Embed Size (px)

Citation preview

Michael A. PaganoDean, College of Urban Planning &

Public AffairsUniversity of Illinois at Chicago

[email protected] View From 18th Street Bridge, a watercolor by Pat Wright

Tuesdays at APA Chicago29 January 2013

The Great Recession, Municipal Budgets, and

Land Development

The Great Recession, Municipal Budgets, and Land Development

• Setting the stage:–The contemporary situation

• Challenges– Economy is Changing

• Aligning Economic Base with Fiscal Authority– Fiscal Foundation is Changing

• Narrowing the Tax Base– Linking fiscal architecture and space

• Spatialization of revenue structures

• Options: The Fiscal Policy Space• A new sustainable fiscal architecture?

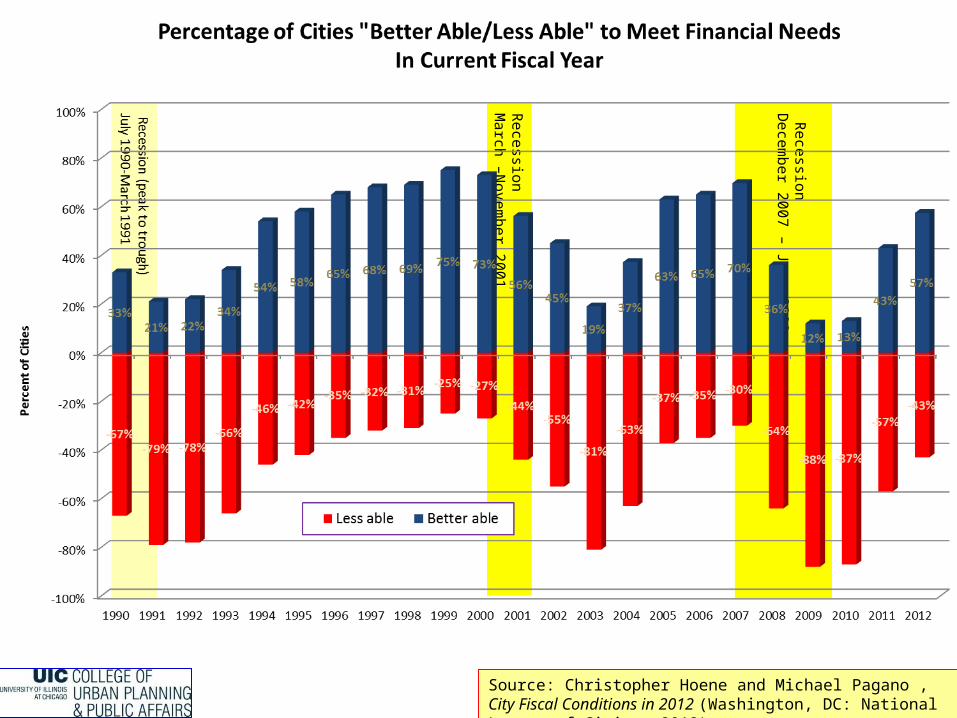

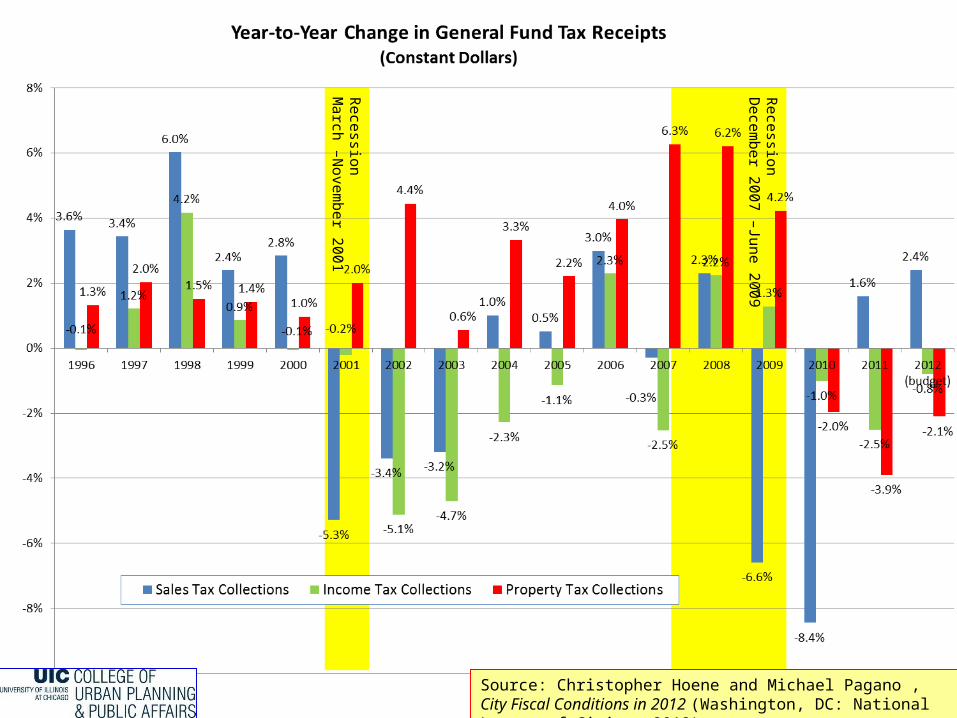

RecessionD

ecember 2007 – June 2009

RecessionM

arch –Novem

ber 2001

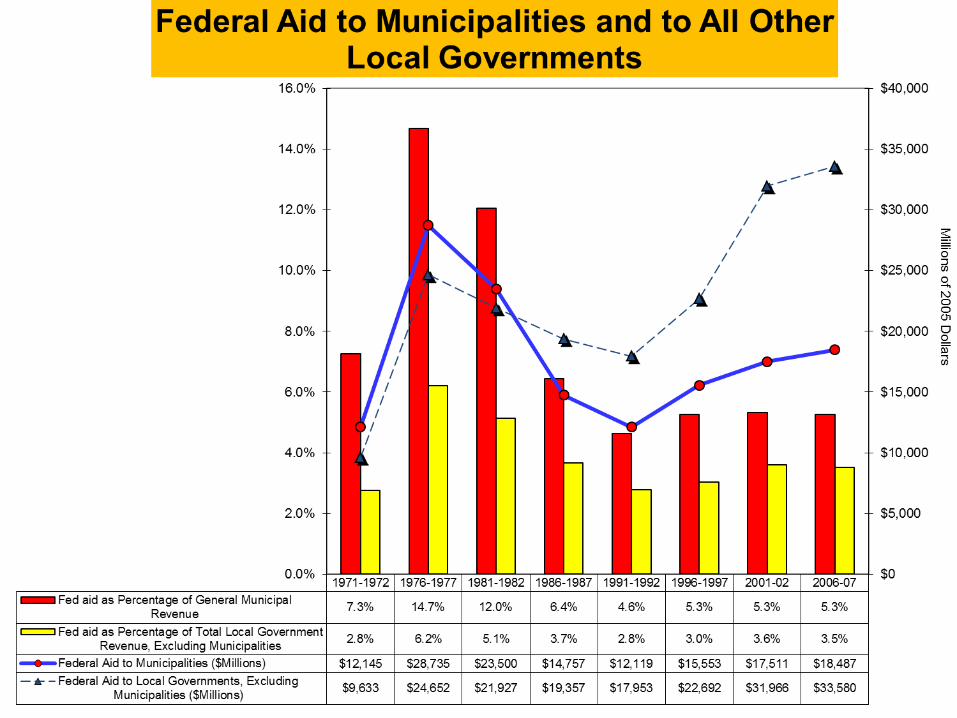

Source: Christopher Hoene and Michael Pagano , City Fiscal Conditions in 2012 (Washington, DC: National League of Cities, 2012)

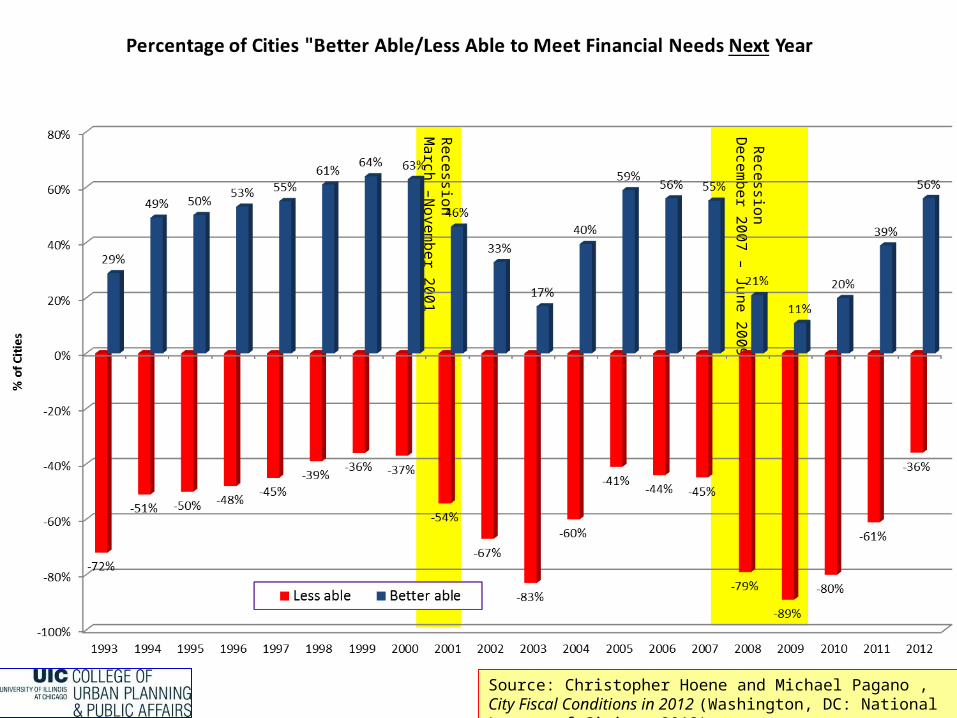

RecessionM

arch –Novem

ber 2001

RecessionD

ecember 2007 – June 2009

Source: Christopher Hoene and Michael Pagano , City Fiscal Conditions in 2012 (Washington, DC: National League of Cities, 2012)

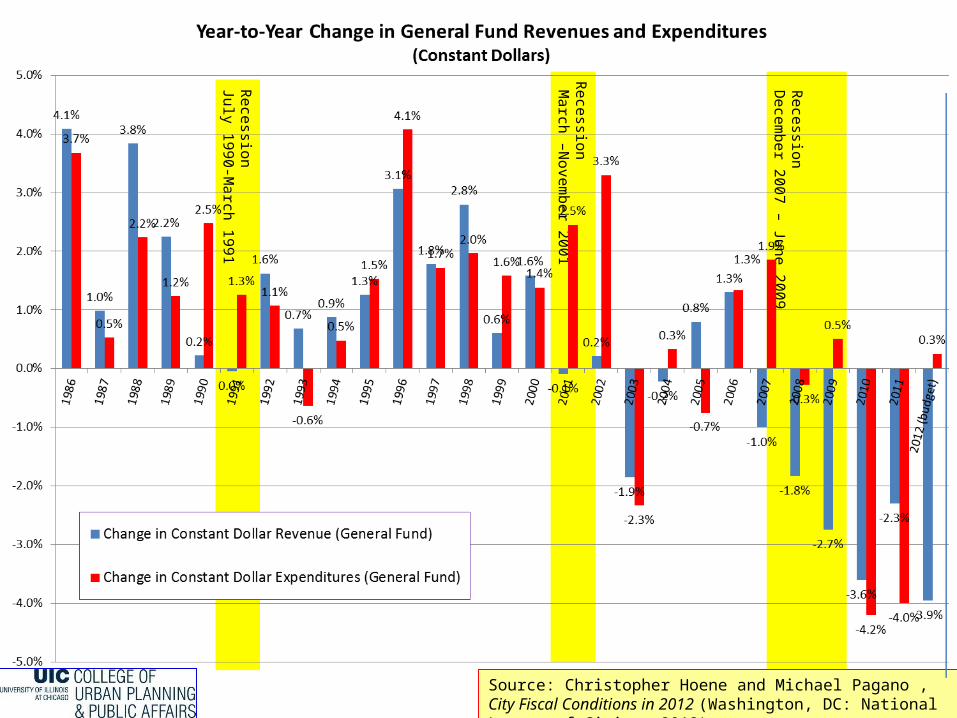

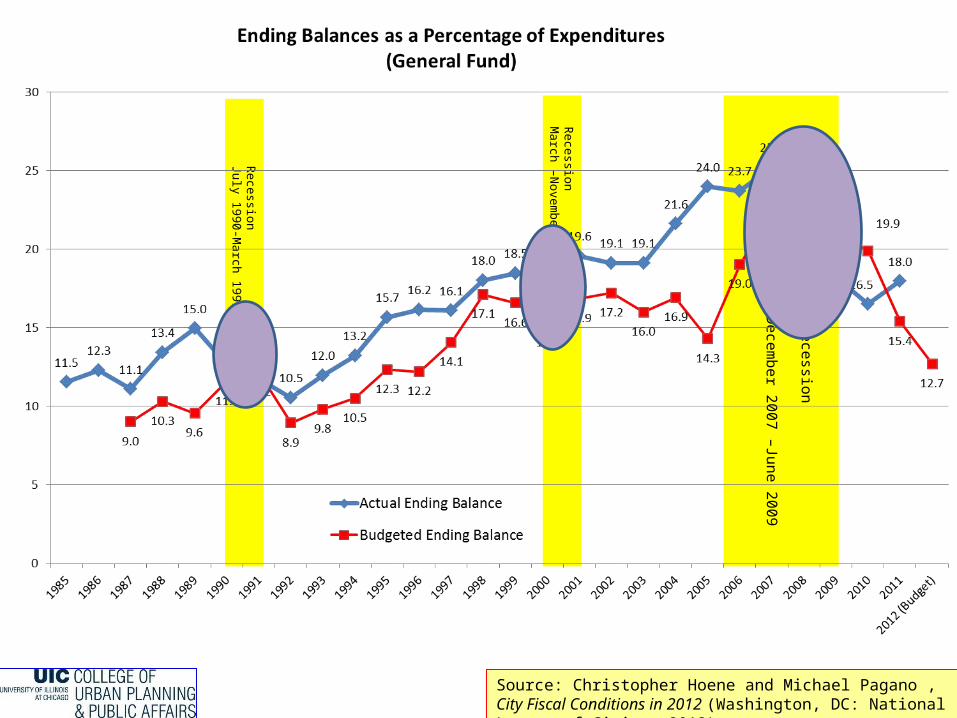

Recession D

ecember 2007 – June 2009

Recession M

arch –Novem

ber 2001

RecessionJuly 1990-M

arch 1991

Source: Christopher Hoene and Michael Pagano , City Fiscal Conditions in 2012 (Washington, DC: National League of Cities, 2012)

RecessionD

ecember 2007 –June 2009

RecessionM

arch –Novem

ber 2001

Source: Christopher Hoene and Michael Pagano , City Fiscal Conditions in 2012 (Washington, DC: National League of Cities, 2012)

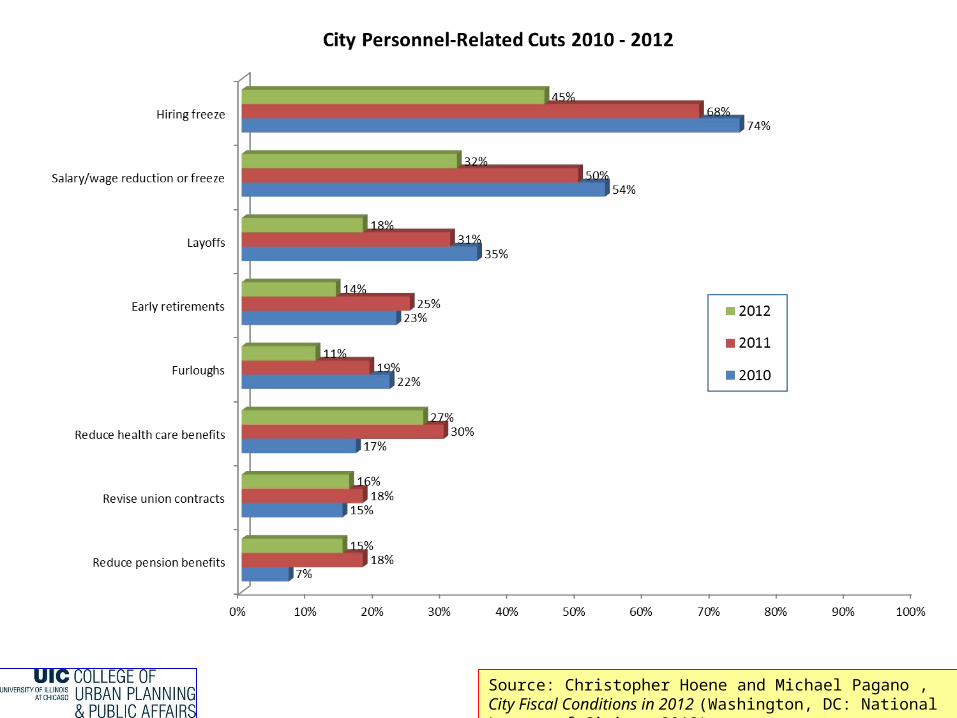

Source: Christopher Hoene and Michael Pagano , City Fiscal Conditions in 2012 (Washington, DC: National League of Cities, 2012)

Recession D

ecember 2007 –June 2009

Recession M

arch –Novem

ber 2001

Recession July 1990-M

arch 1991

Source: Christopher Hoene and Michael Pagano , City Fiscal Conditions in 2012 (Washington, DC: National League of Cities, 2012)

The Great Recession, Municipal Budgets, and Land Development

• Setting the stage:– The contemporary situation

• Challenges– Economy is Changing:• Aligning Economic Base with Fiscal Authority

– Fiscal Foundation is Changing:• Narrowing the Tax Base

– Linking fiscal architecture and space• Spatialization of revenue structures

• Options: The Fiscal Policy Space• A new sustainable fiscal architecture?

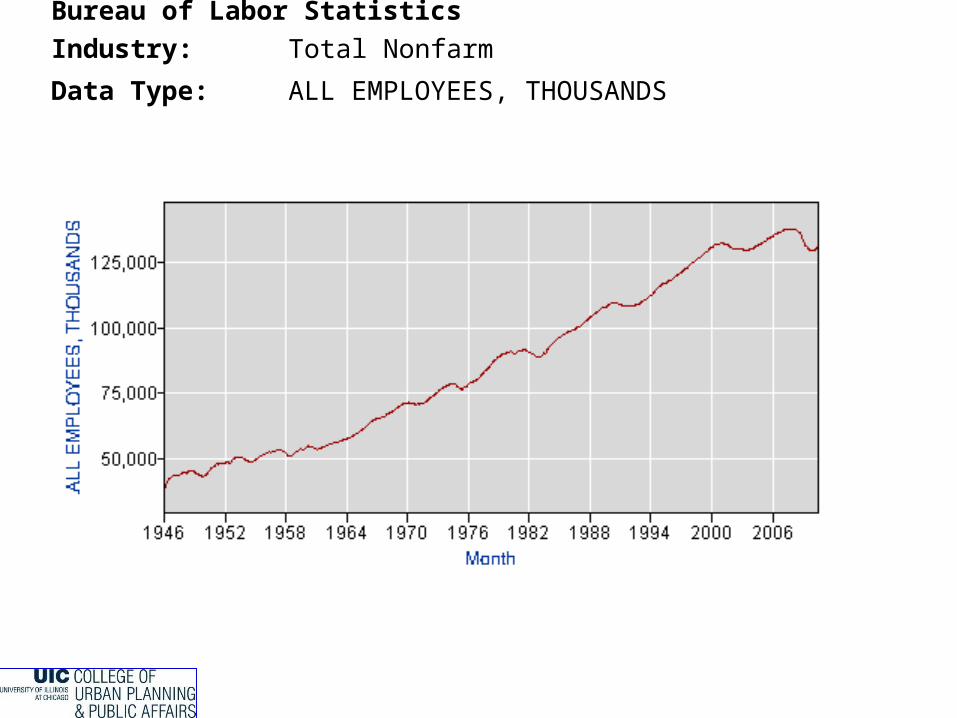

Bureau of Labor StatisticsIndustry: Total Nonfarm

Data Type: ALL EMPLOYEES, THOUSANDS

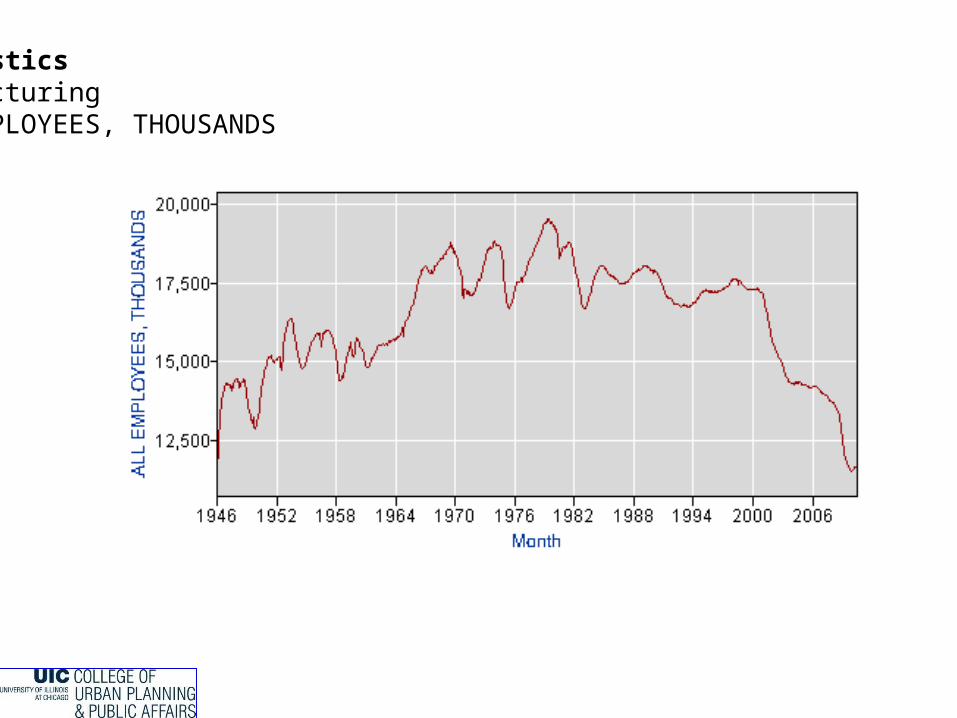

Bureau of Labor StatisticsIndustry: ManufacturingData Type: ALL EMPLOYEES, THOUSANDS

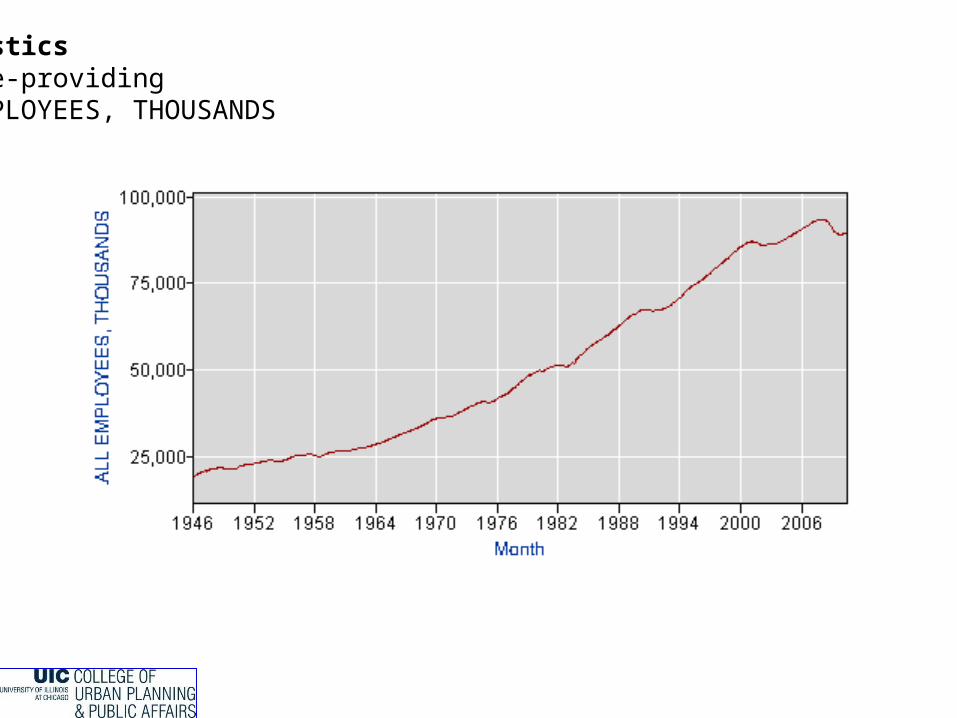

Bureau of Labor StatisticsIndustry: Service-providingData Type: ALL EMPLOYEES, THOUSANDS

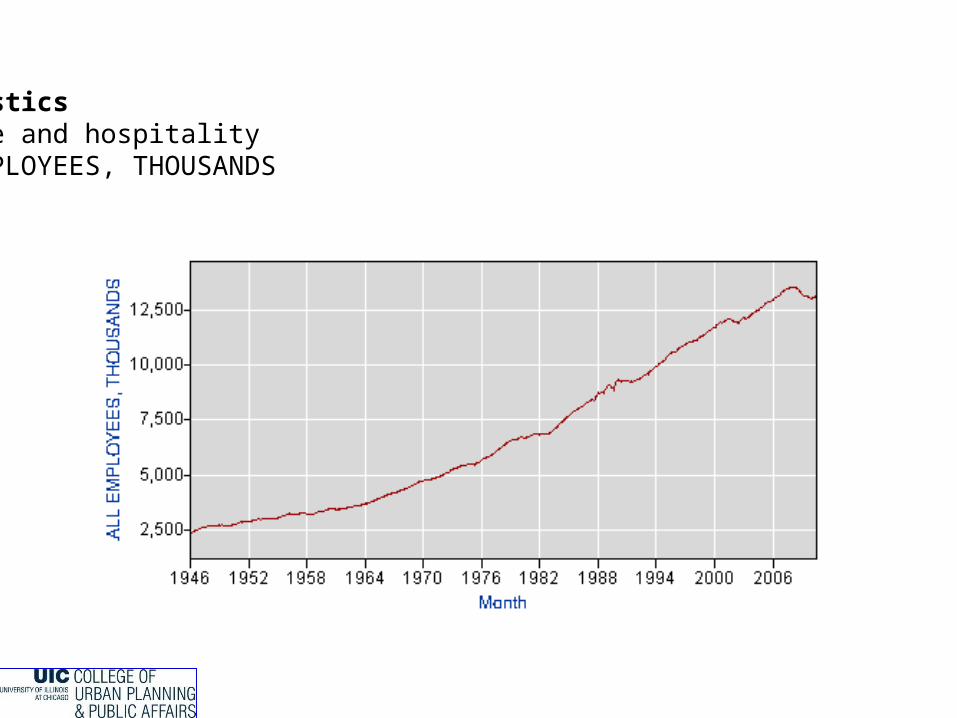

Bureau of Labor StatisticsIndustry: Leisure and hospitalityData Type: ALL EMPLOYEES, THOUSANDS

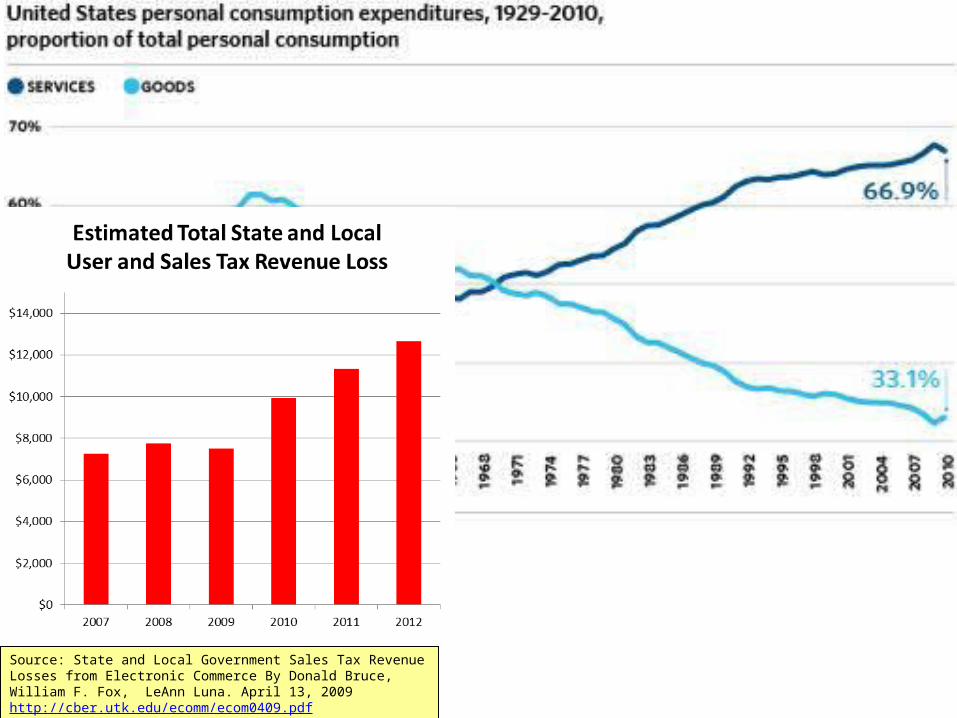

Source: State and Local Government Sales Tax Revenue Losses from Electronic Commerce By Donald Bruce, William F. Fox, LeAnn Luna. April 13, 2009 http://cber.utk.edu/ecomm/ecom0409.pdf

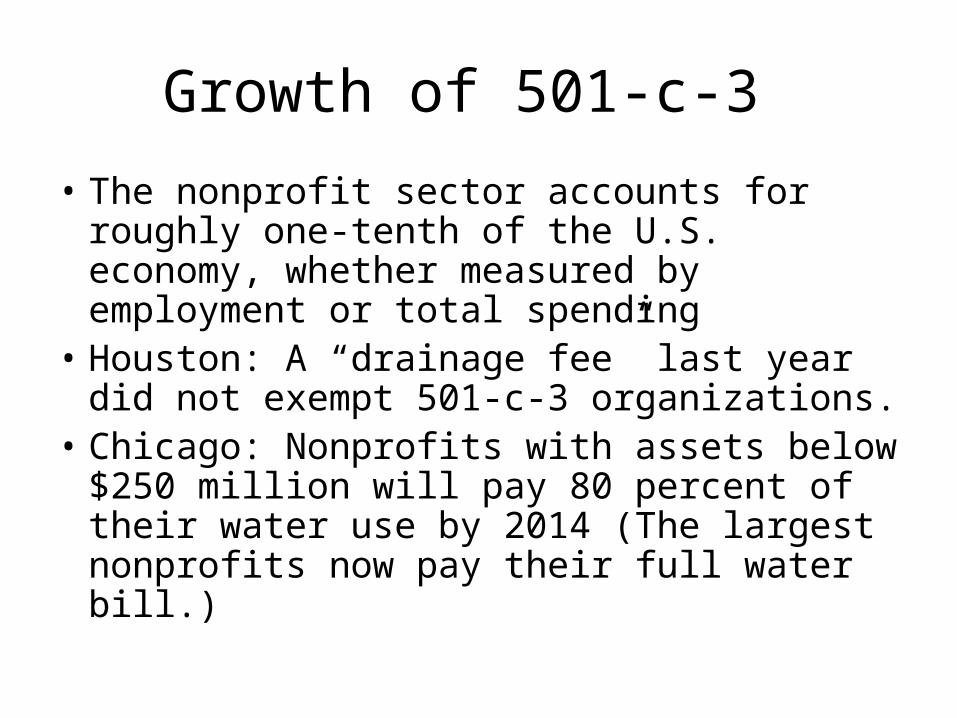

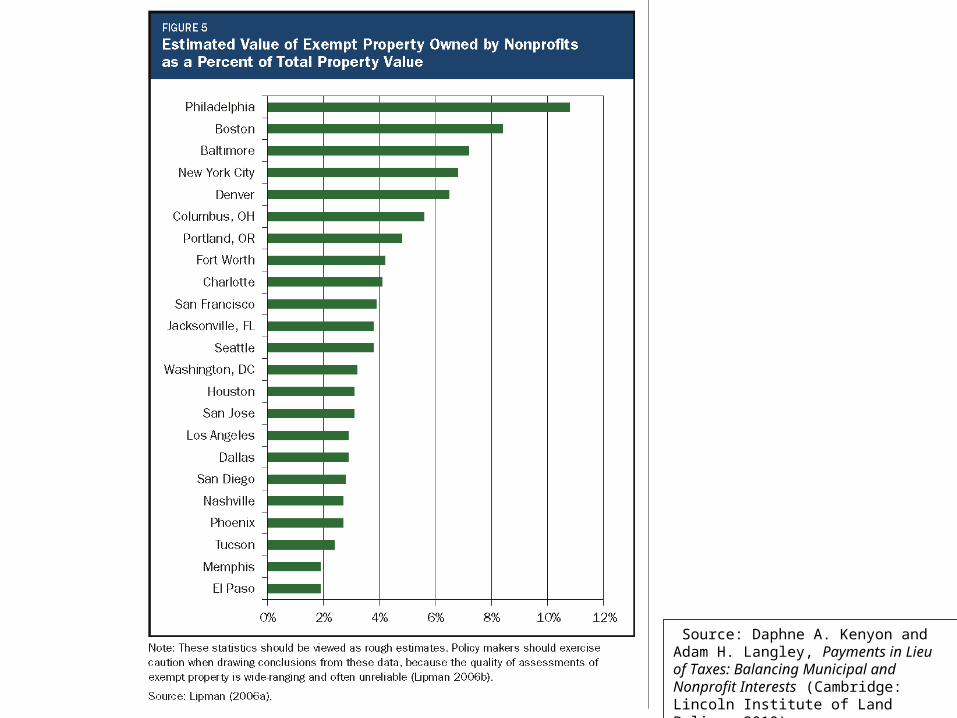

Growth of 501-c-3

• The nonprofit sector accounts for roughly one-tenth of the U.S. economy, whether measured by employment or total spending• Houston: A “drainage fee” last year did not

exempt 501-c-3 organizations.• Chicago: Nonprofits with assets below $250

million will pay 80 percent of their water use by 2014 (The largest nonprofits now pay their full water bill.)

Source: Daphne A. Kenyon and Adam H. Langley, Payments in Lieu of Taxes: Balancing Municipal and Nonprofit Interests (Cambridge: Lincoln Institute of Land Policy, 2010).

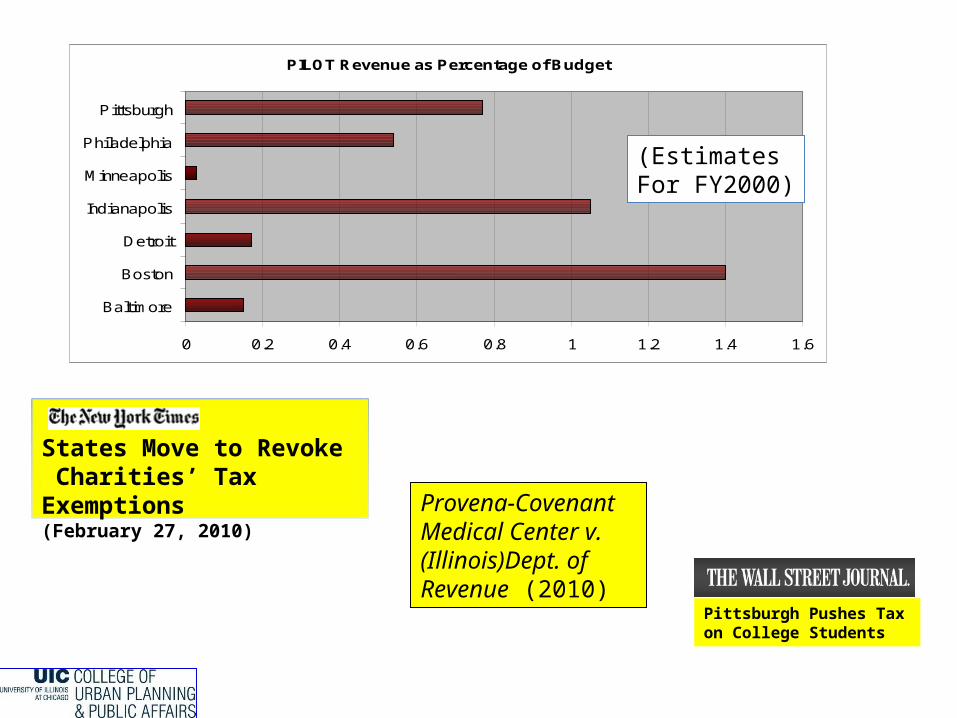

PILOT Revenue as Percentage of Budget

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6

Baltimore

Boston

Detroit

Indianapolis

Minneapolis

Philadelphia

Pittsburgh

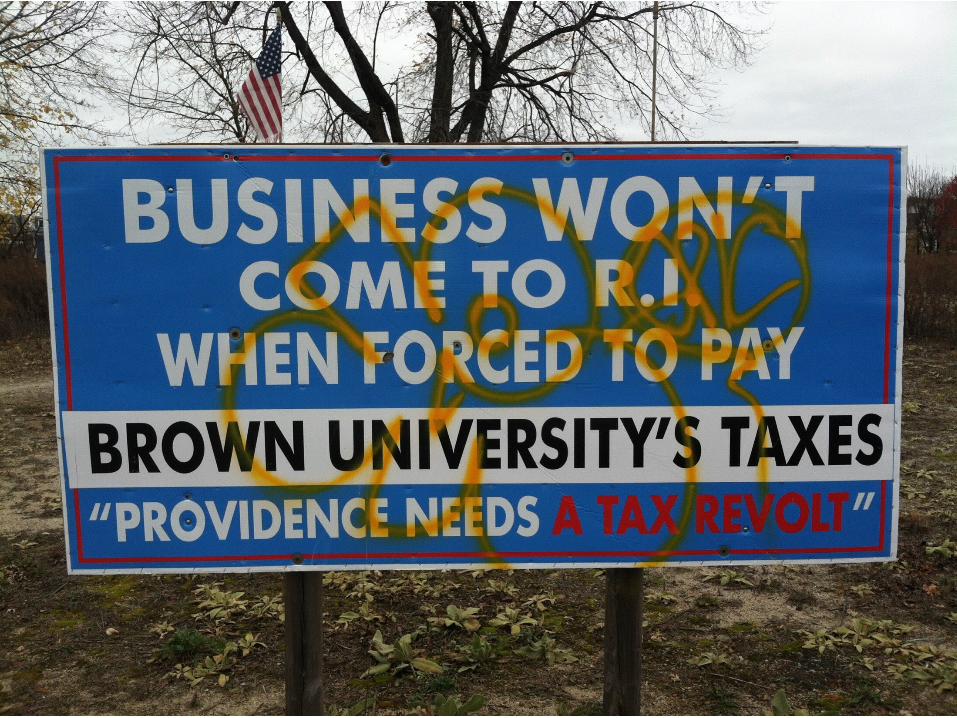

States Move to Revoke Charities’ Tax Exemptions(February 27, 2010) Provena-Covenant

Medical Center v. (Illinois)Dept. of Revenue (2010)

Pittsburgh Pushes Tax on College Students

(EstimatesFor FY2000)

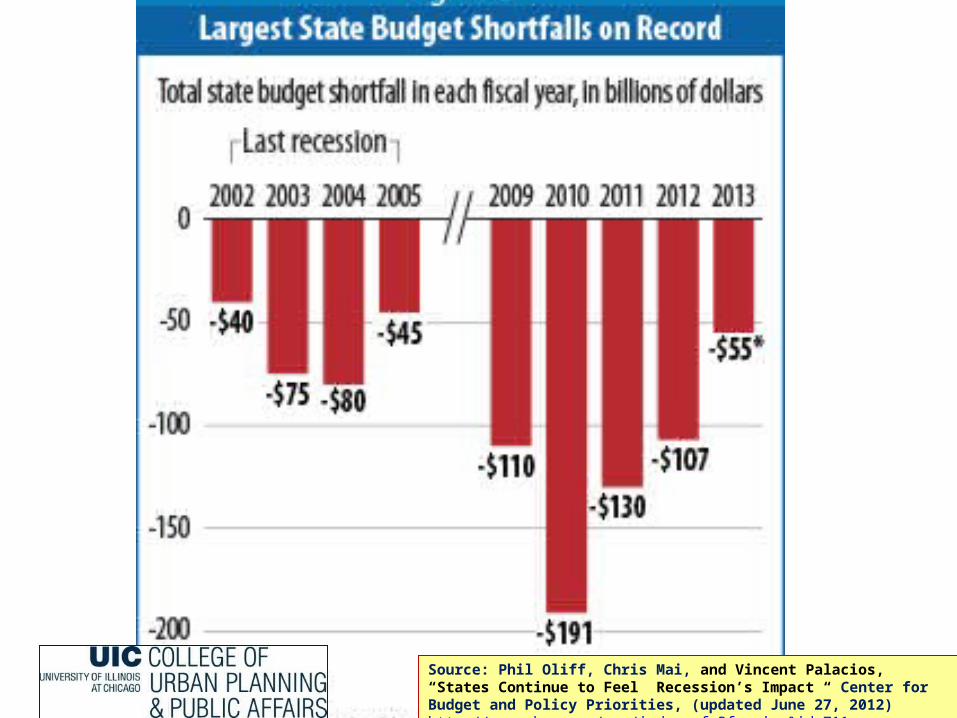

Source: Phil Oliff, Chris Mai, and Vincent Palacios, “States Continue to Feel Recession’s Impact “ Center for Budget and Policy Priorities, (updated June 27, 2012) http://www.cbpp.org/cms/index.cfm?fa=view&id=711

Parcels will be identified for development that maximize revenues or minimize costs. This choice is informed by a city’s revenue structure and manifests itself spatially in the design, land-use designations and development patterns of the city and region, or the spatialization of spatialization of revenue structures.revenue structures.

Spatialization of Revenue Structures

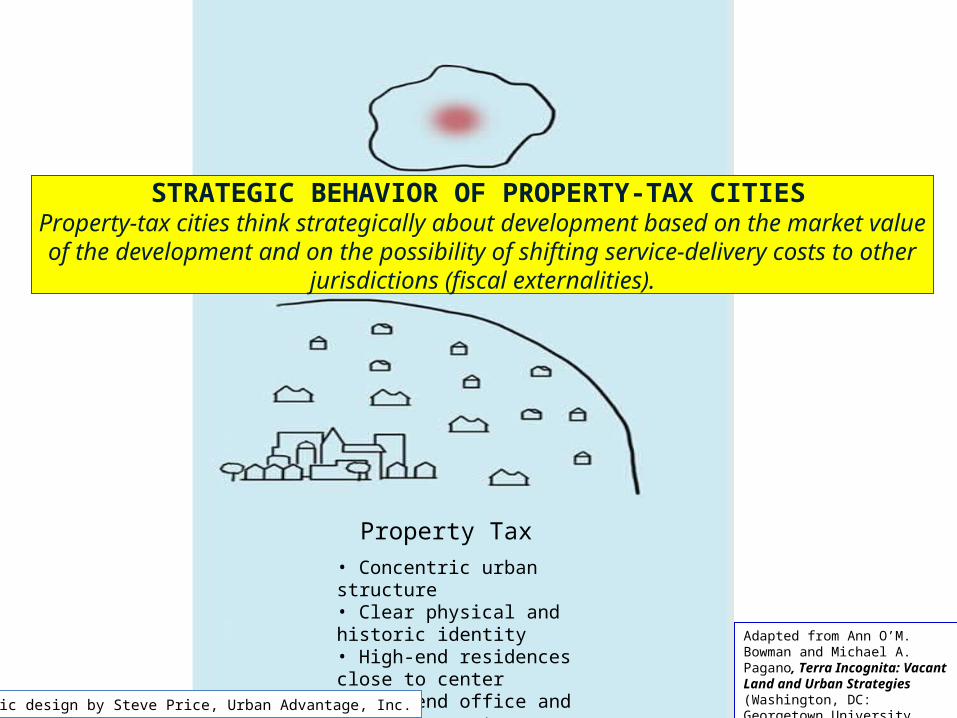

• Concentric urban structure• Clear physical and historic identity • High-end residences close to center• High-end office and retail in center

Graphic design by Steve Price, Urban Advantage, Inc.

Property Tax

Adapted from Ann O’M. Bowman and Michael A. Pagano, Terra Incognita: Vacant Land and Urban Strategies (Washington, DC: Georgetown University Press, 2004).

STRATEGIC BEHAVIOR OF PROPERTY-TAX CITIES

Property-tax cities think strategically about development based on the market value of the development and on the possibility of shifting service-delivery costs to other jurisdictions

(fiscal externalities).

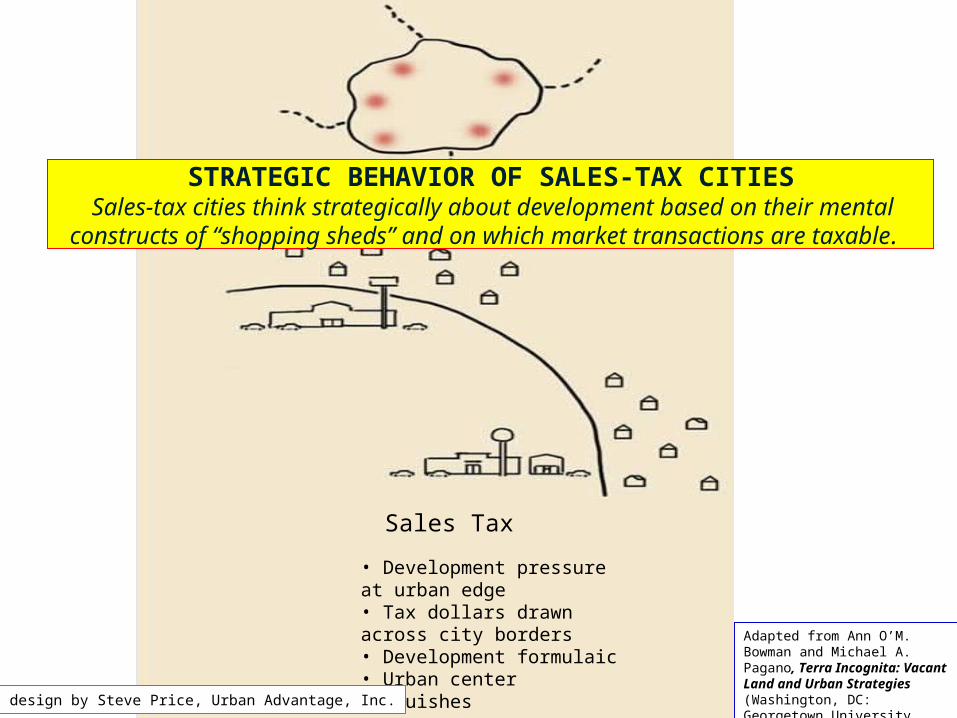

• Development pressure at urban edge• Tax dollars drawn across city borders• Development formulaic• Urban center languishes

Sales Tax

Graphic design by Steve Price, Urban Advantage, Inc.

Adapted from Ann O’M. Bowman and Michael A. Pagano, Terra Incognita: Vacant Land and Urban Strategies (Washington, DC: Georgetown University Press, 2004).

STRATEGIC BEHAVIOR OF SALES-TAX CITIES Sales-tax cities think strategically about development based on their mental constructs of

“shopping sheds” and on which market transactions are taxable.

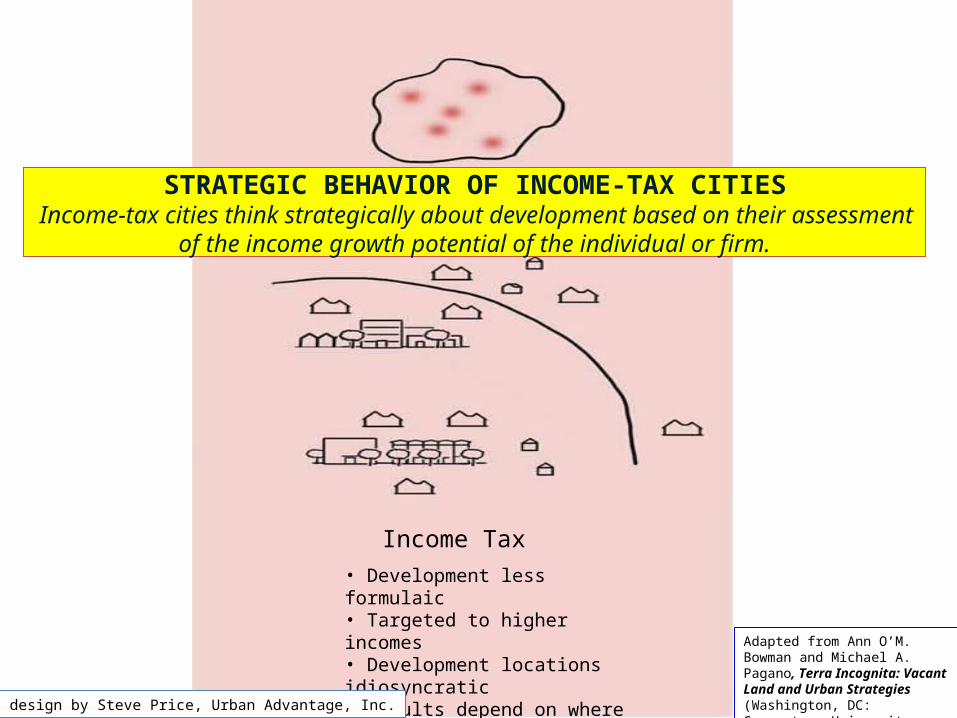

• Development less formulaic• Targeted to higher incomes• Development locations idiosyncratic• Results depend on where tax collected

Income Tax

Graphic design by Steve Price, Urban Advantage, Inc.

STRATEGIC BEHAVIOR OF INCOME-TAX CITIES Income-tax cities think strategically about development based on their assessment of the

income growth potential of the individual or firm.

Adapted from Ann O’M. Bowman and Michael A. Pagano, Terra Incognita: Vacant Land and Urban Strategies (Washington, DC: Georgetown University Press, 2004).

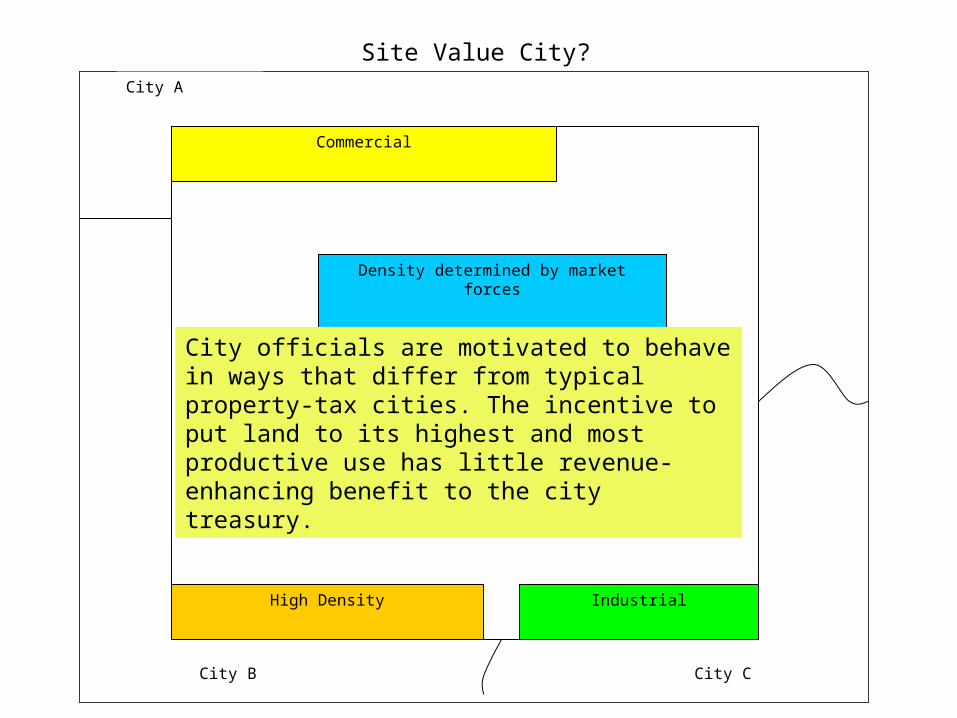

Density determined by market forces

Commercial

IndustrialHigh Density

City B City C

City A

City officials are motivated to behave in ways that differ from typical property-tax cities. The incentive to put land to its highest and most productive use has little revenue-enhancing benefit to the city treasury.

Site Value City?

The Great Recession, Municipal Budgets, and Land Development

• Setting the stage:– The contemporary situation

• Challenges– Economy is Changing:• Aligning Economic Base with Fiscal Authority

– Fiscal Foundation is Changing:• Narrowing the Tax Base

– Linking fiscal architecture and space• Spatialization of revenue structures

• Options: The Fiscal Policy Space• A new sustainable fiscal architecture?

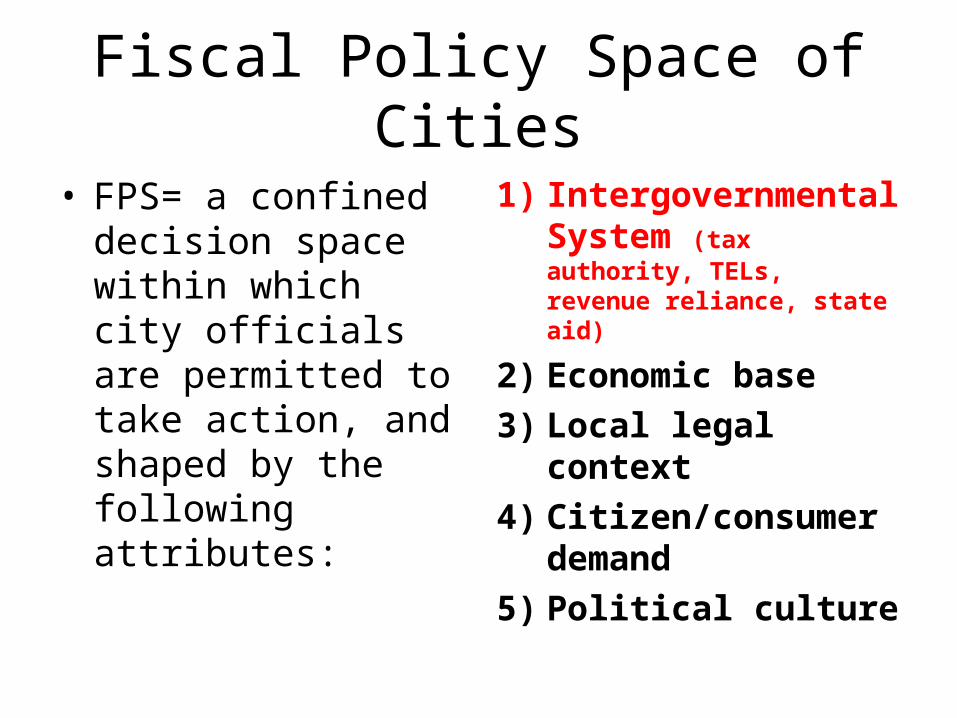

Fiscal Policy Space of Cities

• FPS= a confined decision space within which city officials are permitted to take action, and shaped by the following attributes:

1) Intergovernmental System (tax authority, TELs, revenue reliance, state aid)

2) Economic base3) Local legal context4) Citizen/consumer

demand5) Political culture

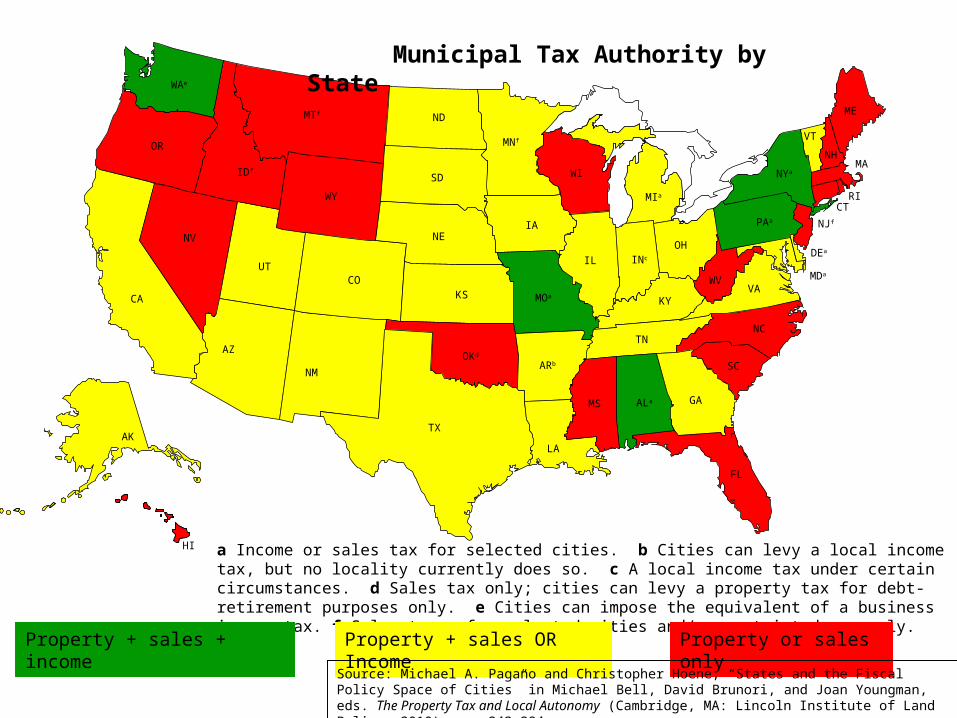

MTf

WY

IDf

WAe

OR

NV

UT

CA

AZ

ND

SD

NE

CO

NM

TX

OKd

KS

ARb

LA

MOa

IA

MNf

WI

IL INc

KY

TN

MS ALa GA

FL

SC

NC

VAWV

OH

MIa

NYa

PAa

MDa

DEa

NJf

CTRI

MA

ME

VT

NH

AK

HI a Income or sales tax for selected cities. b Cities can levy a local income tax, but no locality currently does so. c A local income tax under certain circumstances. d Sales tax only; cities can levy a property tax for debt-retirement purposes only. e Cities can impose the equivalent of a business income tax. f Sales taxes for selected cities and/or restricted use only.

Property + sales + income Property + sales OR Income Property or sales only

Municipal Tax Authority by State

Source: Michael A. Pagano and Christopher Hoene, “States and the Fiscal Policy Space of Cities” in Michael Bell, David Brunori, and Joan Youngman, eds. The Property Tax and Local Autonomy (Cambridge, MA: Lincoln Institute of Land Policy, 2010), pp. 243-284.

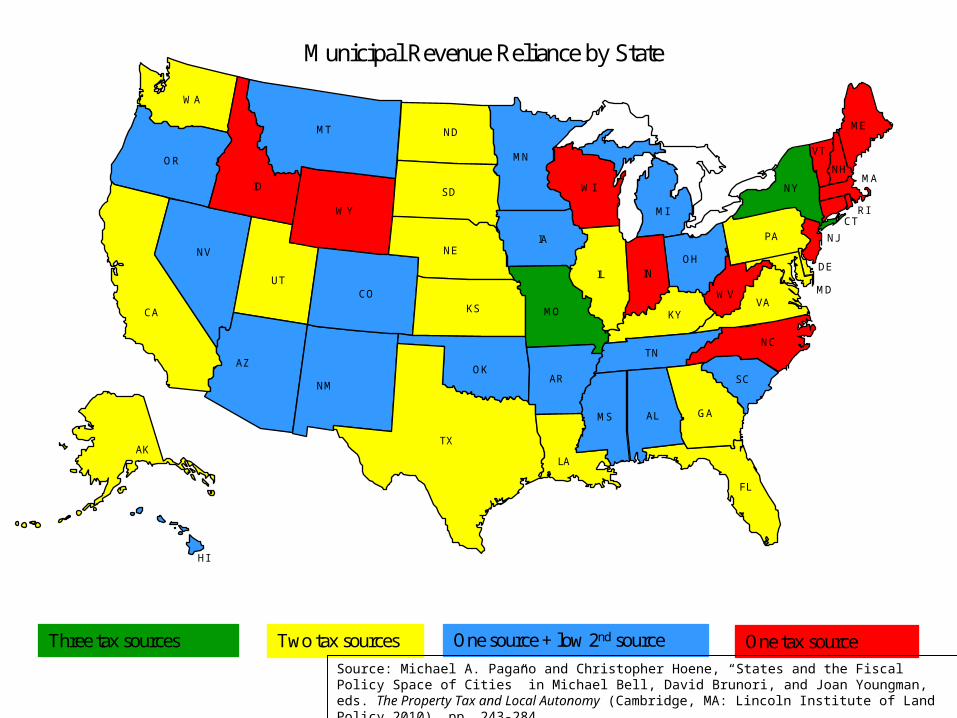

MT

WY

ID

WA

OR

NV

UT

CA

AZ

ND

SD

NE

CO

NM

TX

OK

KS

AR

LA

MO

IA

MN

WI

IL IN

KY

TN

MS AL GA

FL

SC

NC

VAWV

OH

MI

NY

PA

MD

DE

NJ

CTRI

MA

ME

VT

NH

AK

HI

Three tax sources Two tax sources One tax sourceOne source + low 2nd source

Municipal Revenue Reliance by State

Source: Michael A. Pagano and Christopher Hoene, “States and the Fiscal Policy Space of Cities” in Michael Bell, David Brunori, and Joan Youngman, eds. The Property Tax and Local Autonomy (Cambridge, MA: Lincoln Institute of Land Policy,2010), pp. 243-284.

MT

WY

ID

WA

OR

NV

UT

CA

AZ

ND

SD

NE

CO

NM

TX

OK

KS

AR

LA

MO

IA

MN

WI

IL IN

KY

TN

MS AL GA

FL

SC

NC

VAWV

OH

MI

NY

PA

MD

DE

NJ

CTRI

MA

ME

VT

NH

AK

HI

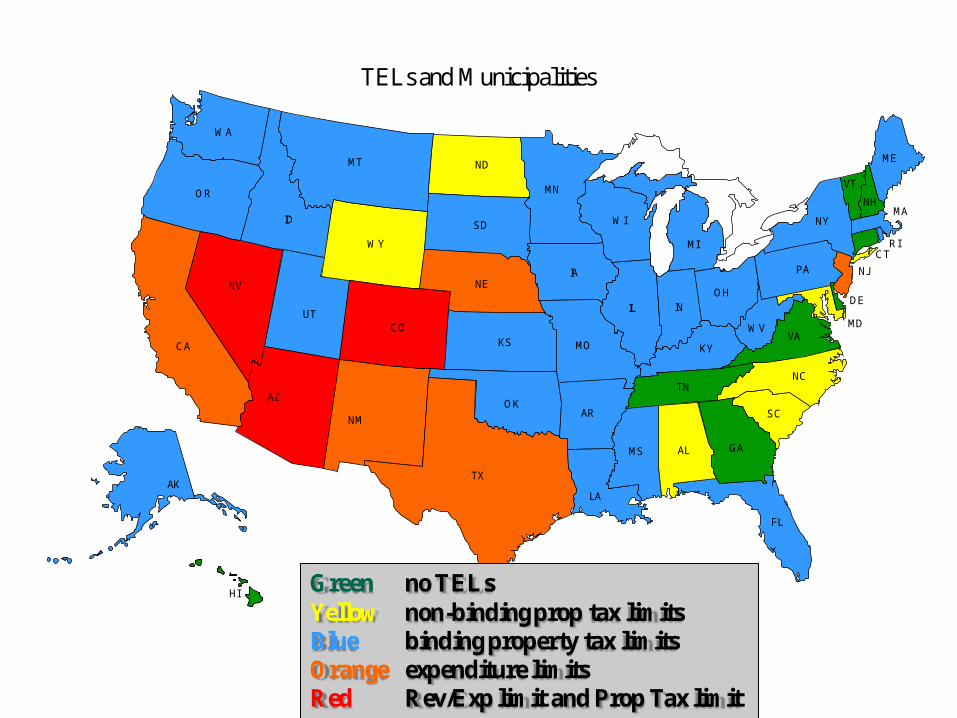

TELs and Municipalities

Green no TELsYellow non-binding prop tax limitsBlue binding property tax limitsOrange expenditure limitsRed Rev/Exp limit and Prop Tax limit

MT

WY

ID

WA

OR

NV

UT

CA

AZ

ND

SD

NE

CO

NM

TX

OK

KS

AR

LA

MO

IA

MN

WI

IL IN

KY

TN

MS AL GA

FL

SC

NC

VAWV

OH

MI

NY

PA

MD

DE

NJ

CTRI

MA

ME

VT

NH

AK

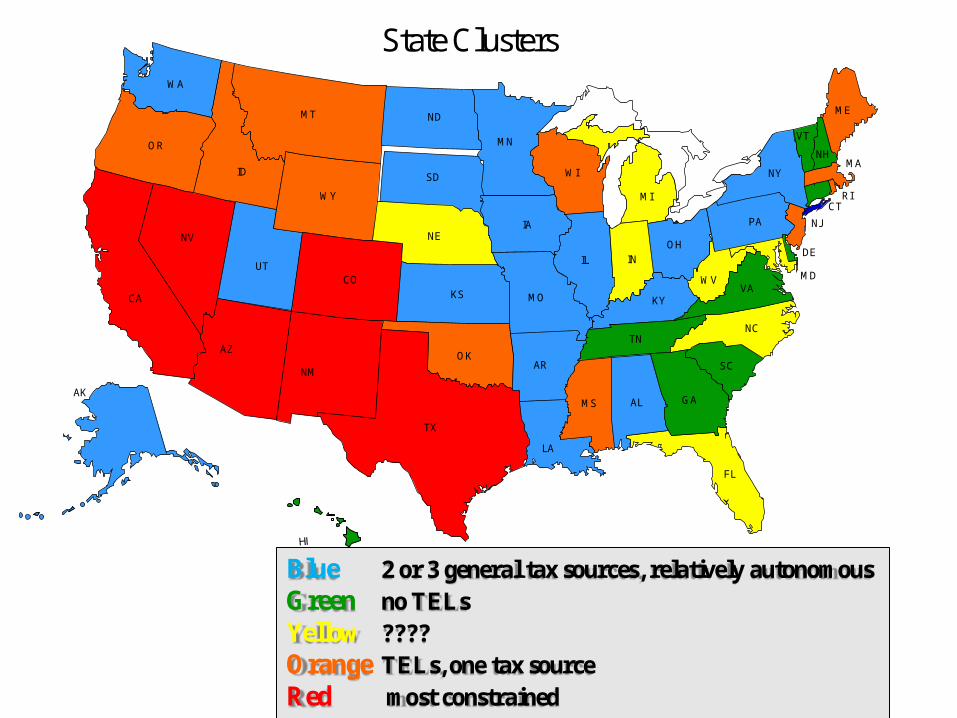

State Clusters

Blue 2 or 3 general tax sources, relatively autonomousGreen no TELsYellow ????Orange TELs, one tax sourceRed most constrained

The Great Recession, Municipal Budgets, and Land Development

• Setting the stage:– The contemporary situation

• Challenges– Economy is Changing:• Aligning Economic Base with Fiscal Authority

– Fiscal Foundation is Changing:• Narrowing the Tax Base

– Linking fiscal architecture and space• Spatialization of revenue structures

• Options: The Fiscal Policy Space

• A new sustainable fiscal architecture?

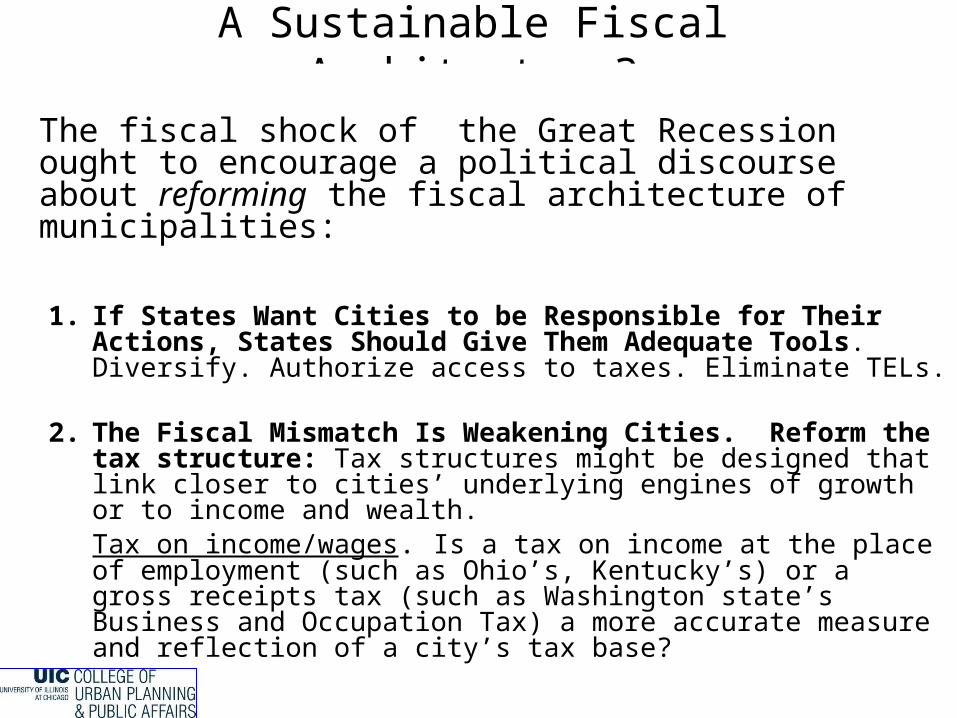

A Sustainable Fiscal Architecture?

The fiscal shock of the Great Recession ought to encourage a political discourse about reforming the fiscal architecture of municipalities:

1. If States Want Cities to be Responsible for Their Actions, States Should Give Them Adequate Tools. Diversify. Authorize access to taxes. Eliminate TELs.

2. The Fiscal Mismatch Is Weakening Cities. Reform the tax structure: Tax structures might be designed that link closer to cities’ underlying engines of growth or to income and wealth. Tax on income/wages. Is a tax on income at the place of employment (such as Ohio’s, Kentucky’s) or a gross receipts tax (such as Washington state’s Business and Occupation Tax) a more accurate measure and reflection of a city’s tax base?

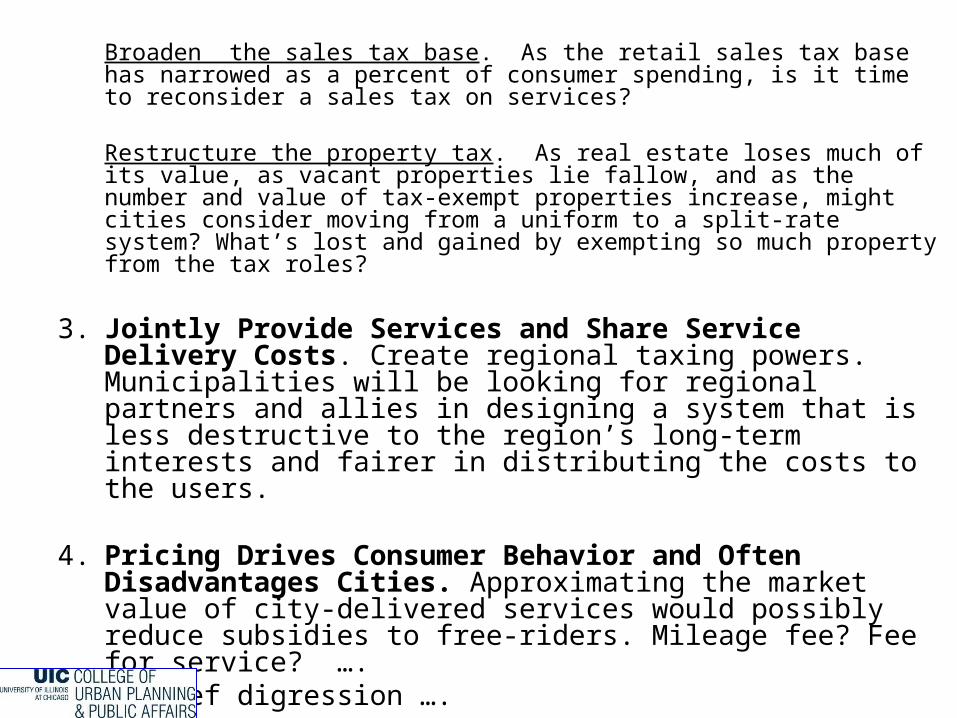

Broaden the sales tax base. As the retail sales tax base has narrowed as a percent of consumer spending, is it time to reconsider a sales tax on services?

Restructure the property tax. As real estate loses much of its value, as vacant properties lie fallow, and as the number and value of tax-exempt properties increase, might cities consider moving from a uniform to a split-rate system? What’s lost and gained by exempting so much property from the tax roles?

3. Jointly Provide Services and Share Service Delivery Costs. Create regional taxing powers. Municipalities will be looking for regional partners and allies in designing a system that is less destructive to the region’s long-term interests and fairer in distributing the costs to the users.

4. Pricing Drives Consumer Behavior and Often Disadvantages Cities. Approximating the market value of city-delivered services would possibly reduce subsidies to free-riders. Mileage fee? Fee for service? ….

a brief digression ….

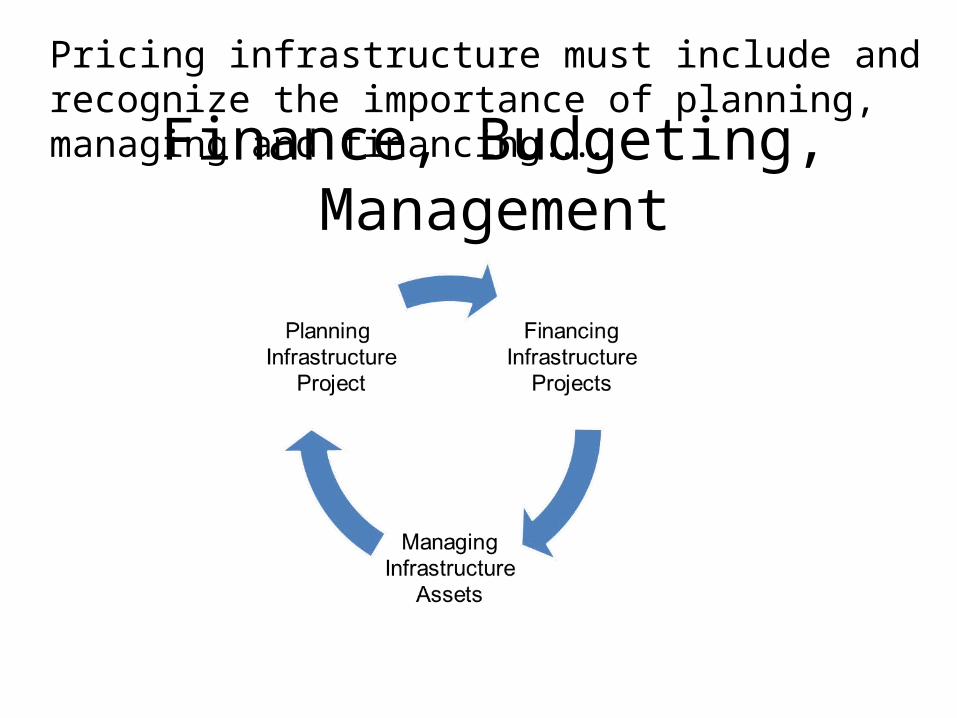

Finance, Budgeting, Management

Pricing infrastructure must include and recognize the importance of planning, managing and financing.….

The Utah Model. Government Performance Project Grade (2008): A

Statutory Set aside of 1.1% of value of fixed assets in the Operating Budget for maintenance and repair of state buildings.

Political Challenge: Future legislatures are (theoretically)bound by prior legislature’s decisions.

5. Revisit the Social Compact. The social compact of the last century that bound generations, socio-economic classes, neighborhoods, cities and regions needs to be reconsidered in light of demographic shifts, the transformation of the underlying economy, the forces of globalization, and an irrepressible resolve to enhance the human condition.

…. And returning to the Elements of a Sustainable Fiscal Architecture …

• fairness of revenue systems;• Spatial/land-use effects of revenue structures;• Benefits principle v. ability-to-pay; • pro-cyclical nature of local and state budget

practice; • accumulated long-term liabilities (pensions,

OPEBs, and infrastructure); • definition of “core services”; • pricing services and infrastructure assets; • Horizontal and vertical regional partnerships in

service delivery …

The Great Recession, Municipal Budgets, and

Land Development

Michael A. PaganoDean, College of Urban Planning &

Public AffairsUniversity of Illinois at Chicago

[email protected] View From 18th Street Bridge, a watercolor by Pat Wright

THANK YOU

Tuesdays at APA Chicago29 January 2013