedback Body of Knowledge, etc.

Primary interviews were conducted among all respondent groups

Met

hod Primary interviews were conducted among all respondent groups

Multiple interviews conducted across channel partners & user segments to understand the usage practices

Secondary research to understand competition activity, growth rate and future of user segments

Multiple interviews across competition to gain key insights

9

Sample coverage

Chandigarh

Respondent category Sample

coverage

End users

A t ti 10

Delhi

Chandigarh Automotive 10

Auto component 35

White goods/consumer durables 10

Kitchen equipment 8

Mumbai

AhmedabadGeneral engineering 30

Electrical and electronics industries 20

Energy & Power equipment, incl. boilers, wind

bi di l d i

15

Bangalore

Mumbai

Puneenergy, turbines, diesel and gas engines, etc.

Ship building 5

Infrastructure/ construction equipment 15

Process equipment and machinery 20Chennai

CoimbatoreRailways/ other heavy transportation 5

Others ‐ office equipment, furniture, etc 10

Manufacturers and suppliers – Domestic and Imports 42

Multiple interviews across companiesTotal 225 Multiple interviews across companies

10

Definitions and explanations of words used in the report

Words frequently used in the report Definitions

Micro precision machines » Accuracy of more than 1 micronMicro precision machines

Multi operational machines

» Combining two or more operations in one, such as adding, joining, threading and punching, laser marking, assembly and quality inspection with in press or combining shearing with punching machines, etc

» Using ultrasonic vibrations to decrease the coefficient of friction to

Vibration Forming

Using ultrasonic vibrations to decrease the coefficient of friction to avoid wrinkling and cracking while press forming of high quality products

Hydro Forming» Specialized type of die forming that uses a high pressure hydraulic fluid

to press room temperature working material into a dieHydro Forming p p g

Roll Forming» Continuous bending operation in which a long strip of metal is passed

through consecutive sets of rolls

Composite Forming» Forming of Composite material such as diaphragm forming for composite

Composite Forming

Dry press Forming» Forming that does not require lubricants

Silent Forming» Low vibration and noise with higher speed and motion control

Hard to work materials» Inconel, niobium, tantalum, molybdenum, plastics, plastic-metal

composites, metal glass

11

Overview of Indian economyOverview of Indian economy

12

Strong demographic profile with the growing urban population is expected to drive demand in various sectors

Unemployment rate (%)

1079 1096 1112 1129 1145 1161 1177 1193 1208 1224 1239Urban Rural Total Population

Population growth trend (mn numbers)

• Indian population growing at a CAGR of 1.39%

• 31% urban population – has been consistently

310 317 324 331 338 346 353 360 368 375 383

770 779 788 797 806 815 824 832 840 848 856

1079 1096 1112 1129 1145 p p y

growing at a CAGR of 2.15%

• India has the largest number of median age

citizens (15-35 years of age)

I di t d t ti th t ti2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

• In the top 20 cities, high income groups are expected to triple by 2016 and more than half of the households are expected fall in the middle income group • IT & other services driven jobs and construction activities have instigated huge migration of population• Sooner than expected and planned urbanization, calls for huge domestic demand particularly for infrastructure

• India expected to continue as the youngest nation

over the next 20 years

8.8 8.8 9.5 9.2 8.97 8

Rural Urban

Sooner than expected and planned urbanization, calls for huge domestic demand particularly for infrastructure

CAGR – 3.2%CAGR – 1.4%

Growth in number of households (Mn units) Unemployment rate (%)

7.8 7.2

142 144 146 148 150 152 155 157 159 161

55 57 58 60 61 63 65 66 68 70

2002 2003 2004 2005 2006 2007 20082005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: CMIESource: Central Statistical Organization

13

The recent global financial crisis has selectively impacted the Indian economy

GDP growth slowing Fiscal deficit expected to touch 10% - last seen in FY91

Source: RBI, Planning Commission, Edelweiss Research Source: Budget documents, CMIE, IIFL Research, Citi Research

Industrial Recession - Negative IIP growth Export contracts decline for the first time in the last few years

Source: CSO, IIFL Research Source: Bloomberg

14

The Government and Central Banks have handled the economy with several key and focused measures

M t

RateMeasures

425 bps reduction in Repo rate to 4.75% from Sep 2008 levels; reverse repo rate reduced by 275 bpsInterest rate on NRI deposits have been increased

MonetaryMeasures

QuantitativeMeasures

400 bps reduction in Cash Reserve Ratio (CRR) to 5%; 100 bps reduction in Statutory Liquidity Ratio (SLR) allowing higher repo ability for banks

OtherMeasures

Sale of foreign exchange to augment forex supply in the domestic market

DemandAugmentation

Additional plan expenditure of USD 4 bn in FY09 for rural infrastructure and social security scheme:States are allowed to raise additional market borrowings of 0.5 percent of their Gross State Domestic Product (GSDP), amounting to about USD 6 bn, for capital expenditures in FY09

FiscalMeasures

in FY09

InvestmentDemand

IIFCL authorized to raise USD 8 bn through tax-free bondsIIFCL refinance facility to facilitate financial closure of projectsFII limit in corporate bond raised to USD 15 bn from USD 6 bnAll in cost ceiling on ECB removedAll in cost ceiling on ECB removed

ImprovingDistressamongff t d

Government back-up guarantee made available to ECGC to provide guarantees for exports to difficult markets/ productsCredit flow to export sector ensured EXIM bank refinance through refinance RBIAcross-the-board cut of 4 percent in Cenvataffected

businessesAcross-the-board cut of 4 percent in CenvatRBI’s refinance facility of USD 1.4 bn for SIDBI to cater to SME sector

15

India’s resilience is reflected in its strong fundamentals

GDP Growth Down, But Not Out Savings rates higher and better aligned

FY10 OverallGrowth(%)

Month ofProjection

Countercyclical fiscal and monetary

CMIE 7.0 Feb 2009

Economic Advisory Council to Prime Minister

6.5 – 7.0 April 2009

Standard & Poor 6.0 January 2009

Asian Development Bank 5.0 March 2009

IMF 5 3 March 2009

measures to provide fillip to growth Most agencies’ forecasts for India’s GDP

Source: Edelweiss Research, Press Releases

An Interplay of demographics, reforms andglobali ation to pro ide f rther c shion

Stronger corporate balance sheet to shield against do nt rns

IMF 5.3 March 2009

OECD 4.3 March 2009

EIU 5.0 March 2009

for FY10 are between 4-7 percent

Source: CSO

globalization to provide further cushion downturns

Demographics Youth (under 25 years) account for about 50 per cent of India’s total populationBy 2050, expected to have the largest working age population worldwide

I di h t k l d i hi h d i lGlobalization India has taken lead in high-end commercial servicesMajor overseas acquisitions made by Indian companies

Reforms Continuous liberalization for FDI policies in sectors like telecom, media, healthcare, retail, etc.

Source: IBEF Source: Citi - India Macroscope, July 2008

16

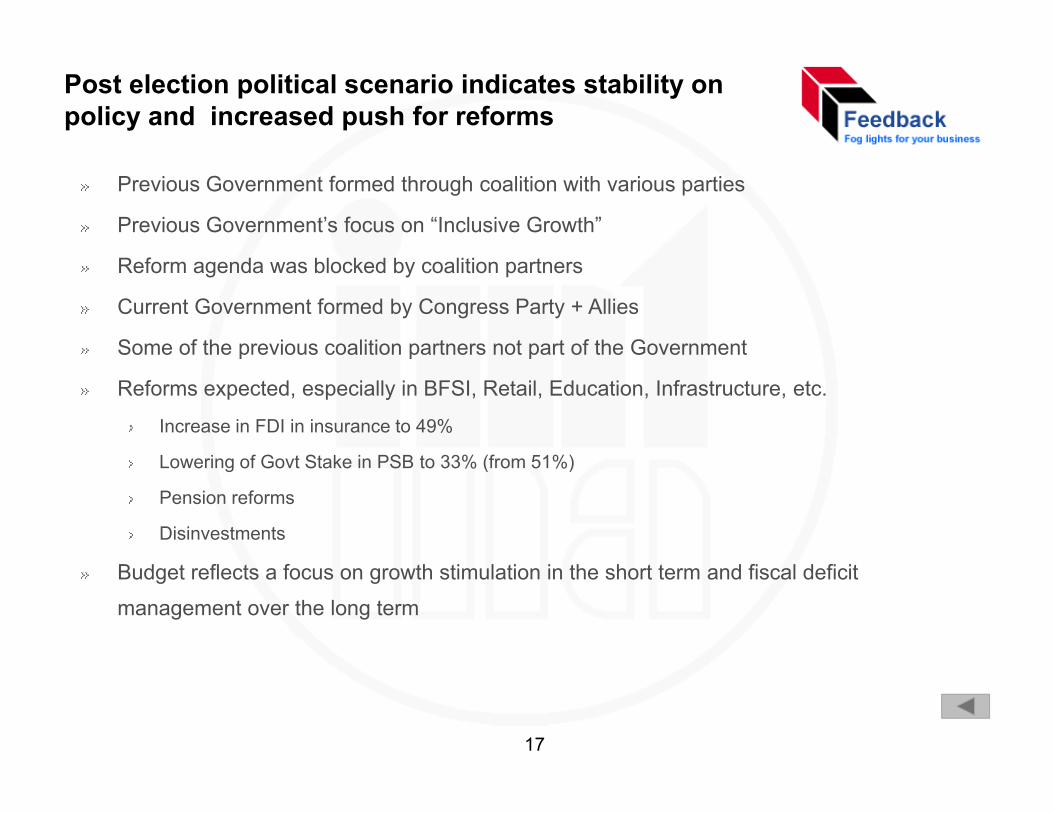

Post election political scenario indicates stability on policy and increased push for reforms

Previous Government formed through coalition with various parties

Previous Government’s focus on “Inclusive Growth”

Reform agenda was blocked by coalition partners

Current Government formed by Congress Party + Allies

Some of the previous coalition partners not part of the Governmentp p p

Reforms expected, especially in BFSI, Retail, Education, Infrastructure, etc.

Increase in FDI in insurance to 49%

L i f G t St k i PSB t 33% (f 51%)Lowering of Govt Stake in PSB to 33% (from 51%)

Pension reforms

Disinvestments

Budget reflects a focus on growth stimulation in the short term and fiscal deficit

management over the long term

17

Manufacturing sector overviewManufacturing sector overview• Components and background

• Industry size and manufacturing sector output

• Private and Government investments

• Future growth rates

18

Indian manufacturing sector: Overview

• India has the fourth-largest manufacturing base amongemerging economies, with 25.5 mn employees

• Manufacturing growth averaged 9% in the last 4 yearsManufacturing growth averaged 9% in the last 4 years(2004-08), with a record 12.3% growth in 2006-07

• Core manufacturing sector comprises:– Metals: Steel, Aluminum– Textiles & Garments– Electronics Hardware– Chemicals– Automobiles– Auto Components

Gems and Jewellery– Gems and Jewellery– Food & Agro Products

• The manufacturing sector is estimated to command amarket capitalization of USD 520 bn by 2014-15, againstUSD 272 bn as of Sept 30, 2007 (Confederation of Indianp , (Industry)

• India’s manufacturing sector has more investments as aproportion of gross domestic product than any othereconomy, except for China

Source: IBEF, Feedback Analysis

19

Indian manufacturing sector: Overview

Indian manufacturing sector isexpected to grow at 12-14 % over the next decade India is a stable

democracy withystrong

macroeconomicfundamentals

The BPOIndian manufacturing

competitivelypositioned for a high

growth rate era

India is ranked43 in the latestGCI index (1)ahead of otherBRIC i

Indian economyexpected togrow at 8-10% over the

t d d

The BPOmigration to

India is gettingreplicated in themanufacturing

BRIC economies next decade Sector

FDI inflow intoIndia has

doubled from

The quality of the Indian work force is one of India’s key competitive advantages

doubled fromUSD 3.4 bn in

2001 to USD 8 bnin 2005

competitive advantages

(1) Global Competitiveness IndexSource: National Manufacturing Competitiveness Council, IMaCS analysis

20

Key manufacturing sectors

Segment Industry size

Auto Industry• The Indian auto industry is a USD 64 bn industry (Automotives ‐

Auto IndustryUSD 45 bn, auto components ‐ USD 19 bn)

Chemicals• Size of the chemical industry in India (Petrochemicals to Paints)

is USD 40‐45 bn

Electronics• The electronics industry is estimated USD 20.5 bn (consumer

electronics to electronic components)

Engineering • A USD 22bn industry, including heavy and light engineering

Food Processing • Over USD 80 bn industry, growing at 9‐2%

• A USD 27 bn industry (Gold growing at 15% p a and Diamond atGems & Jewellery

A USD 27 bn industry (Gold growing at 15% p.a and Diamond at

27% p.a)

Leather • USD 6 – 7 bn

Textiles • USD 52 bn

Source: Feedback, Analysis Secondary sources21

Metal forming machinery user segments: Industry size 2008-09 estimates

Segments Value (Rs Cr) Examples of products

Domestic Production Imports Total

Automotive 192,500 10,000 202,500 Passenger cars, Commercial Vehicles, Two wheelers

Auto Ancillary 67,000 5,000 72,000 Transmission & Steering, Engine, Suspension & Braking, Body parts & Chassis

Communication 22,300 41,450 63,750 Mobile phones, Switching equipment, Transmission

Electrical 58 000 2 300 60 300 S itchgears Cables & Wires Motors TransformersElectrical 58,000 2,300 60,300 Switchgears, Cables & Wires, Motors, Transformers, UPS, Lighting

General Engineering 45,741 11,435 57,176 Construction equipment, Textile machinery, Engines, Boilers, Turbines, Bearings, Valves

Consumer Durables 17,701 1,129 18,830 Washing machines, Air‐conditioners, Refrigerators, iMicrowave Ovens

Plastic Components 15,700 2,200 17,900 Home equipment, Writing instruments, Molded furniture

Packaging 14,000 NA 14,000+ Plastic containers, Metal cans, Glass bottles, Caps and Closures

Computing 9,400 4,600 14,000 Monitors, Cabinets, Modems, Printers, Keyboards

Consumer Electronics 11,248 2,100 13,348 Video & Audio products, STB, Watches, Clocks

Others 83,100 1,200 84,300 Defense, Railways, Ship building, Medical equipment, Bath fittings, Hardware

Total Rs cr 536 690 81 414 618 104

Source: Feedback, Secondary sources

Total – Rs cr 536,690 81,414 618,104

Total USD bn 114 17 132 (1 USD = Rs. 47)

1. Industry listing based on the descending order of the industry size 22

Infrastructure improvements to spur manufacturing sector

Investment in infrastructure estimated at USD 125 bn between 2005 – 2010

Four laning 6,000 km of highways that link India’s top 4 metros is nearly

India’s long coastline (7,517 km) and the 12 major ports cater close to 90% of India’s

India has 450 airports, including 11international airports

Roads Ports Airports

top 4 metros is nearly complete (Golden Quadrilateral)

The project linking the ten j t f th t t

cater close to 90% of India s foreign trade in volume terms and 70% in value termsFDI investment up to 100%

airports

India plans to invest USD 5.07 bn in the next five years

major ports of the country to the GQ mentioned above is nearing completion

FDI investment up to 100%

ppermitted in the port sector. 18 port privatization projects worth USD 1.39B are under way (Private participants are P&O PSA Maersk

FDI investment up to 100% permitted in the airport sector

P i ti ti f N D lhipermitted in the road sector P&O, PSA, Maersk, Gammon India, CWC and Dubai Port Authority)

Privatization of New Delhi and Mumbai airports has been completed

Emphasis on infrastructure development would help Indian manufacturing to becomeEmphasis on infrastructure development would help Indian manufacturing to becomecompetitive

Source: IBEF, Feedback Analysis23

Indian manufacturing sector: Regulatory scenario

Central (Federal) GovernmentGovernment of India offers a fi t h lid f

State (Provincial) GovernmentEach State & Union Territory

five year tax holiday forPower projectsFirms engaged in exportsNew industries in notified states

y(UT) offers its unique industrial and sectoral policy and incentivesThe policies offered relate to i d t i l t t tRegulatory

Units in Electronic hardware, software parksEOUs and Free TradeZones

Tax deductions of 100% on

industrial estates, taxes, power tariff, capital investment subsidiesStates and UTs in India typically follow a Single Window

RegulatoryAdvantage

Better projecteconomicsTax deductions of 100% on

export profitsDeduction of 30% on net income for 10 years for new industries

follow a Single Window Clearance (SWC) mechanismCustomized packages designed for capital intensive projectsCompetition among the states

economics

dust esDeduction in respect of certain inter-corporate dividends

p gand UTs to attract investment proven to be beneficial for investors

Source: IBEF, Feedback Analysis

24

India as a manufacturing hub

Proximity to markets

Proximity to other Asian economies

Pro imit to emerging markets s ch as Africa

Proven product development capabilities

More than 125 Fortune 500 companies having R&D centers in India Proximity to emerging markets such as Africa

Shipments to Europe cheaper from India than from Brazil and Thailand

Companies can leverage on India’s acknowledged leadership in the IT industry

Availability of manpower

0.4 mn engineering graduates every year

7 l bl kf

Large and growing domestic demand

The rate of savings in India has increased steadily from 23.7% in

India as a manufacturing

Stable economic policies

Continuity in economic reforms and

7 mn employable workforce every year FY’01 to 37.7% in FY’08

Export potential

Growing as an export hub for

ghub

policies related to investments equipment and components

Competitive manufacturing cost

Skilled labor cost in India is among the lowest in the worldamong the lowest in the world

Source: Feedback Analysis, Secondary sources

25

Indian manufacturing sector: Recent developments

• Globally, India is being increasingly preferred for contract manufacturing, giving rise toopportunities in pharmaceuticals, auto components, consumer electronics and many moresegmentsGl b l i h i I di b i f th l t t i• Global passenger car companies are choosing India, being one of the low cost countries,to manufacture new generation compact cars

• The industry is seeing an increased number of global players moving to India, as thegovernment has permitted foreign players to set up 100% owned subsidiariesgovernment has permitted foreign players to set up 100% owned subsidiaries

• LG, Samsung, Louis Vuitton, Frette, Skoda Auto, Hyundai, Alstom, Toshiba, Ingersoll Randare some of the major companies, which are considering making India their globalmanufacturing hubs

• Focus on manufacturing optimization has increased, which is in turn being supported bythe developed Indian IT industry

• In India, medium sized manufacturing companies (with 100 to 999 staff) are presently thepredominant IT spenders creating solutions to cater to increased customer demand forpredominant IT spenders, creating solutions to cater to increased customer demand forhigh-quality products with reduced lead time, and the need for integration of differentbusiness functions, to combat competition

• Increasing pressure on lead time, costs and quality is making companies progress to thehub and spoke model of manufacturing. Every process in each multiphase manufacturingprocess, is handled by a hub attached with vendors as spokes

26

Indian manufacturing sector: Private + Govt. investments

Approx USD 650 - 800 bn worth investments are likely over the next 10 years

USD 200 bn investment in

powerpower

Source: Centre for Monitoring Indian Economy, Projects Today, Feedback Analysis

Values in USD bn27

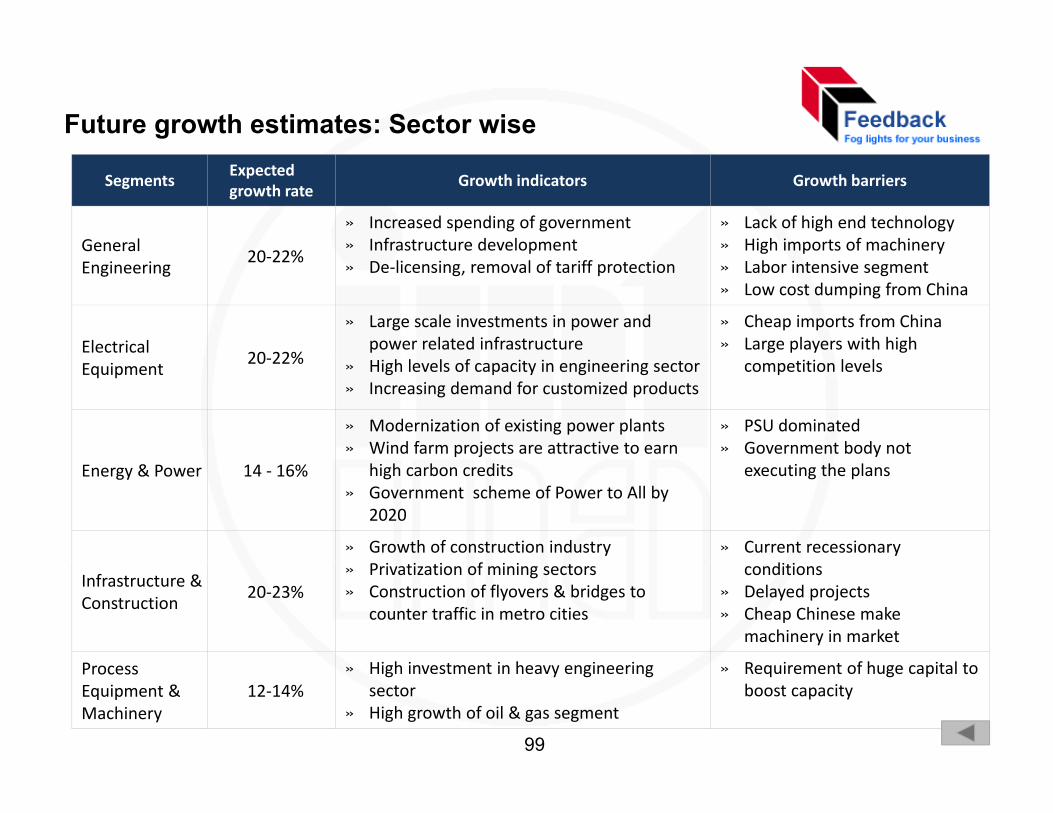

Industry growth drivers and growth rates

Industry Growth rates Drivers

Cement 8 - 10% • Infrastructure spending – Private and Government • Capacity enhancement to meet local & global demandy g• Construction industry growing at 8-10% • Capacity additions by large players• International players entering India

Metals 10 12% • Rapid growth in construction consumer goods and automotive sectorsMetals 10 - 12% • Rapid growth in construction, consumer goods and automotive sectors, which are the key users of metals – steel and aluminum

• Steel production projected at 100 mn tonnes by 2020• Zinc and Copper investments worth USD 40 bn over 5 years• Aluminium investments worth USD 15 bn over the next 5 years• Aluminium investments worth USD 15 bn over the next 5 years

Power 8 - 10% • 78,000 MW capacity during 11th plan (2007 – 2012) and 82,200 MW capacity during 12th plan (2012 – 2017)

• Multi sector investments in metals like steel, copper, aluminum likely to drive growth in the power sectordrive growth in the power sector

Chemical 6 - 8% • Focus to meet local and global demand, key driver for the chemical sector• Resultant inflow of FDI and technology transfers has created an

environment for dynamic growthI di i l b l i h b l i t titi• India emerging as global sourcing hub – leveraging cost competitiveness

Source: Feedback Analysis, Secondary sources

28

Industry growth drivers and growth rates

Industry Growth Drivers

Paper & Pulp

8 - 10% • Decrease in duty levels has brought domestic prices in line with international prices –hence demand for local production

• Government impetus in educational sector has increased demand• 122 projects worth USD 1800 mn were announced in 2007, 51% currently under

implementation• Capacity additions which grew at a CAGR of 25%, likely to reduce over the next two

t thto three years• Projects worth Rs. 970 mn (USD 19.4 mn) were announced in 2008 alone

Sugar 7 - 8% • Increase in area of sugarcane production from 3.1 mn acres to 3.8 mn acres• In 2007, projects worth USD 872 mn were announced; 43% of them are currently

under implementation• In 2008, projects worth USD 960 mn were announced

Rubber 6 - 8% • Demand and supply gap – potential for local manufacturing• Industry expected to grow at 8% and production at 3%Industry expected to grow at 8% and production at 3%• Investments in automobile sector – Global OEMs and introduction of newer models

Mining 3% • Sector open to private players for exploration; share of private sector mines to increase to 18% from the present 7%

• Government focus on mechanization – growth in continuous mines and underground• Government focus on mechanization – growth in continuous mines and underground mine production to reach 50 bn Tons in 2012 from 10 mn Tons in 2008

• Coal reserves of 20 bn Tons to be de-blocked for power projectsSource: Feedback Analysis, Secondary sources 29

Metal forming machinery industry Global trends- Global trends

• Metal Forming Machinery Production and consumption by country

• Machine tools Imports and Exports by country

• Technology trends and developments

30

Global metal forming machinery production by country

4500

Values in USD mn

13%30%

21%

India ranks 19th

Global metal forming machinery industry valued at USD 22 bn in 2008

Production share Global Vs India

3000

3500

4000 21%Metal forming machinery only

% indicates growth over previous year

Production share – Global Vs India

1500

2000

2500

2007

2008

11%

-8%

0

500

1000

16%

11% -7% 12% 14% 15% 30% 7% 0% 14% 12%0%0%-1%

11%11%

11% 9%12%7%6%14%

11%

India’s contribution to the world’s production of metal forming machinery is less than 1%

Despite widespread recession in the latter part of the year, the total world output rose 15% in 2008. The

Indian figures based on Feedback estimates Source: Gardner Publications

Despite widespread recession in the latter part of the year, the total world output rose 15% in 2008. The 28 countries listed above produced an estimated USD 81.5 bn worth machine tools last year, compared to shipments of USD 71 bn in 2007

31

Global machine tools consumption by country

18,000

20,000

Values in USD mn

20%

Also includes machine tools

% indicates growth over previous year

Global machine tool consumption valued at USD 76 bn in 2008

Machine tool consumption share –Global Vs India

12,000

14,000

16,000

33%

Global Vs India

6,000

8,000

10,000

2007

2008

5%

15%13%

21%-12%

0

2,000

4,00040%

6% 31% 10% 15% -5% -3% 1% 62% 32% 15%33%13%0%9% 0%

12% -3%0%13%3%

-21%

India is the 9th largest consumer of machine tools in the world

Global metal forming machine consumption grew by 12% in 2008, while Indian consumption rose by 73%

Indian figures based on Feedback estimates Source: Gardner Publications

during the same period

32

Global machine tools imports by country

8,000

9,000

10,000

Values in USD mn

6%

% indicates growth over previous year

5,000

6,000

7,000

8,000

14%

19%

2,000

3,000

4,0002007

200817% -34%

79%

2% 5%14%-1%13%

4%0%

0

1,00028% 0% 3% 14% 9% -1% -5% 38% 70% 15%31%0%10%

0% 3%2% 5%14%

India is the 7th largest importer of machine tools in the world

Indian imports of machine tools grew by 4% in 2008, while metal forming machinery imports grew at a CAGR of 50% between 2005-08

Indian figures based on feedback estimates Source: Gardner Publications

New machine imports grew at 59%, whereas used machine imports grew by 13.6% in the same period

33

Global machine tools exports by country

12,000

Values in USD mn

10%

% indicates growth over previous year

8,000

10,00015%

4,000

6,000

2007

2008

15%

12%

3%

15%27%

0

2,000

15%

9% -2% 10% 1% -4% 0% -3% 0% -20% 33%15%11%32%28% 20%

-7% 11%20%11%20%

6%27%

Indian saw a 20% decline in exports due to recessionary factors; the average price of metal forming machinery exported from India dropped by 22% in 2008, when compared to 2007

Indian figures based on feedback estimates Source: Gardner Publications

Germany, Japan and Italy are the large exporters

34

Technology trends by product category

Product category

Technology developments ‐ Global Technology developments ‐ India

Presses » Energy efficient running systems and » Automatic set forming machines to save time gy g yoperating mechanisms

» Micro‐precision press for advanced technology fields

» Servo technology for optimal motor drive control

g» Need for eco friendly products will increase the usage of servo motor & drive usage across the machines

» Operator friendly machines

control

Sheet metal working

» Automatically set forming criteria and conveying time

» Safe & silent forming » Forming of hard to work material

» High tonnage machines which can form hard to work material, due to growing auto & aviation sectors

» Enhanced running efficiency» Maintenance free machines» Forming of hard to work material » Maintenance free machines

Sections » Multi operational machines to save time » Eco friendly machines to reduced waste and toxicity; Light, durable, enhanced recycling

» Machines compatible with sequential forming recurring material replacement time will be preferred

» Increased focus on technology upgrade will shift the demand towards automated precise forming machinesdemand towards automated precise forming machines

Others » Forming of hard to work materials» Composite forming» Vibration forming, promoting enhanced formabilit and dr processing

» Enhanced formability by hydro forming machines will increase its acceptance

» Increased usage of stainless steel will create shift in sage of higher capacit precision machinesformability and dry processing usage of higher capacity precision machines

35

Global technological trends (1/4)

Forming machine technology that contributes to net-

Ultra-precision, high rigidityImproves mother machine dynamic geometrical precision (slide and bolster straightness, parallel positioning, angles, bottom dead center eccentric load etc)shape forming center, eccentric load, etc)

High-performance with digital controlOptimal slide motion controlOptimal press moving part pressure force, speed, and positionDynamic geometrical accuracy controlElastic deformation, bottom dead center position control

Forming machine technology that contributes to energy

Energy efficient running systems and operating mechanismsServo technology for optimal motor drive controlReduced friction drag, lubrication free sliding partscontributes to energy

and resource conservation

g, g pMulti operational machines to save time

Controls such as up-down, left-right, forward-reverse operations in single machine

36

Global technological trends (2/4)

• Compact structure (resource, energy efficient)– Net shape forming with high‐precision, highly rigid press

Forming machine technology that

ib – Benefits of reducing workplace size (installation area, height)

– Reducing material and energy costs

– Enhancing LCA (life cycle assessment)

Improved performance In line forming

contributes to energy and resource conservation

– Improved performance In‐line forming

• Universal applicability– One unit performs the functions of a wide variety of press

machines

– Double & triple action presses with cutting and shearing applications

• Forming of hard to work materialsSlid i d i di i– Slide motion, speed setting discretion

– Localized heating, temperature control

• Composite formingMulti process forming– Multi‐process forming

– Module press

37

Global technological trends (3/4)

• Safety– Combine safety and productivity

Operator friendly metal forming

hi • Silent forming– Low vibration and noise

• Dry press forming

machines

– Emission free

• Maintenance free for production management, preventive maintenance, malfunction diagnosis

• Enhanced r nning efficienc• Enhanced running efficiency– Automatically set forming criteria and conveying time

– Automatically replace die and material

– Forming simulation and press dockingForming simulation and press docking

38

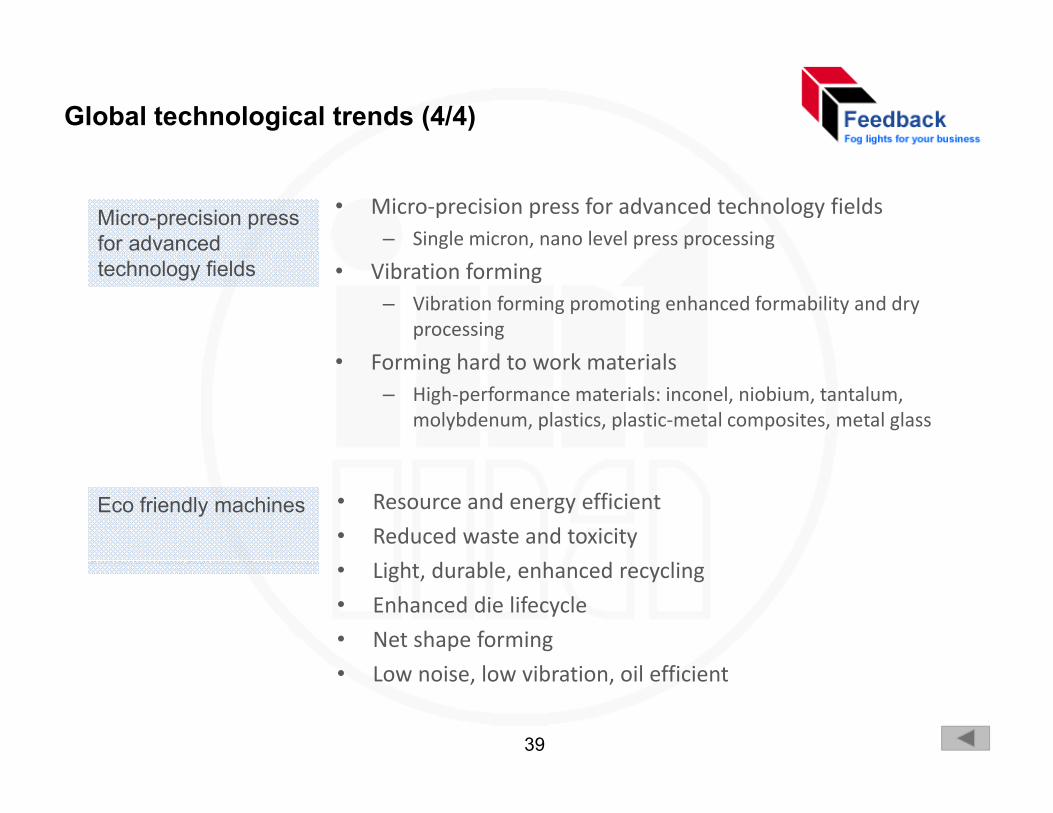

Global technological trends (4/4)

• Micro‐precision press for advanced technology fields– Single micron, nano level press processing

Micro-precision press for advanced

• Vibration forming – Vibration forming promoting enhanced formability and dry

processing

F i h d k i l

technology fields

• Forming hard to work materials– High‐performance materials: inconel, niobium, tantalum,

molybdenum, plastics, plastic‐metal composites, metal glass

• Resource and energy efficient

• Reduced waste and toxicityEco friendly machines

• Light, durable, enhanced recycling

• Enhanced die lifecycle

• Net shape forming

• Low noise, low vibration, oil efficient

39

Metal Forming Machinery Industry in IndiaIndustry in India • Industry structure

• Product offerings – Indian and International manufacturers

C i f I di d i t ti l f t• Comparison of Indian and international manufacturers

• Customer perceptions

• Challenges faced by the metal forming machinery manufacturers

40

Metal forming machinery: Product landscape

Metal forming machinery

Presses Sheet metal working Sections

Mechanical Presses Press Brakes Tube forming

Others

Forging machines/ Hydraulic Presses Servo PressesC-Frame PressesCoining Presses

Punch Press

Shears

Laser cutting Machines

machines

Bar and angle shearing

Tube Bending

Hammers

Die casting machines

Hydro-forming machines

Fine Blanking PressesTransfer PressesKnuckle Joint PressesPowder Compacting

Machines

Bending and Rolling Machines

Water Cutting

Tube Bending machines

machines

Extrusion machines

Wire forming machines p g

PressesFriction Screw PressesTrimming PressesDie-spotting presses

gMachines

Plasma Cutting Machines

Thread/Spline rolling machines

Spring coiling machinesp g p machines

41

Metal forming machinery: Industry structure

Parameters

Domestic manufacturers Imports

Large Medium Small Imports (N hi )

Imports (U d hi )(New machines) (Used machines)

Number of players

5 15 50 10 15

Select names ISGECHindustan

Nugen MachineryBajaj machinery

Basant WorksAnjani

AmadaAida

Techno Crafts Divehi Tools Die

HydraulicSEWElectroPneumaticBEMCO

j j yEmco Press mastersEnergy MissionJekson MachineryBemco Hi tech

jTechnoplast KB HydraulicsManookSPM ControlsPress well

LVDShulerKomatsuSeyiChinfong

Casting IndiaMachino ImpexoMatrix Capital NetworksBEMCO

hydraulicsBemco Hi‐tech Press well

HydraulicsHensel IndiaPress & Press Tools

ChinfongElectonica

NetworksSri Durga Agencies

Manufacturing capability

» Presses 10 –3000T

» Presses 10 – 1000T » Presses 10 – 250T » All ranges » All ranges

Turnover range (Rs cr)

» 30 – 150 » 10 – 15 » 2 – 8 » 50 – 400 » 2 – 6

New machine importers also include import agents like Magal, Electonica, Batliboi, etcDomestic manufacturers and importers can supply convention, NC and CNC range of machines. Differentiation is in the proprietary software and in-house kit development capabilities

42

Metal forming machinery manufacturers: Geographical presence and clusters

ISGEC

Hindustan HydraulicsBasant Mechanical WorksMankoo India Pvt. Ltd.

Bajaj Machine ToolsEmco Press master Pvt Ltd.Anjani Technoplast Ltd.KB Hydraulics

New Delhi & NCR

LudhianaYamuna nagar

M.S.S.S. Mechanical WorksMankoo Machine Tools Pvt LtdRavi Industrial CorporationBasant IndustriesMilap Heavy EngineersM M hi T l

KB HydraulicsPress wel IndustriesAshok Manufacturing Company

Komatsu IndiaAid

Ahmedabad

Mann Machine Tools

Nugen Machines LtdEnergy MissionJekson Machinery Pvt Ltd

Rajkot

AidaMD Corp.Machine Toll AssociatesAssociated Technocrats

MumbaiPune

Belgaum

yPress & Press toolsFlu - tec

Press well HydraulicsViraj Hydraulics

Singhal Engineering Works

Schuler IndiaAmada IndiaEmpire Machine tools

BangaloreViraj HydraulicsJayshakthi Machine tools

l DBemco Hydraulics

ElectroPneumatic

Hensel India Pvt LtdElectronic

Key pockets

Magal LVDy

Bemco HitechSPM ControlsSudhir HydraulicDomestic manufacturers Importers

43

Domestic supplier offerings: Presses and Sections

Indian Manufacturersclassification

Companies

Presses Section

-Fra

me

chan

ical

ydra

ulic

Serv

o

rans

fer

-spo

tting

imm

ing

oini

ng

ckle

Joi

nt

on S

crew

Bla

nkin

g

owde

r m

pact

ing

and

angl

e ng

/pun

chin

g

e B

endi

ng

e fo

rmin

g

classification

C-

Mec Hy S Tr

Die

-

Tri C

Knu

c

Fric

ti

Fine

P oC

om

Bar

ash

earin

Tube

Tube

ISGECHindustan hydraulicsLarge hydraulics ElectropneumaticsSEW

Bemco Hydraulics Bajaj Machine Tools

Medium

Emco Pressmaster Energy Mission

Jekson Machinery Bemco Hitech

Small

Basant MechanicalAnjani Technoplast KB HydraulicsMankoo India Pvt. M.S.S.S. MechanicalMankoo MachineSPM Controls

Presence Note: The list does not include the complete list of suppliers covered44

Domestic supplier offerings: Sheet metal working machinery

Indian Companies

Sheet metal working

Brak

es

ars

g an

d ac

hine

s

Pres

s/

Punc

h ss se

r TPP

in

es

Cut

ting

ines

bras

ive

uttin

g in

es

Manufacturersclassification

Pre

ss B

Shea

Bend

inR

ollin

g M

Pun

ch P

Turr

et P

Pre

Lase

r/Las

Mac

h

Pla

sma

CM

ach

Wat

er/A

bJe

t Cu

Mac

h

LargeISGECHindustan hydraulicsLarge Hindustan hydraulics

Singhal engineering works

Medium

Nugen MachinesBajaj Machine ToolsEnergy Mission Jekson MachineryJekson Machinery Bemco HitechAnjani Technoplast Mankoo IndiaSPM Controls Ravi Industrial Corporation

SmallMilap Heavy EngineersPress & Press tools Flu - tecViraj Hydraulics Jayshakthi Machine tools

Presence Note: The list does not include the complete list of suppliers covered

Ashok Manufacturing Co

45

New imported brands offerings: Presses

Segment Companies

Presses

me ical

ulic

o er

tting

ng

ng

Join

t

Scre

w

nkin

g

er

ctin

g

Segment Companies

C-F

ram

Mec

han

Hyd

rau

Ser

vo

Tran

sfe

Die

-spo

t

Trim

mi

Coi

nin

Knu

ckle

J

Fric

tion

S

Fine

Bla

n

Pow

deC

ompa

c

Importer Komatsu Indianew machine Schuler India

Amada India

Empire Machine toolstools

Magal LVD

Komatsu India

Aida

MD Corp.

Associated Technocrats

Importer old U d hipmachine Used machine

Presence Note: The list does not include the complete list of suppliers covered

46

New imported brands offerings: Sheet metal working and Sections

Segment Companies

Sheet metal working Section

s B

rake

s

hear

s

ding

and

R

ollin

g ac

hine

sPu

nch

ss/T

urre

t ch

Pre

sser

/Las

er

Mac

hine

s

ma

Cut

ting

achi

nes

r/Abr

asiv

e C

uttin

g ac

hine

san

d an

gle

ing/

punc

hin

g

Ben

ding

ac

hine

s

e fo

rmin

g ac

hine

s

Pre

ss Sh

Bend R Ma P

Pre

sPu

ncLa

seTP

P

Plas

mM

a

Wat

erJe

t M

aB

ar a

shea

r

Tube m

a

Tube ma

Importer new machine

Komatsu India

Schuler India

Amada India

Empire Machine tools

Magal LVD

Komatsu India

Aida

Batliboi

Electronica

MD Corp.Associated Technocrats

Importer old machine Used Machine

Presence

Note: The list does not include the complete list of suppliers covered

47

Domestic manufacturers: Segmental focus

IndianMfrs category

Company

Auto

mot

ive

Aut

o C

ompo

nent

s

Con

sum

er

dura

bles

Kitc

hen

equi

pmen

ts

Gen

eral

en

gine

erin

g

Ele

ctric

al a

nd

elec

troni

cs

Ene

rgy

&

pow

er

Infra

&

Con

strn

Proc

ess

equi

pmen

t

Rai

lway

s

Offi

ce

equi

pmen

t

Shi

p bu

ildin

g

Oth

ers

ISGEC

LargeHindustan hydraulics ElectroPneumaticSinghal engineering worksBemco Hydraulics Nugen Machines LtdBajaj Machine ToolsE P tMedium Emco Pressmaster Energy Mission Jekson Machinery Bemco HitechBasant Mechanical WorksAnjani Technoplast KB HydraulicsKB HydraulicsMankoo India M.S.S.S. Mechanical WorksMankoo Machine ToolsSPM Controls Ravi Industrial CorporationPresswel Industries

Small Basant IndustriesMilap Heavy EngineersHensel India Press well Hydraulics Ashok Manufacturing Company Press & Press tools Fl tFlu - tecViraj Hydraulics Jayshakthi Machine tools Mann Machine Tools

48

Imported brands: Segmental focus

Segment Company

tom

otiv

e

Com

pone

nts

onsu

mer

ur

able

s

Kitc

hen

uipm

ents

Gen

eral

gi

neer

ing

ctric

al a

nd

ectro

nics

gy &

pow

er

stru

ctur

e &

ns

truct

ion

Proc

ess

uipm

ent

ailw

ays

e eq

uipm

ent

p bu

ildin

g

Oth

ers

Aut

Aut

o C Co du K

equ G

eng

Elec ele

Ene

rg

Infra

sco

n P eq R

Offi

ce Ship O

Komatsu India

Schuler India

Amada India

Empire Machine tools

Magal LVD

Importers Komatsu India

Aida

Batliboi

ElectronicaElectronica

MD Corp.

Associated TechnocratsMachine TollMachine Toll Associates

49

Domestic manufacturers Vs Importers: A comparison

Parameters Domestic manufactures Imported suppliers

Product portfolio » Capability to manufacture a wide range of machinery but lack of experienceL l l f i i

» Complete product portfolio for continuous press line L h l l b l d d d» Low level of customization

» Presses ‐ the only strong product line» Latest technology, global standards, accepted

across customer segments

Reach » Only 8 manufacturers with national presence

» National presence» Customers look for specific brands, normally

» High instance of small players active in a specific cluster for specific machinery

operate through dealers

Technology » The domestic manufacturers have not graduated to a higher level of reverse

i d d

» Have complete solution for each process line (A‐Z solution) Hi h l l f i iengineered products

» Focus on machinery sales and not on solutions

» High level of customization » High level of automation with minimum

human intervention to increase productivity & quality of end product

M f t i O l 2 4 f t d R&D H t R&D t t d t thManufacturing capabilities

» Only 2 – 4 manufacturers spend on R&D » Focus on select product ranges

» Have strong R&D team to upgrade to the latest technology

» Offer complete solution (packaged offering)

50

New Vs Used imported machinery: Application areas

Imported machinery supply

Machinery detailsProduct applications

Sector Applications Reason for preferring imported machinerysupply ppimported machinery

Complete press line Auto OEMSkin panel pressing & blanking

To boost productivity

Consumer Bending & piercing of Low maintenance & highNew machines

Mechanical pressConsumer durables

Bending & piercing of sheet metal

Low maintenance & high accuracy

Tube bending machine

Consumer durables

For bending copper tubes

Best in the industry & value added features

Bending & rollingShi b ildi Sh b di

Lack of efficient domesticBending & rolling machine

Ship building Sheet bending Lack of efficient domestic suppliers

Punch press General engineering

Sheet bending for outer cover of a machine

Not a critical application, only for bending & is cost effective

Used machines

Bending & rolling machine

Energy & power For bending the body of boiler

Cost effective solution to get the desired accuracy , better than the local machineries

Pl tti A t P i d 50% l thPlasma cutting machine

Auto components

Cutting sheet metal Priced 50% lower than new machines

51

Domestic manufacturers Vs Importers: Marketing set up

Parameter Domestic manufacturers Importers

Marketing setup

» Large players have marketing offices inkey consumption pockets

» Large players have marketing offices inIndiap y p p

» Marketing – 2 to 4 personnel at eachoffice

» Service – 2 personnel in key pockets

M di & ll i t t

» Marketing ‐ Dedicated, 4‐5 personnelfor all India coverage

» Service ‐ 2 to 3 personnel across regions

Readily available spares & service» Medium & small companies operate outof head office

» Marketing – 1 or 2 personnel coveringthe entire region

» Readily available spares & service

» Small time importers have sales agentsin India

» 1 to 2 marketing personnel for all India» Service – 2 – 3 personnel covering the

entire region

» Medium & small players have limitedreach and limited product offering

» Availability of spares a concern withsmall importers

» Used machine importers have strongpresence in key consumption pockets

» Availability of spares is an issue withmedium & small players

presence in key consumption pockets

» Do not have a marketing setup

» Marketing done through magazines,internet, exhibitions

» Few used machine suppliers also intorefurbishing of old machinery

52

Domestic manufacturers Vs importers: Target segment

Parameter Domestic manufacturers Importers

Targeted segment

» Leading players target large OEMs, fabricators etc

» Leading brands focus on large OEMs and integrated turnkey solutionssegment fabricators, etc

» Segments catered to – Auto, auto components, general engineering, ship building, railways, process equipment electrical

integrated turnkey solutions

» Segments catered – Auto OEMs, tier 1 auto component manufacturers, railways, ship building, consumer durables, defense

f dequipment, electrical

» Medium & small companies target tier 2 auto component manufacturers, sheet metal workers, electrical,

i t kit h

» Auto components ‐ preferred segment across medium and small importers (brands)

» Tier 1 & 2 auto components process equipment, kitchen equipment manufacturers

» MNCs do not buy machinery from Indian manufacturers

manufacturers, Railways, general engineering, consumer durables, process equipment, etc

» Used machine importers target small time

» Technology transfer from parent company

» Parent company specifies the machinery details and brand

fabricators and small scale industries

» Segments catered – small time fabricators, enclosure manufacturers, office equipment manufacturer, kitchen

i l i iequipment, general engineering

53

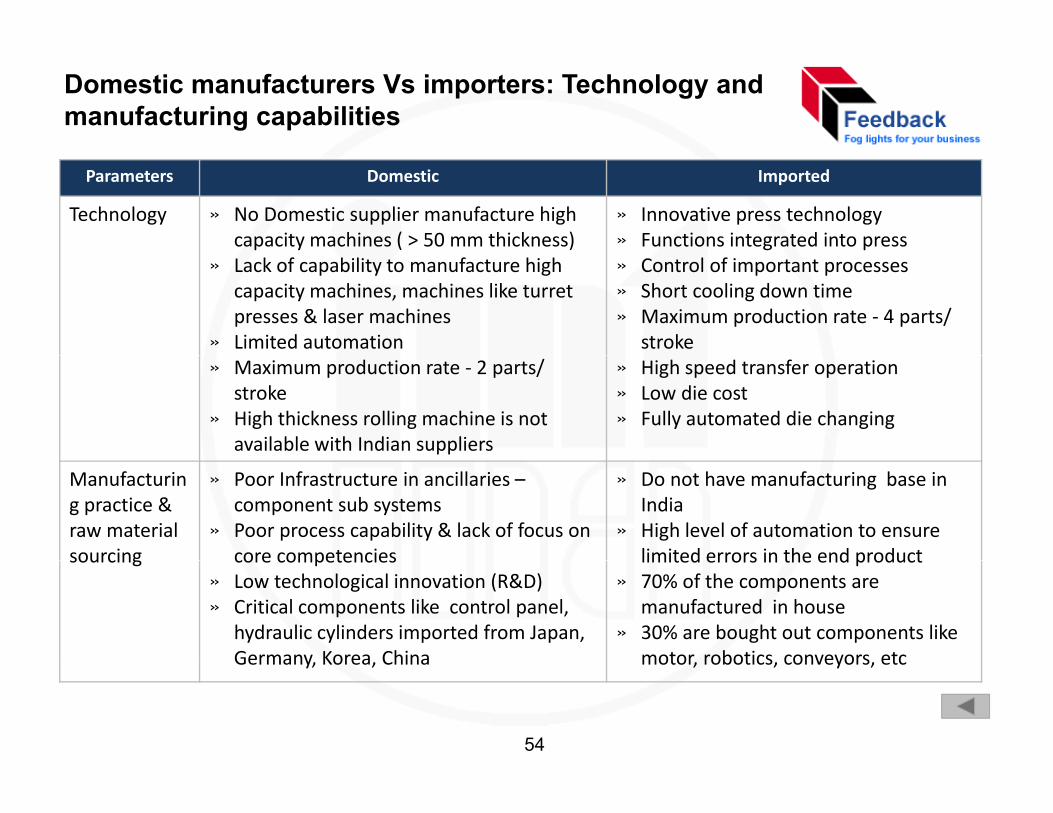

Domestic manufacturers Vs importers: Technology and manufacturing capabilities

Parameters Domestic Imported

Technology » No Domestic supplier manufacture high capacity machines ( > 50 mm thickness)

» Innovative press technology » Functions integrated into press

» Lack of capability to manufacture high capacity machines, machines like turret presses & laser machines

» Limited automation

» Control of important processes» Short cooling down time» Maximum production rate ‐ 4 parts/

stroke » Maximum production rate ‐ 2 parts/

stroke» High thickness rolling machine is not

available with Indian suppliers

» High speed transfer operation » Low die cost » Fully automated die changing

Manufacturing practice & raw material sourcing

» Poor Infrastructure in ancillaries –component sub systems

» Poor process capability & lack of focus on core competencies

» Do not have manufacturing base in India

» High level of automation to ensure limited errors in the end productsourcing core competencies

» Low technological innovation (R&D)» Critical components like control panel,

hydraulic cylinders imported from Japan, Germany, Korea, China

limited errors in the end product » 70% of the components are

manufactured in house » 30% are bought out components like

motor, robotics, conveyors, etc

54

Germany, Korea, China motor, robotics, conveyors, etc

Domestic manufacturers Vs Importers: Customer perceptions

Parameter Domestic manufacturers Importers

Availability » Imported spare parts, lead time an issue» Technical assistance requires focus

» Maintain inventory of spare parts» Technically competent serviceq

» Only large manufacturers have ownspare parts division

» Lack in CNC programming and softwaredevelopment

y pengineers – high uptime

» Chinese spares considered to becheap, cost effective

» Used machines readily available inp» Poor product design

ythe international market

Performance » Maximum production rate ‐ 2 parts/stroke

» Higher production rate ‐ 4 parts/strokestroke

» Poor product lifecycle, required to go infor retrofitting after 5 – 6 years

» Indian manufacturers have notgraduated to the higher level of reverse

stroke» Increased machine life, retro fitting

done after 10 years of usage» New machine technology for

different applicationsgraduated to the higher level of reverseengineering, like the Japanese & Koreanfirms

» Conventional machines becomeextremely productive and flexible by

different applications» Fully automated die changing

mechanism, improves productivity

extremely productive and flexible byretrofitting them with CNC controllers

55

Customers verbatim on Indian manufacturers’ capability to innovate and compete with imported brands

» “Designing of most of the Indian made machines considered to be more conventional &market driven, rather than technology driven”

» “Domestic manufacturers’ core competency lies in manufacturing low cost & reasonablypriced metal forming machines”

» “The capability to conceptualize a product to achieve certain design & performancep y p p g pcharacteristics (Design & performance wise) is not found in Indigenous metal formingmachines”

» “Only a few large players have technology tie ups with foreign players and are able toy g p y gy p g p ycompete with imported machineries”

» “Machinery manufactured by major players in India is through technology transfer fromMNCs & it is seen that, whenever technology transfer happens, a gap always exists where, gy pp , g p ythe receiver ends up with lower/ obsolete technology than what the supplier has”

» “The R&D capabilities are limited to 5-6 major players only and most of them are involved insolving problems that arise in manufacturing, rather than developing new technology driveng p g, p g gyproducts”

56

Metal Forming Machinery Market estimates– Market estimates

• Approach and Methodology • Overall market, 2008-09 as the base year• Market estimates by:

– Type of machinery– Import Vs Domestic manufacturing

D ti f t i l t– Domestic manufacturing clusters

57

Metal forming machinery: Market estimate - Approach and Methodology

Suppliers classified as large, medium, small and Methodology includes rigorous field coverage and secondary research

Methodology

pp g , ,Importers based on capacity, production, sales,

spread, brand & other relevant criteria

Universe of suppliers estimated

yTop down approachPersonal interviews conducted with individuals across 25 organizations

Time frame: October December 2009

All large players met, sampling of importers, medium and small players across regions to ensure

Universe of suppliers estimatedTime frame: October - December 2009

2008-09, base year with forecast until 2015The study focuses on metal forming machineryOur assessment includes machinery manufactured

Total turnover estimated at product type, segment type & region

geographic spreadin India, imported new machines and used machinesThe emphasis is on value rather than volumeUnit used to represent the market in this presentation is in Rs Crore, unless specified otherwise

Survey norms extrapolated to relevant universe of suppliers

otherwiseTo maintain the confidentiality of the business transactions the supplier names (Domestic manufacturers and Importers) are not represented in the relevant market

Aggregated to arrive at total marketAggregated to arrive at total market

are not represented in the relevant market information charts

58

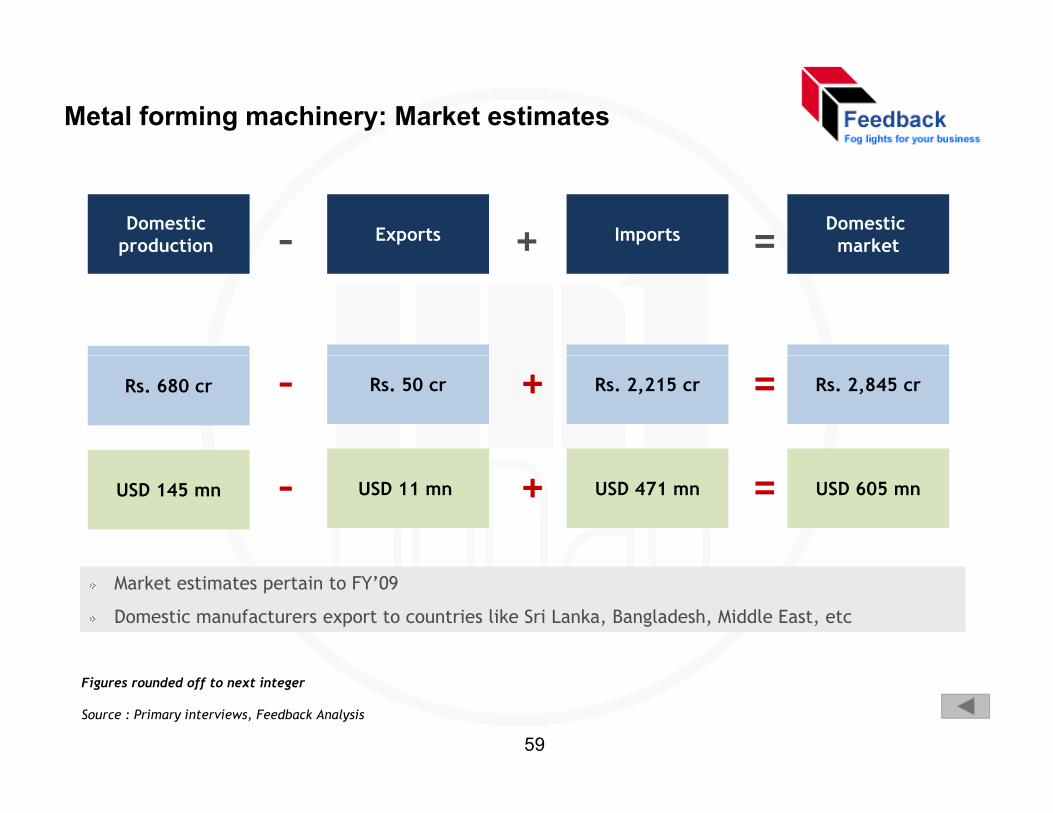

Metal forming machinery: Market estimates

Domestic market

Domestic production ImportsExports =+–p

+–Rs. 680 cr Rs. 50 cr Rs. 2,215 cr Rs. 2,845 cr=

+–USD 145 mn USD 11 mn USD 471 mn USD 605 mn=

Market estimates pertain to FY’09

Domestic manufacturers export to countries like Sri Lanka, Bangladesh, Middle East, etc

Source : Primary interviews, Feedback Analysis

Figures rounded off to next integer

59

Imported machinery accounts for over 3/4th of the total consumption in India

Domestic manufacturing by manufacturers

Imported Vs Domestic supply

Value : Rs. 630 Cr ( USD 134 mn)

Imported machinery market by manufacturers

Value : Rs. 2,845 Cr (USD 605 mn)

Value : Rs.2,215 Cr (USD 471 mn)Figures rounded off to next integer

60

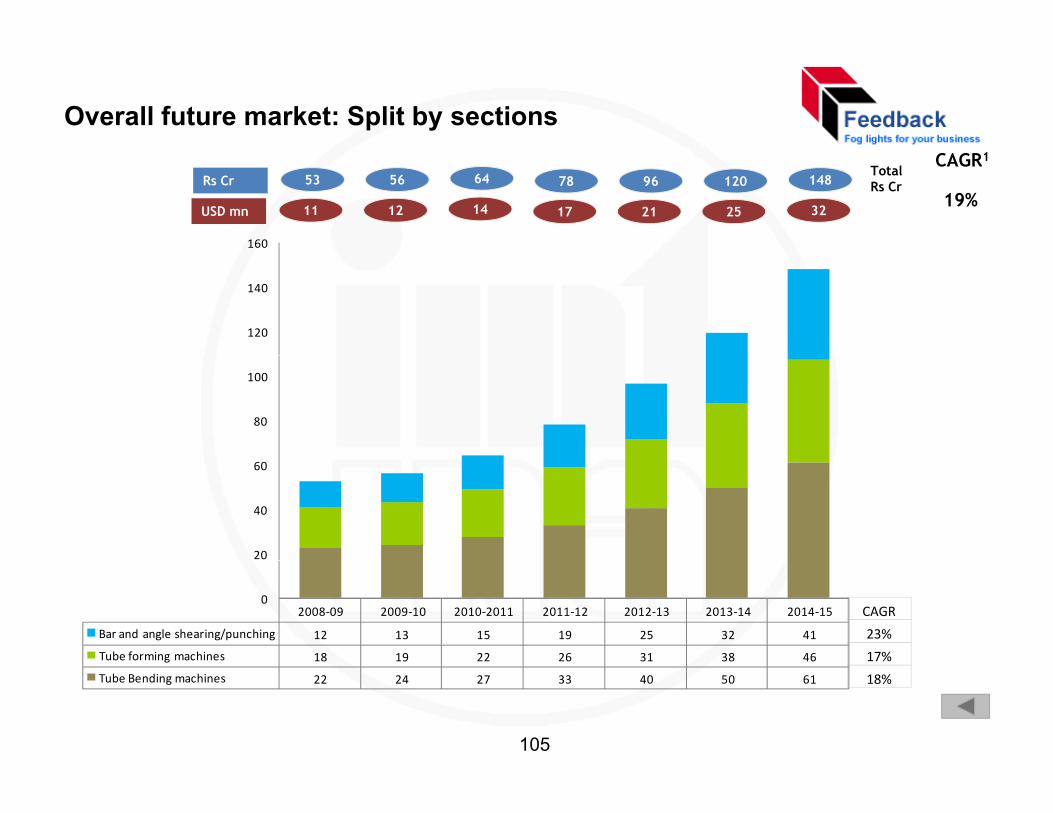

Metal forming machinery market: By type of machines

Others In Rs. crore Die casting machines 87Extrusion machines 45Hydro forming machines 35

Sections In Rs. crore

Tube forming machines 18

35Forging machines/Hammers 35Wire forming machines 7Gear rolling machines 3Spring coiling 6

Tube Bending machines 22

Bar and angle shearing/punching

12

PressesIn Rs. Sheet Metal Working In Rs. crore

Thread/Spline rolling machines 7

Total 225Total 53

Pressescrore

Mechanical Presses 30‐ 4000+ T 710Hydraulic Presses 30‐4000+ T 330Servo Presses 115C‐Frame Presses 70C i i P 40

Laser/Laser TPP Machines 305

Press Brakes 275

Punch Press/Turret Punch Press 235

Value : Rs. 2,845 cr

USD 605 mnCoining Presses 40Fine Blanking Presses 40Transfer Presses 35Knuckle Joint Presses 30Trimming Presses 25Friction Screw Presses 15

Plasma Cutting Machines 150

Shears 90

Bending and Rolling Machines 65

W t / Ab i J t C tti Friction Screw Presses 15Powder Compacting Presses 13Die‐spotting presses 6Total 1,430

Water/ Abrasive Jet Cutting Machines

20

Total 1,140

Figures rounded off to next integer 61

Metal forming machinery market: By consumption segments

Value : Rs. 2,845 cr (USD 605 mn)

Auto & auto components account for 36% of the total metal forming machinery consumption in India

62

Domestic production of metal forming machinery by clusters

Metal forming machinery X Clusters Ahmedabad Bangalore Belgaum

Delhi / NCR Ludhiana Mumbai Pune Rajkot Others1 Total

Hydraulic presses 14 ‐ 30 36 18 0 7 3 45 153

Die‐spotting presses ‐ ‐ 3 ‐ ‐ ‐ ‐ ‐ ‐ 3

C‐Frame presses 3 ‐ 2 1.3 13 22 5 4 32 82.3

Presses

Transfer presses ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 0

Trimming presses ‐ ‐ 0.8 ‐ ‐ ‐ ‐ ‐ 1.22 2.02

Knuckle Joint ‐ ‐ ‐ ‐ 6 ‐ ‐ ‐ 8 14

Coining Presses ‐ ‐ 0.8 ‐ ‐ ‐ ‐ ‐ 1.2 2

Friction Screw ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 0

Fi Bl kiFine Blanking ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 0

Servo presses ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 0

Powder Compacting ‐ ‐ ‐ ‐ ‐ ‐ 2 ‐ ‐ 2

Mechanical presses 1 6 ‐ 135 24.3 ‐ ‐ ‐ 72 238.3

Press Brakes 13.35 ‐ 0.75 5.14 19.25 2.45 ‐ 2.8 26 69.74

Sh 13 4 3 1 2 6 1 2 45 1 55 32 5 60 2

Sheet

Shears 13.4 ‐ 3 1.2 6.1 2.45 ‐ 1.55 32.5 60.2

Bending and Rolling 2 ‐ ‐ 1.37 ‐ ‐ ‐ ‐ 2.7 6.07

Water/Abrasive Jet Cutting 2 ‐ ‐ 4.8 ‐ ‐ ‐ ‐ 11 17.8

Laser/Laser TPP ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 0

Plasma Cutting 1 6 2 6 4 2Sheet metal working

Plasma Cutting ‐ ‐ ‐ 1.6 ‐ ‐ ‐ ‐ 2.6 4.2

Punch Press/Turret Punch Press ‐ ‐ ‐ 2.1 ‐ ‐ ‐ ‐ 3.4 5.5

Bar and angle shearing/punching ‐ ‐ ‐ 1.9 ‐ ‐ ‐ ‐ 2.4 4.3

Tube Bending ‐ ‐ ‐ ‐ ‐ ‐ 14 ‐ ‐ 14

Sections Tube Bending 14 14

Tube forming ‐ ‐ ‐ ‐ ‐ ‐ 3.9 ‐ ‐ 3.9

Grand Total 48.75 6 40.35 190.41 86.65 26.9 31.9 11.35 240 682.33

Grand Total – USD mn 10.4 1.27 8.6 40.5 18.4 5.7 6.8 2.4 51 1451Others include – clusters such as Auragnabad, Jalandar, Kolhapur etc and the extrapolated numbers for other manufacturers

All values in Rs. cr63

Imported machinery break up – New machines Vs Used Machine

Total imports – Rs 2,215 croreNew Vs Used

machinery

New machinery – 1,975 (89%) Used machinery – 240 (11%)

By type

Presses 857

(43%)

Sheet metal working

955 (48%)

Sections34

(2%)

Others128 (7%)

Presses113

(47%)

Sheet metal working

32(13%)

Sections1 (1%)

Others94

(39%)

2024 6.8 0.21182 203 7.2 27.2USDmn

Nearly 90% of the imported machinery are new machines

Values in Rs. cr

% indicates the contribution to total imports

64

Market estimates by segmentsMarket estimates by segments

65

Auto sector: Metal forming machinery consumption estimated at Rs 628 cr

Split by Players (Domestic) Split by Players (Imported)

Value : Rs. 42 Cr (USD 8.9 mn) Value : Rs. 586 Cr (USD 124.7 mn)

Dominated by company 1 (49%) followed bycompany 2

Company 1 sales strong in mechanical pressesfor auto segment

L t hi li d b ll

Importer 1 contributing to 68% of the totalauto OEM industry consumption

2 mechanical press lines installed by company 1No usage of second hand machines seen in the

Low tonnage machines supplied by smallplayers for bending & shearing applications

auto sector

66

Auto sector: Metal forming machinery consumption and the supply sources

Split by Machine (Domestic) Split by Machine (Imported)

Value : Rs. 42 Cr (USD 8.9 mn) Value : Rs. 586 Cr (USD 124.7 mn)

67

Auto components: Metal forming machinery consumption estimated at Rs 407 cr

Split by Players (Domestic) Split by Players (Imported)

Used importers

18%

Importer 114% Importer 2

11%

Importer 38%

Other importers

37%

18%

Other Importers

12%

Value : Rs. 188 Cr (USD 40 mn) Value : Rs. 219 Cr (USD 46.6 mn)

Dominated by company 1 (26%) followed bycompany 2 (7%)

( )

Dominated by importer 1 (14%) followed byimporter 2(11%)

68

Auto components: Metal forming machinery consumption and the supply sources

Split by Machine ( Domestic ) Split by Machine ( Imported )

Value : Rs. 188 Cr (USD 40 mn) Value : Rs. 219 Cr (USD 46.6 mn)

69

Consumer durables: Metal forming machinery consumption estimated at Rs 110 cr

Company 2 C 3 Importer 1

Split by Players (Domestic) Split by Players (Imported)

Company 119%

Company 28%

Company 37%

Other importers

Importer 139%

Importer 26%

Other companies

66%

Other importers47% Importer 3

7%

Importer 41%

Value : Rs. 19 Cr (USD 4 mn) Value : Rs. 91 Cr (USD 19.3 mn)

Dominated by company 1 (20%) followed bycompany 2 (8%)

Very few suppliers for consumer durables

MNC t f i th t h l f t

Importer 1 with a 39% market share is thelargest imported brand

MNCs prefer to import new machinery forblanking & pressing applicationsMNCs transferring the technology from parent

company

blanking & pressing applications

70

Consumer durables: Metal forming machinery consumption and the supply sources

Split by Machine ( Domestic ) Split by Machine ( Imported )

Value : Rs. 19 Cr (USD 4 mn) Value : Rs. 91 Cr (USD 19.3 mn)

71

Kitchen equipment: Metal forming machinery consumption estimated at Rs 48 cr

Company 19%

Split by Players ( Domestic )

Company 29%

Company 35%

Only second hand imports - Rs. 12 cr

Most of the kitchen utensilsCompany 4

4%

Company 53%

Company 62%

Other companies66%

manufacturers are SSI units, who cannotafford new imported machinery

Sourcing is highly localizedCompany 7

2%

Value : Rs. 36 Cr (USD 7.6 mn)

Highly dominated by Rajkot & Ludhiana basedsuppliers

72

Kitchen equipment: Metal forming machinery consumption and the supply sources

Split by Machine (Domestic) Split by Machine (Imported)

Value : Rs. 36 Cr (USD 7.6 mn) Value : Rs. 12 Cr (USD 2.5 mn)

73

General engineering: Metal forming machinery consumption estimated at Rs 614 cr

Used machine

Split by Players ( Domestic ) Split by Players (Imported)

Other importers

70%

importers14%

Importer 18%70% 8%

Importer 25%

Importer 33%3%

Value : Rs. 108 Cr( USD 23 mn) Value : Rs. 506 Cr (USD 107.6 mn)

Company 1 holds 19% of market, followed bycompany 2Large demand across the General Engineeringsector is contributed by smaller companiespresent across the consumption pockets

Importer 1 market leader with 7% market sharefollowed by importer 2Typically catering to the heavy sheet metalindustryIndustry is catered by large number of importerspresent across the consumption pockets Industry is catered by large number of importersin this sector and also by Used machine imports

74

General Engineering: Metal forming machinery consumption and the supply sources

Split by Machine ( Domestic ) Split by Machine ( Imported )

Value : Rs. 108 Cr (USD 23 mn) Value : Rs. 506 Cr (USD 107.6 mn)

75

Electrical equipment: Metal forming machinery consumption estimated at Rs 162 cr

Split by Players ( Domestic ) Split by Players (Imported)

Importer 128% Importer 2

15%

Other importers

52%

Importer 35%

Value : Rs 34 Cr (USD 7 2 mn) Value : Rs 128 Cr (USD 27 2 mn)Value : Rs. 34 Cr (USD 7.2 mn)

Company 1, market leader with 22% share,followed by company 2 (9%)Organised customers prefer sourcing the

hi f t d d ti l b d

Value : Rs. 128 Cr (USD 27.2 mn)

importer 1, market leader with 28% marketshare3 major importers accounts for 48% of the

k t hmachinery from reputed and national brands market share

76

Electrical equipment: Metal forming machinery consumption and the supply sources

Split by Machine ( Domestic ) Split by Machine ( Imported )

Value : Rs. 34 Cr (USD 7.2 mn) Value : Rs. 128 Cr (USD 27.2 mn)

77

Energy & power: Metal forming machinery consumption estimated at Rs 219 cr

Company 2

Split by Players ( Domestic ) Split by Players ( Imported)

10% Company 310%

Other

Importer 2

21%Used

Company 143% Other

companiesImporter

1

importers32%

21%machine Importer10%

p37%

l R 48 C ( SD 10 2 ) V l R 171 C (USD 36 4 )

37%

Value : Rs. 48 Cr (USD 10.2 mn )

Company 1 market leader with 43% share

3 companies together accounts for 63% of the domestic supply

Value : Rs. 171 Cr (USD 36.4 mn)

Importer 1 is the market leader with 37% market share

Company 2 targeting large panel domestic supply Company 2 targeting large panel manufacturers

78

Energy & power: Metal forming machinery consumption and the supply sources

Split by Machine (Domestic) Split by Machine (Imported)

Value : Rs. 48 Cr (USD 10.2 mn) Value : Rs. 171 Cr (USD 36.4 mn)

79

Infrastructure & construction: Metal forming machinery consumption estimated at Rs 142 cr

Split by Players ( Domestic ) Split by Players (Imported)

Company 113%

Company 213%

Company 38% Importer 1

28% Used machine importers

Other companies

66%

Other importers

58%

9%

Importer 25%

Value : Rs. 23 Cr (USD 4.9 mn)

C 1 & 2 h h fi i i i h 13%

Value : Rs. 119 Cr (USD 25.3 mn)

I 1 k l d i h 28% kCompany 1 & 2 share the first position with 13%share followed by company 3(8%)Apart from a few large & medium sizecompanies, not many Indian manufacturerstargeting this segment

Importer 1, market leader with 28% marketshare

Targeting construction equipment manufacturersInfrastructure a key growing segment withconsiderable expected investmentg g g

Potential segment with huge expectedinvestment

p

80

Infrastructure & Construction: Metal forming machinery consumption and the supply sources

Split by Machine (Domestic) Split by Machine (Imported)

Value : Rs. 23 Cr (USD 4.9 mn) Value : Rs. 119 Cr (USD 25.3 mn)

81

Process equipment & machinery: Metal forming machinery consumption estimated at Rs 120 cr

UsedC 1

Company 28%

Company 37%

Split by Players ( Domestic ) Split by Players ( Imported)

Importer 125%

Used machine importers

18%

Importer 211%

Company 113%

8% 7%

Company 45%

Company 54%

Other importers

11%4%

Other companies

63% 46%63%

Value : Rs. 97 Cr (USD 20.6 mn)Value : Rs. 23 Cr (USD 4.9 mn)

Company 1, market leader with 13% sharefollowed by company 2

Majority sales in the western part of India

Importer 1, market leader with 25% marketshare

Importer 2 Tools has a market share of 11%

82

Process equipment and machinery: Metal forming machinery consumption and the supply sources

Split by Machine (Domestic) Split by Machine (Imported)

Value : Rs. 23 Cr (USD 4.9 mn) Value : Rs. 119 Cr (USD 20.6 mn)

83

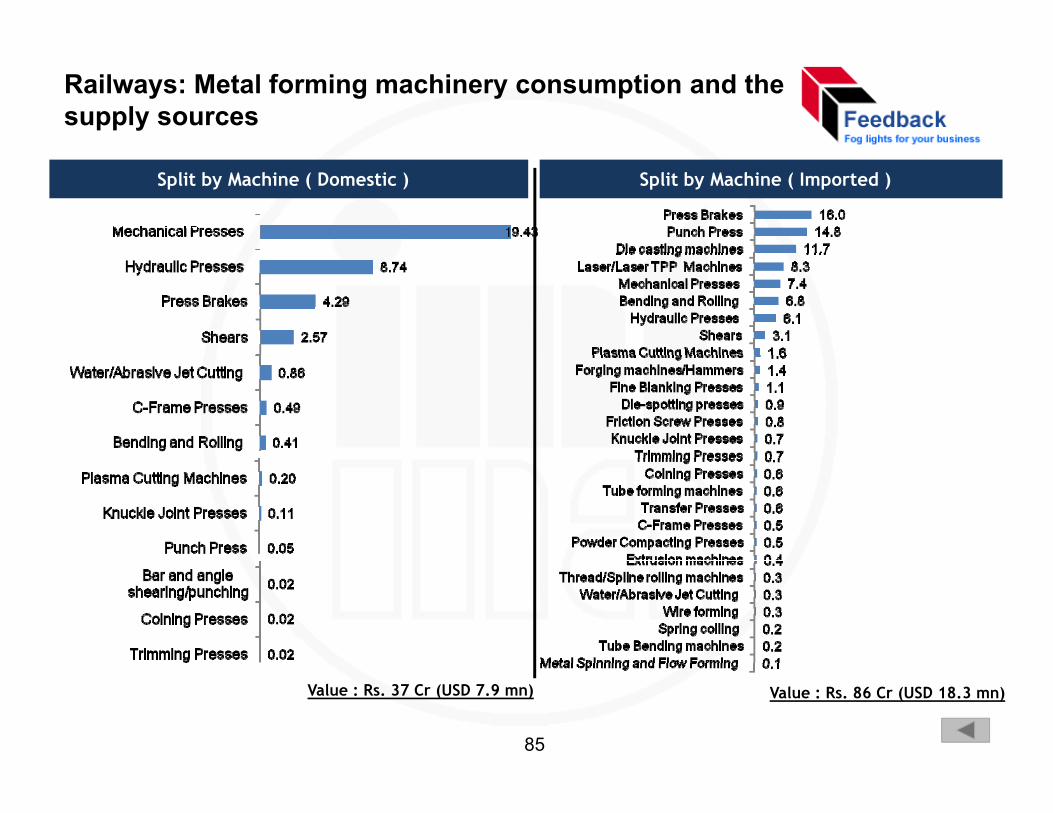

Railways: Metal forming machinery consumption estimated at Rs 123 cr

Company 2

Split by Players ( Domestic ) Split by Players ( Imported)

Importer 128%

Importer 216%

Used machine importers

10%

Importer 36%

Company 155%

Company 210%

Company 35%

Other importers

55%

Other companies

30% p40%

30%

Value : Rs. 37 Cr (USD 7.9 mn) Value : Rs. 86 Cr (USD 18.3 mn)

Company 1 market leader, holding 55% of thedomestic market

Targeting wagon & coach manufacturers

Company 1, market leader with 28% marketshare

Targeting new companies like Bombardier

High potential segment

84

Railways: Metal forming machinery consumption and the supply sources

Split by Machine ( Domestic ) Split by Machine ( Imported )

Value : Rs. 37 Cr (USD 7.9 mn) Value : Rs. 86 Cr (USD 18.3 mn)

85

Office equipment: Metal forming machinery consumption estimated at Rs 56 cr

Split by Players ( Domestic ) Split by Players ( Importers )

Used machine importers

Company 119%

Company 28%

Company 38%

New machine importers

74%

importers26%

74%Other companies

65%

Value : Rs. 10 Cr (USD 2.1 mn)

Company 1, market leader with 19% ofdomestic market

Company 1 targeting office equipment

Highly unorganized segment

Metal forming machine usage is very limited

Value : Rs. 46 Cr (USD 9.8 mn)

Company 1 targeting office equipmentmanufacturing segment

86

Office equipment: Metal forming machinery consumption and the supply sources

Split by Machine (Domestic) Split by Machine (Imported)

Value : Rs. 10 Cr (USD 2.1 mn) Value : Rs. 46 Cr (USD 9.8 mn)

87

Ship building: Metal forming machinery consumption estimated at Rs 64 cr

Split by Players ( Importers )

Used machine importers

Other importers

81%

p19%

Value : Rs. 64 Cr (USD 13.6 mn)

Domestic suppliers to ship building segment limited to just 1 company and they have sold machinery worth Rs Domestic suppliers to ship building segment limited to just 1 company and they have sold machinery worth Rs 3.1 cr

88

Ship building: Metal forming machinery consumption and the supply sources

Split by Machine (Domestic) Split by Machine (Imported)

Value : Rs. 3.1 Cr (USD 0.6 mn) Value : Rs. 64 Cr (USD 13.6 mn

89

Others: Metal forming machinery consumption estimated at Rs 153 cr

C 1Company 2 Company 3

Split by Players ( Domestic ) Split by Players ( Imported)

Used machine importers

22% Importer 212%

Importer 34%

Company 111%

5% 4%

Other importers

29%

Importer 128%

Importer 44%

Importer 51%

Other companies

80%Value : Rs. 89 Cr (USD 18.9 mn ) Value : Rs. 64 Cr (USD 13.6 mn)

Company 1, market leader with 11% ofdomestic market

Targeting sheet metal & enclosure market,aerospace, etc

Company 1, market leader with 28% marketshare

Targeting RBI for coining press

Targeting aerospace segment etcHigh potential segment

Targeting aerospace segment, etc

90

Others: Metal forming machinery consumption and the supply sources

Split by Machine ( Domestic) Split by Machine (Imported)

Value : Rs. 89 Cr (USD 18.9 mn)Value : Rs. 64 Cr (USD 13.6 mn)

91

Metal forming machinery –F t 2008 2015Forecast 2008 - 2015• Approach and Methodology

• Historical trends

• Forecasts by– Segments

– Type of machinery

S t d t f hi– Segments and type of machinery

92

Future market estimates: Approach

MFM growth is proportional to the respective industry segment growthI di id l hi ’ h i i l

Possibility of occurrences such as war, economic slowdown Bl b i d d b

Discounts Assumptions

Individual machine’s growth is proportional to the total MFM growth in a segment in the absence of any technological changes

Blue ocean strategy being adopted by any organization Value growth due to price increase

Correlation is used between total investments in manufacturing industry and MFM market

Methodology

Considering possible technological changes, the total MFM growth has been transferred to the individual machine’s growth

Cross-checkIndividual product segment growth has been rechecked establishing correlation with total MFM growth rate

90-95%

Confidence levels

93

Future market estimates: Methodology

GDP Forecast Targeted Investments Targeted growth rate across primary

sectorsCorrelation

Overall MFM futureEstimation of

individual segment's

Historical product

segment growth

Expert interviews

individual segment s growth rates

M hi iProduct

Correlation

Machine wise segment wise future

Correction in line with

segment wise future

Cross-check

future technological changes

Final future estimatesa u u e es a es

Secondary data Feedback analysisMethodology

94

Future market estimates: Methodology

Step 1