Embed Size (px)

Citation preview

Mining Monitor (March 2018)

Strategic Research Division

12 March 2018

The Bank of Tokyo-Mitsubishi UFJ, Ltd.

MUFG Union Bank, N.A.

Table of Contents

1. Overview 3

2. Iron Ore 5

3. Coal 8

4. Copper 11

5. Aluminum 14

Mining Monitor | 12 March 2018 2

6. Nickel 17

7. Zinc 20

8. Gold 23

Appendix 26

1. Overview

Mining Monitor | 12 March 2018 3

Ryosuke Ohno

Strategic Research Division

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

Mining Monitor | 12 March 2018 4

Mined Commodity Price Trends

In February 2018, trends in mined commodity prices relatively stabilized.

1. Overview

Mined Commodity Price Trends

On the whole, trends in mined commodity

prices relatively stabilized in February

2018.

Iron ore price rallied as the steel

production cuts in China is favoring the

use of more efficient quality grade one.

Average coking coal price fell, however,

strong buying interests from China led a

spot price recovery late in February.

Thermal coal price fell as tight supply in

China has eased after the rail transport

for coal has resumed to normal.

Aluminum price declined mainly by a

sharp build-up in aluminum inventories

due to increased Chinese exports.

Nickel price continued to rise, driven by

near-term supply reduction and longer-

term expectations of increased demand.

Average zinc price rose, however, the

price declined in late-February due to

concerns about rising supply in China.

Copper and gold prices were volatile as

these tracked the US dollar, however, the

average prices stabilized.

2017

Yr Avr Jul Aug Sep Oct Nov Dec Jan Feb

Iron Ore ($/t) 71 65 77 73 62 63 69 73 75

MoM - 17% 19% -6% -15% 2% 10% 6% 2%

YoY 22% 14% 27% 27% 5% -14% -14% -9% -16%

Coking Coal ($/t) 189 166 197 205 182 190 239 240 229

MoM - 13% 19% 4% -11% 5% 26% 0% -4%

YoY 33% 74% 73% 8% -22% -37% -10% 30% 42%

Thermal Coal ($/t) 88 84 95 96 97 95 99 105 103

MoM - 6% 13% 2% 1% -2% 4% 6% -3%

YoY 34% 33% 41% 33% 6% -2% 17% 26% 26%

Copper ($/t) 6,192 6,015 6,517 6,610 6,842 6,854 6,850 7,118 7,040

MoM - 5% 8% 1% 4% 0% 0% 4% -1%

YoY 27% 24% 37% 40% 44% 27% 21% 24% 18%

Aluminum ($/t) 1,968 1,903 2,030 2,096 2,131 2,097 2,080 2,210 2,182

MoM - 1% 7% 3% 2% -2% -1% 6% -1%

YoY 23% 17% 24% 33% 28% 21% 20% 23% 17%

Nickel ($/t) 10,410 9,491 10,890 11,216 11,336 11,972 11,495 12,865 13,596

MoM - 6% 15% 3% 1% 6% -4% 12% 6%

YoY 8% -8% 5% 11% 10% 8% 5% 29% 28%

Zinc ($/t) 2,891 2,787 2,981 3,117 3,265 3,229 3,196 3,442 3,533

MoM - 8% 7% 5% 5% -1% -1% 8% 3%

YoY 38% 28% 31% 36% 41% 26% 20% 27% 24%

Gold ($/oz) 1,259 1,238 1,284 1,315 1,283 1,282 1,267 1,332 1,331

MoM - -2% 4% 2% -2% 0% -1% 5% 0%

YoY 1% -8% -4% -1% 1% 4% 10% 12% 8%

Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

2017 2018

Chern Woon Lam

Strategic Research Division (Singapore)

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

2. Iron Ore

Mining Monitor | 12 March 2018 5

In February, iron ore prices rallied and

ended the month at $77/t. The average

price in February was $75/t, up 2%

from January’s $73/t. The steel

production cuts in China is favouring

the use of more efficient quality grade

iron ore such as the benchmark 62%

grade.

Chinese iron ore port inventories rose

to a record 156mn tons in the last

week of February.

The near-term positive outlook is

buoyed by the expectations of greater

steel production when the Chinese

winter supply curbs end. Banks like

Goldman Sachs and Citigroup are

forecasting iron ore prices to reach

$80-85/t in the next three months.

Iron ore pricing in the rest of 2018 may

be supported if a new round of

production curbs at Chinese city

Tangshan goes through. The

restrictions will raise steel prices and

the improved margins will allow mills to

pay more for iron ore.

6

Iron Ore Prices and Inventories

Prices rallied in February, as the use of efficient quality grade benchmark iron ore is favoured.

Near-term outlook is buoyed by expectations of greater steel production post-Chinese winter curbs.

2. Iron Ore

1) Price Trends

Mining Monitor | 12 March 2018

0

40

80

120

160

200

0

50

100

150

200

250

No

v-1

1

Feb

-12

Ma

y-1

2

Aug-1

2

No

v-1

2

Feb

-13

Ma

y-1

3

Aug-1

3

No

v-1

3

Feb

-14

Ma

y-1

4

Aug-1

4

No

v-1

4

Fe

b-1

5

Ma

y-1

5

Aug-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

China Iron Ore Port Inventory (RHS) Iron Ore Fines 62%, CFR China Import Spot Price (LHS)

($/t) (Mt)

Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

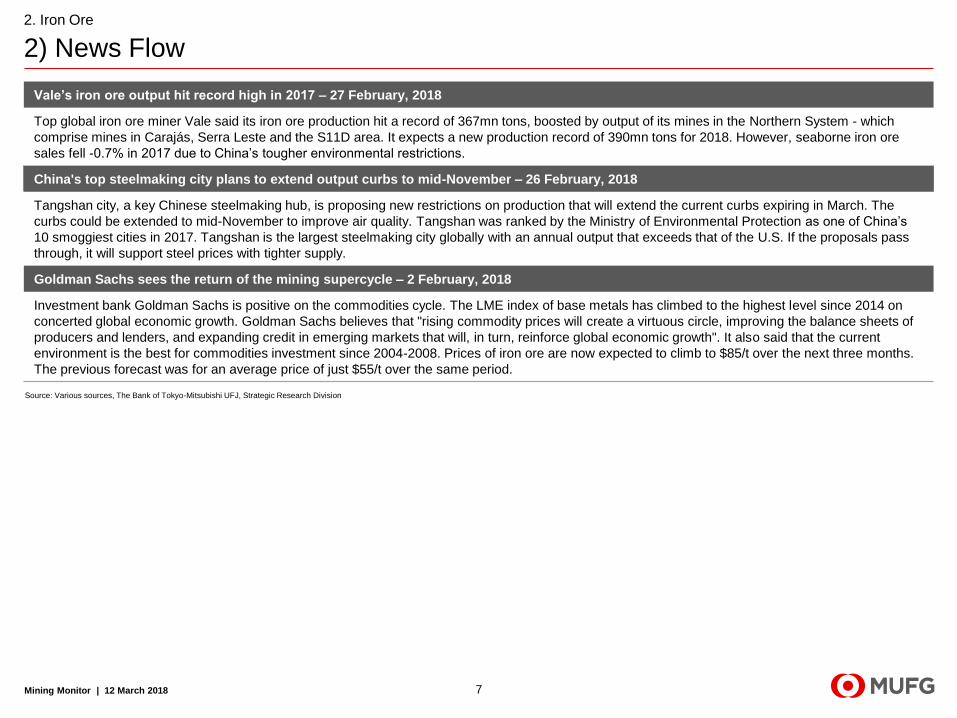

Vale’s iron ore output hit record high in 2017 – 27 February, 2018

Top global iron ore miner Vale said its iron ore production hit a record of 367mn tons, boosted by output of its mines in the Northern System - which

comprise mines in Carajás, Serra Leste and the S11D area. It expects a new production record of 390mn tons for 2018. However, seaborne iron ore

sales fell -0.7% in 2017 due to China’s tougher environmental restrictions.

China's top steelmaking city plans to extend output curbs to mid-November – 26 February, 2018

Tangshan city, a key Chinese steelmaking hub, is proposing new restrictions on production that will extend the current curbs expiring in March. The

curbs could be extended to mid-November to improve air quality. Tangshan was ranked by the Ministry of Environmental Protection as one of China’s

10 smoggiest cities in 2017. Tangshan is the largest steelmaking city globally with an annual output that exceeds that of the U.S. If the proposals pass

through, it will support steel prices with tighter supply.

Goldman Sachs sees the return of the mining supercycle – 2 February, 2018

Investment bank Goldman Sachs is positive on the commodities cycle. The LME index of base metals has climbed to the highest level since 2014 on

concerted global economic growth. Goldman Sachs believes that "rising commodity prices will create a virtuous circle, improving the balance sheets of

producers and lenders, and expanding credit in emerging markets that will, in turn, reinforce global economic growth". It also said that the current

environment is the best for commodities investment since 2004-2008. Prices of iron ore are now expected to climb to $85/t over the next three months.

The previous forecast was for an average price of just $55/t over the same period.

7

2. Iron Ore

2) News Flow

Source: Various sources, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Mining Monitor | 12 March 2018

William Cheung

Strategic Research Division (Hong Kong)

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

3. Coal

Mining Monitor | 12 March 2018 8

Average global coking coal price fell

by 4.3% from previous month to

$229/ton in February.

But it should be noted that price rose

greatly from $215/ton on 1 February

to $235/ton on 28 February, driven

by strong buying interests from

China amid restocking from Chinese

steelmakers ahead of Lunar New

Year holidays and strengthening

Chinese yuan against US dollar. Yet,

overall price were still below the

average price last month.

Average global thermal coal price fell

marginally by 2.6% month-on-month

to $103/ton in February.

The price decrease was due to ease

of supply tightness in China, as rail

transport for coal has resumed

normal when blizzard stopped. Also,

factories stopping work during the

Lunar New Year holidays reduced

the usage of electricity, which helped

relieve the demand pressure to a

certain extent.

Mining Monitor | 12 March 2018 9

Coal Prices

Average coking coal price fell in February, but strong buying interests from China led price recovery later this month.

Average thermal coal price fell as supply tightness has been eased after rail transport for coal has resumed normal.

3. Coal

1) Price Trends

0

50

100

150

200

250

300

350

Feb

-10

Ma

y-1

0

Aug-1

0

No

v-1

0

Feb

-11

Ma

y-1

1

Aug-1

1

No

v-1

1

Feb

-12

Ma

y-1

2

Aug-1

2

No

v-1

2

Feb

-13

Ma

y-1

3

Aug-1

3

No

v-1

3

Feb

-14

Ma

y-1

4

Aug-1

4

No

v-1

4

Feb

-15

Ma

y-1

5

Aug-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

Spot Price (Coking Coal) Spot Price (Thermal Coal)($/t)

Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

China to cut coal capacity by 150 million tons in 2018 – 5 March 2018

China will continue to cut coal production capacity by 150 million tons in 2018, according to the work report from NDRC (National Development and

Reform Commission) at the opening of the annual meeting of 13th National People's Congress held in early March. At the same time, coal-fired power

generating units with a capacity of below 300,000 kilowatts will be closed this year. The work report underscores China’s determination to remove coal

excess capacity, as gluts of coal production dragged down corporate profit and economic growth. Last month, NDRC said it aimed to meet its target for

reducing coal capacity two years earlier. China has cut 250 million tons of coal capacity last year, taking the total since 2016 to 460 million tons, almost

hitting its 2020 target of 500 million tons.

Coking coal price recovers in February, but still below January level – 19 February 2018

Coking coal price recovered from late January to February 2018 driven by strong buying interests from China, a result of restocking from Chinese steel

mills ahead of the Lunar New Year holidays and strengthening performance of Chinese yuan against US dollar. Domestic supply of coking coal in China

came under pressure due to the ongoing winter production cut. This in turn attracted Chinese buyers to return to the seaborne coking coal market in late

January. Besides, Chinese yuan has been strengthening against US dollar over the past few weeks, which made coal imports to China more attractive.

However, the 30-day average coking coal price on 19 February was still 12.7% below last month average, which was caused by a reduced level of

concern about Australia’s supply disruption, as well as slowing inventory re-stocking from Asian steelmakers and traders.

Thermal coal price falls marginally as coal inventories grow after rough winter – 12 February 2018

Coal inventories of power companies in China started to grow again in mid-February after severe supply shortages caused by rail transport disruption

due to blizzard as well as surging electricity consumption. As blizzard stopped, rail transport for coal has resumed normal recently. Also, factories

stopping work during the long Lunar New Year holidays would reduce the usage of electricity, which might help relieve the pressure on coal demand.

Therefore, the tightness of thermal coal market is likely to ease in February, according to the NDRC. For these reasons, the global thermal coal price fell

from $104.4/ton on 31 January 2018 to $98.7/ton on 12 February 2018.

China gives new inventive to drive quality coal – 9 February 2018

Coal companies in China will be encouraged to shut inefficient mines and replace them with larger one if they meet the standard set by the NDRC.

Companies that agree to establish long-term contracts with power plants or set up joint ventures with power utilities will be allowed to expand their

capacities by 130 percent to 300 percent. The NDRC will give those coal companies to shut outdated production within a year. This latest measure

plans to increase high-quality coal supply. It also aims to tie among coal mines, coal-related businesses and power utilities to stabilize thermal coal

price.

Mining Monitor | 12 March 2018 10

3. Coal

2) News Flow

Source: Various sources, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Katia Tavarez

Strategic Research (NY)

MUFG UNION BANK, N.A.

4. Copper

Mining Monitor | 12 March 2018 11

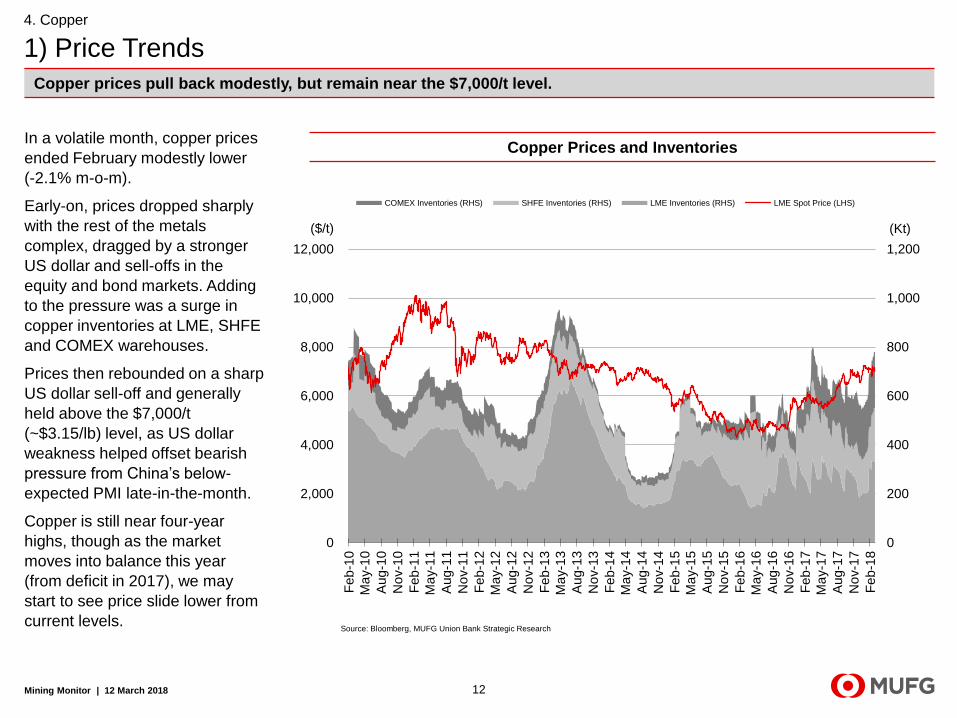

In a volatile month, copper prices

ended February modestly lower

(-2.1% m-o-m).

Early-on, prices dropped sharply

with the rest of the metals

complex, dragged by a stronger

US dollar and sell-offs in the

equity and bond markets. Adding

to the pressure was a surge in

copper inventories at LME, SHFE

and COMEX warehouses.

Prices then rebounded on a sharp

US dollar sell-off and generally

held above the $7,000/t

(~$3.15/lb) level, as US dollar

weakness helped offset bearish

pressure from China’s below-

expected PMI late-in-the-month.

Copper is still near four-year

highs, though as the market

moves into balance this year

(from deficit in 2017), we may

start to see price slide lower from

current levels.

Mining Monitor | 12 March 2018 12

Copper Prices and Inventories

Copper prices pull back modestly, but remain near the $7,000/t level.

4. Copper

1) Price Trends

0

200

400

600

800

1,000

1,200

0

2,000

4,000

6,000

8,000

10,000

12,000

Feb

-10

Ma

y-1

0

Aug-1

0

No

v-1

0

Feb

-11

Ma

y-1

1

Aug-1

1

No

v-1

1

Feb

-12

Ma

y-1

2

Aug-1

2

No

v-1

2

Feb

-13

Ma

y-1

3

Aug-1

3

No

v-1

3

Feb

-14

Ma

y-1

4

Aug-1

4

No

v-1

4

Feb

-15

Ma

y-1

5

Au

g-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

COMEX Inventories (RHS) SHFE Inventories (RHS) LME Inventories (RHS) LME Spot Price (LHS)

($/t) (Kt)

Source: Bloomberg, MUFG Union Bank Strategic Research

Union fears Codelco privatization – 2 March, 2018

The union representative in the board of Chile’s Codelco voiced concerns that the incoming government’s proposal to split Codelco is the first step

toward privatization. During his campaign, President-elect Sebastian Pinera stressed that he would give Codelco more independence to make the

company more efficient. He also noted the need for ‘deep reflection’ on funding. More recently, Chile’s incoming Mining Minister Baldo Prokurica told

newspaper La Tercera that the government plans to break up the company into northern and southern units. Prokurica did not mention any plans to

privatize Codelco.

Southern Copper wins auction for $2.5bn Peru project – 21 February, 2018

Southern Copper won the bid for the Peruvian government’s first auction of the Michiquillay copper project – the first tender in almost ten years.

Southern Copper won the tender with a proposal to transfer US$400 million to the government and pay 3 percent royalties. With mineral resources of

1,150 Mt and a copper grade of 0.63%, the mine would produce 225Kt per year (along with by-products like molybdenum, gold, and silver) for an initial

mine life of over 25 years at a ‘very competitive cash-cost’. The estimated capital investment is around US$2.5 billion. Michiquillay will start production

in 2025 and will become one of Peru’s largest mines.

China copper imports end 2017 at multi-year lows – 8 February, 2018

In January, China imported 400Kt of refined copper (-2% m-o-m, +16% y-o-y). This positive yearly reading follows the negative print from December,

and, according to analysts, may reflect China’s clampdown on copper scrap.

Mining Monitor | 12 March 2018 13

4. Copper

2) News Flow

Source: Various sources, MUFG Union Bank Strategic Research

Erik Lambert

Strategic Research Division (London)

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

5. Aluminum

Mining Monitor | 12 March 2018 14

Mining Monitor | 12 March 2018

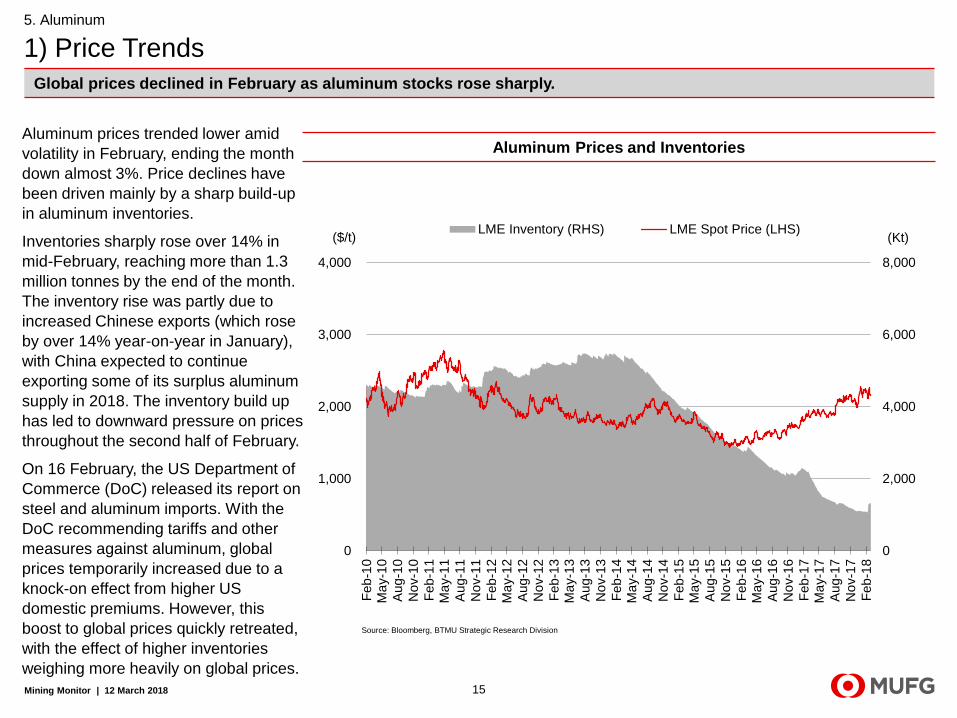

Aluminum prices trended lower amid

volatility in February, ending the month

down almost 3%. Price declines have

been driven mainly by a sharp build-up

in aluminum inventories.

Inventories sharply rose over 14% in

mid-February, reaching more than 1.3

million tonnes by the end of the month.

The inventory rise was partly due to

increased Chinese exports (which rose

by over 14% year-on-year in January),

with China expected to continue

exporting some of its surplus aluminum

supply in 2018. The inventory build up

has led to downward pressure on prices

throughout the second half of February.

On 16 February, the US Department of

Commerce (DoC) released its report on

steel and aluminum imports. With the

DoC recommending tariffs and other

measures against aluminum, global

prices temporarily increased due to a

knock-on effect from higher US

domestic premiums. However, this

boost to global prices quickly retreated,

with the effect of higher inventories

weighing more heavily on global prices.

15

Aluminum Prices and Inventories

Global prices declined in February as aluminum stocks rose sharply.

5. Aluminum

1) Price Trends

0

2,000

4,000

6,000

8,000

0

1,000

2,000

3,000

4,000

Feb

-10

Ma

y-1

0

Aug-1

0

No

v-1

0

Feb

-11

Ma

y-1

1

Aug-1

1

No

v-1

1

Feb

-12

Ma

y-1

2

Aug-1

2

No

v-1

2

Feb

-13

Ma

y-1

3

Aug-1

3

No

v-1

3

Feb

-14

Ma

y-1

4

Aug-1

4

No

v-1

4

Feb

-15

Ma

y-1

5

Aug-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

LME Inventory (RHS) LME Spot Price (LHS)($/t) (Kt)

Source: Bloomberg, BTMU Strategic Research Division

Surging stockpiles push aluminium prices to two-month low - 14 February, 2018

Aluminum prices fell on Wednesday following a rapid build up in warehouse stocks; these inventory increases suggested strong market supply.

Inventories at warehouses registered by LME increased by more than 200,000 tonnes in the past week to over 1.3 million tonnes. Inventories in

Shanghai Futures Exchange warehouses also increased, after rising more than 600% in 2017. As much as 7 million tonnes of aluminum remains

outside of the exchange warehouse system as a result of market surpluses that built up in previous years.

China's industry ministry to crack down on aluminum price speculation – 1 March, 2018

China’s Ministry of Industry and Information Technology (MIIT) agreed to increase monitoring of the price of aluminum in order to prevent excessive

speculation in the market. The Ministry agreed to work with metals associations and other departments to avoid speculation. Chinese aluminum prices

fell roughly 17% since September, after rising more than 25% for the first eight months of 2017.

Trump to impose steep tariffs on steel, aluminum; stokes trade war fears – 2 March, 2018

US President Donald Trump announced plans to impose tariffs on aluminum imports. The 10% tariffs on aluminum imports were expected to increase

prices for end-users of the metal, and concerned several lawmakers regarding potential retaliatory measures that could be taken by other trading

partners of the US. Canadian aluminium exports to the United States were believed to be particularly vulnerable to the tariffs.

Mining Monitor | 12 March 2018 16

5. Aluminum

2) News Flow

Source: Various sources, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Erik Lambert

Strategic Research Division (London)

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

6. Nickel

Mining Monitor | 12 March 2018 17

Nickel prices continued their uptrend,

moving briefly above $14,000/tonne, a

level not achieved since mid-2015.

Prices then settled around $13,740 at

the end of the month. Continued

market bullishness has been driven

by fundamental trends supporting

higher prices.

On the supply side, some nickel

miners reported lower-than-expected

mining output in February; Sumitomo

Corporation expected production at its

Ambatovy project in Madagascar to

run at only 50% utilization for the

remainder of Q1 following disruption

due to a January cyclone, for

example. Lower mining output

contributed to a continuous decline in

inventories throughout February,

which have pressured prices.

Price increases have also been driven

by speculators, investing in nickel

given the metal’s use in lithium-ion

batteries. Demand for these batteries

is expected to increase significantly

as electric vehicle penetration grows

in the coming decade.

Mining Monitor | 12 March 2018 18

Nickel Prices and Inventories

Nickel prices continued their uptrend into February, driven higher by near-term supply reductions and longer-term

expectations of increased demand.

6. Nickel

1) Price Trends

0

100

200

300

400

500

0

10,000

20,000

30,000

40,000

Feb

-10

Ma

y-1

0

Aug-1

0

No

v-1

0

Feb

-11

Ma

y-1

1

Aug-1

1

No

v-1

1

Feb

-12

Ma

y-1

2

Aug-1

2

No

v-1

2

Feb

-13

Ma

y-1

3

Aug-1

3

No

v-1

3

Feb

-14

Ma

y-1

4

Aug-1

4

No

v-1

4

Feb

-15

Ma

y-1

5

Aug-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

LME Inventory (RHS) LME Spot Price (LHS)($/t) (Kt)

Source: Bloomberg, BTMU Strategic Research Division

Nickel usage to grow 4%/year to 2027, deficit to narrow: Roskill – 8 February, 2018

Primary nickel consumption was expected to increase by around 4% per year from 2017-2027. A recent report by Roskill Information Services notes

that growth is expected to be driven by stainless steel production growth and increases in battery manufacturing. The company noted that “demand for

primary nickel in this market is anticipated to increase by 2.5% per year over the course of our forecast period, thanks to rising output in China and

Indonesia.”

Nickel hits multi-year high as industrial metals surge - 14 February, 2018

Nickel hit multi-year highs on Wednesday amid broader growth in industrial metals. Nickel on the LME closed up nearly 5% at $14,100, the highest level

since May 2015. Increasing Chinese imports, tight supply and interest from investment funds are expected to keep upward pressure on nickel prices.

Vale’s nickel production fell slightly in 2017 – 21 February, 2018

Production at the Indonesian subsidiary of Braziliain nickel miner Vale fell in 2017 to 76,807 metric tonnes, compared to 77,581 metric tonnes in 2016.

Planned maintenance in the fourth quarter contributed to the production declines. However, despite the production declines, revenues for the year were

expected to increase due to the effect of increasing nickel prices.

Mining Monitor | 12 March 2018 19

6. Nickel

2) News Flow

Source: Various sources, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

7. Zinc

Mining Monitor | 12 March 2018 20

Erik Lambert

Strategic Research Division (London)

THE BANK OF TOKYO-MITSUBISHI UFJ, LTD.

Zinc prices stalled in February, with an

end-of-month decline leaving prices

down 3%, capping the metal’s recent

rally.

Although LME zinc inventories have

continued to decline, which keeps

upward pressure on prices, signs of

higher future zinc production have put

a brake on bullishness in the sector.

Between January and February

several major zinc miners reported

increases in production in Q4 2017,

including Vedanta and MMG; this

furthered market perception of

production increases into 2018.

The late-February decline was directly

driven by concerns about rising supply

in China. A sharp increase in Chinese

zinc concentrates (mined supply for

smelters) imports in January, with

concentrates imports rising 48.5%

compared to December, signalled the

potential for a large amount of future

Chinese production to come onto the

market.

Mining Monitor | 12 March 2018 21

Zinc Prices and Inventories

Signs of robust 2018 production stalled zinc’s recent price rally in February.

7. Zinc

1) Price Trends

0

500

1,000

1,500

2,000

0

1,000

2,000

3,000

4,000

Feb

-10

Ma

y-1

0

Aug-1

0

No

v-1

0

Feb

-11

Ma

y-1

1

Aug-1

1

No

v-1

1

Feb

-12

Ma

y-1

2

Aug-1

2

No

v-1

2

Feb

-13

Ma

y-1

3

Aug-1

3

No

v-1

3

Feb

-14

Ma

y-1

4

Aug-1

4

No

v-1

4

Feb

-15

Ma

y-1

5

Aug-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

LME Inventory (RHS) LME Spot Price (LHS)($/t) (Kt)

Source: Bloomberg, BTMU Strategic Research Division

Zinc miners, smelters spar over supply as 2018 terms delayed - 16 February, 2018

Zinc miners and smelters did not come to an agreement on 2018 financial terms for zinc processing at a recent industry gathering. Any future

agreement is likely to be delayed until March or April, as industry players negotiate amid a potential for growing zinc supply in H2 2018. Traders

expected that smelters would accept lower fees to process concentrate into metal, with subdued mine supply ongoing for three years.

Vedanta seeks to expand zinc output after price rally – 19 February, 2018

Zinc miner Vedanta could expand its African zinc operations, in order to capitalize on prices which reached their highest levels in a decade, following

underinvestment in production and the rally in zinc prices, which reached their highest levels since 2007. The recent rally has boosted Vedanta’s profits.

Vedanta’s CEO was bullish on zinc prices, noting that the “the market is in deficit for both zinc concentrate and metal.”

Aluminum Slips Ahead of Trump Tariff Decision While Zinc Sinks - 01 March, 2018

Zinc lost two percent on Thursday, as a range of metals were under market pressure. Zinc traded at $3,381 per tonne, falling for a third day in a row.

Declines were driven particularly by signs of supply growth in China. Sharp increases in zinc concentrates imports to China in January, particularly from

Australia, has been the driver of the price declines. According to Macquarie analyst Vivienne Lloyd: “We still think zinc is going to make one last push

higher on Chinese galvanized steel restocking from end-March, but the concentrates import data is focusing minds on the new material that’s going to

be coming into the market this year.”

Mining Monitor | 12 March 2018 22

7. Zinc

2) News Flow

Source: Various sources , The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

Katia Tavarez

Strategic Research (NY)

MUFG UNION BANK, N.A.

8. Gold

Mining Monitor | 12 March 2018 23

Mining Monitor | 12 March 2018 24

Gold Prices, ETF Holdings, DXY Index and 10Yr US TIPS Yield

A volatile month for gold as it tracked the US dollar.

8. Gold

1) Price Trends

Gold prices came under pressure

in February (-2.0% m-o-m),

trading erratically throughout the

month but remaining above the

$1,300/lb threshold.

Gold tracked the US dollar’s

volatile movements closely, falling

sharply in early-February as the

dollar strengthened (and

bond/equity markets sold-off) and

rising quickly thereafter as the

dollar weakened. Despite dollar

support, gold prices ultimately

turned lower in the second-half of

February, pressured by rising real

rates in the US.

With the recent leg down in

prices, funds reduced bullish bets

on gold, with money manager net

length at the COMEX falling to

their lowest level this year. Gold

ETF holdings fell only modestly,

remaining near 4 ½ year highs.

1,000

1,300

1,600

1,900

2,200

2,500

2,800

800

1,000

1,200

1,400

1,600

1,800

2,000

Feb

-10

Ma

y-1

0

Aug-1

0

No

v-1

0

Feb

-11

Ma

y-1

1

Aug-1

1N

ov-1

1

Feb

-12

Ma

y-1

2

Aug-1

2

No

v-1

2

Feb

-13

Ma

y-1

3

Aug-1

3

No

v-1

3

Feb

-14

Ma

y-1

4

Aug-1

4

No

v-1

4

Feb

-15

Ma

y-1

5

Aug-1

5

No

v-1

5F

eb

-16

Ma

y-1

6

Aug-1

6N

ov-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

(t) ETF Holdings (RHS) Gold Price (LHS)($/oz)

Source: World Gold Council, GFMS, Bloomberg, MUFG Union Bank Strategic Research

Note: ETF Holdings are expressed in aggregate tons.

1.0

1.5

2.0

2.5

3.0

3.5

4.0

9

10

11

12

13

14

15

Feb

-10

Ma

y-1

0

Aug-1

0

No

v-1

0

Feb

-11

Ma

y-1

1

Aug-1

1

No

v-1

1

Feb

-12

Ma

y-1

2

Aug-1

2

No

v-1

2

Feb

-13

Ma

y-1

3

Aug-1

3

No

v-1

3

Feb

-14

Ma

y-1

4

Aug-1

4

No

v-1

4

Feb

-15

Ma

y-1

5

Aug-1

5

No

v-1

5

Feb

-16

Ma

y-1

6

Aug-1

6

No

v-1

6

Feb

-17

Ma

y-1

7

Aug-1

7

No

v-1

7

Feb

-18

Index DXY Inverse (LHS) 10Yr UST Yield (RHS) (%)

Source: Bloomberg, MUFG Union Bank Strategic Research

Mining Monitor | 12 March 2018 25

8. Gold

2) News Flow

Lundin Gold sees growth after Ecuador project – 5 March, 2018

Lundin Gold’s CEO said that the company is looking to becoming an at least one-million-a-year producer of gold with three to four operations. The

Canadian company will focus on North and Latin America for growth. Lundin Gold is firstly focused, however, on building its Fruta del Norte mine that

will be Ecuador’s biggest gold mine and for which the miner recently raised nearly half a billion in a private placement. The start of production for that

project is targeted for end-2019. It will produce over 325K ounces of gold annual with a mine life of 15 years.

Barrick will increase output starting in 2021 – 22 February, 2018

Barrick Gold, the world’s largest gold producer, will increase gold production by advancing four projects that could add more than 1 million ounces in

output starting in 2021. The company said that the Cortez Deep South, Goldrush and Turquoise Ridge projects in the US have been approved, and that

work on extending the life of the Lagunas Norte Mine in Peru is under way. These announcements come as Newmont Mining closes the gap with

Barrick in terms of annual production. In fact, guidance from both companies for the 2018-22 period suggest that Newmont will overtake Barrick as the

largest gold producer over the next few years. In its 2018 guidance, Barrick reduced its production forecasts, targeting 4.5 – 5.5 million ounces of gold

for 2018 and 4.2 – 4.6 million ounces per year for the 2019-22 period. Newmont, meanwhile, expects that it will produce 4.9 – 5.4 million ounces for

2018 and 4.6 – 5.1 million ounces for the 2019-22 period.

Source: Various sources, MUFG Union Bank Strategic Research

Mining Monitor | 12 March 2018 26

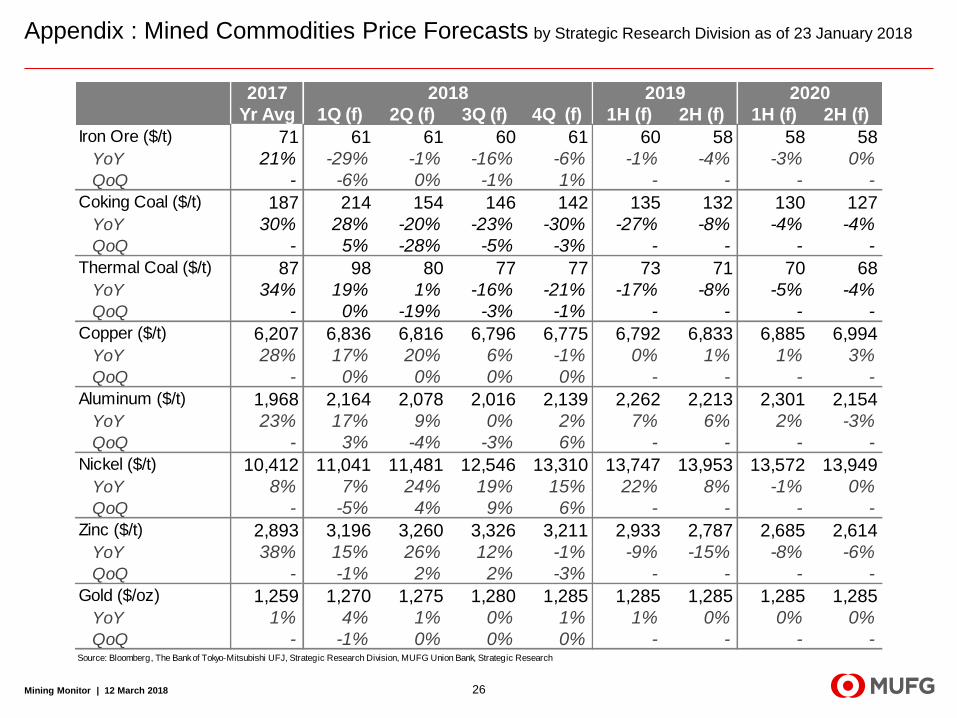

Appendix : Mined Commodities Price Forecasts by Strategic Research Division as of 23 January 2018

2017

Yr Avg 1Q (f) 2Q (f) 3Q (f) 4Q (f) 1H (f) 2H (f) 1H (f) 2H (f)

Iron Ore ($/t) 71 61 61 60 61 60 58 58 58

YoY 21% -29% -1% -16% -6% -1% -4% -3% 0%

QoQ - -6% 0% -1% 1% - - - -

Coking Coal ($/t) 187 214 154 146 142 135 132 130 127

YoY 30% 28% -20% -23% -30% -27% -8% -4% -4%

QoQ - 5% -28% -5% -3% - - - -

Thermal Coal ($/t) 87 98 80 77 77 73 71 70 68

YoY 34% 19% 1% -16% -21% -17% -8% -5% -4%

QoQ - 0% -19% -3% -1% - - - -

Copper ($/t) 6,207 6,836 6,816 6,796 6,775 6,792 6,833 6,885 6,994

YoY 28% 17% 20% 6% -1% 0% 1% 1% 3%

QoQ - 0% 0% 0% 0% - - - -

Aluminum ($/t) 1,968 2,164 2,078 2,016 2,139 2,262 2,213 2,301 2,154

YoY 23% 17% 9% 0% 2% 7% 6% 2% -3%

QoQ - 3% -4% -3% 6% - - - -

Nickel ($/t) 10,412 11,041 11,481 12,546 13,310 13,747 13,953 13,572 13,949

YoY 8% 7% 24% 19% 15% 22% 8% -1% 0%

QoQ - -5% 4% 9% 6% - - - -

Zinc ($/t) 2,893 3,196 3,260 3,326 3,211 2,933 2,787 2,685 2,614

YoY 38% 15% 26% 12% -1% -9% -15% -8% -6%

QoQ - -1% 2% 2% -3% - - - -

Gold ($/oz) 1,259 1,270 1,275 1,280 1,285 1,285 1,285 1,285 1,285

YoY 1% 4% 1% 0% 1% 1% 0% 0% 0%

QoQ - -1% 0% 0% 0% - - - -Source: Bloomberg, The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division, MUFG Union Bank, Strategic Research

20202018 2019

Disclaimer

Mining Monitor | 12 March 2018 27

This report is intended only for information purposes and is not intended to constitute an offer or solicitation to buy or sell securities or any

other products. Contents of the report are information as at publish date and are subject to change without notice. This report has not been

prepared to provide legal, taxational, financial, market-judgmental, or any other advises on propriety of any transactions. In taking any

action, each reader is requested to act on the basis of his or her own judgment upon consulting certified lawyers, accountants or other

professionals regarding the accuracy, validity and reliability of information appeared in this report.

Bank of Tokyo-Mitsubishi UFJ is regulated by the Financial Services Authority.

No part of this publication may be reproduced, stored in a retrieval system or transmitted without the prior written permission of The Bank

of Tokyo-Mitsubishi UFJ Limited.

Copyright© 2018 The Bank of Tokyo-Mitsubishi UFJ, Ltd. All rights reserved.

Publisher:The Bank of Tokyo-Mitsubishi UFJ, Strategic Research Division

2-7-1, Marunouchi, Chiyoda-ku, Tokyo 100-8388, Japan

Contact details for inquiries : Shino Yamamoto

(TEL:03-3240-7935、e-mail: [email protected])