Embed Size (px)

Citation preview

MetroPac Movers, Inc.(A Subsidiary of MetroPac LogisticsCompany, Inc.)

Financial StatementsDecember 31, 2018 and 2017

and

Independent Auditor’s Report

*SGVFS036564*

INDEPENDENT AUDITOR’S REPORT

The Board of Directors and the StockholdersMetroPac Movers, Inc.

Report on the Audit of the Financial Statements

Opinion

We have audited the financial statements of MetroPac Movers, Inc. (a subsidiary of MetroPac LogisticsCompany, Inc.) (the Company) which comprise the statements of financial position as atDecember 31, 2018 and 2017, and the statements of comprehensive income, statements of changes inequity and statements of cash flows for the years ended December 31, 2018 and 2017, and notes to thefinancial statements, including a summary of significant accounting policies.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financialposition of the Company as at December 31, 2018 and 2017, and its financial performance and its cashflows for the years ended December 31, 2018 and 2017 in accordance with Philippine Financial ReportingStandards (PFRSs).

Basis for Opinion

We conducted our audits in accordance with Philippine Standards on Auditing (PSAs). Ourresponsibilities under those standards are further described in the Auditor’s Responsibilities for the Auditof the Financial Statements section of our report. We are independent of the Company in accordancewith the Code of Ethics for Professional Accountants in the Philippines (Code of Ethics) together with theethical requirements that are relevant to our audit of the financial statements in the Philippines, and wehave fulfilled our other ethical responsibilities in accordance with these requirements and the Code ofEthics. We believe that the audit evidence we have obtained is sufficient and appropriate to provide abasis for our opinion.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements inaccordance with PFRSs, and for such internal control as management determines is necessary to enablethe preparation of financial statements that are free from material misstatement, whether due to fraud orerror.

In preparing the financial statements, management is responsible for assessing the Company’s ability tocontinue as a going concern, disclosing, as applicable, matters related to going concern and using thegoing concern basis of accounting unless management either intends to liquidate the Company or to ceaseoperations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s financial reporting process.

SyCip Gorres Velayo & Co.6760 Ayala Avenue1226 Makati CityPhilippines

Tel: (632) 891 0307Fax: (632) 819 0872ey.com/ph

BOA/PRC Reg. No. 0001, October 4, 2018, valid until August 24, 2021SEC Accreditation No. 0012-FR-5 (Group A), November 6, 2018, valid until November 5, 2021

A member firm of Ernst & Young Global Limited

*SGVFS036564*

- 2 -

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole arefree from material misstatement, whether due to fraud or error, and to issue an auditor’s report thatincludes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that anaudit conducted in accordance with PSAs will always detect a material misstatement when it exists.Misstatements can arise from fraud or error and are considered material if, individually or in theaggregate, they could reasonably be expected to influence the economic decisions of users taken on thebasis of these financial statements.

As part of an audit in accordance with PSAs, we exercise professional judgment and maintainprofessional skepticism throughout the audit. We also:

∂ Identify and assess the risks of material misstatement of the financial statements, whether due to fraudor error, design and perform audit procedures responsive to those risks, and obtain audit evidence thatis sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a materialmisstatement resulting from fraud is higher than for one resulting from error, as fraud may involvecollusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

∂ Obtain an understanding of internal control relevant to the audit in order to design audit proceduresthat are appropriate in the circumstances, but not for the purpose of expressing an opinion on theeffectiveness of the Company’s internal control.

∂ Evaluate the appropriateness of accounting policies used and the reasonableness of accountingestimates and related disclosures made by management.

∂ Conclude on the appropriateness of management’s use of the going concern basis of accounting and,based on the audit evidence obtained, whether a material uncertainty exists related to events orconditions that may cast significant doubt on the Company’s ability to continue as a going concern.If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’sreport to the related disclosures in the financial statements or, if such disclosures are inadequate, tomodify our opinion. Our conclusions are based on the audit evidence obtained up to the date of ourauditor’s report. However, future events or conditions may cause the Company to cease to continueas a going concern.

∂ Evaluate the overall presentation, structure and content of the financial statements, including thedisclosures, and whether the financial statements represent the underlying transactions and events in amanner that achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scopeand timing of the audit and significant audit findings, including any significant deficiencies in internalcontrol that we identify during our audit.

A member firm of Ernst & Young Global Limited

*SGVFS036564*

- 3 -

Report on the Supplementary Information Required Under Revenue Regulations 15-2010

Our audits were conducted for the purpose of forming an opinion on the basic financial statements takenas a whole. The supplementary information required under Revenue Regulations 15-2010 in Note 28 tothe financial statements is presented for purposes of filing with the Bureau of Internal Revenue and is nota required part of the basic financial statements. Such information is the responsibility of themanagement of MetroPac Movers, Inc. The information has been subjected to the auditing proceduresapplied in our audit of the basic financial statements. In our opinion, the information is fairly stated, in allmaterial respects, in relation to the basic financial statements taken as a whole.

SYCIP GORRES VELAYO & CO.

Meynard A. BonoenPartnerCPA Certificate No. 0110259SEC Accreditation No. 1739-A (Group A), February 7, 2019, valid until February 6, 2022Tax Identification No. 301-105-435BIR Accreditation No. 08-001998-136-2018, December 17, 2018, valid until December 16, 2021PTR No. 7332531, January 3, 2019, Makati City

June 6, 2019

A member firm of Ernst & Young Global Limited

*SGVFS036564*

METROPAC MOVERS, INC.(A Subsidiary of MetroPac Logistics Company, Inc.)STATEMENTS OF FINANCIAL POSITION

December 312018 2017

ASSETSCurrent AssetsCash and cash equivalents (Notes 5 and 26) P=776,464,724 P=95,640,053Trade and other receivables (Notes 6, 18 and 26) 601,819,317 1,135,329,733Other current assets (Notes 1 and 7) 324,832,088 105,774,864

Total Current Assets 1,703,116,129 1,336,744,650Noncurrent AssetsLoans receivable (Note 18) 920,659,908 518,603,651Property and equipment (Notes 1 and 8) 1,629,310,760 351,918,396Software cost (Note 9) 5,112,890 1,805,255Investment in and advances to subsidiaries (Note 11) 580,681,903 447,612,866Equity instruments at fair value through other comprehensive

income (FVOCI) (Note 12) 100,429,147 –Goodwill and intangibles (Notes 1 and 10) 1,406,267,482 1,426,209,600Other noncurrent assets (Notes 1 and 13) 149,417,393 609,002,741

Total Noncurrent Assets 4,791,879,483 3,355,152,509P=6,494,995,612 P=4,691,897,159

LIABILITIES AND EQUITYCurrent LiabilitiesTrade payables and other current liabilities (Notes 14, 18 and 26) P=975,116,044 P=708,671,647Short-term loan (Note 15) 300,000,000 –Subscription payable (Note 11) – 3,750,000Current portion of:

Finance lease liability (Notes 17 and 24) 7,410,382 11,961,388Long-term loan (Notes 15 and 26) 259,876,344 154,000,000

Total Current Liabilities 1,542,402,770 878,383,035Noncurrent LiabilitiesNoncurrent portion of:

Finance lease liability (Notes 17 and 24) 21,881,592 46,344,499Long-term loan (Notes 15 and 26) 802,820,185 606,000,000

Other noncurrent liabilities (Note 16) 11,731,478 34,662,116Total Noncurrent Liabilities 836,433,255 687,006,615Total Liabilities 2,378,836,025 1,565,389,650

EquityCapital stock (Note 19) 3,961,550,676 3,040,623,714Additional paid-in capital (Note 19) 988,253,924 –Deposit for future stock subscription (Note 19) – 408,800,000Equity reserve (Note 19) (34,340,727) (21,683,717)Other comprehensive income reserve (Notes 12 and 22) (296,485,907) (766,775)Retained earnings (Deficit) (502,818,379) (300,465,713)

Total Equity 4,116,159,587 3,126,507,509P=6,494,995,612 P=4,691,897,159

See accompanying Notes to Financial Statements.

*SGVFS036564*

METROPAC MOVERS, INC.(A Subsidiary of MetroPac Logistics Company, Inc.)STATEMENTS OF COMPREHENSIVE INCOMEFOR THE YEARS ENDED DECEMBER 31, 2018 AND 2017

2018 2017

REVENUES (Note 18)Warehouse management P=539,934,476 P=624,458,539Trucking services 292,353,543 159,328,875Warehouse rent 205,782,962 151,042,717Freight forwarding services 37,623,534 –Equipment rent 9,478,697 62,777,303Others 9,948,656 13,340,605

1,095,121,868 1,010,948,039

COSTS OF SERVICES (Note 20) 912,079,086 783,880,972

GROSS PROFIT 183,042,782 227,067,067

OPERATING EXPENSES (Note 21) (601,900,883) (596,656,921)

INTEREST INCOME (Notes 5, 11 and 13) 51,777,313 1,484,631

INTEREST EXPENSE (Notes 15, 16 and 17) (67,618,327) (9,503,208)

OTHER INCOME (Notes 1 and 18) 235,461,098 –

OTHER EXPENSES (813,769) (1,802,402)

LOSS BEFORE INCOME TAX (200,051,786) (379,410,833)

PROVISION FOR FINAL TAX (Note 23) 2,300,880 120,275

NET LOSS (202,352,666) (379,531,108)

OTHER COMPREHENSIVE LOSSOther comprehensive income not to be reclassified to profit or loss

in subsequent periodRemeasurement gain (loss) on retirement liability, net of tax

(Note 22) 3,851,721 (766,775)Remeasurement loss in fair value of unquoted equity

investments (Note 12) (299,570,853) –Total (295,719,132) (766,775)

TOTAL COMPREHENSIVE LOSS (P=498,071,798) (P=380,297,883)

See accompanying Notes to Financial Statements.

*SGVFS036564*

METROPAC MOVERS, INC.(A Subsidiary of MetroPac Logistics Company, Inc.)STATEMENTS OF CHANGES IN EQUITYFOR THE YEARS ENDED DECEMBER 31, 2018 AND 2017

CapitalStock

(Note 18)

AdditionalPaid-inCapital

(Note 18)

Deposit forFuture StockSubscription

(Note 18)

EquityReserve(Note 18)

OtherComprehensive

Income(Note 21)

RetainedEarnings (Deficit) Total

At January 1, 2018 P=3,040,623,714 P=– P=408,800,000 (P=21,683,717) (P=766,775) (P=300,465,713) P=3,126,507,509Total comprehensive loss:

Net loss – – – – – (202,352,666) (202,352,666)Other comprehensive loss – – – – (295,719,132) – (295,719,132)Total – – – – (295,719,132) (202,352,666) (498,071,798)

Issuance of capital stock (Note 1) 920,926,962 988,253,924 (408,800,000) – – – 1,500,380,886Transaction costs on issuance of

capital stock – – – (12,657,010) – – (12,657,010)

At December 31, 2018 P=3,961,550,676 P=988,253,924 P=– (P=34,340,727) (P=296,485,907) (P=502,818,379) P=4,116,159,587

At January 1, 2017 P=1,704,200,000 P=– P=– (P=15,001,598) P=– P=79,065,395 P=1,768,263,797Total comprehensive loss:

Net loss – – – – – (379,531,108) (379,531,108)Other comprehensive loss – – – (766,775) – (766,775)

Total – – – – (766,775) (379,531,108) (380,297,883)Issuance of capital stock (Note 1) 1,336,423,714 – – – – – 1,336,423,714Transaction costs on issuance of

capital stock – – – (6,682,119) – – (6,682,119)Deposit for future stock

subscription – – 408,800,000 – – – 408,800,000

At December 31, 2017 P=3,040,623,714 P=– P=408,800,000 (P=21,683,717) (P=766,775) (P=300,465,713) P=3,126,507,509

See accompanying Notes to Financial Statements.

*SGVFS036564*

METROPAC MOVERS, INC.(A Subsidiary of MetroPac Logistics Company, Inc.)STATEMENTS OF CASH FLOWSFOR THE YEARS ENDED DECEMBER 31, 2018 AND 2017

2018 2017

CASH FLOWS FROM OPERATING ACTIVITIESLoss before income tax (P=200,051,786) (P=379,410,833)Adjustments for:

Provision for expected credit losses (ECL)/doubtful accounts(Notes 6 and 21) 214,770,985 6,922,956

Depreciation and amortization (Notes 8, 9, 10, 20 and 21) 112,181,645 77,699,684Interest expense (Notes 15, 16 and 17) 67,618,327 9,503,208Interest income (Notes 5, 11 and 13) (51,777,313) (1,484,631)Pension expense (Notes 21 and 22) 4,926,481 6,285,202Gain on sale of property and equipment (Note 8) (2,776,406) –Deferred rent amortization – net (Note 20) 1,699,917 522,338Impairment loss (Notes 10 and 21) – 324,168,256

Income before working capital changes 146,591,850 44,206,180Decrease (increase) in:

Trade and other receivables (374,483,032) (507,813,167)Due from related parties 114,539,661 (244,121,794)Other current assets (219,057,224) 6,932,592

Increase (decrease) in:Trade payables and other current liabilities 391,804,047 400,693,798Due to related parties (90,500,000) (17,779,902)

Net cash used in operations (31,104,698) (317,882,293)Interest received 9,625,651 601,375Interest paid (56,677,706) (2,745,369)Final tax paid (2,300,880) (120,275)Net cash flows used in operating activities (80,457,633) (320,146,562)

CASH FLOWS FROM INVESTING ACTIVITIESAcquisitions of/additions to:

Property and equipment (Note 8) (862,580,621) (182,564,863)Software cost (Note 9) (4,393,654) (1,577,904)Investments (Note 11) (30,000,000) (236,000,010)

Disposal of property and equipment (Note 8) – 21,993,826Issuance of loans to subsidiaries (Notes 11 and 18) (385,185,000) (690,000,000)Increase in other noncurrent assets 59,540,755 (410,204,643)Net cash flows used in investing activities (1,222,618,520) (1,498,353,594)

(Forward)

*SGVFS036564*

- 2 -

2018 2017

CASH FLOWS FROM FINANCING ACTIVITIESProceeds from:

Issuance of capital stock (Note 19) P=1,429,880,886 P=608,000,000Long-term loan (Note 15) 510,000,000 770,000,000Short-term loan (Note 15) 470,000,000 –Deposits for future stock subscription (Note 19) – 408,800,000

Payments of/for:Transaction costs on issuance of capital stock (Note 19) (12,657,010) (6,682,119)Long-term loan (Note 15) (204,368,421) (10,000,000)Short-term loan (Note 15) (170,000,000) –Finance lease liability (31,378,831) (31,235,238)Transaction costs on issuance of loan (Note 15) (3,825,800) –Subscription payable (Note 11) (3,750,000) (3,750,000)

Net cash flows provided by financing activities 1,983,900,824 1,735,132,643

NET INCREASE (DECREASE) IN CASH AND CASHEQUIVALENTS 680,824,671 (83,367,513)

CASH AND CASH EQUIVALENTS AT BEGINNINGOF YEAR (Note 5) 95,640,053 179,007,566

CASH AND CASH EQUIVALENTS AT END OF YEAR(Note 5) P=776,464,724 P=95,640,053

See accompanying Notes to Financial Statements.

*SGVFS036564*

METROPAC MOVERS, INC.(A Subsidiary of MetroPac Logistics Company, Inc.)NOTES TO FINANCIAL STATEMENTS

1. Corporate Information

MetroPac Movers, Inc. (the Company or MMI) was incorporated in the Philippines and registeredwith the Philippine Securities and Exchange Commission (SEC) on September 1, 2015. TheCompany is engaged in the business of logistics services relating to products, commodities, articles,and goods, including but not limited to, storage, warehousing, warehouse and inventory management,transport and delivery, domestic international freight and cargo forwarder of all classes of goods andmerchandise either by land, sea or air, non vessel operating common carrier, courier, express andparcel services, messengerial services, brokerage services and other allied services.

As at December 31, 2017, the Company is a wholly owned subsidiary by MetroPac LogisticsCompany, Inc. (MLCI), an entity incorporated in the Philippines. MLCI is a subsidiary of MetroPacific Investments Corporation (MPIC), whose shares of stock are listed with the SEC. OnDecember 5, 2018, a minority interest of 0.9% had been sold to an individual shareholder. As atDecember 31, 2018, MLCI’s ownership interest is reduced to 99.1% (see Note 19).

Metro Pacific Holdings, Inc. (MPHI) owns 41.9% of the total issued common shares (or 42.0% of thetotal outstanding common shares) of MPIC as at December 31, 2018 and 2017, respectively. As soleholder of the voting Class A Preferred Shares of MPIC, MPHI’s combined voting interest as a resultof all of its shareholdings is estimated at 55.0% as at December 31, 2018 and 2017.

MPHI is a Philippine corporation whose stockholders are Enterprise Investment Holdings, Inc. (EIH;60.0% interest), Intalink B.V. (26.7% interest) and First Pacific International Limited (FPIL; 13.3%interest). First Pacific Company Limited (FPC), a company incorporated in Bermuda and listed inHong Kong, through its subsidiaries, Intalink B.V. and FPIL, holds 40.0% equity interest in EIH andinvestment financing which under Hong Kong Generally Accepted Accounting Principles, requireFPC to account for the results and assets and liabilities of EIH and its subsidiaries as part of FPCgroup of companies in Hong Kong.

The principal office address of the Company is 12th Floor, VGP Center, Ayala Avenue, Makati City.

The accompanying financial statements were approved and authorized for issue by the Board ofDirectors (BOD) on June 6, 2019.

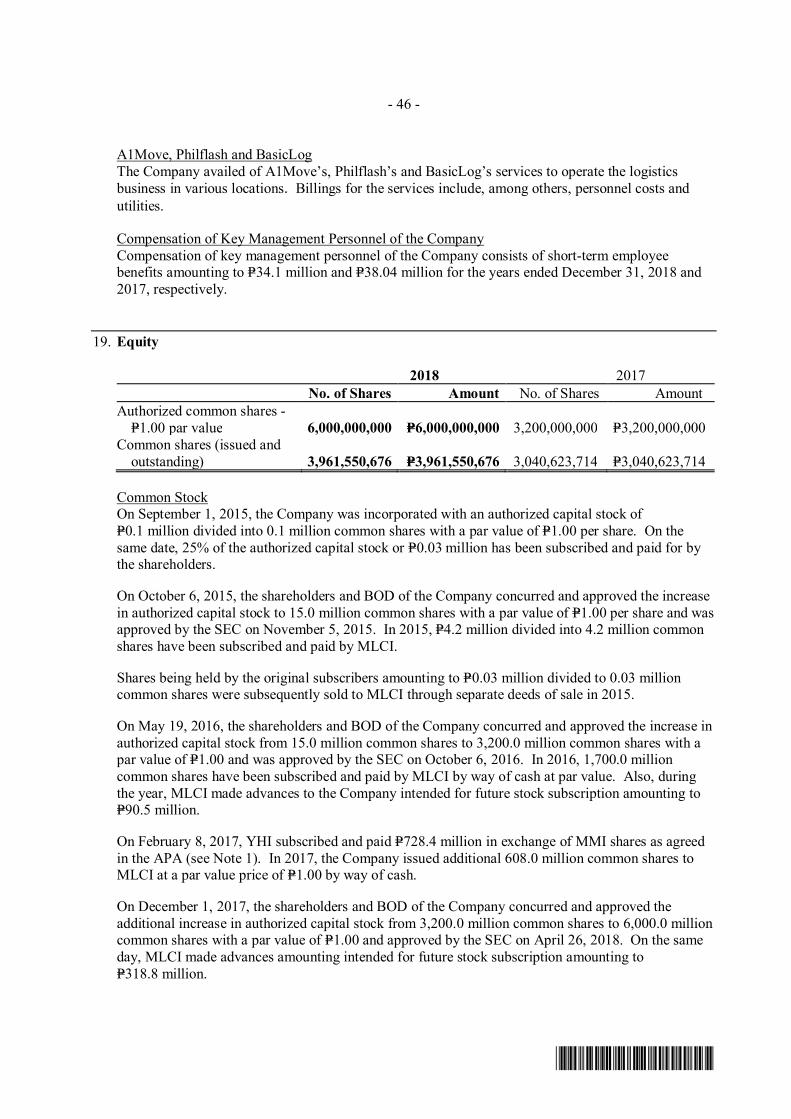

Asset Purchase Agreement (APA)On May 19, 2016, MMI completed the purchase of the assets and certain contracts of Basic LogisticsCorporation (Basic), A1Move Logistics, Inc. (A1Move), Philflash Logistics, Inc. (Philflash) andBasicLog Trade and Marketing Enterprises (BasicLog), collectively known as the Sellers, all ofwhich are involved in the logistics business.

The transaction involves the acquisition by MMI of the assets and certain contracts of the Sellers for atotal purchase price consideration of P=2,168.3 million, inclusive of applicable value-added taxes. Ofthe total purchase price, P=1,400.0 million was paid in cash, P=39.9 million was deposited into anominated escrow agent and the remaining balance of P=728.4 million will be offset against theSellers’ subscription of the Company’s common shares (see Notes 14 and 18).

After the completion of the transaction, a separate company that will be designated by the Sellers willacquire twenty-four percent (24%) of the outstanding capital stock of MMI.

- 2 -

*SGVFS036564*

On February 8, 2017, Yellowbear Holdings, Inc. (YHI), the separate company designated by theSellers to acquire common shares of the Company, subscribed to 728.4 million common shares with apar value of P=1.00 per share. Consequently, acquisition payable to the Sellers amounting toP=728.4 million were offset against YHI’s subscription of the Company’s common shares(see Notes 17 and 18).

MMI will expand its logistics business utilizing the assets and businesses initially acquired from theSellers.

The transaction was carried out through an APA involving, among others, (a) the sale by the Sellersof identified logistics assets, (b) the novation of certain key contracts of the Sellers with theirrespective clients, (c) the execution of new contracts required to ensure continued operations of thebusiness under MMI, and (d) the transfer of certain key officers and employees of the Sellers to MMI.

The acquisition of the assets has been accounted for using the acquisition method. The final fairvalues of the assets acquired as at the date of acquisition:

FinalValues

(In Millions)Property and equipment (Note 8) P=154Intangible assets (Note 10) 91Total identifiable net assets at fair value 245Goodwill (Note 10) 1,691Total acquisition cost 1,936Input VAT (Notes 7 and 13) 232Total purchase price P=2,168

The goodwill comprises the value of expected synergies arising from the acquisition and a customerlist, which is not separately recognized. Based on assessment, the customer list is not separable andtherefore, it does not meet the criteria for recognition as an intangible asset under PAS 38, IntangibleAssets. None of the goodwill recognized is expected to be deductible for income tax purposes.

On February 28, 2018, a Memorandum of Agreement (MOA) was entered by and between theCompany, MLCI, YHI, and Sheldon Yap. Sheldon Yap and the Company agreed to settle claimsfrom failure to meet stipulations in the APA resulting in a net receivable amounting toP=238.6 million. The Company recognized income amounting to P=216.9 million under“Other income” account in the 2018 statement of comprehensive income.

2. Basis of Preparation, Statement of Compliance and Changes in Accounting Policies

Basis of PreparationThe accompanying financial statements have been prepared on a historical cost basis, except forfinancial assets at fair value through other comprehensive income (FVOCI) that are measured at fairvalue. The financial statements are presented in Philippine Peso, which is the Company’s functionaland presentation currency, and all values are rounded to the nearest peso unless otherwise indicated.

The Company elected not to prepare consolidated financial statements under the exemption providedin Philippine Financial Reporting Standards (PFRS) 10, Consolidated Financial Statements. MPICprepares consolidated financial statements in conformity with PFRS and such consolidated financial

- 3 -

*SGVFS036564*

statements are filed with the SEC and Philippine Stock Exchange and are available for public use.MPIC’s consolidated financial statements may be obtained at 10th Floor, MGO Building, Legaspicorner Dela Rosa Streets, Legaspi Village, Makati City.

The accompanying financial statements are prepared for submission to the SEC and Bureau ofInternal Revenue (BIR).

Statement of ComplianceThe accompanying financial statements have been prepared in accordance with PFRS.

Changes in Accounting PoliciesThe accounting policies adopted are consistent with those of the previous financial year except for theadoption of the following new and amended Philippine Accounting Standards (PAS), PFRS andPhilippine Interpretation effective January 1, 2018. Adoption of the following standards andamendments did not have any material impact on the Company’s financial statements:

ƒ Amendments to PFRS 2, Share-based Payment, Classification and Measurement of Share-basedPayment Transactions

ƒ PFRS 9, Financial Instruments

The Company adopted PFRS 9 with a date of initial application of January 1, 2018. PFRS 9replaces PAS 39, Financial Instruments: Recognition and Measurement and all previous versionsof PFRS 9. The standard introduces new requirements for classification and measurement,impairment and hedge accounting.

The Company has adopted PFRS 9 using the modified retrospective approach. The Companychose not to restate comparative figures as permitted by the transitional provisions of PFRS 9,thereby resulting in the following impact:∂ Comparative information for prior periods will not be restated. The classification and

measurement requirements previously applied in accordance with PAS 39 and disclosuresrequired in PFRS 7, Financial Instruments: Disclosures will be retained for the comparativeperiods. Accordingly, the information presented for 2017 does not reflect the requirements ofPFRS 9.

∂ The Company will disclose the accounting policies for both the current period and thecomparative periods, one applying PFRS 9 beginning January 1, 2018 and one applyingPAS 39 as of December 31, 2017.

∂ As comparative information is not restated, the Company is not required to provide a thirdstatement of financial information at the beginning of the earliest comparative period inaccordance with PAS 1, Presentation of Financial Statements.

As at January 1, 2018, the Company has reviewed and assessed all of its existing financial assets.

The effect of adopting PFRS 9 as at January 1, 2018 was, as follows:

a. Classification and measurement

Under PFRS 9, the Company initially measures a financial asset at its fair value plus, in thecase of a financial asset not at fair value through profit or loss, transaction costs.

Under PFRS 9, financial assets are subsequently measured at fair value through profit or loss(FVTPL), amortized cost, or FVOCI. The classification is based on two criteria: theCompany’s business model for managing the assets; and, whether the instruments’contractual cash flows represent ‘solely payments of principal and interest’ on the principalamount outstanding (the ‘SPPI criterion’).

- 4 -

*SGVFS036564*

The assessment of the Company’s business models was made as of the date of initialapplication, January 1, 2018, and then applied retrospectively to those financial assets thatwere not derecognized before January 1, 2018. The assessment of whether contractual cashflows on financial assets are solely comprised of principal and interest was made based on thefacts and circumstances as at the initial recognition of the assets.

The new classifications and measurements of the Company’s financial assets are as follows:

ƒ Financial assets at amortized cost are financial assets that are held within a businessmodel with the objective to hold the financial assets in order to collect contractual cashflows that meet the SPPI criterion. This category includes the Company’s cash and cashequivalents, trade and other receivables, refundable deposits and loans receivable(see Notes 5, 6, 18 and 26).

ƒ Equity instruments at FVOCI, with no recycling of gains or losses to profit or loss onderecognition. This category only includes equity instruments, which the Companyintends to hold for the foreseeable future and which the Company has irrevocably electedto classify upon initial recognition or transition. The Company classified its investmentin unquoted equity instruments at FVOCI. Equity instruments at FVOCI are not subjectto impairment assessment under PFRS 9 (see Note 12).

The following are the changes in the classification of the Company’s financial asset as atJanuary 1, 2018:

PFRS 9 measurementcategory

Amortized costPAS 39 measurement categoryLoans and receivablesCash and cash equivalents P=94,843,903 P=94,843,903Trade and other receivables 1,166,329,733 1,166,329,733Refundable deposits 40,283,824 40,283,824Loans receivables 518,603,651 518,603,651

The Company has not designated any financial liabilities as at fair value through profit orloss. There are no changes in classification and measurement for the Company’s financialliabilities.

b. Impairment

The adoption of PFRS 9 has fundamentally changed the Company’s accounting forimpairment losses for financial assets by replacing PAS 39’s incurred loss approach with aforward-looking expected credit loss (ECL) approach. PFRS 9 requires the Company torecord an allowance for ECLs for all financial assets at amortized cost. Under PFRS 9, thelevel of provision for credit and impairment losses has generally increased due to theincorporation of a more forward-looking approach in determining provisions.

Based on the Company’s assessment, which considers factors such as the nature of thefinancial assets at amortized cost, the financial capacity and historical experience transactingwith counterparties and a combination of forward-looking economic factors which is relevantto the recoverability of these assets, provision for impairment losses is recognized. TheCompany’s assessment of credit risk from financial assets at amortized cost is disclosed inNote 26.

- 5 -

*SGVFS036564*

c. HedgingThe adoption of the hedge accounting requirement of PFRS 9 did not have an impact sincethe Company had no existing hedge relationships as at January 1, 2018.

ƒ Amendments to PFRS 4, Insurance Contracts, Applying PFRS 9, Financial Instruments, withPFRS 4

ƒ PFRS 15, Revenue from Contracts with Customers

PFRS 15 supersedes PAS 11 Construction Contracts, PAS 18 Revenue, and relatedInterpretations and it applies, with limited exceptions, to all revenue arising from contracts withcustomers. PFRS 15 establishes a five-step model to account for revenue arising from contractswith customers and requires that revenue be recognized at an amount that reflects theconsideration to which an entity expects to be entitled in exchange for transferring goods orservices to a customer.

The standard requires entities to exercise judgement, taking into consideration all of the relevantfacts and circumstances when applying each step of the model to contracts with theircustomers. The standard also specifies the accounting for the incremental costs of obtaining acontract and the costs directly related to fulfilling a contract. In addition, the standard requiresrelevant disclosures.

The Company adopted PFRS 15 using the modified retrospective method with the date of initialapplication of January 1, 2018. Under this method, the standard can be applied either to allcontracts at the date of initial application or only to contracts that are not completed at thisdate. The Company elected to apply the standard to contracts not yet completed as atJanuary 1, 2018. Therefore, the comparative information was not restated and continues to bereported under PAS 11, PAS 18 and related Interpretations.

Upon adoption of PFRS 15, the Company has concluded revenue is recognized over time whenthe Company renders and completes the performance obligation agreed with the customer, whosimultaneously receives and consumes the benefit provided by the Company, as the agreedservice is performed.

Under PFRS 15, entities must disaggregate revenue from contracts with customers into categoriesthat depict how the nature, amount, timing and uncertainty of revenue and cash flows are affectedby economic factors. The Company has determined that a disaggregation of revenue using typesof services and the timing of the transfer of goods or services (at a point in time vs over time) isadequate for its circumstances. The Company’s revenues, which are presented in the Company’sstatements of comprehensive income, substantially comprises of services which revenuerecognition is over time.

The adoption of PFRS 15 did not have a material impact on the other comprehensive income orthe Company’s operating, investing and financing cash flows since the manner of recognizingrevenue prior to the adoption of the new standard is aligned with the requirements of PFRS 15.Accordingly, no adjustments in the statements of financial position as of December 31, 2018were recognized.

- 6 -

*SGVFS036564*

ƒ Amendments to PAS 28, Investments in Associates and Joint Ventures, Measuring an Associateor Joint Venture at Fair Value (Part of Annual Improvements to PFRSs 2014 - 2016 Cycle)

ƒ Amendments to PAS 40, Investment Property, Transfers of Investment Propertyƒ Philippine Interpretation IFRIC-22, Foreign Currency Transactions and Advance Consideration

The Company has not early adopted any other standard, interpretation or amendment that has beenissued but is not yet effective.

Future Changes in Accounting PoliciesThe Company will adopt the new and revised standards and interpretations enumerated below that arerelevant to the Company when these become effective. Except as otherwise indicated, the Companydoes not expect the adoption of these new and revised standards and amendments to PFRS andPhilippine Interpretations of the International Financial Reporting Interpretations Committee (IFRIC)to have a significant impact on the Company’s financial statements.

Effective beginning on or after January 1, 2019

ƒ Amendments to to PFRS 9, Prepayment Features with Negative Compensation

The amendments to PFRS 9 allow debt instruments with negative compensation prepaymentfeatures to be measured at amortized cost or fair value through other comprehensive income(FVOCI). An entity shall apply these amendments for annual reporting periods beginning on orafter January 1, 2019. Earlier application is permitted.

ƒ PFRS 16, Leases

PFRS 16 sets out the principles for the recognition, measurement, presentation and disclosure ofleases and requires lessees to account for all leases under a single on-balance sheet model similarto the accounting for finance leases under PAS 17, Leases. It will result in almost all leases beingrecognized on the balance sheet by lessees, as the distinction between operating and financeleases is removed. Under the new standard, an asset (the right to use the leased item) and afinancial liability to pay rentals are recognized. The only exceptions are short-term and low-value leases.

Lessor accounting under PFRS 16 is substantially unchanged from today’s accounting underPAS 17. Lessors will continue to classify all leases using the same classification principle as inPAS 17 and distinguish between two types of leases: operating and finance leases.

Lessees will be also required to remeasure the lease liability upon the occurrence of certain events(e.g., a change in the lease term, a change in future lease payments resulting from a change in anindex or rate used to determine those payments). The lessee will generally recognize the amountof the remeasurement of the lease liability as an adjustment to the right-of-use asset.

PFRS 16 also requires lessees and lessors to make more extensive disclosures than under PAS 17.Early application is permitted, but not before an entity applies PFRS 15. A lessee can choose toapply the standard using either a full retrospective or a modified retrospective approach. Thestandard’s transition provisions permit certain reliefs.

The Company is currently assessing the impact of adopting this standard.

- 7 -

*SGVFS036564*

ƒ Amendments to PAS 19, Employee Benefits, Plan Amendment, Curtailment or Settlement

The amendments to PAS 19 address the accounting when a plan amendment, curtailment orsettlement occurs during a reporting period. The amendments specify that when a planamendment, curtailment or settlement occurs during the annual reporting period, an entity isrequired to:

∂ Determine current service cost for the remainder of the period after the plan amendment,curtailment or settlement, using the actuarial assumptions used to remeasure the net definedbenefit liability (asset) reflecting the benefits offered under the plan and the plan assets afterthat event; and

∂ Determine net interest for the remainder of the period after the plan amendment, curtailmentor settlement using: the net defined benefit liability (asset) reflecting the benefits offeredunder the plan and the plan assets after that event; and the discount rate used to remeasurethat net defined benefit liability (asset).

The amendments also clarify that an entity first determines any past service cost, or a gain or losson settlement, without considering the effect of the asset ceiling. This amount is recognized inprofit or loss. An entity then determines the effect of the asset ceiling after the plan amendment,curtailment or settlement. Any change in that effect, excluding amounts included in the netinterest, is recognized in other comprehensive income.

The amendments apply to plan amendments, curtailments, or settlements occurring on or after thebeginning of the first annual reporting period that begins on or after January 1, 2019, with earlyapplication permitted. The amendments will apply to any future plan amendments, curtailments,or settlements of the Company.

ƒ Amendments to PAS 28, Long-term Interests in Associates and Joint Ventures

The amendments clarify that an entity applies PFRS 9 to long-term interests in an associate orjoint venture to which the equity method is not applied but that, in substance, form part of the netinvestment in the associate or joint venture (long-term interests). This clarification is relevantbecause it implies that the expected credit loss model in PFRS 9 applies to such long-terminterests.

The amendments also clarified that, in applying PFRS 9, an entity does not take account of anylosses of the associate or joint venture, or any impairment losses on the net investment,recognized as adjustments to the net investment in the associate or joint venture that arise fromapplying PAS 28.

The amendments should be applied retrospectively and are effective from January 1, 2019, withearly application permitted. Since the Company does not have such long-term interests inassociates and joint ventures, the amendments will not have an impact on its financial statements.

ƒ Philippine Interpretation IFRIC-23, Uncertainty over Income Tax Treatments

The interpretation addresses the accounting for income taxes when tax treatments involveuncertainty that affects the application of PAS 12, Income Taxes, and does not apply to taxes orlevies outside the scope of PAS 12, nor does it specifically include requirements relating tointerest and penalties associated with uncertain tax treatments.

- 8 -

*SGVFS036564*

The interpretation specifically addresses the following:

∂ whether an entity considers uncertain tax treatments separately∂ the assumptions an entity makes about the examination of tax treatments by taxation

authorities∂ how an entity determines taxable profit (tax loss), tax bases, unused tax losses, unused tax

credits and tax rates∂ how an entity considers changes in facts and circumstances

An entity must determine whether to consider each uncertain tax treatment separately or togetherwith one or more other uncertain tax treatments. The approach that better predicts the resolutionof the uncertainty should be followed.

The Company is currently assessing the impact of adopting this interpretation.

ƒ Annual Improvements to PFRSs 2015-2017 Cycle

∂ Amendments to PFRS 3, Business Combinations, and PFRS 11, Joint Arrangements,Previously Held Interest in a Joint Operation

The amendments clarify that, when an entity obtains control of a business that is a jointoperation, it applies the requirements for a business combination achieved in stages,including remeasuring previously held interests in the assets and liabilities of the jointoperation at fair value. In doing so, the acquirer remeasures its entire previously held interestin the joint operation.

A party that participates in, but does not have joint control of, a joint operation might obtainjoint control of the joint operation in which the activity of the joint operation constitutes abusiness as defined in PFRS 3. The amendments clarify that the previously held interests inthat joint operation are not remeasured.

An entity applies those amendments to business combinations for which the acquisition dateis on or after the beginning of the first annual reporting period beginning on or afterJanuary 1, 2019 and to transactions in which it obtains joint control on or after the beginningof the first annual reporting period beginning on or after January 1, 2019, with earlyapplication permitted. These amendments are currently not applicable to the Company butmay apply to future transactions.

∂ Amendments to PAS 12, Income Tax Consequences of Payments on Financial InstrumentsClassified as Equity

The amendments clarify that the income tax consequences of dividends are linked moredirectly to past transactions or events that generated distributable profits than to distributionsto owners. Therefore, an entity recognizes the income tax consequences of dividends inprofit or loss, other comprehensive income or equity according to where the entity originallyrecognized those past transactions or events.

An entity applies those amendments for annual reporting periods beginning on or afterJanuary 1, 2019, with early application is permitted.

- 9 -

*SGVFS036564*

∂ Amendments to PAS 23, Borrowing Costs, Borrowing Costs Eligible for Capitalization

The amendments clarify that an entity treats as part of general borrowings any borrowingoriginally made to develop a qualifying asset when substantially all of the activities necessaryto prepare that asset for its intended use or sale are complete.

An entity applies those amendments to borrowing costs incurred on or after the beginning ofthe annual reporting period in which the entity first applies those amendments. An entityapplies those amendments for annual reporting periods beginning on or after January 1, 2019,with early application permitted.

The Company is currently assessing the impact of adopting this standard.

Effective beginning on or after January 1, 2020

ƒ Amendments to PFRS 3, Definition of a Business

The amendments to PFRS 3 clarify the minimum requirements to be a business, remove theassessment of a market participant’s ability to replace missing elements, and narrow thedefinition of outputs. The amendments also add guidance to assess whether an acquired processis substantive and add illustrative examples. An optional fair value concentration test isintroduced which permits a simplified assessment of whether an acquired set of activities andassets is not a business.

An entity applies those amendments prospectively for annual reporting periods beginning on orafter January 1, 2020, with earlier application permitted.

These amendments will apply on future business combinations of the Company.

ƒ Amendments to PAS 1, Presentation of Financial Statements, and PAS 8, Accounting Policies,Changes in Accounting Estimates and Errors, Definition of Material

The amendments refine the definition of material in PAS 1 and align the definitions used acrossPFRSs and other pronouncements. They are intended to improve the understanding of theexisting requirements rather than to significantly impact an entity’s materiality judgements.

An entity applies those amendments prospectively for annual reporting periods beginning on orafter January 1, 2020, with earlier application permitted.

Effective beginning on or after January 1, 2021

ƒ PFRS 17, Insurance Contracts

PFRS 17 is a comprehensive new accounting standard for insurance contracts coveringrecognition and measurement, presentation and disclosure. Once effective, PFRS 17 will replacePFRS 4, Insurance Contracts. This new standard on insurance contracts applies to all types ofinsurance contracts (i.e., life, non-life, direct insurance and re-insurance), regardless of the type ofentities that issue them, as well as to certain guarantees and financial instruments withdiscretionary participation features. A few scope exceptions will apply.

- 10 -

*SGVFS036564*

The overall objective of PFRS 17 is to provide an accounting model for insurance contracts thatis more useful and consistent for insurers. In contrast to the requirements in PFRS 4, which arelargely based on grandfathering previous local accounting policies, PFRS 17 provides acomprehensive model for insurance contracts, covering all relevant accounting aspects. The coreof PFRS 17 is the general model, supplemented by:∂ A specific adaptation for contracts with direct participation features (the variable fee

approach)∂ A simplified approach (the premium allocation approach) mainly for short-duration contracts

PFRS 17 is effective for reporting periods beginning on or after January 1, 2021, withcomparative figures required. Early application is permitted.

The amendments are not applicable since the Company has no activities that are predominantlyconnected with insurance or issuance of insurance contracts.

Deferred effectivity

ƒ Amendments to PFRS 10 and PAS 28, Sale or Contribution of Assets between an Investor and itsAssociate or Joint Venture

The amendments address the conflict between PFRS 10 and PAS 28 in dealing with the loss ofcontrol of a subsidiary that is sold or contributed to an associate or joint venture. Theamendments clarify that a full gain or loss is recognized when a transfer to an associate or jointventure involves a business as defined in PFRS 3. Any gain or loss resulting from the sale orcontribution of assets that does not constitute a business, however, is recognized only to theextent of unrelated investors’ interests in the associate or joint venture.

On January 13, 2016, the Financial Reporting Standards Council deferred the original effectivedate of January 1, 2016 of the said amendments until the International Accounting StandardsBoard (IASB) completes its broader review of the research project on equity accounting that mayresult in the simplification of accounting for such transactions and of other aspects of accountingfor associates and joint ventures.

3. Summary of Significant Accounting Policies

The accounting policies set out below have been applied consistently to all periods presented in theCompany’s financial statements, unless otherwise indicated.

Current versus Non-current ClassificationThe Company presents assets and liabilities in the statement of financial position based oncurrent/non-current classification.

An asset is current when it is:∂ Expected to be realized or intended to be sold or consumed in the normal operating cycle;∂ Held primarily for the purpose of trading;∂ Expected to be realized within twelve months after the reporting period; or∂ Cash or cash equivalent unless restricted from being exchanged or used to settle a liability for at

least twelve months after the reporting period.

All other assets are classified as non-current.

- 11 -

*SGVFS036564*

A liability is current when:∂ It is expected to be settled in the normal operating cycle;∂ It is held primarily for the purpose of trading;∂ It is due to be settled within twelve months after the reporting period; or∂ There is no unconditional right to defer the settlement of the liability for at least twelve months

after the reporting period.

The Company classifies all other liabilities as non-current.

Deferred tax assets and liabilities are classified as noncurrent assets and liabilities.

Fair Value MeasurementFair value is the price that would be received to sell an asset or paid to transfer a liability in an orderlytransaction between market participants at the measurement date. The fair value measurement isbased on the presumption that the transaction to sell the asset or transfer the liability takes placeeither:

∂ In the principal market for the asset or liability; or,∂ In the absence of a principal market, in the most advantageous market for the asset or liability

The principal or the most advantageous market must be accessible by the Company.

The fair value of an asset or a liability is measured using the assumptions that market participantswould use when pricing the asset or liability, assuming that market participants act in their economicbest interest. A fair value measurement of a non-financial asset takes into account a marketparticipant’s ability to generate economic benefits by using the asset in its highest and best use or byselling it to another market participant that would use the asset in its highest and best use.

The Company uses valuation techniques that are appropriate in the circumstances and for whichsufficient data are available to measure fair value, maximizing the use of relevant observable inputsand minimizing the use of unobservable inputs. All assets and liabilities for which fair value ismeasured or disclosed in the financial statements are categorized within the fair value hierarchy,described, as follows, based on the lowest-level input that is significant to the fair value measurementas a whole:

∂ Level 1 – Quoted (unadjusted) market prices in active markets for identical assets or liabilities∂ Level 2 – Valuation techniques for which the lowest-level input that is significant to the fair

value measurement is directly or indirectly observable∂ Level 3 – Valuation techniques for which the lowest-level input that is significant to the fair

value measurement is unobservable

For assets and liabilities that are recognized in the financial statements on a recurring basis, theCompany determines whether transfers have occurred between levels in the hierarchy by reassessingcategorization (based on the lowest-level input that is significant to the fair value measurement as awhole) at the end of each reporting period.

The fair value for financial instruments not traded in an active market is determined by usingvaluation techniques deemed to be appropriate in the circumstances. Valuation techniques includethe market approach (i.e., using recent arm’s length market transactions adjusted as necessary andreference to the current market value of another instrument that is substantially the same) and theincome approach (i.e. discounted cash flow analysis and option pricing models making as much useof available and supportable market data as possible).

- 12 -

*SGVFS036564*

The Company determines the policies and procedures for both recurring fair value measurement andnon-recurring measurement, such as impairment tests. At each reporting date, the Company analysesthe movements in the values of assets and liabilities which are required to be re-measured orreassessed as per the Company’s accounting policies. For this analysis, the Company verifies themajor inputs applied in the latest valuation by agreeing the information in the valuation computationto contracts, counterparty assessment and other relevant documents.

The Company also compares the changes in the fair value of each asset and liability with relevantexternal sources to determine whether the change is reasonable. The Company likewise presents thevaluation results to its independent auditors. This includes a discussion of the major assumptionsused in the valuations.

For the purpose of fair value disclosures, the Company has determined classes of assets and liabilitiesbased on the nature, characteristics and risks of the asset or liability and the level of the fair valuehierarchy as explained above.

Cash and Cash EquivalentsCash comprises cash in banks, which earns interest at prevailing bank deposit rates, and petty cash.Cash equivalents are short-term, highly liquid investments that are readily convertible to knownamounts of cash with original maturities of three months or less from acquisition date and that aresubject to an insignificant risk of changes in value.

Accounting policy applied for financial instruments beginning January 1, 2018

Financial InstrumentsA financial instrument is any contract that gives rise to a financial asset of one entity and a financialliability or equity instrument of another entity.

Financial Instruments: Financial Assets

Classification of Financial Assets. Financial assets are classified in their entirety based on thecontractual cash flows characteristics of the financial assets and the Company’s business model formanaging the financial assets. The Company classifies its financial assets into the followingmeasurement categories:

ƒ financial assets measured at amortized costƒ financial assets measured at FVTPLƒ financial assets measured at FVOCI, where cumulative gains or losses previously recognized are

reclassified to profit or lossƒ financial assets measured at FVOCI, where cumulative gains or losses previously recognized are

not reclassified to profit or loss.

The Company has no financial assets measured at FVTPL as at December 31, 2018.

Contractual Cash Flows CharacteristicsIf the financial asset is held within a business model, whose objective is to hold assets to collectcontractual cash flows or within a business model whose objective is achieved by both collectingcontractual cash flows and selling financial assets, the Company assesses whether the cash flowsfrom the financial asset represent SPPI on the principal amount outstanding.

- 13 -

*SGVFS036564*

In making this assessment, the Company determines whether the contractual cash flows are consistentwith a basic lending arrangement, i.e., interest includes consideration only for the time value ofmoney, credit risk and other basic lending risks and costs associated with holding the financial assetfor a particular period of time. The assessment as to whether the cash flows meet the test is made inthe currency in which the financial asset is denominated.

Business ModelThe Company’s business model is determined at a level that reflects how groups of financial assetsare managed together to achieve a particular business objective. The Company’s business modeldoes not depend on management’s intentions for an individual instrument.

The Company’s business model refers to how it manages its financial assets in order to generate cashflows. The Company’s business model determines whether cash flows will result from collectingcontractual cash flows, selling financial assets, or both.

All financial assets are recognized initially at fair value plus, in the case of financial assets notrecorded at FVTPL, transaction costs that are attributable to the acquisition of the financial asset.

Purchases or sales of financial assets that require delivery of assets within a time frame established byregulation or convention in the market place (regular way trades) are recognized on the trade date,i.e., the date that the Company commits to purchase or sell the asset.

Financial assets at amortized cost. A financial asset is measured at amortized cost if (i) it is heldwithin a business model whose objective is to hold financial assets in order to collect contractual cashflows and (ii) the contractual terms of the financial asset give rise on specified dates to cash flows thatare solely payments of principal and interest on the principal amount outstanding. These financialassets are initially recognized at fair value plus directly attributable transaction costs andsubsequently measured at amortized cost using the EIR method, less any impairment in value. Gainsand losses are recognized in profit or loss when the asset is derecognized, modified or impaired.

As at December 31, 2018, the Company’s financial assets at amortized cost includes cash and cashequivalents, trade and other receivables, refundable deposits and loans receivables (see Notes 5, 6, 18and 26).

Financial assets at FVOCI (Equity Instruments). The Company may also make an irrevocableelection to measure at FVOCI on initial recognition investments in equity instruments that are neitherheld for trading nor contingent consideration recognized in a business combination in accordancewith PFRS 3. Amounts recognized in OCI are not subsequently transferred to profit or loss.However, the Company may transfer the cumulative gain or loss within equity. Dividends on suchinvestments are recognized in profit or loss, unless the dividend clearly represents a recovery of partof the cost of the investment.

Dividends are recognized in profit or loss only when:ƒ the Company’s right to receive payment of the dividend is establishedƒ it is probable that the economic benefits associated with the dividend will flow to the Company;

and,ƒ the amount of the dividend can be measured reliably.

As at December 31, 2018, the Company’s investments in unquoted equity securities are classified asequity instruments at FVOCI (see Note 12).

- 14 -

*SGVFS036564*

Impairment of Financial Assets. PFRS 9 introduces the single, forward-looking “expected loss”impairment model, replacing the “incurred loss” impairment model under PAS 39.

The Company recognizes an allowance for ECL for all debt instruments not held at fair value throughprofit or loss. ECLs are based on the difference between the contractual cash flows due in accordancewith the contract and all the cash flows that the Company expects to receive, discounted at anapproximation of the original effective interest rate. The expected cash flows will include cash flowsfrom the sale of collateral held or other credit enhancements that are integral to the contract terms.

ECLs are recognized in two stages. For credit exposures for which there has not been a significantincrease in credit risk since initial recognition, ECLs are provided for credit losses that result fromdefault events that are possible within the next 12 months (a 12-month ECL). For those creditexposures for which there has been a significant increase in credit risk since initial recognition, a lossallowance is required for credit losses expected over the remaining life of the exposure, irrespectiveof the timing of the default (a lifetime ECL).

For cash in banks and short-term deposits, expected credit loss is computed based on the externallyavailable credit ratings and default rates of the counterparty, adjusted for forward-lookingmacroeconomic factors.

For trade and other receivables, the Company applies simplified approach in calculating ECLs.Therefore, the Company does not track changes in credit risk, but instead recognized a loss allowancebased on lifetime ECLs at each reporting date. The Company establishes a provision matrix that isbased on its historical credit loss experience, adjusted for forward looking factors specific to thedebtors and the economic environment.

An impairment analysis is performed at each reporting date using a provision matrix to measureexpected credit losses. The provision rates are based on days past due for groupings of variouscustomer segments with similar loss patterns. The calculation reflects the probability-weightedoutcome, the time value of money and reasonable and supportable information that is available at thereporting date about past events, current conditions and forecasts of future economic conditions.

Derecognition of Financial Assets. A financial asset (or, where applicable, a part of a financial assetor part of a group of similar financial assets) is primarily derecognized (i.e., removed from theCompany’s statement of financial position) when:

∂ the rights to receive cash flows from the asset have expired; or,∂ the Company has transferred its rights to receive cash flows from the asset or has assumed an

obligation to pay the received cash flows in full without material delay to a third party under a‘pass-through’ arrangement; and either (a) the Company has transferred substantially all the risksand rewards of the asset, or (b) the Company has neither transferred nor retained substantially allthe risks and rewards of the asset, but has transferred control of the asset.

When the Company has transferred its rights to receive cash flows from an asset or has entered into apass-through arrangement, it evaluates if, and to what extent, it has retained the risks and rewards ofownership. When it has neither transferred nor retained substantially all of the risks and rewards ofthe asset, nor transferred control of the asset, the Company continues to recognize the transferredasset to the extent of its continuing involvement. In that case, the Company also recognizes anassociated liability. The transferred asset and the associated liability are measured on a basis thatreflects the rights and obligations that the Company has retained.

- 15 -

*SGVFS036564*

Continuing involvement that takes the form of a guarantee over the transferred asset is measured atthe lower of the original carrying amount of the asset and the maximum amount of consideration thatthe Company could be required to repay.

Financial Instruments: Financial Liabilities

Initial Recognition and Measurement. Financial liabilities are classified, at initial recognition, asfinancial liabilities at FVPL or as financial liabilities at amortized cost, as appropriate.

All financial liabilities are recognized initially at fair value and, in the case of financial liabilities atamortized cost, net of directly attributable transaction costs.

As at December 31, 2018, the Company does not have financial liabilities at FVPL.

Subsequent Measurement. For purposes of subsequent measurement, financial liabilities areclassified either as financial liabilities at FVPL or financial liabilities at amortized cost.

Financial Liabilities at Amortized Cost. After initial recognition, interest-bearing loans andborrowings are subsequently measured at amortized cost using the EIR method.

Gains and losses are recognized in profit or loss when the liabilities are derecognized as well asthrough the EIR amortization process.

Amortized cost is calculated by taking into account any discount or premium on acquisition and feesor costs that are an integral part of the EIR. The EIR amortization is included in profit or loss.

As at December 31, 2018, this category includes the Company’s trade payables and other currentliabilities (except for statutory payables), subscription payable, short-term and long-term loans andfinance lease liability (see Notes 14, 15, 17, 18 and 26).

Derecognition. A financial liability is derecognized when the obligation under the liability isdischarged or cancelled or expires. When an existing financial liability is replaced by another fromthe same lender on substantially different terms, or the terms of an existing liability are substantiallymodified, such an exchange or modification is treated as the derecognition of the original liability andthe recognition of a new liability. The difference in the respective carrying amounts is recognized inthe statement of comprehensive income.

Accounting policy applied for financial instruments until December 31, 2017

Financial InstrumentsA financial instrument is any contract that gives rise to a financial asset of one entity and a financialliability or equity instrument of another entity.

Financial Instruments: Financial Assets

Initial Recognition and Measurement. Financial assets within the scope of PAS 39 are classified asfinancial assets at fair value through profit or loss, or FVPL, loans and receivables, held-to-maturity,or HTM, investments, available-for-sale financial investments or AFS, or as derivatives designated ashedging instruments in an effective hedge, as appropriate. The Company determines theclassification of its financial assets at initial recognition and, where allowed and appropriate, re-evaluates the designation of such assets at each reporting date.

- 16 -

*SGVFS036564*

Financial assets are recognized initially at fair value plus transaction costs that are attributable to theacquisition of the financial asset, except in the case of financial assets recorded at FVPL.

Purchases or sales of financial assets that require delivery of assets within a time frame established byregulation or convention in the market place (regular way purchases or sales) are recognized on thetrade date, i.e., the date that the Company commits to purchase or sell the asset.

Subsequent Measurement. The subsequent measurement of financial assets depends on theirclassification. As at December 31, 2017, the Company does not have financial assets at FVPL, HTMinvestments and AFS financial assets.

Loans and Receivables. Loans and receivables are non-derivative financial assets with fixed ordeterminable payments which are not quoted in an active market. After initial measurement, suchfinancial assets are carried at amortized cost using the effective interest rate, or EIR, method lessimpairment. This method uses an EIR that exactly discounts the estimated future cash payments orreceipts over the expected life of the financial instrument or a shorter period, where appropriate, tothe net carrying amount of the financial asset. Gains and losses are recognized in the incomestatement when the loans and receivables are derecognized or impaired, as well as through theamortization process. Interest earned is recorded in “Interest income” in the Company’s incomestatement. Assets in this category are included in the current assets except for those with maturitiesgreater than 12 months after the end of the reporting period, which are classified as noncurrent assets.

The Company’s loans and receivables include cash and cash equivalents, trade and other receivables,advances to lessors, refundable deposits and loan receivables as at December 31, 2017 (see Notes 5,6, 18 and 26).

Impairment of Financial Assets. The Company assesses, at each reporting date, whether there isobjective evidence that a financial asset or a group of financial assets is impaired. An impairmentexists if one or more events that has occurred since the initial recognition of the asset (an incurred‘loss event’), has an impact on the estimated future cash flows of the financial asset or the group offinancial assets that can be reliably estimated. Evidence of impairment may include indications thatthe debtors or a group of debtors is experiencing significant financial difficulty, default ordelinquency in interest or principal payments, the probability that they will enter bankruptcy or otherfinancial reorganization and observable data indicating that there is a measurable decrease in theestimated future cash flows, such as changes in arrears or economic conditions that correlate withdefaults.

Derecognition of Financial Assets. A financial asset (or, where applicable, a part of a financial assetor part of a group of similar financial assets) is primarily derecognized (i.e., removed from theCompany’s statement of financial position) when:

∂ The rights to receive cash flows from the asset have expired; or∂ The Company has transferred its rights to receive cash flows from the asset or has assumed an

obligation to pay the received cash flows in full without material delay to a third party under a‘pass-through’ arrangement; and either (a) the Company has transferred substantially all the risksand rewards of the asset, or (b) the Company has neither transferred nor retained substantially allthe risks and rewards of the asset, but has transferred control of the asset.

When the Company has transferred its rights to receive cash flows from an asset or has entered into apass-through arrangement, it evaluates if, and to what extent, it has retained the risks and rewards ofownership.

- 17 -

*SGVFS036564*

When it has neither transferred nor retained substantially all of the risks and rewards of the asset, nortransferred control of the asset, the Company continues to recognize the transferred asset to the extentof its continuing involvement. In that case, the Company also recognizes an associated liability. Thetransferred asset and the associated liability are measured on a basis that reflects the rights andobligations that the Company has retained.

Continuing involvement that takes the form of a guarantee over the transferred asset is measured atthe lower of the original carrying amount of the asset and the maximum amount of consideration thatthe Company could be required to repay.

Financial Instruments: Financial Liabilities

Initial Recognition and Measurement. Financial liabilities within the scope of PAS 39 are classifiedas financial liabilities at FVPL, other financial liabilities, or as derivatives designated as hedginginstruments in an effective hedge, as appropriate. The Company determines the classification of thefinancial liabilities at initial recognition.

Financial liabilities are recognized initially at fair value and, in the case of loans and borrowings, netof directly attributable transaction costs.

Subsequent Measurement. The subsequent measurement of financial liabilities depends on theirclassification as described below:

Financial Liabilities at FVPL. Financial liabilities at FVPL include financial liabilities held-for-trading and financial liabilities designated upon initial recognition as at FVPL. Financial liabilitiesare classified as held-for-trading if they are acquired for the purpose of selling in the near term.Derivative liabilities, including separated embedded derivatives are also classified as at FVPL unlessthey are designated as effective hedging instruments as defined by PAS 39.

Financial liabilities may be designated at initial recognition as at FVPL if any of the following criteriaare met: (i) the designation eliminates or significantly reduces the inconsistent treatment that wouldotherwise arise from measuring the liabilities or recognizing gains or losses on them on differentbases; (ii) the liabilities are part of a group of financial liabilities which are managed and theirperformance are evaluated on a fair value basis, in accordance with a documented risk managementstrategy and information about the company’s financial liabilities is provided internally on that basisto the entity’s key management personnel; or (iii) the financial liabilities contain an embeddedderivative, unless the embedded derivative does not significantly modify the cash flows or it is clear,with little or no analysis, that it would not be separately recorded.

The Company has no financial liabilities carried at FVPL as at December 31, 2017.

Other Financial Liabilities. After initial recognition, other financial liabilities are subsequentlymeasured at amortized cost using the EIR method.

Gains and losses are recognized in the statement of comprehensive income when the liabilities arederecognized as well as through the EIR amortization process. Amortized cost is calculated by takinginto account any discount or premium on acquisition and fees or costs that are an integral part of theEIR.

The Company’s other financial liabilities include trade payables and other current liabilities (exceptfor statutory payables), subscription payable, long-term loans and finance lease liability as atDecember 31, 2017 (see Notes 14, 15, 17, 18 and 26).

- 18 -

*SGVFS036564*

Debt Issue Costs. Debt issue costs are deducted against long-term loans and are amortized over theterms of the related borrowings using the EIR method.

Derecognition. A financial liability is derecognized when the obligation under the liability isdischarged or cancelled or expires. When an existing financial liability is replaced by another fromthe same lender on substantially different terms, or the terms of an existing liability are substantiallymodified, such an exchange or modification is treated as the derecognition of the original liability andthe recognition of a new liability. The difference in the respective carrying amounts is recognized inthe statement of profit or loss.

Offsetting of Financial Assets and Financial LiabilitiesFinancial assets and financial liabilities are offset and the net amount is reported in the statement offinancial position if, and only if, there is a currently enforceable legal right to offset the recognizedamounts and there is an intention to settle on a net basis, or to realize the assets and settle theliabilities simultaneously.

“Day 1” DifferenceWhere the transaction price in a non-active market is different from the fair value of other observablecurrent market transactions in the same instrument or based on a valuation technique which variablesinclude only data from observable market, the Company recognizes the difference between thetransaction price and fair value (a “Day 1” difference) in the Company’s statement of comprehensiveincome unless it qualifies for recognition as some other type of asset or liability. In cases where dataused by the Company are not observable, the difference between the transaction price and modelvalue is only recognized in the income statement when the inputs become observable or when theinstrument is derecognized. For each transaction, the Company determines the appropriate method ofrecognizing the “Day 1” difference amount.

Property and EquipmentProperty and equipment, including assets under finance lease, are carried at cost, excluding day-to-day servicing, less accumulated depreciation, amortization and any impairment loss. The initial costof property and equipment comprises its purchase price, including import duties and non-refundablepurchase taxes and any directly attributable costs of bringing the property and equipment to itsworking condition and location for its intended use. Such cost includes the cost of replacing part ofsuch property and equipment and borrowing cost for long-term construction project when recognitioncriteria are met. When significant parts of property and equipment are required to be replaced atintervals, the Company recognizes such parts as individual assets with specific useful lives anddepreciation, respectively. Likewise, when major repairs are performed, its cost is recognized in thecarrying amount of the property and equipment as a replacement if the recognition criteria aresatisfied.

Expenditures incurred after the property and equipment have been put into operation, such as repairsand maintenance, are normally recognized as expense in the period such costs are incurred. Insituations where it can be clearly demonstrated that the expenditures have resulted in an increase inthe future economic benefits expected to be obtained from the use of property and equipment beyondits originally assessed standard of performance, the expenditures are capitalized as additional cost ofthe property and equipment.

- 19 -

*SGVFS036564*

Depreciation and amortization commence once the property and equipment are available for use andis computed using the straight-line method over the estimated useful lives of the assets as follows:

Warehousing equipment 5 to 10 yearsHeavy equipment 5 yearsTransportation equipment 5 yearsComputer and office equipment 3 to 5 yearsSoftware 3 yearsLeasehold improvement 3 years or term of the lease,

whichever is shorter

The asset’s residual values, useful lives and depreciation and amortization method are reviewed, andadjusted if appropriate, at each financial reporting period.

An item of property and equipment is derecognized upon disposal or when no future economicbenefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset(calculated as the difference between the net disposal proceeds and the carrying amount of the asset)is included in the statement of comprehensive income when the asset is derecognized.

Investment in and Advances to SubsidiariesInvestment in and advances to subsidiaries are accounted for at cost less any impairment in value.

A subsidiary is an entity controlled by the parent company. The parent company controls an entitywhen it is exposed or has rights to variable returns from its involvement with the entity and has theability to affect those returns through its power over the entity, generally accompanied by ashareholding more than one half of the voting rights. The existence and effect of potential votingrights that are currently exercisable or convertible are considered when assessing whether the parentcompany controls another entity.

Business Combinations and GoodwillBusiness combinations are accounted for using the acquisition method. The cost of an acquisition ismeasured as the aggregate of the consideration transferred measured at acquisition date fair value andthe amount of any non-controlling interest (NCI) in the acquiree. For each business combination, theCompany elects whether to measure the NCI in the acquiree at fair value or at the proportionate shareof the acquiree’s identifiable net assets. Acquisition costs incurred are expensed and included ingeneral and administrative expenses.

When the Company acquires a business, it assesses the financial assets and liabilities assumed forappropriate classification and designation in accordance with the contractual terms, economiccircumstances and pertinent conditions as of the acquisition date. This includes the separation ofembedded derivatives in host contracts by the acquiree.

If the business combination is achieved in stages, any previously held equity interest isre-measured at its acquisition date fair value and any resulting gain or loss is recognized in profit orloss. It is then considered in the determination of goodwill.

Any contingent consideration to be transferred by the acquirer will be recognized at fair value at theacquisition date. Contingent consideration classified as an asset or liability that is a financialinstrument and within the scope of PAS 39, is measured at fair value with changes in fair valuerecognized either in the statement of comprehensive income or as a change to other comprehensiveincome. If the contingent consideration is not within the scope of PAS 39, it is measured inaccordance with the appropriate PFRS. Contingent consideration that is classified as equity is not re-measured and subsequent settlement is accounted for within equity.

- 20 -

*SGVFS036564*

Goodwill is initially measured at cost, being the excess of the aggregate of the considerationtransferred and the amount recognized for NCI, and any previous interest held, over the netidentifiable assets acquired and liabilities assumed. If the fair value of the net assets acquired is inexcess of the aggregate consideration transferred, the Company re-assesses whether it has correctlyidentified all of the assets acquired and all of the liabilities assumed and reviews the procedures usedto measure the amounts to be recognized at the acquisition date. If the re-assessment still results in anexcess of the fair value of net assets acquired over the aggregate consideration transferred, then thegain is recognized immediately in profit or loss.

After initial recognition, goodwill is measured at cost less any accumulated impairment losses. Forthe purpose of impairment testing, goodwill acquired in a business combination is, from theacquisition date, allocated to each of the Company’s cash-generating units (CGUs) that are expectedto benefit from the combination, irrespective of whether other assets or liabilities of the acquiree areassigned to those units.