Embed Size (px)

Citation preview

Dewey & LeBoeuf LLP dl.com

MiFID II – Challenges for Commodity Derivatives Markets

Robert Finney, Partner

January 2012

Dewey & LeBoeuf | 2

Agenda

● Why are commodity markets caught up in financial regulatory reform?

● International and European drivers and processes

● Increased European regulatory capture of commodities

● MiFID II: specific commodity proposals – Focus on scope

● Impacts and conclusions on scope issues

Dewey & LeBoeuf | 3

Why are commodities markets caught up in regulatory reform?

● High prices & volatility have socio-economic (& so political) impact – Political populism

– Perennial pariah treatment of “speculators” and “derivatives”?

– Increased political rhetoric in recent years following price increases/volatility in energy as well as foodstuffs and metals

● “Market” as a mechanism is being called into question – Dirigiste price regulation vs framework for price discovery & efficiency

Dewey & LeBoeuf | 4

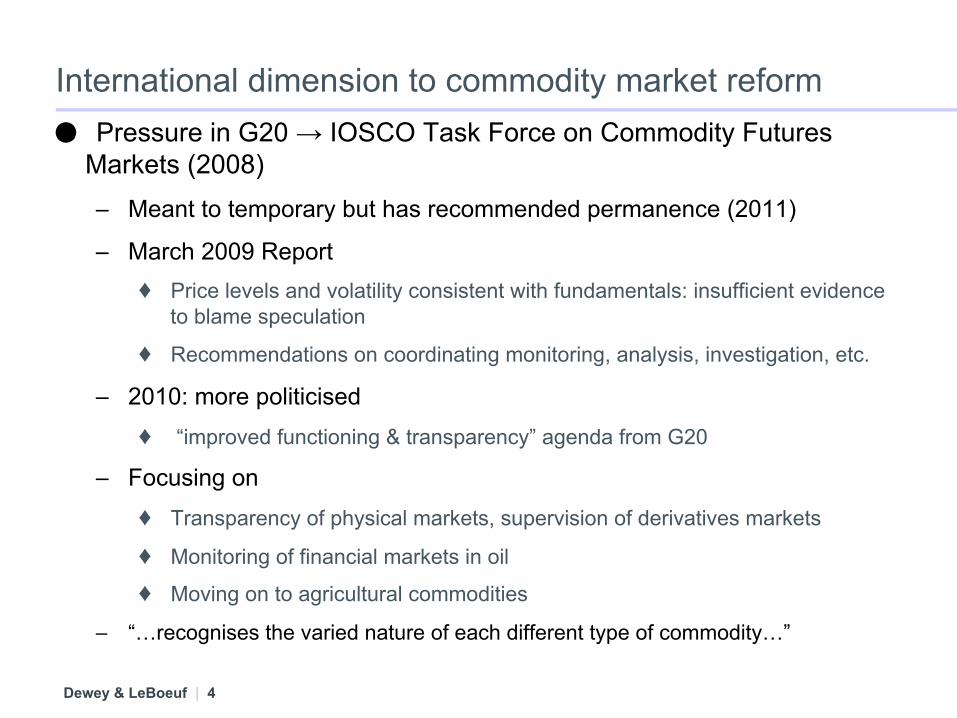

International dimension to commodity market reform ● Pressure in G20 → IOSCO Task Force on Commodity Futures

Markets (2008) – Meant to temporary but has recommended permanence (2011)

– March 2009 Report ♦ Price levels and volatility consistent with fundamentals: insufficient evidence

to blame speculation

♦ Recommendations on coordinating monitoring, analysis, investigation, etc.

– 2010: more politicised ♦ “improved functioning & transparency” agenda from G20

– Focusing on ♦ Transparency of physical markets, supervision of derivatives markets

♦ Monitoring of financial markets in oil

♦ Moving on to agricultural commodities

– “…recognises the varied nature of each different type of commodity…”

Dewey & LeBoeuf | 5

European dimension

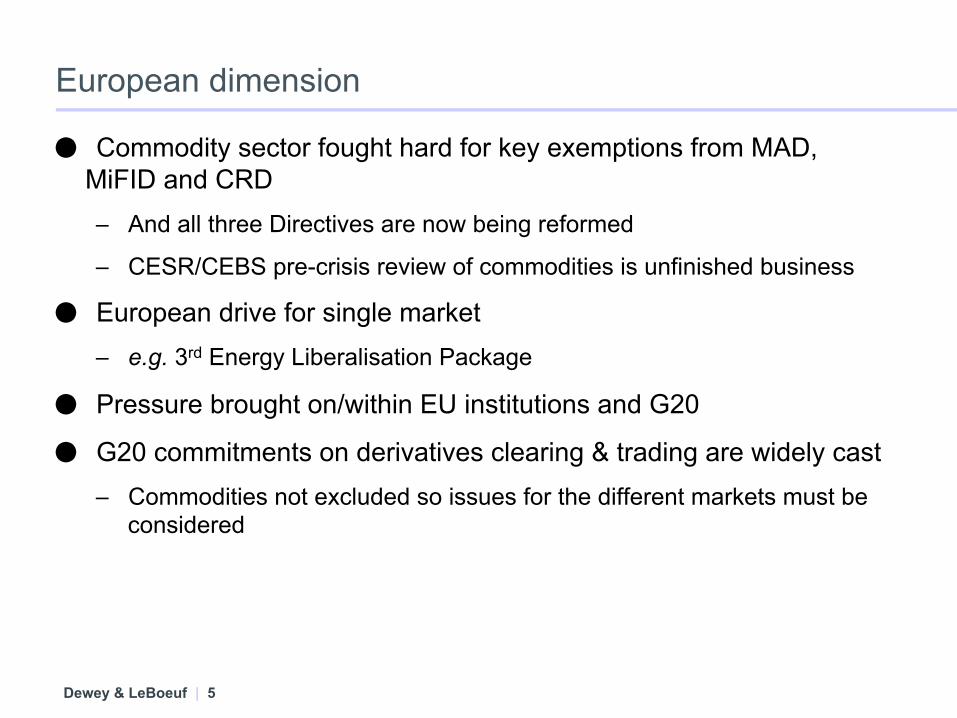

● Commodity sector fought hard for key exemptions from MAD, MiFID and CRD – And all three Directives are now being reformed

– CESR/CEBS pre-crisis review of commodities is unfinished business

● European drive for single market – e.g. 3rd Energy Liberalisation Package

● Pressure brought on/within EU institutions and G20

● G20 commitments on derivatives clearing & trading are widely cast – Commodities not excluded so issues for the different markets must be

considered

Dewey & LeBoeuf | 6

Increased regulatory capture – physicals market

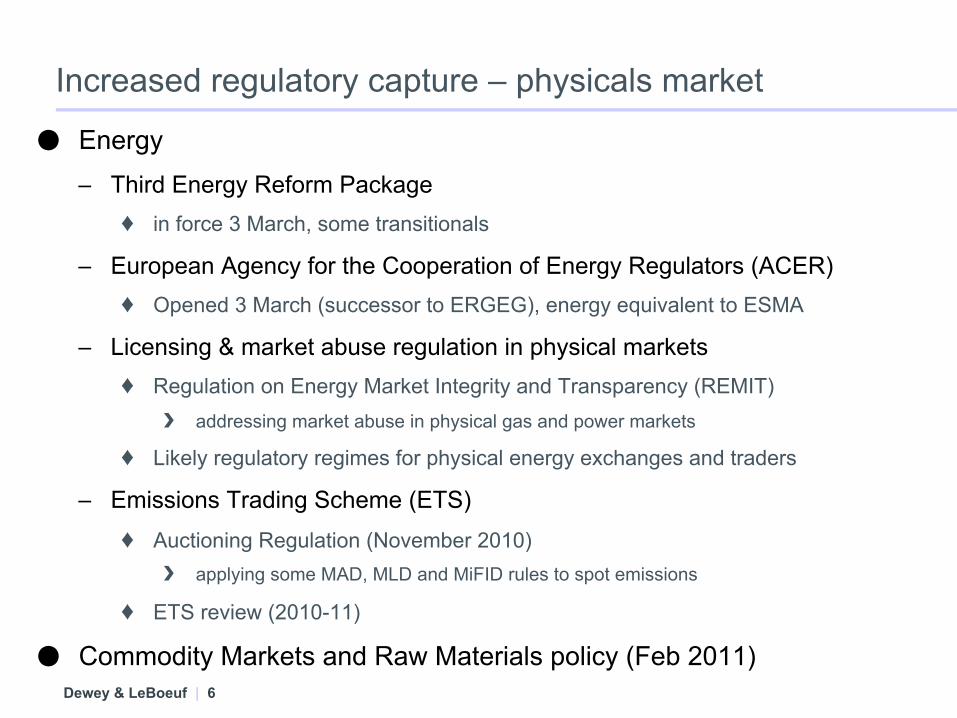

● Energy – Third Energy Reform Package

♦ in force 3 March, some transitionals

– European Agency for the Cooperation of Energy Regulators (ACER) ♦ Opened 3 March (successor to ERGEG), energy equivalent to ESMA

– Licensing & market abuse regulation in physical markets ♦ Regulation on Energy Market Integrity and Transparency (REMIT)

addressing market abuse in physical gas and power markets

♦ Likely regulatory regimes for physical energy exchanges and traders

– Emissions Trading Scheme (ETS) ♦ Auctioning Regulation (November 2010)

applying some MAD, MLD and MiFID rules to spot emissions

♦ ETS review (2010-11)

● Commodity Markets and Raw Materials policy (Feb 2011)

Dewey & LeBoeuf | 7

Increased regulatory capture – derivatives ● MiFID

– To cover more commodity products & more market participants ♦ Favoured exemptions being deleted/restricted

♦ Knock-on effect on scope of EMIR and MAD II

– More platform types and trading strategies to be regulated

– Standardised “derivatives” might require trading on organised platforms ♦ EMIR: broad range of OTC “derivatives” to require reporting & clearing

– Commodity position oversight and intervention

● MAD II (directive & regulation) is broader ♦ More platforms and products

♦ Broader “inside information” definition for commodities

● CRD IV legislative proposal (directive & regulation), July 2011 ♦ Basel III implementation

♦ Separate review for CRD-exempt, MiFID-regulated commodity dealers

Dewey & LeBoeuf | 8

MiFID II: Specific commodities proposals – scope (1)

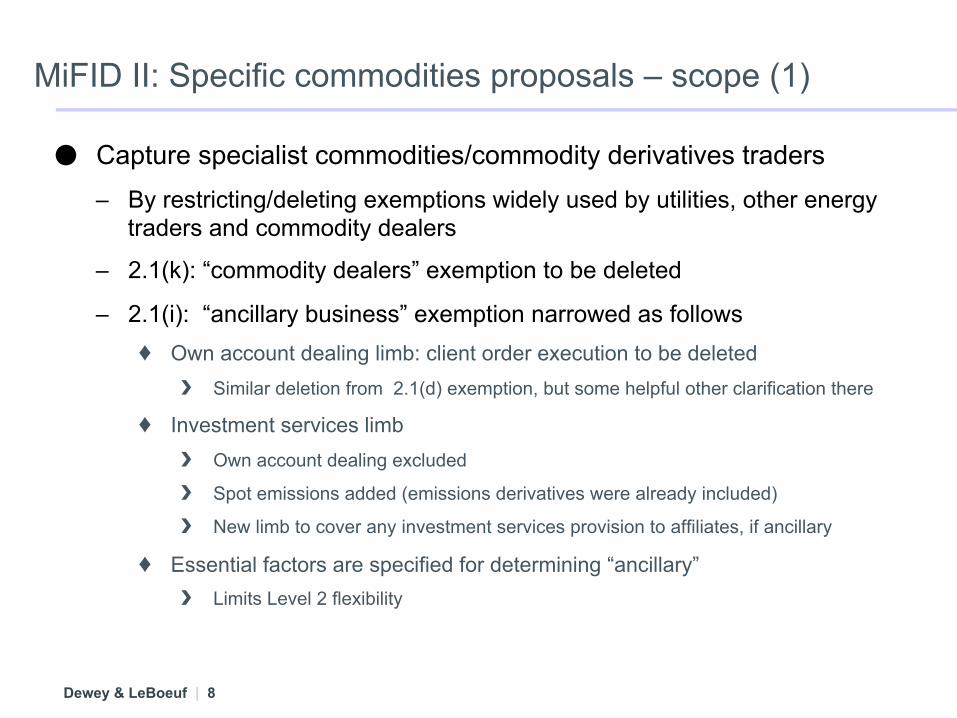

● Capture specialist commodities/commodity derivatives traders – By restricting/deleting exemptions widely used by utilities, other energy

traders and commodity dealers

– 2.1(k): “commodity dealers” exemption to be deleted

– 2.1(i): “ancillary business” exemption narrowed as follows ♦ Own account dealing limb: client order execution to be deleted

Similar deletion from 2.1(d) exemption, but some helpful other clarification there

♦ Investment services limb Own account dealing excluded

Spot emissions added (emissions derivatives were already included)

New limb to cover any investment services provision to affiliates, if ancillary

♦ Essential factors are specified for determining “ancillary” Limits Level 2 flexibility

Dewey & LeBoeuf | 9

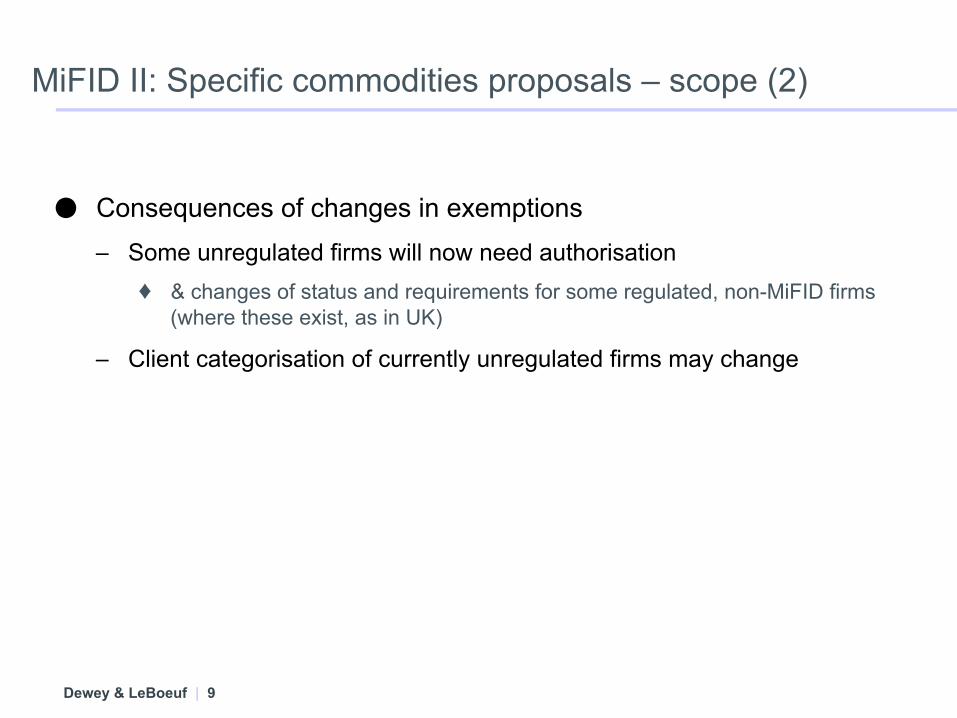

MiFID II: Specific commodities proposals – scope (2)

● Consequences of changes in exemptions – Some unregulated firms will now need authorisation

♦ & changes of status and requirements for some regulated, non-MiFID firms (where these exist, as in UK)

– Client categorisation of currently unregulated firms may change

Dewey & LeBoeuf | 10

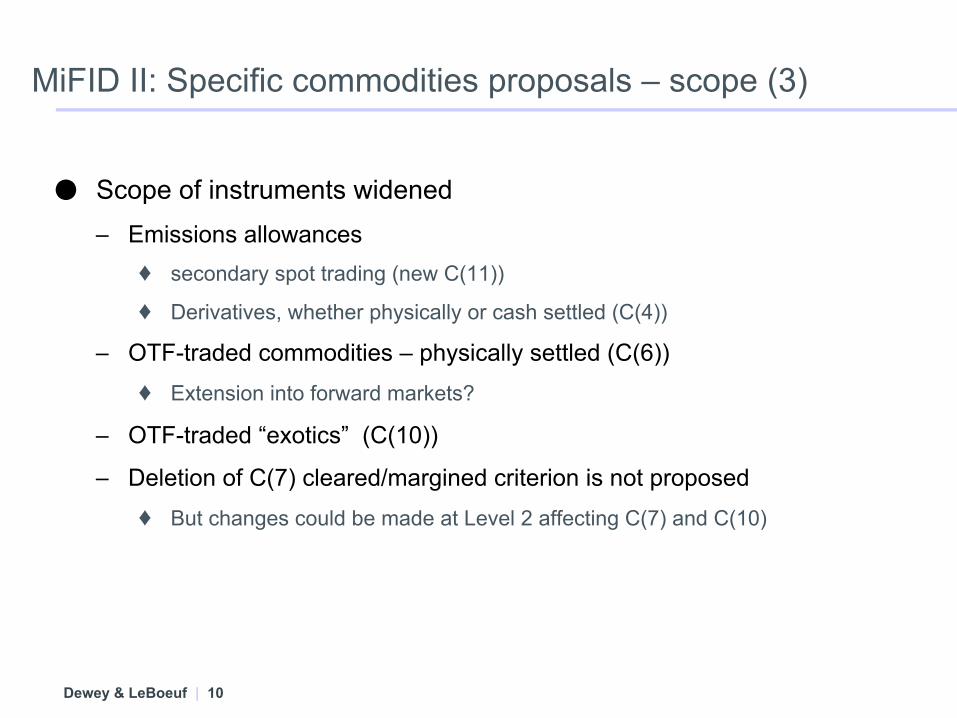

MiFID II: Specific commodities proposals – scope (3)

● Scope of instruments widened – Emissions allowances

♦ secondary spot trading (new C(11))

♦ Derivatives, whether physically or cash settled (C(4))

– OTF-traded commodities – physically settled (C(6)) ♦ Extension into forward markets?

– OTF-traded “exotics” (C(10))

– Deletion of C(7) cleared/margined criterion is not proposed ♦ But changes could be made at Level 2 affecting C(7) and C(10)

Dewey & LeBoeuf | 11

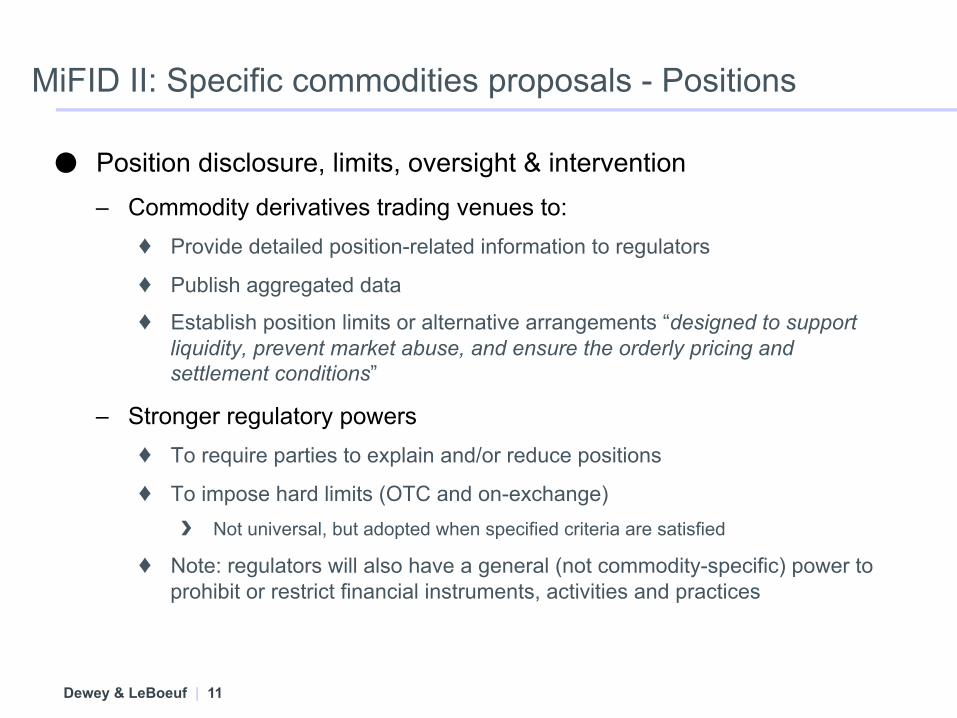

MiFID II: Specific commodities proposals - Positions

● Position disclosure, limits, oversight & intervention – Commodity derivatives trading venues to:

♦ Provide detailed position-related information to regulators

♦ Publish aggregated data

♦ Establish position limits or alternative arrangements “designed to support liquidity, prevent market abuse, and ensure the orderly pricing and settlement conditions”

– Stronger regulatory powers ♦ To require parties to explain and/or reduce positions

♦ To impose hard limits (OTC and on-exchange) Not universal, but adopted when specified criteria are satisfied

♦ Note: regulators will also have a general (not commodity-specific) power to prohibit or restrict financial instruments, activities and practices

Dewey & LeBoeuf | 12

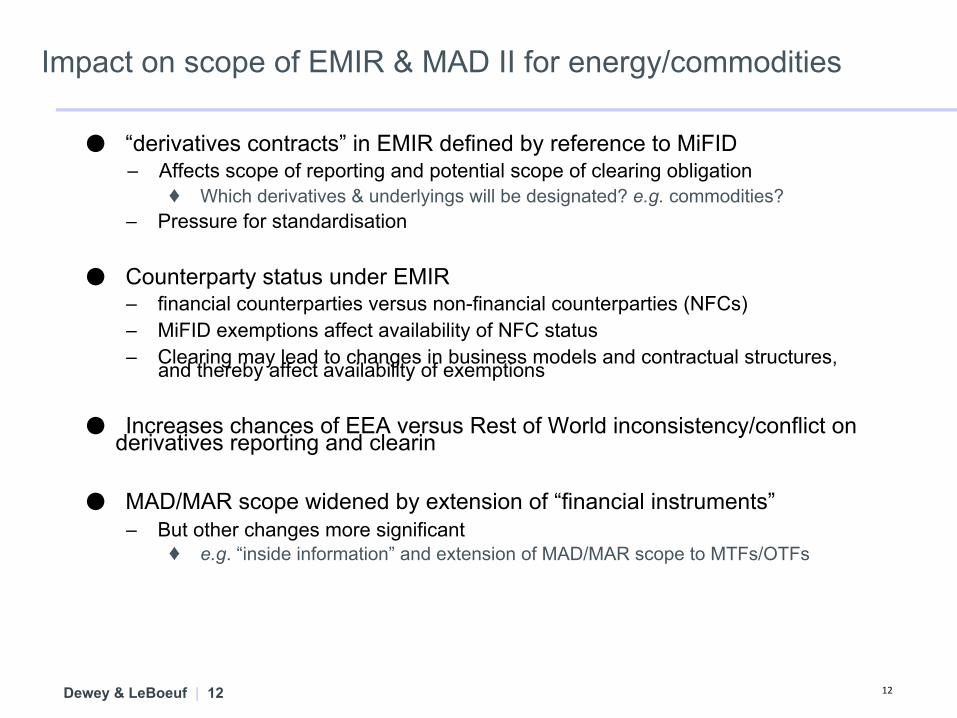

Impact on scope of EMIR & MAD II for energy/commodities

● “derivatives contracts” in EMIR defined by reference to MiFID – Affects scope of reporting and potential scope of clearing obligation

♦ Which derivatives & underlyings will be designated? e.g. commodities? – Pressure for standardisation

● Counterparty status under EMIR – financial counterparties versus non-financial counterparties (NFCs) – MiFID exemptions affect availability of NFC status – Clearing may lead to changes in business models and contractual structures,

and thereby affect availability of exemptions

● Increases chances of EEA versus Rest of World inconsistency/conflict on derivatives reporting and clearin

● MAD/MAR scope widened by extension of “financial instruments” – But other changes more significant

♦ e.g. “inside information” and extension of MAD/MAR scope to MTFs/OTFs

12

Dewey & LeBoeuf | 13

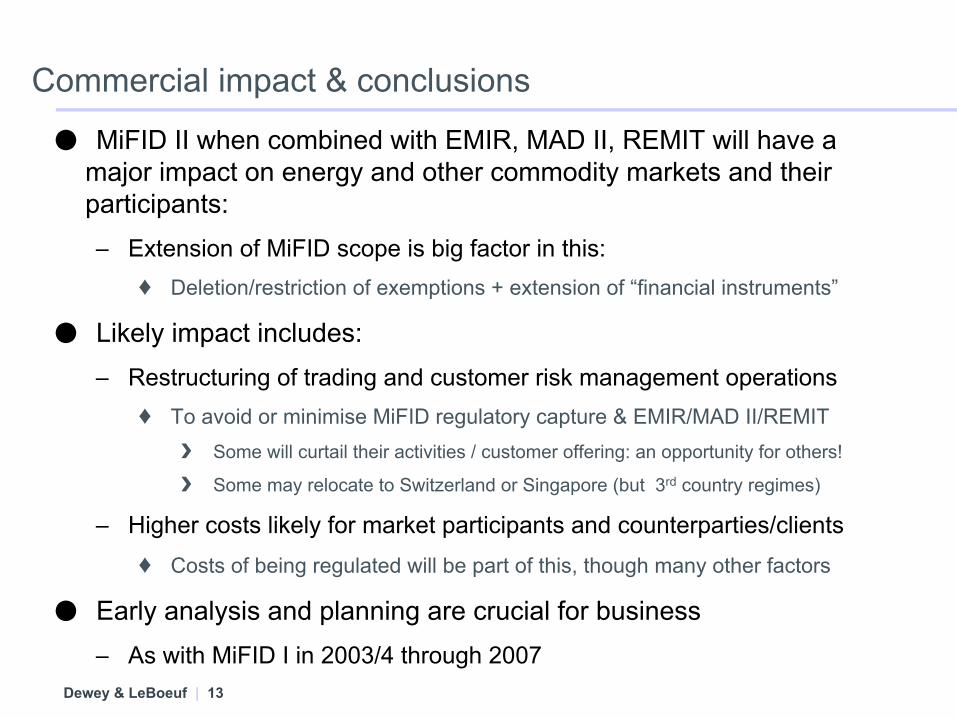

Commercial impact & conclusions

● MiFID II when combined with EMIR, MAD II, REMIT will have a major impact on energy and other commodity markets and their participants: – Extension of MiFID scope is big factor in this:

♦ Deletion/restriction of exemptions + extension of “financial instruments”

● Likely impact includes: – Restructuring of trading and customer risk management operations

♦ To avoid or minimise MiFID regulatory capture & EMIR/MAD II/REMIT Some will curtail their activities / customer offering: an opportunity for others!

Some may relocate to Switzerland or Singapore (but 3rd country regimes)

– Higher costs likely for market participants and counterparties/clients ♦ Costs of being regulated will be part of this, though many other factors

● Early analysis and planning are crucial for business – As with MiFID I in 2003/4 through 2007

Dewey & LeBoeuf | 14

Offices Worldwide

Dewey & LeBoeuf LLP

Dewey & LeBoeuf LLP dl.com

MiFID II – Challenges for Commodity Derivatives Markets

Robert Finney, Partner

January 2012